YTD Activity Total 7(a) and 504

|

|

|

- Emily O’Connor’

- 5 years ago

- Views:

Transcription

1

2 SBA Updates Bill Manger, Associate Administrator Office of Capital Access Steve Kucharski, Director, OPSM Susan Streich, Director, OCRM Jihoon Kim, Director, OFPO Dianna Seaborn, Director, OFA 2

3 7(a) Lending Activity YTD Activity Total 7(a) and 504 Fiscal Year Approved Loans Approved Dollars ,450 $ 14,451,910, ,937 $ 14,118,324, ,645 $ 12,872,759, ,417 $ 11,913,457, ,124 $ 9,688,269, ,527 $ 9,573,714, Lending Activity Fiscal Year Approved Loans Approved Dollars ,133 $ 2,517,641, ,640 $ 2,982,030, ,302 $ 2,667,712, ,211 $ 2,312,747, ,261 $ 2,280,694, ,342 $ 2,917,020,000 Time Period Comparison (activity through 04/30 of each FY) 3

4 Veteran Women Minority YTD Activity Underserved Markets Fiscal Year Approved Loans % of # Approved Dollars % of $ , % $ 5,345,247, % , % $ 5,224,793, % , % $ 4,582,564, % , % $ 4,029,834, % , % $ 3,376,571, % , % $ 3,314,863, % Fiscal Year Approved Loans % of # Approved Dollars % of $ , % $ 2,240,291, % , % $ 2,325,870, % , % $ 2,200,404, % , % $ 1,829,441, % , % $ 1,457,414, % , % $ 1,614,548, % Fiscal Year Approved Loans % of # Approved Dollars % of $ , % $ 582,589, % , % $ 626,580, % , % $ 701,948, % , % $ 681,330, % , % $ 403,078, % , % $ 479,077, % Time Period Comparison (activity through 04/30 of each FY) **Information submitted on a voluntary basis and not verified by SBA for completeness or accuracy 4

5 YTD Activity Mission Programs Microloans Fiscal Year Approved Loans Approved Dollars ,650 $ 36,250, ,621 $ 35,997, ,250 $ 30,990, ,008 $ 29,123, ,134 $ 31,330, ,128 $ 28,597,100 FY18 Microloan approvals underreported due to lag in micro lender reporting. Community Advantage Fiscal Year Approved Loans Approved Dollars $ 79,254, $ 79,070, $ 66,798, $ 51,558, $ 29,309, $ 17,162,700 Time Period Comparison (activity through 04/30 of each FY) 5

6 Steve Kucharski, Director, OPSM Etran System Updates 6

7 Susan Streich, Director, OCRM 504 Lender Oversight Updates 7

8 Jihoon Kim, Acting Director, OFPO Center Updates 8

9 Dianna Seaborn, Director, OFA Policy Updates 9

10 Hot Topics Appraisal reports Required prior to loan closing Dated within 12 months of application At least two of the three valuation methods (cost, income, sales) SBA listed as a client or intended user 10

11 Life Insurance Hot Topics Required when: No succession plan AND Liquidation value of collateral assets is insufficient to cover net debenture amount of SBA loan Based on liquidation value of collateral assets as determined by appraisal (not project cost) 11

12 Hot Topics Statements of Personal History SBA Form 912 (for Borrowers) not required if Questions 1, 2, and 3 are no SBA Form 1244, Section XIX SBA Form 1081 (for CDC staff) Name checks are no longer accepted FBI Form FD-258 (fingerprint card) required 12

13 504 Loan Program Updates 504 Program Statistics 25 year Debenture Appraisal update clarification SOP (J) Updates Credit Elsewhere update 504 Debt Refinancing Final rule 13

14 25 Year Debenture - Overview Launch date April 2, 2018; Federal Register Notice Longer repayment term Lower monthly loan payments Project approved prior to April 2, 2018 may not be extended to 25 years Third Party Loan term must be at least 10 years As of June 1, 2018: 188 applications received $204,398,000 14

15 Modification of 20 year to 25 year Prior to Closing Requests for term modification can be made after SLPC loan approval if approved on or after April 2, 2018 Submit 327 request in ETran with justification for the extended maturity Applicant must provide written consent to the modification and CDC must retain in file The term of the 504 Debenture may not be modified after the debenture closing request is submitted to SBA. 15

16 504 Loans Appraisal Clarification Appraisal Threshold OCC, Board, and FDIC rule increases appraisal threshold to $500,000 Small Business Act states the SBA shall require appraisals at $250,000 Will require a legislative update to match Federal Regulator limits

17 SOP (J) SBA Information Notice , Issuance of SOP (J) SBA Information Notice , Technical corrections issued on 12/15/2017. SBA Policy Notice , Revised Credit Elsewhere and Other Provisions effective 4/3/2018. SOP (J) includes rearrangement of some material, and other small changes that are not included on this presentation. 17

18 Recent Changes Policy Notice Changes affecting both 7(a) and 504 Loan Programs: Credit Elsewhere Increased minimum ownership percentage requiring a review from 10% to 20%; Additional guidance for businesses engaged in any illegal activity; Direct Marijuana Business Indirect Marijuana Business Hemp Related Business Leasing Part of a Building Acquired with Loan Proceeds; Borrower may not lease space to a business that is engaged in any activity that is illegal under federal, state or local law. 18

19 Loans Outside a CDC s Area of Operations Exception Requests: As of August 21, 2017, SLPC is the contact for case-by-case exception requests for submitting loans outside a CDC s area of operations. Requests no longer go through the District offices. 13 CFR was updated The SLPC may approve the application if: a) The applicant CDC has previously assisted the business to obtain a 504 loan; or b) The existing CDC or CDCs serving the area agree to permit the applicant CDC to make the 504 loan; or c) There is no CDC within the Area of Operations.

20 SOP (J) Updates Franchise documentation; Credit Elsewhere; Affiliation based on management; Change of ownership between owners in EPC; Borrower contribution Special Purpose properties Life insurance requirements Historic Properties review Illegal Businesses 20

21 Franchise If brand is not listed on the Directory: CDC must determine the brand is eligible before proceeding with the application SBA will review this decision at time of application for non- PCLP applications and prior to closing for PCLP applications Avoid delays on non-pclp applications Send any agreement not on the Directory to for review prior to submitting the loan application to SLPC When submitting loan application - Include the approval received from SBA s Franchise department as Exhibit 13. Management agreements to SLPC as a pre-application 21

22 SOP (J) Credit Elsewhere Same update for 7(a) and 504 Loan Programs: Revised existing language to make clear that non-federal sources of financing includes sources both related to and unrelated to Applicant Non-Federal sources related to the Applicant: Increased minimum ownership percentage requiring a review from 10% to 20% in Policy Notice Defines non-federal sources unrelated to the applicant to include conventional lenders or other sources of credit including the processing lender 22

23 SOP (J) Affiliation Based on Management Same for 7(a) and 504 Loan Programs Affiliation may be created by a Management Agreement determination based on degree of Applicant business oversight and control Affiliation created - Ineligible: No owner oversight No affiliation created - Eligible: Applicant has meaningful oversight of the management company s activities FINDING OF AFFILIATION May be eligible: The Agreement provides limited discretion over the business operations by the management firm, and the owner(s) retain meaningful oversight of the decision-making process. Combined size will determine eligibility. 23

24 EPC Change of Ownership Change of ownership between owners of Eligible Passive Company: Now permitted when the assets of the EPC are limited to real estate and/or other long term fixed assets that the EPC leases to its Operating Company. Reminders: Real estate must have been held by the EPC for at least 36 months The limitation on what assets can be held by the EPC is in place due to potential litigation that would impact the OC if other real estate unrelated to the OC were allowed to be held by the EPC.

25 Borrower Contribution - Special Purpose Properties Limited or Special Purpose Property requires at least 15% borrower contribution Minimum borrower contribution increases to 20%: If a business (including affiliates) already has an outstanding debenture for a Project involving a Limited or Special Purpose Property If a Project will finance both a New Business and a Limited or Special Purpose Property Minimum required equity injection will not exceed 20%, regardless of whether a business (including its affiliates) has an outstanding debenture(s) for a Project involving a Limited or Special Purpose Property 25

26 Insurance Requirements Guidance for 504 Life Insurance: Required when liquidation value of collateral is insufficient to secure the net debenture amount of the SBA loan Calculation of liquidation value is based on appraisal value (not project cost) 26

27 Insurance Calculation Example Total Project Cost: $5,000,000 (50/30/20 Structure) Breakdown of Project Costs: TPL Amount: $2,500,000 Building/Land: $4,050, Amount: $1,500,000 Equipment: $ 500,000 Borrower: $1,000,000 Other Expenses: $450,000 Liquidation Value = Collateral Appraised Value * Standard Liquidation Rates Collateral Appraised Value Liquidation Rate Liquidation Value Real Estate $4,500,000 75% $3,375,000 Equipment $500,000 50% $250,000 Total Collateral Liquidation Value $3,625,000 Life insurance is required when the liquidation value of the collateral is insufficient to secure the SBA loan. Collateral Liquidation Value $3,625,000 Subtract TPL Amount 1 st lien -$2,500,000 Subtract 504 Loan Amount 2 nd lien -$1,500,000 Liquidated Collateral Shortage =($375,000) Required Life Insurance Amount $375,000 Equipment that is part of appraised value for special use facilities such as hotels / gas stations a 75% liquidation rate will be applied to the overall appraised value. 27

