Online Course on Debt Sustainability Analysis (DSAx) Part 1: Principles of Debt Sustainability

|

|

|

- Amy Merritt

- 6 years ago

- Views:

Transcription

1 Online Course on Debt Sustainability Analysis (DSAx) Part 1: Principles of Debt Sustainability

2 DSAx Part 1: Principles of Debt Sustainability

3 Part 1 Unit 1: Learning Objectives and Structure of Part 1

4 Learning Objectives of Part 1 Learn about key concepts of debt sustainability analysis Understand the dangers of high debt Derive debt dynamics for different types of debt Discuss the role of fiscal adjustment and other macroeconomic policies

5 Structure of Part 1 Unit 1: Overview Unit 2: Defining debt sustainability Unit 3: Why is debt sustainability analysis important? Unit 4: Public debt sustainability in a closed economy: part 1 Unit 5: Debt dynamics Public debt sustainability in a closed economy: part 2

6 Structure of Part 1 Unit 6 Public debt sustainability in an open economy Unit 7 Chipping away at public debt (Adjustment paths and their implications) Unit 8 Role of macroeconomic policies Unit 9 External debt sustainability: part 1 Unit 10 External debt sustainability: part 2

7 Part 1 Unit 2: Defining Debt Sustainability

8 UNIT OBJECTIVES Understand the concept of sustainability Master the relevant terminology Identify relevant indicators of solvency and liquidity Familiarization with various types of DSA conducted by the IMF/World Bank

9 UNIT OUTLINE Debt sustainability from different angles Debt burden indicators Introduction to IMF/World Bank Debt Sustainability Analysis (DSA)

10 Part 1 Unit 2: Lecture 1 What is Sustainability?

11 OUTLINE Debt Sustainability from Different Angles: Academic Pragmatic

12 Intertemporal Solvency Condition Initial debt Future stream of primary expenditure Future stream of income Future flows should be discounted Primary expenditure= Expenditure Interest expenditure Discounting: refers to calculating the present discounted value

13 Intertemporal Solvency Condition When a government, business or individual is solvent, it is able to service its current debt out of future income or surpluses. A person with a small debt and large future income is solvent. Example: Consider a business with debt of $20,000 and a prospect of annual profits of $10,000. The business is solvent as this debt can be serviced from future profits.

14 Intertemporal Solvency Condition A counter-example is a Ponzi-scheme. In such schemes, initial debt is serviced by relying on new investors, rather than serviced out of future surpluses.

15 Solvency is very much like honesty: it can never be fully certified, and proofs are slow to materialize. Guillermo Calvo

16 Academic Definition of Debt Sustainability Debt is sustainable if the intertemporal solvency condition is satisfied, that is, if the expected present value of future primary balances covers the existing stock of debt.

17 The ability to postpone generating primary surpluses to cover for the existing debt obligations into the future makes solvency a relatively weak requirement

18 Academic Perspective Precise Unobservable Forecasting Future

19 Pragmatic Definition of Debt Sustainability Debt is sustainable if projected debt ratios are stable or decline, while also being sufficiently low. Debt is unsustainable if projected debt ratios increase or remain high.

20 Pragmatic Definition of Debt Sustainability Pragmatism consists in recognizing that the ratio of debt to capacity to pay is what matters in order to avoid a debt crisis. To be sustainable, debt cannot grow faster than incomes and the capacity to repay it.

21 Pragmatic Definition of Debt Sustainability Another aspect of pragmatism is to recognize that economies are subject to shocks. A debt ratio which is declining but high can still be unsustainable if it associated with a high risk of default.

22 Example of Pragmatic View of Debt/GDP Sustainable Debt Time

23 Taking Solvency Condition to the Data Solvency vs. Non-explosive Debt Ratios: Useful result when interest rates are higher than the growth rate: if the ratio of debt to GDP is either stable or declining in the long run, the solvency condition is automatically met.

24 Risks to Sustainability The projected trajectory and the level of debt should be based on realistic assumptions about the underlying macroeconomic variables The resulting gross financing needs have to be evaluated The market perception of the sovereign risks has to be factored in based on debt maturity structure, its currency composition, its creditor base, etc.

25 Part 1 Unit 2: Lecture 2 Define Debt Sustainability

26 OUTLINE Debt Sustainability from Different Angles: Economic Policy Definition

27 Economic Policy Definition of Debt Sustainability Debt is sustainable if the country (or its government) does NOT, in the future, need to default or renegotiate or restructure its debt or make implausibly large policy adjustments.

28 Default

29 Debt Restructuring

30 Policy Adjustments

31 Economic Policy Definition of Debt Sustainability Sustainability rules out any of the following situations: a debt restructuring is already needed the borrower accumulates debt at a rate faster than the growth in its capacity to service debt the borrower lives beyond its means by accumulating debt in the knowledge that a major retrenchment will be needed to service these debts

32 RECAP Intertemporal solvency condition is weaker than the economic policy definition of sustainability We call debt sustainable if a country or a government is able to service its debts without the need for implausibly large policy adjustments; renegotiating the terms of debt; or simply defaulting.

33 Part 1 Unit 2: Lecture 3 Debt Burden Indicators for Solvency and Liquidity: Commonly Used Ratios

34 OUTLINE The concept of liquidity Debt burden indicators and their role Key solvency indicators Key liquidity indicators

35 Liquidity We define an entity as liquid if, regardless of whether it satisfies the solvency condition, its liquid assets and available financing are sufficient to meet or roll-over its maturing liabilities.

36 What to Watch for to Minimize Liquidity Risks The projected trajectory AND the level of debt should be based on realistic assumptions Risk factors include Market perception of the sovereign Debt maturity structure The currency composition of debt The availability of liquid assets The creditor base (notably, the share of nonresident creditors)

37 Insolvency vs. Illiquidity Sometimes it can be difficult to distinguish between insolvency and illiquidity situations Liquidity problems are often symptoms of underlying solvency problems: creditors refuse to roll over maturing debt because of solvency concerns Liquidity problems may give rise to insolvency, by raising interest rates or pressuring the exchange rate

38 Vulnerability When we talk about debt sustainability, vulnerability is defined as a risk that the liquidity or solvency conditions are violated and the borrower enters a crisis

39 How Do We Assess the Debt Burden? By examining the projected evolution of a set of debt burden indicators over time What are the indicators?

40 Debt Burden Indicators Ratios of the debt stock or debt service relative to what we define as measures of the ability to service debt (repayment capacity), e.g. GDP export proceeds fiscal revenue Other Gross financing needs, either in level or scaled by the above measures

41 Debt Burden Indicators as Measures of Solvency and Liquidity Ratios of debt stock relative to repayment capacity are indicators of solvency Ratios of debt service are indicators of potential liquidity problems Gross financing needs is an indicator of potential liquidity problems

42 Definitions of Gross Financing Needs Gross financing needs are the amount of financing necessary to cover the deficit plus amortization of debt GFN = Deficit + Amortization GFN = Primary Deficit + Debt Service GFN can be positive or negative

43 Definitions of Debt Service and Amortization Debt service DS = Interest + Amortization Amortization = principal payments coming due on medium- and longterm debt plus short-term debt coming due (maturity of 1 year or less)

44 Illustration: debt/gdp vs. debt/exports Debt Ratios for an Open Economy (exports/gdp=60%) Debt Ratios for a Closed Economy (exports/gdp=10%) Debt/Exports Debt/GDP Debt/X Debt/GDP t t+1 t+2 t+3 0 t t+1 t+2 t+3 Both countries have the same debt/gdp ratio, but very different debt/exports ratio.

