Financial. News and Information Letter of the Cincinnati Chapter Cincinnati Chapter FSP. January/February 2009

|

|

|

- Abigayle Daniel

- 5 years ago

- Views:

Transcription

942-1000 rcottrell@finsvcs.")

1 Cincinnati Chapter FSP Solutions for a Secure Future (formerly the American Society of CLU & ChFC) Financial BOARD OF DIRECTORS OFFICERS: President Andrew F. McClintock, CLU, ChFC, RHU, REBC amcclintock@cinci.rr.com Immediate Past President Ernest J. Martin, CLU, ChFC, CFP emartin@theonfgroup.com President-Elect/Membership Chair Joseph F. Stenken, CLU, ChFC, JD jstenken@nuco.com VP Of Education John D. Dovich CLU, ChFC (513) john@jdovich.com Secretary/Treasurer Stephen P. King, CFP, CLTC steve@wqcorp.com TRUSTEES: Continuing Education/VTC Robert S. Cottrell, CFP, CLTC (513) rcottrell@finsvcs.com Communications Chair James LeBlond, CLU, ChFC jimleb@cinci.rr.com Public Relations Chair Sonya E. King, JD, LLM (859) sking@nuco.com Cincinnati Chapter Pro News and Information Letter of the Cincinnati Chapter January/February 2009 What s Inside: President s Podium SFSP MemberGram Large Case Strategies for the High Net Worth Market Segment SFSP January 29th Meeting When Client Objectives Are at Cross-Purposes, Try Private Split-Dollar Member Get A Member Program Rives to Chari FSP Risk Management Section Welcome New Members SFSP Calendar of Events 4100 Executive Park Dr. #16, Cinti, OH Phone: Fax: SocietyofFSP@aol.com Chapter Administrator: Lauren Estness

