GAAP & IFRS Updates: What you need to know

|

|

|

- Everett Jennings

- 6 years ago

- Views:

Transcription

1 GAAP & IFRS Updates: What you need to know Claire Gemmell Account Manager Rhead Hatch Product Owner

2 Learning Objectives Identify differences in the classification and measurement of financial instruments at initial recognition and subsequently under IFRS 9 Learn how to calculate expected losses under both the IASB s ECL model and the FASB s CECL model Learn about FASB Accounting Standards Updates relevant to investments from 2016 and 2017

3 Agenda IFRS 9 updates IFRS 17 updates IFRS 9 ECL model versus US GAAP CECL model Accounting Standards Updates from GAAP relevant to investments» ASU : Recognition & Measurement of Financial Assets and Financial Liabilities» ASU : Effect of Derivative Contract Novations on Existing Hedge Accounting Relationships» ASU : Contingent Put and Call Options in Debt Instruments» ASU : Simplifying the Transition to the Equity Method of Accounting» ASU : Measurement of Credit Losses on Financial Instruments (CECL discussion)» ASU : Targeted Improvements to Accounting for Hedging Activities

4 IFRS 9 What is it? IFRS 9 is an International Financial Reporting Standard It provides guidance on:» Classification and measurement of financial assets» Impairment of financial assets» Hedge accounting

5 IFRS 9 Why did it come about? Anyone who claims that they fully understand IAS 39 has not read it properly. Sir David Tweedie, former IASB chairman

6 IFRS 9 When is it effective? January 1, 2018 There is a deferral option until January 1, 2021 for companies adopting IFRS 17 insurance contracts

7 IFRS 9: Overview

8 Overview of IFRS 9 Initial measurement of financial assets Initially measured at fair value +/- transaction costs (if not FVTPL) Subsequent measurement: two major classifications» Amortized cost» Fair value If at fair value, gains and losses are recognized in one of two ways:» Profit or loss (FVTPL)» Other comprehensive income (FVTOCI)

9 Classification and Measurement IAS 39 classifications (4)» Held for trading (FVTPL)» Available for sale (AFS)» Held to maturity (HTM)» Loans and receivables IFRS 9 classifications (3)» Fair value through profit or loss (FVPL)» Fair value through other comprehensive income (FVOCI)» Amortized cost

10 Key differences between IAS 39 & IFRS 9 IAS 39 IFRS 9 Rule-based Complex and difficult to apply Classification and Measurement rules Complicated Reclassification rules Multiple impairment models Principle-based Classification based on business model and nature of cash flows Business model-driven reclassification One impairment model

11 All Financial Assets: Classification Decision Tree

12 Debt Assets Only

13 Debt Assets Classification considerations Cash flow characteristics test (SPPI test) instrument level Business model test (aggregate level) FVTPL option elected?

14 SPPI Test IFRS 9 basic lending arrangement: Principal versus interest Interest should be the consideration for basic lending risks» TVM, credit risk, liquidity risk, and administrative costs associated with holding the asset Some things wouldn t meet the test» Commodity or index-linked securities» Convertible debt or embedded derivatives (FVTPL)

15 Debt Classifications 1. Amortized cost» Cash flows are solely payments of principal and interest on the principal amount outstanding» Business model where the objective is to hold the assets to collect their contractual cash flows (rather than to sell)» FVTPL option is NOT elected 2. FVTOCI» Cash flows are solely payments of principal and interest on the principal amount outstanding» Business model where the objective is to hold and sell the assets to collect their contractual cash flows» FVTPL option is NOT elected 3. FVTPL is the default option

16 Debt Measurement If debt assets are classified as FVTOCI: What goes through OCI:» Unrealized gains or losses What goes through P/L:» Interest Income» FX» Impairment gains or losses» Unrealized gains and losses reclassified to P/L on derecognition

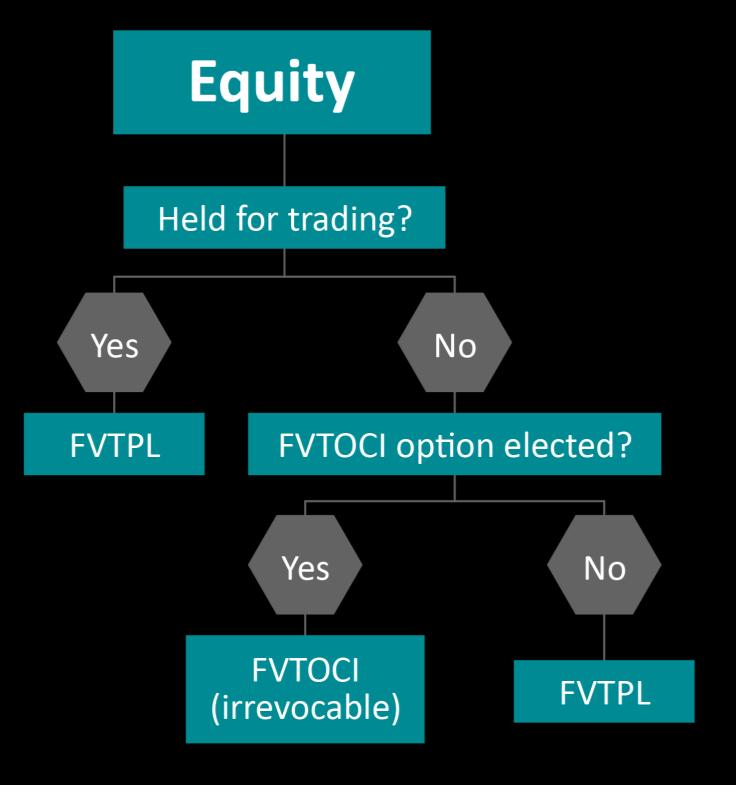

17 Equity Instruments

18 Equity Instruments FVTPL is the default treatment» The entity has the option to designate an instrument as FVTOCI Only available at initial recognition and is irrevocable This option results in all gains and losses being presented in OCI except for dividend income (P/L) FVTOCI is not the same as available for sale (AFS) in IAS 39:» No recycling to P/L on derecognition» No impairment testing leading to recycling from OCI to P/L

19 Financial Liabilities IFRS 9 is very similar to IAS 39» i.e. classification options are still amortized cost or FVTPL

20 IFRS 9 Impairment Changes Change from an incurred loss to an expected loss model Earlier recognition of impairment losses is likely to result Three-stage impairment model for assets that are:» Performing» Underperforming» Non-performing Stage assessment is based on relative (not absolute) credit risk compared to credit risk at initial recognition

21 Three-Stage ECL Model for Impairment STAGE 1 STAGE 2 STAGE 3 Financial asset Performing Credit risk significantly increased Credit-impaired Loss allowance 12-month expected credit losses Lifetime expected credit losses Lifetime expected credit losses Interest revenue On gross carrying amount On gross carrying amount On amortized cost

22 ECL Inputs PD (probability of default)» Likelihood that a loan will not be repaid and will fall into default LGD (loss given default)» The fractional loss due to default, i.e. 100% less the recovery rate EAD (exposure at default)» The total exposure to credit risk (the amount the borrower owes to the lending institution at the time of default) EL PD LGD EAD

23 IFRS 17

24 IFRS 17 Overview The new IFRS standard for insurance contract accounting Has been under development for many years A more robust standard than the current IFRS 4 Effective date 2021 There are parallels with Solvency II in Europe Building blocks approach

25 Accounting Standards Updates issued in 2016

26 ASU Recognition and Measurement of Financial Assets and Financial Liabilities Equity Investments (excluding those accounted for under the Equity Method or those that result in consolidation of the investee) should be measured at Fair Value through Net Income Special treatment available if they do not have readily available fair values» Can be measured at fair value either upon occurrence of an observable price change or upon impairment» Impairment processes simplified to be a qualitative assessment and impairment to fair value Adoption should include a cumulative effect adjustment to the balance sheet Effective date: 2018, including interim periods» Early adoption is not permitted

