INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL. Joint Bank-Fund Debt Sustainability Analysis

|

|

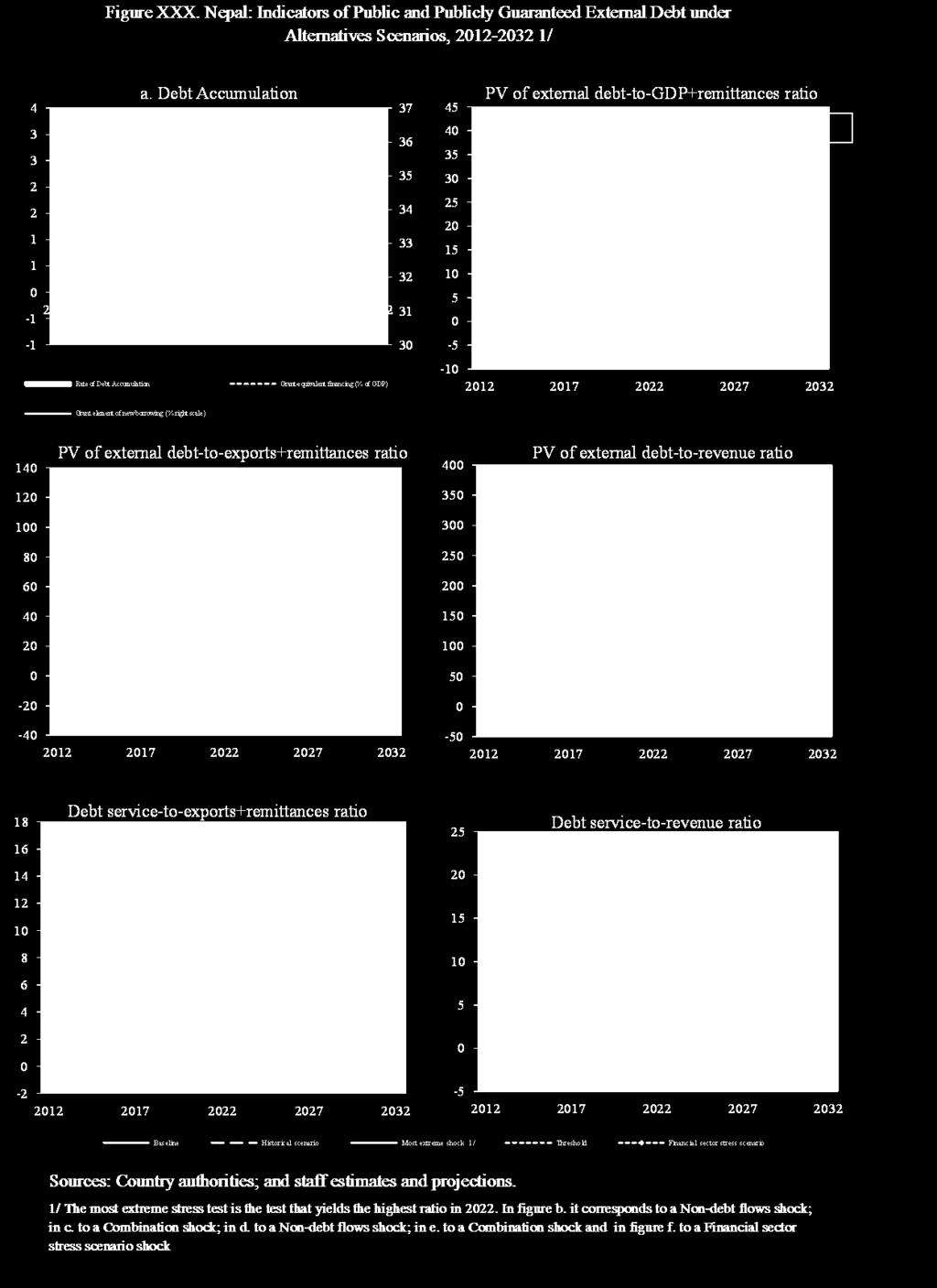

|

- Jane Goodwin

- 5 years ago

- Views:

Transcription

1 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL Joint Bank-Fund Debt Sustainability Analysis Prepared by the staffs of the International Development Association and the International Monetary Fund Approved by Jeffrey D. Lewis and Ernesto May (IDA) Laura Papi and Christian Mumssen (IMF) November 2, 2012 Nepal remains at moderate risk of debt distress. 1 The baseline external public debt indicators show that external debt dynamics are sound and broadly resilient to standard stress tests. Nevertheless, under an alternative scenario reflecting systemic financial sector stress, external debt indicators breach the indicative thresholds, underscoring the pressing need to address financial sector vulnerabilities. 2 A prudent fiscal stance remains appropriate, and net domestic financing of deficits should be contained to around 2 percent of GDP in the near term. However, a marginal increase in net domestic financing (by less than ¾ percent of GDP) to finance much-needed capital spending could be warranted in the context of enhanced public financial management. In this vein, stronger efforts to improve the utilization of foreign aid, particularly grants, would mitigate pressures on the domestic debt market, while structural reforms to boost long-run growth and revenue generation would improve overall public debt sustainability. I. BACKGROUND Public Disclosure Authorized 1. The total stock of public debt in Nepal remained stable at 33¼ percent of GDP by end- 2011/12 3, the same level of 2010/11 and down from around 60 percent a decade ago, largely reflecting a prudent fiscal policy. External public debt stood at 20½ percent of GDP (US$ 3½ billion) by end-2011/12, rising from 18¾ percent of GDP due mainly to exchange rate depreciation against the U.S. dollar. The World Bank and Asian Development Bank (ADB) account for 83 percent of external debt, while Japan is the largest bilateral 1 The risk rating is determined using the Low-Income Country Debt Sustainability Analysis (LIC-DSA) framework. Nepal s fiscal year starts in mid-july. 2 The thresholds are determined based on Nepal s policy performance rating, which is medium according to the CPIA score. 3 The fiscal year ends on July 15.

2 2 creditor accounting for 6¼ percent of total external debt. Domestic public debt stood at 12¾ percent of GDP by end-2011/12, compared to 14½ percent a year ago. II. MACROECONOMIC ASSUMPTIONS 2. Macroeconomic assumptions are broadly similar to those of the previous DSA. Key differences include: (i) a higher path for fiscal revenue over the medium term (taking into account the strong reform momentum in this area); and (ii) a small narrowing of the external current account deficit, which to some extent reflects the correction of exchange rate overvaluation as a result of recent depreciation against the U.S. dollar (Box 1). Other assumptions are as follows: Box 1. Macro Assumptions Comparison Table Previous DSA Current DSA Difference (current vs previous) MT LT 2012 MT LT MT LT Real growth (%) Inflation (GDP deflator, %) Revenue and grants(% GDP) Grants (% GDP) Primary expenditure (% GDP) Primary deficit (% GDP) NDF (% GDP) Exports of G&S (y/y growth) Imports of G&S (y/y growth) Remittances (y/y growth) Current account balance(% GDP) Note: MT stands for medium term sand reflects average over the next 5 years, and LT refers to long term and generally reflects indicators at the end of the projection period. Real GDP growth is projected to slow to 3¾ percent in 2012/13 compared with 4½ percent in 2011/12, and then gradually accelerate to 4 percent in the medium term. This short-term drop in growth reflects a softening global economic outlook, and particularly much slower activity in India. The medium term outlook would be supported by a gradual global recovery, enhanced political stability, and rising investment. Over the long run, resolution of such structural impediments as infrastructure would set growth on a higher sustainable path. Inflation is expected to decline to 8¼ percent in 2012/13 and further to 5 percent over the long run, assuming moderating external price pressures. The exchange rate peg to the Indian rupee is assumed to remain at the current level over the projection period, and the external current account is projected to move from a small surplus in 2012/13 to moderate deficits over the medium and long term. Remittance growth is projected to moderate to 7½ percent over the long

