Viet Nam: Technical Training Manuals for Microfinance Institutions in Vietnam. Advance Course in Financial Management

|

|

|

- Marsha Hawkins

- 5 years ago

- Views:

Transcription

1 Project Number: November 2011 Viet Nam: Technical Training Manuals for Microfinance Institutions in Vietnam Advance Course in Financial Management

2 1

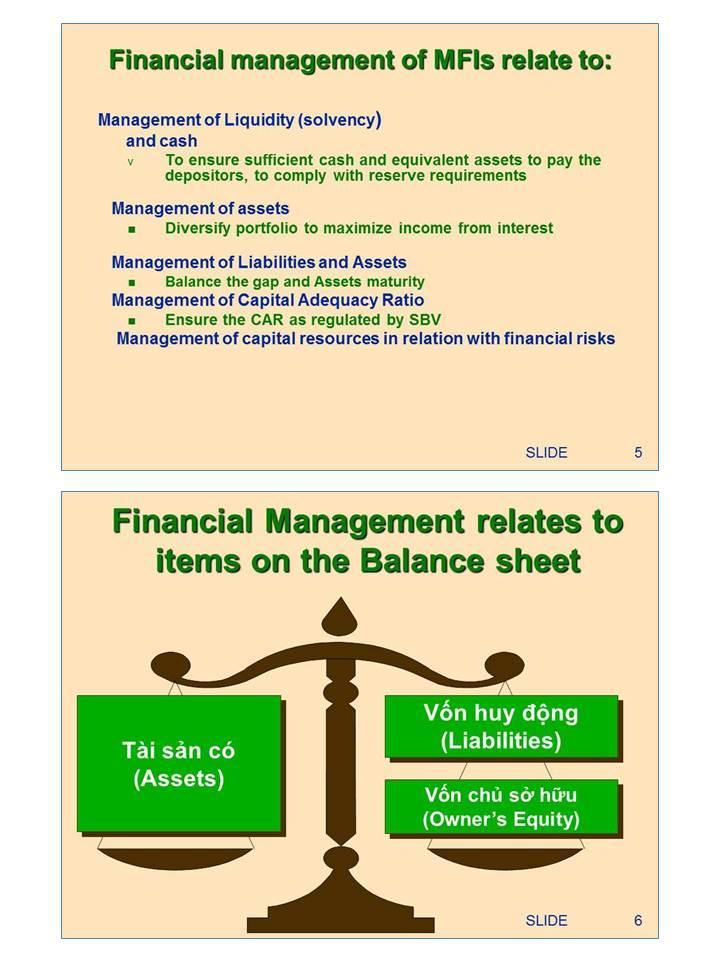

3 COURSE OUTLINE Course Name Target Participants Course Duration Learning Objectives Course Outline Delivery Methods Materials Needed Handouts ADVANCE FINANCIAL MANAGEMENT FOR MICROFINANCE INSTITUTIONS Board, Managers, Chief Accountant, Accountant 3 days By the end of the course, the participants are able to: Gain advanced knowledge and skills in financial management to ensure that the management is making sound management decisions in operating their microfinance institutions. Opening Activities Opening Activities o Welcome Remarks o Training Objectives and o Introductions: Trainer, Guests, Agenda and Participants o House Rules o Project Overview Overview of Financial o Leveling of Expectations management o Review of Financial Management Overview of Financial Overview of Financial management management o Liquidity Management o Assets-Liabilities o Treasury Management management o o Capital Adequacy Ratio Management Financial Structure and Interest Understanding Financial Rate Risks Management Planning o Financial Structure o Financial Plans o Interest Rate Risks Closing Activities o Evaluation o Closing Lecture/Plenary; Small Group Discussions; Exercises; Post-Training Test Computer, LCD Projector, Flipcharts (A0 Paper), Meta Plan Cards, Calculators, Paper, Pens, Tapes, Prizes, Stapler, Paper Clips, Training Kit (Agenda, PPT Presentations, Notepad, Pens, ID), Financial Statements of MFIs SBV Circular No. 07 and 015; TYM Case Study; Financial Planning Model; Guidelines for Financial Planning 2

4 INSTRUCTIONAL DESIGN AT A GLANCE Part I OPENING ACTIVITIES Session 1 Introductions Activity 1 Registration, Welcome Remarks, and Introductions Activity 2 Leveling of Expectations Activity 3 House Rules Part II THE ADVANCE FINANCIAL MANAGEMENT FOR MFI Session 1 Overview of Financial management Activity 4 Review of Financial Management Activity 5 Liquidity Management Activity 6 Treasury Management Activity 7 Asset-Liability Management Activity 8 CAR Management Session 2 Financial Structure and Interest Rate Risk Management Activity 9 Financial Structure Activity 10 Interest Rate Risk Management Session 3 Understanding Financial Planning Activity 11 Development of Financial Plan Part III CLOSING ACTIVITIES Session 1 Wrap Up and Evaluations Activity 12 Evaluation Activity 13 Closing HANDOUT 1 SBV Circular No SBV Circular No TYM Case Study 4 Financial Planning Model 5 Guidelines for Financial Planning 3

5 INSTRUCTIONAL DESIGN SCRIPT PART I OPENING ACTIVITIES Session 1 Introductions Activity 1 Registration, Welcome Remarks and Introductions Purpose To register the participants and distribute the training kit To introduce the ADB-SBV Project, the guests, trainers and participants. Objectives By the end of the activity, the participants are able: Received complete set of the training kit. Know the project, host organization, guests, the trainers, and other participants. Time Materials Steps/Method: 30 minutes Attendance Sheet Training Kit:: - Agenda - Notepad - Pen - ID - Training Material Registration: 1. The support staff facilitates the registration of the participants and the distribution of training kits at least 30 minutes before the start of the training. 2. The support staff checks completeness of the contents of the training kits with the participants. 3. The support staff ensures participants write their names on the IDs and wear the IDs at all times during the training. 4. The support staff ensures all equipment, facilities, supplies and materials required for the training are 40 minutes Brief profile of host organizations and guests Brief profile of the trainers Profile of the Participants, Registration Sheet, Computer, Slide Presentations, Flipcharts, Stands, Pens, Papers, Tapes, LCD Projector, available. Welcome Remarks: Speech 1. The Training Coordinator introduces the host organizations (SBV, ADB, JFPR, ADB Consultants, etc.) and guests (if any). 2. The host organizations and guests deliver their welcome remarks. Introduction of the Trainers: Speech 1. The Training Coordinator welcomes and introduces the trainers (the lead trainer and co-trainers, if any). 2. The Training Coordinator gives the floor to the lead trainer to start the training. Introduction of the Participants: Plenary; Small Group Discussions 1. The lead trainer welcomes the participants. 2. The lead trainer asks the participants to create five groups using their seat arrangements. 3. The lead trainer asks the participants to introduce themselves to the groups, identify a representative of each group, and summarize the points in 15 minutes: a. Introduction of group members; b. Reason for attending this course c. Expectations/learning from this course; d. Total years of experience of the group members. 4

6 PPT slide 2 4. The lead trainer asks the representatives of the groups to describe the members of the group to the rest of the participants. 5. The lead trainer acknowledges each participant and welcomes them to the training. 6. When all groups have presented, the lead trainer thanks the participants and moves to the next activity. PART I OPENING ACTIVITIES Session 1 Introductions Activity 2 LEVELING OF EXPECTATIONS Purpose To determine what are the participants expectations from the training To validate whether the participants expectations can be met by the training Objectives By the end of the activity, the participants will have: Present their motivations and expectations from the training. Know the course agenda and validate coverage of their expectations with the trainers. Identify items or issues that cannot be covered by the training. Time Materials Steps/Method: Note: Combined with the introductions Small Group Discussions; Plenary. 1. The lead trainer use the group outputs in Activity 1, consolidate participants motivations and expectations from the course. Computer, Group Outputs, PPT Slide no. 2 and 3; Flipchart for Parking Lot, Stands, Tapes, LCD Projector Training Objectives and Agenda: 2. The lead trainer presents the training objectives and agenda to participants and validates expectations that can not be covered by the training. 3. The lead trainer also identifies items that cannot be covered, if any, and places them to the Parking Lot Note: The Parking Lot is a place where the trainer can write issues, items or any concern that is covered by the training. This is visited at the end of the training to determine whether items have been covered or need to be discussed in other venue 4. The lead trainer summarizes the participant s outputs and asks the participants for more inputs or questions. 5. When there are no more questions, the lead trainer thanks the participants and move to the next activity. PART I Session 1 Activity 3 Purpose Objectives OPENING ACTIVITIES Introductions HOUSE RULES To ensure that the participants get the optimum learning from the course. By the end of the activity, the participants are able to: 5

7 Define and agree on appropriate behaviors for the duration of the training. Define and agree on appropriate penalties for violations of the house rules. Time Materials Steps/Method: 5-10 minutes Flipcharts, Stands, Pens, Tapes Slide Presentation; Plenary 1. The lead trainer asks the participants what could help them achieve optimum learning from the training and lists them on a flipchart. 2. The lead trainer may initiate discussions by providing standard or frequently mentioned house rules. Such house rules may include: coming on time, turning off or placing on silent mode the mobile phones, participating actively, respecting others, etc. 3. The lead trainer verifies acceptability of the responses with the participants by asking them to agree on each item. 4. When there are no more additions, the lead trainer shares his expectations if not yet covered by the listed items by present PPT slide (no. 3). 5. The lead trainer thanks the participants and closes the session by asking the participants to be always reminded of the house rules for the duration of the training. 6. The lead trainer posts the flipchart to the wall and moves to the next activity. Note: Having completed the introductions, the expectations and the house rules, the participants are now ready to start with the main topics in the course. PART II THE ADVANCE FINANCIAL MANAGEMENT FOR MFIS Session 1 Review of Financial Management Activity 4 Review of Principles of Financial Management Purpose To review the principles of financial management in MFIs. Objectives By the end of the activity, the participants are able to: Refresh understanding of financial management and the principles behind. Time: Materials: Steps/Method: 60 minutes Computer, PPT Slide 4-6, Flipcharts, Pens, Stands, Tapes, LCD Projector Plenary a. The lead trainer conducts a review of the participants understanding of financial management. The lead trainer lists down the responses on flipchart. The responses may include: manage cash, manage assets, manage liability, manage capital, manage equity, manage income, manage expense, make profit, etc. b. The lead trainer summarizes the responses and concludes the review with emphasis on the description of financial management as: 6