27 ASU Effect of Derivative Contract Novations on Existing Hedge Accounting Relationships Novation: Replacing one party in a contract with a new party Historically may have been considered sufficient to require designation of that hedging relationship This update clarifies that a change in counterparty by itself all other hedge accounting criteria remaining the same does not require designation Entities have the option to apply the update on either a prospective basis or a modified retrospective basis Effective Date: 2017

28 ASU Contingent Put and Call Options in Debt Instruments Historically, GAAP indicated that a contingently exercisable put or call option is clearly and closely related to the debt host if it is indexed only to interest rates or credit risk, and not some extraneous event or factor, did not specifically address the contingency itself ASU clarified that an exercise contingency event does not need to be evaluated to determine whether it relates to interest rates and credit risk in an embedded derivative analysis Application upon adoption should be done on a modified retrospective basis Effective Date for public business entities: 2017

29 ASU Simplifying the Transition to the Equity Method of Accounting Changes handling of treatment of a non-equity method investment increases ownership and begins to qualify for equity method treatment FASB eliminated requirement of retrospective equity method treatment, allowing investor to add cost of acquiring additional interest to existing basis, then adopt equity method treatment as of the date it becomes qualified Intent is to ease the burden of transitioning into using Equity Method accounting For adoption, changes should be applied prospectively Effective 2017, including interim periods

30 Current Expected Credit Loss Model (ASU )

31 ASU Why the Update? Measurement of Credit Losses on Financial Instruments Current impairment model required credit losses to be probable before impairment losses could be recognized Both financial institutions and users of their financial statements had concerns about the lack of reporting for credit losses that were expected but had not yet reached the probable threshold Financial crisis in 2008 highlighted this weakness FASB and IASB shared a joint project to rectify this similarity in their impairment guidance ASU is intended to help provide more decision-useful information to financial statement users on a more timely basis

32 ASU Scope Entities holding financial assets and net investments in leases not accounted for at fair value through net income Entities holding loans, debt securities, trade receivables, net investments in leases, off balance sheet credit exposure, reinsurance receivables, any other financial asset not excluded from the scope that have the contractual right to receive cash

33 ASU Assets held at Amortized Cost Current Expected Credit Loss (CECL)» Determination of Credit Loss is now based on Current Expected Credit Loss model» This applies to HTM securities, as well as trade receivables, lease receivables, reinsurance receivables that result from insurance transactions, financial guarantee contracts, and loan commitments» Allowance based approach rather than a reduction to the amortized cost of asset» No threshold to impairment (Best Estimate vs. Allowance)» Required to pool assets when similar risk characteristics exist» Forward looking

34 ASU Deeper into CECL Model Forward Looking Must estimate credit losses over the entire life of the instrument» Requires management to create a model for the contractual life of the instrument» Required to not only consider historical information and current conditions, but also use forecasts about future economic conditions Forecasts should be reasonable and supportable Can use historical loss information beyond timeframes that reasonable and supportable forecasts can be made» Use of discounted cash flows is one approach, but is not a required approach An entity should use judgement to develop an approach that allows the best estimate of future credit losses

35 ASU PCD held at Amortized Cost Purchased assets with a more-than-insignificant amount of credit deterioration since origination held at amortized cost» Initial allowance for credit loss is added to the purchase price in determining amortized cost» Interest Income based on effective interest rate, excluding the discount in the purchase price attributable to credit loss assessment at purchase

36 ASU Available For Sale Assets CECL does not apply to AFS securities ASC reorganized impairment guidance (now in ) and eliminated to Other-Than-Temporary Impairment concept Intent to Sell, or More Likely Than Not will be Required to Sell are still triggers for Impairment recognition» Direct write down of amortized cost

37 ASU Available for Sale Credit Losses Credit losses should now be recorded through an allowance for credit losses» No longer decreases amortized cost Calculated as difference between present value of future expected cash flows and amortized cost Limited to amount by which fair value is less than amortized cost Reversals are allowed as allowance may decrease Should no longer use duration of impairment to avoid recognizing credit loss» Most other qualitative criteria were kept (e.g. severity, adverse conditions, etc.)

38 ASU PCD considered Available for Sale Purchased assets with a more-than-insignificant amount of credit deterioration since origination considered Available for Sale» Initial allowance for credit loss is added to the purchase price in determining» amortized cost» Interest Income based on effective interest rate, excluding the discount in the purchase price attributable to credit loss assessment at purchase

39 ASU : AFS Impairment Decisions

40 ASU Impairment Comparison Topic AFS debt security impairment model* HTM current expected credit loss model Unit of Measurement Allowance Recognition Threshold Measurement of credit loss Acceptable methods for measuring credit losses Individual AFS debt security When a decline in fair value below the amortized cost basis has resulted from a credit loss Excess of the amortized cost basis over the best estimate of the present value of cash flows expected to be collected, limited by the amount that fair value is less than amortized cost DCF Collective (pool) when similar risk characteristics exist; otherwise, individual None Expected credit loss that reflects the risk of loss even if that risk is remote Various methods are appropriate, including DCF, loss rate, PD and others that faithfully estimate collectability by applying the principles in ASC *When the entity has decided to see the debt security or it s more likely than not the entity will be required to sell the security before recovery of the security s amortized cost basis, the security s amortized cost basis should be written down to fair value through earnings at the report date. Source: E&Y Technical Line No : A closer look at the New credit impairment standard (

41 ASU Transition and Effective Date Adoption should include a cumulativeeffect adjustment to retained earnings as of the first period in which the guidance is effective A prospective approach is required for debt securities that have had an OTTI in the past PCD assets should also apply this prospectively, adjusting amortized cost to reflect the addition of the allowance for credit losses Effective Date: 2020, including interim periods» Early adoption allowed for 2019

42 ASU Targeted Improvements to Accounting for Hedging Activities Intended to help better align hedge accounting with companies risk management strategies, reduce barriers to application, and make the results more useful to users of financial statements» Makes more financial and non-financial hedging strategies qualify for hedge accounting» Amends presentation and disclosures about hedging activity» Changes how companies assess hedging effectiveness

43 IFRS 9 ECL vs. US GAAP CECL

44 The IASB s ECL vs. the FASB s CECL Similarities More forward-looking expected loss approaches for recognizing credit losses Recognize losses that have already occurred, plus losses that are expected in the future

45 The IASB s ECL vs. the FASB s CECL Differences The IASB, in its new IFRS 9 legislation, does not call for lifetime expected losses to be recognized unless there is evidence of deteriorating credit quality The FASB s CECL model calls for recognition of losses over the life of the loan» Requiring institutions to recognize losses at the origination of the loan (even if the loan is fully performing) The IASB ECL model applies to AFS and HTM securities, the FASB s CECL model does not apply to AFS securities The IASB ECL model requires the use of discounted cash flows, FASB s CECL model allows discounted cash flows, but allows management entities to decide most appropriate forecasting model

46 Questions?

47 Reminders Take the post-session survey in the Clearwater Events app Session presentations are available on the app Take the Clearwater Client Benchmark Survey in room 440 and earn Clearwater swag. Don t miss the Monday networking reception from 4:30 to 6:30 p.m.

