The names of the Scheduled Banks whose operations are recorded in this volume are as below:

|

|

|

- Madeleine Marsh

- 6 years ago

- Views:

Transcription

1 INTRODUCTION After liberation, the banks operating in Bangladesh (except those incorporated abroad) were nationalised. These banks were merged and grouped into six commercial banks. Of the total six commercial banks, Pubali Bank Ltd. and Uttara Bank Ltd. were subsequently transferred to the private sector with effect from January Rupali Bank was transferred as public limited company from December The rest three State Owned Banks were operating as public limited company from the quarter October- December, The two Govt. owned specialised banks were renamed as Bangladesh Krishi Bank and Bangladesh Shilpa Bank. In March 1987 Bangladesh Krishi Bank was bifurcated and another specialised bank emerged as Rajshahi Krishi Unnayan Bank (RAKUB) for Rajshahi and Rangpur Division. Bank of Small Industries & Commerce Bangladesh Ltd. (BASIC) started its operation as a private bank from September Later on BASIC was brought under direct control of the Government and was reckoned to as a specialised bank with effect from June From July 1995 again the BASIC was categorised as a private bank. In 1997, Government decided to treat this bank as a Specialised bank again. So in this booklet, the BASIC has been treated as a Specialised Bank. Bangladesh Shilpa Bank (BSB) & Bangladesh Shilpa Rin Sangstha (BSRS) merged and renamed as Bangladesh development Bank Limited (BDBL) from the quarter January-March, Standard Chartered Grindlays Bank was merged with Standard Chartered Bank during the Quarter (January-March, 2003). American Express Bank also merged with Standard Chartered Bank during the quarter (October-December, 2005). The Oriental Bank Ltd. an Islamic private bank was renamed as ICB Islamic Bank Ltd. from the quarter (April-June, 2008). Credit Agricole Indosuez, a foreign private bank is renamed as Commercial Bank of Ceylon Ltd. from the quarter (October-December, 2003). Shamil Bank is renamed as Bank Al-Falah Ltd. from the quarter (April-June, 2005). Arab Bangladesh Bank Ltd. is renamed as AB Bank Ltd. from the quarter (January-March, 2008) and Social Investment Bank Ltd. is renamed as Social Islami Bank Ltd. from the quarter (April-June, 2009). It is mentioned that First Security Bank Ltd. has started its operation according to Islamic Sariah from the quarter (January-March, 2009), Shahjalal Bank Ltd. has started its operation according to Islamic Sariah from the quarter April-June, 2001 and it is renamed as Shahjalal Islami Bank Ltd. from the quarter April-June, 2004 and EXIM Bank Ltd. has also started its operation according to Islamic Sariah from the quarter (July- September, 2004). The branches of foreign banks operating in Bangladesh are being treated as foreign private banks. Among all fourth generation Scheduled Banks NRB Commercial Bank Ltd., South Bangla Agriculture and Commerce Bank Ltd., Meghna Bank Ltd., The Farmers Bank Ltd., and Union Bank Ltd. have started their operation from the quarter April-June, Midland Bank Ltd., Modhumoti Bank Ltd., NRB Bank Ltd. have started their operation from the quarter July- September, 2013 and NRB Global Bank Ltd have started their operation from the quarter October-December, It is mentioned that Union Bank Ltd. based on Islamic Sariah. All such banks operating in Bangladesh with different paid-up capital and reserves having a minimum of an aggregate value of Tk. 50 lac and conducting their affairs to the satisfaction of the Bangladesh Bank have been declared as i

2 scheduled banks in terms of section 37(2) of Bangladesh Bank Order In terms of section 13 of Bank Company Act, 1991, the minimum aggregate value was Tk. 20 crore. From 30 March 2003 it was Tk. 100 crore. From 08 October 2007 it was Tk. 200 crore. From 11 August 2011 it has been raised at the minimum of Tk. 400 crore (as per Circular Letter No. BRPD(R-1)717/ dated August 12, 2008). The names of the Scheduled Banks whose operations are recorded in this volume are as below: A. STATE OWNED BANKS: 1. Agrani Bank Limited. 2. Janata Bank Limited. 3. Rupali Bank Limited. 4. Sonali Bank Limited. B. SPECIALSED BANKS: 1. Bangladesh Krishi Bank. 2. Rajshahi Krishi Unnayan Bank. 3. Bank of Small Industries and Commerce Bangladesh Ltd. 4. Bangladesh Development Bank Limited. C. PRIVATE BANKS: a) Foreign Banks: 1. Standard Chartered Bank 2. State Bank of India 3. Habib Bank Ltd. 4. Citi Bank, N.A. 5. Commercial Bank of Ceylon Ltd. 6. National Bank of Pakistan 7. Woori Bank 8. The Hong Kong & Shanghai Banking Corporation Ltd. 9. Bank Al-Falah Ltd. b) Private Banks (Incorporated in Bangladesh excluding Islamic Banks): 1. AB Bank Ltd. 2. National Bank Ltd. 3. The City Bank Ltd. 4. International Finance Investment and Commerce Bank Ltd. 5. United Commercial Bank Ltd. 6. Pubali Bank Ltd. 7. Uttara Bank Ltd. 8. Eastern Bank Ltd. 9. National Credit and Commerce Bank Ltd. 10. Prime Bank Ltd. 11. Southeast Bank Ltd. 12. Dhaka Bank Ltd. 13. Dutch Bangla Bank Ltd. 14. Mercantile Bank Ltd. 15. Standard Bank Ltd. 16. One Bank Ltd. 17. Bangladesh Commerce Bank Ltd. 18. Mutual Trust Bank Ltd. 19. Premier Bank Ltd. 20. Bank Asia Ltd. 21. Trust Bank Ltd. 22. Jamuna Bank Ltd. 23. BRAC Bank Ltd. 24. NRB Commercial Bank Ltd. 25. South Bangla Agriculture and Commerce Bank Ltd. 26. Meghna Bank Ltd. 27. Midland Bank Ltd. 28. The Farmers Bank Ltd. 29. NRB Bank Ltd. 30. Modhumoti Bank Ltd. 31. NRB Global Bank Ltd. c) Islamic Banks 1. Islami Bank Bangladesh Ltd. 2. ICB Islamic Bank Ltd. 3. Al-Arafah Islami Bank Ltd. 4. Social Islami Bank Ltd. 5. EXIM Bank Ltd. 6. First Security Islami Bank Ltd. 7. Shahjalal Islami Bank Ltd. 8. Union Bank Ltd ii

3 The banks play an important role in the economy of the country. Bangladesh Bank has been collecting, compiling and publishing statistics on scheduled banks for the use of researchers, planners and policy makers. The statistical tables contained in this issue have been prepared from the returns submitted by the individual bank branches of scheduled banks as on the last day of the quarter ending December 31, At the end of the period under study the total number of reported bank branches including Head Offices, Islamic Windows and SME service centers stood at 9,141, which contains only 76 branches of foreign banks. For useful presentation of data, banks have been classified into several groups viz. All Banks, State owned Banks, Specialised Banks, Foreign Banks, and Private Banks (Including Islamic Banks). A separate subgroup named as Islamic Banks has been introduced consisting of seven banks (Incorporated in Bangladesh), run on the basis of Islamic Sariah with effect from quarter January-March These banks are 1) Islamic Bank Bangladesh Ltd. 2) ICB Islamic Bank Ltd. 3) Al-Arafah Islami Bank Ltd. 4) Social Islami Bank Ltd. 5) EXIM Bank Ltd. 6) Shahjalal Islami Bank Ltd. 7) First Security Islami Bank Ltd. and 8) Union Bank Ltd. The publication provides a detailed analysis of bank deposits (excluding inter-bank) mainly in the form of by Types & Sectors, by Rates of Interest & Types, by Types of Account ; outstanding advances (excluding inter-bank transactions) mainly in the form of by Rates of Interest & Securities, by Securities, by Size of Account, by Economic Purposes etc. and bills mainly in the form of by Sectors. From the very inception, the Scheduled Banks Statistics were being collected and published on quarterly basis. Later on since December, 1988 the data had been collected on half yearly basis and published on annual basis ending December every year. Subsequently, from December 1990 the data were collected on quarterly basis but published on annual basis. Then it was decided to publish again on quarterly basis from June 1992 and the present publication follows as a sequel to the change in the policy decision. The role of agricultural credit in fostering the economy of the country has gained importance nowadays. To this end in mind agricultural credit statistics time series data were collected and presented pertaining to the period from to (up to December 31, 2014). The figures published in this booklet may differ from those contained in the statement of position of Scheduled Banks released each week by the Bangladesh Bank due to difference in timing and coverage. From the quarter July-September, 2013 the Scheduled Banks were instructed to follow the Guidelines to Fill in the Banking Statistics Returns SBS-1, SBS-2 & SBS-3 fifth edition, published in July In this brochure, all statistical tables have been prepared on the basis of returns, submitted by the scheduled banks as per the booklet, published in July For taking into account, the remittances (in Foreign Currency) by the Wage earners abroad, two types of deposits: 1) Wage Earners & 2) Resident Foreign Currency have been introduced from the quarter ending on December, iii

4 EXPLANATORY NOTES TO THE TABLES Table-1: Divisions/Districts wise distribution of per capita /Advances on the basis of population: The table furnishes the division/district wise distribution of population, number of reporting bank branches, per capita deposits and per capita advances. Table-2 to 7: Distributed by Types of Accounts: These tables show the classification of total demand and time liabilities of scheduled banks (excluding inter-bank) into fourteen broad types such as (a) Current and Cash Credit Account (credit balances), (b) withdrawable on Sight, (c) Savings, (d) Convertible Taka Accounts of Foreigners, (e) Foreign Currency Accounts, (f) Wage Earners, (g) Resident Foreign Currency, (h) SpecialNotice, (i) Fixed, (j) Recurring, (k) Margin (Foreign Currency/Taka), (l) Special Purpose, (m) Negotiable Certificates of & Promissory Notes and (n) Restricted (Blocked). a) Current and Cash Credit Accounts : These are of the nature of demand deposits and comprise current accounts and credit balances of cash credit accounts. Generally no interest is allowed on these deposits. These deposits are to be reported in code no.-100 as usual but from the quarter, October-December, 2005 some banks have started paying interest on this type of account. This later type is to be reported in code no These accounts have chequing facilities and balances are transferable. b) Withdrawable on Sight: This item includes all deposits which cannot be transferred through cheques but are withdrawable on demand such as overdue Fixed Accounts, unclaimed balances, payment orders, telephonic transfers, mail transfers, demand drafts, unclaimed dividends and draft payable accounts, Earnest Money of Tenders/Quotations etc. c) Saving Account: Deposit on these accounts are self-explanatory and generally emanates from the individuals. A portion, varying from time to time, of savings deposits constitutes demand deposits. From 1 st July, % of savings deposits was regarded as demand deposits and from 1 st July 1997, it was 10%. At present from 24 th June, 2007, 9% of savings deposits has been being regarded as demand deposits. d) Convertible Taka Account of Foreigners: Convertible Taka account of foreigners are deposits of foreign individuals, embassies, foreign Governments and international agencies, all of which have non-resident status under foreign exchange regulations. e) Foreign Currency Accounts: Foreign currency accounts consist of the deposits (in foreign currency) of the foreigners (residing abroad or in Bangladesh) and foreign missions & their expatriate employees. f) Wage Earners : The depositors of these accounts are the Bangladeshi nationals, who work abroad. These accounts are fed by the remittances (in foreign currency) from these persons. in NFCD accounts along with interest thereon are also reported in these accounts. g) Resident Foreign Currency : Persons ordinarily residing in Bangladesh may open this account with foreign exchanges brought in at the time of their return from travel abroad. or remittances from persons, working in Bangladesh missions abroad and Retention quota deposits by the exporters are also included in these deposits. h) Special Notice : This item includes the deposits that are deposited for a period ranging from 7 days to 89 days. These types of liabilities are payable on Special notice or after a specified period other than the fixed deposits. Some of these types of deposits are of the nature of time deposits. iv