28 504 Updates on Historic Properties Review Historic properties review required: Projects impacting sites listed or eligible to be listed on the National Register of Historic Places ( NRHP ) Consult with local SBA counsel No further obligation if no potential to cause effect on historic properties Example: purchase with no renovation/no changes If SBA finds no adverse effect and the SHPO agrees or does not object within 30 days, the Agency can proceed with the approval of the loan. If SBA Counsel finds an adverse effect on the historic nature of the property, SBA must consult with the State Historic Preservation Officer (SHPO) to resolve the issue. 28

29 SOP (J) Ineligible and Illegal Businesses Applies to 7(a) and 504 Loan Programs Added guidance on Marijuana-Related Businesses. Direct Marijuana Business Indirect Marijuana Business Hemp-Related Business Added guidance on leasing part of building acquired with loan proceeds to an illegal business. 29

30 SBA received statutory authority to reauthorize the 504 Debt Refinancing Program for up to $7.5 billion annually. This is in addition to the $7.5 billion authorization for the 504 Loan Program. With this change, total 504 lending has a $15 billion authorization for FY18. SBA published the Interim Final Rule on May 25, 2016, and the Policy Notice on May 26, The Interim Final Rule had a 30- day effective date after publication and SBA launched the 504 Debt Refinancing Program on June 24, The Final Rule published on May 7, 2018, becomes effective on June 6,

31 Fees Update As per SBA Information Notice , for loans approved under the 504 Debt Refinancing (without Expansion) Program during FY 2018, the total annual guarantee fee is 0.682% (68.2 basis points). SBA will review the fee annually and issue notices of any change. 31

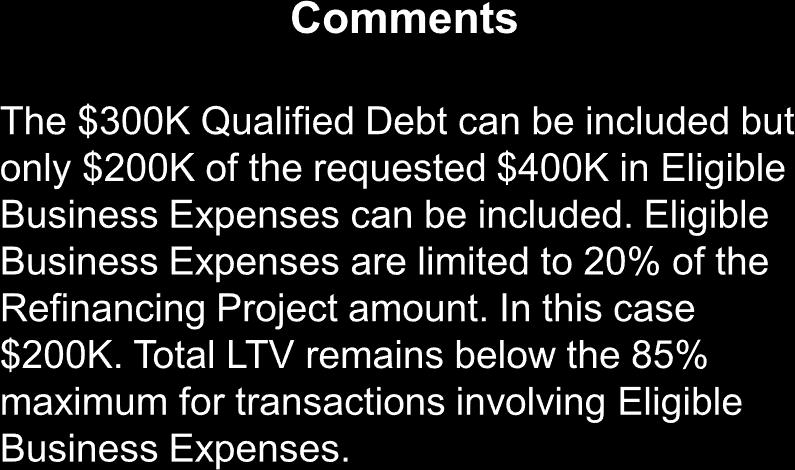

32 Final Rule Changes Debt Refi w/o Expansion Qualified Debt Current on All Payments Due Refinancing Projects - Special Purpose Properties Eligible Business Expenses Update Documentation Requirements Update 32

33 1 Qualified Debt Update The definition of Qualified Debt was revised to allow loans that were refinanced within 2 years prior to the date of application to be eligible for refinancing if: the effect of the most recent loan was to extend the maturity date without advancing any additional proceeds (except to cover closing costs); and the collateral for the most recent loan includes, at a minimum, the same Eligible Fixed Asset(s) that served as collateral for the prior loan that was refinanced. 33

34 : For loans that were refinanced within 2 years prior to the date of application, what documents must be provided to show eligibility as Qualified Debt? : CDCs must submit to SBA copies of the most recent loan and lien instruments, as well as copies of the loan and lien instruments for the loan that was replaced by the most recent loan, to show that the effect of the most recent loan was to extend the prior loan s maturity date without advancing any additional funds to the Borrower (other than to pay the closing costs of the refinancing). 34

35 2 Current on All Payments Due *Modification or refinance within the year prior to application is eligible: Purpose was to extend the maturity date of the loan No additional proceeds were advanced (except for closing costs); and provided that Applicant has been current on all payments due with no deferments for the 1-year period prior to the date of application *NOTE: This does not apply to debt refinance with expansion under the 504 Loan Program 35

36 Scenario 1: : My Borrower s loan will mature in 3 weeks. The Borrower will not be able to come into my office until after that time. If we provide an extension, would this be considered a loan modification that would mean the debt is ineligible? : The lender may provide an extension, and the loan may still be considered current, provided that the purpose of the modification is ONLY to extend the maturity date of the loan and no additional proceeds are advanced. Scenario 2: : My Borrower was unable to refinance its note before it expired; however, the Borrower continued making timely payments. Is this debt eligible? : No. 36

37 3 Borrower Contribution Special Purpose Special Purpose collateral: Borrower must contribute at least 15% Economic Recession: Borrower contribution may be reduced to 10% 37

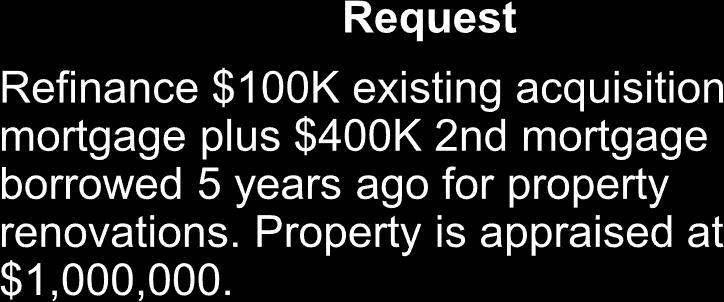

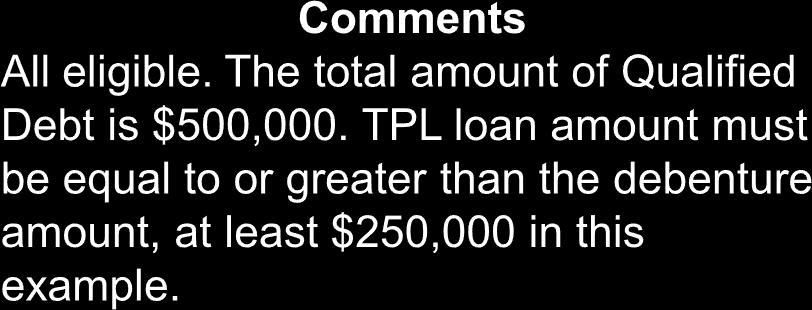

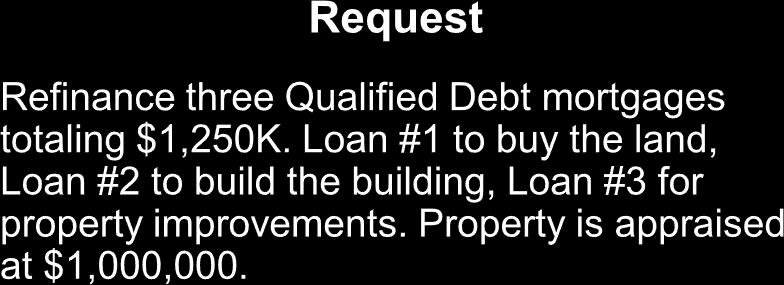

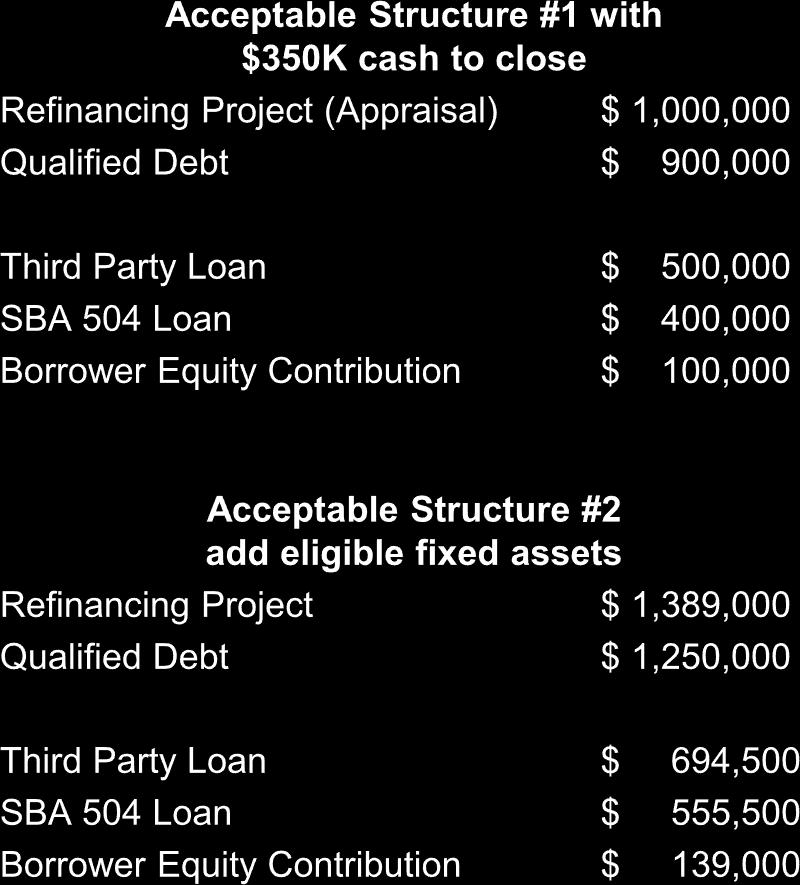

38 4 Eligible Business Expenses Three Things to Consider: Eligible Business Expenses (EBE) can t exceed 20% FMV of Eligible Fixed Assets securing the Qualified Debt Total project financing (TPL loan + SBA loan) can t exceed 85% FMV of the fixed assets serving as collateral; AND Cannot increase the value of the project by adding collateral NOTE: No cash out permitted in debt refinance with expansion 38

