SBA will officially launch the 504 Debt Refinancing program on June 24, 2016

|

|

|

- Gary Jefferson

- 5 years ago

- Views:

Transcription

1

2 SBA has received statutory authority to reauthorize the 504 Debt Refinance Program for up to $7.5 billion. This is in addition to the $7.5 billion authorization for the 504 program. With this change, total 504 lending has a $15 billion authorization. SBA published the Interim Final Rule on May 25, 2016 and the Policy Notice on May 26, The Interim Final Rule has a 30-day effective date after publication. SBA will officially launch the 504 Debt Refinancing program on June 24,

3 On December 18, 2015, Section 521 of Division E of the Consolidated Appropriations Act, 2016 (the Act) authorized the 504 Program to be used for debt refinance. This is a permanent change to the 504 program. The Sacramento Loan Processing Center will begin accepting applications June 24,

4 Notices Policy Notice All regulations and standard operating procedures of the 504 Program apply to refinancing under the Act, with some modifications, as identified in SBA Policy Notice Information Notice Forms changes are identified in SBA Information Notice

5 Fees For loans approved under the 504 Debt Refinancing Program during FY 2016, the total annual guarantee fee is 0.958% (95.8 basis points). SBA will review the fee annually and issue notices of any change. 5

6 - Statutory Changes Three statutory modifications include: 1.) 504 program must be at zero-subsidy 2.) 504 refinance loans are limited to 50% of the CDC s previous fiscal year financing 3.) 504 alternative job goal in Jobs Act eliminated. 6

Limitation of the Debt Refinancing Program to be in effect only in any fiscal year in which the subsidy costs to the Federal")

7 - Zero Subsidy Requirement 1.) Limitation of the Debt Refinancing Program to be in effect only in any fiscal year in which the subsidy costs to the Federal Government of making guarantees under the Debt Refinancing Program and under the 504 Loan Program is zero. 7

8 50% Limit of Prior FY CDC Dollars Loaned 2.) Limitation of a CDC s financings under the Debt Refinancing Program to 50% of the total dollars the CDC loaned under the 504 Loan Program (including the 504 Debt Refinancing Program) during the previous fiscal year. Congress has authorized for waivers to this limitation. SBA will consider waivers in FY 2017, given there is less than 6 months to implement the program this fiscal year. Additional guidance on waivers will be provided in SOP

9 Job Creation and Retention for both 504 Program and 504 Debt Refinance Program 3.) Elimination of the alternative job retention goals authorized previously by the Jobs Act, and requiring all projects to adhere to 504 Program job creation and retention requirements. 9

10 Eligible Business Expenses Eligible Business Expenses are limited to the following business expenses: Other Secured Debt means debt that has been secured for at least 2 years prior to the date of application by the same Eligible Fixed Asset(s) securing the Qualified Debt and for which the Borrower has been current on all payments due for not less than one year preceding the date of application. Current on all payments due means that no payment was more than 30 days past due from either the original payment terms or modified payment terms (including deferments) if such modification was agreed to in writing by the Borrower and the lender of the existing debt not less than one year prior to the date of application; and Business Operating Expenses means business expenses other than Qualified Debt or Other Secured Debt, including salaries, rent, utilities, inventory, or other obligations of the business that were incurred but not paid prior to the date of application or that will become due for payment within 18 months after the date of application. 10

11 - Loan to Value Limitations For projects that refinance only Qualified Debt and Other Secured Debt - the maximum loan to value of the Refinancing Project allowed is 90%. For projects when the amount of Qualified Debt and Other Secured Debt being refinanced is more than 90 percent of the value of the Eligible Fixed Asset securing the Qualified Debt - the Borrower must provide additional cash or other fixed asset collateral acceptable to SBA so as not to exceed a 90% loan to value of the Refinancing Project. For any projects that include the financing of Business Operating Expenses - a maximum 75% loan to value of the Refinancing Project will apply and the Business Operating Expenses portion of the project may not exceed 25% of the value of the Eligible Fixed Asset(s) securing the Qualified Debt. Any fixed assets needed to satisfy the 90% loan to value requirement set forth above will not serve to increase the amount of Business Operating Expenses that may be financed. 11

12 Streamlined 504 Debt Refinance Application and CDC Document Retention Requirements Eligible Business Expenses the application must include a specific description of the Eligible Business Expenses and an itemization of the amount of each expense, with the Form 1244 certification of the accuracy of this information. The borrower retains the Eligible Business Expenses documentation. It is not included in the application or retained by the CDC. 12

13 Transcripts Streamlined 504 Debt Refinancing Application and CDC Documentation Requirements (cont.) The CDC must submit a transcript of the previous 12-month payment history on the Qualified Debt and Other Secured Debt being refinanced which confirms that the Borrower is current on all payments due, as defined in Policy Notice for not less than one year preceding the date of application. (Exhibit 21 of SBA Form 1244). 13

14 Streamlined 504 Debt Refinancing Application and CDC Documentation Requirements (cont.) Lien Verification Documentation on Debt Refinanced In considering the Borrower s application, the CDC must obtain evidence that lien(s) are securing the Qualified Debt and any Other Secured Debt with Eligible Fixed Asset(s), and state in its credit memorandum that it has verified that the lien(s) has been in place for at least 2 years prior to the date of application. The CDC must retain the evidence of the liens in its records (e.g., Preliminary Title Report, Mortgage Deed of Trust, or UCC-1 filing). 14

15 15

16 Refinancing Project The Fair market value of the Eligible Fixed Asset(s) securing the Qualified Debt and any other fixed assets acceptable to SBA (Additional fixed assets may be added only when needed to comply with 90% loan-tovalue limitation). 16

17 Qualified Debt Is a commercial loan: That was incurred not less than 2 years before the date of the application for assistance That is not subject to a guarantee by a Federal Agency The proceeds of which were used to acquire an eligible fixed asset 17

18 Qualified Debt (cont.) Is a commercial loan: Incurred for the benefit of the small business concern Secured by 504 eligible fixed assets For which the borrower has been current on all payments for not less than 1 year before the date of application. May consist of a combination of two or more loans, provided that each of the loans satisfies the Qualified Debt requirements. 18

19 Eligibility Requirements Project does not involve the expansion of a small business concern. The borrower has been in operation for all of the 2-year period ending on the date of the loan. 19

20 Eligibility Requirements The Borrower must have been in operation for all of the two year period ending on the date of application, as evidenced by the financial statements submitted at the time of application. If the ownership of the Borrower has changed, either partially or fully during the two year period, the Borrower is considered a new business and the Borrower s debt is not eligible for refinancing under the 504 Debt Refinancing Program. Any refinancing under the 504 Debt Refinancing Program must include Qualified Debt, as defined in Policy Notice The refinancing may also include Eligible Business Expenses. The amount of any refinancing under the 504 Debt Refinancing Program is subject to the Loan-to-Value Limitations in this Notice. 20

21 Other Application Documentation Requirements Credit memorandum The CDC must provide an analysis in its credit memorandum that the proposed debt refinancing satisfies each of the requirements of the 504 Debt Refinancing Program. Appraisals Appraisals are not required at time of application. Appraisals dated within 6 months of the date the application was approved are required prior to closing, and appraisals must otherwise comply with the requirements for appraisals set forth in SOP (H). Transcripts See updated Streamlined Documentation Process in Policy Notice Lien Verification See updated Streamlined Documentation Process in Policy Notice

22 Financing for Business Expenses - See also Clarification of Definition of Eligible Business Expenses and Loan-to-Value Limitations clarifications in Policy Notice The 504 Debt Refinance Program may provide refinancing of qualified debt and other secured debt in addition to the refinancing of business expenses. SBA has updated its procedural guidance on eligible business expenses and loan to value limitations. 22

23 Application Documentation - See also revised documentation guidance in Policy Notice An application for financing shall include a specific description of the expenses for which the additional financing is requested and an itemization of the amount of each expense. 23

24 PCLP Restriction Loan applications for assistance under the 504 Debt Refinancing Program must be processed by SBA and may not be approved by CDCs under PCLP authority. 24

