Welcome to our Mortgage Fundamentals CE Class!

|

|

|

- Marianna Powell

- 5 years ago

- Views:

Transcription

1 Welcome to our Mortgage Fundamentals CE Class! 1

2 Mortgage Fundamentals CE Course, brought to you by: Mike Porter, President Red Diamond Home Loans Justin Rogers Mortgage Originator Red Diamond Home Loans Whitney Vallenari Chicago Title Ray Scott State Farm Insurance

Pre-Qualification, vs Pre-approval vs Loan Approval vs.")

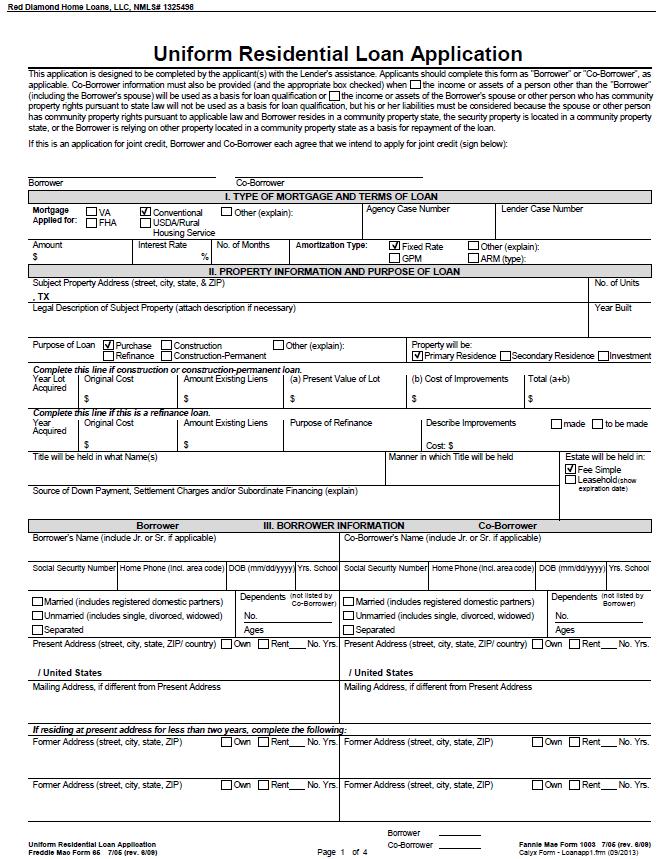

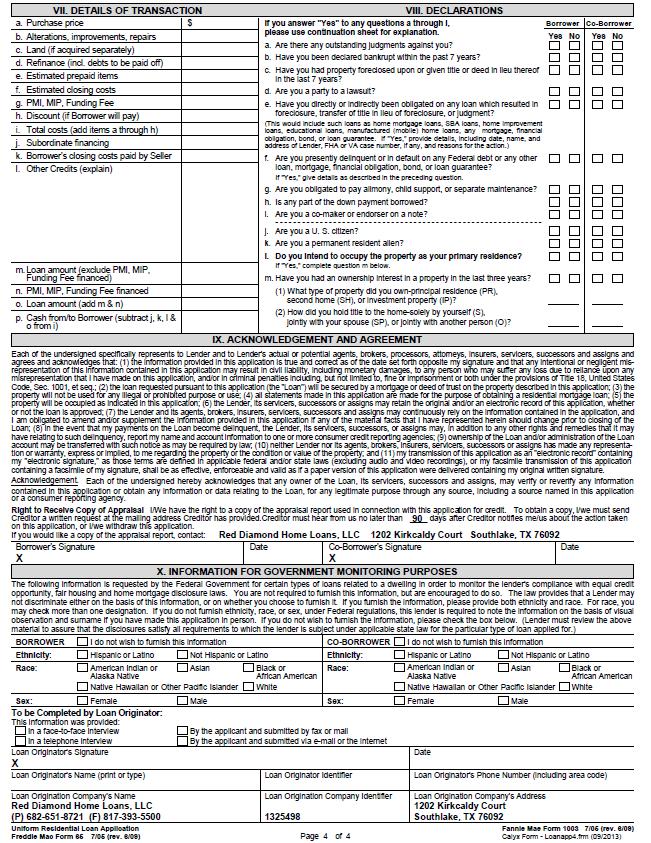

3 Interim Financing Loan Types and Programs Conventional (Conforming & Non-Conforming) Government (FHA, VA) The First Steps The 1003 Form (see attached) Captures a wide variety of borrower information. (A new application will be rolled out in 2018) Pre-Qualification, vs Pre-approval vs Loan Approval vs. Clear to Close The 4 C s (Credit, Capacity, Capital and Collateral) 3

4 Interim Financing The Loan Application Where it all begins Today it s called a 1003 or Uniform Loan Application Main Categories: I. Type of Mortgage and Term of Loan II. Property Info and Loan Purpose III. Borrower Info - Residency IV. Employment Info V. Monthly Income and combined housing expense VI. Assets & Liabilities VII. Details of transaction VIII. Declarations IX. Acknowledgment & Agreement X. Government Monitoring Info 4

5 5

6 6

7 Interim Financing What is the difference between a conditional approval, pre-qualification, pre-approval, approval, final approval, clear to close? Conditional approval/pre-qualification Red Diamond can provide this same day. What can go wrong: Income turns out different than the borrower provided. The client does not have the cash to close. There was declining income. Initial Underwriting approval: Final Approval & Clear to Close: 7

8 Who provides the underwriting guidelines for Mortgage loans: Who are these entities and what do they do? Fannie Mae & Freddie Mac FHA VA Non QM What are the options? The risk is transferred to these entities because the file was underwritten to their guidelines. 8

9 Interim Financing The 4 C s let s discuss at a high level Credit Minimum credit score Capacity Debt to income ratio Capital Down payment/cash to close Collateral Appraisal 9

Capital: Asset")

10 Data and documents are transformed into a closed loan. Documentation Validation 4 C s again: Credit: Minimum credit score for program requirements (Mid Fico of both borrowers) LLPA s? Capacity: Income documentation for debt to income calculation (W-2 s, Tax Returns, K-1 s) Capital: Asset documentation (Bank Statements) for down payment and reserve requirements Collateral: The appraisal must meets underwriting requirements 10