45 Illustration: Gross Financing Needs and Other Debt Burden Indicators STD=10% total debt STD=60% total debt (bill LCU) Gross Financing Needs (deficit plus amortization) Deficit Primary deficit Interest payments Amortization Payments Short-term debt Medium and long-term debt Debt service (interest plus amortization) (%) Gross financing needs-to-gdp 18% 44% Gross financing needs-to-revenue 73% 184% Debt service-to-gdp 17% 43% Debt service-to-revenue 69% 180% Total public debt-to-gdp 66% 66% Total public debt-to-revenue 273% 273%

46 RECAP Concept of Liquidity Debt Burden Indicators: Repayment Capacity (the ability to service debt). Solvency and Liquidity

47 Part 1 Unit 2: Lecture 4 Scope of Debt Sustainability Analysis

48 OUTLINE Scope of the IMF/World Bank Debt Sustainability Analysis (DSA) DSA for Different Types of Debt

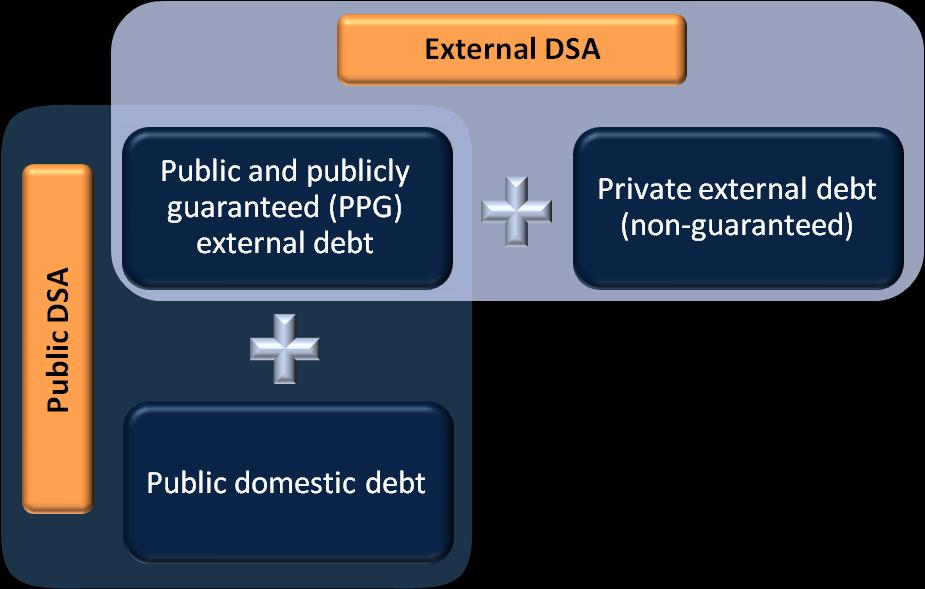

49 DSA and DSF A DSA is produced for a particular country The Debt Sustainability Framework (DSF) is the framework within which DSAs are produced. The DSF is needed to ensure comparability across DSAs produced for different countries.

50 MAC DSA For advanced and emerging economies with access to financial markets, we use the Framework for Fiscal Policy and Public Debt Sustainability Analysis in Market- Access Countries (MAC DSA)

51 MAC DSA (

52 LIC DSF The DSF originated as the framework to assess debt sustainability in lowincome countries (LICs)

53 LIC DSF (

54

55 Sample DSA (

56 Scope of Public DSA The public DSA (also called the fiscal DSA) covers total debt of the public sector, to external and domestic creditors MAC DSA for public debt covers only public debt, not publicly guaranteed debt (PPG) LIC DSA for public debt covers public and publicly guaranteed debt (PPG)

57 Scope of External DSA The external DSA covers external debt in the economy MAC DSA for external debt covers debt owed by both the public sector and the private sector LIC DSA for external debt covers public and publicly guaranteed (PPG) external debt

58 Selected Features of DSA To inform a judgment on debt sustainability, the DSA for MAC and LIC combine the indicators of solvency and liquidity the trajectory and the level of debt and financing needs under a baseline scenario the adverse scenarios recognizing the uncertainty and macro-fiscal risks, e.g. economic cycle (boom-bust) analysis shocks to contingent liabilities, growth, interest rate, exchange rate, etc.

59 Selected Features of MAC DSA DSA MACs for public debt considers The market perception of the sovereign Risks stemming from the debt profile Creditor base Maturity Currency composition The realism of the underlying assumptions

60 Selected Features of LIC DSA LIC DSA considers a long-term prospective the concessionality of debt risk rating: an explicit assessment of the risk of external debt distress

61 RECAP Scope of Debt Sustainability Analysis (DSA) MAC or LIC DSA for Different Types of Debt Public or External

62 Part 1 Unit 3: Why is Debt Sustainability Analysis Important?

63 UNIT OBJECTIVES Understanding the costs of high debt Learn the definition and origin of debt and other crises Understanding the mechanism of debt crisis

64 UNIT OUTLINE Costs Associated with High Debt Types of Economic Crisis Mechanism of Debt Crisis

65 Part 1 Unit 3: Lecture 1 Costs Associated with High Debt

66 UNIT OUTLINE Consequences of High Debt Vulnerability to Sudden Stops Crowding out of private investment Loss of policy flexibility Debt Overhang Debt Restructuring

67 Consequences of High Debt For both public debt and total external debt: Vulnerability to a sudden stop in financing (official or private flows)

68 Impact of Sudden Stops External debt: current and capital account restrictions currency crisis, banking crisis, recession, default Public debt drastic reduction in primary spending currency crisis, banking crisis, recession, default

69 Consequences of High Debt For public debt, consequences include Higher interest rates and crowding out of private investment Less flexibility to conduct countercyclical policy Debt overhang

70 Debt Overhang Definition: The expected tax burden to finance debt is so high that it is a disincentive to current investment/consumption and hence a drag on the economic activity Consequences: lower growth, lower government revenues insufficient funds for primary expenditures higher chance of default

71 Debt Overhang Worries about debt sustainability Rising risk premium Concerns about future financing of the sovereign Worries about fiscal deficits Concerns about economic growth

72 Consequences of Sovereign Debt Restructuring Political and economic penalties Spillovers across segments of the economy (especially if banks are major holders of government debt) Contagion to other countries The 1998 Russian sovereign default and fears in 2010 of a possible Greek default are examples of strong contagion to other countries

73 RECAP Costs Associated with High Debt: Vulnerability Crowding out Loss of flexibility Debt Overhang Debt Restructuring

74 Part 1 Unit 3: Lecture 2 Types of Economic Crises

75 OUTLINE Types of Economic Crises Currency Crises Banking Crises External Debt Crises Sovereign Debt Crises

76 Currency Crises What: an attack in a country s currency results in one, or a combination, of the following large devaluation sharp depreciation large increase in interest rates large fall in reserves When: concerns about the viability of the exchange rate regime or the level of the exchange rate

77 Currency Crises Why: market expects that foreign exchange (FX) reserves will run out because of inconsistent policies or be insufficient to cover short-term debt market expects government to devalue in order to address a policy goal, such as improved competitiveness

78 Banking Crises What: run on banks or large-scale government intervention to rescue banks When: concerns about solvency and liquidity of banks

79 Banking Crises Why: bursting bubble in equity or real estate prices interest rate, exchange rate, or growth shocks bust typically follows lending booms (stimulated by financial liberalization/capital inflows)

80 Debt Crises Debt crises can be associated with either sovereign (public) or commercial (private) debt

81 Sovereign Debt Crises What: defaults, involuntary restructuring of sovereign debt, or belief that this is about to occur When: often combined (or immediately following) banking crises: this was true for over 60 percent of all sovereign debt crises after 1970 (Rogoff and Reinhart, 2010)

82 Sovereign Debt Crises Why: financial rescue packages extended period of low growth fiscal profligacy (including war finance) failed state-owned enterprises natural disasters etc.

83 External Debt Crises What: payment arrears on a substantial fraction of external debt When: cash flow problems or difficulties obtaining foreign exchange Why: sudden stops following capital inflow episode interest rate, exchange rate, or growth shocks

84 RECAP Different Types of Economic Crises: Currency Crises Banking Crises External Debt Crises Sovereign Debt Crises

85 Additional Resources Please watch the video on Latvia : Debt and BoP crisis with internal devaluation and fiscal adjustment

86 Part 1 Unit 3: Lecture 3 Mechanism of Sovereign Debt Crises

87 OUTLINE Sample Mechanism of Debt Crisis Bank-sovereign Interdependence

88 A Sample Mechanism of a Sovereign Debt Crisis Financial sector rescue packages weigh on public debt and the deficit Economic activity nosedives Fiscal revenue collapses while expenditures skyrocket

89 A Sample Mechanism of a Sovereign Debt Crisis The resulting spike in deficits and debt causes concerns about the fiscal balance and debt sustainability Costs of borrowing for the sovereign increase Fiscal position further worsens

90 Bank-Sovereign Interdependence Damage to bank balance sheets bailout costs and increase in sovereign debt Increase in sovereign debt higher possibility of sovereign default, lower ratings damage to bank balance sheets

