Practical aspects - Documentation, Benchmarking and Transfer Pricing Analysis IT/ITES, KPO and Engineering. Vaishali Mane Mumbai

|

|

|

- Prudence James

- 6 years ago

- Views:

Transcription

1 Practical aspects - Documentation, Benchmarking and Transfer Pricing Analysis IT/ITES, KPO and Engineering Vaishali Mane Mumbai

2 Agenda Transfer Pricing A quick background Operation Challenges Litigation Issues Latest updates Case Studies & Judicial Precedents 2

3 Transfer Pricing A quick background 3

4 Import aspect of Transfer Pricing Maintenance of Transfer pricing documentation Functional, financial and economic analysis Determine arms-length range Document past transactions Support proposed transactions Transfer pricing risk assessment review Review functional and risk profile Review price setting policy Determine arm s-length range Identify transfer pricing exposure (if appropriate) Quantify transfer pricing exposure Safe Harbour provisions for IT/ITES, Engineering and KPO Advance Pricing Arrangement (APA) 4

5 Function, Assets and Risk (FAR) Analysis What is FAR? FAR analysis - exercise to determine and document significant economic activities performed by the enterprise and its AEs in an International Transaction The allocation of these activities between those entities involved in the transaction so each entity can be fully characterised Price charged in any transaction reflects the functions performed (taking into account the risks assumed and assets used) FAR analysis essential to determine comparability Functional analysis identifies and compares Economically significant activities Assets used Risks assumed Functions Risks Assets 5

6 Function, Assets and Risk (FAR) Analysis Purpose of FAR Gathering and organizing facts needed to analyze intercompany prices To identify an appropriate level of profit that related parties should earn with respect to intercompany transactions under review To identify effects of functions, risks and assets on its profitability To determine the economic characterization of the entities in the international transaction To determine the most appropriate method for benchmarking the international transaction To identify any uncontrolled transaction involving one of the controlled parties 6

7 Function, Assets and Risk (FAR) Analysis Why do a functional analysis? The arm s length principle is based on comparability: [When] conditions are made or imposed between two [associated] enterprises in their commercial or financial relations which differ from those which would be made between independent enterprises, then any profits which would, but for those conditions, have accrued to one of the enterprises, but, by reason of those conditions, have not so accrued, may be included in the profits of that enterprise and taxed accordingly. * *Paragraph 1 of Article 9 of the OECD Model Tax Convention 7

8 What goes into a Functional Analysis? Transactions Functions Risks Entities Assets Products Markets / Competition Business Processes FAR Analysis Forecasts / Business Plans Organisation / Staff Agreements / Terms Financial Results 8

9 What comes out of Functional Analysis? Internal Comparables Understanding of the Business Basis to search for external comparables FAR Analysis Documentation Characterization of entities Determination of the MAP Method Risk and opportunity assessment 9

10 Importance of FAR Analysis Contract IT/ITE Services Contract Manufacturer Sales Agent Low Function & Low Risk Full fledged service provider Manufacturer/ Developer Marketing/ Distribution High Function & High Risk Comprehensive FAR leads to in-depth understanding of the business and related commercial considerations Allows correct characterization of the business Helps setting up of an appropriate pricing model for inter company transactions Robust FAR analysis - foundation of a sound economic analysis 10

11 Most Appropriate Method Most appropriate method is method best suited to facts and circumstances, providing most reliable measure of ALP Most appropriate method to be selected having regard to the following factors: - Nature and class of international transaction - Functions performed, assets utilized, risks assumed - Availability and reliability of data - Degree of comparability between controlled and uncontrolled transactions - Possibility to make reliable and accurate adjustments - Nature, extent and reliability of assumptions required Typically, Transactional Net Margin Method is selected as the Most Appropriate Method to benchmark IT and ITES transactions 11

12 Operational Challenges 12

13 Challenges Functional Challenges Operational Challenges Risk and working capital adjustment Comparability Challenges 13

14 Functional Challenges Extensive Functional Analysis: Risk-Function Matrix Unavailability of adequate data for conducting robust analysis TP Reports of two AE's would have conflicting conclusion Detailed FAR analysis for tested party and comparable companies is crucial Some international transactions are so unique that can not be compared Corporates and Group Companies hesitant to disclose information of developed IP, etc. 14

15 Comparability Challenges Dearth of comparables Due to emerging economies Use of new technologies, products & services Consolidation &Vertical Integration Non availability of data Cherry picking of comparables Rejection of low mark-up companies selected in Transfer Pricing Study Report Need to fulfill independence filter Use of secret comparables Overall process complexity 15

16 Risk and Working Capital Adjustments 1 Allowable only to comparables and not tested party but obtaining adequate data on comparables is difficult in segment scenario 2 Adjustments such as idle capacity, differences for accounting policy, depreciation etc., are not easily accepted by TPOs 3 Rejects any approximations, estimations and assumptions Adjustments being accepted -Working capital adjustment for IT / ITES sets; 16

17 Transfer Pricing Litigation issues 17

18 Transfer pricing audits Key issues Characterisation of income from resale of software, Determination of Royalty rate Adopting unfavourable stand for the assessee, considering forex as operating or non operating Bench cost adjustment (capacity utilization) allowed in comparability analysis Reduction in size of comparable companies due to losses, non availability of financial info and business close down Use of data not available in the public domain, Officer gathers information gathered U/S 133(6) Skews arithmetic mean as high-margin companies are retained resolved with range Inclusion of super normal mark-up companies Rejection of Turnover criteria Risk Adjustments to be allowed to be adjusted to comparables margins Tax authorities re-doing comparable search Rejection of loss making companies selected in the Report 18

19 Transfer Pricing Latest updates 19

20 Transfer Pricing Latest Updates Updates from Finance Bill 2016 Introduction of Country-by-Country (CBC) Report, effective from FY (AY ) Reduction in time limit for completion of assessment limit for concluding tax assessment reduced from 36 months to 33 months Eliminated Assessing Officer's power to appeal against DRP s Direction New guidelines issued by CBDT stating criteria for selection of cases for specialized transfer pricing scrutiny. Provides guidance for maintenance of the tax authorities database of transfer pricing case referrals. 20