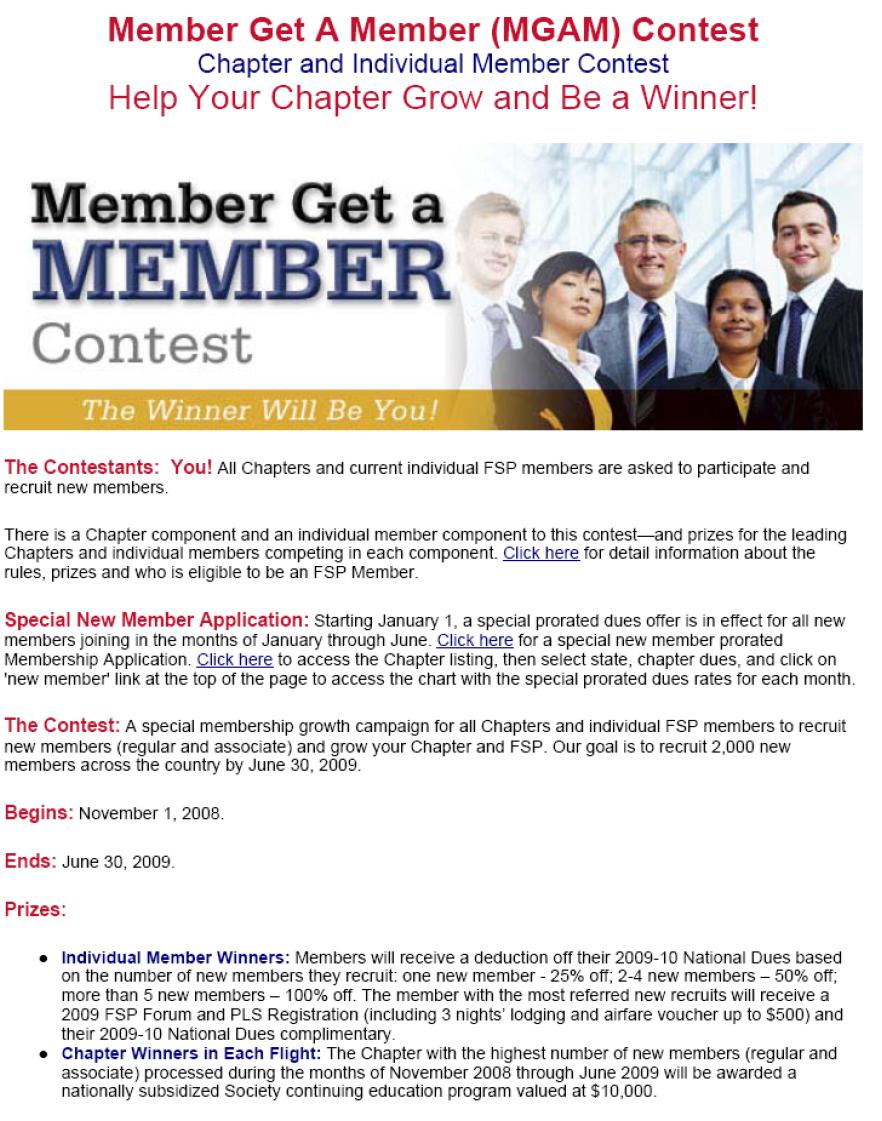

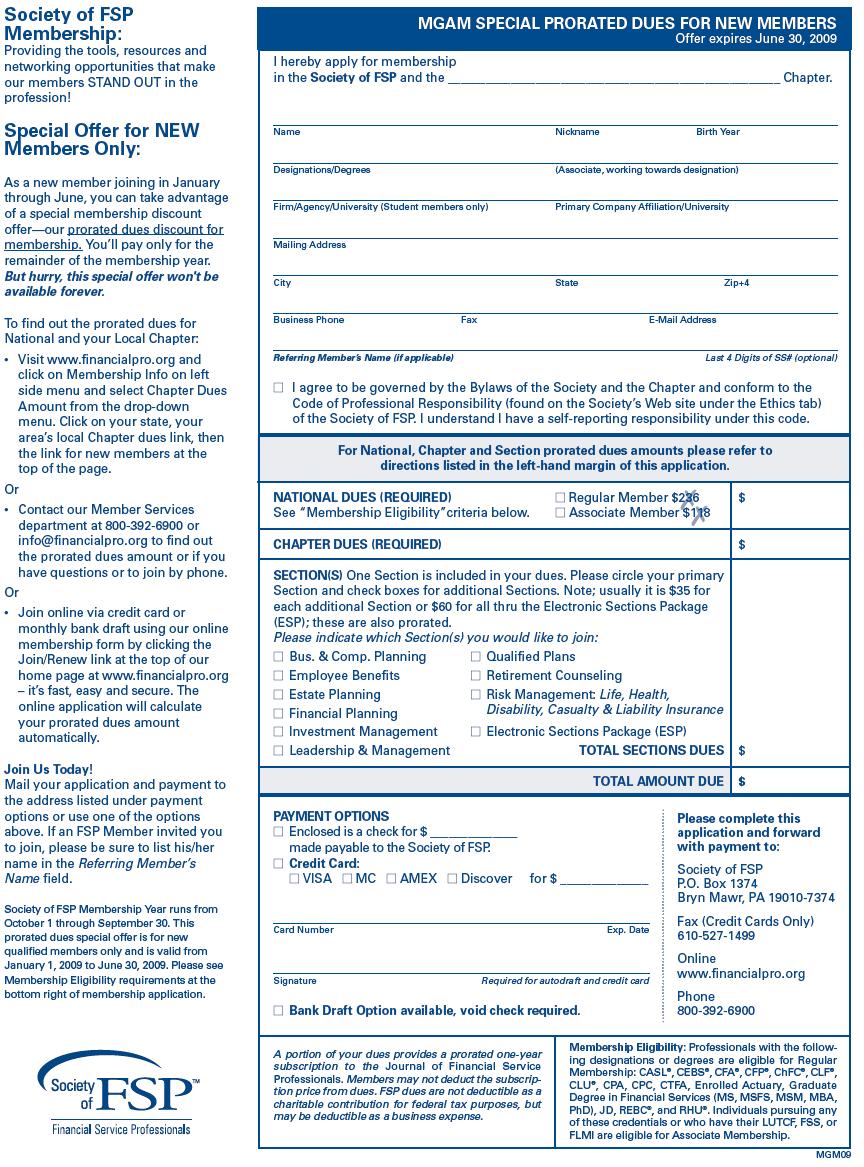

2 Page 2 President s Podium Happy New Year and Best Wishes for a healthy and prosperous 2009! Your Cincinnati Society of FSP has scheduled 4 outstanding CE credit programs for you to attend starting on January 29 th. Please refer to the enclosed schedule. For our annual meeting, May 21st, the President of our National Society, Roderick P. Hanson, CFP, CLU, ChFC, AEP will be our featured speaker. Mark your calendar for the January 29 th meeting, Estate Planning Update 2009 & Succession Planning in the Family Business System: The Role of the Most Trusted Advisor at the Horan Conference Center. Our annual directory will be going to print the latter part of January. If you by chance have not taken care of your dues, please do so right away in order to be included. If you have any questions concerning membership, please don t hesitate to call Joe Stenken our Membership Chair. Please note that between now and the end of June there is a Member Get A Member Contest going on. For one new member recruited you receive 25% off your National dues, for 2 to 4 members receive 50% off, and for 5 or more recruited receive 100% off. Please take a few minutes and share the benefits of FSP with an associate in your office or a CPA or JD with whom you do business. This is an outstanding time for a new member to join. The pro-rated dues effective February 1 are $ The dues schedule and membership application are included in this issue of Financial Pro. The strength and future of our chapter is our members. Thanks for your enthusiastic support. See you on the 29 th! Andy McClintock Andy McClintock CLU, ChFC, RHU, REBC

3 Page 3

4 Large Case Strategies for the High Net Worth Market Segment Page 4 By Rick Blaser and David Hunter Very wealthy and sophisticated clients deserve only the very best and most sophisticated planning techniques. Not only do they deserve these techniques, they need them. The federal estate and gift tax system is designed to tax the wealthy on the transfer of assets from one generation to another, during life and at death. The tax system has limited exemptions for both lifetime transfers and transfers at death and those exemptions do not increase with the size of an estate: the bigger the estate, the larger the tax. The primary objective of most sophisticated wealth transfer plans is to transfer as much wealth as possible to the intended beneficiaries, paying the least amount of estate and gift tax possible. A major part of the implementation is to use the available exemptions in the most beneficial way possible. Following are summaries of sophisticated strategies that may benefit some of your ultra-wealthy clients. Strategy #1: Dynasty trust planning A dynasty trust is an irrevocable trust designed to last for as long as possible under the state perpetuity laws. In some states a trust can be established to last forever. It is called a dynasty trust because, when properly structured, it can create a family dynasty that can last for many generations. This strategy is attractive to the ultra-wealthy for several reasons. First, it appeals to their sense of well-being by ensuring that future generations remember them and their accomplishments. Second, the strategy can yield significant tax benefits because, when properly structured, the assets in the trust avoid estate taxes at every generational level. Under current law, each individual is allowed a generation skipping transfer tax (GST) exemption in the amount of $2 million; married couples have a total of $4 million. People may allocate their GST exemption amount at death or during life. However, because the federal lifetime gift tax exemption amount is only $1 million per person, most married couples chose to use only $2 million of the exemption during their lives. Any remaining GST exemption can be allocated to assets at death. Of the different ways to fund a dynasty trust, the easiest is to gift $2 million to the trust. Once the trust has the money, it may purchase life insurance to leverage assets in the trust. The life insurance can be purchased on the grandparents or parents, which can increase what the grandchildren get, but will probably limit the benefit of the trust to the parents/ insureds. Depending on the size of the estate and the individual considerations of the clients, they may only want to use a portion of their lifetime gifting exemptions for this strategy. The rest of their exemptions can be used for other strategies. If they are interested in creating a dynasty trust with significantly more assets, they may want to explore Strategy #2. Strategy #2: Sale of assets to an Intentionally Defective Grantor Trust An intentionally defective grantor trust (IDGT) is

of the trust. He or she will gift a significant amount of money (typically about 10%) of what will be transferred to the trust.")

5 Page 5 Large Case Strategies for the High Net Worth Market Segment an irrevocable trust designed to be effective for estate and gift tax purposes (i.e., it is outside the estate) but defective (i.e., ignored) for income tax purposes. Under this strategy, one client is the grantor (creator) of the trust. He or she will gift a significant amount of money (typically about 10%) of what will be transferred to the trust. Let s assume that your client seeds the trust with $1 million. The same client then sells $10 million of assets to the trust for a note, leaving the trust with $11 million of assets. All the growth on the assets, over and above the interest due on the note, is outside the estate and goes to benefit the trust beneficiaries. Interest due on the note is usually set at the appropriate applicable federal rate (AFR) for the term of the note, which the IRS publishes monthly. For this strategy to be effective, the assets inside the trust must appreciate (or generate income) at a rate above the interest amount due to the grantor on the note. Clients could also consider selling assets that have a discount associated with them, typically limited partnership interests, non-managing LLC interests or nonvoting S-corporation stock. For example, let s assume that the $10 million of assets purchased by the trust represent limited partnership interests, discounted at 30%. That would mean that the underlying assets in the partnership could be worth $14,285,714 if the partnership is liquidated. Assuming these numbers, the grantor would have (before growth) transferred $4,285,714 of assets from his or her estate. Furthermore, to meet the current long-term interest rate of 5%, the trust assets would only have to generate about 3.5% of income annually. Excess earnings on the trust property could be used to buy life insurance, the proceeds of which could be then used at death to repay the $10 million loan, thus leaving the other assets intact and eliminating the need to liquidate the partnership. If the note is repaid before the death of the insured, the life insurance proceeds enhance the plan by adding to the amount of wealth transferred. The only gift necessary for this strategy is the seed money, thus making it an effective gift tax leveraging strategy. Furthermore, generation transfer tax exemptions can be allocated to the initial seed money to make the trust a dynasty trust a very big dynasty trust! Strategy #3: Private split-dollar with Grantor Retained Annuity Trust rollout This strategy yields maximum gift tax leverage and enables clients to purchase large amounts of life insurance with only minimal gift tax consequences. First, the clients set up an irrevocable life insurance trust (ILIT). The trustee purchases a survivorship life insurance policy for a specific amount of death benefit. The life insurance trust then enters into a private split-dollar agreement with the insureds. Under the agreement, the insureds are entitled to an interest in the policy equal to the greater of their premiums paid or the total cash value of the policy. The insureds pay most of the premium and the life insurance trust pays only a small fraction of the cost (derived from IRS Table 2001 or an alternate term rate of the insurer). Because the trust is only responsible for a fraction of the premium, only minimal gifts are required and significant gift tax leverage can be accomplished. In fact, it is sometimes possible to structure the trust s share of the premium to be lower than the allowable annual gift tax exclusions.

6 Page 6 Large Case Strategies for the High Net Worth Market Segment At the same time the clients create the life insurance trust and enter into the split-dollar arrangement, they create a grantor retained annuity trust. A GRAT is a specially drafted trust whereby the grantor retains an annuity (generally, a fixed annual payment) for a number of years and the trust is entitled to whatever property is left at the end of that annuity stream. For gift tax purposes, the value of a gift to a GRAT is determined by subtracting the actuarially determined value of the annuity from the full value of the property contributed. By creating an annuity stream valued at an amount equal to the value of the property contributed to the GRAT, it is possible to fund a GRAT without any gift tax liability (most of the time the annuity stream is valued at slightly less than the full value of the property so that a gift tax return is required and the statute of limitations will begin). In this strategy, the remainder beneficiary of the GRAT is the life insurance trust involved in the split-dollar agreement with the insureds. Assuming the assets transferred to the GRAT appreciate in value, there may be significant assets left when the annuity stream ends. At the end of the annuity stream, the assets left in the GRAT will pour over to the life insurance trust. The trust will then use all or a portion of the GRAT assets to roll out (repay) the insureds their interest in the life insurance policy. End result: the insurance policy should be fully funded and outside of the estate. The primary advantage of this strategy is gift tax leverage. Unfortunately, there are complex tax rules that make this strategy unattractive for generation-skipping tax (GST) purposes. Strategy #4: Private foundation Given the limited number of estate tax exemptions and deductions available, there will very likely be some level of estate tax levied upon the estate, unless the estate is transferred to a charity. The ultra-wealthy are prime candidates for setting up their own charities, termed private foundations. By establishing a private foundation, clients are afforded the choice of paying tax to the government or giving money to a charity that perpetuates their charitable beliefs. Because the amount of the estate that is transferred to charity does not pass to the family, clients may want to replace the value of the assets given to the charity with life insurance. Some clients can simply use their annual exclusions and/or lifetime gift tax exemption to fund an irrevocable life insurance trust (ILIT) to replace the assets. However, it is unlikely that the annual exclusions and lifetime exemptions would provide enough insurance for many high net worth clients. For these clients a private foundation serves as a complement to the strategies discussed in this article. Rick Blaser, J.D., CLU, ChFC is an advanced sales consultant at The Hartford in Simsbury, Conn. His address is richard.blaser@hartfordlife.com. David Hunter, CFP, CLU, ChFC, CAP, is a senior account executive on The Hartford's Private Wealth Management team. His address in Salem, VA, is david.hunter@hartfordlife.com Copyright 2009 by National Underwriter Life & Health Magazine. A Summit Business Media publication. All Rights Reserved. Reprinted with permission.