5 i) Fixed : These are reclassified by period of maturity and are exclusively time deposits. j) Recurring : According to this scheme the investors would be required to deposit their money limited to maximum of Tk. 500 per month for a period of 10 years and 20 years. Interest on the invested amount will be compounded at the rate of 15% and calculated on yearly basis. Pension schemes are of the nature of time deposits and it was introduced in Later on Scheme e.g. APS, SDPS, SPS, PDS, PSS etc. and Hajj Schemes have been introduced by the various Banks with various interests. k) Margin (Foreign Currency/ Taka) : Equivalent Taka of margin on letters of Credit and margins on guarantee (in Taka & Foreign Currency) are included in this item. l) Special Purpose : This item comprises employees provident funds/pension Accounts, contribution towards insurance funds, Hajj, Staff guarantee/security funds, Security, Gift Certificate, Sundry deposits, Surcharge and Development charge etc. m) Negotiable Certificates of and Promissory Notes: Negotiable certificates of deposits are bearer certificate deposits and are of nature of time deposits. n) Restricted (Blocked) : The balances of restricted (blocked) deposits are reported in this item against Private Sector. According to Special Law, the competent authority blocks these accounts. In blocked period, the depositors cannot withdraw their deposits. Table 8 to 13. Distributed by Divisions/ Districts and Areas (Urban & Rural): These tables show the district-wise distribution of deposits of urban and rural regions of the country. It is mentioned that the transaction of the branches in municipal area is treated as urban area transaction (deposits or advances as the case may be) while the transaction of the branches located out-side the municipal area is regarded as rural area transaction (deposits or advances). Table 14 to 19: Distributed by Sectors and Types: These Tables provide a break up of deposits by different sectors of deposits mentioned in the paragraph number two. Table 20 to 25: Distributed by Rates of Interest/Profit and Types: These tables show the rates of interest allowed by the scheduled banks on different types of deposits. No interest is allowed on current deposits (without interest, Code no.-100)and deposits withdrawable on sight while interest is allowed on current deposits (with interest, Code no.-105), savings deposits, fixed deposits, pension scheme deposits and foreign currency accounts of non-residents and residents. The rate of interest varies from time to time. The amount of deposits against Zero rate of interest under Withdrawable on Sight represents mainly the bills payables such as MT, DD, TT, outstanding drafts etc. Depositors will have the option for withdrawing interest accumulated every twelve months or can have the interest with the principal to be compounded in case of maturity exceeding one year. Profit/Loss is applicable in the cases of Islamic Banks (Islami Bank Bangladesh Ltd., ICB Islamic Bank Ltd., Al-Arafah Islami Bank Ltd., Social Islami Bank Ltd., EXIM Bank Ltd, First Security Islami Bank Ltd., Shahjalal Islami Bank Ltd. and Union Bank Ltd.). Table 26 to 31: Distributed by Size of Accounts: The Statistics of number of Accounts and corresponding amount falling within specified groups are not based exclusively on individual accounts. As the number of accounts is considerably large, the respondents have the option to combine the accounts and amount in such cases when the types of deposits, the category of depositors and the rates of interest allowed thereon are the same. In such cases it is not the actual size of components but the average size of the group that determines the class to which it belongs. Notwithstanding the existence of an element of statistical errors, it is v

6 believed that the estimates would not differ significantly from the actual position. Table 32: Distributed by Size of Accounts and Sectors: The Tables provide a break up of deposits by size of accounts and sector. Table 33: Distributed by Selected Thanas: The statistics show the distribution of deposits in the leading thanas of the country and those have been presented in the descending order of magnitude of deposits. Table 34: Debits to Accounts and Turnover: The table shows debits to various types of deposit accounts during the period under review. This also includes co-efficient of turnover by relating debits to average amounts of deposits. Table 35 to 40: Advances Classified by Securities: These tables show the break-up of scheduled banks advances (excluding interbank) by types of securities pledged or hypothecated. Table 41 to 46: Advances Classified by Economic Purposes: These tables show the advances made by scheduled banks to different economic purposes for which the borrowers borrow. If a borrower pursues more than one profession the classification is done in accordance with his major calling. Table 47 to 52: Advances Classified by Rates of Interest and Securities: These tables give the rates of interest charged by the scheduled banks on various types of securities as well as clean advances. Advances to Zero rate of interest mostly represent (a) Advances to bank s own employees (b) Classified advances (Bad/ Loss) (c) Advances associated with clearing disputes etc. Table 53: Advances Classified by Selected Thanas: This table shows the classification of advances in the leading thanas of the country and those have been presented in the descending order of magnitude of advances. Table 54: Advances Classified by Size of Accounts and Economic Groups: The table provides statistics on advances classified by size of accounts and economic groups. The respondents can group those accounts together where the securities, the economic purpose, the category of borrowers and the rates of interest are the same. As a result the size of distribution suffers from a similar limitation as its analogy in deposits. Table 55 to 60: Advances Classified by Size of Accounts: These tables provides statistics on advances classified by size of accounts. Table 61: Advances Classified by Major Economic Purposes and Sectors: The table provides a break-up of advances classified by major economic purposes to public and private sectors. Table 62 to 67: Advances Classified by Division / Districts and Areas (Urban / Rural): These tables show the district-wise classification of advances of urban and rural regions of the country. Table 68: Advances Classified by Size of Accounts and Sectors: The table provides statistics on advances classified by size of accounts and sector. Table 69 to 74: Advances Classified by Rates of Interest and Major Economic Purposes: These tables provide rates of interest charged by the scheduled banks on advances for different economic purposes. Table 75 to 80: Agricultural Credits Statistics. Table 81: Disbursement, Overdue & Recovery of Agricultural and Non-Farm Rural Credit Position. Table 82: SME Credit Position. Table 83 to 88: Classification of Bills purchased and discounted: The statement provides an account of bills purchased and discounted by major economic purposes of drawees. Along with the corresponding statement on advances the statistics provide information on the structure of bank credit. Table 89: Classification of Bills by Sectors. Table 90: Disbursement, Overdue & Recovery of Advances by Sectors. Table 91: Disbursement, Overdue & Recovery of Advances by Economic Purposes. vi

