Reverse By The Number

|

|

|

- Leonard Antony Barker

- 5 years ago

- Views:

Transcription

1 Reverse By The Number Working Reverse Mortgage Loans in Reverse Vision HighTechLending, Inc., Licensed by the Department of Business Oversight under the California Residential Mortgage Lending Act. NMLS #7147. Licensed in AZ# , CA# , CO #7147, FL #7147, HI #7147, IL #MD , MD #21762, NC #L , NJ #7147, OR #ML4386, PA #49892, TX #7147,UT # , VA #MC-5962, WA # Main Street #350, Irvine, CA 92614

2 Introduction ReverseVision Loan Screen ReverseVision Fee screen ReverseVision Comparison screen The Numbers Rates and Fees Calculations Available Funds Requested Payments Summary Learning Objectives

3 Introduction The ReverseVision loan comparison printout provides an itemization of a loan s numbers. It is one of the most important documents that you disclose to, and discuss with, your borrowers. These numbers include the rates and fees, the calculations, and the available funds and requested payments. The calculations are based on: The age of the youngest borrower or non-borrowing spouse. The interest rate of the product chosen. The value of the home, or maximum claim amount. In short, the loan comparison helps a borrower determine if the reverse mortgage will address and meet their financial goals and needs.

4 ReverseVision Borrower Screen You can generate a basic quote in ReverseVision after you input all the information into the fields on the Borrower screen that display a red stop sign. To generate a proposal, however, you must also input information into fields that display a yellow yield sign.

5 Loan Screen When you complete the fields, click Loan to display the Loan screen. Click a product to display its specific payment plan and interest rate. Note: The Loan link does not display until all required Borrower fields are complete.

6 Fee Screen The Fee screen displays all the fees associated with the loan. Review the screen to compare fees with the GFE validator, and change the fees as necessary.

7 ReverseVision The information on this screen populates the Good Faith Estimate we print out and give to the borrower.

8 Financial Assessment Mortgagee Letters and , which included the HECM Financial Assessment and Property Charge guide, were issued on November 10, FAR uses the Financial Assessment (FA) to evaluate whether a borrower qualifies for the HECM loan, and under what conditions. The FA specifically looks at willingness and capacity of the borrower to meet his or her financial obligations and meet HECM requirements. Willingness: Past performance and credit history. Capacity: Using income, assets and expenses to calculate residual cash flow. The Financial Assessment became effective, industrywide, on April 27, 2015.

9 Financial Assessment, cont. A complete financial analysis of each HECM borrower is a condition of HECM approval. All HECM borrowers verify and document the following: Credit history and property charge payments Income and Assets Expenses Residual Income FAR collects the borrower s authorization to verify the information we need to perform the FA. This includes a Non-Borrowing Spouse (NBS) or Other Non-Borrowing Household Member s (ONBHM) authorization, whenever necessary.

10 Financial Assessment, cont. Include all members of the household when you calculate family size, including non-borrowing spouse and any other individuals who depend on the borrower for support. Omit individuals who have a source of verified income, and do not rely on the borrower for support. Refer to the table to calculate and enter Residual income by family size and region.

11 Financial Assessment, cont. There are two types of Life Expectancy Set- Asides (LESAs): the partially-funded LESA and the fully-funded LESA. Note: Borrowers can choose to have a LESA even if they pass Financial Assessment. However, they cannot cancel a LESA after they obtain it. To determine if a borrower requires a LESA, enter information into the ReverseVision Financial Assessment screens.

12 Financial Assessment, cont. After you enter all information into the Financial Assessment screens, the Assessment Results screen indicates whether or not the borrower requires a LESA, or even that the loan must be denied because of credit issues.

.")

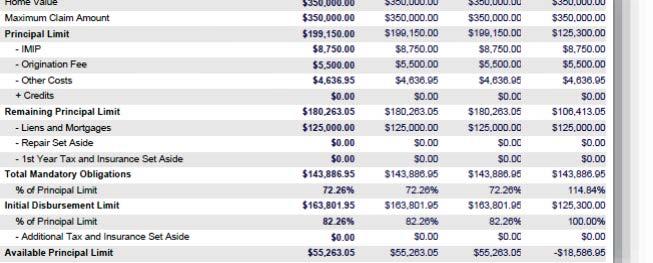

13 Comparison Screen The ReverseVision Comparison screen displays the available products side by side. You can add and delete products, as well as export, print, or a comparison directly from this screen. The product with bolded numbers and an orange column header is the chosen product (see next slide). The products with a green background in the Remaining Principal Balance field provide highest principal limit loan amount.

14 Comparison Screen

15 The Numbers The Comparison screen displays all the numbers associated with the loan, from the index and initial rate, to the principal limit and closing costs. The key to explaining these numbers to your borrower is to look everything over and make sure it makes sense to you before you present the information to the client. The Loan Comparison printout displays the screen information by category: Rates and Fees, Calculation and Available Funds, Requested Payments.

16 Rates and Fees The Rates and Fees section of the loan comparison displays: Margin: A cushioning amount the lender adds to the index rate when determining the initial and current interest rates. The index currently used is the London Interbank Offered Rate, or LIBOR. Initial Interest Rate: The interest rate that is effective on the loan comparison date. This is the rate used to calculate the interest that initially accrues on the outstanding loan balance every month. Expected Interest Rate: The interest rate applied to the amount the borrower can draw from the loan proceeds under the various disbursement options. It is the 10-year LIBOR swap rate

17 Rates and Fees, cont. Ongoing Mortgage Insurance Rate: The annual mortgage insurance premium amount. The formula is (outstanding loan balance) X , which is 1/12 th the annual rate assessed monthly. Cap on Interest Rate: The limit by which an adjustable interest rate can go up or down during a specified time period. Initial Line of Credit Growth: This is the line of credit balance at closing adjusted every month. Note: The margin and the ongoing mortgage insurance remain the same, but the LIBOR is subject to change, either monthly or annually.

+ (Lender")

.")

18 Rates and Fees, cont. The calculation for the growth rate is (1-monthLIBOR Rate) + (Lender s margin ) % (the ongoing mortgage insurance rate) =4.188%

19 Rates and Fees: Calculation

20 Rates and Fees: Calculation, co nt. The Calculation section displays: Home Value: Initially the home value includes the borrower s estimate, loan officer s research, and other factors. Later, it is the underwritten appraised value. The lender changes this value based on the appraisal. Maximum Claim Amount: The lesser of a home s appraised value and the maximum amount that FHA will insure for single family residences in a given county. This amount determines the principal limit for a HECM loan. Note: The current lending limit is $625,500. If the home value EXCEEDS the current lending limit, this field contains the LOWER of the home value or the Maximum Claim Amount.

21 Rates and Fees: Principal Limit This section displays the principal limit and the servicing fee set-aside. Note: The Servicing Set-aside field displays on the ReverseVision Comparison screen. However, it does not currently appear on the Comparison document as FAR does not currently allow for this fee. However, some lenders do allow for this fee. Principal Limit: The loan amount the borrower qualifies for based on the home value, interest rate of the product chosen, and the age of the youngest borrower or nonborrowing spouse. It is also known as the Loan to Value. Note: This number differs among HECM borrowers: The older the borrower, the higher the principal limit.