25 Occupancy Requirements Borrowers for the 504 Debt Refinance Program must meet all current 504 Loan Program occupancy requirements at the time of application. 25

26 Interim Lender Documentation The Interim Lender must execute SBA Form 2288R, Interim Lender Certification for Refinancing Program, similar to what is required in all 504 closings. 26

27 Same Institution Debt When the loan being refinanced is Same Institution Debt (as defined in 13 CFR (g)(15)), the Third Party Lender may modify its existing loan documents (Note, Deed of Trust/Mortgage, etc.) instead of requiring the Borrower to execute and record new loan documents for the Third Party Loan. All modified loan documents must meet SBA s regulatory requirements for a Third Party Loan (see 13 CFR and ). 27

28 Same Institution Debt (cont.) When the loan being refinanced is Same Institution Debt, no Interim Lender may be used; instead, an escrow account is required, and: The Third Party Lender (who, in this case, is also the Lender of the debt being refinanced) must execute SBA Form 2416, Lender Certification for Refinanced Loan. The CDC must create an escrow account at the time of closing of the 504 loan for the purpose of holding the Borrower s cash contribution, if any, and the net debenture proceeds. 28

29 Same Institution Debt (cont.) The following requirements apply to the escrow account ( the account ): The account will be established in accordance with an Escrow Agreement which must be executed by the Borrower, the Third Party Lender, the Escrow Agent and the CDC. The account may be held by the CDC attorney, Title Company or other party approved by SBA District Counsel. The Borrower s cash contribution, if any, must be deposited into the account at the time of closing of the 504 loan. A copy of the Escrow Agreement must be provided to the SBA s District Counsel with evidence of funding by Borrower s cash contribution, if any, at the time of closing of the 504 loan. The net debenture proceeds must be wired to the account, and all funds may be released only upon written approval by the CDC and SBA, provided that CDC/SBA have the required lien positions on the collateral as set forth in the Authorization and Debenture Guaranty. The debt to be refinanced will be satisfied by payment of the escrowed funds to the Third Party Lender. 29

30 Other Than Same Institution Debt When the loan being refinanced is not Same Institution Debt, SBA may permit the lender of the debt to be refinanced to assign its existing loan documents to the Interim Lender if an Interim Lender is used, or to the Third Party Lender if no Interim Lender is used. The existing loan documents may be modified, as appropriate, rather than requiring that new documents be executed for the Refinancing Project. The Interim Lender, if any, may then assign the documents to the Third Party Lender. 30

31 31

32 Forms Changes Revisions have been made to SBA Forms 1244, 2450, 2234 Parts B and C, 2288R, and 1506 to implement the debt refinancing provisions of the Act. Additional 504 Forms were re-issued without changes to complete the forms series, including: SBA Forms 2233, 2234 Part A, 2416, and Information Notice outlines the changes, which are effective as of June 6, All applications for 504 Debt Refinancing loans must utilize the revised forms. 32

33 Form 1244 Application for Section 504 Loan (Expiration ) Page 1, Part A: Added options to Check if Debt Refinancing Loan Application With Expansion or Without Expansion for statistical data tracking purposes New 33

34 Form 1244 (cont.) Page 12, Part D: Under Item 3, added Option B, for information regarding Debt Refinancing Without Expansion New 34

35 Form 2450 Eligibility Information Required for 504 Submission (Non-PCLP) (Expiration ) Pages 3-4, Section V: Added language related to loan eligibility in the case that debt refinance is included in project costs without expansion Revised (d) to Is secured by 504 Eligible Fixed Assets. Revised (f) to the applicant has been current on all payments due for not less than one year prior to the date of application, (which means that no payment was more than 30 days past due from either the original payment terms or modified payment terms if such modification (including deferments) was agreed to in writing no less than one year prior to the date of application). 35

36 Form 2450 (cont.) New 36

37 Form 2234, Part B Supplemental Information for PCLP Processing (Expiration ) Page 2: Revised language in Use of Loan Proceeds related to Other Expenses for consistency with Form 1244 Revised 37

38 Form 2234, Part C Eligibility Information Required for 504 Submission (PCLP) (Expiration ) Page 7-10, Section VII: Added language related to loan eligibility in those cases when debt refinance is included in project costs without expansion Revised (d) to Is secured by 504 Eligible Fixed Asset Revised (f) to the applicant has been current on all payments due for not less than one year prior to the date of application, (which means that no payment was more than 30 days past due from either the original payment terms or modified payment terms if such modification (including deferments) was agreed to in writing no less than one year prior to the date of application). 38

39 Form 2234, Part C (cont.) New 39

40 Form 2288R Interim Lender Certification for Refinanced Loan (Version 02-16) (Formerly known as Form 2288TR Interim Lender Certification for Temporary Refinancing Program) Updated title of form to reflect permanent debt refinancing program Changed form number from 2288TR to 2288R Page 1: Added language regarding timing of the Interim Lender Certification (i.e. not more than 60 days prior to debenture funding ) Page 3: Revised the text of the Interim Lender Certification 40

41 Form 2288R (cont.) Revised Revised 41

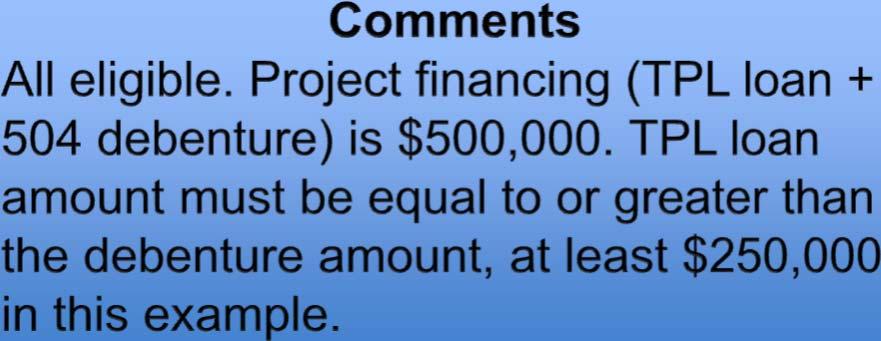

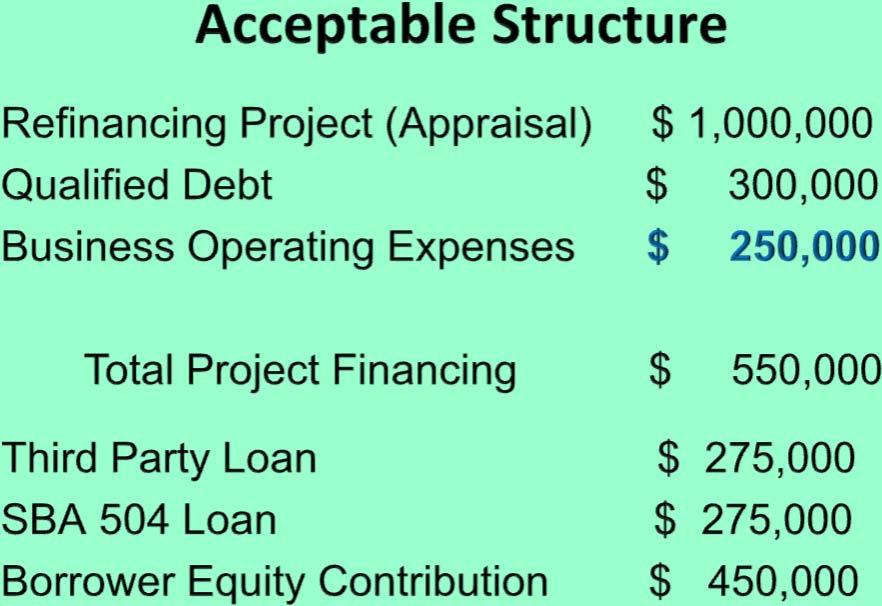

42 Form 2288R (cont.) Revised 42

43 Form 1506 Servicing Agent Agreement (Expiration ) Page 1: Added options to Check if Debt Refinancing Loan Application With Expansion or Without Expansion for statistical data tracking purposes. Page 2: Removed references to Recovery Act and Small Business Jobs Act. New New 43

44 44

45 Comments There is no Qualified Debt to refinance so the project would not be eligible under this program. Each project must have a Qualified Debt to be eligible. 45

46

47

48

49

50 Comments The Qualified Debt is eligible however only $250,000 of the request for Business Operating Expenses is eligible. These expenses are limited to 25% of the Refinance Project amount.