21 Country-by-Country Report Require to file CBC Report from AY (FY ) Threshold to file CBC Report is in line with BEPS [The international consensus is for a threshold of 750 million (i.e. around Rs 5,395 million)] Overview of allocation of income, taxes and business activities by tax jurisdiction and details of all the Constituent Entities of the MNE group included in each aggregation per tax jurisdiction need to be disclosed in the CBC Report Graded structure of penalty prescribed ranging from INR 5,000 to 50,000 per day for non-furnishing, non-maintaining, furnishing inaccurate information, etc. 21

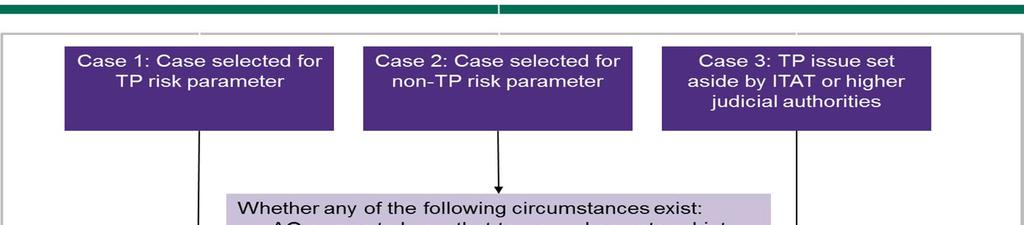

22 Key assessment related provisions Currently, the cases have been selected for TP assessment based on the value of international transactions After completion of almost ten audit cycles, CBDT issued Instruction no. 15 of 2015, (October 2015) in which focus shifted to risk based TP assessments with AO's continuing to being empowered to perform TP assessments, in certain situations. Instruction no 3/2016 replaces Instruction no. 15 of 2015 In 2016, CBDT come out with a new instruction clarifying that the AO is not empowered to conduct TP Assessments. 22

23 Key assessment related provisions 23

24 Dispute Resolution Panel Section 144C Eligible assessee means: o Any person in whose transfer pricing adjustment is proposed and is prejudicial to interest of such assessee as a consequence of order passed under section 92CA(3) o Foreign company Section 2 (23A) Assessing Officer mandated to pass draft order by time limit in case of eligible assessee Finance Bill 2016 provides reduction in time limit for completion of assessment limit for concluding tax assessment reduced from 36 months to 33 months Eligible assessee must within 30 days either file objections before the Dispute Resolution Panel ( DRP ) or accept the variations On acceptance of variation, assessee will receive final order and he has option of filing further appeal before Commissioner (Appeals), as an alternative. Assessing Officer must pass final order within 1 month from receipt of acceptance / expiry of period provided for acceptance. The DRP after enquiry and examination must pass an order within 9 months from end of the month in which draft order was issued either confirming, reducing or enhancing the variation but cannot set aside any matter. The Assessing Officer is bound to follow directions of DRP. Assessee can file further appeal before Income-tax Appellate Authority. Finance Bill 2016 eliminated Assessing Officer's power to appeal against DRP s Direction 24

25 Alternate dispute resolution mechanisms 1 Safe Harbour ( SH ) Rules effective from the FY and available for a period of five years. safe harbours available for IT, ITES, KPO, corporate guarantee, loan, auto manufacturing, etc. safe harbours for specified domestic transactions Government company engaged in business of generation, transmission or distribution of electricity. 2 Advance Pricing Agreement ( APA ) the detailed scheme is effective from 30 August 2012 and from FY is an arrangement between the taxpayer and the Revenue to mutually agree on the transfer pricing method/price to be applied and its application for a period upto five years The Finance Bill, 2014 has introduced roll back provisions for a maximum of 4 years subject to certain conditions 25

26 Transfer Pricing Latest Updates Updates from Finance Bill 2016 Introduction of Country-by-Country (CBC) Report, effective from FY (AY ) Reduction in time limit for completion of assessment limit for concluding tax assessment reduced from 36 months to 33 months Eliminated Assessing Officer's power to appeal against DRP s Direction New guidelines issued by CBDT stating criteria for selection of cases for specialized transfer pricing scrutiny. Provides guidance for maintenance of the tax authorities database of transfer pricing case referrals. 26

27 Transfer Pricing Latest Updates The cases can be referred to the Transfer Pricing Officers when: - Selection of cases under Transfer Pricing risk parameters for International Transactions or SDT or both - Taxpayer has not filed an accountant s report or failed to disclose an international transaction or SDT - There is a transfer pricing adjustment of INR 10 crore or more in earlier years, and the adjustment was upheld by judicial authorities or is pending an appeal - There is a search and seizure or survey operation, and transfer pricing findings have been recorded - Some new guidelines set forth mentioning the role of the Transfer Pricing Officer, the role of Assessing Officers after the determination of the arm s length price, and other rules - Notified role of AO after determination of ALP by the TPO 27

28 Evolving Developments Advanced Pricing Agreement Dispute Resolution Panel (DRP) Specified Domestic Transactions DTC Key lies in implementation Safe Harbor Rules Penalty on Non-reporting transactions Revised OECD Guidelines Scope of International Transactions 28

29 Safe Harbour Rules for IT/ITES, KPO and Engineering Services Eligible international transaction Provision of software development services Provision of information technology enabled services Provision of knowledge process outsourcing services Provision of specified contract R&D services wholly or partly relating to software development with insignificant risks Threshold limit Prescribed (aggregate value of international transaction) Up to INR 500 crore Above INR 500 crore Up to INR 500 crore Above INR 500 crore No limit No limit Safe harbor margin 20% or more on total operating costs 22% or more on total operating costs 20% or more on total operating costs 22% or more on total operating costs 25% or more on total operating costs 30% or more on total operating costs 29

30 Safe Harbour Rules for IT/ITES, KPO and Engineering Services International transaction Provision of software development services Mean i. business application software and information system development using known methods and existing software tools; ii. support for existing systems; iii. converting or translating computer languages; iv. adding user functionality to application programmes; v. debugging of systems; vi. adaptation of existing software; or vii. preparation of user documentation, but does not include any research and development services whether or not in the nature of contract research and development services. 30

