The future of fintech. Amsterdam 9 February 2017

|

|

|

- Milo Cole

- 6 years ago

- Views:

Transcription

1 The future of fintech Amsterdam 9 February 2017

2 Fintech headlines Fidelity gives BlackRock an early leg up in robo advice brawl Reuters, December 2016 One in four UK card payments now contactless Banking Tech, January 2017 Half of Supply Chain Industry Will Invest in Blockchain in 2017 Global Trade magazine, January 2017 New insurtech Ladder is digitizing life insurance Business Insider, January 2017 PayTM plots move into asset management in India Financial Times, January 2017 Fintech Companies Could Give Billions of People More Banking Options Harvard Business News, January 2017 Fintech lures millennial investors away from asset managers Financial Times, January 2017 Brother, can you spare a contactless payment? Homeless go hi-tech Amsterdam tests innovative new method of donating money to the homeless using a contactless payment system International Business Times, January

3 What is fintech? Paytech Robo-advice Virtual currencies P2P lending Regtech Smart contracts Blockchain 3

4 Claire Harrop Adam Ryan 4

5 Participants The Future of Fintech 5

6 Agenda 1 Advanced payment technologies 2 Blockchain/digital currencies 3 Smart contracts 4 Overview of legal issues 5 Regulator engagement 6

7 Advanced payment technologies Section 1

8 Overview Technology overlay Transaction settlement Interbank settlement Central Bank Consumers Merchants Bank Bank 8

9 Overview example of current payment process Purchase transaction Merchant settlement Revenue allocation Interchange fees $1.75 Card issuer ABN Amro, ING, Rabobank, Deutsche Bank, HSBC Consumer $ % Merchant $2.50 $97.50 Network fees $0.25 Card network Visa, MasterCard, Discover Acquiring fees $0.50 Merchant acquirer First Data, Chase paymentech, Barclaycard 9

10 Overview three main themes Process digitalisation Competition from new players Increasing regulation Customer expect more from multichannel banking Non-/Near-bank fintech innovation Increasing complex regulatory environment Central bank/ inter-bank innovation ISO20022 APIs for third party payment providers Mobile banking Person-to-person real-time payments Social media Contactless payments Purchase aggregation New types of authentication Digital wallets Virtual currencies New types of consumer interfaces PSD2 E-money AML/sanctions Competition regulations Data protection and security 10

11 Overview central bank/inter-bank innovation UK US Faster payments taskforce Eurozone Singapore 11

12 Overview bank innovation Bank innovation Cheque processing and bill payment Fingerprint mobile banking Mobile banking Person-to-person payments Social media NFC wallet solutions with Visa and MasterCard 12

13 Bank innovation bunq 13

14 Overview fintech innovation Fintech innovation Payment processors E-money Transaction initiation 14

15 Payment processors adyen 15

16 Overview regulation Regulation Financial services Consumer credit PSD2 E-money directive AML Sanctions Competition Multilateral Interchange Fee regulation Data monopolies Bank competition Data and security Data protection Big data Payment card information security Cyber security 16

17 Financial service EU financial services regulation More onerous regulatory requirements Type of institution Authorisation Examples of services Implications (non-exhaustive) Banks Banking licence (ie accepting deposits) General banking services, including holding customer s money in bank accounts Full gamut of onerous regulatory provisions However, can provide most services Passport into rest of EU Consumer credit (UK only) Depends on jurisdiction. In the UK, must be authorised by FCA to offer consumer credit Operating an electronic system in relation to lending Entering into a regulated credit agreement as lender Debt collection Credit broking (eg effecting introductions relating to credit agreements) Depending on the activity carried out, there are different levels Change in control regime Different regimes across the EU (not harmonised) E-money institution (EMI) Authorised as an EMI Not required if credit institution Category of small EMI exists Issuing e-money E-money is money that is: 1. stored electronically 2. issued on receipt of funds for the purposes of making payment transactions 3. accepted by someone other than the issuer Examples of e-money: mobile money (eg Mpesa) Minimum capital requirements Change in control regime (when acquiring EMI) Safeguarding funds requirements Controls re agents, outsourcing Passport into the rest of the EU Less onerous regulatory requirements Payment services institution (PSI) Authorised as a PSI Not required if credit institution or EMI Category of small PSI exists Money remittance Non-bank credit card issuers (eg American Express) Merchant acquiring firms Execution of payment transactions Execution through mobile device where only acting as intermediary (note very unclear and due to change in PSD2) In PSD2 third party payment services Capital requirements Conduct of business requirements apply to all institutions providing payment services (including credit institutions and EMIs) Passport into the rest of the EU 17

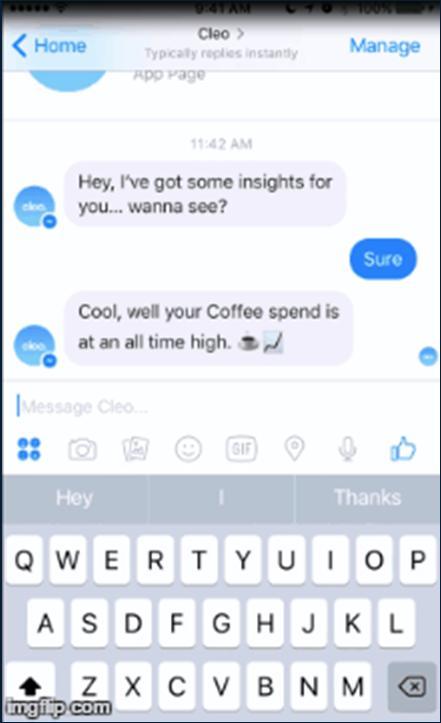

18 Financial services changes in PSD2 Amended exemptions Limited network Exemption for payment services based on specific payment instruments that can be used only in a limited way to: acquire goods or services only in the premises of the issuer or within a limited network of service providers; or acquire a limited range of goods or services If volume over previous 12 months exceeds EUR1,000,000 must seek clearance from the relevant regulator New payment services Payment initiation Payment service enabling access to a payment account. Effectively, initiation of transactions online, together with a confirmation message so that the retailer can ship the product Can be used to make a payment online without using a credit or debit card Examples Sofortüberweisung, Trustly Download Limited exclusively to ancillary payment services carried out by providers of electronic communication networks or services (such as telecom operators) Only intended to apply to low value payments for digital content (such as ringtones, music, games, videos or applications) and charitable activities and tickets Not available for individual transactions exceeding EUR50. Subject to a cap of EUR300 per month Account information Offers consumers a consolidated view of all, or some of, their bank accounts and enable them to access them by online login Examples Tink, AFAS, Cleo 18