3 3 run, largely reflecting a gradually slowing historical trend and economic prospects of migrant host countries. 4 Exports are hampered by structural bottlenecks as well as exchange rate overvaluation, and the ratio of exports to GDP is expected to further decline through the projection period reflecting weak competitiveness. Imports are largely driven by remittances, and thus would also decline in relation to GDP as remittances moderate. Both exports and imports are projected to grow by an annual average of 7-8 percent. Fiscal policy is assumed to remain prudent, with net domestic financing (NDF) standing at 2¼ percent of GDP over the medium term, and at 2¾ percent of GDP in the long run. Revenue and grants are projected to reach 17½ percent and 1¾ percent of GDP over the long run, respectively (compared with 15¾ percent and 2½ percent in 2011/12). Higher revenue is mainly attributable to improved tax administration and revenue policy, while lower grants are associated with the end of the peace process and an expected shift in donor financing from grants to concessional loans. On the expenditure side, current spending has been constrained and capital expenditures under-executed in 2011/12, leading to a lower projection of primary expenditures compared to the previous DSA. Assuming improved budget execution and higher capital spending, primary expenditures would stand at 21¼ percent over the long run. As a consequence, the primary deficit would stand at 2 percent of GDP in the long run (same as in the previous DSA). Concessionality of foreign loans is projected to decline gradually. With rising per capita income and capital spending, new borrowings on relatively less favorable terms, for example, loans from non-traditional donors to finance hydropower projects, could become increasingly important. As a result, the assumed grant element (the measure of concessionality in this DSA exercise), would fall to 32½ percent by A. Baseline III. EXTERNAL DEBT SUSTAINABILITY 3. Under baseline projections, Nepal s debt indicators remain below the indicative sustainability thresholds (Table 3b, Figure 1). As in the previous DSA, remittances are formally included in the analysis because the inflows (accounting for 23 percent of GDP) represent a sizeable and comparatively stable element of the balance of payments. Nevertheless, debt dynamics are also vulnerable to the potential volatility of remittances. The impact of a sharp slowdown in remittances is discussed below. With relatively conservative 4 For empirical study, see Remittances in South Asia and the Philippines: Determinants and Outlook, IMF Selected Issues Paper, 2009.

4 4 assumptions on growth and external borrowing, current projections indicate that the baseline debt ratios would remain sustainable over the long term. B. Stress Tests and Alternative Scenarios 4. Nepal s debt dynamics remain generally sound under standard stress tests. Standard tests include shocks to GDP growth, exports, non-debt creating flows and combinations of these shocks, as well as a one-time 30 percent exchange rate depreciation. Nepal s debt indicators are below the sustainability thresholds under all but the most severe of these stress test scenarios. More specifically, Nepal s debt dynamics remain susceptible to shocks to remittance inflows. A substantial slowdown in remittances reflected in a one standard deviation below average growth of non-debt creating flows in 2013 and 2014 would cause the PV of external debt to export + remittance ratio to exceed the indicative threshold by 10 percentage points in Non-standard scenarios, based on Nepal-specific risks, highlight the financial sector fragilities as a key risk. Higher remittances have eased banks liquidity situation in 2011/12, but heightened credit risk following the recent sharp downturn in real estate prices remains a key vulnerability. A hypothetical financial stress scenario mimics the shocks that could be triggered by a loss of confidence or a drop in remittances leading to selfreinforcing feedback between deposit runs, capital flight, and a systemic financial sector stress. Under this scenario, the ratio of PV of external debt-to-gdp+remittances would rise substantially and stay above the threshold in , peaking in 2016 at 40½ percent; the PV of external debt-to-revenue ratio would be above the threshold across the whole projection period, and peak at 337¾ percent in 2013; and the debt service to revenue ratio would also be slightly above the threshold from 2016 on. (Figure 1). 5 IV. PUBLIC DEBT SUSTAINABILITY 6. Under the baseline scenario, the PV of public debt would be moderately higher at the end of the projection period. As a share of GDP, the PV of public debt increases from 31 percent in 2012 to 36 by the end of the projection period. In percent of revenue and grants, the PV of public debt increases from 171 percent to 190 percent. 7. Although the total level of public debt remains broadly in the same margin, its composition is projected to shift toward domestic debt due to constraints on the 5 Key assumptions include (i) a 50 percent loss of central bank foreign exchange reserves; (ii) a one-time exchange rate depreciation of 33 percent; (iii) an output loss of 30 percent over a 4 year horizon; and (iv) a fiscal cost (for bank resolution and deposit coverage) of 23 percent of GDP presumably financed through domestic debt, but later replaced by foreign debt given the more favorable terms and the need to supplement depleted foreign exchange reserves.

5 5 capacity to mobilize external resources. 6 In the context of the current exchange rate peg, weak competitiveness and financial sector vulnerabilities, sizeable increases in public domestic debt could be increasingly difficult to accommodate. This could lead to higher real interest rates potentially crowding out private sector credit or requiring a tighter rein on primary fiscal expenditures which could endanger anti-poverty and development goals. 8. Stress tests suggest vulnerability to shocks. The largest adverse impact arises from the heightened financial stress scenario outlined above, which would raise the PV of debt to GDP ratio to over 90 percent. Among the standard stress tests, the largest impact on public debt arises from an increase in other debt-creating flows by 10 percent of GDP, which would increase the PV of debt-to-gdp by more than 9 percentage points and leave it at higher levels for a prolonged period. 9. Contingent liabilities arising from, inter alia, the SOE sector and pension scheme could pose risks to this assessment. NOC and NEA are making substantial losses, and hold domestic debt arrears equivalent to 5¾ percent of GDP, with the majority owed to fiscal or quasi-fiscal agencies. Meanwhile, the on-budget pension scheme has no independent source of funding (such as employee contributions), and could over time cause the fiscal stance to deteriorate. Limited information on the pension scheme impedes a reliable estimate of the financing needs in the periods ahead and their potential impact on debt dynamics. The clearance of SOE arrears would presumably be based on first introducing an automatic fuel pricing mechanism supplemented by a social protection scheme, the cost of which depends on the program design. V. AUTHORITIES' VIEWS 10. The authorities concurred with the DSA and its policy messages. They are aware of the risk to debt dynamics posed by financial sector stress and other contingent liabilities. Meanwhile, they recognize the need to improve utilization of donors resources to curb the increase in domestic debt and commit to contain net domestic financing to 2 percent of GDP in 2012/13. However, they stress that systemic financial sector stress is not very likely and the chunk of the banking sector is generally sound though weaknesses concentrate in a few smaller banks and financial companies. They also argue that foreign grants would be stronger than staff projection given the sizable commitments. 6 Domestic debts include T-bills, development bonds, overdraft from the Nepal Rastra Bank, etc. The maturity of T-bills ranges from 28 days to a year, with T-bills of 91 days most actively traded.

6 6 VI. CONCLUSION 11. Nepal faces a moderate risk of external public debt distress but risks could arise from financial sector vulnerabilities, a shock to remittances, or quasi-fiscal liabilities. Although external debt burden indicators generally do not breach the thresholds in both baseline scenario and stress tests, under a heightened financial stress scenario, the debt burden rises notably, with external debt breaching thresholds for prolonged periods. This test stresses the need to urgently address financial sector weaknesses via in-depth reforms. The analysis also suggests that contingent liabilities from SOEs and the pension scheme could pose additional risks to debt dynamics. This highlights the importance of containing net domestic financing of deficits to around 2 percent of GDP in the near term that would create space for contingent liabilities, though there is marginal room to accommodate additional capital spending in case it is strengthened via enhanced public financial management.

7 7

8 8 Figure XXX.Nepal: Indicators of Public Debt Under Alternative Scenarios, / PV of Debt-to-GDP Ratio Baseline Fix Primary Balance Most extreme shock Non-debt flows Historical scenario Financial sector stress scenario PV of Debt-to-Revenue Ratio 2/ Debt Service-to-Revenue Ratio 2/ Sources: Country authorities; and staff estimates and projections. 1/ The most extreme stress test is the test that yields the highest ratio in / Revenues are defined inclusive of grants.