31 Safe Harbour Rules for IT/ITES, KPO and Engineering Services International transaction Provision of information technology enabled services Mean i. back office operations; ii. call centres or contact centre services; iii. data processing and data mining; iv. insurance claim processing; v. legal databases; vi. creation and maintenance of medical transcription excluding medical advice; vii. translation services; viii. payroll; ix. remote maintenance; x. revenue accounting; xi. support centres; xii. website services; xiii. data search integration and analysis; xiv. remote education excluding education content development; or xv. clinical database management services excluding clinical trials, but does not include any research and development services whether or not in the nature of contract research and development services; 31

32 Safe Harbour Rules for IT/ITES, KPO and Engineering Services International transaction Provision of knowledge process outsourcing services Mean The following business process outsourcing services provided mainly with the assistance or use of information technology requiring application of knowledge and advanced analytical and technical skills, namely: i. geographic information system; ii. human resources services; iii. engineering and design services; iv. animation or content development and management; v. business analytics; vi. financial analytics; or vii. market research, but does not include any research and development services whether or not in the nature of contract research and development services; 32

33 Safe Harbour Rules for IT/ITES, KPO and Engineering Services International transaction Provision of specified contract R&D services wholly or partly relating to software development with insignificant risks Mean "contract research and development services wholly or partly relating to software development" means the following, namely: i. research and development producing new theorems and algorithms in the field of theoretical computer science; ii. development of information technology at the level of operating systems, programming languages, data management, communications software and software development tools; iii. iv. development of Internet technology; research into methods of designing, developing, deploying or maintaining software; v. software development that produces advances in generic approaches for capturing, transmitting, storing, retrieving, manipulating or displaying information; vi. vii. viii. experimental development aimed at filling technology knowledge gaps as necessary to develop a software programme or system; research and development on software tools or technologies in specialised areas of computing (image processing, geographic data presentation, character recognition, artificial intelligence and such other areas);or upgradation of existing products where source code has been made available by the principal; 33

34 Landmark Judicial Precedent 34

35 Maersk Global - Background Mumbai Special Bench Ruling on classification of ITES into KPO / BPO and exclusion of high profit making comparables Maersk Global for AY

36 Maersk Global - Background Constitution of special bench Due to divert views of the tribunals on the issue of ITeS sector's classification into KPO / BPO, and exclusion of high profit -making comparables, a special bench (SB) of the Mumbai Tribunal was constituted in the case of Maersk Global for AY (Reported in [2014 ] 43 Taxman.com 100 (Mumbai Trib) (SB)). M/s Omniglobe Information Technologies India Pvt. Ltd. and M/s CRM Services India Ltd. joined as interveners in this matters. Interveners An individual who is not already a part to an existing lawsuit but who makes himself or herself a party either by joining with the plaintiff or uniting with the defendant in resistance of the plaintiff's claim. 36

37 Questions raised before the Special Bench Questions raised before the Special Bench 1. Whether for the purpose of determining arm s length price of international transactions of the assesse-company, providing back office support services to their overseas associated enterprises, companies performing KPO functions should be considered as comparable? 2. In the facts of the assessee s case, whether companies earning abnormally high profit margin should be included in the list of comparable cases for the purpose of determining the arm s length price for an international transaction? 37

38 1. Classification of ITeS as KPO/BPO Facts of the case The Taxpayer is engaged in the business of shared service center and renders services such as transaction processing, data entry, reconciliation of statements, audit of shipping documents and other similar support services. The Taxpayer also rendered I.T. services such as process support, process optimisation and technical support services. The Dispute Resolution Panel ( DRP ) held that the assessee could neither be considered as a lowend service provider nor high-end KPO. Hence, it is considered a mix selection of comparables of I.T. enabled service sector. 38

39 1. Classification of ITeS as KPO/BPO Arguments by the taxpayer The taxpayer is a back office service provider or low-end service provider. A KPO industry is significantly higher on the value chain and involves processes that demand advanced information analysis as well as some judgment and decision-making. Taxpayer in turn is a captive entity, which does not have authority to make any decisions and operates as per the directions and instructions provided by its AE. There is a clear distinction between KPO services and BPO services. Reliance was placed on notification no. SO 2810 (E) dated 18 September, 2013 issued by the CBDT in relation to safe harbour rules wherein the Knowledge Process Outsourcing Services have been defined in distinction to the Information Technology Enabled Services services covering various BPO services. Broad characterisation of BPO and KPO services as ITES, based on the ground of larger size of sample, is not in accordance with the TP regulations. 39

40 1. Classification of ITeS as KPO/BPO Arguments by the intervener The intervener further relied upon the report prepared by the National Skill Development Corporation (NSDC) on Human Resource and Skill Requirements in the IT and ITES Industry Sector and an article KPO- An emerging opportunity for the Chartered Accountants published in July, 2006 issue of Journal The Chartered Accountants to bring out the difference between BPO and KPO. Arguments by Departmental Representatives (DR) The Taxpayer cannot be considered either as BPO or KPO but it lies somewhere in between as the services rendered by it are in the nature of BPO as well as KPO. Even the taxpayer has taken KPOs as comparables. As per Rule 10-TD, safe harbour rules are applicable to the Taxpayer who exercises a valid option for application of safe harbour rules and cannot be used for the purpose of Rule 10B. There is thus no need to make any distinction between BPO and KPO for TNMM and the broad category of ITES can be taken for the purpose of comparability analysis. 40

41 1. Classification of ITeS as KPO/BPO Ruling of Special Bench ITES services cannot be further bifurcated or classified as BPO and KPO services for the purpose of comparability analysis since Classification of ITES sector either as low-end BPO or high-end KPO is not always possible and there might be a third category of entities falling in between BPO and KPO. Determining exact portion of BPO and KPO services may also not be possible in the absence of relevant data maintained by the entity. 41

42 2. Exclusion of high profit making comparables Arguments by the taxpayer The arithmetic mean as referred in section 92C of the Act, envisages existence of arithmetic progression meaning thereby it expects the comparable figures in a specific range. Hence, anything beyond that range should not be taken into consideration. Relied on Para of the Circular No. 14 of 2001 to argue that expectation of the legislature was that there would not be any significant diversion between various Arm s Length Price (ALM) if there are different sets of comparables data. Relied on several cases decided by the different benches of the Tribunal in support of the argument. 42