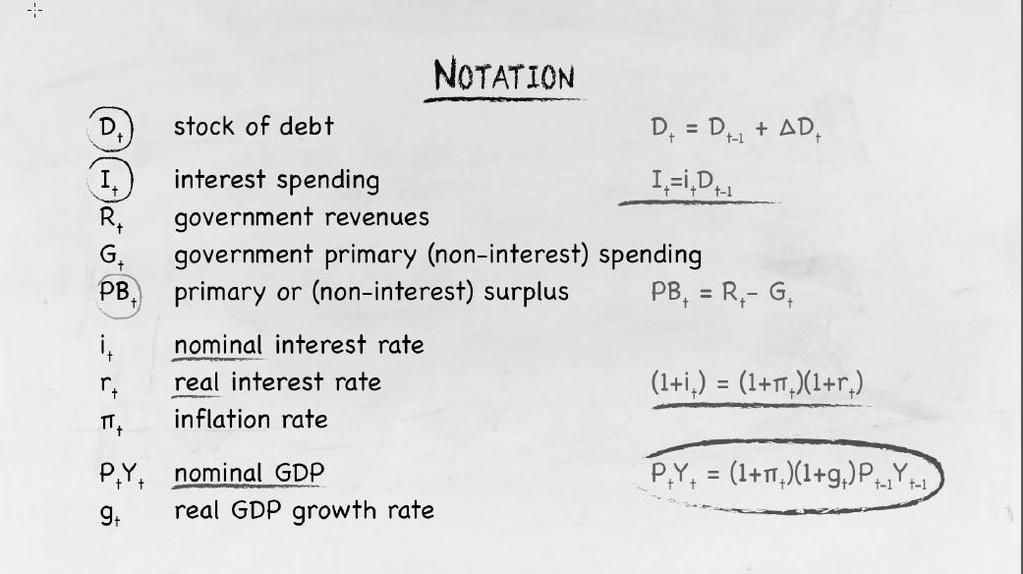

91 Bank-Sovereign Interdependence Lower sovereign ratings Recession

92 RECAP Sample mechanism of debt crisis Bank-sovereign Interdependence

93 Part 1 Unit 4 Public Debt Sustainability in a Closed Economy

94 UNIT OBJECTIVES Learn how to derive the law of motion for public debt Learn how to derive the formal solvency condition for public debt

95 UNIT OUTLINE Closed economy: Law of motion for public debt Solvency condition for public debt

96 Part 1 Unit 4: Lecture 1 Law of Motion for Public Debt

97 OUTLINE The debt-deficit relationship The primary balance The government budget constraint

98 The Relationship between Deficit and Public Debt Current Stock of Debt = Past Stock of Debt + Deficit + Other Flows + Exchange Rate Valuation In the closed economy, we assume debt is issued in local currency, so that there is no contribution of exchange rate valuation. In the open economy, we allow for debt issued in local currency and in foreign currency.

99 Vicious Circle of Debt and Deficit Higher interest payments Deficit Increase in debt Borrowing

100 Relationship between Deficit and Public Debt Budget deficit can be financed by borrowing or other means (e.g., printing money or selling assets) Net new borrowing necessary to finance budget deficit adds to the current stock of debt

101

102

103

104 Note Other flows include asset purchases and expenditure items not included in G bank recapitalization assumption of guaranteed state enterprise debt non-debt sources of financing asset sales such as privatization revenues seigniorage Such non-debt sources of financing enter with a negative sign 104

105 Focusing on Primary Balance: Substitute the primary balance definition: PB t i t D OT D D t 1 t t t 1 Assume other flows are zero: OT t 0

106 Equation for Debt Dynamics: D t (1 i t ) D t 1 PB t 106

107 Example: Evolution of Debt over Time D t (1 i t ) D t 1 PB t t-1 t t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8 t+9 t+10 D 100 t 1 PB t 2 i t 2%

108 Part 1 Unit 4: Lecture 2 Deriving the Solvency Condition

109 OUTLINE Deriving the Solvency Condition from the Flow Budget Constraint: Derive the Intertemporal Budget Constraint Impose Transversality Obtain Solvency Condition

110 Checkpoint: Where Are We? We talked about the debt-deficit relationship We derived the government budget constraint We derived one-period law of motion for public debt

111 Checkpoint: what s next? We will start with the flow budget constraint We will use forward substitution to derive the intertemporal budget constraint Which we need to obtain solvency condition (in present-value terms)

112

113

114

115

116

117

118 Part 1 Unit 5 Public Debt Sustainability In Closed Economy: Part 2

119 UNIT OBJECTIVES Learn how to derive the law of motion for the ratio of public debt-to-gdp for a closed economy Analyze contributions of key macroeconomic variables to debt dynamics Obtain the debt-stabilizing primary balance

120 UNIT OUTLINE Closed economy: Law of motion for public-debtto GDP ratio Automatic debt dynamics Debt-stabilizing primary balance

121 Part 1 Unit 5: Lecture 1 Law of Motion for Public Debt-to-GDP in a Closed Economy

122 OUTLINE Law of motion for public-debtto GDP ratio Key macroeconomic variables affect debt sustainability Primary balance Initial level of debt Growth Real interest rate

123 Checkpoint: Where Are We? We are still in the case of a closed economy (to avoid worrying about the exchange rate-induced variations in debt)

124 Checkpoint: what s next? We are about to get pragmatic and do some derivations in terms of ratios of debt stock to the economy s capacity (GDP) Law-of-motion for debt-to-gdp in hand, we will look at the impact of the key macroeconomic variables on debt dynamics

125

126

127

128

129 Part 1 Unit 5: Lecture 2 Stabilizing Debt in a Closed Economy

130 OUTLINE Automatic debt dynamics Stability of debt Debt stabilizing primary balance The danger of debt momentum

131

132

133

134 Primary Balance to Stabilize Debt: Assuming d is constant one can solve for the debt stabilizing primary balance pb*: pb t r g * t t dt 1 g t 1 Automatic debt dynamics 134

135 Primary Balance to Stabilize Debt: The primary surplus needed to keep the debt/gdp constant equals the debt dynamics. It is proportionate to the gap between real interest rate and real growth rate The primary balance needed to keep the debt/gdp constant will rise directly with the size of the initial debt/gdp, if r>g We can also interpret the equation as telling us the level of debt which can be sustained for a given primary balance 135

136 The Danger of Debt Momentum: The primary surplus needed to keep the debt/gdp constant will rise directly with the size of the initial debt/gdp The higher is the initial debt stock, the more difficult it is to stabilize the debt/gdp ratio Danger of built in momentum, the higher debt-to-gdp ratio gets, the less likely it is to run a sufficiently large primary surplus debt rises Thus, vulnerability rises with debt-to-gdp ratio 136

137 Illustration: Evolution of Debt/GDP over Time: d t ( 1 (1 rt g t ) ) d t 1 pb t %GDP t-1 t t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8 t+9 t+10 d t 1 100% r 2% g 5% pb t 2%

138 UNIT RECAP Law of motion for public-debtto GDP ratio Automatic debt dynamics Debt-stabilizing primary balance

139 Part 1 Unit 6 Public Debt Sustainability In Open Economy

140 UNIT OBJECTIVES Learn how to derive the law of motion for public debt for an open economy Obtain the debt-stabilizing primary balance Analyze contributions of key macroeconomic variables to debt dynamics

141 UNIT OUTLINE Open economy: Law of motion for public debt Debt-stabilizing primary balance Comparative statics

142 Part 1 Unit 6: Lecture 1 Law of Motion for Public Debt in an Open Economy

143 OUTLINE Flow budget constraint with external financing Law of motion for the debt-to- GDP ratio Automatic debt dynamics

144

145

146

147

148

149

150

151

152

153

154 Part 1 Unit 6: Lecture 2 Stabilizing Debt in an Open Economy

155 OUTLINE Debt stabilizing primary balance Comparative statics: role of key macroeconomic variables: Initial level of debt Growth Interest Rate Exchange Rate

156

157

158 Key Comparative Statics: The required primary balance is higher when: The real interest rate - growth differential is large Other flows contribute to an increase in debt (e.g. financial sector support measures, nationalization of private pensions) There is exchange rate depreciation (ε) in countries with large foreign exchange denominated debt (α) Note: The last two are examples of stock-flow adjustments because they help reconcile the change in the value of debt with the deficit

159 Illustration: Key Macro-Economic Variables Country W Country X (% change) Country Y Country Z r d r f g ε* (% GDP) d d d f pb*

160 Illustration: We can calculate pb* by applying the formula, while being careful to express interest rates and growth rates as a percent: pb* ( r w t ) d * (1 For country Z for example: g t g t t (1 r ) f t ) d ( ) (1 0.05) 0.5 pb* % (1 0.04) f

