CR-370 CASH RECEIPTS

|

|

|

- Dayna Hampton

- 6 years ago

- Views:

Transcription

1 CR-370 CASH RECEIPTS UNIT DEPOSITING PROCEDURES GENERAL INTERNAL POLICIES RELATING TO THE CASHIER TIMELY DEPOSITS PREPARING THE BANK DEPOSIT CASHIER S CHANGE FUND POLICY AND PROCEDURES SECURITY OF VAULT AREA & SAFES COMBINATION/KEY(S) FOR SAFE CHECK ACCEPTANCE PROCEDURES RETURNED CHECK PROCESSING COUNTERFEIT CURRENCY SEPARATION OF RESPONSIBILITIES RECORDING TO THE GENERAL LEDGER GIFT PROCESSING & ANNUAL FUND DEPOSITS APPENDICES 370-A Deposit Log 370-B Deposit Transmittal 370-C Cashier s Daily Vault Cash Count Form 370-D Deposit Slip 370-E Cash Receipt 370-F Courier Log 370-G Coin Order Form 370-H Change Order Form 1

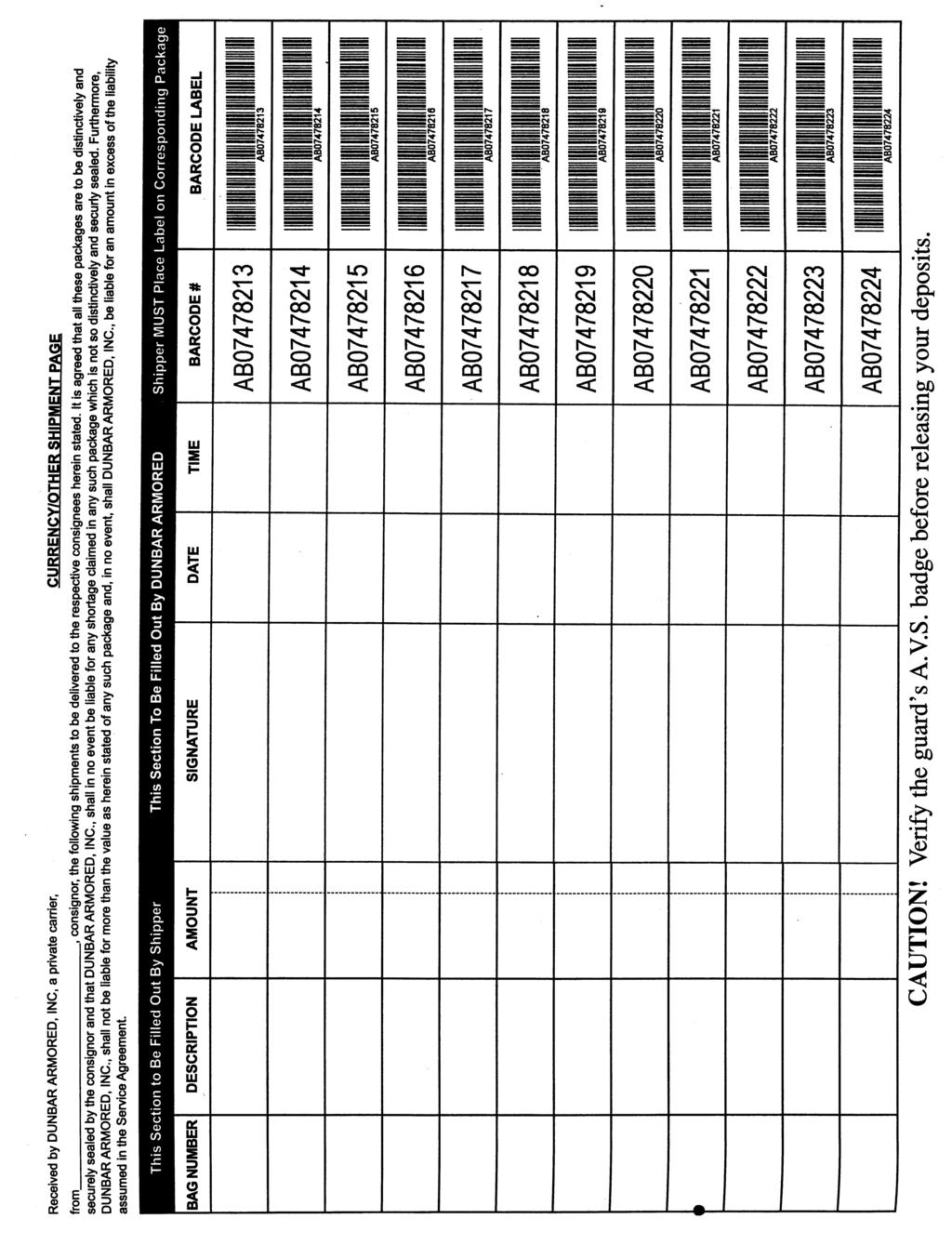

2 370.1 UNIT DEPOSITING PROCEDURES A. Policy The Foundation CFO has the responsibility for reviewing the procedures for proper accountability of cash receipts. A variation from established procedures requires the prior approval of the CFO. All units must document the deposit of cash and negotiables by obtaining a receipt or copy of the Deposit Slip (Appendix 370-D) that indicates the date, amount and initials of the person making the deposit. Enterprise deposits brought to the vault by the units themselves are to be documented in the cashier s Deposit Log (Appendix 370-A) by both the depositor and the cashier. Deposits delivered by 3rd party vendor (i.e. Dunbar) are documented by the copy of the Courier Log (Appendix 370-F). The Bookstore deposits are picked up by the 3 rd party vendor and taken directly to the bank. The Bookstore follows all other procedures covered in this document. B. Procedures for Depositing Counted Monies Counted deposits are those that have been counted by the depositing unit prior to being turned in to the Foundation Cashier. These are normally receipts from cash register sales and consist of cash, checks, and credit cards. Enterprise operations deposit the counted drawer drops. These deposits will be made in the following manner: 1. The deposit is compiled as follows: a. It should be verified that the Deposit Transmittals (Appendix 370-B) have been signed, the date of sales, project name and number, and amount. b. The cash bag must be sealed when received from the units by the vault cashier. 2. The money is deposited as follows: a. 3rd party vendor picks up cash bags from various unit locations and transports them to the Foundation. b. The deposits transported to the vault by 3rd party vendor are documented by the Courier Log (Appendix 370-F). Each unit has their own record book. Deposits brought down individually will be entered into the logbook and signed by the cashier and depositor. c. Deposits are counted. Any corrections to the deposit transmittal should be noted, with an additional explanation made in the Accounting Use Only block on the transmittal. 2

3 d. Foundation Accounting will notify the depositing unit of the actual deposit amount by cash receipt. 3. The Unit s deposit bags are opened and counted as follows: a. The cash is sorted by denomination. b. The currency and coin are counted by the cashier and supervisor or appointed administrative employee and listed on the Deposit Transmittal by denomination. c. The deposit is totaled on the Deposit Transmittal and submitted with the deposit in a sealed bag to the Foundation by a 3 rd party vendor. d. The Bookstore deposits are transported directly to the bank by the 3 rd party vendor. 4. The over or short amounts are determined as follows: a. The cashier opens the bags and counts the monies. The cashiers counts are compared to the Deposit Transmittal. b. In cases where the vault cashier discovers a discrepancy of $25.00 or more the vault cashier will immediately notify the department s unit manager of the discrepancy. c. In cases where the Bookstore s accounting technician discovers a discrepancy and if the variance is $25.00 or more, the discrepancy should be researched and the Bookstore Director and the Director of Enterprise Accounting should be notified. The reason for the variance should be noted on the bookstore s deposit report. d. Any variances in cash of $50.00 or more must be reported immediately to one of the following: Executive Director or Chief Financial Officer. e. In compliance with Executive Order No. 813 any actual or suspected theft, defalcation, fraud or irregularities, must be reported by the next business day to the following: Executive Director or Chief Financial Officer GENERAL INTERNAL POLICIES RELATING TO THE CASHIER The Cashier s vault change fund will be counted daily before the Cashier leaves at the end of the day, and verified by the Director of Enterprise Accounting or their designee. The count and verification are documented on the Cashier s Daily Vault Cash Count Form (Appendix 370-C). 3

4 Monies received will be deposited within one working day after receipt by the Cashier TIMELY DEPOSITS The Foundation Vault Cashier may receive deposits in several different ways depending on the type of unit operation. In each case, however, accountability and documentation must be maintained. The appropriate method in which deposits are received and the corresponding Cashier procedures are as follows: A. 3 rd party vendor delivers directly from Enterprise Units. 1. A completed Deposit Transmittal form must be with the deposits. B. Cashier receives deposit from a non-enterprise unit: 1. The depositor presents the deposit slip and funds to the vault cashier. (Appendix 370-D) 2. The cashier verifies the funds and gives or s the depositor a cash receipt. (Appendix 370-E) C. All departments collecting monies on behalf of the Foundation must deposit the funds in a timely manner, as follows: 1. Units receiving more than $ per day in cash, check or credit card receipts are required to bring their deposits to the Foundation cashier, the next business day or picked up per 3 rd party vendor s transport schedule. 2. Units receiving less than $ per day in cash, check or credit card receipt are required to bring their deposits when they accumulate $500.00, or weekly, whichever comes first, to the Foundation Cashier. 3. Units are required to deposit all cash, checks and credit card receipt at least weekly, regardless of the amount collected. 4. If the staff fails to meet any of the above criteria, the Foundation General Accountant will notify the unit s manager/staff via with a CC: to the Director of Enterprise Accounting and Unit Director. If the delay in depositing funds continues, the Unit Director will be notified, with a CC: to the Chief Financial Officer, Executive Director, Director of Enterprise Accounting and Dean (Vice President for Academic Affairs or Administrative Affairs if applicable). If the delay in depositing funds still continues, a meeting will be held with the Unit Director(s), Chief Financial Officer, Director of Enterprise Accounting, and Dean (Vice President for Academic Affairs or Administrative Affairs if applicable) to discuss and resolve the issue. 4

