ERM + STRATEGIC PLANNING. February 2016 IBAT

|

|

|

- Ronald Baldwin

- 6 years ago

- Views:

Transcription

1 ERM + STRATEGIC PLANNING February 2016 IBAT

2 RISK CATEGORIES OCC defines eight categories + three Credit Risk Interest Rate Risk Liquidity Risk Operational Risk Price Risk Compliance Risk Strategic Risk Reputation Risk Concentration Correlation Historical Trending 2

3 PICK YOUR FLAVOR 3

4 OPERATIONAL RISK IS HIGH (SEMIANNUAL RISK PERSPECTIVE, SPRING 2015) Business models are under increasing pressure as banks: launch new products increase reliance on technology and automated controls reduce staff, outsource critical activities re-engineer business processes Banks are not always adapting risk management and control processes to their changing business strategies 4

5 Opportunities Challenges 5

6 PRUDENT RISK MANAGEMENT The agencies examination and industry outreach activities have revealed an easing of CRE underwriting standards, including less-restrictive loan covenants, extended maturities, longer interest only payment periods, and limited guarantor requirements. The agencies also have observed certain risk management practices at some institutions that cause concern, including a greater number of underwriting policy exceptions and insufficient monitoring of market conditions to assess the risks associated with these concentrations. Joint Agency Statement on Prudent Risk Management for CRE Lending December 18, 2015 Financial Institution Letter FIL

7 FINANCIAL INSTITUTIONS WITH CONCENTRATIONS Historical evidence demonstrates that financial institutions with weak risk management and high CRE credit concentrations are exposed to a greater risk of loss and failure. These actions are consistent with supervisory expectations: Loan policies, underwriting standards, credit risk management practices, and concentration limits are approved by the board Lending strategies, plans to increase lending in a market or type, limits for credit and concentrations, are reviewed to be appropriate in light of changing market conditions Strategies ensure capital adequacy and allowance for loan losses support the bank s lending strategy and are consistent with the inherent risk in the CRE portfolio Perform market analyses (Changing economic conditions) Assess ongoing ability of borrowers and their projects to service all debt as loans convert from interest only to amortizing payments or during periods of rising interest rates Joint Agency Statement on Prudent Risk Management for CRE Lending December 18, 2015 Financial Institution Letter FIL

8 COMMERCIAL LENDING CONCENTRATIONS 73% 8

9 INVESTORS AREN'T THE ONLY ONES RUNNING FOR SAFETY Businesses are indicating an unwillingness to take on risk as loan demand declined for the first time in about four years. Demand for commercial and industrial loans has plunged in 2016, with declines happening across business sizes. Large- and medium-sized businesses had an 11.1 percent decline, while demand from small businesses fell 12.7 percent. Jeff Cox February 2, 2016 Banks report drop in demand for loans - CNBC.com 9

10 IN SHORT, BUSINESS INVESTMENT IS UNLIKELY Banks report weakness in demand for loans from businesses primarily because they are scaling back their investment plans. With energy, mining, manufacturing and agriculture sectors all hurting, we hadn't expected much from business investment this year, but the drop off in loan demand is worse than we expected. Paul Ashworth, chief U.S. economist at Capital Economics Jeff Cox February 2, 2016 Banks report drop in demand for loans - CNBC.com 10

11 ON THE POSITIVE SIDE Banks reported that demand for commercial real estate loans had increased in January and that lending standards for households had eased. But they also expect lending standards to tighten both for commercial real estate and commercial and industrial loans. Jeff Cox February 2, 2016 Banks report drop in demand for loans - CNBC.com 11

12 2015 Mid-Cycle Status Report Supervisory focus for the second half of 2015 and beyond centers on: Strategic Planning and Execution: Adequacy of strategic, capital and succession planning processes in light of assumed risks Corporate Governance: Reinforcing the importance of sound corporate governance Operation Risk: Focus on all phases of risk management, including planning, due diligence internal controls and ongoing monitoring 12

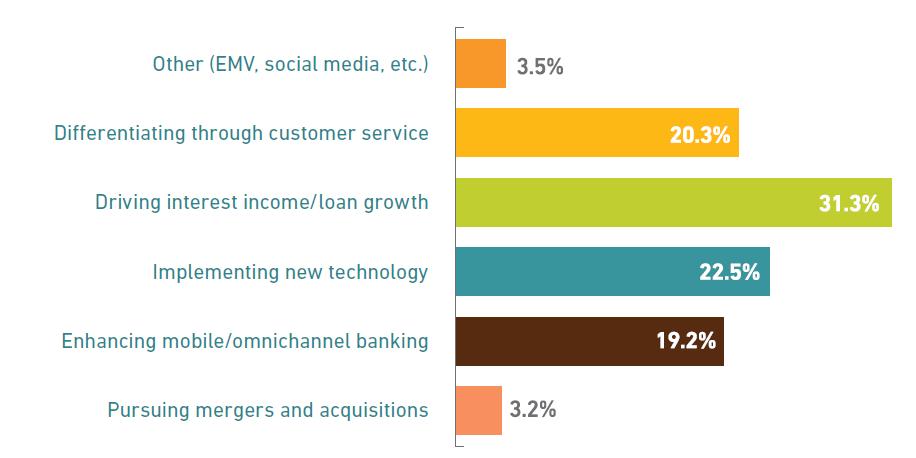

13 BANK DIRECTOR GROWTH STRATEGY SURVEY 13

14 Regulatory Focus (Semiannual Risk Perspective, Spring 2015) Risk management strategies Strategic, cybersecurity, compliance, underwriting and IRR remain top supervisory concerns Strategic objectives in relation to potential exposures Weak underwriting standards in indirect auto, asset based lending, CRE, C&I coupled with liberal repayment terms Banks continue to reevaluate their business models and risk appetites and some take on additional risk by expanding into new, less familiar, or even higher risk products/markets without adequate due diligence 14

15 BANK DIRECTOR GROWTH STRATEGY SURVEY 15

16 Regulatory Focus (Semiannual Risk Perspective, Spring 2015) What is the depth and breadth of potential exposures? In order to deal with competitive pressures and lower expenses, banks are leveraging technology such as cloud computing and mobile banking, which can increase exposure to operational risk Capability and resources of management Management succession planning, attracting appropriate expertise, and retaining key experienced personnel are growing issues especially in credit, BSA/AML, compliance, ERM and audit Strategic planning is a challenge given the current operating environment Risk appetites have not been determined and approved 16

17 WHAT TO START WITH Why would MBSs concern regulators? What is the strategy of a concentration in Jumbos? What would be a strategy for improving NPLs? How is outside risk influencing your strategy? Do you have sufficient BSA/AML expertise? 17

18 SECURITIES PORTFOLIO 18

19 HELOC PERFORMANCE 19

20 NPLS 20

21 CONCENTRATIONS IN CDS 21

22 22

23 LOCAL & REGIONAL ECONOMICS/DEMOGRAPHICS What is the organizations level of risk of exceeding local, regional and national economic & demographic trends and level of competition? 23