9 Table 1a.Nepal: Public Sector Debt Sustainability Framework, Baseline Scenario, (In percent of GDP, unless otherwise indicated) Actual Average 5/ Standard Deviation 5/ Estimate Projections Average Average Public sector debt 1/ o/w foreign-currency denominated Change in public sector debt Identified debt-creating flows Primary deficit Revenue and grants of which: grants Primary (noninterest) expenditure Automatic debt dynamics Contribution from interest rate/growth differential of which: contribution from average real interest rate of which: contribution from real GDP growth Contribution from real exchange rate depreciation Other identified debt-creating flows Privatization receipts (negative) Recognition of implicit or contingent liabilities Debt relief (HIPC and other) Other (specify, e.g. bank recapitalization) Residual, including asset changes Other Sustainability Indicators PV of public sector debt o/w foreign-currency denominated o/w external PV of contingent liabilities (not included in public sector debt) Gross financing need 2/ PV of public sector debt-to-revenue and grants ratio (in percent) PV of public sector debt-to-revenue ratio (in percent) o/w external 3/ Debt service-to-revenue and grants ratio (in percent) 4/ Debt service-to-revenue ratio (in percent) 4/ Primary deficit that stabilizes the debt-to-gdp ratio Key macroeconomic and fiscal assumptions Real GDP growth (in percent) Average nominal interest rate on forex debt (in percent) Average real interest rate on domestic debt (in percent) Real exchange rate depreciation (in percent, + indicates depreciation) Inflation rate (GDP deflator, in percent) Growth of real primary spending (deflated by GDP deflator, in percent) Grant element of new external borrowing (in percent) Sources: Country authorities; and staff estimates and projections. 1/ [Indicate coverage of public sector, e.g., general government or nonfinancial public sector. Also whether net or gross debt is used.] 2/ Gross financing need is defined as the primary deficit plus debt service plus the stock of short-term debt at the end of the last period. 3/ Revenues excluding grants. 4/ Debt service is defined as the sum of interest and amortization of medium and long-term debt. 5/ Historical averages and standard deviations are generally derived over the past 10 years, subject to data availability.

10 10 Table 2a.Nepal: Sensitivity Analysis for Key Indicators of Public Debt Projections Baseline A. Alternative scenarios A1. Real GDP growth and primary balance are at historical averages A2. Primary balance is unchanged from A3. Permanently lower GDP growth 1/ B. Bound tests B1. Real GDP growth is at historical average minus one standard deviations in B2. Primary balance is at historical average minus one standard deviations in B3. Combination of B1-B2 using one half standard deviation shocks B4. One-time 30 percent real depreciation in B5. 10 percent of GDP increase in other debt-creating flows in Baseline A. Alternative scenarios A1. Real GDP growth and primary balance are at historical averages A2. Primary balance is unchanged from A3. Permanently lower GDP growth 1/ B. Bound tests B1. Real GDP growth is at historical average minus one standard deviations in B2. Primary balance is at historical average minus one standard deviations in B3. Combination of B1-B2 using one half standard deviation shocks B4. One-time 30 percent real depreciation in B5. 10 percent of GDP increase in other debt-creating flows in Baseline A. Alternative scenarios A1. Real GDP growth and primary balance are at historical averages A2. Primary balance is unchanged from A3. Permanently lower GDP growth 1/ B. Bound tests PV of Debt-to-GDP Ratio PV of Debt-to-Revenue Ratio 2/ Debt Service-to-Revenue Ratio 2/ B1. Real GDP growth is at historical average minus one standard deviations in B2. Primary balance is at historical average minus one standard deviations in B3. Combination of B1-B2 using one half standard deviation shocks B4. One-time 30 percent real depreciation in B5. 10 percent of GDP increase in other debt-creating flows in Sources: Country authorities; and staff estimates and projections. 1/ Assumes that real GDP growth is at baseline minus one standard deviation divided by the square root of the length of the projection period. 2/ Revenues are defined inclusive of grants.

11 11 Table 3a.: External Debt Sustainability Framework, Baseline Scenario, / (In percent of GDP, unless otherwise indicated) Actual Historical 6/ Standard 6/ Projections Average Deviation Average Average External debt (nominal) 1/ o/w public and publicly guaranteed (PPG) Change in external debt Identified net debt-creating flows Non-interest current account deficit Deficit in balance of goods and services Exports Imports Net current transfers (negative = inflow) o/w official Other current account flows (negative = net inflow) Net FDI (negative = inflow) Endogenous debt dynamics 2/ Contribution from nominal interest rate Contribution from real GDP growth Contribution from price and exchange rate changes Residual (3-4) 3/ o/w exceptional financing PV of external debt 4/ In percent of exports PV of PPG external debt In percent of exports In percent of government revenues Debt service-to-exports ratio (in percent) PPG debt service-to-exports ratio (in percent) PPG debt service-to-revenue ratio (in percent) Total gross financing need (Billions of U.S. dollars) Non-interest current account deficit that stabilizes debt ratio Key macroeconomic assumptions Real GDP growth (in percent) GDP deflator in US dollar terms (change in percent) Effective interest rate (percent) 5/ Growth of exports of G&S (US dollar terms, in percent) Growth of imports of G&S (US dollar terms, in percent) Grant element of new public sector borrowing (in percent) Government revenues (excluding grants, in percent of GDP) Aid flows (in Billions of US dollars) 7/ o/w Grants o/w Concessional loans Grant-equivalent financing (in percent of GDP) 8/ Grant-equivalent financing (in percent of external financing) 8/ Memorandum items: Nominal GDP (Billions of US dollars) Nominal dollar GDP growth PV of PPG external debt (in Billions of US dollars) (PVt-PVt-1)/GDPt-1 (in percent) Gross workers' remittances (Billions of US dollars) PV of PPG external debt (in percent of GDP + remittances) PV of PPG external debt (in percent of exports + remittances) Debt service of PPG external debt (in percent of exports + remittances) Sources: Country authorities; and staff estimates and projections. 0 1/ Includes both public and private sector external debt. 2/ Derived as [r - g - ρ(1+g)]/(1+g+ρ+gρ) times previous period debt ratio, with r = nominal interest rate; g = real GDP growth rate, and ρ = growth rate of GDP deflator in U.S. dollar terms. 3/ Includes exceptional financing (i.e., changes in arrears and debt relief); changes in gross foreign assets; and valuation adjustments. For projections also includes contribution from price and exchange rate changes. 4/ Assumes that PV of private sector debt is equivalent to its face value. 5/ Current-year interest payments divided by previous period debt stock. 6/ Historical averages and standard deviations are generally derived over the past 10 years, subject to data availability. 7/ Defined as grants, concessional loans, and debt relief. 8/ Grant-equivalent financing includes grants provided directly to the government and through new borrowing (difference between the face value and the PV of new debt).