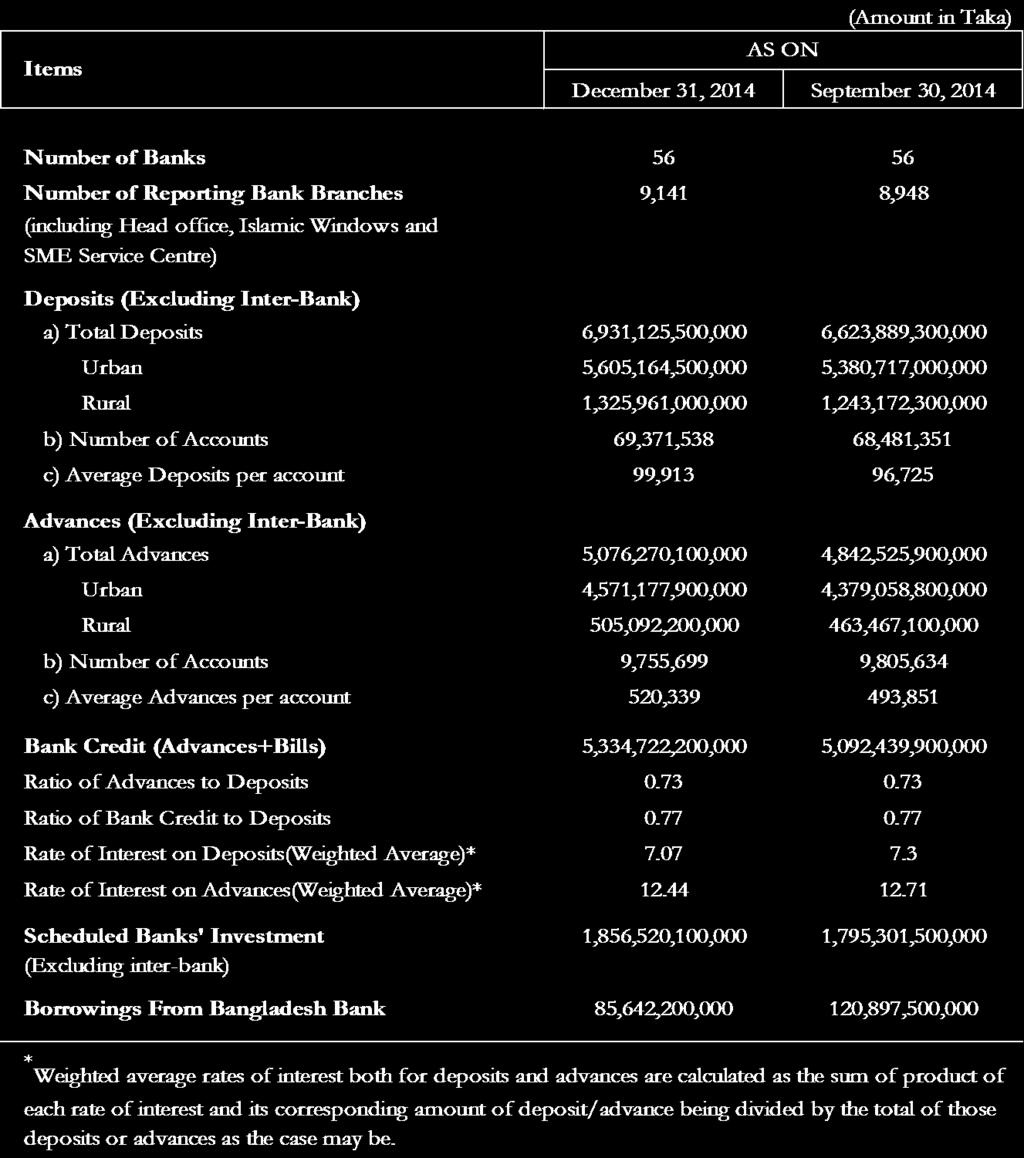

7 A Review on and Advances of Scheduled Banks (As on end December, 2014) Banks : Total deposit liabilities (excluding interbank items) of the scheduled banks increased by Tk crore or 4.64% to Tk crore during the quarter Oct.-Dec., 2014 as compared to increases of Tk crore or 1.99% and Tk crore or 5.15% in the previous quarter (Jul.-Sep., 2014) and the corresponding quarter (Oct.-Dec., 2013) of the last year respectively. The increase in deposits during the quarter was due to increases in urban deposits by Tk crore or 4.17% to Tk crore and in rural deposits by Tk crore or 6.66% to Tk crore. The share of urban deposits to total deposits at the end of the quarter Oct.-Dec., 2014 was 80.87% as compared to 81.23% at the end of the preceding quarter (Jul.-Sep., 2014) and 81.70% at the end of the corresponding quarter (Oct.-Dec., 2013) of the last year. Bank deposits registered an increase of Tk crore or 13.53% from end December, 2013 to end December, 2014 as compared to an increase of Tk crore or 14.68% from end December, 2012 to end December, Banks' Advances: Banks advances increased by Tk crore or 4.83% to Tk crore during the quarter Oct.-Dec., 2014 as compared to increases of Tk crore or 3.12% and Tk crore or 2.84% respectively during the preceding quarter (Jul.-Sep., 2014) and the corresponding quarter (Oct.-Dec., 2013) of the last year. Bank advances in urban areas increased by Tk crore or 4.39% to Tk crore and in rural areas increased by Tk crore or 8.98% to Tk crore during the quarter under review. Bank advances exhibited an increase by Tk crore or 14.37% from end December, 2013 to end December, 2014 as compared to an increase of Tk crore or 8.09% from end December, 2012 to end December, Bills: Bills purchased and discounted by the banks increased by Tk crore or 3.42% to Tk crore during the quarter under review as compared to increases of Tk crore or 11.70% and decreases of Tk crore or 5.51% respectively during the preceding quarter (Jul.-Sep., 2014) and the corresponding quarter (Oct.-Dec., 2013) of the last year. vii

8 Interest Rates (Weighted Average): Weighted average rates of interest on deposits and advances were 7.07% & respectively at the end of the quarter under review as compared to 7.30% & 12.71% in Jul.- Sep., 2014 and 8.34% & 13.47% in Oct.-Dec., 2013 quarters respectively. Quarterly position of banks deposits, outstanding advances and bills is shown in Table-1. At end of the quarter Table-1 Overall, Advances and Bills Advances Bills Purchased Urban Rural Total Urban Rural Total and Discounted Weighted Average Interest Rate on (Taka in Crore) Weighted Average Interest Rate on Advances 2013 Oct.-Dec % 18.30% 100% 89.85% 10.15% 100% (5.01) (5.75) (5.15) (2.75) (3.65) (2.84) (-5.51) 2014 Jan.-Mar % 18.18% 100% 90.09% 9.91% 100% (2.07) (1.27) (1.92) (1.87) (-0.87) (1.59) (-2.08) Apr.-Jun % 18.62% 100% 90.13% 9.87% 100% (3.8) (6.92) (4.37) (4.19) (3.77) (4.14) (1.07) Jul.-Sep % 18.77% 100% 90.43% 9.57% 100% (1.81) (2.78) (1.99) (3.47) (-0.02) (3.12) (11.7) Oct.-Dec % 19.13% 100% 90.05% 9.95% 100% 3.73% (4.17) (6.66) (4.64) (4.39) (8.98) (4.83) (3.42) Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be observed due to rounding off and changes of Fourth Edition to Fifth Edition of Guidelines to fill in the Banking Statistics Returns SBS-1, 2 & 3. viii

and the corresponding quarter (Oct.- Dec., 2013) of the last year.")

9 Banks' Credit Total credit of the Scheduled banks increased by Tk crore or 4.76% to Tk crore during the quarter under review as compared to increases of Tk crore or 3.51% and Tk crore or 2.40% respectively during the preceding quarter (Jul.- Sep., 2014) and the corresponding quarter (Oct.- Dec., 2013) of the last year. Banks' Investment The Scheduled banks' investment increased by Tk crore or 3.41% to Tk crore at the end of the quarter Oct.-Dec., 2014 as compared to increases of Tk crore or 2.18% and Tk crore or 9.69% respectively during the Preceding quarter (Jul.- Table-2 Sep., 2014) and the corresponding quarter (Oct.- Dec., 2013) of the last year. Borrowings from the Bangladesh Bank Scheduled Banks Credit, Investment and Borrowing from Bangladesh Bank The Scheduled Banks' borrowings from the Bangladesh Bank at the end of the quarter under review decreased by Tk crore or 29.16% to Tk crore as compared to increases of Tk. Tk crore or % and decreases of Tk crore or 22.46% respectively during the preceding quarter (Jul.-Sep., 2014) and the corresponding quarter (Oct.-Dec., 2013) of the last year. Quarterly position of the scheduled banks' credit, investment and borrowings from the Bangladesh Bank is shownintable-2. Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be observed due to rounding off. ix

10 by Category of Banks: The increased of Tk crore or 4.64% in total deposit liabilities during the quarter Oct.-Dec., 2014 over the preceding quarter Jul.-Sep., 2014 was shared by increased in Private Banks by Tk crore or 4.41%, Specialised Banks by Tk crore or 5.96%, Islamic Banks by Tk crore or 3.59%, State Owned Banks by Tk crore or 6.36% and Foreign Banks decreased by Tk crore or 2.46%. The net accretion in deposits during the quarter under review over the same quarter (Oct.-Dec., 2013) of the last year amounting to Tk crore or 13.53% was due to increased in deposits of State Owned Banks by Tk crore or 12.82%, Table-3 Distributed by Category of Banks in Private Banks by Tk crore or 15.40%, in Specialised Banks by Tk crore or 10.65%, in Islamic Banks by Tk crore or 20.36% and in Foreign Banks decreased by Tk crore or 1.29%. Of the total deposits of Tk crore at the end of the quarter under review, the shares of State Owned Banks, Specialised Banks, Foreign Banks, Private Banks and Islamic Banks were Tk crore (26.21%), Tk crore (5.42%), Tk crore (4.84%), Tk crore (63.52%) and Tk crore (18.72%) respectively. The position in respect of deposit liabilities by category of Banks is shown in Table-3. Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be observed due to rounding off. x

11 by Types of Accounts: Breakdown by types of deposits accounts revealed that the share of fixed deposits from 53.86% at the end of the quarter Jul.-Sep., 2014 to 53.26% at the end of quarter Oct.-Dec., The amount of fixed deposits increased by Tk crore or 3.45% to Tk crore at the end of the quarter under review as or compared to increases of Tk crore or 2.09% and Tk crore or 4.68% at the end of the preceding quarter (Jul.-Sep., 2014) and the corresponding quarter (Oct.-Dec., 2013) of the last year respectively. The share of savings deposits to total deposits from 16.91% on the September 30, 2014 to 16.88% on the December 31, distributed by types of accounts are shown in Table-4. xi

12 At end of the quarter Current and Cash Credit Account Savings Convertible Taka Account of Foreigners Table-4 Distributed by Types of Accounts Foreign Currency Accounts Wage Earners' Resident Foreign Currency Special Notice Fixed Recurring Other (Taka in Crore) Total 2013 Oct.-Dec % 16.46% 0.17% 0.63% 0.24% 0.85% 8.19% 53.42% 7.06% 5.38% 100% (8.67) (2.68) (-1.67) (21.4) (50.36) (-0.6) (7.83) (4.68) (9.53) (1.44) (5.15) 2014 Jan.-Mar % 16.28% 0.18% 0.75% 0.33% 0.88% 7.36% 54.30% 6.89% 5.36% 100% (3.32) (0.78) (5.05) (20.2) (40.82) (5.4) (-8.44) (3.6) (-0.64) (1.43) (1.92) Apr.-Jun % 16.66% 0.20% 0.40% 0.29% 0.77% 7.88% 53.81% 6.58% 5.65% 100% (5.36) (6.81) (20.54) (-44.86) (-8.01) (-8.53) (11.76) (3.42) (-0.33) (10.17) (4.37) Jul.-Sep % 16.91% 0.21% 0.43% 0.27% 0.82% 7.38% 53.86% 7.06% 5.78% 100% (-4.34) (3.53) (3.16) (11.93) (-6.01) (8.56) (-4.41) (2.09) (9.45) (4.22) (1.99) Oct.-Dec % 16.88% 0.22% 0.41% 0.24% 0.80% 7.92% 53.26% 6.97% 5.69% 100% (9.6) (4.42) (9.46) (-0.47) (-4.93) (2.56) (12.2) (3.45) (3.31) (2.97) (4.64) Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be observed due to rounding off and changes of Fourth Edition to Fifth Edition of Guidelines to fill in the Banking Statistics Returns SBS-1, 2 & Other deposits include Withdrawable on Sight, Margin, Special Purpose, Negotiable Certificates of and Restricted. xii

13 Sector-wise : The share of private sector deposits (82.41%) was 4.68 times more than that of the public sector deposits (17.59%) at the end of the quarter Oct.-Dec., in the private sector increased by Tk crore or 4.55% to Tk crore at the end of the quarter under review as compared to increases of Tk crore or 2.02% and Tk crore or 4.78% at the end of the preceding quarter (Jul.-Sep., 2014) and the corresponding quarter (Oct.-Dec., 2013) of the last year respectively. in the public sector increased by Tk crore or 5.05% to Tk crore at the end of the quarter under review as compared to increases of Tk crore or 1.89% and Tk crore or 6.99% at the preceding quarter (Jul.-Sep., 2014) and the corresponding quarter (Oct.-Dec., 2013) of the last year respectively. Government deposits in the public sector increased by Tk crore or 11.28% to Tk crore as compared to increases of Tk crore or 0.27% and increases of Tk crore or 13.38% at the end of the preceding quarter (Jul.- Sep., 2014) and the corresponding quarter (Oct.- Dec., 2013) of the last year respectively. The details of deposits by public sector and private sector with their corresponding growth rates are shown in Table-5. Table-5 Sector-wise Classification of Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be observed due to rounding off. xiii