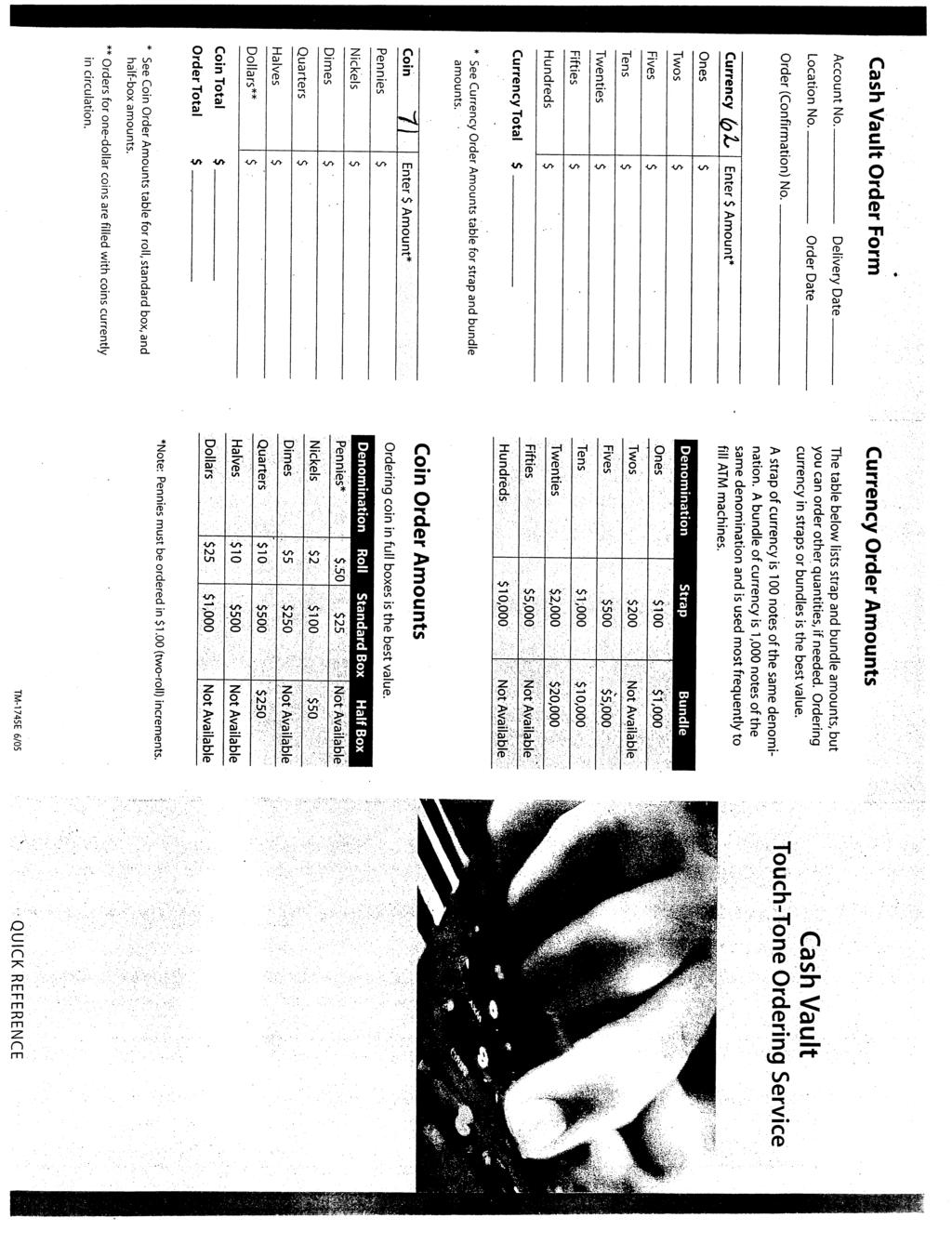

5 5. Under no circumstances are deposits to be forwarded to the Foundation Vault Cashier s Office through Campus mail PREPARING THE BANK DEPOSIT A. Campus Center and Bronco Student Center respectively have several bags per unit, which make one deposit each. Other unit s deposits, i.e. Kellogg West, Los Olivos, etc., are treated as individual deposits. The total of each unit s deposits are entered on the daily cash log. B. One set of bank deposit forms is completed for all cash deposits. The Foundation s yellow copy is given to the Accounting Specialist. For checks, an adding machine tape should be run and the total should be entered as the control total in the Desktop Deposit system. Checks are scanned through the system and a deposit confirmation sheet is printed and the total should match the adding machine tape. An adding machine tape of the cash by denomination should be added to the total deposit. The white and pink copies are placed with the deposit money in the deposits bag. The tape of checks and a Deposit Confirmation sheet, and the scanned checks are placed in a separate bag and kept in the safe for 6 months before being destroyed. Loose coin should be put into a coin envelope or small sealed bag. C. The bank deposit bag is sealed. The amount on the bag is usually equal to the total for the cash log, the exception is a deposit that is picked up and transported directly to the bank following a special event. D. This total should then be listed f or the 3 rd party vendor pick up. E. When the 3 rd party vendor arrives for the daily deposits he signs the log designating the total amount of the day s deposits CASHIER S CHANGE FUND POLICY AND PROCEDURES The Cashier s Change Fund is used for providing all necessary cash for authorized register change funds, purchase of coin and necessary cashing of checks. A specific amount is authorized and documented and the Change Fund must always balance to $18,000 in the safe. It is not to be used for any expenditure other than reimbursing other register funds and change. This Change Fund is the only authorized means of providing coin and currency from the cash room without the specific approval of the Director of Enterprise Accounting. It is the Cashier s responsibility to account for all transactions through this fund and maintain the appropriate mix of coin and currency for normal operations. When requesting currency from the bank the coin order limit is $10,000. A. Procedure to Order Currency and Coin 1. The Change Fund is inspected daily for checks and any overabundance of certain denominations of coin and currency. The Cashier completes a coin order form (370-G) to order the required denominations of coin and currency. 5

6 One copy of the Coin Order form is attached to the cashiers daily vault cash count for reconciling the change fund. (Appendix 370-C) 2. The completed Coin Order form is given to the Financial Analyst who will call in the order to the bank by the 10:30 a.m. deadline. B. Receiving Change Order from the Armored Vehicle Courier 1. It must be verified that the correct amount is received immediately while the courier is still in the cash room. C. Preparing Register Banks from Change Fund for Enterprise Units 1. The changing of the register bank amount is documented by writing down on the Deposit Transmittal the exact amount (by denomination) going to the Cashier. This amount is for buying back coin and small currency to begin the new register. It is a change fund revolving amount, not part of the deposit. Banks will be made up according to each individual register s specifications. Most units keep their register banks on site in a secured safe. 2. A Change Order form (Appendix 370-H) is completed showing the exact denominations going From Cashier and indicating to whom it goes. The person picking up the register banks must sign the Sign out Log. 3. The Change Order form is placed in the Change Fund as a Cash Out document for later reconciliation. D. Making Change 1. Both sides of a Change Order form are completed, i.e., what monies were given out and what was taken in. 2. The Change Order form is placed with the Change Fund for later reconciliation. E. Personal and Petty Cash Check Cashing Procedure 1. Personal checks of not more than $50.00 will be cashed for currently employed, central office, full-time Foundation employees working in Building #55 by the vault cashier during regular business hours. 2. Foundation issued petty cash reimbursement checks will be cashed by the vault cashier during regular business hours. F. Daily Reconciliation of Vault At the close of business every day, Change Fund monies are counted by the vault cashier and verified by the Director of Enterprise Accounting or his/her designee. 6