43 2. Exclusion of high profit making comparables Arguments by the intervener The intervener further argued that if the high margin is earned due to efficiency, these entities cannot be excluded merely on the ground of high margin. However, if such high margin is due to any exterior factor, the concerned entities should be excluded from the list of comparables. Consistency of high margin is also required to be seen to find out as to whether the high margin is a normal situation or abnormal 43

44 2. Exclusion of high profit making comparables Arguments by Departmental Representatives (DR) Arithmetic mean is the most commonly used measure of central tendency. It is defined as a sum of the values of all observations divided by number of observations. By adopting the arithmetic mean to work out the average profit margin of the comparables, Indian law has recognized the extreme values also for comparability. Indian TP Rules specifically deviate from OECD guidelines in this aspect and specify the arithmetic mean for determining the ALP as against the quartile method suggested in the OECD guidelines which excludes the companies that fall in the extreme quartiles for comparability. There is no bar in the relevant Rule 10B(2) to consider the companies earning abnormal profits as comparables to tested party as long as they are functionally comparables. The entity showing extreme results, however, can be excluded for comparability if it is found there are specific or special reasons for such extreme results. 44

45 2. Exclusion of high profit making comparables Ruling of Special Bench Indian TP regulations specify the Arithmetic Mean for determining the ALP which is in deviation with the OECD guidelines suggesting quartile method which excludes the companies that fall in the extreme quartiles for comparability. Even otherwise, OECD guidelines in para 2.63 suggest that where one or more of potential comparables have extreme results consisting loss or unusual high profits, further examination would be needed to understand the reasons for extreme results. In light of the above, potential comparables cannot be excluded merely on the ground that their profit is abnormally high. However, in such cases further investigation should be undertaken to ascertain the reasons for unusual high profit and in order to establish whether entities with such high profit can be taken as comparables. In these cases, Functional assets & Risk analysis (FAR) may be reviewed to ensure that the potential comparables earning high profit satisfies the comparability conditions. If it does not satisfy the comparability analysis or the high profit margin does not reflect the normal business condition, then the high profit margin making entity should not be included in the list of comparables for the purpose of determining the ALM of an international transaction 45

46 Questions and Answers 46

47 Thank you 47

WESTERN INDIAN REGIONAL COUNCIL, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA. Workshop on Transfer Pricing. Safe Harbour Rules- An Overview

WESTERN INDIAN REGIONAL COUNCIL, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Workshop on Transfer Pricing Safe Harbour Rules- An Overview Sanjay Kapadia Background Introduced in Finance (No 2) Act,

WESTERN INDIAN REGIONAL COUNCIL, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Workshop on Transfer Pricing Safe Harbour Rules- An Overview Sanjay Kapadia Background Introduced in Finance (No 2) Act,

GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX

![GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX](/thumbs/90/104493159.jpg "GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX") [TO BE PUBLSIHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] Notification

[TO BE PUBLSIHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] Notification

Special Bench of Mumbai Tribunal rules on approach to selection of comparable data

17 March 2014 Global Tax Alert News from Transfer Pricing EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/

17 March 2014 Global Tax Alert News from Transfer Pricing EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/

Landmark Decisions on Transfer Pricing

Landmark Decisions on Transfer Pricing CITC Amol Tibrewal Vispi T. Patel & Associates 11 April 2014 Global Vantedge - Delhi Tribunal (ITA No 2763 & 2764/DEL/2009) Facts of the case Assessee provided IteS

Landmark Decisions on Transfer Pricing CITC Amol Tibrewal Vispi T. Patel & Associates 11 April 2014 Global Vantedge - Delhi Tribunal (ITA No 2763 & 2764/DEL/2009) Facts of the case Assessee provided IteS

Issues in Transfer Pricing

Issues in Transfer Pricing Vaishali Mane Chartered Accountant, Mumbai 2017 Grant Thornton India LLP. All rights reserved. 1 Contents 1 Transfer Pricing - Basic 2 Recent Developments in Transfer Pricing

Issues in Transfer Pricing Vaishali Mane Chartered Accountant, Mumbai 2017 Grant Thornton India LLP. All rights reserved. 1 Contents 1 Transfer Pricing - Basic 2 Recent Developments in Transfer Pricing

CBDT Instruction No. 3/2016 : A game-changer for TP audits? - Part I

CBDT Instruction No. 3/2016 : A game-changer for TP audits? - Part I Date: Fri, 04/22/2016-15:02 Ajay Kering (Direct or, Grant Thornt on India LLP) Dinesh Ramnani (Manager, Grant Thornt on India LLP) This

CBDT Instruction No. 3/2016 : A game-changer for TP audits? - Part I Date: Fri, 04/22/2016-15:02 Ajay Kering (Direct or, Grant Thornt on India LLP) Dinesh Ramnani (Manager, Grant Thornt on India LLP) This

Transfer Pricing Country Summary India

Page 1 of 13 Transfer Pricing Country Summary India April 2018 Page 2 of 13 Legislation Existence of Transfer Pricing Laws/Guidelines Section 92 of the Income-tax Act, 1961 requires international transactions

Page 1 of 13 Transfer Pricing Country Summary India April 2018 Page 2 of 13 Legislation Existence of Transfer Pricing Laws/Guidelines Section 92 of the Income-tax Act, 1961 requires international transactions

Transfer Pricing Issues - IT/ITES Industry - Financial Services Industry. Darpan Mehta March 20, 2015

Transfer Pricing Issues - IT/ITES Industry - Financial Services Industry Darpan Mehta March 20, 2015 Agenda IT/ITES Industry 1 Financial Services Industry 2 Slide 2 IT/ITES Industry 1 Issues and challenges

Transfer Pricing Issues - IT/ITES Industry - Financial Services Industry Darpan Mehta March 20, 2015 Agenda IT/ITES Industry 1 Financial Services Industry 2 Slide 2 IT/ITES Industry 1 Issues and challenges

Overview of Transfer Pricing

Overview of Transfer Pricing Contents Legislative framework Transfer pricing study Assessment and Litigation Key Recent Developments Page 2 Transfer Pricing in India- Background April 1, 2001 onwards Comprehensive

Overview of Transfer Pricing Contents Legislative framework Transfer pricing study Assessment and Litigation Key Recent Developments Page 2 Transfer Pricing in India- Background April 1, 2001 onwards Comprehensive