51 For more information about the 504 Debt Refinance Program contact: John M. Wade, Acting Director Office of Financial Assistance Linda Reilly, Chief of 504 Program Branch Babak Hosseini, Financial and Loan Specialist, 504 Program Branch

U.S. SMALL BUSINESS ADMINISTRATION. Reauthorization of the 504 Debt Refinancing Program

U.S. SMALL BUSINESS ADMINISTRATION Reauthorization of the 504 Debt Refinancing Program Refinance Program Timeline In December 2015, received statutory authority to reauthorize the 504 Debt Refinance Program

U.S. SMALL BUSINESS ADMINISTRATION Reauthorization of the 504 Debt Refinancing Program Refinance Program Timeline In December 2015, received statutory authority to reauthorize the 504 Debt Refinance Program

Statutory Requirements

In December 2015, SBA received statutory authority to reauthorize the 504 Debt Refinance Program for up to $7.5 billion. This is in addition to the $7.5 billion authorization for the 504 program. With

In December 2015, SBA received statutory authority to reauthorize the 504 Debt Refinance Program for up to $7.5 billion. This is in addition to the $7.5 billion authorization for the 504 program. With

YTD Activity Total 7(a) and 504

and 504") SBA Updates Bill Manger, Associate Administrator Office of Capital Access Steve Kucharski, Director, OPSM Susan Streich, Director, OCRM Jihoon Kim, Director, OFPO Dianna Seaborn, Director, OFA 2 7(a) Lending

SBA Updates Bill Manger, Associate Administrator Office of Capital Access Steve Kucharski, Director, OPSM Susan Streich, Director, OCRM Jihoon Kim, Director, OFPO Dianna Seaborn, Director, OFA 2 7(a) Lending

SUMMARY: This rule finalizes the interim final rule (IFR) that was published on May

that was published on May") This document is scheduled to be published in the Federal Register on 05/07/2018 and available online at https://federalregister.gov/d/2018-09638, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS

This document is scheduled to be published in the Federal Register on 05/07/2018 and available online at https://federalregister.gov/d/2018-09638, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS

ELIGIBILITY INFORMATION REQUIRED FOR 504 SUBMISSION (NON PCLP)

") ELIGIBILITY INFORMATION REQUIRED FOR 504 SUBMISSION (NON PCLP) OMB APPROVAL NO.: 3245-0071 EXPIRATION DATE: 09/30/2016 [The CDC completes this form to help SBA carryout its lender, portfolio and program

ELIGIBILITY INFORMATION REQUIRED FOR 504 SUBMISSION (NON PCLP) OMB APPROVAL NO.: 3245-0071 EXPIRATION DATE: 09/30/2016 [The CDC completes this form to help SBA carryout its lender, portfolio and program

SBA Lending: Documenting, Closing and Servicing 7(a) and CDC/504 Loans

and CDC/504 Loans") Presenting a live 90-minute webinar with interactive Q&A SBA Lending: Documenting, Closing and Servicing 7(a) and CDC/504 Loans Navigating SBA Approval and Authorization Process, Preserving the Loan Guaranty

Presenting a live 90-minute webinar with interactive Q&A SBA Lending: Documenting, Closing and Servicing 7(a) and CDC/504 Loans Navigating SBA Approval and Authorization Process, Preserving the Loan Guaranty

SUMMARY: This rule finalizes the proposed rule that the U.S. Small Business

This document is scheduled to be published in the Federal Register on 03/21/2014 and available online at http://federalregister.gov/a/2014-06237, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS ADMINISTRATION

This document is scheduled to be published in the Federal Register on 03/21/2014 and available online at http://federalregister.gov/a/2014-06237, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS ADMINISTRATION

Appendix D Opinion of CDC Counsel

Appendix D Opinion of CDC Counsel Read this first! This appendix contains the standardized text for the Opinion of CDC Counsel required by the Authorization. All paragraphs are mandatory except when noted

Appendix D Opinion of CDC Counsel Read this first! This appendix contains the standardized text for the Opinion of CDC Counsel required by the Authorization. All paragraphs are mandatory except when noted

First Lien Position 504 Loan Pooling Program PROGRAM GUIDE

First Lien Position 504 Loan Pooling Program PROGRAM GUIDE November 5, 2009 First Lien Position 504 Loan Pooling Program Guide INTRODUCTION SBA s secondary market program for First Lien Position 504 Loans

First Lien Position 504 Loan Pooling Program PROGRAM GUIDE November 5, 2009 First Lien Position 504 Loan Pooling Program Guide INTRODUCTION SBA s secondary market program for First Lien Position 504 Loans

SBA Information Notice

SBA Information Notice TO: All SBA Employees, 7(a) Lenders and Certified Development Companies CONTROL NO.: 5000-17008 SUBJECT: Issuance of SOP 50 10 5(J) EFFECTIVE: October 13, 2017 The purpose of this

SBA Information Notice TO: All SBA Employees, 7(a) Lenders and Certified Development Companies CONTROL NO.: 5000-17008 SUBJECT: Issuance of SOP 50 10 5(J) EFFECTIVE: October 13, 2017 The purpose of this

General Session V Affiliation and Franchise: A Roadmap to the Rule Wednesday, November 9 3:15 pm 4:30 pm Continental Ballroom 4-5

General Session V Affiliation and Franchise: A Roadmap to the Rule Wednesday, November 9 3:15 pm 4:30 pm Continental Ballroom 4-5 Thank you to our Alliance Partners 2 Speakers Linda Reilly, Acting Director,

General Session V Affiliation and Franchise: A Roadmap to the Rule Wednesday, November 9 3:15 pm 4:30 pm Continental Ballroom 4-5 Thank you to our Alliance Partners 2 Speakers Linda Reilly, Acting Director,

Chapter 41 Transfers of Ownership

Chapter 41 Transfers of Ownership 41.1 Transfers of Ownership in the Property or in the Borrower (04/29/16) As used in this Chapter 41, the term transferee refers to The new Borrower if the proposed transaction

Chapter 41 Transfers of Ownership 41.1 Transfers of Ownership in the Property or in the Borrower (04/29/16) As used in this Chapter 41, the term transferee refers to The new Borrower if the proposed transaction

504 Loan Program Rural Initiative - Waiver of Limitation on Lending Authority

This document is scheduled to be published in the Federal Register on 07/19/2018 and available online at https://federalregister.gov/d/2018-15312, and on govinfo.gov Billing Code: 8025-01 SMALL BUSINESS

This document is scheduled to be published in the Federal Register on 07/19/2018 and available online at https://federalregister.gov/d/2018-15312, and on govinfo.gov Billing Code: 8025-01 SMALL BUSINESS

Small Business Administration 504/CDC Loan Guaranty Program

Small Business Administration 504/CDC Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government December 5, 2017 Congressional Research Service 7-5700 www.crs.gov R41184

Small Business Administration 504/CDC Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government December 5, 2017 Congressional Research Service 7-5700 www.crs.gov R41184

CHAPTER 2 - LOAN CLOSING

CHAPTER 2 - LOAN CLOSING This chapter provides the Lender with guidance on closing and disbursing 7(a) loans in compliance with SBA requirements. It explains SBA s requirements by reviewing the 7(a) Loan

CHAPTER 2 - LOAN CLOSING This chapter provides the Lender with guidance on closing and disbursing 7(a) loans in compliance with SBA requirements. It explains SBA s requirements by reviewing the 7(a) Loan

Small Business Administration 504/CDC Loan Guaranty Program

Small Business Administration 504/CDC Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government January 7, 2016 Congressional Research Service 7-5700 www.crs.gov R41184