19 Examples 19

20 Competition Multilateral Interchange Fee Regulation Bank competition Data monopolies EDPS 20

21 Data and security Data protection Cyber security Payment card information security Innovation 21

22 Blockchain / digital currencies Section 2

23

24 Digital currency / payments 24

25 Securities settlement 25

26 Wholesale insurance 26

27 Retail insurance 27

28 Voting 28

29 Smart contracts Section 3

30 Smart contract logic An automated, self-executing agreement 30

31 Smart contract Source: Ethereum 31

32 Non-categorical expression Traditional contracts 32

33 Smart contract spectrum 33

34 Overview of legal issues Section 4

35 Governing law 35

36 Jurisdiction 36

37 Immutability 37

38 The problem of permanence 38

39 Liability 39

40 Data protection 40

41 Cyber security 41

42 Regulator engagement Section 5

43 Regulatory engagement We maintain open channels of communication with international financial regulators, including on Blockchain and smart contracts. Regulators we are talking to about Blockchain and smart contracts: Highlights include: Close contact with FCA Project Innovate team Presentations to the Bank of England on Blockchain Upcoming meeting with Bank of England Manager of Digital Currencies Liaising with MAS innovation team Market leading practice with considerable bench strength across its contentious and non-contentious regulatory teams Chambers UK 2016 Financial Services: Non-Contentious Regulatory 43

44 44

Payment Services Directive II: Unravelling the Mystery 7 March 2017

Payment Services Directive II: Unravelling the Mystery 7 March 2017 John Casanova, Partner Sidley Austin LLP PSD II What is it? New directive which will repeal and replace current EU payment services legislation.

Payment Services Directive II: Unravelling the Mystery 7 March 2017 John Casanova, Partner Sidley Austin LLP PSD II What is it? New directive which will repeal and replace current EU payment services legislation.

The Payment Services Directive. Mortgage Fraud - what are the lessons?

The Payment Services Directive Mortgage Fraud - what are the lessons? Jean Price Head of Retail Banking and Consumer Finance 3 rd September 2008 The Payment Services Directive Overview and objectives Key

The Payment Services Directive Mortgage Fraud - what are the lessons? Jean Price Head of Retail Banking and Consumer Finance 3 rd September 2008 The Payment Services Directive Overview and objectives Key

Payments terminology and acronyms

Payments terminology COMMON ACRONYMS AML anti-money laundering anti-money laundering (aml) is a term mainly used in the legal and financial industries to describe a set of procedures, regulations, or legal

Payments terminology COMMON ACRONYMS AML anti-money laundering anti-money laundering (aml) is a term mainly used in the legal and financial industries to describe a set of procedures, regulations, or legal

Blockchain s Potential Role in Payment Modernization

Blockchain s Potential Role in Payment Modernization Presented by: Christopher J. Mager Managing Director and Head of Global Innovation BNY Mellon Treasury Services October 3rd, 2016 Agenda Payment disruption

Blockchain s Potential Role in Payment Modernization Presented by: Christopher J. Mager Managing Director and Head of Global Innovation BNY Mellon Treasury Services October 3rd, 2016 Agenda Payment disruption

Payment Services Directive: frequently asked questions

European Commission - Fact Sheet Payment Services Directive: frequently asked questions Brussels, 12 January 2018 GENERAL QUESTIONS 1. What is the Payment Services Directive? The first Payment Services

European Commission - Fact Sheet Payment Services Directive: frequently asked questions Brussels, 12 January 2018 GENERAL QUESTIONS 1. What is the Payment Services Directive? The first Payment Services

EU Policy Priorities for Retail Payments

EU Policy Priorities for Retail Payments Conference on 'A new era in payments?' Lisbon, 14 May 2018 Ralf Jacob European Commission FISMA D.3 Retail Financial Services and Payments EU regulations on payments

EU Policy Priorities for Retail Payments Conference on 'A new era in payments?' Lisbon, 14 May 2018 Ralf Jacob European Commission FISMA D.3 Retail Financial Services and Payments EU regulations on payments

EUROPEAN COMMISSION Directorate General Internal Market and Services

EUROPEAN COMMISSION Directorate General Internal Market and Services FINANCIAL INSTITUTIONS 14.10.2013 PSMEG/002/13 INFORMATION PAPER PROPOSALS FOR A NEW PAYMENT SERVICES DIRECTIVE ('PSD2') AND A REGULATION

EUROPEAN COMMISSION Directorate General Internal Market and Services FINANCIAL INSTITUTIONS 14.10.2013 PSMEG/002/13 INFORMATION PAPER PROPOSALS FOR A NEW PAYMENT SERVICES DIRECTIVE ('PSD2') AND A REGULATION

GLOBAL FINTECH HACKCELERATOR

GLOBAL FINTECH HACKCELERATOR Industry Problem Statements Version 2018.05.21 Organised by In partnership with In collaboration with Global FinTech Hackcelerator Powered by 80 Problem statements The global

GLOBAL FINTECH HACKCELERATOR Industry Problem Statements Version 2018.05.21 Organised by In partnership with In collaboration with Global FinTech Hackcelerator Powered by 80 Problem statements The global

PSD2 Access to account (XS2A) Game changing accelerator in financial services

Game changing accelerator in financial services") PSD2 Access to account (XS2A) Game changing accelerator in financial services Douwe Lycklama - 22 March 2016 Tomorrow s transactions today Introduction Innopay: innovation experts since 2002 >25 consultants

PSD2 Access to account (XS2A) Game changing accelerator in financial services Douwe Lycklama - 22 March 2016 Tomorrow s transactions today Introduction Innopay: innovation experts since 2002 >25 consultants

Frequently Asked Questions. (For information purposes only) Banque centrale du Luxembourg

Banque centrale du Luxembourg") Frequently Asked Questions On Banque centrale du Luxembourg regulation 2011/N 9 dated 4 July 2011 relating to the collection of data on payment instruments and operations (For information purposes only)

Frequently Asked Questions On Banque centrale du Luxembourg regulation 2011/N 9 dated 4 July 2011 relating to the collection of data on payment instruments and operations (For information purposes only)

Innovation in Payment Services: The Role of EU Policies

Innovation in Payment Services: The Role of EU Policies The Hague, 18 January 2018 Ralf Jacob European Commission FISMA D.3 Retail Financial Services and Payments Objectives of this presentation Present

Innovation in Payment Services: The Role of EU Policies The Hague, 18 January 2018 Ralf Jacob European Commission FISMA D.3 Retail Financial Services and Payments Objectives of this presentation Present

The Changing EU Regulatory Framework for Retail Payments

The Changing EU Regulatory Framework for Retail Payments 10 th Jubilee Conference on Payments and Market Infrastructures Ohrid, 5-7 July 2017 Ralf Jacob European Commission FISMA D.3 Retail Financial Services

The Changing EU Regulatory Framework for Retail Payments 10 th Jubilee Conference on Payments and Market Infrastructures Ohrid, 5-7 July 2017 Ralf Jacob European Commission FISMA D.3 Retail Financial Services