39 : The fair market value of the collateral for the proposed loan will not support the refinance. What are the options for addressing the collateral shortage? : It depends. Collateral for the most recent loan must include, at a minimum, the same Eligible Fixed Asset(s) that served as collateral for the prior loan. If no EBE, options include adding eligible collateral, and/or subordinated debt if it meets criteria for borrowed equity per the SOP (demonstrates repayment ability, not repaid faster than the 504 loan, etc.) However - If the Refinancing Project includes the financing of EBE, the 504 loan and Third Party Loan may be no more than 85% of the fair market value of the fixed assets that will serve as collateral, and the Borrower may not increase the value of the Refinancing Project by adding any additional assets as collateral. 39

40 4 Eligible Business Expenses Eligible: Operating expenses that were accrued but not paid prior to the date of application or that will become due within 18 months Examples: repairs, maintenance, minor improvements, salaries, rent, utilities, inventory Includes any operating expense that can be deducted as an expense in the taxable year in which it was paid or incurred Business lines of credit & business credit card debt are eligible Ineligible: capital expenditures such as expenditures for expansion and acquisition 40

41 4 Eligible Business Expenses Debt does not qualify as an EBE unless: Incurred with a business credit card or business line of credit and Applicant certifies the debt was exclusively for business uses CDCs must document the nature of the expense and provide an itemization in the credit memorandum 41

42 4 Eligible Business Expenses Both the CDC and the Borrower must certify in the application that the funds will be used for EBE. Borrower may be asked to show that loan proceeds provided for EBE were actually used for EBE Loan proceeds must not be used to refinance any personal expenses. 42

43 : What is the documentation requirement for Eligible Business Expenses (EBE)? Is a gross figure acceptable, or must expenses be itemized? : CDCs must document the nature of the EBE, provide an itemization of the expenses, and certify that they are eligible in the credit memorandum. Additionally: At application, the Borrower must certify that the debt is eligible The TPL must certify the EBE is eligible in its commitment letter EBE documentation should be retained at the CDC so it is available if requested by SBA. 43

44 5 Disbursement Period Disbursement Period - Increased from 6 months to 9 months May request an exception to policy for an extension for an additional 6 months for good cause Total allowable months with an exception to policy is 15 months 44

45 Comments There is no Qualified Debt to refinance so the project would not be eligible under this program. Each project must have a Qualified Debt to be eligible. 45

46

47

48

49

.")

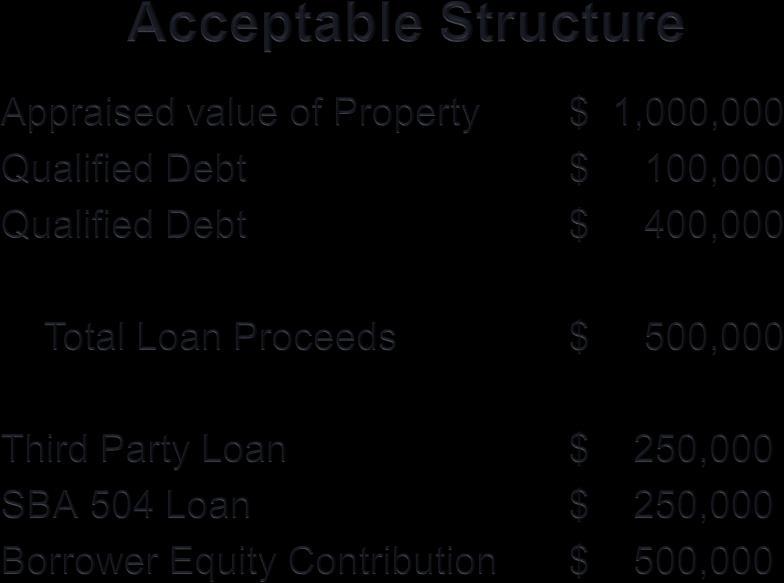

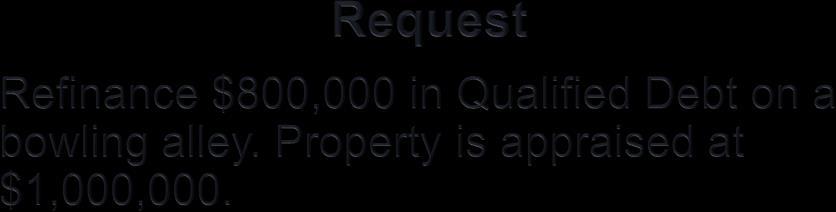

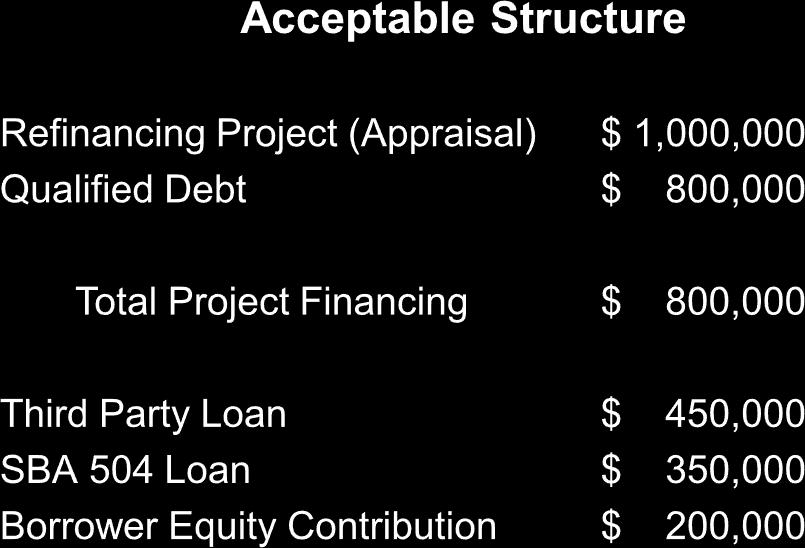

50 Comments The mortgage debt would be a Qualified Debt if the earlier refinancing was, in effect, a replacement for the prior loan with no new funds advanced (other than closing costs). Only $150,000 of the request is eligible as this project is limited to no more than 85% LTV. As a special purpose property the Borrower contribution must be at least 15% and SBA cannot exceed 35%.

51 Debt Refi w/o Expansion Max Borrower contribution required 15%, unless SBA determines risk mitigation requires more Federally guaranteed loans ineligible TPL loan can be reduced to less than 50% of project cost provided: 1) the TPL loan is equal to or greater than the SBA loan, AND 2) SBA not to exceed 40% of the total project cost or 35% for Special Use properties Subject to supplemental annual fee. Current total annual fee is 0.682% Debt Refi with Expansion Max Borrower contribution required 20% Federally guaranteed loans eligible if allowed by originating Federal Agency TPL loan must be at least equal to 50% of Project costs SBA not to exceed 40% of the total project cost or 35% for Special Use properties No supplemental annual fee. Current total annual fee is 0.642% 51

52 Debt Refi w/o Expansion Debt Refi with Expansion Eligible Business Expenses up to 20% of appraised value of the Eligible Fixed Assets w/max LTV of 85%. Collateral must be fixed assets securing the Qualified Debt. No additional collateral can be added to meet LTV requirements. Min. 2 year requirement: Age of original eligible debt, time debt secured by the same Eligible Fixed Asset & time applicant in business Borrower must be current on all payments for preceding year as of date of app. Loan may have been modified/refinanced within the year if no additional funds disbursed and if purpose was to extend maturity date. No cash out. Costs such as prepayment penalties, financing fees or other refi costs required by original debt instrument may be included. Substantial benefit test must provide better rates or terms 10% lower payment Borrower must be current on all payments due on the existing debt for not less than 1 year or for the time the debt has been open if less than 1 year. No allowance for modification or refinance to extend maturity date. 52

53 Linda Reilly Chief, 504 Loan Program (202) Babak Hosseini Finance and Loan Specialist (202) Hien Nguyen Director, SLPC (916) David Miller Supervisory Loan Specialist, SLPC (916) Ginger Allen Finance and Loan Specialist (202) Please send your questions about the 504 Debt Refinancing (without Expansion) Program to: 53

54 Questions? 54

SBA will officially launch the 504 Debt Refinancing program on June 24, 2016

SBA has received statutory authority to reauthorize the 504 Debt Refinance Program for up to $7.5 billion. This is in addition to the $7.5 billion authorization for the 504 program. With this change, total

SBA has received statutory authority to reauthorize the 504 Debt Refinance Program for up to $7.5 billion. This is in addition to the $7.5 billion authorization for the 504 program. With this change, total

Statutory Requirements

In December 2015, SBA received statutory authority to reauthorize the 504 Debt Refinance Program for up to $7.5 billion. This is in addition to the $7.5 billion authorization for the 504 program. With

In December 2015, SBA received statutory authority to reauthorize the 504 Debt Refinance Program for up to $7.5 billion. This is in addition to the $7.5 billion authorization for the 504 program. With

U.S. SMALL BUSINESS ADMINISTRATION. Reauthorization of the 504 Debt Refinancing Program

U.S. SMALL BUSINESS ADMINISTRATION Reauthorization of the 504 Debt Refinancing Program Refinance Program Timeline In December 2015, received statutory authority to reauthorize the 504 Debt Refinance Program