New and revised Standards -Applying IFRS 9 Presentation by: CPA Stephen Obock December 2017

New and revised Standards -Applying IFRS 9 Presentation by: CPA Stephen Obock December 2017 Uphold public interest IFRS 9 What are the key changes? What are the transition requirements? Presentation agenda

New and revised Standards -Applying IFRS 9 Presentation by: CPA Stephen Obock December 2017 Uphold public interest IFRS 9 What are the key changes? What are the transition requirements? Presentation agenda

IFRS 9 for Insurers. Syysseminaari. Aktuaaritoiminnan kehittämissäätiö. 30 November 2017

IFRS 9 for Insurers Syysseminaari Aktuaaritoiminnan kehittämissäätiö 30 November 2017 Agenda 1 Introduction from IAS 39 to IFRS 9 2 Classification 3 Impairment 4 Hedge accounting Page 2 What changes do

IFRS 9 for Insurers Syysseminaari Aktuaaritoiminnan kehittämissäätiö 30 November 2017 Agenda 1 Introduction from IAS 39 to IFRS 9 2 Classification 3 Impairment 4 Hedge accounting Page 2 What changes do

IFRS 9 FINANCIAL INSTRUMENTS

IFRS 9 FINANCIAL INSTRUMENTS Uphold public interest CPA WILFRED OWALLA Why the New Standard? IFRS 9 responds to criticisms that IAS 39 is too complex, inconsistent with the way entities manage their businesses

IFRS 9 FINANCIAL INSTRUMENTS Uphold public interest CPA WILFRED OWALLA Why the New Standard? IFRS 9 responds to criticisms that IAS 39 is too complex, inconsistent with the way entities manage their businesses

IFRS 9 Financial Instruments. IICPAK: The Financial Reporting Workshop 4 th and 5 th December 2014 Hilton Hotel, Nairobi

IFRS 9 Financial Instruments IICPAK: The Financial Reporting Workshop 4 th and 5 th December 2014 Hilton Hotel, Nairobi Why are we discussing this topic? Why are we discussing this topic? Area that is

IFRS 9 Financial Instruments IICPAK: The Financial Reporting Workshop 4 th and 5 th December 2014 Hilton Hotel, Nairobi Why are we discussing this topic? Why are we discussing this topic? Area that is

Putting IFRS 9 into practice Presentation by: CPA Stephen Obock February 2018

Putting IFRS 9 into practice Presentation by: CPA Stephen Obock February 2018 Uphold public interest IFRS 9 What are the key changes? What are the transition requirements? Presentation agenda Introduction

Putting IFRS 9 into practice Presentation by: CPA Stephen Obock February 2018 Uphold public interest IFRS 9 What are the key changes? What are the transition requirements? Presentation agenda Introduction

FINANCIAL REPORTING WORKSHOP **IFRS 9: FINANCIAL INSTRUMENTS** Presentation by: CPA Boniface L Souza, ACIM, CFIP Wednesday, 15 th November 2017

FINANCIAL REPORTING WORKSHOP **IFRS 9: FINANCIAL INSTRUMENTS** Presentation by: CPA Boniface L Souza, ACIM, CFIP Wednesday, 15 th November 2017 Uphold public interest Agenda Why the transition to IFRS

FINANCIAL REPORTING WORKSHOP **IFRS 9: FINANCIAL INSTRUMENTS** Presentation by: CPA Boniface L Souza, ACIM, CFIP Wednesday, 15 th November 2017 Uphold public interest Agenda Why the transition to IFRS

Technical Line FASB final guidance

No. 2016-24 12 October 2016 Technical Line FASB final guidance A closer look at the new credit impairment standard All entities will need to change the way they recognize and measure impairment of financial

No. 2016-24 12 October 2016 Technical Line FASB final guidance A closer look at the new credit impairment standard All entities will need to change the way they recognize and measure impairment of financial

Contents. Financial instruments the complete standard. Fundamental changes call for careful planning. 1. Overview Complete IFRS 9

Financial instruments the complete standard Contents Fundamental changes call for careful planning 1. Overview Complete IFRS 9 2. Classification and measurement Facts 3. Classification and measurement

Financial instruments the complete standard Contents Fundamental changes call for careful planning 1. Overview Complete IFRS 9 2. Classification and measurement Facts 3. Classification and measurement

IFRS News. Special Edition on IFRS 9 (2014) IFRS 9 Financial Instruments is now complete

IFRS 9 Financial Instruments is now complete") Special Edition on IFRS 9 (2014) IFRS News IFRS 9 Financial Instruments is now complete Following several years of development, the IASB has finished its project to replace IAS 39 Financial Instruments:

Special Edition on IFRS 9 (2014) IFRS News IFRS 9 Financial Instruments is now complete Following several years of development, the IASB has finished its project to replace IAS 39 Financial Instruments:

IFRS 9 FINANCIAL INSTRUMENTS (2014) INTERNATIONAL FINANCIAL REPORTING BULLETIN 2014/12

INTERNATIONAL FINANCIAL REPORTING BULLETIN 2014/12") IFRS 9 FINANCIAL INSTRUMENTS (2014) INTERNATIONAL FINANCIAL REPORTING BULLETIN 2014/12 Summary On 24 July 2014, the International Accounting Standards Board (IASB) completed its project on financial instruments

IFRS 9 FINANCIAL INSTRUMENTS (2014) INTERNATIONAL FINANCIAL REPORTING BULLETIN 2014/12 Summary On 24 July 2014, the International Accounting Standards Board (IASB) completed its project on financial instruments

Risk and Accounting. IFRS 9 Financial Instruments. Marco Venuti 2018

Risk and Accounting IFRS 9 Financial Instruments Marco Venuti 2018 Agenda Reasons for issuing IFRS 9 Classification approach by IFRS 9 Classification and Measurement of financial assets Contractual cash

Risk and Accounting IFRS 9 Financial Instruments Marco Venuti 2018 Agenda Reasons for issuing IFRS 9 Classification approach by IFRS 9 Classification and Measurement of financial assets Contractual cash

IFRS 9 Financial Instruments

IFRS 9 Financial Instruments Session 705 Wednesday June 10, 2015 IFRS 9 Financial Instruments Presented by: Betsy G. Rose Assistant Vice President - Product Management State Street Global Exchange Maria

IFRS 9 Financial Instruments Session 705 Wednesday June 10, 2015 IFRS 9 Financial Instruments Presented by: Betsy G. Rose Assistant Vice President - Product Management State Street Global Exchange Maria

IND AS 109 Financial Instruments. 28 March 2015

IND AS 109 Financial Instruments 28 March 2015 Agenda Background Classification and Measurement Expected Credit Losses Hedge accounting Disclosures Business Impacts and Next Steps Key Points to Remember

IND AS 109 Financial Instruments 28 March 2015 Agenda Background Classification and Measurement Expected Credit Losses Hedge accounting Disclosures Business Impacts and Next Steps Key Points to Remember

AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL INFORMATION (UNAUDITED) 31 MARCH 2018

31 MARCH 2018") AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL 31 MARCH 2018 INTERIM CONDENSED CONSOLIDATED INCOME STATEMENT (UNAUDITED) For the period ended 31 March

AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL 31 MARCH 2018 INTERIM CONDENSED CONSOLIDATED INCOME STATEMENT (UNAUDITED) For the period ended 31 March

Session 15PD: GAAP Hot Topics. Moderator: Presenters: Anne Potas

Session 15PD: GAAP Hot Topics Moderator: Presenters: Anne Potas SOA Antitrust Disclaimer SOA Presentation Disclaimer Hot topics in GAAP reporting Anne Potas 28 August 2017 Disclaimer The material contained

Session 15PD: GAAP Hot Topics Moderator: Presenters: Anne Potas SOA Antitrust Disclaimer SOA Presentation Disclaimer Hot topics in GAAP reporting Anne Potas 28 August 2017 Disclaimer The material contained

Hot topics treasury seminar

IFRS 9 Lessons learned from first implementations Discover and unlock your potential Program Introduction and objectives Phase 1 Classification and measurement Phase 2 Impairments Phase 3 Hedge Accounting

IFRS 9 Lessons learned from first implementations Discover and unlock your potential Program Introduction and objectives Phase 1 Classification and measurement Phase 2 Impairments Phase 3 Hedge Accounting