22 Principal Limit: IMIP The Principal Limit section displays any adjustments to the principal limit amount, including IMIP, origination fee, third party costs, and any lender credits. Initial Mortgage Insurance Premium (IMIP) The Initial Mortgage Insurance Premium (IMIP) is always either 0.5% or 2.50% of the Maximum Claim Amount based on the amount of the principal limit, plus mandatory obligations the borrower takes at closing. If the borrower takes more than 60% of the principal limit amount, the IMIP is always 2.50% of the maximum claim amount. If the borrower takes 60% or less the IMIP is 0.5% of the maximum claim amount. This section also displays the origination fee, third party costs, and any lender credits.

23 Principal Limit: Origination Fee Origination Fee The origination fee is calculated according to a formula: (2% of the first $200,000 of the Maximum Claim Amount), + (1% of any value above $200,000) to a maximum of $6,000. Example: The maximum claim amount on a loan is $500,000. First 2%: $200,000 X 2% = $4000 1%: $500,000 $200,000 = $300,000 X 1% = $3,000 $ $3,000 = $7,000 $6,000 The $7,000 calculated total exceeds the maximum origination fee of $6,000, so the origination fee is $6,000.

24 Principal Limit: Other Costs The Other Costs amount is a sum of payments to outside vendors for the appraisal, title inspection, credit report, settlement costs, and so forth. You can view a breakdown of these charges on the ReverseVision Fees screen, and change them as necessary. Other Costs fees display on the Good Faith Estimate, and are usually not negotiable. In addition, some of these fees cannot exceed a 10% tolerance, while others cannot exceed the amount on the GFE AT ALL. If the fees are disclosed too low, and the cost exceeds the amount disclosed, the lender is responsible for paying any amount over the disclosed amount, according to the RESPA laws. Always check, validate and update these fees to ensure they are as accurate as possible.

25 Principal Limit: Credits On some HECM transactions the lender can give the borrower lender credits in order to complete the transaction. For instance, the lender might issue a credit that permits a borrower to fall within certain tolerances, or authorize a credit to cover fees he or she can t afford, or encourage a shopping borrower to move forward with the loan. Credits are not always possible, but is something that lenders use when the numbers allow the transaction to close. Note: Lender credits are not allowable with HECM for Purchase transactions.

26 Remaining Principal Limit Generally borrowers choose to finance their closing costs through the HECM loan. The Remaining Principal Limit is the Principal Limit minus those closing costs. The loan comparison then subtracts from the Remaining Principal Limit any liens, mortgages or repair set-asides the HECM will pay off at closing. In addition you will find the LESA in this section. If the borrower(s) are required to have a LESA the total amount will be subtracted from the Remaining Principal Limit.

27 Liens and Mortgages The title report displays any liens or mortgages that must be satisfied with the HECM loan or the cash proceeds the borrower brings to closing. Other items on the title report that must be paid off at closing include Home Equity Lines of Credit (HELOCs), judgments, FIFAs (these are county-recorded liens against a debtor s real property), property and income taxes, defaulted loans, defaulted lines of credit, defaulted revolving credit, mechanic liens, etc. Note: Sometimes the borrower is not aware of items on the title because people don t usually pull their titles, the way they access their credit reports. Read and understand the various liens, and what your borrowers must do to satisfy them, so you can accurately communicate this to them.

28 Repair Set Asides If the appraiser determines that the home does not meet minimal FHA standards, the HECM loan requires that the borrower either address the issues before closing, or agree to a repair set-aside containing funds for specific repairs, usually related to safety or structural issues on the subject property. Lenders establish repair set-asides for an amount based on either the appraiser s estimated costs for repairs, or bids the borrower provides from licensed contractors. Note: HUD prohibits repair set-asides that exceed 15% of the value of the home. The formula for the set-aside amount is Contractor bids: 150% of the bid (the bid amount X 1.5) Appraiser Estimates: 200% of the estimate (the estimated amount X 2)

29 Tax and Insurance HECM borrowers must live in the property as their primary residence, keep the property up to FHA standards, and pay annual property taxes and insurance (homeowners and flood insurance, as applicable), as well as any other property charges. If they do not pay taxes and insurance or maintain the property, or if the underwriter has reason to believe they will not, the lender will require a LESA. This can be either a partially-funded or a fully-funded LESA. This all depends on willingness and capacity to pay their monthly obligations.

30 Available Principal Limit The Available Principal Limit is what remains after all closing costs, liens and other items are deducted from the loan. This is the amount that is available for the borrower to use. Note: Each column and amount represents a different loan product.

31 Available Funds and Requested Payments This section shows how the borrower chose to receive the available funds. If the loan comparison shows Available cash at closing the borrower can take this amount at closing, and during the first 12 months, per Mortgagee Letter The Cash Request field contains the amount the borrower chose to receive at closing. Note: Borrowers who do not withdraw the full amount during the first 12 months cannot withdraw the remaining balance later. The Total Line of Credit fields display the amount the borrower can hold for later withdrawal. A credit line is only available with ARM loans. The product type determines the amount of available credit during the first year and subsequent years.

32 Available Funds and Requested Payments, cont. Requested payments are monthly term or tenure payments the borrower chooses to receive, during the first year and through subsequent years. Note: Term and tenure payments are only available with ARM loans. Fixed loan products display N/A in this field.

33 Cap the Initial Disbursement Mortgagee Letter stipulates that borrowers can only take: 60% of their Principal Limit, Or, Mandatory obligations plus 10%. Borrowers who need more than 60% to pay for mandatory obligations, or to obtain the additional 10% above the mandatory obligations, pay a higher initial mortgage insurance payment (MIP). The MIP amount increases from 0.5% to 2.5% of the Maximum Claim Amount. The loan officer can cap the initial disbursement in ReverseVision on either the Loan screen or the Comparison screen so the borrower does not use more than 60% of the Principal Limit, and can perhaps bring additional funds to the closing table to save money on initial MIP. This section also allows you to see the total mandatory obligations in both an amount and a percentage.

34 Total Mandatory Obligations ReverseVision calculates all of the mandatory obligations. These include all closing costs, all mortgages, liens and any set asides, including repair set-asides. ReverseVision also calculates the percentage of mandatory obligations against the Principal Limit. This enables you and your borrowers to determine how close they are to the 60% initial limit of funds.

35 Initial Disbursement Limit ReverseVision calculates the exact amount of funds that are ReverseVision calculates the exact amount of funds that are available to the borrower at closing, and for the first 12 months. This amount displays as an exact figure, and as a percentage. The amount is based on a variety of factors, including the liens that must be paid off, the set-asides that are a part of the loan, and the loan product the borrower chose.

