Risk Assessment Questionnaire (RAQ) Summary of Results. Risk Assessment Questionnaire Summary of Results December 2017

|

|

|

- Alexander Townsend

- 5 years ago

- Views:

Transcription

1 Risk Assessment Questionnaire Summary of Results December

2 Contents Introduction 3 Summary of the main results 4 Banks questionnaire 8 1. Business model / strategy / profitability 8 2. Funding / liquidity Asset volume trends Asset quality Conduct, reputation and operational risk FinTech General open question 30 Market analysts questionnaire Business model / strategy / profitability Funding / liquidity Asset volume trends Asset quality 40 Appendix: Risk Assessment Questionnaire for banks 42 Appendix: Risk Assessment Questionnaire for market analysts 43 2

3 Introduction The EBA conducts semi-annual Risk Assessment Questionnaires (RAQs) among banks and market analysts. This booklet presents a summary of responses to the RAQs carried out between September and October banks and 21 market analysts submitted the answers. The RAQ results are published together with the EBA s quarterly Risk Dashboard. They are also one of the sources of the EBA s annual Risk Assessment Report, as published on 24 November 2017 The results are presented in an aggregated form. The charts are numbered, with numbers corresponding to the questions in the distributed questionnaires, which can be found in the Appendix. Results for the same question from former questionnaires may be presented where deemed relevant. For questions for which only one answer was permitted, any potential difference between the sum of shown responses and 100% is due to respondents answering either n/a or no opinion. Should you wish to provide your feedback and/or comments on this booklet, please do not hesitate to do so by contacting risk.assessment@eba.europa.eu. 3

4 Summary of the main results Against the backdrop of benign market conditions, the results of the EBA s RAQs show that banks profitability remains a challenge, even though a slight improvement is expected for the near future. Volume growth is anticipated in specific portfolios like SME and retail lending. On the funding side, banks are expected to attain more instruments eligible for MREL going forward, even though the uncertainty on the specific MREL requirements is considered as a constraint to their issuance. Cyber risk and data security are considered as the main drivers for an increase in operational risk. They are also assumed to be the main factors that might negatively influence market sentiment, along with the uncertainties about the UK s decision to leave the EU. Business model / strategy / profitability Most of the banks expect a change in their assumed level of Cost of Equity. 65% of the banks estimate their CoE between 8% and 10% (up from about 60% in June 2017 and 50% in December 2016), while only less than 8% estimate their CoE at a level below 8% (down from more than 10% in June 2017 and more than 15% in December 2016). The share of banks that agree that their current earnings are covering the CoE remains unchanged at about 50%. Moreover, half of the banks replied that they can operate on a longer-term basis with a Return on Equity (RoE) ranging between 10% and 12% (down from 60% in June 2017). At the same time, the number of banks that are able to operate with a RoE below 10% increased from 20% (June 2017) to now 30%. (Questions 2, 6 and 7 for banks). On a similar note, about 75% of banks agree and somewhat agree that their profitability will increase in the next six to twelve months, down from 80% in June. Similarly, more than 80% ( agree and somewhat agree ) of the market analysts assume that overall profitability will improve, which is unchanged from June Banks consider net fees and commission income as the main driver for increasing profitability (about 90% agree and somewhat agree ), followed by further costs reduction (about 80% agree and somewhat agree ). Net interest income is considered as the third most important driver (about 60% agree and somewhat agree ). (Questions 3 and 4 for banks and Question 1 for market analysts) Geopolitical risks remain a key risk according to market analysts (agreement of 60% down from more than 65% in June 2017). The uncertainties about the UK s decision to leave the EU and monetary policy trends rank high in their opinion (agreement of about 30% for each driver), while a smaller number of market analysts see litigation risks as drivers for negative market sentiment (down from almost 70% in December 2016 and 30% in June 2017 to less than 25% in December this year). The general perception on the risks from elections and referendums decreased with respect to June, as drivers such as IT/cyber risks or the risk of asset price bubbles (both at 24%). (Question 3 for market analysts) More than half of market analysts expect material negative implications to EU banks business, should ongoing negotiations on the terms of the UK s withdrawal from the EU end in an inconclusive or disorderly fashion. The answer to this question for banks shows that only 10% of them saw implications for their own business, suggesting a degree of cautious thinking, as a large number of them (almost 4

5 40%) expects the continuity of financial contracts between parties from the EU 27 and the UK to be a source of concern. (Question 8 and 9 for banks and Question 4 for market analysts) Funding / liquidity More than 60% of banks expect a steepening yield curve to positively impact their bank s earnings in the next 6 12 months, while in June around 30% of them more broadly stated that they would see a material impact (positive or negative). (Question 10 for banks) Less market analysts expect that banks will be able to issue AT1 instruments during the rest of 2017 (about 60% from almost 70% in June) whereas almost 70% of them expect that banks will be able to issue T2 instruments (up from less than 60% in June). 60% of them expect that banks will be able to issue MREL/TLAC eligible debt instruments. (Question 7 for market analysts) The majority of banks intend to attain more instruments eligible for MREL (agreement of almost 55%; this debt class was newly added in this version of the RAQ), while a smaller number intends to rely on retail deposits (35% from 55% in June this year). Only 15% of the banks plan to issue senior unsecured funding (45% in June). Also less market analysts expect banks to issue more senior unsecured instrument (down to 40% from almost 60% in June), while 86% of them expect banks to attain more instruments eligible for MREL. Banks believe that the main constraints to issue subordinated instruments eligible for MREL are the uncertainty on the specific MREL requirements, namely the amounts (60% of banks) and the eligibility of the instruments (55%). Neither banks nor market analysts assume that more central bank funding will be attained (agreement of 0%, down from almost 20% for banks and 45% for market analysts in June 2016). (Question 12 and 13 for banks and Question 8 for market analysts) Asset volume trends and asset quality In line with June 2017 and December 2016, the majority of the banks plan to increase their volumes of SME financing (more than 80%), while a smaller number of banks says that they will increase their consumer credit and residential mortgage exposures. Trading is increasingly considered as a portfolio for which volumes are expected to increase (more than 10% from 3% in June), along with structured finance (45% with respect to 30% in June). Market analysts show a similar opinion on the portfolios for which an increase is expected (agreement of about 95% for SME loans) even though they also see an increase in corporate loans (for about 90% of them). (Question 15a for banks and Question 9a for market analysts) The portfolio for which the biggest share of banks plan a decrease in volumes, in line with June 2017, is Commercial Real Estate (CRE), including all types of real estate developments (agreement of more than almost 30%, slightly up since June). Compared to June this year, also sovereign and institutions, along with asset finance (shipping, aircrafts etc.), rank high in the portfolios for which a decrease in volume is expected (both at almost 30% from 20%). Less market analysts consider CRE as a portfolio which will decrease (agreement of 50%, down from 70% in June). Finally, about 90% ( agree and somewhat agree ) of the market analysts expect more asset sales in specific loan portfolios (e.g. CRE) and a lower number (less than 80%) in specific geographies. (Question 15b for banks and Questions 9b and 11 for market analysts) 5

6 Banks assume that nearly the same portfolios which they plan to increase in volumes will improve in terms of asset quality (namely SME, for more than 50% of them but also corporate loans with an increasing trend with respect to June). A larger number of banks expect trading to improve in terms of asset quality in the next twelve months (almost 20% agreement from 5% in June), which might be the reason for the expected increase in volume reported for this portfolio (see answer to Question 15a for banks). Market analysts expectations are relatively similar: improvements in asset quality are mainly expected for SME financing (increasing to 75% from 70% in June) and for corporate loans (75% from 50% in June). (Question 16a for banks and Question 12a for market analysts) A deterioration in asset quality is mainly assumed for asset finance, even though for a lower portion of respondents (agreement of about 13% by banks, down from 20% in June and about 40% in December 2016), whereas for market analysts the agreement is of almost 60%, up from 50% in June. A higher number of banks expect an increase in the level of impairments in the next 12 to 18 months (almost 30% from 20% in June), while more than 40% expect provisions to remain at roughly the same level (down from 55% in June). (Questions 16b and 18 for banks and Questions 12b for market analysts) Banks consider lengthy and expensive judiciary processes to resolve insolvency and to enforce the repossession of collaterals as one of the main impediments to resolve non-performing loans (NPL) (agreement of about 55%, slightly down compared to June 2017). The lack or scarce liquidity of a market for transactions in NPLs and / or collaterals is considered another important impediment (agreement of about 55% up from 50% in June). (Question 19 for banks) Conduct / reputation / operational risk More than 55% of the banks expect an increase in operational risks in their institution (up from less than 45% in June). The main drivers identified by the banks are cyber risk and data security (around 40% of banks) and compliance with regulatory initiatives (25%). (Question 22 for banks) FinTech In this issue of the RAQ banks were also asked to give feedback on how their business is affected by FinTech related trends. The majority of banks see FinTech companies as a threat to revenues in business lines such as payments and settlements (60%) and retail banking (almost 50%). However, almost 40% of banks instead consider technology as an opportunity to increase revenues in the commercial banking line. Banks mostly reported to be using biometric features (as alternative to conventional authentication through the username/password/token systems) and digital wallet solutions for mobile payments using near-field communication (NFC). (Question 23 and 24 for banks) When asked what their current relation with FinTech companies and emerging technologies/products is, more than 90% of banks responded to be forming commercial partnerships (e.g. joint ventures) with existing Fintech companies to offer new products/services. 100% of them believe that the main driver for having a relation with FinTech companies and/or products/services is the increase in revenues. (Questions 25 and 26 for banks) 6