Small Business Administration 504/CDC Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government January 7, 2016 Congressional Research Service 7-5700 www.crs.gov R41184

Servicing Update: SOP 50 55, Chapter 6 & Chapter 8 Overview. Salon B Monday, October 20, :30 pm 3:30 pm

Servicing Update: SOP 50 55, Chapter 6 & Chapter 8 Overview Salon B Monday, October 20, 2014 2:30 pm 3:30 pm Thank you to our Alliance Partners TRAI N I N G & E D U C AT I O N Speakers Shirley Walls, Supervisory

Servicing Update: SOP 50 55, Chapter 6 & Chapter 8 Overview Salon B Monday, October 20, 2014 2:30 pm 3:30 pm Thank you to our Alliance Partners TRAI N I N G & E D U C AT I O N Speakers Shirley Walls, Supervisory

Today s Presenter. The SBA Authorization Wisconsin SBA Lenders Conference May 19, SBA Loan Closing: Proper Documentation & Pitfalls

2016 Wisconsin SBA Lenders Conference May 19, 2016 SBA Loan Closing: Proper Documentation & Pitfalls Today s Presenter Nick Jellum, Anastasi Jellum P.A. 14985 60 th Street North, Stillwater, MN 55082 Phone:

2016 Wisconsin SBA Lenders Conference May 19, 2016 SBA Loan Closing: Proper Documentation & Pitfalls Today s Presenter Nick Jellum, Anastasi Jellum P.A. 14985 60 th Street North, Stillwater, MN 55082 Phone:

SBA Procedural Notice

SBA Procedural Notice TO: All Employees CONTROL NO.: 5000-722 SUBJECT: PCLP Loan Loss Reserve Requirements EFFECTIVE: 04/05/01 Introduction The Premier Certified Lenders program (PCLP) transfers considerable

SBA Procedural Notice TO: All Employees CONTROL NO.: 5000-722 SUBJECT: PCLP Loan Loss Reserve Requirements EFFECTIVE: 04/05/01 Introduction The Premier Certified Lenders program (PCLP) transfers considerable

Commercial Real Estate Comparison Pricing Summary

Wells Fargo Bank, N.A. Small Business Administration Lending Commercial Real Estate Comparison Pricing Summary Prepared For: Darrin Boyd - David Moore Property Address: 9755 Westoint Drive Indianapolis,

Wells Fargo Bank, N.A. Small Business Administration Lending Commercial Real Estate Comparison Pricing Summary Prepared For: Darrin Boyd - David Moore Property Address: 9755 Westoint Drive Indianapolis,

Refinance Matrix for Rural Development Mortgages. Refinance Type. Refinance Type. Eligibility Eligible Lenders. Lender. Refinancing.

Refinance Matrix for Rural Development Mortgages Lender Eligibility Eligible Lenders Any lender who has been approved by Rural Development and holds an active lender agreement (Form RD 1980-16). Approved

Refinance Matrix for Rural Development Mortgages Lender Eligibility Eligible Lenders Any lender who has been approved by Rural Development and holds an active lender agreement (Form RD 1980-16). Approved

ELIGIBILITY FRIDAY, MARCH 13 8:30 AM 9:30 AM

ELIGIBILITY FRIDAY, MARCH 13 8:30 AM 9:30 AM 504 Loan Program Eligibility Clarifications Preapplications Preapplications for eligibility will be accepted by SLPC for the following: Franchises Heavy duty

ELIGIBILITY FRIDAY, MARCH 13 8:30 AM 9:30 AM 504 Loan Program Eligibility Clarifications Preapplications Preapplications for eligibility will be accepted by SLPC for the following: Franchises Heavy duty

7(a) LOAN APPLICATION PROCESS AT THE LGPC

LOAN APPLICATION PROCESS AT THE LGPC") 7(a) LOAN APPLICATION PROCESS AT THE LGPC 7(a) LOAN GUARANTY PROGRAM Flexible financing for your small business customers Igniting the Flames of Success OFO/OCA LENDER RELATIONS SPECIALISTS TRAINING September

7(a) LOAN APPLICATION PROCESS AT THE LGPC 7(a) LOAN GUARANTY PROGRAM Flexible financing for your small business customers Igniting the Flames of Success OFO/OCA LENDER RELATIONS SPECIALISTS TRAINING September

Effective Date: May 1,

divestiture of all ownership interest and severance of any relationship with the Small Business Applicant (and any associated Eligible Passive Concern) in any capacity, including being an employee (paid

divestiture of all ownership interest and severance of any relationship with the Small Business Applicant (and any associated Eligible Passive Concern) in any capacity, including being an employee (paid

RULES AND AMENDMENTS TO REGULATION Z

Attorneys at Law Arlington Office 2310 W. Interstate 20, Suite 100 Telephone: 918-461-5500 Arlington, Texas 76017-1868 Fax: 817-856-6060 RULES AND AMENDMENTS TO REGULATION Z OCTOBER 1, 2009 In an effort

Attorneys at Law Arlington Office 2310 W. Interstate 20, Suite 100 Telephone: 918-461-5500 Arlington, Texas 76017-1868 Fax: 817-856-6060 RULES AND AMENDMENTS TO REGULATION Z OCTOBER 1, 2009 In an effort

Welcome to the 7(a) Connect Call

Connect Call") Welcome to the 7(a) Connect Call During this call we will provide updates, training tips and hot topics on the Office of Capital Access There will be time allotted for questions and answers. Office of

Welcome to the 7(a) Connect Call During this call we will provide updates, training tips and hot topics on the Office of Capital Access There will be time allotted for questions and answers. Office of

SONYMA FHA Plus Correspondent Term Sheet

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

Primary purpose of Franchise revisions is to streamline procedures for determining size eligibility based on affiliation between Franchisee &

Primary purpose of Franchise revisions is to streamline procedures for determining size eligibility based on affiliation between Franchisee & Franchisor Regulatory Changes 13 CFR 121.301(f)(5) (effective

Primary purpose of Franchise revisions is to streamline procedures for determining size eligibility based on affiliation between Franchisee & Franchisor Regulatory Changes 13 CFR 121.301(f)(5) (effective

Intro to 7(a) Lending

Lending") Intro to 7(a) Lending Presented by Dianna Seaborn Acting Director, Office of Financial Assistance US Small Business Administration 1 Becoming an SBA Lender Credit Unions with share insurance must send

Intro to 7(a) Lending Presented by Dianna Seaborn Acting Director, Office of Financial Assistance US Small Business Administration 1 Becoming an SBA Lender Credit Unions with share insurance must send

USDA HB REVISIONS Effective March 9, 2016 Chapter 5: Origination and Underwriting Review

Chapter 5: Origination and Underwriting Review 5.2 Requesting a Guarantee A. Preliminary Determination of Applicant Eligibility 2. Credit 5.3 Utilizing the Guaranteed Underwriting System (GUS) E. Reserves

Chapter 5: Origination and Underwriting Review 5.2 Requesting a Guarantee A. Preliminary Determination of Applicant Eligibility 2. Credit 5.3 Utilizing the Guaranteed Underwriting System (GUS) E. Reserves

Coleman Certified SBA 7(a) Loan Closer Lance A. Sexton, Coleman Faculty Instructor

Loan Closer Lance A. Sexton, Coleman Faculty Instructor") Coleman Certified SBA 7(a) Loan Closer Lance A. Sexton, Coleman Faculty Instructor Setting Up the SBA Loan File There are a number of ways to set up a loan file. My recommendation for the SBA Loan File

Coleman Certified SBA 7(a) Loan Closer Lance A. Sexton, Coleman Faculty Instructor Setting Up the SBA Loan File There are a number of ways to set up a loan file. My recommendation for the SBA Loan File

Exhibit B: Guide Chapter K33 Mortgages for Newly Constructed Homes

Exhibit B: Guide Chapter K33 for Newly Constructed Homes K33.1: Overview This chapter details the requirements for the three types of for Newly Constructed Homes: Newly Built Home Conversion Renovation

Exhibit B: Guide Chapter K33 for Newly Constructed Homes K33.1: Overview This chapter details the requirements for the three types of for Newly Constructed Homes: Newly Built Home Conversion Renovation