36 Initial Loan Balance The initial loan balance, or the unpaid principal balance (UPB) displays here as both a specific amount, and as a percentage. If the loan is a fixed rate HECM loan the Single Disbursement Lump Sum option is the only option available for loan proceeds. With a fixed rate HECM loan the borrower takes the lump sum at closing, or within the first 12 months, but cannot withdraw the remaining balance after 12 months. If they do not withdraw those funds, they lose them. This unavailable Principal Limit displays on the last line of the Comparison screen. This is the amount the borrower leaves on the table that WILL NOT be available for the future.

37 Summary Understanding the parts and numbers on the ReverseVision Comparison screen allows you to explain these numbers to your borrowers accurately and simply. It s important that they understand all the numbers, and how they are calculated, so they can make informed decisions. Take the time to understand these numbers and assure accuracy before you disclose the proposal or loan documents to your borrower. Take the time to explain the loan comparison to your borrower so everyone is on the same page regarding values, loan amounts, costs, fees, payoffs and limitations. HighTechLending, Inc., Licensed by the Department of Business Oversight under the California Residential Mortgage Lending Act. NMLS #7147. Licensed in AZ# , CA# , CO #7147, FL #7147, HI #7147, IL #MD , MD #21762, NC #L , NJ #7147, OR #ML4386, PA #49892, TX #7147,UT # , VA #MC-5962, WA # Main Street #350, Irvine, CA 92614

Brown - HECM / Reverse Product Guidelines. Loan Parameter HECM Fixed Variable Rate HECM

Brown - HECM / Reverse Product PRODUCTS & UNDERWRITING GUIDELINES Youngest Borrower Age Eligibility Occupancy Allowed States Allowed 62 years and above Owner Occupied Primary Residence Loans are accepted

Brown - HECM / Reverse Product PRODUCTS & UNDERWRITING GUIDELINES Youngest Borrower Age Eligibility Occupancy Allowed States Allowed 62 years and above Owner Occupied Primary Residence Loans are accepted

Enhance Your Financial Security. With a Home Equity Conversion Mortgage

Enhance Your Financial Security With a Home Equity Conversion Mortgage Liberty Home Equity Solutions, Inc. 10951 White Rock Road, Suite 200 Rancho Cordova, CA 95670 800.976.6211 www.reverse.org Unlock

Enhance Your Financial Security With a Home Equity Conversion Mortgage Liberty Home Equity Solutions, Inc. 10951 White Rock Road, Suite 200 Rancho Cordova, CA 95670 800.976.6211 www.reverse.org Unlock

The Math Behind HECMs P R E S E N T E R : C R A I G B A R N E S, R E V E R S E M O R T G A G E F U N D I N G

The Math Behind HECMs P R E S E N T E R : C R A I G B A R N E S, R E V E R S E M O R T G A G E F U N D I N G Session Objectives Today s session will: Illustrate how reverse mortgage interest rates are

The Math Behind HECMs P R E S E N T E R : C R A I G B A R N E S, R E V E R S E M O R T G A G E F U N D I N G Session Objectives Today s session will: Illustrate how reverse mortgage interest rates are

Introduction to Reverse Mortgages

Introduction to Reverse Mortgages Reverse Mortgages for Attorneys Revised May, 2017 Finance of America Reverse Slide 1 Reverse Mortgage Basics How the Program Works Types of Products Financial Assessment

Introduction to Reverse Mortgages Reverse Mortgages for Attorneys Revised May, 2017 Finance of America Reverse Slide 1 Reverse Mortgage Basics How the Program Works Types of Products Financial Assessment

2017 NRMLA Annual Meeting NOV SAN FRANCISCO

1 2017 NRMLA Annual Meeting NOV. 13 15 SAN FRANCISCO 2 The Math Behind the HECM Agenda 3 Interest Rates Expected Rates and Look Up Floor Note Rates Principal Limit Factors Payment Plan Math Ongoing MIP

1 2017 NRMLA Annual Meeting NOV. 13 15 SAN FRANCISCO 2 The Math Behind the HECM Agenda 3 Interest Rates Expected Rates and Look Up Floor Note Rates Principal Limit Factors Payment Plan Math Ongoing MIP

Plaza Home Mortgage Inc. Reverse Mortgage Presentation Basics. May 2018

Plaza Home Mortgage Inc. Reverse Mortgage Presentation Basics May 2018 Your GoToWebinar Toolbar Use speakers or a telephone to listen to the audio. Use the information in your toolbar to dial in from your

Plaza Home Mortgage Inc. Reverse Mortgage Presentation Basics May 2018 Your GoToWebinar Toolbar Use speakers or a telephone to listen to the audio. Use the information in your toolbar to dial in from your

Is a Reverse Mortgage Right for You?

Your Reverse Mortgage Information Brochure Is a Reverse Mortgage Right for You? Reverse mortgages are a unique type of loan that lets you convert the accrued equity of your home into usable funds. Home

Your Reverse Mortgage Information Brochure Is a Reverse Mortgage Right for You? Reverse mortgages are a unique type of loan that lets you convert the accrued equity of your home into usable funds. Home

PART 206 HOME EQUITY CON- VERSION MORTGAGE INSUR- ANCE

203.680 24 CFR Ch. II (4 1 12 Edition) 203.680 Approval of occupancy after conveyance. When an occupied property is conveyed to HUD before HUD has had an opportunity to consider continued occupancy (e.g.,

203.680 24 CFR Ch. II (4 1 12 Edition) 203.680 Approval of occupancy after conveyance. When an occupied property is conveyed to HUD before HUD has had an opportunity to consider continued occupancy (e.g.,

5-2 PERFORMING THE CALCULATIONS. All of the calculations in this chapter may be made with the aid of:

CHAPTER 5. CALCULATION OF PAYMENTS 5-1 PURPOSE. This chapter explains the procedures to follow in designing and changing the borrower's payment plan. This process involves calculating the borrower's net

CHAPTER 5. CALCULATION OF PAYMENTS 5-1 PURPOSE. This chapter explains the procedures to follow in designing and changing the borrower's payment plan. This process involves calculating the borrower's net

Closing Disclosure Form

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Good Faith Estimate (GFE)

") OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator Address Borrower Property Address Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan

OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator Address Borrower Property Address Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan

Reverse Mortgage Authorization Form

Reverse Mortgage Authorization Form Conflict of Interest Disclosure Cambridge Credit Counseling Corp provides counseling to help you make an informed decision concerning reverse mortgage products. We will

Reverse Mortgage Authorization Form Conflict of Interest Disclosure Cambridge Credit Counseling Corp provides counseling to help you make an informed decision concerning reverse mortgage products. We will

REVERSE MORTGAGE GUIDE

REVERSE MORTGAGE GUIDE Reap The Rewards Of A Lifetime Investment In Homeownership INVICTA MORTGAGE GROUP Better programs. Better service. Better financing. Licensed by PA Dept of Banking. NMLS# 111947

REVERSE MORTGAGE GUIDE Reap The Rewards Of A Lifetime Investment In Homeownership INVICTA MORTGAGE GROUP Better programs. Better service. Better financing. Licensed by PA Dept of Banking. NMLS# 111947