161 UNIT RECAP Debt Law-of-Motion Debt-stabilizing Primary Balance Key Comparative Statics

162 Part 1 Unit 7 Chipping Away at Public Debt

163 UNIT OBJECTIVES Understand different adjustment paths and their implications Understand how fiscal adjustment may affect GDP and the risk premium on government debt

164 UNIT OUTLINE Adjustment Paths and Their Implications Front-loaded and back-loaded adjustments Fiscal Adjustment, the Business Cycle, and the Risk Premium History of Past Fiscal Adjustments (video)

165 Part 1 Unit 7: Lecture 1 Adjustment Paths and Their Implications

166 OUTLINE Definition of front-loaded and back-loaded adjustment Circumstances favoring each

167 Front-loaded and Back-loaded Adjustment: Front-loaded adjustment: pb time Back-loaded adjustment: pb time

168 Front-loaded and Back-loaded Adjustment: Front-loaded fiscal adjustment quickly raises the primary balance to the targeted level Back-loaded adjustment phases in the adjustment over time

169 Circumstances Affecting the Timing of Adjustment: Front-loading may be necessary: when facing severe financing constraints to build credibility to seize opportunity of political support Back-loading may be preferable to: support to economic activity ensure quality of measures

170 Circumstances Affecting the Timing of Adjustment: Credibility is very important in the context of high debt, because of its effect on the risk premium and therefore debt dynamics In the case of back-loading, credibility can be enhanced by institutional mechanisms, such as balanced budget rules and procedural rules

171 Circumstances Affecting the Timing of Adjustment: If fiscal adjustment has a negative impact on growth, it may undermine debt sustainability undertake fiscal adjustment in the upswing of the business cycle undertake fiscal adjustment during worldwide recoveries support fiscal adjustment with accommodating monetary policy

172 Front-loaded and Back-loaded Adjustment In the Additional Resources we provide a formula for the fiscal adjustment necessary to reduce debt over a given number of periods. The formula allows one to distinguish frontloaded adjustment from back-loaded adjustment.

173

174

175

176 Additional Resources This material took stock of: The primary balance necessary to reduce debt to certain level the potential impact on cost of funding

177 RECAP The tradeoff between frontloaded and back-loaded fiscal adjustment is front-loading to ease financing constraints and gain credibility vs. back-loading to support growth and work out quality measures

178 Part 1 Unit 7: Lecture 2 Fiscal adjustment and the business cycle

179 OUTLINE How the budget balance affects GDP How the budget balance affects the risk premium

180 Fiscal Adjustment and the Business Cycle

181 Fiscal Adjustment and the Business Cycle Three main channels from primary balance to debt/gdp: directly via the primary balance in the debt dynamics via GDP through demand lower government spending and higher taxes reduce demand via interest rates through credibility (risk premium) and demand crowding out

182 Fiscal Adjustment and the Business Cycle Fiscal consolidation may lead to slower GDP growth High multiplier (closed economy, high unemployment) Coordinated consolidations in economic partners Fiscal consolidation may lead to lower interest rates In high-debt countries credibility effects are particularly important

183 UNIT RECAP Front-loaded vs back-loaded adjustment The speed at which debt can be reduced depends on how fiscal adjustment affects GDP and interest rates.

184 Additional Resources Please watch the video on Chipping Away At Public Debt

185 Part 1 Unit 8 Role of Macroeconomic Policies

186 UNIT OBJECTIVES Understand the role of monetary policy Understand the economic policy tradeoffs

187 UNIT OUTLINE Monetary Policy Stance and Debt Policy Tradeoffs

188 Part 1 Unit 8: Lecture 1 Monetary Policy Stance and Debt

189 OUTLINE Expansionary monetary policy possible effects The effect of monetary policy on interest rates and inflation

190 Monetary policy stance and debt Interest rate Inflation Exchange rate Growth

191 Monetary policy stance and debt Expansionary monetary policy possible effects Lower nominal interest rates Lower real interest rates Higher inflation Higher growth Depreciated exchange rate

192 Monetary policy stance and debt Use the debt dynamics equation and assuming at first no foreign currency debt: if real interest rates fall and growth improves (therefore improving the primary balance), debt is reduced. d t ( 1 (1 rt ) gt) d ( pb ot t 1 t t )

193 Monetary policy stance and debt If there is foreign currency debt, the effect is no longer unambiguous. Debt/GDP could increase, in the case of less than complete pass-through of exchange rate depreciation to inflation. d t ( 1 rt (1 g d t ) ) d f ( 1 it (1 g )( 1 )(1 ) d ) ( pb ot d t f t 1 t t t 1 t t )

194 Illustration: Impact of Monetary Easing d t d d f ( rt gt) dt 1 ( it t gt t) d f t 1 pb t ot t Easing of monetary policy Depreciation No change in Passthrough Passthrough No easing exchange rate 20% 100% (% change) r d i f ε* π g pb (% GDP) d d t d f t d t

195 Monetary Policy Stance and Debt The effect of monetary policy on interest rates and inflation needs to be qualified Expansionary monetary policy tends to reduce short-term interest rates but increase long-term ones, reflecting expectations of future inflation

196 Monetary Policy Stance and Debt Fischer equation: i=r*+π e Interest rates are set based on a required real return r* Given r*, higher πe translates into higher i Ex post r need not equal r* if there is surprise inflation (in which case r<r*)

197 Part 1 Unit 8: Lecture 2 Policy Tradeoffs

198 OUTLINE Sustainable Debt vs. Inflation Sustainable Debt vs. Competitiveness Sustainable Debt vs. Fairness

199 Policy Tradeoffs Fiscal dominance Fear of floating Fairness/income distribution

200 Policy Tradeoffs: Sustainable Debt vs. Inflation Fiscal dominance: inability to conduct contractionary monetary policy because it would jeopardize government debt dynamics Contractionary monetary policy, which would result in higher real interest rates lower growth higher debt/gdp

201 Policy Tradeoffs: Sustainable Debt vs. Competitiveness Fear of Floating: reluctance to allow a floating exchange rate to depreciate Loose monetary policy is helpful for competitiveness and growth, but will raise the value of foreign currency debt expressed in local currency (public and private) and may cause bankruptcies

202 Policy Tradeoffs: Sustainable Debt vs. Competitiveness Fear of floating follows from the original sin the inability of emerging markets to issue external debt in their own currency.

203 Policy Tradeoffs: Sustainable Debt vs. Fairness Inflation as default There is a thin line separating inflation from default since inflation erodes away the value of debt (especially when there is financial repression capping nominal interest rates) Inflation creates a redistribution of wealth from creditors to debtors

204 Part 1 Unit 9 External Debt Sustainability

205 UNIT OBJECTIVES Understanding similarities between external and fiscal sustainability Understanding external debt creating flows Understanding solvency condition for external debt

206 UNIT OUTLINE External DSA External debt creating flows Debt law-of-motion Solvency condition for external debt

207 Part 1 Unit 9: Lecture 1 External Debt Creating Flows

208 OUTLINE External DSA External debt creating flows The adjusted balance

209 External DSA: Similarities between external and fiscal sustainability apply similar methodologies Focus on external debt of the country (including the private sector debt) The current account balance of the balance of payments takes the place of the overall budget balance.

210 Key Differences with Public Debt: The government does not directly control the CAB In a healthy cycle, exports and CAB will improve over time, allowing for repayment of debt Exchange rate normally plays larger role in external sustainability

211 External Debt Creating Flows: Our goal in this unit is to derive a law of motion for external debt, which links debt to past debt and the current account balance. D f t ( 1 i f t )D f t 1 AB t In the process we will define the adjusted balance, AB, which is a modified current account balance.

212 Notation: CA t AB t I t KA t FA t A t L t D f t E t current account balance adjusted balance interest payments on external debt capital account financial account external assets external liabilities external debt liabilities external equity liabilities (P t Y t ) GDP expressed in USD = P t Y t /e t All variables are expressed in USD

213 The Adjusted Balance: Define: AB t ( CAt It) ( Et A t) non-interest current account balance non-debt financing The current account (the sum of net exports, income and current transfers) records interest payments on debt as a negative income item. Here we add interest back to obtain the noninterest CAB.

