IFRS 9 FINANCIAL INSTRUMENTS

|

|

|

- Laurence Chase

- 6 years ago

- Views:

Transcription

1 IFRS 9 FINANCIAL INSTRUMENTS Uphold public interest CPA WILFRED OWALLA

2 Why the New Standard? IFRS 9 responds to criticisms that IAS 39 is too complex, inconsistent with the way entities manage their businesses and risks, and defers the recognition of credit losses on loans and receivables until too late in the credit cycle.

3 CLASSIFICATION AND MEASUREMENT OF FINANCIAL ASSETS 3

4 MAJOR CHANGES IAS 39 Categories Held to maturity investments Loans and receivables IFRS 9 Categories Amortized cost FVOCI FVTPL FVTPL Available-for-sale financial assets

5 MAJOR CHANGES

6 Classification Basis Under IAS 39, classification of financial assets is mostly based on specific definitions for each category which then determines the measurement. Under IFRS 9, classification categories are aligned with the measurement which enhances simplicity. Classification of financial assets is also more principle based and depends on two assessments: Entity s business model for managing the financial asset. ( Business Model Test ); Financial asset s contractual cash flow characteristics. (Cash Flow Characteristics Test ).

7 Business Model IFRS 9 uses the term in relation to how financial assets are managed and extent to which cash flows will result from collecting contractual cash flows, selling financial assets or both Two business models are positively defined: a hold to collect business model a hold to collect and sell business model Debt-type financial assets that are not managed under either of these models will need to be measured at fair value through profit or loss

8 Determining the Business Model An entity s business model refers to how an entity manages its financial assets in order to generate cash flows. Business Model is determined by entity s key management personnel. how performance is evaluated and reported to entity s key management personnel risks affecting performance of business model and how those risks are managed how managers of business are compensated (eg whether compensation is based on fair value of assets managed or on contractual cash flows collected).

9 Level of Determination An entity s business model is determined at a level that reflects how groups of financial assets are managed together to achieve a particular business objective. Accordingly, assessment does not depend on management s intentions for individual instruments. Also, for IFRS 9 purposes, an entity can have more than one business model.

10 example An entity holding a portfolio of mortgage loans may manage some of the loans to collect contractual cash flows while having an objective of selling other loans within the portfolio in the near term. The portfolio would be sub-divided, with part of it being accounted for under a hold to collect business model while the other loans are accounted for at fair value through profit or loss.

11 Hold to collect business model A hold to collect business model is one in which assets are managed to realize cash flows by collecting contractual payments over the instruments lives. In determining whether cash flows are going to be realized by collecting the financial assets contractual payments, it is necessary to consider: frequency, value and timing of sales in prior periods reasons for those sales and expectations about future sales activity. Objective collect contractual payments over life of the instrument entity manages the assets held within the portfolio to collect those particular contractual cash flows

12 Hold to collect and sell business model Key management personnel decide that both collecting contractual cash flows and selling financial assets are integral to achieving the objective of the business model. Entities will need to exercise an element of judgement because there is no threshold for frequency or value of sales that must occur in this business model. However, this business model will typically involve greater frequency and value of sales than a hold to collect model selling financial assets is integral to achieving business model s objective instead of being only incidental to it.

13 Other business models If a debt-type financial asset is not held within either a hold to collect business model or a hold to collect and sell business model, then it will be measured at fair value through profit or loss. IFRS 9 gives a number of examples of models which will result in fair value through profit or loss measurement, including business models in which: entity manages financial assets with the objective of realizing cash flows through the sale of the assets entity manages and evaluates a portfolio of financial assets on a fair value basis a portfolio of financial assets that meets the definition of held for trading is not held to collect contractual cash flows or held both to collect contractual cash flows and to sell financial assets.

14 Model Hold to collect contractual cash flows Hold to collect contractual cash flows and to sell Other (not defined Possible examples trade receivables originated loans and debt securities held to maturity liquidity portfolio assets held by an insurer to back insurance liabilities trading portfolios assets managed on a fair value basis

15 Contractual cash flows characteristics test The contractual cash flow characteristics test is the second of the two tests that determine the classification of a financial asset. For the test to be met, the contractual terms of the financial asset must give rise on specified dates to cash flows that are solely payments of principal and interest. It is only possible to classify a financial asset in the amortised cost or fair value through other comprehensive income category where the test is met.

16 SPPI INTEREST TEST Principal For the purpose of applying this test, principal is the fair value of the financial asset at initial recognition. The Standard acknowledges however that the principal amount may change over the life of the financial asset, for example as a result of repayments of principal Interest Interest consists of consideration for: the time value of money the credit risk associated with the principal amount outstanding during a particular period of time other basic lending risks and costs a profit margin.

17 Classification Decision Tree

18 Categories Conditions to be Met Impact Amortized Cost Financial asset is held within a business model whose objective is to hold financial assets in order to collect contractual cash flows ( Business Model test ). The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding ( SPPI contractual cash flow characteristics test ). (IFRS ) Investments classified as held to maturity under IAS 39 and measured at amortized cost will likely fall into this category. This category will also contain other debt investments, which are classified as loans and receivables under IAS 39, if it meets the SPPI contractual cash flow characteristics and business model test.

19 Categories Conditions to be Met Impact FVOCI Financial asset is held within a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets ( business model test ). Contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding ( SPPI contractual cash flow characteristics test ). Entity may, at initial recognition, make an irrevocable election to present in OCI subsequent changes in the fair value of an investment in an equity instrument within the scope of IFRS 9 (IFRS A & IFRS Although debt investments and equity investments that are designated at FVOCI could fall into this category, the measurement for such debt and equity investments are different as demonstrated in the decision tree above.

20 Categories Conditions to be Met Impact FVTPL A financial asset shall be measured at FVTPL unless it is measured at amortized cost or at FVOCI. An entity may, at initial recognition, irrevocably designate a financial asset as measured at FVTPL if doing so eliminates or significantly reduces a measurement or recognition inconsistency ( accounting mismatch ) that would otherwise arise from measuring assets or liabilities or recognizing the gains and losses on them on different bases. Derivatives and held for trading investments will fall into this category as under IAS 39. In addition, some loans and receivables and equity investments (which under IAS 39 are measured at amortized cost or classified as availablefor-sale and carried at cost or FVOCI respectively), may also fall into this category. IAS 39 contains two other instances where a FVTPL designation can be made. These designations disappear under IFRS 9 because of the new classification model and further simplifies the financial instrument accounting requirements. The available-for-sale category under

21 Investments in Private Entities Measured at Cost Under IAS 39 IAS 39 allows certain equity investments to be measured at cost. Specifically, when: There is no quoted market price in an active market; and Fair value cannot be reliably measured because either: Variability in the range of reasonable fair value estimates is significant; Probabilities of the various estimates within the range cannot be reasonably assessed and used in estimating fair value. IFRS 9 requires that all investments in equity instruments be measured at fair value. IFRS 9 mentions that in limited circumstances cost may approximate fair value, for example, when: Insufficient more recent information is available to measure fair value; or There is a wide range of possible fair value measurements and cost represents the best estimate of fair value in the range.

22 Classification and Measurement of Financial Liabilities IFRS 9 requirements for the classification and measurement of financial liabilities are substantially unchanged from IAS 39 except for the following: Removal of the cost exception for derivative financial liabilities. Changes in fair value as a result of an entity s own credit risk are recognized in OCI. Overall, financial liabilities are still measured at amortized cost except for: Financial liabilities measured at FVTPL (i.e., those held for trading, designated at FVTPL or contingent consideration recognized by an acquirer in a business combination). Loan commitments and financial guarantee contracts for which specific measurement guidance exists.