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) General 1) Q: When does the new RESPA Rule take effect? A: The November 2008 RESPA Rule was effective January 16, 2009. Implementation of the provisions are

New RESPA Rule FAQs (New items are in bold) General 1) Q: When does the new RESPA Rule take effect? A: The November 2008 RESPA Rule was effective January 16, 2009. Implementation of the provisions are

Guidance for Completing the 2010 Good Faith Estimate

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

REVERSE MORTGAGE. Line of Credit Guide ENHANCE. your retirement PLAN

REVERSE MORTGAGE Line of Credit Guide ENHANCE your retirement PLAN (800) 355-1993 Line of Credit Fact: The available funds in your line of credit can increase in value over time. (800) 355-1993 WHAT'S

REVERSE MORTGAGE Line of Credit Guide ENHANCE your retirement PLAN (800) 355-1993 Line of Credit Fact: The available funds in your line of credit can increase in value over time. (800) 355-1993 WHAT'S

The Common Sense Guide: HECM

The Common Sense Guide: HECM Home Equity Conversion Mortgage Prepared by: Ed O Connor Ed O Connor, NMLS# 17212 Your Credit Union Trusted Resource FHA made the program WE make the difference! 1 Steps to

The Common Sense Guide: HECM Home Equity Conversion Mortgage Prepared by: Ed O Connor Ed O Connor, NMLS# 17212 Your Credit Union Trusted Resource FHA made the program WE make the difference! 1 Steps to

Final RESPA Rule Requirements

Final RESPA Rule Requirements 1 Final RESPA Rule Requirements The Department of Housing and Urban Development (HUD) released its final rule on the Real Estate Settlement Procedures Act (RESPA) on November

Final RESPA Rule Requirements 1 Final RESPA Rule Requirements The Department of Housing and Urban Development (HUD) released its final rule on the Real Estate Settlement Procedures Act (RESPA) on November

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility Review credit, income, asset and appraisal guidelines Tips

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility Review credit, income, asset and appraisal guidelines Tips

Understanding Reverse Mortgages

Understanding Reverse Mortgages Their Role in Our Economy and the Business Opportunities Created Peter Bell President & CEO National Reverse Mortgage Lenders Association Demographics Household Wealth Profiles

Understanding Reverse Mortgages Their Role in Our Economy and the Business Opportunities Created Peter Bell President & CEO National Reverse Mortgage Lenders Association Demographics Household Wealth Profiles

A GFE must be issued when the originator receives an application OR six minimum pieces of information sufficient to complete an application including:

PROVIDENT BANK MORTGAGE RESPA REFORM Effective January 1, 2010 RESPA OVERVIEW The goal of RESPA Reform is to provide consumers with the information needed to readily understand loan terms and total settlement

PROVIDENT BANK MORTGAGE RESPA REFORM Effective January 1, 2010 RESPA OVERVIEW The goal of RESPA Reform is to provide consumers with the information needed to readily understand loan terms and total settlement

Tom Dickson, Financial Advisor Channel Leader Phone: E:

Tom Dickson, Financial Advisor Channel Leader Phone: 412.580.5954 E: TDickson@ReverseFunding.com Paul Pomeroy, HECM Specialist Phone: 503-421-0798 E: ppomeroy@reversefunding.com 2015 Reverse Mortgage Funding

Tom Dickson, Financial Advisor Channel Leader Phone: 412.580.5954 E: TDickson@ReverseFunding.com Paul Pomeroy, HECM Specialist Phone: 503-421-0798 E: ppomeroy@reversefunding.com 2015 Reverse Mortgage Funding

Guidance for Completing the 2010 Good Faith Estimate

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

INSTRUCTIONS FOR COMPLETION OF TITLE / SETTLEMENT AGENT APPLICATION

INSTRUCTIONS FOR COMPLETION OF TITLE / SETTLEMENT AGENT APPLICATION Upon your receipt of the attached application, please complete open entries and return the application and supporting documentation to:

INSTRUCTIONS FOR COMPLETION OF TITLE / SETTLEMENT AGENT APPLICATION Upon your receipt of the attached application, please complete open entries and return the application and supporting documentation to:

FAQ on ML Effective Date of the Mortgagee Letter (ML): When is the ML effective?

: When is the ML effective?") FAQ on ML 2011-11 1. Effective Date of the Mortgagee Letter (ML): When is the ML effective? The ML effective dates may vary depending on whether the policy section clarifies existing guidance; issues new

FAQ on ML 2011-11 1. Effective Date of the Mortgagee Letter (ML): When is the ML effective? The ML effective dates may vary depending on whether the policy section clarifies existing guidance; issues new

REAL ESTATE DICTIONARY

Adjustable-rate mortgage (ARM) -- Home loan in which the interest rate is changed periodically based on a standard financial index. Most ARMs have caps on how much an interest rate may increase. Amortization

Adjustable-rate mortgage (ARM) -- Home loan in which the interest rate is changed periodically based on a standard financial index. Most ARMs have caps on how much an interest rate may increase. Amortization

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

The Flawless Reverse Mortgage Signing Experience

The Flawless Reverse Mortgage Signing Experience Objectives Learn what a reverse mortgage is Recognize types of reverse mortgages available Understand restrictions and reasons for accelerated payment Identify

The Flawless Reverse Mortgage Signing Experience Objectives Learn what a reverse mortgage is Recognize types of reverse mortgages available Understand restrictions and reasons for accelerated payment Identify

Financial. Assessment

Financial Assessment What is a financial assessment? Effective in April 2015, the FHA began requiring borrowers to pass a financial assessment prior to obtaining the reverse mortgage. The goal of the financial

Financial Assessment What is a financial assessment? Effective in April 2015, the FHA began requiring borrowers to pass a financial assessment prior to obtaining the reverse mortgage. The goal of the financial

Options for Moving in Retirement Using the HECM for Purchase

Options for Moving in Retirement Using the HECM for Purchase By: John Salter, Ph.D., CFP SUMMARY Many retirees will choose to move from the large home in which they raised their family into something smaller

Options for Moving in Retirement Using the HECM for Purchase By: John Salter, Ph.D., CFP SUMMARY Many retirees will choose to move from the large home in which they raised their family into something smaller

Executive Summary of the 2017 TILA- RESPA Rule

1700 G Street NW, Washington, DC 20552 July 7, 2017 Executive Summary of the 2017 TILA- RESPA Rule On July 7, 2017, the Consumer Financial Protection Bureau (Bureau) issued a final rule (2017 TILA-RESPA

1700 G Street NW, Washington, DC 20552 July 7, 2017 Executive Summary of the 2017 TILA- RESPA Rule On July 7, 2017, the Consumer Financial Protection Bureau (Bureau) issued a final rule (2017 TILA-RESPA

Your Reverse Mortgage Guide. Reaping The Rewards Of A Lifetime Investment In Homeownership

Your Reverse Mortgage Guide Reaping The Rewards Of A Lifetime Investment In Homeownership Contents Make The Most Of Retirement!...3 Program Overview...3 4 What Is A Reverse Mortgage? Why Get A Reverse

Your Reverse Mortgage Guide Reaping The Rewards Of A Lifetime Investment In Homeownership Contents Make The Most Of Retirement!...3 Program Overview...3 4 What Is A Reverse Mortgage? Why Get A Reverse

Reverse Mortgages. Chapter 20 SYNOPSIS. Doni Dolfinger Paulette Wisch, CML Universal Lending Corporation What Is a Reverse Mortgage?

