Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs

|

|

|

- Leo Parrish

- 5 years ago

- Views:

Transcription

1 Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs February, 2014 Contact us: AdvancedSales@voya.com This material is designed to provide general information for use by legal and tax counsel. It is not intended as, nor may it be considered, the legal opinion of Voya Life Companies on tax or other matters. Neither Voya nor its affiliated companies or representatives provide tax or legal advice. Private counsel alone may be responsible and relied upon for those purposes. Similarly, only qualified private legal counsel may recommend the application of this general information to any particular situation or prepare an instrument chosen to implement any design or strategy discussed herein. Many aspects of income and estate taxation and insurance law are uncertain and differences of opinion with respect to such matters frequently occur. In addition, state or local laws and procedural rules may have a material impact on the general discussion. As a result, the strategies discussed may not be suitable for everyone and each individual should consult with his or her own tax advisor and legal counsel before implementing any of the strategies discussed herein. Introduction to GRATs & Rolling GRATs The Grantor retained annuity trust ( GRAT ) is a flexible planning tool which can be used by wealthy clients to (i) reduce estate and gift taxes through an estate freeze, (ii) reduce gift taxes that could be incurred when funding an irrevocable life insurance trust ( ILIT ), or (iii) as an exit strategy for other estate planning techniques such as premium financing or private split dollar. What is a GRAT? A GRAT is a wealth transfer technique where an individual (the Grantor ) transfers assets to an irrevocable trust (the GRAT ) in exchange for a stream of payments (an annuity ) and designates remainder beneficiaries who will receive any assets left over in the trust at the end of the annuity term. In essence, a transfer to a GRAT is like a sale, only the payments for the property are characterized as an annuity that lasts for a term of years rather than as payments of principal and interest. The tax treatment of the transfer to a GRAT depends on the value of the annuity payments retained by the Grantor. If the payment stream to the Grantor is equal to the value of the asset contributed to the GRAT, then there are no gift taxes on the transfer (and any remainder passing to the GRAT beneficiaries will also pass free of gift taxes). 1 What Are Rolling GRATs? Rolling GRATs are a series of short-term GRATs strung together with the intent to increase efficiency and help reduce risk. Rather than having a single GRAT which returns payments for the asset for a period of years, the Grantor places the asset in a 2-year GRAT, and then transfers the payments received from the GRAT into new 2-year GRATs until the original trust term has been reached. The Rolling GRAT technique came to prominence in the famous Walton case which featured a series of 2-year Rolling GRATs. 2 While the focus of the Walton GRAT case was on whether a GRAT could be zeroed out for gift tax purposes, it also had the effect of publicizing the use of a series of short-term GRATs to reduce risk rather than relying on a single long-term GRAT to remove assets from an estate. 3 1 For a full discussion of the transfer tax treatment of GRATs, consult the special valuation rules of Chapter 14 of the Internal Revenue Code (IRC ). 2 Audrey J. Walton v. Commissioner; 115 T.C. No. 41; No (December 22, 2000). 3 Prior to the Walton decision (Audrey J. Walton v. Commissioner; 115 T.C. No. 41; No (December 22, 2000), there was some doubt as to whether a zeroed out GRAT was possible. Treasury Regulations dealing with GRATs included language indicating that it was impossible to have a zeroed out GRAT. See Reg (e), Example 5. In Walton, however, the Tax Court ruled that a right to receive a fixed amount for a term of years, provided that the right is a qualified interest under IRC 2702(b), should be valued for gift tax purposes without regard to life expectancy and thus overturned Example 5 of the Regulations.

2 How Does a Typical GRAT Work? Implementing a GRAT typically involves five steps: 1. Client creates a grantor trust. The first step is to have the client s attorney draft a grantor trust. This is an irrevocable trust which is specially designed so that the trust assets are excluded from the Grantor s estate for estate and gift tax purposes, but the assets are treated as belonging to the Grantor for income tax purposes. This allows the Grantor (your client) to buy and sell from the trust without incurring income taxes on the sales. At the same time, the Grantor has removed the trust assets from his or her estate. 2. Transfer assets to trust in exchange for an annuity. The second step is to transfer assets into the trust in exchange for an annuity. The annuity must be for a fixed amount and be for either a term of years or for the life or lives of the Grantor(s). Once inside the trust, the assets can be used to purchase life insurance. Or, if there is already life insurance, the assets can be used for an exit strategy: to pay off the loan for premium financing or buy out a policy funded through private split dollar. 3. Trust makes annuity payments. The third step is to have the trust make scheduled annual payments to the Grantor. As already mentioned, the IRS requires GRATs to make fixed annuity payments. The payments must be based on either a stated dollar amount or a stated percentage of the initial value of the assets contributed to the trust. Although the IRS calls the payments fixed, it does allow the scheduled payments to systematically increase or decrease by as much as 20% a year. 4. Grantor pays income taxes for the trust. Step four is for the Grantor to pay income taxes on the trust s income. This is a tax-free gifting opportunity for the Grantor. If he or she had kept the assets he or she would pay these taxes. If he or she had given the assets away to his or her children, they would have to pay the taxes. If he or she wanted to pay the taxes for the children he or she would have to pay gift taxes, too. By paying taxes for the trust, he or she makes a tax-free gift and allows the trust assets to grow for his or her children or other remainder beneficiaries designated in the GRAT. 5. At end of GRAT term, remaining assets pass to beneficiaries tax free. Finally, if the Grantor outlives the term of the GRAT, the trust assets will pass to his or her beneficiaries free of any estate taxes. If the trust owns a life insurance policy, the death benefits will pass to the beneficiaries free of income taxes as well. If the Grantor dies before the GRAT term has expired, then all of the trust assets are brought back into the Grantor s estate. So clients should try to limit the length of a GRAT and may even want to purchase life insurance to provide protection against premature death during the GRAT term. Grantor Assets contributed to trust Annuity payments GRAT Remainder Beneficiaries* *Beneficiaries can be individuals or an ILT. 2

3 Advantages of the GRAT The GRAT technique offers clients the following potential benefits: Estate Freeze Future asset growth is removed from the Grantor s estate. No Pre-Funding Required Unlike an installment sale to a grantor trust, a GRAT does not require the Grantor to gift money into the trust prior to the transaction. Exit Strategy A GRAT can be used to provide an ILIT with funds to repay loans and terminate premium financing or private split dollar arrangements. Disadvantages of the GRAT Of course, the GRAT technique also has some possible disadvantages: Estate Inclusion If the client dies before the GRAT term has finished, all of the assets are brought back into his or her estate. 4 Performance Risk The GRAT technique only works if the assets contributed to the trust grow at a higher rate than the 7520 rate used by the IRS to value the annuity payments. How Do Rolling GRATs Work? Instead of relying on a single long-term GRAT, Rolling GRATs use a series of short-term GRATs. The same original contribution amount is used to fund the Rolling GRATs as would have been used to fund a long-term GRAT, but the GRAT term is limited to two years. As payments come out of each 2-year GRAT, the Grantor contributes these amounts to successive 2-year GRATs. Thus, for example, if the Grantor originally considers funding a 10-year GRAT, the Rolling GRAT strategy would replace this with a series of eight 2-year GRATs as follows: (Year 1) GRAT 1 2-year GRAT funded with original contribution amount; (Year 2) GRAT 2 2-year GRAT funded with 1st payment from GRAT 1; (Year 3) GRAT 3 2-year GRAT funded with 2nd payment from GRAT 1 and 1st payment from GRAT 2. Remainder from GRAT 1 paid to beneficiary. (Year 4) (Year 5) (Year 6) (Year 7) (Year 8) (Year 9) (Year 10) GRAT 4 2-year GRAT funded with 2nd payment from GRAT 2 and 1st payment from GRAT 3. Remainder from GRAT 2 paid to beneficiary. GRAT 5 2-year GRAT funded with 2nd payment from GRAT 3 and 1st payment from GRAT 4. Remainder from GRAT 3 paid to beneficiary. GRAT 6 2-year GRAT funded with 2nd payment from GRAT 4 and 1st payment from GRAT 5. Remainder from GRAT 4 paid to beneficiary. GRAT 7 2-year GRAT funded with 2nd payment from GRAT 5 and 1st payment from GRAT 6. Remainder from GRAT 5 paid to beneficiary. GRAT 8 2-year GRAT funded with 2nd payment from GRAT 6 and 1st payment from GRAT 7. Remainder from GRAT 6 paid to beneficiary. Remainder from GRAT 7 paid to beneficiary. Remainder from GRAT 8 paid to beneficiary. 4 If the Grantor fails to survive the selected term for the GRAT, a portion of the GRAT assets will be included in the Grantor s estate. IRC The portion of GRAT assets that will be included in the Grantor s estate is the lesser of the present value of the remaining annuity payments (calculated using the 7520 rate effective for the Grantor s date of death or for the alternate valuation date if the estate elects to use alternate valuation) or the total value of the remaining GRAT assets. See the final GRAT regulations issued in 2008 (73 F.R ). 3