7 Using the Cashier s Daily Cash Count form, the total of cash should equal the Proof total at the bottom of the form: yesterday s cash, plus the coin order received from the bank (Cash In), less cash deposited to pay for today s cash/coin order (Cash Out) SECURITY OF VAULT ROOM & SAFES A. At the close of each business day, the cash vault, Cashier s window, cash room door and all safes must be secured. B. The Director of Enterprise Accounting must be notified if the vault and or safes are left open for any reason. C. All keys and combinations must be continuously safeguarded. D. Only authorized persons are allowed into the vault room. The authorized persons are maintained on a vault room/safe access list which is kept on the inside door of the vault room. This list shows who has access to the vault room and who has access to the safe combinations. E. The alarm system must be functioning. The red light on the movement sensor should go on when a person passes in front of the beam. The silent alarm button and fire extinguisher should be kept unobstructed at all times COMBINATION/KEY(S) FOR SAFE A. When an individual having knowledge of the combination/key(s) leaves or no longer requires the combination/key(s) in the performance of his or her duties the combination/key(s) must be changed and a record of the vendor used and date last changed must be kept on the list of who has access to the vault room or safe, see list discussed under 370.6D. B. An accurate record must be maintained by the Authorized Signor/Unit Director, or their designee of when the vault/safe combination and/or key(s) were last changed CHECK ACCEPTANCE PROCEDURES This section relates to checks presented in payment for goods or services or as a donation to the Foundation. ACCEPTING CHECKS: Subject to limitations or exceptions stated below, checks are accepted by the Foundation in exchange for goods or services provided. 7

8 A. CONDITIONS FOR ACCEPTANCE: To be accepted, each check presented must: 1. Be payable to the Cal Poly Pomona Foundation Inc. except for a check payable to unit with a DBA (Doing Business As) name. 2. Be recently dated - no postdated or stale dated (i.e., dating no earlier than 30 days prior to the day of acceptance), if so the checks will be brought to the attention of the Authorized Signer/Unit Director via by the Foundation cashier, see section for further details. 3. Be properly signed or endorsed for deposit only by the presenter. 4. Be in agreement as to numeric and written amounts. 5. Be legibly written in ink or typed. 6. Have Federal Reserve routing codes printed as part of the MICR encoding at the bottom of the check. 7. Not be altered or grossly mutilated. 8. Not have any unreasonable restrictions placed on the face which excessively limit its application. 9. Contain sufficient information to permit tracing the presenter (e.g. address, telephone number, etc.). 10. Checks and Cash Equivalents bearing the legend Payable/Paid in Full are not to be accepted. B. VERIFYING PRESENTER IDENTIFICATION: IDENTIFICATION REQUIRED -Some form of identification, preferably one having a picture, must be checked to verify the identification of each presenter of a check. NOTE - The Cashier verifying the identification must initial the check. C. RESTRICTIVE ENDORSEMENT AND OTHER INFORMATION REQUIRED: ON ALL CHECKS ACCEPTED -before deposited with the Foundation cashier. All checks must be restrictively endorsed immediately or by the close of each business day. Endorsed check(s) held overnight must be located in a safe or vault in a secure location until deposited with the Foundation. If the total deposit is $500 or more the funds must be deposited in the Foundation the next business day or picked up per 3 rd party vendor s transport schedule. If the total deposit is less than $500 the funds must be deposited in the Foundation within a week or sent with the next 3 rd Party Vendor s scheduled pick-up.. 8

9 D. DISCREPANCY BETWEEN NUMERIC AND WRITTEN AMOUNTS: When the numeric and written amounts on a check do not agree, a new check should be requested. If a corrected check cannot be obtained, the check should clear based on the written amount. The written amount is entered above the numeric amount and circled RETURNED CHECK PROCESSING A. Checks may be returned unpaid by the banking system for a number of reasons; the primary causes of returns are non-sufficient funds, account closed and stop payment. Returned checks must be controlled during the process of attempting to collect on the returned amount. B. When the Financial System Department receives a notice of returned check from the bank, it is forwarded to the Accounts Receivable Specialist in the Accounting Department. The Accounts Receivable Specialist will send all returned checks to the Authorized Signer/Unit Director. The unit director has the responsibility of following up with the maker of the check or requesting the maker be sent to collections. C. NSF checks greater than one year old will be written off with the prior approval of the Chief Financial Officer and Executive Director. All Pledge/donation returned checks are referred to development for their follow-up COUNTERFEIT CURRENCY When a counterfeit note is received, the Cashier should: 1. Notify Campus Police by phone to pick up the counterfeit note. 2. Unit Director, with a CC: to the Executive Director, Chief Financial Officer, and Director of Enterprise Accounting SEPARATION OF RESPONSIBILITIES A. Separation of duties must be maintained when cash is received. No single person should have complete control over the entire process of receiving, processing applying a payment, preparing the bank deposit and verifying the deposit. B. The Cashier responsible for collecting cash, issuing cash receipts, and preparing the departmental deposit shall be someone other than the person verifying the deposit. Deposit verification is the responsibility of the General Accountant and Director of Enterprise Accounting. 9

10 RECORDING TO THE GENERAL LEDGER A. Bank deposits must be reviewed, approved and recorded to the general ledger in a timely manner. All bank deposits must be accounted for in the general ledger during the appropriate month. B. The Cashier with cash handling responsibilities cannot prepare and post journal entries. The General Accountant is responsible for preparing journal entries. All journal automatic and manual entries must be reviewed, approved, and posted by the Director of Enterprise Accounting or their designee. The preparer and reviewer/approver must be different persons GIFT PROCESSING & ANNUAL FUND DEPOSITS Donations made to the Foundation and the University are processed through the Gift Processing and Annual Fund departments. All donations are recorded in Gift Processing s Raiser s Edge system. Cash Receipts are produced as follows: 1. Each day donations are made to the Gift Processing department and to the Annual Fund, a deposit transmittal is printed from their system. The cash is submitted directly to the Foundation cashier in person. Checks are scanned through the Wells Fargo desktop deposit system directly to the bank. 2. Each deposit is documented in the cashier s log by both the depositor and the cashier. 3. The cash is sorted by denomination. The currency, coin and checks are counted and listed on the daily cash log. 4. The amounts of the deposits are verified with the deposit transmittals that are submitted with the deposits by the units. 5. Currency and checks are deposited to the bank as per guidelines specified in section Preparing the Bank Deposit 6. The deposit transmittals are sent to the Accounting Specialist for processing of the cash receipts. 7. The Accounting Specialist will verify cash, check and credit card totals from the deposit transmittal to the cash log, the check deposit reports, and to the credit card batch settlements. 8. Any discrepancies are discussed with Gift Processing. 9. The Accounting Specialist processes the batch through the GL and prints the cash receipts. Copies of the receipts are kept by the accounting department and the other set of receipts are sent back to Gift Processing or Annual Fund for their reconciliation. 10

11 13 Last Revised 2/11/2015

12

13

14 CAL POLY POMONA FOUNDATION, INC. DEPOSIT SLIP Department: Delivered By: Date: Extension: Prepared By: Authorized Signer Signature: To assist us with our review of this deposit, please provide a detailed description of the revenue, such as purpose, benefit and attach any supporting documents. Please refer to page two of this deposit slip for the types of revenue allowed per Executive Order and the corresponding object codes. Payment Type CA CK CC Project Code Object Code Amount Detailed Description: Total $ * YOU MUST COMPLETE THE ABOVE PRIOR TO DEPOSITING AT THE FOUNDATION'S CASHIER * ** All departments collecting monies on behalf of the Foundation must deposit the funds timely defined as follows: Projects receiving more than $ per day are required to make deposits with the Foundation cashier, the next business day. Projects receiving less than $ per day are required to make deposits when they accumulate $100.00, or weekly, whichever comes first with the Foundation Cashier. Projects are required to deposit all cash and checks at least weekly, regardless of the amount collected. To review foundation cash receipt procedures click this link: Cal Poly Pomona Foundation Inc. CR-370 Revised 2/2011 Page 1 of 2

15

16

17

18 21 Last Revised 2/11/2015

Cash Receipting and Check Handling Policy. California State University, Dominguez Hills Foundation

Cash Receipting and Check Handling Policy California State University, Dominguez Hills Foundation PURPOSE The Chief Financial Officer ( CFO ) of the California State University, Dominguez Hills Foundation

Cash Receipting and Check Handling Policy California State University, Dominguez Hills Foundation PURPOSE The Chief Financial Officer ( CFO ) of the California State University, Dominguez Hills Foundation

CA 370 CASH/CHECK HANDLING POLICY Page 1

CSUF ASC POLICY AND PROCEDURES Section: CASH/CHECK HANDLING Approved by: CFO, TARIQ MARJI Subject: CASH/CHECK HANDLING POLICY / PROCEDURE Dept: ASC FINACIAL SERVICES No: CA 370 Rev.: 02/02/11, 01/07/2015

CSUF ASC POLICY AND PROCEDURES Section: CASH/CHECK HANDLING Approved by: CFO, TARIQ MARJI Subject: CASH/CHECK HANDLING POLICY / PROCEDURE Dept: ASC FINACIAL SERVICES No: CA 370 Rev.: 02/02/11, 01/07/2015

Cash Handling Policy & Procedures

Cash Handling Policy & Procedures Purpose SB 2015-2016:14 The cash handling policy and procedures outlined in this document are intended to provide guidance and appropriate segregation of duties on the

Cash Handling Policy & Procedures Purpose SB 2015-2016:14 The cash handling policy and procedures outlined in this document are intended to provide guidance and appropriate segregation of duties on the

UH/Student Business Services Policies and Procedures

UH/Student Business Services Policies and Procedures CASH HANDLING Student Business Services (SBS) is the primary University of Houston department responsible for revenue collection of approved tuition,

UH/Student Business Services Policies and Procedures CASH HANDLING Student Business Services (SBS) is the primary University of Houston department responsible for revenue collection of approved tuition,

This document will pertain to any department, collectively and person, individually in the handling of cash or cash equivalent.