23 Impairment Accounting for impairments is the second major area of fundamental change: Investments in equity instruments. On the one hand, IFRS 9 eliminates impairment assessment requirements for investments in equity instruments because, as indicated above, they now can only be measured at FVPL or FVOCI without recycling of fair value changes to profit and loss. Loans and receivables, including short-term trade receivables. On the other hand, IFRS 9 establishes a new approach for loans and receivables, including trade receivables an expected loss model that focuses on the risk that a loan will default rather than whether a loss has been incurred.

24 Impairment IAS 39 Incurred Loss Model Delays recognition of credit losses until there is objective evidence of impairment. Only past events and current conditions are considered when determining the amount of impairment (i.e., the effects of future credit loss events cannot be considered, even when they are expected). Different impairment models for different financial instruments subject to impairment testing, including equity investments classified as available-forsale. IFRS 9 Expected Credit Loss Model Expected credit losses (ECLs) are recognized at each reporting period, even if no actual loss events have taken place. In addition to past events and current conditions, reasonable and supportable forward-looking information that is available without undue cost or effort is considered in determining impairment. The model will be applied to all financial instruments subject to impairment testing.

25 Expected credit losses Under the expected credit loss model, an entity calculates the allowance for credit losses by considering on a discounted basis the cash shortfalls it would incur in various default scenarios for prescribed future periods and multiplying the shortfalls by the probability of each scenario occurring. IFRS 9 three separate approaches for measuring and recognizing expected credit losses: A general approach that applies to all loans and receivables not eligible for the other approaches; A simplified approach that is required for certain trade receivables and so-called IFRS 15 contract assets and otherwise optional for these assets and lease receivables. A credit adjusted approach that applies to loans that are credit impaired at initial recognition (e.g., loans acquired at a deep discount due to their credit risk).

26 Expected credit losses A distinguishing factor among the approaches is whether the allowance for expected credit losses at any balance sheet date is calculated by considering possible defaults only for the next 12 months ( 12 month ECLs ), or for the entire remaining life of the asset ( Lifetime ECLs ). For those entities which have only short-term receivables less than a year in duration, the simplified and general approach would likely have little practical difference. In all cases, the allowance and any changes to it are recognized by recognizing impairment gains and losses in profit and loss.

27 Overview of Impairment Requirements Under the New IFRS 9 Expected Loss Model

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

Instruments-Classification. Measurement and Impairment. Credibility. Professionalism. AccountAbility

IFRS IFRS 139 Fair Financial Value Instruments-Classification Measurement and Impairment Credibility. Professionalism. AccountAbility Agenda Adoption permutations Scope of the standard Definitions Classification

IFRS IFRS 139 Fair Financial Value Instruments-Classification Measurement and Impairment Credibility. Professionalism. AccountAbility Agenda Adoption permutations Scope of the standard Definitions Classification

Instruments-Possible. Measurement Implementation challenges. Credibility. Professionalism. AccountAbility

IFRS IFRS 139 Fair Financial Value Instruments-Possible Measurement Implementation challenges Credibility. Professionalism. AccountAbility Agenda Adoption permutations Challenges in classification/business

IFRS IFRS 139 Fair Financial Value Instruments-Possible Measurement Implementation challenges Credibility. Professionalism. AccountAbility Agenda Adoption permutations Challenges in classification/business

IFRS 9 for Insurers. Syysseminaari. Aktuaaritoiminnan kehittämissäätiö. 30 November 2017

IFRS 9 for Insurers Syysseminaari Aktuaaritoiminnan kehittämissäätiö 30 November 2017 Agenda 1 Introduction from IAS 39 to IFRS 9 2 Classification 3 Impairment 4 Hedge accounting Page 2 What changes do

IFRS 9 for Insurers Syysseminaari Aktuaaritoiminnan kehittämissäätiö 30 November 2017 Agenda 1 Introduction from IAS 39 to IFRS 9 2 Classification 3 Impairment 4 Hedge accounting Page 2 What changes do

Risk and Accounting. IFRS 9 Financial Instruments. Marco Venuti 2018

Risk and Accounting IFRS 9 Financial Instruments Marco Venuti 2018 Agenda Reasons for issuing IFRS 9 Classification approach by IFRS 9 Classification and Measurement of financial assets Contractual cash

Risk and Accounting IFRS 9 Financial Instruments Marco Venuti 2018 Agenda Reasons for issuing IFRS 9 Classification approach by IFRS 9 Classification and Measurement of financial assets Contractual cash

Overview Why the introduction of IFRS 9?

Overview Why the introduction of IFRS 9? Response to G20 and Financial Stability Board (FSB) 2008 Financial crisis Excessive risk-taking by banks and late recording of impairments on instruments which

Overview Why the introduction of IFRS 9? Response to G20 and Financial Stability Board (FSB) 2008 Financial crisis Excessive risk-taking by banks and late recording of impairments on instruments which

2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

1 Contents Company name: ABC IFRS report: IFRS 9 diagnostic report Month: December 2017 Glossary of abbreviations 3 Background about the entire exercise and how to read the report 4 Disclaimers 5 IFRS

1 Contents Company name: ABC IFRS report: IFRS 9 diagnostic report Month: December 2017 Glossary of abbreviations 3 Background about the entire exercise and how to read the report 4 Disclaimers 5 IFRS

Applying IFRS 9 Part II (Discussion) Presentation by: CPA Stephen Obock February 2018

Presentation by: CPA Stephen Obock February 2018") Applying IFRS 9 Part II (Discussion) Presentation by: CPA Stephen Obock February 2018 Uphold public interest IFRS 9 Discussion and illustrations on the key changes? Presentation agenda Introduction Classification

Applying IFRS 9 Part II (Discussion) Presentation by: CPA Stephen Obock February 2018 Uphold public interest IFRS 9 Discussion and illustrations on the key changes? Presentation agenda Introduction Classification

FINANCIAL REPORTING WORKSHOP **IFRS 9: FINANCIAL INSTRUMENTS** Presentation by: CPA Boniface L Souza, ACIM, CFIP Wednesday, 15 th November 2017

FINANCIAL REPORTING WORKSHOP **IFRS 9: FINANCIAL INSTRUMENTS** Presentation by: CPA Boniface L Souza, ACIM, CFIP Wednesday, 15 th November 2017 Uphold public interest Agenda Why the transition to IFRS

FINANCIAL REPORTING WORKSHOP **IFRS 9: FINANCIAL INSTRUMENTS** Presentation by: CPA Boniface L Souza, ACIM, CFIP Wednesday, 15 th November 2017 Uphold public interest Agenda Why the transition to IFRS

IFRS News. Special Edition on IFRS 9 (2014) IFRS 9 Financial Instruments is now complete

IFRS 9 Financial Instruments is now complete") Special Edition on IFRS 9 (2014) IFRS News IFRS 9 Financial Instruments is now complete Following several years of development, the IASB has finished its project to replace IAS 39 Financial Instruments:

Special Edition on IFRS 9 (2014) IFRS News IFRS 9 Financial Instruments is now complete Following several years of development, the IASB has finished its project to replace IAS 39 Financial Instruments:

IFRS 9 Classification and Measurement Presentation by: CPA Stephen Obock March 2018

IFRS 9 Classification and Measurement Presentation by: CPA Stephen Obock March 2018 Uphold public interest IFRS 9 Classification and Measurement Classification and Similar categories: FVTPL Amortised cost