24 Standalone ERM Pitfalls Regulatory tail wagging the dog ERM is about management, not compliance Compliance is required but not sufficient in planning Just integrates risks Doesn t break down organizational silos Identify interdependencies in planning Boils the ocean Doesn t focus on what is most important Support strategic decisions for your board, shareholders and regulators in planning 24

25 STAGES OF THE MARRIAGE Stage 1: Foundation Setting. Review policies. Verify that limits and guidelines fit your strategies. Stage 2: Identify and Establish Appetite. Aggregate multiple assessments into one for a comprehensive picture of risks related to strategy. Stage 3: Risk & Performance Measurement and Reporting. Include both Key Risk Indicators (KRIs) and Key Performance Indicators (KPIs) that relate to the strategic plan and are being tracked against policy limits and forecasts. Stage 4: Risk/Strategy Management. ERM must impact decisions that reinforce a riskadjusted strategic plan. 25

26 COMBINE RISK & STRATEGY FIRST How would you rate your current strategic planning process? Are you using your budget as your business plan? How often do you reforecast? How are you considering risks associated with your plan and forecast? 26

27 START WITH THEIR FORMAT 27

28 Banks continue to reevaluate their business models and risk appetites and some take on additional risk by expanding into new, less familiar, or even higher risk products/markets without adequate due diligence KPMG Community Bank Survey 2015 Semiannual Risk Perspective, Spring

29 Are you including risk /compliance folks in the strategic planning process? Have you established risk appetites that reach across business units? Do you document risks as a result of strategy and share that with the board? Who is tracking risks and what do they do with the information? 29

30 ERM & STRATEGY IS ABOUT STOPPING THE SUBCULTURE The threat is the subculture that exists within the bank. Those who are leading and supporting an agenda that is counterproductive to the bank s stated culture are leading the subculture. They may appear to agree with the strategic vision, but they have a better way of achieving it. A community bank s competitive advantage is its relationship based culture. If your ROA is below 1.0; if your non-interest bearing deposits aren t growing; if you re not keeping score of cross-sells; if you re not conducting telephone shops; if you don t have a deposit and acquisition strategy; then you don t have a relationship based culture. It s possible to have one without them, and it is quite possible that your bank is dominated by a subculture. Is Your Bank s Subculture Taking Over? SCMG The Texas Independent Banker January/February

31 SHIFTING YOUR BANK FROM MINIMIZING RISK TO BUILDING VALUE The approach of strategic planning should not be some sort of academic exercise to accomplish for the regulators. Rather, top-performing financial institutions in the country utilize planning to: 1. Define success over a specific time horizon 2. Delineate alternative paths to achieve these goals 3. Determine trigger points along the way 4. Examine the execution risks and conduct stress tests 5. Focus the bank on executing the stated goal the top performing banks start with a realistic goal in three to five years and then figure out how to accomplish the task. Strategic Planning in 2016 Robert Fehn FinPro BankNews September

32 1. Mimics risk categories identified by your regulators 2. Easily included into your strategic plan 3. Offers expertise that compliments the software 4. Provides a centralized repository for data collection, scoring, reporting, analyzing and storing in a real time environment 5. Facilitates work flow and risk assessment for management and monitoring 6. Tracks and includes Key Risk Indicators (KRIs) 7. Platform will sync information with Board Portal 32

33 Q&A 33

34 CONTACT ME (888) Ext Thank You! 34

National Risk Committee (NRC) Semiannual Risk Perspective. Fall 2015

Semiannual Risk Perspective. Fall 2015") National Risk Committee (NRC) Semiannual Risk Perspective Fall 2015 NRC Risk Priorities and Actions Underwriting Strategic Risk Interest Rate Risk Cybersecurity Compliance Easing confirmed in examinations

National Risk Committee (NRC) Semiannual Risk Perspective Fall 2015 NRC Risk Priorities and Actions Underwriting Strategic Risk Interest Rate Risk Cybersecurity Compliance Easing confirmed in examinations

Survey of Credit Underwriting Practices 2010

Survey of Credit Underwriting Practices 2010 Office of the Comptroller of the Currency August 2010 Contents Introduction...1 Part I: Overall Results...2 Primary Findings... 2 Commentary on Credit Risk...

Survey of Credit Underwriting Practices 2010 Office of the Comptroller of the Currency August 2010 Contents Introduction...1 Part I: Overall Results...2 Primary Findings... 2 Commentary on Credit Risk...

Survey of Credit Underwriting Practices 2005 Office of the Comptroller of the Currency National Credit Committee

Survey of Credit Underwriting Practices 25 Office of the Comptroller of the Currency National Credit Committee June 25 1 Table of Contents Introduction 3 Part I: Overall Results Primary Findings 4 Commentary...6

Survey of Credit Underwriting Practices 25 Office of the Comptroller of the Currency National Credit Committee June 25 1 Table of Contents Introduction 3 Part I: Overall Results Primary Findings 4 Commentary...6

Delivering Clarity to Credit Unions Through Expertise and Experience

Jeff Owen, The Rochdale Group September 2012 Delivering Clarity to Credit Unions Through Expertise and Experience Enterprise Risk Management Lending Execution and Risk Management Merger Strategy and Realization

Jeff Owen, The Rochdale Group September 2012 Delivering Clarity to Credit Unions Through Expertise and Experience Enterprise Risk Management Lending Execution and Risk Management Merger Strategy and Realization

New Products and Business Initiatives. 27th National Risk Management Training Conference

New Products and Business Initiatives 27th National Risk Management Training Conference Gregory J. Lyons May 1, 2013 Agenda Succeeding in a difficult regulatory environment Why offer, when, and who should

New Products and Business Initiatives 27th National Risk Management Training Conference Gregory J. Lyons May 1, 2013 Agenda Succeeding in a difficult regulatory environment Why offer, when, and who should

Survey of Credit Underwriting Practices Office of the Comptroller of the Currency National Credit Committee October 2004

Survey of Credit Underwriting Practices 2004 Office of the Comptroller of the Currency National Credit Committee October 2004 Table of Contents Introduction 3 Part I: Overall Results Primary Findings 4

Survey of Credit Underwriting Practices 2004 Office of the Comptroller of the Currency National Credit Committee October 2004 Table of Contents Introduction 3 Part I: Overall Results Primary Findings 4

Overview of ERM Assessment Viewpoints (June 2016) Overview

Overview") ERM assessment main category Culture & Governance Control & Capital Adequacy Profile & Measurement Application to Business Management Overview of ERM Assessment Viewpoints (June 2016) Overview Examine

ERM assessment main category Culture & Governance Control & Capital Adequacy Profile & Measurement Application to Business Management Overview of ERM Assessment Viewpoints (June 2016) Overview Examine

CLOUD-based Portfolio Analysis & Stress Testing (OCC & 47)

