SBA AND THE BIZ AQ LOAN DOCUMENTING CHANGES IN OWNERSHIP. Coleman Webinar Friday, January 25, :00 PM 3:15 PM EST

|

|

|

- Godfrey Barnett

- 5 years ago

- Views:

Transcription

1 SBA AND THE BIZ AQ LOAN DOCUMENTING CHANGES IN OWNERSHIP Coleman Webinar Friday, January 25, :00 PM 3:15 PM EST

2 Coleman Report Industry Discussion Bob and Charles Show 1:50-2:00 PM ET. We are featuring a complimentary small business lending industry discussion with Bob Coleman, Editor of the Coleman Report and Charles Green, Author of The SBA Loan Book: Bestselling book on SBA-guaranteed financing. This discussion will start at 1:50 PM ET and end at 2:00 PM ET. 2

3 How to Ask Questions Use Go to Meeting's chat function, you can choose to ask question in writing or verbally. If comfortable, give us your first name, name of bank, and city. Send an to 3

4 E Certificates All Coleman Webinar attendees will receive a e Certificate of Participation. This is documents your continuing education history for the regulators. Also, this documents the answer for SBA s Review question of continuing staff education. Please forward the names of and s of all of those attending the webinar. We will issue e certificates of participation at the conclusion of the webinar. Send all addresses to bob@colemanreport.com 4

5 Expert Panelist Lisa G. Lerner Owner, Member Enhanced Consultive Solutions, LLC ("ECS") Ms. Lerner's professional experience spans over 28 years in the financial arena, with strong expertise in Small Business Administration lending, most recently operating ECS since ECS is an agency (SBA) approved lender service provider and provides guidance, and technical support to small and mid- size lenders. She and her husband, Nelson, are also certified pet therapy teams with their dogs volunteering with the nonprofit organization, Gabriel's Angels- "Pets helping kids." 5

6 6 BUSINESS ACQUISITIONS & PARTNER BUYOUT AND THE SBA LOAN In association with COLEMAN PUBLISHING Essential considerations for this lending opportunity

7 But first, a word of caution. 7 Potential revenue generating opportunity however tread carefully as SBA reviews this type of transaction very closely! (& with good reason) A change of ownership is considered a NEW business. COMPLETELY DOCUMENT CLEAR & JUSTIFIABLE reason(s) for change of ownership.

8 8 Some areas we will discuss today include: Business valuation Site visit Real estate appraisal What analysis to include in the request and credit memo Intangibles Equity injection and MORE

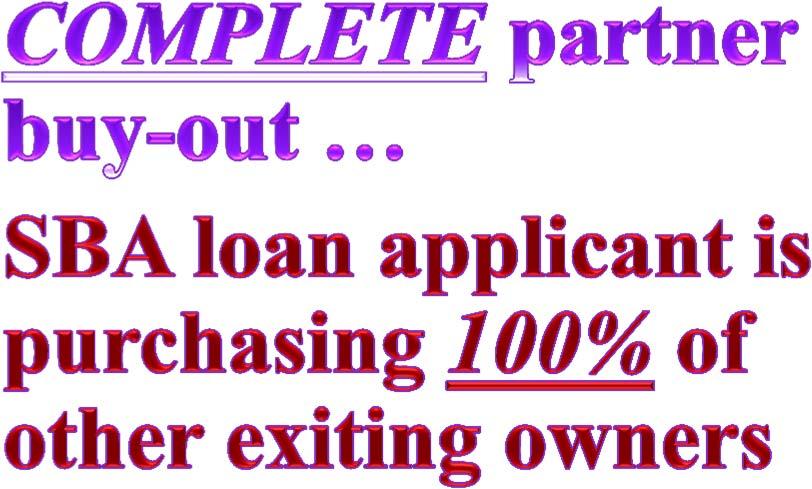

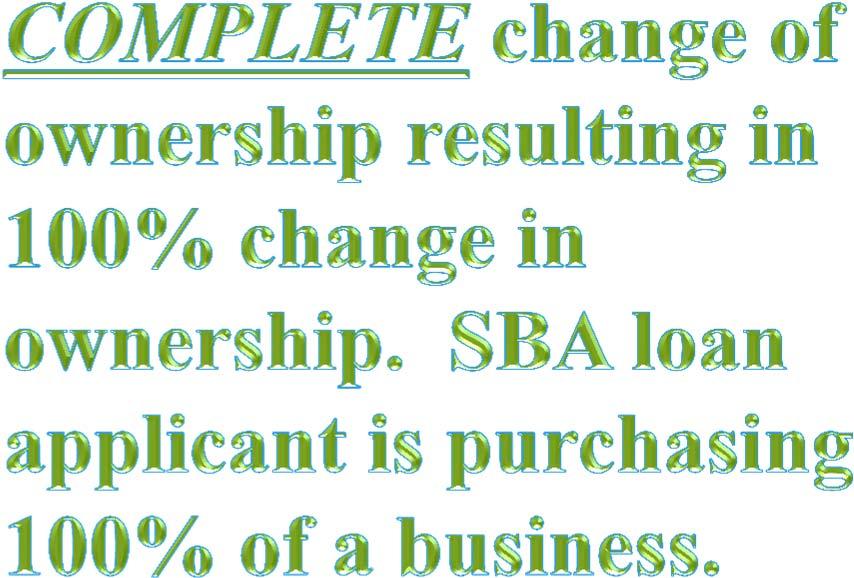

9 Applicable Circumstances.. 9

10 What s a buyer to do? 10 BUYER must not be an individual BUYER must purchase 100% of the stock. NO PARTIAL transactions. Stock redemption rule Applicant business to purchase stock of either departing owner(s) or all stock of all existing owner(s) Asset purchases are still allowed.

11 What s a seller to do? 11 Seller may NOT remain as an officer, director, stockholder, key employee or any other such position EXCEPT AS AN OUTSIDE CONSULTANT. ONLY FOR A MAXIMUM OF 12 MONTHS! NO EXCEPTIONS

12 Should a Seller stay on as a consultant: 12 Purchase agreement or separate document should outline specifics to document the relationship during transition/training period. NOT TO EXCEED 12 months! Purpose: To document that the seller is not considered an associate.

13 Key items to review & include in the application to SBA for BIZ ACQUISITION 13 Buy Sell / purchase agreement Business valuation Pro forma balance sheet Last three years financial statements from seller Interim financial statement (at least less than 90 days old) Lender determination documentation that purchase price reasonable How Lender verified business revenue

14 14 SBA Guidance on change of ownership and who signs the note? Change of ownership A stock purchase may be used to effectuate a change of ownership in a going concern. This method may be used where (1) the corporation redeems or repurchases all outstanding shares from existing shareholders, or (2) a third party buyer purchases all outstanding shares from existing shareholders. In either case, certain documentation is required at loan closing: The buyer(s) and corporation must sign the note; The principals of the buyer will be required to guaranty the loan; and The Lender should obtain an opinion from the Borrower s or Lender s counsel that the transaction complies with state law and specifying that adequate consideration exists and that the corporation cannot deny liability for the debt for failure of consideration.

15 The PURCHASE CONTRACT 15 READ CAREFULLY What is being purchased?

16 16 INTANGIBLES may be a part of the purchase IF purchase price includes intangibles over $500,000, equity injection must be at LEAST 25% of the purchase price IF to be submitted under delegated authority. IF less than 25%, submit via STANDARD 7(a) procedures Purchase price to include ALL assets being acquired!