7 Page 7

8 When Client Objectives Are at Cross-Purposes, Try Private Split-Dollar Page 8 By Bruce A. Guillemette This is a short synopsis of a phone call I received from a producer: I ve got a guy. He s a doctor with a wife and two kids and he s still relatively young: 45-years-old. He doesn t have an estate tax problem yet. He is making a lot of money. He wants to save for retirement and protect his savings from creditors that may arise from future malpractice lawsuits. He also wants to make sure that if he dies, his wife will have enough money to live on. He knows he needs life insurance and heard he could use it to help save for retirement, too. But if his estate grows the way we think it might, we don t want the insurance in his estate. If we put it into a trust, he can t access the cash value. According to the objectives defined, the client needs: Retirement income. Creditor protection for the retirement income. Survivor income/estate liquidity. These objectives conflict with each other. What can we do? Enter private split- dollar The situation may sound similar to those of some of your clients, particularly if you service medical professional clientele. If you ve read the title of this article, you know we recommended a private split-dollar plan as an alternative. Why? Private split-dollar plans allow you accomplish these competing objectives. Although known best for the gift tax leverage they offer, private splitdollar plans can also be arranged to retain access to life insurance policy cash values for retirement income. Here s how it works: The client establishes an irrevocable life insurance trust (ILIT) that will own the policy. The trust is a defective grantor trust for income and estate tax purposes, where the client is both the grantor and the insured. With this type of trust, trust income is taxable to the grantor and any transactions between the grantor and the ILIT are ignored for income tax purposes. The insured s spouse advances money to the ILIT for premium payments. The ILIT will owe the spouse either the amount he or she advances to it or the policy cash values. The ILIT owns the policy to avoid inclusion in the client s taxable estate and to keep it beyond the reach of the client s creditors. Most states laws largely or even entirely protect life insurance from creditors, with the exception of the Internal Revenue Service, provided that the debtor does not own the insurance and that any transfers were not done to defraud creditors. Also, life insurance policy cash values owned by ILITs typically can t be accessed by anyone other than the trustee without subverting estate tax and creditor protection planning. In a private split-dollar plan, the trustee will use the policy values to repay the client s spouse for the money advanced to the trust. The payments the spouse receives from the ILIT may be used to supplement the couple s retirement income. (It helps to have a solid marriage; otherwise, the spouse may be the only one who gets to supplement his or her income.) If the amount owed to the spouse under the

9 Page 9 When Client Objectives Are at Cross-Purposes, Try Private Split-Dollar continued arrangement is limited to the amount of money he or she advanced to the ILIT, the arrangement will be established as a loan regime private split-dollar plan and interest will be either accrued or paid annually. The interest is often accrued to maximize the amounts paid to the spouse. But if the time horizon for repayment is short (e.g., less than 15 years) or if the policy cash values otherwise won t support the repayment obligation that results from accruing the interest, the ILIT can pay the spouse the annual interest due from cash gifts made by the client. Generally, it is not recommended to use economic benefit regime-based split-dollar arrangements because the ILIT would owe the spouse the entire policy cash value, a debt that could only be satisfied at the death of the insured or upon total surrender of the policy. If the spouse pre-deceases the insured, any amount still owed to him or her would be included in their estate. For the insured to be able to derive retirement income from the policy, the amount owed would have to be passed to the insured. While the policy cash values owned by the ILIT would continue to be beyond the reach of the insured s creditors, the death benefit proceeds could be included in his or her estate. How to best deal with this situation if it arises depends on the client s situation at that point in time. At the client s death, the death benefit is paid to the ILIT. The ILIT then repays any remaining money owed to the spouse and uses the remainder to provide the liquidity needed to settle the client s estate and distribute wealth to beneficiaries. Valuable benefits In summary, private split-dollar plans are not just for gift tax leverage. They have the potential to provide clients with 3 additional valuable benefits: retirement income from policy values, survivor income/estate liquidity from policy death benefits, and creditor protection for the retirement fund (policy values) and the death benefit owned by an ILIT. If you encounter situations like the one described at the beginning of this article, consider evaluating how well a private split-dollar plan might work. Bruce A. Guillemette, MSM, CLU, ChFC, FLMI, is assistant vice president of advanced markets case design for AXA Equitable s independent life channel, AXA Distributors, LLC, New York. He can be reached at bruce.guillemette@axa-equitable.com Copyright 2008 by National Underwriter Life & Health Magazine. A Summit Business Media publication. All Rights Reserved. Reprinted with permission.

10

11 Page 11 Dues for the Cincinnati Chapter Note the table below illustrates the total dues amount (both local and national dues amounts) for membership. The Society membership year runs from October 1 to September 30. As a special incentive for new members to join our organization, we are pleased to offer a prorated reduced dues structure program or a 1-month, 2-month, or 3-month free offer for those new members joining at specific points in the membership year. Please note: If you are a renewing member, your membership dues would be the first column labeled "Full Dues Amount." If you are a new member, joining in the months of January thru June, you can take advantage of our special prorated reduced dues structure program. You will pay an amount based on the number of months remaining in the current membership year (our membership year is October 1 to September 30). Select your member type and look for the month in which your dues payment will be paid to find the amount of prorated National and Local Chapter Dues. If you are a new member, joining in the months of July, August or September, your membership dues would be the first column labeled "Full Dues Amount" and you will receive 1-, 2- or 3- months free in addition to your regular 12-months of paid membership. months free in addition

12

13

.")

14 Page 14 Rives to Chair FSP Risk Management Section Bill Rives, Ph.D., CLU, ChFC, RHU, Columbus, OH, has been named Chair of the Risk Management Professional Interest Section for the Society of Financial Services Professionals (FSP). In this volunteer position, he is charged with enhancing the overall value of the Section to FSP members by helping develop practice-specific content for various educational presentations as well as monitoring online discussions to ensure robust and on-topic content. Rives is Senior Lecturer in the Department of Finance of the Fisher College of Business at The Ohio State University. During a career spanning more than three decades, he has held teaching and research appointments at institutions including Duke, Princeton, Rice, Trinity University (San Antonio), the University of Delaware and USAA Real Estate Company, the National Institute on Aging, the National Institute of Mental Health, and the US Department of Commerce. A member of the American Risk and Insurance Association, the National Association of Insurance and Financial Advisors, and the Society of Financial Service Professionals. Rives principal expertise is retirement income planning and retirement asset management, he is a frequent speaker on financial planning issues for professional, civic and non-profit organizations. FSP s nine Professional Interest Sections are national knowledge-sharing communities focused on specific segments of the financial services arena: Business & Compensation Planning; Employee Benefits; Estate Planning; Financial Planning; Investment Management; Leadership and Management; Risk Management; Life, Health, Disability, Casualty & Liability Insurance; Qualified Plans; and Retirement Counseling. Participating in one Section is included in membership dues. Section members have access to an online knowledge exchange, online search capabilities, and targeted FSP educational events in addition to receiving quarterly newsletters and other benefits.

579-9400 tom@jdovich.")