Current Expected Credit Losses (CECL) for Mortgage Banking

for Mortgage Banking") Current Expected Credit Losses (CECL) for Mortgage Banking November 15, 2017 Presented by: Matthew Streadbeck, Partner, Ernst & Young LLP Carrie Kennedy, Partner, Moss Adams, LLP Jonathan Prejean, Managing

Current Expected Credit Losses (CECL) for Mortgage Banking November 15, 2017 Presented by: Matthew Streadbeck, Partner, Ernst & Young LLP Carrie Kennedy, Partner, Moss Adams, LLP Jonathan Prejean, Managing

IFRS 9 FINANCIAL INSTRUMENTS FOR NON FINANCIAL INSTITUTIONS. New member firm training 2010 Page 1

IFRS 9 FINANCIAL INSTRUMENTS FOR NON FINANCIAL INSTITUTIONS New member firm training 2010 Page 1 AGENDA / OUTLINE IFRS 9 Financial Instruments Objective & Scope Key definitions Background & introduction

IFRS 9 FINANCIAL INSTRUMENTS FOR NON FINANCIAL INSTITUTIONS New member firm training 2010 Page 1 AGENDA / OUTLINE IFRS 9 Financial Instruments Objective & Scope Key definitions Background & introduction

Overview Why the introduction of IFRS 9?

Overview Why the introduction of IFRS 9? Response to G20 and Financial Stability Board (FSB) 2008 Financial crisis Excessive risk-taking by banks and late recording of impairments on instruments which

Overview Why the introduction of IFRS 9? Response to G20 and Financial Stability Board (FSB) 2008 Financial crisis Excessive risk-taking by banks and late recording of impairments on instruments which

Contrasting the new US GAAP and IFRS credit impairment models

Contrasting the new and credit impairment models A comparison of the requirements of ASC 326 and 9 No. US2017-24 September 26, 2017 What s inside: Background....1 Overview......1 Key areas....2 Scope......2

Contrasting the new and credit impairment models A comparison of the requirements of ASC 326 and 9 No. US2017-24 September 26, 2017 What s inside: Background....1 Overview......1 Key areas....2 Scope......2

PRESTIGE ASSURANCE PLC THE UNAUDITED FINANCIAL STATEMENTS

PRESTIGE ASSURANCE PLC THE UNAUDITED FINANCIAL STATEMENTS FIRST QUARTER 2018 2 TABLE OF CONTENT Cover Page 1 Table of Content 2 Certification 3 Summary of Significant Accounting Policies 4-33 Financial

PRESTIGE ASSURANCE PLC THE UNAUDITED FINANCIAL STATEMENTS FIRST QUARTER 2018 2 TABLE OF CONTENT Cover Page 1 Table of Content 2 Certification 3 Summary of Significant Accounting Policies 4-33 Financial

IFRS 9 Financial Instruments Thai Life Assurance Association

IFRS 9 Financial Instruments Thai Life Assurance Association 13 December 2016 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

IFRS 9 Financial Instruments Thai Life Assurance Association 13 December 2016 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

Credit impairment. Handbook US GAAP. March kpmg.com/us/frv

Credit impairment Handbook US GAAP March 2018 kpmg.com/us/frv Contents Foreword... 1 About this publication... 2 1. Executive summary... 4 Subtopic 326-20 2. Scope of Subtopic 326-20... 14 3. Recognition

Credit impairment Handbook US GAAP March 2018 kpmg.com/us/frv Contents Foreword... 1 About this publication... 2 1. Executive summary... 4 Subtopic 326-20 2. Scope of Subtopic 326-20... 14 3. Recognition

CIAA Annual Accounting Update

www.pwc.com/ca CIAA Annual Accounting Update October 2017 Agenda for the session Topic Time Breakfast 8:00 8:30 Introductions 8:30 8:45 IFRS 17: Insurance Contracts 8:45 10:00 Break 10:00 10:15 IFRS 9:

www.pwc.com/ca CIAA Annual Accounting Update October 2017 Agenda for the session Topic Time Breakfast 8:00 8:30 Introductions 8:30 8:45 IFRS 17: Insurance Contracts 8:45 10:00 Break 10:00 10:15 IFRS 9:

Understanding IFRS 9 (2014) for Directors By Tan Liong Tong

for Directors By Tan Liong Tong") Understanding IFRS 9 (2014) for Directors By Tan Liong Tong 1. Introduction Many preparers and users of financial statements and other interested parties have expressed concerns that the requirements of

Understanding IFRS 9 (2014) for Directors By Tan Liong Tong 1. Introduction Many preparers and users of financial statements and other interested parties have expressed concerns that the requirements of

Audit Tax Advisory Risk Performance Crowe Horwath LLP 1

PACB Annual Convention FASB s Current Expected Credit Loss (CECL) Model: Navigating the Changes September 28, 2015 Matthew Schell, Partner Crowe Horwath LLP Washington, DC 2015 Crowe Horwath LLP 1 Agenda

PACB Annual Convention FASB s Current Expected Credit Loss (CECL) Model: Navigating the Changes September 28, 2015 Matthew Schell, Partner Crowe Horwath LLP Washington, DC 2015 Crowe Horwath LLP 1 Agenda

Media Industry Accounting Group Annual conference 2017

www.pwc.com/miag Media Industry Accounting Group Annual conference 2017 London 15 June 2017 General accounting update Katie Woods UK E: Katie.woods@uk.pwc.com Slide 2 What s new in 2017? Not much again!

www.pwc.com/miag Media Industry Accounting Group Annual conference 2017 London 15 June 2017 General accounting update Katie Woods UK E: Katie.woods@uk.pwc.com Slide 2 What s new in 2017? Not much again!

FASB Financial Instruments Project

FASB Financial Instruments Project June 18, 2013 2:00 3:15 pm Presented by: Jean Joy, CPA Director of Financial Institutions Wolf & Company, P.C. 99 High Street Boston, MA 02110 P: (617) 428-5432 E: jjoy@wolfandco.com

FASB Financial Instruments Project June 18, 2013 2:00 3:15 pm Presented by: Jean Joy, CPA Director of Financial Institutions Wolf & Company, P.C. 99 High Street Boston, MA 02110 P: (617) 428-5432 E: jjoy@wolfandco.com

IFRS Update of standards and interpretations in issue at 30 June 2015

IFRS Update of standards and interpretations in issue at 30 June 2015 Contents Introduction 2 Section 1: New pronouncements issued as at 30 June 2015 4 Table of mandatory application 4 IFRS 9 Financial

IFRS Update of standards and interpretations in issue at 30 June 2015 Contents Introduction 2 Section 1: New pronouncements issued as at 30 June 2015 4 Table of mandatory application 4 IFRS 9 Financial

Global Financial Reporting.

Asia Pacific Dbriefs Presents: Global Financial Reporting. IFRS: Important Developments Joel Osnoss / Randall Sogoloff / Andrew Spooner 18 January 2012 Agenda Updated IASB work plan IFRS developments Financial

Asia Pacific Dbriefs Presents: Global Financial Reporting. IFRS: Important Developments Joel Osnoss / Randall Sogoloff / Andrew Spooner 18 January 2012 Agenda Updated IASB work plan IFRS developments Financial

AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL INFORMATION (UNAUDITED) 30 SEPTEMBER 2018

30 SEPTEMBER 2018") AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 INTERIM CONDENSED CONSOLIDATED INCOME STATEMENT (UNAUDITED) For the period ended 2018

AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 INTERIM CONDENSED CONSOLIDATED INCOME STATEMENT (UNAUDITED) For the period ended 2018

FASB Insurance Contracts

GAAP and SEC Update FASB Insurance Contracts FASB Initiatives Short-Duration Contracts (Final Standard ASU 2015-09 Issued May 2015) Long-Duration Contracts (Beginning) Focused efforts on targeted improvements