17 Intangibles (continued) 17 IF loan proceeds used to finance intangibles, amounts must be specifically identified in use of proceeds sections of the credit memo, SBA loan authorization VALUE of intangibles: Book value from balance sheet Appraisal Or Business valuation amount less the working capital assets & fixed assets being purchased

18 18 Purchases that include payoff of seller notes If existing debt includes a SBA loan with the same lender, the request MUST be submitted to the LOAN GUARANTY PROCESSING CENTER as a standard 7a package & NOT via a PLP (or any other designated status). IF a complete change of ownership includes an existing SBA loan, the option to ASSUME the debt should be offered to the buyer! depending on the loan terms, of course!

19 Has the business been transferred within 36 months of the date of the loan application? 19 If so, further due diligence is PRUDENT! FURTHER action required also if the loan request is over $250M & real estate included. APPRAISAL REVIEW Complete a site visit! If not, include a prudent & credible reason why not.

20 20 EQUITY INJECTION Must NOT be borrowed! UNLESS: Borrowed equity from seller on FULL standby or PROVEN ability to repay the borrowed equity from NON BUSINESS applicant funds

21 Equity injection (cont d) 21 HOW MUCH? What type? AGAIN..what is DEFINED AS PRUDENT?

22 Guidance directly from SBA! 22 Equity injection Lenders should document equity injection at the same time they document the use of proceeds at closing. The Lender must not disburse a loan until it has proof of any required equity injection. Proper evidence of a Borrower s equity injection may include the copy of a check together with proof it was processed or a copy of an escrow settlement sheet with a bank account statement showing the injection into the business prior to disbursement. A promissory note, gift letter, or financial statement generally are not sufficient evidence. Lack of proper and complete documentation of an equity injection required in the Authorization is one of the most common reasons for a reduction or denial of SBA s guaranty at the time of purchase. If a Lender overlooks this requirement at the time of closing, the Lender usually finds it very difficult to adequately document equity injection at a later date.

23 BUSINESS VALUATIONS 23 A KEY COMPONENT IF financed amount for intangible assets is to be less than or equal to $250M, lender may complete its own valuation & must use same methods as used for non SBA loans. Credit memo must contain a thorough valuation analysis explanation. IF financed amount for intangible assets is to be over $250M, OR if a close relationship exists between buyer & seller, AN INDEPENDENT BUSINESS VALUATION from a QUALIFIED SOURCE is required!

24 WHAT IS A QUALIFIED SOURCE? 24 is an individual who regularly receives compensation for business valuations and is either A CPA that performs valuations in accordance with statements published by the American Institute of CPA s or

25 Qualified source for business valuations (cont d) 25 Accredited by one of the following: Accredited Senior Appraiser, American Society of Appraisers Certified Business Appraiser, Institute of Business Appraisers Accredited in Business Valuation, American Institute of Certified Public Accountants Certified Valuation Analyst, National Association of Certified Valuation Analysts Accredited Valuation Analyst, National Association of Certified Valuation Analysts

26 Business valuation (cont d) 26 To be requested by and prepared for the lender. If submitted as a NON PLP package, valuation to be included with application Going concern appraisal allowed if: Special use property Appraiser experienced in the particular industry Appraisal breaks down values to each component of business

27 Appraiser to identify 27 Scope of work Requested by & prepared for lender What is included in the sale Opinion of value Qualifications of valuator Valuator signature certifying info contained Note: cost of valuation may be passed along to borrower.

28 NO piggy back rides 28 Definition: When one or more lenders provide more than one loan to a borrower at or about the same time, for similar purpose(s) & where SBA loan is junior position to other loans PIGGY BACK LOANS ARE NOT ALLOWED! Of concern since business acquisitions may include multiple loan sources. Keep a watchful eye to avoid this scenario.

29 TERMS of the BIZ ACQ Loan 29 Maturity: maximum is 10 years UNLESS the LARGEST portion of the assets includes real estate which allows for 25 year maturity. Other terms & guidelines are the same as any other 7a loan. For future reference, see on and around page 156 of SOP

30 30 Business acquisitions that include a real estate component Separate real estate appraisal from business valuation. Appraisal report must be prepared in compliance with UNIFORM STANDARDS OF PROFESSIONAL APPRAISAL PRACTICE (USPAP) can be either a self contained or summary appraisal & addressed to lender Independent, no appearance of conflict of interest State licensed or state certified except if property estimated value over $1,000,000, then appraiser must be state certified.

31 SBA Guidance on real estate appraisals 31 A Lender may accept a SELF-CONTAINED APPRAISAL REPORT or a SUMMARY APPRAISAL REPORT however, a RESTRICTED APPRAISAL REPORT is never acceptable for an SBA-guaranteed loan. An acceptable appraisal will: Identify and describe the real property Identify the interest being appraised and include the legal description and known encumbrances State the purpose and intended use of the appraisal Define the value (cost, income or comparable sales) to be estimated State the dates of the appraisal and report Identify all assumptions and limiting conditions Specify how data was collected and reported Describe the information considered, procedures followed, analysis, opinions and conclusion Provide the appraiser s opinion of highest and best use, when appropriate Explain the exclusion of any usual valuation method Provide any additional information that may be appropriate Have the signature and certification of the appraiser and include a disclosure by the appraiser of any involvement or relationship with the owner.

32 Tax Transcript verification 32 Seller s tax returns are to verified with what was provided to the IRS. Sole proprietorship: verify Schedule C IF not possible, verify in another method & carefully document.

for at least a period of two")

33 33 Standby agreements Can be considered equity injection IF AND ONLY IF on full standby (interest and principal) for at least a period of two years

34 504 loans 34 Loan proceeds may be used to acquire long term fixed assets in conjunction with a change of ownership as long as: 1. Jobs will be retained as a result 2. The project meets one of the community development or public policy goals.

35 loans (cont d) Project costs must not exceed the value of the 504 eligible fixed assets. Loan proceeds are not to be used to purchase stock or short term assets.

36 Franchise transactions 36 Verify Franchise is SBA eligible Utilize the franchise registry FRANDATA.COM On SBA SITE: Franchise Findings SBA attorneys have assembled a listing of Issues of Eligibility they have identified in various franchise/license/dealer/jobber or similar agreements (Agreements), which SBA calls Franchise Findings. This list contains the names of those franchises and systems that have requirements in their Agreements that could cause the business to be ineligible for SBA Financial Assistance.. This list is only a guide and is not a substitute for a full review of the Agreement

37 Standard 7a and PLP submissions 37 PLP lenders can submit via standard process and must submit via standard process in certain circumstances. Any lender with an executed 750 agreement can submit to the Standard Loan Guaranty Processing center, Small Loan Advantage also available to any lender with an executed 750 agreement for term loans of up to $350,000.

38 The 159 form 38 For both 7a & 504 loans Fees charged by an agent clearly defined & have a necessary & reasonable relationship to services performed! If over $2, must be itemized, documented clearly

39 The Eligibility Questionnaire 39 Eligibility questionnaire for standard 7(a) guaranty. Requirements are the same for PLP lenders Change of Ownership Addendum F

40 Arm s length transactions 40 How to determine? How to mitigate if transaction does not appear to be at arm s length" NO APPEARANCE OF CONFLICT!

41 Credit memo considerations 41 For your later reference, be sure to review SOP pages for all required points in the credit analysis. EXPLAIN the reason for the change of ownership & why and how the business will benefit. Cash flow! Cash flow! All available collateral, if not one to one. Site visit!

42 SBA Submission guidance 42 Refer to SBA s ten tab submission format Via SBA website E tran Send this file Yup you can still mail or even fax!

43 Documentation considerations 43 Verify business valuation, real estate valuation clearly explained in credit memo. Be sure change in ownership benefits the business & documented clearly. If partner buyout, verify ownership percentages before and after

44 Loan Disbursement considerations 44 One 1050 form at closing Attach proof of how proceeds were disbursed to this form TRUST BUT VERIFY!