11 4 C s and Conventional Loans: Minimum credit score is 620 (no exceptions) Max debt to income roughly 45 Down payment can be a minimum of 3% but most common minimum is 5% Appraisal standards are set by Fannie Mae. They purchase owner occupied and non owner occupied properties. 4-C s and FHA Loans: Minimum score is 580 Maximum debt to income is 55% Down payment is 3.5% Appraisals are completed by FHA approved appraisers. 4 C s and VA Loans: Typical minimum of a 620 score. Maximum debt to income can be as high as 55%. There typically is not a down payment requirement except on higher balance VA loans over $424,100. Appraisals are completed by VA approved appraisers. 11

12 Delinquent credit Collections & charge-offs Foreclosures Bankruptcy s Disputed Accounts How to clean up your credit? - Rising Point Solutions/Abe K is one example The removal of any derogatory item is the key. 12

13 High credit scores have a low cost of PMI, The higher the LTV the higher the PMI cost. MIP does not factor in the credit score. VA does not factor in the credit score 13

14 Maxwell makes Mortgages easy! 14

15 15

16 Manufacturing the loan means putting a complete file together: Minimum credit score - Maximum Debt to Income Maximum Loan to Value - Loan must by approved by the automated underwriting system Two year history required for income - 60 days of bank statements required - Most recent 30 days of paystubs Tax Returns for Self Employed borrowers All of these factors and more go into the loan approval. All situations are different and specific issues will raise other conditions 16

17 Underwriting Process Overview: Typical turn times are 48 hours for an initial review and 24 hours for the resubmission of conditions. Underwriters want a full, complete package to review. The underwriters job is to validate the accuracy of the documentation provided. Mortgage Companies work toward a Final Approval status or a Clear to Close status with underwriting Underwriters evaluate loans according to a set of guidelines from Fannie Mae, Freddie Mac, FHA or VA. Each entity/agency has their own set of very specific guidelines that must be followed. We talk to the underwriter to make sure they fully understand the file and the situation 17

18 18

19 How fast can we close? Red Diamond Closed a Conventional Purchase 12 days after the contract was receipted. August 8 August 24. We had all borrower documents, just needed the appraisal. This timeline depends upon the client and their ability to move quickly and provide the documents that we need 19

20 The Secondary Market for Mortgages: What is the secondary market? Who funds the mortgage market? Who buys Fannie Mae, Freddie Mac, FHA/VA loans? How are they sold? Who does Wall Street sell the mortgage banked securities to? The mortgage market is loaded with participants from Main Street to Wall Street 20

21 Choose your business partners carefully Not all partners are the same 21

22 Manufacturing a Mortgage 1. Application 10. Loan Servicing 2. Conditional Approval 9. Secondary Market 3. Processing/Data Gathering 8. Loan Delivery 7. Warehouse Funding 4. Underwriting 6. Client Signing 5. Clear to Close 6. Doc Prep/Closing Neal Creative Neal Creative click & Learn more

23 In Summary: Thanks for your time and attention today. Hopefully you benefitted from this presentation. Justin is available anytime for a pre-approval, question or any type of client consultation. 23

24 24

25 Thanks for you time! Mike Porter, President Red Diamond Home Loans Justin Rogers Mortgage Originator Red Diamond Home Loans Whitney Vallenari Chicago Title Ray Scott State Farm Insurance

Table of Contents. Book 1. Book 4. Book 2. Book 5. Book 3. The Mortgage Cycle & Its Key Players Regulatory Compliance Loan Types & Programs

1 Table of Contents Book 1 The Mortgage Cycle & Its Key Players Regulatory Compliance Loan Types & Programs Book 2 Taking the Loan Application Book 3 Processing the Loan Automated Underwriting Uniform

1 Table of Contents Book 1 The Mortgage Cycle & Its Key Players Regulatory Compliance Loan Types & Programs Book 2 Taking the Loan Application Book 3 Processing the Loan Automated Underwriting Uniform

Practical Application. Pre-qualified - Buyer supplied information to the lender which is not verified and results in a rough estimate of price range.

Finance 1 Practical Application Pre-qualified - Buyer supplied information to the lender which is not verified and results in a rough estimate of price range. 2 Pre-approval - Includes an application and

Finance 1 Practical Application Pre-qualified - Buyer supplied information to the lender which is not verified and results in a rough estimate of price range. 2 Pre-approval - Includes an application and

Course 1 Section 13: Types of Mortgages and Sources of Financing Section 13 Part 1

Course 1 Section 13: Types of Mortgages and Sources of Financing Section 13 Part 1 SLIDE 1 COVER PAGE SLIDE 2 TOPICS In this section we will cover the following topics: I. Conventional mortgages II. III.

Course 1 Section 13: Types of Mortgages and Sources of Financing Section 13 Part 1 SLIDE 1 COVER PAGE SLIDE 2 TOPICS In this section we will cover the following topics: I. Conventional mortgages II. III.

Federal Reserve System Primary Market Secondary Market

Chapter 14: Real Estate Financing: Practices Introduction to the Real Estate Financing Market Federal Reserve System Primary Market Secondary Market Federal Reserve System Role Maintain sound credit conditions

Chapter 14: Real Estate Financing: Practices Introduction to the Real Estate Financing Market Federal Reserve System Primary Market Secondary Market Federal Reserve System Role Maintain sound credit conditions

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

CHAPTER 14 - FINANCE I. INTRODUCTION FINANCING INSTRUMENTS A. THE DEMAND FOR LOANS. BORROWERS INCLUDE: B. THE SUPPLY OF MONEY FOR LOANS.