15 Page 15 Welcome To Our New Members! Jeffrey L. Bertsch, CLU, ChFC Cincinnati Life 7156 Tarragon Ct Hamilton, OH (513) Thomas J. Lalley, CFP, CFA, MBA, BS John Dovich & Associates LLC 625 Eden Park Dr., Ste 310 Cincinnati, OH (513) John J Maddrill, CLU, CFP, LUTCF Mass Mutual Financial Group 300 E Business Way Ste 390 Cincinnati, OH (513) ext 319 johnmaddrill@finsvcs.com Matthew T. Malafa, MBA John V. Dovich & Assoc. 625 Eden Park Dr., Ste 301 Cincinnati, OH (513) mmalafa@jdovich.com

16 Page 16

Effective Strategies for Wealth Transfer

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Wealth Transfer and Charitable Planning Strategies. Handbook

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Solutions for a S ecure Future Financial Pro (formerly the American Society of CLU & ChFC)

") Cincinnati Chapter FSP www.financialpro.org Solutions for a Secure Future (formerly the American Society of CLU & ChFC) 2009-2010 BOARD OF DIRECTORS OFFICERS: President Joseph F. Stenken, CLU, ChFC, JD

Cincinnati Chapter FSP www.financialpro.org Solutions for a Secure Future (formerly the American Society of CLU & ChFC) 2009-2010 BOARD OF DIRECTORS OFFICERS: President Joseph F. Stenken, CLU, ChFC, JD

Advanced marketing concepts. Brought to you by the Advanced Consulting Group of Nationwide

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Leveraging wealth transfer using a sale to a defective grantor trust

Sale to a Grantor Trust Strategy Leveraging wealth transfer using a sale to a defective grantor trust Not a bank or credit union deposit, obligation or guarantee May lose value Not FDIC or NCUA/NCUSIF

Sale to a Grantor Trust Strategy Leveraging wealth transfer using a sale to a defective grantor trust Not a bank or credit union deposit, obligation or guarantee May lose value Not FDIC or NCUA/NCUSIF

Dynasty Trust. Clients, Business Owners, High Net Worth Individuals, Attorneys, Accountants and Trust Officers:

Platinum Advisory Group, LLC Michael Foley, CLTC, LUTCF Managing Partner 373 Collins Road NE Suite #214 Cedar Rapids, IA 52402 Office: 319-832-2200 Direct: 319-431-7520 mdfoley@mdfoley.com www.platinumadvisorygroupllc.com

Platinum Advisory Group, LLC Michael Foley, CLTC, LUTCF Managing Partner 373 Collins Road NE Suite #214 Cedar Rapids, IA 52402 Office: 319-832-2200 Direct: 319-431-7520 mdfoley@mdfoley.com www.platinumadvisorygroupllc.com

Please understand that this podcast is not intended to be legal advice. As always, you should contact your WEALTH TRANSFER STRATEGIES

WEALTH TRANSFER STRATEGIES Hello and welcome. Northern Trust is proud to sponsor this podcast, Wealth Transfer Strategies, the third in a series based on our book titled Legacy: Conversations about Wealth

WEALTH TRANSFER STRATEGIES Hello and welcome. Northern Trust is proud to sponsor this podcast, Wealth Transfer Strategies, the third in a series based on our book titled Legacy: Conversations about Wealth

Double Discounted Transfers

Advanced Markets planning perspective estate planning Double Discounted Transfers The Silver Lining After the Economic Downturn It seems clear that estate taxes are here to stay. For people who are likely

Advanced Markets planning perspective estate planning Double Discounted Transfers The Silver Lining After the Economic Downturn It seems clear that estate taxes are here to stay. For people who are likely

Link Between Gift and Estate Taxes

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Living Trusts to Avoid Probate. POAs. Asset Protection. HIPAAs. Health Care Directives. Divorce & Asset. Family Limited Partnerships

Asset Protection Planning Strategies Grantor Retained Annuity Section 1035 Rescues Prenuptial Planning Gift for Children BERT! The Wonder Trust Wyoming Close LLCs Sales to IDOTs Gift for Grandchildren

Asset Protection Planning Strategies Grantor Retained Annuity Section 1035 Rescues Prenuptial Planning Gift for Children BERT! The Wonder Trust Wyoming Close LLCs Sales to IDOTs Gift for Grandchildren

Consider what estate planning is all about. In its essence, estate. Perspectives in Estate Planning

Perspectives in Estate Planning For many of us, estate planning is something we know we should do but somehow manage to postpone until some indefinite tomorrow; or, once having done a plan, put it away

Perspectives in Estate Planning For many of us, estate planning is something we know we should do but somehow manage to postpone until some indefinite tomorrow; or, once having done a plan, put it away

Advanced Wealth Transfer Strategies

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

THE ESTATE PLANNER S SIX PACK

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS You should consider creating an Intentionally Defective Irrevocable Trust ( IDIT ) and gifting assets to

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS You should consider creating an Intentionally Defective Irrevocable Trust ( IDIT ) and gifting assets to

WEALTH STRATEGIES. GRATs and Sale to IDGTs: Estate Freeze Techniques

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA GRATs and Sale to IDGTs: Estate Freeze Techniques FREQUENTLY ASKED QUESTIONS ESTATE PLANNING How do two of the techniques used by wealthy clients

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA GRATs and Sale to IDGTs: Estate Freeze Techniques FREQUENTLY ASKED QUESTIONS ESTATE PLANNING How do two of the techniques used by wealthy clients

THREE LEVELS OF FAMILY BUSINESS SUCCESSION PLANNING

SPECIAL REPORT Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 www.disinherit-irs.com THE THREE LEVELS OF FAMILY BUSINESS SUCCESSION PLANNING

SPECIAL REPORT Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 www.disinherit-irs.com THE THREE LEVELS OF FAMILY BUSINESS SUCCESSION PLANNING

White Paper: Dynasty Trust

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

Estate Planning. Insight on. Keep future options open with powers of appointment

Insight on Estate Planning October/November 2011 Keep future options open with powers of appointment A trust that keeps on giving Create a dynasty to make the most of today s exemptions Charitable IRA

Insight on Estate Planning October/November 2011 Keep future options open with powers of appointment A trust that keeps on giving Create a dynasty to make the most of today s exemptions Charitable IRA

Shumaker, Loop & Kendrick, LLP. Sarasota 240 South Pineapple Ave. 10th Floor Sarasota, Florida

The Estate Planner may/june 2013 Exemption portability: Should you rely on it? Decant a trust to add trustee flexibility Using the GST tax exemption to build a dynasty Estate Planning Red Flag Your plan

The Estate Planner may/june 2013 Exemption portability: Should you rely on it? Decant a trust to add trustee flexibility Using the GST tax exemption to build a dynasty Estate Planning Red Flag Your plan

Estate Planning for Small Business Owners

Estate Planning for Small Business Owners HOSTED BY OCEAN FIRST BANK PRESENTED BY MONZO CATANESE HILLEGASS, P.C. SPEAKER: DANIEL S. REEVES, ESQUIRE Topics Tax Overview Trust Ownership Intentionally Defective

Estate Planning for Small Business Owners HOSTED BY OCEAN FIRST BANK PRESENTED BY MONZO CATANESE HILLEGASS, P.C. SPEAKER: DANIEL S. REEVES, ESQUIRE Topics Tax Overview Trust Ownership Intentionally Defective

Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs. Producer Guide. For agent use only. Not for public distribution.

and Rolling GRATs. Producer Guide. For agent use only. Not for public distribution.") Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs Producer Guide Introduction to GRATs and Rolling GRATs The Grantor Retained Annuity Trust ( GRAT ) is a flexible planning tool which can be used

Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs Producer Guide Introduction to GRATs and Rolling GRATs The Grantor Retained Annuity Trust ( GRAT ) is a flexible planning tool which can be used

GIFTING. I. The Basic Tax Rules of Making Lifetime Gifts[1] A Private Clients Group White Paper

![GIFTING. I. The Basic Tax Rules of Making Lifetime Gifts[1] A Private Clients Group White Paper](/thumbs/89/98748865.jpg "GIFTING. I. The Basic Tax Rules of Making Lifetime Gifts[1] A Private Clients Group White Paper") GIFTING A Private Clients Group White Paper Among the goals of most comprehensive estate plans is the reduction of federal and state inheritance taxes. For this reason, a carefully prepared Will or Revocable

GIFTING A Private Clients Group White Paper Among the goals of most comprehensive estate plans is the reduction of federal and state inheritance taxes. For this reason, a carefully prepared Will or Revocable

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

Estate Planning Client Guide

CLIENT GUIDE Advanced Markets Estate Planning Client Guide LIFE-5711 6/17 TABLE OF CONTENTS Why Create an Estate Plan?... 1 Basic Estate Planning Tools... 2 Funding an Irrevocable Life Insurance Trust