214 Part 1 Unit 9: Lecture 2 External Financing Constraint and Debt-Lawof-Motion

215 OUTLINE External Financing Constraint Debt Law-of-motion

216 External Financing Constraint Using the terminology of the BOP and IIP manual (6 th edition), we write: CA t KA We assume for simplicity that the capital account KA (capital transfers for the most part) is zero. t FA t KA t 0

217 External Financing Constraint The financial account of the BOP records the acquisition of assets and the incurrence of liabilities (e.g. as the result of external borrowing). These flows are called transactions. We assume for simplicity that valuation effects are zero, so that the change in the value of assets and liabilities is equal to these BOP transactions. CA t A t L t FA t

218 External Financing Constraint Liabilities can be either debt liabilities or equity liabilities: CA t A t f ( Dt Et ) ΔL t Debt includes debt securities, loans, currency and bank deposits. Equity includes shares and foreign direct investment.

219 Debt Law-of-motion Rewriting the previous equation in terms of current period debt and adding and deducting interest: D f t D f t 1 CA t E t A t I t I t -AB t Next assume as before: I i f D f t t t 1

220 Debt Law-of-motion Finally, using the definition of the adjusted balance and grouping terms involving lagged debt, we find the law-of-motion we had set out to find: D f t ( 1 i f t )D f t 1 AB t

221 Part 1 Unit 9 Lecture 3: Solvency condition for external debt

222 Solvency condition for external debt From the debt law-of-motion we can obtain the intertemporal budget constraint through repeated substitution, as we did for public debt. We then obtain the solvency condition for external debt by imposing the tranversality condition or No-Ponzi condition. Specifically, we require that the present discounted value of external debt at time infinity approaches zero.

223 Solvency Condition For External Debt Using a the same method as for public debt, the intertemporal budget condition extended to N periods is: D f 0 N j 1 ( 1 1 i f t ) j AB j ( 1 1 i f t ) N D f N We extend this formula to time infinity and impose the transversality condition.

224 Solvency Condition Solvency: the present value of all surpluses (of the adjusted balance) is equal to initial debt. f ( 1 ) j D 0 f j 1 1 it AB j

225 RECAP External Debt Sustainability Analysis External Debt Creating Flows Debt Law-of-motion Solvency condition for external debt

226 Part 1 Unit 10 Lecture 1: Deriving External Debt Law-of-Motion

227 OUTLINE Debt Law-of-motion: The Debt-To-GDP Ratio Automatic Debt Dynamics

228 External Debt Law-of-Motion: the Debt-to-GDP Ratio Evolution of external debt at time t: D f t ( 1 i f t We divide by GDP expressed in USD, (P t Y t )*, since external debt is expressed in USD. Using (P t Y t )*= P t Y t /e t )D f t 1 AB t f f f Dt ( 1 it )Dt 1 ( PY t t )* (1 gt)(1 t) Pt 1Y t 1 / e t ABt ( PY )* t t P t Y t

229 Debt Law-of-Motion: the Debt-To-GDP Ratio We convert GDP in local currency back to GDP in USD and use 1+ε t =e t /e t-1 f D f f t ( 1 it )( 1 t ) Dt 1 ( PY t t )* (1 gt)(1 t) ( Pt 1Y t 1)* ABt ( PY )* t t d f t d f t-1 ab t

230 Debt Law-of-Motion: the Debt-to-GDP Ratio It is easy to show that f ( 1 i )( 1 t ) t f ( 1 rt )( 1 (1 * t) t ) where (1 r f t ) f (1 it ) (1 *) (1 *) (1 )(1 *) (1 ) *= foreign inflation rate r f t= real interest rate on foreign debt ε*= real exchange rate depreciation

231 Debt Law-of-Motion: Analytical Representation Evolution of the debt-to-gdp ratio φ t d f t f ( 1 rt )( 1 * (1 gt) t ) d f t 1 ab t For ab t =0 and d t -1>0: If φ t <1, debt converges to zero If φ t >1, debt explodes

(1 ) *(1 t f t f t t t f t f t f t ab d d g ) )( r ( d d 1 1 * 1 ) (1 1 1 automatic debt dynamics φ t")

232 Automatic Debt Dynamics Deducting past debt from both sides and simplifying: t f t t f t t t f t f t f t ab d g r g r d d 1 1 ) (1 ) *(1 t f t f t t t f t f t f t ab d d g ) )( r ( d d 1 1 * 1 ) (1 1 1 automatic debt dynamics φ t -1

233 Debt-Stabilizing Adjusted Balance What level of ab keeps debt constant? To find the answer, simply set d t =d t-1 in the previous expression (denote the constant debt level by d*) f f rt gt * t (1 rt ) * ab* d (1 g ) ab* is the debt-stabilizing primary surplus. Note that it equals the automatic debt dynamics. If ab>ab * debt falls continuously; if ab<ab *, debt explodes and is therefore unsustainable t

234 Key Comparative Statics Debt dynamics are affected by: Real interest rate Growth rate of the economy Current level of indebtedness Net exports Long-term level of other flows Real exchange rate changes

235 Illustration Country X Country Y Country Z (% change) r f g ε (% GDP) d f ab*

236 Illustration We can calculate ab* by applying the formula, while being careful to divide the parameters by 100: f f rt gt * t (1 rt ) ab* d (1 g ) For country Z for example: (1 0.05) ab* % (1 0.04) t *

237 Summary Key Takeaways for External Debt

238 Key Equations Debt law-of-motion Adjusted balance Debt law-of-motion (%GDP) t f t f t f t AB )D i ( D 1 1 ) ( ) ( t t t t t A E I CA AB t f t t f t t t f t f t f t ab d g r g r d d 1 1 ) (1 ) *(1

239 Debt dynamics Debt dynamics are affected by: Real interest rate Growth rate of the economy Current level of indebtedness Net exports Long-term level of other flows Real exchange rate changes

Part 1: Principles of Debt Sustainability

1 Part 1: Principles of Debt Sustainability Unit 1: Structure and Learning Objectives Video-Part 1 Introduction: Irina Yakadina: Hello and welcome! In this part of our course, we will learn the key concepts

1 Part 1: Principles of Debt Sustainability Unit 1: Structure and Learning Objectives Video-Part 1 Introduction: Irina Yakadina: Hello and welcome! In this part of our course, we will learn the key concepts

Greece: Preliminary Debt Sustainability Analysis February 15, 2012

Greece: Preliminary Debt Sustainability Analysis February 15, 2012 Since the fifth review, a number of developments have pointed to a need to revise the DSA. The 2011 outturn was worse than expected, both

Greece: Preliminary Debt Sustainability Analysis February 15, 2012 Since the fifth review, a number of developments have pointed to a need to revise the DSA. The 2011 outturn was worse than expected, both

JOINT IMF/WORLD BANK DEBT SUSTAINABILITY

ZIMBABWE JOINT IMF/WORLD BANK DEBT SUSTAINABILITY May 5, 211 ANALYSIS 1 Approved By Mark Plant and Dominique Desruelle (IMF) Marcelo Giugale and Jeffery Lewis (IDA) Prepared by The International Monetary

ZIMBABWE JOINT IMF/WORLD BANK DEBT SUSTAINABILITY May 5, 211 ANALYSIS 1 Approved By Mark Plant and Dominique Desruelle (IMF) Marcelo Giugale and Jeffery Lewis (IDA) Prepared by The International Monetary

Macroeconomics: Policy, 31E23000, Spring 2018

Macroeconomics: Policy, 31E23000, Spring 2018 Lecture 8: Safe Asset, Government Debt Pertti University School of Business March 19, 2018 Today Safe Asset, basics Government debt, sustainability, fiscal

Macroeconomics: Policy, 31E23000, Spring 2018 Lecture 8: Safe Asset, Government Debt Pertti University School of Business March 19, 2018 Today Safe Asset, basics Government debt, sustainability, fiscal

INTERNATIONAL MONETARY FUND ST. LUCIA. External and Public Debt Sustainability Analysis. Prepared by the Staff of the International Monetary Fund

INTERNATIONAL MONETARY FUND ST. LUCIA External and Public Debt Sustainability Analysis Prepared by the Staff of the International Monetary Fund December 23, 21 This debt sustainability analysis (DSA) assesses

INTERNATIONAL MONETARY FUND ST. LUCIA External and Public Debt Sustainability Analysis Prepared by the Staff of the International Monetary Fund December 23, 21 This debt sustainability analysis (DSA) assesses

(

(https://www.edx.org) IMFx: OL14.01 Debt Sustainability Analysis GLOSSARY OF TERMS: Term Definition Acronym Above the line operation Any accounting operation that is added or deducted before the final

(https://www.edx.org) IMFx: OL14.01 Debt Sustainability Analysis GLOSSARY OF TERMS: Term Definition Acronym Above the line operation Any accounting operation that is added or deducted before the final