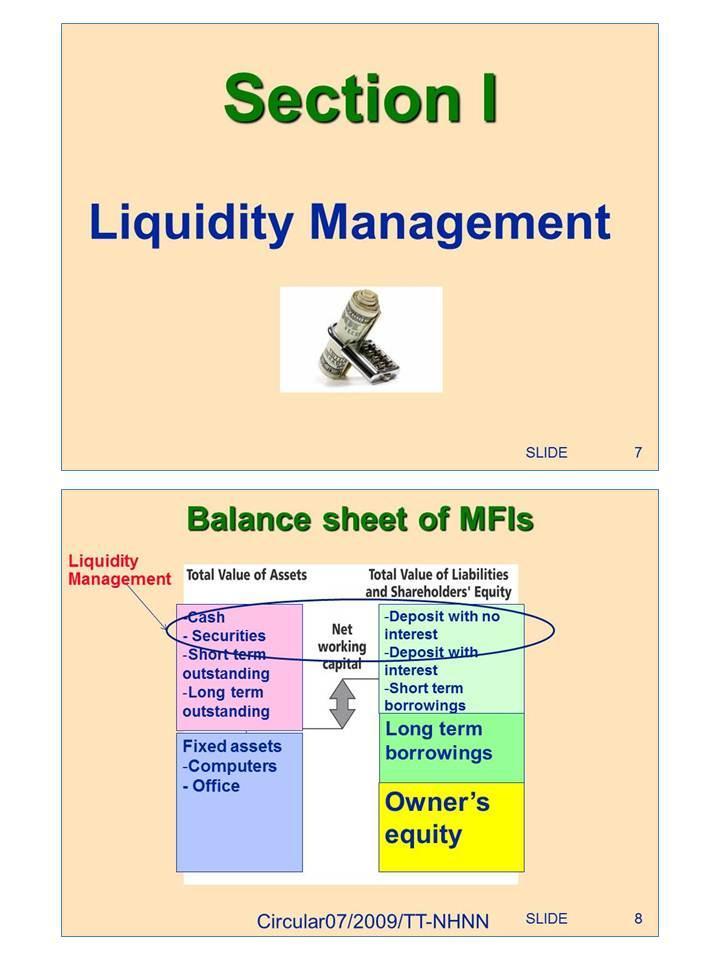

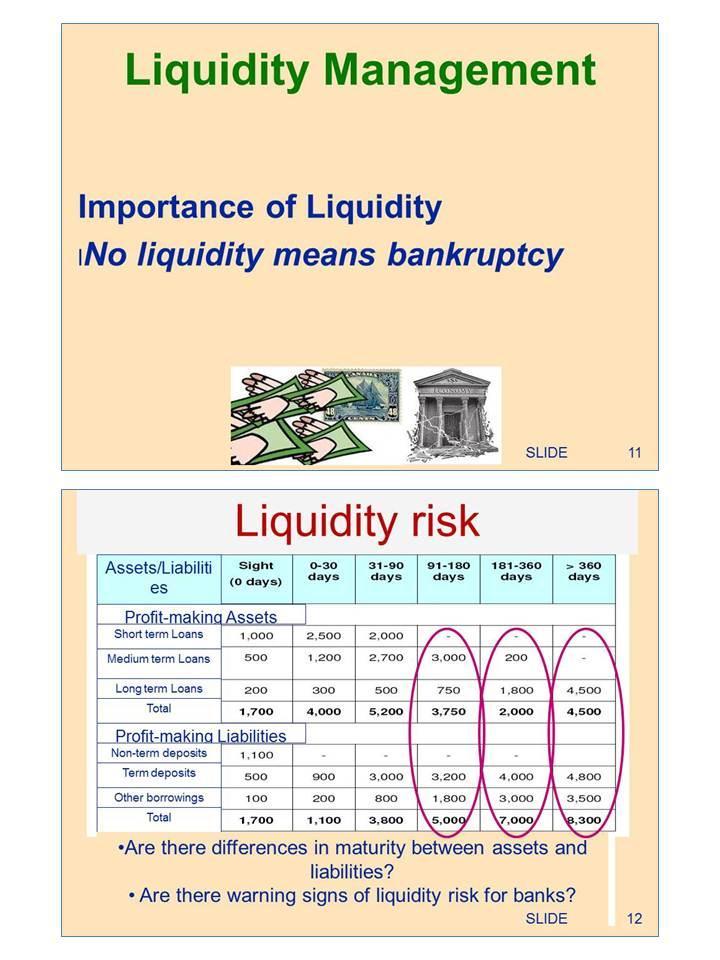

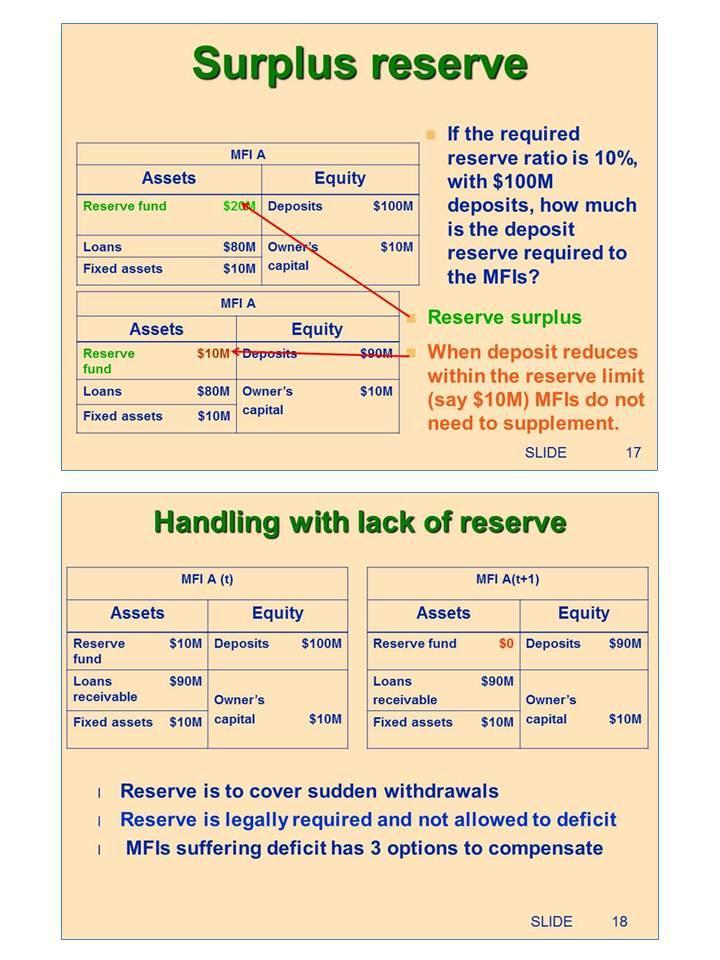

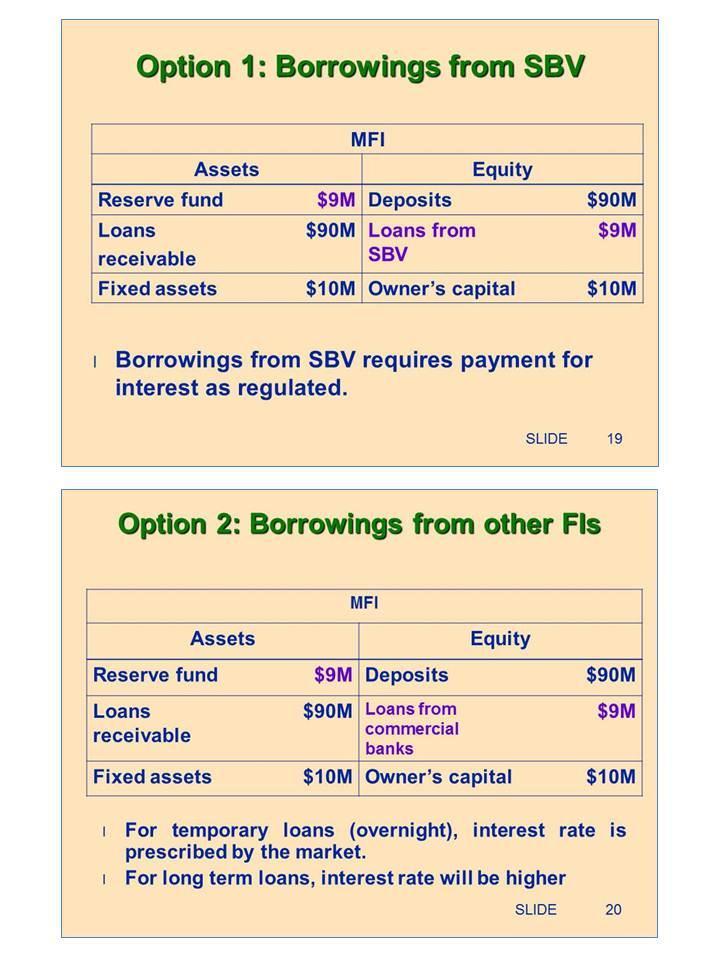

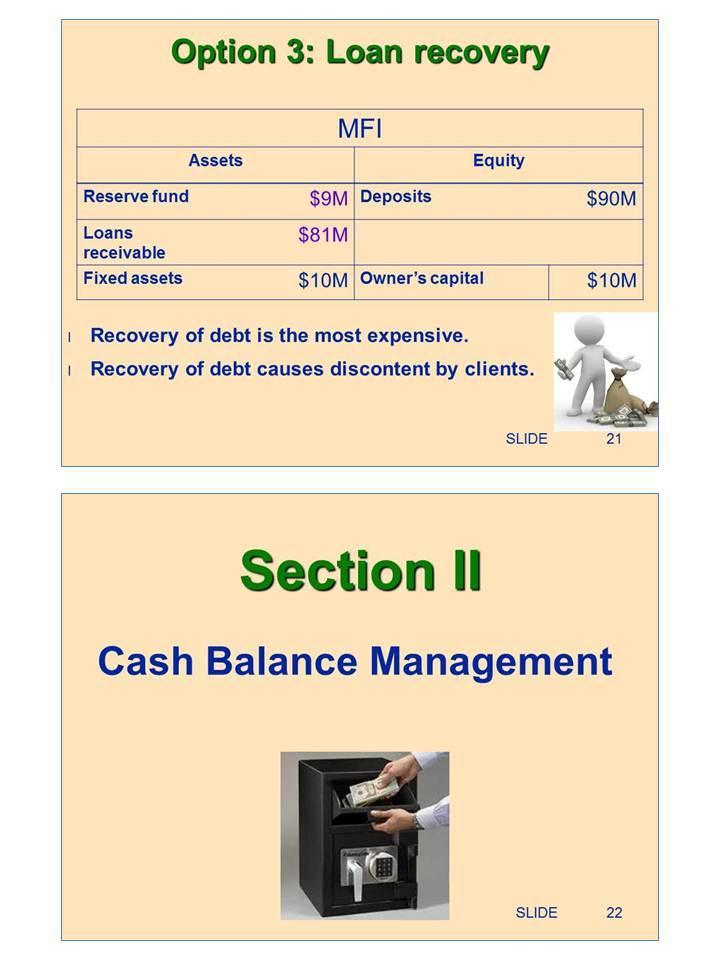

8 Management of Liquidity (solvency) and cash to ensure sufficient cash and equivalent assets to pay the depositors, to comply with reserve requirements; Management of assets to diversify portfolio to maximize income from interest; Management of Liabilities and Assets to balance the gap and Assets maturity; Management of Capital Adequacy Ratio to ensure the CAR as regulated by SBV Management of capital resources in relation with financial risks c. Then the lead trainer asks the participants how financial management relates to items on the balance sheet. The lead trainer summarizes the responses of the participants on a flipchart. d. The lead trainer then explains to the participants the relationship, the critical areas, and the need to manage the financial results and risks to achieve financial sustainability. e. The lead trainer asks the participants if there are questions at this point. If there are no questions, the lead trainer thanks the participants and moves to the next activity. PART II THE ADVANCE FINANCIAL MANAGEMENT FOR MFIS Session 1 Review of Financial Management Activity 5 Liquidity Management Purpose To review the concepts of liquidity management and provision management in MFIs. Objectives By the end of the activity, the participants are able to: Refresh understanding of liquidity management and provisioning as stated in the SBV Circular. Time: Materials: Steps/Method: 60 minutes Computer, PPT Slide 7-21, Flipcharts, Pens, Stands, Tapes, LCD Projector Slide Presentation; Large Group Discussions 1. The lead trainer conducts a review of the participants understanding of liquidity and the importance of managing liquidity. The trainer lists down the response on the flipchart. The responses may include: to meet payment obligations, maintain good image, continued service to clients, etc., 2. The lead trainer summarizes the responses and emphasizes that No liquidity means bankruptcy for MFIs. 3. The lead trainer then asks the participants their understanding of liquidity risk. The lead trainer summarizes the responses from participants and concludes the session with the presentation. 7

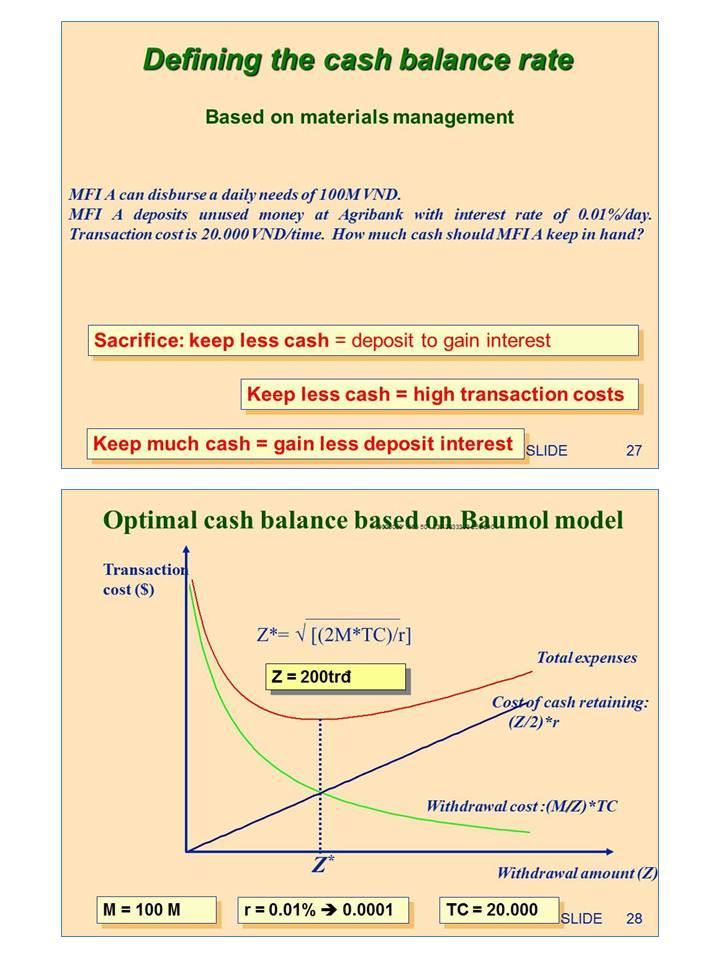

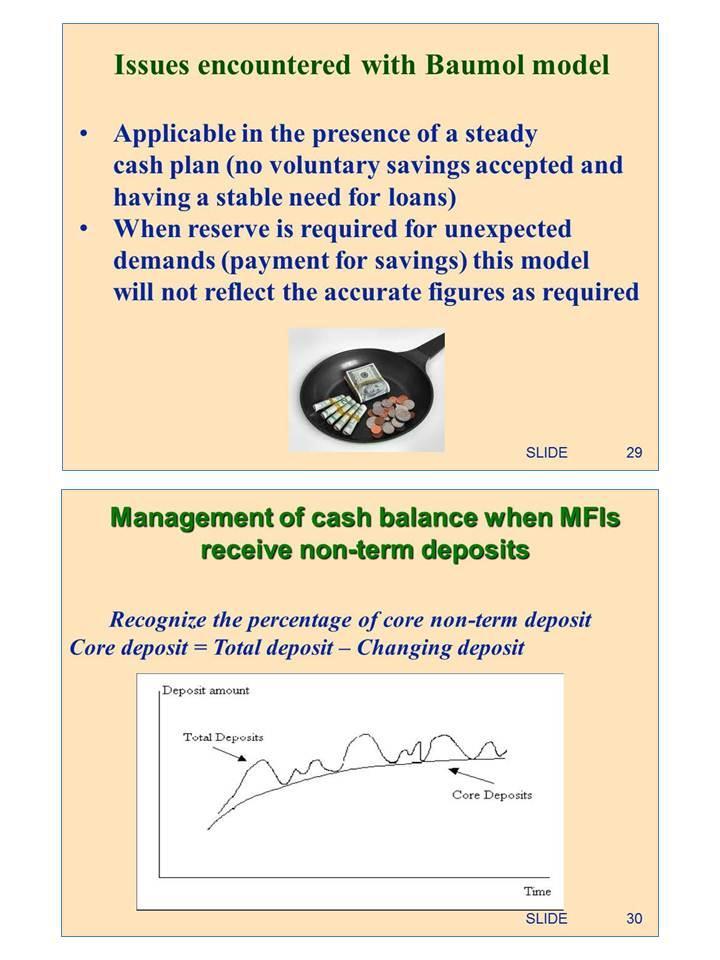

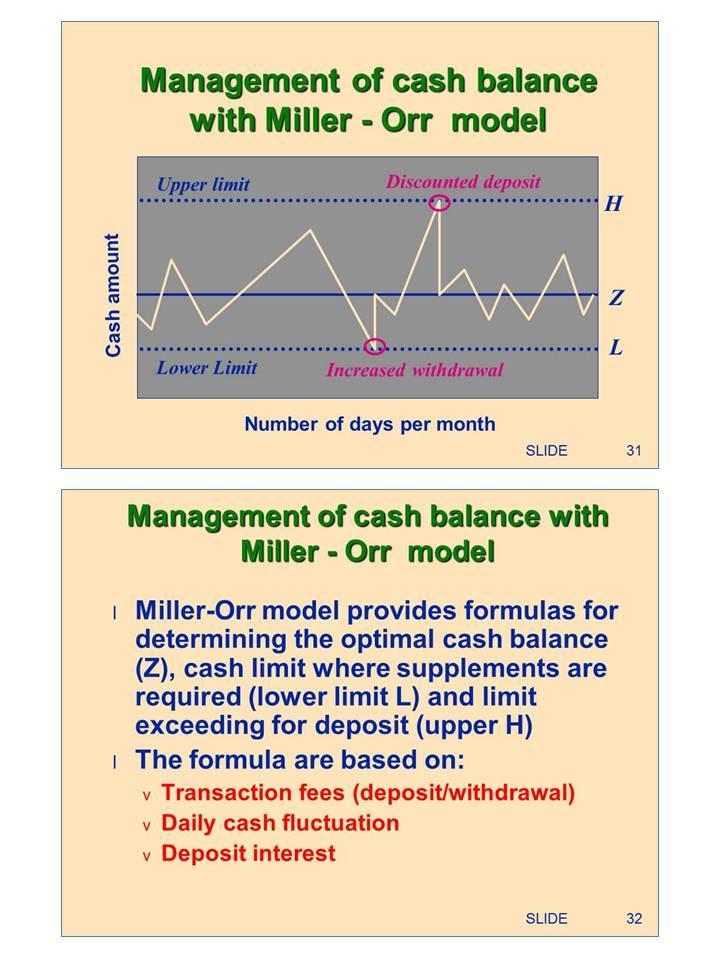

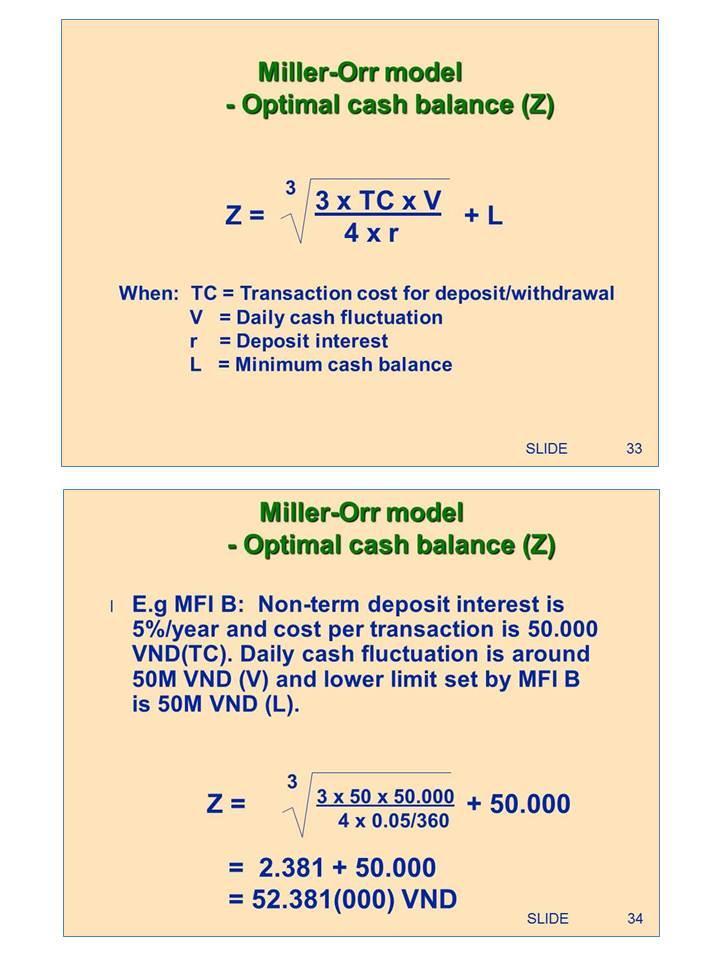

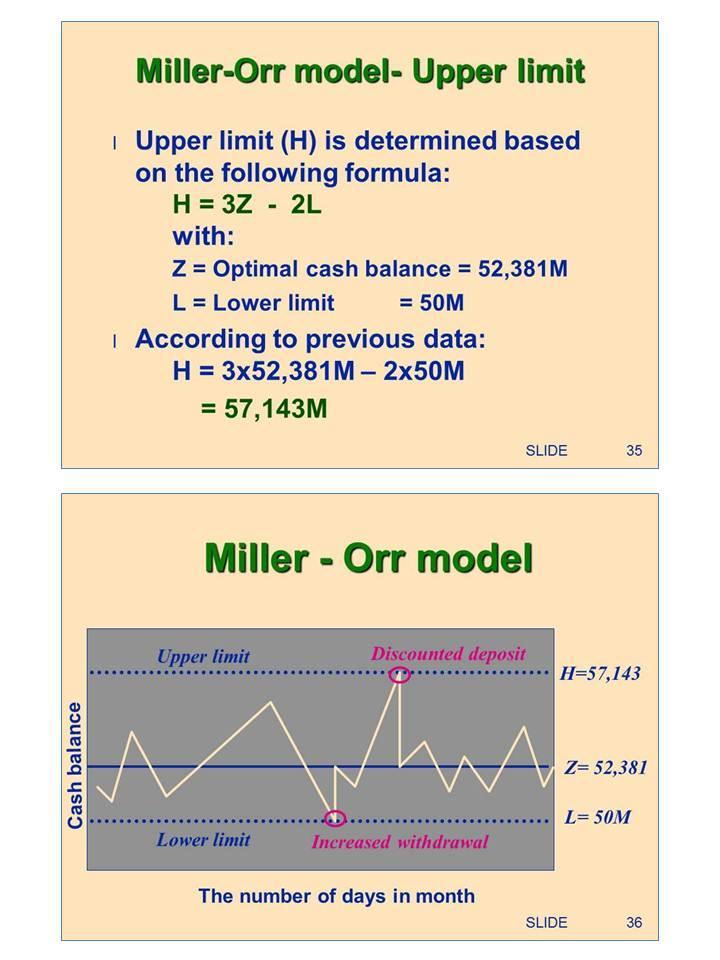

9 4. The lead trainer reminds the participants the liquidity reserve requirements from SBV. The lead trainer further explains the effect of the requirements to a regulated MFI (such as TYM) compared to a non-regulated MFI. 5. The lead trainer asks the participants the minimum level of liquidity maintained in their MFIs. The lead trainer acknowledges the practices of the MFIs and lists them down on a flipchart. The lead trainer emphasizes that: Most MFIs do not apply or do not care about liquidity management because they are not regulated, but when an MFI is licensed like TYM, the MFI has to adhere to the SBV regulations otherwise it may be foreclosed. 6. The lead trainer then asks the participants their understanding of compulsory reserve. The lead trainer summarizes the responses and emphasizes that: Compulsory reserve is the amount required by SBV to protect the MFI from liquidity risks. 7. The lead trainer further explains to the participants that importance of having sufficient reserves by using example of an MFI. 8. The lead trainer asks the participants to analyze the case and provide recommendations to address the MFI s problem. 9. The lead trainer lists down the points raised by the participants on a flipchart. The lead trainer then summarizes the responses and validates appropriate solutions to the participants. 10. The lead trainer asks the participants if there are questions. If there are no questions, the lead trainer thanks the participants and moves to the next activity. PART II THE ADVANCE FINANCIAL MANAGEMENT FOR MFIS Session 1 Review of Financial Management Activity 6 Treasury Management Purpose To review the concepts of treasury management in MFIs. Objectives By the end of the activity, the participants are able to: Refresh understood of treasury management in MFIs. Time: Materials: Steps/Method: 90 minutes Computer, PPT Slide 22-36, Flipcharts, Pens, Stands, Tapes, LCD Projector Plenary 1. The lead trainer conducts a review of the participants understanding of cash balance management. The lead trainer summarizes the responses from participants and emphasizes that: Effective cash balance management is operating with a reasonable amount of cash only. 2. The lead trainer then asks the participants the purpose of managing cash balance. The lead trainer summarizes the responses from the participants and emphasizes that it is import: To ensure meeting the 8