14 Division-wise Urban/Rural Distribution of deposits by administrative areas revealed that Dhaka Division contributed more than half (63.90%) of the total deposits and the share of urban deposits in this division was 54.55% at the end of the quarter under review. The deposits in this division increased by 3.90% to Tk crore at the end of the quarter Oct.-Dec., 2014 as Table-6(Contd.) Division-wise Urban/Rural Distribution of compared to increases of 2.52% and 4.92% at the end of preceding quarter (Jul.-Sep., 2014) and the corresponding quarter of the last year (Oct.-Dec., 2013) respectively. The share of deposits in Rangpur Division (1.79%) and Barisal Division (1.80%) were the lowest. Division wise distribution of deposits in urban and rural areas is shown in Table-6. (Taka in Crore) At the end Chittagong Division Dhaka Division Khulna Division Rajshahi Division of quarter Urban Rural Total Urban Rural Total Urban Rural Total Urban Rural Total 2013 Oct.-Dec % 4.68% 19.72% 55.34% 9.04% 64.38% 3.04% 1.05% 4.09% 2.86% 0.96% 3.82% (5.57) (1.44) (4.56) (4.47) (7.76) (4.92) (8.96) (9.11) (9) (6) (4.83) (5.7) 2014 Jan.-Mar % 4.69% 19.86% 55.40% 8.91% 64.30% 3.01% 1.07% 4.08% 2.81% 0.94% 3.74% (2.81) (2.09) (2.64) (2.02) (0.48) (1.81) (1) (3.93) (1.76) (0.14) (-0.73) (-0.08) Apr.-Jun % 4.81% 19.78% 54.98% 9.04% 64.02% 3.05% 1.18% 4.23% 2.88% 0.96% 3.85% (2.95) (7.05) (3.92) (3.59) (5.93) (3.91) (5.47) (15.44) (8.08) (7.25) (7.45) (7.3) Jul.-Sep % 4.78% 19.64% 55.00% 9.36% 64.36% 3.03% 1.08% 4.12% 2.86% 0.96% 3.82% (1.28) (1.38) (1.31) (2.03) (5.55) (2.52) (1.65) (-6.93) (-0.76) (1.2) (1.87) (1.37) Oct.-Dec % 5.04% 19.92% 54.55% 9.35% 63.90% 3.07% 1.14% 4.21% 2.90% 0.99% 3.88% (4.78) (10.25) (6.11) (3.77) (4.61) (3.9) (5.88) (9.95) (6.95) (6.02) (7.09) (6.29) Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be shown due to separate rounding off. xiv

15 Table-6 (Concld.) Division-wise Urban/Rural Distribution of (Taka in Crore) At the end Barisal Division Sylhet Division Rangpur Division All Divisions of quarter Urban Rural Total Urban Rural Total Urban Rural Total Urban Rural Total 2013 Oct.-Dec % 0.55% 1.75% 2.96% 1.54% 4.49% 1.26% 0.48% 1.75% 81.70% 18.30% % (7.77) (5.78) (7.13) (5.17) (5.25) (5.2) (7.9) (9.02) (8.21) (5.01) (5.75) (5.15) 2014 Jan.-Mar % 0.56% 1.74% 2.99% 1.54% 4.53% 1.26% 0.48% 1.73% 81.82% 18.18% % (0.6) (3.44) (1.49) (3.1) (2.39) (2.86) (1.26) (0.03) (0.92) (2.07) (1.27) (1.92) Apr.-Jun % 0.56% 1.78% 3.00% 1.56% 4.55% 1.28% 0.50% 1.78% 81.38% 18.62% % (7.3) (5.97) (6.87) (4.63) (5.18) (4.82) (6.48) (10.57) (7.6) (3.8) (6.92) (4.37) Jul.-Sep % 0.56% 1.77% 3.01% 1.54% 4.55% 1.26% 0.48% 1.74% 81.23% 18.77% % (0.79) (1.96) (1.16) (2.48) (0.98) (1.97) (0) (-2.32) (-0.66) (1.81) (2.78) (1.99) Oct.-Dec % 0.58% 1.80% 2.97% 1.54% 4.50% 1.29% 0.50% 1.79% 80.87% 19.13% % (5.41) (8.28) (6.32) (3.13) (4.28) (3.52) (7.31) (8.35) (7.6) (4.17) (6.66) (4.64) Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be shown due to separate rounding off. xv

and the corresponding quarter (Oct.-Dec.")

16 Advances by Category of Banks The State owned Banks accounted for 17.97% of the total advances at the end of the quarter under review. Advances made by State Owned Banks increased by 5.41% to Tk crore at the end of the quarter under review as compared to increases of 3.20% and 1.47% at the end of the preceding quarter (Jul.-Sep., 2014) and the corresponding quarter (Oct.-Dec., 2013) of the last year respectively. The share of Specialised Banks advances decreased to 6.87% on the December 31, 2014 from 7.03% on the September 30, Advances classified by category of banks are shown in Table-7. Table -7 Advances Classified by Category of Banks Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be shown due to separate rounding off. xvi

17 Sector-wise Advances Advances in the private sector increased by Tk crore or 4.21% to Tk crore at end of the quarter (Oct.-Dec., 2014) as compared to increases of Tk crore or 3.19% and Tk crore or 2.72% at the preceding quarter (Jul.-Sep., 2014) and the corresponding quarter (Oct.-Dec., 2013) of the last year respectively. Loans to the public sector increased by Tk crore or 39.86% to Tk crore as compared to decreases of Tk crore or 0.65% and increases of Tk crore or 9.55% during the preceding quarter (Jul.-Sep., 2014) and corresponding quarter (Oct.-Dec., 2013) of the last year respectively. The increase in advances to public sector was due to increase in 'Government' sector by Tk crore or % to Tk crore and Other than Government' sector loans increased by Tk crore or 21.00% to Tk crore at the end of the quarter under review. The sector-wise position of advances is shown in Table-8. Table- 8 Sector-wise Classification of Advances Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be shown due to separate rounding off. xvii

18 Economic Purpose-wise Advances Bulk of Advances (39.03%) was used for Trade purpose followed by advances for 'Working Capital Financing' (18.49%) and Term Loan (15.84%) at the end of the quarter Oct.- Dec., Trade loans increased by Tk crore or 0.57% to Tk crore and Term Loan increased by Tk crore or 8.09% to Tk crore at the end of the quarter under review as compared to increases of 6.55% and decreases of 6.28% respectively at the end of the preceding quarter (Jul.-Sep., 2014) and an increase of 4.95% & a decrease of 10.02% respectively at the corresponding quarter (Oct.- Dec., 2013) of the last year. Transport loans increased by 4.31% to Tk crore and Agriculture loans increased by 2.67% to Tk crore as compared to decreases of 2.15% & 3.16% at the end of the preceding quarter (Jul.-Sep., 2014) and a decrease of 3.71% & an increase of 0.65% at the corresponding quarter (Oct.-Dec., 2013) of the last year respectively. 'Construction' loan increased by 1.59% to Tk crore and Working Capital Financing' loan increased by 2.12% to Tk crore and Consumer Finance loan increased by 30.60% to Tk crore respectively at the end of the quarter under review. 'Others' loans showed a increase of Tk crore to Tk crore at the end of the quarter under review as compared to the preceding quarter. Table-9 shows economic purpose-wise classification of advances. Table -9 Economic Purpose-wise Classification of Advances Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be shown due to separate rounding off. xviii

19 Security-wise Advances An analysis of advances classified by securities revealed that 57.12% of the total loans were outstanding against Real Estate and 7.57% loans against Export Documents/ Commodities at the end of the quarter under review. Advances against Real Estate increased by 7.89% to Tk crore and that against Machinery increased by 9.06% to Tk crore at the end of the quarter Oct.-Dec., Other Items' which includes (i) Gold & Gold Ornaments, (ii)vehicles, (iii) Table-10 Security-wise Classification of Advances Hypothecation of Crops, (iv) Assignment of Bills Receivable, (v) Parri Passu Charge, (vi) Other secured and unsecured advances recorded an decrease of 21.12% to Tk crore at the end of the quarter Oct.-Dec., 2014 as compared to increases of 27.36% and 27.21% at the end of the preceding quarter (Jul.-Sep., 2014) and the corresponding quarter (Oct.-Dec., 2013) of the last year respectively. Security wise classification of advances is shown in Table-10. Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be observed due to rounding off and changes of Fourth Edition to Fifth Edition of Guidelines to fill in the Banking Statistics Returns SBS-1, 2 & 3. xix

20 Division-wise Urban/Rural Advances Division-wise break-up of advances revealed that Dhaka Division consumed 67.58% of total advances of which the share of urban and rural stood at 63.01% and 4.57% respectively at the end of the quarter Oct.-Dec., The loans in Dhaka Division increased by 5.36% to Tk crore and in Chittagong Division increased by 2.15% to Tk crore and in Khulna Division increased by 4.29% to Tk crore during the quarter under review. The loans in Sylhet Division increased by 6.23% to Tk crore, in Barisal Division increased by 11.04% to Tk crore, in Rajshahi Division increased by 5.25% to Tk crore and that in Rangpur Division increased by 9.05% to Tk crore. Division-wise distribution of urban and rural loans is shown in Table-11. Table-11 (Contd.) Division-wise Urban/Rural Classification of Advances (Taka in Crore) At the end Chittagong Division Dhaka Division Khulna Division Rajshahi Division of quarter Urban Rural Total Urban Rural Total Urban Rural Total Urban Rural Total 2013 Oct.-Dec % 2.12% 19.80% 62.61% 4.62% 67.23% 3.16% 1.04% 4.20% 3.05% 0.80% 3.85% (787.81%) (-87.9%) (1.29%) ( %) (-92.37%) (3.3%) (201.78%) (-66.98%) (0.38%) (314.49%) (-73.28%) (3.12%) 2014 Jan.-Mar % 1.92% 19.69% 62.73% 4.61% 67.34% 3.14% 1.02% 4.15% 3.12% 0.80% 3.91% (2.11%) (-8.1%) (1.01%) (1.78%) (1.3%) (1.75%) (0.71%) (-0.14%) (0.5%) (3.88%) (1.03%) (3.29%) Apr.-Jun % 1.88% 19.30% 62.88% 4.52% 67.41% 3.25% 1.09% 4.34% 3.21% 0.81% 4.02% (2.07%) (1.87%) (2.05%) (4.4%) (2.27%) (4.25%) (7.83%) (11.86%) (8.82%) (7.25%) (5.84%) (6.96%) Jul.-Sep % 1.85% 19.86% 62.87% 4.38% 67.24% 3.17% 1.05% 4.22% 3.09% 0.79% 3.88% (6.61%) (1.68%) (6.13%) (3.1%) (-0.21%) (2.87%) (0.55%) (-0.75%) (0.23%) (-0.66%) (0.45%) (-0.44%) Oct.-Dec % 1.93% 19.35% 63.01% 4.57% 67.58% 3.18% 1.02% 4.20% 3.10% 0.79% 3.90% (1.44%) (9.09%) (2.15%) (5.07%) (9.42%) (5.36%) (5.19%) (1.57%) (4.29%) (5.21%) (5.42%) (5.25%) Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be shown due to separate rounding off. xx