I. BACKGROUND AND CONTEXT

Review of the Debt Sustainability Framework for Low Income Countries (LIC DSF) Discussion Note August 1, 2016 I. BACKGROUND AND CONTEXT 1. The LIC DSF, introduced in 2005, remains the cornerstone of assessing

Review of the Debt Sustainability Framework for Low Income Countries (LIC DSF) Discussion Note August 1, 2016 I. BACKGROUND AND CONTEXT 1. The LIC DSF, introduced in 2005, remains the cornerstone of assessing

1. Generation One. 2. Generation Two. 3. Sudden Stops. 4. Banking Crises. 5. Fiscal Solvency

Currency Crises 1. Generation One 2. Generation Two 3. Sudden Stops 4. Banking Crises 5. Fiscal Solvency 1 Generation One 1.1 Monetary and Fiscal Policy Initial position long-run equilibrium purchasing

Currency Crises 1. Generation One 2. Generation Two 3. Sudden Stops 4. Banking Crises 5. Fiscal Solvency 1 Generation One 1.1 Monetary and Fiscal Policy Initial position long-run equilibrium purchasing

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND SUDAN. Joint World Bank/IMF 2009 Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND SUDAN Joint World Bank/IMF 29 Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND SUDAN Joint World Bank/IMF 29 Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and

Term Definition Acronym

IMFx DSAx Glossary Term Definition Acronym Above the line operation Any accounting operation that is added or deducted before the final sum is reached; in terms of debt, macro operations and calculations

IMFx DSAx Glossary Term Definition Acronym Above the line operation Any accounting operation that is added or deducted before the final sum is reached; in terms of debt, macro operations and calculations

Answers to Problem Set #6 Chapter 14 problems

Answers to Problem Set #6 Chapter 14 problems 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values for the variables. In this

Answers to Problem Set #6 Chapter 14 problems 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values for the variables. In this

Georgia: Joint Bank-Fund Debt Sustainability Analysis 1

November 6 Georgia: Joint Bank-Fund Debt Sustainability Analysis 1 Background 1. Over the last decade, Georgia s external public and publicly guaranteed (PPG) debt burden has fallen from more than 8 percent

November 6 Georgia: Joint Bank-Fund Debt Sustainability Analysis 1 Background 1. Over the last decade, Georgia s external public and publicly guaranteed (PPG) debt burden has fallen from more than 8 percent

Nicaragua: Joint Bank-Fund Debt Sustainability Analysis 1,2

May 2006 Nicaragua: Joint Bank-Fund Debt Sustainability Analysis 1,2 While Nicaragua s debt burden has been substantially reduced thanks to the HIPC initiative, debt levels remain elevated and subject

May 2006 Nicaragua: Joint Bank-Fund Debt Sustainability Analysis 1,2 While Nicaragua s debt burden has been substantially reduced thanks to the HIPC initiative, debt levels remain elevated and subject

INTERNATIONAL MONETARY FUND DOMINICA. Debt Sustainability Analysis. Prepared by the staff of the International Monetary Fund

INTERNATIONAL MONETARY FUND DOMINICA Debt Sustainability Analysis Prepared by the staff of the International Monetary Fund In consultation with World Bank Staff July 2, 27 This debt sustainability analysis

INTERNATIONAL MONETARY FUND DOMINICA Debt Sustainability Analysis Prepared by the staff of the International Monetary Fund In consultation with World Bank Staff July 2, 27 This debt sustainability analysis

Joint Bank-Fund Debt Sustainability Analysis 2018 Update

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND GRENADA Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND GRENADA Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

ISLAMIC REPUBLIC OF AFGHANISTAN

July 1, 216 REQUEST FOR A THREE YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Bob Matthias Traa (IMF), Satu Kähkönen (IDA) International

July 1, 216 REQUEST FOR A THREE YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Bob Matthias Traa (IMF), Satu Kähkönen (IDA) International

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Balance of Payments, Debt, Financial Crises, and Stabilization Policies

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Debt Sustainability Framework for Low-Income Countries (LICs)

") Debt Sustainability Framework for Low-Income Countries (LICs) Instructor: Machiko Narita, IMF This training material is the property of the International Monetary Fund and is intended for use in IMF Institute

Debt Sustainability Framework for Low-Income Countries (LICs) Instructor: Machiko Narita, IMF This training material is the property of the International Monetary Fund and is intended for use in IMF Institute

CENTRAL AFRICAN REPUBLIC

CENTRAL AFRICAN REPUBLIC June 29, 217 SECOND REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, FINANCING ASSURANCES REVIEW, AND REQUEST FOR AUGMENTATION OF ACCESS DEBT SUSTAINABILITY ANALYSIS 6 Approved

CENTRAL AFRICAN REPUBLIC June 29, 217 SECOND REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, FINANCING ASSURANCES REVIEW, AND REQUEST FOR AUGMENTATION OF ACCESS DEBT SUSTAINABILITY ANALYSIS 6 Approved

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

December 19, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Odd Per Brekk (IMF) and John Panzer (IDA) Prepared by the staff of the International Monetary

December 19, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Odd Per Brekk (IMF) and John Panzer (IDA) Prepared by the staff of the International Monetary

Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2

September 26 Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2 Cape Verde s debt level has increased in recent years. Despite the rising cost of servicing this debt, the country s external sustainability

September 26 Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2 Cape Verde s debt level has increased in recent years. Despite the rising cost of servicing this debt, the country s external sustainability

Suggested Solutions to Problem Set 6

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL. Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL Joint Bank-Fund Debt Sustainability Analysis

Joint Bank-Fund Debt Sustainability Analysis Update

INTERNATIONAL DEVELOPMENT ASSOCIATION Public Disclosure Authorized INTERNATIONAL MONETARY FUND DOMINICA Joint Bank-Fund Debt Sustainability Analysis -218 Update Prepared by the staffs of the International

INTERNATIONAL DEVELOPMENT ASSOCIATION Public Disclosure Authorized INTERNATIONAL MONETARY FUND DOMINICA Joint Bank-Fund Debt Sustainability Analysis -218 Update Prepared by the staffs of the International

Debt Sustainability Risk Analysis with Analytica c

1 Debt Sustainability Risk Analysis with Analytica c Eduardo Ley & Ngoc-Bich Tran We present a user-friendly toolkit for Debt-Sustainability Risk Analysis (DSRA) which provides useful indicators to identify

1 Debt Sustainability Risk Analysis with Analytica c Eduardo Ley & Ngoc-Bich Tran We present a user-friendly toolkit for Debt-Sustainability Risk Analysis (DSRA) which provides useful indicators to identify

Annex I. Debt Sustainability Analysis

Annex I. Debt Sustainability Analysis Italy s public debt is sustainable but subject to significant risks. Italy s public debt ratio continues to rise, and at around 13 percent of GDP, is the second highest

Annex I. Debt Sustainability Analysis Italy s public debt is sustainable but subject to significant risks. Italy s public debt ratio continues to rise, and at around 13 percent of GDP, is the second highest

PAPUA NEW GUINEA STAFF REPORT FOR THE 2015 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

October 8, 215 PAPUA NEW GUINEA STAFF REPORT FOR THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Hoe Ee Khor and Steven Barnett (IMF) Satu Kahkonen (IDA) Prepared by the staffs

October 8, 215 PAPUA NEW GUINEA STAFF REPORT FOR THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Hoe Ee Khor and Steven Barnett (IMF) Satu Kahkonen (IDA) Prepared by the staffs

Developing Countries Chapter 22

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

ISLAMIC REPUBLIC OF AFGHANISTAN

November, STAFF REPORT FOR THE ARTICLE IV CONSULTATION AND FIRST REVIEW UNDER THE STAFF-MONITORED PROGRAM DEBT SUSTAINABILITY ANALYSIS Approved By Adnan Mazarei and Dhaneshwar Ghura (IMF), and Satu Kahkonen

November, STAFF REPORT FOR THE ARTICLE IV CONSULTATION AND FIRST REVIEW UNDER THE STAFF-MONITORED PROGRAM DEBT SUSTAINABILITY ANALYSIS Approved By Adnan Mazarei and Dhaneshwar Ghura (IMF), and Satu Kahkonen

Linking Fiscal and Debt Management Policies The Role of Debt Sustainability Analysis. Seán Nolan. International Monetary Fund December 3, 2014

Linking Fiscal and Debt Management Policies The Role of Debt Sustainability Analysis Seán Nolan International Monetary Fund December 3, 2014 Deb Sustainability Analyses The Tool Box Handling Debt Portfolio