U.S. SMALL BUSINESS ADMINISTRATION Reauthorization of the 504 Debt Refinancing Program Refinance Program Timeline In December 2015, received statutory authority to reauthorize the 504 Debt Refinance Program

Massachusetts District Office April 5, 2018 SEED ANNUAL TRAINING

Massachusetts District Office April 5, 2018 SEED ANNUAL TRAINING 1 See SBA Information Notice 5000-1708, Issuance of SOP 50 10 5 (J), for more detailed information of major changes to SOP, and SBA Information

Massachusetts District Office April 5, 2018 SEED ANNUAL TRAINING 1 See SBA Information Notice 5000-1708, Issuance of SOP 50 10 5 (J), for more detailed information of major changes to SOP, and SBA Information

ELIGIBILITY FRIDAY, MARCH 13 8:30 AM 9:30 AM

ELIGIBILITY FRIDAY, MARCH 13 8:30 AM 9:30 AM 504 Loan Program Eligibility Clarifications Preapplications Preapplications for eligibility will be accepted by SLPC for the following: Franchises Heavy duty

ELIGIBILITY FRIDAY, MARCH 13 8:30 AM 9:30 AM 504 Loan Program Eligibility Clarifications Preapplications Preapplications for eligibility will be accepted by SLPC for the following: Franchises Heavy duty

SUMMARY: This rule finalizes the interim final rule (IFR) that was published on May

that was published on May") This document is scheduled to be published in the Federal Register on 05/07/2018 and available online at https://federalregister.gov/d/2018-09638, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS

This document is scheduled to be published in the Federal Register on 05/07/2018 and available online at https://federalregister.gov/d/2018-09638, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS

General Session V Affiliation and Franchise: A Roadmap to the Rule Wednesday, November 9 3:15 pm 4:30 pm Continental Ballroom 4-5

General Session V Affiliation and Franchise: A Roadmap to the Rule Wednesday, November 9 3:15 pm 4:30 pm Continental Ballroom 4-5 Thank you to our Alliance Partners 2 Speakers Linda Reilly, Acting Director,

General Session V Affiliation and Franchise: A Roadmap to the Rule Wednesday, November 9 3:15 pm 4:30 pm Continental Ballroom 4-5 Thank you to our Alliance Partners 2 Speakers Linda Reilly, Acting Director,

Topics for this Session

welcome Topics for this Session Quick discussion of SBA s debt refinancing requirements Walk through of some refinancing scenarios 2 Copyright 2017, NAGGL, Inc. - Do Not Copy/Distribute 1 Why is SBA So

welcome Topics for this Session Quick discussion of SBA s debt refinancing requirements Walk through of some refinancing scenarios 2 Copyright 2017, NAGGL, Inc. - Do Not Copy/Distribute 1 Why is SBA So

ELIGIBILITY INFORMATION REQUIRED FOR 504 SUBMISSION (NON PCLP)

") ELIGIBILITY INFORMATION REQUIRED FOR 504 SUBMISSION (NON PCLP) OMB APPROVAL NO.: 3245-0071 EXPIRATION DATE: 09/30/2016 [The CDC completes this form to help SBA carryout its lender, portfolio and program

ELIGIBILITY INFORMATION REQUIRED FOR 504 SUBMISSION (NON PCLP) OMB APPROVAL NO.: 3245-0071 EXPIRATION DATE: 09/30/2016 [The CDC completes this form to help SBA carryout its lender, portfolio and program

Servicing Update: SOP 50 55, Chapter 6 & Chapter 8 Overview. Salon B Monday, October 20, :30 pm 3:30 pm

Servicing Update: SOP 50 55, Chapter 6 & Chapter 8 Overview Salon B Monday, October 20, 2014 2:30 pm 3:30 pm Thank you to our Alliance Partners TRAI N I N G & E D U C AT I O N Speakers Shirley Walls, Supervisory

Servicing Update: SOP 50 55, Chapter 6 & Chapter 8 Overview Salon B Monday, October 20, 2014 2:30 pm 3:30 pm Thank you to our Alliance Partners TRAI N I N G & E D U C AT I O N Speakers Shirley Walls, Supervisory

Welcome to the 7(a) Connect Call

Connect Call") Welcome to the 7(a) Connect Call During this call we will provide updates, training tips and hot topics on the Office of Capital Access There will be time allotted for questions and answers. Office of

Welcome to the 7(a) Connect Call During this call we will provide updates, training tips and hot topics on the Office of Capital Access There will be time allotted for questions and answers. Office of

SBA Information Notice

SBA Information Notice TO: All SBA Employees, 7(a) Lenders and Certified Development Companies CONTROL NO.: 5000-17008 SUBJECT: Issuance of SOP 50 10 5(J) EFFECTIVE: October 13, 2017 The purpose of this

SBA Information Notice TO: All SBA Employees, 7(a) Lenders and Certified Development Companies CONTROL NO.: 5000-17008 SUBJECT: Issuance of SOP 50 10 5(J) EFFECTIVE: October 13, 2017 The purpose of this

Intro to 7(a) Lending

Lending") Intro to 7(a) Lending Presented by Dianna Seaborn Acting Director, Office of Financial Assistance US Small Business Administration 1 Becoming an SBA Lender Credit Unions with share insurance must send

Intro to 7(a) Lending Presented by Dianna Seaborn Acting Director, Office of Financial Assistance US Small Business Administration 1 Becoming an SBA Lender Credit Unions with share insurance must send

SBA Lending: Documenting, Closing and Servicing 7(a) and CDC/504 Loans

and CDC/504 Loans") Presenting a live 90-minute webinar with interactive Q&A SBA Lending: Documenting, Closing and Servicing 7(a) and CDC/504 Loans Navigating SBA Approval and Authorization Process, Preserving the Loan Guaranty

Presenting a live 90-minute webinar with interactive Q&A SBA Lending: Documenting, Closing and Servicing 7(a) and CDC/504 Loans Navigating SBA Approval and Authorization Process, Preserving the Loan Guaranty

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C. 20416 Management Advisory Report No. 16-23 DATE: September 30, 2016 TO: Maria Contreras-Sweet Administrator Ann Marie Mehlum

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C. 20416 Management Advisory Report No. 16-23 DATE: September 30, 2016 TO: Maria Contreras-Sweet Administrator Ann Marie Mehlum

7(a) LOAN APPLICATION PROCESS AT THE LGPC

LOAN APPLICATION PROCESS AT THE LGPC") 7(a) LOAN APPLICATION PROCESS AT THE LGPC 7(a) LOAN GUARANTY PROGRAM Flexible financing for your small business customers Igniting the Flames of Success OFO/OCA LENDER RELATIONS SPECIALISTS TRAINING September

7(a) LOAN APPLICATION PROCESS AT THE LGPC 7(a) LOAN GUARANTY PROGRAM Flexible financing for your small business customers Igniting the Flames of Success OFO/OCA LENDER RELATIONS SPECIALISTS TRAINING September

FY 2018 Fees and Miscellaneous Amendments to Business Loan Programs and Surety Bond Guarantee Program. AKA Fees and Catch-All

FY 2018 Fees and Miscellaneous Amendments to Business Loan Programs and Surety Bond Guarantee Program AKA Fees and Catch-All SBA 7(a) Guaranty Fees for FY 18 and Veteran Fee Relief for FY 18 www.sba.gov

FY 2018 Fees and Miscellaneous Amendments to Business Loan Programs and Surety Bond Guarantee Program AKA Fees and Catch-All SBA 7(a) Guaranty Fees for FY 18 and Veteran Fee Relief for FY 18 www.sba.gov

Effective Date: May 1,

divestiture of all ownership interest and severance of any relationship with the Small Business Applicant (and any associated Eligible Passive Concern) in any capacity, including being an employee (paid

divestiture of all ownership interest and severance of any relationship with the Small Business Applicant (and any associated Eligible Passive Concern) in any capacity, including being an employee (paid

SUMMARY: This rule finalizes the proposed rule that the U.S. Small Business

This document is scheduled to be published in the Federal Register on 03/21/2014 and available online at http://federalregister.gov/a/2014-06237, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS ADMINISTRATION

This document is scheduled to be published in the Federal Register on 03/21/2014 and available online at http://federalregister.gov/a/2014-06237, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS ADMINISTRATION

SBA Loan Guarantee Program

SBA Loan Guarantee Program Presented By: United States Small Business Administration Washington D.C. Metro Area District Office (WMADO) 409 3rd Street S.W. 2nd Floor Washington, D.C. 20416 (202)205-8800

SBA Loan Guarantee Program Presented By: United States Small Business Administration Washington D.C. Metro Area District Office (WMADO) 409 3rd Street S.W. 2nd Floor Washington, D.C. 20416 (202)205-8800

Primary purpose of Franchise revisions is to streamline procedures for determining size eligibility based on affiliation between Franchisee &

Primary purpose of Franchise revisions is to streamline procedures for determining size eligibility based on affiliation between Franchisee & Franchisor Regulatory Changes 13 CFR 121.301(f)(5) (effective

Primary purpose of Franchise revisions is to streamline procedures for determining size eligibility based on affiliation between Franchisee & Franchisor Regulatory Changes 13 CFR 121.301(f)(5) (effective

Commercial Real Estate Comparison Pricing Summary

Wells Fargo Bank, N.A. Small Business Administration Lending Commercial Real Estate Comparison Pricing Summary Prepared For: Darrin Boyd - David Moore Property Address: 9755 Westoint Drive Indianapolis,

