Session 2. The IMF's macroeconomic framework

|

|

|

- Tyler Goodwin

- 5 years ago

- Views:

Transcription

1 Session 2. The IMF's macroeconomic framework 1. Overview of the Macro Framework

2 Some takeaways Linkages between sectors and policies are critical Financial programming (FP) is a tool for ensuring accounting and economic consistency in economic analysis and projections FP can help diagnose economic imbalances (domestic or external) and policy fixes FP is also basis for IMF-supported financial programs FP is not itself an economic model, but can be made consistent with any model and behavioral assumptions Who might need FP? Macroeconomic linkages

3 Main Macroeconomic Sectors Real sector: GDP

4 Fiscal policy: Simplified accounts GFSM 1986* GFSM 2001/14* REVENUE EXPENDITURE Current Primary Interest payments Capital NET LENDING (POLICY LOANS) OVERALL BALANCE FINANCING External Domestic Privatization REVENUE EXPENSE Primary Interest payments NET/GROSS OPERATING BALANCE NET ACQUISITION OF NON-FIN. ASSETS EXPENDITURE NET LENDING/BORROWING NET ACQ. OF FIN. ASSETS NET INCURRENCE OF LIABILITIES Fiscal balance Why overall balance? Reflects borrowing needs of government how broad a definition of government? Change in overall balance a proxy for impact of fiscal policy on aggregate demand Key determinant of debt sustainability Other important indicators of fiscal health Cyclically adjusted balance How financed? Key to analyzing potential risks, impact on inflation

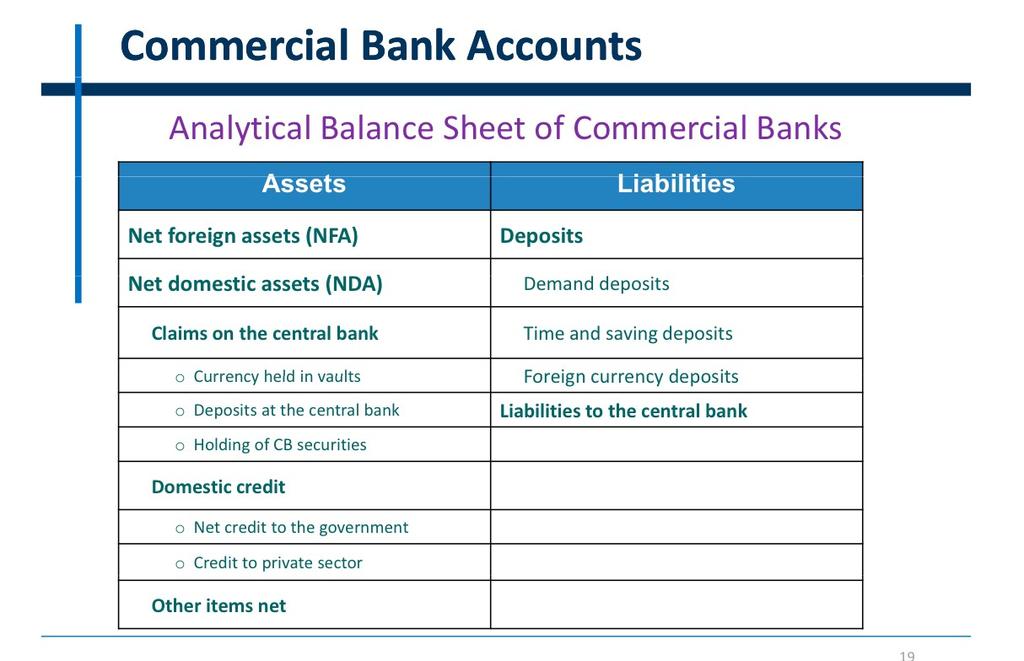

5 Scope of the monetary sector

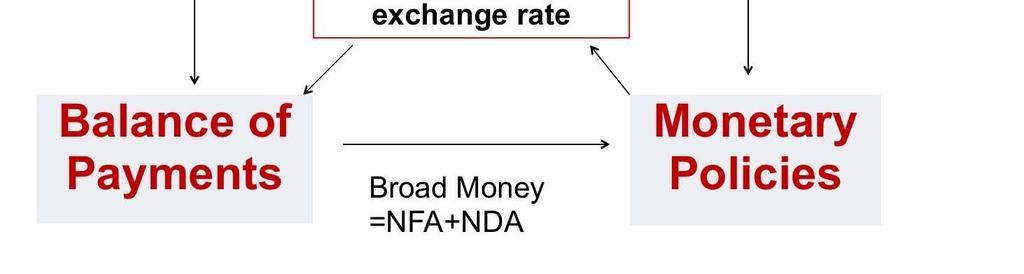

Narrow money (NM) Currency in circulation (CY) Demand deposits (DD) Quasi money (QM) Time & savings deposits (TD) Foreign currency deposits (FC) M = NFA + NDA The external sector: Balance")

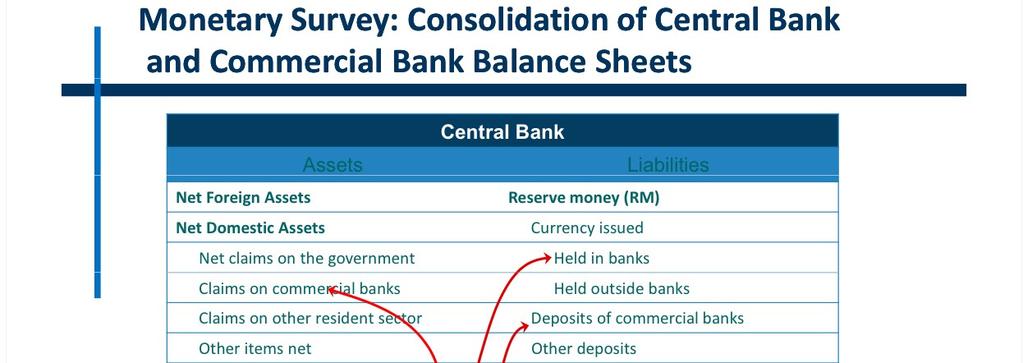

6 Monetary survey: the banking system ASSETS Net Foreign assets (NFA) Net Domestic assets (NDA) Net credit to government (NCG) Credit to private sector (CPS) Other Items, net (OIN) LIABILITIES Broad Money (M) Narrow money (NM) Currency in circulation (CY) Demand deposits (DD) Quasi money (QM) Time & savings deposits (TD) Foreign currency deposits (FC) M = NFA + NDA The external sector: Balance of payments Current account deficit (surplus) means country spends more (less) on goods of other countries than it receives Records transactions with non-residents Current account deficit needs to be financed, which implies capital inflow Positive (negative) CA means country net lender (borrower) to RoW CA = S-I If normal flows don't cover deficit, need to finance by drawing down reserves or via official (IMF) financing Links with macro policies twin deficits

7 Balance of Payments: Details (usually in US$ or euros) Current Account (CAB) Trade Exports Imports Services Primary Income Interest Profits Wages Secondary Income, net Capital and Financial Account Capital Account Financial Account Direct Investment, net Portfolio Investment, net Equity Debt Other Investment, net in International Reserves Errors and Omissions Link with National Accounts

8 Fiscal-external links: Twin deficits? 39 Curent Account Balance (percent GDP) Data for Fiscal Balance (percent of GDP)

9 Macro-financial linkages Macro-financial linkages arise from the key role of the financial system in channeling savings to investment Macroeconomy Financial System Financial programming

10 What is a financial program? A consistent framework of macroeconomic accounts and linkages Utilized in medium-term projections, but not a formal model or forecasting tool by itself Can be consistent with any formal model. Need for behavioral content Accounting consistency: One variable per sector as residual. Also crosschecks across accounts Economic consistency: What is the story? Does it make sense? What policies are assumed? Identifying problems: Consistent story doesn t mean good story Used to design policies and set targets especially in IMF programs Three types of links Accounting identities: Entries should be exactly the same (may not be due to measurement error), e.g.: Exports and imports in real sector accounts equal exports and imports in BoP Δ Credit to government in monetary account = Domestic bank financing in fiscal account Government consumption in national accounts equal current expenditure in fiscal accounts External CA deficit = National S - I Strong accounting links: Entries closely related but not identical, e.g.: E.g. change in the exchange rate introduces gap between ΔNFA in monetary and BOP accounts Behavioral links everywhere! Does the FP make economic sense?