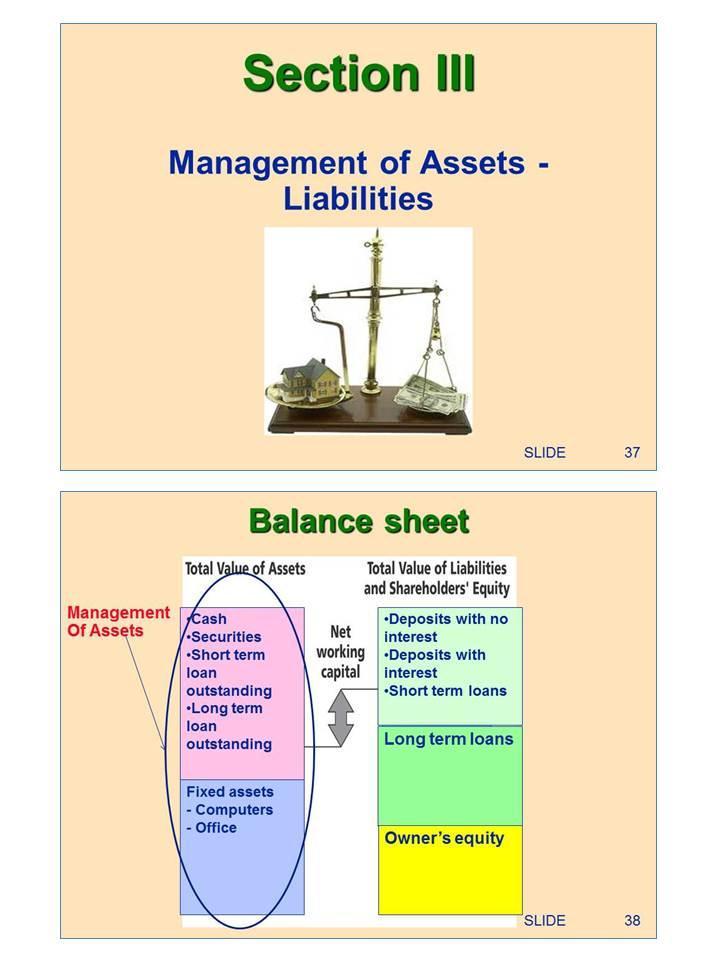

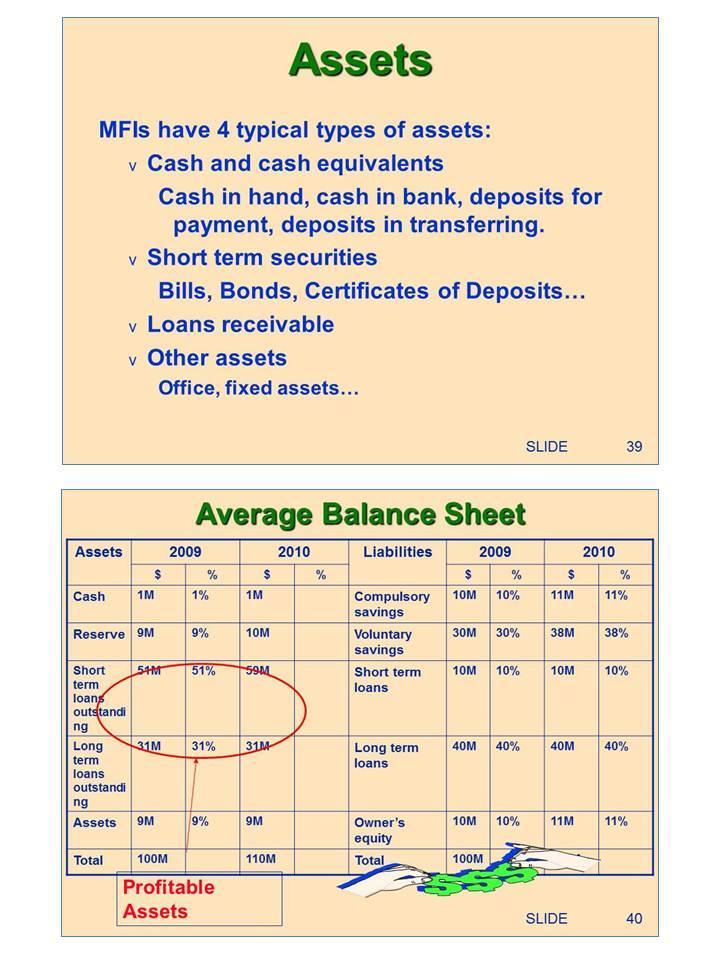

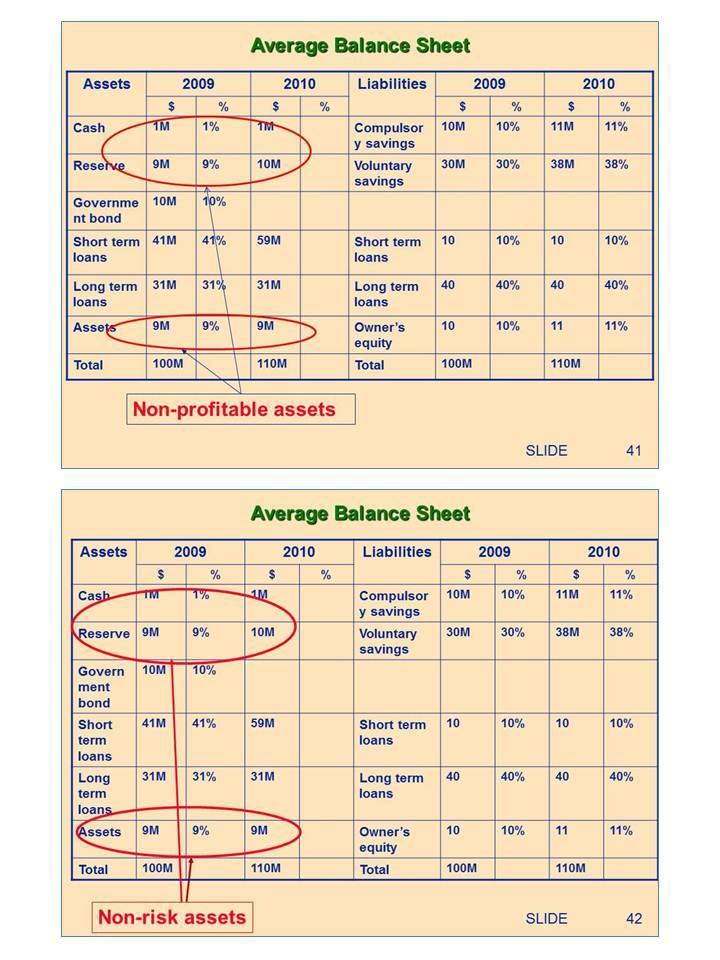

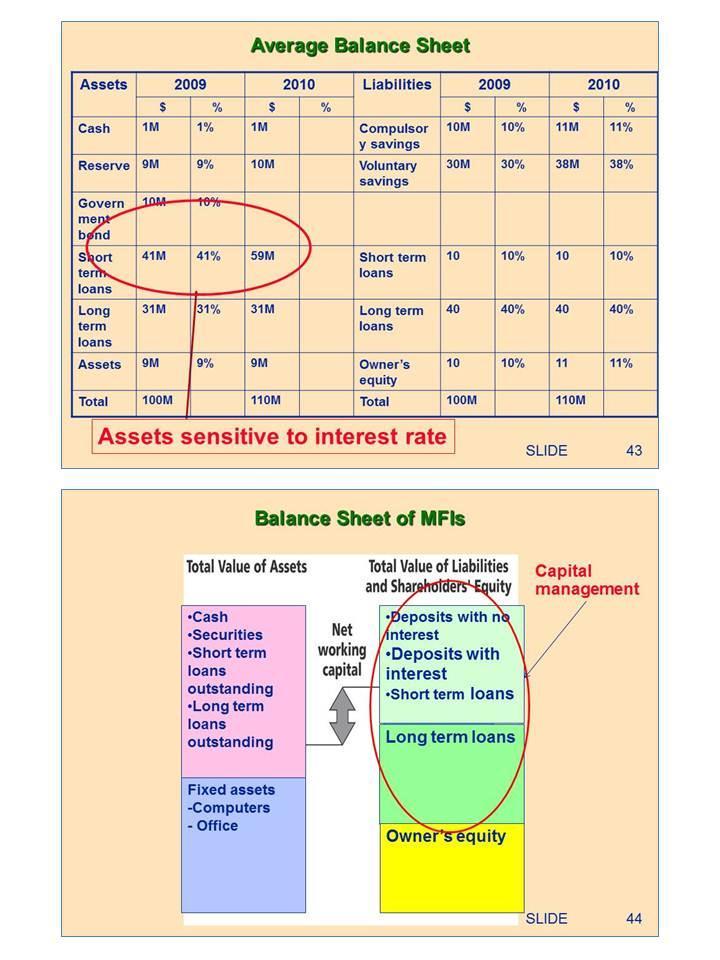

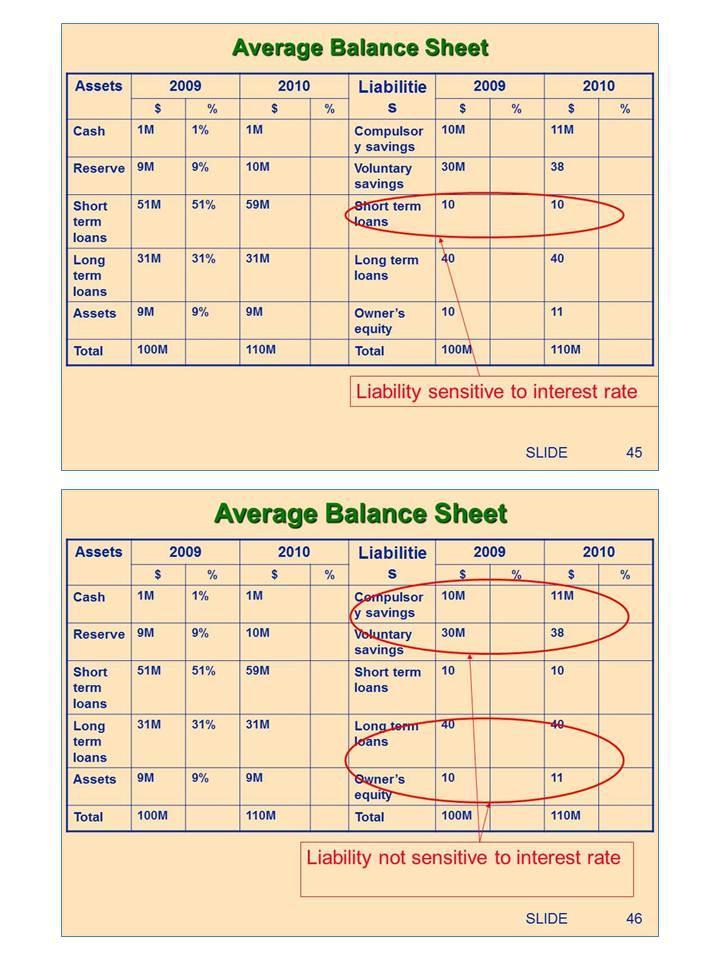

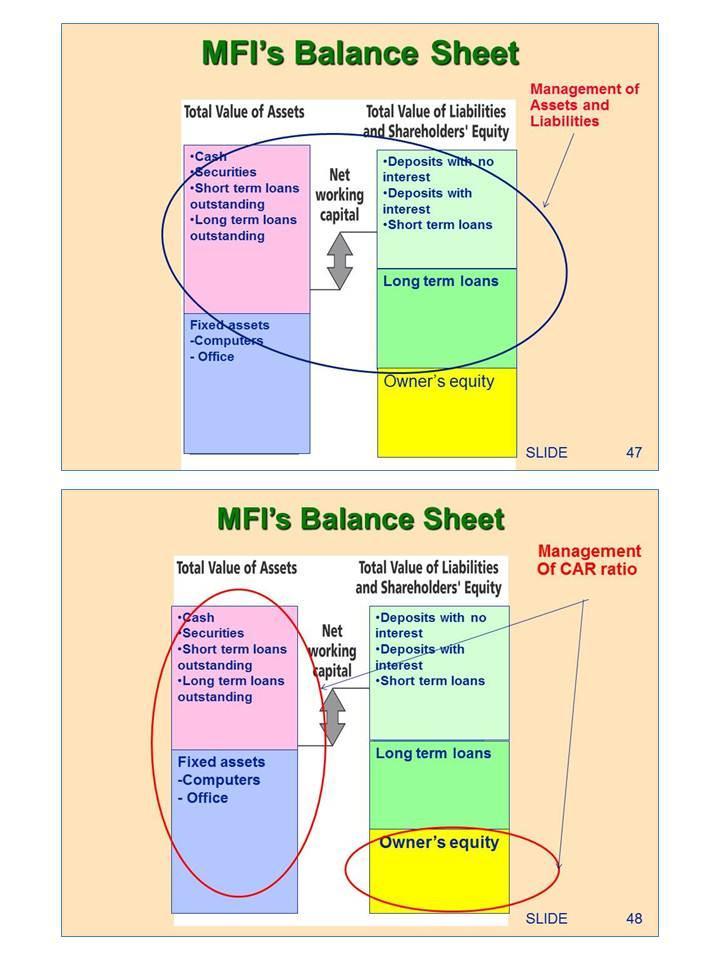

10 daily/weekly payment demands; and To ensure meeting any unexpected demands. 3. The lead trainer then asks the participants the process of determining cash balance. The lead trainer lists down and summarizes the responses from the participants and concludes with the presentation of the processes involved in determining cash balances, trade offs in earnings from investments and sample cash models like the Baumol and Miller-Orr Model. 4. The lead trainer then asks the participants to calculate the effective balance in cash amount base on data provided using the Baumol Model and then compare costs of withdrawing money from deposit accounts and interest earned from deposit accounts. 5. The lead trainer then walks the participants through the process of the exercise, to ensure that all participants are on the same page, and concludes the session 6. The lead trainer asks the participants if there are questions. If there are no questions, the lead trainer thanks the participants and moves to the next activity. PART II THE ADVANCE FINANCIAL MANAGEMENT FOR MFIS Session 1 Review of Financial Management Activity 7 Asset Liability Management Purpose To review the concepts of asset-liability management in MFIs. Objectives By the end of the activity, the participants are able to: Refresh understanding and practice asset-liability management in MFIs. Time: Materials: Steps/Method: 60 minutes Computer, PPT Slide 37-47, Flipcharts, Pens, Stands, Tapes, LCD Projector Plenary; 1. The lead trainer conducts a review of the participants understanding of assets and its position in the balance sheet. The lead trainer summarizes the responses from the participants and emphasizes that: MFIs have 4 typical types of assets as follows: a. Cash and cash equivalents: Cash in hand, cash in bank, deposits for payment, deposits in transferring. b. Short term securities: Bills, Bonds, Certificates of Deposits c. Loans receivables d. Other assets: Office, fixed assets. 2. The lead trainer then explains the classification of assets as follows: Profitable Assets; Non-profitable assets; Non-risk assets; and Assets sensitive to interest rate. 3. The lead trainer asks the participants to analyze a sample of MFI financial statement and categorize their assets. The lead trainer provides the participants about 15 minutes to discuss. 4. The lead trainer asks volunteer participants to share 9

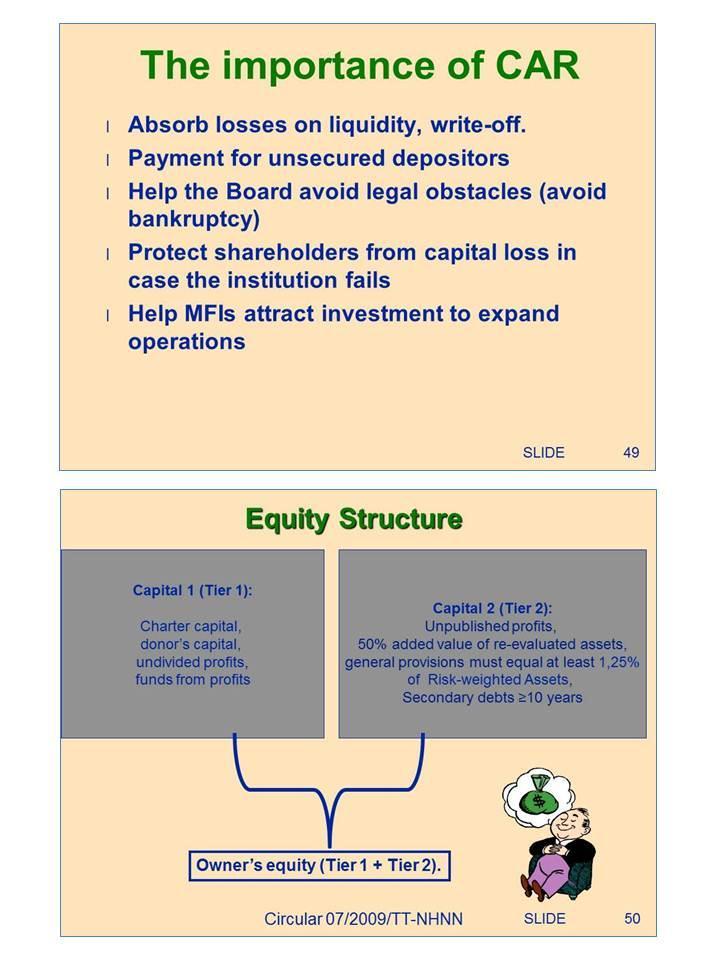

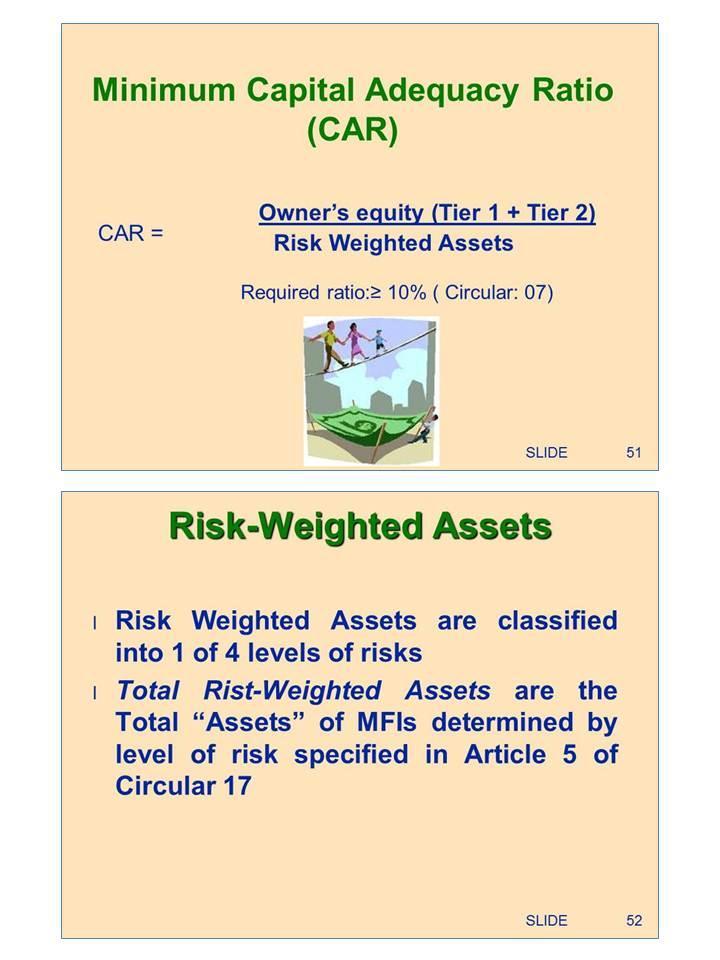

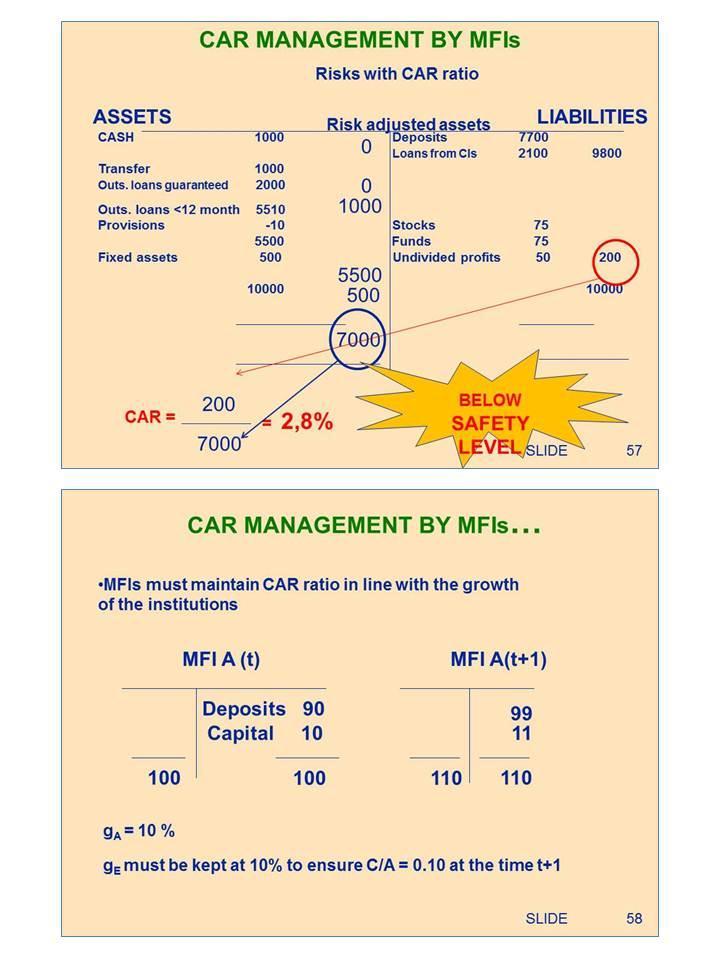

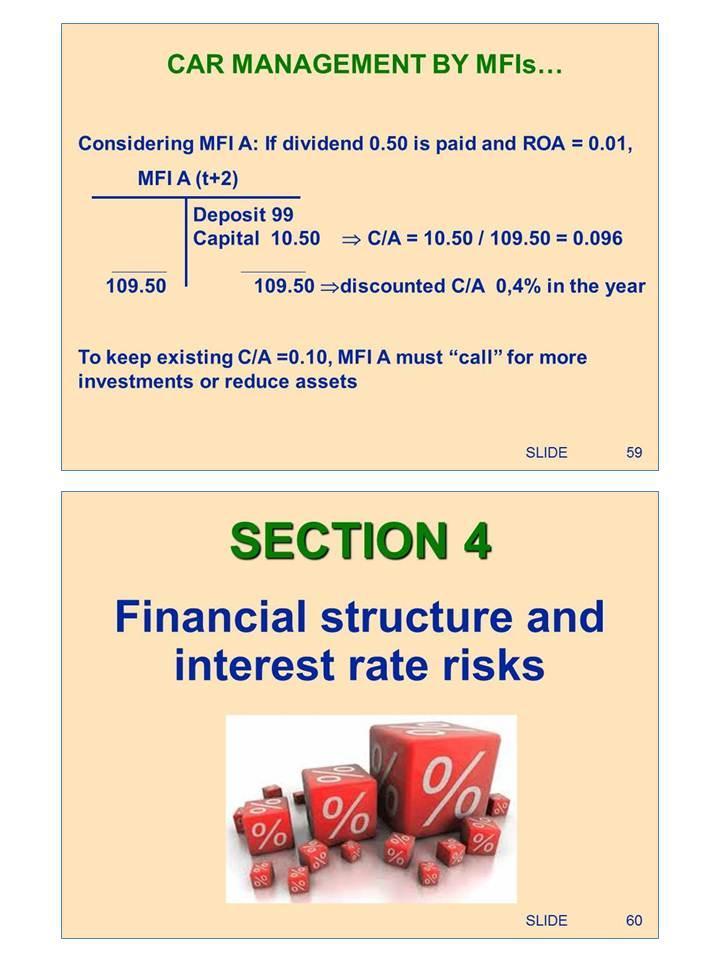

11 their outputs while others observe and provide feedback. The lead trainer summarizes the points raised by the participants and ensures that all participants are on the same page. 5. The lead trainer concludes the discussion and asks the participants if there are questions. If there are no questions, the lead trainer thanks participants and moves to the next topic. 6. The lead trainer conducts a review of the participants understanding of liability and its position in the balance sheet. 7. The lead trainer summarizes the response and emphasizes that: Liabilities are Deposits with no interest; Deposits with interest; Short term loans; and Long term loans. 8. The lead trainer asks the participants which liabilities are sensitive to interest rate and those not sensitive to interest rate. 9. The lead trainer validates the responses form the participants and concludes the discussion with the presentation on effective ways to manage assets and liabilities. 10. The lead trainer then asks the participants if there are questions. If there are no questions, the lead trainer thanks participants and moves to the next activity PART II THE ADVANCE FINANCIAL MANAGEMENT FOR MFIS Session 1 Review of Financial Management Activity 8 Capital Adequacy Ratio (CAR) Management Purpose To review concepts of CAR management in MFIs. Objectives By the end of the activity, the participants are able to: Refresh understanding and practice capital adequacy ratio management in MFIs. Time: Materials: Steps/Method: 90 minutes Computer, PPT Slide 48-59, Flipcharts, Pens, Stands, Tapes, LCD Projector Handout: SBV Circular No. 07 and 015 Plenary; Small Group Discussions; Exercises 1. The lead trainer conducts a review of the participants understanding of CAR. 2. The lead trainer summarizes responses from the participants and emphasizes on the importance as follows: Absorbs losses on liquidity, write-off. Payment for unsecured depositors Helps the Board avoid legal obstacles (avoid bankruptcy) Protects shareholders from capital loss in case the institution fails Helps MFIs attract investment to expand operations 3. The lead trainer reviews with the participants the formula in calculating CAR as specified in SBV Circular 10