") CLOUD-based Portfolio Analysis & Stress Testing (OCC 2006-46 & 47) CLOUDecision A Fynsaas Financials Company Mark Copenhaver, Business Development Melissa Moul, Customer & Product Services Agenda What

CLOUD-based Portfolio Analysis & Stress Testing (OCC 2006-46 & 47) CLOUDecision A Fynsaas Financials Company Mark Copenhaver, Business Development Melissa Moul, Customer & Product Services Agenda What

Comptroller of the Currency Administrator of National Banks SURVEY OF CREDIT UNDERWRITING PRACTICES 2000

Comptroller of the Currency Administrator of National Banks SURVEY OF CREDIT UNDERWRITING PRACTICES 2000 SURVEY OF CREDIT UNDERWRITING PRACTICES 2000 Office of the Comptroller of the Currency Credit

Comptroller of the Currency Administrator of National Banks SURVEY OF CREDIT UNDERWRITING PRACTICES 2000 SURVEY OF CREDIT UNDERWRITING PRACTICES 2000 Office of the Comptroller of the Currency Credit

Credit Underwriting Practices

Comptroller of the Currency Administrator of National Banks US Department of the Treasury 2011 Survey of OF THE R C LE UR R EN C Y CO M P T R O L Credit Underwriting Practices 186 3 Contents Introduction...

Comptroller of the Currency Administrator of National Banks US Department of the Treasury 2011 Survey of OF THE R C LE UR R EN C Y CO M P T R O L Credit Underwriting Practices 186 3 Contents Introduction...

CREDIT RISK MANAGEMENT GUIDANCE FOR HOME EQUITY LENDING

Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision National Credit Union Administration CREDIT

Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision National Credit Union Administration CREDIT

Capital Speedboat Session 2. Charting your way through troubling waters FARIN & Associates Inc. Agenda

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

Draft for Consultation FICOM ICAAP Guide

Draft for Consultation FICOM ICAAP Guide BC Credit Unions November 2017 www.fic.gov.bc.ca Table of Contents INTRODUCTION... 1 FEATURES OF AN EFFECTIVE ICAAP... 2 I. Board and Management Oversight... 2

Draft for Consultation FICOM ICAAP Guide BC Credit Unions November 2017 www.fic.gov.bc.ca Table of Contents INTRODUCTION... 1 FEATURES OF AN EFFECTIVE ICAAP... 2 I. Board and Management Oversight... 2

Comptroller of the Currency Administrator of National Banks. Survey of Credit Underwriting Practices 2001

Comptroller of the Currency Administrator of National Banks Survey of Credit Underwriting Practices Comptroller of the Currency Administrator of National Banks Washington, DC 20219 June To: Board Members

Comptroller of the Currency Administrator of National Banks Survey of Credit Underwriting Practices Comptroller of the Currency Administrator of National Banks Washington, DC 20219 June To: Board Members

CRE Loan Concentrations in 2017: What You Need To Know

CRE Loan Concentrations in 2017: What You Need To Know NEW JERSEY BANKERS ASSOCIATION 113 th Annual Conference The Breakers, Palm Beach, FL May 17-21, 2017 Michael T. Rave Partner Day Pitney LLP mrave@daypitney.com

CRE Loan Concentrations in 2017: What You Need To Know NEW JERSEY BANKERS ASSOCIATION 113 th Annual Conference The Breakers, Palm Beach, FL May 17-21, 2017 Michael T. Rave Partner Day Pitney LLP mrave@daypitney.com

Consultation Paper. FSB Principles for Sound Residential Mortgage. Underwriting Practices

Consultation Paper FSB Principles for Sound Residential Mortgage Underwriting Practices 26 October 2011 Table of Contents Page Definitions... i I. Introduction... 1 II. Principles... 2 1. Effective verification

Consultation Paper FSB Principles for Sound Residential Mortgage Underwriting Practices 26 October 2011 Table of Contents Page Definitions... i I. Introduction... 1 II. Principles... 2 1. Effective verification

Business Auditing - Enterprise Risk Management. October, 2018

Business Auditing - Enterprise Risk Management October, 2018 Contents The present document is aimed to: 1 Give an overview of the Risk Management framework 2 Illustrate an ERM model Page 2 What is a risk?

Business Auditing - Enterprise Risk Management October, 2018 Contents The present document is aimed to: 1 Give an overview of the Risk Management framework 2 Illustrate an ERM model Page 2 What is a risk?

Guidance from Bank Regulators on Managing Commercial Real Estate Concentrations

GLOBAL BANKING & MARKETS Guidance from Bank Regulators on Managing Commercial Real Estate Concentrations Richard Daingerfield Chief Legal Officer, The Royal Bank of Scotland plc NY Branch Chair, Banking

GLOBAL BANKING & MARKETS Guidance from Bank Regulators on Managing Commercial Real Estate Concentrations Richard Daingerfield Chief Legal Officer, The Royal Bank of Scotland plc NY Branch Chair, Banking

Risk Review Committee Charter

Risk Review Committee Charter 1. About the Charter Purpose The Board of Directors of Coast Capital Savings (the Board ) has delegated to the Risk Review Committee (the Committee ) the responsibilities

Risk Review Committee Charter 1. About the Charter Purpose The Board of Directors of Coast Capital Savings (the Board ) has delegated to the Risk Review Committee (the Committee ) the responsibilities

CHARTER PEOPLE S UNITED FINANCIAL, INC. ENTERPRISE RISK COMMITTEE

CHARTER PEOPLE S UNITED FINANCIAL, INC. ENTERPRISE RISK COMMITTEE Purpose and Authority: The Enterprise Risk Committee (the Committee ) has been established by the Board of Directors of People s United

CHARTER PEOPLE S UNITED FINANCIAL, INC. ENTERPRISE RISK COMMITTEE Purpose and Authority: The Enterprise Risk Committee (the Committee ) has been established by the Board of Directors of People s United

Southeast Bankers Outreach Forum

Southeast Bankers Outreach Forum CRE Exposures and Sound Risk Management Practices Date: September 28, 2017 Presented by: Trey Wheeler Assistant Vice President Office - 404.498.7152 trey.wheeler@atl.frb.org

Southeast Bankers Outreach Forum CRE Exposures and Sound Risk Management Practices Date: September 28, 2017 Presented by: Trey Wheeler Assistant Vice President Office - 404.498.7152 trey.wheeler@atl.frb.org

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE. Nepal Rastra Bank Bank Supervision Department. August 2012 (updated July 2013)

") INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics. Key Lending Issues from an Examiner Perspective

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics Key Lending Issues from an Examiner Perspective Lending Hot Topics Credit Risk Related Items Concentration Risks & Trends Residential Real Estate

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics Key Lending Issues from an Examiner Perspective Lending Hot Topics Credit Risk Related Items Concentration Risks & Trends Residential Real Estate

BB&T Corporation. Dodd-Frank Act Company-run Mid-cycle Stress Test Disclosure BB&T Severely Adverse Scenario. October 18, 2018.