Chapter 20 Reverse Mortgages Doni Dolfinger Paulette Wisch, CML Universal Lending Corporation SYNOPSIS 20-1. What Is a Reverse Mortgage? 20-2. Reverse Mortgage Financial Assessment 20-3. Eligibility, Responsibility,

Chapter 20 Reverse Mortgages Doni Dolfinger Paulette Wisch, CML Universal Lending Corporation SYNOPSIS 20-1. What Is a Reverse Mortgage? 20-2. Reverse Mortgage Financial Assessment 20-3. Eligibility, Responsibility,

The Newfi First-Time Homebuyer s Guide

The Newfi First-Time Homebuyer s Guide Newfi is a licensed tradename of Nexera Holding LLC. NMLS No. 1231327; HUD Lender ID 0038900004. Newfi is an Equal Housing Lender. The basics What is a mortgage?

The Newfi First-Time Homebuyer s Guide Newfi is a licensed tradename of Nexera Holding LLC. NMLS No. 1231327; HUD Lender ID 0038900004. Newfi is an Equal Housing Lender. The basics What is a mortgage?

GINNIE MAE Guaranteed Home Equity Conversion Mortgage-Backed Securities (Issuable in Series)

") Base Prospectus July 1, 2011 Government National Mortgage Association GINNIE MAE Guaranteed Home Equity Conversion Mortgage-Backed Securities (Issuable in Series) The Government National Mortgage Association

Base Prospectus July 1, 2011 Government National Mortgage Association GINNIE MAE Guaranteed Home Equity Conversion Mortgage-Backed Securities (Issuable in Series) The Government National Mortgage Association

Shopping for your home loan. Settlement cost booklet

Shopping for your home loan Settlement cost booklet CFPB (Consumer Financial Protection Bureau) January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development.

Shopping for your home loan Settlement cost booklet CFPB (Consumer Financial Protection Bureau) January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development.

Chicago Volunteer Legal Services Access to Justice Program April 27, 2017

Chicago Volunteer Legal Services Access to Justice Program April 27, 2017 R. Dennis Smith The John Marshall Law School Prepared under grants from the City of Chicago (TACIT) and the Retirement Research

Chicago Volunteer Legal Services Access to Justice Program April 27, 2017 R. Dennis Smith The John Marshall Law School Prepared under grants from the City of Chicago (TACIT) and the Retirement Research

Unlocking the Power of Home

Unlocking the Power of Home The Surprising Secret Weapon In Today s Retirement Planning Toolkit Becky Bell, VP Who Is Longbridge Financial, LLC? We are a national reverse-only lender focused on making

Unlocking the Power of Home The Surprising Secret Weapon In Today s Retirement Planning Toolkit Becky Bell, VP Who Is Longbridge Financial, LLC? We are a national reverse-only lender focused on making

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

DEFINITION OF COMMON TERMS

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

After-tax APRPlus The APRPlus taking into account the effect of income taxes.

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

Closing Information Transaction Information Loan Information. VA Property Lender Loan ID # MIC #

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Reverse mortgages. A discussion guide. Consumer Financial Protection Bureau

Reverse mortgages A discussion guide Consumer Financial Protection Bureau About this discussion guide This guide gives an overview of many key concepts of reverse mortgages. A qualified reverse mortgage

Reverse mortgages A discussion guide Consumer Financial Protection Bureau About this discussion guide This guide gives an overview of many key concepts of reverse mortgages. A qualified reverse mortgage

ENJOY your best YEARS. An Informational Guide for Purchasing a Home with a Reverse Mortgage

(800) 355-1993 NMLS #2052 ENJOY your best YEARS An Informational Guide for Purchasing a Home with a Reverse Mortgage 1... WHAT S INSIDE WHAT IS A REVERSE MORTGAGE & HOW DOES IT WORK? HOW IS IT USED? REVERSE

(800) 355-1993 NMLS #2052 ENJOY your best YEARS An Informational Guide for Purchasing a Home with a Reverse Mortgage 1... WHAT S INSIDE WHAT IS A REVERSE MORTGAGE & HOW DOES IT WORK? HOW IS IT USED? REVERSE

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

Good for 120 days. Minimum Required Investment Little to NO reserves ARMS allowed Manual Underwriting is Allowed

FHA PURCHASE Credit Score 620+ Score required ----------- 580-619 -with 2 month PITI reserves -NO gift funds -Max base loan $417,000 Max LTV 1/1/5 3/1/5 5/2/6 ARMs Appraisal 96.5% Allowed Yes Good for

FHA PURCHASE Credit Score 620+ Score required ----------- 580-619 -with 2 month PITI reserves -NO gift funds -Max base loan $417,000 Max LTV 1/1/5 3/1/5 5/2/6 ARMs Appraisal 96.5% Allowed Yes Good for

Journal CSA. Using a Reverse Mortgage to Age in Place in One s Home Number 68 Vol. 1, Patricia Whitlock, CRMP

CSA Journal Using a Reverse Mortgage to Age in Place in One s Home Number 68 Vol. 1, 2017 Patricia Whitlock, CRMP This document is authorized for use only by Patricia Whitlock. Copying or posting is an

CSA Journal Using a Reverse Mortgage to Age in Place in One s Home Number 68 Vol. 1, 2017 Patricia Whitlock, CRMP This document is authorized for use only by Patricia Whitlock. Copying or posting is an

GFE/TIL AND COC WORKFLOW

Table of Contents Page 1 of the GFE... 2 Tolerance Levels... 5 Page 2 of the GFE... 7 Box 6 of the GFE... 12 How to Calculate Transfer Tax... 13 Page 3 of the GFE... 14 Events Triggering Re-disclosure...

Table of Contents Page 1 of the GFE... 2 Tolerance Levels... 5 Page 2 of the GFE... 7 Box 6 of the GFE... 12 How to Calculate Transfer Tax... 13 Page 3 of the GFE... 14 Events Triggering Re-disclosure...

HUD s New RESPA Rule

1300 Nineteenth Street, NW Fifth Floor Washington, DC 20036 202.628.2000 www.wbsk.com HUD s New RESPA Rule November 24, 2008 On November 17, 2008 the United States Department of Housing and Urban Development

1300 Nineteenth Street, NW Fifth Floor Washington, DC 20036 202.628.2000 www.wbsk.com HUD s New RESPA Rule November 24, 2008 On November 17, 2008 the United States Department of Housing and Urban Development

February 2016 FEBRUARY Sunday Monday Tuesday Wednesday Thursday Friday Saturday. CD is placed in the mail IF DELIVERED BY OVERNIGHT MAIL...