LiftFund (CDC) 504 Checklist and Loan Application

504 Checklist and Loan Application") 1. 2. LiftFund (CDC) 504 Checklist and Loan Application Copy of photo ID (Driver license) History of the Business. (Business Plan for start-ups.) Equal Opportunity Lender 3. Current personal financial

1. 2. LiftFund (CDC) 504 Checklist and Loan Application Copy of photo ID (Driver license) History of the Business. (Business Plan for start-ups.) Equal Opportunity Lender 3. Current personal financial

CHICAGO TITLE INSURANCE COMPANY

CHICAGO TITLE INSURANCE COMPANY SCHEDULE OF TITLE INSURANCE PREMIUMS AND CHARGES FOR USE IN THE STATE OF INDIANA EFFECTIVE: February 8, 2017 (Unless Otherwise Specified Herein) Table of Contents I. BASIC

CHICAGO TITLE INSURANCE COMPANY SCHEDULE OF TITLE INSURANCE PREMIUMS AND CHARGES FOR USE IN THE STATE OF INDIANA EFFECTIVE: February 8, 2017 (Unless Otherwise Specified Herein) Table of Contents I. BASIC

Guidance on Refinancing Existing Loans in the Section 538 Guaranteed Rural Rental Housing Program (GRRHP)

") May 3, 2017 TO: State Directors Rural Development ATTN: Program Directors Multi-Family Housing FROM: Richard A. Davis /s/ Richard A. Davis Acting Administrator Rural Housing Service SUBJECT: Guidance on

May 3, 2017 TO: State Directors Rural Development ATTN: Program Directors Multi-Family Housing FROM: Richard A. Davis /s/ Richard A. Davis Acting Administrator Rural Housing Service SUBJECT: Guidance on

FINAL CAPLINES CHANGES TO SOP (D)

") FINAL CAPLINES CHANGES TO SOP 50 10 5(D) 9-15-2011 Subpart A: Chapter 1 Pg. 9 Deleted additional qualifications for lenders to participate in CAPLines, including removing the Lenders Qualification Survey

FINAL CAPLINES CHANGES TO SOP 50 10 5(D) 9-15-2011 Subpart A: Chapter 1 Pg. 9 Deleted additional qualifications for lenders to participate in CAPLines, including removing the Lenders Qualification Survey

Selling Guide Announcement SEL

Selling Guide Announcement SEL-2012-09 Updates to Refi Plus and DU Refi Plus September 14, 2012 The positive impact of Refi Plus and DU Refi Plus continues, enabling borrowers who have demonstrated an

Selling Guide Announcement SEL-2012-09 Updates to Refi Plus and DU Refi Plus September 14, 2012 The positive impact of Refi Plus and DU Refi Plus continues, enabling borrowers who have demonstrated an

DISCLOSURE STATEMENT REGARDING THE CITY OF CONCORD FIRST TIME HOMEBUYER PROGRAM AND SHARED APPRECIATION LOAN

DISCLOSURE STATEMENT REGARDING THE CITY OF CONCORD FIRST TIME HOMEBUYER PROGRAM AND SHARED APPRECIATION LOAN THIS IS AN IMPORTANT DOCUMENT. EVERY BORROWER THAT RECEIVES A LOAN FROM THE CITY OF CONCORD

DISCLOSURE STATEMENT REGARDING THE CITY OF CONCORD FIRST TIME HOMEBUYER PROGRAM AND SHARED APPRECIATION LOAN THIS IS AN IMPORTANT DOCUMENT. EVERY BORROWER THAT RECEIVES A LOAN FROM THE CITY OF CONCORD

Deep Dive into Portfolio Management and the National Guaranty Purchase Center. Presented by: Susan Suckfiel and Vanessa Piccioni

Deep Dive into Portfolio Management and the National Guaranty Purchase Center Presented by: Susan Suckfiel and Vanessa Piccioni Overview 10-Tab Packages & the Purchase Review Common Reasons for Repairs

Deep Dive into Portfolio Management and the National Guaranty Purchase Center Presented by: Susan Suckfiel and Vanessa Piccioni Overview 10-Tab Packages & the Purchase Review Common Reasons for Repairs

$278,440,000 U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES

OFFERING CIRCULAR $278,440,000 (Approximate) U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES Guaranteed by the U.S. SMALL BUSINESS ADMINISTRATION (an independent agency of the

OFFERING CIRCULAR $278,440,000 (Approximate) U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES Guaranteed by the U.S. SMALL BUSINESS ADMINISTRATION (an independent agency of the

U.S. Small Business Administration Programs & Services. New Hampshire

U.S. Small Business Administration Programs & Services New Hampshire 1 Advantage of SBA s Guaranty Most Viable Business Profile Experienced management High Debt Service Cash flow Sterling credit Generous

U.S. Small Business Administration Programs & Services New Hampshire 1 Advantage of SBA s Guaranty Most Viable Business Profile Experienced management High Debt Service Cash flow Sterling credit Generous

AHP 2018 Implementation Plan Native American Homeownership Initiative (NAHI) Program Guidelines

Program Guidelines") I. (NAHI) Program Guidelines 1. Program Summary In 2018 the Bank will make $1,000,000 available on a first-come first-served basis to eligible members that have executed a Down Payment Subsidy Agreement.

I. (NAHI) Program Guidelines 1. Program Summary In 2018 the Bank will make $1,000,000 available on a first-come first-served basis to eligible members that have executed a Down Payment Subsidy Agreement.

SBA 504 Loan Application EQUAL OPPORTUNITY LENDER

SBA 504 Loan Application EQUAL OPPORTUNITY LENDER Business Profile Is the following business the: Borrower, Operating Company Legal Business Name: Address/City/State/Zip Code: Nature of Business Taxpayer

SBA 504 Loan Application EQUAL OPPORTUNITY LENDER Business Profile Is the following business the: Borrower, Operating Company Legal Business Name: Address/City/State/Zip Code: Nature of Business Taxpayer

Complimentary Coleman Report Live!

Complimentary Coleman Report Live! Featuring Bob Coleman & Charles Green 1:50-2:00 PM E.T. Log on 10 minutes early before every Coleman webinar for a briefing on issues vital to the small business lending

Complimentary Coleman Report Live! Featuring Bob Coleman & Charles Green 1:50-2:00 PM E.T. Log on 10 minutes early before every Coleman webinar for a briefing on issues vital to the small business lending

$279,425,000 (Approximate) U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES

U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES") OFFERING CIRCULAR $279,425,000 (Approximate) U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES Guaranteed by the U.S. SMALL BUSINESS ADMINISTRATION (an independent agency of the

OFFERING CIRCULAR $279,425,000 (Approximate) U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES Guaranteed by the U.S. SMALL BUSINESS ADMINISTRATION (an independent agency of the

$262,864,000 (Approximate) U.S. GOVERNMENT GUARANTEED 2.85% DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES SERIES J Due October 1, 2037

U.S. GOVERNMENT GUARANTEED 2.85% DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES SERIES J Due October 1, 2037") OFFERING CIRCULAR $262,864,000 (Approximate) U.S. GOVERNMENT GUARANTEED 2.85% DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES SERIES 2017-20 J Due October 1, 2037 CUSIP: 83162C YX5 Guaranteed by the U.S.

OFFERING CIRCULAR $262,864,000 (Approximate) U.S. GOVERNMENT GUARANTEED 2.85% DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES SERIES 2017-20 J Due October 1, 2037 CUSIP: 83162C YX5 Guaranteed by the U.S.