Recent Transfer Pricing Developments

Recent Transfer Pricing Developments CA Rachesh Kotak September 08, 2017 Setting the context Old world New world Compliance driven Reliance on local documentation One-sided approaches Protracted litigation

Recent Transfer Pricing Developments CA Rachesh Kotak September 08, 2017 Setting the context Old world New world Compliance driven Reliance on local documentation One-sided approaches Protracted litigation

Future of TP. Documentation & Certification. 7th October Presented by- CA Dilip Gupta

Future of TP Documentation & Certification 7th October 2017 Presented by- CA Dilip Gupta Journey of TP regulations in India Major Milestones Final Rules on Range and multiple year data concept Introduction

Future of TP Documentation & Certification 7th October 2017 Presented by- CA Dilip Gupta Journey of TP regulations in India Major Milestones Final Rules on Range and multiple year data concept Introduction

Transfer Pricing. Recent Trends & Key Developments. PHD Chamber International Tax Conference September 04, 2014 New Delhi. Statement of Credentials 1

Transfer Pricing Recent Trends & Key Developments PHD Chamber International Tax Conference September 04, 2014 New Delhi Statement of Credentials 1 SESSION DETAILS Topic: Transfer Pricing Recent Trends

Transfer Pricing Recent Trends & Key Developments PHD Chamber International Tax Conference September 04, 2014 New Delhi Statement of Credentials 1 SESSION DETAILS Topic: Transfer Pricing Recent Trends

Mumbai Tribunal rules on transfer pricing aspects of intra-group software development services

13 March 2013 Global Tax Alert News and views from Transfer Pricing Mumbai Tribunal rules on transfer pricing aspects of intra-group software development services Executive summary This Tax Alert summarizes

13 March 2013 Global Tax Alert News and views from Transfer Pricing Mumbai Tribunal rules on transfer pricing aspects of intra-group software development services Executive summary This Tax Alert summarizes

TAX CONTROVERSIES AND LITIGATION IN INDIA - AVOIDANCE AND THE SOLUTIONS. S.R. Wadhwa, Advocate 1

TAX CONTROVERSIES AND LITIGATION IN INDIA - AVOIDANCE AND THE SOLUTIONS S.R. Wadhwa, Advocate 1 BY: S.R. Wadhwa Ph. No. 9810414433 Email: wadhwasr@hotmail.com Website: wadhwataxconsultant.com S.R. Wadhwa,

TAX CONTROVERSIES AND LITIGATION IN INDIA - AVOIDANCE AND THE SOLUTIONS S.R. Wadhwa, Advocate 1 BY: S.R. Wadhwa Ph. No. 9810414433 Email: wadhwasr@hotmail.com Website: wadhwataxconsultant.com S.R. Wadhwa,

Did you know! Transactions M.2 Safe harbour rules M.3 Dispute resolution panel

M Transfer pricing Doing business in India 209 Did you know! India has emerged as the world s number one, along with the US, in annual solar power generation. In wind power production, when it comes to

M Transfer pricing Doing business in India 209 Did you know! India has emerged as the world s number one, along with the US, in annual solar power generation. In wind power production, when it comes to

Introduction to Transfer Pricing Regulations

Introduction to Transfer Pricing Regulations January 24, 2015 Vispi T. Patel Vispi T. Patel & Associates 1 Agenda Transfer Pricing Regulations in India Practical applicability of Transfer Pricing Regulations

Introduction to Transfer Pricing Regulations January 24, 2015 Vispi T. Patel Vispi T. Patel & Associates 1 Agenda Transfer Pricing Regulations in India Practical applicability of Transfer Pricing Regulations

TRANSFER PRICING ( TP ) LITIGATION TP ASSESSMENT AND DISPUTE RESOLUTION PANEL ( DRP )

LITIGATION TP ASSESSMENT AND DISPUTE RESOLUTION PANEL ( DRP )") TRANSFER PRICING ( TP ) LITIGATION TP ASSESSMENT AND DISPUTE RESOLUTION PANEL ( DRP ) Contributed by : CA Kushal Dedhia (a member of the association) he can be reached at kushaldedhia05@gmail.com Your

TRANSFER PRICING ( TP ) LITIGATION TP ASSESSMENT AND DISPUTE RESOLUTION PANEL ( DRP ) Contributed by : CA Kushal Dedhia (a member of the association) he can be reached at kushaldedhia05@gmail.com Your

Key Transfer Pricing Rulings

Key Transfer Pricing Rulings 8 Sept 2017 - Prasad Pardiwala Presenters : Rahul & Pranav Case Law - 1 Instrumenterium Special bench on Base Erosion Facts/ Issue: The taxpayer advanced an interest free loan

Key Transfer Pricing Rulings 8 Sept 2017 - Prasad Pardiwala Presenters : Rahul & Pranav Case Law - 1 Instrumenterium Special bench on Base Erosion Facts/ Issue: The taxpayer advanced an interest free loan

Practical Experiences

Practical Experiences Presented by: Dinesh Supekar PwC Snapshot of assessment issues covered 1. Marketing intangibles FMCG Industry 2. Selection of comparables Automobile Industry 3. Commission income

Practical Experiences Presented by: Dinesh Supekar PwC Snapshot of assessment issues covered 1. Marketing intangibles FMCG Industry 2. Selection of comparables Automobile Industry 3. Commission income

Arm s Length Principle. Kavita Sethia Gambhir

Arm s Length Principle Kavita Sethia Gambhir January 2017 Introduction 2 Background Economic Globalization Multinational Structure Different Objectives Top Management/Key Personnel Shareholders Tax Authorities

Arm s Length Principle Kavita Sethia Gambhir January 2017 Introduction 2 Background Economic Globalization Multinational Structure Different Objectives Top Management/Key Personnel Shareholders Tax Authorities

TRANSFER PRICING DATED CA. Ashwani Rastogi, New Delhi

TRANSFER PRICING DATED 8.6.2017 1 India has signed the historic multilateral convention to implement tax treaty related measures to prevent Base Erosion and Profit Shifting (BEPS), at Paris with More than

TRANSFER PRICING DATED 8.6.2017 1 India has signed the historic multilateral convention to implement tax treaty related measures to prevent Base Erosion and Profit Shifting (BEPS), at Paris with More than