CHAPTER 14 - FINANCE I. INTRODUCTION A. THE DEMAND FOR LOANS. BORROWERS INCLUDE: B. THE SUPPLY OF MONEY FOR LOANS. C. THE FEDERAL RESERVE BOARD. II. FINANCING INSTRUMENTS A. THE USE OF PROPERTY AS SECURITY

CHAPTER 14 - FINANCE I. INTRODUCTION A. THE DEMAND FOR LOANS. BORROWERS INCLUDE: B. THE SUPPLY OF MONEY FOR LOANS. C. THE FEDERAL RESERVE BOARD. II. FINANCING INSTRUMENTS A. THE USE OF PROPERTY AS SECURITY

CONFORMING LIBOR ARMS PROGRAM HIGHLIGHTS

Program Summary Loan Term & Program Category A 30 year conforming conventional LIBOR ARM that is fixed for the initial 3, 5, or 7 years then rolls into a one year ARM for the remainder of the loan term.

Program Summary Loan Term & Program Category A 30 year conforming conventional LIBOR ARM that is fixed for the initial 3, 5, or 7 years then rolls into a one year ARM for the remainder of the loan term.

First Mortgage EXPERIENCE BASED THE LENDER & OUR CLIENTS. Mortgage Planner Marketing

First Mortgage EXPERIENCE BASED THE LENDER & OUR CLIENTS Mortgage Planner Marketing Qualified & Formal Approval Becoming qualified is the first step. This means having your debt ratios and credit report

First Mortgage EXPERIENCE BASED THE LENDER & OUR CLIENTS Mortgage Planner Marketing Qualified & Formal Approval Becoming qualified is the first step. This means having your debt ratios and credit report

Non-QM. Qualified Mortgages General QMs. GSE QMs. Agency QMs. Points & Fees 5%

Subprime 2006 No down payment required (80/20) or 100% LTV Average 580 credit score Income stated No reserves Negative Amortization and balloon payments No appraisal requirements Prepayment penalties Exceptions

Subprime 2006 No down payment required (80/20) or 100% LTV Average 580 credit score Income stated No reserves Negative Amortization and balloon payments No appraisal requirements Prepayment penalties Exceptions

Welcome! Credit Scoring and Sub-Prime Lending

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

CONFORMING FIXED LENDER PAID MORTGAGE INSURANCE PROGRAM HIGHLIGHTS

Program Summary Loan Term & Program Category A conforming conventional loan with a fixed interest rate for the term of the loan. Loan Term Program Category 30-year Conf Fixed 30 15-year Conf Fixed 15 Transaction

Program Summary Loan Term & Program Category A conforming conventional loan with a fixed interest rate for the term of the loan. Loan Term Program Category 30-year Conf Fixed 30 15-year Conf Fixed 15 Transaction

The Non-QM. Investor Advantage Program. Presented by Nations Direct Mortgage. Intended for mortgage professionals. Not intended for consumers.

The Non-QM Investor Advantage Program Presented by Nations Direct Mortgage Investor Advantage What is the Investor Advantage program? The Investor Advantage Credit Grade is designed for investment, nonowner

The Non-QM Investor Advantage Program Presented by Nations Direct Mortgage Investor Advantage What is the Investor Advantage program? The Investor Advantage Credit Grade is designed for investment, nonowner

Financing Residential Real Estate. Qualifying the Buyer

Financing Residential Real Estate Lesson 8: Qualifying the Buyer Introduction In this lesson we will cover: the underwriting process, qualifying the buyer, and factors taken into account when a buyer s

Financing Residential Real Estate Lesson 8: Qualifying the Buyer Introduction In this lesson we will cover: the underwriting process, qualifying the buyer, and factors taken into account when a buyer s

Chapter 9 Product Matrix

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

AUTOMATED UNDERWRITING, CONVENTIONAL

Automated Underwriting rev. 04 Revised 7/2/2013 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs have more

Automated Underwriting rev. 04 Revised 7/2/2013 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs have more

The Non-QM. Investor Advantage Program. Presented by Nations Direct Mortgage. Intended for mortgage professionals. Not intended for consumers.

The Non-QM Investor Advantage Program Presented by Nations Direct Mortgage Investor Advantage NO Income NO Reserves NO Debt Coverage Ratio NO Limitation on Financed Properties NO Prepayment Penalty Investor

The Non-QM Investor Advantage Program Presented by Nations Direct Mortgage Investor Advantage NO Income NO Reserves NO Debt Coverage Ratio NO Limitation on Financed Properties NO Prepayment Penalty Investor

FNMA vs FHLMC Guideline Comparisons

FNMA vs FHLMC Guideline Comparisons Table A: Guidelines for Maximum LTV and Loan Amounts Max LTV/ Loan Amount FANNIE MAE FREDDIE MAC Primary Residence 1 Unit Max LTV Max ARM LTV Max Loan Amount* Max LTV

FNMA vs FHLMC Guideline Comparisons Table A: Guidelines for Maximum LTV and Loan Amounts Max LTV/ Loan Amount FANNIE MAE FREDDIE MAC Primary Residence 1 Unit Max LTV Max ARM LTV Max Loan Amount* Max LTV

Mortgage Underwriting Policy Manual Table of Contents [Sample Client] Table of Contents

![Mortgage Underwriting Policy Manual Table of Contents [Sample Client] Table of Contents](/thumbs/94/118769120.jpg "Mortgage Underwriting Policy Manual Table of Contents [Sample Client] Table of Contents") TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 9 1.1 GOALS AND OBJECTIVES... 9 1.2 REQUIRED REVIEW... 9 1.3 APPLICABILITY... 9 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 10 2.1 INTERNAL CONTROLS... 10

TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 9 1.1 GOALS AND OBJECTIVES... 9 1.2 REQUIRED REVIEW... 9 1.3 APPLICABILITY... 9 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 10 2.1 INTERNAL CONTROLS... 10

Guidelines Correspondent. Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits:

LTV Limits:") Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Property Type w/o Sec Fin. PURCHASE MORTGAGES w/sec Fin. Max TLTV Max HTLTV Loan Limits 1 Unit

Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Property Type w/o Sec Fin. PURCHASE MORTGAGES w/sec Fin. Max TLTV Max HTLTV Loan Limits 1 Unit

Mortgage Underwriting Policy Manual Table of Contents [Sample Client] Table of Contents