BB&T Corporation Dodd-Frank Act Company-run Mid-cycle Stress Test Disclosure BB&T Severely Adverse Scenario October 18, 2018 1 Introduction BB&T Corporation (BB&T) is one of the largest financial services

BB&T Corporation Dodd-Frank Act Company-run Mid-cycle Stress Test Disclosure BB&T Severely Adverse Scenario October 18, 2018 1 Introduction BB&T Corporation (BB&T) is one of the largest financial services

Account Level Administration and Investment Responsibilities Specifically Unique and Hard to Value Assets

November 4, 2015 Donald F. Moore, Jr./Bearmoor, LLC and Brad Davidson/Unique Asset Partners LLC Account Level Administration and Investment Responsibilities Specifically Unique and Hard to Value Assets

November 4, 2015 Donald F. Moore, Jr./Bearmoor, LLC and Brad Davidson/Unique Asset Partners LLC Account Level Administration and Investment Responsibilities Specifically Unique and Hard to Value Assets

Managing Commercial Real Estate Lending Risk from Loan Origination through Maturity: The Potential for Pain

by Managing Commercial Real Estate Lending Risk from Loan Origination through Maturity: The Potential for Pain Regulators have strongly signaled their unease with growing CRE concentrations Smaller banks

by Managing Commercial Real Estate Lending Risk from Loan Origination through Maturity: The Potential for Pain Regulators have strongly signaled their unease with growing CRE concentrations Smaller banks

Liquidity Management. 158 Route 206 Gladstone, NJ P: (908) Home FinPro, Inc.

Home FinPro, Inc.") Liquidity Management 158 Route 206 Gladstone, NJ 07934 P: (908) 234-9398 finpro@finpro.us www.finpro.us 0 Liquidity: you always have too much until you need it!! 1 Banks must take a holistic view of its

Liquidity Management 158 Route 206 Gladstone, NJ 07934 P: (908) 234-9398 finpro@finpro.us www.finpro.us 0 Liquidity: you always have too much until you need it!! 1 Banks must take a holistic view of its

NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL

GUIDANCE MANUAL") NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL Created by the NAIC Group Solvency Issues Working Group Of the Solvency Modernization Initiatives (EX) Task Force 2011 National Association

NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL Created by the NAIC Group Solvency Issues Working Group Of the Solvency Modernization Initiatives (EX) Task Force 2011 National Association

Risk Concentrations Principles

Risk Concentrations Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS Basel December

Risk Concentrations Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS Basel December

CRE Lending Best Practices

CRE Lending Best Practices Understanding the risk and rewards P R E S E N T E D B Y Rob Ashbaugh Executive Risk Management Consultant Sageworks Disclaimer This presentation may include statements that

CRE Lending Best Practices Understanding the risk and rewards P R E S E N T E D B Y Rob Ashbaugh Executive Risk Management Consultant Sageworks Disclaimer This presentation may include statements that

Timothy F Geithner: Hedge funds and their implications for the financial system

Timothy F Geithner: Hedge funds and their implications for the financial system Keynote address by Mr Timothy F Geithner, President and Chief Executive Officer of the Federal Reserve Bank of New York,

Timothy F Geithner: Hedge funds and their implications for the financial system Keynote address by Mr Timothy F Geithner, President and Chief Executive Officer of the Federal Reserve Bank of New York,

BB&T Corporation. Dodd-Frank Act Company-run Mid-cycle Stress Test Disclosure BB&T Severely Adverse Scenario

BB&T Corporation Dodd-Frank Act Company-run Mid-cycle Stress Test Disclosure BB&T Severely Adverse Scenario October 19, 2017 1 Introduction BB&T Corporation (BB&T) is one of the largest financial services

BB&T Corporation Dodd-Frank Act Company-run Mid-cycle Stress Test Disclosure BB&T Severely Adverse Scenario October 19, 2017 1 Introduction BB&T Corporation (BB&T) is one of the largest financial services

TRENDS IN ASSET QUALITY AVERAGE LEVEL OF ADVERSELY GRADED ASSETS

Trends in Asset Quality Average Levels Based on Steve H. Powell & Company client data, during the Fourth Quarter 2016, the average level of adversely graded assets decreased as a percentage of total assets

Trends in Asset Quality Average Levels Based on Steve H. Powell & Company client data, during the Fourth Quarter 2016, the average level of adversely graded assets decreased as a percentage of total assets

Victoria Bennett Regional Lending Specialist. NCUA Hot Topics. CUNA Lending Council Conference. November 4, 2014

Victoria Bennett Regional Lending Specialist NCUA Hot Topics CUNA Lending Council Conference November 4, 2014 AGENDA Short update on credit unions Discussion of hot topics Suggestions 12000 Decline in

Victoria Bennett Regional Lending Specialist NCUA Hot Topics CUNA Lending Council Conference November 4, 2014 AGENDA Short update on credit unions Discussion of hot topics Suggestions 12000 Decline in

GUIDELINE ON ENTERPRISE RISK MANAGEMENT

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

Assessing Credit Risk

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

Understanding Enterprise Risk Management: An Overview

Understanding Enterprise Risk Management: An Overview 05/2016 What is Risk? An uncertain event It exists in the future Has a cause and effect Impacts objectives Its effect may be positive and/or negative

Understanding Enterprise Risk Management: An Overview 05/2016 What is Risk? An uncertain event It exists in the future Has a cause and effect Impacts objectives Its effect may be positive and/or negative

Susan Schmidt Bies: Enterprise perspectives in financial institution supervision

Susan Schmidt Bies: Enterprise perspectives in financial institution supervision Remarks by Ms Susan Schmidt Bies, Member of the Board of Governors of the US Federal Reserve System, at the University of

Susan Schmidt Bies: Enterprise perspectives in financial institution supervision Remarks by Ms Susan Schmidt Bies, Member of the Board of Governors of the US Federal Reserve System, at the University of

Meridian Finance & Investment Limited Disclosure under Pillar III on Capital Adequacy and Market Discipline As on December 31, 2017

Meridian Finance & Investment Limited Disclosure under Pillar III on Capital Adequacy and Market Discipline As on December 31, 2017 Significance of Capital Adequacy Capital is the foundation of any business.

Meridian Finance & Investment Limited Disclosure under Pillar III on Capital Adequacy and Market Discipline As on December 31, 2017 Significance of Capital Adequacy Capital is the foundation of any business.