CLIENT GUIDE Advanced Markets Estate Planning Client Guide LIFE-5711 6/17 TABLE OF CONTENTS Why Create an Estate Plan?... 1 Basic Estate Planning Tools... 2 Funding an Irrevocable Life Insurance Trust

Preserving Family Wealth with an Estate Freeze. cn ING North America Insurance Corporation

Walton GRAT: Preserving Family Wealth with an Estate Freeze Thanks for sharing your time with me today. I d like to tell you about a powerful and flexible estate planning idea. This strategy is called

Walton GRAT: Preserving Family Wealth with an Estate Freeze Thanks for sharing your time with me today. I d like to tell you about a powerful and flexible estate planning idea. This strategy is called

2000 Financial Independence Group

Qualified Account Replacement Trust The Scenario: Many financial planners encounter clients who have accumulated millions of dollars in qualified accounts for which they do not foresee a need. If younger

Qualified Account Replacement Trust The Scenario: Many financial planners encounter clients who have accumulated millions of dollars in qualified accounts for which they do not foresee a need. If younger

Tax Bulletin: Effectively Using a QPRT Strategy in Your Estate Plan

Tax Bulletin: Effectively Using a QPRT Strategy in Your Estate Plan PAUL F. NAPOLEON, Senior Vice President & Head of Tax Services SAMANTHA BRIJLALL, Tax Associate Estate planning is an area of wealth

Tax Bulletin: Effectively Using a QPRT Strategy in Your Estate Plan PAUL F. NAPOLEON, Senior Vice President & Head of Tax Services SAMANTHA BRIJLALL, Tax Associate Estate planning is an area of wealth

CLIENT ALERT - ESTATE, GIFT AND GENERATION-SKIPPING TRANSFER TAX

CLIENT ALERT - ESTATE, GIFT AND GENERATION-SKIPPING TRANSFER TAX January 2013 JANUARY 2013 CLIENT ALERT - ESTATE, GIFT AND GENERATION-SKIPPING TRANSFER TAX Dear Clients and Friends: On January 2, 2013,

CLIENT ALERT - ESTATE, GIFT AND GENERATION-SKIPPING TRANSFER TAX January 2013 JANUARY 2013 CLIENT ALERT - ESTATE, GIFT AND GENERATION-SKIPPING TRANSFER TAX Dear Clients and Friends: On January 2, 2013,

Sale to an Intentionally Defective Irrevocable Trust

Sale to an Intentionally Defective Irrevocable Trust Concept An Intentionally Defective Irrevocable Trust (IDIT) is an irrevocable trust established by a grantor generally for the benefit of the grantor

Sale to an Intentionally Defective Irrevocable Trust Concept An Intentionally Defective Irrevocable Trust (IDIT) is an irrevocable trust established by a grantor generally for the benefit of the grantor

Steve Leimberg's Estate Planning Newsletter - Archive Message #2442

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #2442 Date: 08-Aug-16 From: Steve Leimberg's Estate Planning Newsletter Steve Oshins and Bob Keebler: Creative Planning Strategies Once

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #2442 Date: 08-Aug-16 From: Steve Leimberg's Estate Planning Newsletter Steve Oshins and Bob Keebler: Creative Planning Strategies Once

Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs

& Rolling GRATs") Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs February, 2014 Contact us: AdvancedSales@voya.com This material is designed to provide general information for use

Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs February, 2014 Contact us: AdvancedSales@voya.com This material is designed to provide general information for use

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

Wealth Transfer Planning Opportunities

ADVANCED MARKETS BEYOND TAX REFORM Wealth Transfer Planning Opportunities BECAUSE YOU ASKED As part of the Tax Cuts and Jobs Act of 2017, the estate tax, gift, and GST exemptions have been increased from

ADVANCED MARKETS BEYOND TAX REFORM Wealth Transfer Planning Opportunities BECAUSE YOU ASKED As part of the Tax Cuts and Jobs Act of 2017, the estate tax, gift, and GST exemptions have been increased from

Issues INSIGHTS AND. Wealth Transfer Strategies for Rising Interest Rates

Issues AND INSIGHTS May 2018 Wealth Transfer Strategies for Rising Interest Rates IN THIS ARTICLE Interest rates are a key component of wealth transfer strategies, and any changes in the rates will affect

Issues AND INSIGHTS May 2018 Wealth Transfer Strategies for Rising Interest Rates IN THIS ARTICLE Interest rates are a key component of wealth transfer strategies, and any changes in the rates will affect

TRUSTS & ESTATES ADVISORY

Estate Planning Techniques In A Low Interest Rate Environment Interest rates remain at historic lows and it seems that rates will not be rising as quickly as most commentators once thought. Consequently,

Estate Planning Techniques In A Low Interest Rate Environment Interest rates remain at historic lows and it seems that rates will not be rising as quickly as most commentators once thought. Consequently,

Framing Your Legacy. With Transfer Tax Certainty, It Is Time to Consider Your Estate And Life Insurance Planning MKT13-65

Framing Your Legacy With Transfer Tax Certainty, It Is Time to Consider Your Estate And Life Insurance Planning MKT13-65 This material is not intended to be used, nor can it be used by any taxpayer, for

Framing Your Legacy With Transfer Tax Certainty, It Is Time to Consider Your Estate And Life Insurance Planning MKT13-65 This material is not intended to be used, nor can it be used by any taxpayer, for

Spousal Lifetime Access Trust Producer Guide. Transferring wealth. and retaining. spousal access

Spousal Lifetime Access Trust Producer Guide Transferring wealth and retaining spousal access Life. your waysm Lifeyour. way MetLife understands your business. We respect your entrepreneurial spirit as

Spousal Lifetime Access Trust Producer Guide Transferring wealth and retaining spousal access Life. your waysm Lifeyour. way MetLife understands your business. We respect your entrepreneurial spirit as

Beat the estate tax blow: with deferred annuities and an irrevocable trust

Beat the estate tax blow: with deferred annuities and an irrevocable trust JAN 01, 2012 BY The hinge around which estate planning revolves is gifting. The future growth in value of the asset from the date

Beat the estate tax blow: with deferred annuities and an irrevocable trust JAN 01, 2012 BY The hinge around which estate planning revolves is gifting. The future growth in value of the asset from the date

Passing on family wealth without making gifts

Passing on family wealth without making gifts New wealth transfer opportunities As part of a year-end agreement to avoid the Fiscal Cliff crisis, Congress passed the American Taxpayer Relief Act of 0 (ATRA

Passing on family wealth without making gifts New wealth transfer opportunities As part of a year-end agreement to avoid the Fiscal Cliff crisis, Congress passed the American Taxpayer Relief Act of 0 (ATRA

Estate Planning. Insight on. Tax Relief act provides temporary certainty for your estate plan

Insight on Estate Planning February/March 2011 Tax Relief act provides temporary certainty for your estate plan 3 postmortem strategies that add flexibility to your estate plan Can a SCIN allow you to

Insight on Estate Planning February/March 2011 Tax Relief act provides temporary certainty for your estate plan 3 postmortem strategies that add flexibility to your estate plan Can a SCIN allow you to

Estate Freezing Techniques. For Producer or Broker/Dealer Use Only. Not for Public Distribution.

Estate Freezing Techniques Agenda Identify Potential Clients Qualified Personal Residence Trust (QPRT) Grantor Retained Annuity Trust (GRAT) Installment Sale to an Intentionally Defective Irrevocable Trust

Estate Freezing Techniques Agenda Identify Potential Clients Qualified Personal Residence Trust (QPRT) Grantor Retained Annuity Trust (GRAT) Installment Sale to an Intentionally Defective Irrevocable Trust

Typical Succession Scenario

Uplifting Gifting: Using Additional Exemption to Maximize Business Succession Planning Eric Green Robert Nemzin Richard Barnes October 21, 2011 1 Typical Succession Scenario Client has substantial portion

Uplifting Gifting: Using Additional Exemption to Maximize Business Succession Planning Eric Green Robert Nemzin Richard Barnes October 21, 2011 1 Typical Succession Scenario Client has substantial portion

Wealth Transfer Planning in 2012: Perfect Storm of Opportunity

Wealth Transfer Planning in 2012: Perfect Storm of Opportunity 04.23.2012 04.23.2012 NEWS BY: FARHAD AGHDAMI 2012 may present the single greatest opportunity for wealth transfer planning in recent memory.