Transfer Pricing Methods and Selection of Most Appropriate Method. Vaishali Mane Partner Grant Thornton India LLP Mumbai

Transfer Pricing Methods and Selection of Most Appropriate Method Vaishali Mane Partner Grant Thornton India LLP Mumbai Agenda Transfer Pricing Quick background Arm's Length Principle Overview of Methods

Transfer Pricing Methods and Selection of Most Appropriate Method Vaishali Mane Partner Grant Thornton India LLP Mumbai Agenda Transfer Pricing Quick background Arm's Length Principle Overview of Methods

Arm s length principle in India: selected issues

Arm s length principle in India: selected issues 1 Timing issues OECD perspective Different country approaches: the arm s length price setting and the arm s length outcome testing approaches: Year Y-1

Arm s length principle in India: selected issues 1 Timing issues OECD perspective Different country approaches: the arm s length price setting and the arm s length outcome testing approaches: Year Y-1

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961 Borivali (Central) CPE Study Circle of WIRC of The Institute Of Chartered Accountants Of India Vispi

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961 Borivali (Central) CPE Study Circle of WIRC of The Institute Of Chartered Accountants Of India Vispi

India. The Organisation for Economic Co-operation. Indraneel R Chaudhury, Suchint Majmudar, Ganesh Krishnamurthy and Shilpa S, PwC India

India Indraneel R Chaudhury, Suchint Majmudar, Ganesh Krishnamurthy and Shilpa S, PwC India The Organisation for Economic Co-operation and Development ( OECD ) recently released a White Paper on Transfer

India Indraneel R Chaudhury, Suchint Majmudar, Ganesh Krishnamurthy and Shilpa S, PwC India The Organisation for Economic Co-operation and Development ( OECD ) recently released a White Paper on Transfer

Indian tax administration issues revised guidance on transfer pricing audit procedures

11 March 2016 Global Tax Alert News from Transfer Pricing Indian tax administration issues revised guidance on transfer pricing audit procedures EY Global Tax Alert Library Access both online and pdf versions

11 March 2016 Global Tax Alert News from Transfer Pricing Indian tax administration issues revised guidance on transfer pricing audit procedures EY Global Tax Alert Library Access both online and pdf versions

An overview of Transfer Pricing

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel Vispi T. Patel & Associates 19 th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel Vispi T. Patel & Associates 19 th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer

India revises Country Chapter comments in UN Practical Manual on Transfer Pricing Issues for Developing Countries

14 November 2016 Global Tax Alert News from Transfer Pricing India revises Country Chapter comments in UN Practical Manual on Transfer Pricing Issues for Developing Countries EY Global Tax Alert Library

14 November 2016 Global Tax Alert News from Transfer Pricing India revises Country Chapter comments in UN Practical Manual on Transfer Pricing Issues for Developing Countries EY Global Tax Alert Library

Transfer Pricing Backdrop in. Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016

Transfer Pricing Backdrop in India Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016 Presentation Outline Introduction ti Transfer Pricing Regulations in India Arms

Transfer Pricing Backdrop in India Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016 Presentation Outline Introduction ti Transfer Pricing Regulations in India Arms

An overview of Transfer Pricing

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel 19th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel 19th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

Methodology to benchmark Intra group services, Management services and Cost allocation

Methodology to benchmark Intra group services, Management services and Cost allocation with case study Presentation for 3rd Intensive Study Course on Transfer Pricing Organised by The Chamber Of Tax Consultants

Methodology to benchmark Intra group services, Management services and Cost allocation with case study Presentation for 3rd Intensive Study Course on Transfer Pricing Organised by The Chamber Of Tax Consultants

India s High Court of Delhi rules on transfer pricing aspects of intra-group service transactions

30 May 2014 Global Tax Alert News from Transfer Pricing EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/

30 May 2014 Global Tax Alert News from Transfer Pricing EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/

B S R & Co. LLP. Specified Domestic Transactions. Pankil Sanghvi Director. 10 October 2015

Specified Domestic Transactions B S R & Co. LLP Pankil Sanghvi Director 10 October 2015 1 Background Genesis of Domestic Transfer Pricing Regulations Supreme Court (SC) in the case of CIT v Glaxo SmithKline

Specified Domestic Transactions B S R & Co. LLP Pankil Sanghvi Director 10 October 2015 1 Background Genesis of Domestic Transfer Pricing Regulations Supreme Court (SC) in the case of CIT v Glaxo SmithKline

INDIA TRANSFER PRICING UPDATES MARCH 2019

Uday Ved Global Tax Partner INDIA TRANSFER PRICING UPDATES MARCH 2019 KNAV Thought Leadership has started an initiative to publish a monthly newsletter dedicated to transfer pricing updates and amendments

Uday Ved Global Tax Partner INDIA TRANSFER PRICING UPDATES MARCH 2019 KNAV Thought Leadership has started an initiative to publish a monthly newsletter dedicated to transfer pricing updates and amendments

India. Vispi T. Patel and Kejal P. Visharia*

India Vispi T. Patel and Kejal P. Visharia* Ruling in Marubeni Case on Benchmarking and Determining Arm s Length Consideration for the International Provision of Agency and Marketing Support Services The

India Vispi T. Patel and Kejal P. Visharia* Ruling in Marubeni Case on Benchmarking and Determining Arm s Length Consideration for the International Provision of Agency and Marketing Support Services The

2 nd All India Tax Summit. - Achromic Point. Transfer Pricing. CA Sachin Kumar B P

2 nd All India Tax Summit - Achromic Point Transfer Pricing CA Sachin Kumar B P 2001: TP regulations introduced -Mandatory compliance agreement - Stringent penalty provisions 2005: First TP audit cycle

2 nd All India Tax Summit - Achromic Point Transfer Pricing CA Sachin Kumar B P 2001: TP regulations introduced -Mandatory compliance agreement - Stringent penalty provisions 2005: First TP audit cycle

CBDT Draft Rules on "range concept" and "multiple year data" - A boon or bane?