7 General open questions In the open question about sources of risks and vulnerabilities which are expected to increase further in the next six to twelve months, banks mainly refer to regulatory risks and other types of risks (such as shadow banking, Fintech and cyber risk). Market analysts mainly refer to the introduction of new accounting standards. 7

8 Banks questionnaire 1. Business model / strategy / profitability Question 1: December 2017 results Question 1: Comparison with former results 8

9 Question 2 (only agree as possible answer) Question 3 and 4: December 2017 results 9

10 Question 3: Comparison with former results Question 4: Comparison with former results 10

11")

11 Question 5 (only agree as possible answer) Question 6 (only agree as possible answer) 11

12 Question 7 (only agree as possible answer) Question 8: December 2017 results Question 9: December 2017 results 12

13 Question 10: December 2017 results 13

14 2. Funding / liquidity Question 11: December 2017 results Question 11: Comparison with former results 14

15 Question 12 (only agree as possible answer) Option b) was newly added to the questionnaire in December 2017 and for this reason it does not show any comparative data for former periods. Question 13: December 2017 results 15

16 3. Asset volume trends Question 14: December 2017 results Question 14: Comparison with former results 16

17 17

18 Question 15: December 2017 results 18

19 Question 15a: Comparison with former results 19

20 Question 15b: Comparison with former results 20

21 4. Asset quality Question 16: December 2017 results 21

22 Question 16a: Comparison with former results 22

")

23 Question 16b: Comparison with former results Question 17 (only agree as possible answer) 23

24")

24 Question 18 (only agree as possible answer) Question 19 (only agree as possible answer) 24

25 5. Conduct, reputation and operational risk Question 20 (only agree as possible answer) Question 21(only agree as possible answer) 25

26 Question 22: December 2017 results Question 22: Comparison with former results 26

27 6. FinTech Question 23: December 2017 results 27

28 Question 24: December 2017 results 28

29 Question 25: December 2017 results Question 26: December 2017 results 29

30 7. General open question Looking at the EU banking sector, you expect other sources of risk or vulnerabilities to increase further in the next 6-12 months. Please indicate possible additional sources of risks and vulnerabilities: 30

31 Market analysts questionnaire 1. Business model / strategy / profitability Question 1: December 2017 results Question 1: Comparison with former results 31

Questions without comparative data for former")

32 Question 2 (only agree as possible answer) Question 3 (only agree as possible answer) Questions without comparative data for former periods were newly added to the questionnaire in June The possible answer 3.o) was slightly reworded with respect to June this year. 32

33")

33 Question 4: December 2017 results Question 5: December 2017 results Question 6 (only agree as possible answer) 33

34 2. Funding / liquidity Question 7: December 2017 results Question 7: Comparison with former results 34

35 Question 8 (only agree as possible answer) Option b) was newly added to the questionnaire in December 2017 and for this reason it does not show any comparative data for former periods. 35

36 3. Asset volume trends Question 9: December 2017 results 36

37 Question 9a: Comparison with former results Question 9b: Comparison with former results 37

38 Question 10 (only agree as possible answer) Question 11: December 2017 results 38

39 Question 11: Comparison with former results 39

40 4. Asset quality Question 12: December 2017 results 40

41 Question 12a: Comparison with former results Question 12b: Comparison with former results 41

42 Appendix: Risk Assessment Questionnaire for banks [added on the following pages] 42

43 Risk Assessment Questionnaire for Banks Autumn 2017 Fields marked with * are mandatory. Respondent information * First Name * Last Name * Position * Division * Banking institution * address Business model/strategy/profitability For the purposes of this survey, business model relates to the business mix underpinning the capacity of a bank to preserve and grow sustainable and predictable risk-adjusted earnings in markets and sectors in which it maintains a material presence. In view of this: 1

44 * Q1 You envisage making material changes to your bank s business model going forward. Agree Disagree N/A If you agree: Agree Disagree N /A * a. you expect material changes to your bank s business model arising from a potential M&A transaction * b. you expect material changes to your bank s business model due to increasing competition arising from banking disintermediation (e.g. FinTech, shadow banking, infrastructure finance by insurance companies) * c. you expect material structural changes in your group due to regulatory requirements on resolvability If you agree with c., this results from the following regulatory changes: Agree Disagree N /A * i. Regulations on capital * ii. Regulations on liquidity and funding * iii. Regulations on resolution/bail-in * iv. Regulations and policies on banking structures (activity ring-fencing, etc.) * Q2 Your bank can operate on a longer-term basis with a return on equity (ROE): a. Below 10%. b. Between 10% and 12%. c. Between 12% and 14% d. Above 14%. * Q3 You expect an overall increase in your bank's profitability in the 6-12 next months: Agree Somewhat Agree Somewhat Disagree Disagree N/A 2

45 Q4 You primarily target this area for increasing profitability in your bank in the next months: Agree Somewhat Agree Somewhat Disagree Disagree N /A * a. Net interest income * b. Net Fees and Commissions income * c. Other operating income * d. Operating expenses / costs reduction * e. Impairments * f. Other * Q5 You are reducing operating expenses / costs through (please do not agree with more than 3 options): between 1 and 3 choices a. Overhead reduction and staff costs reduction b. Outsourcing c. Off-shoring or near-shoring d. Cutting of non-profitable units e. Increasing automatisation and digitalisation f. Other * Q6 Your current earnings are covering the cost of equity: Agree Disagree N/A * Q7 You estimate COE at: a. Below 8%. b. Between 8% and 10%. c. Between 10% and 12%. d. Above 12%. * Q8 You expect material negative implications to your bank s business should ongoing negotiations on the terms of the UK s withdrawal from the EU end inconclusive or in a disorderly fashion. Agree Disagree N/A 3

46 * Q9 The continuity of financial contracts your bank has entered into between parties from the EU 27 and the UK is an issue of concern in case of a disorderly or inconclusive conclusion of UK EU withdrawal negotiations. Agree Disagree N/A * Q10 Looking at your bank, you expect an observed steepening yield curve to positively impact your bank s earnings in the next 6 12 months. Agree Disagree N/A Funding/liquidity * Q11 Do you plan to issue CET1 instruments in the next 12 months? Agree Disagree * Q12 You intend to attain more ( please do not agree with more than 2 options): between 1 and 2 choices a. Senior unsecured funding. b. Instruments eligible for MREL. c. Subordinated debt. d. Secured funding (covered bonds). e. Securitisation. f. Deposits (from wholesale clients). g. Deposits (from retail clients). h. Central Bank funding. i. Short-term interbank funding. * Q13 Which are the main constraints to issue subordinated instruments eligible for MREL (please do not agree with more than 2 options)? between 1 and 2 choices a. Pricing (the instruments yields are too high). b. No sufficient investor demand (e.g. these instruments are not attractive in risk-return considerations). c. No sufficient investor demand (due to regulatory and supervisory uncertainty). d. Uncertainty on required MREL amounts. e. Uncertainty on eligibility of instruments for MREL. Asset volume trends 4

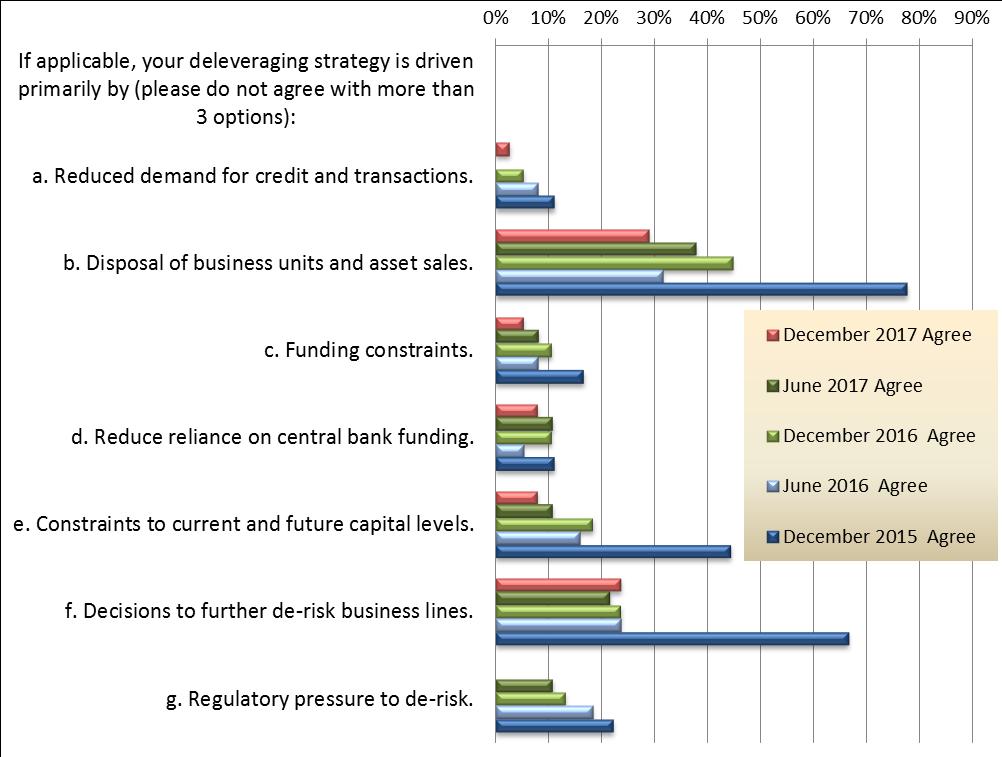

47 * Q14 Further asset deleverage is an element of your strategy. Agree Disagree N/A * If applicable, your deleveraging strategy is driven primarily by (please do not agree with more than 3 options): between 1 and 3 choices a. Reduced demand for credit and transactions. b. Disposal of business units and asset sales. c. Funding constraints. d. Reduce reliance on central bank funding. e. Constraints to current and future capital levels. f. Decisions to further de-risk business lines. g. Regulatory pressure to de-risk. Q15 Which portfolios do you plan to increase/decrease in volume during the next 12 months? Increase Decrease N /A * a. Commercial Real Estate (including all types of real estate developments) * b. SME * c. Residential Mortgage * d. Consumer Credit * e. Corporate * f. Trading (i.e. financial assets at Fair Value through Profit and Loss) * g. Structured Finance * h. Sovereign and institutions * i. Project Finance * j. Asset Finance (Shipping, Aircrafts etc.) * k. Other Asset composition & quality 5