Student BusinessServices CASH HANDLING PROCEDURES Sage Hall Phone: (805) 437 8810 Fax: (805) 437 8900 PURPOSE The purpose of this document is to establish campus protocol and procedural guidelines for

Student BusinessServices CASH HANDLING PROCEDURES Sage Hall Phone: (805) 437 8810 Fax: (805) 437 8900 PURPOSE The purpose of this document is to establish campus protocol and procedural guidelines for

CASH HANDLING PROCEDURES

CASH HANDLING PROCEDURES 1.0 OBJECTIVE: The primary purpose of this document is to established campus protocol and guidelines for the handling of cash and cash equivalents including appropriate segregation

CASH HANDLING PROCEDURES 1.0 OBJECTIVE: The primary purpose of this document is to established campus protocol and guidelines for the handling of cash and cash equivalents including appropriate segregation

Who Should Know This Policy 1 Definitions 2 Contacts 2 Policy Specifics and Procedures 2 Forms 6 Related Documents 6 Revision History 7 FAQ 7

Cash Receipting Policy Type: Administrative Responsible Office: Treasury Services, Office of the Vice President for Finance and Budget Initial Policy Approved: Undated Current Revision Approved: 08/21/2017

Cash Receipting Policy Type: Administrative Responsible Office: Treasury Services, Office of the Vice President for Finance and Budget Initial Policy Approved: Undated Current Revision Approved: 08/21/2017

CASH HANDLING PROCEDURES

CASH HANDLING PROCEDURES 1.0 OBJECTIVE: The primary purpose of this document is to established campus protocol and procedural guidelines for the handling of cash and cash equivalents and appropriate segregation

CASH HANDLING PROCEDURES 1.0 OBJECTIVE: The primary purpose of this document is to established campus protocol and procedural guidelines for the handling of cash and cash equivalents and appropriate segregation

Policy Title: Funds Handling Policy

Procedure Title: Procedure 10 #: Funds Handling Procedures FA-PR-1202 Effective Date: 12/1/2010 Date of Last Revision: 7/12/2012 Oversight Department: Financial Services Next Review Date: 7/11/2014 Procedure

Procedure Title: Procedure 10 #: Funds Handling Procedures FA-PR-1202 Effective Date: 12/1/2010 Date of Last Revision: 7/12/2012 Oversight Department: Financial Services Next Review Date: 7/11/2014 Procedure

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES

GUIDELINES AND PROCEDURES") FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

FUNDS HANDLING (Cash Receipts) GUIDELINES AND PROCEDURES Reference: Policy No.3600 Revision: August 20, 2014 Funds Handling and Deposit of State and Local Funds 2014.1 1.0 Guidelines 2.0 Definitions 3.0

UNT Cash Control and Departmental Deposit Handbook

UNT Cash Control and Departmental Deposit Handbook University of North Texas September 2018 Volume 1, Issue 2 STUDENT FINANCIAL SERVICES Table of Contents General Overview...3 Proper Handling of University

UNT Cash Control and Departmental Deposit Handbook University of North Texas September 2018 Volume 1, Issue 2 STUDENT FINANCIAL SERVICES Table of Contents General Overview...3 Proper Handling of University

Colorado State University-Pueblo Fiscal Rules

-- Policy No: Policy Area : Subject: 5.7 Cash Handling,Finance & Administration Departmental Cash Handling Policy Purpose The purpose of this policy is to provide all CSU-Pueblo departments who may receive

-- Policy No: Policy Area : Subject: 5.7 Cash Handling,Finance & Administration Departmental Cash Handling Policy Purpose The purpose of this policy is to provide all CSU-Pueblo departments who may receive

F ISCAL ACCOUNTABILITY PROCEDURES PROCEDURE 3.4 CASH HANDLING OVERVIEW ADMINISTRATIVE PROCEDURES. Adopted Date: 08/02/2014 Revised Date: 10/12/2017

PROCEDURE 3.4 CASH HANDLING Adopted Date: 08/02/2014 Revised Date: 10/12/2017 OVERVIEW City departments or agencies that accept cash, checks, and payment cards are responsible for ensuring the secure deposit

PROCEDURE 3.4 CASH HANDLING Adopted Date: 08/02/2014 Revised Date: 10/12/2017 OVERVIEW City departments or agencies that accept cash, checks, and payment cards are responsible for ensuring the secure deposit

TEMPLE UNIVERSITY POLICIES AND PROCEDURES MANUAL

TEMPLE UNIVERSITY POLICIES AND PROCEDURES MANUAL Title: Cash Handling Policy Number: 05.20.12 Issuing Authority: Office of Financial Affairs Responsible Officer: Chief Financial Officer and Treasurer Date

TEMPLE UNIVERSITY POLICIES AND PROCEDURES MANUAL Title: Cash Handling Policy Number: 05.20.12 Issuing Authority: Office of Financial Affairs Responsible Officer: Chief Financial Officer and Treasurer Date

University Main Cashiering: Cashiering Handling Procedures

University Main Cashiering: Cashiering Handling Procedures MAY 6, 2018 University Main Cashiering Services, Bldg. 98 B1-123 Phone: (909) 869-2010 PURPOSE The purpose of this document is to establish campus

University Main Cashiering: Cashiering Handling Procedures MAY 6, 2018 University Main Cashiering Services, Bldg. 98 B1-123 Phone: (909) 869-2010 PURPOSE The purpose of this document is to establish campus

UNIVERSITY CASH HANDLING PROCEDURES University Main Cashiering Services

Student Accounting & Cashiering Services Finance & Administrative Services Bldg. 98, B1-123 P: (909) 869-2010 F: (909) 869-5354 UNIVERSITY CASH HANDLING PROCEDURES University Main Cashiering Services PURPOSE

Student Accounting & Cashiering Services Finance & Administrative Services Bldg. 98, B1-123 P: (909) 869-2010 F: (909) 869-5354 UNIVERSITY CASH HANDLING PROCEDURES University Main Cashiering Services PURPOSE

Law Library UH Law Center CASH HANDLING PROCEDURES 2017

Law Library UH Law Center CASH HANDLING PROCEDURES 2017 Collecting Fine Payments: Payments must be made in cash or by check for the exact amount only. Only law fines are paid at the Law Library. Payments

Law Library UH Law Center CASH HANDLING PROCEDURES 2017 Collecting Fine Payments: Payments must be made in cash or by check for the exact amount only. Only law fines are paid at the Law Library. Payments

THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY

Number THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY Division Accounting & Financial Reporting Date April 18, 2012 Purpose To reduce the risk of theft, loss or misplacement of cash and checks

Number THE UNIVERSITY OF ALABAMA IN HUNTSVILLE CASH HANDLING POLICY Division Accounting & Financial Reporting Date April 18, 2012 Purpose To reduce the risk of theft, loss or misplacement of cash and checks

Bursar s Office University Department Cash Receipting System Users. Updated 03/16/2018

Bursar s Office University Department Cash Receipting System Users Updated 03/16/2018 1 University Cash Receipting System Users Customers of the University may use several forms of payment, but a cash-handling

Bursar s Office University Department Cash Receipting System Users Updated 03/16/2018 1 University Cash Receipting System Users Customers of the University may use several forms of payment, but a cash-handling

Conrad N. Hilton College of Hotel & Restaurant Management Cash Handling Procedures For Fiscal Year 2013

Conrad N. Hilton College of Hotel & Restaurant Management Cash Handling Procedures For Fiscal Year 2013 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving

Conrad N. Hilton College of Hotel & Restaurant Management Cash Handling Procedures For Fiscal Year 2013 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving

COLLEGE STATION INDEPENDENT SCHOOL DISTRICT QUICK REFERENCE GUIDE FOR CASH HANDLING, DEPOSITS, AND PETTY CASH

QUICK REFERENCE GUIDE FOR CASH HANDLING, DEPOSITS, AND PETTY CASH Contact the business office (764-5467 or AR@csisd.org) if you have any questions about these procedures and to order more deposit slips,

QUICK REFERENCE GUIDE FOR CASH HANDLING, DEPOSITS, AND PETTY CASH Contact the business office (764-5467 or AR@csisd.org) if you have any questions about these procedures and to order more deposit slips,

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures INDEX: SECTION 1: INTRODUCTION SECTION 2: MISSION, AUTHORITY AND RESPONSIBILITIES 2.1

COLLEGE OF SOUTHERN NEVADA FINANCE & FACILITIES DIVISION Cash and Payment Handling Operations Policies and Procedures INDEX: SECTION 1: INTRODUCTION SECTION 2: MISSION, AUTHORITY AND RESPONSIBILITIES 2.1

The University of Montana Treasury Area (Treasury) maintains a cashiering function for the purpose of receiving monies due The University.

maintains a cashiering function for the purpose of receiving monies due The University.") Business Services The University of Montana Missoula, Montana 59812-1254 Procedure: 120001 Revision Date: 5/4/16 Revision Number: 7 PROCEDURE: Department Cashier Procedures OVERVIEW... 1 STATUTES AND GUIDELINES...