Wealth Transfer Planning in 2012: Perfect Storm of Opportunity 04.23.2012 04.23.2012 NEWS BY: FARHAD AGHDAMI 2012 may present the single greatest opportunity for wealth transfer planning in recent memory.

Estate Planning Strategies for the Business Owner

National Life Group is a trade name of of National Life Insurance Company, Montpelier, VT and its affiliates. TC74345(0613)1 Estate Planning Strategies for the Business Owner Presented by: Connie Dello

National Life Group is a trade name of of National Life Insurance Company, Montpelier, VT and its affiliates. TC74345(0613)1 Estate Planning Strategies for the Business Owner Presented by: Connie Dello

Estate and gift tax provision highlights

Legislative Update Tax Cuts and Jobs Act Estate and gift tax provision highlights On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs Act (P.L. 115-97). Highlights of the key provisions

Legislative Update Tax Cuts and Jobs Act Estate and gift tax provision highlights On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs Act (P.L. 115-97). Highlights of the key provisions

tax strategist the A simple plan Installment sale offers alternative to complex estate planning strategies Balance competing

the May/June 2008 tax strategist A simple plan Installment sale offers alternative to complex estate planning strategies Balance competing goals with a QTIP trust Take care when choosing IRA beneficiaries

the May/June 2008 tax strategist A simple plan Installment sale offers alternative to complex estate planning strategies Balance competing goals with a QTIP trust Take care when choosing IRA beneficiaries

WILLMS, S.C. LAW FIRM

WILLMS, S.C. LAW FIRM TO: FROM: Clients and Friends of Willms, S.C. Attorney Andrew J. Willms DATE: October 15, 2012 RE: Year-End Tax Planning for 2012 As you are probably well aware, most of the changes

WILLMS, S.C. LAW FIRM TO: FROM: Clients and Friends of Willms, S.C. Attorney Andrew J. Willms DATE: October 15, 2012 RE: Year-End Tax Planning for 2012 As you are probably well aware, most of the changes

Bypass Trust (also called B Trust or Credit Shelter Trust)

") Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

How the Smiths Integrated Twelve Tax Planning Tools to Minimize Taxes and Maximize Benefits for Retirement, Family, and Favorite Charities.

How the Smiths Integrated Twelve Tax Planning Tools to Minimize Taxes and Maximize Benefits for Retirement, Family, and Favorite Charities. So that you can appreciate how a typical family benefits from

How the Smiths Integrated Twelve Tax Planning Tools to Minimize Taxes and Maximize Benefits for Retirement, Family, and Favorite Charities. So that you can appreciate how a typical family benefits from

Financing strategies for survivorship life insurance owned by an irrevocable life insurance trust (ILIT)

") Financing strategies for survivorship life insurance owned by an irrevocable life insurance trust (ILIT) Annual Basic description (all of the trust agreements used for these ILITs are assumed to be grantor

Financing strategies for survivorship life insurance owned by an irrevocable life insurance trust (ILIT) Annual Basic description (all of the trust agreements used for these ILITs are assumed to be grantor

Succession & Estate Planning Opportunities: Creating a Company Legacy

Succession & Estate Planning Opportunities: Creating a Company Legacy Presented by: Patricia Quintana-Perron, CPA, CHBC, CFP, PFS Cara Benningfield, CPA May 12, 2011 To Receive CPE Credit Participate in

Succession & Estate Planning Opportunities: Creating a Company Legacy Presented by: Patricia Quintana-Perron, CPA, CHBC, CFP, PFS Cara Benningfield, CPA May 12, 2011 To Receive CPE Credit Participate in

Estate Planning under the New Tax Law

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

ESTATE PLANNING. Estate Planning

ESTATE PLANNING Estate Planning 2 Why do you need estate planning? Estate planning is a way for your family to create a plan in case something happens to you. It may help you take care of both the financial

ESTATE PLANNING Estate Planning 2 Why do you need estate planning? Estate planning is a way for your family to create a plan in case something happens to you. It may help you take care of both the financial

Determined by Seller (not to exceed life expectancy) Deductibility of Interest Depends on Property None

Deductibility of Interest Depends on Property None") chapter chapter 7 SCIN Private Annuity Term of Payment Determined by Seller (not to exceed life expectancy) Life of Annuitant Deductibility of Interest Depends on Property None Buyer s Adjusted Basis Purchase

chapter chapter 7 SCIN Private Annuity Term of Payment Determined by Seller (not to exceed life expectancy) Life of Annuitant Deductibility of Interest Depends on Property None Buyer s Adjusted Basis Purchase

Sale to an Intentionally Defective Irrevocable Trust

Concept Sale to an Intentionally Defective Irrevocable Trust An Intentionally Defective Irrevocable Trust (IDIT) is an irrevocable trust established by a grantor generally for the benefit of the grantor

Concept Sale to an Intentionally Defective Irrevocable Trust An Intentionally Defective Irrevocable Trust (IDIT) is an irrevocable trust established by a grantor generally for the benefit of the grantor

The Use of Pass-Through Entities in Asset Protection and Wealth Transfer Planning

The Use of Pass-Through Entities in Asset Protection and Wealth Transfer Planning DANIEL W DALY III 2323 S. Shepherd, 14 th Floor Houston, TX 77019 713-979- 4701 daly@ohdlegal.com www.ohdlegal.com Judge

The Use of Pass-Through Entities in Asset Protection and Wealth Transfer Planning DANIEL W DALY III 2323 S. Shepherd, 14 th Floor Houston, TX 77019 713-979- 4701 daly@ohdlegal.com www.ohdlegal.com Judge

ESTATE PLANNING OPPORTUNITIES UNDER THE TAX RELIEF ACT OF

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 Winter 2011 www.disinherit-irs.com Editor: Julius Giarmarco, J.D., LL.M. The Tax Relief

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 Winter 2011 www.disinherit-irs.com Editor: Julius Giarmarco, J.D., LL.M. The Tax Relief

Insight on estate planning

Insight on estate planning august.september.2007 What to do with the collectibles? Incorporate them into your estate plan Trusting your heirs The ins and outs of an inheritor s trust All in the family

Insight on estate planning august.september.2007 What to do with the collectibles? Incorporate them into your estate plan Trusting your heirs The ins and outs of an inheritor s trust All in the family

A Deep Dive Into Private Financing

A Deep Dive Into Private Financing Bob Finnegan, J.D., CLU, AEP Sr. VP, Advanced Sales Attorney, Highland Capital Brokerage bfinnegan@highland.com 518.424.8928 Funding Hierarchy (Simple to Complex) Clients

A Deep Dive Into Private Financing Bob Finnegan, J.D., CLU, AEP Sr. VP, Advanced Sales Attorney, Highland Capital Brokerage bfinnegan@highland.com 518.424.8928 Funding Hierarchy (Simple to Complex) Clients

Tax planning: Charitable giving and estate planning

Tax planning: Charitable giving and estate planning Understanding how the tax law affects charitable giving and estate planning Given the complexity of changes to the tax code in the United States, there

Tax planning: Charitable giving and estate planning Understanding how the tax law affects charitable giving and estate planning Given the complexity of changes to the tax code in the United States, there

Strategic Issues for Financial Planners Texas A&M University October 28, 2012

Estate Planning Under the Tax Relief Act of 2010 Strategic Issues for Financial Planners Texas A&M University October 28, 2012 Presented by: Joe Chenoweth, CLU, ChFC, AEP Vice President, Estate & Financial

Estate Planning Under the Tax Relief Act of 2010 Strategic Issues for Financial Planners Texas A&M University October 28, 2012 Presented by: Joe Chenoweth, CLU, ChFC, AEP Vice President, Estate & Financial

A Unique Opportunity to Transfer Wealth Without Tax: Taking Advantage of the 2012 Gift Tax Exemption

A Unique Opportunity to Transfer Wealth Without Tax: Taking Advantage of the 2012 Gift Tax Exemption By Andrew H. Friedman, The Washington Update ESTATE PLANNING SERVICES APRIL 2012 T ax provisions enacted

A Unique Opportunity to Transfer Wealth Without Tax: Taking Advantage of the 2012 Gift Tax Exemption By Andrew H. Friedman, The Washington Update ESTATE PLANNING SERVICES APRIL 2012 T ax provisions enacted