IFRS 9 Classification and Measurement Presentation by: CPA Stephen Obock March 2018 Uphold public interest IFRS 9 Classification and Measurement Classification and Similar categories: FVTPL Amortised cost

QAU. Alert IN THIS ISSUE. Issue No

QAU Alert Issue No. 02-2015 IN THIS ISSUE In July 2014, the International Accounting Standard Board (IASB) issued the final version of IFRS 9 Financial Instruments that combines together the classification

QAU Alert Issue No. 02-2015 IN THIS ISSUE In July 2014, the International Accounting Standard Board (IASB) issued the final version of IFRS 9 Financial Instruments that combines together the classification

Contents. Financial instruments the complete standard. Fundamental changes call for careful planning. 1. Overview Complete IFRS 9

Financial instruments the complete standard Contents Fundamental changes call for careful planning 1. Overview Complete IFRS 9 2. Classification and measurement Facts 3. Classification and measurement

Financial instruments the complete standard Contents Fundamental changes call for careful planning 1. Overview Complete IFRS 9 2. Classification and measurement Facts 3. Classification and measurement

IFRS 9 Financial Instruments. IICPAK: The Financial Reporting Workshop 4 th and 5 th December 2014 Hilton Hotel, Nairobi

IFRS 9 Financial Instruments IICPAK: The Financial Reporting Workshop 4 th and 5 th December 2014 Hilton Hotel, Nairobi Why are we discussing this topic? Why are we discussing this topic? Area that is

IFRS 9 Financial Instruments IICPAK: The Financial Reporting Workshop 4 th and 5 th December 2014 Hilton Hotel, Nairobi Why are we discussing this topic? Why are we discussing this topic? Area that is

AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL INFORMATION (UNAUDITED) 31 MARCH 2018

31 MARCH 2018") AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL 31 MARCH 2018 INTERIM CONDENSED CONSOLIDATED INCOME STATEMENT (UNAUDITED) For the period ended 31 March

AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL 31 MARCH 2018 INTERIM CONDENSED CONSOLIDATED INCOME STATEMENT (UNAUDITED) For the period ended 31 March

In depth IFRS 9 Impact on the Pharmaceutical Industry December 2017 No. INT

www.pwc.co.uk In depth IFRS 9 Impact on the Pharmaceutical Industry December 2017 No. INT2017-10 Contents Application of IFRS 9 in the pharmaceutical and life sciences industry 1 Introduction a snapshot

www.pwc.co.uk In depth IFRS 9 Impact on the Pharmaceutical Industry December 2017 No. INT2017-10 Contents Application of IFRS 9 in the pharmaceutical and life sciences industry 1 Introduction a snapshot

GAAP & IFRS Updates: What you need to know

GAAP & IFRS Updates: What you need to know Claire Gemmell Account Manager Rhead Hatch Product Owner Learning Objectives Identify differences in the classification and measurement of financial instruments

GAAP & IFRS Updates: What you need to know Claire Gemmell Account Manager Rhead Hatch Product Owner Learning Objectives Identify differences in the classification and measurement of financial instruments

EMIRATES NBD BANK PJSC

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE THREE MONTHS PERIOD ENDED 31 MARCH 2018 GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE THREE MONTHS PERIOD ENDED 31 MARCH 2018 GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

Understanding IFRS 9 (2014) for Directors By Tan Liong Tong

for Directors By Tan Liong Tong") Understanding IFRS 9 (2014) for Directors By Tan Liong Tong 1. Introduction Many preparers and users of financial statements and other interested parties have expressed concerns that the requirements of

Understanding IFRS 9 (2014) for Directors By Tan Liong Tong 1. Introduction Many preparers and users of financial statements and other interested parties have expressed concerns that the requirements of

Acumen Conference IFRS 9 for insurers

Acumen Conference IFRS 9 for insurers December 9, 2015 Agenda Insurer deliberations and implications of IFRS 9 Asset classification: evaluation of business model Impairment model Interplay of IFRS 9 and

Acumen Conference IFRS 9 for insurers December 9, 2015 Agenda Insurer deliberations and implications of IFRS 9 Asset classification: evaluation of business model Impairment model Interplay of IFRS 9 and

IND AS 109 Financial Instruments. 28 March 2015

IND AS 109 Financial Instruments 28 March 2015 Agenda Background Classification and Measurement Expected Credit Losses Hedge accounting Disclosures Business Impacts and Next Steps Key Points to Remember

IND AS 109 Financial Instruments 28 March 2015 Agenda Background Classification and Measurement Expected Credit Losses Hedge accounting Disclosures Business Impacts and Next Steps Key Points to Remember

EMIRATES NBD BANK PJSC

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE NINE MONTHS PERIOD ENDED 30 SEPTEMBER GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE NINE MONTHS PERIOD ENDED 30 SEPTEMBER GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

Putting IFRS 9 into practice Presentation by: CPA Stephen Obock February 2018

Putting IFRS 9 into practice Presentation by: CPA Stephen Obock February 2018 Uphold public interest IFRS 9 What are the key changes? What are the transition requirements? Presentation agenda Introduction

Putting IFRS 9 into practice Presentation by: CPA Stephen Obock February 2018 Uphold public interest IFRS 9 What are the key changes? What are the transition requirements? Presentation agenda Introduction

IFRS 9. Financial instruments for corporates Are you good to go? September kpmg.com/ifrs

IFRS 9 Financial instruments for corporates Are you good to go? September 2017 kpmg.com/ifrs Are you good to go? IFRS 9 will change the way many corporates account for their financial instruments. You

IFRS 9 Financial instruments for corporates Are you good to go? September 2017 kpmg.com/ifrs Are you good to go? IFRS 9 will change the way many corporates account for their financial instruments. You

IAS 32 & IFRS 9 Financial Instruments

Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 & IFRS 9 Financial Instruments Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 Financial

Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 & IFRS 9 Financial Instruments Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 Financial

AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL INFORMATION (UNAUDITED) 30 SEPTEMBER 2018

30 SEPTEMBER 2018") AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 INTERIM CONDENSED CONSOLIDATED INCOME STATEMENT (UNAUDITED) For the period ended 2018

AL AHLI BANK OF KUWAIT K.S.C.P. AND ITS SUBSIDIARIES INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 INTERIM CONDENSED CONSOLIDATED INCOME STATEMENT (UNAUDITED) For the period ended 2018

Arab Banking Corporation (B.S.C.)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL 31 MARCH 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Threemonth period ended All figures in US$ Million Reviewed Three months ended

INTERIM CONDENSED CONSOLIDATED FINANCIAL 31 MARCH 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Threemonth period ended All figures in US$ Million Reviewed Three months ended

An Overview of the Impairment Requirements of IFRS 9 Financial Instruments

An Overview of the Impairment Requirements of IFRS 9 Financial Instruments February 2017 Introduction... 2 Key Differences Between IAS 39 and IFRS 9 Impairment Models... 2 General Impairment Approach...

An Overview of the Impairment Requirements of IFRS 9 Financial Instruments February 2017 Introduction... 2 Key Differences Between IAS 39 and IFRS 9 Impairment Models... 2 General Impairment Approach...