12 12 Table 3b.Nepal: Sensitivity Analysis for Key Indicators of Public and Publicly Guaranteed External Debt, (In percent) Projections Baseline A. Alternative Scenarios A1. Key variables at their historical averages in / A2. New public sector loans on less favorable terms in B. Bound Tests PV of external debt-to-gdp+remittances ratio B1. Real GDP growth at historical average minus one standard deviation in B2. Export value growth at historical average minus one standard deviation in / B3. US dollar GDP deflator at historical average minus one standard deviation in B4. Net non-debt creating flows at historical average minus one standard deviation in / B5. Combination of B1-B4 using one-half standard deviation shocks B6. One-time 30 percent nominal depreciation relative to the baseline in / Baseline A. Alternative Scenarios A1. Key variables at their historical averages in / A2. New public sector loans on less favorable terms in B. Bound Tests PV of external debt-to-exports+remittances ratio B1. Real GDP growth at historical average minus one standard deviation in B2. Export value growth at historical average minus one standard deviation in / B3. US dollar GDP deflator at historical average minus one standard deviation in B4. Net non-debt creating flows at historical average minus one standard deviation in / B5. Combination of B1-B4 using one-half standard deviation shocks B6. One-time 30 percent nominal depreciation relative to the baseline in / Baseline A. Alternative Scenarios A1. Key variables at their historical averages in / A2. New public sector loans on less favorable terms in B. Bound Tests PV of external debt-to-revenue ratio B1. Real GDP growth at historical average minus one standard deviation in B2. Export value growth at historical average minus one standard deviation in / B3. US dollar GDP deflator at historical average minus one standard deviation in B4. Net non-debt creating flows at historical average minus one standard deviation in / B5. Combination of B1-B4 using one-half standard deviation shocks B6. One-time 30 percent nominal depreciation relative to the baseline in /

13 13 Baseline A. Alternative Scenarios A1. Key variables at their historical averages in / A2. New public sector loans on less favorable terms in B. Bound Tests Table 3b.Nepal: Sensitivity Analysis for Key Indicators of Public and Publicly Guaranteed External Debt, (continued) (In percent) Debt service-to-exports+remittances ratio B1. Real GDP growth at historical average minus one standard deviation in B2. Export value growth at historical average minus one standard deviation in / B3. US dollar GDP deflator at historical average minus one standard deviation in B4. Net non-debt creating flows at historical average minus one standard deviation in / B5. Combination of B1-B4 using one-half standard deviation shocks B6. One-time 30 percent nominal depreciation relative to the baseline in / Baseline A. Alternative Scenarios A1. Key variables at their historical averages in / A2. New public sector loans on less favorable terms in B. Bound Tests Debt service-to-revenue ratio B1. Real GDP growth at historical average minus one standard deviation in B2. Export value growth at historical average minus one standard deviation in / B3. US dollar GDP deflator at historical average minus one standard deviation in B4. Net non-debt creating flows at historical average minus one standard deviation in / B5. Combination of B1-B4 using one-half standard deviation shocks B6. One-time 30 percent nominal depreciation relative to the baseline in / Memorandum item: Grant element assumed on residual financing (i.e., financing required above baseline) 6/ Sources: Country authorities; and staff estimates and projections. 1/ Variables include real GDP growth, growth of GDP deflator (in U.S. dollar terms), non-interest current account in percent of GDP, and non-debt creating flows. 2/ Assumes that the interest rate on new borrowing is by 2 percentage points higher than in the baseline., while grace and maturity periods are the same as in the baseline. 3/ Exports values are assumed to remain permanently at the lower level, but the current account as a share of GDP is assumed to return to its baseline level after the shock (implicitly assuming an offsetting adjustment in import levels). 4/ Includes official and private transfers and FDI. 5/ Depreciation is defined as percentage decline in dollar/local currency rate, such that it never exceeds 100 percent. 6/ Applies to all stress scenarios except for A2 (less favorable financing) in which the terms on all new financing are as specified in footnote 2.

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BENIN JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BENIN JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS Public Disclosure Authorized Prepared by the staffs of

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BENIN JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS Public Disclosure Authorized Prepared by the staffs of

JOINT IMF/WORLD BANK DEBT SUSTAINABILITY

ZIMBABWE JOINT IMF/WORLD BANK DEBT SUSTAINABILITY May 5, 211 ANALYSIS 1 Approved By Mark Plant and Dominique Desruelle (IMF) Marcelo Giugale and Jeffery Lewis (IDA) Prepared by The International Monetary

ZIMBABWE JOINT IMF/WORLD BANK DEBT SUSTAINABILITY May 5, 211 ANALYSIS 1 Approved By Mark Plant and Dominique Desruelle (IMF) Marcelo Giugale and Jeffery Lewis (IDA) Prepared by The International Monetary

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA August 27, 212 STAFF REPORT FOR THE 212 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde-Wolf and Elliott Harris (IMF) and Jeffrey

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA August 27, 212 STAFF REPORT FOR THE 212 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde-Wolf and Elliott Harris (IMF) and Jeffrey

STAFF REPORT FOR THE 2015 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE

January 5, 216 BANGLADESH STAFF REPORT FOR THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Markus Rodlauer and Catherine Anne Maria Pattillo (IMF) and Satu Kahkonen (IDA)

January 5, 216 BANGLADESH STAFF REPORT FOR THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Markus Rodlauer and Catherine Anne Maria Pattillo (IMF) and Satu Kahkonen (IDA)

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

February 9, 218 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Markus Rodlauer and Johannes Wiegand (IMF), and John Panzer (IDA) Prepared by Staffs of the International

February 9, 218 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Markus Rodlauer and Johannes Wiegand (IMF), and John Panzer (IDA) Prepared by Staffs of the International

FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS

December 17, 215 FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Masato Miyazaki (IMF) and John Panzer (IDA) The Debt Sustainability Analysis (DSA)

December 17, 215 FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Masato Miyazaki (IMF) and John Panzer (IDA) The Debt Sustainability Analysis (DSA)

(January 2016). The fiscal year for Rwanda is from July June; however, this DSA is prepared on a calendar

. The fiscal year for Rwanda is from July June; however, this DSA is prepared on a calendar") May 25, 216 RWANDA FIFTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT AND REQUEST FOR EXTENSION, AND REQUEST FOR AN ARRANGEMENT UNDER THE STANDBY CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By

May 25, 216 RWANDA FIFTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT AND REQUEST FOR EXTENSION, AND REQUEST FOR AN ARRANGEMENT UNDER THE STANDBY CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND REPUBLIC OF CONGO. Joint Bank-Fund Debt Sustainability Analysis 2013 Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND REPUBLIC OF CONGO Joint Bank-Fund Debt Sustainability Analysis 213 Update Public Disclosure Authorized Prepared

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND REPUBLIC OF CONGO Joint Bank-Fund Debt Sustainability Analysis 213 Update Public Disclosure Authorized Prepared

CENTRAL AFRICAN REPUBLIC

CENTRAL AFRICAN REPUBLIC June 29, 217 SECOND REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, FINANCING ASSURANCES REVIEW, AND REQUEST FOR AUGMENTATION OF ACCESS DEBT SUSTAINABILITY ANALYSIS 6 Approved

CENTRAL AFRICAN REPUBLIC June 29, 217 SECOND REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, FINANCING ASSURANCES REVIEW, AND REQUEST FOR AUGMENTATION OF ACCESS DEBT SUSTAINABILITY ANALYSIS 6 Approved

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA. Joint Bank-Fund Debt Sustainability Analysis 1

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA Joint Bank-Fund Debt Sustainability Analysis 1 Public Disclosure Authorized Public Disclosure Authorized

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA Joint Bank-Fund Debt Sustainability Analysis 1 Public Disclosure Authorized Public Disclosure Authorized

ISLAMIC REPUBLIC OF AFGHANISTAN

July 1, 216 REQUEST FOR A THREE YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Bob Matthias Traa (IMF), Satu Kähkönen (IDA) International

July 1, 216 REQUEST FOR A THREE YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Bob Matthias Traa (IMF), Satu Kähkönen (IDA) International

INTERNATIONAL MONETARY FUND ST. LUCIA. External and Public Debt Sustainability Analysis. Prepared by the Staff of the International Monetary Fund

INTERNATIONAL MONETARY FUND ST. LUCIA External and Public Debt Sustainability Analysis Prepared by the Staff of the International Monetary Fund December 23, 21 This debt sustainability analysis (DSA) assesses

INTERNATIONAL MONETARY FUND ST. LUCIA External and Public Debt Sustainability Analysis Prepared by the Staff of the International Monetary Fund December 23, 21 This debt sustainability analysis (DSA) assesses

REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS

May 18, 217 REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Dominique Desruelle and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA)

May 18, 217 REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Dominique Desruelle and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA)

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA

August 29, 213 THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITYANALYSIS Approved By Michael Atingi-Ego and Elliott Harris (IMF) and Jeffrey