AMENDED AND RESTATED GSE RESCISSION RELIEF PRINCIPLES FOR IMPLEMENTATION OF MASTER POLICY REQUIREMENT #28 (RESCISSION RELIEF/INCONTESTABILITY)

") AMENDED AND RESTATED GSE RESCISSION RELIEF PRINCIPLES FOR IMPLEMENTATION OF MASTER POLICY REQUIREMENT #28 (RESCISSION RELIEF/INCONTESTABILITY) Background December 21, 2017 These amended and restated GSE

AMENDED AND RESTATED GSE RESCISSION RELIEF PRINCIPLES FOR IMPLEMENTATION OF MASTER POLICY REQUIREMENT #28 (RESCISSION RELIEF/INCONTESTABILITY) Background December 21, 2017 These amended and restated GSE

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

CFPB Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Small Business Administration 7(a) Loan Guaranty Program

Loan Guaranty Program") Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government May 1, 2013 CRS Report for Congress Prepared for Members and Committees of Congress

Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government May 1, 2013 CRS Report for Congress Prepared for Members and Committees of Congress

10/15/2012. Banking 101. Current Banking Landscape. The New Banking World

The New Banking World Banking 101 Current Banking Landscape 1 Survival of the Fittest Economic Developments Role Investors Community Bank 860 North Rapids Rd. Manitowoc, WI 54220 920-686-5604 Tim Schneider,

The New Banking World Banking 101 Current Banking Landscape 1 Survival of the Fittest Economic Developments Role Investors Community Bank 860 North Rapids Rd. Manitowoc, WI 54220 920-686-5604 Tim Schneider,

Bulletin NUMBER: TO: Freddie Mac Sellers and Servicers August 16, 2011

Bulletin NUMBER: 2011-15 TO: Freddie Mac Sellers and Servicers August 16, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are: Quality control Revising Guide Chapter

Bulletin NUMBER: 2011-15 TO: Freddie Mac Sellers and Servicers August 16, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are: Quality control Revising Guide Chapter

National Correspondent Division Lender Guide

GLOSSARY As used in the Agreement and this Guide, the terms herein shall have the following meanings, unless the context requires otherwise: Accepted Servicing Practice(s): With respect to any Loan, as

GLOSSARY As used in the Agreement and this Guide, the terms herein shall have the following meanings, unless the context requires otherwise: Accepted Servicing Practice(s): With respect to any Loan, as

Understanding Modular Home Construction Financing. A Customer Guide

Understanding Modular Home Construction Financing. A Customer Guide Table of Contents 1 Welcome 2 Why Choose M&T? 4 The Seven Steps of Modular Home Construction Financing 4 Getting Pre-Approved 5 Applying

Understanding Modular Home Construction Financing. A Customer Guide Table of Contents 1 Welcome 2 Why Choose M&T? 4 The Seven Steps of Modular Home Construction Financing 4 Getting Pre-Approved 5 Applying

PERSONAL FINANCIAL STATEMENT

OMB Approval No. 3245-0188 PERSONAL FINANCIAL STATEMENT U.S. SMALL BUSINESS ADMINISTRATION As of, 20 Complete this form for: (1) each proprietor, or (2) each limited partner who owns 20% or more interest

OMB Approval No. 3245-0188 PERSONAL FINANCIAL STATEMENT U.S. SMALL BUSINESS ADMINISTRATION As of, 20 Complete this form for: (1) each proprietor, or (2) each limited partner who owns 20% or more interest

Section 1.02 Eligible Mortgage Loans

Section 1.02 Eligible Mortgage Loans In This Section This section contains the following topics: Related Bulletins... 2 Approved Products and Services... 3 SunTrust Employee Loans... 3 General... 3 Eligible

Section 1.02 Eligible Mortgage Loans In This Section This section contains the following topics: Related Bulletins... 2 Approved Products and Services... 3 SunTrust Employee Loans... 3 General... 3 Eligible

WASHINGTON STATE HOUSING FINANCE COMMISSION

WASHINGTON STATE HOUSING FINANCE COMMISSION BELLINGHAM DPA - HOMEBUYER RECAPTURE AGREEMENT This Agreement regarding homebuyer assistance, dated as of (the Agreement ), is made and entered into by and between

WASHINGTON STATE HOUSING FINANCE COMMISSION BELLINGHAM DPA - HOMEBUYER RECAPTURE AGREEMENT This Agreement regarding homebuyer assistance, dated as of (the Agreement ), is made and entered into by and between

MONTGOMERY DEVELOPMENT FUND LOW INTEREST LOAN PROGRAM GUIDELINES AND APPLICATION FORMS

LOW INTEREST LOAN PROGRAM GUIDELINES AND APPLICATION FORMS Program Description: The Village of Montgomery is introducing two new programs to further economic development in the Village. The purpose of

LOW INTEREST LOAN PROGRAM GUIDELINES AND APPLICATION FORMS Program Description: The Village of Montgomery is introducing two new programs to further economic development in the Village. The purpose of

1-12 STREAMLINE REFINANCES.

Cash-out refinances for debt consolidation represent considerable risk, especially if the borrowers have not had an attendant increase in income. Such transactions must be carefully evaluated. 1-12 STREAMLINE

Cash-out refinances for debt consolidation represent considerable risk, especially if the borrowers have not had an attendant increase in income. Such transactions must be carefully evaluated. 1-12 STREAMLINE

Junior Accessory Dwelling Unit Loan Program Guidelines

Junior Accessory Dwelling Unit Loan Program Guidelines I. PROGRAM PURPOSE AND INTRODUCTION Napa County s JADU Incentive Program seeks to encourage the production of affordable units in the unincorporated

Junior Accessory Dwelling Unit Loan Program Guidelines I. PROGRAM PURPOSE AND INTRODUCTION Napa County s JADU Incentive Program seeks to encourage the production of affordable units in the unincorporated

The Chase Guaranteed Rural Housing Purchase Program Features

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

MSF LENDING GUIDE GENERAL

Announcement 08-16C Guideline Updates and Changes Effective Immediately for all loans: The following areas of Mortgage Solutions guidelines have been updated. All changes and additions appear in red. MSF

Announcement 08-16C Guideline Updates and Changes Effective Immediately for all loans: The following areas of Mortgage Solutions guidelines have been updated. All changes and additions appear in red. MSF

Compliance Checklists

Compliance Checklists Lender Checklist... Ck-1 Broker Checklist... Ck-7 Servicer Checklist... Ck-13 Checklist for Other Service Providers... Ck-15 Ck-i Ck-ii THE RESPA MANUAL Ck-1 Compliance Checklists

Compliance Checklists Lender Checklist... Ck-1 Broker Checklist... Ck-7 Servicer Checklist... Ck-13 Checklist for Other Service Providers... Ck-15 Ck-i Ck-ii THE RESPA MANUAL Ck-1 Compliance Checklists

CITY OF TUSTIN TUSTIN HOUSING AUTHORITY AFFORDABLE HOUSING OWNERSHIP PROGRAMS FACT SHEET (BUYER)

") CITY OF TUSTIN TUSTIN HOUSING AUTHORITY AFFORDABLE HOUSING OWNERSHIP PROGRAMS FACT SHEET (BUYER) GENERAL PURPOSE The purpose of this document is to provide the prospective homeowner with a summary of the

CITY OF TUSTIN TUSTIN HOUSING AUTHORITY AFFORDABLE HOUSING OWNERSHIP PROGRAMS FACT SHEET (BUYER) GENERAL PURPOSE The purpose of this document is to provide the prospective homeowner with a summary of the

FAQ on ML Effective Date of the Mortgagee Letter (ML): When is the ML effective?