Tax Bulletin: 2017 Year-End Tax Planning Considerations

Tax Bulletin: 2017 Year-End Tax Planning Considerations PAUL F. NAPOLEON, Senior Vice President & Head of Tax Services On December 2, 2017, the full Senate passed its amended version of the Tax Cuts and

Tax Bulletin: 2017 Year-End Tax Planning Considerations PAUL F. NAPOLEON, Senior Vice President & Head of Tax Services On December 2, 2017, the full Senate passed its amended version of the Tax Cuts and

THE SCIENCE OF GIFT GIVING After the Tax Relief Act. Presented by Edward Perkins JD, LLM (Tax), CPA

, CPA") THE SCIENCE OF GIFT GIVING After the Tax Relief Act Presented by Edward Perkins JD, LLM (Tax), CPA THE SCIENCE OF GIFT GIVING AFTER THE TAX RELIEF ACT AN ESTATE PLANNING UPDATE Written and Presented by

THE SCIENCE OF GIFT GIVING After the Tax Relief Act Presented by Edward Perkins JD, LLM (Tax), CPA THE SCIENCE OF GIFT GIVING AFTER THE TAX RELIEF ACT AN ESTATE PLANNING UPDATE Written and Presented by

Memorandum FILE. Naim D. Bulbulia, Esq. Estate Planning Primer

Memorandum TO FROM FILE Naim D. Bulbulia, Esq. DATE May 5, 2005 RE Estate Planning Primer The following memorandum has been prepared in order to provide you with an overview of estate and gift tax law

Memorandum TO FROM FILE Naim D. Bulbulia, Esq. DATE May 5, 2005 RE Estate Planning Primer The following memorandum has been prepared in order to provide you with an overview of estate and gift tax law

Taming the Planning B.E.A.S.T.

Taming the Planning B.E.A.S.T. Tulsa Estate Planning Forum October 9 th, 2017 James M. Duggan, M.B.A., J.D. DUGGAN BERTSCH, LLC 303 West Madison, Suite 1000 Chicago, Illinois 60606-3321 e-mail: jduggan@dugganbertsch.com

Taming the Planning B.E.A.S.T. Tulsa Estate Planning Forum October 9 th, 2017 James M. Duggan, M.B.A., J.D. DUGGAN BERTSCH, LLC 303 West Madison, Suite 1000 Chicago, Illinois 60606-3321 e-mail: jduggan@dugganbertsch.com

Credit shelter trusts and portability

Credit shelter trusts and portability Comparing strategies to help manage estate taxes Married couples have two strategies to choose from to help protect their families from estate taxes. Choosing the

Credit shelter trusts and portability Comparing strategies to help manage estate taxes Married couples have two strategies to choose from to help protect their families from estate taxes. Choosing the

BECOME THE KEY TO YOUR CLIENTS WEALTH PRESERVATION

COVER STORY BECOME THE KEY TO YOUR CLIENTS WEALTH PRESERVATION HOW TO USE LPL S HELP TO LEAVE NO OPPORTUNITY BEHIND PLAN 32 LPL Magazine Winter 2016 Only 18% of affluent investors are receiving estate

COVER STORY BECOME THE KEY TO YOUR CLIENTS WEALTH PRESERVATION HOW TO USE LPL S HELP TO LEAVE NO OPPORTUNITY BEHIND PLAN 32 LPL Magazine Winter 2016 Only 18% of affluent investors are receiving estate

ESTATE PLANNING 1 / 11

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 What happens to my money and assets after I die? No matter what your age or income, you need to

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 What happens to my money and assets after I die? No matter what your age or income, you need to

Life Insurance-Premium Financing BY MATT HEALY MANAGING DIRECTOR, CLIENT RISK MANAGEMENT

Life Insurance-Premium Financing BY MATT HEALY MANAGING DIRECTOR, CLIENT RISK MANAGEMENT Investment and insurance products are: NOT A DEPOSIT NOT FDIC INSURED MAY LOSE VALUE NOT BANK GUARANTEED NOT INSURED

Life Insurance-Premium Financing BY MATT HEALY MANAGING DIRECTOR, CLIENT RISK MANAGEMENT Investment and insurance products are: NOT A DEPOSIT NOT FDIC INSURED MAY LOSE VALUE NOT BANK GUARANTEED NOT INSURED

Shumaker, Loop & Kendrick, LLP. Sarasota 240 South Pineapple Ave. 10th Floor Sarasota, Florida

The Estate Planner July/August 2012 Is your estate plan flexible? Estate tax law uncertainty requires options No time like the present With favorable estate tax and real estate environments, use a QPRT

The Estate Planner July/August 2012 Is your estate plan flexible? Estate tax law uncertainty requires options No time like the present With favorable estate tax and real estate environments, use a QPRT

Issues AND. Tax-Powered Philanthropy: Doing well by doing good

Issues AND INSIGHTS February 2015 Tax-Powered Philanthropy: Doing well by doing good IN THIS ARTICLE Higher tax rates offer greater potential savings from charitable giving Strategies such as outright

Issues AND INSIGHTS February 2015 Tax-Powered Philanthropy: Doing well by doing good IN THIS ARTICLE Higher tax rates offer greater potential savings from charitable giving Strategies such as outright

Why Use Legacy Trusts?

Why Use Legacy Trusts? Prepared by: Christopher Cline Senior Vice President, Senior Regional Fiduciary Manager Reviewed by: Morry Zygman Vice President, Strategic Business Segments, Legacy Trust In This

Why Use Legacy Trusts? Prepared by: Christopher Cline Senior Vice President, Senior Regional Fiduciary Manager Reviewed by: Morry Zygman Vice President, Strategic Business Segments, Legacy Trust In This

Shared Dollar Life Insurance: An inter-generational approach to retirement planning

Shared Dollar Life Insurance: An inter-generational approach to retirement planning What will retirement look like for our children? If you are like most working people, from time to time you think about

Shared Dollar Life Insurance: An inter-generational approach to retirement planning What will retirement look like for our children? If you are like most working people, from time to time you think about

Important Tax information about CLATs

Important Tax information about CLATs By Jeffrey A. Baskies Jeffrey A. Baskies is an honors graduate of Trinity College and Harvard Law School. Jeff is a Florida Bar certified expert in Wills, Trusts and

Important Tax information about CLATs By Jeffrey A. Baskies Jeffrey A. Baskies is an honors graduate of Trinity College and Harvard Law School. Jeff is a Florida Bar certified expert in Wills, Trusts and

DYNASTY TRUSTS (A general explanation)

") DYNASTY TRUSTS (A general explanation) Dynasty Trusts, also called Legacy Trusts, are set up to benefit future generations. Assets are transferred into the Trust and invested for many years so that future

DYNASTY TRUSTS (A general explanation) Dynasty Trusts, also called Legacy Trusts, are set up to benefit future generations. Assets are transferred into the Trust and invested for many years so that future

Financing strategies for single-insured life insurance owned by an irrevocable life insurance trust (ILIT)

") Financing strategies for single-insured life insurance owned by an irrevocable life insurance trust (ILIT) Annual Basic description (all of the trust agreements used for these ILITs are assumed to be grantor

Financing strategies for single-insured life insurance owned by an irrevocable life insurance trust (ILIT) Annual Basic description (all of the trust agreements used for these ILITs are assumed to be grantor

WEALTH TRANSFER STRATEGIES FOR FAMILIES DECEMBER 13, 2018

WEALTH TRANSFER STRATEGIES FOR FAMILIES DECEMBER 13, 2018 To Receive CPE Credit Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group

WEALTH TRANSFER STRATEGIES FOR FAMILIES DECEMBER 13, 2018 To Receive CPE Credit Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group

September /October Some strings attached Stretching your legacy Don t underestimate the power of Crummey trusts Estate Planning Red Flag

The Estate Planner September/October 2007 Some strings attached Maintaining control over your charitable contributions without losing your deduction Stretching your legacy Dynasty trusts benefit many generations

The Estate Planner September/October 2007 Some strings attached Maintaining control over your charitable contributions without losing your deduction Stretching your legacy Dynasty trusts benefit many generations