4 What Are the Advantages of Rolling GRATs? Rolling GRATs offer clients several potential advantages over the use of a single long-term GRAT. The most significant advantage is the reduction of the risk for estate inclusion. If a Grantor dies before the end of a GRAT term, some or all of the assets remaining in the GRAT may be included in the Grantor s estate. By using a series of short-term GRATs, the Grantor is assured of moving at least some assets out of his or her estate as each short-term GRAT reaches maturity. Additionally, using a series of short-term GRATs and re-contributing payments received from the GRATs into successive Rolling GRATs may also be more efficient over the long run than relying on a single GRAT. Even if the Grantor outlives the term of a long-term GRAT, he or she may have been able to remove more assets from the estate by using a series of short-term GRATs over the same period. This will be true if the discount rate applied to the short-term GRATs is the same as the rate applied to the long-term GRAT. On the other hand, if the IRS discount rate prescribed under 7520 increases after the year of initial funding, Rolling GRATs may prove less efficient than a long-term GRAT. But even with this risk, Rolling GRATs have the advantage of starting to get assets out of the estate earlier than long-term GRATs and reducing the all-ornothing potential for estate inclusion that comes with long-term GRATs. For an example of the comparison between a long-term GRAT and Rolling GRATs, see Appendix A at the end of this White Paper. Uses of GRATs & Rolling GRATs GRATs and Rolling GRATs have several applications in estate planning and life insurance. GRATs can be used for an estate freeze, as a way to reduce gifting needs for irrevocable life insurance trusts ( ILITs ), and as an exit strategy for techniques such as premium financing. What is an Estate Freeze? One of the primary uses for GRATs is to help wealthy clients create an estate freeze. Financial professionals use the term freeze to describe an attempt to move all future asset growth outside of an individual s estate. Generally, an estate freeze is any technique that allows a person to fix or freeze an asset s value for estate and gift tax purposes at a given time, so that any future appreciation in value of the asset can pass to selected recipients at no additional tax cost. The goal of an estate freeze is to limit the date-of-death value of an asset or an estate to the value the asset or estate has today. GRATs contribute to an estate freeze by leveraging the difference between anticipated growth on estate assets and the standard growth expectation used by the IRS to value gift transfers. For any given month, the IRS publishes a table of rates to be used to measure the value of gifts, loans, and annuities. The rates published include short-term, mid-term, and long-term rates for valuing loans, and the 7520 rate for valuing annuity payments. These rates reflect the IRS view on what growth rates a typical asset should experience in future years. The rate applied to measure the value of the remainder interest in a GRAT is the 7520 rate. 5 A GRAT can create an estate freeze to the extent assets contributed to the trust out-perform the rate established by the IRS. For example, if a GRAT is established at a time when the 7520 rate is 5.0%, and assets contributed to the GRAT actually grow at an annual rate of 8.0%, then the extra 3.0% of growth is removed from the Grantor s estate free of any gift or estate taxes (assuming the Grantor survives for the entire term of the GRAT). 6 Thus, GRATs work best with assets that are expected to experience high growth during the GRAT s term. 4 5 IRC 2702(a)(2)(B). 6 IRC 2039.

5 How Can GRATs Be Used to Reduce Gift Taxes for ILITs? In addition to being used as a stand-alone technique for reducing estate and gift taxes through estate freezes, GRATs can be used in conjunction with irrevocable life insurance trusts ( ILITs ) to reduce the gift taxes that may be incurred when funding large ongoing life insurance premiums. Financial professionals use ILITs to help clients create a source of funds to pay anticipated estate taxes without subjecting those funds to taxation. 7 The trustee of the ILIT purchases life insurance on the Grantor and the trust agreement provides direction on how the death benefit should be applied. The Grantor (and his or her spouse) must make contributions to the ILIT so that the trustee will have funds to pay the insurance premiums. The ILIT may include withdrawal rights (often called Crummey Powers ) for trust beneficiaries which allow the Grantor s contributions to qualify as present interest gifts meaning that the Grantor can use his or her annual gift exclusion rather than using up a portion of his or her available lifetime exclusion. A problem arises for wealthier clients who decide to purchase larger life insurance policies to meet estate liquidity needs. As of 2014, as indexed for inflation, an individual s annual gift exclusion is limited to $14,000 per beneficiary (or $28,000 if married and the spouse consents to gift-splitting). 8 If the life insurance policy purchased by the ILIT calls for annual premiums that are greater than $14,000/$28,000 per trust beneficiary, the Grantor will have to use some of his or her lifetime gift exclusion each year premiums are due. To avoid this problem, clients can use a GRAT to fund the ILIT. Rather than naming children or other family members as the remainder beneficiary of the GRAT, the Grantor names the ILIT as the beneficiary. A series of short-term GRATs (2-year or 3-year terms) can be used to create an ongoing source of gift tax-free contributions to the ILIT which will provide funds for the ILIT trustee to pay insurance premiums. What Is an Exit Strategy? GRATs can be especially useful as an exit strategy for other wealth transfer techniques. All wealth transfer strategies include some element of risk. The level of risk is higher for some strategies than others. And for some strategies such as premium financing, split dollar, and private split dollar the level of risk increases with time. An exit strategy is a technique clients can use to reduce risk by providing the funds needed to terminate wealth transfer strategies that become too expensive. Premium financing, for example, carries an interest rate risk i.e., there is a risk that interest rates will increase over time. Similarly, split dollar and private split dollar become more expensive over time because the measure of the gift the economic benefit or term costs of life insurance coverage increases as the insured becomes older. For each technique, the client can choose to accept this risk, avoid this risk, or plan for this risk by having an exit strategy. The GRAT works as an exit strategy for premium financing, private split dollar, and similar techniques by creating a set of funds which can be used to terminate a transaction when it is no longer producing economic advantages to the client. In the case of premium financing, for example, if interest rates are fixed for a period of time the client can fund a GRAT that will provide a remainder benefit to the ILIT at the end of the fixed interest rate period. If interest rates increase, the ILIT trustee can use the funds received from the GRAT to pay off the loan. If interest rates do not increase, the trustee can hold onto the funds for use in terminating the financing arrangement in the future. Meanwhile, the assets passed to the ILIT from the GRAT are also moved outside of the Grantor s estate. 7 Under IRC 2042, proceeds of a life insurance policy insuring the life of the decedent are included in the decedents estate if the proceeds are payable to the estate or if the decedent retained any incidents of ownership in the life insurance policy at the time of death. 8 IRC 2503(b) provides that the first $10,000 of gifts to a donee may be excluded from taxable gifts provided the transfer is of a present interest. Section 2503(b)(2) provides that for gifts after 1998, this amount is to be adjusted for inflation. As of 2014, the annual exclusion amount is $14,000 per donee. 5