48 Q16 Which portfolios do you expect to improve/deteriorate in asset quality in the next 12 months? Improve Deteriorate N /A * a. Commercial Real Estate (including all types of real estate developments) * b. SME * c. Residential Mortgage * d. Consumer Credit * e. Corporate * f. Trading (i.e. financial assets at Fair Value through Profit and Loss) * g. Structured Finance * h. Sovereign and institutions * i. Project Finance * j. Asset Finance (Shipping, Aircrafts etc.) * k. Other * Q17 Does your bank have significant exposure in portfolios of car loans and credit card finance? a. Agree b. Disagree c. N/A * If you agree: You expect increasing risk levels in these portfolios in the next 12 months. Agree Disagree N/A * Q18 Based on your view on future trends in credit quality and impairment levels for your bank, impairment provisions over the time horizon of the next months: a. Will increase. b. Will remain at roughly the same level. c. Will decrease. 6

49 * Q19 What are the impediments to resolve non-performing loans (please do not agree with more than 3 options): between 1 and 3 choices a. Lack of financial resources b. Lack of qualified human resources c. Tax disincentives to provision against and write off NPLs d. Lengthy and expensive judiciary process to resolve insolvency and enforce on collateral e. Lack of out-of-court tools for settlement of minor claims f. Lack of a market for NPLs/collaterals g. Lack of public or industry-wide defeasance structure (bad bank) (additional option which seems to be missing) h. Other i. There is no impediment Conduct, Reputation and Operational risk * Q20 Since the end of your Financial Year 2007/8, your firm has paid out in the form of compensation, redress, litigation and similar payments [converted to EUR] an aggregate amount of: a. Less than EUR 10m. b. Between EUR 10m and EUR 50m. c. Between EUR 50m and 100m. d. Between EUR 100m and EUR 500m. e. Between EUR 500m and EUR 1bn. f. More than EUR 1bn. * Q21 Looking at your bank, you expect litigation costs to be heightened/elevated in the next 6-12 months. Agree Disagree N/A * Q22 You see an increase in operational risk in your bank. Agree Disagree N/A 7

50 * If applicable, the main driver for increasing operational risk is (please do not agree with more than 3 options): between 1 and 3 choices a. Cyber risk and data security b. IT failures c. Outsourcing d. Regulatory initiatives e. Conduct and legal risk f. Geopolitical risk g. Organisational change h. Money laundering, terrorist financing and sanctions non-compliance i. Fraud j. other FinTech Q23 How do you see FinTech companies affecting the current business model of your bank (in the following business lines)? Please select the most relevant answer for each business line. Opportunity Threat to Opportunity Threat to No impact to increase decrease to decrease increase / not revenues revenues costs costs relevant * a. Retail banking * b. Commercial banking * c. Corporate finance * d. Trading and sales * e. Payment and settlement * f. Agency services * g. Asset management * h. Retail brokerage 8

51 Please note: For the purposes this questionnaire FinTech is defined as Technologically enabled financial innovation that could result in new business models, applications, processes, or products with an associated material effect on financial markets and institutions and the provision of financial services (Financial Stability Board, Standing Committee on Assessment of Vulnerabilities, FinTech: Describing the Landscape and Framework for Analysis, 16 March 2016) For definitions of business lines please refer to Table 2 in Article 317 of Regulation (EU) No 575/

52 Q24 What is the level of involvement of your institution in the following FinTech related activities? Pilot Commercial testing Under Under No use / with development discussion activity launched consumers * a. Use of biometric authentication for customer identification purposes (use biometric features as alternative to conventional authentication through the username/password/token systems). * b. Use of robo-advisors for investment advice. * c. Use of big data and algorithms for credit scoring. * d. Use of DLT (distributed ledger technology) in smart contracts for trade finance. * e. Digital wallet solutions for mobile payments using NFC (near-field communication). * f. Use of DLT (distributed ledger technology) for digital identity (through blockchain based system, customers can control their own identity and share attributes with others by means of an explicit user consent). * g. Use of cloud computing for material activities. 11

53 Q25 What is your institution s current relation with FinTech companies and emerging technologies /products? Agree Disagree * a. You form commercial partnerships (e.g. joint ventures) with existing Fintech companies to offer new products/services. * b. You acquire existing Fintech companies to offer new products/services. * c. You invest in Fintech companies (e.g. venture capital). * d. You develop own products/services in-house using new technologies without cooperating with FinTech companies. * e. You participate in non-commercial partnerships with FinTech companies (research, share knowledge e.g. through FinTech incubators/accelerators). * f. You set-up/sponsor FinTech incubators/accelerators. * g. You currently do not have any ongoing relation with FinTech companies. * h. You plan to have a relation with FinTech companies in the future. Q26 What are the main drivers for having a relation with FinTech companies and/or products /services? Agree Disagree N /A * a. Maintain existing customers. * b. Attract new customers. * c. Increase revenues. * d. Decrease costs. * e. Reduce future competition pressure. * f. Follow market trend (e.g. from a marketing and franchise perspective). General issues Looking at the EU banking sector, you expect other sources of risk or vulnerabilities to increase further in the next 6-12 months. Please indicate possible additional sources of risks and vulnerabilities. 12

54 Appendix: Risk Assessment Questionnaire for market analysts [added on the following pages] 43

55 Risk Assessment Questionnaire for Market Analysts Autumn 2017 Fields marked with * are mandatory. Respondent information * First Name * Last Name * Position * Division * Company * adress Please select your choice for every box. Your response should reflect the degree of agreement to the statement made. A. Business model/strategy/profitability 1

56 Q1 Short term earnings expectations for banks are: Agree Somewhat agree Somewhat disagree Disagree N /A * a) Overall profitability will improve * b) Overall cost efficiency will improve * c) Total revenues will increase * d) Net interest margin will increase * e) Provisions/Impairments will increase * Q2 The current market sentiment is positively influenced by the following factors (please do not agree with more than 3 options): between 1 and 3 choices a) Adjustments in business models and strategies with expectations of effective delivery b) Improved risk metrics for banks (capital, funding, liquidity, asset quality) and positive impact of new regulatory requirements. c) Stronger earnings d) Changing governance and risk culture (incl. lower risk appetite) e) Improved market sentiment due to regulatory and policy steps (TLTRO, QE, ESM, banking union, etc.) adjusting downward tail risk. f) regulatory easing through competition between countries / regions? g) Expectation of increasing benchmark interest rates h) More transparency and visibility in banks financial disclosures, such as Pillar 3 2

57 * Q3 The current market sentiment is negatively influenced by the following factors (please do not agree with more than 4 options): between 1 and 4 choices a) Monetary policy divergence between the EU and other countries b) Monetary policy trends in the EU (incl. deflation) c) Geopolitical risks (e.g. risks from war, terrorism etc. that have impact on other countries) d) Emerging market risks (e.g. fast decrease in asset quality, higher volatility of asset and FX markets in emerging countries) e) IT/cyber risks f) Litigation risks of banks g) Decreasing market liquidity h) Risks of increasing volatility, e.g. in FX and financial markets i) Asset price bubble(s) j) Re-emergence of the Eurozone crisis k) Regulatory and supervisory uncertainty: risk weights (for credit, market and operationl risks, TRIM and similar effects) l) Regulatory uncertainty: BRRD / MREL / TLAC m) regulatory easing through competition between countries / regions? n) Commodity and energy prices / markets o) Political uncertainty in the EU (elections and referendums on EU membership, regional independence etc.) p) Political uncertainty outside the EU (elections, political instability, conflicts or standstill in emerging and developed countries) q) Uncertainties about the UK s decision to leave the EU * Q4 You expect material negative implications to EU bank s business should ongoing negotiations on the terms of the UK s withdrawal from the EU end inconclusive or in a disorderly fashion. Agree Disagree N/A * Q5 The continuity of financial contracts between banks and / or other parties from the EU 27 and the UK is an issue of concern in case of a disorderly or inconclusive conclusion of UK EU withdrawal negotiations. Agree Disagree N/A * Q6 Looking at the EU banking sector, you expect heightened litigation costs in the next 6-12 months: Agree Disagree N/A B. Funding/liquidity 3