DIRECTIVES. (Text with EEA relevance) Having regard to the Treaty on the Functioning of the European Union, and in particular Article 114 thereof,

Having regard to the Treaty on the Functioning of the European Union, and in particular Article 114 thereof,") 23.12.2015 Official Journal of the European Union L 337/35 DIRECTIVES DIRECTIVE (EU) 2015/2366 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 25 November 2015 on payment services in the internal market,

23.12.2015 Official Journal of the European Union L 337/35 DIRECTIVES DIRECTIVE (EU) 2015/2366 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 25 November 2015 on payment services in the internal market,

Copyright 2015 Ingenico Payment Services. $name

$name Table of contents 1. What is Interchange? 2. What are scheme fees? 3. What is Interchange ++ Pricing? 4. What's new? 5. Are there any exceptions? 6. Where can I find more information? Page 1 of 7-16/03/2016

$name Table of contents 1. What is Interchange? 2. What are scheme fees? 3. What is Interchange ++ Pricing? 4. What's new? 5. Are there any exceptions? 6. Where can I find more information? Page 1 of 7-16/03/2016

A decade of Dutch fintech

Europe s largest fintech event, Money20/20, was held in Amsterdam this year (4 to 6 June 2018), accentuating the positive development of the Dutch fintech climate. With an estimated number of 430 companies

Europe s largest fintech event, Money20/20, was held in Amsterdam this year (4 to 6 June 2018), accentuating the positive development of the Dutch fintech climate. With an estimated number of 430 companies

For personal use only

27 th January 2017 Report to shareholders for the Quarter Ended 31 st December 2016 isignthis Ltd (isignthis or the Company) (ASX : ISX) is pleased to provide the following business update and for the

27 th January 2017 Report to shareholders for the Quarter Ended 31 st December 2016 isignthis Ltd (isignthis or the Company) (ASX : ISX) is pleased to provide the following business update and for the

PSD I and PSD II Presentation Global Money Transfer Summit 2013

PSD I and PSD II Presentation Global Money Transfer Summit 2013 29-30 October 2013 Structure of the presentation PSD I: Impact PSD II: Overview of main proposed changes Assessment of proposed changes relative

PSD I and PSD II Presentation Global Money Transfer Summit 2013 29-30 October 2013 Structure of the presentation PSD I: Impact PSD II: Overview of main proposed changes Assessment of proposed changes relative

Your questions on PSD

Your questions on PSD Payment Services Directive 2007/64/EC s and answers The questions on this page have been submitted by users of this website or by correspondence directly with the Commission services.

Your questions on PSD Payment Services Directive 2007/64/EC s and answers The questions on this page have been submitted by users of this website or by correspondence directly with the Commission services.

Simplify Global Corporate Payments.

Simplify Global Corporate Payments www.mychoicecorporate.com MyChoiceCorporate Overview MyChoice Prepaid Debit Cards allow businesses to streamline commission, business, incen ve, and travel payments and

Simplify Global Corporate Payments www.mychoicecorporate.com MyChoiceCorporate Overview MyChoice Prepaid Debit Cards allow businesses to streamline commission, business, incen ve, and travel payments and

UPCOMING SCHEME CHANGES

UPCOMING SCHEME CHANGES MERCHANTS/PARTNERS/ISO COPY Payvision Ref: Payvision-Upcoming Scheme Changes (v1.0)-october 2015 Page 1 Rights of use: COMPLYING WITH ALL APPLICABLE COPYRIGHT LAWS IS THE RESPONSABILITY

UPCOMING SCHEME CHANGES MERCHANTS/PARTNERS/ISO COPY Payvision Ref: Payvision-Upcoming Scheme Changes (v1.0)-october 2015 Page 1 Rights of use: COMPLYING WITH ALL APPLICABLE COPYRIGHT LAWS IS THE RESPONSABILITY

Your questions on PSD

Your questions on PSD Payment Services Directive 2007/64/EC s and answers The questions on this page have been submitted by users of this website or by correspondence directly with the Commission services.

Your questions on PSD Payment Services Directive 2007/64/EC s and answers The questions on this page have been submitted by users of this website or by correspondence directly with the Commission services.

Proposed Payment Services Bill

t CONSULTATION PAPER P021-2017 November 2017 Proposed Payment Services Bill Monetary Authority Of Singapore 1 CONSULTATION PAPER ON THE PROPOSED PAYMENT SERVICES BILL 21 November 2017 Contents 1 Preface...

t CONSULTATION PAPER P021-2017 November 2017 Proposed Payment Services Bill Monetary Authority Of Singapore 1 CONSULTATION PAPER ON THE PROPOSED PAYMENT SERVICES BILL 21 November 2017 Contents 1 Preface...

Financial Inclusion and Fintech

Financial Inclusion and Fintech The views expressed in this presentation are those of the author and do not necessarily represent the views of the NBC. 2 Agenda Financial Inclusion Landscape Regulatory

Financial Inclusion and Fintech The views expressed in this presentation are those of the author and do not necessarily represent the views of the NBC. 2 Agenda Financial Inclusion Landscape Regulatory

A report showing the merchant s settlement. The acquirer settlement report is generated by the acquiring bank at the end of every billing cycle.

A Acquirer (acquiring bank) An acquirer is an organisation that is licensed as a member of Visa/MasterCard as an affiliated bank and processes credit card transactions for (online) businesses. Acquirers

A Acquirer (acquiring bank) An acquirer is an organisation that is licensed as a member of Visa/MasterCard as an affiliated bank and processes credit card transactions for (online) businesses. Acquirers

PSD2 & Account Access

PSD & Account Access Impacts & Opportunities ESF+ 13 th April 016 1 PSD Background Potential Opportunities 1 What are the key PSD elements? 1 Scope Extension Payment Initiation and Account Information

PSD & Account Access Impacts & Opportunities ESF+ 13 th April 016 1 PSD Background Potential Opportunities 1 What are the key PSD elements? 1 Scope Extension Payment Initiation and Account Information

CARDS vs ACH in the new immediate, open payments world. Richard Ransom Bottomline Technologies

CARDS vs ACH in the new immediate, open payments world Richard Ransom Bottomline Technologies A B O U T B O T T O M L I N E T E C H N O L O G I E S Simple Easy and consistent access to parties, types,

CARDS vs ACH in the new immediate, open payments world Richard Ransom Bottomline Technologies A B O U T B O T T O M L I N E T E C H N O L O G I E S Simple Easy and consistent access to parties, types,

$110100$010. Crypto Currencies. Good or Evil? 10$ $100010

100110101$110100$010 Crypto Currencies Good or Evil? 0 1 0 $ 0 1 1 0 1 0 1 0 1 1 0 $ 1 1 1 0 0 1 0 1 What are Crypto-Currencies Crypto-currencies, such as Bitcoin, are digital currencies that rely on cryptographic