45 Keep perspective! 45 Some reminders to ask yourself & your colleagues: Does it all make sense? What is the biggest impact? What is the worst case scenario?

46 In conclusion KEY POINTS 46 Valuation IS KEY!!! CLEARLY define reason for change Address intangibles 100% change in ownership AND VERIFY! Watch for any appearance of conflict. Example: seller not to be an associate.

47 Thank you for tuning in 47 Lisa G. Lerner, Enhanced Consultive Solutions, LLC Helping you achieve your SBA lending goals Loan Administration/Expertise in SBA Lending In association with COLEMAN PUBLISHING, INC.

HOW TO DOCUMENT EQUITY INJECTION GETTING IT RIGHT, 100% OF THE TIME. Coleman Webinar November 14, 2012

HOW TO DOCUMENT EQUITY INJECTION GETTING IT RIGHT, 100% OF THE TIME Coleman Webinar November 14, 2012 Small Business Banking News of the Day Talk Show Bob and Charles Show 1:50-2:00 PM ET. We are featuring

HOW TO DOCUMENT EQUITY INJECTION GETTING IT RIGHT, 100% OF THE TIME Coleman Webinar November 14, 2012 Small Business Banking News of the Day Talk Show Bob and Charles Show 1:50-2:00 PM ET. We are featuring

Complimentary Coleman Report Live!

Complimentary Coleman Report Live! Featuring Bob Coleman & Charles Green 1:50-2:00 PM E.T. Log on 10 minutes early before every Coleman webinar for a briefing on issues vital to the small business lending

Complimentary Coleman Report Live! Featuring Bob Coleman & Charles Green 1:50-2:00 PM E.T. Log on 10 minutes early before every Coleman webinar for a briefing on issues vital to the small business lending

Coleman Certified SBA 7(a) Loan Closer Lance A. Sexton, Coleman Faculty Instructor

Loan Closer Lance A. Sexton, Coleman Faculty Instructor") Coleman Certified SBA 7(a) Loan Closer Lance A. Sexton, Coleman Faculty Instructor Setting Up the SBA Loan File There are a number of ways to set up a loan file. My recommendation for the SBA Loan File

Coleman Certified SBA 7(a) Loan Closer Lance A. Sexton, Coleman Faculty Instructor Setting Up the SBA Loan File There are a number of ways to set up a loan file. My recommendation for the SBA Loan File

Growing Strategically through Business Acquisition. Monday July am 12 pm

Growing Strategically through Business Acquisition Monday July 16 11 am 12 pm On the line Jessica Fialkovich, Co-Founder & President Transworld Business Advisors Rocky Mountain Jessica Stutz, Special Markets

Growing Strategically through Business Acquisition Monday July 16 11 am 12 pm On the line Jessica Fialkovich, Co-Founder & President Transworld Business Advisors Rocky Mountain Jessica Stutz, Special Markets

7(a) LOAN APPLICATION PROCESS AT THE LGPC

LOAN APPLICATION PROCESS AT THE LGPC") 7(a) LOAN APPLICATION PROCESS AT THE LGPC 7(a) LOAN GUARANTY PROGRAM Flexible financing for your small business customers Igniting the Flames of Success OFO/OCA LENDER RELATIONS SPECIALISTS TRAINING September

7(a) LOAN APPLICATION PROCESS AT THE LGPC 7(a) LOAN GUARANTY PROGRAM Flexible financing for your small business customers Igniting the Flames of Success OFO/OCA LENDER RELATIONS SPECIALISTS TRAINING September

Effective Date: May 1,

divestiture of all ownership interest and severance of any relationship with the Small Business Applicant (and any associated Eligible Passive Concern) in any capacity, including being an employee (paid

divestiture of all ownership interest and severance of any relationship with the Small Business Applicant (and any associated Eligible Passive Concern) in any capacity, including being an employee (paid

CHAPTER 2 - LOAN CLOSING

CHAPTER 2 - LOAN CLOSING This chapter provides the Lender with guidance on closing and disbursing 7(a) loans in compliance with SBA requirements. It explains SBA s requirements by reviewing the 7(a) Loan

CHAPTER 2 - LOAN CLOSING This chapter provides the Lender with guidance on closing and disbursing 7(a) loans in compliance with SBA requirements. It explains SBA s requirements by reviewing the 7(a) Loan

SBA One Training Session

SBA One Training Session Topic: Tips & Tricks: Loan Origination Date/Time: March 14 th, 2017 at 2 PM ET Presenter: Genevieve Sansom is a Vice President Relationship Manager with Bank of New York Mellon

SBA One Training Session Topic: Tips & Tricks: Loan Origination Date/Time: March 14 th, 2017 at 2 PM ET Presenter: Genevieve Sansom is a Vice President Relationship Manager with Bank of New York Mellon

SBA One Training Session

SBA One Training Session Topic: A Closer Look: Loan Origination Date/Time: February 27 th, 2017 at 2 PM ET Presenter: Josh Dykema works for SBA s Office of Performance and Systems Management (OPSM). OPSM

SBA One Training Session Topic: A Closer Look: Loan Origination Date/Time: February 27 th, 2017 at 2 PM ET Presenter: Josh Dykema works for SBA s Office of Performance and Systems Management (OPSM). OPSM

SBA One Tips & Tricks Wisconsin Lenders Conference 2017 SBA Simplified LLC May 18, 2017

SBA One Tips, Tricks & Issues May 18, 2017 SBA Lender Training Wisconsin Dells, Wisconsin Presenter: Coralie Myers info@sbasimplified.com 1 Points to Remember About SBA One A Work in Progress Give Feedback

SBA One Tips, Tricks & Issues May 18, 2017 SBA Lender Training Wisconsin Dells, Wisconsin Presenter: Coralie Myers info@sbasimplified.com 1 Points to Remember About SBA One A Work in Progress Give Feedback

Complimentary Coleman Report Live!

Complimentary Coleman Report Live! Featuring Bob Coleman & Beth Solomon 11:50-12:00 PM E.T. Log on 10 minutes early before every Coleman webinar for a briefing on issues vital to the small business lending

Complimentary Coleman Report Live! Featuring Bob Coleman & Beth Solomon 11:50-12:00 PM E.T. Log on 10 minutes early before every Coleman webinar for a briefing on issues vital to the small business lending

ELIGIBILITY INFORMATION REQUIRED FOR PLP SUBMISSION Rev. 11/25/08

ELIGIBILITY INFORMATION REQUIRED FOR PLP SUBMISSION Rev. 11/25/08 1. Fill out all of this section. If a question in this section is answered No, the loan is not eligible. Applicant Name Lender Name Purpose

ELIGIBILITY INFORMATION REQUIRED FOR PLP SUBMISSION Rev. 11/25/08 1. Fill out all of this section. If a question in this section is answered No, the loan is not eligible. Applicant Name Lender Name Purpose

Massachusetts District Office April 5, 2018 SEED ANNUAL TRAINING

Massachusetts District Office April 5, 2018 SEED ANNUAL TRAINING 1 See SBA Information Notice 5000-1708, Issuance of SOP 50 10 5 (J), for more detailed information of major changes to SOP, and SBA Information

Massachusetts District Office April 5, 2018 SEED ANNUAL TRAINING 1 See SBA Information Notice 5000-1708, Issuance of SOP 50 10 5 (J), for more detailed information of major changes to SOP, and SBA Information

Today s Presenter. The SBA Authorization Wisconsin SBA Lenders Conference May 19, SBA Loan Closing: Proper Documentation & Pitfalls

2016 Wisconsin SBA Lenders Conference May 19, 2016 SBA Loan Closing: Proper Documentation & Pitfalls Today s Presenter Nick Jellum, Anastasi Jellum P.A. 14985 60 th Street North, Stillwater, MN 55082 Phone:

2016 Wisconsin SBA Lenders Conference May 19, 2016 SBA Loan Closing: Proper Documentation & Pitfalls Today s Presenter Nick Jellum, Anastasi Jellum P.A. 14985 60 th Street North, Stillwater, MN 55082 Phone:

Deep Dive into Portfolio Management and the National Guaranty Purchase Center. Presented by: Susan Suckfiel and Vanessa Piccioni

Deep Dive into Portfolio Management and the National Guaranty Purchase Center Presented by: Susan Suckfiel and Vanessa Piccioni Overview 10-Tab Packages & the Purchase Review Common Reasons for Repairs

Deep Dive into Portfolio Management and the National Guaranty Purchase Center Presented by: Susan Suckfiel and Vanessa Piccioni Overview 10-Tab Packages & the Purchase Review Common Reasons for Repairs

Guaranty Purchase Roles and Responsibilities. SBA Fresno Commercial Loan Servicing Center Presents GUIDANCE ON SBA 7A LOAN SERVICING & PURCHASING

SBA Fresno Commercial Loan Servicing Center Presents GUIDANCE ON SBA 7A LOAN SERVICING & PURCHASING Green = Fresno Yellow = Little Rock Guaranty Purchase Roles and Responsibilities Both FCLSC and LRCLSC

SBA Fresno Commercial Loan Servicing Center Presents GUIDANCE ON SBA 7A LOAN SERVICING & PURCHASING Green = Fresno Yellow = Little Rock Guaranty Purchase Roles and Responsibilities Both FCLSC and LRCLSC

SBA Lending: Documenting, Closing and Servicing 7(a) and CDC/504 Loans

and CDC/504 Loans") Presenting a live 90-minute webinar with interactive Q&A SBA Lending: Documenting, Closing and Servicing 7(a) and CDC/504 Loans Navigating SBA Approval and Authorization Process, Preserving the Loan Guaranty

Presenting a live 90-minute webinar with interactive Q&A SBA Lending: Documenting, Closing and Servicing 7(a) and CDC/504 Loans Navigating SBA Approval and Authorization Process, Preserving the Loan Guaranty

Welcome to the 7(a) Connect Call

Connect Call") Welcome to the 7(a) Connect Call During this call we will provide updates, training tips and hot topics on the Office of Capital Access There will be time allotted for questions and answers. Office of

Welcome to the 7(a) Connect Call During this call we will provide updates, training tips and hot topics on the Office of Capital Access There will be time allotted for questions and answers. Office of

ANALYZING POTENTIAL OWNERSHIP TRANSITION OPTIONS UTILIZING DEFERRED COMPENSATION ARRANGEMENTS

ANALYZING POTENTIAL OWNERSHIP TRANSITION OPTIONS UTILIZING DEFERRED COMPENSATION ARRANGEMENTS by Ronald J. Adams, CPA, CVA, ABV, CBA, CFF, FVS, CGMA Many smaller companies want to share ownership with

ANALYZING POTENTIAL OWNERSHIP TRANSITION OPTIONS UTILIZING DEFERRED COMPENSATION ARRANGEMENTS by Ronald J. Adams, CPA, CVA, ABV, CBA, CFF, FVS, CGMA Many smaller companies want to share ownership with

SBA Information Notice

SBA Information Notice TO: All SBA Employees, 7(a) Lenders and Certified Development Companies CONTROL NO.: 5000-17008 SUBJECT: Issuance of SOP 50 10 5(J) EFFECTIVE: October 13, 2017 The purpose of this

SBA Information Notice TO: All SBA Employees, 7(a) Lenders and Certified Development Companies CONTROL NO.: 5000-17008 SUBJECT: Issuance of SOP 50 10 5(J) EFFECTIVE: October 13, 2017 The purpose of this

Lending confidence. The Intricacies of SBA Lending: What You Need to Know

Lending confidence. The Intricacies of SBA Lending: What You Need to Know The Intricacies of SBA Lending: What You Need to Know Is your financial institution looking to get into the SBA lending market?

Lending confidence. The Intricacies of SBA Lending: What You Need to Know The Intricacies of SBA Lending: What You Need to Know Is your financial institution looking to get into the SBA lending market?

Office of Capital Access. Monthly LRS Call. April 19, 2017

Office of Capital Access Monthly LRS Call April 19, 2017 Bill Manger Associate Administrator Office of Capital Access U.S. Small Business Administration Email: william.manger@sba.gov 2 Agency Goal New

Office of Capital Access Monthly LRS Call April 19, 2017 Bill Manger Associate Administrator Office of Capital Access U.S. Small Business Administration Email: william.manger@sba.gov 2 Agency Goal New

LiftFund (CDC) 504 Checklist and Loan Application

504 Checklist and Loan Application") 1. 2. LiftFund (CDC) 504 Checklist and Loan Application Copy of photo ID (Driver license) History of the Business. (Business Plan for start-ups.) Equal Opportunity Lender 3. Current personal financial

1. 2. LiftFund (CDC) 504 Checklist and Loan Application Copy of photo ID (Driver license) History of the Business. (Business Plan for start-ups.) Equal Opportunity Lender 3. Current personal financial

How to Complete the New SBA 7(a) Litigation 7 Tab Package SOP (Effective Date: March 1, 2013)

Litigation 7 Tab Package SOP (Effective Date: March 1, 2013)") How to Complete the New SBA 7(a) Litigation 7 Tab Package SOP 50 57 (Effective Date: March 1, 2013) The United States Small Business Administration ( SBA ), in SOP 50 57 ( SOP ), recently promulgated Litigation

How to Complete the New SBA 7(a) Litigation 7 Tab Package SOP 50 57 (Effective Date: March 1, 2013) The United States Small Business Administration ( SBA ), in SOP 50 57 ( SOP ), recently promulgated Litigation

SBA will officially launch the 504 Debt Refinancing program on June 24, 2016

SBA has received statutory authority to reauthorize the 504 Debt Refinance Program for up to $7.5 billion. This is in addition to the $7.5 billion authorization for the 504 program. With this change, total

SBA has received statutory authority to reauthorize the 504 Debt Refinance Program for up to $7.5 billion. This is in addition to the $7.5 billion authorization for the 504 program. With this change, total

SBA Highlights. Michelle Torres DFW District Office 4300 Amon Carter Blvd Ste 114 Fort Worth, TX February 15, 2018

SBA Highlights Michelle Torres DFW District Office 4300 Amon Carter Blvd Ste 114 Fort Worth, TX 76155 February 15, 2018 TIPS & REMINDERS New SBA Form 1919 and SBA Form 1920 Veteran Fee Waivers: SBA Express=

SBA Highlights Michelle Torres DFW District Office 4300 Amon Carter Blvd Ste 114 Fort Worth, TX 76155 February 15, 2018 TIPS & REMINDERS New SBA Form 1919 and SBA Form 1920 Veteran Fee Waivers: SBA Express=

Small Business Administration 7(a) Loan Guaranty Program

Loan Guaranty Program") Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government February 12, 2015 Congressional Research Service 7-5700 www.crs.gov R41146 Summary

Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government February 12, 2015 Congressional Research Service 7-5700 www.crs.gov R41146 Summary

Wholesale Originations Best Practices

Wholesale Originations Best Practices Available at: http://www.freddiemac.com/singlefamily/quality_control.html Table of Contents CHAPTER 1 WHOLESALE ORIGINATIONS... WO1-1 INTRODUCTION... WO1-1 GENERAL

Wholesale Originations Best Practices Available at: http://www.freddiemac.com/singlefamily/quality_control.html Table of Contents CHAPTER 1 WHOLESALE ORIGINATIONS... WO1-1 INTRODUCTION... WO1-1 GENERAL