CBDT Draft Rules on "range concept" and "multiple year data" - A boon or bane? Date: May 25,2015 Keyur Shah (Part ner, Financial Services T ransfer Pricing, EY) Jaiman Pat el (Direct or, Financial Services

CBDT Draft Rules on "range concept" and "multiple year data" - A boon or bane? Date: May 25,2015 Keyur Shah (Part ner, Financial Services T ransfer Pricing, EY) Jaiman Pat el (Direct or, Financial Services

TRANSFER PRICING UNDER INCOME TAX ACT, N.Madhan B.Com., CA & Grad CWA. 22 August 2015

TRANSFER PRICING UNDER INCOME TAX ACT, 1961 N.Madhan B.Com., CA & Grad CWA 1 22 August 2015 Contents Concept of Transfer Pricing Important Terminologies Nature of Methods & its Applicability Importance

TRANSFER PRICING UNDER INCOME TAX ACT, 1961 N.Madhan B.Com., CA & Grad CWA 1 22 August 2015 Contents Concept of Transfer Pricing Important Terminologies Nature of Methods & its Applicability Importance

CORAM: HON'BLE DR. JUSTICE S.MURALIDHAR HON'BLE MR. JUSTICE VIBHU BAKHRU O R D E R %

$~ * IN THE HIGH COURT OF DELHI AT NEW DELHI 10. + ITA 102/2015 RAMPGREEN SOLUTIONS PVT LTD... Appellant Through: Mr Ajay Vohra, Sr. Advocate with Mr Aditya Vohra, Advocate. versus COMMISSIONER OF INCOME

$~ * IN THE HIGH COURT OF DELHI AT NEW DELHI 10. + ITA 102/2015 RAMPGREEN SOLUTIONS PVT LTD... Appellant Through: Mr Ajay Vohra, Sr. Advocate with Mr Aditya Vohra, Advocate. versus COMMISSIONER OF INCOME

TRANSFER PRICING IN INDIA A REVENUE PERSPECTIVE

TRANSFER PRICING IN INDIA A REVENUE PERSPECTIVE A PRESENTATION BY AKHILESH RANJAN DIRECTOR OF INCOME TAX (INTERNATIONAL TAXATION), NEW DELHI 02.12.2005 HISTORICALLY Concept of transfer pricing always there

TRANSFER PRICING IN INDIA A REVENUE PERSPECTIVE A PRESENTATION BY AKHILESH RANJAN DIRECTOR OF INCOME TAX (INTERNATIONAL TAXATION), NEW DELHI 02.12.2005 HISTORICALLY Concept of transfer pricing always there

Transfer Pricing - An Overview

Transfer Pricing - An Overview BCAS Study Course Hitesh D. Gajaria 7 February 2015 Transfer Pricing: An Introduction 1 Transfer Pricing - The impact of getting it wrong could be Fatal!!! Japan s top pharmaceutical

Transfer Pricing - An Overview BCAS Study Course Hitesh D. Gajaria 7 February 2015 Transfer Pricing: An Introduction 1 Transfer Pricing - The impact of getting it wrong could be Fatal!!! Japan s top pharmaceutical

Secondary Adjustments What Lies beneath

Secondary Adjustments What Lies beneath UTPAL DOSHI June 2017 Contents -Transfer Pricing Adjustments - Secondary Adjustment - provisions - Global practice / OECD - Key issues - Illustrations - Way forward

Secondary Adjustments What Lies beneath UTPAL DOSHI June 2017 Contents -Transfer Pricing Adjustments - Secondary Adjustment - provisions - Global practice / OECD - Key issues - Illustrations - Way forward

INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA DOMESTIC TRANSFER PRICING PROVISIONS CA.T. P. OSTWAL 21st September 2012 1 Introduction TP was earlier limited to International Transactions The Finance Act

INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA DOMESTIC TRANSFER PRICING PROVISIONS CA.T. P. OSTWAL 21st September 2012 1 Introduction TP was earlier limited to International Transactions The Finance Act

d e vreser st ighr lla

Article 7 and 9 of the model conventions including International and Domestic TP Beginners Study Course on International Taxation July 4, 2015 Neha Arora 2 Contents Article 7 of the Model Convention Approaches

Article 7 and 9 of the model conventions including International and Domestic TP Beginners Study Course on International Taxation July 4, 2015 Neha Arora 2 Contents Article 7 of the Model Convention Approaches

Transfer Pricing Audits Indian experience.

Transfer Pricing Audits Indian experience. International Tax Conference - 2005 Vispi T. Patel Deloitte Haskins & Sells. Background of Indian TPR OECD s View Transfer pricing can deprive governments of

Transfer Pricing Audits Indian experience. International Tax Conference - 2005 Vispi T. Patel Deloitte Haskins & Sells. Background of Indian TPR OECD s View Transfer pricing can deprive governments of

Vision To be the most admired professional services firm serving clients globally

Vision To be the most admired professional services firm serving clients globally C h a l l e n g e U s OVERVIEW OF COST PLUS METHOD October 8, 2014 2 All rights reserved Preliminary & Tentative CONTENTS

Vision To be the most admired professional services firm serving clients globally C h a l l e n g e U s OVERVIEW OF COST PLUS METHOD October 8, 2014 2 All rights reserved Preliminary & Tentative CONTENTS

Background. Facts of the case. 11 April 2016

11 April 2016 Turnover filter considered at 10 times; Comparables with RPTs up to 15 percent accepted; standard deduction of +/- 5 percent benefit under the erstwhile provisions of Incometax Act confirmed

11 April 2016 Turnover filter considered at 10 times; Comparables with RPTs up to 15 percent accepted; standard deduction of +/- 5 percent benefit under the erstwhile provisions of Incometax Act confirmed

GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX

![GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX](/thumbs/90/104493156.jpg "GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX") [TO BE PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] Notification

[TO BE PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] Notification

Indian subsidiary of group holding company of Netherlands entity does not constitute permanent establishment in India

15 February 2017 Indian subsidiary of group holding company of Netherlands entity does not constitute permanent establishment in India Background Recently, the Delhi Bench of the Income-tax Appellate Tribunal

15 February 2017 Indian subsidiary of group holding company of Netherlands entity does not constitute permanent establishment in India Background Recently, the Delhi Bench of the Income-tax Appellate Tribunal

COUNTRY CHAPTER EXCERPT. India

COUNTRY CHAPTER EXCERPT India Mukesh Butani and Sanjiv Malhotra, Taxand India. The authors can be contacted at +91 124 339 5000, mukesh.butani@bmrlegal.in / sanjiv.malhotra@bmradvisors.com 1. Tax Authority