58 Q7 Do you expect that banks will be able to issue subordinated debt instruments during the rest of this year? Agree Somewhat agree Somewhat disagree Disagree N /A * a) Banks will be able to issue BRRD / MREL / TLAC eligible debt instruments * b) Banks will be able to issue AT1 instruments * c) Banks will be able to issue T2 instruments If you agree or somewhat agree with above: Do you expect increasing costs for such issuances compared to last year? Agree Somewhat agree Somewhat disagree Disagree N /A * a) for BRRD / MREL / TLAC eligible debt instruments * b) for AT1 instruments * c) for T2 instruments * Q8 You expect banks to attain more ( please do not agree with more than 2 options): between 1 and 2 choices a) Senior unsecured funding b) Instruments eligible for MREL. c) Subordinated debt d) Secured funding (e.g. covered bonds) e) Securitisation f) Deposits (from wholesale clients) g) Deposits (from retail clients) h) Central Bank funding i) Short-term interbank funding. C. Asset composition & quality 4

59 Q9 Portfolios you expect to increase/decrease in volumes (on a net basis): Increase * a) Commercial Real Estate (including all types of real estate developments) * b) SME Decrease N /A * c) Residential Mortgage * d) Consumer Credit * e) Corporate * f) Trading (i.e. financial assets at Fair Value through Profit and Loss) * g) Structured Finance * h) Sovereign and institutions * i) Project Finance * j) Asset Finance (Shipping, Aircrafts etc.) * k) Other * Q10 Asset reduction (in a deleveraging setting) is mostly the consequence of (please do not agree with more than 2 options): between 1 and 2 choices a) Reduced demand for credit and transactions b) Funding constraints c) Constraints to current and future capital levels d) Regulatory pressure to de-risk e) Other Q11 You expect more asset sales initiated by EU banks in the next 12 months: Agree Somewhat Agree Somewhat Disagree Disagree N /A * a) Specific loan portfolios (e.g. CRE) * b) Specific geographies * c) Across the board 5

60 Q12 For which sectors do you expect an improvement/deterioration in asset quality in the following 12 months? Improvement Deterioration N /A * a) Commercial Real Estate (including all types of real estate developments) * b) SME * c) Residential Mortgage * d) Consumer Credit * e) Corporate * f) Trading (i.e. financial assets at Fair Value through Profit and Loss) * g) Structured Finance * h) Sovereign and institutions * i) Project Finance * j) Asset Finance (Shipping, Aircrafts etc.) * k) Other Q13 Looking at the EU banking sector, you expect other sources of risk or vulnerabilities to increase further in the next 6-12 months. Please indicate possible additional sources of risks and vulnerabilities. 6

207 382 1771/2 E-mail: info@eba.europa.eu http://www.eba.europa.eu 44")

61 EUROPEAN BANKING AUTHORITY Floor 46, One Canada Square London E14 5AA Tel: +44 (0) Fax: +44 (0) /

Risk Assessment Questionnaire (RAQ) Summary of Results. Risk Assessment Questionnaire Summary of Results July 2018

Summary of Results. Risk Assessment Questionnaire Summary of Results July 2018") Risk Assessment Questionnaire Summary of Results July 2018 1 Contents Introduction 3 Summary of the main results 4 Banks questionnaire 8 1. Business model / strategy / profitability 8 2. Funding / liquidity

Risk Assessment Questionnaire Summary of Results July 2018 1 Contents Introduction 3 Summary of the main results 4 Banks questionnaire 8 1. Business model / strategy / profitability 8 2. Funding / liquidity

Risk Assessment Questionnaire (RAQ) Summary of the results. Risk Assessment Questionnaire Summary of the Results December 2018

Summary of the results. Risk Assessment Questionnaire Summary of the Results December 2018") Risk Assessment Questionnaire Summary of the Results December 2018 1 Contents Introduction 3 Summary of the main results 4 Banks questionnaire 8 1. Business model / strategy / profitability 8 2. Funding

Risk Assessment Questionnaire Summary of the Results December 2018 1 Contents Introduction 3 Summary of the main results 4 Banks questionnaire 8 1. Business model / strategy / profitability 8 2. Funding

2018 EU-WIDE TRANSPARENCY EXERCISE AND RISK ASSESSMENT REPORT

2018 EU-WIDE TRANSPARENCY EXERCISE AND RISK ASSESSMENT REPORT Mario Quagliariello Director of Economic Analysis and Statistics Background Briefing with analysts and journalists 14 December 2018 Outline

2018 EU-WIDE TRANSPARENCY EXERCISE AND RISK ASSESSMENT REPORT Mario Quagliariello Director of Economic Analysis and Statistics Background Briefing with analysts and journalists 14 December 2018 Outline

RISK DASHBOARD DATA AS OF Q3 2017

RI DASHBOARD DA AS OF Q3 2017 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6 Total

RI DASHBOARD DA AS OF Q3 2017 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6 Total

Economic and monetary. developments. The results of the euro area bank lending survey for the second quarter of 2014

Economic and monetary Monetary and financial Box 2 The results of the euro area bank lending survey for the second quarter of 214 This box summarises the main results of the euro area bank lending survey

Economic and monetary Monetary and financial Box 2 The results of the euro area bank lending survey for the second quarter of 214 This box summarises the main results of the euro area bank lending survey

RISK DASHBOARD DATA AS OF Q3 2016

RI DASHBOARD DA AS OF Q3 2016 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6 Total

RI DASHBOARD DA AS OF Q3 2016 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6 Total

RISK ASSESSMENT OF THE EUROPEAN BANKING SYSTEM NOVEMBER 2017

RISK ASSESSMENT OF THE EUROPEAN BANKING SYSTEM NOVEMBER 2017 Europe Direct is a service to help you find answers to your questions about the European Union Freephone number (*): 00 800 6 7 8 9 10 11 (*)

RISK ASSESSMENT OF THE EUROPEAN BANKING SYSTEM NOVEMBER 2017 Europe Direct is a service to help you find answers to your questions about the European Union Freephone number (*): 00 800 6 7 8 9 10 11 (*)

RISK DASHBOARD DATA AS OF Q2 2017

RI DASHBOARD DA AS OF Q2 2017 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6 Total

RI DASHBOARD DA AS OF Q2 2017 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6 Total

RISK DASHBOARD DATA AS OF Q4 2015

RISK DASHBOARD DATA AS OF Q4 20 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6 Total

RISK DASHBOARD DATA AS OF Q4 20 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6 Total

The euro area bank lending survey. Fourth quarter of 2017

The euro area bank lending survey Fourth quarter of 217 January 218 Contents Introduction 2 1 Overview of the results 3 Box 1 General notes 4 2 Developments in credit standards, terms and conditions, and

The euro area bank lending survey Fourth quarter of 217 January 218 Contents Introduction 2 1 Overview of the results 3 Box 1 General notes 4 2 Developments in credit standards, terms and conditions, and

NatWest Markets Factbook

NatWest Markets Factbook 23/02/2018 Key messages 1 NatWest Markets is the financial markets division of The Royal Bank of Scotland Group plc (RBS Group plc) The Royal Bank of Scotland plc (RBS plc) is

NatWest Markets Factbook 23/02/2018 Key messages 1 NatWest Markets is the financial markets division of The Royal Bank of Scotland Group plc (RBS Group plc) The Royal Bank of Scotland plc (RBS plc) is

RISK DASHBOARD DATA AS OF Q2 2018

RISK DASHBOARD DATA AS OF Q2 2018 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the EU banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio

RISK DASHBOARD DATA AS OF Q2 2018 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the EU banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio

RISK DASHBOARD DATA AS OF Q1 2016

RISK DASHBOARD DA AS OF Q1 2016 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6 Total

RISK DASHBOARD DA AS OF Q1 2016 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6 Total

BANK LENDING SURVEY Results for Portugal January 2017

BANK LENDING SURVEY Results for Portugal January 2017 I. Overall assessment According to the results of the January survey conducted on the five banking groups included in the Portuguese sample, credit

BANK LENDING SURVEY Results for Portugal January 2017 I. Overall assessment According to the results of the January survey conducted on the five banking groups included in the Portuguese sample, credit

NatWest Markets Factbook

NatWest Markets Factbook 11/06/2018 Key messages 1, formerly The Royal Bank of Scotland plc is the markets busiess of The Royal Bank of Scotland Group plc. Providing investment banking services to the

NatWest Markets Factbook 11/06/2018 Key messages 1, formerly The Royal Bank of Scotland plc is the markets busiess of The Royal Bank of Scotland Group plc. Providing investment banking services to the

EBA REPORT ON ASSET ENCUMBRANCE SEPTEMBER 2018

EBA REPORT ON ASSET ENCUMBRANCE SEPTEMBER 2018 1 Contents List of figures 3 Executive summary 4 Analysis of the asset encumbrance of European banks 7 Sample 7 Scope of the report 7 Total encumbrance 8

EBA REPORT ON ASSET ENCUMBRANCE SEPTEMBER 2018 1 Contents List of figures 3 Executive summary 4 Analysis of the asset encumbrance of European banks 7 Sample 7 Scope of the report 7 Total encumbrance 8

2016 European Union Stress Test Process: Methodology and practice

2016 European Union Stress Test Process: Methodology and practice Mario Quagliariello, Head of the Risk Analysis Unit XIV JORNADA ANUAL DE RIESGOS 12 November 2015, Madrid Outline 2016 EU-wide stress test

2016 European Union Stress Test Process: Methodology and practice Mario Quagliariello, Head of the Risk Analysis Unit XIV JORNADA ANUAL DE RIESGOS 12 November 2015, Madrid Outline 2016 EU-wide stress test

Q Interim Management Statement

Q3 208 Interim Management Statement HIGHLIGHTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER 208 Strong and sustainable financial performance with increased profits and returns Statutory profit after tax of 3.7

Q3 208 Interim Management Statement HIGHLIGHTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER 208 Strong and sustainable financial performance with increased profits and returns Statutory profit after tax of 3.7