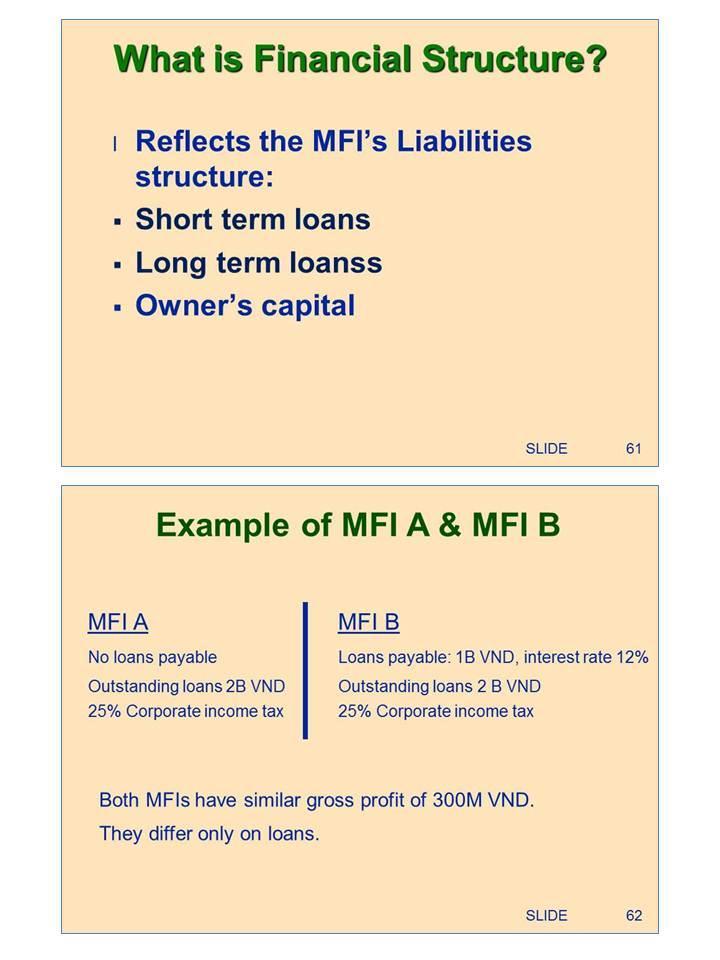

12 No. 07 and Circular No. 015 to ensure that all participants are on the same page. 4. The lead trainer emphasizes to participants that: In general, the higher the ratio the safer and sounder the MFI is. Well capitalized MFIs generally require less supervisory attention. Capital is paramount to regulators, in other words capital is king! Capital is the cushion that protects the MFI clients and owners from operating losses, unforeseen events, economic downturns and insolvency. The standard ratio is greater than or equal to 10%. A low or decreasing ratio can be cause for concern and should trigger additional analysis by the examiner. 5. To deepen the participants understanding, the lead trainer walks the participants through an example of calculation. The lead trainer asks how much is the minimum acceptable ration for the MFIs and compares that with the example. 6. The lead trainer then asks the participant if there are questions on the discussions. If there are no questions, the lead trainer moves to the next activity, an exercise. 7. The lead trainer asks the participants to form five groups. The lead trainer provides the groups a case study of MFI situation and asks the groups to calculate CAR. 8. The lead trainer provides the groups 30 minutes for discussions and another 5 minutes for the presentation of results. 9. The lead trainer asks two volunteer groups to present while others observe and provide their feedback. 10. The lead trainer summarizes the points raised and validates the appropriate responses to ensure that all participants are on the same page. 11. The lead trainer asks the participants if there are questions. If there are no questions, lead trainer thanks the participants and move to the next activity. PART II THE ADVANCE FINANCIAL MANAGEMENT FOR MFIS Session 2 Financial Structure and Interest Rate Risk Management Activity 9 Financial structure Purpose To introduce the concept of financial structure of MFIs. Objectives By the end of the activity, the participants are able to: Understand the concepts and practice analyzing financial structure of MFIs. Time: Materials: Steps/Method: 90 minutes Computer, PPT Slide 60- Plenary 1. The lead trainer asks the participants which items in the 63, Flipcharts, balance sheet contribute to income and which Pens, Stands, contribute to expenditure in MFIs. 11