21 Table-11 (Concld.) Division-wise Urban/Rural Classification of Advances (Taka in Crore) At the end Barisal Division Sylhet Division Rangpur Division All Divisions of quarter Urban Rural Total Urban Rural Total Urban Rural Total Urban Rural Total 2013 Oct.-Dec % 0.44% 1.10% 1.09% 0.43% 1.52% 1.60% 0.71% 2.30% 89.85% 10.15% % (58.03) (-29.42) (5.86) (156.01) (-59.02) (3.02) (142.95) (-53.44) (5.89) (817.22) (-88.39) (2.84) 2014 Jan.-Mar % 0.44% 1.09% 1.10% 0.43% 1.53% 1.59% 0.69% 2.28% 90.09% 9.91% % (0.05) (2.57) (1.06) (2.85) (2.53) (2.76) (1.16) (-0.69) (0.59) (1.87) (-0.87) (1.59) Apr.-Jun % 0.44% 1.09% 1.08% 0.42% 1.50% 1.65% 0.71% 2.35% 90.13% 9.87% % (4.09) (3.76) (3.96) (1.82) (1.44) (1.72) (7.85) (6.24) (7.36) (4.19) (3.77) (4.14) Jul.-Sep % 0.42% 1.05% 1.07% 0.41% 1.48% 1.60% 0.67% 2.27% 90.43% 9.57% % (0.09) (-0.88) (-0.3) (2.6) (0.29) (1.95) (0.16) (-2.43) (-0.62) (3.47) (-0.02) (3.12) Oct.-Dec % 0.48% 1.11% 1.02% 0.49% 1.50% 1.68% 0.67% 2.36% 90.05% 9.95% % (5.55) (19.25) (11.04) (-0.56) (23.96) (6.23) (10.31) (6.02) (9.05) (4.39) (8.98) (4.83) Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may be shown due to separate rounding off. xxi

22 Division-wise Advances/ Ratio Ratio of Advances to deposits in Chittagong, Dhaka, Khulna, Rajshahi, Barisal, Sylhet and Rangpur Division were 0.71, 0.77, 0.73, 0.73, 0.45, 0.24 and 0.97 respectively at the end of the quarter under review as compared to 0.74, Table-11-A Division-wise Advance/Deposit Ratio 0.76, 0.75, 0.74, 0.43, 0.24 and 0.95 respectively at the end of the previous quarter (Jul.-Sep., 2014). Table-11A shows the Division-wise Advance/ Deposit Ratio. Growth of Scheduled Bank Branches The number of scheduled bank branches in the country increased by 191 or 2.16% to 9040 during the quarter Oct.-Dec., 2014 as compared to increase of 55 or 0.63% to 8849 and 203 or 2.39% to 8685 during the preceding quarter (Jul.-Sep., 2014) and the corresponding quarter (Oct.-Dec., 2013) of the last year respectively. The share of rural branches during the quarter was 56.97%. The number of urban branches increased by 90 or 2.37% during the quarter under review as compared to an increased by 28 or 0.74% during the preceding quarter (Jul.- Grameen Bank A total of 2,568 branches of Grameen Bank were in operation at the end December, It has extended its services to 81,390 villages of Bangladesh where in 8,640,225 members Sep., 2014). The number of branch licenses held unutilised by the banks changed from 152 to 86 (urban branches 43 and rural branches 43) at the end of the quarter under review as compared to the end of the preceding quarter (Jul.-Sep., 2014). During the quarter under review 56 urban and 70 rural branches licenses were issued. The growth of bank branches of State Owned Banks, Specialised Banks, Foreign Banks and Private Banks is shown in Table-12. Division/Area-wise distribution of bank branches is shown in Table-13. (323,239 males and 8,316,986 females) were organised into groups for providing financial assistance. xxii

23 Table-12 Number of Scheduled Bank Branches Operating in Bangladesh At end of State Owned Banks SpecialisedBanks Foreign Private Banks All Banks the quarter Urban Rural Total Urban Rural Total Banks Urban Rural Total Urban Rural Total 2013 Oct.-Dec % 25.93% 40.53% 2.05% 15.15% 17.20% 0.79% 25.42% 16.05% 41.47% 42.87% 57.13% 100% (0.24) (0.63) (0.49) (0.56) (0.61) (0.61) (4.55) (4.05) (6.74) (5.08) (2.56) (2.27) (2.39) 2014 Jan.-Mar % 25.87% 40.47% 2.03% 15.09% 17.12% 0.79% 25.49% 16.13% 41.62% 42.91% 57.09% 100% (0.47) (0.27) (0.34) (-0.56) (0.08) (0) (0) (0.77) (1) (0.86) (0.59) (0.42) (0.5) Apr.-Jun % 25.70% 40.21% 2.01% 15.00% 17.01% 0.80% 25.57% 16.41% 41.98% 42.89% 57.11% 100% (0.16) (0.09) (0.11) (0) (0.15) (0.13) (1.45) (1.08) (2.49) (1.62) (0.72) (0.78) (0.76) Jul.-Sep % 25.58% 40.02% 2.01% 14.91% 16.92% 0.79% 25.71% 16.57% 42.28% 42.94% 57.06% 100% (0.08) (0.18) (0.14) (0.56) (0) (0.07) (0) (1.16) (1.59) (1.33) (0.74) (0.54) (0.63) Oct.-Dec % 25.12% 39.30% 1.97% 14.62% 16.59% 0.77% 26.11% 17.22% 43.33% 43.03% 56.97% 100% (0.39) (0.31) (0.34) (0) (0.23) (0.2) (0) (3.74) (6.21) (4.7) (2.37) (2) (2.16) Source: Banking Regulation and Policy Department, Bangladesh Bank. Note: 1. Figures in the parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may observe due to rounding off. xxiii

24 Table-13 (Contd.) Region-wise Position of Scheduled Bank Branches Source: Banking Regulation and Policy Department, Bangladesh Bank. Note: 1. Figures in the parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may observe due to rounding off. xxiv

25 Table-13 (Concld.) Region-wise Position of Scheduled Bank Branches Source: Banking Regulation and Policy Department, Bangladesh Bank. Note: 1. Figures in the parentheses represent rates of growth in percent over the preceding quarter. 2. Minor differences may observe due to rounding off. xxv

26 Current and Cash Credit Account Savings Convertible Taka Account of Foreigners Foreign Currency Accounts Wage Earner's Resident Foreign Currency Special Notice Fixed Recurring Other Distributed by Account Types (All Banks) Sep-14 Dec-14 (Taka in Crore) xxvi

27 Agriculture, Fishi ng & Forestry Term Loan Working Capital Financing Construction Transport Trade & Commerce Consumer Finance Others Advances Classified by Economic Purposes (All Banks) Sep-14 Dec-14 (Taka in Crore) xxvii

28 INDICATORS xxviii

29 Weighted Average Rates of Interest on As on Banks All Savings Special Notice Fixed For Less than 6 Months For 6 Months to Less than 1 Year For 1 Year to Less than 2 Years For 2 Years to Less than 3 Years For 3 Years and Above Other All Banks State owned Banks Private Banks (a+b) a) Domestic b) Foreign Specialised Banks Islamic Banks Weighted Average Rates of Interest on Advances By Major Economic Purposes As On Banks All Advances Agriculture Fishing & Forestry Term Loan Industry Working Capital Financing Construc -tion Transport Trade & Commerce Other Institutional Loan Consumer Finance Miscellaneous All Banks State Owned Banks Private Banks (a+b) a) Domestic b) Foreign Specialised Banks Islamic Banks xxix

The names of the scheduled banks whose operations are recorded in this volume are as below:

INTRODUCTION After liberation, the banks operating in Bangladesh (except those incorporated abroad) were nationalised. These banks were merged and grouped into six commercial banks. Of the total six commercial

INTRODUCTION After liberation, the banks operating in Bangladesh (except those incorporated abroad) were nationalised. These banks were merged and grouped into six commercial banks. Of the total six commercial

The names of the Scheduled Banks whose operations are recorded in this volume are as below: A. STATE OWNED BANKS:

INTRODUCTION After liberation, the banks operating in Bangladesh (except those incorporated abroad) were nationalised. These banks were merged and grouped into six commercial banks. Of the total six commercial

INTRODUCTION After liberation, the banks operating in Bangladesh (except those incorporated abroad) were nationalised. These banks were merged and grouped into six commercial banks. Of the total six commercial

The names of the Scheduled Banks whose operations are recorded in this volume are as below: A. STATE OWNED BANKS:

INTRODUCTION After liberation, the banks operating in Bangladesh (except those incorporated abroad) were nationalised. These banks were merged and grouped into six commercial banks. Of the total six commercial

INTRODUCTION After liberation, the banks operating in Bangladesh (except those incorporated abroad) were nationalised. These banks were merged and grouped into six commercial banks. Of the total six commercial

QUARTERLY SCHEDULED BANKS STATISTICS. April-June, 2017 STATISTICS DEPARTMENT BANGLADESH BANK

QUARTERLY SCHEDULED BANKS STATISTICS April-June, 2017 STATISTICS DEPARTMENT BANGLADESH BANK EDITORIAL COMMITTEE CHAIRMAN A.K.M. Fazlul Haque Mia Executive Director (Specialized) MEMBERS Mohammad Ballal

QUARTERLY SCHEDULED BANKS STATISTICS April-June, 2017 STATISTICS DEPARTMENT BANGLADESH BANK EDITORIAL COMMITTEE CHAIRMAN A.K.M. Fazlul Haque Mia Executive Director (Specialized) MEMBERS Mohammad Ballal

Appendix-3. Bangladesh: Some Selected Statistics

Bangladesh: Some Selected Statistics 233 Table-I : Trends of Major Macroeconomic Indicators Indicators FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 R FY15 P 1 2 3 4 5 6 7 8 9 10 11 1. GDP growth (at FY06

Bangladesh: Some Selected Statistics 233 Table-I : Trends of Major Macroeconomic Indicators Indicators FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 R FY15 P 1 2 3 4 5 6 7 8 9 10 11 1. GDP growth (at FY06

Industrial Promotion and Development Company of Bangladesh Limited

Industrial Promotion and Development Company of Bangladesh Limited Unaudited financial statements as at and for the third quarter ended September 30, 2016 Condensed Balance Sheet (Un-audited) as at September

Industrial Promotion and Development Company of Bangladesh Limited Unaudited financial statements as at and for the third quarter ended September 30, 2016 Condensed Balance Sheet (Un-audited) as at September

Developments of Islamic Banking in Bangladesh

Developments of Islamic Banking in Bangladesh January- March, 2017 Quarterly Report Preparation Committee 1 Chairman Dr. Md. Akhtaruzzaman Economic Adviser Coordinator Md. Abdul Awwal Sarker General Manager

Developments of Islamic Banking in Bangladesh January- March, 2017 Quarterly Report Preparation Committee 1 Chairman Dr. Md. Akhtaruzzaman Economic Adviser Coordinator Md. Abdul Awwal Sarker General Manager

GUIDELINES TO FILL IN SBS-1, SBS-2 & SBS-3

DRAFT COPY GUIDELINES TO FILL IN THE BANKING STATISTICS RETURNS SBS-1, SBS-2 & SBS-3 (FIFTH EDITION) STATISTICS DEPARTMENT BANGLADESH BANK HEAD OFFICE DHAKA Request for suggestion/recommendation Any suggestion/recommendation

DRAFT COPY GUIDELINES TO FILL IN THE BANKING STATISTICS RETURNS SBS-1, SBS-2 & SBS-3 (FIFTH EDITION) STATISTICS DEPARTMENT BANGLADESH BANK HEAD OFFICE DHAKA Request for suggestion/recommendation Any suggestion/recommendation