Results of the 2017 low-interest-rate survey Press conference on 30 August 2017

Results of the 2017 low-interest-rate survey Press conference on 2017 low-interest-rate survey Bundesbank and BaFin surveyed 1,555 German credit institutions between April and June this year on their profitability

Results of the 2017 low-interest-rate survey Press conference on 2017 low-interest-rate survey Bundesbank and BaFin surveyed 1,555 German credit institutions between April and June this year on their profitability

Getting on with delivering our Plan

Getting on with delivering our Plan Ewen Stevenson Chief Financial Officer Goldman Sachs European Financials Conference Rome 16 June 2015 Click Our investment to edit Master thesis title style We are focusing

Getting on with delivering our Plan Ewen Stevenson Chief Financial Officer Goldman Sachs European Financials Conference Rome 16 June 2015 Click Our investment to edit Master thesis title style We are focusing

Q Interim Management Statement

Q3 2018 Interim Management Statement LLOYDS BANKING GROUP PLC Q3 2018 INTERIM MANAGEMENT STATEMENT HIGHLIGHTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER 2018 Strong and sustainable financial performance with

Q3 2018 Interim Management Statement LLOYDS BANKING GROUP PLC Q3 2018 INTERIM MANAGEMENT STATEMENT HIGHLIGHTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER 2018 Strong and sustainable financial performance with

Draft Technical Standards on criteria for MREL. 19 January 2015

Draft Technical Standards on criteria for MREL 19 January 2015 Contents 1. Context 2. Main features of draft Technical Standards 3. MREL and TLAC 4. Next steps 5. Questions? 1. Context: BRRD requirements

Draft Technical Standards on criteria for MREL 19 January 2015 Contents 1. Context 2. Main features of draft Technical Standards 3. MREL and TLAC 4. Next steps 5. Questions? 1. Context: BRRD requirements

TRENDS IN LENDING Third Quarter Report 2018

УНУТРАШЊА УПОТРЕБА TRENDS IN LENDING Third Quarter Report 218 Belgrade, December 218 УНУТРАШЊА УПОТРЕБА Introductory note Trends in Lending is an in-depth analysis of the latest trends in lending, which

УНУТРАШЊА УПОТРЕБА TRENDS IN LENDING Third Quarter Report 218 Belgrade, December 218 УНУТРАШЊА УПОТРЕБА Introductory note Trends in Lending is an in-depth analysis of the latest trends in lending, which

FITCH AFFIRMS CREDIT EUROPE BANK N.V. AND RUSSIAN SUBSIDIARY AT 'BB-'; OUTLOOK STABLE

FITCH AFFIRMS CREDIT EUROPE BANK N.V. AND RUSSIAN SUBSIDIARY AT 'BB-'; OUTLOOK STABLE Fitch Ratings-London/Paris/Moscow-27 November 2014: Fitch Ratings has affirmed the Long-term Issuer Default Ratings

FITCH AFFIRMS CREDIT EUROPE BANK N.V. AND RUSSIAN SUBSIDIARY AT 'BB-'; OUTLOOK STABLE Fitch Ratings-London/Paris/Moscow-27 November 2014: Fitch Ratings has affirmed the Long-term Issuer Default Ratings

European Banking Barometer Reflecting a challenged industry

European Banking Barometer 1 Reflecting a challenged industry Contents Page 1 Economic environment Business outlook and focus areas 1 Business priorities and product line expectations Headcount and compensation

European Banking Barometer 1 Reflecting a challenged industry Contents Page 1 Economic environment Business outlook and focus areas 1 Business priorities and product line expectations Headcount and compensation

THE EURO AREA BANK LENDING SURVEY 2ND QUARTER OF 2013

THE EURO AREA BANK LENDING SURVEY 2ND QUARTER OF 213 JULY 213 European Central Bank, 213 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

THE EURO AREA BANK LENDING SURVEY 2ND QUARTER OF 213 JULY 213 European Central Bank, 213 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

Building a better bank for customers and shareholders

Building a better bank for customers and shareholders Ewen Stevenson, Chief Financial Officer Goldman Sachs European Financials Conference Paris, 9 th June 2016 Investment case Core bank delivering sustainable

Building a better bank for customers and shareholders Ewen Stevenson, Chief Financial Officer Goldman Sachs European Financials Conference Paris, 9 th June 2016 Investment case Core bank delivering sustainable

Half Yearly Financial Report 2016 Santander UK plc

Half Yearly Financial Report 2016 Santander UK plc PART OF THE SANTANDER GROUP This page intentionally blank Santander UK plc Half Yearly Financial Report 2016 2 Introduction 4 Financial review 18 Risk

Half Yearly Financial Report 2016 Santander UK plc PART OF THE SANTANDER GROUP This page intentionally blank Santander UK plc Half Yearly Financial Report 2016 2 Introduction 4 Financial review 18 Risk

The euro area bank lending survey. Second quarter of 2018

The euro area bank lending survey Second quarter of 218 July 218 Contents Introduction 2 1 Overview of the results 3 Box 1 General notes 5 2 Developments in credit standards, terms and conditions, and

The euro area bank lending survey Second quarter of 218 July 218 Contents Introduction 2 1 Overview of the results 3 Box 1 General notes 5 2 Developments in credit standards, terms and conditions, and

RISK DASHBOARD DATA AS OF Q4 2017

RISK DASHBOARD DATA AS OF Q4 2017 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6

RISK DASHBOARD DATA AS OF Q4 2017 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio 6

TITLE SLIDE IS IN SENTENCE CASE.

TITLE SLIDE IS IN SENTENCE CASE. GREEN Presentation to Analysts BACKGROUND. and Investors INTERIM MANAGEMENT STATEMENT 25 October HIGHLIGHTS FOR THE FIRST NINE MONTHS OF Strong financial performance continues

TITLE SLIDE IS IN SENTENCE CASE. GREEN Presentation to Analysts BACKGROUND. and Investors INTERIM MANAGEMENT STATEMENT 25 October HIGHLIGHTS FOR THE FIRST NINE MONTHS OF Strong financial performance continues

Half Year Results for the Six Months to 31 January 2019

Close Brothers Group plc T +44 (0)20 7655 3100 10 Crown Place E enquiries@closebrothers.com London EC2A 4FT W www.closebrothers.com Registered in England No. 520241 Half Year Results for the Six Months

Close Brothers Group plc T +44 (0)20 7655 3100 10 Crown Place E enquiries@closebrothers.com London EC2A 4FT W www.closebrothers.com Registered in England No. 520241 Half Year Results for the Six Months

Bank Lending Survey. 1 Overall assessment. 2 Presentation of the results. Results for Portugal July Supply

Bank Lending Survey Results for Portugal July 2018 1 Overall assessment According to the results of the July 2018 survey to the five banks included in the Portuguese sample, credit standards applied on

Bank Lending Survey Results for Portugal July 2018 1 Overall assessment According to the results of the July 2018 survey to the five banks included in the Portuguese sample, credit standards applied on

The euro area bank lending survey. Third quarter of 2016

The euro area bank lending survey Third quarter of 216 October 216 Contents Introduction 2 1 Overview of the results 3 Box 1 General notes 4 2 Developments in credit standards, terms and conditions, and

The euro area bank lending survey Third quarter of 216 October 216 Contents Introduction 2 1 Overview of the results 3 Box 1 General notes 4 2 Developments in credit standards, terms and conditions, and

EBA REPORT ON ASSET ENCUMBRANCE JULY 2017

EBA REPORT ON ASSET ENCUMBRANCE JULY 2017 1 Contents List of figures 3 Executive summary 4 Analysis of the asset encumbrance of European banks 6 Sample 6 Scope of the report 6 Total encumbrance 7 Encumbrance

EBA REPORT ON ASSET ENCUMBRANCE JULY 2017 1 Contents List of figures 3 Executive summary 4 Analysis of the asset encumbrance of European banks 6 Sample 6 Scope of the report 6 Total encumbrance 7 Encumbrance

The euro area bank lending survey. Fourth quarter of 2018

The euro area bank lending survey Fourth quarter of 218 January 219 Contents Introduction 2 1 Overview of results 3 Box 1 General notes 5 2 Developments in credit standards, terms and conditions, and net

The euro area bank lending survey Fourth quarter of 218 January 219 Contents Introduction 2 1 Overview of results 3 Box 1 General notes 5 2 Developments in credit standards, terms and conditions, and net

The Bank of England s approach to setting a minimum requirement for own funds and eligible liabilities (MREL)

") November 2016 The Bank of England s approach to setting a minimum requirement for own funds and eligible liabilities (MREL) Responses to Consultation and Statement of Policy November 2016 The Bank of

November 2016 The Bank of England s approach to setting a minimum requirement for own funds and eligible liabilities (MREL) Responses to Consultation and Statement of Policy November 2016 The Bank of

RBS Treasury. Structural hedges: a summary 13 th June Information Classification: Public

RBS Treasury Structural hedges: a summary 13 th June 2018 Information Classification: Public Contents Comparison of rolling hedge rate and 3M LIBOR The components of the structural hedge Hedging mechanics

RBS Treasury Structural hedges: a summary 13 th June 2018 Information Classification: Public Contents Comparison of rolling hedge rate and 3M LIBOR The components of the structural hedge Hedging mechanics

Interim Financial Report 2017

Interim Financial Report 2017 ABN AMRO Bank N.V. II Notes to the reader Executive Board Report Introduction This is the Interim Financial Report for the year 2017 of ABN AMRO Bank N.V. (ABN AMRO Bank).