ELIGIBILITY MATRIX & SUMMARY GUIDELINES 15 & 30 YR Fixed Rates

Revised 6/2/2014 Changes from prior versions are in red font Overlays to Fannie guidelines are underlined Correspondent Lending Jumbo "Premier" Fixed Rate and ARM Product Profile Based on a Fannie Mae

Revised 6/2/2014 Changes from prior versions are in red font Overlays to Fannie guidelines are underlined Correspondent Lending Jumbo "Premier" Fixed Rate and ARM Product Profile Based on a Fannie Mae

Selling an Insurance Agency

Selling an Insurance Agency Financing for insurance professionals a complimentary whitepaper for agents and brokers How to get the right price from the right buyer As a wave of consolidation readies itself

Selling an Insurance Agency Financing for insurance professionals a complimentary whitepaper for agents and brokers How to get the right price from the right buyer As a wave of consolidation readies itself

and Sheltering Your Capital Gain

Selling to Your Employees through a Worker Cooperative - and Sheltering Your Capital Gain Eric D. Britton & Mark C. Stewart Editor's note: Since 1984, Federal Tax law has permitted owners who sell 30%

Selling to Your Employees through a Worker Cooperative - and Sheltering Your Capital Gain Eric D. Britton & Mark C. Stewart Editor's note: Since 1984, Federal Tax law has permitted owners who sell 30%

GENERAL FINANCING QUESTIONS

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

January-June 2019 Loan Application and Information

January-June 2019 Loan Application and Information Introduction The Loan Repayment Assistance Program of Minnesota ( LRAP or LRAP MN ) exists to support recent law graduates in choosing employment in the

January-June 2019 Loan Application and Information Introduction The Loan Repayment Assistance Program of Minnesota ( LRAP or LRAP MN ) exists to support recent law graduates in choosing employment in the

Topics for this Session

welcome Topics for this Session Quick discussion of SBA s debt refinancing requirements Walk through of some refinancing scenarios 2 Copyright 2017, NAGGL, Inc. - Do Not Copy/Distribute 1 Why is SBA So

welcome Topics for this Session Quick discussion of SBA s debt refinancing requirements Walk through of some refinancing scenarios 2 Copyright 2017, NAGGL, Inc. - Do Not Copy/Distribute 1 Why is SBA So

July 1, 2019 June 30, 2020 Loan Application Information and Instructions

P July 1, 2019 June 30, 2020 Loan Application Information and Instructions Introduction LRAP Minnesota helps reduce the education debt burden experienced by dedicated public interest lawyers who represent

P July 1, 2019 June 30, 2020 Loan Application Information and Instructions Introduction LRAP Minnesota helps reduce the education debt burden experienced by dedicated public interest lawyers who represent

PROCEDURAL MANUAL ALABAMA HOUSING FINANCE AUTHORITY

PROCEDURAL MANUAL ALABAMA HOUSING FINANCE AUTHORITY CONTENTS INTRODUCTION SECTION I DEFINITIONS... 4 SECTION II MORTGAGOR ELIGIBILITY EVALUATION... 6 A. Income Restrictions... 6 B. Occupancy... 6 C. Residence

PROCEDURAL MANUAL ALABAMA HOUSING FINANCE AUTHORITY CONTENTS INTRODUCTION SECTION I DEFINITIONS... 4 SECTION II MORTGAGOR ELIGIBILITY EVALUATION... 6 A. Income Restrictions... 6 B. Occupancy... 6 C. Residence

2018 SBA 7(a) LOAN CLOSING TRAINING ONLINE ON DEMAND ON YOUR SCHEDULE

LOAN CLOSING TRAINING ONLINE ON DEMAND ON YOUR SCHEDULE") 2018 SBA 7(a) LOAN CLOSING TRAINING ONLINE ON DEMAND ON YOUR SCHEDULE REGISTRATION IS ALWAYS OPEN Need 7(a) Loan Closing Training or CLE hours? Want the convenience of training on your schedule? Want affordable

2018 SBA 7(a) LOAN CLOSING TRAINING ONLINE ON DEMAND ON YOUR SCHEDULE REGISTRATION IS ALWAYS OPEN Need 7(a) Loan Closing Training or CLE hours? Want the convenience of training on your schedule? Want affordable

Glossary BankNewport All rights reserved.

Glossary 2015 BankNewport All rights reserved. Glossary 2 504 Loan Program Includes a loan secured with a senior lien from a private-sector lender covering up to 50% of the project cost, a loan secured

Glossary 2015 BankNewport All rights reserved. Glossary 2 504 Loan Program Includes a loan secured with a senior lien from a private-sector lender covering up to 50% of the project cost, a loan secured

Alger Insurance and Consulting LLC Commercial Lending Application

Alger Insurance and Consulting LLC Commercial Lending Application COMMERCIAL LOAN APPLICATION This checklist is provided to assist in gathering the necessary information needed for the initial evaluation

Alger Insurance and Consulting LLC Commercial Lending Application COMMERCIAL LOAN APPLICATION This checklist is provided to assist in gathering the necessary information needed for the initial evaluation

MEGA ALT ARM (MA5/1)

") MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

Victor W. Vaccaro, Jr., CPA/ABV, CFF, CDA

Victor W. Vaccaro, Jr., CPA/ABV, CFF, CDA Successful Strategies for Ownership Transition If you don t know where you re going, you ll end up someplace else. - Yogi Berra 2 What is a Business Succession

Victor W. Vaccaro, Jr., CPA/ABV, CFF, CDA Successful Strategies for Ownership Transition If you don t know where you re going, you ll end up someplace else. - Yogi Berra 2 What is a Business Succession

RULES OF TENNESSEE DEPARTMENT OF TREASURY CHAPTER SMALL AND MINORITY-OWNED BUSINESS ASSISTANCE PROGRAM TABLE OF CONTENTS

RULES OF TENNESSEE DEPARTMENT OF TREASURY CHAPTER 1700-6-1 SMALL AND MINORITY-OWNED BUSINESS ASSISTANCE PROGRAM TABLE OF CONTENTS 1700-6-1-.01 In General 1700-6-1-.08 Authority Over Program Fund 1700-6-1-.02

RULES OF TENNESSEE DEPARTMENT OF TREASURY CHAPTER 1700-6-1 SMALL AND MINORITY-OWNED BUSINESS ASSISTANCE PROGRAM TABLE OF CONTENTS 1700-6-1-.01 In General 1700-6-1-.08 Authority Over Program Fund 1700-6-1-.02

Statutory Requirements

In December 2015, SBA received statutory authority to reauthorize the 504 Debt Refinance Program for up to $7.5 billion. This is in addition to the $7.5 billion authorization for the 504 program. With

In December 2015, SBA received statutory authority to reauthorize the 504 Debt Refinance Program for up to $7.5 billion. This is in addition to the $7.5 billion authorization for the 504 program. With

Mortgage Processing Policy Manual Table of Contents [Sample Client] Table of Contents

![Mortgage Processing Policy Manual Table of Contents [Sample Client] Table of Contents](/thumbs/94/118687243.jpg "Mortgage Processing Policy Manual Table of Contents [Sample Client] Table of Contents") Table of Contents Table of Contents TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING...

Table of Contents Table of Contents TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING...

How to Pre-Screen Deals from a Business Appraiser & BDO s Perspective 2015 AMERICA EAST CONFERENCE August 13, 2015

How to Pre-Screen Deals from a Business Appraiser & BDO s Perspective 2015 AMERICA EAST CONFERENCE August 13, 2015 Neal Patel, CBA, CVA Scott Gilman Neal Patel, CBA, CVA Neal Patel, CBA, CVA is the Principal

How to Pre-Screen Deals from a Business Appraiser & BDO s Perspective 2015 AMERICA EAST CONFERENCE August 13, 2015 Neal Patel, CBA, CVA Scott Gilman Neal Patel, CBA, CVA Neal Patel, CBA, CVA is the Principal

IS AN ESOP RIGHT FOR YOU?