6 Gift and Estate Tax Consequences of GRATs The purpose of the GRAT transaction is to move assets out of the Grantor s estate and into the hands of children and heirs with little or no gift or estate taxes. To accomplish this goal, the Grantor sets the annuity payments from the trust at a level that is high enough that no gift results upon the contribution of assets to the trust. Whether the GRAT results in a gift depends on the value of the remainder interest in the trust determined on the date the GRAT is created. To determine the value of the remainder interest, the present value of the annuity stream to be paid to the Grantor is subtracted from the fair market value of the assets contributed to the trust. 9 The IRS characterizes a GRAT as a transfer to a trust with a retained interest i.e., the right to receive annuity payments from the trust is an interest retained by the Grantor. For gift tax purposes, transfers to trusts with retained interests are subject to special valuation rules outlined in the Internal Revenue Code. 10 Under the special valuation rules, the value of the gift to the remainder beneficiaries is determined by taking the total value of the assets transferred to the trust and subtracting the value of the interest retained by the Grantor. But if the retained interest of the Grantor does not meet the requirements of a qualified interest, the value of the retained interest will be treated as being zero. 11 This means that if a transfer does not meet the requirements of 2702, the full value of the transferred assets will be treated as a gift even though the Grantor is receiving payments for the assets. To be a qualified interest, the interest retained upon the transfer of property to a trust must be either the right to receive payments of a fixed amount no less than annually (GRAT), or the right to receive payments no less than annually of a fixed percentage of the value (determined annually) of the trust assets (Grantor retained unitrust or GRUT ). 12 In the case of a GRAT, the fixed amount may be expressed in terms of dollars or as a percentage of the initial total value of the assets contributed. 13 GRATs may provide payments for a term of years or for the life of the Grantor. Where the retained interest meets the requirements of a qualified interest, the value of the income stream is determined by using the discount factor published by the IRS under IRC The 7520 rate is published monthly and is 120% of the mid-term applicable federal rate ( AFR ) for the month rounded to the nearest two-tenths of a percent. Ideally, a Grantor wants to fix payments from the GRAT at a level that would result in no gift taxes. To do this, the Grantor sets the payments at an amount that would be valued as equal to the fair market value of the assets transferred to the trust. 14 This results in a value of zero for the GRAT s remainder interest, meaning that there is no gift in the transaction. While the IRS has argued that all GRATs must involve some gift, a recent tax case held that, so long as the annuity payments are set high enough, a transfer to a GRAT can be structured so that there is no gift (such GRATs are sometimes referred to as Walton GRATs or zeroed out GRATs ). 15 Finally, it should be noted that the beneficial gift tax treatment applies only if the Grantor outlives the GRAT term. 16 If the Grantor dies before the GRAT has terminated, a portion of the trust assets will be brought back into the Grantor s estate. 17 This is true even if the GRAT calls for annuity payments to be made to the Grantor s estate for the full remainder of the trust term. Thus, long-term GRATs carry a risk that assets will be included in the Grantor s estate if he or she does not survive the GRAT term. 6 9 IRC 2702(a)(2)(B). 10 IRC IRC 2702(a)(2)(A). 12 IRC 2702(b). 13 Final regulations under 2702 allow some flexibility for the term fixed amount. Annuity payments can be systematically increased or decreased by up to 20% per year. A GRAT which provides for increasing annual payments is sometimes referred to as a Ramp-Up GRAT. 14 IRC 2702(a)(2)(B). 15 Walton v. Commissioner, 115 T.C. No. 41 (12/22/2000). 16 IRC The portion of GRAT assets that will be included in the Grantor s estate is the lesser of the present value of the remaining annuity payments (calculated using the 7520 rate effective for the Grantor s date of death or for the alternate valuation date if the estate elects to use alternate valuation) or the total value of the remaining GRAT assets. See the final GRAT regulations issued in 2008 (73 F.R ).

7 Income Tax Consequences of a Grantor Trust As indicated above, a GRAT is a grantor trust that, in exchange for the Grantor s contribution of assets, makes annuity payments to the Grantor which qualify as a retained interest under IRC This raises two questions: (i) What is a grantor trust?; and (ii) What are the income tax consequences of using a grantor trust? What Is a Grantor Trust? Grantor trust is a term used in the Internal Revenue Code to describe any trust over which the Grantor or other owner retains the power to control or direct the trust s income or assets. 18 In essence, a grantor trust is a trust that is not recognized as a separate entity for income tax purposes, but which may be a distinct entity for estate and gift tax purposes. The Grantor (also known as trustor, settlor, or creator) is the creator of the trust relationship and is the owner of the assets initially contributed to the trust. The Grantor establishes in the trust instrument the terms and provisions of the trust relationship between the Grantor, the trustee, and the beneficiary. If a Grantor retains certain powers over or benefits in a trust, the income of the trust will be taxed to the Grantor, rather than to the trust. 19 Examples of such powers include: the power to decide who receives income, the power to vote or to direct the vote of the stock held by the trust or to control the investment of the trust funds, and the power to revoke the trust, etc. All revocable trusts are by definition grantor trusts. An irrevocable trust can be treated as a grantor trust if any of the grantor trust definitions contained in IRC 671, 673, 674, 675, 676, or 677 are met. If a trust is a grantor trust, then, for income tax purposes, the Grantor is treated as the owner of the assets, the trust is disregarded as a separate tax entity, and all income is taxed to the Grantor. Income Tax Consequences There are a number of income tax consequences to having a trust structured as a grantor trust : 1. Trust income is taxed to the Grantor. The first, and most obvious, consequence is that any income generated inside the trust is taxed to the Grantor. This applies both to ordinary income from receipt of dividends and to capital gains generated from the sale of trust assets. Although it may be permissible for the trust to reimburse the Grantor for payment of income taxes, there should be no requirement, agreement, or understanding that the trust will automatically do so. If such an agreement or understanding exists, the IRS has ruled that the trust assets will be included in the Grantor s estate under IRC The fact that the Grantor is responsible for income taxes of a grantor trust should not necessarily be viewed negatively. Many financial professionals consider the Grantor s responsibility for income taxes as an advantage of the grantor trust arrangement. This is because, in essence, the payment of such taxes is a tax-free gift to the trust beneficiaries. If the trust were required to pay the income taxes, this would reduce the amount of assets ultimately passing to the trust beneficiaries. In fact, if the Grantor wanted to add funds to the trust to pay taxes and prevent this loss of benefits, he or she would have to make a taxable gift. Moreover, the fact that taxes are being paid by an outside source increases the likelihood that trust assets will grow at a rate higher than the rate prescribed by the IRS to value the initial transfer to the trust. 18 IRC See Rev. Rul Rev. Rul

8 2. Transfers between Grantor and trust ignored. A second tax consequence to grantor trust status is that transfers between the Grantor and the trust will be ignored for income tax purposes. Whether the Grantor contributes assets to the trust in exchange for annuity payments or sells assets to the trust in exchange for a note requiring payments of principal and interest, there is no transfer for income tax purposes. This means that the contribution or sale does not trigger any recognition of capital gains by the Grantor. It also means that payments from the trust, whether in the form of annuity payments or principal and income payments, do not create income for the Grantor. For all income tax purposes, the grantor trust is treated as if it doesn t exist the Grantor is responsible for the same income taxes as if he or she continued to own the assets outright and no new income is created by payments from the trust. 3. No basis adjustment for contributed assets. A third tax consequence to grantor trust treatment is that the basis of assets transferred to a grantor trust is unaffected by the transfer, regardless of how the assets are transferred into the trust. Because transfers between a Grantor and a grantor trust are ignored for income tax purposes, there is no adjustment to the basis of assets that are sold to the trust. This is consistent with the fact that the Grantor does not recognize any gain on such transactions. It also means that trust beneficiaries will not benefit from a step-up in basis at the Grantor s death. 4. Transfer for value problems avoided. A final set of tax consequences from grantor trust status has to do with life insurance. Life insurance is a unique asset under the Internal Revenue Code with specialized tax treatment. In particular, death benefits received from a life insurance policy are not ordinarily subject to income taxes. 21 The income tax-free nature of such benefits, however, can be lost if, during the insured s life, the policy is subject to a transfer for value and the transfer does not fall into one of several exceptions to the transfer for value rules. 22 Because a grantor trust is ignored for income tax purposes, a transfer of a life insurance policy between the Grantor and the trust will not be characterized as a transfer for value. Moreover, if the Grantor is the person insured under the policy, transfers to the grantor trust will qualify as a transfer to the insured which is an exception under the transfer for value rules. 23 Conclusion GRATs and Rolling GRATs are powerful planning tools which can be used to help transfer assets out of an estate with little or no gift tax consequences. GRATs are especially useful for creating estate freezes, reducing gifts to ILITs, and as an exit strategy for premium financing. Rolling GRATs can be used to reduce the risk of estate inclusion that would be caused by a Grantor s early death. 21 IRC 101(a)(1). 22 IRC 101(a)(2) See, e.g., Rev. Rul