DELIVERY METHODS & TIMING CHEAT SHEET IF DELIVERED BY MAIL... Closing Disclosure (CD) is sent to borrower in the mail 3 day mailing rule applies for the receipt of the disclosure Then 3 day waiting period

DELIVERY METHODS & TIMING CHEAT SHEET IF DELIVERED BY MAIL... Closing Disclosure (CD) is sent to borrower in the mail 3 day mailing rule applies for the receipt of the disclosure Then 3 day waiting period

First Time Homebuyers

First Time Homebuyers Presented By: Rich Goodwin, Vice President of Mortgage Lending Copyright 2000-2014 Guaranteed Rate. All rights reserved. Our Competitive Advantage Fast and transparent mortgage process

First Time Homebuyers Presented By: Rich Goodwin, Vice President of Mortgage Lending Copyright 2000-2014 Guaranteed Rate. All rights reserved. Our Competitive Advantage Fast and transparent mortgage process

Underwriting Guideline Matrix

: Program / Product Codes: 30 Year Fixed (W130) 15 Year Fixed (W132) Subject to Change Without Notice Valid as of: 12/18/2017 Copyright 2017 Skyline Financial Corp. dba NewLeaf Wholesale, Nationwide Mortgage

: Program / Product Codes: 30 Year Fixed (W130) 15 Year Fixed (W132) Subject to Change Without Notice Valid as of: 12/18/2017 Copyright 2017 Skyline Financial Corp. dba NewLeaf Wholesale, Nationwide Mortgage

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

Reverse Mortgage FAQs

Reverse Mortgage FAQs NMLS# 1313859 Frequently Asked Questions about Reverse Mortgages At ReverseMortgages.com, we get a lot of questions from our clients about reverse mortgages, the process of getting

Reverse Mortgage FAQs NMLS# 1313859 Frequently Asked Questions about Reverse Mortgages At ReverseMortgages.com, we get a lot of questions from our clients about reverse mortgages, the process of getting

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 9 GFE Interest rate expiration... 9 GFE Expiration... 10 GFE Denial... 10 GFE

New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 9 GFE Interest rate expiration... 9 GFE Expiration... 10 GFE Denial... 10 GFE

CHILDREN & CAREGIVERS A FAMILY GUIDE TO REVERSE MORTGAGES

NMLS #7230 CHILDREN & CAREGIVERS A FAMILY GUIDE TO REVERSE MORTGAGES 89% The percentage of adult children who want their parents to pay their bills and not worry about leaving an inheritance. *Based on

NMLS #7230 CHILDREN & CAREGIVERS A FAMILY GUIDE TO REVERSE MORTGAGES 89% The percentage of adult children who want their parents to pay their bills and not worry about leaving an inheritance. *Based on

TRID TILA RESPA Integrated Disclosures

Experience Extraordinary TRID TILA RESPA Integrated Disclosures May 13, 2015 Loan Estimate Completion Kara Lamphere Loan Estimate Breakdown The GFE and Initial TIL combined = the Loan Estimate ( LE ) http://files.consumerfinance.gov/f/201403_cfpb_loan-estimate_model-form-h24.pdf

Experience Extraordinary TRID TILA RESPA Integrated Disclosures May 13, 2015 Loan Estimate Completion Kara Lamphere Loan Estimate Breakdown The GFE and Initial TIL combined = the Loan Estimate ( LE ) http://files.consumerfinance.gov/f/201403_cfpb_loan-estimate_model-form-h24.pdf

Market Update RESPA Revisions to the GFE and HUD-1

Market Update RESPA Revisions to the GFE and HUD-1 PHH Mortgage is working to make the transition easier for you and your customers Effective for loan applications taken as of January 1, 2010, all lenders

Market Update RESPA Revisions to the GFE and HUD-1 PHH Mortgage is working to make the transition easier for you and your customers Effective for loan applications taken as of January 1, 2010, all lenders

ONE-TIME CLOSE CONSTRUCTION LOAN INFORMATION PACKET

ONE-TIME CLOSE CONSTRUCTION LOAN INFORMATION PACKET At AmeriFirst we are committed to providing you with all the information you need regarding your construction loan. This guide will walk you through

ONE-TIME CLOSE CONSTRUCTION LOAN INFORMATION PACKET At AmeriFirst we are committed to providing you with all the information you need regarding your construction loan. This guide will walk you through

FHA Streamline Program Conforming and High Balance Fixed Rate and ARMs

FHA Streamline Program Conforming and High Balance Fixed Rate and ARMs Primary Residence Transaction Type Units LTV CLTV Loan Amount 1 Streamline w/appraisal 4 1 90% 90% FHA Limit Streamline w/ Appraisal

FHA Streamline Program Conforming and High Balance Fixed Rate and ARMs Primary Residence Transaction Type Units LTV CLTV Loan Amount 1 Streamline w/appraisal 4 1 90% 90% FHA Limit Streamline w/ Appraisal

HOME BUYING MADE EASY

HOME BUYING MADE EASY Know what you need to get it right. Brought to you by: PNC Mortgage Loan Officer NMLS# HOME BUYING MADE EASY PNC, PNC HomeHQ, PNC Home Insight

HOME BUYING MADE EASY Know what you need to get it right. Brought to you by: PNC Mortgage Loan Officer NMLS# HOME BUYING MADE EASY PNC, PNC HomeHQ, PNC Home Insight

Closing Information Transaction Information Loan Information. VA Property Loan ID # Lender MIC # Sale Price $

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Financial Assessment

Financial Assessment K A R I N H I L L U. S. D E P T. O F H O U S I N G & U R B A N D E V E L O P M E N T P A U L F I O R E A M E R I C A N A D V I S O R S G R O U P T R A C Y M I L L I G A N O N E R E

Financial Assessment K A R I N H I L L U. S. D E P T. O F H O U S I N G & U R B A N D E V E L O P M E N T P A U L F I O R E A M E R I C A N A D V I S O R S G R O U P T R A C Y M I L L I G A N O N E R E

Closing Disclosure $0 NO. $0 a month. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

If You Could Live In Your Home Forever and Never Have To Make A Regular Monthly Mortgage Payment, Would You Do It?

If You Could Live In Your Home Forever and Never Have To Make A Regular Monthly Mortgage Payment, Would You Do It? Hint: Nearly everyone I ask says YES! Some say What s the Catch!? -wrh It is an amazing

If You Could Live In Your Home Forever and Never Have To Make A Regular Monthly Mortgage Payment, Would You Do It? Hint: Nearly everyone I ask says YES! Some say What s the Catch!? -wrh It is an amazing

2010 HUD-1: New RESPA Rule Overview

CB Title Agency of NY, LLC CB Title Group, LLC 140 Mountain Avenue Suite 101 Springfield, NJ 07081 P: 973-921-0990 F: 973-921-0902 www.cbtitlegroup.com Date: November 13, 2009 To: All Clients and Friends

CB Title Agency of NY, LLC CB Title Group, LLC 140 Mountain Avenue Suite 101 Springfield, NJ 07081 P: 973-921-0990 F: 973-921-0902 www.cbtitlegroup.com Date: November 13, 2009 To: All Clients and Friends

Is A Reverse Mortgage Right for You?