![Mortgage Underwriting Policy Manual Table of Contents [Sample Client] Table of Contents](/thumbs/95/125798693.jpg "Mortgage Underwriting Policy Manual Table of Contents [Sample Client] Table of Contents") TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 9 1.1 GOALS AND OBJECTIVES... 9 1.2 REQUIRED REVIEW... 9 1.3 APPLICABILITY... 9 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 10 2.1 INTERNAL CONTROLS... 10

TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 9 1.1 GOALS AND OBJECTIVES... 9 1.2 REQUIRED REVIEW... 9 1.3 APPLICABILITY... 9 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 10 2.1 INTERNAL CONTROLS... 10

FFBF Wholesale / Correspondent Overlays

Conventional FHA VA USDA Assets Large Deposits Any large deposit not consistent with the borrower s earnings, employment and/or savings profile must be explained and sourced with acceptable documentation

Conventional FHA VA USDA Assets Large Deposits Any large deposit not consistent with the borrower s earnings, employment and/or savings profile must be explained and sourced with acceptable documentation

The Way to Greater Efficiency. Correspondent Lending

The Way to Greater Efficiency Correspondent Lending High-level service and partnership that uniquely leverages technology, processes and people to ensure effi cient and timely loan purchases Meeting the

The Way to Greater Efficiency Correspondent Lending High-level service and partnership that uniquely leverages technology, processes and people to ensure effi cient and timely loan purchases Meeting the

Financing Residential Real Estate. Lesson 11: FHA-Insured Loans

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE. Reserves

Click Here For PDF Version Full/Alternative Documentation 1-2 Unit 1 Unit 3-4 Unit PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Qualifying Ratios Required MI Minimum LTV CLTV Loan Amount

Click Here For PDF Version Full/Alternative Documentation 1-2 Unit 1 Unit 3-4 Unit PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Qualifying Ratios Required MI Minimum LTV CLTV Loan Amount

Mortgage Lender Sentiment Survey

Mortgage Lender Sentiment Survey Providing Insights Into Current Lending Activities and Market Expectations 2015 Published: March 18, 2015 2011 Fannie Mae. Trademarks of Fannie Mae. 2015 Fannie Mae. Trademarks

Mortgage Lender Sentiment Survey Providing Insights Into Current Lending Activities and Market Expectations 2015 Published: March 18, 2015 2011 Fannie Mae. Trademarks of Fannie Mae. 2015 Fannie Mae. Trademarks

AINSWORTH FINANCIAL MORTGAGE CORPORATION 2017 LOAN ORIGINATOR TRAINING COURSE MANUAL

2017 LOAN ORIGINATOR TRAINING COURSE MANUAL Ainsworth Financial Mortgage Corporation 2015 Privacy Policy. The training course material is attended for official use of AFMC only. NMLS #362869 Ainsworth

2017 LOAN ORIGINATOR TRAINING COURSE MANUAL Ainsworth Financial Mortgage Corporation 2015 Privacy Policy. The training course material is attended for official use of AFMC only. NMLS #362869 Ainsworth

More on Mortgages. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

FNMA Home Affordable Refinance Program (HARP) Transaction Type Number of Units Fixed Rate Max LTV/CLTV

Transaction Type Number of Units Fixed Rate Max LTV/CLTV") FNMA Conventional Conforming Product Offering Transaction Type Number of Fixed Rate Cash-Out Refinance Second Home Adjustable Rate 1 Unit 97/97% 90/90% 2 Unit 85/85% 75/75% 3 4 75/75% 65/65% 1 Unit 80/80%

FNMA Conventional Conforming Product Offering Transaction Type Number of Fixed Rate Cash-Out Refinance Second Home Adjustable Rate 1 Unit 97/97% 90/90% 2 Unit 85/85% 75/75% 3 4 75/75% 65/65% 1 Unit 80/80%

AIG Investments Underwriting Guidelines

AIG Investments Underwriting Guidelines September 18, 2017 MC-2-A987H-1016 2017 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated. The Underwriting

AIG Investments Underwriting Guidelines September 18, 2017 MC-2-A987H-1016 2017 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated. The Underwriting

Wholesale Overlay Matrix

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

<logo> Offered through 21 st Century Home Loans WHOLESALE DIVISION

CHF ACCESS Training Offered through 21 st Century Home Loans WHOLESALE DIVISION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie

CHF ACCESS Training Offered through 21 st Century Home Loans WHOLESALE DIVISION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie

CHOOSING THE RIGHT MORTGAGE PARTNER

CHOOSING THE RIGHT MORTGAGE PARTNER Your mortgage partner should play a vital role in both a seller listing situation and in the case of when working with a buyer. IN THE CASE OF A LISTING Provide seller

CHOOSING THE RIGHT MORTGAGE PARTNER Your mortgage partner should play a vital role in both a seller listing situation and in the case of when working with a buyer. IN THE CASE OF A LISTING Provide seller

Your Guide to Home Financing

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

HARP Refinance Guide. How You can Benefit from the HARP Program

HARP Refinance Guide How You can Benefit from the HARP Program Contents How HARP Can Help You You Might Qualify for HARP but Not Know It HARP Qualification Basics HARP History HARP 1.0 HARP 2.0 HARP 3.0

HARP Refinance Guide How You can Benefit from the HARP Program Contents How HARP Can Help You You Might Qualify for HARP but Not Know It HARP Qualification Basics HARP History HARP 1.0 HARP 2.0 HARP 3.0

Full/Alternative Documentation PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Property Type Max. LTV Max. CLTV

Click here for PDF version Full/Alternative Documentation PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Loan Credit Score 3 Program 1- to 2-unit 95% 1 n/a $300,000 28/36 2 months 660 Standard

Click here for PDF version Full/Alternative Documentation PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Loan Credit Score 3 Program 1- to 2-unit 95% 1 n/a $300,000 28/36 2 months 660 Standard

After-tax APRPlus The APRPlus taking into account the effect of income taxes.