FEBRUARY 2018 Greg Daugherty 614.227.2005 gdaugherty@porterwright.com A guide to understanding employee stock ownership plans In recent years, ESOPs have become an increasingly popular business succession

FEBRUARY 2018 Greg Daugherty 614.227.2005 gdaugherty@porterwright.com A guide to understanding employee stock ownership plans In recent years, ESOPs have become an increasingly popular business succession

Investor s Guide for Equity CrowdFunding Under Regulation CrowdFunding (Title III)

") Investor s Guide for Equity CrowdFunding Under Regulation CrowdFunding (Title III) DreamFunded Marketplace, LLC. May 2016 Introduction As recent history shows, crowdfunding can be an incredible tool for

Investor s Guide for Equity CrowdFunding Under Regulation CrowdFunding (Title III) DreamFunded Marketplace, LLC. May 2016 Introduction As recent history shows, crowdfunding can be an incredible tool for

(TC) TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE

TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE") AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

How to Package a Project Loan Request By James Conlow

How to Package a Project Loan Request By James Conlow Financing is about one thing: Profitable Exit for the Financier. The financing request for a loan must satisfy a single basic requirement: 1. Verified

How to Package a Project Loan Request By James Conlow Financing is about one thing: Profitable Exit for the Financier. The financing request for a loan must satisfy a single basic requirement: 1. Verified

SBA One SBA SB A s N ew Streamlilined O nliline L endi ding Platform

SBA One SBA s New Streamlined donline Lending Platform Agenda I. Overview II. Getting Started III. My Workspace IV. Loan Origination Solution & RAPID V. Document Management & E Signature VI. VII. PARRIS

SBA One SBA s New Streamlined donline Lending Platform Agenda I. Overview II. Getting Started III. My Workspace IV. Loan Origination Solution & RAPID V. Document Management & E Signature VI. VII. PARRIS

Loan sizes start at 1+ million or higher No collateral from client neededcollateral

Loan sizes start at 1+ million or higher No collateral from client neededcollateral provided from third party Short term loan (30, 60, 90, 6 months, 1 year with rollover options) All Payments made upfront

Loan sizes start at 1+ million or higher No collateral from client neededcollateral provided from third party Short term loan (30, 60, 90, 6 months, 1 year with rollover options) All Payments made upfront

Breakout Session V Environmental Reviews: Get Them Right Tuesday, November 8 1:45 pm 2:45 pm Golden Gate Ballroom 2-3

Breakout Session V Environmental Reviews: Get Them Right Tuesday, November 8 1:45 pm 2:45 pm Golden Gate Ballroom 2-3 Thank you to our Alliance Partners 2 Speakers Eric Adams, District Counsel U.S. Small

Breakout Session V Environmental Reviews: Get Them Right Tuesday, November 8 1:45 pm 2:45 pm Golden Gate Ballroom 2-3 Thank you to our Alliance Partners 2 Speakers Eric Adams, District Counsel U.S. Small

Avoiding Common Underwriting Errors

September 2015 2012 Genworth Financial, Inc. All rights reserved. Agenda General Underwriting Tips Resources and tools Capacity Credit History Capital Common Sense Compliance 1 Resources Job Aides, Tools

September 2015 2012 Genworth Financial, Inc. All rights reserved. Agenda General Underwriting Tips Resources and tools Capacity Credit History Capital Common Sense Compliance 1 Resources Job Aides, Tools

Land Acquisition and Development Finance Part VI

Land Acquisition and Development Finance Part VI In last month s Learn article, we discussed financing structures for development using OPM (Other People s Money). In this article we will discuss organization

Land Acquisition and Development Finance Part VI In last month s Learn article, we discussed financing structures for development using OPM (Other People s Money). In this article we will discuss organization

Closing Disclosure Form

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

SUBORDINATION REQUIREMENTS

SUBORDINATION REQUIREMENTS This communication is in response to your request for the (SLS) subordination requirements. Below are the general guidelines for either a refinance or loan modification subordination.

SUBORDINATION REQUIREMENTS This communication is in response to your request for the (SLS) subordination requirements. Below are the general guidelines for either a refinance or loan modification subordination.

A FIDUCIARY'S GUIDE TO SELECTING A FINANCIAL ADVISER AND REVIEWING AN ESOP STOCK VALUATION REPORT

Winter 2006 ESOP Financial Advisory Insights Insights 17 A FIDUCIARY'S GUIDE TO SELECTING A FINANCIAL ADVISER AND REVIEWING AN ESOP STOCK VALUATION REPORT Timothy J. Meinhart This discussion summarizes

Winter 2006 ESOP Financial Advisory Insights Insights 17 A FIDUCIARY'S GUIDE TO SELECTING A FINANCIAL ADVISER AND REVIEWING AN ESOP STOCK VALUATION REPORT Timothy J. Meinhart This discussion summarizes

FINAL CAPLINES CHANGES TO SOP (D)

") FINAL CAPLINES CHANGES TO SOP 50 10 5(D) 9-15-2011 Subpart A: Chapter 1 Pg. 9 Deleted additional qualifications for lenders to participate in CAPLines, including removing the Lenders Qualification Survey

FINAL CAPLINES CHANGES TO SOP 50 10 5(D) 9-15-2011 Subpart A: Chapter 1 Pg. 9 Deleted additional qualifications for lenders to participate in CAPLines, including removing the Lenders Qualification Survey

MINIMUM MORTGAGE: None

LOAN PROGRAM DESCRIPTION:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 3 AGE OF DOCUMENTS:... 3 APPLICATION REQUIREMENTS:...

LOAN PROGRAM DESCRIPTION:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 3 AGE OF DOCUMENTS:... 3 APPLICATION REQUIREMENTS:...

Correspondent Lending SEPTEMBER 2016 COMMON SUSPENSE DEFICIENCIES IN FOCUS DEFICIENCY REQUIREMENTS

Nationstar Mortgage is committed to providing the performance tools needed by our Correspondents to better manage their overall quality efforts. By focusing on this process, we are able to spotlight areas

Nationstar Mortgage is committed to providing the performance tools needed by our Correspondents to better manage their overall quality efforts. By focusing on this process, we are able to spotlight areas

Small Business Administration 7(a) Loan Guaranty Program

Loan Guaranty Program") Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government May 1, 2013 CRS Report for Congress Prepared for Members and Committees of Congress

Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government May 1, 2013 CRS Report for Congress Prepared for Members and Committees of Congress

Correspondent Lending Division Seller Partner Eligibility Policy

Correspondent Lending Division Seller Partner Eligibility Policy Overview Nations Direct Mortgage, LLC Correspondent Division (NDM Correspondent) is designed as an opportunity to partner with experienced

Correspondent Lending Division Seller Partner Eligibility Policy Overview Nations Direct Mortgage, LLC Correspondent Division (NDM Correspondent) is designed as an opportunity to partner with experienced

CORRESPONDENT LENDING ANNOUNCEMENT

CORRESPONDENT LENDING ANNOUNCEMENT AIG Correspondent Lending Guideline Update Summary April 12, 2018 The following is a summary of the updates to AIG Correspondent Lending s Seller s Guide, Conforming

CORRESPONDENT LENDING ANNOUNCEMENT AIG Correspondent Lending Guideline Update Summary April 12, 2018 The following is a summary of the updates to AIG Correspondent Lending s Seller s Guide, Conforming

AFR JUMBO OVERVIEW COPYRIGHT 2017 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