GAAP and SEC Update FASB Insurance Contracts FASB Initiatives Short-Duration Contracts (Final Standard ASU 2015-09 Issued May 2015) Long-Duration Contracts (Beginning) Focused efforts on targeted improvements

IFRS 9 Financial Instruments Thai General Assurance Association

IFRS 9 Financial Instruments Thai General Assurance Association 9 March 2017 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

IFRS 9 Financial Instruments Thai General Assurance Association 9 March 2017 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

IFRSs, IFRICs AND AMENDMENTS AVAILABLE FOR EARLY ADOPTION FOR 31 DECEMBER 2016 YEAR ENDS

IFRSs, IFRICs AND AMENDMENTS AVAILABLE FOR EARLY ADOPTION FOR 31 DECEMBER 2016 YEAR ENDS INTERNATIONAL FINANCIAL REPORTING BULLETIN 2017/05 IFRSs, IFRICs and amendments available for early adoption for

IFRSs, IFRICs AND AMENDMENTS AVAILABLE FOR EARLY ADOPTION FOR 31 DECEMBER 2016 YEAR ENDS INTERNATIONAL FINANCIAL REPORTING BULLETIN 2017/05 IFRSs, IFRICs and amendments available for early adoption for

Implementing IFRS 9: a guide for lessors

Implementing IFRS 9: a guide for lessors Implementing IFRS 9: a guide for lessors IFRS 9 brings together the classification and measurement, impairment and hedge accounting sections of the IASB s project

Implementing IFRS 9: a guide for lessors Implementing IFRS 9: a guide for lessors IFRS 9 brings together the classification and measurement, impairment and hedge accounting sections of the IASB s project

Technical Line FASB final guidance

No. 2018-09 4 October 2018 Technical Line FASB final guidance What s changing under the new standard on credit losses? In this issue: Overview... 1 Key considerations... 2 Effective date and transition...

No. 2018-09 4 October 2018 Technical Line FASB final guidance What s changing under the new standard on credit losses? In this issue: Overview... 1 Key considerations... 2 Effective date and transition...

EY IFRS Core Tools. IFRS Update of standards and interpretations in issue at 31 December 2014

EY IFRS Core Tools IFRS Update of standards and interpretations in issue at 31 December 2014 Contents Introduction 2 Section 1: New pronouncements issued as at 31 December 2014 4 Table of mandatory application

EY IFRS Core Tools IFRS Update of standards and interpretations in issue at 31 December 2014 Contents Introduction 2 Section 1: New pronouncements issued as at 31 December 2014 4 Table of mandatory application

Good General Insurance (International) Limited

Limited") Good General Insurance (International) Limited Selected Illustrative disclosures for IFRS 17 Insurance Contracts (Premium allocation approach), IFRS 9 Financial Instruments and IFRS 7 Financial Instruments:

Good General Insurance (International) Limited Selected Illustrative disclosures for IFRS 17 Insurance Contracts (Premium allocation approach), IFRS 9 Financial Instruments and IFRS 7 Financial Instruments:

Financial Instruments IND AS 109

Financial Instruments IND AS 109 Study Group Meeting of CTC 13 June 2017 Agenda Introduction Classification and measurement Expected credit losses (ECL) Page 1 14 June 2017 IFRS 9 Financial Instruments

Financial Instruments IND AS 109 Study Group Meeting of CTC 13 June 2017 Agenda Introduction Classification and measurement Expected credit losses (ECL) Page 1 14 June 2017 IFRS 9 Financial Instruments

IAS 32 & IFRS 9 Financial Instruments

Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 & IFRS 9 Financial Instruments Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 Financial

Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 & IFRS 9 Financial Instruments Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 Financial

Credit impairment under ASC 326

Financial reporting developments A comprehensive guide Credit impairment under ASC 326 Recognizing credit losses on financial assets measured at amortized cost, AFS debt securities and certain beneficial

Financial reporting developments A comprehensive guide Credit impairment under ASC 326 Recognizing credit losses on financial assets measured at amortized cost, AFS debt securities and certain beneficial

IFRSs, IFRICs AND AMENDMENTS AVAILABLE FOR EARLY ADOPTION FOR 31 DECEMBER 2015 YEAR ENDS

IFRSs, IFRICs AND AMENDMENTS AVAILABLE FOR EARLY ADOPTION FOR 31 DECEMBER 2015 YEAR ENDS INTERNATIONAL FINANCIAL REPORTING BULLETIN 2016/02 IFRSs, IFRICs and amendments available for early adoption for

IFRSs, IFRICs AND AMENDMENTS AVAILABLE FOR EARLY ADOPTION FOR 31 DECEMBER 2015 YEAR ENDS INTERNATIONAL FINANCIAL REPORTING BULLETIN 2016/02 IFRSs, IFRICs and amendments available for early adoption for

Technical Line FASB final guidance

No. 2017-09 16 March 2017 Technical Line FASB final guidance How the new credit impairment standard will affect entities outside the financial services industry In this issue: Overview... 1 Key considerations...

No. 2017-09 16 March 2017 Technical Line FASB final guidance How the new credit impairment standard will affect entities outside the financial services industry In this issue: Overview... 1 Key considerations...

IFRS Project Insights Financial Instruments: Classification and Measurement

IFRS Project Insights Financial Instruments: Classification and Measurement 2 October 2012 The IASB s financial instrument project will replace IAS 39 Financial Instruments: Recognition and Measurement.

IFRS Project Insights Financial Instruments: Classification and Measurement 2 October 2012 The IASB s financial instrument project will replace IAS 39 Financial Instruments: Recognition and Measurement.

EMIRATES NBD BANK PJSC

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

EMIRATES NBD BANK PJSC

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE THREE MONTHS PERIOD ENDED 31 MARCH 2018 GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE THREE MONTHS PERIOD ENDED 31 MARCH 2018 GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

Instruments-Classification. Measurement and Impairment. Credibility. Professionalism. AccountAbility

IFRS IFRS 139 Fair Financial Value Instruments-Classification Measurement and Impairment Credibility. Professionalism. AccountAbility Agenda Adoption permutations Scope of the standard Definitions Classification

IFRS IFRS 139 Fair Financial Value Instruments-Classification Measurement and Impairment Credibility. Professionalism. AccountAbility Agenda Adoption permutations Scope of the standard Definitions Classification

Financial Instruments

Financial Instruments A summary of IFRS 9 and its effects March 2017 IFRS 9 Financial Instruments Roadmap financial assets Debt (including hybrid contracts) Derivatives Equity (at instrument level) Pass

Financial Instruments A summary of IFRS 9 and its effects March 2017 IFRS 9 Financial Instruments Roadmap financial assets Debt (including hybrid contracts) Derivatives Equity (at instrument level) Pass

BFRS 9 Financial Instruments Overview and Key Changes from Current Standard and Requirements. 28 April 2016

BFRS 9 Financial Instruments Overview and Key Changes from Current Standard and Requirements 28 April 2016 Why is BFRS 9 Important? BFRS 9 will impact all entities, but especially banks, insurers and other

BFRS 9 Financial Instruments Overview and Key Changes from Current Standard and Requirements 28 April 2016 Why is BFRS 9 Important? BFRS 9 will impact all entities, but especially banks, insurers and other

ANNOUNCEMENT. Subject: Financial Results of the Group of Hellenic Bank Public Company Ltd for the six-month period ended 30 th June 2018

10 th September, 2018 ANNOUNCEMENT Subject: Financial Results of the Group of Hellenic Bank Public Company Ltd for the six-month period ended 30 th June 2018 Hellenic Bank Public Company Ltd (the Bank

10 th September, 2018 ANNOUNCEMENT Subject: Financial Results of the Group of Hellenic Bank Public Company Ltd for the six-month period ended 30 th June 2018 Hellenic Bank Public Company Ltd (the Bank