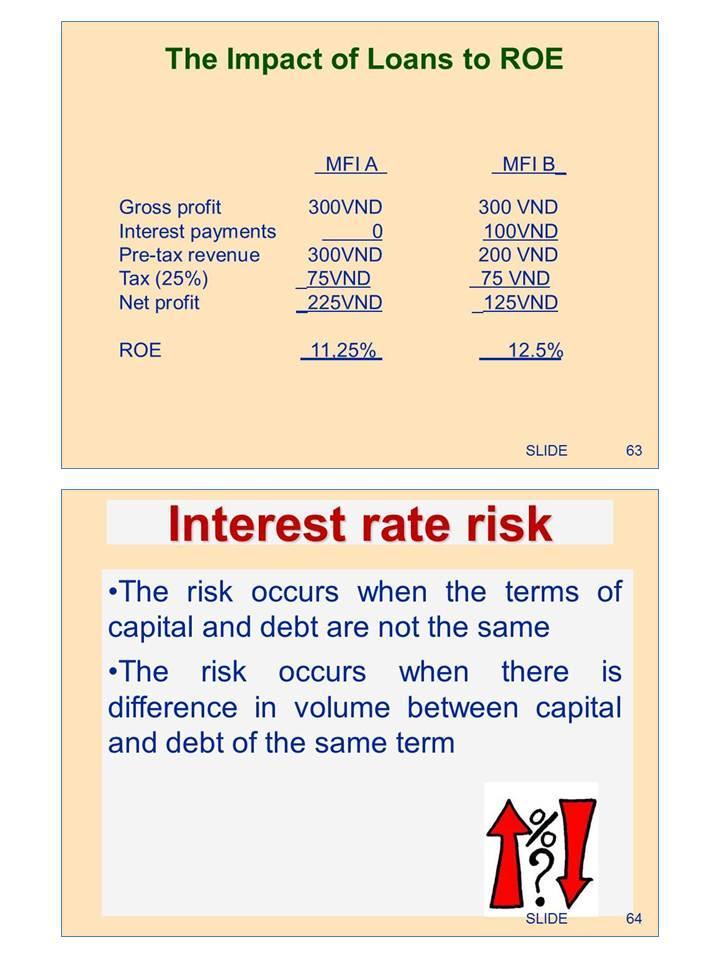

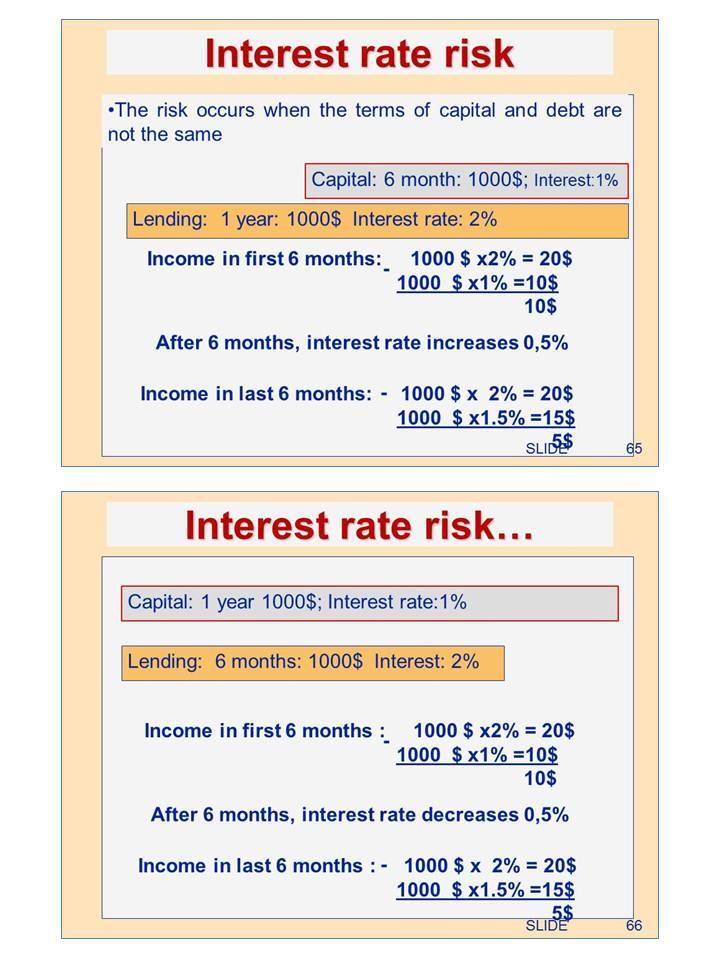

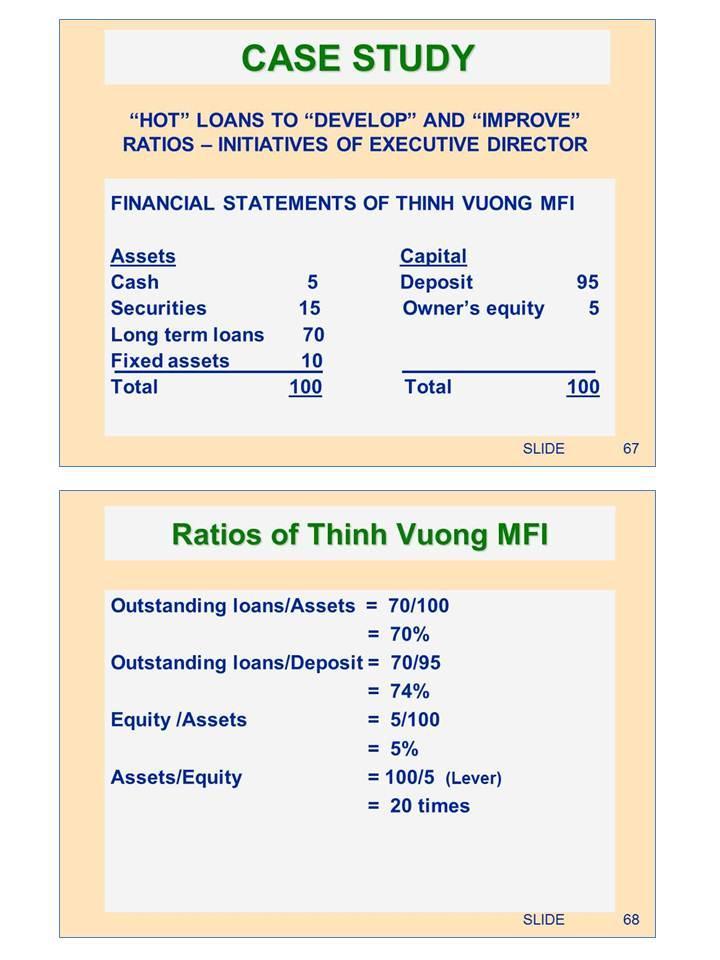

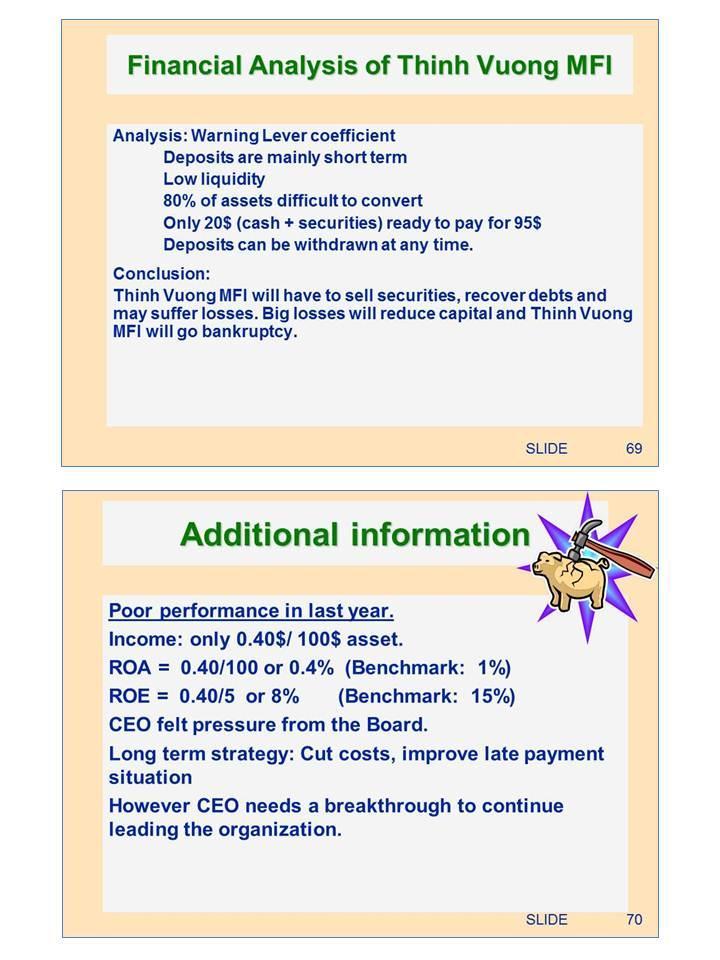

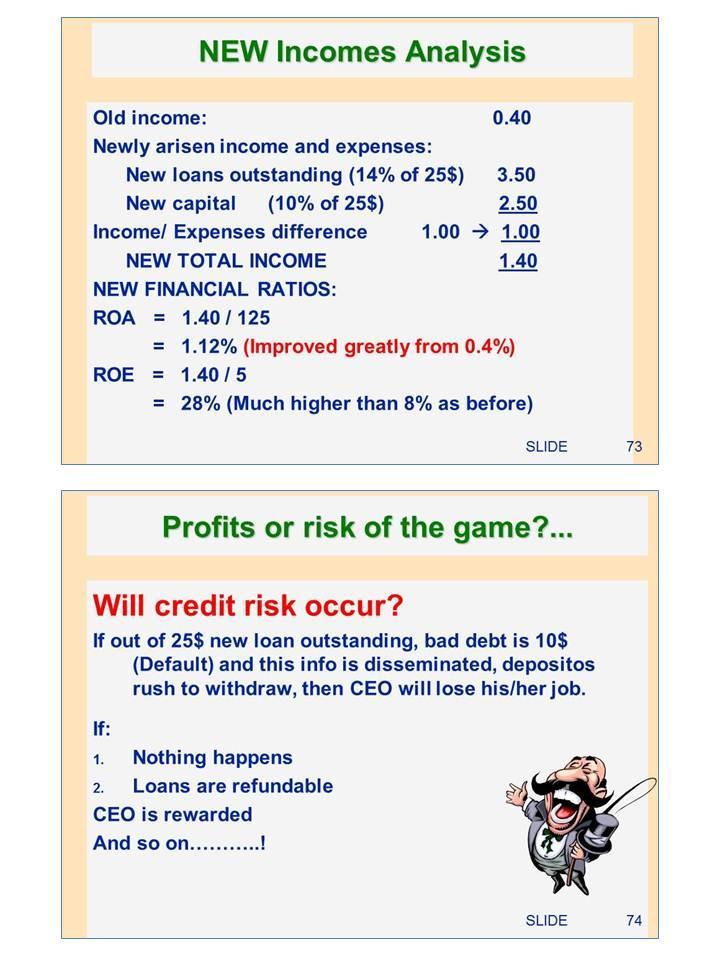

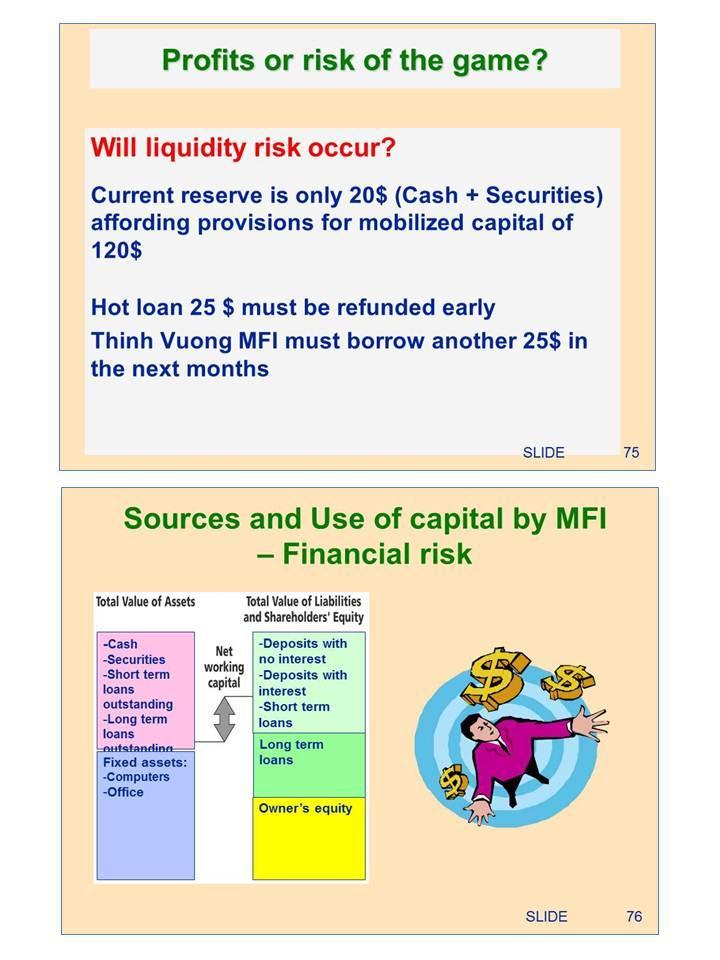

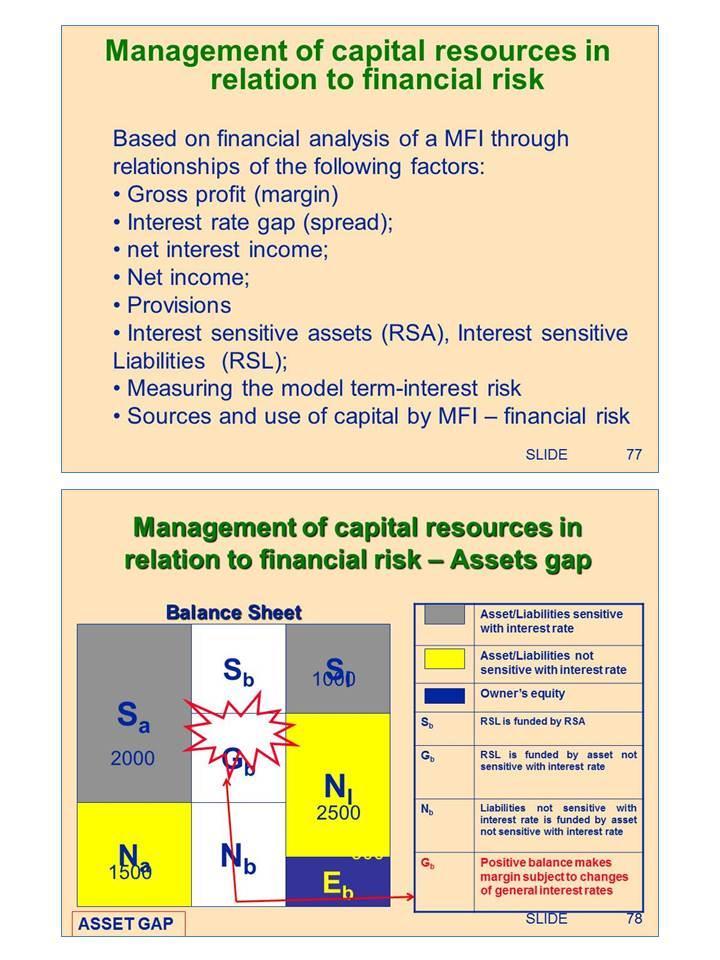

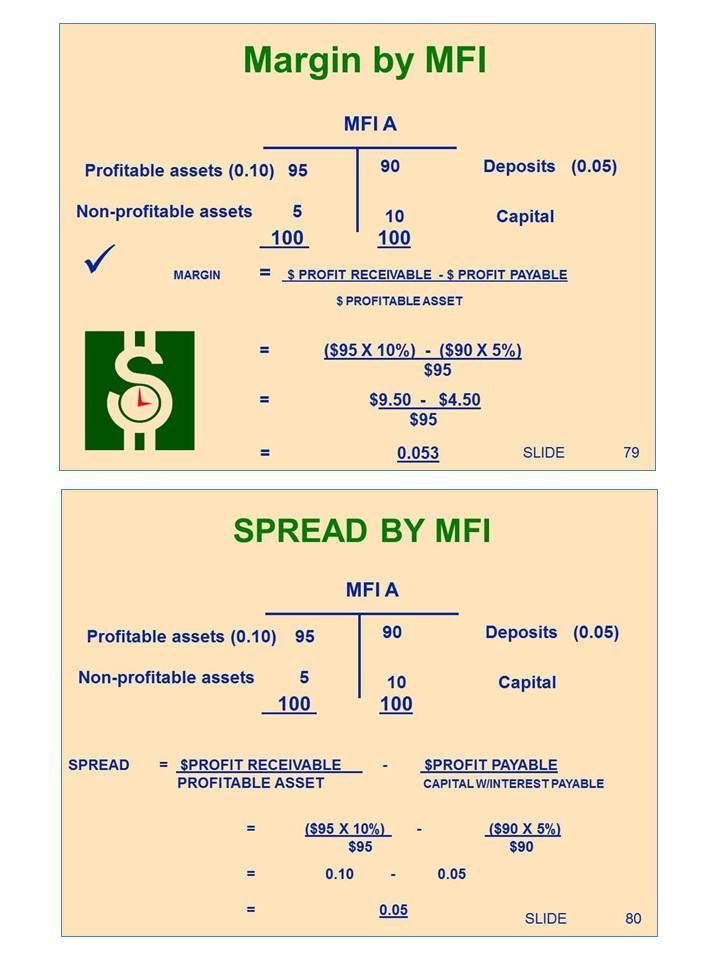

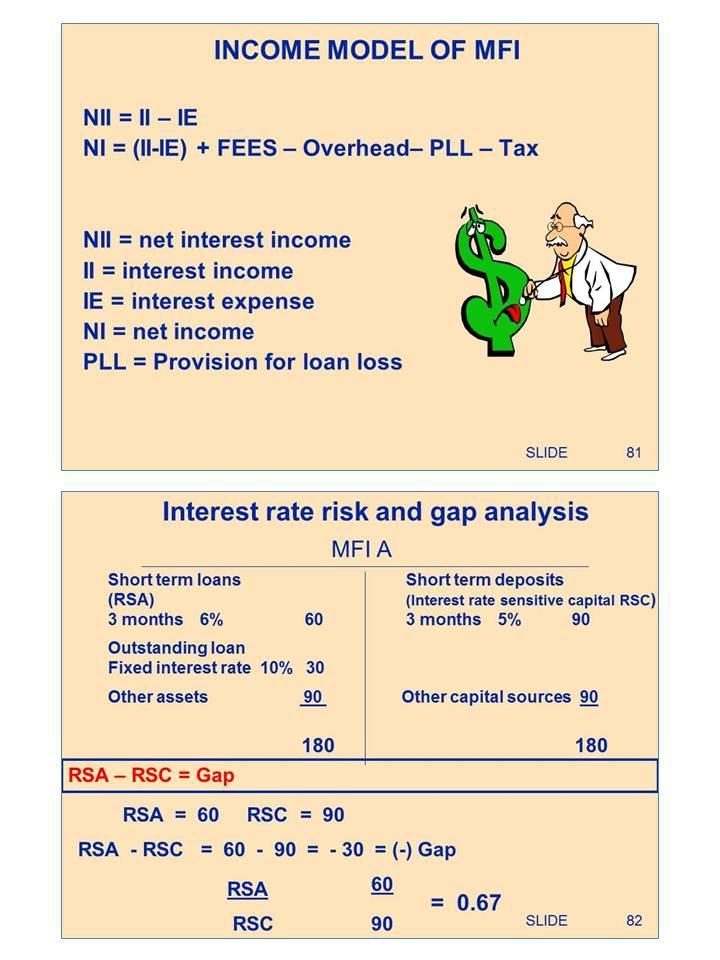

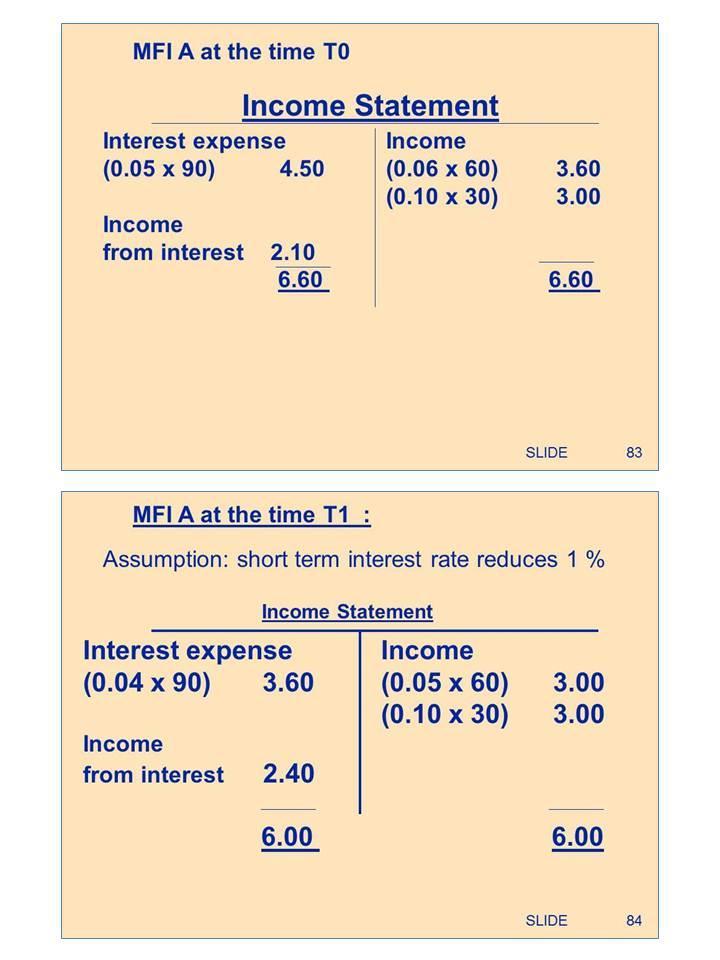

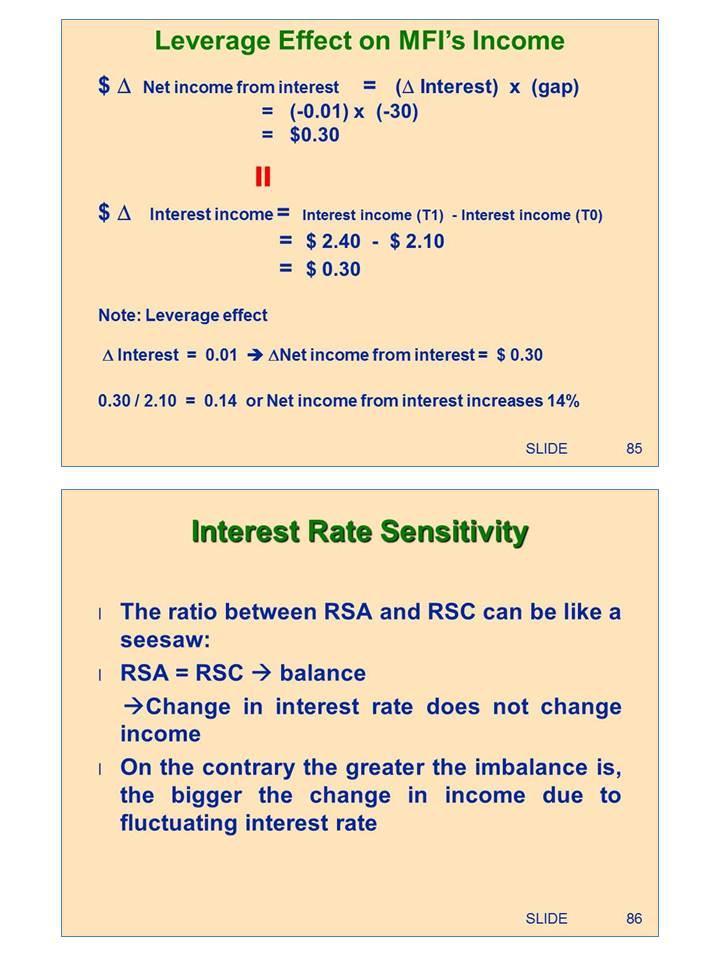

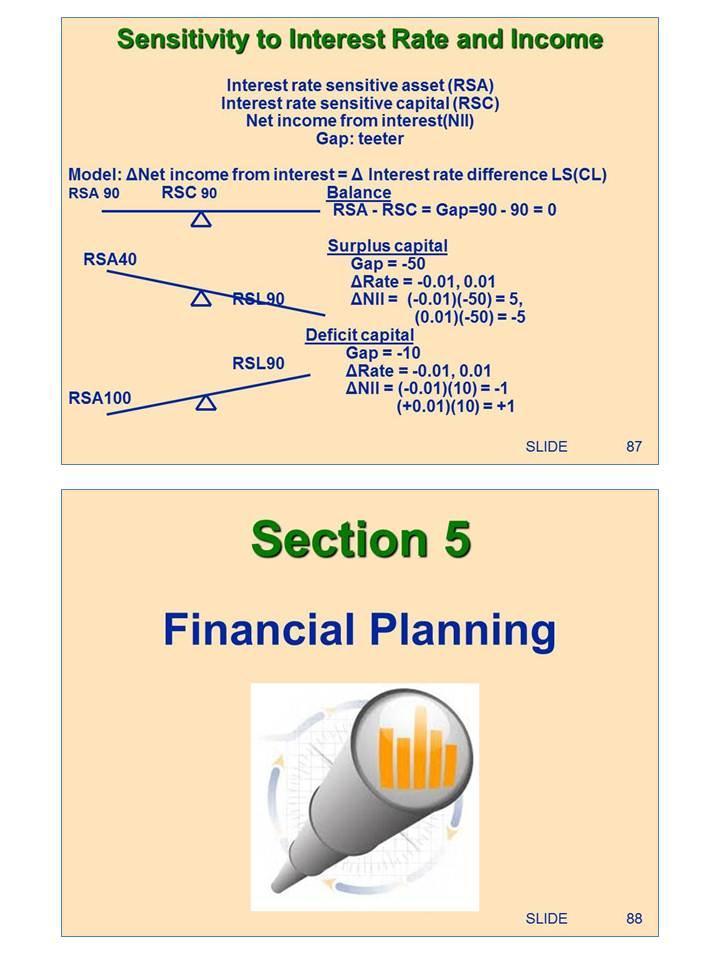

13 Tapes, LCD Projector, MFI Financial Reports 2. The lead trainer lists down responses on a flipchart. The responses may include: main income source is outstanding loan and deposit in bank account; expenditure is short term loans, long term loan, owner s capital, etc. 3. The lead trainer acknowledges the responses and concludes the discussions on the effective financial structure for an MFI and the impact of interest rate to the financial structure by showing examples of MFI financial structures. 4. The lead trainer then asks the participants to do the same using a different sample MFI. The lead trainer guides the participants through the process to ensure that all participants are on the same page. 5. The lead trainer then asks participants if there are questions. If there are questions, the lead trainer thanks the participants and move to the next activity. PART II THE ADVANCE FINANCIAL MANAGEMENT FOR MFIS Session 2 Financial Structure and Interest Rate Risk Management Activity 10 Interest Rate Risk Management Purpose To introduce the concept of interest rate risk management in MFIs. Objectives By the end of the activity, the participants are able to: Understand the concepts and practice interest rate risk management in MFIs. Time: Materials: Steps/Method: 90 minutes Computer, PPT Slide 64-79, Flipcharts, Pens, Stands, Tapes, LCD Projector Handout: TYM Case Study Plenary; Exercises 1. The lead trainer asks the participant their understanding of interest rate risk. 2. The lead trainer summarizes responses and emphasizes that: The risk occurs when the terms of capital and debt are not the same.; The risk occurs when there is difference in volume between capital and debt of the same term. 3. To deepen their understanding, the lead trainer walks the participants through an example of interest rate risk. The lead trainer uses the case of using high interest rate on loans to improve financial ratios 4. The lead trainer asks the participants if there questions on the case study to ensure that all participants are on the same page. If there are no questions, the lead trainer continues with the discussions. 5. The lead trainer explains to the participants the management of capital resources in relation to financial risk and emphasizes the need to do financial analysis based on the relationships of the following factors: a. Gross profit (margin) b. Interest rate gap (spread); c. net interest income; 12

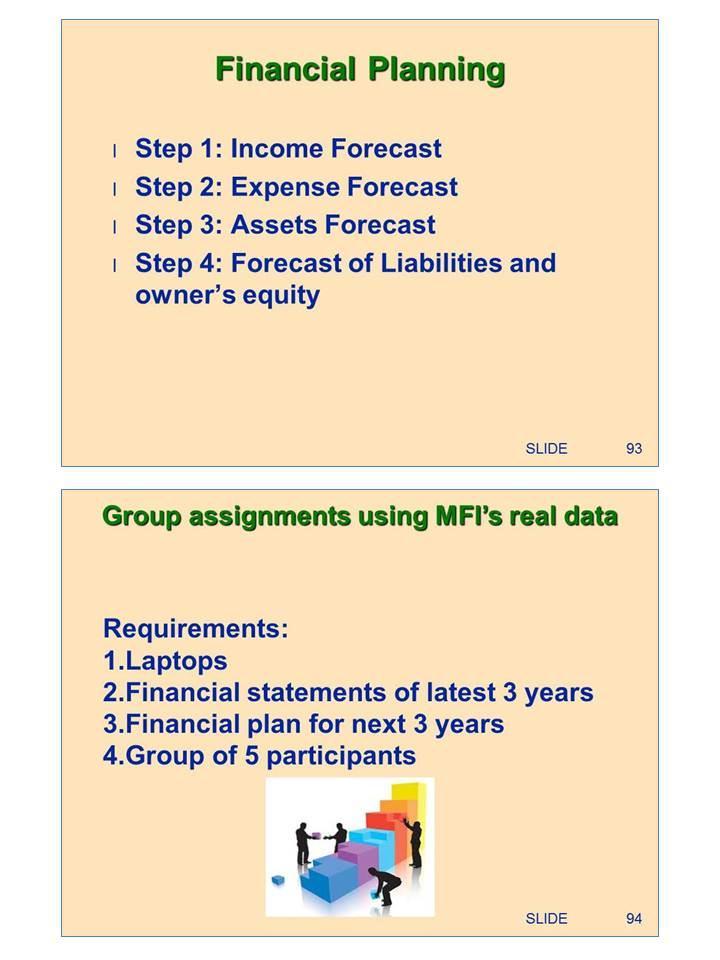

14 PPT Slide d. Net income; e. Provisions f. Rate sensitive assets (RSA), Rate-sensitive Liabilities (RSL); g. Measuring the model term-interest risk h. Sources and use of capital by MFI financial risk 6. The lead trainer then asks participant if there are questions. If there are no questions, the lead trainer thanks the participants and moves to the next activity, an exercise. 7. The lead trainer asks the participants to calculate the following using the sample MFI data: a. Spread of interest b. Interest rate risk and gap analysis c. Leverage effect on MFI s income d. Sensitivity to interest Rate and Income 8. The lead trainer walks the participants through the process and calculates the items above together to ensure that the all participants understand and are on the same page. 9. The lead trainer asks the participants if there are questions. If there no questions, the trainer thanks the participants and moves to the next activity. PART II THE ADVANCE FINANCIAL MANAGEMENT FOR MFIS Session 3 Understanding Financial Planning Activity 11 Development of Financial Plans for MFIs Purpose To introduce the concepts and practice financial planning in MFIs. Objectives By the end of the activity, the participants are able to: Understand and practice financial planning in MFIs. Time: Materials: Steps/Method: 180 minutes Computer, PPT Slide 88-92, Flipcharts, Pens, Stands, Tapes, LCD Projector Handout: Financial Planning Model Handout: Guidelines for Financial Planning Participant Plenary; Small Group Discussion; Exercises 1. The lead trainer asks the participants their understanding of financial planning process. 2. The lead trainer summarizes responses and emphasizes the importance such as: Financial planning is required to realize the strategy and is part of the strategic implementation plan. 3. The lead trainer asks the participants to form five groups and discuss following questions: a. What resources (financial, technical, human resources etc..) are needed to realize the strategy? b. What resources are available? c. Is it necessary to recruit and train new staff? d. Is it necessary to reallocate resources to implement the strategy? If yes, how? e. In consideration of resources availability, is it necessary to revise the strategy? 13