TWO-YEAR WINDOW FOR GIFT TAX PLANNING OPPORTUNITY

BE IN A POSITION OF STRENGTH SM WithumSmith+Brown s Tax Services Team Newsletter ESTATE & TRUST 03-04 SUCCESSION PLANNING FOR THE TRANSFER OF A BUSINESS TWO-YEAR WINDOW FOR GIFT TAX PLANNING OPPORTUNITY

BE IN A POSITION OF STRENGTH SM WithumSmith+Brown s Tax Services Team Newsletter ESTATE & TRUST 03-04 SUCCESSION PLANNING FOR THE TRANSFER OF A BUSINESS TWO-YEAR WINDOW FOR GIFT TAX PLANNING OPPORTUNITY

Estate planning using life insurance

Estate planning using life insurance With the right life insurance strategy, you can safeguard who and what you care about, while creating opportunities for your wealth to go further. To take advantage

Estate planning using life insurance With the right life insurance strategy, you can safeguard who and what you care about, while creating opportunities for your wealth to go further. To take advantage

Estate Planning. Uncertain Times. IRS Circular 230 Disclosure

Estate Planning IRS Circular 230 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments)

Estate Planning IRS Circular 230 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments)

Understanding Dynasty Trusts

Understanding Dynasty Trusts Understanding Dynasty Trusts DISCUSSION TOPICS What is a Dynasty Trust? How to Set Up a Dynasty Trust What are the Benefits of a Charitable Lead Trust? INVEST Trust Services

Understanding Dynasty Trusts Understanding Dynasty Trusts DISCUSSION TOPICS What is a Dynasty Trust? How to Set Up a Dynasty Trust What are the Benefits of a Charitable Lead Trust? INVEST Trust Services

Financial. What s Inside:

Cincinnati Chapter FSP www.financialpro.org Solutions for a Secure Future (formerly the American Society of CLU & ChFC) Financial 2007-2008 BOARD OF DIRECTORS President Ernest J. Martin, CLU, ChFC, CFP

Cincinnati Chapter FSP www.financialpro.org Solutions for a Secure Future (formerly the American Society of CLU & ChFC) Financial 2007-2008 BOARD OF DIRECTORS President Ernest J. Martin, CLU, ChFC, CFP

Grantor Retained Annuity Trusts in 2013: Tax-Efficient Estate Planning Techniques Leveraging GRATs to Preserve and Transfer Assets

Presenting a live 90-minute webinar with interactive Q&A Grantor Retained Annuity Trusts in 2013: Tax-Efficient Estate Planning Techniques Leveraging GRATs to Preserve and Transfer Assets WEDNESDAY, MARCH

Presenting a live 90-minute webinar with interactive Q&A Grantor Retained Annuity Trusts in 2013: Tax-Efficient Estate Planning Techniques Leveraging GRATs to Preserve and Transfer Assets WEDNESDAY, MARCH

Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

Caring for longer than a lifetime

Life insurance Caring for longer than a lifetime Your 5-minute Guide Life goes on prepare for it Your love for your family will live forever. However, we all know we won t live forever. Life insurance

Life insurance Caring for longer than a lifetime Your 5-minute Guide Life goes on prepare for it Your love for your family will live forever. However, we all know we won t live forever. Life insurance

Estate Planning. Insight on. Looking for a stimulus package for your estate plan?

Insight on Estate Planning April/May 2009 Looking for a stimulus package for your estate plan? Know the basics of basis A matter of principle A principle trust can help achieve your estate planning goals

Insight on Estate Planning April/May 2009 Looking for a stimulus package for your estate plan? Know the basics of basis A matter of principle A principle trust can help achieve your estate planning goals

A Guide to Estate Planning

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

Administrative Office 330 Wenneker Drive, St. Louis, MO 63124, Fax: , Issue: November 2013

Administrative Office 330 Wenneker Drive, St. Louis, MO 63124, 314.569.0218 www.financialpro.org/stlouis Fax: 314.567.1101, Issue: November 2013 St. Louis Mission Statement The Society of Financial Services

Administrative Office 330 Wenneker Drive, St. Louis, MO 63124, 314.569.0218 www.financialpro.org/stlouis Fax: 314.567.1101, Issue: November 2013 St. Louis Mission Statement The Society of Financial Services

CHAPTER FOURTEEN. EXISTING QPRTs COMMON SITUATIONS AND OPTIONS. November James A. Flaggert

CHAPTER FOURTEEN EXISTING QPRTs COMMON SITUATIONS AND OPTIONS November 2011 James A. Flaggert Davis Wright Tremaine LLP 1201 Third Avenue, Suite 2200 Seattle, WA 98101 Phone: (206) 757-8044 Fax: (206)

CHAPTER FOURTEEN EXISTING QPRTs COMMON SITUATIONS AND OPTIONS November 2011 James A. Flaggert Davis Wright Tremaine LLP 1201 Third Avenue, Suite 2200 Seattle, WA 98101 Phone: (206) 757-8044 Fax: (206)

Federal Estate and Gift Tax and Use of Applicable Exclusion Amount 3. Pennsylvania Inheritance Tax 5. Gifting Techniques 6

Prepared by Howard Vigderman Last Updated August 8, 2016 Federal Estate and Gift Taxes, Pennsylvania Inheritances Taxes and Measures to Reduce Them 2 Even with the federal estate tax exemption at an historically

Prepared by Howard Vigderman Last Updated August 8, 2016 Federal Estate and Gift Taxes, Pennsylvania Inheritances Taxes and Measures to Reduce Them 2 Even with the federal estate tax exemption at an historically

MEDICAID PLANNING. The facts... Assets in a revocable living trust are not protected and must be used to pay for the costs of long-term care.

MEDICAID PLANNING Assets in a revocable living trust are not protected and must be used to pay for the costs of long-term care. If you are married, your home is exempt and cannot be taken when applying

MEDICAID PLANNING Assets in a revocable living trust are not protected and must be used to pay for the costs of long-term care. If you are married, your home is exempt and cannot be taken when applying

About Seiler LLP. Trust & Estate Insights 2017 Seiler LLP. All rights reserved.

2017 About Seiler LLP For 60 years, Seiler LLP has provided advisory, tax and accounting services to some of the world s most affluent individuals, families, privately-held businesses and non-profit organizations.

2017 About Seiler LLP For 60 years, Seiler LLP has provided advisory, tax and accounting services to some of the world s most affluent individuals, families, privately-held businesses and non-profit organizations.

TRUST AND ESTATE PLANNING GLOSSARY

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

11/9/2012. Estate and Charitable Planning Before the End of IRS Circular 230. Historical Estate Tax Rates and Exemptions

Estate and Charitable Planning Before the End of 2012 SOL S. REIFER, J.D., LL.M. KYLE C. POST, J.D., LL.M. WRIGHT GINSBERG BRUSILOW P.C. 14755 PRESTON ROAD, SUITE 600 DALLAS, TEXAS 75254 972-788-1600 sreifer@wgblawfirm.com

Estate and Charitable Planning Before the End of 2012 SOL S. REIFER, J.D., LL.M. KYLE C. POST, J.D., LL.M. WRIGHT GINSBERG BRUSILOW P.C. 14755 PRESTON ROAD, SUITE 600 DALLAS, TEXAS 75254 972-788-1600 sreifer@wgblawfirm.com

Estate P LANNER. the. Roll with it Keep wealth in the family using rolling GRATs

the Estate P LANNER May/June 2006 Roll with it Keep wealth in the family using rolling GRATs Administrative checklist for after a family member passes away Tips for tax-wise charitable giving Too much

the Estate P LANNER May/June 2006 Roll with it Keep wealth in the family using rolling GRATs Administrative checklist for after a family member passes away Tips for tax-wise charitable giving Too much

Building a bridge to the future

An Educational Guide for Families and Individuals Building a bridge to the future Personalized Trust and Wealth Management Services Financial Strategies Managing the details of a friend or family member

An Educational Guide for Families and Individuals Building a bridge to the future Personalized Trust and Wealth Management Services Financial Strategies Managing the details of a friend or family member

Workplace Education Series

Preserving Your Savings for Future Generations (Estate Planning) Kelly Quinlan Regional Vice President, Estate Planning March 1, 2018 So, you would like to leave behind a legacy Your questions at this

Preserving Your Savings for Future Generations (Estate Planning) Kelly Quinlan Regional Vice President, Estate Planning March 1, 2018 So, you would like to leave behind a legacy Your questions at this