THE POWER OF BEING UNDERSTOOD AUDIT TAX CONSULTING

THE POWER OF BEING UNDERSTOOD AUDIT TAX CONSULTING This slide presentation has been prepared for general guidance only, and does not constitute professional advice. You should not act upon the information

THE POWER OF BEING UNDERSTOOD AUDIT TAX CONSULTING This slide presentation has been prepared for general guidance only, and does not constitute professional advice. You should not act upon the information

FASB/IASB/SEC Update. American Accounting Association. Tom Linsmeier FASB Member August 4, 2014

American Accounting Association FASB/IASB/SEC Update Tom Linsmeier FASB Member August 4, 2014 The views expressed in this presentation are those of the presenter. Official positions of the FASB are reached

American Accounting Association FASB/IASB/SEC Update Tom Linsmeier FASB Member August 4, 2014 The views expressed in this presentation are those of the presenter. Official positions of the FASB are reached

EY IFRS Core Tools IFRS Update

EY IFRS Core Tools IFRS Update of standards and interpretations in issue at 31 August 2014 Contents Introduction 2 Section 1: New pronouncements issued as at 31 August 2014 4 Table of mandatory application

EY IFRS Core Tools IFRS Update of standards and interpretations in issue at 31 August 2014 Contents Introduction 2 Section 1: New pronouncements issued as at 31 August 2014 4 Table of mandatory application

EMIRATES NBD BANK PJSC

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE NINE MONTHS PERIOD ENDED 30 SEPTEMBER GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE NINE MONTHS PERIOD ENDED 30 SEPTEMBER GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

FINANCIAL INSTRUMENTS. The future of IFRS financial instruments accounting IFRS NEWSLETTER

IFRS NEWSLETTER FINANCIAL INSTRUMENTS Issue 4, July 2012 In July, differences in approach emerged between the IASB and FASB on the way forward to achieving a converged impairment model; these are a cause

IFRS NEWSLETTER FINANCIAL INSTRUMENTS Issue 4, July 2012 In July, differences in approach emerged between the IASB and FASB on the way forward to achieving a converged impairment model; these are a cause

First Impressions: IFRS 9 Financial Instruments

IFRS First Impressions: IFRS 9 Financial Instruments September 2014 kpmg.com/ifrs Contents Fundamental changes call for careful planning 2 Setting the standard 3 1 Key facts 4 2 How this could impact you

IFRS First Impressions: IFRS 9 Financial Instruments September 2014 kpmg.com/ifrs Contents Fundamental changes call for careful planning 2 Setting the standard 3 1 Key facts 4 2 How this could impact you

Navigating the changes to New Zealand Equivalents to International Financial Reporting Standards

Navigating the changes to New Zealand Equivalents to International Financial Reporting Standards Contents Overview 3 Effective dates of new standards, interpretations and amendments (issued as at 31 Dec

Navigating the changes to New Zealand Equivalents to International Financial Reporting Standards Contents Overview 3 Effective dates of new standards, interpretations and amendments (issued as at 31 Dec

FINANCIAL INSTRUMENTS. The future of IFRS financial instruments accounting IFRS NEWSLETTER

IFRS NEWSLETTER FINANCIAL INSTRUMENTS Issue 20, February 2014 All the due process requirements for IFRS 9 have been met, and a final standard with an effective date of 1 January 2018 is expected in mid-2014.

IFRS NEWSLETTER FINANCIAL INSTRUMENTS Issue 20, February 2014 All the due process requirements for IFRS 9 have been met, and a final standard with an effective date of 1 January 2018 is expected in mid-2014.

FINANCIAL REPORTING WORKSHOP **IFRS 9: FINANCIAL INSTRUMENTS** Presentation by: CPA Boniface L Souza, ACIM, CFIP Wednesday, 15 th November 2017

FINANCIAL REPORTING WORKSHOP **IFRS 9: FINANCIAL INSTRUMENTS** Presentation by: CPA Boniface L Souza, ACIM, CFIP Wednesday, 15 th November 2017 Uphold public interest Agenda Why the transition to IFRS

FINANCIAL REPORTING WORKSHOP **IFRS 9: FINANCIAL INSTRUMENTS** Presentation by: CPA Boniface L Souza, ACIM, CFIP Wednesday, 15 th November 2017 Uphold public interest Agenda Why the transition to IFRS

Acumen Financial Institutions Accounting and Reporting. IFRS 9 Financial Instruments Classification 9 June 2015

Acumen 2015 Financial Institutions Accounting and Reporting IFRS 9 Financial Instruments Classification 9 June 2015 About the presenters Presenter 1 George W. Prieksaitis Partner +1 416 943 2542 george.w.prieksaitis@ca.ey.co

Acumen 2015 Financial Institutions Accounting and Reporting IFRS 9 Financial Instruments Classification 9 June 2015 About the presenters Presenter 1 George W. Prieksaitis Partner +1 416 943 2542 george.w.prieksaitis@ca.ey.co

Quarterly Accounting Update: On the Horizon

Quarterly Accounting Update: On the Horizon The following selected FASB exposure drafts and projects are outstanding as of June 30, 2015. FASB Simplification Initiative The FASB s Simplification Initiative

Quarterly Accounting Update: On the Horizon The following selected FASB exposure drafts and projects are outstanding as of June 30, 2015. FASB Simplification Initiative The FASB s Simplification Initiative

Financial Instruments. October 2015 Slide 2

Presented by: Cost transaction price (in general) Amortised Cost (B/s) EIR - Effective interest method (I/s) OCI - Other Comprehensive Income FVTPL Fair value through profit or loss FVOCI Fair value through

Presented by: Cost transaction price (in general) Amortised Cost (B/s) EIR - Effective interest method (I/s) OCI - Other Comprehensive Income FVTPL Fair value through profit or loss FVOCI Fair value through

AN OFFERING FROM BDO S NATIONAL ASSURANCE PRACTICE SIGNIFICANT ACCOUNTING & REPORTING MATTERS

AN OFFERING FROM BDO S NATIONAL ASSURANCE PRACTICE SIGNIFICANT ACCOUNTING & REPORTING MATTERS Significant Accounting & Reporting Matters Second Quarter 2011 1 FIRST QUARTER 2016 BDO is the brand name for

AN OFFERING FROM BDO S NATIONAL ASSURANCE PRACTICE SIGNIFICANT ACCOUNTING & REPORTING MATTERS Significant Accounting & Reporting Matters Second Quarter 2011 1 FIRST QUARTER 2016 BDO is the brand name for

BANCO DE BOGOTA (NASSAU) LIMITED Financial Statements

LIMITED Financial Statements") Financial Statements Page Independent Auditors Report 1 Statement of Financial Position 3 Statement of Comprehensive Income 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 7-46 Statement

Financial Statements Page Independent Auditors Report 1 Statement of Financial Position 3 Statement of Comprehensive Income 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 7-46 Statement

IFRS 9 Application to banks

IFRS 9 Application to banks May 2017 Agenda Introduce IFRS 9 Financial Instruments as applied to banks Focus on impairment Discuss key challenges and milestones 2 Why is there a new standard? IFRS 9 was

IFRS 9 Application to banks May 2017 Agenda Introduce IFRS 9 Financial Instruments as applied to banks Focus on impairment Discuss key challenges and milestones 2 Why is there a new standard? IFRS 9 was

Interim Condensed Consolidated Financial Statements

Interim Condensed Consolidated Financial Statements 31 March 2018 Interim Consolidated Statement of Income Three Months to Three Months to Three Months to Three Months to 31 March 31 March 31 March 31

Interim Condensed Consolidated Financial Statements 31 March 2018 Interim Consolidated Statement of Income Three Months to Three Months to Three Months to Three Months to 31 March 31 March 31 March 31

Ahli United Bank B.S.C.