External (BoP) Fiscal Monetary 2.")

11 Building a baseline: Basic steps 1. Project baseline under existing policies, typically: Real (GDP) External (BoP) Fiscal Monetary 2. Check accounting consistency 3. Check economic consistency: the story 4. Iterate!

Reconcile supply and demand sides judgment needed Short-term (cyclical) vs long-term (potential) Forecast prices")

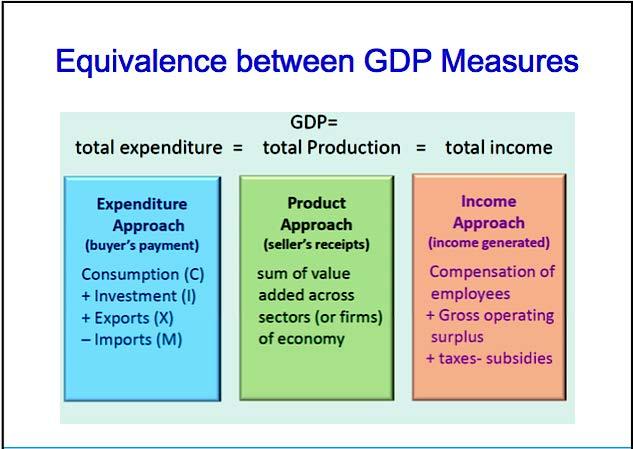

12 Forecasting national accounts Forecast real output Supply: Determinants of potential growth, Y=f(A, K,L) Demand: Expenditure side of GDP, Y=C+I+G+(X-M) Reconcile supply and demand sides judgment needed Short-term (cyclical) vs long-term (potential) Forecast prices GDP deflator Nominal forecasts Determinants of private consumption Disposable income Net worth impact of asset booms and busts Interest rates, access to credit Demographics: life-cycle behavior Impact of government and corporate savings? Social safety nets and other policies

13 Analyzing private investment Structural component. Maintenance spending less depreciation Interest rate. Higher real r means fewer profitable projects Accelerator effects. Faster growth means higher investment maintain capital-output ratio; growth lowers risk premia Corporate balance sheets. Stronger balance sheets mean more collateral, easier self-financing Tobin s Q. Cash flow/liquidity. Access to credit Animal spirits expected future demand Taxation/subsidies Forecasting the external sector Forecast imports and exports: Key variables include income (own and partners), exchange rates, terms of trade Net interest payments depend on external debt outstanding, new debt, interest rates, risk premia Official transfers based on past trends, discussions with country and donors. Private transfers ( remittances) based on history, plausible assumptions Capital account most difficult track record, country plans, global environment, country risk Reserves are either a residual or target, in program context

MV= PQ Money supply: M2 = NFA + NDA NFA comes from BoP Stable?")

14 Forecasting the fiscal sector Revenue based on real economy, inflation, measures: Changes in tax base, effective rates Non-interest spending: Mandated (e.g. pensions) vs. discretionary Interest payments: Depends on debt level and stricture, interest rates, and exchange rate Estimation iterative, since depends on new debt, which is function of primary deficit Financing: External financing from BoP. Domestic financing as a residual and/or plausible assumptions (as a start) Discussions with government officials are critical. Forecasting the monetary sector Demand for money: Forecast money demand equation or velocity: Md/P = f (Y, i) MV= PQ Money supply: M2 = NFA + NDA NFA comes from BoP Stable? Government credit from fiscal accounts (or vice versa) NDA - Credit to government = Credit to private sector Reconcile money demand and supply: May need to look again at other sectors e.g. inflation. Projecting reserve money: The money multiplier

15 Assessing the baseline forecast Do accounting identities hold? Does the story make sense? Top-down vs. bottom-up approaches Macro imbalances or vulnerabilities? Policy goals met? Is monetary expansion too rapid? Is the fiscal stance sustainable? Is CA deficit too large? Is investment sufficient? Are results sensitive to changes in key assumptions? What sorts of policy changes may be required? Revise, as necessary! Checks on economic consistency: Examples Time series. Many variables follow trends, e.g. national savings. If not the case in FP, is there a reason? Monetary. Is rate of money growth consistent with inflation and growth projections? Is projected credit growth consistent with GDP growth? Fiscal. Is the deficit consistent with projected interest rate and private investment (crowding out) External. Are inflows consistent with monetary policy or global outlook? Are trade projections consistent with key projected global prices? Sustainability. Are developments in fiscal and external sectors consistent with sustainability?

