Understanding Reverse Mortgages

|

|

|

- Buck Garrett

- 5 years ago

- Views:

Transcription

1 Understanding Reverse Mortgages Their Role in Our Economy and the Business Opportunities Created Peter Bell President & CEO National Reverse Mortgage Lenders Association

2 Demographics Household Wealth Profiles Presentation Overview What is a Reverse Mortgage Originating HECM Loans Business Opportunities

3 Demographics

4

5 Source: Joint Center for Housing Studies, Housing and Tenure Projections 2016

6 The number of Americans age 65 and older will more than double by 2060 (US Census Bureau, 2014)

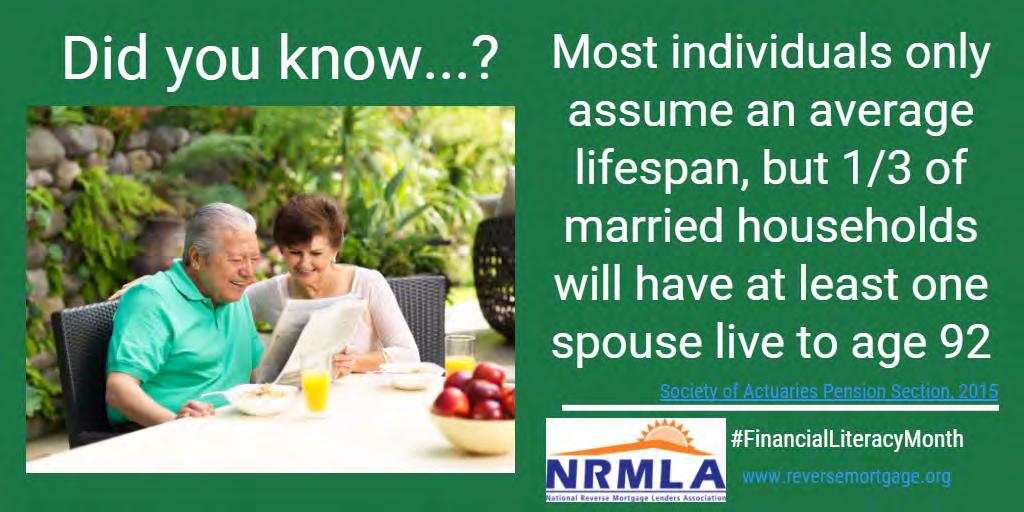

7 By 2030, there will be more than 74 million adults aged 65 and older in the U.S., accounting for 20% of the population. Aging in America For the first time in our nation s history, the 65 and older cohort will eclipse the total number of Americans who are under 18 years old. This aging population will have longer lifespans and more years spent in retirement, outside of the paid workforce -- one in four 65- year-olds today are expected to live past age 90 and one in 10 are expected to live past 95.

8

9 Household Wealth Profiles

10 Falling Short: 50% of households are at risk of being unable to maintain their pre-retirement standard of living in retirement.

11 Retirement Insecurity For many older Americans, making their meager resources last over an unknown period of time is a primary stress factor. They are one mishap away from facing a personal financial crisis.

12 Retirement Insecurity Social Security provides most of the retirement income for about half of households 65 and older But replaces only 40% of pre-retirement earnings

13 Only 29% of households on the cusp of retirement (aged 50-64) will leave the workforce with a traditional pension, compared to 49% of today s 65-and-older households. Retirement Insecurity A majority, 60%, of US workers report that their total household savings and investments, excluding the value of their home and any defined benefit pension, is less than $25,000.

14 Household Demographics # in Millions Total Households 116M Owner Occupied 74M Aged 65 & Older 21M Mortgage Free 15M

15 Home Equity

16 Home equity has the potential to enhance retirement security because the homeownership rate generally exceeds ownership rates for most financial assets. According to the Federal Reserve s 2013 Survey of Consumer Finances: 65.2 percent of American households owned their primary residences 49.2 percent had retirement accounts 19.2 percent had cash-value life insurance policies 13.8 percent had stocks, and 10 percent had savings bonds (Bricker et al. 2014)

17 Senior Home Equity The equity accumulated in a home, to many American families, represents the largest component of personal wealth. Typical retiree households might have one or two incomes from Social Security, a modest pension and/or limited income from low-yielding fixedincome instruments, and, perhaps, a diminished 401(k) account. The equity they have built up in their home is often, by far, their greatest asset, an important resource for funding their future. The homeownership rate among older Americans is nearly 80% and in the fourth quarter of 2016, homeowners aged 62 and older held a combined $6.2 trillion in home equity, a $170 billion increased over the previous quarter. Since Q1 2000, home equity has increased more than $4 trillion, since the National Reverse Mortgage Lenders Association and data analytics firm Risk Span, Inc. first reported the aggregate amount of senior home equity as part of the Reverse Mortgage Market Index.

18 Senior Home Equity

19 Reverse Mortgage Market Index

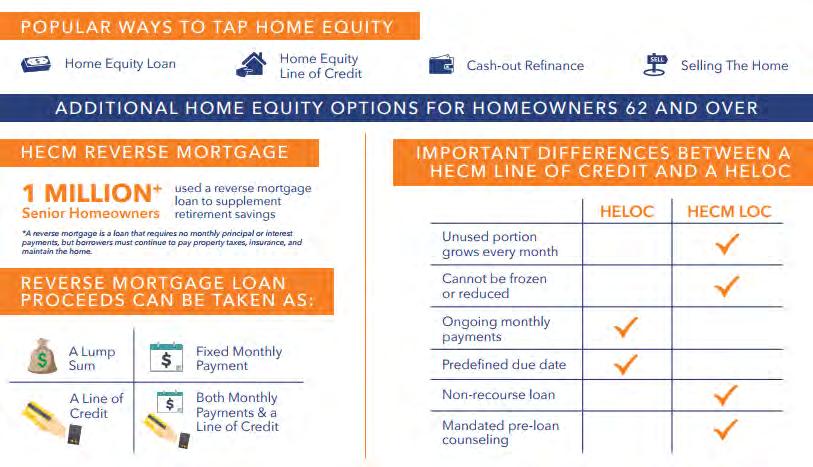

20 Equity Extraction Tools

21

22 You spend a career supporting your home and then when you retire, your home supports you What is a reverse mortgage?

23 What is a reverse mortgage? A reverse mortgage, in simple terms, is a home equity loan that creates liquidity for older homeowners and does not need to be repaid until the borrower moves, sells the house, or passes away.

24 What is a reverse mortgage? Loan amounts are determined by a formula based on the home s appraised value, the youngest borrower s age, and current interest rates.

25 What is a reverse mortgage? Borrowers, or their heirs, typically repay the loan with either proceeds from the sale of the house or with funds available from other assets.

26 What is a reverse mortgage? Reverse mortgages were designed to help seniors, aged 62 and older, convert equity into cash that could be used to supplement a fixed retirement income and pay for medical and other daily expenses.