AFTAB AUTOMOBILES LIMITED

AFTAB AUTOMOBILES LIMITED FIRST QUARTERLY REPORT 2018-2019 Dear Shareholder, We are pleased to forward herewith the un-audited Consolidated Statement of Profit or Loss and other Comprehensive Income for

AFTAB AUTOMOBILES LIMITED FIRST QUARTERLY REPORT 2018-2019 Dear Shareholder, We are pleased to forward herewith the un-audited Consolidated Statement of Profit or Loss and other Comprehensive Income for

IDLC Finance Limited. Financial Statements

IDLC Finance Limited Financial Statements as at and for the period ended September 30, 2017 IDLC Finance Limited and Its Subsidiaries Consolidated Balance Sheet (Un-audited) as at September 30, 2017 Note

IDLC Finance Limited Financial Statements as at and for the period ended September 30, 2017 IDLC Finance Limited and Its Subsidiaries Consolidated Balance Sheet (Un-audited) as at September 30, 2017 Note

AB Bank Limited BCIC Bhaban Dilkusha Commercial Area Dhaka AB Bank Limited and its Subsidiaries

AB Bank Limited BCIC Bhaban 30-31 Dilkusha Commercial Area Dhaka 1000 AB Bank Limited and its Subsidiaries Consolidated and separate financial statements for the period ended March 31, 2018 31.03.2018

AB Bank Limited BCIC Bhaban 30-31 Dilkusha Commercial Area Dhaka 1000 AB Bank Limited and its Subsidiaries Consolidated and separate financial statements for the period ended March 31, 2018 31.03.2018

GUIDELINES TO FILL IN THE BANKING STATISTICS RETURNS SBS-1, SBS-2 & SBS-3. (Fifth edition) STATISTICS DEPARTMENT BANGLADESH BANK

STATISTICS DEPARTMENT BANGLADESH BANK") GUIDELINES TO FILL IN THE BANKING STATISTICS RETURNS SBS-1, SBS-2 & SBS-3 (Fifth edition) STATISTICS DEPARTMENT BANGLADESH BANK July 2013 Editorial Committee 1. Md. Nur-un-Nabi General Manager 2. Md. Lutful

GUIDELINES TO FILL IN THE BANKING STATISTICS RETURNS SBS-1, SBS-2 & SBS-3 (Fifth edition) STATISTICS DEPARTMENT BANGLADESH BANK July 2013 Editorial Committee 1. Md. Nur-un-Nabi General Manager 2. Md. Lutful

Developments of Islamic Banking in Bangladesh April-June, 2015

Developments of Islamic Banking in Bangladesh April-June, 2015 Research Department Bangladesh Bank 1 Quarterly Report Preparation Committee 1 Chairman Dr. Md. Akhtaruzzaman Economic Adviser Coordinator

Developments of Islamic Banking in Bangladesh April-June, 2015 Research Department Bangladesh Bank 1 Quarterly Report Preparation Committee 1 Chairman Dr. Md. Akhtaruzzaman Economic Adviser Coordinator

Major Economic Indicators

Volume: 11/2015 Major Economic Indicators Monthly Update: November 2015 Major Economic Indicators Monetary Policy Department Bangladesh Bank Contents Page No. Executive summary.. 1-2 1. Monetary and credit

Volume: 11/2015 Major Economic Indicators Monthly Update: November 2015 Major Economic Indicators Monetary Policy Department Bangladesh Bank Contents Page No. Executive summary.. 1-2 1. Monetary and credit

Prospectus Rules. Chapter 2. Drawing up the prospectus

Prospectus Rules Chapter Drawing up the PR : Drawing up the included in a.3 Minimum information to be included in a.3.1 EU Minimum information... Articles 3 to 3 of the PD Regulation provide for the minimum

Prospectus Rules Chapter Drawing up the PR : Drawing up the included in a.3 Minimum information to be included in a.3.1 EU Minimum information... Articles 3 to 3 of the PD Regulation provide for the minimum

Industrial Promotion and Development Company of Bangladesh Limited

Industrial Promotion and Development Company of Bangladesh Limited Un-audited Financial Statements as at and for the half year ended 30 June 2011 Industrial Promotion and Development Company of Bangladesh

Industrial Promotion and Development Company of Bangladesh Limited Un-audited Financial Statements as at and for the half year ended 30 June 2011 Industrial Promotion and Development Company of Bangladesh

Industrial Promotion and Development Company of Bangladesh Limited

Industrial Promotion and Development Company of Bangladesh Limited Un-audited Financial Statements as at and for the month ended 30 September 2011 Industrial Promotion and Development Company of Bangladesh

Industrial Promotion and Development Company of Bangladesh Limited Un-audited Financial Statements as at and for the month ended 30 September 2011 Industrial Promotion and Development Company of Bangladesh

STATISTICS ON SCHEDULED BANKS IN PAKISTAN

STATISTICS ON SCHEDULED BANKS IN PAKISTAN June 2013 STATE BANK OF PAKISTAN STATISTICS & DATA WAREHOUSE DEPARTMENT www.sbp.org.pk Our Mission To promote monetary and financial stability and foster a sound

STATISTICS ON SCHEDULED BANKS IN PAKISTAN June 2013 STATE BANK OF PAKISTAN STATISTICS & DATA WAREHOUSE DEPARTMENT www.sbp.org.pk Our Mission To promote monetary and financial stability and foster a sound

AIRCRAFT FINANCE TRUST ASSET BACKED NOTES, SERIES MONTHLY REPORT TO NOTEHOLDERS All amounts in US dollars unless otherwise stated

Payment Date 15th of each month Convention Modified Following Business Day Current Payment Date July 17, 2006 Current Calculation Date July 11, 2006 Previous Calculation Date June 9, 2006 1. Account Activity

Payment Date 15th of each month Convention Modified Following Business Day Current Payment Date July 17, 2006 Current Calculation Date July 11, 2006 Previous Calculation Date June 9, 2006 1. Account Activity

CURRICULUM MAPPING FORM

Course Accounting 1 Teacher Mr. Garritano Aug. I. Starting a Proprietorship - 2 weeks A. The Accounting Equation B. How Business Activities Change the Accounting Equation C. Reporting Financial Information

Course Accounting 1 Teacher Mr. Garritano Aug. I. Starting a Proprietorship - 2 weeks A. The Accounting Equation B. How Business Activities Change the Accounting Equation C. Reporting Financial Information

Major Economic Indicators: Monthly Update

Volume 08/2018 August 2018 BANGLADESH BANK Contents Page No. Executive summary 1-2 1. Monetary and credit developments 3 2. Reserve money developments 4 3. CPI and inflation 5 4. Liquidity position of

Volume 08/2018 August 2018 BANGLADESH BANK Contents Page No. Executive summary 1-2 1. Monetary and credit developments 3 2. Reserve money developments 4 3. CPI and inflation 5 4. Liquidity position of

IPDC of Bangladesh Limited Condensed Interim Financial Statements (Un-audited) As at and for the third quarter ended September 30, 2015

As at and for the third quarter ended September 30, 2015") Condensed Interim Financial Statements (Un-audited) As at and for the third quarter ended September 30, 2015 Condensed Balance Sheet (Un-audited) as at September 30, 2015 30 September 31 December As at

Condensed Interim Financial Statements (Un-audited) As at and for the third quarter ended September 30, 2015 Condensed Balance Sheet (Un-audited) as at September 30, 2015 30 September 31 December As at

Major Economic Indicators: Monthly Update

Volume 05/2018 May 2018 Major Economic Indicators: Monthly Update Monetary Policy Department BANGLADESH BANK Contents Page No. Executive summary 1-2 1. Monetary and credit developments 3 2. Reserve money

Volume 05/2018 May 2018 Major Economic Indicators: Monthly Update Monetary Policy Department BANGLADESH BANK Contents Page No. Executive summary 1-2 1. Monetary and credit developments 3 2. Reserve money

Major Economic Indicators: Monthly Update

Volume 12/2017 December 2017 Major Economic Indicators: Monthly Update Monetary Policy Department BANGLADESH BANK Contents Page No. Executive summary 1-2 1. Monetary and credit developments 3 2. Reserve

Volume 12/2017 December 2017 Major Economic Indicators: Monthly Update Monetary Policy Department BANGLADESH BANK Contents Page No. Executive summary 1-2 1. Monetary and credit developments 3 2. Reserve

Major Economic Indicators: Monthly Update

Volume 03/2018 March 2018 Major Economic Indicators: Monthly Update Monetary Policy Department BANGLADESH BANK Contents Page No. Executive summary 1-2 1. Monetary and credit developments 3 2. Reserve money

Volume 03/2018 March 2018 Major Economic Indicators: Monthly Update Monetary Policy Department BANGLADESH BANK Contents Page No. Executive summary 1-2 1. Monetary and credit developments 3 2. Reserve money

Southeast Bank Limited

Southeast Bank Limited Report and financial statements for the year ended 31 December 2005 Auditors' report to the shareholders of Southeast Bank Limited We have audited the accompanying balance sheet

Southeast Bank Limited Report and financial statements for the year ended 31 December 2005 Auditors' report to the shareholders of Southeast Bank Limited We have audited the accompanying balance sheet

BRAC BANK LIMITED. Consolidated Balance Sheet As on March 31, Note March-2011 December-2010

BRAC BANK LIMITED Consolidated Balance Sheet As on March 31, 2011 Note March-2011 December-2010 PROPERTY AND ASSETS Cash 3.a 12,206,515,582 9,853,046,265 Cash in hand 3,542,987,674 3,578,604,502 (Including

BRAC BANK LIMITED Consolidated Balance Sheet As on March 31, 2011 Note March-2011 December-2010 PROPERTY AND ASSETS Cash 3.a 12,206,515,582 9,853,046,265 Cash in hand 3,542,987,674 3,578,604,502 (Including

Major Economic Indicators: Monthly Update

Volume 02/2018 February 2018 Major Economic Indicators: Monthly Update Monetary Policy Department BANGLADESH BANK Contents Page No. Executive summary 1-2 1. Monetary and credit developments 3 2. Reserve

Volume 02/2018 February 2018 Major Economic Indicators: Monthly Update Monetary Policy Department BANGLADESH BANK Contents Page No. Executive summary 1-2 1. Monetary and credit developments 3 2. Reserve

Aftab Automobiles Limited and its Subsidiary Un-Audited consolidated Statement of Profit or Loss and other Comprehensive Income

Aftab Automobiles Limited 2nd Quarter (Half-yearly ) Report 2018-2019 Dear Shareholders, We are pleased to forward herewith the un-audited Consolidated Statement of Profit or Loss and other Comprehensive

Aftab Automobiles Limited 2nd Quarter (Half-yearly ) Report 2018-2019 Dear Shareholders, We are pleased to forward herewith the un-audited Consolidated Statement of Profit or Loss and other Comprehensive

Industrial Promotion and Development Company of Bangladesh Limited

Industrial Promotion and Development Company of Bangladesh Limited Un-audited Financial statements as at and for the first quarter ended 31 March 2011 Industrial Promotion and Development Company of Bangladesh

Industrial Promotion and Development Company of Bangladesh Limited Un-audited Financial statements as at and for the first quarter ended 31 March 2011 Industrial Promotion and Development Company of Bangladesh

GRUPO FINANCIERO GALICIA S.A. REPORTS FINANCIAL RESULTS FOR THE QUARTER AND FISCAL YEAR ENDED DECEMBER 31, 2014

FOR IMMEDIATE RELEASE For more information contact: Pedro A. Richards Chief Executive Officer Telefax: (5411) 4343-7528 investors@gfgsa.com www.gfgsa.com GRUPO FINANCIERO GALICIA S.A. REPORTS FINANCIAL

FOR IMMEDIATE RELEASE For more information contact: Pedro A. Richards Chief Executive Officer Telefax: (5411) 4343-7528 investors@gfgsa.com www.gfgsa.com GRUPO FINANCIERO GALICIA S.A. REPORTS FINANCIAL

International Monetary Fund Washington, D.C.