Wells Fargo Bank, N.A. Small Business Administration Lending Commercial Real Estate Comparison Pricing Summary Prepared For: Darrin Boyd - David Moore Property Address: 9755 Westoint Drive Indianapolis,

Office of Capital Access. Monthly LRS Call. April 19, 2017

Office of Capital Access Monthly LRS Call April 19, 2017 Bill Manger Associate Administrator Office of Capital Access U.S. Small Business Administration Email: william.manger@sba.gov 2 Agency Goal New

Office of Capital Access Monthly LRS Call April 19, 2017 Bill Manger Associate Administrator Office of Capital Access U.S. Small Business Administration Email: william.manger@sba.gov 2 Agency Goal New

$278,440,000 U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES

OFFERING CIRCULAR $278,440,000 (Approximate) U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES Guaranteed by the U.S. SMALL BUSINESS ADMINISTRATION (an independent agency of the

OFFERING CIRCULAR $278,440,000 (Approximate) U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES Guaranteed by the U.S. SMALL BUSINESS ADMINISTRATION (an independent agency of the

Coleman Certified SBA 7(a) Loan Closer Lance A. Sexton, Coleman Faculty Instructor

Loan Closer Lance A. Sexton, Coleman Faculty Instructor") Coleman Certified SBA 7(a) Loan Closer Lance A. Sexton, Coleman Faculty Instructor Setting Up the SBA Loan File There are a number of ways to set up a loan file. My recommendation for the SBA Loan File

Coleman Certified SBA 7(a) Loan Closer Lance A. Sexton, Coleman Faculty Instructor Setting Up the SBA Loan File There are a number of ways to set up a loan file. My recommendation for the SBA Loan File

$279,425,000 (Approximate) U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES

U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES") OFFERING CIRCULAR $279,425,000 (Approximate) U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES Guaranteed by the U.S. SMALL BUSINESS ADMINISTRATION (an independent agency of the

OFFERING CIRCULAR $279,425,000 (Approximate) U.S. GOVERNMENT GUARANTEED DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES Guaranteed by the U.S. SMALL BUSINESS ADMINISTRATION (an independent agency of the

LiftFund (CDC) 504 Checklist and Loan Application

504 Checklist and Loan Application") 1. 2. LiftFund (CDC) 504 Checklist and Loan Application Copy of photo ID (Driver license) History of the Business. (Business Plan for start-ups.) Equal Opportunity Lender 3. Current personal financial

1. 2. LiftFund (CDC) 504 Checklist and Loan Application Copy of photo ID (Driver license) History of the Business. (Business Plan for start-ups.) Equal Opportunity Lender 3. Current personal financial

DISCLOSURE STATEMENT U.S. SMALL BUSINESS ADMINISTRATION 504 LOAN PROGRAM

DISCLOSURE STATEMENT U.S. SMALL BUSINESS ADMINISTRATION 504 LOAN PROGRAM The SBA 504 Loan Program offers eligible Small Business Concerns (SBC s) the means to finance expansion projects through a long-term,

DISCLOSURE STATEMENT U.S. SMALL BUSINESS ADMINISTRATION 504 LOAN PROGRAM The SBA 504 Loan Program offers eligible Small Business Concerns (SBC s) the means to finance expansion projects through a long-term,

Deep Dive into Portfolio Management and the National Guaranty Purchase Center. Presented by: Susan Suckfiel and Vanessa Piccioni

Deep Dive into Portfolio Management and the National Guaranty Purchase Center Presented by: Susan Suckfiel and Vanessa Piccioni Overview 10-Tab Packages & the Purchase Review Common Reasons for Repairs

Deep Dive into Portfolio Management and the National Guaranty Purchase Center Presented by: Susan Suckfiel and Vanessa Piccioni Overview 10-Tab Packages & the Purchase Review Common Reasons for Repairs

$262,864,000 (Approximate) U.S. GOVERNMENT GUARANTEED 2.85% DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES SERIES J Due October 1, 2037

U.S. GOVERNMENT GUARANTEED 2.85% DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES SERIES J Due October 1, 2037") OFFERING CIRCULAR $262,864,000 (Approximate) U.S. GOVERNMENT GUARANTEED 2.85% DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES SERIES 2017-20 J Due October 1, 2037 CUSIP: 83162C YX5 Guaranteed by the U.S.

OFFERING CIRCULAR $262,864,000 (Approximate) U.S. GOVERNMENT GUARANTEED 2.85% DEVELOPMENT COMPANY PARTICIPATION CERTIFICATES SERIES 2017-20 J Due October 1, 2037 CUSIP: 83162C YX5 Guaranteed by the U.S.

Servicing Update: SOP 50 55, Chapter 6 & Chapter 8 Overview. Mount Whitney Room Tuesday, June 17, :00 pm 4:00 pm

Servicing Update: SOP 50 55, Chapter 6 & Chapter 8 Overview Mount Whitney Room Tuesday, June 17, 2014 3:00 pm 4:00 pm Thank you to our Alliance Partners Fresno, CA June 17-18 Speakers Ray Kulina, Assistant

Servicing Update: SOP 50 55, Chapter 6 & Chapter 8 Overview Mount Whitney Room Tuesday, June 17, 2014 3:00 pm 4:00 pm Thank you to our Alliance Partners Fresno, CA June 17-18 Speakers Ray Kulina, Assistant

ELIGIBILITY INFORMATION REQUIRED FOR PLP SUBMISSION Rev. 11/25/08

ELIGIBILITY INFORMATION REQUIRED FOR PLP SUBMISSION Rev. 11/25/08 1. Fill out all of this section. If a question in this section is answered No, the loan is not eligible. Applicant Name Lender Name Purpose

ELIGIBILITY INFORMATION REQUIRED FOR PLP SUBMISSION Rev. 11/25/08 1. Fill out all of this section. If a question in this section is answered No, the loan is not eligible. Applicant Name Lender Name Purpose

Attendees may pick up your conference materials (name badges Registration

CONFERENCE AGENDA Session(s) are subject to change. All meeting rooms are on the Lobby Level of the hotel. For more info, visit our website at www.tnlendersconference.com. Indicates a session available

CONFERENCE AGENDA Session(s) are subject to change. All meeting rooms are on the Lobby Level of the hotel. For more info, visit our website at www.tnlendersconference.com. Indicates a session available

Guidance on Refinancing Existing Loans in the Section 538 Guaranteed Rural Rental Housing Program (GRRHP)

") May 3, 2017 TO: State Directors Rural Development ATTN: Program Directors Multi-Family Housing FROM: Richard A. Davis /s/ Richard A. Davis Acting Administrator Rural Housing Service SUBJECT: Guidance on

May 3, 2017 TO: State Directors Rural Development ATTN: Program Directors Multi-Family Housing FROM: Richard A. Davis /s/ Richard A. Davis Acting Administrator Rural Housing Service SUBJECT: Guidance on

Product Guidelines Freddie Mac Relief Refinance - Open Access

; Important Note: The program has been extended to allow application received dates on or before December 31, 2018 and settlement dates on or before September 30, 2019. Occupancy 1-4 Units 1-4 Units Max

; Important Note: The program has been extended to allow application received dates on or before December 31, 2018 and settlement dates on or before September 30, 2019. Occupancy 1-4 Units 1-4 Units Max

SBA Procedural Notice

SBA Procedural Notice TO: All Employees CONTROL NO.: 5000-722 SUBJECT: PCLP Loan Loss Reserve Requirements EFFECTIVE: 04/05/01 Introduction The Premier Certified Lenders program (PCLP) transfers considerable

SBA Procedural Notice TO: All Employees CONTROL NO.: 5000-722 SUBJECT: PCLP Loan Loss Reserve Requirements EFFECTIVE: 04/05/01 Introduction The Premier Certified Lenders program (PCLP) transfers considerable

LENDER RELATION SPECIALIST TRAINING

LENDER RELATION SPECIALIST TRAINING 504 SERVICING, LIQUIDATION AND POST SERVICING Wednesday, September 6, 2017 A message from the Little Rock and Fresno Commercial Loan Service Centers.. While the Loan

LENDER RELATION SPECIALIST TRAINING 504 SERVICING, LIQUIDATION AND POST SERVICING Wednesday, September 6, 2017 A message from the Little Rock and Fresno Commercial Loan Service Centers.. While the Loan

10/15/2012. Banking 101. Current Banking Landscape. The New Banking World

The New Banking World Banking 101 Current Banking Landscape 1 Survival of the Fittest Economic Developments Role Investors Community Bank 860 North Rapids Rd. Manitowoc, WI 54220 920-686-5604 Tim Schneider,

The New Banking World Banking 101 Current Banking Landscape 1 Survival of the Fittest Economic Developments Role Investors Community Bank 860 North Rapids Rd. Manitowoc, WI 54220 920-686-5604 Tim Schneider,

Finding the Money You Need

Finding the Money You Need O ne key to a successful business start-up and expansion is your ability to obtain and secure appropriate financing. Raising capital is the most basic of all business activities.

Finding the Money You Need O ne key to a successful business start-up and expansion is your ability to obtain and secure appropriate financing. Raising capital is the most basic of all business activities.