100110101$110100$010 Crypto Currencies Good or Evil? 0 1 0 $ 0 1 1 0 1 0 1 0 1 1 0 $ 1 1 1 0 0 1 0 1 What are Crypto-Currencies Crypto-currencies, such as Bitcoin, are digital currencies that rely on cryptographic

Payments Services: Regulatory Timeline. February 2017

Payments Services: Regulatory Timeline February 2017 The next couple of years will see a range of legislative and regulatory developments affecting those in the payment services industry. As well as initiatives

Payments Services: Regulatory Timeline February 2017 The next couple of years will see a range of legislative and regulatory developments affecting those in the payment services industry. As well as initiatives

FCA Business Plan 2017/18

FCA Business Plan 2017/18 17 May 2017 www.moorestephens.co.uk PRECISE. PROVEN. PERFORMANCE. Andrew Jacobs Agenda Introduction Andrew Jacobs Main themes of 2017/18 Business Plan Giovanni Giro Governance

FCA Business Plan 2017/18 17 May 2017 www.moorestephens.co.uk PRECISE. PROVEN. PERFORMANCE. Andrew Jacobs Agenda Introduction Andrew Jacobs Main themes of 2017/18 Business Plan Giovanni Giro Governance

AMPLIFY CREDIT CARD. Business Conditions of Use.

AMPLIFY BUSINESS CREDIT CARD Business Conditions of Use. Effective Date: 30 May 2018 Your Credit Contract includes this Conditions of Use brochure, the letter which advises both your credit limit and other

AMPLIFY BUSINESS CREDIT CARD Business Conditions of Use. Effective Date: 30 May 2018 Your Credit Contract includes this Conditions of Use brochure, the letter which advises both your credit limit and other

Developments on the EU Financial Services Legislative agenda

Developments on the EU Financial Services Legislative agenda London, 2 February 2016 Dr. David P. Doyle EU Policy Expert Financial Services Regulation 1 Inter-connecting challenges facing the EU over 2016

Developments on the EU Financial Services Legislative agenda London, 2 February 2016 Dr. David P. Doyle EU Policy Expert Financial Services Regulation 1 Inter-connecting challenges facing the EU over 2016

the security of retail payments

The European Forum on the security of retail payments Pierre Petit Payment Forum Helsinki, 10 May 2012 Outline I. Origin and mandate II. Recommendations for the security of internet payments III. Future

The European Forum on the security of retail payments Pierre Petit Payment Forum Helsinki, 10 May 2012 Outline I. Origin and mandate II. Recommendations for the security of internet payments III. Future

PSD2 (Payment Services Directive) & RTS (Regulatory Technical Standards)

& RTS (Regulatory Technical Standards)") PSD2 (Payment Services Directive) & RTS (Regulatory Technical Standards) Begoña Blanco Sánchez Head of Payments -Product management Daily Banking ING Belgium Creobis 16/5/2017 Agenda PSD2 Objectives RTS

PSD2 (Payment Services Directive) & RTS (Regulatory Technical Standards) Begoña Blanco Sánchez Head of Payments -Product management Daily Banking ING Belgium Creobis 16/5/2017 Agenda PSD2 Objectives RTS

Blockchain for financials

Blockchain for financials An introduction to core functionality October 2017 What is a blockchain (or distributed ledger)? A distributed ledger is a system that allows parties who don t fully trust each

Blockchain for financials An introduction to core functionality October 2017 What is a blockchain (or distributed ledger)? A distributed ledger is a system that allows parties who don t fully trust each

Draft Guidance GC 15/2. Guidance on the PSR s approach as a competent authority for the EU Interchange Fee Regulation

Draft Guidance GC 15/2 Guidance on the PSR s approach as a competent authority for the EU Interchange Fee Regulation Contents 1 Overview... 3 Introduction... 3 The PSR s role as a UK competent authority

Draft Guidance GC 15/2 Guidance on the PSR s approach as a competent authority for the EU Interchange Fee Regulation Contents 1 Overview... 3 Introduction... 3 The PSR s role as a UK competent authority

Bank of Mauritius. National Payment Switch

Bank of Mauritius National Payment Switch January 2016 1 Introduction The Bank of Mauritius (Bank) is empowered under the Bank of Mauritius Act to safeguard the safety, soundness and efficiency of payment,

Bank of Mauritius National Payment Switch January 2016 1 Introduction The Bank of Mauritius (Bank) is empowered under the Bank of Mauritius Act to safeguard the safety, soundness and efficiency of payment,

14971/14 CS/MT/mf 1 DGG 1C

Council of the European Union Brussels, 31 October 2014 (OR. en) Interinstitutional File: 2013/0264(COD) 14971/14 EF 289 ECOFIN 1005 CONSOM 224 CODEC 2150 NOTE From: To: Subject: Presidency Delegations

Council of the European Union Brussels, 31 October 2014 (OR. en) Interinstitutional File: 2013/0264(COD) 14971/14 EF 289 ECOFIN 1005 CONSOM 224 CODEC 2150 NOTE From: To: Subject: Presidency Delegations

New Regulations in Payments Services

New Regulations in Payments Services Bucharest, 7 November 2013 Mirela Iovu Vicepresident CEC Bank Member of Legal Support Group of European Payments Council 1 New Regulations / Projects Regulation (UE)

New Regulations in Payments Services Bucharest, 7 November 2013 Mirela Iovu Vicepresident CEC Bank Member of Legal Support Group of European Payments Council 1 New Regulations / Projects Regulation (UE)

2017 FinTech Predictions. December 2016

2017 FinTech Predictions December 2016 Introduction 2016 has been a year where FinTech was a catalyst for significant change. 2017 promises to be an exciting year, with more sophistication and growth following

2017 FinTech Predictions December 2016 Introduction 2016 has been a year where FinTech was a catalyst for significant change. 2017 promises to be an exciting year, with more sophistication and growth following

Guidance on the PSR s approach as a competent authority for the EU Interchange Fee Regulation

Guidance on the PSR s approach as a competent authority for the EU Interchange Fee Regulation Contents 1. Overview 4 Introduction 4 The PSR s role as a UK competent authority for the IFR 4 The purpose

Guidance on the PSR s approach as a competent authority for the EU Interchange Fee Regulation Contents 1. Overview 4 Introduction 4 The PSR s role as a UK competent authority for the IFR 4 The purpose

PayLink. Common Payment Gateway Domestic SWITCH. Irida Huta

PayLink Common Payment Gateway Domestic SWITCH Irida Huta Objective Common Payment Gateway Domestic SWITCH Schema concept - Business Technical implementation with a licensed software platform with the

PayLink Common Payment Gateway Domestic SWITCH Irida Huta Objective Common Payment Gateway Domestic SWITCH Schema concept - Business Technical implementation with a licensed software platform with the

Energy Web Foundation blockchain and digital security in energy. OECD workshop, 15 February 2018

Energy Web Foundation blockchain and digital security in energy OECD workshop, 15 February 2018 Agenda 1 What 2 is EWF? Blockchain and digital security in energy 3 The EWF Blockchain Platform: functionality

Energy Web Foundation blockchain and digital security in energy OECD workshop, 15 February 2018 Agenda 1 What 2 is EWF? Blockchain and digital security in energy 3 The EWF Blockchain Platform: functionality

Commercial Payment Services Conditions

Commercial Payment Services Conditions 7207 January 2018 Contents Commercial Payment Services Conditions Definitions 1. Subject and applicable conditions 1.1. Subject 1.2. Other applicable conditions 1.3.