APPLYING IFRS 9 TO RELATED COMPANY LOANS

APPLYING IFRS 9 TO RELATED COMPANY LOANS 2 APPLYING IFRS 9 TO RELATED COMPANY LOANS APPLYING IFRS 9 TO RELATED COMPANY LOANS 3 TABLE OF CONTENTS 1. Introduction 5 2. Common examples and key considerations

APPLYING IFRS 9 TO RELATED COMPANY LOANS 2 APPLYING IFRS 9 TO RELATED COMPANY LOANS APPLYING IFRS 9 TO RELATED COMPANY LOANS 3 TABLE OF CONTENTS 1. Introduction 5 2. Common examples and key considerations

FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED 31 DECEMBER 2017 (WITH INDEPENDENT AUDITORS REPORT THEREON)

") years Bank of Albania FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED 31 DECEMBER 2017 (WITH INDEPENDENT AUDITORS REPORT THEREON) 143 Bank of Albania Bank of Albania 144 years Bank of Albania 145 Bank

years Bank of Albania FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED 31 DECEMBER 2017 (WITH INDEPENDENT AUDITORS REPORT THEREON) 143 Bank of Albania Bank of Albania 144 years Bank of Albania 145 Bank

Good General Insurance (International) Limited

Limited") Good General Insurance (International) Limited Selected Illustrative disclosures for IFRS 17 Insurance Contracts (Premium allocation approach), IFRS 9 Financial Instruments and IFRS 7 Financial Instruments:

Good General Insurance (International) Limited Selected Illustrative disclosures for IFRS 17 Insurance Contracts (Premium allocation approach), IFRS 9 Financial Instruments and IFRS 7 Financial Instruments:

EMIRATES NBD BANK PJSC

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

IFRS 9 The final standard

EUROMONEY CREDIT RESEARCH POLL: Please participate. Click on http://www.euromoney.com/fixedincome2015 to take part in the online survey. IFRS 9 The final standard In July 2014, the International Accounting

EUROMONEY CREDIT RESEARCH POLL: Please participate. Click on http://www.euromoney.com/fixedincome2015 to take part in the online survey. IFRS 9 The final standard In July 2014, the International Accounting

BANQUE SAUDI FRANSI Page 6 NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS For the nine months period ended September 30, 2018 and 20

BANQUE SAUDI FRANSI Page 6 1. General Banque Saudi Fransi (the Bank) is a Saudi Joint Stock Company established by Royal Decree No. M/23 dated Jumada Al Thani 17, 1397H (corresponding to June 4, 1977).

BANQUE SAUDI FRANSI Page 6 1. General Banque Saudi Fransi (the Bank) is a Saudi Joint Stock Company established by Royal Decree No. M/23 dated Jumada Al Thani 17, 1397H (corresponding to June 4, 1977).

Acumen Financial Institutions Accounting and Reporting. IFRS 9 Financial Instruments Classification 9 June 2015

Acumen 2015 Financial Institutions Accounting and Reporting IFRS 9 Financial Instruments Classification 9 June 2015 About the presenters Presenter 1 George W. Prieksaitis Partner +1 416 943 2542 george.w.prieksaitis@ca.ey.co

Acumen 2015 Financial Institutions Accounting and Reporting IFRS 9 Financial Instruments Classification 9 June 2015 About the presenters Presenter 1 George W. Prieksaitis Partner +1 416 943 2542 george.w.prieksaitis@ca.ey.co

Sagicor Real Estate X Fund Limited. Financial Statements 31 December 2014

Financial Statements Draft date: 31/03/2015 Index Page Independent Auditors' Report to the Shareholders Financial Statements Consolidated Statement of Comprehensive Income 1 Consolidated Statement of Financial

Financial Statements Draft date: 31/03/2015 Index Page Independent Auditors' Report to the Shareholders Financial Statements Consolidated Statement of Comprehensive Income 1 Consolidated Statement of Financial

IFRS 9 Financial Instruments

IFRS 9 Financial Instruments 26 October 2018 1 Agenda Overview of requirements of IFRS 9 Incorporation of forward looking information Considerations for modelling Changes in accounting policies and disclosures

IFRS 9 Financial Instruments 26 October 2018 1 Agenda Overview of requirements of IFRS 9 Incorporation of forward looking information Considerations for modelling Changes in accounting policies and disclosures

THE SAUDI INVESTMENT BANK (A Saudi joint stock company)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS For the six-month period ended June 30, 2018 INTERIM CONSOLIDATED STATEMENT OF FINANCIAL POSITION ASSETS Dec. 31, 2018 Notes (Audited) Cash and balances

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS For the six-month period ended June 30, 2018 INTERIM CONSOLIDATED STATEMENT OF FINANCIAL POSITION ASSETS Dec. 31, 2018 Notes (Audited) Cash and balances

Clarien Bank Limited. Consolidated Financial Statements (With Independent Auditors Report Thereon) For the nine months ended September 30, 2018

For the nine months ended September 30, 2018") Clarien Bank Limited Consolidated Financial Statements (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report to the Shareholder 2 Consolidated Statement of Financial

Clarien Bank Limited Consolidated Financial Statements (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report to the Shareholder 2 Consolidated Statement of Financial

Financial Instruments. October 2015 Slide 2

Presented by: Cost transaction price (in general) Amortised Cost (B/s) EIR - Effective interest method (I/s) OCI - Other Comprehensive Income FVTPL Fair value through profit or loss FVOCI Fair value through

Presented by: Cost transaction price (in general) Amortised Cost (B/s) EIR - Effective interest method (I/s) OCI - Other Comprehensive Income FVTPL Fair value through profit or loss FVOCI Fair value through

BANCO DE BOGOTA (NASSAU) LIMITED Financial Statements

LIMITED Financial Statements") Financial Statements Page Independent Auditors Report 1 Statement of Financial Position 3 Statement of Comprehensive Income 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 7-46 Statement

Financial Statements Page Independent Auditors Report 1 Statement of Financial Position 3 Statement of Comprehensive Income 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 7-46 Statement

Disclaimer. HKFRS 9 (2014) Classification and Measurement of Financial Assets and Financial Liabilities

Classification and Measurement of Financial Assets and Financial Liabilities") HKFRS 9 (2014) Classification and Measurement of Financial Assets and Financial Liabilities Date 23 August 2017 Time 19:00 21:00 Venue Duke of Windsor Social Service Building www.zhtraining.com Disclaimer

HKFRS 9 (2014) Classification and Measurement of Financial Assets and Financial Liabilities Date 23 August 2017 Time 19:00 21:00 Venue Duke of Windsor Social Service Building www.zhtraining.com Disclaimer

Financial Instruments

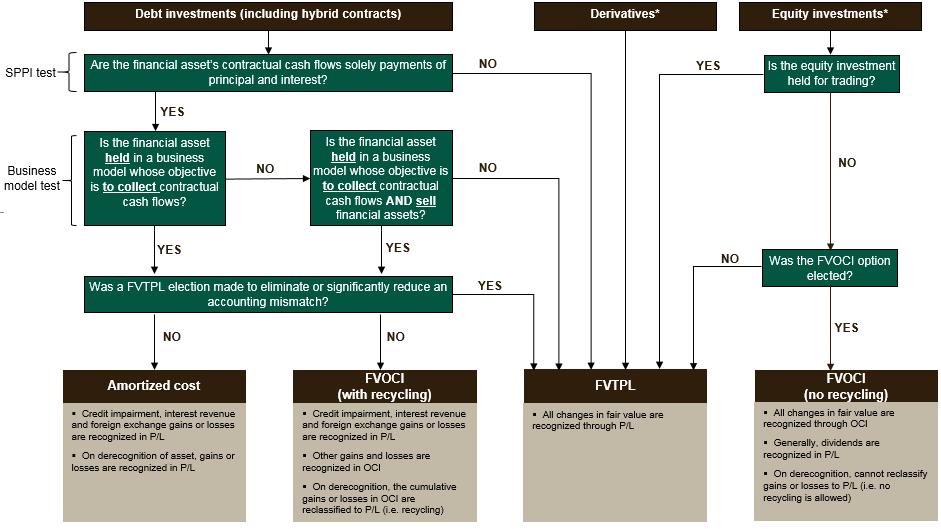

Financial Instruments A summary of IFRS 9 and its effects March 2017 IFRS 9 Financial Instruments Roadmap financial assets Debt (including hybrid contracts) Derivatives Equity (at instrument level) Pass