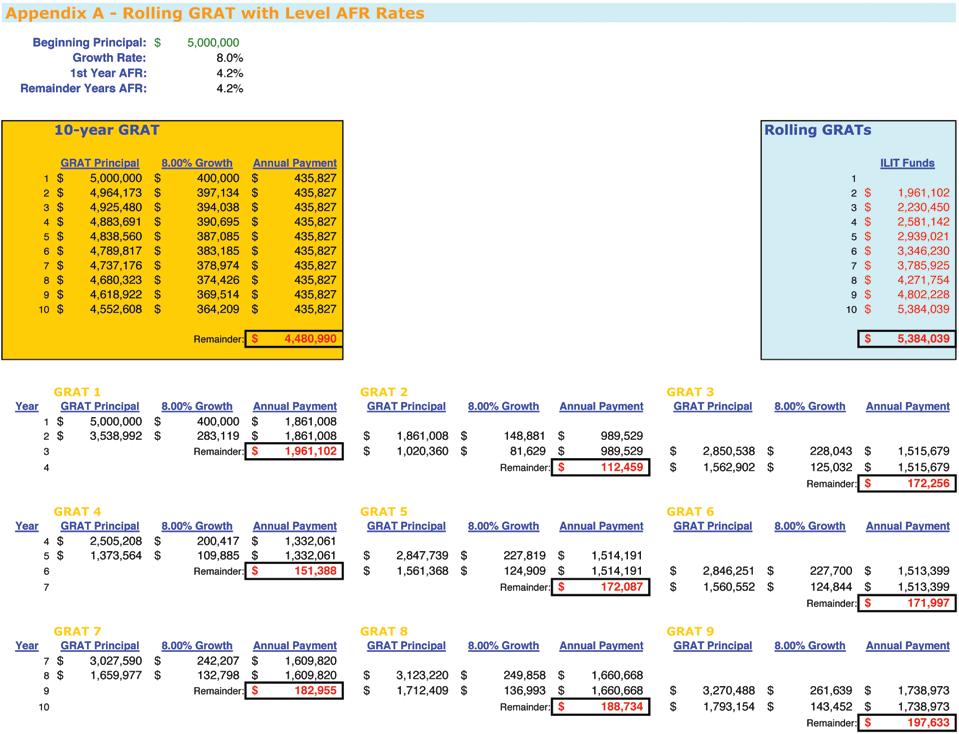

9 Appendix A 10-year GRAT v. Rolling GRAT The following tables compare the effectiveness of a single 10-year GRAT versus a series of 2-year Rolling GRATs. For both hypothetical scenarios it is assumed that the Grantor will contribute $5 million to a GRAT in the first year, it is also assumed the assets will receive a 30% discount. It is assumed that the assets used will experience 8.0% annual growth in all years. And it is assumed that the IRS prescribed applicable federal rate (AFR) for all years is 4.2%. The tables show, at the end of each year, how much money has been returned to the Grantor (blue), how much money is retained in a GRAT or GRATs (orange), and how much money has been transferred out of the Grantor s estate (light green). 10-year GRAT $12,000,000 $10,000,000 $8,000,000 $6,000,000 $4,000,000 $2,000, ILIT Assets $4,480,990 GRAT Assets $4,964,173 $4,925,480 $4,883,691 $4,838,560 $4,789,817 $4,737,176 $4,680,323 $4,618,922 $4,552,608 Grantor Assets $435,827 $906,520 $1,414,869 $1,963,885 $2,556,823 $3,197,196 $3,888,799 $4,635,730 $5,442,415 $6,313,635 This hypothetical example is for illustrative purposes only and should not be deemed a representation of past or future results. This example does not represent any specific product, nor does it reflect sales charges or other expenses that may be required for some investments. Actual annual growth and AFR rates may vary each year. 9

10 Rolling GRATs $12,000,000 $10,000,000 $8,000,000 $6,000,000 $4,000,000 $2,000,000 ILIT Assets GRAT Assets Grantor Assets $1,961,102 $2,230,450 $2,581,142 $2,939,021 $3,346,230 $3,785,925 $4,271,754 $4,802,228 $5,384,039 $5,400,000 $3,870,898 $4,068,110 $4,221,303 $4,407,619 $4,588,142 $4,783,197 $4,982,897 $1,793,154 $3,399,641 $5,410,586 This hypothetical example is for illustrative purposes only and should not be deemed a representation of past or future results. This example does not represent any specific product, nor does it reflect sales charges or other expenses that may be required for some investments. Actual annual growth and AFR rates may vary each year. 10

11 11

12 These materials are not intended to and cannot be used to avoid tax penalties and they were prepared to support the promotion or marketing of the matters addressed in this document. Each taxpayer should seek advice from an independent tax advisor. The Voya Life Companies and their agents and representatives do not give tax or legal advice. This information is general in nature and not comprehensive, the applicable laws may change and the strategies suggested may not be suitable for everyone. Clients should seek advice from their tax and legal advisors regarding their individual situation. Life insurance products are issued by ReliaStar Life Insurance Company (Minneapolis, MN), ReliaStar Life Insurance Company of New York (Woodbury, NY) and Security Life of Denver Insurance Company (Denver, CO). Variable universal life insurance products are distributed by Voya America Equities, Inc. Within the state of New York, only ReliaStar Life Insurance Company of New York is admitted and its products issued. All are members of the Voya family of companies Voya Services Company. All rights reserved. CN /01/2014 Voya.com

Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs. Producer Guide. For agent use only. Not for public distribution.

and Rolling GRATs. Producer Guide. For agent use only. Not for public distribution.") Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs Producer Guide Introduction to GRATs and Rolling GRATs The Grantor Retained Annuity Trust ( GRAT ) is a flexible planning tool which can be used

Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs Producer Guide Introduction to GRATs and Rolling GRATs The Grantor Retained Annuity Trust ( GRAT ) is a flexible planning tool which can be used

Preserving Family Wealth with an Estate Freeze. cn ING North America Insurance Corporation

Walton GRAT: Preserving Family Wealth with an Estate Freeze Thanks for sharing your time with me today. I d like to tell you about a powerful and flexible estate planning idea. This strategy is called

Walton GRAT: Preserving Family Wealth with an Estate Freeze Thanks for sharing your time with me today. I d like to tell you about a powerful and flexible estate planning idea. This strategy is called

WEALTH STRATEGIES. GRATs and Sale to IDGTs: Estate Freeze Techniques

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA GRATs and Sale to IDGTs: Estate Freeze Techniques FREQUENTLY ASKED QUESTIONS ESTATE PLANNING How do two of the techniques used by wealthy clients

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA GRATs and Sale to IDGTs: Estate Freeze Techniques FREQUENTLY ASKED QUESTIONS ESTATE PLANNING How do two of the techniques used by wealthy clients

Giving is a part of life. Charitable Giving With Life Insurance

Giving is a part of life Charitable Giving With Life Insurance If you are interested in giving more to charity, life insurance may be able to help. When properly implemented, a life insurance policy may

Giving is a part of life Charitable Giving With Life Insurance If you are interested in giving more to charity, life insurance may be able to help. When properly implemented, a life insurance policy may

THE ESTATE PLANNER S SIX PACK

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Effective Strategies for Wealth Transfer

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Executive Benefits for Nonprofit & Tax-Exempt Organizations

Executive Benefits for Nonprofit & Tax-Exempt Organizations Recruit, retain, and reward your top talent with nonqualified retirement or estate planning benefits As a nonprofit or tax-exempt organization,

Executive Benefits for Nonprofit & Tax-Exempt Organizations Recruit, retain, and reward your top talent with nonqualified retirement or estate planning benefits As a nonprofit or tax-exempt organization,

Passing on family wealth without making gifts

Passing on family wealth without making gifts New wealth transfer opportunities As part of a year-end agreement to avoid the Fiscal Cliff crisis, Congress passed the American Taxpayer Relief Act of 0 (ATRA

Passing on family wealth without making gifts New wealth transfer opportunities As part of a year-end agreement to avoid the Fiscal Cliff crisis, Congress passed the American Taxpayer Relief Act of 0 (ATRA

White Paper: Avoiding Incidents of Policy Ownership to Eliminate Estate Tax

White Paper: Avoiding Incidents of Policy Ownership to Eliminate Estate Tax MARKET TREND: As planning approaches and products become more complex, care must be taken to avoid the retention or acquisition