Interim Financial Report 2017 ABN AMRO Bank N.V. II Notes to the reader Executive Board Report Introduction This is the Interim Financial Report for the year 2017 of ABN AMRO Bank N.V. (ABN AMRO Bank).

RISK DASHBOARD DATA AS OF Q1 2018

RISK DASHBOARD DATA AS OF Q1 2018 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the EU banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio

RISK DASHBOARD DATA AS OF Q1 2018 2 Contents 1 Summary 3 2 Overview of the main risks and vulnerabilities in the EU banking sector 4 3 Heatmap 5 4 Risk Indicators (RIs) 4.1 Solvency Tier 1 capital ratio

Assessing Capital Markets Union

6 Assessing Capital Markets Union Quarterly Assessment by Paul Richards Summary It is too early to make an assessment of Capital Markets Union, but not too early to give a market view of the tests by which

6 Assessing Capital Markets Union Quarterly Assessment by Paul Richards Summary It is too early to make an assessment of Capital Markets Union, but not too early to give a market view of the tests by which

BANK LENDING SURVEY. October de Results for Portugal

BANK LENDING SURVEY October de 13 Results for Portugal I. Overall assessment In general, both credit standards and conditions and terms applied in to companies and households remained broadly unchanged,

BANK LENDING SURVEY October de 13 Results for Portugal I. Overall assessment In general, both credit standards and conditions and terms applied in to companies and households remained broadly unchanged,

BANK LENDING SURVEY Results for Portugal April 2018

BANK LENDING SURVEY Results for Portugal April 2018 I. Overall assessment According to the results of the April 2018 survey of the five banks included in the Portuguese sample, credit standards applied

BANK LENDING SURVEY Results for Portugal April 2018 I. Overall assessment According to the results of the April 2018 survey of the five banks included in the Portuguese sample, credit standards applied

the EURO AREA BANK LENDING SURVEY

the EURO AREA BANK LENDING SURVEY 4TH QUARTER OF 213 In 214 all ECB publications feature a motif taken from the 2 banknote. JANUARY 214 European Central Bank, 214 Address Kaiserstrasse 29, 6311 Frankfurt

the EURO AREA BANK LENDING SURVEY 4TH QUARTER OF 213 In 214 all ECB publications feature a motif taken from the 2 banknote. JANUARY 214 European Central Bank, 214 Address Kaiserstrasse 29, 6311 Frankfurt

BANK OF AMERICA MERRILL LYNCH FINANCIALS CONFERENCE. George Culmer 25 September 2018

BANK OF AMERICA MERRILL LYNCH FINANCIALS CONFERENCE George Culmer 25 September 2018 Unique business model generating strong and sustainable returns Distinctive competitive strengths Differentiated multi-brand,

BANK OF AMERICA MERRILL LYNCH FINANCIALS CONFERENCE George Culmer 25 September 2018 Unique business model generating strong and sustainable returns Distinctive competitive strengths Differentiated multi-brand,

Royal Bank of Canada. Pillar 3 Report

Royal Bank of Canada Pillar 3 Report As at January 3, 09 TABLE OF CONTENTS CAUTION REGARDING FORWARD-LOOKING STATEMENTS... ABOUT ROYAL BANK OF CANADA... CAPITAL FRAMEWORK... TLAC FRAMEWORK... DISCLOSURE

Royal Bank of Canada Pillar 3 Report As at January 3, 09 TABLE OF CONTENTS CAUTION REGARDING FORWARD-LOOKING STATEMENTS... ABOUT ROYAL BANK OF CANADA... CAPITAL FRAMEWORK... TLAC FRAMEWORK... DISCLOSURE

The Governor and Company of the Bank of Ireland Interim Report. For the six months ended 30 June 2018

The Governor and Company of the Bank of Ireland Interim Report For the six months ended 30 June 2018 The Governor and Company of the Bank of Ireland Interim Report for the six months ended 30 June 2018

The Governor and Company of the Bank of Ireland Interim Report For the six months ended 30 June 2018 The Governor and Company of the Bank of Ireland Interim Report for the six months ended 30 June 2018

Banking Digest QUARTERLY Q BASEL III REQUIREMENTS SUMMARY INDICATORS PERFORMANCE HIGHLIGHTS

QUARTERLY Banking Digest Q1-18 BERMUDA MONETARY AUTHORITY BASEL III REQUIREMENTS As of 1 January 18, Bermuda s banks are required to meet a Net-Stable Funding Ratio (NSFR) as part of the Authority s implementation

QUARTERLY Banking Digest Q1-18 BERMUDA MONETARY AUTHORITY BASEL III REQUIREMENTS As of 1 January 18, Bermuda s banks are required to meet a Net-Stable Funding Ratio (NSFR) as part of the Authority s implementation

2018 HALF-YEAR RESULTS News Release

News Release BASIS OF PRESENTATION This release covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the six months ended 30 June 2018. IFRS 9 and IFRS 15: On 1

News Release BASIS OF PRESENTATION This release covers the results of Lloyds Banking Group plc together with its subsidiaries (the Group) for the six months ended 30 June 2018. IFRS 9 and IFRS 15: On 1

INVESTMENT AND COMPANY REPORTING Economic analysis and evaluation. Survey with Enterprise Europe Network on SME credit information

EUROPEAN COMMISSION Directorate-General for Financial Stability, Financial Services and Capital Markets Union INVESTMENT AND COMPANY REPORTING Economic analysis and evaluation Ref. Ares(2015)4530032-23/10/2015

EUROPEAN COMMISSION Directorate-General for Financial Stability, Financial Services and Capital Markets Union INVESTMENT AND COMPANY REPORTING Economic analysis and evaluation Ref. Ares(2015)4530032-23/10/2015

CIBC Investor Presentation Q1 F18

CIBC Investor Presentation Q F8 February, 08 Forward-Looking Statements A NOTE ABOUT FORWARD-LOOKING STATEMENTS: From time to time, we make written or oral forward-looking statements within the meaning

CIBC Investor Presentation Q F8 February, 08 Forward-Looking Statements A NOTE ABOUT FORWARD-LOOKING STATEMENTS: From time to time, we make written or oral forward-looking statements within the meaning

BoA Merrill Lynch Banking & Insurance CEO Conference London, 25 September 2012

BoA Merrill Lynch Banking & Insurance CEO Conference London, 25 September 2012 Annika Falkengren President & CEO The message from last year s conference Stability Sustainable growth Continuous improvement

BoA Merrill Lynch Banking & Insurance CEO Conference London, 25 September 2012 Annika Falkengren President & CEO The message from last year s conference Stability Sustainable growth Continuous improvement

Isabelle Vaillant Director of Regulation. European Institute of Financial Regulation (EIFR) 23 Septembre 2016

23 Septembre 2016") Isabelle Vaillant Director of Regulation European Institute of Financial Regulation (EIFR) 23 Septembre 2016 Overview of the presentation 1 EBA mission and scope of action 2 EBA Single Rulebook 3 Regulatory

Isabelle Vaillant Director of Regulation European Institute of Financial Regulation (EIFR) 23 Septembre 2016 Overview of the presentation 1 EBA mission and scope of action 2 EBA Single Rulebook 3 Regulatory

Group Results for the nine-month period ended 30 September 2016

COMMENTARY Group Results for the nine-month period ended 28 November Building a stronger bank, by making further progress in our strategic priorities 9M financial performance summary Profit before provisions

COMMENTARY Group Results for the nine-month period ended 28 November Building a stronger bank, by making further progress in our strategic priorities 9M financial performance summary Profit before provisions

Standard Chartered PLC - Interim management statement. Highlights. 1 November 2016

1 November 2016 Standard Chartered PLC - Interim management statement Highlights Standard Chartered PLC today releases its interim management statement for the quarter 30 September 2016. All figures are

1 November 2016 Standard Chartered PLC - Interim management statement Highlights Standard Chartered PLC today releases its interim management statement for the quarter 30 September 2016. All figures are

Basel 4: The way ahead

Basel 4: The way Piecing the jigsaw together May 2018 The way 2 Contents 01 Introduction 01 / Introduction 02 02 / Implications for banks 03 03 / Banks strategic options 06 04 / Missing pieces of the jigsaw

Basel 4: The way Piecing the jigsaw together May 2018 The way 2 Contents 01 Introduction 01 / Introduction 02 02 / Implications for banks 03 03 / Banks strategic options 06 04 / Missing pieces of the jigsaw

2017 Results. 27 February 2018

2017 Results 27 February 2018 FY17 Financial Performance 37.8p EPS 1 +29% 192.1m Stat profit 2 +37% RoTE of 14% up from 12.4% in FY16 13.8% CET1 Ratio 6.0p Total dividend +18% 297p TNAV +9% Note: (1) Basic

2017 Results 27 February 2018 FY17 Financial Performance 37.8p EPS 1 +29% 192.1m Stat profit 2 +37% RoTE of 14% up from 12.4% in FY16 13.8% CET1 Ratio 6.0p Total dividend +18% 297p TNAV +9% Note: (1) Basic

Italian Banks - Accelerating the Sales of NPL to Improve Asset Quality

Italian Banks - Accelerating the Sales of NPL to Improve Asset Quality 31 July 2017 Commentary Carola Saldias Senior Director Financial Institutions Analytical Team carola.saldias@dagongeurope.com Evgeni

Italian Banks - Accelerating the Sales of NPL to Improve Asset Quality 31 July 2017 Commentary Carola Saldias Senior Director Financial Institutions Analytical Team carola.saldias@dagongeurope.com Evgeni

An update of regulatory developments and impact on banks regulatory compliance

[Please select] [Please select] Michael Grill Pär Torstensson Michael Wedow DG-Macro-Prudential Policy and Financial Stability An update of regulatory developments and impact on banks regulatory compliance

[Please select] [Please select] Michael Grill Pär Torstensson Michael Wedow DG-Macro-Prudential Policy and Financial Stability An update of regulatory developments and impact on banks regulatory compliance

REVIEW OF THE SURVEY OF THE FINANCIAL BEHAVIOUR OF HOUSEHOLDS SURVEY REVIEW OF THE BANK LENDING

REVIEW OF THE SURVEY OF THE FINANCIAL BEHAVIOUR 14 13 Q1 OF HOUSEHOLDS REVIEW OF THE BANK LENDING SURVEY ISSN 2335-841 (ONLINE) REVIEW OF THE BANK LENDING SURVEY 14/2 The lending survey of commercial banks

REVIEW OF THE SURVEY OF THE FINANCIAL BEHAVIOUR 14 13 Q1 OF HOUSEHOLDS REVIEW OF THE BANK LENDING SURVEY ISSN 2335-841 (ONLINE) REVIEW OF THE BANK LENDING SURVEY 14/2 The lending survey of commercial banks

TITLE SLIDE IS IN SENTENCE CASE. GREEN BACKGROUND.