Financial Instruments A summary of IFRS 9 and its effects March 2017 IFRS 9 Financial Instruments Roadmap financial assets Debt (including hybrid contracts) Derivatives Equity (at instrument level) Pass

Sberbank of Russia and its subsidiaries Interim Condensed Consolidated Financial Statements and Report on Review. 31 March 2018

Sberbank of Russia and its subsidiaries Interim Condensed Consolidated Financial Statements and Report on Review Interim Condensed Consolidated Financial Statements and Report on Review CONTENTS Report

Sberbank of Russia and its subsidiaries Interim Condensed Consolidated Financial Statements and Report on Review Interim Condensed Consolidated Financial Statements and Report on Review CONTENTS Report

Applying IFRS. IFRS 9 for non-financial entities. March 2016

Applying IFRS IFRS 9 for non-financial entities March 2016 Contents 1. Introduction 3 2. Classification of financial instruments 4 2.1 Contractual cash flow characteristics test 5 2.2 Business model assessment

Applying IFRS IFRS 9 for non-financial entities March 2016 Contents 1. Introduction 3 2. Classification of financial instruments 4 2.1 Contractual cash flow characteristics test 5 2.2 Business model assessment

PRESTIGE ASSURANCE PLC THE UNAUDITED FINANCIAL STATEMENTS

PRESTIGE ASSURANCE PLC THE UNAUDITED FINANCIAL STATEMENTS FIRST QUARTER 2018 2 TABLE OF CONTENT Cover Page 1 Table of Content 2 Certification 3 Summary of Significant Accounting Policies 4-33 Financial

PRESTIGE ASSURANCE PLC THE UNAUDITED FINANCIAL STATEMENTS FIRST QUARTER 2018 2 TABLE OF CONTENT Cover Page 1 Table of Content 2 Certification 3 Summary of Significant Accounting Policies 4-33 Financial

FINANCIAL INSTRUMENTS. The future of IFRS financial instruments accounting IFRS NEWSLETTER

IFRS NEWSLETTER FINANCIAL INSTRUMENTS Issue 4, July 2012 In July, differences in approach emerged between the IASB and FASB on the way forward to achieving a converged impairment model; these are a cause

IFRS NEWSLETTER FINANCIAL INSTRUMENTS Issue 4, July 2012 In July, differences in approach emerged between the IASB and FASB on the way forward to achieving a converged impairment model; these are a cause

First Impressions: IFRS 9 Financial Instruments

IFRS First Impressions: IFRS 9 Financial Instruments September 2014 kpmg.com/ifrs Contents Fundamental changes call for careful planning 2 Setting the standard 3 1 Key facts 4 2 How this could impact you

IFRS First Impressions: IFRS 9 Financial Instruments September 2014 kpmg.com/ifrs Contents Fundamental changes call for careful planning 2 Setting the standard 3 1 Key facts 4 2 How this could impact you

Arab Banking Corporation (B.S.C.)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Ninemonth period ended Reviewed Three months ended Nine months ended 30 September

INTERIM CONDENSED CONSOLIDATED FINANCIAL 30 SEPTEMBER 2018 (REVIEWED) INTERIM CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Ninemonth period ended Reviewed Three months ended Nine months ended 30 September

EUROBANK ERGASIAS S.A.

FOR THE THREE MONTHS ENDED 31 MARCH 2018 8 Othonos Street, Athens 105 57, Greece www.eurobank.gr, Tel.: (+30) 210 333 7000 General Commercial Registry Νο: 000223001000 Index to the Condensed Consolidated

FOR THE THREE MONTHS ENDED 31 MARCH 2018 8 Othonos Street, Athens 105 57, Greece www.eurobank.gr, Tel.: (+30) 210 333 7000 General Commercial Registry Νο: 000223001000 Index to the Condensed Consolidated

IFRS 9 Financial Instruments Thai Life Assurance Association

IFRS 9 Financial Instruments Thai Life Assurance Association 13 December 2016 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

IFRS 9 Financial Instruments Thai Life Assurance Association 13 December 2016 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

BANQUE SAUDI FRANSI Page 6 1. General Banque Saudi Fransi (the Bank) is a Saudi Joint Stock Company established by Royal Decree No. M/23 dated Jumada Al Thani 17, 1397H (corresponding to June 4, 1977).

BANQUE SAUDI FRANSI Page 6 1. General Banque Saudi Fransi (the Bank) is a Saudi Joint Stock Company established by Royal Decree No. M/23 dated Jumada Al Thani 17, 1397H (corresponding to June 4, 1977).

IFRS 9 Financial Instruments Thai General Assurance Association

IFRS 9 Financial Instruments Thai General Assurance Association 9 March 2017 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

IFRS 9 Financial Instruments Thai General Assurance Association 9 March 2017 What impact will IFRS 9 have on your business? More data required IFRS 9 More judgment involved Detailed guidance which may

Consolidated Financial Statements For the Year Ended 31 December 2018

Consolidated Financial Statements For the Year Ended 31 December 2018 Consolidated Income Statement 2018 2017 Notes QR000 QR000 Interest Income 25 50,744,709 41,958,662 Interest Expense 26 (31,711,804)

Consolidated Financial Statements For the Year Ended 31 December 2018 Consolidated Income Statement 2018 2017 Notes QR000 QR000 Interest Income 25 50,744,709 41,958,662 Interest Expense 26 (31,711,804)

Arab National Bank. (A Saudi Joint Stock Company) Interim Condensed Consolidated Financial Statements For the period ended 30 June 2018

Interim Condensed Consolidated Financial Statements For the period ended 30 June 2018") Arab National Bank (A Saudi Joint Stock Company) Interim Condensed Consolidated Financial Statements For the period ended 30 June 2018 INTERIM CONSOLIDATED STATEMENT OF FINANCIAL POSITION (SAR 000) As

Arab National Bank (A Saudi Joint Stock Company) Interim Condensed Consolidated Financial Statements For the period ended 30 June 2018 INTERIM CONSOLIDATED STATEMENT OF FINANCIAL POSITION (SAR 000) As

BANK ALJAZIRA (A Saudi Joint Stock Company)

") BANK ALJAZIRA UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE THREE MONTH AND SIX MONTH PERIODS ENDED 30 JUNE 2018 FOR THE SIX MONTH PERIOD ENDED 30 JUNE 2018 1. GENERAL These

BANK ALJAZIRA UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE THREE MONTH AND SIX MONTH PERIODS ENDED 30 JUNE 2018 FOR THE SIX MONTH PERIOD ENDED 30 JUNE 2018 1. GENERAL These

Classification of financial instruments under IFRS 9

Applying IFRS Classification of financial instruments under IFRS 9 May 2015 Contents 1. Introduction... 4 2. Classification of financial assets... 4 2.1 Debt instruments... 5 2.2 Equity instruments and