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

Prioritize QC with Pre-Funding. April 19, 2012 Presented By: Brady W. Meadows

Prioritize QC with Pre-Funding April 19, 2012 Presented By: Brady W. Meadows Because of the large number of registrants, the lines will be muted. To ask a question, click the plus sign next to Questions

Prioritize QC with Pre-Funding April 19, 2012 Presented By: Brady W. Meadows Because of the large number of registrants, the lines will be muted. To ask a question, click the plus sign next to Questions

Chapter 15 Real Estate Financing: Practice

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

Wells Fargo Bank, N.A. General Information Statement

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

Home Affordable Refinance Program

Home Affordable Refinance Program This paper is about HARP. We will explain what the program is about and how it can help many people get their mortgage payments into an affordable range. About HARP Home

Home Affordable Refinance Program This paper is about HARP. We will explain what the program is about and how it can help many people get their mortgage payments into an affordable range. About HARP Home

Desktop Underwriter/Desktop Originator Release Notes

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.2 June Update April 24, 2018 During the weekend of June 23, 2018, Fannie Mae will implement an update to Desktop Underwriter (DU ) Version

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.2 June Update April 24, 2018 During the weekend of June 23, 2018, Fannie Mae will implement an update to Desktop Underwriter (DU ) Version

GSE Reform: Consumer Costs in a Reformed System

ONE VOICE. ONE VISION. ONE RESOURCE. GSE Reform: Consumer Costs in a Reformed System In evaluating any proposal for GSE reform, three major objectives must be balanced: protecting taxpayers, attracting

ONE VOICE. ONE VISION. ONE RESOURCE. GSE Reform: Consumer Costs in a Reformed System In evaluating any proposal for GSE reform, three major objectives must be balanced: protecting taxpayers, attracting

Dream Big Jumbo Is Now Available The Smart Series is live! Check page 2 for more info. Check out our enhaned conventional LPMI pricing.

Effective Fri 02/23/2018 10:20 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

Effective Fri 02/23/2018 10:20 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

GUILD MORTGAGE COMPANY Loan program cheat sheet. 100% Financing REHAB PROGRAM 97% FINANCING PROGRAMS CONFORMING ARMS NON CONFORMING ARMS

GUILD MORTGAGE COMPANY Loan program cheat sheet Mar-09 100% Financing REHAB PROGRAM USDA - Rural Housing FHA 203K Streamline VA 97% FINANCING PROGRAMS CONFORMING ARMS FNMA FLEX Win World FNMA My Community

GUILD MORTGAGE COMPANY Loan program cheat sheet Mar-09 100% Financing REHAB PROGRAM USDA - Rural Housing FHA 203K Streamline VA 97% FINANCING PROGRAMS CONFORMING ARMS FNMA FLEX Win World FNMA My Community

DTI on all FHA & VA loans will cap at 55%, anything above with DU approve/eligible requires management approval

This summary of overlays is provided as a resource tool to aid in identifying most UFF WEST Mortgage overlays to Fannie Mae, Freddie Mac, FHA, and VA Lending requirements. This document is a reference

This summary of overlays is provided as a resource tool to aid in identifying most UFF WEST Mortgage overlays to Fannie Mae, Freddie Mac, FHA, and VA Lending requirements. This document is a reference

Dream Big Jumbo Is Now Available

Effective Tue 04/10/2018 9:54 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

Effective Tue 04/10/2018 9:54 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

Lesson 13: Applying for a Mortgage Loan

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

Federal Home Loan Bank of Des Moines. Credit Union Workshop - MPF

Federal Home Loan Bank of Des Moines Credit Union Workshop - MPF 1 MPF Agenda MPF Credit Union Activity Xtra (FNMA) Traditional (Risk Sharing) Direct (Jumbo) 2 3 4 Investor: Fannie Mae (DU) MPF Xtra Direct

Federal Home Loan Bank of Des Moines Credit Union Workshop - MPF 1 MPF Agenda MPF Credit Union Activity Xtra (FNMA) Traditional (Risk Sharing) Direct (Jumbo) 2 3 4 Investor: Fannie Mae (DU) MPF Xtra Direct

REV-1 TABLE OF CONTENTS. Page CHAPTER 1. GENERAL INFORMATION

CHAPTER 1. GENERAL INFORMATION TABLE OF CONTENTS Page 1-1 LEGISLATIVE HISTORY... 1-1 1-2 PURPOSE OF THE PROGRAM... 1-1 1-3 CHARACTERISTICS OF THE MORTGAGE... 1-1 1-4 PRINCIPAL LIMIT... 1-2 1-5 PAYMENT

CHAPTER 1. GENERAL INFORMATION TABLE OF CONTENTS Page 1-1 LEGISLATIVE HISTORY... 1-1 1-2 PURPOSE OF THE PROGRAM... 1-1 1-3 CHARACTERISTICS OF THE MORTGAGE... 1-1 1-4 PRINCIPAL LIMIT... 1-2 1-5 PAYMENT

First Time Homebuyers

First Time Homebuyers Presented By: Rich Goodwin, Vice President of Mortgage Lending Copyright 2000-2014 Guaranteed Rate. All rights reserved. Our Competitive Advantage Fast and transparent mortgage process

First Time Homebuyers Presented By: Rich Goodwin, Vice President of Mortgage Lending Copyright 2000-2014 Guaranteed Rate. All rights reserved. Our Competitive Advantage Fast and transparent mortgage process

Chapter 11 11/18/2014. Mortgages and Mortgage Markets. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

WHOLESALE BORROWER PAID COMPENSATION RATE SHEET. Liberty Savings Bank Contact Information

Rate Sheet Date: Rate Sheet Price Code: 3/8/2019 3453 *Effective at 11:00 am EST WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank Contact

Rate Sheet Date: Rate Sheet Price Code: 3/8/2019 3453 *Effective at 11:00 am EST WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank Contact

AGENCY CONFORMING & HIGH BALANCE (Fannie Mae DU) BORROWER PAID

BORROWER PAID") AGENCY CONFORMING & HIGH BALANCE (Fannie Mae DU) BORROWER PAID 30 & 25 Year Fixed Agency DU (DU30, DU25) 20 Year Fixed Agency DU (DU20) 15 & 10 Year Fixed Agency DU (DU15, DU10) 4.750 107.140 107.029 106.957

AGENCY CONFORMING & HIGH BALANCE (Fannie Mae DU) BORROWER PAID 30 & 25 Year Fixed Agency DU (DU30, DU25) 20 Year Fixed Agency DU (DU20) 15 & 10 Year Fixed Agency DU (DU15, DU10) 4.750 107.140 107.029 106.957

Financing Residential Real Estate. Conventional Financing

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of a conventional loan, qualifying standards

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of a conventional loan, qualifying standards

11/9/2017. Chapter 11. Mortgages and Mortgage Markets. Traditional and Modern Housing Finance: From S&Ls to Securities. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Guidelines Correspondent. Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits:

LTV Limits:") Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Second Home Investment & Non- Owner Property Type Condominiums are ineligible for this product.

Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Second Home Investment & Non- Owner Property Type Condominiums are ineligible for this product.

Best Practices for Wholesale Lending

July 15, 2010 Best Practices for Wholesale Lending by Anna DeSimone On May 20, HUD stopped accepting applications from brokers for FHA approval but began allowing them to originate loans if they are sponsored

July 15, 2010 Best Practices for Wholesale Lending by Anna DeSimone On May 20, HUD stopped accepting applications from brokers for FHA approval but began allowing them to originate loans if they are sponsored

Accenture Mortgage Cadence. Loan Fulfillment Center. Forms Job Aid

Accenture Mortgage Cadence Loan Fulfillment Center f Table of Contents FORM FORMATS...8 1003 UNIFORM RESIDENTIAL LOAN APPLICATION...9 1008 UNIFORM UNDERWRITING AND TRANSMITTAL SUMMARY... 10 1008 Uniform

Accenture Mortgage Cadence Loan Fulfillment Center f Table of Contents FORM FORMATS...8 1003 UNIFORM RESIDENTIAL LOAN APPLICATION...9 1008 UNIFORM UNDERWRITING AND TRANSMITTAL SUMMARY... 10 1008 Uniform

RESIDENTIAL CONSTRUCTION LENDING POLICY

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

Section 1.04 Automated Underwriting

Section 1.04 Automated Underwriting In This Section This section contains the following topics. Overview... 2 Related Bulletins... 2 AUS Guidelines... 3 Implementation... 3 Loans Not Rated Approve or Accept...

Section 1.04 Automated Underwriting In This Section This section contains the following topics. Overview... 2 Related Bulletins... 2 AUS Guidelines... 3 Implementation... 3 Loans Not Rated Approve or Accept...

Risky Borrowers or Risky Mortgages?

Risky Borrowers or Risky Mortgages? Lei Ding, Roberto G. Quercia, Janneke Ratcliffe Center for Community Capital, University of North Carolina, Chapel Hill, USA Wei Li Center for Responsible Lending, Durham,

Risky Borrowers or Risky Mortgages? Lei Ding, Roberto G. Quercia, Janneke Ratcliffe Center for Community Capital, University of North Carolina, Chapel Hill, USA Wei Li Center for Responsible Lending, Durham,

Processing VA Mortgages

Introduction The Department of Veterans Affairs (VA) Freddie Mac allows Loan Product Advisor automated underwriting service to assess VA loan applications. The Department of Veterans Affairs then guarantees

Introduction The Department of Veterans Affairs (VA) Freddie Mac allows Loan Product Advisor automated underwriting service to assess VA loan applications. The Department of Veterans Affairs then guarantees

Broker. Financing Real Estate. Chapter 12. Copyright Gold Coast Schools 1

Broker Chapter 12 Financing Real Estate Copyright Gold Coast Schools 1 Learning Objectives Describe the difference between a note and a mortgage Explain the benefits of having the first recorded lien on

Broker Chapter 12 Financing Real Estate Copyright Gold Coast Schools 1 Learning Objectives Describe the difference between a note and a mortgage Explain the benefits of having the first recorded lien on

USDA Guaranteed Rural Housing Product Profile

USDA Guaranteed Rural Housing Product Profile PROGRAM CODES: 30RH Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 620 100%* 620 *exclusive

USDA Guaranteed Rural Housing Product Profile PROGRAM CODES: 30RH Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 620 100%* 620 *exclusive

LoanStream Select Program

19000 MacArthur Boulevard, 2nd Floor Ratesheet Co RS-WS Effective Date: 4/2/2019 #1 Wholesale Rate Sheet Table of Contents Contact list Tab Product LSM Select: All FNMA/FHLCM Corporate Headquarters: Phone:

19000 MacArthur Boulevard, 2nd Floor Ratesheet Co RS-WS Effective Date: 4/2/2019 #1 Wholesale Rate Sheet Table of Contents Contact list Tab Product LSM Select: All FNMA/FHLCM Corporate Headquarters: Phone:

USDA Guaranteed Rural Housing Product Profile

Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 640 100%* 640 *exclusive of financed guarantee fee A full appraisal (e.g. form 1004 or

Appraisals LTV/CLTV 100%* Purchase Maximum LTV/FICO Requirements Min FICO Rate and Term Refinance LTV/CLTV Min FICO 640 100%* 640 *exclusive of financed guarantee fee A full appraisal (e.g. form 1004 or

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Wells Fargo Bank, N.A. General Information Statement

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

Basics in Mortgage Lending Test for Loan Officers

Basics in Mortgage Lending Test for Loan Officers Name: Date: Company Name: 1. The purpose of the Equal Credit Opportunity Act is: To discourage predatory lending To create new avenues and programs for

Basics in Mortgage Lending Test for Loan Officers Name: Date: Company Name: 1. The purpose of the Equal Credit Opportunity Act is: To discourage predatory lending To create new avenues and programs for

Application. Servicing Questionniare (applicable only if retaining the servicing of the loans)

") Application Application Overview Member Name: Application Contact: Contact Phone Number: Contact Email Address: Application Date: Submission Instructions The following items must be sent to FHLBI for application

Application Application Overview Member Name: Application Contact: Contact Phone Number: Contact Email Address: Application Date: Submission Instructions The following items must be sent to FHLBI for application