HOME EQUITY LENDING Constitutional Requirements for a Texas Home Equity Loan

HOME EQUITY LENDING Constitutional Requirements for a Texas Home Equity Loan 1) The home equity loan is voluntary (applicant is not required to obtain a Home Equity loan) and the Home Equity lien is created

HOME EQUITY LENDING Constitutional Requirements for a Texas Home Equity Loan 1) The home equity loan is voluntary (applicant is not required to obtain a Home Equity loan) and the Home Equity lien is created

FINAL CAPLINES CHANGES TO SOP (D)

") FINAL CAPLINES CHANGES TO SOP 50 10 5(D) 9-15-2011 Subpart A: Chapter 1 Pg. 9 Deleted additional qualifications for lenders to participate in CAPLines, including removing the Lenders Qualification Survey

FINAL CAPLINES CHANGES TO SOP 50 10 5(D) 9-15-2011 Subpart A: Chapter 1 Pg. 9 Deleted additional qualifications for lenders to participate in CAPLines, including removing the Lenders Qualification Survey

Max LTV/CLTV FICO 1 Unit 95/95% /90% 620 Purchase 85/85% 620 Refi 75/75% 2 Units Purchase & Refi- 85/85% 620 N/A N/A 75/75% 620

Revision: October 25, 2016 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied

Revision: October 25, 2016 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied

Implementing New CDC Governance Rules Broadmoor Hall C 10:45 am 11:45 am

Implementing New CDC Governance Rules Broadmoor Hall C 10:45 am 11:45 am Office of Capital Access Final Rule 504 Loan Program Corporate Governance Rules Office of Financial Assistance Office of Financial

Implementing New CDC Governance Rules Broadmoor Hall C 10:45 am 11:45 am Office of Capital Access Final Rule 504 Loan Program Corporate Governance Rules Office of Financial Assistance Office of Financial

Compliance Checklists

Compliance Checklists Lender Checklist... Ck-1 Broker Checklist... Ck-7 Servicer Checklist... Ck-13 Checklist for Other Service Providers... Ck-15 Ck-i Ck-ii THE RESPA MANUAL Ck-1 Compliance Checklists

Compliance Checklists Lender Checklist... Ck-1 Broker Checklist... Ck-7 Servicer Checklist... Ck-13 Checklist for Other Service Providers... Ck-15 Ck-i Ck-ii THE RESPA MANUAL Ck-1 Compliance Checklists

Small Business Loan Guaranty Program

Revised April 2013 Small Business Loan Guaranty Program Overview Created as part of the Small Business Jobs Act of 2010, the State Small Business Credit Initiative (SSBCI) was designed to help increase

Revised April 2013 Small Business Loan Guaranty Program Overview Created as part of the Small Business Jobs Act of 2010, the State Small Business Credit Initiative (SSBCI) was designed to help increase

Chesapeake Business Finance Corp.

Chesapeake Business Finance Corp. John Sower, President 1101 30 th St NW #500 Sower1@erols.com Washington, DC 20007 www.chesapeake504.com Tel: 202-625-4373 Cell: 202-257-5871 Fax: 202-342-0389 John Sower

Chesapeake Business Finance Corp. John Sower, President 1101 30 th St NW #500 Sower1@erols.com Washington, DC 20007 www.chesapeake504.com Tel: 202-625-4373 Cell: 202-257-5871 Fax: 202-342-0389 John Sower

LOAN SERVICING AND EQUITY INTEREST AGREEMENT

LOAN SERVICING AND EQUITY INTEREST AGREEMENT THIS LOAN SERVICING AND EQUITY INTEREST AGREEMENT ( Agreement ) is made as of, 20 by and among Cushman Rexrode Capital Corporation, a California corporation

LOAN SERVICING AND EQUITY INTEREST AGREEMENT THIS LOAN SERVICING AND EQUITY INTEREST AGREEMENT ( Agreement ) is made as of, 20 by and among Cushman Rexrode Capital Corporation, a California corporation

Lender Letter LL

Lender Letter LL-2017-09 November 2, 2017 To: All Fannie Mae Single-Family Servicers Fannie Mae Extend Modification for Disaster Relief and Other Clarifications for Mortgage Loans Impacted by Disaster

Lender Letter LL-2017-09 November 2, 2017 To: All Fannie Mae Single-Family Servicers Fannie Mae Extend Modification for Disaster Relief and Other Clarifications for Mortgage Loans Impacted by Disaster

Agency Income Guideline Revisions Note: SunTrust Mortgage specific overlays are underlined.

Rental Income Correspondent Section 2.01 Agency Loan Programs- Guideline Standard Agency (non- AUS, DU & LPA) Agency Plus (DU & LPA) Texas Cash- Out Refi (DU) Income / Rental Income Non-AUS Eligible Properties

Rental Income Correspondent Section 2.01 Agency Loan Programs- Guideline Standard Agency (non- AUS, DU & LPA) Agency Plus (DU & LPA) Texas Cash- Out Refi (DU) Income / Rental Income Non-AUS Eligible Properties

Complimentary Coleman Report Live!

Complimentary Coleman Report Live! Featuring Bob Coleman & Charles Green 1:50-2:00 PM E.T. Log on 10 minutes early before every Coleman webinar for a briefing on issues vital to the small business lending

Complimentary Coleman Report Live! Featuring Bob Coleman & Charles Green 1:50-2:00 PM E.T. Log on 10 minutes early before every Coleman webinar for a briefing on issues vital to the small business lending

HOW TO DOCUMENT EQUITY INJECTION GETTING IT RIGHT, 100% OF THE TIME. Coleman Webinar November 14, 2012

HOW TO DOCUMENT EQUITY INJECTION GETTING IT RIGHT, 100% OF THE TIME Coleman Webinar November 14, 2012 Small Business Banking News of the Day Talk Show Bob and Charles Show 1:50-2:00 PM ET. We are featuring

HOW TO DOCUMENT EQUITY INJECTION GETTING IT RIGHT, 100% OF THE TIME Coleman Webinar November 14, 2012 Small Business Banking News of the Day Talk Show Bob and Charles Show 1:50-2:00 PM ET. We are featuring

Intro into SBA Lending. Randy Griffin, President CSRA Business Lending

Intro into SBA Lending Randy Griffin, President CSRA Business Lending Small Business Administration (SBA) CREATION By Congress on July 30, 1953 Independent US Federal Agency Previously no agency or department

Intro into SBA Lending Randy Griffin, President CSRA Business Lending Small Business Administration (SBA) CREATION By Congress on July 30, 1953 Independent US Federal Agency Previously no agency or department

Loan Policy. Including Loan Program Parameters & Underwriting Guidelines. Last Updated 11/30/18

Loan Policy Including Loan Program Parameters & Underwriting Guidelines Last Updated 11/30/18 Commercial Lending X ( CLX ) is a national commercial financing consulting firm. CLX specializes in helping

Loan Policy Including Loan Program Parameters & Underwriting Guidelines Last Updated 11/30/18 Commercial Lending X ( CLX ) is a national commercial financing consulting firm. CLX specializes in helping

VA IRRRL PROGRAM MATRIX

MAXIMUM LTV **Mortgage Only Report IRRRL PROGRAM 1-4 Unit Properties, Condos, and PUD s (Primary Residence) NO FICO PROGRAM MINIMUM FICO MAX LTV 580 100% 620 125% **No FICO 660 UNLIMITED High Balance 100%

MAXIMUM LTV **Mortgage Only Report IRRRL PROGRAM 1-4 Unit Properties, Condos, and PUD s (Primary Residence) NO FICO PROGRAM MINIMUM FICO MAX LTV 580 100% 620 125% **No FICO 660 UNLIMITED High Balance 100%

CHAPTER 2 - LOAN CLOSING

CHAPTER 2 - LOAN CLOSING This chapter provides the Lender with guidance on closing and disbursing 7(a) loans in compliance with SBA requirements. It explains SBA s requirements by reviewing the 7(a) Loan

CHAPTER 2 - LOAN CLOSING This chapter provides the Lender with guidance on closing and disbursing 7(a) loans in compliance with SBA requirements. It explains SBA s requirements by reviewing the 7(a) Loan

General Session V Governance Concerns: How Does Your Organization Stack Up? Grand Ballroom Salons 1-4 2:15 pm 3:15 pm

General Session V Governance Concerns: How Does Your Organization Stack Up? Grand Ballroom Salons 1-4 2:15 pm 3:15 pm Thank you to our Alliance Partners Speakers Linda Rusche, Director, Office of Financial

General Session V Governance Concerns: How Does Your Organization Stack Up? Grand Ballroom Salons 1-4 2:15 pm 3:15 pm Thank you to our Alliance Partners Speakers Linda Rusche, Director, Office of Financial

Fannie Mae Reports Net Income of $5.1 Billion for Second Quarter 2012

Contact: Pete Bakel Resource Center: 1-800-732-6643 202-752-2034 Date: August 8, 2012 Fannie Mae Reports Net Income of $5.1 Billion for Second Quarter 2012 Net Income of $7.8 Billion for First Half 2012

Contact: Pete Bakel Resource Center: 1-800-732-6643 202-752-2034 Date: August 8, 2012 Fannie Mae Reports Net Income of $5.1 Billion for Second Quarter 2012 Net Income of $7.8 Billion for First Half 2012

Iowa s State Small Business Credit Initiative (SSBCI) Derek Lord, Community Investments Team Leader

Derek Lord, Community Investments Team Leader") Iowa s State Small Business Credit Initiative (SSBCI) Derek Lord, Community Investments Team Leader SSBCI Overview» Created by the Small Business Jobs Act of 2010 U.S. Treasury provided $1.5 billion for

Iowa s State Small Business Credit Initiative (SSBCI) Derek Lord, Community Investments Team Leader SSBCI Overview» Created by the Small Business Jobs Act of 2010 U.S. Treasury provided $1.5 billion for