Applying IFRS Classification of financial instruments under IFRS 9 May 2015 Contents 1. Introduction... 4 2. Classification of financial assets... 4 2.1 Debt instruments... 5 2.2 Equity instruments and

5 MF&G TRUST & FINANCE LIMITED Statement of Profit or Loss and Other Comprehensive Income Nine-month period ended (with comparative period for twelve months ended December 31, 2017) Net interest income

5 MF&G TRUST & FINANCE LIMITED Statement of Profit or Loss and Other Comprehensive Income Nine-month period ended (with comparative period for twelve months ended December 31, 2017) Net interest income

PwC ReportingInBrief. Ind AS 109, Financial Instruments for corporates

PwC ReportingInBrief Ind AS 109, Financial Instruments for corporates In brief India has early adopted IFRS 9, Financial Instruments by notifying the corresponding Ind AS 109, Financial Instruments. Ind

PwC ReportingInBrief Ind AS 109, Financial Instruments for corporates In brief India has early adopted IFRS 9, Financial Instruments by notifying the corresponding Ind AS 109, Financial Instruments. Ind

THE POWER OF BEING UNDERSTOOD AUDIT TAX CONSULTING

THE POWER OF BEING UNDERSTOOD AUDIT TAX CONSULTING This slide presentation has been prepared for general guidance only, and does not constitute professional advice. You should not act upon the information

THE POWER OF BEING UNDERSTOOD AUDIT TAX CONSULTING This slide presentation has been prepared for general guidance only, and does not constitute professional advice. You should not act upon the information

New and revised Standards -Applying IFRS 9 Presentation by: CPA Stephen Obock December 2017

New and revised Standards -Applying IFRS 9 Presentation by: CPA Stephen Obock December 2017 Uphold public interest IFRS 9 What are the key changes? What are the transition requirements? Presentation agenda

New and revised Standards -Applying IFRS 9 Presentation by: CPA Stephen Obock December 2017 Uphold public interest IFRS 9 What are the key changes? What are the transition requirements? Presentation agenda

Good Bank (International) Limited. Illustrative disclosures for IFRS 9 impairment and transition

Limited. Illustrative disclosures for IFRS 9 impairment and transition") Good Bank (International) Limited Illustrative disclosures for IFRS 9 impairment and transition Contents ABBREVIATIONS AND KEY...2 INTRODUCTION...3 CONSOLIDATED INCOME STATEMENT...4 CONSOLIDATED STATEMENT

Good Bank (International) Limited Illustrative disclosures for IFRS 9 impairment and transition Contents ABBREVIATIONS AND KEY...2 INTRODUCTION...3 CONSOLIDATED INCOME STATEMENT...4 CONSOLIDATED STATEMENT

IFRS 9 Classification and Measurement

IFRS 9 Classification and Measurement January 2017 0 Contents Overview of IFRS 9 What s new? Main changes from IAS 39 Classification of financial assets Measurement of financial assets Reclassifications

IFRS 9 Classification and Measurement January 2017 0 Contents Overview of IFRS 9 What s new? Main changes from IAS 39 Classification of financial assets Measurement of financial assets Reclassifications

Financial Instruments IND AS 109

Financial Instruments IND AS 109 Study Group Meeting of CTC 13 June 2017 Agenda Introduction Classification and measurement Expected credit losses (ECL) Page 1 14 June 2017 IFRS 9 Financial Instruments

Financial Instruments IND AS 109 Study Group Meeting of CTC 13 June 2017 Agenda Introduction Classification and measurement Expected credit losses (ECL) Page 1 14 June 2017 IFRS 9 Financial Instruments

INVEST BANK P.S.C. CONDENSED CONSOLIDATED INTERIM FINANCIAL INFORMATION FOR THE THREE MONTH PERIOD ENDED 31 MARCH 2018

INVEST BANK P.S.C. CONDENSED CONSOLIDATED INTERIM FINANCIAL INFORMATION FOR THE THREE MONTH PERIOD ENDED 31 MARCH 2018 . CONDENSED CONSOLIDATED INTERIM FINANCIAL INFORMATION Pages Review report on condensed

INVEST BANK P.S.C. CONDENSED CONSOLIDATED INTERIM FINANCIAL INFORMATION FOR THE THREE MONTH PERIOD ENDED 31 MARCH 2018 . CONDENSED CONSOLIDATED INTERIM FINANCIAL INFORMATION Pages Review report on condensed

Financial instruments IFRS 9 development Project phase Exposure draft Status / next steps 1a. Classification & measurement of financial assets 1b. Cla

www.pwc.com Financial instruments Financial instruments Disclosures Hedging Impairment Derecognition Accounting for financial assets and financial liabilities Compound Instruments Equity or liability Definitions

www.pwc.com Financial instruments Financial instruments Disclosures Hedging Impairment Derecognition Accounting for financial assets and financial liabilities Compound Instruments Equity or liability Definitions

FRS 109 Financial Instruments

FRS 109 Financial Instruments Shirley Ang Partner, Assurance 17 August 2017 Foo Kon Tan LLP. All rights reserved. -1- FRS 109 Financial Instruments FRS 109 Financial Instruments to replace IAS / FRS 39

FRS 109 Financial Instruments Shirley Ang Partner, Assurance 17 August 2017 Foo Kon Tan LLP. All rights reserved. -1- FRS 109 Financial Instruments FRS 109 Financial Instruments to replace IAS / FRS 39

AASB 9: Financial Instruments Transition. Tuesday 20 June 2017

AASB 9: Financial Instruments Transition Tuesday 20 June 2017 Your facilitators are Patricia Stebbens Aaron Laurie Mohamad Shahin Justin Turnbull 2 Agenda Introduction Classification and measurement Impairment

AASB 9: Financial Instruments Transition Tuesday 20 June 2017 Your facilitators are Patricia Stebbens Aaron Laurie Mohamad Shahin Justin Turnbull 2 Agenda Introduction Classification and measurement Impairment

SAUDI INDUSTRIAL SERVICES COMPANY (A SAUDI JOINT STOCK COMPANY) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)") INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) FOR THE THREE MONTH AND SIX MONTH PERIODS ENDED 30 JUNE INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) For the three month

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) FOR THE THREE MONTH AND SIX MONTH PERIODS ENDED 30 JUNE INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) For the three month

ECOBANK TRANSNATIONAL INCORPORATED. Condensed Unaudited Consolidated Interim Financial Statements

ECOBANK TRANSNATIONAL INCORPORATED For period ended 30 June 2018 For the period ended 30 June 2018 CONTENTS Condensed unaudited consolidated interim financial statements: Press release Condensed unaudited

ECOBANK TRANSNATIONAL INCORPORATED For period ended 30 June 2018 For the period ended 30 June 2018 CONTENTS Condensed unaudited consolidated interim financial statements: Press release Condensed unaudited

SEB Group IFRS 15 and IFRS 9 transition disclosures Summary of transition disclosure

SEB Group IFRS 15 and IFRS 9 transition disclosures Summary of transition disclosure This transition document has been created to explain the changes to SEB s financial statements as of 1 2018. These changes

SEB Group IFRS 15 and IFRS 9 transition disclosures Summary of transition disclosure This transition document has been created to explain the changes to SEB s financial statements as of 1 2018. These changes

RIYAD BANK INTERIM CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION

INTERIM CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION 31 March 31 December 31 March 2018 2017 2017 (Unaudited) (Audited) (Unaudited) Notes SAR'000 SAR'000 SAR'000 ASSETS Cash and balances with

INTERIM CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION 31 March 31 December 31 March 2018 2017 2017 (Unaudited) (Audited) (Unaudited) Notes SAR'000 SAR'000 SAR'000 ASSETS Cash and balances with

EUROBANK ERGASIAS S.A.