Linking Fiscal and Debt Management Policies The Role of Debt Sustainability Analysis Seán Nolan International Monetary Fund December 3, 2014 Deb Sustainability Analyses The Tool Box Handling Debt Portfolio

CÔTE D'IVOIRE ANALYSIS UPDATE. June 2, Prepared by the International Monetary Fund and the International Development Association

CÔTE D'IVOIRE June 2, 217 FIRST REVIEWS UNDER EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUESTS FOR MODIFICATION OF PERFORMANCE CRITERIA

CÔTE D'IVOIRE June 2, 217 FIRST REVIEWS UNDER EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUESTS FOR MODIFICATION OF PERFORMANCE CRITERIA

Refresher on Fiscal Accounts, Analysis and Forecasting

Refresher on Fiscal Accounts, Analysis and Forecasting Workshop on Financial Programming and Policies Yangon, Myanmar February 16-27, 2015 Milan Zavadjil Consultant Contents 1. Refresher on Fiscal Accounts

Refresher on Fiscal Accounts, Analysis and Forecasting Workshop on Financial Programming and Policies Yangon, Myanmar February 16-27, 2015 Milan Zavadjil Consultant Contents 1. Refresher on Fiscal Accounts

The fiscal adjustment after the crisis in Argentina

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION REPUBLIC OF MODOVA

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION REPUBLIC OF MODOVA Joint IMF/World Bank Debt Sustainability Analysis Under the Debt Sustainability Framework for Low-Income Countries

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION REPUBLIC OF MODOVA Joint IMF/World Bank Debt Sustainability Analysis Under the Debt Sustainability Framework for Low-Income Countries

REQUEST FOR A THREE-YEAR POLICY SUPPORT

SENEGAL June 9, 15 REQUEST FOR A THREE-YEAR POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum (IMF), and John Panzer (IDA) Prepared by the staffs of the

SENEGAL June 9, 15 REQUEST FOR A THREE-YEAR POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum (IMF), and John Panzer (IDA) Prepared by the staffs of the

Session 2. The IMF's macroeconomic framework

Session 2. The IMF's macroeconomic framework 1. Overview of the Macro Framework Some takeaways Linkages between sectors and policies are critical Financial programming (FP) is a tool for ensuring accounting

Session 2. The IMF's macroeconomic framework 1. Overview of the Macro Framework Some takeaways Linkages between sectors and policies are critical Financial programming (FP) is a tool for ensuring accounting

Fiscal/Monetary Coordination When the Anchor Cable Has Snapped. Christopher A. Sims Princeton University

Fiscal/Monetary Coordination When the Anchor Cable Has Snapped Christopher A. Sims Princeton University sims@princeton.edu May 22, 2009 Outline Introduction The Fed balance sheet Implications for monetary

Fiscal/Monetary Coordination When the Anchor Cable Has Snapped Christopher A. Sims Princeton University sims@princeton.edu May 22, 2009 Outline Introduction The Fed balance sheet Implications for monetary

Other similar crisis: Euro, Emerging Markets

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Fiscal Policy and Economic Growth

Chapter 5 Fiscal Policy and Economic Growth In this chapter we introduce the government into the exogenous growth models we have analyzed so far. We first introduce and discuss the intertemporal budget

Chapter 5 Fiscal Policy and Economic Growth In this chapter we introduce the government into the exogenous growth models we have analyzed so far. We first introduce and discuss the intertemporal budget

STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

July 25, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Catherine Pattillo (IMF) and John Panzer (IDA) Prepared by the staffs of the

July 25, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Catherine Pattillo (IMF) and John Panzer (IDA) Prepared by the staffs of the

March 2007 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

March 27 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS The staff s debt sustainability analysis (DSA) suggests that the Kyrgyz Republic s external debt continues to pose a heavy burden,

March 27 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS The staff s debt sustainability analysis (DSA) suggests that the Kyrgyz Republic s external debt continues to pose a heavy burden,

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

International financial crises

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

Uganda: Joint Bank-Fund Debt Sustainability Analysis

February 26 Uganda: Joint Bank-Fund Debt Sustainability Analysis 1. Uganda s risk of debt distress is moderate. Its net present value (NPV) of debt-toexports ratio stands at 179 percent in 24/5, or below

February 26 Uganda: Joint Bank-Fund Debt Sustainability Analysis 1. Uganda s risk of debt distress is moderate. Its net present value (NPV) of debt-toexports ratio stands at 179 percent in 24/5, or below

Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1

1 December 26 Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1 1. Malawi s risk of debt distress after debt relief under the HIPC Initiative and the Multilateral

1 December 26 Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1 1. Malawi s risk of debt distress after debt relief under the HIPC Initiative and the Multilateral

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND SENEGAL. Joint Bank/Fund Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND SENEGAL Joint Bank/Fund Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and the International

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND SENEGAL Joint Bank/Fund Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and the International

Debt Management DPI 6 Coordination with Fiscal Policy

Debt Management DPI 6 Coordination with Fiscal Policy Regional workshop WB-CEMLA (SN-DeMPA) Mexico City, March18 to 22 2013 Jaime Coronado Q. Coordinator Public Debt Programs CEMLA Summary Coordination

Debt Management DPI 6 Coordination with Fiscal Policy Regional workshop WB-CEMLA (SN-DeMPA) Mexico City, March18 to 22 2013 Jaime Coronado Q. Coordinator Public Debt Programs CEMLA Summary Coordination

Reforms in a Debt Overhang

Structural Javier Andrés, Óscar Arce and Carlos Thomas 3 National Bank of Belgium, June 8 4 Universidad de Valencia, Banco de España Banco de España 3 Banco de España National Bank of Belgium, June 8 4

Structural Javier Andrés, Óscar Arce and Carlos Thomas 3 National Bank of Belgium, June 8 4 Universidad de Valencia, Banco de España Banco de España 3 Banco de España National Bank of Belgium, June 8 4

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NIGERIA

Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NIGERIA Joint Bank-Fund Debt Sustainability Analysis for 212 Under the Debt Sustainability

Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NIGERIA Joint Bank-Fund Debt Sustainability Analysis for 212 Under the Debt Sustainability

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL. Joint IMF/IDA Debt Sustainability Analysis

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL Joint IMF/IDA Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL Joint IMF/IDA Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

Chapter 18. The International Financial System

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Exam Number. Section

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course ANSWER KEY Final Exam March 1, 2010 Note: These are only suggested answers. You may have received partial or full credit for your answers

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course ANSWER KEY Final Exam March 1, 2010 Note: These are only suggested answers. You may have received partial or full credit for your answers

Marine Melikyan Public Debt Management Department Ministry of Finance Sovereign Debt Management Forum October 2016 Washington DC

Marine Melikyan Public Debt Management Department Ministry of Finance Sovereign Debt Management Forum 19-20 October 2016 Washington DC 1 Data for 2016 and 2017 are forcasted based on draft of 2017 budget

Marine Melikyan Public Debt Management Department Ministry of Finance Sovereign Debt Management Forum 19-20 October 2016 Washington DC 1 Data for 2016 and 2017 are forcasted based on draft of 2017 budget

Government debt. Lecture 9, ECON Tord Krogh. September 10, Tord Krogh () ECON 4310 September 10, / 55

ECON 4310 September 10, / 55") Government debt Lecture 9, ECON 4310 Tord Krogh September 10, 2013 Tord Krogh () ECON 4310 September 10, 2013 1 / 55 Today s lecture Topics: Basic concepts Tax smoothing Debt crisis Sovereign risk Tord

Government debt Lecture 9, ECON 4310 Tord Krogh September 10, 2013 Tord Krogh () ECON 4310 September 10, 2013 1 / 55 Today s lecture Topics: Basic concepts Tax smoothing Debt crisis Sovereign risk Tord

(January 2016). The fiscal year for Rwanda is from July June; however, this DSA is prepared on a calendar

. The fiscal year for Rwanda is from July June; however, this DSA is prepared on a calendar") May 25, 216 RWANDA FIFTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT AND REQUEST FOR EXTENSION, AND REQUEST FOR AN ARRANGEMENT UNDER THE STANDBY CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By

May 25, 216 RWANDA FIFTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT AND REQUEST FOR EXTENSION, AND REQUEST FOR AN ARRANGEMENT UNDER THE STANDBY CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By

CÔTE D'IVOIRE. Approved by Dominique Desruelle and Daria Zakharova (IMF); and Paloma Anos-Casero (IDA) November 21, 2017