SBA Export Financing. Grow your exports with financing

SBA Export Financing Grow your exports with financing Small Business Who are you calling small? Defined at 13 C.F.R. 121 (Explained at SBA.gov) Industry Code (NAICS) Size Standards (examples) Manufacturing

SBA Export Financing Grow your exports with financing Small Business Who are you calling small? Defined at 13 C.F.R. 121 (Explained at SBA.gov) Industry Code (NAICS) Size Standards (examples) Manufacturing

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION LOAN POLICIES Affordable Housing Development Affordable Housing Acquisition & Preservation Multi-family Housing Rehabilitation Community Facilities Table

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION LOAN POLICIES Affordable Housing Development Affordable Housing Acquisition & Preservation Multi-family Housing Rehabilitation Community Facilities Table

Your Guide to Home Financing

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

SMALL BUSINESS ADMINISTRATION

SMALL BUSINESS ADMINISTRATION General and special funds: Federal Funds SALARIES AND EXPENSES For necessary expenses of the Small Business Administration as authorized by Public Law 103 403, including hire

SMALL BUSINESS ADMINISTRATION General and special funds: Federal Funds SALARIES AND EXPENSES For necessary expenses of the Small Business Administration as authorized by Public Law 103 403, including hire

VILLAGE OF LITTLE CHUTE SMALL BUSINESS MICRO LOAN PROGRAM

VILLAGE OF LITTLE CHUTE SMALL BUSINESS MICRO LOAN PROGRAM CONTACT Charles P. Kell, Village Administrator 108 West Main Street Little Chute, Wisconsin 54140 Telephone: (920) 788-7380 Ext. 202 E-mail: chuck@littlechutewi.org

VILLAGE OF LITTLE CHUTE SMALL BUSINESS MICRO LOAN PROGRAM CONTACT Charles P. Kell, Village Administrator 108 West Main Street Little Chute, Wisconsin 54140 Telephone: (920) 788-7380 Ext. 202 E-mail: chuck@littlechutewi.org

The information you need to submit perfect 504 packages

The information you need to submit perfect 504 packages Benefits of Centralized Processing What is e504? Benefits of e504 Submissions Screen outs 10 Most Common Errors in Using e504 Most common omissions

The information you need to submit perfect 504 packages Benefits of Centralized Processing What is e504? Benefits of e504 Submissions Screen outs 10 Most Common Errors in Using e504 Most common omissions

HOW TO LOSE YOUR SBA GUARANTY

HOW TO LOSE YOUR SBA GUARANTY War Stories about lenders that did it the wrong way Presented by: Ethan W. Smith, Esq. Agenda: Basic Program Concepts/Terms Nature of the Guaranty Delegated Authority (PLP)

HOW TO LOSE YOUR SBA GUARANTY War Stories about lenders that did it the wrong way Presented by: Ethan W. Smith, Esq. Agenda: Basic Program Concepts/Terms Nature of the Guaranty Delegated Authority (PLP)

U.S. Small Business Administration Programs & Services. New Hampshire

U.S. Small Business Administration Programs & Services New Hampshire 1 Advantage of SBA s Guaranty Most Viable Business Profile Experienced management High Debt Service Cash flow Sterling credit Generous

U.S. Small Business Administration Programs & Services New Hampshire 1 Advantage of SBA s Guaranty Most Viable Business Profile Experienced management High Debt Service Cash flow Sterling credit Generous

Conventional and Government Program Overlays

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

What CPAs Need to Know About Alternative Financing

What CPAs Need to Know About Alternative Financing The Need for Alternative Capital Historically, institutional banks have represented the bulk of small business lenders. However, even before the Great

What CPAs Need to Know About Alternative Financing The Need for Alternative Capital Historically, institutional banks have represented the bulk of small business lenders. However, even before the Great

CITY OF DE PERE REVOLVING LOAN FUND MANUAL. Prepared by the: Planning and Economic Development Department

CITY OF DE PERE REVOLVING LOAN FUND MANUAL Prepared by the: Planning and Economic Development Department In conjunction with the Wisconsin Economic Development Corporation Adopted: January 15, 2013 TABLE

CITY OF DE PERE REVOLVING LOAN FUND MANUAL Prepared by the: Planning and Economic Development Department In conjunction with the Wisconsin Economic Development Corporation Adopted: January 15, 2013 TABLE

Today s Business Environment

6/21/2013 SECURING FINANCING IN TODAY S BUSINESS ENVIRONMENT Presented by Ken Paton Today s Business Environment In recovery from worst recession since the Great Depression Hundreds of bank failures More

6/21/2013 SECURING FINANCING IN TODAY S BUSINESS ENVIRONMENT Presented by Ken Paton Today s Business Environment In recovery from worst recession since the Great Depression Hundreds of bank failures More

Conventional and Government Program Overlays

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Commercial Real. Estate. CMBS Conduit. Loan. Program. Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage

Commercial Real Estate CMBS Conduit Loan Program Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage City Capital Realty Shawn Rabban 310-714-5616 shawnrabban@yahoo.com CAL

Commercial Real Estate CMBS Conduit Loan Program Retail Medical Office Industrial Warehouse Hotel Apartment Mixed-Use Self-Storage City Capital Realty Shawn Rabban 310-714-5616 shawnrabban@yahoo.com CAL

#9: Funding Your Company

Food Business Entrepreneurial Training Academy #9: Funding Your Company Alameda County SBDC FREMONT, CA 2/5/2019 Thank you to our partners Thank you to our sponsors Questions To Get Started How much money

Food Business Entrepreneurial Training Academy #9: Funding Your Company Alameda County SBDC FREMONT, CA 2/5/2019 Thank you to our partners Thank you to our sponsors Questions To Get Started How much money

Reverse Mortgage Authorization Form

Reverse Mortgage Authorization Form Conflict of Interest Disclosure Cambridge Credit Counseling Corp provides counseling to help you make an informed decision concerning reverse mortgage products. We will

Reverse Mortgage Authorization Form Conflict of Interest Disclosure Cambridge Credit Counseling Corp provides counseling to help you make an informed decision concerning reverse mortgage products. We will

First Lien Position 504 Loan Pooling Program PROGRAM GUIDE

First Lien Position 504 Loan Pooling Program PROGRAM GUIDE November 5, 2009 First Lien Position 504 Loan Pooling Program Guide INTRODUCTION SBA s secondary market program for First Lien Position 504 Loans

First Lien Position 504 Loan Pooling Program PROGRAM GUIDE November 5, 2009 First Lien Position 504 Loan Pooling Program Guide INTRODUCTION SBA s secondary market program for First Lien Position 504 Loans

US SHARE FUND Financial Services

US SHARE FUND Financial Services US SHARE FUND; With the partner funds and Banks is focused on profitable growth through niche financial services provided locally, nationally and via the Internet. These

US SHARE FUND Financial Services US SHARE FUND; With the partner funds and Banks is focused on profitable growth through niche financial services provided locally, nationally and via the Internet. These

Desktop Underwriter/Desktop Originator Release Notes

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.2 September Update July 24, 2018 During the weekend of Sept. 22, 2018, Fannie Mae will implement an update to Desktop Underwriter (DU

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.2 September Update July 24, 2018 During the weekend of Sept. 22, 2018, Fannie Mae will implement an update to Desktop Underwriter (DU

Term Sheet The Moderne Project Loan Agreement between The Milwaukee Moderne, LLC and the City of Milwaukee October 21, 2009

Term Sheet The Moderne Project Loan Agreement between The Milwaukee Moderne, LLC and the City of Milwaukee October 21, 2009 Project: The City of Milwaukee will fund two project loans to assist with the

Term Sheet The Moderne Project Loan Agreement between The Milwaukee Moderne, LLC and the City of Milwaukee October 21, 2009 Project: The City of Milwaukee will fund two project loans to assist with the

SUMMARY: The U.S. Small Business Administration (SBA) is re-examining the

is re-examining the") This document is scheduled to be published in the Federal Register on 12/08/2014 and available online at http://federalregister.gov/a/2014-28698, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS ADMINISTRATION

This document is scheduled to be published in the Federal Register on 12/08/2014 and available online at http://federalregister.gov/a/2014-28698, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS ADMINISTRATION

Announcement November 2, Updates and Clarifications to the Home Affordable Modification Program

Announcement 09-31 November 2, 2009 Amends these Guides: Servicing Updates and Clarifications to the Home Affordable Modification Program Introduction Announcement 09-05R, Reissuance of the Introduction

Announcement 09-31 November 2, 2009 Amends these Guides: Servicing Updates and Clarifications to the Home Affordable Modification Program Introduction Announcement 09-05R, Reissuance of the Introduction

FHLMC Relief Refinance Open Access

The Federal Housing Finance Agency (FHFA) Home Affordable Refinance Program ( HARP ) is designed to assist borrowers who have demonstrated an acceptable payment history on their existing Freddie Mac mortgage

The Federal Housing Finance Agency (FHFA) Home Affordable Refinance Program ( HARP ) is designed to assist borrowers who have demonstrated an acceptable payment history on their existing Freddie Mac mortgage

Appendix D Opinion of CDC Counsel

Appendix D Opinion of CDC Counsel Read this first! This appendix contains the standardized text for the Opinion of CDC Counsel required by the Authorization. All paragraphs are mandatory except when noted

Appendix D Opinion of CDC Counsel Read this first! This appendix contains the standardized text for the Opinion of CDC Counsel required by the Authorization. All paragraphs are mandatory except when noted