FOR THE NINE MONTHS ENDED 30 SEPTEMBER 2018 8 Othonos Street, Athens 105 57, Greece www.eurobank.gr, Tel.: (+30) 210 333 7000 General Commercial Registry Νο: 000223001000 Index to the Condensed Consolidated

FOR THE NINE MONTHS ENDED 30 SEPTEMBER 2018 8 Othonos Street, Athens 105 57, Greece www.eurobank.gr, Tel.: (+30) 210 333 7000 General Commercial Registry Νο: 000223001000 Index to the Condensed Consolidated

Implementing IFRS 9: a guide for lessors

Implementing IFRS 9: a guide for lessors Implementing IFRS 9: a guide for lessors IFRS 9 brings together the classification and measurement, impairment and hedge accounting sections of the IASB s project

Implementing IFRS 9: a guide for lessors Implementing IFRS 9: a guide for lessors IFRS 9 brings together the classification and measurement, impairment and hedge accounting sections of the IASB s project

FINANCIAL INSTRUMENTS. The future of IFRS financial instruments accounting IFRS NEWSLETTER

IFRS NEWSLETTER FINANCIAL INSTRUMENTS Issue 20, February 2014 All the due process requirements for IFRS 9 have been met, and a final standard with an effective date of 1 January 2018 is expected in mid-2014.

IFRS NEWSLETTER FINANCIAL INSTRUMENTS Issue 20, February 2014 All the due process requirements for IFRS 9 have been met, and a final standard with an effective date of 1 January 2018 is expected in mid-2014.

IFRS 9 FINANCIAL INSTRUMENTS FOR NON FINANCIAL INSTITUTIONS. New member firm training 2010 Page 1

IFRS 9 FINANCIAL INSTRUMENTS FOR NON FINANCIAL INSTITUTIONS New member firm training 2010 Page 1 AGENDA / OUTLINE IFRS 9 Financial Instruments Objective & Scope Key definitions Background & introduction

IFRS 9 FINANCIAL INSTRUMENTS FOR NON FINANCIAL INSTITUTIONS New member firm training 2010 Page 1 AGENDA / OUTLINE IFRS 9 Financial Instruments Objective & Scope Key definitions Background & introduction

Interim consolidated financial statements for six months ended 30 June 2018

Interim consolidated financial statements for six months ended 30 Prepared in accordance with International Accounting Standard IAS 34 Interim Financial Reporting Contents Consolidated statement of financial

Interim consolidated financial statements for six months ended 30 Prepared in accordance with International Accounting Standard IAS 34 Interim Financial Reporting Contents Consolidated statement of financial

BANK ALBILAD (A Saudi Joint Stock Company)

") Consolidated Financial Statements For the year ended December 31, 2018 CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT DECEMBER 31, 2018 AND 2017 Notes 2018 SAR 000 2017 SAR 000 ASSETS Cash and

Consolidated Financial Statements For the year ended December 31, 2018 CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT DECEMBER 31, 2018 AND 2017 Notes 2018 SAR 000 2017 SAR 000 ASSETS Cash and

Deutsche Bank. IFRS 9 Transition Report

IFRS 9 Transition Report April 2018 Table of Contents Introduction... 3 IFRS 9 Implementation Program... 3 Impact Analysis... 4 Key Metrics... 4 Classification and Measurement... 4 Impairment... 5 Classification

IFRS 9 Transition Report April 2018 Table of Contents Introduction... 3 IFRS 9 Implementation Program... 3 Impact Analysis... 4 Key Metrics... 4 Classification and Measurement... 4 Impairment... 5 Classification

Contrasting the new US GAAP and IFRS credit impairment models

Contrasting the new and credit impairment models A comparison of the requirements of ASC 326 and 9 No. US2017-24 September 26, 2017 What s inside: Background....1 Overview......1 Key areas....2 Scope......2

Contrasting the new and credit impairment models A comparison of the requirements of ASC 326 and 9 No. US2017-24 September 26, 2017 What s inside: Background....1 Overview......1 Key areas....2 Scope......2

B A N G K O K B A N K B E R H A D ( W) (Incorporated in Malaysia) Interim Condensed Financial Statements 30 September 2018

(Incorporated in Malaysia) Interim Condensed Financial Statements 30 September 2018") B A N G K O K B A N K B E R H A D (299740-W) Interim Condensed Financial Statements 30 September 2018 Contents Page(s) Performance review and commentary on the prospects 1 Interim condensed statements

B A N G K O K B A N K B E R H A D (299740-W) Interim Condensed Financial Statements 30 September 2018 Contents Page(s) Performance review and commentary on the prospects 1 Interim condensed statements

BANK ALBILAD (A Saudi Joint Stock Company)

") UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS PERIOD ENDED SEPTEMBER 30, 2018 INTERIM CONSOLIDATED STATEMENT OF FINANCIAL POSITION Notes 30, 2018 SAR 000 (Unaudited)

UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS PERIOD ENDED SEPTEMBER 30, 2018 INTERIM CONSOLIDATED STATEMENT OF FINANCIAL POSITION Notes 30, 2018 SAR 000 (Unaudited)

Exposure Draft (ED/2012/4), Classification and Measurement - Limited Amendments to IFRS 9

, Classification and Measurement - Limited Amendments to IFRS 9") 27 March 2013 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Re: Exposure Draft (ED/2012/4), Classification and Measurement - Limited Amendments to IFRS 9 Ladies

27 March 2013 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Re: Exposure Draft (ED/2012/4), Classification and Measurement - Limited Amendments to IFRS 9 Ladies

IFRS 9 AND IFRS 17 INTERACTION

The Actuarial Society of Hong Kong IFRS 9 AND IFRS 17 INTERACTION 2017 Insurance IFRS Seminar David Ogloza Session 23 IFRS 17 Transition Interaction with IFRS 9 IFRS 9 is effective for periods beginning

The Actuarial Society of Hong Kong IFRS 9 AND IFRS 17 INTERACTION 2017 Insurance IFRS Seminar David Ogloza Session 23 IFRS 17 Transition Interaction with IFRS 9 IFRS 9 is effective for periods beginning

JAB Holding Company S.à r.l., Luxembourg

JAB Holding Company S.à r.l. Luxembourg Interim Condensed Financial Statements as at and for the six months period ended 30 June 2018 4, Rue Jean Monnet, 2180 Luxembourg B 164.586 Index Page Report of

JAB Holding Company S.à r.l. Luxembourg Interim Condensed Financial Statements as at and for the six months period ended 30 June 2018 4, Rue Jean Monnet, 2180 Luxembourg B 164.586 Index Page Report of

IFRS 9 Readiness for Credit Unions

IFRS 9 Readiness for Credit Unions Classification & Measurement Implementation Guide June 2017 IFRS READINESS FOR CREDIT UNIONS This document is prepared based on Standards issued by the International

IFRS 9 Readiness for Credit Unions Classification & Measurement Implementation Guide June 2017 IFRS READINESS FOR CREDIT UNIONS This document is prepared based on Standards issued by the International