Commercial Payment Services Conditions 7207 January 2018 Contents Commercial Payment Services Conditions Definitions 1. Subject and applicable conditions 1.1. Subject 1.2. Other applicable conditions 1.3.

Combined Conditions of Use and Credit Guide. Effective as at 30 June 2017.

Combined Conditions of Use and Credit Guide. Effective as at 30 June 2017. Introduction. Your Credit Card Contract includes this Conditions of Use brochure, the letter which advises both your credit limit

Combined Conditions of Use and Credit Guide. Effective as at 30 June 2017. Introduction. Your Credit Card Contract includes this Conditions of Use brochure, the letter which advises both your credit limit

BACK TO BASICS: BLOCKCHAIN, FINTECH, INSURTECH AND PROPTECH

BACK TO BASICS: BLOCKCHAIN, FINTECH, INSURTECH AND PROPTECH WIN In-House Counsel Day Melbourne 2018 Thursday 15 March 2018 www.dlapiper.com Thursday 15 March 2018 0 Our objectives today 1. An overview

BACK TO BASICS: BLOCKCHAIN, FINTECH, INSURTECH AND PROPTECH WIN In-House Counsel Day Melbourne 2018 Thursday 15 March 2018 www.dlapiper.com Thursday 15 March 2018 0 Our objectives today 1. An overview

UKTI - Thai Business Delegation

UKTI - Thai Business Delegation June 3 rd, 2016 Level39, Canary Wharf Agenda 14.00-14.05 Welcome, introductions and agenda Julian Skan 14.05-14.15 Overview of TheCityUK Cameron Jones & Bryan Cress 14.15-14.30

UKTI - Thai Business Delegation June 3 rd, 2016 Level39, Canary Wharf Agenda 14.00-14.05 Welcome, introductions and agenda Julian Skan 14.05-14.15 Overview of TheCityUK Cameron Jones & Bryan Cress 14.15-14.30

The EMA s position on the proposed inclusion of custodian wallet providers in the scope of the 4 th Money Laundering Directive

The EMA s position on the proposed inclusion of providers in the scope of the 4 th Money Laundering Directive This paper addresses the proposals for an amendment Directive ( 5MLD ) to the 4 th Money Laundering

The EMA s position on the proposed inclusion of providers in the scope of the 4 th Money Laundering Directive This paper addresses the proposals for an amendment Directive ( 5MLD ) to the 4 th Money Laundering

The Perimeter Guidance Manual. Chapter 15. Guidance on the scope of the Payment Services Regulations 2017

The Perimeter Guidance Manual Chapter Guidance on the scope of the Payment Services PERG : Guidance on the Section.1 : Introduction.1 Introduction The purpose of this chapter is to help businesses in the

The Perimeter Guidance Manual Chapter Guidance on the scope of the Payment Services PERG : Guidance on the Section.1 : Introduction.1 Introduction The purpose of this chapter is to help businesses in the

The Excellence Acceleration Program in Fintech sector

The Excellence Acceleration Program in Fintech sector SALONE DEI PAGAMENTI - MILANO, 24th NOVEMBER 2017 Digital Magics 2017 - All rights reserved www.digitalmagics.com Program s Objectives Create a center

The Excellence Acceleration Program in Fintech sector SALONE DEI PAGAMENTI - MILANO, 24th NOVEMBER 2017 Digital Magics 2017 - All rights reserved www.digitalmagics.com Program s Objectives Create a center

Media Presentation. For the Half Year Ended 31 December 2016 COMMONWEALTH BANK OF AUSTRALIA ACN FEBRUARY 2017

Media Presentation For the Half Year Ended 31 December 2016 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 15 FEBRUARY 2017 Today Strategic Update Financials Outlook Delivering on our Vision In the last

Media Presentation For the Half Year Ended 31 December 2016 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 15 FEBRUARY 2017 Today Strategic Update Financials Outlook Delivering on our Vision In the last

Combined Conditions of Use and Credit Guide. Effective as at 30 June 2017.

Combined Conditions of Use and Credit Guide. Effective as at 30 June 2017. Important changes to Altitude card accounts. The Reserve Bank of Australia introduced new industry wide regulations on 1 July

Combined Conditions of Use and Credit Guide. Effective as at 30 June 2017. Important changes to Altitude card accounts. The Reserve Bank of Australia introduced new industry wide regulations on 1 July

Commercial Payment Services Conditions

Commercial Payment Services Conditions 7207 January 2019 Contents Commercial Payment Services Conditions Definitions 1. Subject and applicable conditions 1.1. Subject 1.2. Other applicable conditions 1.3.

Commercial Payment Services Conditions 7207 January 2019 Contents Commercial Payment Services Conditions Definitions 1. Subject and applicable conditions 1.1. Subject 1.2. Other applicable conditions 1.3.

Advanced Card Payments Overview Dan Kramer

Advanced Card Payments Overview Dan Kramer Senior Vice President, SHAZAM Agenda PIN-Based Transactions Signature-Based Transactions EFT Regulations Tokenization PIN-Based Transactions Intra-Network PIN-Based

Advanced Card Payments Overview Dan Kramer Senior Vice President, SHAZAM Agenda PIN-Based Transactions Signature-Based Transactions EFT Regulations Tokenization PIN-Based Transactions Intra-Network PIN-Based

Blockchain Impact on Architecture & Security. Emanuele Galdi Rome, September 28 th #CWIN17

Blockchain Impact on Architecture & Security Emanuele Galdi Rome, September 28 th #CWIN17 The Blockchain is a lot like sex in high school: everyone is talking about it, nobody really knows how to do it,

Blockchain Impact on Architecture & Security Emanuele Galdi Rome, September 28 th #CWIN17 The Blockchain is a lot like sex in high school: everyone is talking about it, nobody really knows how to do it,

PaySys SEPA Newsletter November 2013

Topics of this issue: 1. SecuRe Pay: Be SuRe to hear more of it 2. Card Payments in the Netherlands: No innovation anymore? 3. Scope of the proposed IF-Regulation: Which scheme is in and which is out?

Topics of this issue: 1. SecuRe Pay: Be SuRe to hear more of it 2. Card Payments in the Netherlands: No innovation anymore? 3. Scope of the proposed IF-Regulation: Which scheme is in and which is out?