Certified Enterprise Risk Professional (CERP) Test Content Outline

Test Content Outline") Certified Enterprise Risk Professional (CERP) Test Content Outline SECTION 1: RISK GOVERNANCE Domain 1: Board and Senior Management Oversight (8%) Task 1: Provide relevant, timely, and accurate information

Certified Enterprise Risk Professional (CERP) Test Content Outline SECTION 1: RISK GOVERNANCE Domain 1: Board and Senior Management Oversight (8%) Task 1: Provide relevant, timely, and accurate information

Risk Management. Investor Day 2016

Risk Management Investor Day 2016 Risk Management at U.S. Bancorp Risk and governance starts at the top The Risk Management Committee of the Board of Directors approves and oversees the risk management

Risk Management Investor Day 2016 Risk Management at U.S. Bancorp Risk and governance starts at the top The Risk Management Committee of the Board of Directors approves and oversees the risk management

Office of Material Loss Reviews Report No. MLR Material Loss Review of Great Basin Bank of Nevada, Elko, Nevada

Office of Material Loss Reviews Report No. MLR-10-008 Material Loss Review of Great Basin Bank of Nevada, Elko, Nevada December 2009 Executive Summary Why We Did The Audit Material Loss Review of Great

Office of Material Loss Reviews Report No. MLR-10-008 Material Loss Review of Great Basin Bank of Nevada, Elko, Nevada December 2009 Executive Summary Why We Did The Audit Material Loss Review of Great

INTERNAL AUDIT. Supervisory Examiner

INTERNAL AUDIT Elliott Davis Decosimo May 2015 Michael P. Egan Supervisory Examiner Overview Back to Basics Approach Risk Assessments Audit Planning Audit Workprograms & Sampling Methodology Deficiency

INTERNAL AUDIT Elliott Davis Decosimo May 2015 Michael P. Egan Supervisory Examiner Overview Back to Basics Approach Risk Assessments Audit Planning Audit Workprograms & Sampling Methodology Deficiency

IT Risk in Credit Unions - Thematic Review Findings

IT Risk in Credit Unions - Thematic Review Findings January 2018 Central Bank of Ireland Findings from IT Thematic Review in Credit Unions Page 2 Table of Contents 1. Executive Summary... 3 1.1 Purpose...

IT Risk in Credit Unions - Thematic Review Findings January 2018 Central Bank of Ireland Findings from IT Thematic Review in Credit Unions Page 2 Table of Contents 1. Executive Summary... 3 1.1 Purpose...

Residential Mortgage. Underwriting Policy. Sound Business & Financial Practices

Residential Mortgage 2019 Underwriting Policy Three Point Capital Corp. ( TPC ) has published this Residential Mortgage Underwriting Policy ( TPC Policy ), which was adapted from and based on the November

Residential Mortgage 2019 Underwriting Policy Three Point Capital Corp. ( TPC ) has published this Residential Mortgage Underwriting Policy ( TPC Policy ), which was adapted from and based on the November

Credit Risk Management and the ALCO Process

Credit Risk Management and the ALCO Process David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Definition: Asset/Liability Management asset/liability management is the processes of

Credit Risk Management and the ALCO Process David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Definition: Asset/Liability Management asset/liability management is the processes of

Credit Risk Management and the ALCO Process. Asset/Liability Management

Credit Risk Management and the ALCO Process David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Asset/Liability Management Definition: asset/liability management is the processes of

Credit Risk Management and the ALCO Process David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Asset/Liability Management Definition: asset/liability management is the processes of

LOAN PORTFOLIO MANAGEMENT - YEAR 2

LOAN PORTFOLIO MANAGEMENT - YEAR 2 Loan Portfolio Management - Strategies & Tools Michael A. Wear Senior Credit Analyst First National Bank of Omaha Omaha, NE mikewear@hotmail.com 402-871-9067 July 30,

LOAN PORTFOLIO MANAGEMENT - YEAR 2 Loan Portfolio Management - Strategies & Tools Michael A. Wear Senior Credit Analyst First National Bank of Omaha Omaha, NE mikewear@hotmail.com 402-871-9067 July 30,

STRESS TESTING GUIDELINE

c DRAFT STRESS TESTING GUIDELINE November 2011 TABLE OF CONTENTS Preamble... 2 Introduction... 3 Coming into effect and updating... 6 1. Stress testing... 7 A. Concept... 7 B. Approaches underlying stress

c DRAFT STRESS TESTING GUIDELINE November 2011 TABLE OF CONTENTS Preamble... 2 Introduction... 3 Coming into effect and updating... 6 1. Stress testing... 7 A. Concept... 7 B. Approaches underlying stress

Enterprise Risk Management and the ALCO Process

Enterprise Risk Management and the ALCO Process Session 1: Gathering the Parts David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 ext 4217 Agenda Session 1 Overview of ERM Evolution of ERM

Enterprise Risk Management and the ALCO Process Session 1: Gathering the Parts David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 ext 4217 Agenda Session 1 Overview of ERM Evolution of ERM

Amex Bank of Canada. Basel III Pillar III Disclosures December 31, AXP Internal Page 1 of 15

December 31, 2013 AXP Internal Page 1 of 15 Table of Contents 1 Scope of application 3 2 Capital structure and adequacy 4 3 Credit risk management 6 4 Asset liability management 11 Structural interest

December 31, 2013 AXP Internal Page 1 of 15 Table of Contents 1 Scope of application 3 2 Capital structure and adequacy 4 3 Credit risk management 6 4 Asset liability management 11 Structural interest

Pillar 3 Disclosure Statement

Pillar 3 Disclosure Statement Last Updated: December, 2017 Disclosure Statement This Pillar 3 Disclosure as at September 30, 2017 contains statements that are considered "forwardlooking statements," including

Pillar 3 Disclosure Statement Last Updated: December, 2017 Disclosure Statement This Pillar 3 Disclosure as at September 30, 2017 contains statements that are considered "forwardlooking statements," including

Risk appetite frameworks: good progress but still room for improvement

Risk appetite frameworks: good progress but still room for improvement Speech by Danièle Nouy, Chair of the Supervisory Board of the ECB, at a conference on banks risk appetite frameworks, Ljubljana, 10

Risk appetite frameworks: good progress but still room for improvement Speech by Danièle Nouy, Chair of the Supervisory Board of the ECB, at a conference on banks risk appetite frameworks, Ljubljana, 10

Guidance Note System of Governance - Insurance Transition to Governance Requirements established under the Solvency II Directive

Guidance Note Transition to Governance Requirements established under the Solvency II Directive Issued : 31 December 2013 Table of Contents 1.Introduction... 4 2. Detailed Guidelines... 4 General governance

Guidance Note Transition to Governance Requirements established under the Solvency II Directive Issued : 31 December 2013 Table of Contents 1.Introduction... 4 2. Detailed Guidelines... 4 General governance

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes. George Brady. IAIS Deputy Secretary General

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes George Brady IAIS Deputy Secretary General Table of Contents 1. Introduction 2. Governance and an Enterprise Risk Management (ERM)

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes George Brady IAIS Deputy Secretary General Table of Contents 1. Introduction 2. Governance and an Enterprise Risk Management (ERM)

Mid-Term Plan FY Primary Secondary Bank: the partner of choice Leveraging Core Competencies

May 14, 2018 Company name: Aozora Bank, Ltd. Name of representative: Shinsuke Baba, President and CEO Listed exchange: TSE, Code 8304 Enquiries: Atsuhiko Goto Business Strategy Division (03 6752 1111)

May 14, 2018 Company name: Aozora Bank, Ltd. Name of representative: Shinsuke Baba, President and CEO Listed exchange: TSE, Code 8304 Enquiries: Atsuhiko Goto Business Strategy Division (03 6752 1111)

What Is Asset/Liability Management?