12/20/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

12/20/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

Wrap Note Checklist - p 1 Information needed for Sales Contract and Closing

Home Owner Name(s): Property Address: Name(s) on the Deed: How Quickly Can you Close: Loan Information Lender Name: Lender Phone Number: Loan Number: Loan Origination Date: Loan Type (Fixed, ARM, Interest

Home Owner Name(s): Property Address: Name(s) on the Deed: How Quickly Can you Close: Loan Information Lender Name: Lender Phone Number: Loan Number: Loan Origination Date: Loan Type (Fixed, ARM, Interest

RxLegacy Pharmacy Ownership Overview

RxLegacy Pharmacy Ownership Overview ACPE # 0130 9999 17 074 L04 P&T Accredited for 2.5 CE Hours Disclosure & Session Objectives Amanda Fields, APRx General Counsel afields@aprx.org (preferred) 877 634

RxLegacy Pharmacy Ownership Overview ACPE # 0130 9999 17 074 L04 P&T Accredited for 2.5 CE Hours Disclosure & Session Objectives Amanda Fields, APRx General Counsel afields@aprx.org (preferred) 877 634

Investors Choice Commercial Leasing, LLC Credit Policy. Effective August 1, 2017

Investors Choice Commercial Leasing, LLC Credit Policy Effective August 1, 2017 1 Investors Choice Commercial Leasing, LLC (ICCL)Credit Policies and Procedures have been designed to insure transactions

Investors Choice Commercial Leasing, LLC Credit Policy Effective August 1, 2017 1 Investors Choice Commercial Leasing, LLC (ICCL)Credit Policies and Procedures have been designed to insure transactions

Victor W. Vaccaro, Jr., CPA/ABV, CFF, CDA

Victor W. Vaccaro, Jr., CPA/ABV, CFF, CDA Successful Strategies for Ownership Transition If you don t know where you re going, you ll end up someplace else. - Yogi Berra 2 What is a Business Succession

Victor W. Vaccaro, Jr., CPA/ABV, CFF, CDA Successful Strategies for Ownership Transition If you don t know where you re going, you ll end up someplace else. - Yogi Berra 2 What is a Business Succession

Private Party Purchase Cover Sheet

Private Party Purchase Cover Sheet To: Lending Operations From: FARM BUREAU AGENT E-mail: LendingFax@farmbureaubank.com Contact Number: ( ) - Fax: 800.499.4950 Email: farmbureau@agent.com Date: Total Number

Private Party Purchase Cover Sheet To: Lending Operations From: FARM BUREAU AGENT E-mail: LendingFax@farmbureaubank.com Contact Number: ( ) - Fax: 800.499.4950 Email: farmbureau@agent.com Date: Total Number

Insurance Distribution Company Due Diligence & Contracts presented by Chris Hughes Merger & Acquisition Services

Insurance Distribution Company Due Diligence & Contracts presented by Chris Hughes Merger & Acquisition Services The materials presented during the webinar are for informational purposes only. They are

Insurance Distribution Company Due Diligence & Contracts presented by Chris Hughes Merger & Acquisition Services The materials presented during the webinar are for informational purposes only. They are

A Place to Rent. 1/3 of people in the United States Single people, young married couples, and older adults Mobile lifestyles

Obtaining Housing A Place to Rent 1/3 of people in the United States Single people, young married couples, and older adults Mobile lifestyles Security Deposit A payment that ensures the owner against financial

Obtaining Housing A Place to Rent 1/3 of people in the United States Single people, young married couples, and older adults Mobile lifestyles Security Deposit A payment that ensures the owner against financial

USDA STREAMLINE ASSIST

USDA STREAMLINE ASSIST (MUST CURRENTLY BE A USDA LOAN-CANNOT BE DIRECT) Minimum Credit Score Max Loan Amount Balance Appraisal Seasoning Current Mortgage Credit Can GUS be used Net Tangible Benefit Annual

USDA STREAMLINE ASSIST (MUST CURRENTLY BE A USDA LOAN-CANNOT BE DIRECT) Minimum Credit Score Max Loan Amount Balance Appraisal Seasoning Current Mortgage Credit Can GUS be used Net Tangible Benefit Annual

HOME MORTGAGE PROGRAMS

HOME MORTGAGE PROGRAMS OPERATING MANUAL CONNECTICUT HOUSING FINANCE AUTHORITY 999 West Street, Rocky Hill, CT 06067-4005 Main: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Revision 12-2017

HOME MORTGAGE PROGRAMS OPERATING MANUAL CONNECTICUT HOUSING FINANCE AUTHORITY 999 West Street, Rocky Hill, CT 06067-4005 Main: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Revision 12-2017

JUMBO PRIME PROGRAM (FIXED & ARM)

") JUMBO PRIME PROGRAM (FIXED & ARM) PRIMARY RESIDENCE Purchase & Rate/Term Refinance (1),(2) Units Min. FICO LTV/CLTV/ HCLTV Max. DTI Max. Loan Amount 700 80% 43% 1 unit 680 80% 35% 680 70% 43% 740 80% 43%

JUMBO PRIME PROGRAM (FIXED & ARM) PRIMARY RESIDENCE Purchase & Rate/Term Refinance (1),(2) Units Min. FICO LTV/CLTV/ HCLTV Max. DTI Max. Loan Amount 700 80% 43% 1 unit 680 80% 35% 680 70% 43% 740 80% 43%

ESOPS: CONTINUING A LEGACY

ESOPS: CONTINUING A LEGACY November 19, 2015 Cara Benningfield, CPA Director cbenningfield@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing

ESOPS: CONTINUING A LEGACY November 19, 2015 Cara Benningfield, CPA Director cbenningfield@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing

Fannie & High BalanceGuidelines

Fannie & High BalanceGuidelines Agency Finance Type Occupancy Term High balance and transactions with non-occupant coborrowers are limited to 95% LTV/CLTV. High Balance Cash Out Transactions are limited

Fannie & High BalanceGuidelines Agency Finance Type Occupancy Term High balance and transactions with non-occupant coborrowers are limited to 95% LTV/CLTV. High Balance Cash Out Transactions are limited

10, 15, 20, 25 & 30 YR Fixed Rates

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

HOMEPATH BUYERS GUIDE

HOMEPATH BUYERS GUIDE WWW.HOMEPATH.COM Buyers Guide Buyers Guide For a Fannie Mae-owned Home Whether you re buying your first home or your fifth, the experience can be exciting, confusing, overwhelming

HOMEPATH BUYERS GUIDE WWW.HOMEPATH.COM Buyers Guide Buyers Guide For a Fannie Mae-owned Home Whether you re buying your first home or your fifth, the experience can be exciting, confusing, overwhelming

HOW TO LOSE YOUR SBA GUARANTY

HOW TO LOSE YOUR SBA GUARANTY War Stories about lenders that did it the wrong way Presented by: Ethan W. Smith, Esq. Agenda: Basic Program Concepts/Terms Nature of the Guaranty Delegated Authority (PLP)

HOW TO LOSE YOUR SBA GUARANTY War Stories about lenders that did it the wrong way Presented by: Ethan W. Smith, Esq. Agenda: Basic Program Concepts/Terms Nature of the Guaranty Delegated Authority (PLP)

Small Business Administration 7(a) Loan Guaranty Program

Loan Guaranty Program") Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government February 18, 2016 Congressional Research Service 7-5700 www.crs.gov R41146 Summary

Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government February 18, 2016 Congressional Research Service 7-5700 www.crs.gov R41146 Summary

Loan Prospector Documentation Matrix

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Finding the Money You Need

Finding the Money You Need O ne key to a successful business start-up and expansion is your ability to obtain and secure appropriate financing. Raising capital is the most basic of all business activities.

Finding the Money You Need O ne key to a successful business start-up and expansion is your ability to obtain and secure appropriate financing. Raising capital is the most basic of all business activities.