16 Don't assume away the problem! From baseline to program

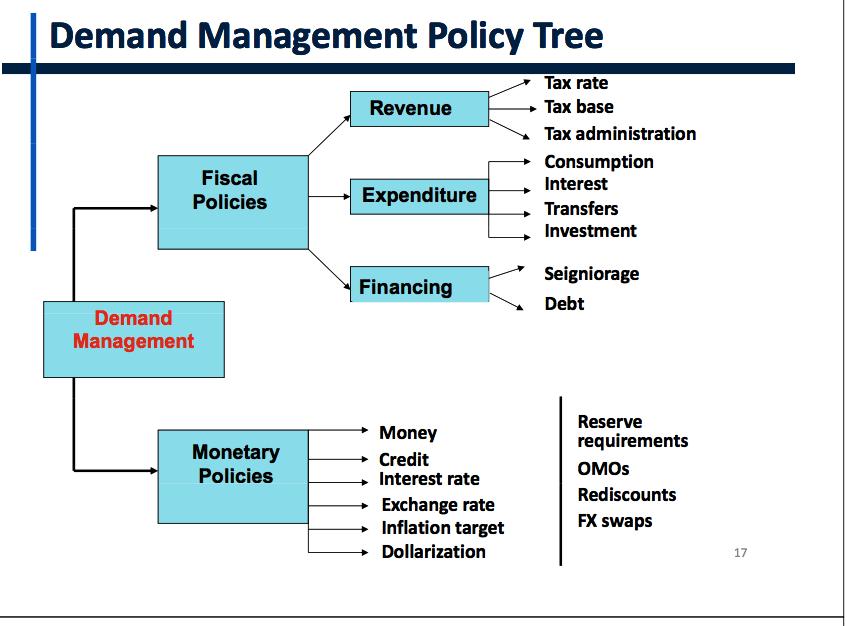

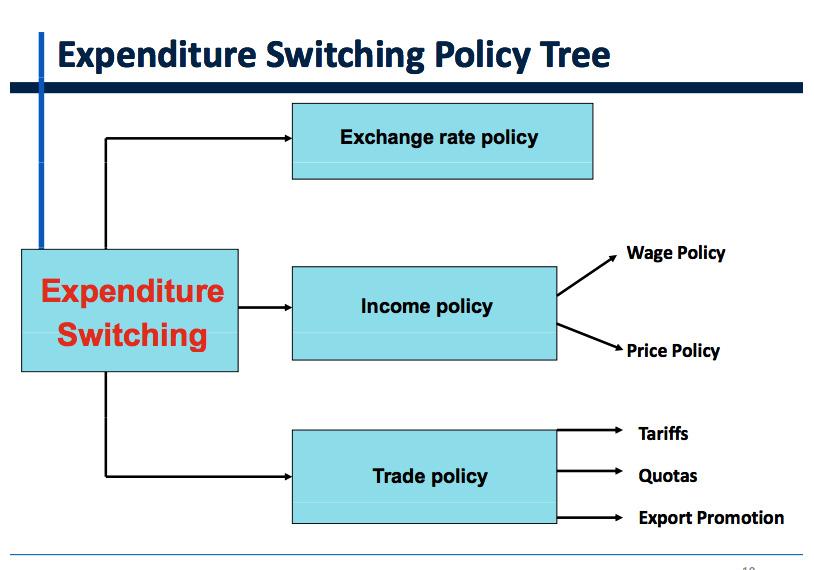

17 From baseline to policies Baseline projections are based on no policy changes Baseline may be internally consistent but still fail to achieve growth objectives or may reveal imbalances, e.g. high inflation, unsustainable debt, too large CA deficits, balance sheet risks Policies should be designed to address these imbalances What sources of imbalance? E.g. excessive government spending, overvalued exchange rate, rapid monetary expansion, large corporate borrowing? Seriousness of imbalances? Do they need to be addressed immediately, gradually? Re-do financial programming exercise with new policies iterative process What kinds of policies? Fiscal/external imbalances typically require some adjustment demand management External imbalances can also be addressed via changes in exchange rate, income, or trade policies expenditure switching Raising potential growth and limiting financial risks require structural reforms. Focus will vary across countries.

18

19 Setting program targets

20 Setting monetary targets Monetary: M = NDA + NFA = DC + R Programs often use ceiling on domestic credit to control M growth and meet inflation target. In that case, R can be residual. But building reserves is, in many cases, a policy goal. So, often, a floor is set on R and DC is a policy variable. How large do reserves need to be? Correct approach depends stability of money demand and on exchange rate and capital controls regime e.g. free-floating XR doesn't require reserves. With fixed XR, reserves are residual. Setting fiscal targets Fiscal: FB DCg + Fg DC is from monetary sector and Fg from external FB is set consistent with the identity above If its judged that this FB is too tight can seek other financing, but then need to reexamine debt sustainability and/or crowding-out of private credit. Other sources of financing exist as well, e.g. nonbank purchases of bonds, or IMF budget financing.

21 Setting external targets External: M - X + ilf = Fp + Fg - R Project M, X, Fp and R target, and treat Fg as a residual. Is there a "financing gap"? If so, need new additional financing and/or adjustment to bring down CA deficit. Alternatively, Fp and X can be projected separately. Fg is then set at a sustainable level of external debt. R is set as a target, and M is a residual. Compare this M to a benchmark M projected separately, to judge realism Ensuring a fully-financed program For IMF lending, a program must be fully financed on both fiscal and BOP side and public debt must be sustainable. If this doesn t hold options include: Lower fiscal deficits/slower growth Loans and debt relief by official creditors Commitment of private creditors to roll-over debt (e.g. Vienna Initiative) Catalytic role of IMF lending Debt restructuring Gross financing need=deficit + amortization of debt Financing gap=gross financing need - Identified funding

22 Adjustment vs. financing Program design needs to make a basic decision: How much of an imbalance should be addressed by adjustment and how much by financing? Relying mainly on financing makes sense when imbalance is seen as shortterm in nature and when resources available at a reasonable cost. IMF financial support limits needed short-term adjustment but adds to future debt. So no impact on ultimate adjustment? But IMF support allows orderly and gradual adjustment, easing burden and allowing for supply-side response Also, more credible policies can lower costs of adjustment and allow return to market borrowing at lower rates Extra slides

23 Central Bank Balance Sheet Examples (1) Example (1): On the first day of its operations, the central bank decides to buy foreign currency worth Kip 100 from commercial banks: Assets CB s NFA Net Foreign Assets 1000 Foreign exchange 1000 CB s Net NDADomestic Assets Liabilities Reserve money 1000 Currency in circulation 0 Deposits of commercial banks

24 Central Bank Balance Sheet Examples (2) Note we keep the previous transaction (Example 1) as a starting point. Example (2): Next, the central bank provides credit of Kip 100 to government, which uses this credit to pay its suppliers: Assets CB s NFA 100 Foreign exchange 100 CB s NDA 1000 Net domestic credit 1000 Liabilities Reserve money Currency in circulation 1000 Deposits of commercial banks Central Bank Balance Sheet Examples (3) Example (3): The central bank engages in open market operations to reduce base money supply by selling central bank securities of Kip 100 to commercial banks: Assets CB s NFA 100 Foreign exchange 100 CB s NDA 1000 Net domestic credit 1000 NCG 100 Net Claims on commercial banks Claims 0 Liabilities 1000 Liabilities Reserve money Currency in circulation 100 Deposits of commercial banks

25

26 Monetary Survey Why Does It Matter? Rapid broad money growth can pose risks because: Indicative of rapid demand expansion that can turn inflationary. Broad money growth is often driven by rapid credit expansion, which could lead to a buildup of risks in financial sector. Large foreign liabilities, possibly arising from commercial bank borrowing abroad, can put external sustainability at risk. 51 Money Supply and the Multiplier Currency outside banks Reserves Base Money Currency outside banks Deposits Money Stock or Broad Money (M1)

.")

r =")

27 Money Multiplier The extent of endogenous money creation can be analyzed via the money multiplier, which links broad money (M2) to reserve money (RM): where C = currency in circulation, R = reserves held at CB (commercial bank deposits at CB), and D = deposits of private sector with commercial banks). The money multiplier is a function of c = currency-to-deposits ratio (behavioral variable) r = reserve-to-deposits ratio (policy variable)

L-1 Macroeconomic Framework and Linkages

L-1 Macroeconomic Framework and Linkages IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Stephan Danninger This training material is the

L-1 Macroeconomic Framework and Linkages IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Stephan Danninger This training material is the

Macroeconomic Accounts and Policies: Financial Programming and Macro Interrelationships (*)

") Macroeconomic Accounts and Policies: Financial Programming and Macro Interrelationships (*) World Bank/Poverty and Equity Summer University, Washington, DC, July 20-21, 2017 Alvaro Manoel International

Macroeconomic Accounts and Policies: Financial Programming and Macro Interrelationships (*) World Bank/Poverty and Equity Summer University, Washington, DC, July 20-21, 2017 Alvaro Manoel International

Interrelations among Macroeconomic Accounts

Interrelations among Macroeconomic Accounts INTRODUCTION Macroeconomic statistics cover either: the whole economy (example : National Accounts) or a large and well-defined part of it (example : Government

Interrelations among Macroeconomic Accounts INTRODUCTION Macroeconomic statistics cover either: the whole economy (example : National Accounts) or a large and well-defined part of it (example : Government

The Monetary and Financial Sector

The Monetary and Financial Sector Introduction What Does the Financial Sector Do? The financial sector intermediates and facilitates the resources flowing across economic sectors. The financial sector

The Monetary and Financial Sector Introduction What Does the Financial Sector Do? The financial sector intermediates and facilitates the resources flowing across economic sectors. The financial sector

Financial Programing and Policies, Part 2 Module 5

Financial Programing and Policies, Part 2 Module 5 Forecasting the Government Sector This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute

Financial Programing and Policies, Part 2 Module 5 Forecasting the Government Sector This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute

INTRODUCTION TO MONETARY ACCOUNTS

INTRODUCTION TO MONETARY ACCOUNTS Yangon October 2, 2014 Jan Gottschalk, TAOLAM This activity is supported by a grant from Japan. Overview 2 I. Introduction II. III. IV. Central Bank Accounts Commercial

INTRODUCTION TO MONETARY ACCOUNTS Yangon October 2, 2014 Jan Gottschalk, TAOLAM This activity is supported by a grant from Japan. Overview 2 I. Introduction II. III. IV. Central Bank Accounts Commercial