Edit 1003 Form. Figure 1 - Tabs of the 1003

Edit 1003 Form The OpenClose 1003 is organized into multiple tabs that coincide with the sections of the 1003 plus three extra tabs to store additional information on the loan file. Figure 1 - Tabs of

Edit 1003 Form The OpenClose 1003 is organized into multiple tabs that coincide with the sections of the 1003 plus three extra tabs to store additional information on the loan file. Figure 1 - Tabs of

the Mortgage Process Designs for Learning

The Fundamentals of the Mortgage Process Designs for Learning 1 Legal Disclaimer The information presented in these training materials is based on guidelines and practices accepted within the mortgage

The Fundamentals of the Mortgage Process Designs for Learning 1 Legal Disclaimer The information presented in these training materials is based on guidelines and practices accepted within the mortgage

Attention All Correspondent Lending Sellers: April 20, 2018 CA Announcing Freddie Mac Home Possible and Home Possible Advantage

Attention All Correspondent Lending Sellers: April 20, 2018 CA 18-037 Announcing Freddie Mac Home Possible and Home Possible Advantage Subject Summary Effective Date Home Possible Advantage Mortgage Maximum

Attention All Correspondent Lending Sellers: April 20, 2018 CA 18-037 Announcing Freddie Mac Home Possible and Home Possible Advantage Subject Summary Effective Date Home Possible Advantage Mortgage Maximum

999 West Street, Rocky Hill, CT Phone: (860) Fax: (860) Website:

Fax: (860) Website:") 999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

FUSION SERVICING DIRECTOR COMPLETE LOAN SERVICING SOLUTION

FUSION SERVICING DIRECTOR COMPLETE LOAN SERVICING SOLUTION 2 FINASTRA Brochure Fusion Servicing Director Complete Loan Servicing Solution From loan boarding through payoff, Fusion Servicing Director streamlines

FUSION SERVICING DIRECTOR COMPLETE LOAN SERVICING SOLUTION 2 FINASTRA Brochure Fusion Servicing Director Complete Loan Servicing Solution From loan boarding through payoff, Fusion Servicing Director streamlines

Guideline Reference Applies to ALL Products

Guideline Reference Applies to ALL Products 4506-T CG Ch 5E Loan Documents & Notes CG Ch 6F Employment & Documentation CG Ch 7G FHA Employment & Evaluation & Documentation Product summaries IRS Form 4506T

Guideline Reference Applies to ALL Products 4506-T CG Ch 5E Loan Documents & Notes CG Ch 6F Employment & Documentation CG Ch 7G FHA Employment & Evaluation & Documentation Product summaries IRS Form 4506T

Section 1.04 Automated Underwriting

Section 1.04 Automated Underwriting In This Section This section contains the following topics. Overview... 2 General... 2 Related Bulletins... 2 AUS Guidelines... 3 Implementation... 3 Loans Not Rated

Section 1.04 Automated Underwriting In This Section This section contains the following topics. Overview... 2 General... 2 Related Bulletins... 2 AUS Guidelines... 3 Implementation... 3 Loans Not Rated

PennyMac Correspondent Group Overlays, February 25, 2019 X Indicates Overlay

PennyMac Correspondent Group Overlays, February 25, 2019 Indicates Overlay GOVERNMENT FHA Full doc FHA Streamline VA Full Doc VA IRRRL Rural Housing Topic Overlay/Modification 203(k) Specific PennyMac

PennyMac Correspondent Group Overlays, February 25, 2019 Indicates Overlay GOVERNMENT FHA Full doc FHA Streamline VA Full Doc VA IRRRL Rural Housing Topic Overlay/Modification 203(k) Specific PennyMac

12-Step Home Mortgage Steps

1 You should review your credit report for any errors before submitting your mortgage application. Your credit report is used by banks and other lending institutions to determine your creditworthiness.

1 You should review your credit report for any errors before submitting your mortgage application. Your credit report is used by banks and other lending institutions to determine your creditworthiness.

Conventional Financing

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of conventional loans, qualifying standards

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of conventional loans, qualifying standards

Silvergate Funding, Inc ( SFI ) IN FOCUS BULLETIN April 17, 2014

IN FOCUS BULLETIN April 17, 2014") Silvergate Funding, Inc ( SFI ) IN FOCUS BULLETIN 2014-05 April 17, 2014 Week of April 14 Hours of Operation The financial markets close early on Thursday and are closed on Friday April 18. SFI Secondary

Silvergate Funding, Inc ( SFI ) IN FOCUS BULLETIN 2014-05 April 17, 2014 Week of April 14 Hours of Operation The financial markets close early on Thursday and are closed on Friday April 18. SFI Secondary

Sponsored by: Mortgage 101

Sponsored by: Mortgage 101 Who is Equity Resources, Inc? Direct mortgage banker - Fannie Mae and Ginnie Mae Seller Servicer FHA/VA/Conventional/RD loans Underwrite in our main office Company began in 1993

Sponsored by: Mortgage 101 Who is Equity Resources, Inc? Direct mortgage banker - Fannie Mae and Ginnie Mae Seller Servicer FHA/VA/Conventional/RD loans Underwrite in our main office Company began in 1993

999 West Street, Rocky Hill, CT Phone: (860) Fax: (860) Website:

Fax: (860) Website:") 999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

ditech BUSINESS LENDING CONFORMING TEXAS HOME EQUITY PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION ditech BUSINESS LENDING CONFORMING TEXAS HOME EQUITY PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10 to 30 year term in annual increments

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING CONFORMING TEXAS HOME EQUITY PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10 to 30 year term in annual increments

Freddie Mac Standard Modification Overview for Housing Counselors. Counselor Connection Baltimore, Maryland May 8, 2012

Freddie Mac Standard Modification Overview for Housing Counselors Counselor Connection Baltimore, Maryland May 8, 2012 Objectives Understand how Servicers will apply Freddie Mac requirements for the Standard

Freddie Mac Standard Modification Overview for Housing Counselors Counselor Connection Baltimore, Maryland May 8, 2012 Objectives Understand how Servicers will apply Freddie Mac requirements for the Standard