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

Quarterly Conversations with the Federal Reserve Bank of St. Louis

Quarterly Conversations with the Federal Reserve Bank of St. Louis Live from Bear State Bank Little Rock, AR September 8, 2016 1 Options to Join the Conversation Webinar and audio Click on the link: https://www.webcaster4.com/webcast/page/584/16844

Quarterly Conversations with the Federal Reserve Bank of St. Louis Live from Bear State Bank Little Rock, AR September 8, 2016 1 Options to Join the Conversation Webinar and audio Click on the link: https://www.webcaster4.com/webcast/page/584/16844

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers Objectives and Key Requirements of this Prudential Standard Effective risk management is fundamental to the prudent management

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers Objectives and Key Requirements of this Prudential Standard Effective risk management is fundamental to the prudent management

FINANCIAL SECURITY AND STABILITY

FINANCIAL SECURITY AND STABILITY Durmuş Yılmaz Governor Central Bank of the Republic of Turkey Measuring and Fostering the Progress of Societies: The OECD World Forum on Statistics, Knowledge and Policy

FINANCIAL SECURITY AND STABILITY Durmuş Yılmaz Governor Central Bank of the Republic of Turkey Measuring and Fostering the Progress of Societies: The OECD World Forum on Statistics, Knowledge and Policy

Description: Sound Risk Management Practices. Subject: Leveraged Financing PURPOSE

Subject: Leveraged Financing Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision Description: Sound

Subject: Leveraged Financing Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision Description: Sound

Understanding Business Borrowers $150 COURSE DESCRIPTIONS

ABA SELF-PACED BUSINESS BANKING AND COMMERCIAL LENDING PROGRAMS A $10.00 shipping, recordkeeping and administrative fee will be added to all self-paced enrollments. Course Descriptions Below Register Now!

ABA SELF-PACED BUSINESS BANKING AND COMMERCIAL LENDING PROGRAMS A $10.00 shipping, recordkeeping and administrative fee will be added to all self-paced enrollments. Course Descriptions Below Register Now!

SCHOOLBUILD WEBINAR SERIES: CHARTER SCHOOL FACILITY FINANCE 101

SCHOOLBUILD WEBINAR SERIES: CHARTER SCHOOL FACILITY FINANCE 101 October 19 th, 2016 Presented by: Michelle Liberati, Executive Vice President, Charter Schools Development Corporation Molly Melloh, Director,

SCHOOLBUILD WEBINAR SERIES: CHARTER SCHOOL FACILITY FINANCE 101 October 19 th, 2016 Presented by: Michelle Liberati, Executive Vice President, Charter Schools Development Corporation Molly Melloh, Director,

Executing Effective Validations

Executing Effective Validations By Sarah Davies Senior Vice President, Analytics, Research and Product Management, VantageScore Solutions, LLC Oneof the key components to successfully utilizing risk management

Executing Effective Validations By Sarah Davies Senior Vice President, Analytics, Research and Product Management, VantageScore Solutions, LLC Oneof the key components to successfully utilizing risk management

ERM Sample Flashcards

ERM Sample Flashcards You have downloaded a sample of our ERM flashcards. The flashcards are designed to help you memorize key material for the SOA s ERM exam. The flashcards are in a Q&A format that is

ERM Sample Flashcards You have downloaded a sample of our ERM flashcards. The flashcards are designed to help you memorize key material for the SOA s ERM exam. The flashcards are in a Q&A format that is

Managing Third Party Risk in the ACH Network

Managing Third Party Risk in the ACH Network Tony DaSilva, AAP, CISA Senior Examiner Federal Reserve Bank of Atlanta Paul A. Carrubba Partner Adams and Reese LLP Disclaimer THE VIEWS AND OPINIONS EXPRESSED

Managing Third Party Risk in the ACH Network Tony DaSilva, AAP, CISA Senior Examiner Federal Reserve Bank of Atlanta Paul A. Carrubba Partner Adams and Reese LLP Disclaimer THE VIEWS AND OPINIONS EXPRESSED

Measurement of Market Risk

Measurement of Market Risk Market Risk Directional risk Relative value risk Price risk Liquidity risk Type of measurements scenario analysis statistical analysis Scenario Analysis A scenario analysis measures

Measurement of Market Risk Market Risk Directional risk Relative value risk Price risk Liquidity risk Type of measurements scenario analysis statistical analysis Scenario Analysis A scenario analysis measures

Consumer Compliance Hot Topics

Consumer Compliance Hot Topics Agenda Regulatory Timeline: Issued in 2014 On the Horizon for 2015 Areas of Supervisory Focus: Fair Lending Unfair or Deceptive Acts or Practices (UDAP) Flood Vendor Management

Consumer Compliance Hot Topics Agenda Regulatory Timeline: Issued in 2014 On the Horizon for 2015 Areas of Supervisory Focus: Fair Lending Unfair or Deceptive Acts or Practices (UDAP) Flood Vendor Management

Risk Appetite. What is risk appetite?

Risk Appetite Presented by Mike Claffey 30 March 2011 What is risk appetite? Risk appetite is the degree of risk that an organisation is willing to accept in order to achieve its objectives, both in terms

Risk Appetite Presented by Mike Claffey 30 March 2011 What is risk appetite? Risk appetite is the degree of risk that an organisation is willing to accept in order to achieve its objectives, both in terms

RMA 2016 Annual Risk Management Conference Dallas, TX

RMA 2016 Annual Risk Management Conference Dallas, TX 1 Michael G. Nassy EVP and Chief Credit Officer First Virginia Community Bank mnassy@fvcbank.com (703) 436-3886 Roger G. Shumway EVP and Chief Credit

RMA 2016 Annual Risk Management Conference Dallas, TX 1 Michael G. Nassy EVP and Chief Credit Officer First Virginia Community Bank mnassy@fvcbank.com (703) 436-3886 Roger G. Shumway EVP and Chief Credit

REINSURANCE RISK MANAGEMENT GUIDELINE

DRAFT DRAFT REINSURANCE RISK MANAGEMENT GUIDELINE Initial publication: April 2010 Update: July 2013 Table of Contents Preamble... 2 Introduction... 3 Scope... 5 Coming into effect and updating... 6 1.

DRAFT DRAFT REINSURANCE RISK MANAGEMENT GUIDELINE Initial publication: April 2010 Update: July 2013 Table of Contents Preamble... 2 Introduction... 3 Scope... 5 Coming into effect and updating... 6 1.