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 JUNE 2018 INTERIM CONSOLIDATED STATEMENT OF INCOME Six months ended 30 June 30 June 2018 2017 2018 2017 Note USD'000 USD'000 USD'000 USD'000 Interest

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 JUNE 2018 INTERIM CONSOLIDATED STATEMENT OF INCOME Six months ended 30 June 30 June 2018 2017 2018 2017 Note USD'000 USD'000 USD'000 USD'000 Interest

CECL for Commercial Entities

CECL for Commercial Entities St. Louis, MO April 12, 2018 With You Today: Anthony Burzinski Managing Director Accounting Advisory Services KPMG LLP aburzinski@kpmg.com Alan Kuska Director Accounting Advisory

CECL for Commercial Entities St. Louis, MO April 12, 2018 With You Today: Anthony Burzinski Managing Director Accounting Advisory Services KPMG LLP aburzinski@kpmg.com Alan Kuska Director Accounting Advisory

Heads Up. IASB Issues IFRS on Classification and Measurement of Financial Assets.

vember 17, 2009 Volume 16, Issue 42 Heads Up In This Issue: Introduction Scope Classification Classification Criteria Equity Investments Embedded Derivatives Application Issues Reclassification Impact

vember 17, 2009 Volume 16, Issue 42 Heads Up In This Issue: Introduction Scope Classification Classification Criteria Equity Investments Embedded Derivatives Application Issues Reclassification Impact

Good Bank (International) Limited. Illustrative disclosures for IFRS 9 impairment and transition

Limited. Illustrative disclosures for IFRS 9 impairment and transition") Good Bank (International) Limited Illustrative disclosures for IFRS 9 impairment and transition Contents ABBREVIATIONS AND KEY...2 INTRODUCTION...3 CONSOLIDATED INCOME STATEMENT...4 CONSOLIDATED STATEMENT

Good Bank (International) Limited Illustrative disclosures for IFRS 9 impairment and transition Contents ABBREVIATIONS AND KEY...2 INTRODUCTION...3 CONSOLIDATED INCOME STATEMENT...4 CONSOLIDATED STATEMENT

IFRS 9 Financial Instruments for broker-dealers

IFRS 9 Financial Instruments for broker-dealers IFRS 9 Financial Instruments for broker-dealers 1 Overview 09 10 11 12 13 14 2015 2016 2017 2018 IASB Exposure Draft (ED) 1 Final IFRS 9 Standard * GPPC

IFRS 9 Financial Instruments for broker-dealers IFRS 9 Financial Instruments for broker-dealers 1 Overview 09 10 11 12 13 14 2015 2016 2017 2018 IASB Exposure Draft (ED) 1 Final IFRS 9 Standard * GPPC

Arab Banking Corporation (B.S.C.)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL 31 MARCH 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Threemonth period ended All figures in US$ Million Reviewed Three months ended

INTERIM CONDENSED CONSOLIDATED FINANCIAL 31 MARCH 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Threemonth period ended All figures in US$ Million Reviewed Three months ended

ECOBANK TRANSNATIONAL INCORPORATED. Condensed Unaudited Consolidated Interim Financial Statements

ECOBANK TRANSNATIONAL INCORPORATED For period ended 30 June 2018 For the period ended 30 June 2018 CONTENTS Condensed unaudited consolidated interim financial statements: Press release Condensed unaudited

ECOBANK TRANSNATIONAL INCORPORATED For period ended 30 June 2018 For the period ended 30 June 2018 CONTENTS Condensed unaudited consolidated interim financial statements: Press release Condensed unaudited

Applying IFRS 9 Part II (Discussion) Presentation by: CPA Stephen Obock February 2018

Presentation by: CPA Stephen Obock February 2018") Applying IFRS 9 Part II (Discussion) Presentation by: CPA Stephen Obock February 2018 Uphold public interest IFRS 9 Discussion and illustrations on the key changes? Presentation agenda Introduction Classification

Applying IFRS 9 Part II (Discussion) Presentation by: CPA Stephen Obock February 2018 Uphold public interest IFRS 9 Discussion and illustrations on the key changes? Presentation agenda Introduction Classification

Financial instruments: FASB issues standard on recognition and measurement

Financial instruments: FASB issues standard on recognition and measurement Prepared by: Faye Miller, Partner, National Professional Standards Group, RSM US LLP faye.miller@rsmus.com, +1 410 246 9194 January

Financial instruments: FASB issues standard on recognition and measurement Prepared by: Faye Miller, Partner, National Professional Standards Group, RSM US LLP faye.miller@rsmus.com, +1 410 246 9194 January

Arab Banking Corporation (B.S.C.)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Ninemonth period ended Reviewed Three months ended Nine months ended 30 September

INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Ninemonth period ended Reviewed Three months ended Nine months ended 30 September

IFRS 9 for Financial Services Presentation and Disclosure. Ulana Oswald Senior Manager. December 9, 2015

IFRS 9 for Financial Services Presentation and Disclosure Ulana Oswald Senior Manager December 9, 2015 Presentation and Disclosure: Classification and Measurement Page 1 Classification and measurement

IFRS 9 for Financial Services Presentation and Disclosure Ulana Oswald Senior Manager December 9, 2015 Presentation and Disclosure: Classification and Measurement Page 1 Classification and measurement

First Quarter Financial Report For the period ended June 30, 2018

First Quarter Financial Report -19 For the period ended Farm Credit Canada Farm Credit Canada (FCC) is a financially self-sustaining federal Crown corporation, reporting to Canadians and Parliament through

First Quarter Financial Report -19 For the period ended Farm Credit Canada Farm Credit Canada (FCC) is a financially self-sustaining federal Crown corporation, reporting to Canadians and Parliament through

IFRS 9 The final standard

EUROMONEY CREDIT RESEARCH POLL: Please participate. Click on http://www.euromoney.com/fixedincome2015 to take part in the online survey. IFRS 9 The final standard In July 2014, the International Accounting

EUROMONEY CREDIT RESEARCH POLL: Please participate. Click on http://www.euromoney.com/fixedincome2015 to take part in the online survey. IFRS 9 The final standard In July 2014, the International Accounting

ACCOUNTING STANDARDS UPDATE

ACCOUNTING STANDARDS UPDATE Gordon J. Dobner, CPA, Partner BKD, LLP gdobner@bkd.com 713-499-4605 Objectives: 1. Review significant upcoming new accounting standards 2. Examine the level of potential impact

ACCOUNTING STANDARDS UPDATE Gordon J. Dobner, CPA, Partner BKD, LLP gdobner@bkd.com 713-499-4605 Objectives: 1. Review significant upcoming new accounting standards 2. Examine the level of potential impact

IFRS 9 - Preliminary Plan

IFRS 9 - Preliminary Plan Safest road to compliance BCC recommended implementation approach Presented by Antoine Wakim Timeline - IFRS 9 enhancement project Nov 2009 Classification and Measurement (C&M)

IFRS 9 - Preliminary Plan Safest road to compliance BCC recommended implementation approach Presented by Antoine Wakim Timeline - IFRS 9 enhancement project Nov 2009 Classification and Measurement (C&M)

Neo Solar Power Corp. and Subsidiaries

Neo Solar Power Corp. and Subsidiaries Consolidated Financial Statements for the Three Months Ended and and Independent Auditors Review Report NEO SOLAR POWER CORP. AND SUBSIDIARIES CONSOLIDATED BALANCE

Neo Solar Power Corp. and Subsidiaries Consolidated Financial Statements for the Three Months Ended and and Independent Auditors Review Report NEO SOLAR POWER CORP. AND SUBSIDIARIES CONSOLIDATED BALANCE

Get ready for FRS 109: Classifying and measuring financial instruments. July 2018

Get ready for FRS 109: Classifying and measuring financial instruments July 2018 Contents Preface 03 1 Overview of classification and measurement requirements 04 2 The business model test 06 2.1 Determining

Get ready for FRS 109: Classifying and measuring financial instruments July 2018 Contents Preface 03 1 Overview of classification and measurement requirements 04 2 The business model test 06 2.1 Determining