15 Requirements: - Laptops - Financial Statements for the last 3 years - Financial Plans for next 3 years 4. The lead trainer provides 15 minutes for the participants to discuss the exercise and another 5 minutes to present their outputs. 5. The lead trainer asks for one volunteer group to present while the others observe and provide feedback. 6. The lead trainer summarizes the points raised and concludes the discussions with the presentation of the financial planning model and the four steps as follows: Step 1: Income Forecast Step 2: Expense Forecast Step 3: Assets Forecast Step 4: Forecast of Liabilities and owner s equity 7. The lead trainer asks participants if there are questions at this point. If there are no questions, the lead trainer moves to the next activity, an exercise. 8. The lead trainer asks the participants to form five groups and prepare a financial plan for the MFI following the steps discussed and based on the data at hand. 9. The lead trainer provides 90 minutes for the groups to prepare the financial plan and another 15 minutes to present. 10. The lead trainer asks for a volunteer group to present while the others observe and provide feedback. 11. The lead trainer summarizes the points raised and concludes the discussions. 12. The lead trainer asks the participants if there are questions. If there are no questions, the lead trainer thanks the participants and moves to the next activity. PART IV CLOSING ACTIVITIES SESSION 1 Wrap Up and Evaluations Activity 12 Evaluations Purpose To validate whether the training objectives have been met. Objectives By the end of the activity, the participants are able to: Validate achievement of the training objectives, participants training expectations, and resolve parking lot issues. Complete the evaluation form. Time: Materials: Steps/Method: minutes Pens, Agenda, PPT Slide 3, Computer, LCD Projector Evaluation Forms Plenary; Post Training Evaluation 1. The support staff distributes the evaluation forms to the participants and asks them to fill up the form. 2. The support staff provides a short explanation on the content and how the form should be filled up by the participants. 3. The support staff collects the forms from the participants. 1. The training coordinator reviews the training objectives against the learning experiences of the participants along with their expectations from the training. 14

16 2. The training coordinator reviews the issues listed in the parking lot, if any and tries to resolve such issues. 3. The training coordinator asks the participants if they want to share anything to the group. 4. The lead trainer asks the participants if all is clear. If there are no questions, the lead trainer thanks the participants and moves to the next activity. PART III CLOSING ACTIVITIES SESSION 1 Closing Activity 13 Closing Remarks Purpose To officially mark the end of the training. Objectives By the end of the activity, the participants are able to: Complete the requirements of the training. Receive the certificate of completion. Time: Materials: Steps/Method: minutes Certificates Plenary 1. The training coordinator requests the representatives of host institutions (e.g. ADB, SBV) to deliver the closing remarks. 2. The training coordinator thanks all the people that supports the delivery of the training (ADB, SBV, PMU, MFI, others) and thanks the participants for the hard work and active participation. 3. The hosts organization representatives issue the certificate of completion to the participants. 4. The host, trainers and participants pose for the group picture. 15

17 PRESENTATION MATERIAL 16

18 17

19 18

20 19

21 20

22 21

23 22

24 23

25 24

26 25

27 26

28 27

29 28

30 29

31 30

32 31

33 32

34 33

35 34

36 35

37 36

38 37

39 38

40 39

41 40

42 41

43 42

44 43

45 44

46 45

47 46

48 47

49 48

50 49

51 50

52 51

53 52

54 53

55 54

56 55

57 56

58 57

59 58

60 59

61 60

62 61

63 62

64 HANDOUTS Handout 1 SBV Circular No. 07 STATE BANK SOCIALIST REPUBLIC OF VIETNAM OF VIETNAM Independence Freedom Happiness No. 07/2009/TT-NHNN Hanoi, 17 April 2009 CIRCULAR OF GOVERNOR OF THE STATE BANK OF VIETNAM Providing for prudential ratios in operation of small scaled financial institutions Pursuant to the Law on the State Bank of Vietnam No. 01/1997/QH10 issued in 1997 and the Law on the amendment, supplement of several Articles of the Law on the State Bank of Vietnam No. 10/2003/QH11 issued in 2003; - Pursuant to the Law on the Credit Institutions No. 02/1997/QH10 issued in 1997 and the Law on the amendment, supplement of several Articles of the Law on the Credit Institutions No. 20/2004/QH11 issued in 2004; - Pursuant to the Decree No.178/2007/ND-CP dated 03/12/2007 of the Government providing for the functions, duties, authorities and organizational structure of the Ministries, Ministerial level agencies; - Pursuant to the Decree No. 28/2005/ND-CP dated 09/03/2005 on the organization and operation of small scaled financial institutions operating in Vietnam and the Decree No.165/2007/ND-CP dated 15/11/2007 on the amendment, supplement, abrogation of several articles of the Decree No.28/2005/ND-CP, The State Bank of Vietnam (hereinafter referred to as the State Bank) hereby provides for prudential ratios in operation of small scaled financial institutions as follows: 63

65 CHAPTER I. GENERAL PROVISIONS Article 1. Governing scope and subjects of application 1. Small scaled financial institutions operating in Vietnam shall be required to maintain prudential ratios in accordance with provisions of this Circular, including: a. The minimum capital adequacy ratio; b. The lending limit to customer c. The liquidity ratio. 2. Based on inspection, examination result of the State Bank Inspectorate on the operational performance of small-scaled financial institutions, the State Bank may request small scaled financial institutions to maintain prudential ratios, which are higher than ratios stipulated in Article 4 and Article 7 of this Circulation. Article 2. Interpretation In this Circulation, following terms shall be construed as follows: 1. The total risk adjusted Assets shall be the total value of Assets of small scaled financial institution which is adjusted to the risk level provided for in Article 5 of this Circular. 2. Claims are on-balance sheet Assets formed from deposits, loans and from the performance of other operational activities under the guidance of the State Bank. 3. Immovable assets of the borrower are lands to which the borrower has the legal use right; houses, construction works tied to land and other immovable assets in accordance with provisions of applicable laws under the ownership of the borrower. In the event where immovable asset has been leased by the borrower, the use of asset as a pledged asset must be agreed by the lessee during the lease term. 4. A single customer is a legal entity, an individual, a family household, a cooperative group, a private enterprise, a partnership company, or other organizations that have credit relationship with a small scaled financial institution. 64

66 5. A group of related customers includes two or more customers who have credit relationship with a small-scaled financial institution and have mutual credit relationship, belonging to one of following cases: 5.1. An individual customer who owns at least 25% of charter capital of another legal entity, which is being a customer of a small scaled financial institution; 5.2. An individual customer who is a member of the family household in accordance with provisions of the Civil Code, which is being a customer of the small scaled financial institution or other individuals of which (including individuals who are independent subjects, taking selfliability with their own asset) are also being customers of the small scaled financial institution An individual customer who is a member of a cooperative group in accordance with provisions in the Civil Code, while such cooperative group is a customer of the small scaled financial institution An individual customer who is a partner of a partnership company, which is a customer of the small scaled financial institution An individual customer who is an owner of a private enterprise, which is a customer of the small scaled financial institution An individual customer who is a member of the administrative, executive and controlling mechanism of a legal entity which is being a customer of the small scaled financial institution A legal entity customer who owns at least 50% of charter capital of another legal entity which is being a customer of the small scaled financial institution A legal entity customer who is being a customer of the small scaled financial institution, meanwhile the representative of which is a member in the administrative, executive and controlling mechanism of another legal entity, which is also a customer of the small scaled financial institution. 6. Total loans outstanding shall include the entire balance of current loans and overdue loans of small scaled financial institutions. 7. Undistributed profit shall be the profit, which is determined through auditing by an independent auditing institution after the tax payment and setting up of funds have been 65

67 completed in accordance with provisions of applicable laws and retained for the small scaled financial institution s capital supplement in accordance with provisions of applicable laws. CHAPTER II. SPECIFIC PROVISIONS Article 3. Own capital 1. Own capital of a small- scaled financial institution shall include: 1.1. Tier 1 capital: a. Charter capital; b. Capital officially financed, without refund, by organizations, individuals to small-scaled financial institutions; c. Funds as provided for by the Ministry of Finance (Including: reserve fund for supplement of the charter capital; financial provisions fund; fund for the operational investment and development); d. Undistributed profits. The Tier 1 capital shall be used as the basis for the determination of the limit on purchase of, investment in fixed assets of the small scaled financial institution Tier 2 capital: a. 50% of the increased value of fixed assets, which are revaluated under provisions of applicable laws; b. Debt of the small scaled financial institution which satisfy following conditions: - Being the debt, of which the creditor is subordinate to other creditors, specifically: in any case, such creditor shall only be paid after the small scaled financial institution has completely made payment to all other secured and unsecured creditors; - Its initial term is more than 10 years at the minimum; - It is not secured by asset of the very small-scaled financial institution; 66

68 - The small scaled financial institution is entitled to stop the interest payment and carry over accumulated interests to the following year, if the interest payment results in the loss in the current year s business activity; - The small-scaled financial institution is only entitled to repay its debt to the creditor prior to the maturity after obtaining the written approval from the State Bank. - The increase of interest rate shall only be made after 5 years from the signing of the contract and for one time only during the loan term. c. General provisions (reserves), which are equal to 1.25% of the total risk adjusted Assets at the maximum. 2. Limitation on the determination of tier 2 capital: 2.1. Total value of the tier 2 capital shall be 100% value of the tier 1 capital at the maximum Total value of debts stipulated in point 1.2.b Paragraph 1 of this Article shall be equal to 50% value of the tier 1 capital at the maximum During the last 5 years prior to the maturity date, debts included into the tier 2 capital shall be annually deducted by 20% from the initial value. 3. Amounts to be deducted from the own capital: 3.1. The entire decreased value of fixed assets due to revaluation in accordance with provisions of applicable laws Business losses, including accumulated losses. Article 4. Minimum capital adequacy ratio 1. Small scaled financial institution must maintain a minimum ratio of 10% of the own capital over the total risk adjusted Assets. 2. The way to determine the minimum capital adequacy ratio is guided in Appendix A attached to this Circular. 67

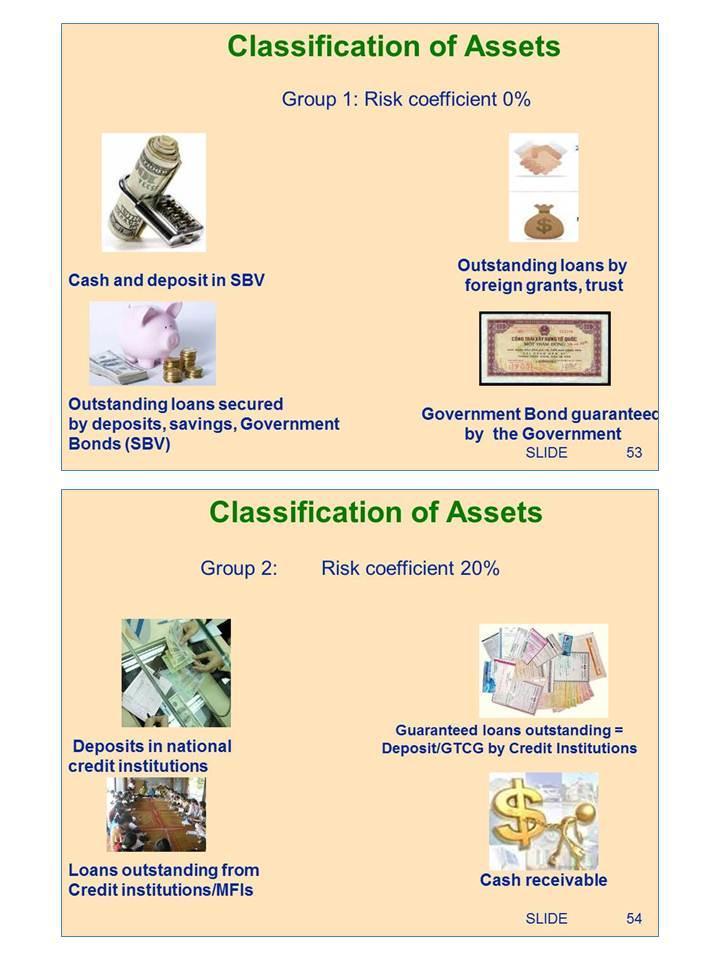

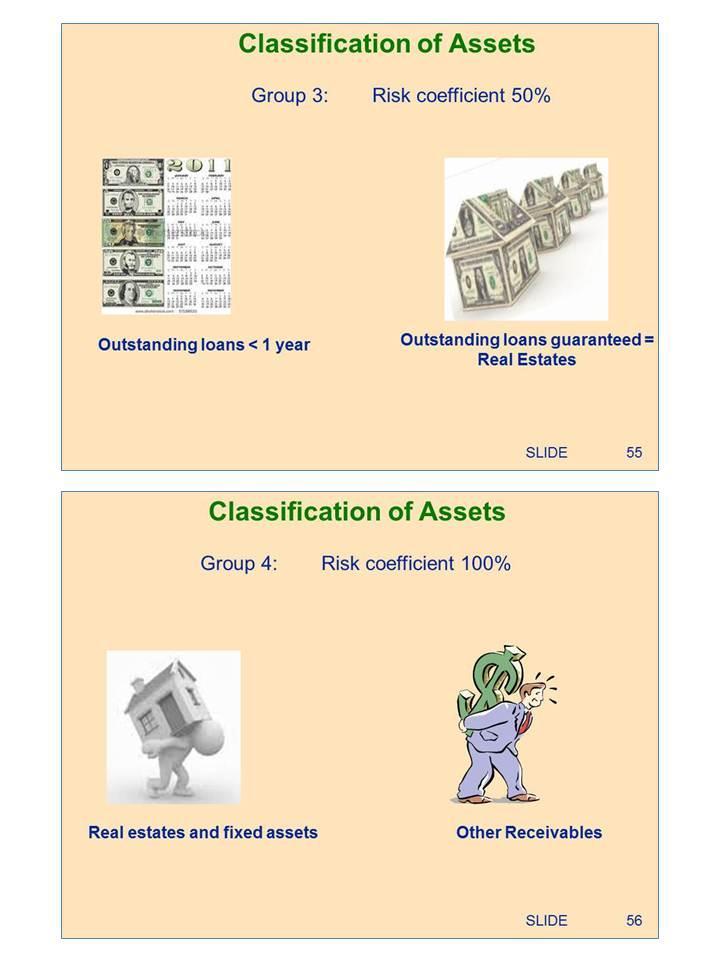

69 Article 5. Classification of Assets Assets are classified by risk levels as follows: 1. The group of Assets with risk coefficient of 0% includes: 1.1. Cash; 1.2. Deposits at the State Bank; 1.3. Loans from funds financed, entrusted for lending under trust contracts, by which, the small scaled financial institution only enjoys trust fees and shall not be subject to any risk; 1.4. Loans secured by 100% of deposit (voluntary savings and/or compulsory savings) at the very small scaled financial institution; 1.5. Outstanding principal and interest of the loan which is secured by compulsory savings at the very small scale financial institution; 1.6. Claims from Vietnam Government, including: Government bond (Treasury bills, Treasury bonds, bonds for Central Government s projects, investment bonds, Government bond for construction of Motherland), bonds guaranteed by the Government; 1.7. Loans secured by valuable papers which are issued by the Government, State Bank. 2. The group of Assets with the risk coefficient of 20%, includes: 2.1. Deposits at domestic commercial banks, credit institutions; 2.2. Loans outstanding (principals, interests) to credit institutions, other small scaled financial institutions (if any); 2.3. Loans outstanding (principals, interests) to be secured by deposits at credit institutions, which are operating in Vietnam; 2.4. Loans outstanding (principals, interests) to be secured by valuable papers, which are issued by credit institutions operating in Vietnam, state-owned financial institutions; 2.5. Cash, which is in collection process. 68

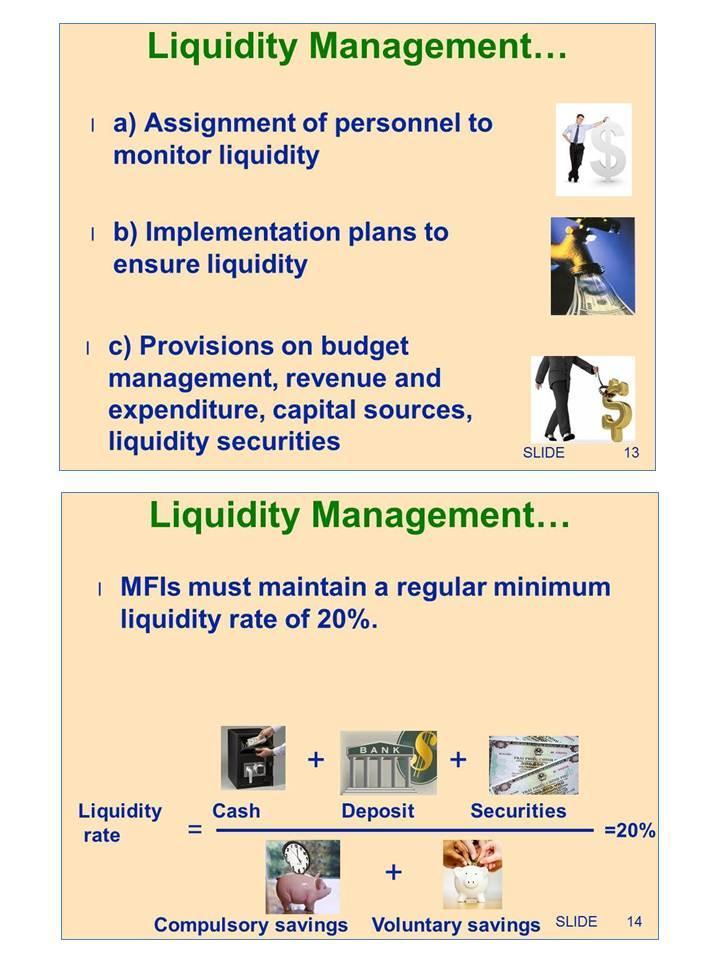

70 3. The group of Assets with the risk coefficient of 50%, includes 3.1. Loans outstanding (principals, interests) to be secured by immovable assets of the borrower; 3.2. Small scaled credit outstanding (principals, interests) to small-scaled financial customers with loan term of less than 1 year. 4. The group of Assets with the risk coefficient of 100%, includes: 4.1. Immovable assets and other fixed assets; 4.2. Other claims other than those stipulated in Paragraphs 1, 2 and 3 of this Article. Article 6. Internal regulations 1. Pursuant to provisions of this Circular, current provisions of the State Bank and actual performance, the small scaled financial institution shall draw up and issue internal regulations on: 1.1. The determination and classification of a single customer, a group of related customers, lending limits applicable to a single customer and a group of related customers, including following contents: a. Criteria for determining, classifying a single customer and a group of related customers shall be implemented in accordance with provisions in Paragraph 4 and Paragraph 5 in Article 2 of this Circular. b. Determination of lending limits applicable to a single customer and a group of related customer; competence to decide lending to a single customer and a group of related customer. c. Determination of the manner of following up loans exceeding 5% of own capital of the small scaled financial institution. d. Limit, maximum lending ratio in total loan outstanding to small scaled financial customers and those other than small-scaled financial customers Management of the liquidity with following main contents: 69