PSD2 and other European legal developments

PSD2 and other European legal developments 9th Conference on Payments and Securities Settlement Systems, Ohrid, 5-8 June 2016 Michiel van Doeveren and Rui Pimentel Overview EU legal framework covering

PSD2 and other European legal developments 9th Conference on Payments and Securities Settlement Systems, Ohrid, 5-8 June 2016 Michiel van Doeveren and Rui Pimentel Overview EU legal framework covering

Cash and Card Usage by the Public and Merchants

Cash and Card Usage by the Public and s by John Winchcombe December 2016 Cash Essentials www.cashessentials.org Cash and Card Usage by the Public and s Executive summary This paper reports on the cost

Cash and Card Usage by the Public and s by John Winchcombe December 2016 Cash Essentials www.cashessentials.org Cash and Card Usage by the Public and s Executive summary This paper reports on the cost

Banking Monitor - Edition 2. July Overview

Banking Monitor - Edition 2 July 2017 Overview Contents 01 Blockchain 02 Payments 03 Cognitive Technology The section talks about introduction of digital currencies such as bitcoin by financial institutions,

Banking Monitor - Edition 2 July 2017 Overview Contents 01 Blockchain 02 Payments 03 Cognitive Technology The section talks about introduction of digital currencies such as bitcoin by financial institutions,

Commerzbank 4.0 simple digital efficient Performance and strategy implementation on track

Performance and strategy implementation on track Goldman Sachs 22nd Annual European Financials Conference Disclaimer This presentation contains forward-looking statements. Forward-looking statements are

Performance and strategy implementation on track Goldman Sachs 22nd Annual European Financials Conference Disclaimer This presentation contains forward-looking statements. Forward-looking statements are

PSD2 and draft EBA RTS: a lot of issues remain unclear. Scott McInnes, Bird & Bird LLP. 3 May 2017

PSD2 and draft EBA RTS: a lot of issues remain unclear Scott McInnes, Bird & Bird LLP 3 May 2017 Brussels Partner Scott McInnes specialises in competition law, as well as the regulation of financial services

PSD2 and draft EBA RTS: a lot of issues remain unclear Scott McInnes, Bird & Bird LLP 3 May 2017 Brussels Partner Scott McInnes specialises in competition law, as well as the regulation of financial services

General blockchain landscape in Vietnam. Nicole Nguyen HCMC March 2018

General blockchain landscape in Vietnam Nicole Nguyen HCMC March 2018 Outline Background How BC is shaping in the world Perspective Challenges vs. Opportunities Blockchain basic Concept, components, features

General blockchain landscape in Vietnam Nicole Nguyen HCMC March 2018 Outline Background How BC is shaping in the world Perspective Challenges vs. Opportunities Blockchain basic Concept, components, features

Risk Assessment Questionnaire (RAQ) Summary of Results. Risk Assessment Questionnaire Summary of Results December 2017

Summary of Results. Risk Assessment Questionnaire Summary of Results December 2017") Risk Assessment Questionnaire Summary of Results December 2017 1 Contents Introduction 3 Summary of the main results 4 Banks questionnaire 8 1. Business model / strategy / profitability 8 2. Funding /

Risk Assessment Questionnaire Summary of Results December 2017 1 Contents Introduction 3 Summary of the main results 4 Banks questionnaire 8 1. Business model / strategy / profitability 8 2. Funding /

Digital Strategy

Digital Strategy 2018 2020 2 Digital Strategy About us, with gross premium of over EUR 16 billion, is the third- largest reinsurer in the world. We transact all lines of property & casualty and life &

Digital Strategy 2018 2020 2 Digital Strategy About us, with gross premium of over EUR 16 billion, is the third- largest reinsurer in the world. We transact all lines of property & casualty and life &

Brussels, XXX COM(2013) 547 /3 2013/0264 (COD) Proposal for a

547 /3 2013/0264 (COD) Proposal for a") EUROPEAN COMMISSION Brussels, XXX COM(2013) 547 /3 2013/0264 (COD) Proposal for a DIRECTIVE OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL on payment services in the internal market and amending Directives

EUROPEAN COMMISSION Brussels, XXX COM(2013) 547 /3 2013/0264 (COD) Proposal for a DIRECTIVE OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL on payment services in the internal market and amending Directives

FinTech and Financial Inclusion

B B B FinTech and Financial Inclusion Martin Čihák Advisor and Unit Chief, International Monetary Fund Regional Conference Financial Inclusion in Asia-Pacific: The Way Forward Cambodia, December 7 8, 2017

B B B FinTech and Financial Inclusion Martin Čihák Advisor and Unit Chief, International Monetary Fund Regional Conference Financial Inclusion in Asia-Pacific: The Way Forward Cambodia, December 7 8, 2017

S p e c i a l R e p o r t

S p e c i a l R e p o r t U.S. Economic Indicators Powered by This report is based upon information we consider reliable, but its accuracy and completeness cannot be guaranteed. Information provided is

S p e c i a l R e p o r t U.S. Economic Indicators Powered by This report is based upon information we consider reliable, but its accuracy and completeness cannot be guaranteed. Information provided is

Contents. For Corporates Payment Services Directive II (PSD2)

") For Corporates Payment Services Directive II (PSD2) Contents 2. Introduction 2. Key Changes 3. Key Roles: Who is Who? 4. What is a PISP? 5. What is an AISP? 6. Impacts and Considerations 6. The Benefits

For Corporates Payment Services Directive II (PSD2) Contents 2. Introduction 2. Key Changes 3. Key Roles: Who is Who? 4. What is a PISP? 5. What is an AISP? 6. Impacts and Considerations 6. The Benefits

Credit Card Conditions of use. Terms and Conditions

Credit Card Conditions of use Terms and Conditions Effective: 20 March 2014 This document does not contain all the terms of this agreement or all of the information we are required by law to give you before

Credit Card Conditions of use Terms and Conditions Effective: 20 March 2014 This document does not contain all the terms of this agreement or all of the information we are required by law to give you before

FinTech Opportunities and Challenges for securities companies

FinTech Opportunities and Challenges for securities companies 23 rd ASF AGM 2018 Lynn Kuo CIO and Executive Vice President Head of Innovation Technology Department CAPITAL Securities Corp. 23 rd ASF AGM

FinTech Opportunities and Challenges for securities companies 23 rd ASF AGM 2018 Lynn Kuo CIO and Executive Vice President Head of Innovation Technology Department CAPITAL Securities Corp. 23 rd ASF AGM

Consumer Payment Services Conditions

Consumer Payment Services Conditions 3247 EN Contents Consumer Payment Services Conditions This is a translation of the original Dutch text and is furnished for the customer s convenience only. No rights

Consumer Payment Services Conditions 3247 EN Contents Consumer Payment Services Conditions This is a translation of the original Dutch text and is furnished for the customer s convenience only. No rights