White Paper: Avoiding Incidents of Policy Ownership to Eliminate Estate Tax MARKET TREND: As planning approaches and products become more complex, care must be taken to avoid the retention or acquisition

Advanced marketing concepts. Brought to you by the Advanced Consulting Group of Nationwide

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Wealth Transfer and Charitable Planning Strategies. Handbook

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Shared Dollar Life Insurance: An inter-generational approach to retirement planning

Shared Dollar Life Insurance: An inter-generational approach to retirement planning What will retirement look like for our children? If you are like most working people, from time to time you think about

Shared Dollar Life Insurance: An inter-generational approach to retirement planning What will retirement look like for our children? If you are like most working people, from time to time you think about

GRANTOR RETAINED ANNUITY TRUSTS

GRANTOR RETAINED ANNUITY TRUSTS A Private Clients Group White Paper Grantor Retained Annuity Trusts are one estate planning tool used to reduce inheritance taxes by removing assets from an estate. A Grantor

GRANTOR RETAINED ANNUITY TRUSTS A Private Clients Group White Paper Grantor Retained Annuity Trusts are one estate planning tool used to reduce inheritance taxes by removing assets from an estate. A Grantor

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS You should consider creating an Intentionally Defective Irrevocable Trust ( IDIT ) and gifting assets to

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS You should consider creating an Intentionally Defective Irrevocable Trust ( IDIT ) and gifting assets to

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

THE SCIENCE OF GIFT GIVING After the Tax Relief Act. Presented by Edward Perkins JD, LLM (Tax), CPA

, CPA") THE SCIENCE OF GIFT GIVING After the Tax Relief Act Presented by Edward Perkins JD, LLM (Tax), CPA THE SCIENCE OF GIFT GIVING AFTER THE TAX RELIEF ACT AN ESTATE PLANNING UPDATE Written and Presented by

THE SCIENCE OF GIFT GIVING After the Tax Relief Act Presented by Edward Perkins JD, LLM (Tax), CPA THE SCIENCE OF GIFT GIVING AFTER THE TAX RELIEF ACT AN ESTATE PLANNING UPDATE Written and Presented by

Business Owner s Bonus Plan. Producer Guide. For agent/registered representative use only. Not for public distribution.

Business Owner s Bonus Plan Producer Guide For agent/registered representative use only. Not for public distribution. Business Owner s Bonus Plan Producer Guide The Business Owner s Bonus Plan is a personally

Business Owner s Bonus Plan Producer Guide For agent/registered representative use only. Not for public distribution. Business Owner s Bonus Plan Producer Guide The Business Owner s Bonus Plan is a personally

Double Discounted Transfers

Advanced Markets planning perspective estate planning Double Discounted Transfers The Silver Lining After the Economic Downturn It seems clear that estate taxes are here to stay. For people who are likely

Advanced Markets planning perspective estate planning Double Discounted Transfers The Silver Lining After the Economic Downturn It seems clear that estate taxes are here to stay. For people who are likely

Leveraging wealth transfer using a sale to a defective grantor trust

Sale to a Grantor Trust Strategy Leveraging wealth transfer using a sale to a defective grantor trust Not a bank or credit union deposit, obligation or guarantee May lose value Not FDIC or NCUA/NCUSIF

Sale to a Grantor Trust Strategy Leveraging wealth transfer using a sale to a defective grantor trust Not a bank or credit union deposit, obligation or guarantee May lose value Not FDIC or NCUA/NCUSIF

Charitable Planning CLIENT GUIDE

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Intentionally Defective (?) Grantor Trusts

Grantor Trusts") Intentionally Defective (?) Grantor Trusts Owen@GivnerKaye.com 1 What We Will Cover [Part 1]: 1. How Did The Grantor Trust Rules Originate? P. 3 2. Common Examples of Grantor Trusts. P. 4 3. What Do We

Intentionally Defective (?) Grantor Trusts Owen@GivnerKaye.com 1 What We Will Cover [Part 1]: 1. How Did The Grantor Trust Rules Originate? P. 3 2. Common Examples of Grantor Trusts. P. 4 3. What Do We

Estate Planning for Small Business Owners

Estate Planning for Small Business Owners HOSTED BY OCEAN FIRST BANK PRESENTED BY MONZO CATANESE HILLEGASS, P.C. SPEAKER: DANIEL S. REEVES, ESQUIRE Topics Tax Overview Trust Ownership Intentionally Defective

Estate Planning for Small Business Owners HOSTED BY OCEAN FIRST BANK PRESENTED BY MONZO CATANESE HILLEGASS, P.C. SPEAKER: DANIEL S. REEVES, ESQUIRE Topics Tax Overview Trust Ownership Intentionally Defective

GIFTING. I. The Basic Tax Rules of Making Lifetime Gifts[1] A Private Clients Group White Paper

![GIFTING. I. The Basic Tax Rules of Making Lifetime Gifts[1] A Private Clients Group White Paper](/thumbs/89/98748865.jpg "GIFTING. I. The Basic Tax Rules of Making Lifetime Gifts[1] A Private Clients Group White Paper") GIFTING A Private Clients Group White Paper Among the goals of most comprehensive estate plans is the reduction of federal and state inheritance taxes. For this reason, a carefully prepared Will or Revocable

GIFTING A Private Clients Group White Paper Among the goals of most comprehensive estate plans is the reduction of federal and state inheritance taxes. For this reason, a carefully prepared Will or Revocable

The Estate Planner s Passthrough or Passback Entity of Choice the Grantor Trust (Part Two)

") The Estate Planner s Passthrough or Passback Entity of Choice the Grantor Trust (Part Two) 1. A Tree is not a Tree When You call it a Bush This column discussed in the edition of the JPTE the importance

The Estate Planner s Passthrough or Passback Entity of Choice the Grantor Trust (Part Two) 1. A Tree is not a Tree When You call it a Bush This column discussed in the edition of the JPTE the importance

Spousal Lifetime Access Trust (SLAT)

") Spousal Lifetime Access Trust (SLAT) Concept A Spousal Lifetime Access Trust (SLAT) is an irrevocable trust that can own permanent life insurance and/or other assets. A SLAT permits the non-insured spouse

Spousal Lifetime Access Trust (SLAT) Concept A Spousal Lifetime Access Trust (SLAT) is an irrevocable trust that can own permanent life insurance and/or other assets. A SLAT permits the non-insured spouse

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

Intergenerational split dollar.

Taxation - Income, Estate, and Gift Intergenerational split dollar. Summary. In Estate of Morrissette, 1 the U.S. Tax Court granted summary judgment, holding that intergenerational split dollar may be

Taxation - Income, Estate, and Gift Intergenerational split dollar. Summary. In Estate of Morrissette, 1 the U.S. Tax Court granted summary judgment, holding that intergenerational split dollar may be

Comprehensive Charitable Planning

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

CHAPTER 8 Trusts DISCUSSION QUESTIONS

CHAPTER 8 Trusts DISCUSSION QUESTIONS 1. Why are trusts used in estate planning? Trusts are used in estate planning to provide for the management of assets and flexibility in the operation of the estate

CHAPTER 8 Trusts DISCUSSION QUESTIONS 1. Why are trusts used in estate planning? Trusts are used in estate planning to provide for the management of assets and flexibility in the operation of the estate

BASICS * Irrevocable Life Insurance Trusts

KAREN S. GERSTNER & ASSOCIATES, P.C. 5615 Kirby Drive, Suite 306 Houston, Texas 77005-2448 Telephone (713) 520-5205 Fax (713) 520-5235 www.gerstnerlaw.com BASICS * Irrevocable Life Insurance Trusts Synopsis

KAREN S. GERSTNER & ASSOCIATES, P.C. 5615 Kirby Drive, Suite 306 Houston, Texas 77005-2448 Telephone (713) 520-5205 Fax (713) 520-5235 www.gerstnerlaw.com BASICS * Irrevocable Life Insurance Trusts Synopsis

Grantor Trusts. Maine Tax Forum

Grantor Trusts Maine Tax Forum Jeremiah W. Doyle IV Senior Vice President BNY Mellon Private Wealth Management Boston, MA jere.doyle@bnymellon.com (617) 722-7420 November, 2017 1 Grantor Trusts AGENDA