: When is the ML effective?") FAQ on ML 2011-11 1. Effective Date of the Mortgagee Letter (ML): When is the ML effective? The ML effective dates may vary depending on whether the policy section clarifies existing guidance; issues new

FAQ on ML 2011-11 1. Effective Date of the Mortgagee Letter (ML): When is the ML effective? The ML effective dates may vary depending on whether the policy section clarifies existing guidance; issues new

SELF-HELP ENTERPRISES CITY OF VISALIA Affordable Housing Program HOME funded 2 nd mortgage loan

SELF-HELP ENTERPRISES CITY OF VISALIA Affordable Housing Program HOME funded 2 nd mortgage loan (for families at or below 80% AMI) Program is administered by Self-Help Enterprises, and overseen by the

SELF-HELP ENTERPRISES CITY OF VISALIA Affordable Housing Program HOME funded 2 nd mortgage loan (for families at or below 80% AMI) Program is administered by Self-Help Enterprises, and overseen by the

Correspondent Lending FHA Fixed Rate

Agency Correspondent Lending FHA Fixed Rate Correspondent Lending FHA Fixed Rate Maximum Loan Amount County Minimum Loan Amount $50,000 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM DU Approve, LP Accept

Agency Correspondent Lending FHA Fixed Rate Correspondent Lending FHA Fixed Rate Maximum Loan Amount County Minimum Loan Amount $50,000 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM DU Approve, LP Accept

Small Business Loan Guaranty Program

Revised April 2013 Small Business Loan Guaranty Program Overview Created as part of the Small Business Jobs Act of 2010, the State Small Business Credit Initiative (SSBCI) was designed to help increase

Revised April 2013 Small Business Loan Guaranty Program Overview Created as part of the Small Business Jobs Act of 2010, the State Small Business Credit Initiative (SSBCI) was designed to help increase

Small Business Administration 7(a) Loan Guaranty Program

Loan Guaranty Program") Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government February 12, 2015 Congressional Research Service 7-5700 www.crs.gov R41146 Summary

Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government February 12, 2015 Congressional Research Service 7-5700 www.crs.gov R41146 Summary

AmeriSave Wholesale USDA Effective Date: February 2017 USDA 30 Rural Housing 30 Year Fixed Only

AmeriSave Wholesale USDA Effective Date: February 2017 Product Term: USDA 30 Rural Housing 30 Year Fixed Only Loan Purpose Loan Amount Eligible Borrowers Ineligible Borrowers Purchase Guaranteed: $424,100

AmeriSave Wholesale USDA Effective Date: February 2017 Product Term: USDA 30 Rural Housing 30 Year Fixed Only Loan Purpose Loan Amount Eligible Borrowers Ineligible Borrowers Purchase Guaranteed: $424,100

Office of the State Bank Commissioner

Agency 17 Office of the State Bank Commissioner Articles 17-11. DOCUMENTATION REQUIREMENTS. 17-24. MORTGAGE BUSINESS. 17-25. CREDIT SERVICES ORGANIZATIONS. Article 11. DOCUMENTATION REQUIREMENTS 17-11-18.

Agency 17 Office of the State Bank Commissioner Articles 17-11. DOCUMENTATION REQUIREMENTS. 17-24. MORTGAGE BUSINESS. 17-25. CREDIT SERVICES ORGANIZATIONS. Article 11. DOCUMENTATION REQUIREMENTS 17-11-18.

8:1 CONFORMING FIXED RATE

8:1 CONFORMING FIXED RATE LOAN PRODUCT CODES LOAN PRODUCT LOAN TERM/AMORTIZATION* 101 30 Year Fixed Rate 241-360 months 104 20 Year Fixed Rate 181-240 months 102 15 Year Fixed Rate 121-180 months 110 10

8:1 CONFORMING FIXED RATE LOAN PRODUCT CODES LOAN PRODUCT LOAN TERM/AMORTIZATION* 101 30 Year Fixed Rate 241-360 months 104 20 Year Fixed Rate 181-240 months 102 15 Year Fixed Rate 121-180 months 110 10

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION LOAN POLICIES Affordable Housing Development Affordable Housing Acquisition & Preservation Multi-family Housing Rehabilitation Community Facilities Table

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION LOAN POLICIES Affordable Housing Development Affordable Housing Acquisition & Preservation Multi-family Housing Rehabilitation Community Facilities Table

Supplemental Directive May 11, Home Affordable Unemployment Program. Help for Unemployed Borrowers. Background

Supplemental Directive 10-04 May 11, 2010 Home Affordable Unemployment Program Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility, underwriting and

Supplemental Directive 10-04 May 11, 2010 Home Affordable Unemployment Program Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility, underwriting and

SAFE Final Rules - Registration of Residential Mortgage Loan Originators (OCC) 9/3/2010 8:45:44 AM

9/3/2010 8:45:44 AM") CODE OF FEDERAL REGULATIONS TITLE 12. BANKS AND BANKING CHAPTER I. COMPTROLLER OF THE CURRENCY, DEPARTMENT OF THE TREASURY PART 34. REAL ESTATE LENDING AND APPRAISALS SUBPART F. REGISTRATION OF RESIDENTIAL

CODE OF FEDERAL REGULATIONS TITLE 12. BANKS AND BANKING CHAPTER I. COMPTROLLER OF THE CURRENCY, DEPARTMENT OF THE TREASURY PART 34. REAL ESTATE LENDING AND APPRAISALS SUBPART F. REGISTRATION OF RESIDENTIAL

Alger Insurance and Consulting LLC Commercial Lending Application

Alger Insurance and Consulting LLC Commercial Lending Application COMMERCIAL LOAN APPLICATION This checklist is provided to assist in gathering the necessary information needed for the initial evaluation

Alger Insurance and Consulting LLC Commercial Lending Application COMMERCIAL LOAN APPLICATION This checklist is provided to assist in gathering the necessary information needed for the initial evaluation

STG High Liability (Over $25 Million) Mechanic's Lien Coverage

Mechanic's Lien Coverage") Page 1 of 5 STG High Liability (Over $25 Million) Mechanic's Lien Coverage Approval Request Name of Issuing Office: File No. _ Contact Person: Phone Number for Contact Person: E-mail address for Contact

Page 1 of 5 STG High Liability (Over $25 Million) Mechanic's Lien Coverage Approval Request Name of Issuing Office: File No. _ Contact Person: Phone Number for Contact Person: E-mail address for Contact

MEGA ALT ARM (MA5/1)

") MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

Small Business Administration 7(a) Loan Guaranty Program

Loan Guaranty Program") Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government February 18, 2016 Congressional Research Service 7-5700 www.crs.gov R41146 Summary

Small Business Administration 7(a) Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government February 18, 2016 Congressional Research Service 7-5700 www.crs.gov R41146 Summary

Interagency Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Construction Conversion and Renovation Mortgages

Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation Mortgages, refer to Freddie Mac s

Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation Mortgages, refer to Freddie Mac s

Any person, who for direct or indirect compensation, assists a consumer in obtaining or applying to obtain a residential mortgage loan; or

Mortgage Reform and Anti-Predatory Lending Act Although it has received far less attention than other titles of the Dodd-Frank Act (the Act or Dodd-Frank ), such as those addressing derivatives, too big

Mortgage Reform and Anti-Predatory Lending Act Although it has received far less attention than other titles of the Dodd-Frank Act (the Act or Dodd-Frank ), such as those addressing derivatives, too big

Special Feature Codes

Special Feature Codes The following is a list of Fannie Mae s published special feature codes (SFC) applicable to delivery of single- family mortgage loans. Lenders should also review their Master Agreement

Special Feature Codes The following is a list of Fannie Mae s published special feature codes (SFC) applicable to delivery of single- family mortgage loans. Lenders should also review their Master Agreement

This regulation Part is promulgated pursuant to the authority granted in R.I. Gen. Laws and (b).