Investor Presentation. March 2017

Investor Presentation March 2017 Safe Harbor Statement Safe Harbor statement under Private Securities Litigation Reform Act of 1995: This presentation contains forward-looking statements, including statements

Investor Presentation March 2017 Safe Harbor Statement Safe Harbor statement under Private Securities Litigation Reform Act of 1995: This presentation contains forward-looking statements, including statements

IMPLEMENTATION NOTE. Corporate Governance Oversight at IRB Institutions

IMPLEMENTATION NOTE Subject: Category: Capital No: A-1 Date: January 2006 I. Introduction This document elaborates on some of the requirements for the internal ratings-based (IRB) approach contained in

IMPLEMENTATION NOTE Subject: Category: Capital No: A-1 Date: January 2006 I. Introduction This document elaborates on some of the requirements for the internal ratings-based (IRB) approach contained in

BB&T Corporation. Dodd-Frank Act Company-run Stress Test Disclosure

BB&T Corporation Dodd-Frank Act Company-run Stress Test Disclosure June 21, 2018 1 Introduction BB&T Corporation (BB&T) is one of the largest financial services holding companies in the U.S. with approximately

BB&T Corporation Dodd-Frank Act Company-run Stress Test Disclosure June 21, 2018 1 Introduction BB&T Corporation (BB&T) is one of the largest financial services holding companies in the U.S. with approximately

2018 ICBA Regulator Panel Agricultural Lending

2018 ICBA Regulator Panel Agricultural Lending March 15, 2018 Keith Osborne ADC Wichita Field Office 1 Agenda Agricultural Lending Risk Management Practices Risk Rating Agricultural Loans References Questions

2018 ICBA Regulator Panel Agricultural Lending March 15, 2018 Keith Osborne ADC Wichita Field Office 1 Agenda Agricultural Lending Risk Management Practices Risk Rating Agricultural Loans References Questions

Revising the principles for the supervision of financial conglomerates

Revising the principles for the supervision of financial conglomerates Conglomerates conference Brussels 28 June 2012 Olivier Prato Teresa Rutledge 1 Introduction About the Joint Forum G-20 request resulted

Revising the principles for the supervision of financial conglomerates Conglomerates conference Brussels 28 June 2012 Olivier Prato Teresa Rutledge 1 Introduction About the Joint Forum G-20 request resulted

STRESS TESTING Transition to DFAST compliance

WHITE PAPER STRESS TESTING Transition to DFAST compliance Abstract The objective of this document is to explain the challenges related to stress testing that arise when a Community Bank crosses $0 Billion

WHITE PAPER STRESS TESTING Transition to DFAST compliance Abstract The objective of this document is to explain the challenges related to stress testing that arise when a Community Bank crosses $0 Billion

BERMUDA MONETARY AUTHORITY THE INSURANCE CODE OF CONDUCT FEBRUARY 2010

Table of Contents 0. Introduction..2 1. Preliminary...3 2. Proportionality principle...3 3. Corporate governance...4 4. Risk management..9 5. Governance mechanism..17 6. Outsourcing...21 7. Market discipline

Table of Contents 0. Introduction..2 1. Preliminary...3 2. Proportionality principle...3 3. Corporate governance...4 4. Risk management..9 5. Governance mechanism..17 6. Outsourcing...21 7. Market discipline

BOFI HOLDING, INC. Investor Presentation September 2017

BOFI HOLDING, INC. Investor Presentation September 2017 NASDAQ: BOFI0 Safe Harbor This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act

BOFI HOLDING, INC. Investor Presentation September 2017 NASDAQ: BOFI0 Safe Harbor This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act

CAPITAL MANAGEMENT GUIDELINE

CAPITAL MANAGEMENT GUIDELINE May 2015 Capital Management Guideline 1 Preambule TABLE OF CONTENTS Preamble... 3 Scope... 4 Coming into effect and updating... 5 Introduction... 6 1. Capital management...

CAPITAL MANAGEMENT GUIDELINE May 2015 Capital Management Guideline 1 Preambule TABLE OF CONTENTS Preamble... 3 Scope... 4 Coming into effect and updating... 5 Introduction... 6 1. Capital management...

A.M. Best s New Risk Management Standards

A.M. Best s New Risk Management Standards Stephanie Guethlein McElroy, A.M. Best Manager, Rating Criteria and Rating Relations Hubert Mueller, Towers Perrin, Principal March 24, 2008 Introduction A.M.

A.M. Best s New Risk Management Standards Stephanie Guethlein McElroy, A.M. Best Manager, Rating Criteria and Rating Relations Hubert Mueller, Towers Perrin, Principal March 24, 2008 Introduction A.M.

EMERGING CONSUMER RISKS FOR COMMUNITY BANKS

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

Leveraging an organization s current risk management to create a sustainable ERM program. Thursday, January 15, 2015

Leveraging an organization s current risk management to create a sustainable ERM program Thursday, January 15, 2015 Augustine Doe Ron Marx AGENDA Pg 1 Pg 2 Pg 3 Pg 4 Pg 5 Pg 6 Pg 7 Pg 8 Pg 9 Pg 10 Pg 11

Leveraging an organization s current risk management to create a sustainable ERM program Thursday, January 15, 2015 Augustine Doe Ron Marx AGENDA Pg 1 Pg 2 Pg 3 Pg 4 Pg 5 Pg 6 Pg 7 Pg 8 Pg 9 Pg 10 Pg 11

Providing simple solutions to complex problems with another helpful white paper from Banker s Toolbox September 2014

September 2014 A Table of Contents Introduction pg. 3-4 Risk Management pg. 5 Individual Lending Decisions pg. 6 Strategic & Capital Planning pg. 7 Conclusion pg. 8 About Banker s Toolbox pg. 9 ABA Endorsement

September 2014 A Table of Contents Introduction pg. 3-4 Risk Management pg. 5 Individual Lending Decisions pg. 6 Strategic & Capital Planning pg. 7 Conclusion pg. 8 About Banker s Toolbox pg. 9 ABA Endorsement

P&G Banking A D V I S O R Spring 2009

P&G Banking A D V I S O R Spring 2009 Why ERM? Enterprise risk management on critical upswing Commercial real estate De-stressing with stress testing Uncover cash sources with cost segregation 6 ways to

P&G Banking A D V I S O R Spring 2009 Why ERM? Enterprise risk management on critical upswing Commercial real estate De-stressing with stress testing Uncover cash sources with cost segregation 6 ways to

Sampo Group Risk Management Principles. 9 May 2018

Sampo Group Risk Management Principles 9 May 2018 Table of contents 1. The Objectives, Tasks and Motivation of the Risk Management Process 4 2. General Group Level Risk Statements 7 2.1 Risk Appetite 7

Sampo Group Risk Management Principles 9 May 2018 Table of contents 1. The Objectives, Tasks and Motivation of the Risk Management Process 4 2. General Group Level Risk Statements 7 2.1 Risk Appetite 7

Enterprise Risk Management

Enterprise Risk Management Navigating the Enterprise Risk Management Landscape Alp E. Can Director of Enterprise Risk Management, FHLBank Atlanta North Carolina Bankers Association August 31, 2016 Building

Enterprise Risk Management Navigating the Enterprise Risk Management Landscape Alp E. Can Director of Enterprise Risk Management, FHLBank Atlanta North Carolina Bankers Association August 31, 2016 Building