Business Services The University of Montana Missoula, Montana 59812-1254 Procedure: 120001 Revision Date: 5/4/16 Revision Number: 7 PROCEDURE: Department Cashier Procedures OVERVIEW... 1 STATUTES AND GUIDELINES...

CASH ACCOUNTING MANUAL

Auditor-Controller & Treasurer-Tax Collector March 2011 1. INTRODUCTION... 4 1.1. Purpose of manual... 4 1.2. Applicability of manual... 4 1.3. Using the manual... 4 2. AUTHORITY AND RESPONSIBILITY...

Auditor-Controller & Treasurer-Tax Collector March 2011 1. INTRODUCTION... 4 1.1. Purpose of manual... 4 1.2. Applicability of manual... 4 1.3. Using the manual... 4 2. AUTHORITY AND RESPONSIBILITY...

COLORADO STATE UNIVERSITY Financial Procedure Instructions FPI 6-1

COLORADO STATE UNIVERSITY Financial Procedure Instructions FPI 6-1 1. Procedure Title: Receipt and Deposit of Cash and Checks 2. Procedure Purpose and Effect: To outline procedures for proper safeguarding

COLORADO STATE UNIVERSITY Financial Procedure Instructions FPI 6-1 1. Procedure Title: Receipt and Deposit of Cash and Checks 2. Procedure Purpose and Effect: To outline procedures for proper safeguarding

BULLETIN NO.: BUS-49 DATE: 2/01/02 PAGE: 1 of 15 POLICY FOR HANDLING CASH AND CASH EQUIVALENTS. Vice President--Financial Management Anne C.

PAGE: 1 of 15 POLICY FOR HANDLING CASH AND CASH EQUIVALENTS Vice President--Financial Management Anne C. Broome Content Page I. References 2 A. Business and Finance Bulletins 2 B. Accounting Manual 2 II.

PAGE: 1 of 15 POLICY FOR HANDLING CASH AND CASH EQUIVALENTS Vice President--Financial Management Anne C. Broome Content Page I. References 2 A. Business and Finance Bulletins 2 B. Accounting Manual 2 II.

Cash Handling. Presented By: Jesse Barrios Assistant Bursar

Cash Handling Presented By: Jesse Barrios Assistant Bursar Purpose Define and outline University Processes handling, receiving, transporting and depositing of cash. The Bursar is the University s primary

Cash Handling Presented By: Jesse Barrios Assistant Bursar Purpose Define and outline University Processes handling, receiving, transporting and depositing of cash. The Bursar is the University s primary

Peralta Community College District AP 6300

ADMINISTRATIVE PROCEDURE 6300 GENERAL ACCOUNTING A. Functions The Accounting Office, under the direction of the Vice Chancellor for Finance and Administration and the Associate Vice Chancellor for Finance

ADMINISTRATIVE PROCEDURE 6300 GENERAL ACCOUNTING A. Functions The Accounting Office, under the direction of the Vice Chancellor for Finance and Administration and the Associate Vice Chancellor for Finance

1. Cash includes coin, currency, checks, money orders, and credit card transactions.

1.0 Purpose BEREA COLLEGE Cash Handling Policy Document Document No. No. FIN032 FIN006 Revision Effective Date Date 3/2018 7/2008 Review Revision Date Date 3/2018 Next Pages Review Date 3/2019 1-3 Pages

1.0 Purpose BEREA COLLEGE Cash Handling Policy Document Document No. No. FIN032 FIN006 Revision Effective Date Date 3/2018 7/2008 Review Revision Date Date 3/2018 Next Pages Review Date 3/2019 1-3 Pages

FISCAL MANAGEMENT (Replaces current SBCCD AP 6300)

") 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 AP 6300 AP 6300 San Bernardino Community College District Administrative Procedure

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 AP 6300 AP 6300 San Bernardino Community College District Administrative Procedure

University of Colorado Denver

University of Colorado Denver Fiscal Policy Title: Source: Prepared by: Approved by: Cash Receipts and Deposits Finance Office Controller Associate Vice Chancellor for Finance and Administration Effective

University of Colorado Denver Fiscal Policy Title: Source: Prepared by: Approved by: Cash Receipts and Deposits Finance Office Controller Associate Vice Chancellor for Finance and Administration Effective

Administrative Procedure CHAPTER 6 BUSINESS AND FINANCIAL SERVICES. AP District Cashiering, Collections, and Deposits

Page 1 of 12 Administrative Procedure CHAPTER 6 BUSINESS AND FINANCIAL SERVICES AP 6300.12 District Cashiering, Collections, and Deposits Office(s) of Primary Responsibility: Vice Chancellor of Business

Page 1 of 12 Administrative Procedure CHAPTER 6 BUSINESS AND FINANCIAL SERVICES AP 6300.12 District Cashiering, Collections, and Deposits Office(s) of Primary Responsibility: Vice Chancellor of Business

FAYETTEVILLE POLICIES AND PROCEDURES 306.0

FAYETTEVILLE POLICIES AND PROCEDURES 306.0 Cash Handling Procedures The handling of University monies requires that certain basic procedures be followed precisely at all times. Procedures for the handling

FAYETTEVILLE POLICIES AND PROCEDURES 306.0 Cash Handling Procedures The handling of University monies requires that certain basic procedures be followed precisely at all times. Procedures for the handling

CASH HANDLING PROCEDURES. CALIFORNIA STATE UNIVERSITY, FRESNO ACCOUNTING SERVICES May 1, 2018

CASH HANDLING PROCEDURES CALIFORNIA STATE UNIVERSITY, FRESNO ACCOUNTING SERVICES May 1, 2018 Table of Contents 1.0 Introduction 1.1 Purpose...1 1.2 Scope...1 1.3 Contacts...1 1.4 Definition of Terms...1-2

CASH HANDLING PROCEDURES CALIFORNIA STATE UNIVERSITY, FRESNO ACCOUNTING SERVICES May 1, 2018 Table of Contents 1.0 Introduction 1.1 Purpose...1 1.2 Scope...1 1.3 Contacts...1 1.4 Definition of Terms...1-2

CASH HANDLING. These procedures apply to any individual handling or processing University or Auxiliary Organization cash or cash equivalents.

PURPOSE To provide procedures and guidance for accepting cash and cash equivalents, providing physical and electronic security of cash and cash equivalents and ensuring appropriate segregation of duties

PURPOSE To provide procedures and guidance for accepting cash and cash equivalents, providing physical and electronic security of cash and cash equivalents and ensuring appropriate segregation of duties

INTERNAL CONTROLS MICHAEL N. WATKINS, ASSOCIATE REGIONAL DIRECTOR/FINANCE BOY SCOUTS OF AMERICA, SOUTHERN REGION, P.O. BOX , KENNESAW, GA 30160

INTERNAL CONTROLS MICHAEL N. WATKINS, ASSOCIATE REGIONAL DIRECTOR/FINANCE BOY SCOUTS OF AMERICA, SOUTHERN REGION, P.O. BOX 440728, KENNESAW, GA 30160 INTERNAL CONTROLS Executive Summary The following suggestions

INTERNAL CONTROLS MICHAEL N. WATKINS, ASSOCIATE REGIONAL DIRECTOR/FINANCE BOY SCOUTS OF AMERICA, SOUTHERN REGION, P.O. BOX 440728, KENNESAW, GA 30160 INTERNAL CONTROLS Executive Summary The following suggestions

SAVANNAH STATE UNIVERSITY Cash Operations Manual. Savannah State University Office of the Comptroller 11/30/2011

2011 SAVANNAH STATE UNIVERSITY Cash Operations Manual Savannah State University Office of the Comptroller 11/30/2011 Savannah State University Cash Operations Manual Contents I. INTRODUCTION TO CASH OPERATIONS...

2011 SAVANNAH STATE UNIVERSITY Cash Operations Manual Savannah State University Office of the Comptroller 11/30/2011 Savannah State University Cash Operations Manual Contents I. INTRODUCTION TO CASH OPERATIONS...