Grantor Trusts Maine Tax Forum Jeremiah W. Doyle IV Senior Vice President BNY Mellon Private Wealth Management Boston, MA jere.doyle@bnymellon.com (617) 722-7420 November, 2017 1 Grantor Trusts AGENDA

A Guide to Estate Planning

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

Sale to a Grantor Trust (SAGT)

") Sale to a Grantor Trust (SAGT) Advanced Markets Client Guide An innovative estate planning tool John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York

Sale to a Grantor Trust (SAGT) Advanced Markets Client Guide An innovative estate planning tool John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York

Grantor Annuity Trust A LEGACY OPPORTUNITY IN A LOW INTEREST RATE ENVIRONMENT

Grantor Annuity Trust A LEGACY OPPORTUNITY IN A LOW INTEREST RATE ENVIRONMENT The Prudential Insurance Company of America 0266054-00005-00 Ed. 06/2016 Exp. 12/29/2017 ABOUT THIS BROCHURE This brochure

Grantor Annuity Trust A LEGACY OPPORTUNITY IN A LOW INTEREST RATE ENVIRONMENT The Prudential Insurance Company of America 0266054-00005-00 Ed. 06/2016 Exp. 12/29/2017 ABOUT THIS BROCHURE This brochure

Temporary Estate, Gift and GST Tax Laws Provide Unprecedented Opportunities in 2012

Month Year Temporary Estate, Gift and GST Tax Laws Provide Unprecedented Opportunities in 2012 BY RENEE M. GABBARD, LISA M. LAFOURCADE & MEGAN S. ACOSTA It appears that the current favorable estate, gift

Month Year Temporary Estate, Gift and GST Tax Laws Provide Unprecedented Opportunities in 2012 BY RENEE M. GABBARD, LISA M. LAFOURCADE & MEGAN S. ACOSTA It appears that the current favorable estate, gift

numer cal anal ysi shown, esul nei her guar ant ees nor ect ons, and act ual esul may gni cant Any assumpt ons est es, on, her val ues hypot het cal

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Understanding TRUSTS. A Summary of Trusts for Estate Planning VLC

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

Advanced Sales. The Importance of Life Insurance. White Paper: The Own Your Own Policy Buy-Sell. Your future. Made easier. Number 11-1 June 1, 2011

Advanced Sales White Paper: The Own Your Own Policy Buy-Sell Number 11-1 June 1, 2011 Contact us: AdvancedSales@us.ing.com Buy-sell and business continuation agreements are important business planning

Advanced Sales White Paper: The Own Your Own Policy Buy-Sell Number 11-1 June 1, 2011 Contact us: AdvancedSales@us.ing.com Buy-sell and business continuation agreements are important business planning

Comprehensive Charitable Planning

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Charitable remainder trusts and life insurance

Life insurance Allianz Life Insurance Company of North America Charitable remainder trusts and life insurance (R-3/2018) Estate planning with highly appreciated assets When designed properly, a trust can

Life insurance Allianz Life Insurance Company of North America Charitable remainder trusts and life insurance (R-3/2018) Estate planning with highly appreciated assets When designed properly, a trust can

Understanding CRTs. A Summary of Charitable Remainder Trusts (CRTs) VLC

VLC") Understanding CRTs A Summary of Charitable Remainder Trusts (CRTs) VLC0439-0917 GET READY FOR RETIREMENT If your retirement planning objectives include lifetime income planning, estate tax reduction, 1

Understanding CRTs A Summary of Charitable Remainder Trusts (CRTs) VLC0439-0917 GET READY FOR RETIREMENT If your retirement planning objectives include lifetime income planning, estate tax reduction, 1

Link Between Gift and Estate Taxes

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

THE DESIGN, FUNDING, ADMINISTRATION & REPAIR OF GRATS, QPRTS & SALES TO IDGTS

THE DESIGN, FUNDING, ADMINISTRATION & REPAIR OF GRATS, QPRTS & SALES TO IDGTS The Estate Planning Council of Greater Miami October 20, 2016 Louis Nostro, Esquire Nostro Jones, P.A. Miami, Florida lnostro@nostrojones.com

THE DESIGN, FUNDING, ADMINISTRATION & REPAIR OF GRATS, QPRTS & SALES TO IDGTS The Estate Planning Council of Greater Miami October 20, 2016 Louis Nostro, Esquire Nostro Jones, P.A. Miami, Florida lnostro@nostrojones.com

A Unique Opportunity to Transfer Wealth Without Tax: Taking Advantage of the 2012 Gift Tax Exemption

A Unique Opportunity to Transfer Wealth Without Tax: Taking Advantage of the 2012 Gift Tax Exemption By Andrew H. Friedman, The Washington Update ESTATE PLANNING SERVICES APRIL 2012 T ax provisions enacted

A Unique Opportunity to Transfer Wealth Without Tax: Taking Advantage of the 2012 Gift Tax Exemption By Andrew H. Friedman, The Washington Update ESTATE PLANNING SERVICES APRIL 2012 T ax provisions enacted

Family Business Succession Planning

Corbenic Partners 1525 Valley Center Parkway Suite 310 Bethlehem, PA 18017 610-814-2474 www.corbenicpartners.com Family Business Succession Planning June 1, 2017 Page 1 of 9, see disclaimer on final page

Corbenic Partners 1525 Valley Center Parkway Suite 310 Bethlehem, PA 18017 610-814-2474 www.corbenicpartners.com Family Business Succession Planning June 1, 2017 Page 1 of 9, see disclaimer on final page

It s All About the Business

It s All About the Business Planning Strategies Integrated with Life Insurance to Help a Business Owner Accomplish Goals for Retirement, Business Perpetuation, Successful Business Transition, and Estate

It s All About the Business Planning Strategies Integrated with Life Insurance to Help a Business Owner Accomplish Goals for Retirement, Business Perpetuation, Successful Business Transition, and Estate

Charitable Giving Techniques

Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving, although appropriate for some,

Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving, although appropriate for some,

Sale to an Intentionally Defective Irrevocable Trust

Sale to an Intentionally Defective Irrevocable Trust Concept An Intentionally Defective Irrevocable Trust (IDIT) is an irrevocable trust established by a grantor generally for the benefit of the grantor

Sale to an Intentionally Defective Irrevocable Trust Concept An Intentionally Defective Irrevocable Trust (IDIT) is an irrevocable trust established by a grantor generally for the benefit of the grantor

USING TRANSAMERICA S ANNUITIES IN IRREVOCABLE TRUSTS

USING TRANSAMERICA S ANNUITIES IN IRREVOCABLE TRUSTS Annuities may lose value and are not insured by the FDIC or any federal government agency. They are not a deposit of or guaranteed by any bank, bank

USING TRANSAMERICA S ANNUITIES IN IRREVOCABLE TRUSTS Annuities may lose value and are not insured by the FDIC or any federal government agency. They are not a deposit of or guaranteed by any bank, bank

Financing strategies for single-insured life insurance owned by an irrevocable life insurance trust (ILIT)

") Financing strategies for single-insured life insurance owned by an irrevocable life insurance trust (ILIT) Annual Basic description (all of the trust agreements used for these ILITs are assumed to be grantor

Financing strategies for single-insured life insurance owned by an irrevocable life insurance trust (ILIT) Annual Basic description (all of the trust agreements used for these ILITs are assumed to be grantor

Bring SPF. Take CPE. JULY 6, 7, & 8. Ocean City, MD Clarion Resort Fontainebleau Hotel

Bring SPF. Take CPE. JULY 6, 7, & 8 Ocean City, MD Clarion Resort Fontainebleau Hotel It s not about climbing the ladder. It s about serving your team, your organization, and yourself. It s about being

Bring SPF. Take CPE. JULY 6, 7, & 8 Ocean City, MD Clarion Resort Fontainebleau Hotel It s not about climbing the ladder. It s about serving your team, your organization, and yourself. It s about being

How To Use an Intentionally Defective Irrevocable Trust To Freeze an Estate

How To Use an Intentionally Defective Irrevocable Trust To Freeze an Estate Michael D. Mulligan All section references are to the Internal Revenue Code ( IRC ) unless otherwise indicated. ETIP, to estate

How To Use an Intentionally Defective Irrevocable Trust To Freeze an Estate Michael D. Mulligan All section references are to the Internal Revenue Code ( IRC ) unless otherwise indicated. ETIP, to estate

Federal Estate and Gift Tax and Use of Applicable Exclusion Amount 3. Pennsylvania Inheritance Tax 5. Gifting Techniques 6

Prepared by Howard Vigderman Last Updated August 8, 2016 Federal Estate and Gift Taxes, Pennsylvania Inheritances Taxes and Measures to Reduce Them 2 Even with the federal estate tax exemption at an historically

Prepared by Howard Vigderman Last Updated August 8, 2016 Federal Estate and Gift Taxes, Pennsylvania Inheritances Taxes and Measures to Reduce Them 2 Even with the federal estate tax exemption at an historically

Counselor s Corner. SLAT: Is It Possible to Have Access to Trust Assets Without Estate Inclusion?