2007 International Monetary Fund June 2007 IMF Country Report No. 07/229 Bangladesh: Statistical Appendix This Statistical Appendix for Bangladesh was prepared by a staff team of the International Monetary

2007 International Monetary Fund June 2007 IMF Country Report No. 07/229 Bangladesh: Statistical Appendix This Statistical Appendix for Bangladesh was prepared by a staff team of the International Monetary

SECOND-QUARTER 2017 FINANCIAL REVIEW. July 25, 2017

SECOND-QUARTER 2017 FINANCIAL REVIEW July 25, 2017 FORWARD-LOOKING STATEMENTS Forward-looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking

SECOND-QUARTER 2017 FINANCIAL REVIEW July 25, 2017 FORWARD-LOOKING STATEMENTS Forward-looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking

LONG TERM (SUBORDINATED) DEPOSITS- SERIES-II

DEPOSITS- SERIES-II") Regd. Office :Mohan Terrace. 64/72, Mody Street, Mumbai- 400 001 Central Office: MARUTAGIRI, Plot No. 13/9A, Samant Estate, Sonawala Road, Goregaon (East), Mumbai- 400 063 Contact: 022-6189 0000 (B) Email:

Regd. Office :Mohan Terrace. 64/72, Mody Street, Mumbai- 400 001 Central Office: MARUTAGIRI, Plot No. 13/9A, Samant Estate, Sonawala Road, Goregaon (East), Mumbai- 400 063 Contact: 022-6189 0000 (B) Email:

STATISTICS ON SCHEDULED BANKS IN PAKISTAN

STATISTICS ON SCHEDULED BANKS IN PAKISTAN June 2010 STATE BANK OF PAKISTAN STATISTICS & DATAWARE HOUSE DEPARTMENT www.sbp.org.pk Our Mission To promote monetary and financial stability and foster a sound

STATISTICS ON SCHEDULED BANKS IN PAKISTAN June 2010 STATE BANK OF PAKISTAN STATISTICS & DATAWARE HOUSE DEPARTMENT www.sbp.org.pk Our Mission To promote monetary and financial stability and foster a sound

AFTAB AUTOMOBILES LIMITED

AFTAB AUTOMOBILES LIMITED FIRST QUARTERLY REPORT 2016-2017 Dear Shareholder, As per SEC-Notification No. SEC/CMRRCD/2008-183/Admin/03-34 dated September 27,2009, we are pleased to forward herewith the

AFTAB AUTOMOBILES LIMITED FIRST QUARTERLY REPORT 2016-2017 Dear Shareholder, As per SEC-Notification No. SEC/CMRRCD/2008-183/Admin/03-34 dated September 27,2009, we are pleased to forward herewith the

Dutch-Bangla Bank Limited Balance Sheet As at 30 September 2017 (Main Operation and Off-shore Banking Unit)

") PROPERTY AND ASSETS Notes 30-Sep-17 31-Dec-16 30-Sep-16 (Audited) (Un-audited) Main Operation Off-shore Total Total Total Cash In hand (including foreign currencies) 4 13,529,861,916-13,529,861,916 11,051,999,011

PROPERTY AND ASSETS Notes 30-Sep-17 31-Dec-16 30-Sep-16 (Audited) (Un-audited) Main Operation Off-shore Total Total Total Cash In hand (including foreign currencies) 4 13,529,861,916-13,529,861,916 11,051,999,011

Bank AL Habib Limited Schedule of Bank Charges ISLAMIC BANKING

Bank AL Habib Limited Schedule of Bank Charges ISLAMIC BANKING (Excluding FED Charges) Effective From January 01, 2019 to June 30, 2019 Bank AL Habib Limited Page 1 of 10 I N T E R N A T I O N A L A. IMPORTS:

Bank AL Habib Limited Schedule of Bank Charges ISLAMIC BANKING (Excluding FED Charges) Effective From January 01, 2019 to June 30, 2019 Bank AL Habib Limited Page 1 of 10 I N T E R N A T I O N A L A. IMPORTS:

Ordinance on Terminology, Forms, and Preparation Methods of Consolidated Financial Statements

Ordinance on Terminology, Forms, and Preparation Methods of Consolidated Financial Statements (Ordinance of the Ministry of Finance No. 28 of October 30, 1976) Pursuant to the provisions of Article 193

Ordinance on Terminology, Forms, and Preparation Methods of Consolidated Financial Statements (Ordinance of the Ministry of Finance No. 28 of October 30, 1976) Pursuant to the provisions of Article 193

STATISTICS ON SCHEDULED BANKS IN PAKISTAN

STATISTICS ON SCHEDULED BANKS IN PAKISTAN June 2017 STATE BANK OF PAKISTAN STATISTICS & DATA WAREHOUSE DEPARTMENT www.sbp.org.pk Our Mission To promote monetary and financial stability and foster a sound

STATISTICS ON SCHEDULED BANKS IN PAKISTAN June 2017 STATE BANK OF PAKISTAN STATISTICS & DATA WAREHOUSE DEPARTMENT www.sbp.org.pk Our Mission To promote monetary and financial stability and foster a sound

STATISTICS ON SCHEDULED BANKS IN PAKISTAN

STATISTICS ON SCHEDULED BANKS IN PAKISTAN December 2017 STATE BANK OF PAKISTAN STATISTICS & DATA WAREHOUSE DEPARTMENT www.sbp.org.pk Our Mission To promote monetary and financial stability and foster a

STATISTICS ON SCHEDULED BANKS IN PAKISTAN December 2017 STATE BANK OF PAKISTAN STATISTICS & DATA WAREHOUSE DEPARTMENT www.sbp.org.pk Our Mission To promote monetary and financial stability and foster a

BANK MELLAT, HEAD OFFICE: TAHRAN-IRAN İSTANBUL TURKEY MAIN, ANKARA AND İZMİR BRANCHES INDEPENDENT AUDITOR S REPORT, FINANCIAL STATEMENTS AND NOTES

BANK MELLAT, HEAD OFFICE: TAHRAN-IRAN İSTANBUL TURKEY MAIN, ANKARA AND İZMİR BRANCHES INDEPENDENT AUDITOR S REPORT, FINANCIAL STATEMENTS AND NOTES FOR THE YEAR ENDED 31 DECEMBER 2017 (TRANSLATED INTO ENGLISH

BANK MELLAT, HEAD OFFICE: TAHRAN-IRAN İSTANBUL TURKEY MAIN, ANKARA AND İZMİR BRANCHES INDEPENDENT AUDITOR S REPORT, FINANCIAL STATEMENTS AND NOTES FOR THE YEAR ENDED 31 DECEMBER 2017 (TRANSLATED INTO ENGLISH

Tk per instance excluding DPS & Loan Installment Payment No charge for Defence Personnel & TBL Employees

Sl Description Schedule of s - 2012 A A1 General Banking & Local Remittance Current Accounts/Al-Wadiah: A1-i Incidental A1-ii Account Maintenance Fee Tk.500 (Half Yearly) A1-iii Account closing charge

Sl Description Schedule of s - 2012 A A1 General Banking & Local Remittance Current Accounts/Al-Wadiah: A1-i Incidental A1-ii Account Maintenance Fee Tk.500 (Half Yearly) A1-iii Account closing charge

IPDC of Bangladesh Limited Condensed Financial Statements (Un-audited) For the Third Quarter Ended September 30, 2012

For the Third Quarter Ended September 30, 2012") Condensed Financial Statements (Un-audited) For the Third Quarter Ended September 30, 2012 Condensed Balance Sheet (Un-audited) as at September 30, 2012 September 30, December 31, As at Note 2012 2011

Condensed Financial Statements (Un-audited) For the Third Quarter Ended September 30, 2012 Condensed Balance Sheet (Un-audited) as at September 30, 2012 September 30, December 31, As at Note 2012 2011

OFFER DOCUMENT ISSUE OF LONG TERM (SUBORDINATED) DEPOSITS (LTD) (Series-V) UNDER LOWER TIER - II CAPITAL.

DEPOSITS (LTD) (Series-V) UNDER LOWER TIER - II CAPITAL.") Registered and Corporate Office:- Corporate Center, Ekanath Thakur Bhavan, Plot No. 953, Appasaheb Marathe Marg, Prabhadevi, Mumbai - 400 025 Tel. No. : +91-22 - 6600 5555 Website : www.saraswatbank.com

Registered and Corporate Office:- Corporate Center, Ekanath Thakur Bhavan, Plot No. 953, Appasaheb Marathe Marg, Prabhadevi, Mumbai - 400 025 Tel. No. : +91-22 - 6600 5555 Website : www.saraswatbank.com

CUSTOMERS. PEOPLE. PARTNERS.