; and Paloma Anos-Casero (IDA) November 21, 2017") CÔTE D'IVOIRE November 21, 217 SECOND REVIEWS UNDER AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY AND THE EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY DEBT SUSTAINABILITY ANALYSIS Approved

CÔTE D'IVOIRE November 21, 217 SECOND REVIEWS UNDER AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY AND THE EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY DEBT SUSTAINABILITY ANALYSIS Approved

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA. Joint Bank-Fund Debt Sustainability Analysis 1

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA Joint Bank-Fund Debt Sustainability Analysis 1 Public Disclosure Authorized Public Disclosure Authorized

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA Joint Bank-Fund Debt Sustainability Analysis 1 Public Disclosure Authorized Public Disclosure Authorized

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND REPUBLIC OF CONGO. Joint Bank-Fund Debt Sustainability Analysis 2013 Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND REPUBLIC OF CONGO Joint Bank-Fund Debt Sustainability Analysis 213 Update Public Disclosure Authorized Prepared

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND REPUBLIC OF CONGO Joint Bank-Fund Debt Sustainability Analysis 213 Update Public Disclosure Authorized Prepared

The sharp accumulation in government debt can t go on forever

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

REPUBLIC OF THE MARSHALL ISLANDS

REPUBLIC OF THE MARSHALL ISLANDS December 19, 213 STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Stephan Danninger, Ranil Salgado, Jeffrey D. Lewis and Sudhir

REPUBLIC OF THE MARSHALL ISLANDS December 19, 213 STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Stephan Danninger, Ranil Salgado, Jeffrey D. Lewis and Sudhir

FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS

December 17, 215 FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Masato Miyazaki (IMF) and John Panzer (IDA) The Debt Sustainability Analysis (DSA)

December 17, 215 FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Masato Miyazaki (IMF) and John Panzer (IDA) The Debt Sustainability Analysis (DSA)

LEARNING OBJECTIVES AND STRUCTURE OF PART 2

The Public DSA Framework for Market Access Countries Instructor: Adina Popescu (IMF) Unit 1 LEARNING OBJECTIVES AND STRUCTURE OF PART 2 This training material is the property of the International Monetary

The Public DSA Framework for Market Access Countries Instructor: Adina Popescu (IMF) Unit 1 LEARNING OBJECTIVES AND STRUCTURE OF PART 2 This training material is the property of the International Monetary

MALAWI. Approved By. December 27, Prepared by the staffs of the International Monetary Fund and the International Development Association

December 27, 213 MALAWI THIRD AND FOURTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUESTS FOR WAIVER OF PERFORMANCE CRITERIA, EXTENSION OF THE ARRANGEMENT, REPHASING OF DISBURSEMENTS, AND

December 27, 213 MALAWI THIRD AND FOURTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUESTS FOR WAIVER OF PERFORMANCE CRITERIA, EXTENSION OF THE ARRANGEMENT, REPHASING OF DISBURSEMENTS, AND

January 2008 NIGER: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

January 28 NIGER: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS Niger remains at moderate risk of debt distress. Despite low debt ratios following debt relief, most recently in 26 under the MDRI, Niger

January 28 NIGER: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS Niger remains at moderate risk of debt distress. Despite low debt ratios following debt relief, most recently in 26 under the MDRI, Niger

Fiscal consolidation in EU. Dariusz K. Rosati Warsaw,

Fiscal consolidation in EU Dariusz K. Rosati Warsaw, 21.10.2011. Fiscal situation in EU: an overview Before the crisis 2008 2009, fiscal position differed in different EU countries: in the Euro Area countries

Fiscal consolidation in EU Dariusz K. Rosati Warsaw, 21.10.2011. Fiscal situation in EU: an overview Before the crisis 2008 2009, fiscal position differed in different EU countries: in the Euro Area countries

Vietnam: Joint Bank-Fund Debt Sustainability Analysis 1

1 November 2006 Vietnam: Joint Bank-Fund Debt Sustainability Analysis 1 Public sector debt sustainability Since the time of the last joint DSA, the most important new signal on the likely direction of

1 November 2006 Vietnam: Joint Bank-Fund Debt Sustainability Analysis 1 Public sector debt sustainability Since the time of the last joint DSA, the most important new signal on the likely direction of

Macroeconomic Accounts and Policies: Introduction and Internal and External Balances(*)

") Macroeconomic Accounts and Policies: Introduction and Internal and External Balances(*) World Bank/Poverty and Equity Summer University, Washington, DC, July 20-21, 2017 Alvaro Manoel International Consultant

Macroeconomic Accounts and Policies: Introduction and Internal and External Balances(*) World Bank/Poverty and Equity Summer University, Washington, DC, July 20-21, 2017 Alvaro Manoel International Consultant

MINISTRY OF FINANCE AND ECONOMIC AFFAIRS DEBT SUSTAINABILITY ANALYSIS Directorate of Debt Management and Economic Cooperation

MINISTRY OF FINANCE AND ECONOMIC AFFAIRS A S D DEBT SUSTAINABILITY ANALYSIS 2015 Directorate of Debt Management and Economic Cooperation Table of Contents LIST OF TABLES... 2 LIST OF FIGURES... 2 LIST

MINISTRY OF FINANCE AND ECONOMIC AFFAIRS A S D DEBT SUSTAINABILITY ANALYSIS 2015 Directorate of Debt Management and Economic Cooperation Table of Contents LIST OF TABLES... 2 LIST OF FIGURES... 2 LIST

Public Debt Management

The World Bank Public Debt Management Emre Balibek Senior Debt Specialist Macroeconomics and Fiscal Management Global Practice Structure Public Debt Management (PDM) Risks in PDMs Medium Term Debt Management

The World Bank Public Debt Management Emre Balibek Senior Debt Specialist Macroeconomics and Fiscal Management Global Practice Structure Public Debt Management (PDM) Risks in PDMs Medium Term Debt Management

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

May 9, 17 STAFF REPORT FOR THE 17 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Jorge Roldos and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA) Prepared by the staff of the International

May 9, 17 STAFF REPORT FOR THE 17 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Jorge Roldos and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA) Prepared by the staff of the International

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016 THIS TRAINING MATERIAL IS THE PROPERTY OF THE JOINT VIENNA INSTITUTE (JVI)

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016 THIS TRAINING MATERIAL IS THE PROPERTY OF THE JOINT VIENNA INSTITUTE (JVI)

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SIERRA LEONE. Joint IMF/World Bank Debt Sustainability Analysis 2010

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SIERRA LEONE Joint IMF/World Bank Debt Sustainability Analysis 21 Prepared by the staffs of the International Monetary Fund and the

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SIERRA LEONE Joint IMF/World Bank Debt Sustainability Analysis 21 Prepared by the staffs of the International Monetary Fund and the

Economic Policy in the Crisis. Lars Calmfors Jönköping International Business School, 2 November 2009

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Final exam Non-detailed correction 3 hours. This are indicative directions on how structure the essay questions and what was expected.

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

Macroeconomic Diagnostics (MDSx) Module

Module") Macroeconomic Diagnostics (MDSx) Module 11 External Sustainability and External Vulnerability This training material is the property of the International Monetary Fund (IMF) and is intended for use in

Macroeconomic Diagnostics (MDSx) Module 11 External Sustainability and External Vulnerability This training material is the property of the International Monetary Fund (IMF) and is intended for use in

STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

February 7, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Vitaliy Kramarenko (IMF) and Paloma Anós Casero (IDA) Prepared by the staffs

February 7, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Vitaliy Kramarenko (IMF) and Paloma Anós Casero (IDA) Prepared by the staffs

17.2 U.S. Government Spending and Revenue Introduction. Chapter 17 The Government and the Macroeconomy. In 2008, federal spending

Chapter 17 The Government and the Macroeconomy By Charles I. Jones Media Slides Created By Dave Brown Penn State University 17.2 U.S. Government Spending and Revenue In 2008, federal spending Was about

Chapter 17 The Government and the Macroeconomy By Charles I. Jones Media Slides Created By Dave Brown Penn State University 17.2 U.S. Government Spending and Revenue In 2008, federal spending Was about

INTERNATIONAL MONETARY FUND. Information Note on Modifications to the Fund s Debt Sustainability Assessment Framework for Market Access Countries

INTERNATIONAL MONETARY FUND Information Note on Modifications to the Fund s Debt Sustainability Assessment Framework for Market Access Countries Prepared by the Policy Development and Review Department

INTERNATIONAL MONETARY FUND Information Note on Modifications to the Fund s Debt Sustainability Assessment Framework for Market Access Countries Prepared by the Policy Development and Review Department