Cash Handling and Funds Collection. Policies and Procedures Presented by Treasury Services

Cash Handling and Funds Collection Policies and Procedures Presented by Treasury Services Agenda Receiving Funds Safeguarding Funds Sale of Goods and Inventory Official Cash Receipts Approval to Collect

Cash Handling and Funds Collection Policies and Procedures Presented by Treasury Services Agenda Receiving Funds Safeguarding Funds Sale of Goods and Inventory Official Cash Receipts Approval to Collect

Conrad N Hilton College of Hotel & Restaurant Management Cash Handling Procedures Fiscal Year 2014

I. PURPOSE AND OVERVIEW Conrad N Hilton College of Hotel & Restaurant Management Cash Handling Procedures Fiscal Year 2014 In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving

I. PURPOSE AND OVERVIEW Conrad N Hilton College of Hotel & Restaurant Management Cash Handling Procedures Fiscal Year 2014 In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving

CSU. ICSUAM Section 6000 Financing, Treasury, and Risk Management

CSU ICSUAM Section 6000 Financing, Treasury, and Risk Management Table of Contents 6320.00 Petty Cash Funds and Change Funds... 3 6330.00 Incoming Cash and Checks... 5 **DRAFT** 6320.00 Petty Cash Funds

CSU ICSUAM Section 6000 Financing, Treasury, and Risk Management Table of Contents 6320.00 Petty Cash Funds and Change Funds... 3 6330.00 Incoming Cash and Checks... 5 **DRAFT** 6320.00 Petty Cash Funds

College/Division Guidelines For Establishing Cash Handling Policy and Procedures Fiscal Year 20XX

College/Division Guidelines For Establishing Cash Handling Policy and Procedures Fiscal Year 20XX All cash transactions involving the University, its colleges, or any departments are subject to all applicable

College/Division Guidelines For Establishing Cash Handling Policy and Procedures Fiscal Year 20XX All cash transactions involving the University, its colleges, or any departments are subject to all applicable

Cash Handling & Deposit Procedures for Departments

Cash Handling & Deposit Procedures for Departments STUDENT ACCOUNT SERVICES BPSF CA-108 - Finance & Accounting Last Update: May 2016 Table of Contents Revenue Collection and Deposits Purpose....1 Introduction....1

Cash Handling & Deposit Procedures for Departments STUDENT ACCOUNT SERVICES BPSF CA-108 - Finance & Accounting Last Update: May 2016 Table of Contents Revenue Collection and Deposits Purpose....1 Introduction....1

Cash Operations Training Mary H. Loomis, CPA, Comptroller

Cash Operations Training - 2012 Mary H. Loomis, CPA, Comptroller Purpose of the Cash Operations Manual The purpose of the cash operations manual is to consolidate the cash handling/cash operations policies

Cash Operations Training - 2012 Mary H. Loomis, CPA, Comptroller Purpose of the Cash Operations Manual The purpose of the cash operations manual is to consolidate the cash handling/cash operations policies

Office of the Bursar 7/11/2018 1

These are Ohio University-wide guidelines and shall apply to all staff members of the University. The cash handling guidelines focus on preventing the mishandling or loss of cash and situations where charges

These are Ohio University-wide guidelines and shall apply to all staff members of the University. The cash handling guidelines focus on preventing the mishandling or loss of cash and situations where charges

Brownfield ISD Business Office Procedures Manual

Brownfield ISD Business Office Procedures Manual Brownfield Independent School District 601 Tahoka Road, Brownfield, Texas 79316 Phone (806) 637-2591 Fax (806) 637-8934 Table of Contents Section 1 Introduction..

Brownfield ISD Business Office Procedures Manual Brownfield Independent School District 601 Tahoka Road, Brownfield, Texas 79316 Phone (806) 637-2591 Fax (806) 637-8934 Table of Contents Section 1 Introduction..

OFFICE OF SCHOOL SUPPORT SERVICES MEMORANDUM NO. FS7-2009

Office of School Support Services 44-36 Vernon Boulevard Long Island City, NY 11101 +1 718 707 4300 tel OFFICE OF SCHOOL SUPPORT SERVICES MEMORANDUM NO. FS7-2009 TO: PRINCIPALS OF ALL DAY SCHOOLS ADMINISTRATIVE

Office of School Support Services 44-36 Vernon Boulevard Long Island City, NY 11101 +1 718 707 4300 tel OFFICE OF SCHOOL SUPPORT SERVICES MEMORANDUM NO. FS7-2009 TO: PRINCIPALS OF ALL DAY SCHOOLS ADMINISTRATIVE

Procedure Guidelines and Business Process Guide

Procedure Guidelines and Business Process Guide Department: Procedure Title: Author(s): Cashiering Cash Handling Kathryn Dunham, Brett Holman, Lorlie Leetham Date: 11/2/12 ICSUAM Policy/ authoritative

Procedure Guidelines and Business Process Guide Department: Procedure Title: Author(s): Cashiering Cash Handling Kathryn Dunham, Brett Holman, Lorlie Leetham Date: 11/2/12 ICSUAM Policy/ authoritative

Departmental Funds Receipting

Departmental Funds Receipting 05.141 Authority: History: Source of Authority: Vice Chancellor Business Affairs Effective November 1, 1990, entitled Cash Receipts ; updated May 26, 1999, updated November

Departmental Funds Receipting 05.141 Authority: History: Source of Authority: Vice Chancellor Business Affairs Effective November 1, 1990, entitled Cash Receipts ; updated May 26, 1999, updated November

Cash Accountability Policy

Cash Accountability Policy January 2018 Table of Contents 1. POLICY... 3 2. SCOPE... 3 3. DEFINITIONS... 3 4. CASH RECEIPTS... 4 4.1 Management of Cash Drawers... 4 4.2 Foreign Funds... 5 4.3 Remote Check

Cash Accountability Policy January 2018 Table of Contents 1. POLICY... 3 2. SCOPE... 3 3. DEFINITIONS... 3 4. CASH RECEIPTS... 4 4.1 Management of Cash Drawers... 4 4.2 Foreign Funds... 5 4.3 Remote Check

ASU FINANCIAL SERVICES CASH HANDLING DESK MANUAL TABLE OF CONTENTS

ASU FINANCIAL SERVICES CASH HANDLING DESK MANUAL TABLE OF CONTENTS Section Page Number(s) Introduction 2 Cashiering Services 3 13 Travel Reimbursements 14 21 Accounts Payable 22 24 Accounting Services

ASU FINANCIAL SERVICES CASH HANDLING DESK MANUAL TABLE OF CONTENTS Section Page Number(s) Introduction 2 Cashiering Services 3 13 Travel Reimbursements 14 21 Accounts Payable 22 24 Accounting Services

ALAMOGORDO PUBLIC SCHOOLS CASH CONTROL PROCEDURES

ALAMOGORDO PUBLIC SCHOOLS CASH CONTROL PROCEDURES Objective: To secure public funds and to protect the staff member, as well as the District, against any type of fraud or misapproation of funds that might

ALAMOGORDO PUBLIC SCHOOLS CASH CONTROL PROCEDURES Objective: To secure public funds and to protect the staff member, as well as the District, against any type of fraud or misapproation of funds that might

Undergraduate Student Success Services University Testing Services. Cash Handling. Revised 7/06/17

Undergraduate Student Success Services University Testing Services Cash Handling Revised 7/06/17 I:\smarino\Budget\Cash Handling\Cash Handling 7-06-17.doc 1 PURPOSE AND OVERVIEW In accordance with MAPP

Undergraduate Student Success Services University Testing Services Cash Handling Revised 7/06/17 I:\smarino\Budget\Cash Handling\Cash Handling 7-06-17.doc 1 PURPOSE AND OVERVIEW In accordance with MAPP

T HE N EW Y ORK C ITY D EPARTMENT OF E DUCATION JOEL I. KLEIN, Chancellor

T HE N EW Y ORK C ITY D EPARTMENT OF E DUCATION JOEL I. KLEIN, Chancellor OFFICE OF SCHOOL SUPPORT SERVICES ERIC GOLDSTEIN, Chief Executive 44-36 Vernon Boulevard, Long Island City, NY 11101 Telephone:

T HE N EW Y ORK C ITY D EPARTMENT OF E DUCATION JOEL I. KLEIN, Chancellor OFFICE OF SCHOOL SUPPORT SERVICES ERIC GOLDSTEIN, Chief Executive 44-36 Vernon Boulevard, Long Island City, NY 11101 Telephone:

Accounting Policies and Procedures Manual

Accounting Policies and Procedures Manual Wake Forest Area Chamber of Commerce Accounting Policies and Procedures Manual Table of Contents Contents Introduction... 3 Division of Duties... 4 Cash Receipts

Accounting Policies and Procedures Manual Wake Forest Area Chamber of Commerce Accounting Policies and Procedures Manual Table of Contents Contents Introduction... 3 Division of Duties... 4 Cash Receipts

PAYMENT CARD INDUSTRY

DATA SECURITY POLICY Page 1 of 1 I. PURPOSE To provide guidelines and procedures to ensure that all money paid to the College in the form of cash, checks or payment cards is properly receipted, accounted

DATA SECURITY POLICY Page 1 of 1 I. PURPOSE To provide guidelines and procedures to ensure that all money paid to the College in the form of cash, checks or payment cards is properly receipted, accounted

Cash & Check Handling Policy

Effective Date: October 27, 2006 Latest Revision: July 9, 2012 Policy Statement This policy sets requirements for the collection and secure processing of coin, currency, checks, e-checks, cashier s checks,

Effective Date: October 27, 2006 Latest Revision: July 9, 2012 Policy Statement This policy sets requirements for the collection and secure processing of coin, currency, checks, e-checks, cashier s checks,

CASH RECEIPT POLICY. Section 3 Page 1

Section 3 Page 1 3a. Daily Cash Receipting Policy The following documents the process in place to deter a potential fraud in the Accounting department with regards to the Cash Receipts Process for non-student

Section 3 Page 1 3a. Daily Cash Receipting Policy The following documents the process in place to deter a potential fraud in the Accounting department with regards to the Cash Receipts Process for non-student

Florida A&M University Division of Administrative and Financial Services Office of the Controller Cash Management Department

Florida A&M University Division of Administrative and Financial Services Office of the Controller Cash Management Department CASH COLLECTION AND CONTROLS MANUAL Adopted January 2007 Revised January 2012

Florida A&M University Division of Administrative and Financial Services Office of the Controller Cash Management Department CASH COLLECTION AND CONTROLS MANUAL Adopted January 2007 Revised January 2012