Minority Business Enterprise and Women Owned Business Enterprise Loan Mobilization Program Rules

Minority Business Enterprise and Women Owned Business Enterprise Loan Mobilization Program Rules I. Introduction Overview The Minority Business Loan Mobilization Program was created by the Arkansas Economic

Minority Business Enterprise and Women Owned Business Enterprise Loan Mobilization Program Rules I. Introduction Overview The Minority Business Loan Mobilization Program was created by the Arkansas Economic

9/25/2018 PLAN SPONSOR ESOP ACCOUNTING AN OVERVIEW

PLAN SPONSOR ESOP ACCOUNTING AN OVERVIEW September 26, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is the person who registered

PLAN SPONSOR ESOP ACCOUNTING AN OVERVIEW September 26, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is the person who registered

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

Member Business Lending

MOTIVATE. BUILD. LEAD. Member Business Lending Foremost provider of Commerical lending services WHO WE ARE Member Business Lending (MBL) is a credit union service organization (CUSO) established in 2004

MOTIVATE. BUILD. LEAD. Member Business Lending Foremost provider of Commerical lending services WHO WE ARE Member Business Lending (MBL) is a credit union service organization (CUSO) established in 2004

Loan Product Advisor SM FHA TOTAL Mortgage Scorecard Documentation Matrix

Loan Product Advisor SM FHA TOTAL Mortgage Scorecard Documentation Matrix The information in this matrix is provided as a tool to help you document Federal Housing Administration (FHA) mortgages. The matrix

Loan Product Advisor SM FHA TOTAL Mortgage Scorecard Documentation Matrix The information in this matrix is provided as a tool to help you document Federal Housing Administration (FHA) mortgages. The matrix

Manufactured Homes Underwriting Reminders

Use this quick reference to help determine if the requirements for sale of a Mortgage secured by a Manufactured Home (MH) to Freddie Mac are met. Refer to Freddie Mac s Single-Family Seller/Servicer Guide

Use this quick reference to help determine if the requirements for sale of a Mortgage secured by a Manufactured Home (MH) to Freddie Mac are met. Refer to Freddie Mac s Single-Family Seller/Servicer Guide

Claim and Foreclosure Bidding Servicing Guide

Claims I Mortgage Insurance Claim and Foreclosure Bidding Servicing Guide Revised Let s help someone buy a house today. 8783606.0516 GENWORTH MORTGAGE INSURANCE CORPORATION CLAIM AND FORECLOSURE BIDDING

Claims I Mortgage Insurance Claim and Foreclosure Bidding Servicing Guide Revised Let s help someone buy a house today. 8783606.0516 GENWORTH MORTGAGE INSURANCE CORPORATION CLAIM AND FORECLOSURE BIDDING

HomePath Online Offers Guide for Listing Agents

HomePath Online Offers Guide for Listing Agents 2016 Fannie Mae. Trademarks of Fannie Mae. June 2016 1 Table of Contents Introduction... 3 HomePath Online Offers User Support... 3 Registration and Login...

HomePath Online Offers Guide for Listing Agents 2016 Fannie Mae. Trademarks of Fannie Mae. June 2016 1 Table of Contents Introduction... 3 HomePath Online Offers User Support... 3 Registration and Login...

SECONDARY PARTICIPATION GUARANTY AGREEMENT

OMB NO.: 3245-0185 EXPIRATION DATE: 2/28/2017 SBA LOAN NUMBER SECONDARY PARTICIPATION GUARANTY AGREEMENT IMPORTANT INFORMATION THIS FORM IS TO BE USED FOR THE INITIAL TRANSFER ONLY. ALL SUBSEQUENT TRANSFERS

OMB NO.: 3245-0185 EXPIRATION DATE: 2/28/2017 SBA LOAN NUMBER SECONDARY PARTICIPATION GUARANTY AGREEMENT IMPORTANT INFORMATION THIS FORM IS TO BE USED FOR THE INITIAL TRANSFER ONLY. ALL SUBSEQUENT TRANSFERS

Underwriting Procedures

Underwriting Section 4 Underwriting Procedures ----------------------------------------------------------------- 4.2 Underwriting Turn-Around --------------------------------------------------------------

Underwriting Section 4 Underwriting Procedures ----------------------------------------------------------------- 4.2 Underwriting Turn-Around --------------------------------------------------------------

Presenting a 90-minute encore presentation featuring live Q&A. Today s faculty features:

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Deductions, Limitations, Complexities and Opportunities for Pass-Through Entities Determining Qualified Business Income,

Presenting a 90-minute encore presentation featuring live Q&A New Section 199A: Deductions, Limitations, Complexities and Opportunities for Pass-Through Entities Determining Qualified Business Income,

Company Name Secondary Marketing Policies and Originator Compensation. Table of Contents

Table of Contents Table of Contents...1 Employee Policy Acknowledgement...1 Loan Originator Duties...2 Licensing and Professional Education Requirements (SAFE Act)... 3 Compensation... 5 Creditor vs. Originator...

Table of Contents Table of Contents...1 Employee Policy Acknowledgement...1 Loan Originator Duties...2 Licensing and Professional Education Requirements (SAFE Act)... 3 Compensation... 5 Creditor vs. Originator...

Small Business Loan Guaranty Program

Revised April 2013 Small Business Loan Guaranty Program Overview Created as part of the Small Business Jobs Act of 2010, the State Small Business Credit Initiative (SSBCI) was designed to help increase

Revised April 2013 Small Business Loan Guaranty Program Overview Created as part of the Small Business Jobs Act of 2010, the State Small Business Credit Initiative (SSBCI) was designed to help increase

DIMENSIONS Spring 2012

DIMENSIONS Spring 2012 Understand Your Contracts: Right Cost Language Can Mean More Profitable Jobs Project owners today are more concerned about reducing construction costs than at any time in the recent

DIMENSIONS Spring 2012 Understand Your Contracts: Right Cost Language Can Mean More Profitable Jobs Project owners today are more concerned about reducing construction costs than at any time in the recent

FINANCING YOUR BUSINESS

FINANCING YOUR BUSINESS Financing is one of the most important aspects of starting a new business. Your ability to provide and raise adequate capital will determine the fate of the business venture. Insufficient

FINANCING YOUR BUSINESS Financing is one of the most important aspects of starting a new business. Your ability to provide and raise adequate capital will determine the fate of the business venture. Insufficient

program compliance loan operations training chfa conventional loan programs for processors and underwriters

program compliance loan operations training chfa conventional loan programs for processors and underwriters Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training

program compliance loan operations training chfa conventional loan programs for processors and underwriters Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training

Table of Contents. Book 1. Book 4. Book 2. Book 5. Book 3. The Mortgage Cycle & Its Key Players Regulatory Compliance Loan Types & Programs

1 Table of Contents Book 1 The Mortgage Cycle & Its Key Players Regulatory Compliance Loan Types & Programs Book 2 Taking the Loan Application Book 3 Processing the Loan Automated Underwriting Uniform

1 Table of Contents Book 1 The Mortgage Cycle & Its Key Players Regulatory Compliance Loan Types & Programs Book 2 Taking the Loan Application Book 3 Processing the Loan Automated Underwriting Uniform

RE CAPITAL GROUP PRIVATE LENDER PRESENTATION

RE CAPITAL GROUP www.recapitalgroup.net PRIVATE LENDER PRESENTATION Be The Bank! Become A Private Money Lender Invest In Real Estate For Guaranteed Returns of up to 12% Annually What Is Private Money Lending?

RE CAPITAL GROUP www.recapitalgroup.net PRIVATE LENDER PRESENTATION Be The Bank! Become A Private Money Lender Invest In Real Estate For Guaranteed Returns of up to 12% Annually What Is Private Money Lending?