Objectives of the lecture

Assessing the External Position Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views expressed herein

Assessing the External Position Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views expressed herein

The New Role of Growth Financing

OMV Aktiengesellschaft The New Role of Growth Financing Conference on European Economic Integration Vienna, 15 November 2010 Wolfgang Ruttenstorfer CEO and Chairman of the Executive Board OMV Aktiengesellschaft

OMV Aktiengesellschaft The New Role of Growth Financing Conference on European Economic Integration Vienna, 15 November 2010 Wolfgang Ruttenstorfer CEO and Chairman of the Executive Board OMV Aktiengesellschaft

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL. Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL Joint Bank-Fund Debt Sustainability Analysis

Refresher on Fiscal Accounts, Analysis and Forecasting

Refresher on Fiscal Accounts, Analysis and Forecasting Workshop on Financial Programming and Policies Yangon, Myanmar February 16-27, 2015 Milan Zavadjil Consultant Contents 1. Refresher on Fiscal Accounts

Refresher on Fiscal Accounts, Analysis and Forecasting Workshop on Financial Programming and Policies Yangon, Myanmar February 16-27, 2015 Milan Zavadjil Consultant Contents 1. Refresher on Fiscal Accounts

Overview. I. Monetary Statistics II. Money Creation III. Summary. Jan Gottschalk TAOLAM

Monetary Statistics & Money Supply Overview Jan Gottschalk TAOLAM This training material is the property of the IMF Singapore Regional Training Institute (STI) and is intended for the use in STI courses.

Monetary Statistics & Money Supply Overview Jan Gottschalk TAOLAM This training material is the property of the IMF Singapore Regional Training Institute (STI) and is intended for the use in STI courses.

L-6 Assessing the External Position

L-6 Assessing the External Position IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Yoke Wang Tok This training material is the property

L-6 Assessing the External Position IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Yoke Wang Tok This training material is the property

FPPx Glossary Term Sector Definition Acronym

FPPx Glossary Term Sector Definition Acronym Absorption Real The sum of domestic expenditures on consumption and investment. A Consumer price index (CPI) Real A measure of the general level of prices based

FPPx Glossary Term Sector Definition Acronym Absorption Real The sum of domestic expenditures on consumption and investment. A Consumer price index (CPI) Real A measure of the general level of prices based

CHAPTER 1 BASIC CONCEPTS IN MONETARY PROGRAMMING 1.1 Introduction The Central Bank of Nigeria is the institution vested with the responsibility for designing monetary policy which has to be consistent

CHAPTER 1 BASIC CONCEPTS IN MONETARY PROGRAMMING 1.1 Introduction The Central Bank of Nigeria is the institution vested with the responsibility for designing monetary policy which has to be consistent

6 The Open Economy. This chapter:

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

JOINT IMF/WORLD BANK DEBT SUSTAINABILITY

ZIMBABWE JOINT IMF/WORLD BANK DEBT SUSTAINABILITY May 5, 211 ANALYSIS 1 Approved By Mark Plant and Dominique Desruelle (IMF) Marcelo Giugale and Jeffery Lewis (IDA) Prepared by The International Monetary

ZIMBABWE JOINT IMF/WORLD BANK DEBT SUSTAINABILITY May 5, 211 ANALYSIS 1 Approved By Mark Plant and Dominique Desruelle (IMF) Marcelo Giugale and Jeffery Lewis (IDA) Prepared by The International Monetary

SOUTH ASIA. Chapter 2. Recent developments

SOUTH ASIA GLOBAL ECONOMIC PROSPECTS January 2014 Chapter 2 s GDP growth rose to an estimated 4.6 percent in 2013 from 4.2 percent in 2012, but was well below its average in the past decade, reflecting

SOUTH ASIA GLOBAL ECONOMIC PROSPECTS January 2014 Chapter 2 s GDP growth rose to an estimated 4.6 percent in 2013 from 4.2 percent in 2012, but was well below its average in the past decade, reflecting

Class Notes. Chapter 5 Saving and Investment in the Open Economy Learning Objectives

1 Chapter 5 Saving and Investment in the Open Economy Learning Objectives A. Explain how the balance of payments is calculated (Sec. 5.1) B. Discuss goods market equilibrium in an open economy (Sec. 5.2)

1 Chapter 5 Saving and Investment in the Open Economy Learning Objectives A. Explain how the balance of payments is calculated (Sec. 5.1) B. Discuss goods market equilibrium in an open economy (Sec. 5.2)

FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS

December 17, 215 FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Masato Miyazaki (IMF) and John Panzer (IDA) The Debt Sustainability Analysis (DSA)

December 17, 215 FOURTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS Approved By Roger Nord and Masato Miyazaki (IMF) and John Panzer (IDA) The Debt Sustainability Analysis (DSA)

Helpful Hint Fiscal Policy and the AS-AD Model

Helpful Hint Fiscal Policy and the AS-AD Model In this Helpful Hint, we analyze the effects of a change in fiscal policy using the AS-AD model. In doing so, it is useful to consider a specific example.

Helpful Hint Fiscal Policy and the AS-AD Model In this Helpful Hint, we analyze the effects of a change in fiscal policy using the AS-AD model. In doing so, it is useful to consider a specific example.

INTERNATIONAL MONETARY FUND

INTERNATIONAL MONETARY FUND Joint Vienna Institute / Institute for Capacity Development Course on Fiscal Policy Analysis (JV18.05) March 19 March 30, 2018 Vienna, Austria PROGRAM Monday, March 19 8:30

INTERNATIONAL MONETARY FUND Joint Vienna Institute / Institute for Capacity Development Course on Fiscal Policy Analysis (JV18.05) March 19 March 30, 2018 Vienna, Austria PROGRAM Monday, March 19 8:30

MANAGING CAPITAL FLOWS

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

(January 2016). The fiscal year for Rwanda is from July June; however, this DSA is prepared on a calendar

. The fiscal year for Rwanda is from July June; however, this DSA is prepared on a calendar") May 25, 216 RWANDA FIFTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT AND REQUEST FOR EXTENSION, AND REQUEST FOR AN ARRANGEMENT UNDER THE STANDBY CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By

May 25, 216 RWANDA FIFTH REVIEW UNDER THE POLICY SUPPORT INSTRUMENT AND REQUEST FOR EXTENSION, AND REQUEST FOR AN ARRANGEMENT UNDER THE STANDBY CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By

Bank Indonesia s Experience on Policy Mix

Bank Indonesia s Experience on Policy Mix Sahminan Department of Economic and Monetary Policy Bank Indonesia Central Bank Policy Mix: Issues, Challenges and Policy Responses Jakarta, 9-13 April 2018 Outline

Bank Indonesia s Experience on Policy Mix Sahminan Department of Economic and Monetary Policy Bank Indonesia Central Bank Policy Mix: Issues, Challenges and Policy Responses Jakarta, 9-13 April 2018 Outline

Chapter 16: Payments among Nations

Chapter 16: Payments among Nations Accounting Principles The balance of payments (BOP) is an accounting of a country's international transactions for a particular time period Double-entry accounting. Each

Chapter 16: Payments among Nations Accounting Principles The balance of payments (BOP) is an accounting of a country's international transactions for a particular time period Double-entry accounting. Each

Glossary of Terms: Printable Format

IMFx: FPP.2x Financial Programming and Policies, Part 2: Program Design Glossary of Terms: Printable Format Term Sector Definition Acronym Absorption Real The sum of domestic expenditures on consumption

IMFx: FPP.2x Financial Programming and Policies, Part 2: Program Design Glossary of Terms: Printable Format Term Sector Definition Acronym Absorption Real The sum of domestic expenditures on consumption