August 29, 213 THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITYANALYSIS Approved By Michael Atingi-Ego and Elliott Harris (IMF) and Jeffrey

Risk of external debt distress:

November 1, 17 SEVENTH AND EIGHTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUEST FOR WAIVER OF NONOBSERVANCE OF PERFORMANCE CRITERIA DEBT SUSTAINABILITY ANALYSIS Risk of external debt

November 1, 17 SEVENTH AND EIGHTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUEST FOR WAIVER OF NONOBSERVANCE OF PERFORMANCE CRITERIA DEBT SUSTAINABILITY ANALYSIS Risk of external debt

PAPUA NEW GUINEA STAFF REPORT FOR THE 2015 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

October 8, 215 PAPUA NEW GUINEA STAFF REPORT FOR THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Hoe Ee Khor and Steven Barnett (IMF) Satu Kahkonen (IDA) Prepared by the staffs

October 8, 215 PAPUA NEW GUINEA STAFF REPORT FOR THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Hoe Ee Khor and Steven Barnett (IMF) Satu Kahkonen (IDA) Prepared by the staffs

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NIGERIA

Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NIGERIA Joint Bank-Fund Debt Sustainability Analysis for 212 Under the Debt Sustainability

Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NIGERIA Joint Bank-Fund Debt Sustainability Analysis for 212 Under the Debt Sustainability

KYRGYZ REPUBLIC THIRD REVIEW UNDER THE THREE-YEAR ARRANGEMENT

December, 1 THIRD REVIEW UNDER THE THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUEST FOR MODIFICATION OF PERFORMANCE CRITERIA DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Juha Kähkönen

December, 1 THIRD REVIEW UNDER THE THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUEST FOR MODIFICATION OF PERFORMANCE CRITERIA DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Juha Kähkönen

KINGDOM OF LESOTHO SIXTH REVIEW UNDER THE THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS

August 2, 213 KINGDOM OF LESOTHO SIXTH REVIEW UNDER THE THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde- Wolf and Chris Lane (IMF) Marcelo

August 2, 213 KINGDOM OF LESOTHO SIXTH REVIEW UNDER THE THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde- Wolf and Chris Lane (IMF) Marcelo

STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

July 25, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Catherine Pattillo (IMF) and John Panzer (IDA) Prepared by the staffs of the

July 25, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Catherine Pattillo (IMF) and John Panzer (IDA) Prepared by the staffs of the

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA. Joint Bank-Fund Debt Sustainability Analysis - Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis - Update Prepared by the Staff

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis - Update Prepared by the Staff

Joint Bank-Fund Debt Sustainability Analysis Update

INTERNATIONAL DEVELOPMENT ASSOCIATION Public Disclosure Authorized INTERNATIONAL MONETARY FUND DOMINICA Joint Bank-Fund Debt Sustainability Analysis -218 Update Prepared by the staffs of the International

INTERNATIONAL DEVELOPMENT ASSOCIATION Public Disclosure Authorized INTERNATIONAL MONETARY FUND DOMINICA Joint Bank-Fund Debt Sustainability Analysis -218 Update Prepared by the staffs of the International

STAFF REPORT OF THE 2015 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE. Risk of external debt distress

April 7, 215 STAFF REPORT OF THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Paul Cashin and Mark Flanagan (IMF) Satu Kahkonen (IDA) Risk of external debt distress Prepared

April 7, 215 STAFF REPORT OF THE 215 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Paul Cashin and Mark Flanagan (IMF) Satu Kahkonen (IDA) Risk of external debt distress Prepared

SIERRA LEONE. Approved By. June 16, 2016

SIERRA LEONE June 16, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION AND FIFTH REVIEW UNDER THE EXTENDED CREDIT FACILITY AND FINANCING ASSURANCES REVIEW AND REQUEST FOR AN EXTENSION OF THE EXTENDED

SIERRA LEONE June 16, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION AND FIFTH REVIEW UNDER THE EXTENDED CREDIT FACILITY AND FINANCING ASSURANCES REVIEW AND REQUEST FOR AN EXTENSION OF THE EXTENDED

STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1

June 8, 2016 STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Paul Cashin and Andrea Richter Hume (IMF) and Satu Kahkonen (IDA) Prepared by International Monetary

June 8, 2016 STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Paul Cashin and Andrea Richter Hume (IMF) and Satu Kahkonen (IDA) Prepared by International Monetary

REPUBLIC OF THE MARSHALL ISLANDS

REPUBLIC OF THE MARSHALL ISLANDS December 19, 213 STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Stephan Danninger, Ranil Salgado, Jeffrey D. Lewis and Sudhir

REPUBLIC OF THE MARSHALL ISLANDS December 19, 213 STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Stephan Danninger, Ranil Salgado, Jeffrey D. Lewis and Sudhir

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND MALI. Joint Bank-Fund Debt Sustainability Analysis Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND MALI Public Disclosure Authorized Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND MALI Public Disclosure Authorized Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION REPUBLIC OF MODOVA

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION REPUBLIC OF MODOVA Joint IMF/World Bank Debt Sustainability Analysis Under the Debt Sustainability Framework for Low-Income Countries

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION REPUBLIC OF MODOVA Joint IMF/World Bank Debt Sustainability Analysis Under the Debt Sustainability Framework for Low-Income Countries

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LAO PEOPLE S DEMOCRATIC REPUBLIC

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LAO PEOPLE S DEMOCRATIC REPUBLIC Joint Bank/Fund Debt Sustainability Analysis 28 1 Prepared by the staffs of the International Development

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LAO PEOPLE S DEMOCRATIC REPUBLIC Joint Bank/Fund Debt Sustainability Analysis 28 1 Prepared by the staffs of the International Development

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SIERRA LEONE. Joint IMF/World Bank Debt Sustainability Analysis 2010

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SIERRA LEONE Joint IMF/World Bank Debt Sustainability Analysis 21 Prepared by the staffs of the International Monetary Fund and the

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SIERRA LEONE Joint IMF/World Bank Debt Sustainability Analysis 21 Prepared by the staffs of the International Monetary Fund and the

DEMOCRATIC REPUBLIC OF TIMOR-LESTE

DEMOCRATIC REPUBLIC OF TIMOR-LESTE January 13, 212 STAFF REPORT FOR THE 211 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Ray Brooks and Dhaneshwar Ghura (IMF) Prepared By 1 International

DEMOCRATIC REPUBLIC OF TIMOR-LESTE January 13, 212 STAFF REPORT FOR THE 211 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Ray Brooks and Dhaneshwar Ghura (IMF) Prepared By 1 International

January 2008 NIGER: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

January 28 NIGER: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS Niger remains at moderate risk of debt distress. Despite low debt ratios following debt relief, most recently in 26 under the MDRI, Niger

January 28 NIGER: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS Niger remains at moderate risk of debt distress. Despite low debt ratios following debt relief, most recently in 26 under the MDRI, Niger

REQUEST FOR A THREE-YEAR POLICY SUPPORT

SENEGAL June 9, 15 REQUEST FOR A THREE-YEAR POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum (IMF), and John Panzer (IDA) Prepared by the staffs of the

SENEGAL June 9, 15 REQUEST FOR A THREE-YEAR POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum (IMF), and John Panzer (IDA) Prepared by the staffs of the

Uganda: Joint Bank-Fund Debt Sustainability Analysis

February 26 Uganda: Joint Bank-Fund Debt Sustainability Analysis 1. Uganda s risk of debt distress is moderate. Its net present value (NPV) of debt-toexports ratio stands at 179 percent in 24/5, or below

February 26 Uganda: Joint Bank-Fund Debt Sustainability Analysis 1. Uganda s risk of debt distress is moderate. Its net present value (NPV) of debt-toexports ratio stands at 179 percent in 24/5, or below

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND UGANDA. Joint World Bank/IMF Debt Sustainability Analysis Update

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND UGANDA Joint World Bank/IMF Debt Sustainability Analysis Update Prepared by staffs of the International Development Association and