.") 230 RICR 40 10 3 TITLE 230 DEPARTMENT OF BUSINESS REGULATION CHAPTER 40 BANKING SUBCHAPTER 10 LENDING PART 3 Home Loan Protection Act 3.1 Authority This regulation Part is promulgated pursuant to the authority

230 RICR 40 10 3 TITLE 230 DEPARTMENT OF BUSINESS REGULATION CHAPTER 40 BANKING SUBCHAPTER 10 LENDING PART 3 Home Loan Protection Act 3.1 Authority This regulation Part is promulgated pursuant to the authority

TILA RESPA Integrated Disclosure

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

TABLE OF CONTENTS. Section 2 Terms and Conditions

TABLE OF CONTENTS Section 1 Introduction Washington State Housing Finance Commission...1.1 Benefits of the Home Advantage Program...1.1 Purpose and Scope...1.2 Process Overview...1.2 Manual Updates & Revisions...1.4

TABLE OF CONTENTS Section 1 Introduction Washington State Housing Finance Commission...1.1 Benefits of the Home Advantage Program...1.1 Purpose and Scope...1.2 Process Overview...1.2 Manual Updates & Revisions...1.4

Freddie Mac Revises Miscellaneous Eligibility and Property Requirements

Freddie Mac Revises Miscellaneous Eligibility and Property Requirements By Anna DeSimone, President October 15, 2014 On October 15, 2014, Freddie Mac issued Bulletin 2014-18: Selling Updates. This Single-Family

Freddie Mac Revises Miscellaneous Eligibility and Property Requirements By Anna DeSimone, President October 15, 2014 On October 15, 2014, Freddie Mac issued Bulletin 2014-18: Selling Updates. This Single-Family

Du Refi Plus Guidelines

Du Refi Plus Guidelines Units Contiguous States, DC Alaska, Hawaii Max Loan Amount Conforming 1 Unit 2 Unit 3 Unit 4 Unit $417,000 $533,850 $645,300 $801,950 $625,500 $800,775 $967,950 $1,202,925 Units

Du Refi Plus Guidelines Units Contiguous States, DC Alaska, Hawaii Max Loan Amount Conforming 1 Unit 2 Unit 3 Unit 4 Unit $417,000 $533,850 $645,300 $801,950 $625,500 $800,775 $967,950 $1,202,925 Units

Know Before You Owe Policy Manual Table of Contents [Sample Client] Table of Contents. Sample

![Know Before You Owe Policy Manual Table of Contents [Sample Client] Table of Contents. Sample](/thumbs/96/128500341.jpg "Know Before You Owe Policy Manual Table of Contents [Sample Client] Table of Contents. Sample") TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 4 1.1 GOALS AND OBJECTIVES... 4 1.2 REQUIRED REVIEW... 4 1.3 APPLICABILITY... 4 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 5 2.1 INTERNAL CONTROLS... 5

TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 4 1.1 GOALS AND OBJECTIVES... 4 1.2 REQUIRED REVIEW... 4 1.3 APPLICABILITY... 4 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 5 2.1 INTERNAL CONTROLS... 5

CITY OF DE PERE REVOLVING LOAN FUND MANUAL. Prepared by the: Planning and Economic Development Department

CITY OF DE PERE REVOLVING LOAN FUND MANUAL Prepared by the: Planning and Economic Development Department In conjunction with the Wisconsin Economic Development Corporation Adopted: January 15, 2013 TABLE

CITY OF DE PERE REVOLVING LOAN FUND MANUAL Prepared by the: Planning and Economic Development Department In conjunction with the Wisconsin Economic Development Corporation Adopted: January 15, 2013 TABLE

Winnebago County Industrial Development Board The Wave of the Future WINNEBAGO COUNTY CDBG-ED REVOLVING LOAN FUND MANUAL

Winnebago County Industrial Development Board The Wave of the Future WINNEBAGO COUNTY CDBG-ED REVOLVING LOAN FUND MANUAL Adopted by County Board -MARCH 2000 Updated May 2013 TABLE OF CONTENTS SECTION 1

Winnebago County Industrial Development Board The Wave of the Future WINNEBAGO COUNTY CDBG-ED REVOLVING LOAN FUND MANUAL Adopted by County Board -MARCH 2000 Updated May 2013 TABLE OF CONTENTS SECTION 1

Member Business Lending

MOTIVATE. BUILD. LEAD. Member Business Lending Foremost provider of Commerical lending services WHO WE ARE Member Business Lending (MBL) is a credit union service organization (CUSO) established in 2004

MOTIVATE. BUILD. LEAD. Member Business Lending Foremost provider of Commerical lending services WHO WE ARE Member Business Lending (MBL) is a credit union service organization (CUSO) established in 2004

Express Bridge Loan Pilot Program; Modification of Fee Policy. ACTION: Notification of change to Express Bridge Loan Pilot Program and impact on

This document is scheduled to be published in the Federal Register on 05/07/2018 and available online at https://federalregister.gov/d/2018-09627, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS

This document is scheduled to be published in the Federal Register on 05/07/2018 and available online at https://federalregister.gov/d/2018-09627, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS

Chesapeake Business Finance Corp.

Chesapeake Business Finance Corp. John Sower, President 1101 30 th St NW #500 Sower1@erols.com Washington, DC 20007 www.chesapeake504.com Tel: 202-625-4373 Cell: 202-257-5871 Fax: 202-342-0389 John Sower

Chesapeake Business Finance Corp. John Sower, President 1101 30 th St NW #500 Sower1@erols.com Washington, DC 20007 www.chesapeake504.com Tel: 202-625-4373 Cell: 202-257-5871 Fax: 202-342-0389 John Sower

FHA Section 542(c) Risk-Sharing Program for Multifamily Housing Program Rules

Risk-Sharing Program for Multifamily Housing Program Rules") FHA Section 542(c) Risk-Sharing Program for Multifamily Housing Program Rules Purpose Kentucky Housing Corporation (KHC) has partnered with HOPE of Kentucky, LLC, and the Community Reinvestment Fund, USA

FHA Section 542(c) Risk-Sharing Program for Multifamily Housing Program Rules Purpose Kentucky Housing Corporation (KHC) has partnered with HOPE of Kentucky, LLC, and the Community Reinvestment Fund, USA

APPENDIX B - CONSUMER LOAN POLICY. Table of Contents

APPENDIX B - CONSUMER LOAN POLICY Table of Contents 1. CONSUMER LOAN POLICY... 1 2. STANDARD UNDERWRITING... 1 3. REFERRAL SOURCES... 4 4. UNDERWRITING OF EXISTING LOANS:... 4 5. UNDERWRITING LOAN POLICY

APPENDIX B - CONSUMER LOAN POLICY Table of Contents 1. CONSUMER LOAN POLICY... 1 2. STANDARD UNDERWRITING... 1 3. REFERRAL SOURCES... 4 4. UNDERWRITING OF EXISTING LOANS:... 4 5. UNDERWRITING LOAN POLICY

Enhanced Coverage Commitment Guide

Operations I Mortgage Insurance Enhanced Coverage Commitment Guide October 1, 2014 Let s help someone buy a house today. 9899206.0814 GENWORTH MORTGAGE INSURANCE CORPORATION ENHANCED COVERAGE COMMITMENT

Operations I Mortgage Insurance Enhanced Coverage Commitment Guide October 1, 2014 Let s help someone buy a house today. 9899206.0814 GENWORTH MORTGAGE INSURANCE CORPORATION ENHANCED COVERAGE COMMITMENT

Desktop Underwriter/Desktop Originator Release Notes

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.2 September Update July 24, 2018 During the weekend of Sept. 22, 2018, Fannie Mae will implement an update to Desktop Underwriter (DU

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.2 September Update July 24, 2018 During the weekend of Sept. 22, 2018, Fannie Mae will implement an update to Desktop Underwriter (DU

AG-AMERICA COMMERCIAL FARM AND RANCH LOAN APPROVAL GUIDE

AG-AMERICA COMMERCIAL FARM AND RANCH Table of Contents CHAPTER 301 LOAN APPROVAL OVERVIEW... 1 301.1 Preliminary Loan Approval... 1 Credit Standards... 1 302.2 Preliminary Loan Approval... 1 1. Loan Application...

AG-AMERICA COMMERCIAL FARM AND RANCH Table of Contents CHAPTER 301 LOAN APPROVAL OVERVIEW... 1 301.1 Preliminary Loan Approval... 1 Credit Standards... 1 302.2 Preliminary Loan Approval... 1 1. Loan Application...

Exhibit B. Affordable Housing Corporation of Lake County Homebuyer Programs PROMISSORY NOTE. Secured by a Subordinate Second Mortgage

Exhibit B Affordable Housing Corporation of Lake County Homebuyer Programs PROMISSORY NOTE Secured by a Subordinate Second Mortgage Month XX, 20XX xxxxx Illinois [Date] [City or Village] [State] [Property

Exhibit B Affordable Housing Corporation of Lake County Homebuyer Programs PROMISSORY NOTE Secured by a Subordinate Second Mortgage Month XX, 20XX xxxxx Illinois [Date] [City or Village] [State] [Property