AQA Economics A-level

AQA Economics A-level Macroeconomics Topic 2: How the Macroeconomy Works, Circular Flow of Income, AD- AS Analysis and Related Concepts 2.3 The determinants of aggregate demand Notes Aggregate demand is

AQA Economics A-level Macroeconomics Topic 2: How the Macroeconomy Works, Circular Flow of Income, AD- AS Analysis and Related Concepts 2.3 The determinants of aggregate demand Notes Aggregate demand is

Balance of Payments, Debt, Financial Crises, and Stabilization Policies

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2

September 26 Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2 Cape Verde s debt level has increased in recent years. Despite the rising cost of servicing this debt, the country s external sustainability

September 26 Cape Verde: Joint Bank-Fund Debt Sustainability Analysis 1 2 Cape Verde s debt level has increased in recent years. Despite the rising cost of servicing this debt, the country s external sustainability

CIE Economics A-level

CIE Economics A-level Topic 4: The Macroeconomy f) Money supply (theory) Notes Quantity theory of money (MV = PT) The Quantity Theory of Money states that there is inflation if the money supply increases

CIE Economics A-level Topic 4: The Macroeconomy f) Money supply (theory) Notes Quantity theory of money (MV = PT) The Quantity Theory of Money states that there is inflation if the money supply increases

Chapter 1: The Balance of Payments (BoP)

") Chapter 1: The Balance of Payments (BoP) 2: Definition and Rules 2.1 Overview 2.2 Current Account 2.3 Capital Account 2.4 Financial Account 2.5 Balance-of-Payments Equilibrium 2.6 Net Errors and Omissions

Chapter 1: The Balance of Payments (BoP) 2: Definition and Rules 2.1 Overview 2.2 Current Account 2.3 Capital Account 2.4 Financial Account 2.5 Balance-of-Payments Equilibrium 2.6 Net Errors and Omissions

2 Macroeconomic Scenario

The macroeconomic scenario was conceived as realistic and conservative with an effort to balance out the positive and negative risks of economic development..1 The World Economy and Technical Assumptions

The macroeconomic scenario was conceived as realistic and conservative with an effort to balance out the positive and negative risks of economic development..1 The World Economy and Technical Assumptions

Yangon, Myanmar February 16 27, Jan Gottschalk. IMF-TAOLAM training activities are supported by funding of the Government of Japan

Introduction Financial Programming and Policies Yangon, Myanmar February 16 27, 2015 Jan Gottschalk TAOLAM IMF-TAOLAM training activities are supported by funding of the Government of Japan Outline I.

Introduction Financial Programming and Policies Yangon, Myanmar February 16 27, 2015 Jan Gottschalk TAOLAM IMF-TAOLAM training activities are supported by funding of the Government of Japan Outline I.

GDP and macroeconomic and fiscal forecasts

PFTAC GDP Compilation and Forecasting Workshop GDP and macroeconomic and fiscal forecasts Suva, Fiji October 18, 2016 Financial programming... is a quantitative approach used at the International Monetary

PFTAC GDP Compilation and Forecasting Workshop GDP and macroeconomic and fiscal forecasts Suva, Fiji October 18, 2016 Financial programming... is a quantitative approach used at the International Monetary

3 General Government Deficit and Debt

3 General Government Deficit and Debt 3.1 The Government s Strategy and the Medium-Term Fiscal Targets The main objectives of the government in the area of fiscal policy (see Section 1), which will be

3 General Government Deficit and Debt 3.1 The Government s Strategy and the Medium-Term Fiscal Targets The main objectives of the government in the area of fiscal policy (see Section 1), which will be

CÔTE D'IVOIRE ANALYSIS UPDATE. June 2, Prepared by the International Monetary Fund and the International Development Association

CÔTE D'IVOIRE June 2, 217 FIRST REVIEWS UNDER EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUESTS FOR MODIFICATION OF PERFORMANCE CRITERIA

CÔTE D'IVOIRE June 2, 217 FIRST REVIEWS UNDER EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY AND AN ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, AND REQUESTS FOR MODIFICATION OF PERFORMANCE CRITERIA

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

External Account and Foreign Debt Management

The Lahore Journal of Economics Special Edition External Account and Foreign Debt Management Ashfaque H. Khan * Abstract The paper highlights strong gains in the macro area. The author also shows how total

The Lahore Journal of Economics Special Edition External Account and Foreign Debt Management Ashfaque H. Khan * Abstract The paper highlights strong gains in the macro area. The author also shows how total

Debt Sustainability Framework for Low-Income Countries (LICs)

") Debt Sustainability Framework for Low-Income Countries (LICs) Instructor: Machiko Narita, IMF This training material is the property of the International Monetary Fund and is intended for use in IMF Institute

Debt Sustainability Framework for Low-Income Countries (LICs) Instructor: Machiko Narita, IMF This training material is the property of the International Monetary Fund and is intended for use in IMF Institute

ISLAMIC REPUBLIC OF AFGHANISTAN

July 1, 216 REQUEST FOR A THREE YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Bob Matthias Traa (IMF), Satu Kähkönen (IDA) International

July 1, 216 REQUEST FOR A THREE YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Bob Matthias Traa (IMF), Satu Kähkönen (IDA) International

Coordination between fiscal and debt management policies Emerging Issues

Sovereign Debt Management Forum 2014 Background Note for Breakout Session 3 Coordination between fiscal and debt management policies Emerging Issues Introduction Debt management cannot be carried out in

Sovereign Debt Management Forum 2014 Background Note for Breakout Session 3 Coordination between fiscal and debt management policies Emerging Issues Introduction Debt management cannot be carried out in

LECTURES 7-9: POLICY INSTRUMENTS, including MONEY. L7: Goals and Instruments Policy goals: Internal balance & External balance Policy instruments

LECTURES 7-9: POLICY INSTRUMENTS, including MONEY L7: Goals and Instruments Policy goals: Internal balance & External balance Policy instruments The Swan Diagram The principle of goals & instruments L8:

LECTURES 7-9: POLICY INSTRUMENTS, including MONEY L7: Goals and Instruments Policy goals: Internal balance & External balance Policy instruments The Swan Diagram The principle of goals & instruments L8:

Slovak Macroeconomic Outlook

Slovak Macroeconomic Outlook CFA society 29 March 2017 Jan Toth Deputy Governor National Bank of Slovakia Summary Acceleration of GDP growth in the medium-term due to start of the new productions in the

Slovak Macroeconomic Outlook CFA society 29 March 2017 Jan Toth Deputy Governor National Bank of Slovakia Summary Acceleration of GDP growth in the medium-term due to start of the new productions in the

Consumption expenditure The five most important variables that determine the level of consumption are:

The aggregate expenditure model: A macroeconomic model that focuses on the relationship between total spending and real GDP, assuming the price level is constant. Macroeconomic equilibrium: AE = GDP Consumption

The aggregate expenditure model: A macroeconomic model that focuses on the relationship between total spending and real GDP, assuming the price level is constant. Macroeconomic equilibrium: AE = GDP Consumption

AP Macroeconomics - Mega Macro Review Sheet Answers

AP Macroeconomics - Mega Macro Review Sheet Answers 1. The business cycle. 2. Aggregate supply curve (with breakdown of sections). 3. Expansionary ( easy ) monetary policy (Buy bonds, discount rate, reserve

AP Macroeconomics - Mega Macro Review Sheet Answers 1. The business cycle. 2. Aggregate supply curve (with breakdown of sections). 3. Expansionary ( easy ) monetary policy (Buy bonds, discount rate, reserve

1. When the Federal government uses taxation and spending actions to stimulate the economy it is conducting:

1. When the Federal government uses taxation and spending actions to stimulate the economy it is conducting: A. Fiscal policy B. Incomes policy C. Monetary policy D. Employment policy 2. When the Federal