Refinance Transactions: New Maximum Mortgage Calculation. The Housing and Economic Recovery Act of 2008 revised the National Housing Act to:

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 15, 2008 MORTGAGEE LETTER 2008-40 TO: ALL APPROVED MORTGAGEES

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 15, 2008 MORTGAGEE LETTER 2008-40 TO: ALL APPROVED MORTGAGEES

Bridge to HUD Loan Platform Multifamily Acquisition/Refinance

Multifamily Acquisition/Refinance Underwriting Term Amortization Maximum LTV Acquisition or refinance (including cash-out) because of timing challenges associated with going directly to HUD, including

Multifamily Acquisition/Refinance Underwriting Term Amortization Maximum LTV Acquisition or refinance (including cash-out) because of timing challenges associated with going directly to HUD, including

Breakout Session V Environmental Reviews: Get Them Right Tuesday, November 8 1:45 pm 2:45 pm Golden Gate Ballroom 2-3

Breakout Session V Environmental Reviews: Get Them Right Tuesday, November 8 1:45 pm 2:45 pm Golden Gate Ballroom 2-3 Thank you to our Alliance Partners 2 Speakers Eric Adams, District Counsel U.S. Small

Breakout Session V Environmental Reviews: Get Them Right Tuesday, November 8 1:45 pm 2:45 pm Golden Gate Ballroom 2-3 Thank you to our Alliance Partners 2 Speakers Eric Adams, District Counsel U.S. Small

Small Business Administration 504/CDC Loan Guaranty Program

Small Business Administration 504/CDC Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government December 5, 2017 Congressional Research Service 7-5700 www.crs.gov R41184

Small Business Administration 504/CDC Loan Guaranty Program Robert Jay Dilger Senior Specialist in American National Government December 5, 2017 Congressional Research Service 7-5700 www.crs.gov R41184

Fannie Mae Reports Net Income of $10.1 Billion and Comprehensive Income of $10.3 Billion for Second Quarter 2013

Resource Center: 1-800-732-6643 Contact: Pete Bakel 202-752-2034 Date: August 8, 2013 Fannie Mae Reports Net Income of $10.1 Billion and Comprehensive Income of $10.3 Billion for Second Quarter 2013 Fannie

Resource Center: 1-800-732-6643 Contact: Pete Bakel 202-752-2034 Date: August 8, 2013 Fannie Mae Reports Net Income of $10.1 Billion and Comprehensive Income of $10.3 Billion for Second Quarter 2013 Fannie

DISCLOSURE STATEMENT REGARDING THE CITY OF CONCORD FIRST TIME HOMEBUYER PROGRAM AND SHARED APPRECIATION LOAN

DISCLOSURE STATEMENT REGARDING THE CITY OF CONCORD FIRST TIME HOMEBUYER PROGRAM AND SHARED APPRECIATION LOAN THIS IS AN IMPORTANT DOCUMENT. EVERY BORROWER THAT RECEIVES A LOAN FROM THE CITY OF CONCORD

DISCLOSURE STATEMENT REGARDING THE CITY OF CONCORD FIRST TIME HOMEBUYER PROGRAM AND SHARED APPRECIATION LOAN THIS IS AN IMPORTANT DOCUMENT. EVERY BORROWER THAT RECEIVES A LOAN FROM THE CITY OF CONCORD

COLORADO LENDING SOURCE, LTD. CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31, 2016

COLORADO LENDING SOURCE, LTD. CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31, 2016 Contents Page Independent Auditors Report... 1-3 Financial Statements Consolidated Statement Of Financial Position... 4

COLORADO LENDING SOURCE, LTD. CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31, 2016 Contents Page Independent Auditors Report... 1-3 Financial Statements Consolidated Statement Of Financial Position... 4

OCC Guidance on Higher Loan to Value Lending in Communities Targeted for Revitalization. Housing Works Conference Raleigh, NC October 25, 2017

OCC Guidance on Higher Loan to Value Lending in Communities Targeted for Revitalization Housing Works Conference Raleigh, NC October 25, 2017 Supervisory Loan-to-Value Limits for Residential Loans SLTV

OCC Guidance on Higher Loan to Value Lending in Communities Targeted for Revitalization Housing Works Conference Raleigh, NC October 25, 2017 Supervisory Loan-to-Value Limits for Residential Loans SLTV

Issue Date 2/24/11 Effective Date As Noted WPA

Changes and Other Topics Purpose This communication: Adds an MSI overlay to Streamline Refinances. Addresses the Mortgagee Letters 11-10 and 11-11. Clarification for Trusts and POA s. Clarification for

Changes and Other Topics Purpose This communication: Adds an MSI overlay to Streamline Refinances. Addresses the Mortgagee Letters 11-10 and 11-11. Clarification for Trusts and POA s. Clarification for

CROP LOAN GUARANTEE PROGRAM

CROP LOAN GUARANTEE PROGRAM LENDER MANUAL 1 P age Contents ABOUT THIS MANUAL... 3 WHO TO CONTACT... 3 ELIGIBILITY... 4 A. ELIGIBLE LENDERS... 4 B. ELIGIBLE BORROWERS... 5 C. ELIGIBLE LOANS... 6 D. ELIGIBLE

CROP LOAN GUARANTEE PROGRAM LENDER MANUAL 1 P age Contents ABOUT THIS MANUAL... 3 WHO TO CONTACT... 3 ELIGIBILITY... 4 A. ELIGIBLE LENDERS... 4 B. ELIGIBLE BORROWERS... 5 C. ELIGIBLE LOANS... 6 D. ELIGIBLE

2018 SBA 7(a) LOAN CLOSING TRAINING ONLINE ON DEMAND ON YOUR SCHEDULE

LOAN CLOSING TRAINING ONLINE ON DEMAND ON YOUR SCHEDULE") 2018 SBA 7(a) LOAN CLOSING TRAINING ONLINE ON DEMAND ON YOUR SCHEDULE REGISTRATION IS ALWAYS OPEN Need 7(a) Loan Closing Training or CLE hours? Want the convenience of training on your schedule? Want affordable

2018 SBA 7(a) LOAN CLOSING TRAINING ONLINE ON DEMAND ON YOUR SCHEDULE REGISTRATION IS ALWAYS OPEN Need 7(a) Loan Closing Training or CLE hours? Want the convenience of training on your schedule? Want affordable

COMMERCIAL REVOLVING LOAN FUND

COMMERCIAL REVOLVING LOAN FUND 8.1 PURPOSE The City of Columbia, through economic development projects financed by the Commercial Revolving Loan Fund, seeks to improve the number and caliber of job opportunities,

COMMERCIAL REVOLVING LOAN FUND 8.1 PURPOSE The City of Columbia, through economic development projects financed by the Commercial Revolving Loan Fund, seeks to improve the number and caliber of job opportunities,

Guidelines: Kentucky Collateral Support Program (KYCSP) Participants

Participants") Guidelines: Kentucky Collateral Support Program (KYCSP) May 2014 The Kentucky Collateral Support Program (KYCSP) (the Program ) provides a pledged asset (cash collateral account) to an enrolled lender

Guidelines: Kentucky Collateral Support Program (KYCSP) May 2014 The Kentucky Collateral Support Program (KYCSP) (the Program ) provides a pledged asset (cash collateral account) to an enrolled lender

Staff Connections - World Bank Intranet

Page 1 of 7 Staff Connections - World Bank Intranet 06 Compensation 06.18 Financial Assistance to Staff Members 01. Subject, Applicability and Definitions 02. General Provisions 03. Loans for Settling-In

Page 1 of 7 Staff Connections - World Bank Intranet 06 Compensation 06.18 Financial Assistance to Staff Members 01. Subject, Applicability and Definitions 02. General Provisions 03. Loans for Settling-In

Programs and Resources to Advance Women s Entrepreneurship. U.S. Small Business Administration Answers Resources Support For Your Small Business

Programs and Resources to Advance Women s Entrepreneurship Focus on Women s Entrepreneurship Since it was established in response to an executive order in 1979, the U.S. Small Business Administration s

Programs and Resources to Advance Women s Entrepreneurship Focus on Women s Entrepreneurship Since it was established in response to an executive order in 1979, the U.S. Small Business Administration s

Section 1.02 Eligible Mortgage Loans

Section 1.02 Eligible Mortgage Loans In This Section This section contains the following topics: Related Bulletins... 2 Approved Products and Services... 3 SunTrust Employee Loans... 3 General... 3 Eligible

Section 1.02 Eligible Mortgage Loans In This Section This section contains the following topics: Related Bulletins... 2 Approved Products and Services... 3 SunTrust Employee Loans... 3 General... 3 Eligible

Program Qualifications

This matrix is intended as an aid to assist in determining if a property/loan qualifies for certain USDA offered programs. It is not intended as a replacement for USDA guidelines. Users are expected to

This matrix is intended as an aid to assist in determining if a property/loan qualifies for certain USDA offered programs. It is not intended as a replacement for USDA guidelines. Users are expected to

Frequently Asked Questions CDC Training: 504 Servicing Updates within Electronic Lending-Servicing (ETRAN) March 2018

March 2018") Frequently Asked Questions CDC Training: 504 Servicing Updates within Electronic Lending-Servicing (ETRAN) March 2018 Customer Service Q: When should I contact Wells Fargo Customer Service versus CLS Customer

Frequently Asked Questions CDC Training: 504 Servicing Updates within Electronic Lending-Servicing (ETRAN) March 2018 Customer Service Q: When should I contact Wells Fargo Customer Service versus CLS Customer