IFRS Update of standards and interpretations in issue at 31 March 2016

IFRS Update of standards and interpretations in issue at 31 March 2016 Contents Introduction 2 Section 1: New pronouncements issued as at 31 March 2016 4 Table of mandatory application 4 IFRS 9 Financial

IFRS Update of standards and interpretations in issue at 31 March 2016 Contents Introduction 2 Section 1: New pronouncements issued as at 31 March 2016 4 Table of mandatory application 4 IFRS 9 Financial

Unaudited interim condensed financial statements For the nine month period ended 30 th September 2018

interim condensed financial statements For the nine month period ended 30 th September Registered office and principal place of business: Bank Dhofar Building Bank Al Markazi street Post Box 1507,Ruwi

interim condensed financial statements For the nine month period ended 30 th September Registered office and principal place of business: Bank Dhofar Building Bank Al Markazi street Post Box 1507,Ruwi

U.S. GAAP & IFRS: Today and Tomorrow Sept , New York. Financial Instruments

U.S. GAAP & IFRS: Today and Tomorrow Sept. 13-14, 2010 New York Financial Instruments Donald Doran Society of Actuaries US GAAP Seminar Financial Instruments Joint Project September 14, 2010 *connectedthinking

U.S. GAAP & IFRS: Today and Tomorrow Sept. 13-14, 2010 New York Financial Instruments Donald Doran Society of Actuaries US GAAP Seminar Financial Instruments Joint Project September 14, 2010 *connectedthinking

Our Ref.: C/FRSC. Sent electronically through the IASB website ( 19 April 2013

Our Ref.: C/FRSC Sent electronically through the IASB website (www.ifrs.org) 19 April 2013 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sirs, IASB Exposure

Our Ref.: C/FRSC Sent electronically through the IASB website (www.ifrs.org) 19 April 2013 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sirs, IASB Exposure

FASB's new credit impairment model: At a loss for what to do The Dbriefs Financial Executives series

FASB's new credit impairment model: At a loss for what to do The Dbriefs Financial Executives series Bob Uhl, Partner, Deloitte & Touche LLP Jon Howard, Partner, Deloitte & Touche LLP Jonathan Prejean,

FASB's new credit impairment model: At a loss for what to do The Dbriefs Financial Executives series Bob Uhl, Partner, Deloitte & Touche LLP Jon Howard, Partner, Deloitte & Touche LLP Jonathan Prejean,

Ready for New Classification & Measurement Rules for Financial Instruments?

Ready for New Classification & Measurement Rules for Financial Instruments? While the effective date has arrived for public business entities (PBE) to implement Accounting Standards Update (ASU) 2016-01,

Ready for New Classification & Measurement Rules for Financial Instruments? While the effective date has arrived for public business entities (PBE) to implement Accounting Standards Update (ASU) 2016-01,

Accounting Standards Updates ( ASUs ) effective in 2017 for calendar year-end entities:

effective in 2017 for calendar year-end entities:") Accounting Standards Updates ( ASUs ) effective in 2017 for calendar year-end entities: ASU Title Effective in 2017 for Public, Nonpublic, or Both? ASU 2014-10 Development Stage Entities (Topic 915): Elimination

Accounting Standards Updates ( ASUs ) effective in 2017 for calendar year-end entities: ASU Title Effective in 2017 for Public, Nonpublic, or Both? ASU 2014-10 Development Stage Entities (Topic 915): Elimination

IPSAS Update. Task Force on Accounting Standards Meeting. Financial instruments ED 62. Bekzod Rakhimov 2-3 October 2017, Rome

IPSAS Update Financial instruments ED 62 Task Force on Accounting Standards Meeting Bekzod Rakhimov 2-3 October 2017, Rome Background to ED The IPSASB issued IPSAS 28 Financial Instruments: Presentation,

IPSAS Update Financial instruments ED 62 Task Force on Accounting Standards Meeting Bekzod Rakhimov 2-3 October 2017, Rome Background to ED The IPSASB issued IPSAS 28 Financial Instruments: Presentation,

Accounting for Financial Instruments: A Comprehensive Update on the Joint Project

The Dbriefs Financial Reporting series presents: Accounting for Financial Instruments: A Comprehensive Update on the Joint Project Robert Uhl, Partner, Deloitte & Touche LLP Magnus Orrell, Director, Deloitte

The Dbriefs Financial Reporting series presents: Accounting for Financial Instruments: A Comprehensive Update on the Joint Project Robert Uhl, Partner, Deloitte & Touche LLP Magnus Orrell, Director, Deloitte

Voices on Reporting. 18 November KPMG.com/in

Voices on Reporting 18 November 2015 KPMG.com/in Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting

Voices on Reporting 18 November 2015 KPMG.com/in Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting

IFRS update Israel December 2013

www.pwc.com IFRS update Israel December Agenda 1. What s new? 2. Developments at the IASB - Leases - Revenue - Financial instruments - Conceptual framework - Rate regulation 3. Future improvements to IFRSs

www.pwc.com IFRS update Israel December Agenda 1. What s new? 2. Developments at the IASB - Leases - Revenue - Financial instruments - Conceptual framework - Rate regulation 3. Future improvements to IFRSs

CECL Current technical developments Part II

CECL Current technical developments Part II Current Developments in FASB s Current Expected Credit Loss Model December 11, 2018 We will be starting soon Please disable pop-up blocking software before viewing

CECL Current technical developments Part II Current Developments in FASB s Current Expected Credit Loss Model December 11, 2018 We will be starting soon Please disable pop-up blocking software before viewing

Comparison of the FASB s and the IASB s Proposed Models for Financial Instruments (as of May 2010)

") Comparison of the FASB s and the IASB s Proposed Models for Financial Instruments (as of May 2010) The following table provides a side-by-side comparison of the FASB s and the IASB s proposed models for

Comparison of the FASB s and the IASB s Proposed Models for Financial Instruments (as of May 2010) The following table provides a side-by-side comparison of the FASB s and the IASB s proposed models for

At the Crossing between Risk and Accounting. Loan-loss Provisioning with Expected Credit Losses

At the Crossing between Risk and Accounting Loan-loss Provisioning with Expected Credit Losses AGENDA 2013 Agenda 1 The role of loan-loss provisioning models during the Crisis 2 3 Expected impacts on the

At the Crossing between Risk and Accounting Loan-loss Provisioning with Expected Credit Losses AGENDA 2013 Agenda 1 The role of loan-loss provisioning models during the Crisis 2 3 Expected impacts on the

Unaudited interim condensed financial statements For the three month period ended 31 st March 2018

interim condensed financial statements For the three month period ended 2018 Registered office and principal place of business: Bank Dhofar Building Bank Al Markazi street Post Box 1507,Ruwi Postal Code

interim condensed financial statements For the three month period ended 2018 Registered office and principal place of business: Bank Dhofar Building Bank Al Markazi street Post Box 1507,Ruwi Postal Code

Financial instruments: FASB standard on recognition and measurement

Financial instruments: FASB standard on recognition and measurement Prepared by: Faye Miller, Partner, National Professional Standards Group, RSM US LLP faye.miller@rsmus.com, +1 410 246 9194 Updated April

Financial instruments: FASB standard on recognition and measurement Prepared by: Faye Miller, Partner, National Professional Standards Group, RSM US LLP faye.miller@rsmus.com, +1 410 246 9194 Updated April

Financial Instruments Impairment

Financial Instruments Impairment SPECIAL REPORT New Product or Service of the Year Content Content Marketing Solution 2 Financial Instruments Impairment Financial Instruments Impairment Financial instruments

Financial Instruments Impairment SPECIAL REPORT New Product or Service of the Year Content Content Marketing Solution 2 Financial Instruments Impairment Financial Instruments Impairment Financial instruments