Collections, Contributions, and Accounts Receivable Policies

Collections, Contributions, and Accounts Receivable Policies The Office of the Student Financial Services is responsible for monitoring, processing and recording the collection of all funds collected by

Collections, Contributions, and Accounts Receivable Policies The Office of the Student Financial Services is responsible for monitoring, processing and recording the collection of all funds collected by

BUSINESS POLICIES AND PROCEDURES MANUAL Revised 5-11 Controller s Office

30.53.1 CASHIER'S SECTION Location and Hours Deposit Times Account Questions SAFEGUARDS The Cashier's Section of the Controller's Office collects student tuition and fees, payments of obligations of students,

30.53.1 CASHIER'S SECTION Location and Hours Deposit Times Account Questions SAFEGUARDS The Cashier's Section of the Controller's Office collects student tuition and fees, payments of obligations of students,

Oklahoma State University Office of the Bursar Collection of Funds Procedures

Oklahoma State University Office of the Bursar Collection of Funds Procedures See P&P 3-0331 COLLECTIONS, DEPOSIT AND CONTROL OF CASH OR CHECKS OR CREDIT CARDS RECEIVED IN THE NAME OF OKLAHOMA STATE UNIVERSITY

Oklahoma State University Office of the Bursar Collection of Funds Procedures See P&P 3-0331 COLLECTIONS, DEPOSIT AND CONTROL OF CASH OR CHECKS OR CREDIT CARDS RECEIVED IN THE NAME OF OKLAHOMA STATE UNIVERSITY

TITLE II ADMINISTRATIVE REGULATIONS

TITLE II ADMINISTRATIVE REGULATIONS CHAPTER 18 CASH HANDLING POLICY 18.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to account for the handling

TITLE II ADMINISTRATIVE REGULATIONS CHAPTER 18 CASH HANDLING POLICY 18.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to account for the handling

Business Services Cash Handling: Department Manual

Business Services Cash Handling: Department Manual Deborah Michaels Associate Director, Business Services Cash Management Tina Cripe Administrative Program Assistant, Banking Specialist http://www.sou.edu/bus_serv/bursar/index.html

Business Services Cash Handling: Department Manual Deborah Michaels Associate Director, Business Services Cash Management Tina Cripe Administrative Program Assistant, Banking Specialist http://www.sou.edu/bus_serv/bursar/index.html

Handling Cash. A guide for campus departments

Handling Cash A guide for campus departments Handling cash for the university is an important responsibility. This booklet has been created to help make it easier to correctly meet that responsibility.

Handling Cash A guide for campus departments Handling cash for the university is an important responsibility. This booklet has been created to help make it easier to correctly meet that responsibility.

The University of Texas System. 1. Title. Cash Management and Cash Handling Policy. 2. Policy

1. Title 2. Policy Cash Management and Cash Handling Policy Sec. 1 Sec. 2 Sec. 3 Sec. 4 Sec. 5 Purpose. The purpose of this Policy is to institute controls and standardize cash management policy elements

1. Title 2. Policy Cash Management and Cash Handling Policy Sec. 1 Sec. 2 Sec. 3 Sec. 4 Sec. 5 Purpose. The purpose of this Policy is to institute controls and standardize cash management policy elements

CITY OF KENNEDALE INTERNAL CONTROLS & CASH HANDLING POLICY

CITY OF KENNEDALE INTERNAL CONTROLS & CASH HANDLING POLICY ORIGINALLY ADOPTED BY CITY COUNCIL: NOVEMBER 17, 2011 PREFACE The intent of the City of Kennedale s Internal Controls & Cash Handling Policy is

CITY OF KENNEDALE INTERNAL CONTROLS & CASH HANDLING POLICY ORIGINALLY ADOPTED BY CITY COUNCIL: NOVEMBER 17, 2011 PREFACE The intent of the City of Kennedale s Internal Controls & Cash Handling Policy is

inv001_cash Page 1 of 6 Finance Department, UCT, Private Bag, Rondebosch, 7701, Cape Town, South Africa

Policy & title Effective date Objective Scope Applicable to Additional information Policy & INV001 Handling Cash 1 June 2002 To ensure procedures and internal controls are in place to prevent the mishandling

Policy & title Effective date Objective Scope Applicable to Additional information Policy & INV001 Handling Cash 1 June 2002 To ensure procedures and internal controls are in place to prevent the mishandling

F REQUENTLY A SKED Q UESTIONS

Consolidated Banking F REQUENTLY A SKED Q UESTIONS 1 What do I do to start a new year with Consolidated Banking? All users should log into SinglePoint; make sure passwords work; and entitlements are correct.

Consolidated Banking F REQUENTLY A SKED Q UESTIONS 1 What do I do to start a new year with Consolidated Banking? All users should log into SinglePoint; make sure passwords work; and entitlements are correct.

ACCOUNTS PAYABLE POLICIES AND PROCEDURES...

ACCOUNTS PAYABLE POLICIES AND PROCEDURES..... Petty Cash Fund Procedures General Information Establishing a Petty Cash Fund Increasing a Petty Cash Fund Decreasing a Petty Cash Fund Changing a Custodian

ACCOUNTS PAYABLE POLICIES AND PROCEDURES..... Petty Cash Fund Procedures General Information Establishing a Petty Cash Fund Increasing a Petty Cash Fund Decreasing a Petty Cash Fund Changing a Custodian

Cash Handling Policy

Town of Chapel Hill, NC Governance Policy Effective Date: February 1, 2016 I. POLICY II. PURPOSE III. PROCEDURE IV. RESPONSIBILITIES V. APPENDICES VI. POLICY HISTORY Approved By: Roger L. Stancil, Town

Town of Chapel Hill, NC Governance Policy Effective Date: February 1, 2016 I. POLICY II. PURPOSE III. PROCEDURE IV. RESPONSIBILITIES V. APPENDICES VI. POLICY HISTORY Approved By: Roger L. Stancil, Town

Office of Budget and Finance. Cash Accountability Policy

Office of Budget and Finance Cash Accountability Policy Effective Date: January 1, 2018 Agenda Cash Accountability Policy Cash Certification / Acknowledgment Forms Exceptions and Alternative Procedures

Office of Budget and Finance Cash Accountability Policy Effective Date: January 1, 2018 Agenda Cash Accountability Policy Cash Certification / Acknowledgment Forms Exceptions and Alternative Procedures

PFIN 5: Banking Procedures 24

PFIN 5: Banking Procedures 24 5 1 Checking Accounts OBJECTIVES Explain the purpose and use of a checking account. Prepare a checkbook register. Write a check and prepare a deposit slip. Prepare a bank

PFIN 5: Banking Procedures 24 5 1 Checking Accounts OBJECTIVES Explain the purpose and use of a checking account. Prepare a checkbook register. Write a check and prepare a deposit slip. Prepare a bank

PROCESS STUDENT PAYMENTS

PROCESS STUDENT PAYMENTS Contents Training Objectives...3 Student Payments Overview...4 Security Access to Student Financials...5 Accepting Student Payments... 12 Processing Cash Payments... 16 Accepting

PROCESS STUDENT PAYMENTS Contents Training Objectives...3 Student Payments Overview...4 Security Access to Student Financials...5 Accepting Student Payments... 12 Processing Cash Payments... 16 Accepting

STUDENT ACTIVITY PROCEDURE MANUAL

SCHOOL DISTRICT OF RIVERVIEW GARDENS STUDENT ACTIVITY PROCEDURE MANUAL This manual is designed to provide a set of standardized accounting guidelines and procedures for the administration of the Riverview

SCHOOL DISTRICT OF RIVERVIEW GARDENS STUDENT ACTIVITY PROCEDURE MANUAL This manual is designed to provide a set of standardized accounting guidelines and procedures for the administration of the Riverview

CITY OF PALO ALTO OFFICE OF THE CITY AUDITOR

CITY OF PALO ALTO OFFICE OF THE CITY AUDITOR The Honorable City Council Palo Alto, California June 3, 2013 Special Advisory Memorandum - Cash Handling s This is an informational report and no action is

CITY OF PALO ALTO OFFICE OF THE CITY AUDITOR The Honorable City Council Palo Alto, California June 3, 2013 Special Advisory Memorandum - Cash Handling s This is an informational report and no action is

KENTUCKY COMMUNITY AND TECHNICAL COLLEGE SYSTEM BUSINESS PROCEDURES MANUAL

Effective: July 1, 2013 Supersedes: Business Procedure 3.12 dated July 1, 2011 Applies To: Colleges and System Office Procedure Responsibility: KCTCS Business Services Page 1 of 21 Cash Accounting Section

Effective: July 1, 2013 Supersedes: Business Procedure 3.12 dated July 1, 2011 Applies To: Colleges and System Office Procedure Responsibility: KCTCS Business Services Page 1 of 21 Cash Accounting Section

Agency Account Policies & Procedures

Agency Account Policies & Procedures Overview CAS has been designated as the organization authorized to administer Agency accounts on the SUNY Plattsburgh campus and, as fiscal agent, to receive, hold,

Agency Account Policies & Procedures Overview CAS has been designated as the organization authorized to administer Agency accounts on the SUNY Plattsburgh campus and, as fiscal agent, to receive, hold,