TITLE SLIDE IS IN SENTENCE CASE. GREEN BACKGROUND. BANK OF AMERICA MERRILL LYNCH CEO CONFERENCE António Horta-Osório 00 Month 0000 Presenters Name 29 September 2015 AGENDA A differentiated business model

TITLE SLIDE IS IN SENTENCE CASE. GREEN BACKGROUND. BANK OF AMERICA MERRILL LYNCH CEO CONFERENCE António Horta-Osório 00 Month 0000 Presenters Name 29 September 2015 AGENDA A differentiated business model

How to ensure enough Loss Absorbing Capacity: From TLAC to MREL

How to ensure enough Loss Absorbing Capacity: From TLAC to MREL Nikoletta Kleftouri European Banking Authority 13 December 2016 FINSAC Workshop on bail-in and MREL Plan 1. Why do we need loss absorbing

How to ensure enough Loss Absorbing Capacity: From TLAC to MREL Nikoletta Kleftouri European Banking Authority 13 December 2016 FINSAC Workshop on bail-in and MREL Plan 1. Why do we need loss absorbing

Consultation paper on amendments to supervisory reporting with regard to FINREP. Public hearing, 3 October 2018

Consultation paper on amendments to supervisory reporting with regard to FINREP Public hearing, 3 October 2018 Release v2.9 of the reporting framework (I) For framework release v2.9, EBA intends to move

Consultation paper on amendments to supervisory reporting with regard to FINREP Public hearing, 3 October 2018 Release v2.9 of the reporting framework (I) For framework release v2.9, EBA intends to move

The Royal Bank of Scotland Group

The Royal Bank of Scotland Group Q311 Fixed Income Investor Call 4 th November 2011 John Cummins Group Treasurer Liam Coleman Deputy Group Treasurer Emete Hassan Head of Debt Investor Relations Important

The Royal Bank of Scotland Group Q311 Fixed Income Investor Call 4 th November 2011 John Cummins Group Treasurer Liam Coleman Deputy Group Treasurer Emete Hassan Head of Debt Investor Relations Important

FITCH AFFIRMS ABN AMRO BANK AT 'A+'; OUTLOOK STABLE

FITCH AFFIRMS ABN AMRO BANK AT 'A+'; OUTLOOK STABLE Fitch Ratings-London-24 February 2017: Fitch Ratings has affirmed ABN AMRO Bank N.V.'s Long-Term Issue Default Rating (IDR) at 'A+' with a Stable Outlook,

FITCH AFFIRMS ABN AMRO BANK AT 'A+'; OUTLOOK STABLE Fitch Ratings-London-24 February 2017: Fitch Ratings has affirmed ABN AMRO Bank N.V.'s Long-Term Issue Default Rating (IDR) at 'A+' with a Stable Outlook,

FIRSTRAND GROUP. Harry Kellan. cfo s report

Harry Kellan cfo s report 3 INTRODUCTION Globally the economic environment improved and this allowed the US Federal Reserve to continue with gradual monetary policy normalisation. Economic activity in

Harry Kellan cfo s report 3 INTRODUCTION Globally the economic environment improved and this allowed the US Federal Reserve to continue with gradual monetary policy normalisation. Economic activity in

the Bank of Canada s Financial System Survey

the Bank of Canada s Financial System Survey BANK OF CANADA Financial System Review JUNE 2018 51 The Bank of Canada s Financial System Survey Guillaume Bédard-Pagé, Ian Christensen, Scott Kinnear and Maxime

the Bank of Canada s Financial System Survey BANK OF CANADA Financial System Review JUNE 2018 51 The Bank of Canada s Financial System Survey Guillaume Bédard-Pagé, Ian Christensen, Scott Kinnear and Maxime

Íslandsbanki hf. CONSOLIDATED INTERIM FINANCIAL STATEMENTS 1H18. First half 2018 financial highlights. Second quarter 2018 financial highlights

Íslandsbanki hf. CONSOLIDATED INTERIM FINANCIAL STATEMENTS 1H18 First half 2018 financial highlights Profit after tax was ISK 7.1bn (1H17: ISK 8.0bn) generating an 8.2% annualised return on equity (1H17:

Íslandsbanki hf. CONSOLIDATED INTERIM FINANCIAL STATEMENTS 1H18 First half 2018 financial highlights Profit after tax was ISK 7.1bn (1H17: ISK 8.0bn) generating an 8.2% annualised return on equity (1H17:

Commerzbank: Operating profit increased by 40% to more than EUR 1 bn in 2014 implementation of strategic agenda proceeding to plan

Press release For business desks 12 February 2015 Commerzbank: Operating profit increased by 40% to more than EUR 1 bn in 2014 implementation of strategic agenda proceeding to plan Net profit increased

Press release For business desks 12 February 2015 Commerzbank: Operating profit increased by 40% to more than EUR 1 bn in 2014 implementation of strategic agenda proceeding to plan Net profit increased

CIBC Investor Presentation Q2 F18

CIBC Investor Presentation Q2 F8 May 23, 208 Forward-Looking Statements 2 A NOTE ABOUT FORWARD-LOOKING STATEMENTS: From time to time, we make written or oral forward-looking statements within the meaning

CIBC Investor Presentation Q2 F8 May 23, 208 Forward-Looking Statements 2 A NOTE ABOUT FORWARD-LOOKING STATEMENTS: From time to time, we make written or oral forward-looking statements within the meaning

For further questions, please contact Paulina Przewoska, senior policy analyst at Finance Watch.

Finance Watch response to FSB s consultation on Adequacy of Loss-Absorbing Capacity of Global Systemically Important Banks in resolution Brussels, 30 January 2015 Finance Watch is an independent, non-profit

Finance Watch response to FSB s consultation on Adequacy of Loss-Absorbing Capacity of Global Systemically Important Banks in resolution Brussels, 30 January 2015 Finance Watch is an independent, non-profit

Rabobank. FY2018 results Analyst presentation

Rabobank FY2018 results Analyst presentation 14 February 2019 Excellent customer focus Highlights FY2018 Growing a better world together Banking for the Netherlands Banking for Food Excellent customer

Rabobank FY2018 results Analyst presentation 14 February 2019 Excellent customer focus Highlights FY2018 Growing a better world together Banking for the Netherlands Banking for Food Excellent customer

Process and next steps

14 December 2016 MREL REPORT: Frequently Asked Questions Process and next steps 1. Why have you issued an interim and a final MREL report? What are the main differences between the two reports? As per

14 December 2016 MREL REPORT: Frequently Asked Questions Process and next steps 1. Why have you issued an interim and a final MREL report? What are the main differences between the two reports? As per

RISK DASHBOARD. April

RISK DASHBOARD April 2017 1 Risks Level Trend 1. Macro risks High 2. Credit risks Medium 3. Market risks Medium 4. Liquidity and funding risks Medium 5. Profitability and solvency Medium 6. Interlinkages

RISK DASHBOARD April 2017 1 Risks Level Trend 1. Macro risks High 2. Credit risks Medium 3. Market risks Medium 4. Liquidity and funding risks Medium 5. Profitability and solvency Medium 6. Interlinkages

Management Discussion and Analysis

Management Discussion and Analysis Overview +/( ) % Selected income statement items ($ million) Net interest income 6,220 5,528 13 Net fee and commission income 1,967 1,873 5 Other non-interest income

Management Discussion and Analysis Overview +/( ) % Selected income statement items ($ million) Net interest income 6,220 5,528 13 Net fee and commission income 1,967 1,873 5 Other non-interest income

BEST PRACTICES FOR FINANCIAL INSTITUTIONS FACING CHALLENGES IN EFFECTIVELY AND EFFICIENTLY MANAGING NON-PERFORMING LOANS JULY 2016

BEST PRACTICES FOR FINANCIAL INSTITUTIONS FACING CHALLENGES IN EFFECTIVELY AND EFFICIENTLY MANAGING NON-PERFORMING LOANS JULY 216 INTRODUCTION Non-performing loans (NPLs) have increased significantly across

BEST PRACTICES FOR FINANCIAL INSTITUTIONS FACING CHALLENGES IN EFFECTIVELY AND EFFICIENTLY MANAGING NON-PERFORMING LOANS JULY 216 INTRODUCTION Non-performing loans (NPLs) have increased significantly across