All of the Method None of the Madness

CECL Simplified Current Expected Credit Losses ASU 2016-13 All of the Method None of the Madness The ProBank Austin 2017 Webinar Series November 9, 2017 11:00 AM ESDT Live Case Study - CECL I. Example

CECL Simplified Current Expected Credit Losses ASU 2016-13 All of the Method None of the Madness The ProBank Austin 2017 Webinar Series November 9, 2017 11:00 AM ESDT Live Case Study - CECL I. Example

The company s capital (in millions of $) determined according to Basel III requirements is:

determined according to Basel III requirements is:") Basel Pillar Three Disclosure as of September 30, 2017 1. Introduction Industrial Alliance Trust Inc. ( ia Trust or the company ) is a trust and loan company subject to the Trust and Loan Companies Act

Basel Pillar Three Disclosure as of September 30, 2017 1. Introduction Industrial Alliance Trust Inc. ( ia Trust or the company ) is a trust and loan company subject to the Trust and Loan Companies Act

Identifying, Assessing and Mitigating Potential Redlining Risk

Identifying, Assessing and Mitigating Potential Redlining Risk Objectives Understanding Potential Redlining Risk Understanding the Reasonable Expected Market Area (REMA) vs CRA Assessment Area Understanding

Identifying, Assessing and Mitigating Potential Redlining Risk Objectives Understanding Potential Redlining Risk Understanding the Reasonable Expected Market Area (REMA) vs CRA Assessment Area Understanding

Securitization. Management exercises authority that should rest with the board or engages in activities that expose the institution to excessive risk.

Securitization Standards Examiners should evaluate the above-captioned function against the following control and performance standards. The Standards represent control and performance objectives that

Securitization Standards Examiners should evaluate the above-captioned function against the following control and performance standards. The Standards represent control and performance objectives that

Susan Schmidt Bies: A supervisory perspective on enterprise risk management

Susan Schmidt Bies: A supervisory perspective on enterprise risk management Remarks by Ms Susan Schmidt Bies, Member of the Board of Governors of the US Federal Reserve System, at the American Bankers

Susan Schmidt Bies: A supervisory perspective on enterprise risk management Remarks by Ms Susan Schmidt Bies, Member of the Board of Governors of the US Federal Reserve System, at the American Bankers

Pillar 2 - Supervisory Review Process

B ASEL II F RAMEWORK The Supervisory Review Process (Pillar 2) Rules and Guidelines Revised: February 2018 CAYMAN ISLANDS MONETARY AUTHORITY Cayman Islands Monetary Authority Page 1 Table of Contents Introduction...

B ASEL II F RAMEWORK The Supervisory Review Process (Pillar 2) Rules and Guidelines Revised: February 2018 CAYMAN ISLANDS MONETARY AUTHORITY Cayman Islands Monetary Authority Page 1 Table of Contents Introduction...

Beneficial Ownership and Due Diligence for Commercial Lenders NEW JERSEY BANKERS ASSOCIATION COMMERCIAL REAL ESTATE CONFERENCE JUNE 29, 2017

Beneficial Ownership and Due Diligence for Commercial Lenders NEW JERSEY BANKERS ASSOCIATION COMMERCIAL REAL ESTATE CONFERENCE JUNE 29, 2017 Agenda Why does due diligence matter? The Mechanics of due diligence

Beneficial Ownership and Due Diligence for Commercial Lenders NEW JERSEY BANKERS ASSOCIATION COMMERCIAL REAL ESTATE CONFERENCE JUNE 29, 2017 Agenda Why does due diligence matter? The Mechanics of due diligence

INTEGRATED RISK MANAGEMENT GUIDELINE

INTEGRATED RISK MANAGEMENT GUIDELINE Initial publication: April 2009 Updated: May 2015 TABLE OF CONTENTS Preamble... ii Scope... iii Coming into effect and updating... iv Introduction... v 1. Integrated

INTEGRATED RISK MANAGEMENT GUIDELINE Initial publication: April 2009 Updated: May 2015 TABLE OF CONTENTS Preamble... ii Scope... iii Coming into effect and updating... iv Introduction... v 1. Integrated

P&G Banking A D V I S O R Summer 2012

P&G Banking A D V I S O R Summer 2012 Managing outsourcing risks Wealth management programs How to carry a millionaire Bank Wire Cross-collateralization: Handle with care Cross-collateralization: Handle

P&G Banking A D V I S O R Summer 2012 Managing outsourcing risks Wealth management programs How to carry a millionaire Bank Wire Cross-collateralization: Handle with care Cross-collateralization: Handle

NCUA Regulatory Update on ALM

Peter Jensen, Regional Capital Markets Specialist NCUA, Region 4, Division of Special Actions NCUA Regulatory Update on ALM University for Credit Unions September 23, 2014 Agenda Introduction Interest

Peter Jensen, Regional Capital Markets Specialist NCUA, Region 4, Division of Special Actions NCUA Regulatory Update on ALM University for Credit Unions September 23, 2014 Agenda Introduction Interest

11/15/2016. Enterprise Risk Management. Building FHLBank Atlanta s ERM Program. FHLBank Atlanta. Navigating the Enterprise Risk Management Landscape

Enterprise Risk Management Navigating the Enterprise Risk Management Landscape Alp E. Can Director of Enterprise Risk Management, FHLBank Atlanta Virginia Bankers Association November 16, 2016 Building

Enterprise Risk Management Navigating the Enterprise Risk Management Landscape Alp E. Can Director of Enterprise Risk Management, FHLBank Atlanta Virginia Bankers Association November 16, 2016 Building

Regulatory Impact Assessment RBNZ Liquidity requirements for locally incorporated banks

Regulatory Impact Assessment RBNZ Liquidity requirements for locally incorporated banks Executive summary 1 A strong liquidity profile across banks is important for the maintenance of a sound and efficient

Regulatory Impact Assessment RBNZ Liquidity requirements for locally incorporated banks Executive summary 1 A strong liquidity profile across banks is important for the maintenance of a sound and efficient

1. INTRODUCTION 1 2. OVERVIEW OF THE BUSINESS 1 4. CAPITAL ADEQUACY & OWN FUNDS 6 5. CAPITAL REQUIREMENTS 7 6. REMUNERATION POLICY 10

etoro (UK) Limited Pillar 3 Risk Management Disclosure Report 2016 Contents 1. INTRODUCTION 1 2. OVERVIEW OF THE BUSINESS 1 3. RISK MANAGEMENT OBJECTIVES & POLICIES 1 4. CAPITAL ADEQUACY & OWN FUNDS 6

etoro (UK) Limited Pillar 3 Risk Management Disclosure Report 2016 Contents 1. INTRODUCTION 1 2. OVERVIEW OF THE BUSINESS 1 3. RISK MANAGEMENT OBJECTIVES & POLICIES 1 4. CAPITAL ADEQUACY & OWN FUNDS 6