1. When the Federal government uses taxation and spending actions to stimulate the economy it is conducting: A. Fiscal policy B. Incomes policy C. Monetary policy D. Employment policy 2. When the Federal

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA August 27, 212 STAFF REPORT FOR THE 212 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde-Wolf and Elliott Harris (IMF) and Jeffrey

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA August 27, 212 STAFF REPORT FOR THE 212 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Anne-Marie Gulde-Wolf and Elliott Harris (IMF) and Jeffrey

STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

February 7, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Vitaliy Kramarenko (IMF) and Paloma Anós Casero (IDA) Prepared by the staffs

February 7, 217 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Vitaliy Kramarenko (IMF) and Paloma Anós Casero (IDA) Prepared by the staffs

March 2007 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS

March 27 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS The staff s debt sustainability analysis (DSA) suggests that the Kyrgyz Republic s external debt continues to pose a heavy burden,

March 27 KYRGYZ REPUBLIC: JOINT BANK-FUND DEBT SUSTAINABILITY ANALYSIS The staff s debt sustainability analysis (DSA) suggests that the Kyrgyz Republic s external debt continues to pose a heavy burden,

ISLAMIC REPUBLIC OF AFGHANISTAN

November, STAFF REPORT FOR THE ARTICLE IV CONSULTATION AND FIRST REVIEW UNDER THE STAFF-MONITORED PROGRAM DEBT SUSTAINABILITY ANALYSIS Approved By Adnan Mazarei and Dhaneshwar Ghura (IMF), and Satu Kahkonen

November, STAFF REPORT FOR THE ARTICLE IV CONSULTATION AND FIRST REVIEW UNDER THE STAFF-MONITORED PROGRAM DEBT SUSTAINABILITY ANALYSIS Approved By Adnan Mazarei and Dhaneshwar Ghura (IMF), and Satu Kahkonen

Minutes of the Monetary Policy Committee meeting, August 2016

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, August 2016 Published 7 September 2016 The Act on the Central Bank of Iceland stipulates that

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, August 2016 Published 7 September 2016 The Act on the Central Bank of Iceland stipulates that

Mission (im)possible: connecting bank credit, money creation and economic imbalances

possible: connecting bank credit, money creation and economic imbalances") Mission (im)possible: connecting bank credit, money creation and economic imbalances Simonas Krėpšta Bank of Lithuania February 16, 2017 Reassessing the role of credit (1) Source: BIS (2016). 2 Reassessing

Mission (im)possible: connecting bank credit, money creation and economic imbalances Simonas Krėpšta Bank of Lithuania February 16, 2017 Reassessing the role of credit (1) Source: BIS (2016). 2 Reassessing

PRIVATE VERSUS PUBLIC SECTOR SAVING-INVESTMENT GAP IN THE MACEDONIAN ECONOMY A COMPARATIVE STUDY

PRIVATE VERSUS PUBLIC SECTOR SAVING-INVESTMENT GAP IN THE MACEDONIAN ECONOMY A COMPARATIVE STUDY Gjorgji Gockov, Elena Naumovska, Kiril Jovanovski, Ljupco Eftimov Ss. Cyril and Methodius University in

PRIVATE VERSUS PUBLIC SECTOR SAVING-INVESTMENT GAP IN THE MACEDONIAN ECONOMY A COMPARATIVE STUDY Gjorgji Gockov, Elena Naumovska, Kiril Jovanovski, Ljupco Eftimov Ss. Cyril and Methodius University in

Sovereign Credit Outlook. Richard Francis Director, Latin America Sovereigns Corficolombiana Conference December 5, 2018

Sovereign Credit Outlook Richard Francis Director, Latin America Sovereigns Corficolombiana Conference December 5, 218 Agenda Global Perspective Regional Overview Sovereign Ratings and Recent Actions Colombia

Sovereign Credit Outlook Richard Francis Director, Latin America Sovereigns Corficolombiana Conference December 5, 218 Agenda Global Perspective Regional Overview Sovereign Ratings and Recent Actions Colombia

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL. Joint IMF/IDA Debt Sustainability Analysis

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL Joint IMF/IDA Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

INTERNATIONAL MONETARY FUND AND INTERNATIONAL DEVELOPMENT ASSOCIATION SENEGAL Joint IMF/IDA Debt Sustainability Analysis Prepared by the Staffs of the International Monetary Fund and the International

The Effects of Dollarization on Macroeconomic Stability

The Effects of Dollarization on Macroeconomic Stability Christopher J. Erceg and Andrew T. Levin Division of International Finance Board of Governors of the Federal Reserve System Washington, DC 2551 USA

The Effects of Dollarization on Macroeconomic Stability Christopher J. Erceg and Andrew T. Levin Division of International Finance Board of Governors of the Federal Reserve System Washington, DC 2551 USA

REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS

May 18, 217 REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Dominique Desruelle and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA)

May 18, 217 REQUEST FOR A THREE-YEAR ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY DEBT SUSTAINABILITY ANALYSIS Approved By Dominique Desruelle and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA)

Model Question Paper Economics - II (MSF1A4)

") Model Question Paper Economics - II (MSF1A4) Answer all 74 questions. Marks are indicated against each question. 1. Which of the following is true if the central bank of a country sells government securities

Model Question Paper Economics - II (MSF1A4) Answer all 74 questions. Marks are indicated against each question. 1. Which of the following is true if the central bank of a country sells government securities

Basel Rules, endogenous Money Growth, Financial Accumulation and Debt Crisis

Basel Rules, endogenous Money Growth, Financial Accumulation and Debt Crisis Trond Andresen Department of Engineering Cybernetics The Norwegian University of Science and Technology

Basel Rules, endogenous Money Growth, Financial Accumulation and Debt Crisis Trond Andresen Department of Engineering Cybernetics The Norwegian University of Science and Technology

01jan195001jan196001jan197001jan198001jan199001jan200001jan201001jan2020 date

Turkish Lira Example British Pound 0 1.0e+06 2.0e+06 3.0e+06 4.0e+06 5.0e+06 01jan195001jan196001jan197001jan198001jan199001jan200001jan201001jan2020 date British Pound British Pound Ozan Hatipoglu (Department

Turkish Lira Example British Pound 0 1.0e+06 2.0e+06 3.0e+06 4.0e+06 5.0e+06 01jan195001jan196001jan197001jan198001jan199001jan200001jan201001jan2020 date British Pound British Pound Ozan Hatipoglu (Department

OVERVIEW OF CONCEPTS AND DEFINITIONS

OVERVIEW OF CONCEPTS AND DEFINITIONS Venkat Josyula Developing and Improving Sectoral Financial Accounts Algiers, January 20-21, 2016 The views expressed herein are those of the author and should not necessarily

OVERVIEW OF CONCEPTS AND DEFINITIONS Venkat Josyula Developing and Improving Sectoral Financial Accounts Algiers, January 20-21, 2016 The views expressed herein are those of the author and should not necessarily

ECO102. Macroeconomics Lecture 5

ECO102 Macroeconomics Lecture 5 ECO201 Macroeconomics Chapter 24: The Government and Fiscal Policy ECO102 Macroeconomics The Government and Fiscal Policy Government in the Economy!! Government Purchases

ECO102 Macroeconomics Lecture 5 ECO201 Macroeconomics Chapter 24: The Government and Fiscal Policy ECO102 Macroeconomics The Government and Fiscal Policy Government in the Economy!! Government Purchases

L-3 Analyzing Aggregate Demand

L-3 Analyzing Aggregate Demand IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Natan Epstein Deputy Director, STI This training material

L-3 Analyzing Aggregate Demand IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Natan Epstein Deputy Director, STI This training material

Policy in Papua New Guinea: releasing the golden bullet

Policy in Papua New Guinea: releasing the golden bullet Martin Davies Washington and Lee University and Development Policy Center, Crawford School of Public Policy, Australian National University Outline