Q Results. 26 th October

Q3 2018 Results 26 th October Key Messages Good performance in a highly competitive market and uncertain economic outlook Q3 2018 Attributable profit 448m, + 14% vs. Q3 2017 Strong capital positon, 16.7%

Q3 2018 Results 26 th October Key Messages Good performance in a highly competitive market and uncertain economic outlook Q3 2018 Attributable profit 448m, + 14% vs. Q3 2017 Strong capital positon, 16.7%

CaixaBank: riding out the storm

KBW- European Financials Conference CaixaBank: riding out the storm Gonzalo Gortázar, CFO London, September 20th 2011 la Caixa Disclaimer The information contained in this presentation does not constitute

KBW- European Financials Conference CaixaBank: riding out the storm Gonzalo Gortázar, CFO London, September 20th 2011 la Caixa Disclaimer The information contained in this presentation does not constitute

Q Interim Management Statement

Q1 2018 Interim Management Statement HIGHLIGHTS FOR THE THREE MONTHS ENDED 31 MARCH 2018 Strong financial performance with significant increase in profit and returns on a statutory and underlying basis

Q1 2018 Interim Management Statement HIGHLIGHTS FOR THE THREE MONTHS ENDED 31 MARCH 2018 Strong financial performance with significant increase in profit and returns on a statutory and underlying basis

European Banking Barometer 1H14. Confidence masks challenges

an Banking Barometer H Confidence masks challenges Contents Page Economic environment an sovereign debt crisis Business outlook and focus areas Business priorities and product line expectations Headcount

an Banking Barometer H Confidence masks challenges Contents Page Economic environment an sovereign debt crisis Business outlook and focus areas Business priorities and product line expectations Headcount

EXECUTIVE SUMMARY JOINT COMMITTEE REPORT ON RISKS AND VULNERABILITIES IN THE EU FINANCIAL SYSTEM SEPTEMBER September 2017 JC

21 September 2017 JC 2017 46 JOINT COMMITTEE REPORT ON RISKS AND VULNERABILITIES IN THE EU FINANCIAL SYSTEM SEPTEMBER 2017 Executive summary... 1 1 Introduction... 2 2 Risks related to the UK s withdrawal

21 September 2017 JC 2017 46 JOINT COMMITTEE REPORT ON RISKS AND VULNERABILITIES IN THE EU FINANCIAL SYSTEM SEPTEMBER 2017 Executive summary... 1 1 Introduction... 2 2 Risks related to the UK s withdrawal

The euro area bank lending survey. Third quarter of 2018

The euro area bank lending survey Third quarter of 218 October 218 Contents Introduction 2 1 Overview of results 3 Box 1 General notes 5 2 Developments in credit standards, terms and conditions, and net

The euro area bank lending survey Third quarter of 218 October 218 Contents Introduction 2 1 Overview of results 3 Box 1 General notes 5 2 Developments in credit standards, terms and conditions, and net

Lloyds Bank plc. Q Interim Management Statement. 25 October 2018

Lloyds Bank plc Q3 2018 Interim Management Statement 25 October 2018 REVIEW OF PERFORMANCE As a result of the requirements of the ring-fencing regulations, the Bank sold its subsidiary, Scottish Widows

Lloyds Bank plc Q3 2018 Interim Management Statement 25 October 2018 REVIEW OF PERFORMANCE As a result of the requirements of the ring-fencing regulations, the Bank sold its subsidiary, Scottish Widows

FITCH AFFIRMS RABOBANK AT 'AA-'; OUTLOOK STABLE

FITCH AFFIRMS RABOBANK AT 'AA-'; OUTLOOK STABLE Fitch Ratings-London/Paris-24 November 2017: Fitch Ratings has affirmed Cooperatieve Rabobank U.A.'s (Rabobank) Long-Term Issuer Default Rating (IDR) at

FITCH AFFIRMS RABOBANK AT 'AA-'; OUTLOOK STABLE Fitch Ratings-London/Paris-24 November 2017: Fitch Ratings has affirmed Cooperatieve Rabobank U.A.'s (Rabobank) Long-Term Issuer Default Rating (IDR) at

LLOYDS BANKING GROUP PLC ANNUAL REPORT AND ACCOUNTS FOR THE YEAR ENDED 31 DECEMBER 2017

21 February 2018 LLOYDS BANKING GROUP PLC ANNUAL REPORT AND ACCOUNTS FOR THE YEAR ENDED 31 DECEMBER In accordance with Listing Rule 9.6.1, Lloyds Banking Group plc has submitted today the following document

21 February 2018 LLOYDS BANKING GROUP PLC ANNUAL REPORT AND ACCOUNTS FOR THE YEAR ENDED 31 DECEMBER In accordance with Listing Rule 9.6.1, Lloyds Banking Group plc has submitted today the following document

Q Results. 27 th October 2017

Q3 2017 Results 27 th October 2017 Key messages Q3 attributable profit of 392m; Adjusted ROTE 8.2% Cost, capital and lending targets on track for fourth consecutive year Targeting a bottom line profit

Q3 2017 Results 27 th October 2017 Key messages Q3 attributable profit of 392m; Adjusted ROTE 8.2% Cost, capital and lending targets on track for fourth consecutive year Targeting a bottom line profit

International Macroeconomic Environment:

Advanced Economies: Reduced Downward Risks in a Still Weak Global Environment Global economic activity remained subdued in the review period from November 2012 to May 2013 despite bold policy action to

Advanced Economies: Reduced Downward Risks in a Still Weak Global Environment Global economic activity remained subdued in the review period from November 2012 to May 2013 despite bold policy action to

Banking Digest QUARTERLY Q BASEL III REQUIREMENTS SUMMARY INDICATORS BANKING INSIGHT PERFORMANCE HIGHLIGHTS

QUARTERLY Banking Digest Q3-18 BERMUDA MONETARY AUTHORITY BASEL III REQUIREMENTS As of 1 January 18, Bermuda s banks are required to meet a Net-Stable Funding Ratio (NSFR) as part of the Authority s implementation

QUARTERLY Banking Digest Q3-18 BERMUDA MONETARY AUTHORITY BASEL III REQUIREMENTS As of 1 January 18, Bermuda s banks are required to meet a Net-Stable Funding Ratio (NSFR) as part of the Authority s implementation

GLOSSARY 158 GLOSSARY. Balance-sheet liquidity. The ability of an institution to meet its obligations in a corresponding volume and term structure.

158 GLOSSARY GLOSSARY Balance-sheet liquidity Balance-sheet recession Bank Lending Survey (BLS) The ability of an institution to meet its obligations in a corresponding volume and term structure. A situation

158 GLOSSARY GLOSSARY Balance-sheet liquidity Balance-sheet recession Bank Lending Survey (BLS) The ability of an institution to meet its obligations in a corresponding volume and term structure. A situation

Introduction Post crisis Bank resolution principles with a focus on the BRRD in the EU

Introduction Post crisis Bank resolution principles with a focus on the BRRD in the EU Pamela Lintner Sr. Financial Sector Specialist Workshop on the role of the Judiciary in Bank resolution for Judges

Introduction Post crisis Bank resolution principles with a focus on the BRRD in the EU Pamela Lintner Sr. Financial Sector Specialist Workshop on the role of the Judiciary in Bank resolution for Judges

TRENDS IN LENDING. Fourth Quarter Report 2017

TRENDS IN LENDING Fourth Quarter Report 217 Belgrade, March 218 Introductory note Trends in Lending is an in-depth analysis of the latest trends in lending, which aims to ensure better understanding of

TRENDS IN LENDING Fourth Quarter Report 217 Belgrade, March 218 Introductory note Trends in Lending is an in-depth analysis of the latest trends in lending, which aims to ensure better understanding of

Lloyds Banking Group plc Half-Year Pillar 3 disclosures. 28 July 2016

Lloyds Banking Group plc 2016 Half-Year Pillar 3 disclosures 28 July 2016 BASIS OF PRESENTATION This report presents the condensed half-year Pillar 3 disclosures of Lloyds Banking Group plc ( the Group

Lloyds Banking Group plc 2016 Half-Year Pillar 3 disclosures 28 July 2016 BASIS OF PRESENTATION This report presents the condensed half-year Pillar 3 disclosures of Lloyds Banking Group plc ( the Group

CIBC Investor Presentation Q4 F18

CIBC Investor Presentation Q4 F8 November 29, 208 Forward-Looking Statements 2 A NOTE ABOUT FORWARD-LOOKING STATEMENTS: From time to time, we make written or oral forward-looking statements within the

CIBC Investor Presentation Q4 F8 November 29, 208 Forward-Looking Statements 2 A NOTE ABOUT FORWARD-LOOKING STATEMENTS: From time to time, we make written or oral forward-looking statements within the

COMMENTARY. GROUP RESULTS for the six-month period ended 30 June 2016

COMMENTARY GROUP RESULTS for the six-month period ended 30 June 30 August TABLE OF CONTENTS Page 1. Fix and Build strategy is delivering results 3 2. Strategic targets and outlook 3-4 3. Results Overview

COMMENTARY GROUP RESULTS for the six-month period ended 30 June 30 August TABLE OF CONTENTS Page 1. Fix and Build strategy is delivering results 3 2. Strategic targets and outlook 3-4 3. Results Overview

VIRGIN MONEY HOLDINGS (UK) PLC: Q TRADING UPDATE VIRGIN MONEY POWERS AHEAD WITH RECORD MORTGAGE LENDING IN Q1 2016