Is A Reverse Mortgage Right for You? NewRetirement s Guide to Reverse Mortgages www.newretirement.com 888-411-RETIRE (7384) Table of Contents What is a Reverse Mortgage? Are You Eligible For a Reverse

Is A Reverse Mortgage Right for You? NewRetirement s Guide to Reverse Mortgages www.newretirement.com 888-411-RETIRE (7384) Table of Contents What is a Reverse Mortgage? Are You Eligible For a Reverse

HECM FINANCIAL ASSESSMENT AND PROPERTY CHARGE GUIDE REVISED JULY 13, 2016 EFFECTIVE FOR HECM CASE NUMBERS ASSIGNED ON OR AFTER OCTOBER 3, 2016

HECM FINANCIAL ASSESSMENT AND PROPERTY CHARGE GUIDE REVISED JULY 13, 2016 EFFECTIVE FOR HECM CASE NUMBERS ASSIGNED ON OR AFTER OCTOBER 3, 2016 7-13-16 Page 1 Table of Contents Financial Assessment Overview...

HECM FINANCIAL ASSESSMENT AND PROPERTY CHARGE GUIDE REVISED JULY 13, 2016 EFFECTIVE FOR HECM CASE NUMBERS ASSIGNED ON OR AFTER OCTOBER 3, 2016 7-13-16 Page 1 Table of Contents Financial Assessment Overview...

Shopping for your home loan

Consumer Financial Protection Bureau This booklet was initially prepared by the U.S. Department of Housing and Urban Development. The Consumer Financial Protection Bureau (CFPB) has made technical updates

Consumer Financial Protection Bureau This booklet was initially prepared by the U.S. Department of Housing and Urban Development. The Consumer Financial Protection Bureau (CFPB) has made technical updates

203(k) Program Full and Streamline

Program Full and Streamline") General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home The new first mortgage includes the purchase price or

General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home The new first mortgage includes the purchase price or

Reverse Mortgage. Examination Procedures

Examination Procedures Reverse Mortgage Servicing Exam Date: Exam ID No. These examination procedures apply to reverse mortgage Prepared By: servicing and are a stand-alone resource to complete a reverse

Examination Procedures Reverse Mortgage Servicing Exam Date: Exam ID No. These examination procedures apply to reverse mortgage Prepared By: servicing and are a stand-alone resource to complete a reverse

Mortgage. A Beginner s. Rates. Guide

Mortgage Rates A Beginner s Guide US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

Mortgage Rates A Beginner s Guide US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

Home Equity Conversion Mortgage HECM. Presented By: Doris Batty NMLS #

Home Equity Conversion Mortgage HECM Presented By: Doris Batty NMLS # 420458 What is a Reverse Mortgage? Created for homeowners 62 & older. Converting their home s equity into cash. Payment stream reversed.

Home Equity Conversion Mortgage HECM Presented By: Doris Batty NMLS # 420458 What is a Reverse Mortgage? Created for homeowners 62 & older. Converting their home s equity into cash. Payment stream reversed.

Good Faith Estimate Training 2/3/14

Good Faith Estimate Training 2/3/14 Objectives At the end of this training you will be able to: Understand RESPA Reform Recognize a complete Loan Application Understand GFE requirements Know requirements

Good Faith Estimate Training 2/3/14 Objectives At the end of this training you will be able to: Understand RESPA Reform Recognize a complete Loan Application Understand GFE requirements Know requirements

Why Should You Consider Refinancing?

Why Should You Consider Refinancing? Reason 1: Lower Your Interest Rate Interest rates may have gone down due to market conditions since you purchased or last refinanced your home. Since the interest rate

Why Should You Consider Refinancing? Reason 1: Lower Your Interest Rate Interest rates may have gone down due to market conditions since you purchased or last refinanced your home. Since the interest rate

Listing of Various HUD Handbook Changes

Listing of Various HUD Handbook 4000.1 Changes Please note this list is not all-inclusive, all FHA loans with cases assigned on or after 9/14/15 must meet all new handbook requirements.. http://portal.hud.gov/hudportal/hud?src=/program_offices/administration/hudclips/handbooks/hsgh

Listing of Various HUD Handbook 4000.1 Changes Please note this list is not all-inclusive, all FHA loans with cases assigned on or after 9/14/15 must meet all new handbook requirements.. http://portal.hud.gov/hudportal/hud?src=/program_offices/administration/hudclips/handbooks/hsgh

Enjoy Retirement In Your Dream Home HOME EQUITY CONVERSION MORTGAGE FOR PURCHASE GUIDE

Enjoy Retirement In Your Dream Home HOME EQUITY CONVERSION MORTGAGE FOR PURCHASE GUIDE At TowneBank Mortgage, we recognize the unique financial needs of the senior community. A Home Equity Conversion

Enjoy Retirement In Your Dream Home HOME EQUITY CONVERSION MORTGAGE FOR PURCHASE GUIDE At TowneBank Mortgage, we recognize the unique financial needs of the senior community. A Home Equity Conversion

RESP RE A SP A & & Good Good Fa F ith ith Estima tima e R quir quir d e d Disclosure Disclosur s Corresponden Corr esponden t Lending July 22, 2013

RESPA & Good Faith Estimate Required Disclosures Correspondent Lending July 22, 2013 What s Different and When is it Effective? January 1, 2010 (1003 dated on or after) New GFE form: does not indicate

RESPA & Good Faith Estimate Required Disclosures Correspondent Lending July 22, 2013 What s Different and When is it Effective? January 1, 2010 (1003 dated on or after) New GFE form: does not indicate

Closing Disclosure $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

TRID RULE UPDATES AND THE BLACK HOLE CONUNDRUM JONATHAN FOXX *

TRID RULE UPDATES AND THE BLACK HOLE CONUNDRUM JONATHAN FOXX * On August 11, 2017, the Consumer Financial Protection Bureau ( Bureau ) issued a Final Rule (2017 TILA-RESPA Rule or 2017 Rule, hereinafter

TRID RULE UPDATES AND THE BLACK HOLE CONUNDRUM JONATHAN FOXX * On August 11, 2017, the Consumer Financial Protection Bureau ( Bureau ) issued a Final Rule (2017 TILA-RESPA Rule or 2017 Rule, hereinafter

One loan to renovate. Your homebuyer guide to renovation

One loan to renovate Your homebuyer guide to renovation Maybe you ve found the perfect location, but the house needs improving. Maybe staying in your current (but outdated) home is what s important. Either

One loan to renovate Your homebuyer guide to renovation Maybe you ve found the perfect location, but the house needs improving. Maybe staying in your current (but outdated) home is what s important. Either