Counselor s Corner SLAT: Is It Possible to Have Access to Trust Assets Without Estate Inclusion? Situation: Most gift tax exemption estate strategies require assets to be given away with no strings attached.

Counselor s Corner SLAT: Is It Possible to Have Access to Trust Assets Without Estate Inclusion? Situation: Most gift tax exemption estate strategies require assets to be given away with no strings attached.

Financing strategies for survivorship life insurance owned by an irrevocable life insurance trust (ILIT)

") Financing strategies for survivorship life insurance owned by an irrevocable life insurance trust (ILIT) Annual Basic description (all of the trust agreements used for these ILITs are assumed to be grantor

Financing strategies for survivorship life insurance owned by an irrevocable life insurance trust (ILIT) Annual Basic description (all of the trust agreements used for these ILITs are assumed to be grantor

Wealth Transfer Planning in 2012: Perfect Storm of Opportunity

Wealth Transfer Planning in 2012: Perfect Storm of Opportunity 04.23.2012 04.23.2012 NEWS BY: FARHAD AGHDAMI 2012 may present the single greatest opportunity for wealth transfer planning in recent memory.

Wealth Transfer Planning in 2012: Perfect Storm of Opportunity 04.23.2012 04.23.2012 NEWS BY: FARHAD AGHDAMI 2012 may present the single greatest opportunity for wealth transfer planning in recent memory.

Spousal Lifetime Access Trust (SLAT)

") Concept Spousal Lifetime Access Trust (SLAT) A Spousal Lifetime Access Trust (SLAT) is an irrevocable trust that can own permanent life insurance and/or other assets. A SLAT permits the non-insured spouse

Concept Spousal Lifetime Access Trust (SLAT) A Spousal Lifetime Access Trust (SLAT) is an irrevocable trust that can own permanent life insurance and/or other assets. A SLAT permits the non-insured spouse

White Paper: Dynasty Trust

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

Estate Freeze Transactions

STRATEGIC THINKING The idea behind an estate freeze is to transfer value to the next generation at a low current value and to remove appreciation after the transfer date from the transferor s estate. Estate

STRATEGIC THINKING The idea behind an estate freeze is to transfer value to the next generation at a low current value and to remove appreciation after the transfer date from the transferor s estate. Estate

New York State Bar Association Tax Aspects of Real Property Transactions. Estate Planning for Investment Real Estate: Don t Forget the Income Tax Side

New York State Bar Association Tax Aspects of Real Property Transactions Estate Planning for Investment Real Estate: Don t Forget the Income Tax Side By Stephen M. Breitstone, Esq. Meltzer, Lippe, Goldstein

New York State Bar Association Tax Aspects of Real Property Transactions Estate Planning for Investment Real Estate: Don t Forget the Income Tax Side By Stephen M. Breitstone, Esq. Meltzer, Lippe, Goldstein

Benefits of Using Trusts with Selling Your Business

Select Portfolio Management, Inc. Dave Jones, MBA Wealth Adviser 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Benefits of Using Trusts

Select Portfolio Management, Inc. Dave Jones, MBA Wealth Adviser 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Benefits of Using Trusts

The Need for an Estate Liquidity Review. Estate Liquidity Review Producer Guide. For agent use only. Not for public distribution.

The Need for an Estate Liquidity Review Estate Liquidity Review Producer Guide Estate Liquidity Review The Need for an Estate Liquidity Review Death triggers a long list of costs that must be paid from

The Need for an Estate Liquidity Review Estate Liquidity Review Producer Guide Estate Liquidity Review The Need for an Estate Liquidity Review Death triggers a long list of costs that must be paid from

THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014)

") THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014) Presented to: CENTENNIAL ESTATE PLANNING COUNCIL November

THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014) Presented to: CENTENNIAL ESTATE PLANNING COUNCIL November

Using a Grantor Retained Annuity Trust (GRAT) for Wealth Transfer Purposes. Private Wealth Advisory

for Wealth Transfer Purposes. Private Wealth Advisory") Using a Grantor Retained Annuity Trust (GRAT) for Wealth Transfer Purposes Private Wealth Advisory What Is a GRAT? A grantor retained annuity trust (GRAT) is a wealth transfer technique used by taxpayers

Using a Grantor Retained Annuity Trust (GRAT) for Wealth Transfer Purposes Private Wealth Advisory What Is a GRAT? A grantor retained annuity trust (GRAT) is a wealth transfer technique used by taxpayers

Executive Benefits. Recruit, Retain and Reward Your Top Talent

Executive Benefits Recruit, Retain and Reward Your Top Talent Executive Benefits Recruit, Retain and Reward Your Top Talent Are you being faced with increased competition for talented key executives? In

Executive Benefits Recruit, Retain and Reward Your Top Talent Executive Benefits Recruit, Retain and Reward Your Top Talent Are you being faced with increased competition for talented key executives? In

Sale to an Intentionally Defective Irrevocable Trust

Concept Sale to an Intentionally Defective Irrevocable Trust An Intentionally Defective Irrevocable Trust (IDIT) is an irrevocable trust established by a grantor generally for the benefit of the grantor

Concept Sale to an Intentionally Defective Irrevocable Trust An Intentionally Defective Irrevocable Trust (IDIT) is an irrevocable trust established by a grantor generally for the benefit of the grantor

Law.com Home Newswire LawJobs CLE Center LawCatalog Our Sites Advertise

Page 1 of 6 Law.com Home Newswire LawJobs CLE Center LawCatalog Our Sites Advertise Home Advertising Classifieds Public Notices About Contact Free Limited Access Home > This Week's News > Free: Estate

Page 1 of 6 Law.com Home Newswire LawJobs CLE Center LawCatalog Our Sites Advertise Home Advertising Classifieds Public Notices About Contact Free Limited Access Home > This Week's News > Free: Estate

Thursday, 7 April 2016 #WRM 16-14

Thursday, 7 April 2016 #WRM 16-14 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms. The

Thursday, 7 April 2016 #WRM 16-14 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms. The

The CPA s Guide to Financial & Estate Planning Planning with Life Insurance. Presented by: Steven G. Siegel, J.D., LL.M.

The CPA s Guide to Financial & Estate Planning Planning with Life Insurance Presented by: Steven G. Siegel, J.D., LL.M. (Taxation) Earn CPE #AICPApfp 2 Helpful Hints #AICPApfp 3 About the PFP Section &

The CPA s Guide to Financial & Estate Planning Planning with Life Insurance Presented by: Steven G. Siegel, J.D., LL.M. (Taxation) Earn CPE #AICPApfp 2 Helpful Hints #AICPApfp 3 About the PFP Section &

FAMILY WEALTH GOAL ACHIEVER - INITIAL

FAMILY WEALTH GOAL ACHIEVER - INITIAL PREPARED FOR: February 18, 2009 Flip-CRT PLAN FOR DISCUSSION PURPOSES ONLY PRESENTED BY InKnowVision, LLC Randy A. Fox randy@inknowvision.com Phone: 630-596-5090 Copyright

FAMILY WEALTH GOAL ACHIEVER - INITIAL PREPARED FOR: February 18, 2009 Flip-CRT PLAN FOR DISCUSSION PURPOSES ONLY PRESENTED BY InKnowVision, LLC Randy A. Fox randy@inknowvision.com Phone: 630-596-5090 Copyright

Tax Bulletin: Effectively Using a QPRT Strategy in Your Estate Plan

Tax Bulletin: Effectively Using a QPRT Strategy in Your Estate Plan PAUL F. NAPOLEON, Senior Vice President & Head of Tax Services SAMANTHA BRIJLALL, Tax Associate Estate planning is an area of wealth

Tax Bulletin: Effectively Using a QPRT Strategy in Your Estate Plan PAUL F. NAPOLEON, Senior Vice President & Head of Tax Services SAMANTHA BRIJLALL, Tax Associate Estate planning is an area of wealth

White Paper Trusts Overview

White Paper Overview www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents...