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND UGANDA Joint World Bank/IMF Debt Sustainability Analysis Update Prepared by staffs of the International Development Association and

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERANTIONAL MONETARY FUND BURKINA FASO. Joint Bank-Fund Debt Sustainability Analysis 2013 Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERANTIONAL MONETARY FUND BURKINA FASO Joint Bank-Fund Debt Sustainability Analysis 213 Update Public Disclosure Authorized Prepared

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERANTIONAL MONETARY FUND BURKINA FASO Joint Bank-Fund Debt Sustainability Analysis 213 Update Public Disclosure Authorized Prepared

Vietnam: Joint Bank-Fund Debt Sustainability Analysis 1

1 November 2006 Vietnam: Joint Bank-Fund Debt Sustainability Analysis 1 Public sector debt sustainability Since the time of the last joint DSA, the most important new signal on the likely direction of

1 November 2006 Vietnam: Joint Bank-Fund Debt Sustainability Analysis 1 Public sector debt sustainability Since the time of the last joint DSA, the most important new signal on the likely direction of

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LIBERIA

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LIBERIA Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis 1 Update 1 Prepared by the

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LIBERIA Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis 1 Update 1 Prepared by the

Risk of external debt distress: Augmented by significant risks stemming from domestic public debt?

July 5, 217 SEVENTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUEST FOR EXTENSION AND AUGMENTATION OF ACCESS DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum

July 5, 217 SEVENTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUEST FOR EXTENSION AND AUGMENTATION OF ACCESS DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum

TOGO. Joint Bank-Fund Debt Sustainability Analysis Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND TOGO Public Disclosure Authorized Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND TOGO Public Disclosure Authorized Public Disclosure Authorized Joint Bank-Fund Debt Sustainability Analysis

CÔTE D'IVOIRE ANALYSIS UPDATE. June 2, Prepared by the International Monetary Fund and the International Development Association

CÔTE D'IVOIRE June 2, 217 FIRST REVIEWS UNDER EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUESTS FOR MODIFICATION OF PERFORMANCE CRITERIA

CÔTE D'IVOIRE June 2, 217 FIRST REVIEWS UNDER EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUESTS FOR MODIFICATION OF PERFORMANCE CRITERIA

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION

November 21, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION AND FOURTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND FINANCING ASSURANCES REVIEW DEBT SUSTAINABILITY ANALYSIS Approved

November 21, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION AND FOURTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND FINANCING ASSURANCES REVIEW DEBT SUSTAINABILITY ANALYSIS Approved

Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2

September 26 Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2 Cape Verde s debt level has increased in recent years. Despite the rising cost of servicing this debt, the country s external sustainability

September 26 Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2 Cape Verde s debt level has increased in recent years. Despite the rising cost of servicing this debt, the country s external sustainability

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATION MONETARY FUND SOLOMON ISLANDS. Joint World bank-fund Debt Sustainability Analysis 2013 Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATION MONETARY FUND SOLOMON ISLANDS Public Disclosure Authorized Joint World bank-fund Debt Sustainability Analysis 213 Update Prepared

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATION MONETARY FUND SOLOMON ISLANDS Public Disclosure Authorized Joint World bank-fund Debt Sustainability Analysis 213 Update Prepared

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA. Joint IMF/World Bank Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA Joint IMF/World Bank Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA Joint IMF/World Bank Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

STAFF REPORT FOR THE 2018 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

May 1, 218 BANGLADESH STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Kenneth Kang and Kevin Fletcher (IMF) and John Panzer (IDA) Prepared by International Monetary

May 1, 218 BANGLADESH STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Kenneth Kang and Kevin Fletcher (IMF) and John Panzer (IDA) Prepared by International Monetary

Nepal: Joint Bank-Fund Debt Sustainability Analysis

February 26 Nepal: Joint Bank-Fund Debt Sustainability Analysis Public debt dynamics are assessed using the Low Income Country Debt Sustainability Analysis (LIC-DSA) framework. The DSA was conducted jointly

February 26 Nepal: Joint Bank-Fund Debt Sustainability Analysis Public debt dynamics are assessed using the Low Income Country Debt Sustainability Analysis (LIC-DSA) framework. The DSA was conducted jointly

Nicaragua: Joint Bank-Fund Debt Sustainability Analysis 1,2

May 2006 Nicaragua: Joint Bank-Fund Debt Sustainability Analysis 1,2 While Nicaragua s debt burden has been substantially reduced thanks to the HIPC initiative, debt levels remain elevated and subject

May 2006 Nicaragua: Joint Bank-Fund Debt Sustainability Analysis 1,2 While Nicaragua s debt burden has been substantially reduced thanks to the HIPC initiative, debt levels remain elevated and subject

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND SENEGAL. Joint Bank/Fund Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND SENEGAL Joint Bank/Fund Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and the International

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND SENEGAL Joint Bank/Fund Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and the International

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND THE GAMBIA. Joint Bank-Fund Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND THE GAMBIA Joint Bank-Fund Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and the International

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND THE GAMBIA Joint Bank-Fund Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and the International

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

May 9, 17 STAFF REPORT FOR THE 17 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Jorge Roldos and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA) Prepared by the staff of the International

May 9, 17 STAFF REPORT FOR THE 17 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Jorge Roldos and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA) Prepared by the staff of the International

LAO PEOPLE'S DEMOCRATIC REPUBLIC

LAO PEOPLE'S DEMOCRATIC REPUBLIC August 16, 212 STAFF REPORT FOR THE 212 ARTICLE IV CONSULTATION DEBT SUSTAINABILITYANALYSIS 1 Approved By David Cowen and Masato Miyazaki (IMF) Andrew D. Mason and Jeffrey

LAO PEOPLE'S DEMOCRATIC REPUBLIC August 16, 212 STAFF REPORT FOR THE 212 ARTICLE IV CONSULTATION DEBT SUSTAINABILITYANALYSIS 1 Approved By David Cowen and Masato Miyazaki (IMF) Andrew D. Mason and Jeffrey

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND ISLAMIC REPUBLIC OF MAURITANIA

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND ISLAMIC REPUBLIC

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND ISLAMIC REPUBLIC

Joint Bank-Fund Debt Sustainability Analysis 2018 Update 1

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND DEMOCRATIC REPUBLIC OF SÃO TOMÉ AND PRÍNCIPE Public Disclosure Authorized Public Disclosure Authorized Public

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND DEMOCRATIC REPUBLIC OF SÃO TOMÉ AND PRÍNCIPE Public Disclosure Authorized Public Disclosure Authorized Public

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND MALAWI. Joint Bank Fund Debt Sustainability Analysis Update

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND MALAWI Joint Bank

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND MALAWI Joint Bank

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL. Joint IMF/IDA Debt Sustainability Analysis

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL Joint IMF/IDA Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL Joint IMF/IDA Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1

1 December 26 Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1 1. Malawi s risk of debt distress after debt relief under the HIPC Initiative and the Multilateral

1 December 26 Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1 1. Malawi s risk of debt distress after debt relief under the HIPC Initiative and the Multilateral

STAFF REPORT FOR THE 2014 ARTICLE IV CONSULTATION AND SECOND REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS

November 19, 214 RWANDA STAFF REPORT FOR THE 214 ARTICLE IV CONSULTATION AND SECOND REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Dan Ghura (IMF) and

November 19, 214 RWANDA STAFF REPORT FOR THE 214 ARTICLE IV CONSULTATION AND SECOND REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Dan Ghura (IMF) and

Joint Bank-Fund Debt Sustainability Analysis 2018 Update

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND GRENADA Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND GRENADA Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association

ISLAMIC REPUBLIC OF AFGHANISTAN

November, STAFF REPORT FOR THE ARTICLE IV CONSULTATION AND FIRST REVIEW UNDER THE STAFF-MONITORED PROGRAM DEBT SUSTAINABILITY ANALYSIS Approved By Adnan Mazarei and Dhaneshwar Ghura (IMF), and Satu Kahkonen