Policy in Papua New Guinea: releasing the golden bullet Martin Davies Washington and Lee University and Development Policy Center, Crawford School of Public Policy, Australian National University Outline

Low-Income Countries (LICs): Overview

: Overview") Debt Sustainability Framework for Low-Income Countries (LICs): Overview OUTL LINE Lecture 1: Objectives and structure Lecture 2: What is the LIC DSF? Lecture 3: Relationship to IMF/WB policies and facilities

Debt Sustainability Framework for Low-Income Countries (LICs): Overview OUTL LINE Lecture 1: Objectives and structure Lecture 2: What is the LIC DSF? Lecture 3: Relationship to IMF/WB policies and facilities

MINISTRY OF FINANCE AND ECONOMIC AFFAIRS DEBT SUSTAINABILITY ANALYSIS Directorate of Debt Management and Economic Cooperation

MINISTRY OF FINANCE AND ECONOMIC AFFAIRS A S D DEBT SUSTAINABILITY ANALYSIS 2015 Directorate of Debt Management and Economic Cooperation Table of Contents LIST OF TABLES... 2 LIST OF FIGURES... 2 LIST

MINISTRY OF FINANCE AND ECONOMIC AFFAIRS A S D DEBT SUSTAINABILITY ANALYSIS 2015 Directorate of Debt Management and Economic Cooperation Table of Contents LIST OF TABLES... 2 LIST OF FIGURES... 2 LIST

International Trade in Goods and Assets. 1. The economic activity of a small, open economy can affect the world prices.

Chapter 13 International Trade in Goods and Assets Overview In order to understand the role of international trade, this chapter presents three models of a small, open economy where domestic economic actors

Chapter 13 International Trade in Goods and Assets Overview In order to understand the role of international trade, this chapter presents three models of a small, open economy where domestic economic actors

International Monetary Policy

International Monetary Policy 11 Balance of Payments and National Accounting 1 Michele Piffer London School of Economics 1 Course prepared for the Shanghai Normal University, College of Finance, April

International Monetary Policy 11 Balance of Payments and National Accounting 1 Michele Piffer London School of Economics 1 Course prepared for the Shanghai Normal University, College of Finance, April

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

February 9, 218 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Markus Rodlauer and Johannes Wiegand (IMF), and John Panzer (IDA) Prepared by Staffs of the International

February 9, 218 STAFF REPORT FOR THE 217 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Markus Rodlauer and Johannes Wiegand (IMF), and John Panzer (IDA) Prepared by Staffs of the International

COMMISSION STAFF WORKING DOCUMENT

EUROPEAN COMMISSION Brussels, 27.7.2016 SWD(2016) 263 final COMMISSION STAFF WORKING DOCUMENT Analysis by the Commission services of the budgetary situation in Spain following the adoption of the COUNCIL

EUROPEAN COMMISSION Brussels, 27.7.2016 SWD(2016) 263 final COMMISSION STAFF WORKING DOCUMENT Analysis by the Commission services of the budgetary situation in Spain following the adoption of the COUNCIL

Chapter 19. What Macroeconomics Is All About. In this chapter you will learn to. Key Macroeconomic Variables. Output and Income

Chapter 19 What Macroeconomics Is All About In this chapter you will learn to 1. Describe the meaning and importance of the key macroeconomic variables, including national income, unemployment, inflation,

Chapter 19 What Macroeconomics Is All About In this chapter you will learn to 1. Describe the meaning and importance of the key macroeconomic variables, including national income, unemployment, inflation,

REQUEST FOR A THREE-YEAR POLICY SUPPORT

SENEGAL June 9, 15 REQUEST FOR A THREE-YEAR POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum (IMF), and John Panzer (IDA) Prepared by the staffs of the

SENEGAL June 9, 15 REQUEST FOR A THREE-YEAR POLICY SUPPORT INSTRUMENT DEBT SUSTAINABILITY ANALYSIS UPDATE Approved By Roger Nord and Peter Allum (IMF), and John Panzer (IDA) Prepared by the staffs of the

Executive Directors welcomed the continued

ANNEX IMF EXECUTIVE BOARD DISCUSSION OF THE OUTLOOK, AUGUST 2006 The following remarks by the Acting Chair were made at the conclusion of the Executive Board s discussion of the World Economic Outlook

ANNEX IMF EXECUTIVE BOARD DISCUSSION OF THE OUTLOOK, AUGUST 2006 The following remarks by the Acting Chair were made at the conclusion of the Executive Board s discussion of the World Economic Outlook

Outlook for the Chilean Economy

Outlook for the Chilean Economy Jorge Marshall, Vice-President of the Board, Central Bank of Chile. Address to the Fifth Annual Latin American Banking Conference, Salomon Smith Barney, New York, March

Outlook for the Chilean Economy Jorge Marshall, Vice-President of the Board, Central Bank of Chile. Address to the Fifth Annual Latin American Banking Conference, Salomon Smith Barney, New York, March

The Real Sector. Real sector refers to real economic transactions of an economy.

The Real Sector INTRODUCTION Real sector refers to real economic transactions of an economy. Main players: Households Non-financial corporations Financial corporations General government Rest of the world

The Real Sector INTRODUCTION Real sector refers to real economic transactions of an economy. Main players: Households Non-financial corporations Financial corporations General government Rest of the world

Notes on the monetary transmission mechanism in the Czech economy

Notes on the monetary transmission mechanism in the Czech economy Luděk Niedermayer 1 This paper discusses several empirical aspects of the monetary transmission mechanism in the Czech economy. The introduction

Notes on the monetary transmission mechanism in the Czech economy Luděk Niedermayer 1 This paper discusses several empirical aspects of the monetary transmission mechanism in the Czech economy. The introduction

STAFF REPORT FOR THE 2016 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

July 25, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Catherine Pattillo (IMF) and John Panzer (IDA) Prepared by the staffs of the

July 25, 216 STAFF REPORT FOR THE 216 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Daniela Gressani and Catherine Pattillo (IMF) and John Panzer (IDA) Prepared by the staffs of the

The Economics of the Federal Budget Deficit

Order Code RL31235 The Economics of the Federal Budget Deficit Updated January 24, 2007 Brian W. Cashell Specialist in Quantitative Economics Government and Finance Division The Economics of the Federal

Order Code RL31235 The Economics of the Federal Budget Deficit Updated January 24, 2007 Brian W. Cashell Specialist in Quantitative Economics Government and Finance Division The Economics of the Federal

Basic macroeconomic concepts

Basic macroeconomic concepts in preparation for API-120 Prof. Jeffrey Frankel MPA/ID program August 2015 Lecture (i) -- GDP definitions Reading on growth accounting: Krugman, 1994, The Myth of the Asian

Basic macroeconomic concepts in preparation for API-120 Prof. Jeffrey Frankel MPA/ID program August 2015 Lecture (i) -- GDP definitions Reading on growth accounting: Krugman, 1994, The Myth of the Asian

Trade Reform and Macroeconomic Policy in Vietnam. Rod Tyers and Lucy Rees Australian National University

Trade Reform and Macroeconomic Policy in Vietnam Rod Tyers and Lucy Rees Australian National University 1 Robustness of Gains From Trade Liberalisation Long run gains have been mostly positive Short run

Trade Reform and Macroeconomic Policy in Vietnam Rod Tyers and Lucy Rees Australian National University 1 Robustness of Gains From Trade Liberalisation Long run gains have been mostly positive Short run

Macroeconomic Management in Emerging-Market Economies with Open Capital Accounts. Outline

Macroeconomic Management in Emerging-Market Economies with Open Capital Accounts Klaus Schmidt-Hebbel, Central Bank of Chile Seminar on Crisis Prevention in Emerging Markets IMF-Singapore Training Institute