27 What is a reverse mortgage? Over time and with the help of financial planning experts, we ve learned reverse mortgages are a versatile and beneficial tool in a comprehensive retirement income plan

28 What makes a reverse mortgage a good way to access home equity? Borrowers can use loan proceeds without restriction Flexibility Borrowers choose when to make P&I repayments (Monthly or wait until they are required to do so at the end of the loan) Borrowers choose how they want to receive loan proceeds

29 What s a HECM? HECMs are reverse mortgages that are insured by the Federal Housing Administration Home Equity Conversion Mortgage

30 The National Housing Act of 1987, Section 255 outlined the specifics of the demonstration program. The purpose of the program was: Brief History of HECM To meet the special needs of elderly homeowners by reducing the effect of the economic hardship caused by increasing costs of meeting health, housing and subsistence needs at a time of reduced income, through insurance of home equity conversion mortgages to permit the conversion of a portion of accumulated home equity into liquid assets. Among the requirements contained in the original statute were: Adequate third-party counseling including explaining other financial options A fixed or variable interest rate or future sharing of property appreciation A list of disclosures to be delivered at least 10 days before closing Borrower protection against disappearance of lender & obligations beyond fair market value of their home at sale Scheduled reports to Congress

31 HECM & FHA Insurance HUD s HECM program offers FHA insurance for lenders who originate reverse mortgages to senior homeowners. Subject to the FHA s loan limit of $679,650 Some lenders offer proprietary loans including jumbo reverse mortgages for high value homes

32 HECM and FHA Insurance Borrower pays the insurance fees, and those charges are added to the borrower s outstanding principal balance. Private sector lenders, not the federal government, make reverse mortgages.

33 Insurance protects lenders against losses on their loans. These lenders must be FHAapproved, and the program statute and regulations determine the loan amounts available to borrowers. HECM and FHA Insurance The borrower is required to pay an upfront Mortgage Insurance Premium, as well as an annual Mortgage Insurance Premium.

34 Insurance protects lenders against losses on their loans. These lenders must be FHAapproved, and the program statute and regulations determine the loan amounts available to borrowers. HECM and FHA Insurance The borrower is required to pay an upfront Mortgage Insurance Premium, as well as an annual Mortgage Insurance Premium.

35 HECM is a Non-Recourse Loan Source: Understanding Reverse At the resolution of the loan, if the loan balance exceeds the value of the collateralized property, HUD reimburses the lender for the difference, up to a Maximum Claim Amount.

36 The Basics Homeowner maintains ownership and title, not the lender One homeowner must be 62 or older Non-borrowing spouses may be under 62 Monthly mortgage payments are not required SS or Medicare are not affected by draws The borrower can sell the home at any time Age, interest rates, and home value determine principal limits

37 Borrower Requirements & Responsibilities Pay property taxes Pay home insurance Pay all other property charges Occupy home as primary residence Maintain home

38 What are the Costs? Out of pocket costs Appraisal fee and Counseling fee Closing costs Origination fee Initial Mortgage Insurance Premium (IMIP) Traditional third party fees Ongoing Costs Mortgage insurance Interest Servicing fees (if applicable)

39 Borrower costs & obligations Upfront costs: Initial FHA mortgage insurance premium (IMIP) Origination fee Third party costs Ongoing costs: Interest charges FHA mortgage insurance premiums Servicing fees if charged

40 Key Terms 1 2 Principal Limit Maximum Claim Amount

41 Principal Limit Calculations Principal Limit Factors (PLFs) Not the same as Loan-to-Value (LTV) Based on Age and Expected Interest Rates Older borrowers GENERALLY have higher PLFs Borrowers with younger spouses may have lower PLFs Expected Rates are calculated using the 10-year LIBOR SWAP Principal Limit Factors - Percentages (%) Principal Limits - Dollars ($)

42 PLF Table Age R0 PLF0 R1 PLF1 R2 PLF2 R3 PLF3 R4 PLF4 R5 PLF5 R6 PLF6 R7 PLF7 4% Interest Rates

43

44

45 Reverse Mortgage Payment Plan Options Payment Plan Description Line of Credit Borrower funds are available as needed upon written request. Tenure Borrower receives all funds in fixed monthly payment. Modified Tenure Borrower receives a lower fixed monthly payment and a line of credit. Term Borrower receives fixed monthly payment for a fixed period or term. X amount per month for Y months. Modified Term One-Time Lump Sum Borrower receives a fixed monthly payment for a fixed period or term and a line of credit. Borrower receives all funds at funding. Only available with a fixed rate.

46 Disbursement Limits Mandatory Obligations Items that must be paid at closing (or the first year of the loan) like existing liens and closing costs. Examples: Lien payoffs Initial Mortgage Insurance Premiums (IMIP) Loan origination fee Third party closing costs First year distributions from a fully-funded LESA Repair set-asides And more

47 Disbursement Limits Maximum Disbursement is the GREATER of: 60% of the Principal Limit, or Mandatory Obligations + 10% of PL FIXED One time at closing ARMs Within the first year Example: Principal Limit $200,000 Disbursement Limit $120,000, or MO + $20,000

48 Originating HECM Loans

49 Eligible homeowners obtain reverse mortgages for many reasons including: Repairing or modifying the home to meet the physical needs of getting older Supplementing retirement income to meet expenses Managing the costs of in-home care Paying off an existing mortgage Paying bills Paying property taxes Providing a source of funds for living expenses in lieu of liquidating financial investments during times of market downturn or disruption Establishing a line of credit for use as a financial safety net Helping retirement savings last longer Purchasing a retirement home

50 Getting Started All borrowers must be 62 years old, or older. All borrowers must be US citizens or legal residents. HECMs are federally insured. Only primary residences qualify. The property must be owner-occupied. The maximum claim amount is $679,650 renewable annually All borrowers must receive counseling. The reverse mortgage professional provides a list of 12 counseling agencies to the borrower.

51 Property Eligible Properties Eligible property types include the following: New or existing single family homes New or existing 2-4 units, as long as one unit is the borrower s primary residence FHA-approved condominiums Manufactured homes that meet FHA standards

52 Property Ineligible Properties Ineligible property types include the following: Investment properties Vacation homes Properties with illegal accessory units, or mixed-use properties with more than 49% commercial use. Cooperatives Bed and breakfasts Single-wide manufactured homes

53 Vesting All properties must be vested in the name of the borrower only in one of the following ways: Fee Simple: Absolute title to land, and the most common type of vesting. Life Estate: An estate whose duration is limited to the life of the party holding it, or some other person. Leasehold: A kind of rental agreement where the owner gives another the right to occupy or use the land for a period of time. Trust: A relationship in which one or more persons hold the individual s property, subject to certain duties to use and protect it, for the benefit of others. Land Trust: An agreement whereby one party agrees to hold ownership of a piece of real property for the benefit of another party.

54 The Workflow Process Counseling Application Processing Underwriting Closing

55 Non-Borrowing Spouse, Guardians or Power of Attorney s etc. Completed over phone or face to face Check state requirements Program eligibility, financial implications and repaying loan Borrower is mentally competent in understanding HECM product Until counseling is completed, signed and dated, the LO is not legally permitted to incur any costs on borrower(s) behalf Can be completed before or after initial application Counseling Application Processing Underwriting Closing

56 Information entered into loan origination software Authorization to process HECM loan Fees, interest rate, amount Includes required upfront general and state specific disclosures Financial assessment information gathered from the borrower(s) Upfront disclosures to be signed by non-borrowing spouse Counseling Application Processing Underwriting Closing

57 Order the HECM FHA Case Number Assignment Order appraisal and other third party services Borrower(s) income, assets, credit history, property charge payment history and other items needed After loan fully processed and third party services received, moves to Underwriting Counseling Application Processing Underwriting Closing

58 Borrower(s) and subject property fall within HECM guidelines Financial Assessment Borrower(s) willingness/capacity to continue paying obligations Residual income of borrower(s) after all expenses accounted for, review credit history and property charge payment history Issue an initial loan decision Conditions may apply After final approval, moves to Closing Counseling Application Processing Underwriting Closing

from title/settlement company Counseling Application Processing Underwriting")

59 Notify file is cleared for closing Final closing figures obtained from title/settlement company Closing date set Three(3) day right of rescission (for all refi transactions) Right to cancel loan with no penalty Lender disburses HECM funds to title/settlement company Borrower receives proceeds (if applicable) from title/settlement company Counseling Application Processing Underwriting Closing

60 The loan funds Counseling Application Processing Underwriting Closing

61 When is the Loan Due? When the home is sold When the last owner permanently vacates When the last borrower passes away* *Note: Eligible Non-Borrowing Spouses may still occupy the home by deferring the due and payable status of the loan.

62 HECM HMBS

63 HECM Mortgage Backed securities (HMBS) Ginnie Mae s Home Equity Conversion Mortgage (HECM) securities program Ginnie Mae as guarantor HMBS securities

64 HECM Mortgage Backed securities (HMBS) A Participation is that portion of a HECM loan securitized into an HMBS security. One HECM loan may have multiple Participations in various HMBS securities throughout the life of the loan. Although HMBS securities will likely contain many Participations from many different HECM loans, there may only exist a one-to-one relationship between any one Participation and the HMBS security for which it serves as pool collateral.

65 HECM Mortgage Backed securities (HMBS) Issuers are responsible for purchasing any Participation when the outstanding principal balance of the related HECM loan is equal to or greater than 98% of the Maximum Claim Amount If a HECM loan is found to be defective at any time after the related Participations have been pooled, the Issuer must cure the defect or purchase all related Participations. Substitutions of Participations related to HECM loans in HMBS pools are not permitted Issuers are required to pay a monthly guaranty fee to Ginnie Mae for each HMBS security for which the Issuer is Issuer of record.

66 HECM Mortgage Backed securities (HMBS) Each pool must have an original principal amount of at least $1,000,000 Each HMBS pool must include at least 3 Participations, each of which is related to a distinct HECM loan HMBS security holders are not entitled to scheduled payments of principal or interest The issuer may, at that issuer s option, purchase any pooled participation from GNMA once the associated HECM becomes due and payable.

67 Support for Reverse Mortgages

68

69

70

71

72 Business Opportunities

73

74 Equity Extraction Tools Home Equity Loan Home Equity Line of Credit Cash-Out Refinancing Selling the home and buying a less expensive one Selling the home and renting

75 HECM or HELOC? Benefits of a HELOC: Lower interest rates in most cases Lower upfront costs May be more suitable for short term-needs Benefits of a HECM: Loan does not become due as long as all the loan obligations are met Line of credit cannot be frozen due to changing market values No monthly p&i mortgage payments

76

77

78

79 Generational Lending

80 Referral Partners Real Estate Agents H4P Home Builders of 55+ H4P Financial Planners Certified Divorce Financial Analysts Care Managers In-Home Care Executives National Aging in Place Council

81 NRMLA as a Resource

82 Nrmlaonline.org

83 Reversemortgage.org

84 Reverse Mortgage Self-Evaluation: A Checklist of Key Considerations What You Need to Know About Your HECM After Closing What Do I Do When My Loan is Due?

85

86 Demographics Household Wealth Profiles Presentation Summary What is a Reverse Mortgage Originating HECM Loans Business Opportunities

87 Q&A

88 Peter Bell President & CEO National Reverse Mortgage Lenders Association National Reverse Mortgage Lenders Association th St., NW Suite 420 Washington, DC (p)

Your Reverse Mortgage Guide. Reaping The Rewards Of A Lifetime Investment In Homeownership

Your Reverse Mortgage Guide Reaping The Rewards Of A Lifetime Investment In Homeownership Contents Make The Most Of Retirement!...3 Program Overview...3 4 What Is A Reverse Mortgage? Why Get A Reverse

Your Reverse Mortgage Guide Reaping The Rewards Of A Lifetime Investment In Homeownership Contents Make The Most Of Retirement!...3 Program Overview...3 4 What Is A Reverse Mortgage? Why Get A Reverse

Is A Reverse Mortgage Right for You?

Is A Reverse Mortgage Right for You? NewRetirement s Guide to Reverse Mortgages www.newretirement.com 888-411-RETIRE (7384) Table of Contents What is a Reverse Mortgage? Are You Eligible For a Reverse

Is A Reverse Mortgage Right for You? NewRetirement s Guide to Reverse Mortgages www.newretirement.com 888-411-RETIRE (7384) Table of Contents What is a Reverse Mortgage? Are You Eligible For a Reverse

GINNIE MAE Guaranteed Home Equity Conversion Mortgage-Backed Securities (Issuable in Series)

") Base Prospectus July 1, 2011 Government National Mortgage Association GINNIE MAE Guaranteed Home Equity Conversion Mortgage-Backed Securities (Issuable in Series) The Government National Mortgage Association

Base Prospectus July 1, 2011 Government National Mortgage Association GINNIE MAE Guaranteed Home Equity Conversion Mortgage-Backed Securities (Issuable in Series) The Government National Mortgage Association

Reverse Mortgage Authorization Form

Reverse Mortgage Authorization Form Conflict of Interest Disclosure Cambridge Credit Counseling Corp provides counseling to help you make an informed decision concerning reverse mortgage products. We will

Reverse Mortgage Authorization Form Conflict of Interest Disclosure Cambridge Credit Counseling Corp provides counseling to help you make an informed decision concerning reverse mortgage products. We will

REVERSE MORTGAGE GUIDE

REVERSE MORTGAGE GUIDE Reap The Rewards Of A Lifetime Investment In Homeownership INVICTA MORTGAGE GROUP Better programs. Better service. Better financing. Licensed by PA Dept of Banking. NMLS# 111947

REVERSE MORTGAGE GUIDE Reap The Rewards Of A Lifetime Investment In Homeownership INVICTA MORTGAGE GROUP Better programs. Better service. Better financing. Licensed by PA Dept of Banking. NMLS# 111947

Is a Reverse Mortgage Right for You?

Your Reverse Mortgage Information Brochure Is a Reverse Mortgage Right for You? Reverse mortgages are a unique type of loan that lets you convert the accrued equity of your home into usable funds. Home

Your Reverse Mortgage Information Brochure Is a Reverse Mortgage Right for You? Reverse mortgages are a unique type of loan that lets you convert the accrued equity of your home into usable funds. Home

Chicago Volunteer Legal Services Access to Justice Program April 27, 2017

Chicago Volunteer Legal Services Access to Justice Program April 27, 2017 R. Dennis Smith The John Marshall Law School Prepared under grants from the City of Chicago (TACIT) and the Retirement Research

Chicago Volunteer Legal Services Access to Justice Program April 27, 2017 R. Dennis Smith The John Marshall Law School Prepared under grants from the City of Chicago (TACIT) and the Retirement Research

Reverse mortgages. A discussion guide. Consumer Financial Protection Bureau

Reverse mortgages A discussion guide Consumer Financial Protection Bureau About this discussion guide This guide gives an overview of many key concepts of reverse mortgages. A qualified reverse mortgage

Reverse mortgages A discussion guide Consumer Financial Protection Bureau About this discussion guide This guide gives an overview of many key concepts of reverse mortgages. A qualified reverse mortgage

What You Need to Know About Your HECM After Closing

What You Need to Know About Your HECM After Closing www.reversemortgage.org INDEX How do I know who my Servicer is?... 2 Staying in touch... 2 Receiving payments from your HECM... 2 Occupancy... 3 Property

What You Need to Know About Your HECM After Closing www.reversemortgage.org INDEX How do I know who my Servicer is?... 2 Staying in touch... 2 Receiving payments from your HECM... 2 Occupancy... 3 Property

HUD s Reverse Mortgage Insurance Program: Home Equity Conversion Mortgages

: Home Equity Conversion Mortgages (name redacted) Specialist in Housing Policy March 31, 2017 Congressional Research Service 7-... www.crs.gov R44128 Summary Reverse mortgages allow older homeowners to

: Home Equity Conversion Mortgages (name redacted) Specialist in Housing Policy March 31, 2017 Congressional Research Service 7-... www.crs.gov R44128 Summary Reverse mortgages allow older homeowners to

Enhance Your Financial Security. With a Home Equity Conversion Mortgage

Enhance Your Financial Security With a Home Equity Conversion Mortgage Liberty Home Equity Solutions, Inc. 10951 White Rock Road, Suite 200 Rancho Cordova, CA 95670 800.976.6211 www.reverse.org Unlock

Enhance Your Financial Security With a Home Equity Conversion Mortgage Liberty Home Equity Solutions, Inc. 10951 White Rock Road, Suite 200 Rancho Cordova, CA 95670 800.976.6211 www.reverse.org Unlock

Home Equity Conversion Mortgage HECM. Presented By: Doris Batty NMLS #

Home Equity Conversion Mortgage HECM Presented By: Doris Batty NMLS # 420458 What is a Reverse Mortgage? Created for homeowners 62 & older. Converting their home s equity into cash. Payment stream reversed.

Home Equity Conversion Mortgage HECM Presented By: Doris Batty NMLS # 420458 What is a Reverse Mortgage? Created for homeowners 62 & older. Converting their home s equity into cash. Payment stream reversed.

Presenters: Lynn M. Connors, Reverse Mortgage Specialist and Sales Manager Commonfund Mortgage Corp.

Reverse Mortgages July 28, 2016 Presenters: Lynn M. Connors, Reverse Mortgage Specialist and Sales Manager Commonfund Mortgage Corp. Jennifer, N. Levy, Esq., Senior Staff Attorney at JASA Legal Services

Reverse Mortgages July 28, 2016 Presenters: Lynn M. Connors, Reverse Mortgage Specialist and Sales Manager Commonfund Mortgage Corp. Jennifer, N. Levy, Esq., Senior Staff Attorney at JASA Legal Services

Brown - HECM / Reverse Product Guidelines. Loan Parameter HECM Fixed Variable Rate HECM

Brown - HECM / Reverse Product PRODUCTS & UNDERWRITING GUIDELINES Youngest Borrower Age Eligibility Occupancy Allowed States Allowed 62 years and above Owner Occupied Primary Residence Loans are accepted

Brown - HECM / Reverse Product PRODUCTS & UNDERWRITING GUIDELINES Youngest Borrower Age Eligibility Occupancy Allowed States Allowed 62 years and above Owner Occupied Primary Residence Loans are accepted

Enhancing your retirement on your way to a better life!

Enhancing your retirement on your way to a better life! Find out what a HECM Reverse Mortgage is and how you may qualify today! WHAT IS A HECM REVERSE MORTGAGE? Home Equity Conversion Mortgages (HECM),

Enhancing your retirement on your way to a better life! Find out what a HECM Reverse Mortgage is and how you may qualify today! WHAT IS A HECM REVERSE MORTGAGE? Home Equity Conversion Mortgages (HECM),

HECM for Purchase A Homebuilder s Toolkit

HECM for Purchase A Homebuilder s Toolkit This material has not been reviewed, approved or issued by HUD, FHA or any government agency. NRMLA is not affiliated with or acting on behalf of or at the direction

HECM for Purchase A Homebuilder s Toolkit This material has not been reviewed, approved or issued by HUD, FHA or any government agency. NRMLA is not affiliated with or acting on behalf of or at the direction

2017 NRMLA Annual Meeting NOV SAN FRANCISCO

1 2017 NRMLA Annual Meeting NOV. 13 15 SAN FRANCISCO 2 The Math Behind the HECM Agenda 3 Interest Rates Expected Rates and Look Up Floor Note Rates Principal Limit Factors Payment Plan Math Ongoing MIP

1 2017 NRMLA Annual Meeting NOV. 13 15 SAN FRANCISCO 2 The Math Behind the HECM Agenda 3 Interest Rates Expected Rates and Look Up Floor Note Rates Principal Limit Factors Payment Plan Math Ongoing MIP

Reverse Mortgage FAQs

Reverse Mortgage FAQs NMLS# 1313859 Frequently Asked Questions about Reverse Mortgages At ReverseMortgages.com, we get a lot of questions from our clients about reverse mortgages, the process of getting

Reverse Mortgage FAQs NMLS# 1313859 Frequently Asked Questions about Reverse Mortgages At ReverseMortgages.com, we get a lot of questions from our clients about reverse mortgages, the process of getting

Unlocking the Power of Home

Unlocking the Power of Home The Surprising Secret Weapon In Today s Retirement Planning Toolkit Becky Bell, VP Who Is Longbridge Financial, LLC? We are a national reverse-only lender focused on making

Unlocking the Power of Home The Surprising Secret Weapon In Today s Retirement Planning Toolkit Becky Bell, VP Who Is Longbridge Financial, LLC? We are a national reverse-only lender focused on making

Reverse By The Number

Reverse By The Number Working Reverse Mortgage Loans in Reverse Vision HighTechLending, Inc., Licensed by the Department of Business Oversight under the California Residential Mortgage Lending Act. NMLS

Reverse By The Number Working Reverse Mortgage Loans in Reverse Vision HighTechLending, Inc., Licensed by the Department of Business Oversight under the California Residential Mortgage Lending Act. NMLS

Instructions for Completing the Uniform Residential Loan Application

Instructions for Completing the Uniform Residential Loan Application Uniform Residential Loan Application The Uniform Residential Loan Application (URLA) contains the following sections: Section 1. Borrower

Instructions for Completing the Uniform Residential Loan Application Uniform Residential Loan Application The Uniform Residential Loan Application (URLA) contains the following sections: Section 1. Borrower

The Math Behind HECMs P R E S E N T E R : C R A I G B A R N E S, R E V E R S E M O R T G A G E F U N D I N G

The Math Behind HECMs P R E S E N T E R : C R A I G B A R N E S, R E V E R S E M O R T G A G E F U N D I N G Session Objectives Today s session will: Illustrate how reverse mortgage interest rates are

The Math Behind HECMs P R E S E N T E R : C R A I G B A R N E S, R E V E R S E M O R T G A G E F U N D I N G Session Objectives Today s session will: Illustrate how reverse mortgage interest rates are

Actuarial Review of the Federal Housing Administration Mutual Mortgage Insurance Fund HECM Loans For Fiscal Year 2013

Actuarial Review of the Federal Housing Administration Mutual Mortgage Insurance Fund HECM Loans For Fiscal Year 2013 December 11, 2013 Prepared for U.S. Department of Housing and Urban Development By

Actuarial Review of the Federal Housing Administration Mutual Mortgage Insurance Fund HECM Loans For Fiscal Year 2013 December 11, 2013 Prepared for U.S. Department of Housing and Urban Development By

The Flawless Reverse Mortgage Signing Experience

The Flawless Reverse Mortgage Signing Experience Objectives Learn what a reverse mortgage is Recognize types of reverse mortgages available Understand restrictions and reasons for accelerated payment Identify

The Flawless Reverse Mortgage Signing Experience Objectives Learn what a reverse mortgage is Recognize types of reverse mortgages available Understand restrictions and reasons for accelerated payment Identify

Financing Residential Real Estate. Lesson 11: FHA-Insured Loans

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

A Toolkit for Real Estate Agents

Using a Reverse Mortgage to Buy a Home A Toolkit for Real Estate Agents This material has not been reviewed, approved or issued by HUD, FHA or any government agency. NRMLA is not affiliated with or acting

Using a Reverse Mortgage to Buy a Home A Toolkit for Real Estate Agents This material has not been reviewed, approved or issued by HUD, FHA or any government agency. NRMLA is not affiliated with or acting

After-tax APRPlus The APRPlus taking into account the effect of income taxes.

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

Introduction to Reverse Mortgages

Introduction to Reverse Mortgages Reverse Mortgages for Attorneys Revised May, 2017 Finance of America Reverse Slide 1 Reverse Mortgage Basics How the Program Works Types of Products Financial Assessment

Introduction to Reverse Mortgages Reverse Mortgages for Attorneys Revised May, 2017 Finance of America Reverse Slide 1 Reverse Mortgage Basics How the Program Works Types of Products Financial Assessment

Fitting Home Equity into a Retirement Income Strategy

Fitting Home Equity into a Retirement Income Strategy Wade Pfau, Ph.D., CFA RetirementResearcher.com/reverse-mortgages What s Different About Retirement? Reduced earnings capacity Visible spending constraint

Fitting Home Equity into a Retirement Income Strategy Wade Pfau, Ph.D., CFA RetirementResearcher.com/reverse-mortgages What s Different About Retirement? Reduced earnings capacity Visible spending constraint

The Common Sense Guide: HECM

The Common Sense Guide: HECM Home Equity Conversion Mortgage Prepared by: Ed O Connor Ed O Connor, NMLS# 17212 Your Credit Union Trusted Resource FHA made the program WE make the difference! 1 Steps to

The Common Sense Guide: HECM Home Equity Conversion Mortgage Prepared by: Ed O Connor Ed O Connor, NMLS# 17212 Your Credit Union Trusted Resource FHA made the program WE make the difference! 1 Steps to

Enjoy Retirement In Your Dream Home HOME EQUITY CONVERSION MORTGAGE FOR PURCHASE GUIDE

Enjoy Retirement In Your Dream Home HOME EQUITY CONVERSION MORTGAGE FOR PURCHASE GUIDE At TowneBank Mortgage, we recognize the unique financial needs of the senior community. A Home Equity Conversion

Enjoy Retirement In Your Dream Home HOME EQUITY CONVERSION MORTGAGE FOR PURCHASE GUIDE At TowneBank Mortgage, we recognize the unique financial needs of the senior community. A Home Equity Conversion

Section DU Refi Plus Loan Program

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

Options for Moving in Retirement Using the HECM for Purchase

Options for Moving in Retirement Using the HECM for Purchase By: John Salter, Ph.D., CFP SUMMARY Many retirees will choose to move from the large home in which they raised their family into something smaller

Options for Moving in Retirement Using the HECM for Purchase By: John Salter, Ph.D., CFP SUMMARY Many retirees will choose to move from the large home in which they raised their family into something smaller

(TC) TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE

TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE") AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

Reverse Mortgages. Chapter 20 SYNOPSIS. Doni Dolfinger Paulette Wisch, CML Universal Lending Corporation What Is a Reverse Mortgage?

Chapter 20 Reverse Mortgages Doni Dolfinger Paulette Wisch, CML Universal Lending Corporation SYNOPSIS 20-1. What Is a Reverse Mortgage? 20-2. Reverse Mortgage Financial Assessment 20-3. Eligibility, Responsibility,

Chapter 20 Reverse Mortgages Doni Dolfinger Paulette Wisch, CML Universal Lending Corporation SYNOPSIS 20-1. What Is a Reverse Mortgage? 20-2. Reverse Mortgage Financial Assessment 20-3. Eligibility, Responsibility,

The Flawless Reverse Mortgage Signing. Objectives. What is a Reverse Mortgage? Session: 125 & 224

The Flawless Reverse Mortgage Signing Session: 125 & 224 Objectives Learn what a reverse mortgage is Recognize available reverse mortgages Understand restrictions and reasons for accelerated payment Identify

The Flawless Reverse Mortgage Signing Session: 125 & 224 Objectives Learn what a reverse mortgage is Recognize available reverse mortgages Understand restrictions and reasons for accelerated payment Identify

In-Focus FEATURING THE STATE OF DIGITAL MORTGAGE AN EXCERPT FROM MOVING FORWARD IN REVERSE

In-Focus FEATURING THE STATE OF DIGITAL MORTGAGE AN EXCERPT FROM Volume 3, 1, Issue 2 1 2018 2016 Strategic Mortgage Finance Group, LLC. All Rights Reserved. February, July, 2016 2018 By Jim Cameron A

In-Focus FEATURING THE STATE OF DIGITAL MORTGAGE AN EXCERPT FROM Volume 3, 1, Issue 2 1 2018 2016 Strategic Mortgage Finance Group, LLC. All Rights Reserved. February, July, 2016 2018 By Jim Cameron A

Section 255 of the National Housing Act (the enabling legislation for HECMs)

") Section 255 of the National Housing Act (the enabling legislation for HECMs) Section 1715z-20. Insurance of home equity conversion mortgages for elderly homeowners (a) Purpose The purpose of this section

Section 255 of the National Housing Act (the enabling legislation for HECMs) Section 1715z-20. Insurance of home equity conversion mortgages for elderly homeowners (a) Purpose The purpose of this section

Ginnie Mae MBS Loan-Level Disclosure Definitions Version 1.2

The following four sections provide the definitions, calculations, and descriptions of the data elements under Ginnie Mae s MBS Loan-Level Disclosure: Section # Section Name 1 Definition of Terms 2 Definitions

The following four sections provide the definitions, calculations, and descriptions of the data elements under Ginnie Mae s MBS Loan-Level Disclosure: Section # Section Name 1 Definition of Terms 2 Definitions

Reverse Mortgages: How to use Reverse Mortgages to Secure Your Retirement

Wade D. Pfau, Ph.D., CFA Program Title: Reverse Mortgages: How to use Reverse Mortgages to Secure Your Retirement Bio Wade D. Pfau, Ph.D., CFA, is a Professor of Retirement Income in the Ph.D. program

Wade D. Pfau, Ph.D., CFA Program Title: Reverse Mortgages: How to use Reverse Mortgages to Secure Your Retirement Bio Wade D. Pfau, Ph.D., CFA, is a Professor of Retirement Income in the Ph.D. program

6/18/2015. Residential Mortgage Types and Borrower Decisions. Role of the secondary market Mortgage types:

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

PART 206 HOME EQUITY CON- VERSION MORTGAGE INSUR- ANCE

203.680 24 CFR Ch. II (4 1 12 Edition) 203.680 Approval of occupancy after conveyance. When an occupied property is conveyed to HUD before HUD has had an opportunity to consider continued occupancy (e.g.,

203.680 24 CFR Ch. II (4 1 12 Edition) 203.680 Approval of occupancy after conveyance. When an occupied property is conveyed to HUD before HUD has had an opportunity to consider continued occupancy (e.g.,

Commercial Real. Estate. CMBS Conduit. Loan. Program. Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage

Commercial Real Estate CMBS Conduit Loan Program Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage City Capital Realty Shawn Rabban 310-714-5616 shawnrabban@yahoo.com CAL

Commercial Real Estate CMBS Conduit Loan Program Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage City Capital Realty Shawn Rabban 310-714-5616 shawnrabban@yahoo.com CAL

The TRUTH about REVERSE MORTGAGE. (Everything you need to know) By Julie A. Colangelo Reverse Mortgage Development & Training Manager

By Julie A. Colangelo Reverse Mortgage Development & Training Manager") The TRUTH about REVERSE MORTGAGE (Everything you need to know) By Julie A. Colangelo Reverse Mortgage Development & Training Manager A LETTER FROM THE HEART By JULIE A. COLANGELO The reality of our world

The TRUTH about REVERSE MORTGAGE (Everything you need to know) By Julie A. Colangelo Reverse Mortgage Development & Training Manager A LETTER FROM THE HEART By JULIE A. COLANGELO The reality of our world

Non Conforming JUMBO Programs

Non Conforming JUMBO Programs Select QM Eligibility Matrix Fixed Rate and Hybrid ARM Products Primary Residence Purchase, Rate and Term Transaction Type Units FICO LTV/CLTV/HCLTV Loan Amount 1 760 85%

Non Conforming JUMBO Programs Select QM Eligibility Matrix Fixed Rate and Hybrid ARM Products Primary Residence Purchase, Rate and Term Transaction Type Units FICO LTV/CLTV/HCLTV Loan Amount 1 760 85%

More on Mortgages. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

Bringing Retirement Dreams Within Reach

Bringing Retirement Dreams Within Reach Downsizing or relocating in retirement is easier with the Home Equity Conversion Mortgage (HECM) for Purchase CONNECTING THE REVERSE MORTGAGE INDUSTRY SINCE 2007

Bringing Retirement Dreams Within Reach Downsizing or relocating in retirement is easier with the Home Equity Conversion Mortgage (HECM) for Purchase CONNECTING THE REVERSE MORTGAGE INDUSTRY SINCE 2007

High-Cost Area (High Balance) Loan Amounts

Loan Amounts") Program Qualifications Eligible loans are conforming and high balance loans receiving a DU Version 10.0 or later Approve/Eligible. Maximum Loan Amounts Conforming Maximum Loan Amounts Units Continental

Program Qualifications Eligible loans are conforming and high balance loans receiving a DU Version 10.0 or later Approve/Eligible. Maximum Loan Amounts Conforming Maximum Loan Amounts Units Continental

Your plan, your reverse mortgage

Your plan, your reverse mortgage You ve worked hard your whole life to build your nest egg so it s worth taking a look at every available option to ensure your retirement assets are used in the most profitable

Your plan, your reverse mortgage You ve worked hard your whole life to build your nest egg so it s worth taking a look at every available option to ensure your retirement assets are used in the most profitable

SECTION 8 HOMEOWNERSHIP PROGRAM

SECTION 8 HOMEOWNERSHIP PROGRAM 1.0 INTRODUCTION This administrative plan has been prepared as an addendum to the existing Section 8 Administrative Plan. This Plan addresses those areas that are pertinent

SECTION 8 HOMEOWNERSHIP PROGRAM 1.0 INTRODUCTION This administrative plan has been prepared as an addendum to the existing Section 8 Administrative Plan. This Plan addresses those areas that are pertinent

CRA PORTFOLIO NON-CONFORMING PROGRAM

LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPRAISAL REQUIREMENTS:... 3 ASSUMABILITY:...

LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPRAISAL REQUIREMENTS:... 3 ASSUMABILITY:...

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile Overlays to Fannie Mae are underlined

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

Annual Report to Congress Regarding the Financial Status of the FHA Mutual Mortgage Insurance Fund Fiscal Year 2010

Annual Report to Congress Regarding the Financial Status of the FHA Mutual Mortgage Insurance Fund Fiscal Year 2010 U.S. Department of Housing and Urban Development November 15, 2010 Secretary s Foreword

Annual Report to Congress Regarding the Financial Status of the FHA Mutual Mortgage Insurance Fund Fiscal Year 2010 U.S. Department of Housing and Urban Development November 15, 2010 Secretary s Foreword

Financing Residential Real Estate. FHA-Insured Loans

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, graduated payment mortgages, FHA insurance premiums, sales concessions such

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, graduated payment mortgages, FHA insurance premiums, sales concessions such

SONYMA Conventional Plus Correspondent Term Sheet

Product Type 30 Year Fixed Rate Mortgage. Sales Focus This program combines the flexibility offered by Fannie Mae s HomeReady Mortgage along with SONYMA s Down Payment Assistance Loan (DPAL). It is designed

Product Type 30 Year Fixed Rate Mortgage. Sales Focus This program combines the flexibility offered by Fannie Mae s HomeReady Mortgage along with SONYMA s Down Payment Assistance Loan (DPAL). It is designed

Choose to Reverse. Buy a house or get money back using a Reverse Mortgage Financing Program for Seniors. by Natalie Danielson

Choose to Reverse Buy a house or get money back using a Reverse Mortgage Financing Program for Seniors by Natalie Danielson www.clockhours.com Choose to Reverse Reverse Mortgage Financing Program Session

Choose to Reverse Buy a house or get money back using a Reverse Mortgage Financing Program for Seniors by Natalie Danielson www.clockhours.com Choose to Reverse Reverse Mortgage Financing Program Session

Journal CSA. Using a Reverse Mortgage to Age in Place in One s Home Number 68 Vol. 1, Patricia Whitlock, CRMP

CSA Journal Using a Reverse Mortgage to Age in Place in One s Home Number 68 Vol. 1, 2017 Patricia Whitlock, CRMP This document is authorized for use only by Patricia Whitlock. Copying or posting is an

CSA Journal Using a Reverse Mortgage to Age in Place in One s Home Number 68 Vol. 1, 2017 Patricia Whitlock, CRMP This document is authorized for use only by Patricia Whitlock. Copying or posting is an

Reverse Lending Overview and Survey

February 7, 2018 Reverse Lending Overview and Survey Jim Cameron, Senior Partner Our Story OUR VISION STRATMOR is the most trusted consulting firm in the mortgage industry based on a reputation for providing

February 7, 2018 Reverse Lending Overview and Survey Jim Cameron, Senior Partner Our Story OUR VISION STRATMOR is the most trusted consulting firm in the mortgage industry based on a reputation for providing

AHP 2018 Implementation Plan Native American Homeownership Initiative (NAHI) Program Guidelines

Program Guidelines") I. (NAHI) Program Guidelines 1. Program Summary In 2018 the Bank will make $1,000,000 available on a first-come first-served basis to eligible members that have executed a Down Payment Subsidy Agreement.

I. (NAHI) Program Guidelines 1. Program Summary In 2018 the Bank will make $1,000,000 available on a first-come first-served basis to eligible members that have executed a Down Payment Subsidy Agreement.

Reverse MBS A Look at a Burgeoning Agency MBS Asset Class

July 28, 2010 Ronald E. Thompson, Jr. Managing Director, Global Head of ABS/MBS Strategy +44 (0)20 7997 2163 rthompson@knight.com Reverse MBS A Look at a Burgeoning Agency MBS Asset Class Reverse mortgage

July 28, 2010 Ronald E. Thompson, Jr. Managing Director, Global Head of ABS/MBS Strategy +44 (0)20 7997 2163 rthompson@knight.com Reverse MBS A Look at a Burgeoning Agency MBS Asset Class Reverse mortgage

Housing America s Future: New Directions for National Policy Report of the Bipartisan Policy Center Housing Commission

Housing America s Future: New Directions for National Policy Report of the Bipartisan Policy Center Housing Commission About the Housing Commission Created by the Bipartisan Policy Center, a non-profit

Housing America s Future: New Directions for National Policy Report of the Bipartisan Policy Center Housing Commission About the Housing Commission Created by the Bipartisan Policy Center, a non-profit

10, 15, 20, 25 & 30 YR Fixed Rates

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Federal National Mortgage Association

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

Legal Basics: Foreclosure Prevention. March 21, 2017 Odette Williamson National Consumer Law Center

Legal Basics: Foreclosure Prevention March 21, 2017 Odette Williamson National Consumer Law Center National Consumer Law Center 2013 National Consumer Law Center Advocate on behalf of low-income consumers

Legal Basics: Foreclosure Prevention March 21, 2017 Odette Williamson National Consumer Law Center National Consumer Law Center 2013 National Consumer Law Center Advocate on behalf of low-income consumers

MEGA ALT ARM (MA5/1)

") MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

CHILDREN & CAREGIVERS A FAMILY GUIDE TO REVERSE MORTGAGES

NMLS #7230 CHILDREN & CAREGIVERS A FAMILY GUIDE TO REVERSE MORTGAGES 89% The percentage of adult children who want their parents to pay their bills and not worry about leaving an inheritance. *Based on

NMLS #7230 CHILDREN & CAREGIVERS A FAMILY GUIDE TO REVERSE MORTGAGES 89% The percentage of adult children who want their parents to pay their bills and not worry about leaving an inheritance. *Based on

Primers. GNMA HECM Primer and Relative Value. gy MBS Strate. Overview. Please see the last page of this publication for important disclosures.

Primers gy MBS Strate Please see the last page of this publication for important disclosures. February 25 2011 GNMA HECM Primer and Relative Value Overview A reverse mortgage is a type of loan that allows

Primers gy MBS Strate Please see the last page of this publication for important disclosures. February 25 2011 GNMA HECM Primer and Relative Value Overview A reverse mortgage is a type of loan that allows

Plaza Home Mortgage Inc. Reverse Mortgage Presentation Basics. May 2018

Plaza Home Mortgage Inc. Reverse Mortgage Presentation Basics May 2018 Your GoToWebinar Toolbar Use speakers or a telephone to listen to the audio. Use the information in your toolbar to dial in from your

Plaza Home Mortgage Inc. Reverse Mortgage Presentation Basics May 2018 Your GoToWebinar Toolbar Use speakers or a telephone to listen to the audio. Use the information in your toolbar to dial in from your

Timing Is Everything. Building a better retirement with a. Home Equity Conversion Mortgage (HECM)

") Timing Is Everything Building a better retirement with a Home Equity Conversion Mortgage (HECM) CONNECTING THE REVERSE MORTGAGE INDUSTRY SINCE 2007 Executive Summary The ability of Americans to realize

Timing Is Everything Building a better retirement with a Home Equity Conversion Mortgage (HECM) CONNECTING THE REVERSE MORTGAGE INDUSTRY SINCE 2007 Executive Summary The ability of Americans to realize

Reverse Mortgage Foreclosure Updates & Methods of Resolution September 19, 2017

Reverse Mortgage Foreclosure Updates & Methods of Resolution September 19, 2017 Presenter: Jennifer N. Levy, Esq. BIOGRAPHY Jennifer is a Senior Staff Attorney at JASA Legal Services for the Elderly in

Reverse Mortgage Foreclosure Updates & Methods of Resolution September 19, 2017 Presenter: Jennifer N. Levy, Esq. BIOGRAPHY Jennifer is a Senior Staff Attorney at JASA Legal Services for the Elderly in

Reverse Mortgage Originations and Performance in Philadelphia

Reverse Mortgage Originations and Performance in Philadelphia Jaclene Begley, Fannie Mae Lauren Lambie-Hanson, Federal Reserve Bank of Philadelphia* Mike Witowski, Federal Reserve Bank of Philadelphia

Reverse Mortgage Originations and Performance in Philadelphia Jaclene Begley, Fannie Mae Lauren Lambie-Hanson, Federal Reserve Bank of Philadelphia* Mike Witowski, Federal Reserve Bank of Philadelphia

Fannie & High BalanceGuidelines

Fannie & High BalanceGuidelines Agency Finance Type Occupancy Term High balance and transactions with non-occupant coborrowers are limited to 95% LTV/CLTV. High Balance Cash Out Transactions are limited

Fannie & High BalanceGuidelines Agency Finance Type Occupancy Term High balance and transactions with non-occupant coborrowers are limited to 95% LTV/CLTV. High Balance Cash Out Transactions are limited

Houston Housing Authority HOMEOWNERSHIP PROGRAM PLAN

Houston Housing Authority HOMEOWNERSHIP PROGRAM PLAN Revised June 2017 Houston Housing Authority HOUSING CHOICE VOUCHER HOMEOWNERSHIP PROGRAM PROGRAM GUIDE TABLES OF CONTENTS Program Description Eligibility

Houston Housing Authority HOMEOWNERSHIP PROGRAM PLAN Revised June 2017 Houston Housing Authority HOUSING CHOICE VOUCHER HOMEOWNERSHIP PROGRAM PROGRAM GUIDE TABLES OF CONTENTS Program Description Eligibility

Reverse Mortgage/Home Equity Conversion Mortgage (HECM)

") Reverse Mortgage/Home Equity Conversion Mortgage (HECM) All members of NAOSA agree to always act in a client s best interest. Over and above all state, federal and specific industry rules and regulations,

Reverse Mortgage/Home Equity Conversion Mortgage (HECM) All members of NAOSA agree to always act in a client s best interest. Over and above all state, federal and specific industry rules and regulations,

DEFINITION OF COMMON TERMS

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

A GUIDE FOR REALTORS. Using a Reverse Mortgage to Purchase a Home

A GUIDE FOR REALTORS Using a Reverse Mortgage to Purchase a Home This material has not been reviewed, approved or issued by HUD, FHA or any government agency. RMNW is not affiliated with or acting on behalf

A GUIDE FOR REALTORS Using a Reverse Mortgage to Purchase a Home This material has not been reviewed, approved or issued by HUD, FHA or any government agency. RMNW is not affiliated with or acting on behalf

Chapter 15 Real Estate Financing: Practice

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

ELIGIBILITY MATRIX & SUMMARY GUIDELINES 15 & 30 YR Fixed Rates

Revised 6/2/2014 Changes from prior versions are in red font Overlays to Fannie guidelines are underlined Correspondent Lending Jumbo "Premier" Fixed Rate and ARM Product Profile Based on a Fannie Mae

Revised 6/2/2014 Changes from prior versions are in red font Overlays to Fannie guidelines are underlined Correspondent Lending Jumbo "Premier" Fixed Rate and ARM Product Profile Based on a Fannie Mae

PURCHASE. Max LTV w/o Sec. Fin. Max LTV w/ Sec. Fin. Max TLTV w/ Sec. Fin.

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

Retain your most valuable customers using a Generational Lending approach

Retain your most valuable customers using a Generational Lending approach By offering the FHA-insured Home Equity Conversion Mortgage (HECM) loan, you can keep your customers for life. CONNECTING THE REVERSE

Retain your most valuable customers using a Generational Lending approach By offering the FHA-insured Home Equity Conversion Mortgage (HECM) loan, you can keep your customers for life. CONNECTING THE REVERSE

Fannie Mae has specific requirements for multiple financed properties:

Fannie Mae has specific requirements for multiple financed properties: If subject loan is owner occupied, Fannie Mae has no limit on number of properties financed If subject is second home or investment

Fannie Mae has specific requirements for multiple financed properties: If subject loan is owner occupied, Fannie Mae has no limit on number of properties financed If subject is second home or investment

City of Carpinteria. Workforce Homebuyer. Down Payment Loan Program. Program Guide and Disclosure. City of Carpinteria

Housing Trust Fund of Santa Barbara County City of Carpinteria Workforce Homebuyer Down Payment Loan Program Program Guide and Disclosure 2017 City of Carpinteria 5775 Carpinteria Avenue Carpinteria, CA

Housing Trust Fund of Santa Barbara County City of Carpinteria Workforce Homebuyer Down Payment Loan Program Program Guide and Disclosure 2017 City of Carpinteria 5775 Carpinteria Avenue Carpinteria, CA

U.S. Department of Housing and Urban Development Community Planning and Development

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice CPD 96-9 All Secretary's Representatives All State/Area Coordinators Issued: December 20,

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice CPD 96-9 All Secretary's Representatives All State/Area Coordinators Issued: December 20,

Billing Code DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT. [Docket No. FR-5735-N-05]

![Billing Code DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT. [Docket No. FR-5735-N-05]](/thumbs/89/100123266.jpg "Billing Code DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT. [Docket No. FR-5735-N-05]") This document is scheduled to be published in the Federal Register on 04/29/2015 and available online at http://federalregister.gov/a/2015-10019, and on FDsys.gov Billing Code 4210-67 DEPARTMENT OF HOUSING

This document is scheduled to be published in the Federal Register on 04/29/2015 and available online at http://federalregister.gov/a/2015-10019, and on FDsys.gov Billing Code 4210-67 DEPARTMENT OF HOUSING

Section 2.23 Veterans Administration (VA) Loan Program

Loan Program") Section 2.23 Veterans Administration (VA) Loan Program In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Correspondent Lenders with

Section 2.23 Veterans Administration (VA) Loan Program In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Correspondent Lenders with

Section 504 Single Family Housing Program

Section 504 Single Family Housing Program Rural Development is An Equal Opportunity Lender, Provider, and Employer Complaints of Discrimination Should Be Sent To: USDA, Director, Office of Civil Rights,

Section 504 Single Family Housing Program Rural Development is An Equal Opportunity Lender, Provider, and Employer Complaints of Discrimination Should Be Sent To: USDA, Director, Office of Civil Rights,

Reverse Mortgages. Presented By: Bruce Laukaitis. SVP Reverse Mortgage Division. Residential Home Funding Corp

Reverse Mortgages Presented By: Bruce Laukaitis SVP Reverse Mortgage Division Residential Home Funding Corp. 973-575-0097 What is a Reverse Mortgage? A reverse mortgage enables seniors, age 62 and older,

Reverse Mortgages Presented By: Bruce Laukaitis SVP Reverse Mortgage Division Residential Home Funding Corp. 973-575-0097 What is a Reverse Mortgage? A reverse mortgage enables seniors, age 62 and older,

Premium Jumbo Fixed & 10/1 ARM

Last Update 11/29/2017 Primary (Purchase & Rate/Term NO MI OPTION) Primary (Purchase) Primary (Rate/Term Ref.) Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV

Last Update 11/29/2017 Primary (Purchase & Rate/Term NO MI OPTION) Primary (Purchase) Primary (Rate/Term Ref.) Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV

REV-1 TABLE OF CONTENTS. Page CHAPTER 1. GENERAL INFORMATION

CHAPTER 1. GENERAL INFORMATION TABLE OF CONTENTS Page 1-1 LEGISLATIVE HISTORY... 1-1 1-2 PURPOSE OF THE PROGRAM... 1-1 1-3 CHARACTERISTICS OF THE MORTGAGE... 1-1 1-4 PRINCIPAL LIMIT... 1-2 1-5 PAYMENT

CHAPTER 1. GENERAL INFORMATION TABLE OF CONTENTS Page 1-1 LEGISLATIVE HISTORY... 1-1 1-2 PURPOSE OF THE PROGRAM... 1-1 1-3 CHARACTERISTICS OF THE MORTGAGE... 1-1 1-4 PRINCIPAL LIMIT... 1-2 1-5 PAYMENT

20 Hour SAFE Comprehensive: Financing Residential Real Estate

20 Hour SAFE Comprehensive: Financing Residential Real Estate COURSE MANUAL Days 1-4 Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director 9/16 NMLS Rules of Conduct for Students (ROC) Day 1 Real

20 Hour SAFE Comprehensive: Financing Residential Real Estate COURSE MANUAL Days 1-4 Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director 9/16 NMLS Rules of Conduct for Students (ROC) Day 1 Real

GENERAL FINANCING QUESTIONS

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

Premium Jumbo 7/1 & 5/1 ARM

Premium Jumbo 7/1 & 5/1 ARM Program Codes: PJ 7/1 & PJ 5/1 ARM Purchase and Rate/Term Refinance Primary (Purchase) Primary (Rate/Term Ref.) Max Loan Amt Max LTV/CLTV Min Fico DTI Reserves Max Loan Amt

Premium Jumbo 7/1 & 5/1 ARM Program Codes: PJ 7/1 & PJ 5/1 ARM Purchase and Rate/Term Refinance Primary (Purchase) Primary (Rate/Term Ref.) Max Loan Amt Max LTV/CLTV Min Fico DTI Reserves Max Loan Amt

SEDGWICK COUNTY, KANSAS & SHAWNEE COUNTY, KANSAS SINGLE FAMILY MORTGAGE LOAN PROGRAM PROGRAM GUIDELINES

v7 SEDGWICK COUNTY, KANSAS & SHAWNEE COUNTY, KANSAS SINGLE FAMILY MORTGAGE LOAN PROGRAM PROGRAM GUIDELINES These Program Guidelines constitute the Program Guidelines referred to in the Servicing Agreement

v7 SEDGWICK COUNTY, KANSAS & SHAWNEE COUNTY, KANSAS SINGLE FAMILY MORTGAGE LOAN PROGRAM PROGRAM GUIDELINES These Program Guidelines constitute the Program Guidelines referred to in the Servicing Agreement

Trio is the best solution

Trio is the best solution Why trio exists W H Y T R I O E X I S T S : Here s the reality Approximately 30% of mortgage applicants are denied. The US housing market has high demand for an alternative to

Trio is the best solution Why trio exists W H Y T R I O E X I S T S : Here s the reality Approximately 30% of mortgage applicants are denied. The US housing market has high demand for an alternative to

SELECT MORTGAGE GUIDELINES

SELECT MORTGAGE GUIDELINES Guidelines are for use by mortgage professionals only and subject to change without notice. TABLE OF CONTENTS TABLE OF CONTENTS... 2 RESPONSIBLE LENDING STATEMENT... 6 PRODUCT

SELECT MORTGAGE GUIDELINES Guidelines are for use by mortgage professionals only and subject to change without notice. TABLE OF CONTENTS TABLE OF CONTENTS... 2 RESPONSIBLE LENDING STATEMENT... 6 PRODUCT

FHA FIXED PROGRAM HIGHLIGHTS

Product Summary These guidelines represent the companies underwriting requirements for FHA fixed rate and ARM mortgages, and are to be utilized in conjunction with the following FHA Handbooks: 4155.1 for

Product Summary These guidelines represent the companies underwriting requirements for FHA fixed rate and ARM mortgages, and are to be utilized in conjunction with the following FHA Handbooks: 4155.1 for

REVERSE MORTGAGES JUST MAKE SENSE. How to Expand Your Business Now

REVERSE MORTGAGES JUST MAKE SENSE How to Expand Your Business Now At your fingertips It s an opportune time to explore how to expand your business within the Finance of America family. We ve created this

REVERSE MORTGAGES JUST MAKE SENSE How to Expand Your Business Now At your fingertips It s an opportune time to explore how to expand your business within the Finance of America family. We ve created this

Section 2.06 Key Loan Program

Section 2.06 Key Loan Program In this Product Description This product description contains the following topics. Overview... 2 Features and Benefits... 3 Related Bulletins... 3 Loan Terms... 4 ARM Parameters...

Section 2.06 Key Loan Program In this Product Description This product description contains the following topics. Overview... 2 Features and Benefits... 3 Related Bulletins... 3 Loan Terms... 4 ARM Parameters...

Ability-to-Repay Rule

This summary is provided by the Minnesota Credit Union Network for informational purposes only, and is intended to provide credit unions with the general regulatory requirements and effective dates for

This summary is provided by the Minnesota Credit Union Network for informational purposes only, and is intended to provide credit unions with the general regulatory requirements and effective dates for

Assistance Program: City of Tuscaloosa Home Purchase Assistance Program Code: DALTUSHPP

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year