IFRS IN PRACTICE IFRS 9 Financial Instruments

IFRS IN PRACTICE 2018 IFRS 9 Financial Instruments 2 IFRS IN PRACTICE 2018 IFRS 9 FINANCIAL INSTRUMENTS IFRS IN PRACTICE 2018 IFRS 9 FINANCIAL INSTRUMENTS 3 TABLE OF CONTENTS 1. Introduction 5 2. Definitions

IFRS IN PRACTICE 2018 IFRS 9 Financial Instruments 2 IFRS IN PRACTICE 2018 IFRS 9 FINANCIAL INSTRUMENTS IFRS IN PRACTICE 2018 IFRS 9 FINANCIAL INSTRUMENTS 3 TABLE OF CONTENTS 1. Introduction 5 2. Definitions

AL RAJHI BANKING AND INVESTMENT CORPORATION (A SAUDI JOINT STOCK COMPANY)

") AL RAJHI BANKING AND INVESTMENT CORPORATION INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) FOR THE THREE - MONTH PERIOD ENDED 31 MARCH 2018 1. GENERAL Al Rajhi Banking and Investment

AL RAJHI BANKING AND INVESTMENT CORPORATION INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) FOR THE THREE - MONTH PERIOD ENDED 31 MARCH 2018 1. GENERAL Al Rajhi Banking and Investment

Get ready for FRS 109: Classifying and measuring financial instruments. July 2018

Get ready for FRS 109: Classifying and measuring financial instruments July 2018 Contents Preface 03 1 Overview of classification and measurement requirements 04 2 The business model test 06 2.1 Determining

Get ready for FRS 109: Classifying and measuring financial instruments July 2018 Contents Preface 03 1 Overview of classification and measurement requirements 04 2 The business model test 06 2.1 Determining

Reem Investments PJSC CONSOLIDATED FINANCIAL STATEMENTS AND CHAIRMAN S REPORT

CONSOLIDATED FINANCIAL STATEMENTS AND CHAIRMAN S REPORT 31 DECEMBER 2018 CHAIRMAN S REPORT 31 DECEMBER 2018 AUDITOR S REPORT AND CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2018 CONSOLIDATED INCOME

CONSOLIDATED FINANCIAL STATEMENTS AND CHAIRMAN S REPORT 31 DECEMBER 2018 CHAIRMAN S REPORT 31 DECEMBER 2018 AUDITOR S REPORT AND CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2018 CONSOLIDATED INCOME

BFRS 9 Financial Instruments Overview and Key Changes from Current Standard and Requirements. 28 April 2016

BFRS 9 Financial Instruments Overview and Key Changes from Current Standard and Requirements 28 April 2016 Why is BFRS 9 Important? BFRS 9 will impact all entities, but especially banks, insurers and other

BFRS 9 Financial Instruments Overview and Key Changes from Current Standard and Requirements 28 April 2016 Why is BFRS 9 Important? BFRS 9 will impact all entities, but especially banks, insurers and other

Hot topics treasury seminar

IFRS 9 Lessons learned from first implementations Discover and unlock your potential Program Introduction and objectives Phase 1 Classification and measurement Phase 2 Impairments Phase 3 Hedge Accounting

IFRS 9 Lessons learned from first implementations Discover and unlock your potential Program Introduction and objectives Phase 1 Classification and measurement Phase 2 Impairments Phase 3 Hedge Accounting

Accounting for Financial Instruments

International Financial Reporting Standards Accounting for Financial Instruments (IFRS 9) Executive IFRS workshop for Regulators Diplomatic Academy of Vienna Darrel Scott, IASB member The views expressed

International Financial Reporting Standards Accounting for Financial Instruments (IFRS 9) Executive IFRS workshop for Regulators Diplomatic Academy of Vienna Darrel Scott, IASB member The views expressed

Arab National Bank. (A Saudi Joint Stock Company) Interim Condensed Consolidated Financial Statements For the period ended 30 September 2018

Interim Condensed Consolidated Financial Statements For the period ended 30 September 2018") Arab National Bank (A Saudi Joint Stock Company) Interim Condensed Consolidated Financial Statements For the period ended 30 September 2018 ARAB NATIONAL BANK - Saudi Joint Stock Company INTERIM CONSOLIDATED

Arab National Bank (A Saudi Joint Stock Company) Interim Condensed Consolidated Financial Statements For the period ended 30 September 2018 ARAB NATIONAL BANK - Saudi Joint Stock Company INTERIM CONSOLIDATED

Summary of IFRS 9 accounting standard adoption

Summary of IFRS 9 accounting standard adoption 1 July 2018 1 Contents Pag. 1. IFRS 9 and the Mediobanca Group 3 1.1 Regulatory scenario 3 1.2 Current project 4 1.3 Classification and measurement 5 1.4

Summary of IFRS 9 accounting standard adoption 1 July 2018 1 Contents Pag. 1. IFRS 9 and the Mediobanca Group 3 1.1 Regulatory scenario 3 1.2 Current project 4 1.3 Classification and measurement 5 1.4

IFRS 9 for Financial Services Presentation and Disclosure. Ulana Oswald Senior Manager. December 9, 2015

IFRS 9 for Financial Services Presentation and Disclosure Ulana Oswald Senior Manager December 9, 2015 Presentation and Disclosure: Classification and Measurement Page 1 Classification and measurement

IFRS 9 for Financial Services Presentation and Disclosure Ulana Oswald Senior Manager December 9, 2015 Presentation and Disclosure: Classification and Measurement Page 1 Classification and measurement

AL RAJHI BANKING AND INVESTMENT CORPORATION (A SAUDI JOINT STOCK COMPANY)

") AL RAJHI BANKING AND INVESTMENT CORPORATION INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) FOR THE THREE - MONTH AND NINE - MONTH PERIODS ENDED 30 SEPTEMBER 2018 1. GENERAL Al Rajhi

AL RAJHI BANKING AND INVESTMENT CORPORATION INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) FOR THE THREE - MONTH AND NINE - MONTH PERIODS ENDED 30 SEPTEMBER 2018 1. GENERAL Al Rajhi

ECOBANK TRANSNATIONAL INCORPORATED. Condensed Unaudited Consolidated Interim Financial Statements

ECOBANK TRANSNATIONAL INCORPORATED For period ended 30 September 2018 For the period ended 30 September 2018 CONTENTS Condensed unaudited consolidated interim financial statements: Press release Condensed

ECOBANK TRANSNATIONAL INCORPORATED For period ended 30 September 2018 For the period ended 30 September 2018 CONTENTS Condensed unaudited consolidated interim financial statements: Press release Condensed

AL RAJHI BANKING AND INVESTMENT CORPORATION (A SAUDI JOINT STOCK COMPANY)

") (A SAUDI JOINT STOCK COMPANY) CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2018 TOGETHER WITH THE INDEPENDENT AUDITORS REPORT 1. GENERAL a) Incorporation and operation Al

(A SAUDI JOINT STOCK COMPANY) CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2018 TOGETHER WITH THE INDEPENDENT AUDITORS REPORT 1. GENERAL a) Incorporation and operation Al

Standard Chartered Bank Malaysia Berhad (Incorporated in Malaysia) and its subsidiaries. Financial statements for the three months ended 31 March 2018

and its subsidiaries. Financial statements for the three months ended 31 March 2018") Standard Chartered Malaysia Berhad and its subsidiaries Financial statements for the three months ended Domiciled in Malaysia Registered office/principal place of business Level 16, Menara Standard Chartered

Standard Chartered Malaysia Berhad and its subsidiaries Financial statements for the three months ended Domiciled in Malaysia Registered office/principal place of business Level 16, Menara Standard Chartered