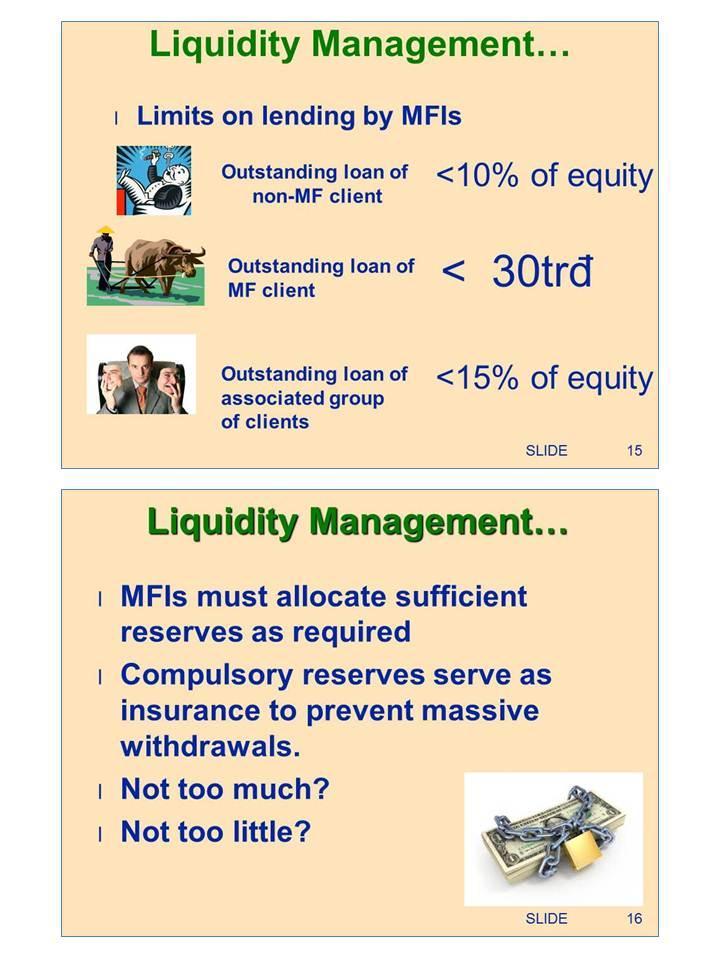

71 a. Assigning an officer who is in charge of supervising the liquidity of small-scaled financial institutions. b. Implementation plans to secure the liquidity in case of temporary default as well as in case of potential insolvency. c. Regulations on the management of budget, receipts, expenses, daily capital source and provisions on holding valuable papers which are freely convertible into cash. 2. Board of Directors of small-scaled financial institutions shall be responsible for the consideration, assessment of internal regulations as stated in Paragraph 1 of this Article for timely adjustment in necessary cases in order to ensure the prudential activities of small-scaled financial institutions. Article 7. Lending limit to customer 1. Lending limit of a small scaled financial institution to its customer shall be as follows: 1.1. Total loans outstanding of the small scaled financial institution to a single customer, who is not a small scaled financial institution, shall not exceed 10% of the small scaled financial institution s own capital Total loans outstanding of the small scaled financial institution to a small scaled financial institution shall not exceed VND 30 million. This loan level may be adjusted from time to time by the Governor of the State Bank Total loans outstanding of the small scaled financial institution to a group of related customers as stated in Paragraph 5 Article 2 of this Circular shall not exceed 15% of the small scaled financial institution s own capital, in which, the lending limit to a single customer shall not exceed the ratios provided for in Points 1.1 and 1.2 in Paragraph 1 of this Article. 2. Limits stipulated in Paragraph 1 of this Article shall not be applicable to following cases: 2.1. Loans from entrusted funds of Vietnam Government, of organizations, individuals against which the small scaled financial institution is not required to make and use provisions for dealing with credit risks. 70

72 2.2. Loans secured entirely by deposits of the customer at the very small scale financial institution Loans to credit institutions, other small scaled financial institutions with the term of less than 1 year (if any) Loans secured by Vietnamese Government s bonds, bonds guaranteed by the Vietnam Government. Article 8. Liquidity ratio The small- scaled financial institution must regularly maintain the minimum liquidity ratio of 20%. 2. This ratio shall be calculated as follows: 2.1. Numerator: includes assets as cash and assets which are easily convertible into cash, specifically as follows: a. Cash; b. Deposits at the State Bank (excluding required reserve deposit); c. Deposits at credit institutions; d. Government bonds, bonds guaranteed by the Government Denominator: Total deposits, including compulsory savings and voluntary savings. 3. The way to determine liquidity is guided in Appendix B attached to this Circular. Article 9. Reporting, dealing with violations 1. Small scaled financial institutions shall make report on their implementation of provisions on prudential ratios in accordance with current provisions of the Governor of the State Bank on the statistic reporting regime applicable to small scaled financial institutions. 2. Any small scaled financial institution which violates provisions of this Circular, depending on the seriousness of the violation, shall be subject to administrative punishment in line with provisions of applicable laws. 71

73 Article 10. Implementation effectiveness CHAPTER III. IMPLEMENTING PROVISIONS This Circular shall be effective after 45 days since its signing date. Article 11. Responsibility of implementation The Director of the Administrative Department, the Director of the Banks and Non-banking Credit Institutions Department, Heads of related units of the State Bank, General Managers of State Bank branches in provinces and cities under the central Government s management, Chairman of the Board of Directors and General Directors (Directors) of small scaled financial institutions shall be responsible for the implementation of this Circular. In the implementation, any query that may arise should be timely reflected to the State Bank for instruction and settlement. The Governor of the State Bank of Vietnam NGUYEN VAN GIAU (Signed and sealed) 72

74 APPENDIX A: THE WAY TO DETERMINE THE MINIMUM CAPITAL ADEQUACY RATIO A. The own capital for the determination of the minimum capital adequacy ratio of the small scaled financial institution (SSFI) A as of 31/3/2008: As of 31/3/2008, state of capital and assets of the SSFI A is as follows: 1. Tier 1 capital: Unit: VND billion Item Amount a. Charter capital (appropriated capital, contributed capital) 30 b. Capital officially financed without refund by organizations, 10 individuals c. Reserve fund for the supplement of the charter capital 2 d. Financial provisions fund 2 dd. Fund for operational investment and development 1 e. Undistributed profits 2 TOTAL Tier 2 capital: Unit: VND billion Item Increased Calculating Amount to amount ratio be included into the tier 2 capital a. The increased value of revaluated fixed assets % 0.1 under provisions of applicable laws b. Debts with remaining term of over 5 years 100% 3 c. General provisions 100% 1 TOTAL 4.1 Note: - Total debts are VND 3 billion, equaling 6.4% of tier 1 capital (less than 50% of tier 1 capital), satisfying requirements stated in item b, point 1.2, Article 3 of this Circular. The own capital (A) of the SSFI A as of 31/3/2008 = Tier 1 capital + tier 2 capital = VND 47 billion + VND 4.1 billion = VND 51.1 billion 3. Amounts to be deducted from own capital: 73

75 - Decreased value of fixed assets due to revaluation in accordance with provisions of applicable laws: 0 - Business losses, including accumulated losses: VND 0 billion. Own capital (A) for calculation of prudential ratios of SSFI A = Own capital amounts deductible A = VND 51.1 billion VND 0 billion = VND 51.1 billion B. Value of risk-adjusted Assets on balance sheet (B) Unit: VND billion Item Book value Risk coefficient Value of risk adjusted Assets 1. Group of Assets with the risk coefficient of 0% a. Cash 20 0% 0 b. Deposits at SBV 5 0% 0 c Loans from funds financed, entrusted for lending under 30 0% 0 trust contracts, by which, the small scaled financial institution only enjoys trust fees and shall not be subject to any risk; d. Loans secured by 100% of deposit (voluntary savings 3 0% 0 and/or compulsory savings) at the very small scaled financial institution dd. Outstanding principal and interest of the loan which is secured by compulsory savings at the very small scale financial institution 5 0% 0 e. Claims from Vietnam Government, including: 5 0% 0 Government bond, bonds guaranteed by the Government; g. Loans secured by valuable papers which are issued by 5 0% 0 the Government, State Bank 2. Group of Assets with the risk coefficient of 20% a. Deposits at domestic commercial banks, credit 20 20% 4 institutions b. Loans outstanding (principals, interests) to credit 0 20% 0 institutions, other small scaled financial institutions (if any); c. Loans outstanding (principals, interests) to be secured 5 20% 1 74

76 by deposits at credit institutions, which are operating in Vietnam; d. Loans outstanding (principals, interests) to be secured 3 20% 0.6 by valuable papers, which are issued by credit institutions operating in Vietnam, state-owned financial institutions dd. Cash, which is in collection process 2 20% Group of Assets with the risk coefficient of 50% a. Loans outstanding (principals, interests) to be secured 50 50% 25 by immovable assets of the borrower; b. Small scaled credit outstanding (principals, interests) to % 165 small-scaled financial customers with loan term of less than 1 year. 4. Group of Assets with the risk coefficient of 100% a. Immovable assets and other fixed assets 8 100% 8 b. Other claims % 50 Total (B) 254 C. Minimum capital adequacy ratio C = (A/B)*100% = (51.1/254)*100% = % Appendix B. the way to Determine liquidity ratio Unit: VND billion Item Book value I. Numerator A 1. Cash 2. Deposits at SBV 3. Deposits at CIs 4. Government bonds, bonds guaranteed by the Government II. Denominator B Total deposits, including compulsory savings and voluntary savings. III. Liquidity ratio (A/B*100%) 75

77 Handout 2 SBV Circular No. 15 STATE BANK SOCIALIST REPUBLIC OF VIETNAM OF VIETNAM Independence Freedom Happiness No. 15/2010/TT-NHNN Hanoi, June 6, 2010 CIRCULAR ON DEBT CLASSIFICATION, PROVISIONING, AND THE USE OF PROVISIONS TO MANAGE THE CREDIT RISKS OF SMALL FINANCIAL INSTITUTIONS Pursuant to the December 12, 1997 Vietnam State Bank Law and the June 17, 2003 Law Amending and Supplementing a Number of Articles of the Vietnam State Bank Law; Pursuant to the December 12, 1997 Credit Institutions Law and the June 15, 2004 Law Amending and Supplementing a Number of Articles of the Credit Institutions Law; Pursuant to the Government's Decree No. 96/ 2008/ND-CP of August 26, 2008, defining the functions, tasks, powers and organizational structure of the State Bank of Vietnam; Pursuant to No. 28/2005/ND-CP dated March 9, 2005, on organization and operation of smallsized financial institutions in Vietnam and Decree No. 165/2007/ND-CP dated November 15, 2007, amending, supplementing and annulling a number of articles of Decree No. 28/2005/ND- CP; Below The State Bank of Vietnam (below referred to as the State Bank) stipulates debt classification, provisioning, and the use of provision to manage credit risks of small financial institution: Chapter 1 GENERAL PROVISIONS Article 1. Governing scope and subjects of application 1. Small financial institutions (SFI) operating in Vietnam (below referred to as SFI) have to classify their debts, provision and use the provision to manage credit risks in conformity with this Circular. 2. Provisioning and the use of provision is carried out in compliance with regulations on finance for SFI. Article 2. Interpretation of terms 76

Viet Nam: Technical Training Manuals for Microfinance Institutions In Vietnam

Project Number: 42492-012 November 2011 Viet Nam: Technical Training Manuals for Microfinance Institutions In Vietnam Basic Course in Risk Management 1 COURSE OUTLINE Course Name Target Participants Course

Project Number: 42492-012 November 2011 Viet Nam: Technical Training Manuals for Microfinance Institutions In Vietnam Basic Course in Risk Management 1 COURSE OUTLINE Course Name Target Participants Course

Section I GENERAL PROVISIONS

The English translation provided by the Website of the State Bank of Vietnam (SBV) may only be used for reference. In case a different interpretation of the translated information contained in this website

The English translation provided by the Website of the State Bank of Vietnam (SBV) may only be used for reference. In case a different interpretation of the translated information contained in this website

SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness No. 12/2014/TT-NHNN Hanoi, March 31, 2014

STATE BANK OF VIETNAM ------- SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness --------------- No. 12/2014/TT-NHNN Hanoi, March 31, 2014 CIRCULAR REQUIREMENTS FOR TAKING FOREIGN LOANS APPLIED

STATE BANK OF VIETNAM ------- SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness --------------- No. 12/2014/TT-NHNN Hanoi, March 31, 2014 CIRCULAR REQUIREMENTS FOR TAKING FOREIGN LOANS APPLIED

DECREE GENERAL PROVISION

THE GOVERNMENT -------- SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness --------------- No.: 58/2012/ND-CP Ha Noi, July 20, 2012 DECREE STIPULATING IN DETAIL AND GUIDING THE IMPLEMENTATION

THE GOVERNMENT -------- SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness --------------- No.: 58/2012/ND-CP Ha Noi, July 20, 2012 DECREE STIPULATING IN DETAIL AND GUIDING THE IMPLEMENTATION

`ORDINANCE ON FOREIGN EXCHANGE

STANDING COMMITTEE NATIONAL ASSEMBLY No: 28/2005/PL-UBTVQH11 SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness `ORDINANCE ON FOREIGN EXCHANGE Pursuant to the 1992 Constitutions of the Socialist

STANDING COMMITTEE NATIONAL ASSEMBLY No: 28/2005/PL-UBTVQH11 SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness `ORDINANCE ON FOREIGN EXCHANGE Pursuant to the 1992 Constitutions of the Socialist

Recent banking reforms

Recent banking reforms September 2005 >>> This update discusses the main regulatory reforms in the banking sector in Vietnam over the past 12 months. This publication is copyright. Except as permitted

Recent banking reforms September 2005 >>> This update discusses the main regulatory reforms in the banking sector in Vietnam over the past 12 months. This publication is copyright. Except as permitted

Monthly Legal Briefing

Monthly Legal Briefing Edition 1 April 2014 Banking & Finance Corporate Dispute Resolution Intellectual Property Real Estate & Infrastructure Banking & Finance 1. Decree No. 26/2014/ND-CP on organizing

Monthly Legal Briefing Edition 1 April 2014 Banking & Finance Corporate Dispute Resolution Intellectual Property Real Estate & Infrastructure Banking & Finance 1. Decree No. 26/2014/ND-CP on organizing

SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness. General Provisions

GOVERNMENT No. -2006-ND-CP Draft 1653 SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness Hanoi, [ ] 2006 DECREE PROVIDING GUIDELINES FOR IMPLEMENTATION OF LAW ON INVESTMENT Pursuant to the

GOVERNMENT No. -2006-ND-CP Draft 1653 SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness Hanoi, [ ] 2006 DECREE PROVIDING GUIDELINES FOR IMPLEMENTATION OF LAW ON INVESTMENT Pursuant to the

GOVERNMENT DECREE PROVIDING DETAILED REGULATIONS ON THE IMPLEMENTATION OF THE LAW ON FOREIGN INVESTMENT IN VIETNAM

GOVERNMENT No. 24-2000-ND-CP SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness Hanoi, 31 July 2000 GOVERNMENT DECREE PROVIDING DETAILED REGULATIONS ON THE IMPLEMENTATION OF THE LAW ON FOREIGN

GOVERNMENT No. 24-2000-ND-CP SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness Hanoi, 31 July 2000 GOVERNMENT DECREE PROVIDING DETAILED REGULATIONS ON THE IMPLEMENTATION OF THE LAW ON FOREIGN

Global Restructuring & Insolvency Guide

Global Restructuring & Insolvency Guide Vietnam On 1 January 2015, Law No. 51/2014/QH13 on Bankruptcy, dated 19 June 2014, issued by the National Assembly (the New Bankruptcy Law ), officially took effect

Global Restructuring & Insolvency Guide Vietnam On 1 January 2015, Law No. 51/2014/QH13 on Bankruptcy, dated 19 June 2014, issued by the National Assembly (the New Bankruptcy Law ), officially took effect

AN UPDATE ON NON-PERFORMING LOANS RESOLUTION AND BANKING REFORM IN VIET NAM. by Hoang Tien Loi. Meeting held on April 2006

AN UPDATE ON NON-PERFORMING LOANS RESOLUTION AND BANKING REFORM IN VIET NAM by Hoang Tien Loi Meeting held on 27-28 April 2006 This document reproduces a report by Mr. Hoang Tien Loi written after the

AN UPDATE ON NON-PERFORMING LOANS RESOLUTION AND BANKING REFORM IN VIET NAM by Hoang Tien Loi Meeting held on 27-28 April 2006 This document reproduces a report by Mr. Hoang Tien Loi written after the

THE GOVERNMENT SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness No. 78/2015/ND-CP Hanoi, September 14, 2015

THE GOVERNMENT SOCIALIST REPUBLIC OF VIETNAM ------- Independence - Freedom - Happiness --------------- No. 78/2015/ND-CP Hanoi, September 14, 2015 DECREE ENTERPRISE REGISTRATION Pursuant to the Law on

THE GOVERNMENT SOCIALIST REPUBLIC OF VIETNAM ------- Independence - Freedom - Happiness --------------- No. 78/2015/ND-CP Hanoi, September 14, 2015 DECREE ENTERPRISE REGISTRATION Pursuant to the Law on

List of Adjustments and amendments in ABBANK Charter 2018

1 List of Adjustments and amendments in ABBANK Charter 2018 Current Charter Adjustments / amendements Legal bases CHAPTER I DEFINITION OF TERMS IN THE CHARTER Article 1: Definitions 1. In this Charter,

1 List of Adjustments and amendments in ABBANK Charter 2018 Current Charter Adjustments / amendements Legal bases CHAPTER I DEFINITION OF TERMS IN THE CHARTER Article 1: Definitions 1. In this Charter,

VIETNAM SAFEGUARD FRAMEWORK FOR FINANCIAL SERVICES LIBERALIZATION UNDER ASEAN FRAMEWORK AGREEMENT ON SERVICES

VIETNAM SAFEGUARD FRAMEWORK FOR FINANCIAL SERVICES LIBERALIZATION UNDER ASEAN FRAMEWORK AGREEMENT ON SERVICES -------------------------- Sector: BANKING Modes of supply: 1) Cross-border supply 2) Consumption

VIETNAM SAFEGUARD FRAMEWORK FOR FINANCIAL SERVICES LIBERALIZATION UNDER ASEAN FRAMEWORK AGREEMENT ON SERVICES -------------------------- Sector: BANKING Modes of supply: 1) Cross-border supply 2) Consumption

No.: 40/2018/ND-CP Hanoi, on March 12, DECREE on management of business activities under multi-level method

THE GOVERNMENT SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness No.: 40/2018/ND-CP Hanoi, on March 12, 2018 DECREE on management of business activities under multi-level method Pursuant

THE GOVERNMENT SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness No.: 40/2018/ND-CP Hanoi, on March 12, 2018 DECREE on management of business activities under multi-level method Pursuant

Chinatrust Commercial Bank, Ho Chi Minh City Branch. Financial statements for the year ended 31 December 2010

Financial statements for the year ended 31 December 2010 Corporate Information Banking Licence No 04/NHNN-GP 6 February 2002 The banking licence was issued by the State Bank of Vietnam and is valid for

Financial statements for the year ended 31 December 2010 Corporate Information Banking Licence No 04/NHNN-GP 6 February 2002 The banking licence was issued by the State Bank of Vietnam and is valid for

CIRCULAR ON SPECIAL SALES TAX

MINISTRY OF FINANCE No. 18-2005-TT-BTC SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness Hanoi, 8 March 2005 CIRCULAR ON SPECIAL SALES TAX Amending adding to Circular 119-2003-TT-BTC of

MINISTRY OF FINANCE No. 18-2005-TT-BTC SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness Hanoi, 8 March 2005 CIRCULAR ON SPECIAL SALES TAX Amending adding to Circular 119-2003-TT-BTC of

REGULATION ON THE LIQUIDITY RISK MANAGEMENT FOR MICROFINANCE INSTITUTIONS. Chapter I General Provision. Article 1 Purpose and Scope

Pursuant to Article 35, paragraph 1.1 of the Law No. 03/L-209 on Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No.77 / 16 August 2010), and Article 114 of the Law

Pursuant to Article 35, paragraph 1.1 of the Law No. 03/L-209 on Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No.77 / 16 August 2010), and Article 114 of the Law

VIETNAM JOINT STOCK COMMERCIAL BANK FOR INDUSTRY AND TRADE. SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness. Hanoi, 14 April, 2014

VIETNAM JOINT STOCK COMMERCIAL BANK FOR INDUSTRY AND TRADE 108 Tran Hung Đao Street, Hoan Kiem District, Hanoi Tel: 04.39421030; Fax: 04.3921032 Business Reg. Certificate No. 0100111948 dated 29/04/2014

VIETNAM JOINT STOCK COMMERCIAL BANK FOR INDUSTRY AND TRADE 108 Tran Hung Đao Street, Hoan Kiem District, Hanoi Tel: 04.39421030; Fax: 04.3921032 Business Reg. Certificate No. 0100111948 dated 29/04/2014

VIETNAM INSURANCE LAW UPDATE

VIETNAM INSURANCE LAW UPDATE Introduction Although Vietnam s insurance market has experienced double-digit growth in recent years, and the sector has opened up since Vietnam joined the World Trade Organization

VIETNAM INSURANCE LAW UPDATE Introduction Although Vietnam s insurance market has experienced double-digit growth in recent years, and the sector has opened up since Vietnam joined the World Trade Organization

NATIONAL ASSEMBLY SOCIALIST REPUBLIC OF VIETNAM XIth NATIONAL ASSEMBLY 7 th SESSION (from... to ) AMENDED AND SUPPLEMENTED CUSTOMS LAW

AMENDED AND SUPPLEMENTED CUSTOMS LAW") Draft NATIONAL ASSEMBLY Law No.../2005/QH 10 SOCIALIST REPUBLIC OF VIETNAM Independence Liberty Happiness NATIONAL ASSEMBLY SOCIALIST REPUBLIC OF VIETNAM XIth NATIONAL ASSEMBLY 7 th SESSION (from... to...