November, STAFF REPORT FOR THE ARTICLE IV CONSULTATION AND FIRST REVIEW UNDER THE STAFF-MONITORED PROGRAM DEBT SUSTAINABILITY ANALYSIS Approved By Adnan Mazarei and Dhaneshwar Ghura (IMF), and Satu Kahkonen

FEDERATED STATES OF MICRONESIA

FEDERATED STATES OF MICRONESIA August 4, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Alison Stuart and Zuzana Murgasova (IMF), and John Panzer (IDA) Prepared

FEDERATED STATES OF MICRONESIA August 4, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Alison Stuart and Zuzana Murgasova (IMF), and John Panzer (IDA) Prepared

Georgia: Joint Bank-Fund Debt Sustainability Analysis 1

November 6 Georgia: Joint Bank-Fund Debt Sustainability Analysis 1 Background 1. Over the last decade, Georgia s external public and publicly guaranteed (PPG) debt burden has fallen from more than 8 percent

November 6 Georgia: Joint Bank-Fund Debt Sustainability Analysis 1 Background 1. Over the last decade, Georgia s external public and publicly guaranteed (PPG) debt burden has fallen from more than 8 percent

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

December 19, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Odd Per Brekk (IMF) and John Panzer (IDA) Prepared by the staff of the International Monetary

December 19, 217 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Odd Per Brekk (IMF) and John Panzer (IDA) Prepared by the staff of the International Monetary

March 2007 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

March 27 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS The staff s debt sustainability analysis (DSA) suggests that the Kyrgyz Republic s external debt continues to pose a heavy burden,

March 27 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS The staff s debt sustainability analysis (DSA) suggests that the Kyrgyz Republic s external debt continues to pose a heavy burden,

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND SUDAN. Joint World Bank/IMF 2009 Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND SUDAN Joint World Bank/IMF 29 Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND SUDAN Joint World Bank/IMF 29 Debt Sustainability Analysis Prepared by the Staffs of the International Development Association and

LIBERIA. Approved By. December 3, December 7, Prepared by the International Monetary Fund and International Development Association

December 3, 15 December 7, 15 FOURTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT AND REQUESTS FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA, MODIFICATION OF PERFORMANCE CRITERIA, AND REPHASING

December 3, 15 December 7, 15 FOURTH REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT AND REQUESTS FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA, MODIFICATION OF PERFORMANCE CRITERIA, AND REPHASING

STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

February 7, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Vitaliy Kramarenko (IMF) and Paloma Anós Casero (IDA) Prepared by the staffs

February 7, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Vitaliy Kramarenko (IMF) and Paloma Anós Casero (IDA) Prepared by the staffs

STAFF REPORT FOR THE 2018 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS. Risk of external debt distress:

May 24, 218 STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Risk of external debt distress: Augmented by significant risks stemming from domestic public and/or private external

May 24, 218 STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Risk of external debt distress: Augmented by significant risks stemming from domestic public and/or private external

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

May 12, 217 BANGLADESH STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Peter Allum (IMF) and John Panzer (IDA) Prepared by International Monetary Fund International

May 12, 217 BANGLADESH STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Peter Allum (IMF) and John Panzer (IDA) Prepared by International Monetary Fund International

DOCUMENT OF INTERNATIONAL MONETARY FUND AND FOR OFFICIAL USE ONLY. SM/07/347 Supplement 2

DOCUMENT OF INTERNATIONAL MONETARY FUND AND FOR OFFICIAL USE ONLY FOR AGENDA SM/7/347 Supplement 2 November 5, 27 To: From: Subject: Members of the Executive Board The Secretary Myanmar Staff Report for

DOCUMENT OF INTERNATIONAL MONETARY FUND AND FOR OFFICIAL USE ONLY FOR AGENDA SM/7/347 Supplement 2 November 5, 27 To: From: Subject: Members of the Executive Board The Secretary Myanmar Staff Report for

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA. Joint IMF/World Bank Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA Joint IMF/World Bank Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the World Bank Approved

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND KENYA Joint IMF/World Bank Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the World Bank Approved

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BURUNDI. Joint Bank/Fund Debt Sustainability Analysis 2010

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BURUNDI Joint Bank/Fund

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND BURUNDI Joint Bank/Fund

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION DEMOCRATIC REPUBLIC OF CONGO

71 INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION DEMOCRATIC REPUBLIC OF CONGO Joint IMF/World Bank Debt Sustainability Analysis 29 Prepared by the Staffs of the International Monetary

71 INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION DEMOCRATIC REPUBLIC OF CONGO Joint IMF/World Bank Debt Sustainability Analysis 29 Prepared by the Staffs of the International Monetary

Joint Bank-Fund Debt Sustainability Analysis 2018 Update

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CHAD Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CHAD Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association

LAO PEOPLE'S DEMOCRATIC REPUBLIC

December 15, 2014 LAO PEOPLE'S DEMOCRATIC REPUBLIC STAFF REPORT FOR THE 2014 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Markus Rodlauer and Chris Lane (IMF) Satu Kahkonen (World

December 15, 2014 LAO PEOPLE'S DEMOCRATIC REPUBLIC STAFF REPORT FOR THE 2014 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Markus Rodlauer and Chris Lane (IMF) Satu Kahkonen (World

INTERNATIONAL MONETARY FUND SOLOMON ISLANDS. Joint IMF/World Bank Debt Sustainability Analysis 1

INTERNATIONAL MONETARY FUND SOLOMON ISLANDS Joint IMF/World Bank Debt Sustainability Analysis 1 Prepared by Staffs of the International Monetary Fund and World Bank Approved by Hoe Ee Khor and Masato Miyazaki

INTERNATIONAL MONETARY FUND SOLOMON ISLANDS Joint IMF/World Bank Debt Sustainability Analysis 1 Prepared by Staffs of the International Monetary Fund and World Bank Approved by Hoe Ee Khor and Masato Miyazaki

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND UNION OF THE COMOROS. Joint IMF/World Bank Debt Sustainability Analysis 2009

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND UNION OF THE COMOROS Joint IMF/World Bank Debt Sustainability Analysis 29 Prepared by the staffs of the International Development Association

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND UNION OF THE COMOROS Joint IMF/World Bank Debt Sustainability Analysis 29 Prepared by the staffs of the International Development Association

INTERNATIONAL MONETARY FUND DOMINICA. Debt Sustainability Analysis. Prepared by the staff of the International Monetary Fund

INTERNATIONAL MONETARY FUND DOMINICA Debt Sustainability Analysis Prepared by the staff of the International Monetary Fund In consultation with World Bank Staff July 2, 27 This debt sustainability analysis

INTERNATIONAL MONETARY FUND DOMINICA Debt Sustainability Analysis Prepared by the staff of the International Monetary Fund In consultation with World Bank Staff July 2, 27 This debt sustainability analysis

Burkina Faso: Joint Bank-Fund Debt Sustainability Analysis

September 2005 Burkina Faso: Joint Bank-Fund Debt Sustainability Analysis 1. This document assesses the sustainability of Burkina Faso s external public debt using the Debt Sustainability Analysis (DSA)

September 2005 Burkina Faso: Joint Bank-Fund Debt Sustainability Analysis 1. This document assesses the sustainability of Burkina Faso s external public debt using the Debt Sustainability Analysis (DSA)

The Gambia: Joint Bank-Fund Debt Sustainability Analysis

1 December 26 The Gambia: Joint Bank-Fund Debt Sustainability Analysis 1. This debt sustainability analysis (DSA), prepared jointly by the staffs of the International Monetary Fund and the World Bank,

1 December 26 The Gambia: Joint Bank-Fund Debt Sustainability Analysis 1. This debt sustainability analysis (DSA), prepared jointly by the staffs of the International Monetary Fund and the World Bank,

REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS

March 24, 217 REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Dominique Desruelle and Peter Allum (IMF) and Paloma Anos-Casero (IDA) Prepared

March 24, 217 REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Dominique Desruelle and Peter Allum (IMF) and Paloma Anos-Casero (IDA) Prepared

CAMEROON. Approved By. Prepared by the staffs of the International Monetary Fund and the International Development Association.