Kamehameha Schools Hawai`i Team/Club Apparel Sales Request for Approval Form (For non-fundraising effort)

") Kamehameha Schools Hawai`i Team/Club Apparel Sales Request for Approval Form (For non-fundraising effort) Team/Group: : Coach/Advisor: Period for apparel sale: NOTE: No more than 5 school days may be allowed

Kamehameha Schools Hawai`i Team/Club Apparel Sales Request for Approval Form (For non-fundraising effort) Team/Group: : Coach/Advisor: Period for apparel sale: NOTE: No more than 5 school days may be allowed

Weber State University. Cash Handling Training

Weber State University Cash Handling Training Cash Handling It s your responsibility Whether you take in a lot of money or you collect pennies ..it is important to maintain good cash handling procedures:

Weber State University Cash Handling Training Cash Handling It s your responsibility Whether you take in a lot of money or you collect pennies ..it is important to maintain good cash handling procedures:

CITY OF MONT BELVIEU CITY COUNCIL POLICY

Page 1 of 14 4.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to accounts for the handling of Mont Belvieu s municipal cash and to maintain public

Page 1 of 14 4.01 Purpose The Cash Handling Policy was established for the purpose of ensuring adequate internal controls to accounts for the handling of Mont Belvieu s municipal cash and to maintain public

Policy Statement CASH RECEIPTS HANDLING AND SECURITY

PROCEDURE: CASH RECEIPTS HANDLING AND SECURITY (Youth Sector) CODE: FS-9.P Origin: Financial Services Authority: Resolution #04-02-25-8 Reference(s): Policy Statement CASH RECEIPTS HANDLING AND SECURITY

PROCEDURE: CASH RECEIPTS HANDLING AND SECURITY (Youth Sector) CODE: FS-9.P Origin: Financial Services Authority: Resolution #04-02-25-8 Reference(s): Policy Statement CASH RECEIPTS HANDLING AND SECURITY

Fairfield ISD Accounts Payable Procedures

Fairfield ISD Accounts Payable Procedures Revised: January 31, 2017 Contents General Instructions... 2 Compliance with State Law... 3 Verification of Check Transactions... 3 Travel Payments... 3 Construction

Fairfield ISD Accounts Payable Procedures Revised: January 31, 2017 Contents General Instructions... 2 Compliance with State Law... 3 Verification of Check Transactions... 3 Travel Payments... 3 Construction

Guidelines for Church Financial Review

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

INSTRUCTIONS FOR OPERATION OF STUDENT ACTIVITIES ACCOUNTS

1 INSTRUCTIONS FOR OPERATION OF STUDENT ACTIVITIES ACCOUNTS TABLE OF CONTENTS Introduction 4 Responsibilities of Advisors, Bookkeeper, and Principal 5 General Requirements for Accounting for Activities

1 INSTRUCTIONS FOR OPERATION OF STUDENT ACTIVITIES ACCOUNTS TABLE OF CONTENTS Introduction 4 Responsibilities of Advisors, Bookkeeper, and Principal 5 General Requirements for Accounting for Activities

CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

James Monroe Museum Procedure for Handling and Recording Incoming Payments

James Monroe Museum Procedure for Handling and Recording Incoming Payments Effective Date of Policy July 1, 2010 Overview and Purpose All payments to the University of Mary Washington (UMW) are recorded

James Monroe Museum Procedure for Handling and Recording Incoming Payments Effective Date of Policy July 1, 2010 Overview and Purpose All payments to the University of Mary Washington (UMW) are recorded

REPORT TO THE WAKE COUNTY BOARD OF COMMISSIONERS ON WAKE COUNTY ACTIONS TAKEN AS A RESULT OF THE REGISTER OF DEEDS OFFICE THEFT.

Purpose of Report REPORT TO THE WAKE COUNTY BOARD OF COMMISSIONERS ON WAKE COUNTY ACTIONS TAKEN AS A RESULT OF THE REGISTER OF DEEDS OFFICE THEFT Background and Context Cash Policies Deposit Locations

Purpose of Report REPORT TO THE WAKE COUNTY BOARD OF COMMISSIONERS ON WAKE COUNTY ACTIONS TAKEN AS A RESULT OF THE REGISTER OF DEEDS OFFICE THEFT Background and Context Cash Policies Deposit Locations

CASH HANDLING PROCEDURES FOR ACTIVITY FUND CUSTODIANS

Mika Barton, Treasurer Ext. 1646 CASH HANDLING PROCEDURES FOR ACTIVITY FUND CUSTODIANS Absolutely NO Petty Cash permitted at any time. RECEIPTING Before allowing teachers/sponsors to collect money from

Mika Barton, Treasurer Ext. 1646 CASH HANDLING PROCEDURES FOR ACTIVITY FUND CUSTODIANS Absolutely NO Petty Cash permitted at any time. RECEIPTING Before allowing teachers/sponsors to collect money from

Revision date: September 21, 2018 Responsible Agent(s): Controller and Treasurer Original effective date: Scope: All Campuses

: Controller and Treasurer Original effective date: Scope: All Campuses") Name of Policy: Receipt of cash Policy Number: 3364-40-22 Approving Officer: Executive Vice President for Finance & Administration/Chief Financial Officer (CFO) or equivalent position Revision date: September

Name of Policy: Receipt of cash Policy Number: 3364-40-22 Approving Officer: Executive Vice President for Finance & Administration/Chief Financial Officer (CFO) or equivalent position Revision date: September

Proper Controls and Handling of Cash

ARCHDIOCESE OF ST. LOUIS Proper Controls and Handling of Cash Best Practices Best Practices for Cash Handling and Management for Parishes This document serves to provide some best practices for cash handling

ARCHDIOCESE OF ST. LOUIS Proper Controls and Handling of Cash Best Practices Best Practices for Cash Handling and Management for Parishes This document serves to provide some best practices for cash handling

Cash Handling. Developed by The University of Texas at Dallas Office of Budget and Finance

Cash Handling Developed by The University of Texas at Dallas Office of Budget and Finance Purpose of this training UT Dallas must follow state laws and UT System policies regarding the proper use of state

Cash Handling Developed by The University of Texas at Dallas Office of Budget and Finance Purpose of this training UT Dallas must follow state laws and UT System policies regarding the proper use of state

Reviewed by: Chuck Roper (Treasury) Sue Potter (A/P) Bill Santiago (Purchasing)

Sue Potter (A/P) Bill Santiago (Purchasing)") Topic: s Date: 03/30/15 Prepared by: Kathy Sawtells Reviewed by: Chuck Roper (Treasury) Sue Potter (A/P) Bill Santiago (Purchasing) Title: Controller Purpose: There are times when small or emergency purchases

Topic: s Date: 03/30/15 Prepared by: Kathy Sawtells Reviewed by: Chuck Roper (Treasury) Sue Potter (A/P) Bill Santiago (Purchasing) Title: Controller Purpose: There are times when small or emergency purchases

Cash Receipts This memo provides guidelines for recording and safeguarding parish cash receipts.

Cash Receipts This memo provides guidelines for recording and safeguarding parish cash receipts. Collection and Placing of Offertory in Pre-numbered Tamper-evident Bags That line the Overflow Collection

Cash Receipts This memo provides guidelines for recording and safeguarding parish cash receipts. Collection and Placing of Offertory in Pre-numbered Tamper-evident Bags That line the Overflow Collection

UNITED I.S.D. TAX OFFICE OPERATIONS MANUAL

UNITED I.S.D. TAX OFFICE OPERATIONS MANUAL 1. Mission Statement 2. Organizational chart 3. Job Descriptions 4. Tax Calendar 5. Teller Procedures TABLE OF CONTENTS 6. Refund Check Procedures 7. Balancing

UNITED I.S.D. TAX OFFICE OPERATIONS MANUAL 1. Mission Statement 2. Organizational chart 3. Job Descriptions 4. Tax Calendar 5. Teller Procedures TABLE OF CONTENTS 6. Refund Check Procedures 7. Balancing

THAT United International Finance Department. Cash Handling Procedures Training Presentation

THAT United International Finance Department Training Presentation 1 Cash Handling It s my job Whether you take in lots of money or you collect pennies 2 OBJECTIVES Understand the principles of good cash

THAT United International Finance Department Training Presentation 1 Cash Handling It s my job Whether you take in lots of money or you collect pennies 2 OBJECTIVES Understand the principles of good cash

Colorado Community College System SYSTEM ACCOUNTING PROCEDURES MANUAL (SAP)

") Colorado Community College System SYSTEM ACCOUNTING PROCEDURES MANUAL (SAP) June 27, 2017 TABLE OF CONTENTS SAP # Description: Page # SAP-1 Adoption of Accounting Procedures 4 SAP-2 Standard Tuition Refund

Colorado Community College System SYSTEM ACCOUNTING PROCEDURES MANUAL (SAP) June 27, 2017 TABLE OF CONTENTS SAP # Description: Page # SAP-1 Adoption of Accounting Procedures 4 SAP-2 Standard Tuition Refund

Ch.6 Internal Control and Accounting for Cash

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

GLASA. Greater Los Angeles Softball Association. Accounting Policies & Procedures Manual

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

Chapter II: Internal Controls II-10

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

CASH HANDLING POLICIES

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.