White Paper Overview www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents...

Wealth Transfer. Shark Fin CHARITABLE LEAD ANNUITY TRUST

Wealth Transfer Shark Fin CHARITABLE LEAD ANNUITY TRUST 2 SHARK FIN: CHARITABLE LEAD ANNUITY TRUST Shark Fin CLAT EXECUTIVE SUMMARY A Charitable Lead Annuity Trust (CLAT) pays a fixed amount of the trust

Wealth Transfer Shark Fin CHARITABLE LEAD ANNUITY TRUST 2 SHARK FIN: CHARITABLE LEAD ANNUITY TRUST Shark Fin CLAT EXECUTIVE SUMMARY A Charitable Lead Annuity Trust (CLAT) pays a fixed amount of the trust

Revocable Trust Vs. Irrevocable Trust

I am not an attorney but here to help you undertand what things are... Speak to An Asset protection Attorney and find the best solution for you... Revocable Trust Vs. Irrevocable Trust Trusts are relatively

I am not an attorney but here to help you undertand what things are... Speak to An Asset protection Attorney and find the best solution for you... Revocable Trust Vs. Irrevocable Trust Trusts are relatively

CHARITABLE GIFTS. A charitable gift has a number of different tax benefits, which benefits differ if the gift is made during life or at death.

CHARITABLE GIFTS Charitable Gifts As stated on this website, the current applicable exclusion amount is $5,490,000. This amount will be increased annually for inflation. If an individual dies with an estate

CHARITABLE GIFTS Charitable Gifts As stated on this website, the current applicable exclusion amount is $5,490,000. This amount will be increased annually for inflation. If an individual dies with an estate

ESTATE PLANNING OPPORTUNITIES UNDER THE TAX RELIEF ACT OF

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 Winter 2011 www.disinherit-irs.com Editor: Julius Giarmarco, J.D., LL.M. The Tax Relief

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 Winter 2011 www.disinherit-irs.com Editor: Julius Giarmarco, J.D., LL.M. The Tax Relief

TRUST AND ESTATE PLANNING GLOSSARY

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

Charitable Trusts. Charitable Trusts

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

For a more detailed overview, see Charitable Remainder Trusts, 2. Treas. Regs (a)(5)(i).

(5)(i).") Two CRUTs and a CLAT: Using Split Interest Charitable Trusts to Defer Gain and Eliminate Estate Taxes Terence Condren & Thomas Cosinuke December 3, 2015 1. Framing the Discussion a. "True charity is the

Two CRUTs and a CLAT: Using Split Interest Charitable Trusts to Defer Gain and Eliminate Estate Taxes Terence Condren & Thomas Cosinuke December 3, 2015 1. Framing the Discussion a. "True charity is the

Charitable Giving Techniques

Charitable Giving Techniques Helping achieve your charitable and estate-planning goals Trust Tip A trust can be thought of as having two parts an income interest and a remainder interest. The income interest

Charitable Giving Techniques Helping achieve your charitable and estate-planning goals Trust Tip A trust can be thought of as having two parts an income interest and a remainder interest. The income interest

Personal Trust Services

Personal Trust Services Morgan Stanley Trust National Association 1 Morgan Stanley Trust, N.A. is dedicated to providing comprehensive and customized trustee services to wealthy families. As an experienced

Personal Trust Services Morgan Stanley Trust National Association 1 Morgan Stanley Trust, N.A. is dedicated to providing comprehensive and customized trustee services to wealthy families. As an experienced

Maximize The Value of Your IRA Using Life Insurance

Maximize The Value of Your IRA Using Life Insurance A Supplemental Illustration Prepared for Valued Client Prepared by Premier Producer Premier Brokerage 1 Sales Drive Bellevue, WA 98004 Life insurance

Maximize The Value of Your IRA Using Life Insurance A Supplemental Illustration Prepared for Valued Client Prepared by Premier Producer Premier Brokerage 1 Sales Drive Bellevue, WA 98004 Life insurance

PRACTICAL TIPS FOR CHARITABLE PLANNING

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

UPIA Amendment Saves Marital Deduction for Retirement Plans. by Steven B. Gorin 1

UPIA Amendment Saves Marital Deduction for Retirement Plans by Steven B. Gorin 1 In the summer of 2008, the Uniform Law Commission amended Section 409 of the Uniform Principal & Income Act (the UPIA ).

UPIA Amendment Saves Marital Deduction for Retirement Plans by Steven B. Gorin 1 In the summer of 2008, the Uniform Law Commission amended Section 409 of the Uniform Principal & Income Act (the UPIA ).

Estate Freezing Techniques. For Producer or Broker/Dealer Use Only. Not for Public Distribution.

Estate Freezing Techniques Agenda Identify Potential Clients Qualified Personal Residence Trust (QPRT) Grantor Retained Annuity Trust (GRAT) Installment Sale to an Intentionally Defective Irrevocable Trust

Estate Freezing Techniques Agenda Identify Potential Clients Qualified Personal Residence Trust (QPRT) Grantor Retained Annuity Trust (GRAT) Installment Sale to an Intentionally Defective Irrevocable Trust

Creates the trust. Holds legal title to the trust property and administers the trust. Benefits from the trust.

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA Understanding the Uses of Trusts WEALTH TRANSFER OVERVIEW. The purpose of this brochure is to provide a general discussion of basic trust principles.

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA Understanding the Uses of Trusts WEALTH TRANSFER OVERVIEW. The purpose of this brochure is to provide a general discussion of basic trust principles.

Bypass Trust (also called B Trust or Credit Shelter Trust)

") Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

Determined by Seller (not to exceed life expectancy) Deductibility of Interest Depends on Property None

Deductibility of Interest Depends on Property None") chapter chapter 7 SCIN Private Annuity Term of Payment Determined by Seller (not to exceed life expectancy) Life of Annuitant Deductibility of Interest Depends on Property None Buyer s Adjusted Basis Purchase

chapter chapter 7 SCIN Private Annuity Term of Payment Determined by Seller (not to exceed life expectancy) Life of Annuitant Deductibility of Interest Depends on Property None Buyer s Adjusted Basis Purchase

tax strategist the A simple plan Installment sale offers alternative to complex estate planning strategies Balance competing

the May/June 2008 tax strategist A simple plan Installment sale offers alternative to complex estate planning strategies Balance competing goals with a QTIP trust Take care when choosing IRA beneficiaries

the May/June 2008 tax strategist A simple plan Installment sale offers alternative to complex estate planning strategies Balance competing goals with a QTIP trust Take care when choosing IRA beneficiaries

Advanced Wealth Transfer Strategies

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

KEVIN MATZ & ASSOCIATES PLLC

KEVIN MATZ & ASSOCIATES PLLC An abridged version of this article was published in the February 2013 issue of Tax Stringer. So What Does It Mean To Have a Permanent Estate and Gift Tax System Anyway? --

KEVIN MATZ & ASSOCIATES PLLC An abridged version of this article was published in the February 2013 issue of Tax Stringer. So What Does It Mean To Have a Permanent Estate and Gift Tax System Anyway? --

Family Business Succession Planning

Raymond James Financial Services, Inc. Frank Bugh Branch Manager 345 Owen Lane Suite 134 Waco, TX 76710 254-776-9330 Frank.Bugh@RaymondJames.com www.raymondjames.com/waco Family Business Succession Planning

Raymond James Financial Services, Inc. Frank Bugh Branch Manager 345 Owen Lane Suite 134 Waco, TX 76710 254-776-9330 Frank.Bugh@RaymondJames.com www.raymondjames.com/waco Family Business Succession Planning

White Paper: Irrevocable Life Insurance Trusts

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

Wealth Transfer Planning