Draft NATIONAL ASSEMBLY Law No.../2005/QH 10 SOCIALIST REPUBLIC OF VIETNAM Independence Liberty Happiness NATIONAL ASSEMBLY SOCIALIST REPUBLIC OF VIETNAM XIth NATIONAL ASSEMBLY 7 th SESSION (from... to...

ORDINANCE ON MEASURES AGAINST SUBSIDIZED PRODUCTS IMPORTED INTO VIETNAM

STANDING COMMITTEE OF NATIONAL ASSEMBLY SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness No. 22-2004-PL-UBTVQH11 ORDINANCE ON MEASURES AGAINST SUBSIDIZED PRODUCTS IMPORTED INTO VIETNAM

STANDING COMMITTEE OF NATIONAL ASSEMBLY SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness No. 22-2004-PL-UBTVQH11 ORDINANCE ON MEASURES AGAINST SUBSIDIZED PRODUCTS IMPORTED INTO VIETNAM

As mentioned above, insurance intermediaries in Vietnam include agents and brokers.

Vietnam TILLEKE & GIBBINS CONSULTANTS Aaron Le Marquer vietnam@tilleke.com 1. Insurance intermediation activities 1.1 Is the distribution of insurance products (hereinafter referred to as insurance intermediation

Vietnam TILLEKE & GIBBINS CONSULTANTS Aaron Le Marquer vietnam@tilleke.com 1. Insurance intermediation activities 1.1 Is the distribution of insurance products (hereinafter referred to as insurance intermediation

No: 353/TCT-CS Hanoi, 29 January Tax Department of provinces or cities under central authority

MINISTRY OF FINANCE General Department of Taxation SOCIALIST REPUBLIC OF VIETNAM Independence Freedom Happiness No: 353/TCT-CS Hanoi, 29 January 2010 To: Tax Department of provinces or cities under central

MINISTRY OF FINANCE General Department of Taxation SOCIALIST REPUBLIC OF VIETNAM Independence Freedom Happiness No: 353/TCT-CS Hanoi, 29 January 2010 To: Tax Department of provinces or cities under central

Ho Chi Minh City Development Bank

Report of the Board of Management and Audited consolidated financial statements Reference: 60752693/16527313 INDEPENDENT AUDITORS REPORT To: The Shareholders of Ho Chi Minh City Development Bank We have

Report of the Board of Management and Audited consolidated financial statements Reference: 60752693/16527313 INDEPENDENT AUDITORS REPORT To: The Shareholders of Ho Chi Minh City Development Bank We have

THE MINISTRY OF FINANCE

THE MINISTRY OF FINANCE Circular No. 28/2011/TT-BTC of February 28, 2011, guiding a number of articles of the Law on Tax Administration and the Government s Decree No. 85/2007/ND-CP of May 25, 2007, and

THE MINISTRY OF FINANCE Circular No. 28/2011/TT-BTC of February 28, 2011, guiding a number of articles of the Law on Tax Administration and the Government s Decree No. 85/2007/ND-CP of May 25, 2007, and

RESOLUTIONS OF VPBANK ANNUAL GENERAL MEETING 2017

VIETNAM PROSPERITY BANK (VPBANK) 89 Lang Ha Dong Da Hanoi Tax code: 0100233583 Registration date: September 8, 2013 37 th amendment: March 31, 2017 SOCIALIST REPUBLIC OF VIETNAM Independence Freedom Happiness

VIETNAM PROSPERITY BANK (VPBANK) 89 Lang Ha Dong Da Hanoi Tax code: 0100233583 Registration date: September 8, 2013 37 th amendment: March 31, 2017 SOCIALIST REPUBLIC OF VIETNAM Independence Freedom Happiness

I. SUBJECTS AND SCOPE OF APPLICATION. II. Compensation, allowance

Circular N o 10/2003/TT- BLDTBXH dated 18 April 2003 of the MOLISA Instructing the implementation of compensation to the victims of occupational accidents and diseases Implementing the Government Decree

Circular N o 10/2003/TT- BLDTBXH dated 18 April 2003 of the MOLISA Instructing the implementation of compensation to the victims of occupational accidents and diseases Implementing the Government Decree

Independence - Freedom - Happiness LAW ON SECURITIES 1

NATIONAL ASSEMBLY No. 70-2006-QH11 SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness LAW ON SECURITIES 1 Pursuant to the 1992 Constitution of the Socialist Republic of Vietnam as amended

NATIONAL ASSEMBLY No. 70-2006-QH11 SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness LAW ON SECURITIES 1 Pursuant to the 1992 Constitution of the Socialist Republic of Vietnam as amended

Chinatrust Commercial Bank, Ho Chi Minh City Branch. Financial statements for the year ended 31 December 2011

Financial statements for the year ended 31 December 2011 Corporate Information Banking Licence No 04/NHNN-GP 6 February 2002 The banking licence was issued by the State Bank of Vietnam and is valid for

Financial statements for the year ended 31 December 2011 Corporate Information Banking Licence No 04/NHNN-GP 6 February 2002 The banking licence was issued by the State Bank of Vietnam and is valid for

THE SOCIALIST REPUBLIC OF VIETNAM Independence Freedom - Happiness

THE SOCIALIST REPUBLIC OF VIETNAM Independence Freedom - Happiness VIETNAM JSC BANK FOR PRIVATE ENTERPRISES Business registration No. 055689 issued by Hanoi Department of Planning and Investment on September

THE SOCIALIST REPUBLIC OF VIETNAM Independence Freedom - Happiness VIETNAM JSC BANK FOR PRIVATE ENTERPRISES Business registration No. 055689 issued by Hanoi Department of Planning and Investment on September

Visit

March 2014 edition contents Issue of valuable papers by credit institutions Further guidance on electronic gaming for foreign gamers 2 3 In brief: In this edition we cover a new circular on valuable papers

March 2014 edition contents Issue of valuable papers by credit institutions Further guidance on electronic gaming for foreign gamers 2 3 In brief: In this edition we cover a new circular on valuable papers

NEWSLETTER Edition 4, 2012

Edition 4, 2012 Dear Readers, We welcome our readers to the latest edition of the Frasers Newsletter for 2012, with some interesting updates on recent legislation and developments within Frasers. Frasers

Edition 4, 2012 Dear Readers, We welcome our readers to the latest edition of the Frasers Newsletter for 2012, with some interesting updates on recent legislation and developments within Frasers. Frasers

HDBank Corn Ii6t 161 ich coo nh6t

HDBank Corn Ii6t 161 ich coo nh6t CONSOLIDATED FINANCIAL STATEMENTS FOR THE THIRD QUARTER OF 2018 For period from 1 January 2018 to 30 September 2018 TRANSLATION TABLE OF CONTENTS Pages Consolidated balance

HDBank Corn Ii6t 161 ich coo nh6t CONSOLIDATED FINANCIAL STATEMENTS FOR THE THIRD QUARTER OF 2018 For period from 1 January 2018 to 30 September 2018 TRANSLATION TABLE OF CONTENTS Pages Consolidated balance

Independence - Freedom - Happiness LAW ON ENTERPRISES

NATIONAL ASSEMBLY No. 13-1999-QH10 SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness LAW ON ENTERPRISES To contribute to the promotion of internal forces for the cause of industrialization

NATIONAL ASSEMBLY No. 13-1999-QH10 SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness LAW ON ENTERPRISES To contribute to the promotion of internal forces for the cause of industrialization

THE LAW OF THE KYRGYZ REPUBLIC. On the National Bank of the Kyrgyz Republic

Bishkek July 29, 1997, # 59 THE LAW OF THE KYRGYZ REPUBLIC On the National Bank of the Kyrgyz Republic Chapter I. General provisions Chapter II. Reporting by the Bank of Kyrgyzstan Chapter III. Capital

Bishkek July 29, 1997, # 59 THE LAW OF THE KYRGYZ REPUBLIC On the National Bank of the Kyrgyz Republic Chapter I. General provisions Chapter II. Reporting by the Bank of Kyrgyzstan Chapter III. Capital

SOCIALIST REPUBLIC OF VIETNAM CONSTRUCTION. Independence - Freedom - Happiness

THE MINISTRY OF SOCIALIST REPUBLIC OF VIETNAM CONSTRUCTION Independence - Freedom - Happiness -------- --------------- No. 1/213/TT-BXD Hanoi, February 8 th 213 CIRCULAR GUIDING THE CALCULATION AND MANAGEMENT

THE MINISTRY OF SOCIALIST REPUBLIC OF VIETNAM CONSTRUCTION Independence - Freedom - Happiness -------- --------------- No. 1/213/TT-BXD Hanoi, February 8 th 213 CIRCULAR GUIDING THE CALCULATION AND MANAGEMENT

DECREE No. 108/2006/ND-CP OF SEPTEMBER 22, 2006, DETAILING AND GUIDING THE IMPLEMENTATION OF A NUMBER OF ARTICLES OF THE INVESTMENT LAW THE

DECREE No. 108/2006/ND-CP OF SEPTEMBER 22, 2006, DETAILING AND GUIDING THE IMPLEMENTATION OF A NUMBER OF ARTICLES OF THE INVESTMENT LAW THE GOVERNMENT Pursuant to the December 25, 2001 Law on Organization

DECREE No. 108/2006/ND-CP OF SEPTEMBER 22, 2006, DETAILING AND GUIDING THE IMPLEMENTATION OF A NUMBER OF ARTICLES OF THE INVESTMENT LAW THE GOVERNMENT Pursuant to the December 25, 2001 Law on Organization

Vietnam Legal Briefing

Vietnam Legal Briefing Decree No. 95/2008/ND-CP dated 25 August 2008: Organisation and operation of finance leasing companies Decree No. 97/2008/ND-CP dated 28 August 2008: Management, provision and use

Vietnam Legal Briefing Decree No. 95/2008/ND-CP dated 25 August 2008: Organisation and operation of finance leasing companies Decree No. 97/2008/ND-CP dated 28 August 2008: Management, provision and use

Vietnam Technological and Commercial Joint Stock Bank

Vietnam Technological and Commercial Joint Stock Bank The consolidated financial statements in accordance with the Vietnamese Accounting Standards and Accounting System for Credit Institutions For the

Vietnam Technological and Commercial Joint Stock Bank The consolidated financial statements in accordance with the Vietnamese Accounting Standards and Accounting System for Credit Institutions For the

The Awa Bank, Ltd. Consolidated Financial Statements. The Awa Bank, Ltd. and its Consolidated Subsidiaries. Years ended March 31, 2016 and 2017

The Awa Bank, Ltd. Consolidated Financial Statements Years ended March 31, 2016 and 2017 Consolidated Balance Sheets Thousands of U.S. dollars (Note 1) 2016 2017 2017 Assets Cash and due from banks (Notes

The Awa Bank, Ltd. Consolidated Financial Statements Years ended March 31, 2016 and 2017 Consolidated Balance Sheets Thousands of U.S. dollars (Note 1) 2016 2017 2017 Assets Cash and due from banks (Notes

SOCIALIST REPUBLIC OF VIET NAM Independence - Freedom - Happiness

SOCIALIST REPUBLIC OF VIET NAM Independence - Freedom - Happiness No: 1562/ MB-HS On information disclosure of separate and consolidated financial statements for QIII/2016 Hanoi, October 31st, 2016 Attention

SOCIALIST REPUBLIC OF VIET NAM Independence - Freedom - Happiness No: 1562/ MB-HS On information disclosure of separate and consolidated financial statements for QIII/2016 Hanoi, October 31st, 2016 Attention

Financial Sector Deepening Program RECONCILIATION OF THE ORIGINAL SUBPROGRAM 2 TO THE REVISED SUBPROGRAM 2

Financial Sector Deepening Program, (RRP VIE: 44251-034) Financial Sector Deepening Program RECONCILIATION OF THE ORIGINAL SUBPROGRAM 2 TO THE REVISED SUBPROGRAM 2 1. 2. 3. 4. 5. 6. 7. 8. 9. 1.1.3 Output

Financial Sector Deepening Program, (RRP VIE: 44251-034) Financial Sector Deepening Program RECONCILIATION OF THE ORIGINAL SUBPROGRAM 2 TO THE REVISED SUBPROGRAM 2 1. 2. 3. 4. 5. 6. 7. 8. 9. 1.1.3 Output

DIRECTIVE NO.DO2-93/MCR MINIMUM CAPITAL RATIOS FOR BANKS

DIRECTIVE NO.DO2-93/MCR MINIMUM CAPITAL RATIOS FOR BANKS Arrangement of Sections PART I Preliminary 1. Short Title 2. Authorization 3. Application 4. Interpretations PART II Statement of Policy 1. Objectives

DIRECTIVE NO.DO2-93/MCR MINIMUM CAPITAL RATIOS FOR BANKS Arrangement of Sections PART I Preliminary 1. Short Title 2. Authorization 3. Application 4. Interpretations PART II Statement of Policy 1. Objectives

SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness No. 15/2015/NĐ-CP Hanoi, February 14, 2015 DECREE

THE GOVERNMENT ------- SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness --------------- No. 15/2015/NĐ-CP Hanoi, February 14, 2015 DECREE ON INVESTMENT IN THE FORM OF PUBLIC-PRIVATE PARTNERSHIP

THE GOVERNMENT ------- SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness --------------- No. 15/2015/NĐ-CP Hanoi, February 14, 2015 DECREE ON INVESTMENT IN THE FORM OF PUBLIC-PRIVATE PARTNERSHIP

SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness

GOVERNMENT No. 23-2007-ND-CP SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness Hanoi, 12 February 2007 DECREE PROVIDING REGULATIONS FOR IMPLEMENTATION OF COMMERCIAL LAW REGARDING PURCHASE

GOVERNMENT No. 23-2007-ND-CP SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness Hanoi, 12 February 2007 DECREE PROVIDING REGULATIONS FOR IMPLEMENTATION OF COMMERCIAL LAW REGARDING PURCHASE

Legal news. Contents. Vision & Associates A TTORNEYS. PATENT & TRADEMARK A GENTS. I NVESTMENT & MANAGEMENT C ONSULTANTS.

A TTORNEYS. PATENT & TRADEMARK A GENTS. I NVESTMENT & MANAGEMENT C ONSULTANTS Legal news Contents Law on Transfer of Technology... 2 Other Sectors... 4 Finance... 4 Banking... 5 Securities... 5 Insurance...

A TTORNEYS. PATENT & TRADEMARK A GENTS. I NVESTMENT & MANAGEMENT C ONSULTANTS Legal news Contents Law on Transfer of Technology... 2 Other Sectors... 4 Finance... 4 Banking... 5 Securities... 5 Insurance...

Vietnam Law on Credit Institutions

Vietnam Law on Credit Institutions In order to ensure the soundness, prudence and efficient operations of credit institutions, to protect the interest of the State and the rights and legitimate interests

Vietnam Law on Credit Institutions In order to ensure the soundness, prudence and efficient operations of credit institutions, to protect the interest of the State and the rights and legitimate interests

THE SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness No. 31/2015/QD-TTg Hanoi, August 4, 2015 DECISION

THE PRIME MINISTER ------- THE SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness --------------- No. 31/2015/QD-TTg Hanoi, August 4, 2015 DECISION ALLOWANCE OF BAGGAGE, MOVABLES, GIFTS,

THE PRIME MINISTER ------- THE SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness --------------- No. 31/2015/QD-TTg Hanoi, August 4, 2015 DECISION ALLOWANCE OF BAGGAGE, MOVABLES, GIFTS,

REPORT BY THE BOARD OF DIRECTORS ON BUSINESS PERFORMANCE IN 2013

VIETNAM JOINT STOCK COMMERCIAL BANK FOR INDUSTRY AND TRADE 108 Tran Hung Dao, Hoan Kiem, Hanoi Tel: 04.39421030; Fax: 04.39421032 Tax code: 0100111948 THE SOCIALIST REPUBLIC OF VIETNAM Independence Freedom

VIETNAM JOINT STOCK COMMERCIAL BANK FOR INDUSTRY AND TRADE 108 Tran Hung Dao, Hoan Kiem, Hanoi Tel: 04.39421030; Fax: 04.39421032 Tax code: 0100111948 THE SOCIALIST REPUBLIC OF VIETNAM Independence Freedom

PPP TO BOOST INFRASTRUCTURE DEVELOPMENT INVESTMENT

PPP TO BOOST INFRASTRUCTURE DEVELOPMENT INVESTMENT By Pham Minh Long/Vuong Son Ha Reason for and Role of Public-Private Partnership Despite considerable efforts to improve Vietnam s infrastructure, the

PPP TO BOOST INFRASTRUCTURE DEVELOPMENT INVESTMENT By Pham Minh Long/Vuong Son Ha Reason for and Role of Public-Private Partnership Despite considerable efforts to improve Vietnam s infrastructure, the

LAW ON INVESTMENT TABLE OF CONTENTS

LAW ON INVESTMENT TABLE OF CONTENTS CHAPTER I... 1 General Provisions... 1 Article 1 Governing scope... 1 Article 2 Applicable entities... 1 Article 3 Interpretation of terms... 1 Article 4 Policies on

LAW ON INVESTMENT TABLE OF CONTENTS CHAPTER I... 1 General Provisions... 1 Article 1 Governing scope... 1 Article 2 Applicable entities... 1 Article 3 Interpretation of terms... 1 Article 4 Policies on

EXECUTIVE SUMMARY - A STUDY ON "FORMALIZATION" OF HOUSEHOLD BUSINESS IN VIETNAM

EXECUTIVE SUMMARY - A STUDY ON "FORMALIZATION" OF HOUSEHOLD BUSINESS IN VIETNAM Central Institute for Economic Management would like to thank the Mekong Business Initiative for supporting the preparation

EXECUTIVE SUMMARY - A STUDY ON "FORMALIZATION" OF HOUSEHOLD BUSINESS IN VIETNAM Central Institute for Economic Management would like to thank the Mekong Business Initiative for supporting the preparation

REGULATION ON THE LIQUIDITY RISK MANAGEMENT CHAPTER I GENERAL PROVISION. Article 1 Purpose and Scope

Pursuant to Article 35, paragraph 1.1 of the Law No. 03/L-209 on Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No.77 / 16 August 2010), and Articles 19 and 85 of the

Pursuant to Article 35, paragraph 1.1 of the Law No. 03/L-209 on Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No.77 / 16 August 2010), and Articles 19 and 85 of the

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENT For the fiscal year ended on December 31, 2006

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENT For the fiscal year ended on December 31, 2006 SUMMARY OF THE SIGNIFICANT ACCOUNTING POLICIES Basis of preparation The consolidated financial statements of

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENT For the fiscal year ended on December 31, 2006 SUMMARY OF THE SIGNIFICANT ACCOUNTING POLICIES Basis of preparation The consolidated financial statements of

THE PRIME MINISTER ------- No. 71/2010/QD-TTg SOCIALIST REPUBLIC OF VIET NAM Independence - Freedom Happiness --------- Hanoi, November 09, 2010 DECISION PROMULGATING THE REGULATION ON PILOT INVESTMENT

THE PRIME MINISTER ------- No. 71/2010/QD-TTg SOCIALIST REPUBLIC OF VIET NAM Independence - Freedom Happiness --------- Hanoi, November 09, 2010 DECISION PROMULGATING THE REGULATION ON PILOT INVESTMENT

THE DEVELOPMENT OF CO-OPBANK & PEOPLE S CREDIT FUND SYSTEM IN VIETNAM

THE DEVELOPMENT OF CO-OPBANK & PEOPLE S CREDIT FUND SYSTEM IN VIETNAM Content: I. Introduction II. Co-op Bank III. People s Credit Funds I. INTRODUCTION 1. Overview: On 1 st July 2013, Co-opBank was officially