June 22, 218 STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION, SECOND REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUESTS FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA AND MODIFICATION

June 22, 218 STAFF REPORT FOR THE 218 ARTICLE IV CONSULTATION, SECOND REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUESTS FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA AND MODIFICATION

INTERNATIONAL MONETARY FUND THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA. Joint IMF/World Bank Debt Sustainability Analysis 2010

49 INTERNATIONAL MONETARY FUND THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA Joint IMF/World Bank Debt Sustainability Analysis 21 Prepared by the staffs of the International Monetary Fund and the International

49 INTERNATIONAL MONETARY FUND THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA Joint IMF/World Bank Debt Sustainability Analysis 21 Prepared by the staffs of the International Monetary Fund and the International

REQUEST FOR DISBURSEMENT UNDER THE RAPID CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS

July 17, 215 NEPAL REQUEST FOR DISBURSEMENT UNDER THE RAPID CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Kalpana Kochhar and Ranil Salgado (IMF) and Satu Kahkonen (IDA) Prepared by the staffs

July 17, 215 NEPAL REQUEST FOR DISBURSEMENT UNDER THE RAPID CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Kalpana Kochhar and Ranil Salgado (IMF) and Satu Kahkonen (IDA) Prepared by the staffs

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CHAD

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CHAD Joint Fund-Bank Debt Sustainability Analysis under the Debt Sustainability Framework for Low-Income Countries Prepared by the staffs

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CHAD Joint Fund-Bank Debt Sustainability Analysis under the Debt Sustainability Framework for Low-Income Countries Prepared by the staffs

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA. Joint World Bank/IMF Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA Joint World Bank/IMF Debt Sustainability Analysis Prepared by staffs of the International Development Association and International

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND RWANDA Joint World Bank/IMF Debt Sustainability Analysis Prepared by staffs of the International Development Association and International

Joint Bank-Fund Debt Sustainability Analysis 2018 Update

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CAMEROON Joint Bank-Fund Debt Sustainability Analysis 218 Update Public Disclosure Authorized Public Disclosure

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND CAMEROON Joint Bank-Fund Debt Sustainability Analysis 218 Update Public Disclosure Authorized Public Disclosure

REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS

June 16, 217 REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde-Wolf and Bob Traa (IMF); and Paloma Anos-Casero (IDA) The

June 16, 217 REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde-Wolf and Bob Traa (IMF); and Paloma Anos-Casero (IDA) The

MALAWI. Approved By. December 27, Prepared by the staffs of the International Monetary Fund and the International Development Association

December 27, 213 MALAWI THIRD AND FOURTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUESTS FOR WAIVER OF PERFORMANCE CRITERIA, EXTENSION OF THE ARRANGEMENT, REPHASING OF DISBURSEMENTS, AND

December 27, 213 MALAWI THIRD AND FOURTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUESTS FOR WAIVER OF PERFORMANCE CRITERIA, EXTENSION OF THE ARRANGEMENT, REPHASING OF DISBURSEMENTS, AND

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION MALDIVES

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION MALDIVES Joint IMF/World Bank Debt Sustainability Analysis under the Debt Sustainability Framework for Low Income Countries 1 Prepared

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION MALDIVES Joint IMF/World Bank Debt Sustainability Analysis under the Debt Sustainability Framework for Low Income Countries 1 Prepared

TONGA JOINT IMF/WORLD BANK DEBT SUSTAINABILITY ANALYSIS Approved By. July 2, 2013

July 2, 213 JOINT IMF/WORLD BANK DEBT SUSTAINABILITY ANALYSIS 213 Approved By (IMF) Luis Breuer (IDA) Sudhir Shetty; Jeffrey D. Lewis Prepared By The International Monetary Fund and The International Development

July 2, 213 JOINT IMF/WORLD BANK DEBT SUSTAINABILITY ANALYSIS 213 Approved By (IMF) Luis Breuer (IDA) Sudhir Shetty; Jeffrey D. Lewis Prepared By The International Monetary Fund and The International Development

CÔTE D'IVOIRE. Approved By. November 23, Prepared by the International Monetary Fund and the International Development Association

CÔTE D'IVOIRE November 23, 216 REQUESTS FOR AN EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Roger

CÔTE D'IVOIRE November 23, 216 REQUESTS FOR AN EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Roger

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND GHANA. Joint IMF and World Bank Debt Sustainability Analysis

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND GHANA Joint IMF and World Bank Debt Sustainability Analysis Prepared by the staffs of the World Bank and the International Monetary Fund

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND GHANA Joint IMF and World Bank Debt Sustainability Analysis Prepared by the staffs of the World Bank and the International Monetary Fund

LAO PEOPLE'S DEMOCRATIC REPUBLIC

LAO PEOPLE'S DEMOCRATIC REPUBLIC January 6, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Markus Rodlauer (IMF) John Panzer (IDA) Prepared By International

LAO PEOPLE'S DEMOCRATIC REPUBLIC January 6, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS 1 Approved By Markus Rodlauer (IMF) John Panzer (IDA) Prepared By International

CÔTE D'IVOIRE. Approved by Dominique Desruelle and Daria Zakharova (IMF); and Paloma Anos-Casero (IDA) November 21, 2017

; and Paloma Anos-Casero (IDA) November 21, 2017") CÔTE D'IVOIRE November 21, 217 SECOND REVIEWS UNDER AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY AND THE EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY DEBT SUSTAINABILITY ANALYSIS Approved

CÔTE D'IVOIRE November 21, 217 SECOND REVIEWS UNDER AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY AND THE EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY DEBT SUSTAINABILITY ANALYSIS Approved

Approved By. November 13, Prepared by the Staffs of the International Monetary Fund and the World Bank.

November 13, 215 NIGER SIXTH AND SEVENTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUEST FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA, REQUEST FOR AUGMENTATION OF ACCESS, AND EXTENSION

November 13, 215 NIGER SIXTH AND SEVENTH REVIEWS UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, REQUEST FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRITERIA, REQUEST FOR AUGMENTATION OF ACCESS, AND EXTENSION

May 2006 SIERRA LEONE: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

May 2006 SIERRA LEONE: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS This document assesses the sustainability of Sierra Leone s external and domestic public debt. The debt sustainability analysis (DSA)

May 2006 SIERRA LEONE: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS This document assesses the sustainability of Sierra Leone s external and domestic public debt. The debt sustainability analysis (DSA)

REPUBLIC OF MADAGASCAR

June 14, 217 REPUBLIC OF MADAGASCAR STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION, FIRST REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUESTS FOR WAIVER OF NONOBSERVANCE OF PERFORMANCE

June 14, 217 REPUBLIC OF MADAGASCAR STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION, FIRST REVIEW UNDER THE EXTENDED CREDIT FACILITY ARRANGEMENT, AND REQUESTS FOR WAIVER OF NONOBSERVANCE OF PERFORMANCE

International Monetary Fund Washington, D.C.

2006 International Monetary Fund December 2006 IMF Country Report No. 06/442 Honduras: Debt Sustainability Analysis 2006 This Debt Sustainability Analysis paper for Honduras was prepared jointly by a staff

2006 International Monetary Fund December 2006 IMF Country Report No. 06/442 Honduras: Debt Sustainability Analysis 2006 This Debt Sustainability Analysis paper for Honduras was prepared jointly by a staff

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND HAITI. Joint Bank-Fund Debt Sustainability Analysis 2012

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND HAITI Joint Bank-Fund Debt Sustainability Analysis 212 Prepared by the Staffs of the and the International Development Association

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND HAITI Joint Bank-Fund Debt Sustainability Analysis 212 Prepared by the Staffs of the and the International Development Association