Payments POCKET GUIDE. in Your Pocket

Payments POCKET GUIDE in Your Pocket 1 Definitions 3D Secure An XML-based protocol that is designed to add an extra layer of security for online credit and debit card transactions. It has been adopted

Payments POCKET GUIDE in Your Pocket 1 Definitions 3D Secure An XML-based protocol that is designed to add an extra layer of security for online credit and debit card transactions. It has been adopted

How is Financial Technology Changing Regulation and Supervision

How is Financial Technology Changing Regulation and Supervision OCTOBER 24, 2018 Nobu Sugimoto Senior Financial Sector Expert Financial Supervision and Regulation Division Monetary & Capital Markets Department

How is Financial Technology Changing Regulation and Supervision OCTOBER 24, 2018 Nobu Sugimoto Senior Financial Sector Expert Financial Supervision and Regulation Division Monetary & Capital Markets Department

Country Crowdfunding Factsheet

Country Crowdfunding Factsheet Sweden Date: June 2018 ECN Country Factsheet - Sweden - June 2018 2 European Crowdfunding Network The European Crowdfunding Network AISBL (ECN) is the professional network

Country Crowdfunding Factsheet Sweden Date: June 2018 ECN Country Factsheet - Sweden - June 2018 2 European Crowdfunding Network The European Crowdfunding Network AISBL (ECN) is the professional network

Payment Services and Electronic Money Our Approach

DRAFT FOR CONSULTATION Payment Services and Electronic Money Our Approach The FCA s role under the Payment Services Regulations 2017 and the Electronic Money Regulations 2011 DRAFT April 2017 1 DRAFT FOR

DRAFT FOR CONSULTATION Payment Services and Electronic Money Our Approach The FCA s role under the Payment Services Regulations 2017 and the Electronic Money Regulations 2011 DRAFT April 2017 1 DRAFT FOR

Chapter 4 E-commerce Security and Payment Systems

Chapter 4 E-commerce Security and Payment Systems Copyright 2016 Pearson Education, Ltd. 4.5 E-COMMERCE PAYMENT SYSTEMS Copyright 2016 Pearson Education, Ltd. Slide 1-2 E-commerce Payment Systems In this

Chapter 4 E-commerce Security and Payment Systems Copyright 2016 Pearson Education, Ltd. 4.5 E-COMMERCE PAYMENT SYSTEMS Copyright 2016 Pearson Education, Ltd. Slide 1-2 E-commerce Payment Systems In this

Blockchain. Deepak Agarwal ICMA Conference Presenter

Blockchain Deepak Agarwal ICMA Conference Presenter Deepak Agarwal Plante Moran Plante Moran fast facts Agenda Blockchain overview Public sector initiatives Blockchain Overview What is blockchain? A blockchain

Blockchain Deepak Agarwal ICMA Conference Presenter Deepak Agarwal Plante Moran Plante Moran fast facts Agenda Blockchain overview Public sector initiatives Blockchain Overview What is blockchain? A blockchain

ACH Industry Update, Audit Weaknesses and Emerging Payment Trends

ACH Industry Update, Audit Weaknesses and Emerging Payment Trends Presented by Adrian Brown, AAP Director of Education The Payments Authority is the association for payments people. ACH CARD CHECK WIRE

ACH Industry Update, Audit Weaknesses and Emerging Payment Trends Presented by Adrian Brown, AAP Director of Education The Payments Authority is the association for payments people. ACH CARD CHECK WIRE

Business Vantage Visa Credit Card. Conditions of Use. Effective Date: 4 November 2016

Business Vantage Visa Credit Card Conditions of Use 1 Effective Date: 4 November 2016 Business Vantage Visa Conditions of Use Bank of Melbourne This document does not contain all the terms of this agreement

Business Vantage Visa Credit Card Conditions of Use 1 Effective Date: 4 November 2016 Business Vantage Visa Conditions of Use Bank of Melbourne This document does not contain all the terms of this agreement

Table of Contents. 1. Real Estate Market Opportunity in Global Real Estate World DLT Tech for Real Estate...2

ABSTRACT: This whitepaper provides a short description about RESTA s secure platform for overseas real estate investments, the Distributed Ledger Technology(DLT)for banks and real estate entities which

ABSTRACT: This whitepaper provides a short description about RESTA s secure platform for overseas real estate investments, the Distributed Ledger Technology(DLT)for banks and real estate entities which

Guidance for implementation of the revised Payment Services Directive. PSD2 guidance

Guidance for implementation of the revised Payment Services Directive PSD2 guidance About the EBF The European Banking Federation is the voice of the European banking sector, uniting 32 national banking

Guidance for implementation of the revised Payment Services Directive PSD2 guidance About the EBF The European Banking Federation is the voice of the European banking sector, uniting 32 national banking

Consumer Credit Cards. Conditions of Use. Effective as at 20 March 2013.

Consumer Credit Cards. Conditions of Use. Effective as at 20 March 2013. Your Credit Card Contract includes this Conditions of Use brochure, the letter which advises both your credit limit and other prescribed

Consumer Credit Cards. Conditions of Use. Effective as at 20 March 2013. Your Credit Card Contract includes this Conditions of Use brochure, the letter which advises both your credit limit and other prescribed

ICICI Group. Performance and Strategy. February 2016

ICICI Group Performance and Strategy February 2016 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

ICICI Group Performance and Strategy February 2016 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

HOW TO COMPARE CREDIT CARD PROCESSORS

HOW TO COMPARE CREDIT CARD PROCESSORS Credit card processing fees, transaction fees and statement fees vary a lot. The best credit card processor is not necessarily the one that offers you what appears

HOW TO COMPARE CREDIT CARD PROCESSORS Credit card processing fees, transaction fees and statement fees vary a lot. The best credit card processor is not necessarily the one that offers you what appears

Thinking Inside the Box: The UK FCA Sandbox, a Playground for Innovation

Debevoise In Depth Thinking Inside the Box: The UK FCA Sandbox, a Playground for Innovation March 6, 2018 The growing application of blockchain and other distributed ledger technologies to financial products,

Debevoise In Depth Thinking Inside the Box: The UK FCA Sandbox, a Playground for Innovation March 6, 2018 The growing application of blockchain and other distributed ledger technologies to financial products,

AML Regulatory Challenges Facing FinTechs

FinTech Regulatory Challenges and Collaborative Opportunities AML Regulatory Challenges Facing FinTechs Robert Scavone* McMillan LLP *With the generous assistance of Gerald Badali, McMillan LLP Overview

FinTech Regulatory Challenges and Collaborative Opportunities AML Regulatory Challenges Facing FinTechs Robert Scavone* McMillan LLP *With the generous assistance of Gerald Badali, McMillan LLP Overview

Payment Processing. A simple explanation of the entire credit card payment transaction process. We promise.