THIRD-QUARTER 2017 FINANCIAL REVIEW October 24, 2017 CUSTOMERS. PEOPLE. PARTNERS. FORWARD-LOOKING STATEMENTS Forward-looking Statements Certain statements in this financial review relate to future events

THIRD-QUARTER 2017 FINANCIAL REVIEW October 24, 2017 CUSTOMERS. PEOPLE. PARTNERS. FORWARD-LOOKING STATEMENTS Forward-looking Statements Certain statements in this financial review relate to future events

Terms and Conditions for 328 Business Banking:

Terms and Conditions for 328 Business Banking: General Terms & Conditions: 1. Dah Sing Bank, Limited (the Bank ) and Dah Sing Insurance Company (1976) Limited ( Dah Sing Insurance ) reserve the right to

Terms and Conditions for 328 Business Banking: General Terms & Conditions: 1. Dah Sing Bank, Limited (the Bank ) and Dah Sing Insurance Company (1976) Limited ( Dah Sing Insurance ) reserve the right to

DETERMINANTS OF PROFITABILITY OF PRIVATE COMMERCIAL BANKS IN BANGLADESH: AN EMPIRICAL STUDY Presented by Bhaskar Podder ST

DETERMINANTS OF PROFITABILITY OF PRIVATE COMMERCIAL BANKS IN BANGLADESH: AN EMPIRICAL STUDY Presented by Bhaskar Podder ST 112289 Examination Committee Dr. Sundar Venkatesh(Chairperson) Dr. Winai Wongsurawat(Co-chair)

DETERMINANTS OF PROFITABILITY OF PRIVATE COMMERCIAL BANKS IN BANGLADESH: AN EMPIRICAL STUDY Presented by Bhaskar Podder ST 112289 Examination Committee Dr. Sundar Venkatesh(Chairperson) Dr. Winai Wongsurawat(Co-chair)

(CONVENIENCE TRANSLATION OF FINANCIAL STATEMENTS)

") BALANCE SHEET AS OF SEPTEMBER 30, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 30.09.2018 I. FINANCIAL ASSETS (Net) 36.351.297 34.145.223 70.496.520 1.1 Cash and cash equivalents 2.216.435

BALANCE SHEET AS OF SEPTEMBER 30, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 30.09.2018 I. FINANCIAL ASSETS (Net) 36.351.297 34.145.223 70.496.520 1.1 Cash and cash equivalents 2.216.435

(CONVENIENCE TRANSLATION OF FINANCIAL STATEMENTS)

") BALANCE SHEET AS OF DECEMBER 31, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 31.12.2018 I. FINANCIAL ASSETS (Net) 26.600.080 27.411.488 54.011.568 1.1 Cash and cash equivalents 2.537.892

BALANCE SHEET AS OF DECEMBER 31, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 31.12.2018 I. FINANCIAL ASSETS (Net) 26.600.080 27.411.488 54.011.568 1.1 Cash and cash equivalents 2.537.892

(CONVENIENCE TRANSLATION OF FINANCIAL STATEMENTS)

") BALANCE SHEET AS OF DECEMBER 31, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 31.12.2018 I. FINANCIAL ASSETS (Net) 26.245.952 27.373.211 53.619.163 1.1 Cash and cash equivalents 2.125.340

BALANCE SHEET AS OF DECEMBER 31, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 31.12.2018 I. FINANCIAL ASSETS (Net) 26.245.952 27.373.211 53.619.163 1.1 Cash and cash equivalents 2.125.340

GRUPO FINANCIERO GALICIA S.A. REPORTS FINANCIAL RESULTS FOR THE QUARTER AND THE FISCAL YEAR ENDED DECEMBER 31, 2017

FOR IMMEDIATE RELEASE For more information contact: José Luis Ronsini CFO Grupo Financiero Galicia S.A. Telephone: (5411) 4343-7528 Pablo Firvida Institutional Relations Manager Tel.: (54-11) 6329-4881

FOR IMMEDIATE RELEASE For more information contact: José Luis Ronsini CFO Grupo Financiero Galicia S.A. Telephone: (5411) 4343-7528 Pablo Firvida Institutional Relations Manager Tel.: (54-11) 6329-4881

DRAFT COPY GUIDELINES TO FILL IN THE NBFI RETURNS-1, 2 & 3. PART- 1 (NBFI-1 Return)

") DRAFT COPY GUIDELINES TO FILL IN THE NBFI RETURNS-1, 2 & 3 PART- 1 (NBFI-1 Return) CHAPTER 1. INTRODUCTION AND GENERAL INSTRUCTIONS 1.1 Introduction: NBFIs include all depository and non-depository institutions.

DRAFT COPY GUIDELINES TO FILL IN THE NBFI RETURNS-1, 2 & 3 PART- 1 (NBFI-1 Return) CHAPTER 1. INTRODUCTION AND GENERAL INSTRUCTIONS 1.1 Introduction: NBFIs include all depository and non-depository institutions.

Certificate Course on Concurrent Audit of Banks

Certificate Course on Concurrent Audit of Banks Organized by: Internal Audit Standards Board of the ICAI Hosted By... Dates : Date Day 1 9:45 AM to 10:00 AM Inaugural Session I II III Effective Concurrent

Certificate Course on Concurrent Audit of Banks Organized by: Internal Audit Standards Board of the ICAI Hosted By... Dates : Date Day 1 9:45 AM to 10:00 AM Inaugural Session I II III Effective Concurrent

Prospectus Rules. Chapter 2. Drawing up the prospectus

Prospectus ules Chapter Drawing up the Section.1 : General contents of.1 General contents of.1.1 UK General contents of... Sections 87A(), (A), (3) and (4) of the Act provide for the general contents of

Prospectus ules Chapter Drawing up the Section.1 : General contents of.1 General contents of.1.1 UK General contents of... Sections 87A(), (A), (3) and (4) of the Act provide for the general contents of

SME BUSINESS BAROMETER AUGUST 2011 OCTOBER Report prepared for the Department of Business, Innovation and Skills

SME BUSINESS BAROMETER AUGUST 2011 OCTOBER 2011 Report prepared for the Department of Business, Innovation and Skills 1 1 Introduction Background 1.1 The Business Barometer is a series of surveys among

SME BUSINESS BAROMETER AUGUST 2011 OCTOBER 2011 Report prepared for the Department of Business, Innovation and Skills 1 1 Introduction Background 1.1 The Business Barometer is a series of surveys among

Internship Report. Analysis of Banking Industry & Janata Bank Limited

Internship Report On Analysis of Banking Industry & Janata Bank Limited Analysis of Banking Industry & Janata Bank Limited : An Internship Report Submitted to: Dr. Md. Mohan Uddin Professor Submitted by:

Internship Report On Analysis of Banking Industry & Janata Bank Limited Analysis of Banking Industry & Janata Bank Limited : An Internship Report Submitted to: Dr. Md. Mohan Uddin Professor Submitted by:

SECURITIES AND EXCHANGE COMMISSION OF PAKISTAN NOTIFICATION CHAPTER I PRELIMINARY

SECURITIES AND EXCHANGE COMMISSION OF PAKISTAN NOTIFICATION Islamabad, the 28 th September, 2012 S.R.O.1223(I)/2012. In exercise of the powers conferred by section 506A of the Companies Ordinance, 1984

SECURITIES AND EXCHANGE COMMISSION OF PAKISTAN NOTIFICATION Islamabad, the 28 th September, 2012 S.R.O.1223(I)/2012. In exercise of the powers conferred by section 506A of the Companies Ordinance, 1984

AGREEMENT ON SOCIAL SECURITY BETWEEN THE GOVERNMENT OF CANADA AND THE GOVERNMENT OF SWEDEN

AGREEMENT ON SOCIAL SECURITY BETWEEN THE GOVERNMENT OF CANADA AND THE GOVERNMENT OF SWEDEN The Government of Canada and the Government of Sweden, Resolved to continue their co-operation in the field of

AGREEMENT ON SOCIAL SECURITY BETWEEN THE GOVERNMENT OF CANADA AND THE GOVERNMENT OF SWEDEN The Government of Canada and the Government of Sweden, Resolved to continue their co-operation in the field of

Balance Sheet as at March 31, 2010

Balance Sheet as at March 31, 2010 Schedule I Sources of Funds 1 Shareholders Funds (a) Share Capital 1 800,000 800,000 (b) Reserves and Surplus 2 2,535,679 3,335,679 1,987,532 2,787,532 Total 3,335,679

Balance Sheet as at March 31, 2010 Schedule I Sources of Funds 1 Shareholders Funds (a) Share Capital 1 800,000 800,000 (b) Reserves and Surplus 2 2,535,679 3,335,679 1,987,532 2,787,532 Total 3,335,679

Supply of and Demand for Financial Products

Chapter 2 Supply of and Demand for Financial Products 2.1 Payment and Transaction Products Payment and transaction products play key roles in smoothing retail banking and settling payment obligations in

Chapter 2 Supply of and Demand for Financial Products 2.1 Payment and Transaction Products Payment and transaction products play key roles in smoothing retail banking and settling payment obligations in

Research Department Bangladesh Bank

Monthly Report On Government Borrowing from Domestic Sources 1 July-June, FY'17 Research Department Bangladesh Bank 1 The report has been prepared by Money and Banking Division, Research Department, Bangladesh

Monthly Report On Government Borrowing from Domestic Sources 1 July-June, FY'17 Research Department Bangladesh Bank 1 The report has been prepared by Money and Banking Division, Research Department, Bangladesh

STATEMENT OF FINANCIAL POSITION (Un-Audited) AS AT 30 SEPTEMBER 2017

AS AT 30 SEPTEMBER 2017") ASSETS 30-Jun-17 Non-Current Assets 492,403,341 499,553,402 Property, Plant and Equipment 4 486,845,593 493,565,277 Investment in Shares 5 5,557,748 5,988,125 Current Assets 174,706,966 62,573,551 Inventories

ASSETS 30-Jun-17 Non-Current Assets 492,403,341 499,553,402 Property, Plant and Equipment 4 486,845,593 493,565,277 Investment in Shares 5 5,557,748 5,988,125 Current Assets 174,706,966 62,573,551 Inventories

Input Tax Credit Review Audit GST

Input Tax Credit Review Audit GST DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed

Input Tax Credit Review Audit GST DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed

Market Discipline Disclosures on Risk Based Capital (Basel II) as on

as on") Market Discipline Disclosures on Risk Based Capital (Basel II) as on 31.12.2013 The purpose of Market Discipline in Basel- II is to establish more transparent and more disciplined financial market so that

Market Discipline Disclosures on Risk Based Capital (Basel II) as on 31.12.2013 The purpose of Market Discipline in Basel- II is to establish more transparent and more disciplined financial market so that

FIRST QUARTER FINANCIAL STATEMENT (UN-AUDITED)

") FIRST QUARTER FINANCIAL STATEMENT (UN-AUDITED) FOR THE PERIOD ENDED 30 TH SEPTEMBER 2016 CVO PETROCHEMICAL REFINERY LIMITED STATEMENT OF FINANCIAL POSITION (Un-Audited) AS AT 30 SEPTEMBER 2016 ASSETS 30-Sep-16

FIRST QUARTER FINANCIAL STATEMENT (UN-AUDITED) FOR THE PERIOD ENDED 30 TH SEPTEMBER 2016 CVO PETROCHEMICAL REFINERY LIMITED STATEMENT OF FINANCIAL POSITION (Un-Audited) AS AT 30 SEPTEMBER 2016 ASSETS 30-Sep-16

Quarterly Statistical Digest

Quarterly Statistical Digest February 2019 Volume 28, No. 1 The Statistical Digest is a quarterly publication of the Central Bank of The Bahamas, prepared by the Research Department for issue in February,

Quarterly Statistical Digest February 2019 Volume 28, No. 1 The Statistical Digest is a quarterly publication of the Central Bank of The Bahamas, prepared by the Research Department for issue in February,

SECURITIES AND EXCHANGE COMMISSION Consolidated quarterly report QSr 1 / 2005

SECURITIES AND EXCHANGE COMMISSION Consolidated quarterly report QSr 1 / 2005 Pursuant to 93 section 2 and 94 section 1 of the Regulation of the Council of Ministers of March 21, 2005 (Journal of Laws