WHOLESALE BORROWER PAID COMPENSATION RATE SHEET. Liberty Savings Bank Contact Information

Rate Sheet Date: Rate Sheet Price Code: *Effective at 11:00 am EST 09/14/2018 3319 WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank

Rate Sheet Date: Rate Sheet Price Code: *Effective at 11:00 am EST 09/14/2018 3319 WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank

ditech BUSINESS LENDING CONFORMING HIGH-BALANCE PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION ditech BUSINESS LENDING CONFORMING HIGH-BALANCE PRODUCT Conventional Conforming fixed rate mortgage with High- Balance loan limits DU Version 10.2 Servicing retained 10 to 30 year

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING CONFORMING HIGH-BALANCE PRODUCT Conventional Conforming fixed rate mortgage with High- Balance loan limits DU Version 10.2 Servicing retained 10 to 30 year

Loan Policy. Including Loan Program Parameters & Underwriting Guidelines. Last Updated 11/30/18

Loan Policy Including Loan Program Parameters & Underwriting Guidelines Last Updated 11/30/18 Commercial Lending X ( CLX ) is a national commercial financing consulting firm. CLX specializes in helping

Loan Policy Including Loan Program Parameters & Underwriting Guidelines Last Updated 11/30/18 Commercial Lending X ( CLX ) is a national commercial financing consulting firm. CLX specializes in helping

AIG Investments Underwriting Guidelines

AIG Investments Underwriting Guidelines September 5, 2018 MC-2-A987H-1016 2018 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated September 5, 2018.

AIG Investments Underwriting Guidelines September 5, 2018 MC-2-A987H-1016 2018 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated September 5, 2018.

First-time Homebuyer s Guide: Follow These Steps to Get Your First Mortgage

First-time Homebuyer s Guide: Follow These Steps to Get Your First Mortgage Buying your first home is both exhilarating and overwhelming. Stay on top of it all with this step-by-step guide on what to expect

First-time Homebuyer s Guide: Follow These Steps to Get Your First Mortgage Buying your first home is both exhilarating and overwhelming. Stay on top of it all with this step-by-step guide on what to expect

Pennsylvania Wholesale Rate Sheet

Effective Fri 03/15/2019 9:36 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

Effective Fri 03/15/2019 9:36 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

PORTFOLIO ARM BORROWER PAID RATE SHEET For Lender Paid Comp Plan see below

PORTFOLIO ARM BORROWER PAID RATE SHEET For Lender Paid Comp Plan see below 5/1 LIBOR (Portfolio 6/2/6) ARM (JP51, JP51IO) 7/1 LIBOR (Portfolio 6/2/6) ARM (JP71) 10/1 LIBOR (Portfolio 6/2/6) ARM (JP101)

PORTFOLIO ARM BORROWER PAID RATE SHEET For Lender Paid Comp Plan see below 5/1 LIBOR (Portfolio 6/2/6) ARM (JP51, JP51IO) 7/1 LIBOR (Portfolio 6/2/6) ARM (JP71) 10/1 LIBOR (Portfolio 6/2/6) ARM (JP101)

Portfolio Libor Arms Guidelines

Portfolio Libor Arms Guidelines Effective Date: 02/21/2017 Loans meeting the parameters outlined in this guideline matrix must be consistent with the Dodd Frank Wall Street Reform and Consumer Protection

Portfolio Libor Arms Guidelines Effective Date: 02/21/2017 Loans meeting the parameters outlined in this guideline matrix must be consistent with the Dodd Frank Wall Street Reform and Consumer Protection

California Wholesale Rate Sheet

Effective Fri 01/25/2019 9:44 AM EST California Wholesale Rate Sheet Jumbo Series H is Here! - See page 15 for details. Rate Fall-Out Specials on SmartEdge, SmartCondo & Dream Big! Smart Funds - See page

Effective Fri 01/25/2019 9:44 AM EST California Wholesale Rate Sheet Jumbo Series H is Here! - See page 15 for details. Rate Fall-Out Specials on SmartEdge, SmartCondo & Dream Big! Smart Funds - See page

Overview of Types of Mortgages Available

Overview of Types of Mortgages Available There are many different types of mortgages available to home buyers. They are all thoroughly explained here. But here, for the sake of simplicity, we have boiled

Overview of Types of Mortgages Available There are many different types of mortgages available to home buyers. They are all thoroughly explained here. But here, for the sake of simplicity, we have boiled

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

THIS IS NOT LEGAL ADVICE

I. Ability to Repay (ATR) Qualified Mortgage (QM) Overview In 2008 the Board of Governors of the Federal Reserve System adopted a rule under the Truth in Lending Act prohibiting creditors from making higher-priced

I. Ability to Repay (ATR) Qualified Mortgage (QM) Overview In 2008 the Board of Governors of the Federal Reserve System adopted a rule under the Truth in Lending Act prohibiting creditors from making higher-priced

Pennsylvania Wholesale Rate Sheet

Effective Fri 01/25/2019 9:44 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

Effective Fri 01/25/2019 9:44 AM EST HomeReady: 3% down pmnt can come entirely from a gift Home Possible Advantage: Purch & refi loans up to 97% for SFR only. Home Possible: For 1-4 unit properties up

Niche Loan Programs. Featured Loan. Zero Down Loan

Niche Loan Programs To cater the different needs of out clients Shining Star Funding offers diverse Niche Loan Programs. Contact our mortgage specialist to review which product best suits your financial

Niche Loan Programs To cater the different needs of out clients Shining Star Funding offers diverse Niche Loan Programs. Contact our mortgage specialist to review which product best suits your financial

Lender Letter LL

Lender Letter LL-2017-05 To: All Fannie Mae Single-Family Sellers High Loan-to-Value Refinance Option September 08, 2017 At the direction of the Federal Housing Finance Agency (FHFA), Fannie Mae will offer

Lender Letter LL-2017-05 To: All Fannie Mae Single-Family Sellers High Loan-to-Value Refinance Option September 08, 2017 At the direction of the Federal Housing Finance Agency (FHFA), Fannie Mae will offer