SELF-HELP ENTERPRISES CITY OF VISALIA Affordable Housing Program HOME funded 2 nd mortgage loan

SELF-HELP ENTERPRISES CITY OF VISALIA Affordable Housing Program HOME funded 2 nd mortgage loan (for families at or below 80% AMI) Program is administered by Self-Help Enterprises, and overseen by the

SELF-HELP ENTERPRISES CITY OF VISALIA Affordable Housing Program HOME funded 2 nd mortgage loan (for families at or below 80% AMI) Program is administered by Self-Help Enterprises, and overseen by the

Osceola County Purchase Assistance Program Guidelines

Osceola County Purchase Assistance Program Guidelines Purchase Assistance Program Objective The Osceola County Down payment Assistance Program (DPA) is made available through the State Housing Initiatives

Osceola County Purchase Assistance Program Guidelines Purchase Assistance Program Objective The Osceola County Down payment Assistance Program (DPA) is made available through the State Housing Initiatives

RESIDENTIAL CONSTRUCTION LENDING POLICY

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

ditech BUSINESS LENDING FHA STANDARD REFINANCE PRODUCT

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING FHA STANDARD REFINANCE PRODUCT FHA Fixed Rate and ARM Mortgages for Rate and Term Refinance, Cash-Out Refinance and Simple Refinance Transactions Fixed Rate

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING FHA STANDARD REFINANCE PRODUCT FHA Fixed Rate and ARM Mortgages for Rate and Term Refinance, Cash-Out Refinance and Simple Refinance Transactions Fixed Rate

For Preview Only - Please Do Not Copy

Information & Instructions: HUD 1 Settlement closing statement 1. Section 5 of the Real Estate Settlement Procedures Act of 1974 (Public Law 93-533), effective on June 30, 1976 (RESPA), requires certain

Information & Instructions: HUD 1 Settlement closing statement 1. Section 5 of the Real Estate Settlement Procedures Act of 1974 (Public Law 93-533), effective on June 30, 1976 (RESPA), requires certain

REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY

POLICY") I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

FHA CREDIT QUALIFYING STREAMLINE REFINANCE

Table of Contents 1. Eligible Mortgage Product-Existing Loan... 2 2. FICO... 2 3. Eligible Mortgage Product-New Loan... 2 4. Maximium Loan Amount... 2 5. Maximium LTV/CLTV... 2 6. MIP Requirements..2-4

Table of Contents 1. Eligible Mortgage Product-Existing Loan... 2 2. FICO... 2 3. Eligible Mortgage Product-New Loan... 2 4. Maximium Loan Amount... 2 5. Maximium LTV/CLTV... 2 6. MIP Requirements..2-4

REV-1 TABLE OF CONTENTS. Page CHAPTER 1. GENERAL INFORMATION

CHAPTER 1. GENERAL INFORMATION TABLE OF CONTENTS Page 1-1 LEGISLATIVE HISTORY... 1-1 1-2 PURPOSE OF THE PROGRAM... 1-1 1-3 CHARACTERISTICS OF THE MORTGAGE... 1-1 1-4 PRINCIPAL LIMIT... 1-2 1-5 PAYMENT

CHAPTER 1. GENERAL INFORMATION TABLE OF CONTENTS Page 1-1 LEGISLATIVE HISTORY... 1-1 1-2 PURPOSE OF THE PROGRAM... 1-1 1-3 CHARACTERISTICS OF THE MORTGAGE... 1-1 1-4 PRINCIPAL LIMIT... 1-2 1-5 PAYMENT

DRAFT SAMPLE. Closing Information Transaction Information Loan Information

REFINANCE Closing Disclosure DRAFT SAMPLE GREEN = HIGHLIGHTED SECTIONS NEEDED FROM CLSG AGENT RED = LENDER WILL PROVIDE Closing Information Transaction Information Loan Information Date Issued 11/19/2015

REFINANCE Closing Disclosure DRAFT SAMPLE GREEN = HIGHLIGHTED SECTIONS NEEDED FROM CLSG AGENT RED = LENDER WILL PROVIDE Closing Information Transaction Information Loan Information Date Issued 11/19/2015

Home Equity Reverse Mortgage Information Technology (HERMIT) HERMIT System Changes Release 5.4

HERMIT System Changes Release 5.4") Home Equity Reverse Mortgage Information Technology (HERMIT) HERMIT System Changes Release 5.4 Release Date: 09/19/17 Document Date: 09/07/17 September 2017 Version 1.0 INTRODUCTION HERMIT SYSTEM CHANGES

Home Equity Reverse Mortgage Information Technology (HERMIT) HERMIT System Changes Release 5.4 Release Date: 09/19/17 Document Date: 09/07/17 September 2017 Version 1.0 INTRODUCTION HERMIT SYSTEM CHANGES

FHA Streamline Refinance Training

FHA Streamline Refinance Training Offered through First Mortgage Corporation Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This

FHA Streamline Refinance Training Offered through First Mortgage Corporation Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This

MEGA ALT ARM (MA5/1)

") MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law MEMORANDUM. RESPA 101 The New Good Faith Estimate (GFE) Rules

Rules") BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law J. Alton Alsup 10333 Richmond, Suite 860 Telephone 713/468-0400 Board Certified in Residential Real Estate Law Texas Board of Legal Specialization

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law J. Alton Alsup 10333 Richmond, Suite 860 Telephone 713/468-0400 Board Certified in Residential Real Estate Law Texas Board of Legal Specialization

RESPA: Regulation & Integration Process Guide

- 1 - Reverse Mortgage Wholesale & Correspondent Lending RESPA: Regulation & Integration Process Guide The Real Estate Settlement and Procedures Act (RESPA) is a consumer protection statute designed to

- 1 - Reverse Mortgage Wholesale & Correspondent Lending RESPA: Regulation & Integration Process Guide The Real Estate Settlement and Procedures Act (RESPA) is a consumer protection statute designed to

CFPB Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

WHOLESALE Good Faith Estimate Compliance Manual

WHOLESALE Good Faith Estimate Compliance Manual Understanding the 2010 GFE Compliance Department 2/2/2015 2015 Pacific One Lending. http://www.nmlsconsumeraccess.org. Rates, fees and programs are subjected

WHOLESALE Good Faith Estimate Compliance Manual Understanding the 2010 GFE Compliance Department 2/2/2015 2015 Pacific One Lending. http://www.nmlsconsumeraccess.org. Rates, fees and programs are subjected

CFPB TRAINING - EXERCISE 6

Overview: Create a Closing Disclosure Form (CDF) form and one HUD where the HUD is for a Home Equity Line of Credit (HELOC). Use the steps and additional information below for help with key items and where

Overview: Create a Closing Disclosure Form (CDF) form and one HUD where the HUD is for a Home Equity Line of Credit (HELOC). Use the steps and additional information below for help with key items and where

Integrated Disclosure Vocabulary List. Term Definition as of 8/1/2015 Adjustments and Other Credits

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

Closing Disclosure $ % $ $ $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower