REPORT TO THE WAKE COUNTY BOARD OF COMMISSIONERS ON WAKE COUNTY ACTIONS TAKEN AS A RESULT OF THE REGISTER OF DEEDS OFFICE THEFT.

|

|

|

- Gwendolyn Booth

- 5 years ago

- Views:

Transcription

1

2

3 Purpose of Report REPORT TO THE WAKE COUNTY BOARD OF COMMISSIONERS ON WAKE COUNTY ACTIONS TAKEN AS A RESULT OF THE REGISTER OF DEEDS OFFICE THEFT Background and Context Cash Policies Deposit Locations Cash Collection Audits Annual Audits Table of Contents Actions Taken by County Management with Respect to the Register of Deeds Office Timeline of Events Internal Audit Register of Deeds Office Finance Actions Taken by County Management with Respect to County-Wide Cash Handling Policy and Procedures Review Increased Use of Payment Methods Other than Cash Increased Oversight of Cash-Handling Procedures Attachments A B C D E F G Cash Management Policy Cash Collections Procedure Summary of Internal Audit Cash Reviews Management Representation Letter for Annual Audit Draft Memorandum of Understanding between County and Register of Deeds Office Fraud, Waste and Abuse Policy Register of Deeds Office New Currency and Cheque Handling Process

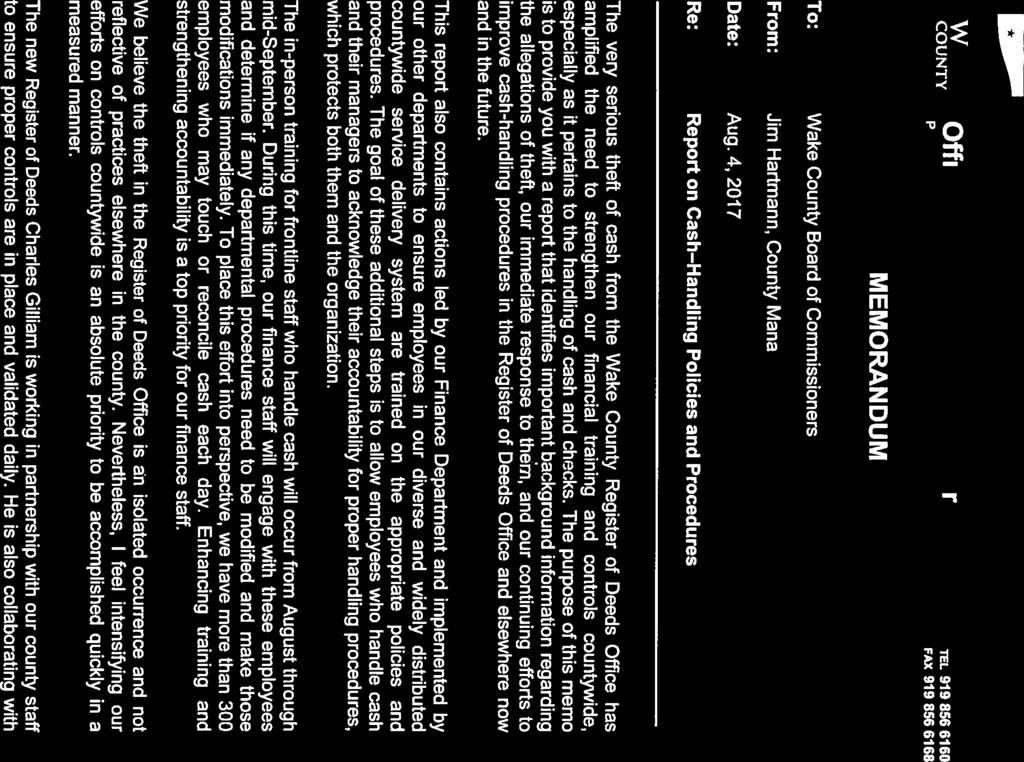

4 PURPOSE OF REPORT North Carolina General Statute ( NCGS ) Chapter 161 speaks to the responsibilities of the registers of deeds. Registers of deeds in North Carolina are separately elected officials accountable to the citizens of the County. NCGS requires that all fees collected under this section be deposited into the county general fund. The purpose of this report is to provide information regarding actions with respect to the with respect to the Register of Deeds Office theft. Additionally, the report includes information regarding cash handling that fall within the responsibilities of the County Manager of efforts taken and forth coming to confirm that sound cash handling procedures are in use throughout the County. BACKGROUND AND CONTEXT For FY 2017, the County collected approximately $390 million in cash and checks. However, the majority of the County s revenues, approximately 80%, are received via electronic funds transferred directly into County bank accounts. The amounts received by electronic fund transfers include property tax, sales tax, funding from the state and federal governments, and amounts from banks and credit card companies for fees collected via credit cards. The County s largest revenue source is property tax. The Revenue Department is charged with collection of these taxes. The Revenue Department is the only department whose core function involves revenue collections. Given the magnitude of the dollars it collects, the Revenue Department has the most stringent controls and systems of any collection site. Effectiveness of these controls is evidenced by a collection percentage for FY 2017 of: 99.9% for real estate and personal property; 99.52% for motor vehicles; and 99.87% overall. Cash Policies: The County updated its cash management policy and cash collections procedure in October These procedures are in place county-wide and generally apply to all areas of cash collection. Outside of the Revenue Department, cash handling is currently decentralized, with County departments and department directors being ultimately accountable for departmental procedures and adherence to county-wide procedures. Departments can tailor specific procedures for their business processes as long as they are consistent with the County s general policy. Attachment A and B: Cash Management Policy and Cash Collection Procedure. Deposit Locations: The County has 71 deposit locations sites throughout the County. A deposit location is a location that collects funds and deposits them in one of the County's bank accounts. Examples of collection locations include libraries, Human Services facilities and landfills. The Finance Department uses a specific 4-digit code to track each deposit location. Approximately $24 million in checks and currency are collected in decentralized locations throughout the County with an average daily cash and check collection of $1,500. Approximately 45% of the deposit locations collect less than $100 per day on average. The average daily deposit per person was $303 in Fiscal Year Cash Collection Audits: Reviews of cash procedures are conducted periodically by the County s Internal Audit Office. From December 2014 to July 2017, the Internal Audit Office performed review procedures at approximately 10 sites. A summary of the reviews and the findings is included in Attachment C. There were no significant findings from these cash reviews and no indications of

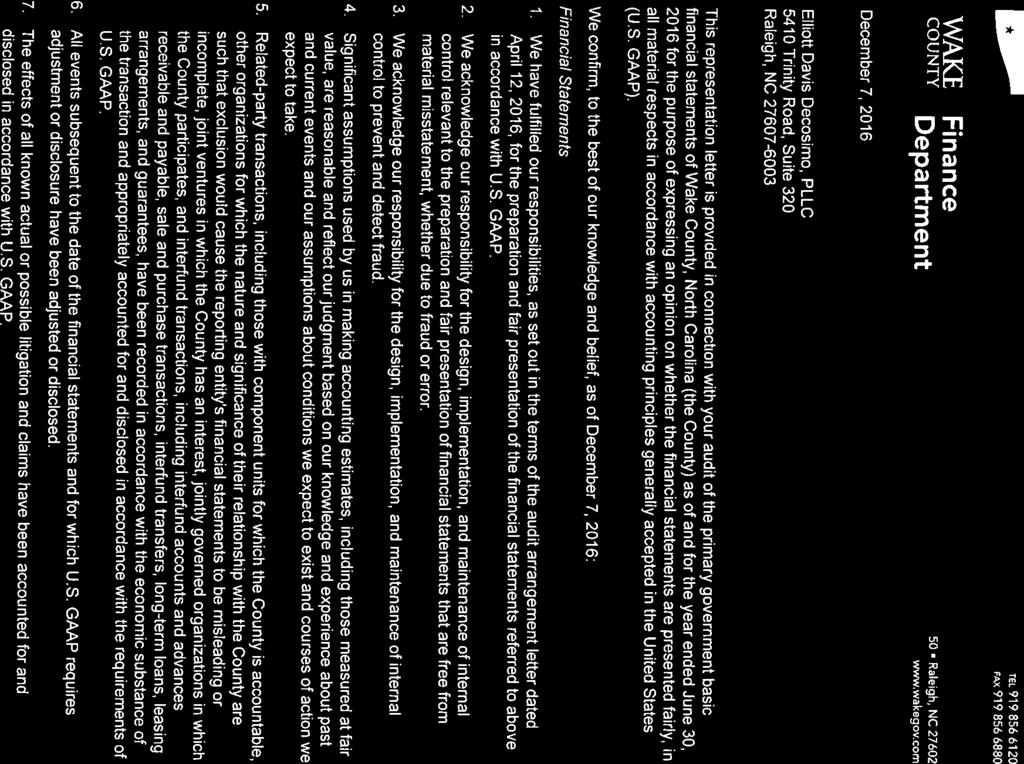

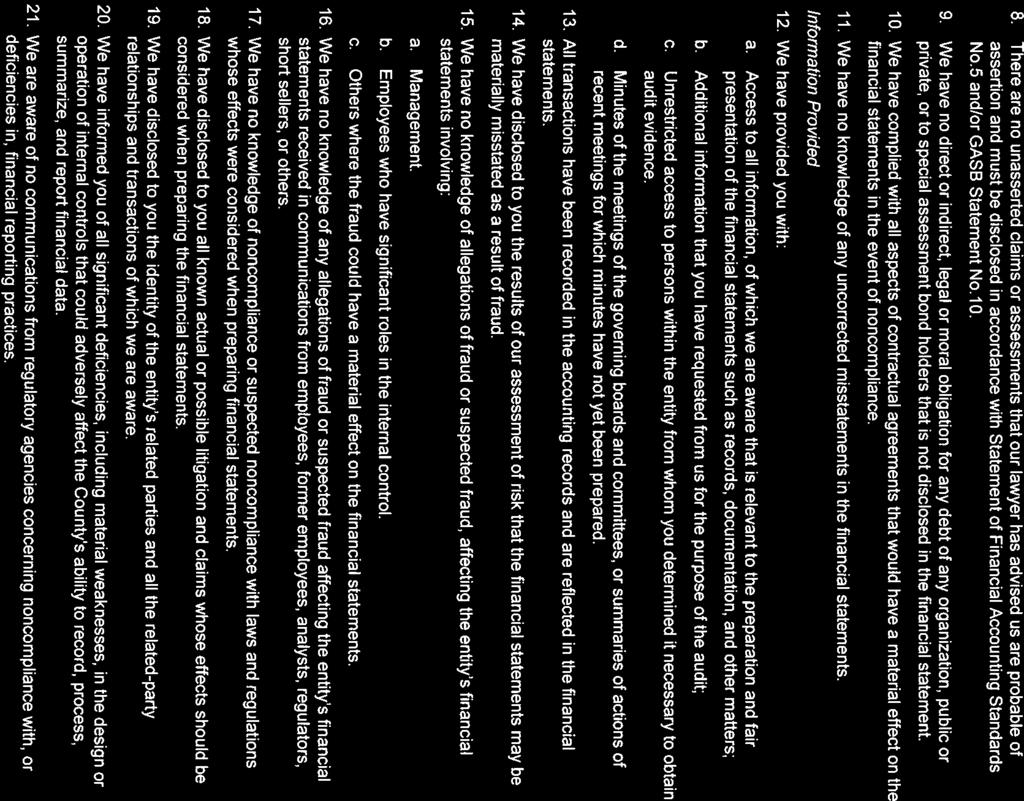

5 mishandling of cash. If Internal Audit receives any information regarding mishandling of cash or other County assets, an investigation is conducted to identify potential issues and improvement of business processes as preventative measures. Annual Audits: The County is required to have an external audit conducted annually. An excerpt of the Independent Auditor s Report from the FY 2016 audit is provided below. The auditor s responsibility is to express opinions on the financial statements based on their audit. The audit also includes evaluating the appropriateness of accounting policies and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. Management is responsible for the maintenance of internal control relevant to the preparation and fair presentation of the financial statements that are free from material misstatement, whether due to fraud or error. For each annual audit, management attests to procedures followed and information provided upon which the auditors rely on in the course of their audits. A copy of the FY 2017 Management Representation is provided as Attachment D. All annual independent audits have resulted in an unqualified, clean opinion. As part of the annual external audit, the auditors may report to the Board any internal control or operational issues identified during the course of their audit work through an audit management letter. During the period of 2007 to 2016, there were no management letters issued by the external auditors. Additionally, there have been no findings in the auditor s reports regarding internal controls over the processing of cash payments. Full copies of the Wake County Compliance Reports can be found at:

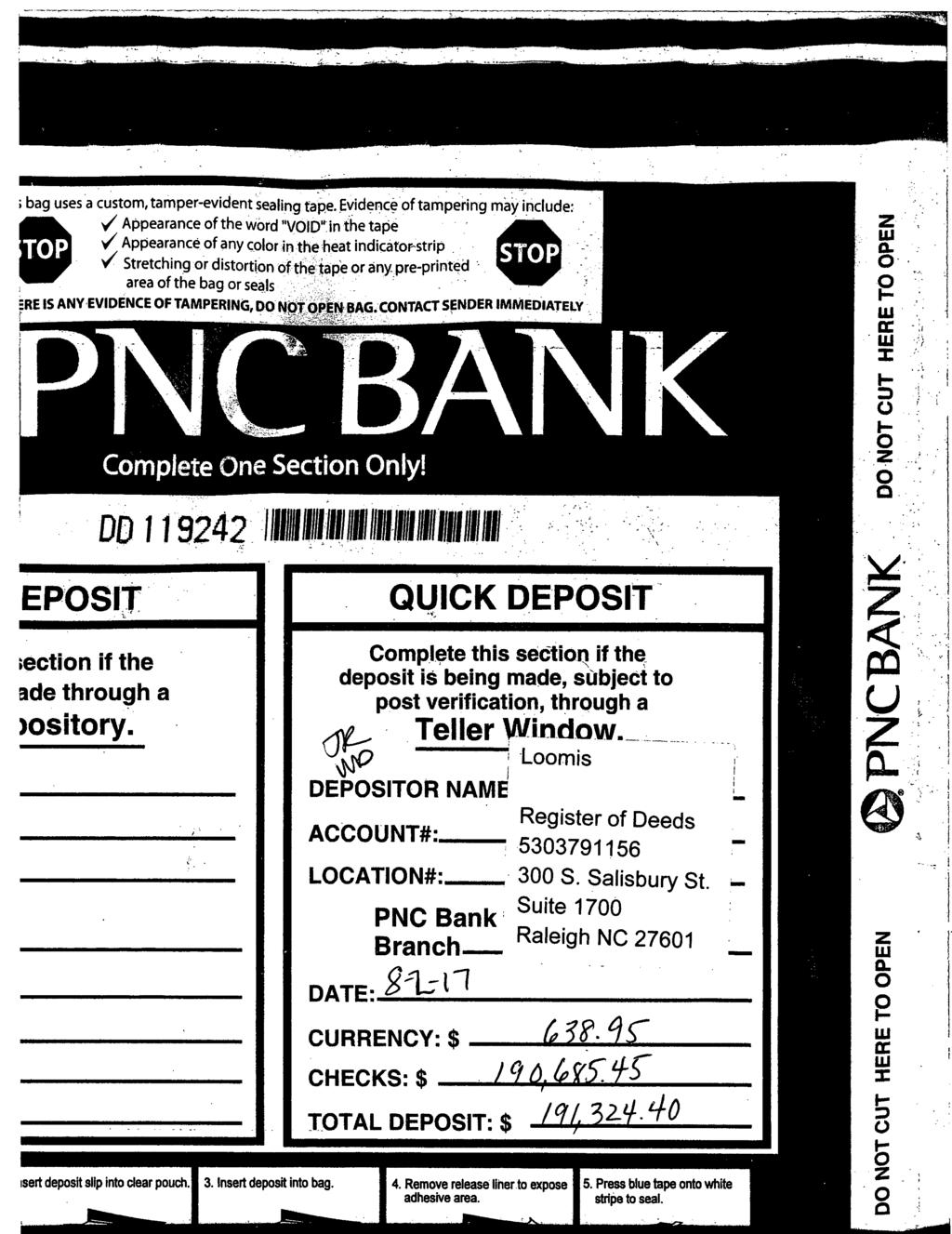

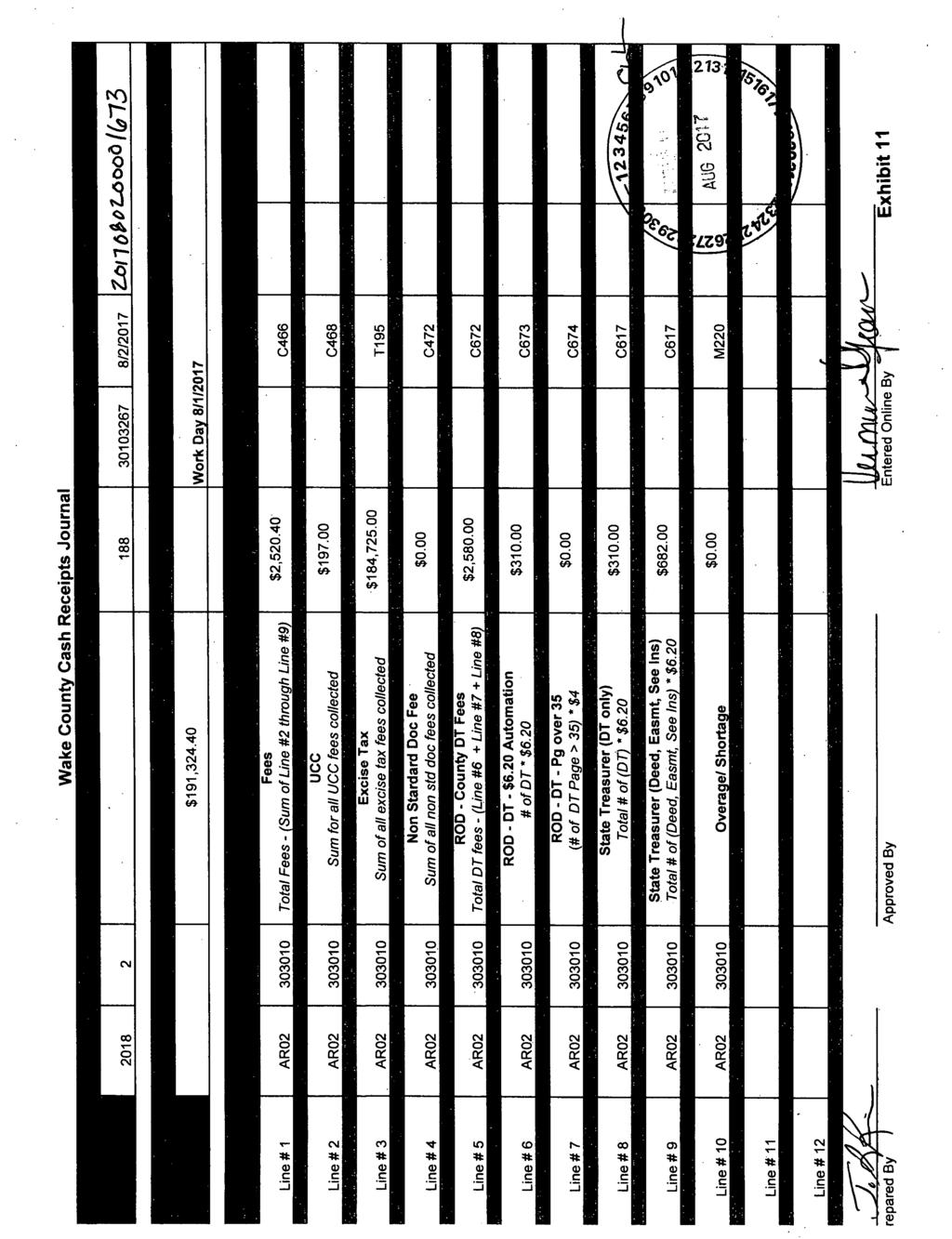

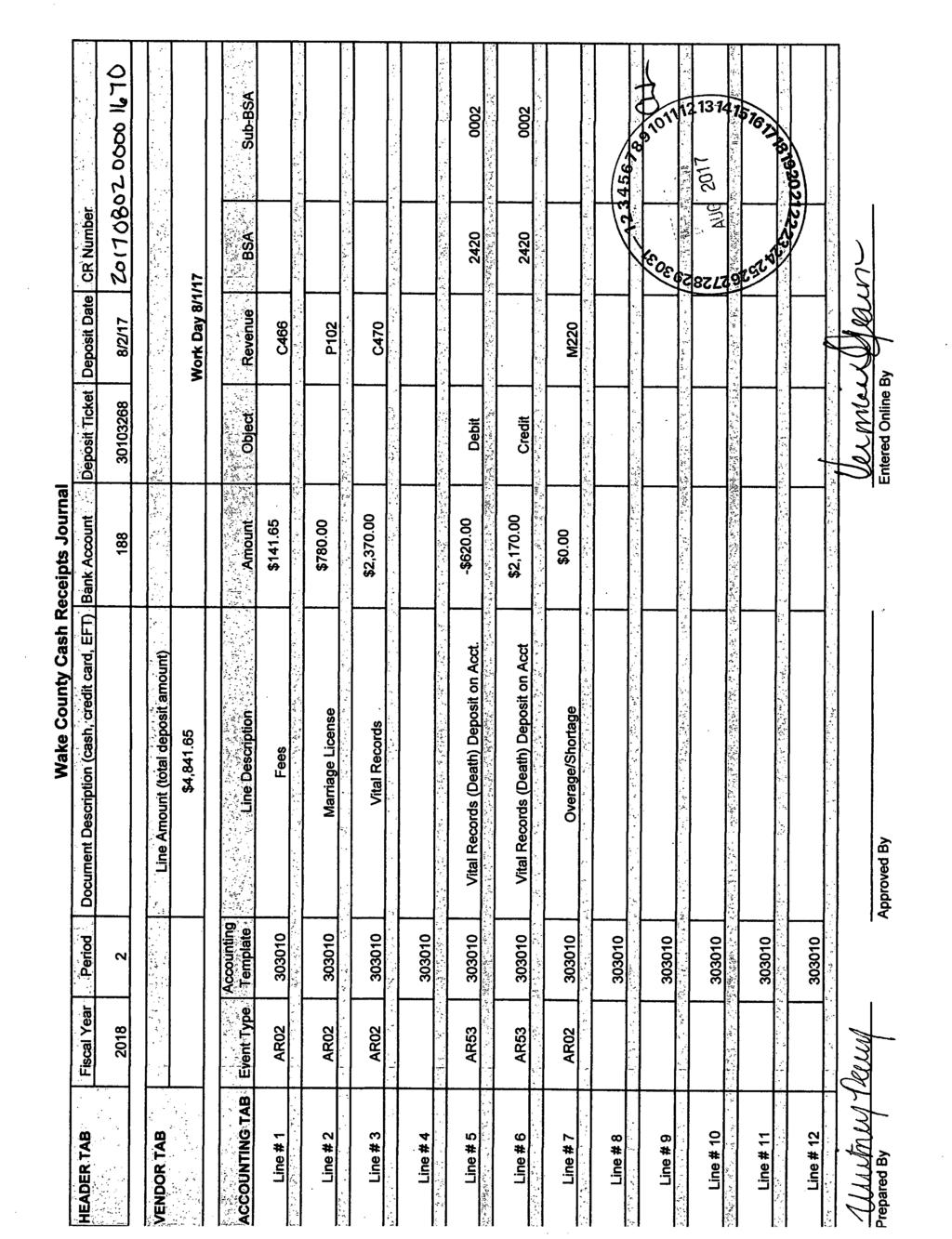

6 ACTIONS TAKEN BY COUNTY MANAGEMENT WITH RESPECT TO THE REGISTER OF DEEDS OFFICE The following section outlines specific actions taken by the County directly related to the Register of Deeds (ROD) Office s cash handling and reconciliation. TIMELINE OF EVENTS Upon being made aware of the issues within the Register of Deeds Office, the following actions were taken: 1. On Jan. 30, 2017, the County Manager was made aware that a Register of Deeds Office employee had identified financial discrepancies in the Register of Deeds Office daily deposits. 2. On Feb.1, 2017, the County Manager and County Attorney consulted with the District Attorney to obtain guidance with respect to steps to move toward a criminal investigation. 3. Pursuant to the District Attorney s direction, on Feb. 1, 2017, the County Manager informed the Internal Audit Director of a problem in the Register of Deeds Office with the cash receipts process. 4. The Internal Audit Director requested that the IT Director make a secure back-up of the land records database and the vital records database prior to beginning any audit work as a precaution against tampering of data. Per the IT Director s on Feb. 1, 2017, at 5:07 p.m., the backups were made and put in a secure location. 5. On Feb. 2, 2017, the County Manager and County Attorney met with the Register of Deeds, Laura Riddick, to inform her of the need to proceed with an internal audit. Following that meeting, Internal Audit met with the Riddick on Feb. 2, 2017, to explain the cash receipts review to be conducted. The review process was explained, and a strategy for communicating about it with the Register of Deeds Office and its employees was determined. Employees were informed that Internal Audit was reviewing and assessing the cash receipts process to improve and enhance the cash-handling and recording procedures. 6. On Feb. 3, 2017, Internal Audit began gathering information to gain an understanding of the Register of Deeds Office functions and processes. The period selected for testing was January 2016 through January 2017, during which 263 deposits were made. Deposit slips and copies of daily reports were made for the January 2016-January 2017 time period (except for the month of August 2016, which were inadvertently shredded). The daily reports copied were obtained from the ROD Office. Deposit slips for the entire period are on file within the Wake County Finance Department. 7. Beginning Feb. 3, 2017, Internal Audit began verifying daily deposit amounts against system reports to verify that all receipts were properly accounted for, based on system documentation. Since this date, deposits made by the ROD Office have reconciled to system reports exactly or within normal cash shortages/overages that have averaged $4.02 in overages. Information regarding systems: The Wake County Finance Department maintains the financial records on behalf of the County. The general ledger revenue amounts and bank deposit amounts were combined into one electronic file and verified using Audit Command Language ( ACL ). ACL is data analytics software used to: Capture, cleanse and normalize data to ensure consistency and accurate results, Identify trends, pinpoint exceptions and highlight potential areas of concern, Join files based on a key field, Determine what records or fields in two files match (or don t), Locate errors and potential fraud,

7 Age and analyze financial or any other time-sensitive transactions; and Schedule, script and automate analyses. The ROD Office utilizes two different computer systems to serve the public. One system covers land records and other recordings, and the second system covers vital records, such as birth, death, marriage, etc. 8. On Feb. 21, 2017, Internal Audit witnessed and controlled the cashiering functions from the beginning of the day until funds were locked in the safe at the end of the day to determine the appropriateness of the procedures. Internal Audit assisted ROD Office employees with preparing the deposit for the work day Feb. 21, In addition, Internal Audit delivered the checks and currency to the bank on Feb. 22, An overage of $16.40 occurred for Feb. 21, Otherwise, all recorded amounts on the daily revenue summary and the daily fee summary agreed to the total amount deposited. 9. Internal Audit Transaction Review: Internal Audit conducted a statistically valid audit sample of 30 deposits. They were selected to vouch for the underlying source documentation from 263 deposits made during the sample period. The sample period was between workdays Monday, Jan. 4, 2016, and Tuesday, Jan. 31, Transactions conducted online via the company Permitium for vital records and erecording for land and other recordings are not included in the deposits indicated above. Selected deposits cover transactions occurring at the Wake County Justice Center, Suite ACL was utilized to select the sample. ACL also recalculated and identified the specific documents associated with the fees earned. After the 30-day sample was reviewed, Internal Audit identified more than $36,000 in unaccounted for transactions. Unaccounted for transactions are transactions that are recorded in the ROD Office s systems (not the general ledger) and supported by documentation indicating services were delivered, but not deposited into Wake County bank accounts. 10. On May 17, 2017, the County engaged Elliott Davis, the County s external auditors, to review the work of Internal Audit related to the ROD Office to substantiate the amount of unaccounted for transactions so the County could file an insurance claim to recover losses resulting the ROD Office theft.

8 INTERNAL AUDIT During the initial stages of our review of the Register of Deeds Office cash receipts function, Internal Audit made several recommendations for improvement in internal controls. Internal Audit verbally communicated these recommendations immediately so corrective action could be taken as soon as possible and monitored daily reconciliations. Below is a summary of those recommendations, all of which comply with the County s cash policies and procedures.: 1. Lock change funds in the safe overnight rather that leaving the funds in the cash drawers. Cash drawers should be empty overnight and left open and unlocked. 2. Staff should count the change fund amounts added to the drawer each morning and have a second staff member verify the count. The same process should be followed at the end of the day. 3. Only one person should use the cash drawer and process transactions for a station to establish clear accountability for the cash and records. 4. Receipt totals for each cash drawer should be reconciled to the record of transactions by each individual cashier and verified by a second employee. 5. The total deposited each day should be completely reconciled to the system reports. Since two separate cashiering systems are utilized by the Register of Deeds Office, two separate deposits should be prepared based upon the cash receipts report from each system. 6. Amounts recorded in the Register of Deeds Office subsidiary systems (Northrop Grumman and Granicus) should be reconciled to the amounts entered into the Advantage general ledger. 7. Responsibility for preparing the deposit, reconciling to the subsidiary systems (Northrop Grumman and Granicus) and making the entry to the Advantage general ledger should be segregated such that the work of one employee automatically provides a cross-check of the work of the other employees. 8. Proper segregation of duties should be documented on deposit information. The individual responsible for preparing the deposit should be indicated, and a different individual s initials should appear to indicate approval of the reconciled deposit. 9. Only supervisors should be allowed to approve voided transactions, and written explanations for voids should be clearly documented. 10. Approval and verification procedures conducted throughout the process should be documented by signing or initialing applicable documents. 11. An overall review for unusual transactions should be performed along with an investigation of overages/shortages. Explanations for overages/shortages should be attached to deposit documentation for amounts greater than $ Records for prepaid accounts should clearly identify the deposit owners and be recorded in the Advantage general ledger. 13. Checks received should be restrictively endorsed for deposit only as soon as they are received. 14. A currency-counting machine with the ability to detect counterfeit bills should be purchased. 15. Use a daily collections form for the information center to accompany cash collections as funds are turned in for deposit preparation. The form we designed for use indicates the amount of collections and chain of custody for collections.

9 REGISTER OF DEEDS OFFICE The new Register of Deeds, Charles Gilliam, supported and continued the new internal controls and processes implemented by Internal Audit in the Register of Deeds Office upon his appointment. Gilliam s summary of the new procedures is included in Attachment G. Additional initiatives planned by Gilliam include: 1. The accounts of the Register of Deeds Office should be audited at least annually by auditors chosen by the County finance officer in accordance with N.C.G.S During FY 2018, conduct an information systems audit of the recording system (e.g. the Northrop Grumman software) to validate internal controls. 3. Begin accepting electronic payments (credit and debit cards) from consumers for transactions in the vital records function (notary, birth, death and marriage records). The Register of Deeds Office is currently working with the County finance office to implement electronic payments by December FINANCE DEPARTMENT As a result of the Internal Audit work, the Finance Department reviewed existing policies with respect to the daily deposit reconciliation for the Register of Deeds Office ( ROD ). Register of Deeds Deposit Documentation Documentation Received in Finance Prior to ROD Office Theft The Finance Department verified that the spreadsheet amounts provided by the ROD Office matched the deposit ticket and the bank file deposit amount. Documentation Received in Finance Subsequent to ROD Office Theft Recording transactions and vital records transactions are done as separate bank deposits and posted as two cash receipt documents in our financial system. Recording Transactions - Documentation Received: The cash accepted to pay for reproduction and copies is now counted, verified and signed by two different individuals. The system-generated daily summary report is now structured by document type and includes quantity count. The department-generated cash receipts journal is now structured by revenue code, and counted, verified and signed by two different individuals. The breakdown between cash and checks on the deposit ticket should equal the breakdown of cash and checks in the system reports. The bank deposit ticket is now counted, verified and initialed by two different individuals. The bank system deposit amount is verified against the department generated cash receipts journal. (This procedure is the same for both prior and subsequent procedures.) Vital Records Transactions - Documentation Received: The system-generated daily fees summary report is now structured by document type and includes a quantity count. The department-generated cash receipts journal is now structured by revenue code, and counted, verified and signed by two different individuals.

10 The breakdown between cash and checks on the deposit ticket should equal the breakdown of cash and checks in the system reports. The bank deposit ticket is now counted, verified and initialed by two different individuals. The bank system deposit amount is verified against the department generated cash receipts journal. (This procedure is the same for both prior and subsequent procedures.) For both types of transactions above, the Finance Department compares and verifies each bullet item to ensure accuracy. Any overage/shortage in the ROD Office greater than $10, must have written and attached documentation. For other departments, currently cash overages and shortages in excess of $50 must be individually reported. Proposed Memorandum of Understanding with Register of Deeds The Finance Department has drafted a Memorandum of Understanding ( MOU ) to clearly and formally document with the Registrar the County s responsibility for oversight of and ability to review the financial transactions and records of the Register of Deeds Office at any time. The MOU has been shared with Registrar Charles Gilliam, and we expect to present it to the Board of Commissioners for consideration in September See Attachment E for the Draft MOA

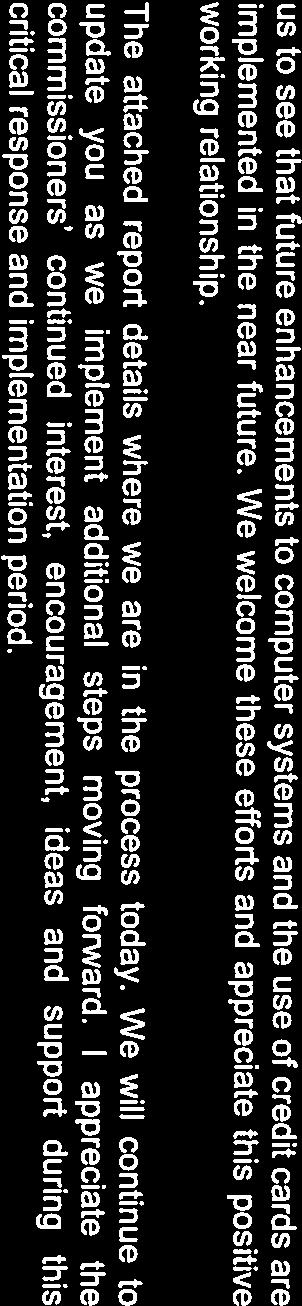

11 ACTIONS TAKEN BY COUNTY MANAGEMENT WITH RESPECT TO COUNTY-WIDE CASH HANDLING The following section outlines specific actions taken by the Finance Department with respect to Countywide cash-handling procedures. Policy and Procedure Review Cash Related: The Finance Department reviewed current policies and procedures related to cash to identify possible revisions for strengthening. To date, no changes are proposed to the internal controlrelated portion of the policy or the procedures as they are sound if followed. It is anticipated that changes will be made with respect to revenue reconciliation and the supporting departmental information that is provided to the Finance Department. Fraud Waste and Abuse: The County did not have a formal policy on fraud, waste and abuse. Having such a policy is considered a best practice. The Finance Department presented a draft policy to the County s Senior Leadership Team ( SLT ) on June 15, The SLT is comprised of the County Manager s Office and all department directors. All county-wide policies are presented to SLT for input, review and ultimately approval, as department directors are responsible for the adherence to County policies within their departments. The policy was released to the organization on Aug. 4, 2017 with an effective date of Aug. 1, See Attachment F Fraud Waste and Abuse Policy Increased Use of Payment Methods Other than Cash Over the past several years, the County has been working to increase the number of locations throughout the county where credit and debit cards are accepted. The County hired its first Payment Card Industry ( PCI ) Compliance Officer in June 2016 to support these expanded efforts. The PCI Compliance Officer in the Finance Department will review collections sites that currently only take cash and checks to implement increased credit and debit card acceptance as soon as is practical. Increased Oversight of Cash-Handling Procedures Wake County Government is comprised of 20 departments and agencies. The directors of those departments and agencies are responsible for the operations of their departments, including compliance with all County policies and procedures. As a result of the Register of Deeds Office incident, the County Manager has directed the Finance Department to work to increase its oversight of cash-handling procedures. An outline of the major components of this increased oversight is provided below. 1. Department / Agency Head Certification: Department and agency heads reporting to the County Manager have delegated authority and accountability for management of their department operations and staff. All County department /agency heads have been required to certify their responsibility for cash handling. The following certification was distributed to on Aug. 2, 2017 with completion expected by Aug. 4, Acknowledgement of Department / Agency Heads Certification Language: I acknowledge that I am aware of and understand the Wake County Cash Management Policy and related cash collection procedures. I understand that daily deposits of all receipts are required to be made into authorized Wake County bank accounts and that revenue reconciliation processes for deposits are required. I understand that my department s compliance with these policies and procedures is my responsibility.

12 2. Designation of a Treasury Contact: Each County department/agency has been asked to designate an employee(s) as a Treasury Contact for every deposit location. The Treasury Contact is a supervisory position that understands a specific deposit location s business processes and the subsystems used by that site to receive funds or track transactions that impact their deposit amounts. Treasury Contacts are expected to be familiar with the daily collection and reconciliation processes at their deposit location(s) and able to provide names of staff involved in these processes. Treasury Contacts will be responsible for ensuring that County and departmental procedures are properly followed. a. The first task of the newly identified Treasury Contacts will be to provide the names and position numbers for each employee that has involvement in the collection and deposit process based on definitions of roles provided by the Finance Department. b. Initial training for the Treasury Contacts is expected to be completed by Aug. 11, Upon completion of the training sessions in his or her new role, Treasury Contacts will be asked to certify awareness of County policies regarding cash handling and the responsibility to comply with those policies. c. Finally, Treasury Contacts will work with the Finance Department and Internal Audit to identify cash handling business processes that need to be improved or strengthened to ensure full compliance with required procedures. Those locations that process higher levels of cash and checks will be prioritized ahead of those that receive limited or infrequent deposits. 3. Training for Cashiers and Immediate Supervisors: Given the current diverse and widely distributed locations of cash handling operations, the Finance Department is developing mandatory training for all cashiers and their immediate supervisors. It is estimated that approximately 300 people across the County will receive the new training. a. Initial Approach: All cash handlers will be required to attend training delivered by the Finance Department. At the conclusion of the training, the cash handlers will be asked to certify their awareness of County policies and procedures regarding cash handling and their responsibility for compliance. It is expected that this training and the certifications will be completed by the middle of September b. Finance will work interactively with the Treasury Contacts and cashiering staff, making sure that they are using procedures as required and that the Finance Department is receiving information for our audit files that demonstrate on-going departmental compliance with cash handling procedures. c. New Hires: Beginning in September 2017, employees hired or promoted into positions that handle, manage, or oversee cash, checks, or credit cards will be required to complete cash handling training and certify their understanding of policies and procedures related to job duties prior to handling cash..

13 WakeCountyCashManagementPolicy X Countywideor Department: Division: Supersedes:N/A EffectiveDate:10/31/2010 ApprovingAuthority:FinanceDirector OriginatingDepartment(s):Finance I. Purpose: Thepurposeofthispolicyistoestablishsoundcashmanagementpracticesthatfulfillthefollowing goals: 1) Ensureefficientutilizationofcashwithagoaltoaccelerateandcontrolcollectionsofcashand receivables, 2) Promotepromptdepositofreceipts, 3) Improvecontroloverdisbursementmethodsincludingtimelypaymentofvendors, 4) Investidlecashbalances,and 5) ComplywithTheLocalGovernmentBudgetandFiscalControlAct,localbudgetordinances, GenerallyAcceptedAccountPrinciples(GAAP)forlocalgovernments,andanyotherrequired statutes,standards,orindustrybestpractices. II. PolicyStatement: WakeCountywilladheretoN.C.G.S.Chapter159,SubchapterIII,Article3,TheLocalGovernment BudgetandFiscalControlAct( GovernmentCommission( Commissiontoissuerulesandregulationsrelatedtoassetsoflocalgovernmentunitsandpublic authoritiesincludingcashmanagement. Inadditiontothisact,theCountywilladheretoGAAPasapplicabletogovernmentsintheUnited StatesofAmerica.TheCountywillalsoimplementinternalcontrolstosafeguardtheCounty s assetsandprovidesoundstewardshipoverthepublic sassets.thispolicyprovidesaframework forthoselegalresponsibilitiesandassociatedstewardshipresponsibilitiesforcashmanagement. Bystatute,theFinanceOfficerhastheresponsibilityforWakeCountycashmanagementplan.The areasofresponsibilityaddressedinthispolicyforthecountyinclude: 1) Receipts, 2) Disbursements, 3) Investments, 4) AccountsReceivable/Billing, 5) Collections,and 6) RemovalofUncollectibleAccountsfromSubsidiaryLedgers OversightofallCountyactivitiesunderthesecategoriesistheresponsibilityoftheFinanceOfficer andcanonlybedelegatedbythefinanceofficer. A. Receipts TheobjectivesofmanagingreceiptsaretousediligenceincollectingfundsowedtotheCounty, provideinternalcontrolovercashandcashequivalents,andexpeditethe movementofmoney

14 collectedintointerestbearingaccounts.throughoutthisprocess,anyonehandlingcashreceipts willadhereton.c.g.s DailyDepositsaswellasotherFederalandStatelaws,County ordinances,industrystandards,andregulations. B. Disbursements TheCountywillmanagedisbursementstomaintainfundsininterestbearingaccountsuntilfunds arerequiredforpayment.doingsoallowsthecountytorealizethemaximumearningpotentialon itsfunds.itisnotintended,however,toencouragelatepaymentorcausedetrimental relationshipswiththevendorswho,ingoodfaith,supplygoodsandservicestothecounty.infact, thecountyshouldtakediscountsfortimelypaymentswhenpossiblebypayingonthediscount dateorduedate.priortodisbursementoffunds,thefinanceofficerordesigneeassignedthe responsibilityforpaymentofobligationswillperformappropriatecashdisbursementpreaudit procedures. C. Investments TheFinanceOfficerdelegatestheresponsibilityofcashmanagementanddailyinvestingofidle cashbalancestothefinancialservicesdirectorandtheinvestmentanalyst.nootherindividuals areauthorizedtoinvestcountyfunds.theobjectiveofinvestmentsistoensureefficientutilization ofcashinamannerconsistentwiththeoverallstrategicgoalsofmaximizinginterestbearing investmentsofcashwhileminimizingidleandnonproductivecashbalances. TheCounty sprioritiesforinvestmentsaresafety,liquidity,andyieldwiththeemphasisonsafety ofprincipalandtimelypaymentofallcountyliabilities.staffmanagesthecounty sfundsin conjunctionwiththecounty scashflowconsultantinaccordancewithguidelinesestablishedby N.C.G.S PertheCounty sinvestmentpolicy,bondproceedsandoperatingportfolioinvestmentsareonly investedwithprimarydealersorbanksthatcarryminimumshorttermratingsofa1fromstandard andpoor sandp1frommoody s.theseratingsarethehighestgradeofshortterm creditworthiness.thecountyattemptstodiversifyitsbusinessamongdealersandbankswhile seekingthebestpricepossible.thecountywillusethecurrentlistofprimarydealers,whichcan befoundonthefederalreservebankofnewyork swebsite,toguideitsselectionofdealers. AllbanksthatholdWakeCountydepositsmustcollateralizethosedepositsusingthepooling methodasrequiredbyn.c.g.s andbedesignatedbytheWakeCountyBoardof Commissionersasanofficialdepository. D. AccountsReceivableandCollections Whenindividuals,businessentitiesandgovernmentsowefundstotheCounty,staffmusttakeall appropriateactionstocollectaccountsreceivableandminimizetheriskoflossduetononpayment whencosteffective. TheCountydoesnotpromotedeferredpaymentplansforamountsowedtotheCounty.However, thefinanceofficermayauthorizedeferredrepaymentplansinordertoprovideeveryopportunity toindividuals,businessentitiesorgovernmentstorepaydebtstothecounty.

15 TheAccountsReceivableandCollectionsPolicycoversthebilling,collection,andrecordkeepingof accountsduetowakecounty.taxesandhousingaccountsarecoveredbyncgeneralstatutes andotherregulationsandarethereforeexcludedfromtheaccountsreceivableandcollections Policy.Refertothispolicyforinformationon: 1) SegregationofdutieswithinAccountsReceivableFunction; 2) Billing; 3) Collections; 4) MaintainingAccountsReceivableRecords/GeneralProgramSpecificSoftware/Subsidiary SystemRequirements; 5) InterestandPenaltyFees; 6) ReturnedChecks(NSF); 7) AccountsReceivableBillingandCollectionsbyContractedVendors;and 8) RemovalofUncollectibleAccountsfromSubsidiaryLedgers. III. IV. V. Definitions: Accountingstandards accountingrulesestablishedbyboardsthatestablishconsistentpractices forentitiestofollowtoensurethatfinancialinformationisconsistentlyreportedandfairlystated andallowsfinancialreaderstomoreeasilycomparedifferententities. Cash Cashisdefinedascoins,currency,checks,moneyorders,creditanddebitcardpayments, ACHpaymentsoranyotherlegallyacceptableelectronicmeans. CashManagement Thestrategybywhichanentityadministersandinvestsitscashandcontrols cashcollections. Disbursements Paymentsmadeinthedischargeofadebtorexpense. Idle/nonproductivecashbalances Situationinwhichcashisinactive;notbeinginvestedthereby notearningreturns/interest. GAAP Generallyacceptedaccountingprinciples(GAAP)areestablishedbythe GovernmentalAccountingStandardsBoard(GASB)whichcurrentlysetsthestandardsfor StateandLocalgovernmentsintheUnitedStatesofAmerica.Aswithmostoftheentities involvedincreatinggaapintheunitedstates,thegasbisanindependent,non governmental,nonprofitfoundation. Liquidity Theabilityofanassettobeconvertedtocashquicklyorwithoutanypricediscountand maintainingtheabilitytopayobligationswhentheybecomedue. PrimaryDealerBanksorsecuritybrokeragesthattradeinUSGovernmentsecuritieswiththe FederalReserveBankofNewYork. Receipts Collectionofpaymentsorcash. ReceivableAnassetoftheCountyreflectingadebtthatisowedtotheCountyandhasnotbeen receivedbythedepartmentservicingthedebt.thiscategoryshallincludebadchecks. Applicability:ThispolicyappliestoallcashrelatedactivitiesandtransactionsofWakeCounty.Any exceptionsordeviationsmustbeapprovedbythefinancedirector. PolicyResponsibilityandManagement: EnforcementTheFinanceOfficerhastheauthorityfortheenforcementandmanagementof thispolicy. Review TheFinanceOfficerwillreviewthisprocedureannually.Ifwarranted,thepolicywill beupdatedandsubmittedthroughthereviewandapprovalprocessinforceatthetime.

16 VI. VII. VIII. Communication TheFinanceOfficerhastheresponsibilityfordisseminating,reviewing, modifying,updating,andinterpretingthispolicy. FinanceDirectorat RelatedPolicies,Procedures,andPublications: AccountsReceivableandCollectionsPolicy PettyCashProcedures PaymentCard/CreditCardTransactionsPolicy PaymentCard/CreditCardTransactionsProcedure DisbursementsProcedures GiftCardProcedures InvestmentPolicyandProcedure Appendices: None History: EffectiveDate Version Section(s)Revised Author 10/31/ NewPolicy P&PCommittee 11/20/ SectionDAccountsReceivableandCollection JohnStephenson

17 Cash Collections Procedure X Countywide or Department: Division: Effective Date: Supersedes: Cash Collections Procedure October 31, 2010 Authority: County Manager Originating Department: Finance I. Purpose: The purpose of this procedure is to provide instructions to employees who handle cash on behalf of Wake County. II. Procedure Statement: Cash Collection procedures provide a consistent framework for the collection and depositing of Wake County receipts. Any variations from the procedures outlined below require approval from the Wake County Finance Department. Collection Resources Required Each collection site will be required to have the following resources: Secure safe or other secured storage location approved by Finance Department for storage of cash during and after work hours; Pre-numbered, three-part payment receipt books issued by Finance Department; an approved electronic cash register; or a computer-based receipt system; Change fund(s) number and amount of fund(s) determined by Finance Department; Bank deposit tickets issued by Finance Department; Daily Receipts Reconciliation forms as designed by Finance Department or an approved substitute - (Appendix 1); A Mail Receipts Log, if appropriate (Appendix 2); A Wake County restricted check endorsement stamp; At least two staff to ensure segregation of duties; and Night drop key and disposable bags for after hours deposits, if appropriate. Custodial Responsibilities Supervisors The Supervisor for each collection site is responsible for the location s cash handling operations. This includes the safeguarding of all collections, assigning cash handling duties to employees, ensuring these employees are well-informed of their responsibilities, and providing required documentation to the Finance Department with the current status of change funds for the site. Supervisors must use the Petty Cash/Change Fund Maintenance Form (Appendix 3) when setting up new change funds, closing change funds, or re-assigning existing change funds. The form must be signed by the custodian, approved by his/her Supervisor and Department Head, and sent to the Finance Department for processing. One or more employees should be designated by the supervisor as backup cashier and assigned their own change fund. More than one person may serve as cashier from the same change fund if approved by the Financial Services Director; however this is discouraged because if shortages occur, it would be difficult to determine responsibility. All employees sharing the fund would be held responsible individually and jointly for any shortage. If a shared change fund is approved, the department s compensating controls must be approved by Finance. Cashiers Cashiers who are assigned a change fund have custodial responsibility over those funds. The cashier is responsible for securing and safeguarding collected funds until they are transferred to

18 another cash handler for processing or deposited to a County-approved financial institution. Transfers may be documented on a Deposit Transfer Form (Appendix 4). Other custodial responsibilities include: Only the assigned custodian(s) will have access to the fund. The change fund custodian(s) will be responsible for the maintenance and security of the fund. Change funds should be verified each work day whether in use or not. The fund may be used for making change only. It may not be used for check cashing, loans, petty cash purchases/reimbursements, or any other activity not directly related to receipting County revenue. The fund must be available for a surprise cash count audit, including a review of related documents at all times throughout the year. At the beginning of each shift, the assigned custodian(s) should verify the dollar amount of cash in the fund. The cash should be counted in the presence of another staff member. The Cash Drawer Verification Form (Appendix 5) should be completed and initialed by the individuals making the count. Discrepancies should be reported to the immediate supervisor, manager and the Finance Department revenue accountant. Closing a Change Fund If it is determined that the change fund is no longer needed, the custodian is responsible for verifying the cash on hand. The total cash should equal the total of the change fund. A supervisor should verify these totals and report any discrepancies to the Finance Department revenue accountant. The change fund should be deposited at the bank and recorded in Advantage on a Cash Receipt (CR) document. Contact the Revenue Accountant in Finance for the correct account codes to use on the CR. The Petty Cash/Change Fund Maintenance Form should be completed to indicate the fund is being closed. The Advantage CR number posted to record the deposit of the change fund should be listed on the form. The custodian and supervisor should sign the form and send it to the Revenue Accountant in Finance. Collecting County Funds and Receipting Revenues Receipting Revenues County locations that collect funds must have an established procedure for documenting all receipts (cash, check, money order, debit/credit card, etc). Cash register receipts, computer-generated receipts, debit/credit card settlement receipts or County-issued pre-numbered handwritten receipts are acceptable forms of documentation. Optimally, one employee (cashier) should be responsible for collecting and receipting all payments received. A receipt for each payment must be issued to the customer, client, taxpayer or other payer. At least one cashier must be available to receipt County funds during the posted hours of operation. Receipt Books If using handwritten receipts, departments must obtain County-issued, three-part, prenumbered receipt books from the Finance Department. Other receipt books are not acceptable. The original copy (white) of the receipt should be given to the customer. The second copy (yellow) should be attached to the funds and turned over to the deposit preparer along with the Daily Receipts Reconciliation Form (Appendix 1). The third copy (pink) should remain in the receipt book.

19 Voided receipts should be marked Void with the white and pink copies maintained in the receipt book. The yellow copy should be attached to the receipts reconciliation form and turned in with any other receipts written. Once a receipt book is completed, the used book, with the voids attached, should be sent to Finance for replacement. Finance staff will audit the receipt book, then sign and return it to the department to be kept according to the Wake County Record Retention schedule. Checks received in the mail The Mail Receipts Log (Appendix 2) must be completed by locations that do not have a cash register or computer system to receipt payments. Checks must be restrictively endorsed upon receipt with a County-approved check endorsement stamp by the cashier or individual receipting the check on behalf of the County. Payment card settlement Wake County accepts Visa and MasterCard payments at County-approved locations. Departments who wish to begin accepting debit/credit card payments must contact the Finance Department for approval. Once approved, Finance will complete required forms and order PCI compliant equipment. All employees that handle customer confidential payment/credit card data will be required to sign the Confidentially of Customer Information Form located in the Wake County Payment Card Transactions Procedures. Debit/credit card batches must be settled at least once per day. When a batch is settled, the credit card terminal produces a settlement report or batch close report listing all transactions and the total for the day. Debit/credit card receipts should be compared to the settlement report to ensure accountability of all receipts. Staple all debit/credit card receipts, including any voided debit/credit card receipts, behind the settlement report. The settlement report and receipts should be sent to the Finance Department on a daily basis once the Cash Receipt is recorded in the financial system. Check Acceptance Wake County accepts personal checks, certified checks, cashier s checks and money orders with proper identification. Checks accepted in person must be in accordance with the Wake County Check Acceptance requirements. Checks must be restrictively endorsed upon receipt with a County-approved check endorsement stamp. The Check Acceptance requirements should be posted in an area clearly visible to customers at all payment locations. This posting should also notify customers of the $25 fee assessed by the County on all returned checks. A sample of the Check Acceptance and Returned Check Fee posting is located in Appendix 6. Cashiers are responsible for reviewing each check or money order for completeness and legibly recording driver s license or phone numbers on the face of the check. Check Acceptance Requirements (for checks accepted in person) Check must be made payable to Wake County. Check must be written for exact amount. Check must be pre-printed with the payer s name, address, bank account and routing number. A street address must be provided if a PO Box is printed on check. For all in-state checks, a valid North Carolina driver s license with a photo ID must be presented. If not pre-printed on the check, cashier must legibly record the issuing state and driver s license number and the phone number on the face of the check. If driver s license is not available, a North Carolina identification card or U.S. passport with a photo ID is acceptable. Out of state checks are not acceptable unless accompanied by a valid NC driver s license, a local address and local phone number. Cashier must legibly record the issuing state and driver s license number and the phone number on the face of the check.

20 Forms of payment not accepted Starter checks and counter checks Two party checks (checks made payable to Wake County and another party) Third party checks (checks made payable to an organization other than the one accepting or cashing check example, a paycheck) Post-dated or pre-dated checks Reconciling Cash and Receipts Cash, checks and credit cards must be reconciled daily. Daily reconciliation and balancing should occur out of public view. At the end of each work day or other cut-off period, the following steps should be followed within the department s existing system: Cashiers must use the Daily Receipts Reconciliation form (Appendix 1) or an equivalent to record each type of receipt accepted that day. This will include the total of all cash receipts written, checks from the Mail Receipts Log and credit card batches. All receipts, including voids, must be accounted for daily. All cash, checks and credit card receipts should be removed from the cash drawer. The amount of cash permanently kept in the drawer for making change should then be counted by both the cashier and the supervisor, and then returned to the drawer. The Cash Drawer Verification Form (Appendix 5) should be signed by both the cashier and the supervisor and placed with the cash in the overnight safe. In the morning, as part of opening, the cashier should recount the change fund in the presence of another staff member and the Cash Drawer Verification Form should be signed by both. The remaining cash, checks and charge slips should then be counted, as they represent the total collected for that day. The amount of the deposit should be reconciled back to the total receipts issued to balance the deposit and determine any overage or shortage in the funds being deposited. Overages and shortages must be recorded on the Daily Receipts Reconciliation Form (Appendix 1). The cashier needs to account for any overage, shortage or loss of cash in the cash drawer. See section on Overage/Shortages/Losses in the following section. A supervisor must sign off on all overages and shortages and should contact Finance Department immediately if there appears to be a growing pattern or anything unusual about the overages and shortages. The cashier must co-sign the Daily Receipts Reconciliation Form (Appendix 1) acknowledging the deposit is correct and, if used, sign the Mail Receipts Log (Appendix 2) acknowledging all checks listed are included in the deposit. The amount of cash/checks received must be verified by a second person, preferably a supervisor and that person must sign off on the Daily Receipts Reconciliation Form (Appendix 1) that the cash/check total has been verified. Overages/Shortages/Losses Overages and shortages must be recorded on a separate accounting line of the Cash Receipt (CR) document posted in the financial system. Overages and shortages are recorded using the location s Accounting Template and Revenue Source code M220. Overages are recorded as a positive amount; shortages are recorded as a negative amount. Overages and shortages of $50 or more must be reported to the Wake County Financial Services Director and Internal Audit within two business days. Any consistent patterns or other irregularities should also be reported to Wake County Finance Department when identified. Any loss of funds should be immediately reported via confirmed communication by the location supervisor to Wake County Security and the Wake County Financial Services Director along with a

21 detailed statement as to the circumstances of the loss. If the loss has been reported to the police, a copy of the Police Report must be sent to Finance within 24 hours of receipt of the Police Report. Losses of revenues are not replaced, but must be recorded in the financial system. Loss of change funds are replaced from departmental budgets. Please contact the Finance Revenue Accountant for instructions on recording losses and replacement of change funds. Preparing and Making the Deposit By North Carolina law, all funds collected must be deposited with a County-approved bank each day when collections exceed $250 per location, at least weekly when funds collected are less than $250 and always by the last day of the month in which funds were collected regardless of the amount. The County s preferred bank is Wachovia and departments are encouraged to use Wachovia whenever possible. Locations who demonstrate a need to deposit with a bank other than Wachovia must get approval from the Finance Department. Please contact Revenue Accountant in Finance for a list of approved banks. Deposit Tickets Deposits must be recorded on a bank deposit ticket issued by the Finance Department. Deposit tickets will be three-part tickets with the location name and location code preprinted on the ticket. Please contact the Finance Department when deposit tickets are needed. For reorders, contact the Finance Department when the supply on hand is down to two books. Tickets will be sent to locations though interoffice mail. Deposit Preparation It is the responsibility of assigned staff at each location to accurately count all currency and checks collected and to accurately record the funds collected on a County-issued deposit ticket. The deposit ticket must be dated the day the deposit is taken to the bank. Record cash and currency in the designated spaces on the deposit ticket. Cash must be separated by denomination and presented face up and facing the same direction. Coins should be secured in an envelope with the enclosed amount noted. Contact Finance Department when large amounts of currency and coins are to be deposited. Each check or money order must be restrictively endorsed For Deposit Only - Wake County on the back of the check in the designated space using a County-issued, preinked endorsement stamp. Contact the Finance Department if a pre-inked endorsement stamp is needed. Individual check amounts must be recorded on the deposit ticket or a calculator tape must be made listing each check. The calculator tape must be attached to the checks and sent to the bank with the deposit. Attach the deposit ticket to cash and checks for delivery to bank. Departments may attach all three copies of the deposit ticket to the deposit or may choose to attach only two copies and leave one copy in the deposit book. The bank will validate all copies of the deposit ticket, keep one, and return other copies to the person who made the deposit. If the deposit custodian does not the take the deposit to the bank but transfers the deposit to another deposit custodian for subsequent delivery to the bank, the deposit must be placed in a locked bag or a sealed disposable bank bag. Each time the deposit is transferred to the custody of another person, that person must sign a Deposit Transfer Form (Appendix 4). Each party should keep a copy of the receipt transfer form for 90 days.

22 The validated deposit ticket should be attached to the Daily Receipts Reconciliation form or substitute along with any other back-up documentation. For Wachovia deposits, departments are allowed to use the night deposit drop box at the physical bank location and therefore will not receive a validated deposit ticket. A non-validated ticket may be sent to the Finance Department instead. For all other banks, departments must send a validated deposit ticket to Finance. The deposit must be recorded on a Cash Receipt (CR) document in the financial system at the time of deposit. The CR number must be written on the deposit ticket/back-up documentation and sent to Finance. See Cash Receipts Processing document for CR instructions. Recording the Deposit in the Financial System Supervisors must ensure that deposits are recorded accurately and in a timely manner financial system and that the supporting documentation is sent to Finance daily. in the The deposit must be recorded on a Cash Receipt (CR) document in the financial system at the time of deposit. Overages/Shortages must be recorded on a separate Accounting Line of the Cash Receipt using revenue source code M220. The CR number must be written on the deposit ticket/back-up documentation and sent to Finance the same day the CR is submitted. See Cash Receipts Processing document for CR instructions. Returned Check-Non-Sufficient Funds (NSF) Procedures A fee of $25 is assessed by Wake County on all returned checks. Wake County does not re-deposit checks that are returned by the bank due to non-sufficient funds. Returned checks are posted in the financial system as a debit (reduction) to departmental revenue budgets and are coded to revenue code C528 NSF Check Charge-backs. When payment has been received for NSF checks, they are posted as a credit to the same revenue code. Department notification A designated contact in each County department will be notified by Finance via of all returned checks for their department. The will contain customer name, check number, check amount and date of the check. Departments should not accept another check from the same customer until the returned check and fees have been paid in full. Once the check has been paid, another will be sent by Finance informing the contact person that the check has been made good. Payment of NSF Checks Departments must not accept payment for returned checks at their locations. The payer must be instructed to call the Finance Office for instructions on how and where to make payment. After a first collection attempt by the Finance Department, uncollected checks are turned over to the District Attorney s Worthless Check Program. If a department accepts payment for an NSF check that has already been turned over to the District Attorney s office, the department will be charged for fees incurred by that program. Collection of NSF Checks Finance sends an initial collection letter to customers. If the customer does not make payment of the returned check plus the $25 fee to the Finance Department within 15 days, the check is turned over to the Wake County Worthless Check Program in the District Attorney s office. The Worthless Check Program assesses additional fees and sends a second collection letter. At this point, payment must be made to the District Attorney s office. Once this process has begun, Wake County can no longer accept payment. If the payer doesn t respond within the allotted time frame, a warrant may be issued for his/her arrest.

23 III. Definitions: Cash Includes currency, coins, personal checks, money orders, cashier s checks and credit card transactions. Cash handler An individual, who frequently handles cash, processes payments and prepares deposits to a main cashiering station. This person may operate cash handling equipment, e.g. a cash register or process payments manually. Confirmed Communication Speaking with a Finance Department staff member to ensure proper notification has occurred. Custodial Responsibility A cash handler who has received County funds is liable for those funds until the funds are deposited with a County bank or signed over to another cash handler for processing. Cut-off period A time of day that the work cycle of a cashier is closed to allow preparation of the deposit. A Loss of funds is when a cashier has obtained physical custody of money and then, due to reasons of negligence (such as leaving the drawer unattended), an act of God, a fire, or an unlawful action (such as a robbery), cannot deposit that money into the Bank. Overage/Shortage - An unintentional collection error such as a change making error. Payer The person or organization who is responsible for paying the amount stated on the face of a negotiable instrument. IV. Applicability: This procedure applies to all Wake County departments that collect cash on behalf of Wake County. V. Procedure Responsibility and Management: Enforcement - The Finance Director has the delegated authority for the enforcement and management of this procedure. Review - The Revenue Accountant will review this procedure annually. If warranted, the procedure will be updated and submitted through the review and approval process in force at that time. Communication - Finance department has the responsibility for disseminating, reviewing, modifying, updating, and interpreting this procedure. Within the department, the responsibility is delegated to the Revenue Accountant. Revenue Accountant (919) VI. VII. Related Policies, Procedures, and Publications: Wake County Cash Management Policy Wake County Payment Card Transactions Policy Wake County Payment Card Procedures Cash Receipts Processing Document e-wake 500 Appendices: The following forms are attached at the end of this Cash Collection document. Appendix 1 Daily Receipts Reconciliation Form & Instructions Appendix 2 Mail Receipts Log & Instructions Appendix 3 Petty Cash/Change Fund Maintenance Form Appendix 4 Deposit Transfer Form Appendix 5 Cash Drawer Verification Form Appendix 6 Check Acceptance Procedures VIII. History: Effective Date Version Section(s) Revised Author Entire procedure resubmitted for approval Karen Thiessen Policy & Procedures Clarifying language added Committee

24 Cash Collections - Attachment F WAKE COUNTY CHECK ACCEPTANCE POLICY Check must be made payable to Wake County. Check must be written for exact amount. Check must be pre-printed with the payer s name, address, bank account and routing number. A street address must be provided if a PO Box is printed on check. A valid North Carolina driver s license with a photo ID must be presented. If driver s license is not available, a North Carolina identification card or U.S. passport with a photo ID is acceptable. Out of state checks are not accepted unless accompanied by NC driver s license, local address and local phone number. Not accepted Starter checks and counter checks Two party checks (checks made payable to Wake County and another party) Third party checks (checks made payable to an organization other than the one accepting or cashing check example, a paycheck) Post-dated or pre-dated checks Wake County reserves the right to refuse acceptance of any check whenever intent, validity, authenticity and/or availability of funds are in question. A FEE OF $25 WILL BE CHARGED BY WAKE COUNTY FOR ALL RETURNED CHECKS. RETURNED CHECKS NOT PAID IN FULL TO WAKE COUNTY BY THE DUE DATE WILL BE TURNED OVER TO THE WAKE COUNTY DISTRICT ATTORNEY S WORTHLESS CHECK PROGRAM. ADDITIONAL FEES WILL BE ASSESSED.

25 Wake County Daily Receipts Reconciliation Form (Sample) CR# DATE DEPARTMENT & LOCATION AMOUNT OF RECEIPTS TO ACCOUNT FOR Enter beginning and ending receipt numbers: to Number of Receipts to Account For: ALL RECEIPT NUMBERS MUST BE ACCOUNTED FOR BELOW: Type of Receipt Total # of Receipts Total $ Amount of Receipts Cash $ Checks /Money Orders $ Voided Receipts 0 Subtotal - from receipts book $ Mail Receipt Log $ Credit Cards $ Total Receipts $ Prepared By Date Attach adding machine tape to back of this form that adds the amounts from the receipt book. AMOUNT OF RECEIPTS TO DEPOSIT TOTAL Total Cash/Coin Counted $ Total Checks Added Per Calculator Tape $ Total Cash/Check Deposit $ Total Credit Card Deposit $ TOTAL DAILY DEPOSIT $ Total Receipts less Total Daily Deposit (Circle one) Over or Short $ Prepared By Reviewed By Date Date

26 Daily Receipts Reconciliation Form (Instructions) Preparer - FILL OUT TOP OF FORM 1 A separate "DAILY RECEIPTS RECONCILIATION FORM" should be prepared each day that total receipts exceed $250 or weekly at a minimum. Each person with a receipt book should complete the top portion of the form The "DAILY RECEIPTS RECONCILIATION" should be dated as of the date the receipts are received or the day the $250 minimum is reached. Indicate the Department and location in the upper right corner. Enter the beginning and ending receipt numbers for the day in the boxes indicated. Accounting for the number of receipts. Indicate the number of receipts issued and the total amount collected for each type of receipt. See below for information to enter for each type of receipt. Type of Payment Received Cash Check/Money Order Voids Mail Receipt Log Credit Cards Total Number of Receipts Isssued Number of receipts issued for cash collections Number of receipts issued for check/money orders Number of voided receipts Total number of checks recorded on Mail Receipt Log Number of credit card transactions as shown on the credit card batch settlement report Total Dollar Amount Total dollar amount of all cash receipts issued Total dollar amount of all check/money order receipts issued Zero Total amount recorded on Mail Receipt Log. Total of credit card batch as shown on credit card batch settlement report. VOIDED RECEIPTS - Write VOID on all copies of voided receipts. The yellow copy of the voided receipt must be attached to the Daily Receipts Reconciliation Form. The white and pink copies of the voided receipt should remain in the receipt book The person completing the mail receipt log will run an adding machine tape of the checks for the mail receipt log and attach it to the log. The number of receipts for the mail receipt log will be the number of checks indicated on the mail receipt log. See specific instructions for the Mail Receipt Log. Accounting for the amount of collections. Run an adding machine tape of the checks and money orders subtotal this figure. Then add the total amount from the mail receipt log and the cash/currency to obtain the total amount of receipts. Total both columns on the form, sign and date DAILY RECEIPTS RECONCILIATION as preparer. The number of credit card transactions should be indicated on the # receipt line and the amount of receipts associated with credit card transactions. Submit copy of individual receipts and settlement report. Total both columns on the form, sign and date DAILY RECEIPTS RECONCILIATION as preparer. Supervisor (or reviewed by) - FILL OUT BOTTOM OF FORM 10 Review all receipts on the top part of the form completeness. Ensure all handwritten receipts are accounted for. Ensure checks recorded on Mail Receipts log match calculator tape attached. Ensure all credit card receipts are accounted for on the batch settlement report Count the currency/coin to make sure it agrees to cash indicated on the deposit slip. Add checks on calculator. Add total currency/coin and checks for total deposit to be made. Ensure that the Credit Card Settlement report is included with the reconciliation. Sign and date "DAILY RECEIPTS RECONCILIATION" indicating approval. Send to Finance with the Daily Mail Receipts log, other supporting documentation and the validated bank deposit ticket.

27 Wake County Cash Drawer Verification Form (Sample) Month Year Change Fund Custodian Date Beginning Cash Counted By: Verified By: Ending Cash Counted By: Verified By:

28 OFFICE OF INTERNAL AUDIT 301 S. McDowell Street Suite 2900 P.O. Box 550 Raleigh, NC Phone (919) MEMORANDUM To: Jim Hartmann, County Manager From: John T. Stephenson, Internal Audit Director CC: Johnna Rogers, Deputy County Manager and Scott Warren, County Attorney Date: July 7, 2017 Re: Cash Receipts Review Summary Internal Audit performed cash receipts reviews throughout the County as indicated below. The plan is to review each revenue-collecting organizational unit over time within the County. Except for the Register of Deeds Office, the completed reviews did not indicate any unaccounted for transactions. Date Completed Organizational Unit Key Recommendations Dec 2014 Community Services Should reconcile permits issued with fees collected. Consider scanning paperwork in satellite offices and ing to main office to improve timeliness of entry into Advantage. Dec 2014 Environmental Services Should reconcile permits issued with fees collected. Jan 2015 Geographic Information Services Reconcile cash receipts daily instead of monthly. Have second person verify amount of cash and checks recorded on cash report. Cumulative receipts less than $250 should be deposited at least weekly.

29 Date Completed Organizational Unit Key Recommendations Aug 2015 Board of Elections Only prepare one reconciliation per day so that total deposit will match a single reconciliation form. Redesign receipts reconciliation form to accommodate multiple receipt number series. Consider using the County Revenue Collection System, which will generate automated receipts in place of the current manual system. Sep 2015 Southern Regional Center Improve legibility of all parts of the deposit slip (information written on the top part sometimes does not show up on back parts). Feb 2016 Libraries Have second person verify amount of cash and checks recorded on cash report. Count cash in drawer at the beginning of every day in the presence of another staff member, with both parties signing off on count. Revise schedule of deposits at some branches to ensure collections in excess of $250 are deposited timely. Cash registers should identify staff member entering a transaction. The validated deposit ticket should be attached to the cash report in accordance with County policy. Mar 2016 Animal Center The preparer and the reviewer should sign off on the daily receipts reconciliation form. Sep 2016 Parks In all instances, a second person should verify amount of cash and checks recorded on cash report and sign off on the form. Count cash in drawer at the beginning of every day in the presence of another staff member, with both parties signing off on count. Jan 2017 Sheriff s Office Revise schedule of deposits at the firing range to ensure cumulative collections in excess of $250 are deposited timely. Page 2 of 3

30 Date Completed Organizational Unit Key Recommendations Current (internal control recommendations communicated in Feb 2017) Register of Deeds There are unexplained differences between amounts charged and amounts deposited. Cumulative amount is extremely significant. Staff should not share cash drawers, change funds should not be left in drawers overnight, change funds should be verified each morning with a second person signing off on the count. Receipts for each drawer should be reconciled to system reports of amounts charged each day. Differences should be investigated and explained. Responsibilities for preparing the deposit, reconciling the deposit to system reports, and preparing journal entries should be assigned to different people. Authority to approve voided transactions should be limited to supervisors, various approvals and verifications should be documented, and an overall review for unusual transactions should be implemented. Page 3 of 3

31

32

33

34

35

36

37

38 DRAFT SUBJECT TO CHANGE MEMORANDUM OF UNDERSTANDING BETWEEN THE WAKE COUNTY REGISTER OF DEEDS AND THE COUNTY OF WAKE WHEREAS, the County of Wake (hereinafter the County ) is a body politic and corporate; and WHEREAS, the Wake County Register of Deeds is an elected County official; and WHEREAS, the Wake County Register of Deeds has statutory authority per Chapter 161 of the North Carolina General Statutes to collect and deposit fees collected into the County s General Fund; and WHEREAS, the Wake County Board of Commissioners has appointed a Finance Director to fulfill the duties of the finance officer through Chapter 159 of the North Carolina General Statutes (also known as the Local Government Budget and Fiscal Control Act); and WHEREAS, the Wake County Register of Deeds office operates as if it were a department of the County with financial transactions managed and reported within the accounting system of the County; and WHEREAS, the County s financial policies and procedures apply only to employees of Wake County government, its agencies, and departments and not to the offices of elected County officials and their staffs; and WHEREAS, the Wake County Board of Commissioners through the appointed Finance Director may provide financial administration services to the offices of elected County officials and their staffs upon written agreement with Wake County, except where such agreement conflicts with other applicable law. THEREFORE, the County of Wake and the Wake County Register of Deeds mutually agree as follows: Section 1. The County of Wake will, by and through its Finance Department, keep the financial accounts and transactions, including disbursement of all funds and receipt and deposit of all moneys accruing to the Register of Deeds in accordance with the Local Government Finance Act. Section 2. The Wake County Register of Deeds agrees to comply with the County of Wake financial policies and procedures in the same manner as other County departments that report to the County Manager or a designee. Section 3. The Wake County Manager or a designee shall have the right to audit, inspect, examine, and make copies of any and all books, accounts, invoices, records, and other writings related to the accounts of the Register of Deeds. Section 4. This Memorandum of Understanding will be effective when signed by both parties involved. It will continue in force from year to year until modified or terminated by written mutual agreement of the parties hereto, or upon ninety (90) days written notice by either party.

39 This Memorandum of Understanding supersedes and replaces all prior Memorandums of Understanding involving this subject matter between the County and the Register of Deeds. COUNTY OF WAKE, NORTH CAROLINA BY: Sig Hutchinson, Chairman Wake County Board of Commissioners The signing of this Memorandum of Understanding was authorized by the Wake County Board of Commissioners at a meeting held on July 21, 2017 Clerk, Wake County Board of Commissioners DATE:, 2008 WAKE COUNTY REGISTER OF DEEDS BY: Charles Gilliam, Registrar DATE:, Wake County Memorandum of Understanding_ROD_05/04/17

40 I. Purpose: Wake County Fraud, Waste and Abuse Awareness Policy X Countywide Department: Division: Supersedes: Effective Date: 8/1/2017 Authority: Wake County Finance Director Originating Department: Finance All employees, elected and appointed officials have the responsibility to be aware of the potential for fraud, waste and abuse and to report any suspicion of fraud, waste or abuse. County leadership has responsibility for the prevention and detection of fraud, waste and abuse by establishing and maintaining effective internal controls that protect County assets from loss, theft, and misuse. It is important that County leadership and employees understand what such activity is and know how to report suspected fraudulent activity. II. Policy Statement: County leadership is responsible for creating a tone at the top that is above reproach and maintaining an environment where employees who report suspected fraud, waste and abuse are free of retribution. Definitions of Fraud, Waste and Abuse: Fraud is a deliberate deception to secure an unfair or unlawful gain or deprive another of a legal right. Fraud is an intentional, false representation that injures another person. Waste is over-utilization of goods or services or unnecessary costs resulting from inefficient practices, systems or controls. Abuse refers to the violation and disregard for county policies which impair the effective and efficient execution of operations. Abuse may directly or indirectly cause financial loss. Examples of fraud might be: Misuse of funds, supplies, or other assets; Improper handling or reporting of cash collected; Authorization of public benefits for family members who are ineligible; Disclosing confidential and proprietary information to outside parties; or Accepting or seeking anything of material value from contractors, vendors, or persons providing services/materials to the County. Examples of waste might be: Destruction, removal, or inappropriate use of records, furniture, or equipment; Improper maintenance or intentional mistreatment of equipment; Purchase of unneeded supplies or equipment; or Purchase of goods at inflated prices. Page 1 of 4

41 Examples of abuse might be: Unauthorized use of County equipment or supplies for non-county purposes, including but not limited to, computers, vehicles, software, or databases; Use of non-personal information on citizens to obtain new customers for an outside business; or Profiting by self or others as a result of inside knowledge. Training Requirements: All employees covered by this policy are mandated to attend fraud, waste and abuse awareness training during their initial hiring orientation, upon promotion to a manager/supervisory position, and every two years as part of an ongoing fraud awareness education program. Training will address the responsibility managers and supervisors have to prevent and detect fraud, waste, and abuse because of their position with the County. During training, participants should receive high level information to help them recognize the common warning signs and indicators of fraud and understand how to report their concerns to appropriate County staff. All training should include the consequences of committing fraud, which may include discipline up to and including dismissal and possible prosecution as allowed under state and federal law. Reporting Responsibilities: Any person (complainant) suspecting fraud, waste or abuse should immediately report their suspicions to their supervisor, manager, or department head. If they prefer to report concerns outside their chain of command, they may report to the Internal Audit Director who will review the information provided and coordinate any initial investigations needed. Regardless of the manner in which the complainant chooses to report concerns and whether they remain anonymous or not, they should be able to report without fear of retribution. Failure to report known fraud, waste, or abuse is to be complicit in it and may leave the employee subject to discipline, up to and including dismissal. Instructions and procedures for reporting suspected fraud, waste, and abuse can be found in Attachment A of this policy. Complainants should not contact the suspected individual, make any effort to determine facts, or demand restitution. They should also refrain from discussing the case or any allegations unless asked to do so by the Internal Audit Director. The Internal Audit Director and staff involved in an active investigation will have free, unrestricted access to all County data, records and premises. Strict confidentiality will be maintained among the complainant, Internal Audit staff, and management throughout the investigation to avoid raising undue accusations or alerting individuals to an ongoing investigation. Inquiries concerning an investigation from the suspected individual, his or her attorney or representative, or any other inquirer should be directed to the County Attorney or the Internal Audit Director. Page 2 of 4

42 Staff is cautioned to use care when reporting fraud, waste, and abuse. An employee who engages carelessly or recklessly in the erroneous reporting of fraud, waste, or abuse may be subject to discipline, up to and including dismissal. Human Resources Responsibilities: Irregularities concerning an employee s moral, ethical, or behavioral conduct should be resolved within the department and by Human Resources, not by the Internal Audit Director. If there is any question as to whether an action constitutes fraud, waste, or abuse, contact the Internal Audit Director for guidance. If an investigation results in a recommendation to terminate and/or prosecute an employee, the recommendation will be reviewed for approval by the designated representatives from Human Resources, the County Attorney s Office, the Wake County District Attorney, and, if necessary, by outside counsel, before any such action is taken. The decision to terminate an employee will be made by the department head in conjunction with Internal Audit, Human Resources, the County Attorney s Office, and the County Manager. Other Departmental Responsibilities: Pinpointing the exact system breakdowns that allowed fraud, waste, or abuse to occur is difficult. However, learning from past incidents is necessary to better prevent and deter recurrences in the future. Consequently, departments may be required to work with Internal Audit staff and/or Finance staff to modify existing business processes or systems to reduce or mitigate internal control weaknesses. III. Definitions: Complainant - the party (individual or group of persons) who makes the complaint in a report to internal audit via the third-party provider. County Leadership Department and Division Heads, Managers, Supervisors, and other members of County s Executive Team. Internal Controls Measures, such as reviews, checks and balances, and procedures that are in place to help the County conduct business in an orderly and efficient manner; protect its assets and resources; deter and detect errors, fraud, and theft; ensure accuracy and completeness of its accounting data; produce reliable and timely financial and management information; and ensure adherence to its policies and plans. IV. Applicability: This policy applies to any irregularity, or suspected irregularity, involving all employees as well as vendors, contractors, outside agencies, and/or any other parties with a business relationship with the County. Investigative activities required will be conducted without regard to the suspected offender s length of service, position, title, or relationship to the County. Page 3 of 4

43 V. Policy Responsibility and Management: The Internal Audit Director is responsible for the administration, revision, interpretation, and application of this policy. The policy will be reviewed annually and revised as needed. The Internal Audit Director will communicate any changes to the Fraud, Waste, and Abuse Awareness Policy to department heads, managers, and supervisors. For questions related to this policy, contact the Internal Audit Director at VI. Related Policies, Procedures, and Publications: Human Resources Ethics Policy VII. VIII. Appendices: History: Effective Date Version Section(s) Revised Author Susan McCullen and John 8/1/ New Policy Stephenson Page 4 of 4

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

Report on Cash-Handling

Report on Cash-Handling Policies and Procedures September 18, 2017 Presentation Overview Purpose of Report Overview of County Cash Collections County Management Actions Regarding: Register of Deeds (ROD)

Report on Cash-Handling Policies and Procedures September 18, 2017 Presentation Overview Purpose of Report Overview of County Cash Collections County Management Actions Regarding: Register of Deeds (ROD)

THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY

Number THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY Division Accounting & Financial Reporting Date April 18, 2012 Purpose To reduce the risk of theft, loss or misplacement of cash and checks

Number THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY Division Accounting & Financial Reporting Date April 18, 2012 Purpose To reduce the risk of theft, loss or misplacement of cash and checks

PAYMENT CARD INDUSTRY

DATA SECURITY POLICY Page 1 of 1 I. PURPOSE To provide guidelines and procedures to ensure that all money paid to the College in the form of cash, checks or payment cards is properly receipted, accounted

DATA SECURITY POLICY Page 1 of 1 I. PURPOSE To provide guidelines and procedures to ensure that all money paid to the College in the form of cash, checks or payment cards is properly receipted, accounted

CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES

GUIDELINES AND PROCEDURES") FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

CASH HANDLING PROCEDURES