Macroeconomic Management in Emerging-Market Economies with Open Capital Accounts Klaus Schmidt-Hebbel, Central Bank of Chile Seminar on Crisis Prevention in Emerging Markets IMF-Singapore Training Institute

STAFF REPORT FOR THE 2017 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS

May 9, 17 STAFF REPORT FOR THE 17 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Jorge Roldos and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA) Prepared by the staff of the International

May 9, 17 STAFF REPORT FOR THE 17 ARTICLE IV CONSULTATION DEBT SUSTAINABILITY ANALYSIS Approved By Jorge Roldos and Andrea Richter Hume (IMF) and Paloma Anos-Casero (IDA) Prepared by the staff of the International

COMMISSION STAFF WORKING DOCUMENT. Analysis of the 2016 Draft Budgetary Plan of GERMANY. Accompanying the document COMMISSION OPINION

EUROPEAN COMMISSION Brussels, 16.11.2015 SWD(2015) 601 final COMMISSION STAFF WORKING DOCUMENT Analysis of the 2016 Draft Budgetary Plan of GERMANY Accompanying the document COMMISSION OPINION on the Draft

EUROPEAN COMMISSION Brussels, 16.11.2015 SWD(2015) 601 final COMMISSION STAFF WORKING DOCUMENT Analysis of the 2016 Draft Budgetary Plan of GERMANY Accompanying the document COMMISSION OPINION on the Draft

This is Policy Effects with Floating Exchange Rates, chapter 10 from the book Policy and Theory of International Finance (index.html) (v. 1.0).

(v. 1.0).") This is Policy Effects with Floating Exchange Rates, chapter 10 from the book Policy and Theory of International Finance (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0

This is Policy Effects with Floating Exchange Rates, chapter 10 from the book Policy and Theory of International Finance (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0

Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1

1 December 26 Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1 1. Malawi s risk of debt distress after debt relief under the HIPC Initiative and the Multilateral

1 December 26 Malawi: Joint Bank-Fund Debt Sustainability Analysis Based on Low-Income County Framework 1 1. Malawi s risk of debt distress after debt relief under the HIPC Initiative and the Multilateral

Policy in Papua New Guinea: recent shocks, new directions

Policy in Papua New Guinea: recent shocks, new directions Keynote Address, CPA PNG Conference, Lae, August 24-25 2017 Martin Davies Associate Professor Washington and Lee University Visiting Associate

Policy in Papua New Guinea: recent shocks, new directions Keynote Address, CPA PNG Conference, Lae, August 24-25 2017 Martin Davies Associate Professor Washington and Lee University Visiting Associate

INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND MALAWI. Joint Bank Fund Debt Sustainability Analysis Update

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND MALAWI Joint Bank

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION AND INTERNATIONAL MONETARY FUND MALAWI Joint Bank

AP Macroeconomics Graphical Overview

AP Macroeconomics Graphical Overview 1. The business cycle. 2. Aggregate supply curve (with breakdown of sections). 3. Expansionary ( easy ) monetary policy (Buy bonds, discount rate, reserve requirement).

AP Macroeconomics Graphical Overview 1. The business cycle. 2. Aggregate supply curve (with breakdown of sections). 3. Expansionary ( easy ) monetary policy (Buy bonds, discount rate, reserve requirement).

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA. Joint Bank-Fund Debt Sustainability Analysis 1

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA Joint Bank-Fund Debt Sustainability Analysis 1 Public Disclosure Authorized Public Disclosure Authorized

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETRY FUND CAMBODIA Joint Bank-Fund Debt Sustainability Analysis 1 Public Disclosure Authorized Public Disclosure Authorized

What is Monetary Policy?

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

The Effectiveness of Non-traditional Monetary Policy and the Inflation Target Policy : The Case of Japan in Comparison with the US

Economics & Management Series EMS-2013-11 The Effectiveness of Non-traditional Monetary Policy and the Inflation Target Policy : The Case of Japan in Comparison with the US Osamu Nakamura International

Economics & Management Series EMS-2013-11 The Effectiveness of Non-traditional Monetary Policy and the Inflation Target Policy : The Case of Japan in Comparison with the US Osamu Nakamura International

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LAO PEOPLE S DEMOCRATIC REPUBLIC

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LAO PEOPLE S DEMOCRATIC REPUBLIC Joint Bank/Fund Debt Sustainability Analysis 28 1 Prepared by the staffs of the International Development

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND LAO PEOPLE S DEMOCRATIC REPUBLIC Joint Bank/Fund Debt Sustainability Analysis 28 1 Prepared by the staffs of the International Development

Macroeconomic Accounts and Policies: Introduction and Internal and External Balances(*)

") Macroeconomic Accounts and Policies: Introduction and Internal and External Balances(*) World Bank/Poverty and Equity Summer University, Washington, DC, July 20-21, 2017 Alvaro Manoel International Consultant

Macroeconomic Accounts and Policies: Introduction and Internal and External Balances(*) World Bank/Poverty and Equity Summer University, Washington, DC, July 20-21, 2017 Alvaro Manoel International Consultant

Sweden: Concluding Statement for the 2019 Article IV Consultation

Sweden: Concluding Statement for the 2019 Article IV Consultation Macroeconomic policies must continue to support Sweden s economic resilience. Growth is expected to slow in 2019, with material downside

Sweden: Concluding Statement for the 2019 Article IV Consultation Macroeconomic policies must continue to support Sweden s economic resilience. Growth is expected to slow in 2019, with material downside

Economic Policy in the Crisis. Lars Calmfors Jönköping International Business School, 2 November 2009

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

IMPROVING FISCAL MANAGEMENT IN GHANA: THE ROLE OF FISCAL POLICY RULES

IMPROVING FISCAL MANAGEMENT IN GHANA: THE ROLE OF FISCAL POLICY RULES Institute of Economic Affairs Accra, Ghana 16 th June, 2015 6/16/2015 Introduction Ghana has a long record of poor fiscal management

IMPROVING FISCAL MANAGEMENT IN GHANA: THE ROLE OF FISCAL POLICY RULES Institute of Economic Affairs Accra, Ghana 16 th June, 2015 6/16/2015 Introduction Ghana has a long record of poor fiscal management

Investment and its Financing: A Macro Perspective

G R O U P O F T W E N T Y Investment and its Financing: A Macro Perspective Annex to the G Surveillance Note Meetings of G Finance Ministers and Central Bank Governors February, 3 Prepared by Staff of

G R O U P O F T W E N T Y Investment and its Financing: A Macro Perspective Annex to the G Surveillance Note Meetings of G Finance Ministers and Central Bank Governors February, 3 Prepared by Staff of

THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA

August 29, 213 THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITYANALYSIS Approved By Michael Atingi-Ego and Elliott Harris (IMF) and Jeffrey

August 29, 213 THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA STAFF REPORT FOR THE 213 ARTICLE IV CONSULTATION DEBT SUSTAINABILITYANALYSIS Approved By Michael Atingi-Ego and Elliott Harris (IMF) and Jeffrey

Georgia: Joint Bank-Fund Debt Sustainability Analysis 1

November 6 Georgia: Joint Bank-Fund Debt Sustainability Analysis 1 Background 1. Over the last decade, Georgia s external public and publicly guaranteed (PPG) debt burden has fallen from more than 8 percent

November 6 Georgia: Joint Bank-Fund Debt Sustainability Analysis 1 Background 1. Over the last decade, Georgia s external public and publicly guaranteed (PPG) debt burden has fallen from more than 8 percent

Joint Bank-Fund Debt Sustainability Analysis 2018 Update

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND GRENADA Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND GRENADA Joint Bank-Fund Debt Sustainability Analysis 218 Update Prepared jointly by the staffs of the International Development Association