Payment Processing A simple explanation of the entire credit card payment transaction process. We promise. We admit it credit card transactions can be confusing. Sure, the initial transaction part when

Payment Processing A simple explanation of the entire credit card payment transaction process. We promise. We admit it credit card transactions can be confusing. Sure, the initial transaction part when

Singapore Airlines Westpac Platinum Credit Cards Conditions of Use

Singapore Airlines Westpac Platinum Credit Cards Conditions of Use 28 October 2016 Conditions of Use Your Credit Card Contract includes this Conditions of Use booklet, the letter which advises both your

Singapore Airlines Westpac Platinum Credit Cards Conditions of Use 28 October 2016 Conditions of Use Your Credit Card Contract includes this Conditions of Use booklet, the letter which advises both your

HSBC Expat Notice of Variation

HSBC Expat Notice of Variation Notice of Variation to the HSBC Expat Banking Terms of Business 1. Summary of main changes to the Terms 1. We have made changes to reflect the transfer of the business of

HSBC Expat Notice of Variation Notice of Variation to the HSBC Expat Banking Terms of Business 1. Summary of main changes to the Terms 1. We have made changes to reflect the transfer of the business of

CEO Jukka Ruuska 3 August Asiakastieto Group Plc Half Year Financial Report

CEO Jukka Ruuska 3 August 2017 Asiakastieto Group Plc Half Year Financial Report 1.1. 30.6.2017 Contents Asiakastieto Group in Brief Highlights Q2 / 2017 Service Development in Asiakastieto New Services

CEO Jukka Ruuska 3 August 2017 Asiakastieto Group Plc Half Year Financial Report 1.1. 30.6.2017 Contents Asiakastieto Group in Brief Highlights Q2 / 2017 Service Development in Asiakastieto New Services

Topic 2: Compare different types of payment card

Topic 2: Compare different types of payment card After completing this topic, you will be able to: define, understand the purpose of, and compare the features of debit and credit cards; define, understand

Topic 2: Compare different types of payment card After completing this topic, you will be able to: define, understand the purpose of, and compare the features of debit and credit cards; define, understand

FLAVORS OF FAST. Country Reports Germany

FLAVORS OF FAST Country Reports Germany Introduction Introduction The fifth edition of global fintech leader FIS faster payments 1 industry report, Flavors of Fast, demonstrates how quickly the global

FLAVORS OF FAST Country Reports Germany Introduction Introduction The fifth edition of global fintech leader FIS faster payments 1 industry report, Flavors of Fast, demonstrates how quickly the global

SIA: THE BOARD APPROVES THE 2016 FINANCIAL STATEMENTS GROWTH IN ECONOMIC RESULTS AND BUSINESS FIGURES

SIA: THE BOARD APPROVES THE 2016 FINANCIAL STATEMENTS GROWTH IN ECONOMIC RESULTS AND BUSINESS FIGURES Economicfinancial figures Dividend Business figures Total consolidated revenues: 468.2 million (+4.2%)

SIA: THE BOARD APPROVES THE 2016 FINANCIAL STATEMENTS GROWTH IN ECONOMIC RESULTS AND BUSINESS FIGURES Economicfinancial figures Dividend Business figures Total consolidated revenues: 468.2 million (+4.2%)

Altitude Business credit cards.

Altitude Business credit cards. Conditions of Use. Effective as at 4 April 2018. Your Credit Card Contract includes this Conditions of Use brochure, the letter which advises your credit limit and the precontractual

Altitude Business credit cards. Conditions of Use. Effective as at 4 April 2018. Your Credit Card Contract includes this Conditions of Use brochure, the letter which advises your credit limit and the precontractual

Mastercard Incorporated (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

Credit Card Payment Trends and Legislation: What s the Impact for Associations? Tuesday, December 8, :00 3:00pm (Eastern)

") Credit Card Payment Trends and Legislation: What s the Impact for Associations? Tuesday, December 8, 2009 2:00 3:00pm (Eastern) Hosted by ASAE Business Services, Inc. and Chase Paymentech December 7, 2009

Credit Card Payment Trends and Legislation: What s the Impact for Associations? Tuesday, December 8, 2009 2:00 3:00pm (Eastern) Hosted by ASAE Business Services, Inc. and Chase Paymentech December 7, 2009

- Public Bank ATM/CDM RM FPX (Financial Process Exchange) RM MobiltyOne * RM EPay * RM MPay Authorised Agent * RM1.

RM MobiltyOne * RM EPay * RM MPay Authorised Agent * RM1.") 1. What is this product about? MPay Balance Account is an account that you can open online, anytime and anywhere without going into a physical office, giving you immediate usage of the account. Once you

1. What is this product about? MPay Balance Account is an account that you can open online, anytime and anywhere without going into a physical office, giving you immediate usage of the account. Once you

Technological Innovations: Challenges for Insurance Supervisors

Technological Innovations: Challenges for Insurance Supervisors 2016 IAIS Annual Conference Panel on Technological Innovation: Insurance Supervision and the Business of Insurance Asunción, Paraguay November

Technological Innovations: Challenges for Insurance Supervisors 2016 IAIS Annual Conference Panel on Technological Innovation: Insurance Supervision and the Business of Insurance Asunción, Paraguay November

Chapter 2 Definition of FinTech and Description of the FinTech Industry

Chapter 2 Definition of FinTech and Description of the FinTech Industry Currently there is not a universally accepted definition of the term FinTech. The following section provides a brief survey of its

Chapter 2 Definition of FinTech and Description of the FinTech Industry Currently there is not a universally accepted definition of the term FinTech. The following section provides a brief survey of its

AUTHORISATION OF FINANCIAL INSTITUTIONS... 3 LICENCING... 3 CRITERIA APPLIED FOR THE GRANT OF A LICENCE... 5

Mdina Malta 1 Contents AUTHORISATION OF FINANCIAL INSTITUTIONS... 3 LICENCING... 3 CRITERIA APPLIED FOR THE GRANT OF A LICENCE... 5 BRANCHES AND AGENCIES OF FINANCIAL INSTITUTIONS... 6 BRANCHES OF OVERSEAS

Mdina Malta 1 Contents AUTHORISATION OF FINANCIAL INSTITUTIONS... 3 LICENCING... 3 CRITERIA APPLIED FOR THE GRANT OF A LICENCE... 5 BRANCHES AND AGENCIES OF FINANCIAL INSTITUTIONS... 6 BRANCHES OF OVERSEAS

Future Trends 2017: The Shift Gains Momentum

Future Trends 2017: The Shift Gains Momentum IASA Spring Meeting April 2017 1 People Market Trend: Pressure on insurance industry driving new expectations, innovations and competition Changing customer

Future Trends 2017: The Shift Gains Momentum IASA Spring Meeting April 2017 1 People Market Trend: Pressure on insurance industry driving new expectations, innovations and competition Changing customer