COUNTRY CHAPTER EXCERPT India Mukesh Butani and Sanjiv Malhotra, Taxand India. The authors can be contacted at +91 124 339 5000, mukesh.butani@bmrlegal.in / sanjiv.malhotra@bmradvisors.com 1. Tax Authority

DOMESTIC TRANSFER PRICING

12 October 2014 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

12 October 2014 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

INDIA BUDGET I. Equalisation levy stems out of OECD s BEPS Action Plan 1 on Digital Economy

INDIA BUDGET 2016 A. International tax I. Equalisation levy stems out of OECD s BEPS Action Plan 1 on Digital Economy New Chapter titled Equalisation Levy introduced in Finance Bill, considering it is

INDIA BUDGET 2016 A. International tax I. Equalisation levy stems out of OECD s BEPS Action Plan 1 on Digital Economy New Chapter titled Equalisation Levy introduced in Finance Bill, considering it is

KPMG FLASH NEWS. Transfer Pricing - Safe Harbour Rules Notified. Background. 20 September 2013 KPMG IN INDIA

KPMG FLASH NEWS KPMG IN INDIA Transfer Pricing - Safe Harbour Rules Notified 20 September 2013 Background To reduce increasing number of transfer pricing audits and prolonged disputes, the Central Board

KPMG FLASH NEWS KPMG IN INDIA Transfer Pricing - Safe Harbour Rules Notified 20 September 2013 Background To reduce increasing number of transfer pricing audits and prolonged disputes, the Central Board

An overview of Transfer Pricing

An overview of Transfer Pricing CTC Vispi T. Patel Vispi T. Patel & Associates Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

An overview of Transfer Pricing CTC Vispi T. Patel Vispi T. Patel & Associates Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

DOMESTIC TRANSFER PRICING CONFERENCE

DOMESTIC TRANSFER PRICING CONFERENCE Importance of FAR & Comparability; Selection of the Most Appropriate Method and Issues in disclosure in new Form 3CEB from SDT perspective 19 October 2013 Pramod Joshi

DOMESTIC TRANSFER PRICING CONFERENCE Importance of FAR & Comparability; Selection of the Most Appropriate Method and Issues in disclosure in new Form 3CEB from SDT perspective 19 October 2013 Pramod Joshi

Union Budget 2014 Analysis of Major Direct tax proposals

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

Sharing insights. News Alert 1 February, 2012

www.pwc.com/in Sharing insights News Alert 1 February, 2012 Sharing of net revenues consistently in controlled and uncontrolled transactions held as a valid comparable uncontrolled price In brief In a

www.pwc.com/in Sharing insights News Alert 1 February, 2012 Sharing of net revenues consistently in controlled and uncontrolled transactions held as a valid comparable uncontrolled price In brief In a

DOMESTIC TRANSFER PRICING

17 November 2013 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

17 November 2013 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

CA TIRTHESH M. BAGADIYA

DOMESTIC TRANSFER PRICING CA TIRTHESH M. BAGADIYA 1 1 Introduction Previously TP applicable only to international transactions By virtue of Finance Act, 2012, TP provision ambit has been extended to Specified

DOMESTIC TRANSFER PRICING CA TIRTHESH M. BAGADIYA 1 1 Introduction Previously TP applicable only to international transactions By virtue of Finance Act, 2012, TP provision ambit has been extended to Specified

DOMESTIC TRANSFER PRICING REGULATIONS

DOMESTIC TRANSFER PRICING REGULATIONS (Taxation of specified domestic transactions in India) By B. D. Jokhakar & Co. Chartered Accountants INDIA TABLE OF CONTENTS Sr. No. Topic Page no. I INTRODUCTION

DOMESTIC TRANSFER PRICING REGULATIONS (Taxation of specified domestic transactions in India) By B. D. Jokhakar & Co. Chartered Accountants INDIA TABLE OF CONTENTS Sr. No. Topic Page no. I INTRODUCTION

Subject: Revised and Updated Guidance for Implementation of Transfer Pricing Provisions-Regarding

Instruction No. 15/2015 F.No. 500/9/2015-APA-11 Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes Foreign Tax and Tax Research Division-I APA-II Section New Delhi,

Instruction No. 15/2015 F.No. 500/9/2015-APA-11 Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes Foreign Tax and Tax Research Division-I APA-II Section New Delhi,

Issues Involving Comparability and Profit Based Methods in Transfer Pricing

G L O B A L T R A N S F E R P R I C I N G S E R V I C E S Issues Involving Comparability and Profit Based Methods in Transfer Pricing International Taxation Conference 2008 December 5, 2008 T A X Uday

G L O B A L T R A N S F E R P R I C I N G S E R V I C E S Issues Involving Comparability and Profit Based Methods in Transfer Pricing International Taxation Conference 2008 December 5, 2008 T A X Uday

Tax - Heads Up. 07 March Contents Page Judicial Updates 2-6 Other Updates 7

Tax - Heads Up 07 March 2014 Contents Page Judicial Updates 2-6 Other Updates 7 1 Virola International ITAT Agra Context: Under the Indian tax laws, certain specified business expenditures including all

Tax - Heads Up 07 March 2014 Contents Page Judicial Updates 2-6 Other Updates 7 1 Virola International ITAT Agra Context: Under the Indian tax laws, certain specified business expenditures including all

Domestic Transfer Pricing

Domestic Transfer Pricing September 15, 2012 CA Darpan Mehta Agenda 1 Domestic TP Transactions 2 Case Study 3 Way Forward Slide 2 Transactions Slide 3 Intent of Indian Transfer Pricing (TP) Regulations

Domestic Transfer Pricing September 15, 2012 CA Darpan Mehta Agenda 1 Domestic TP Transactions 2 Case Study 3 Way Forward Slide 2 Transactions Slide 3 Intent of Indian Transfer Pricing (TP) Regulations

Transfer Pricing Perspective Pharmaceuticals Industry 20 September 2014

www.pwc.in Transfer Pricing Perspective Pharmaceuticals Industry 20 Contents Transfer Pricing environment Key TP Issues Recent Developments Best Practices Slide 2 Transfer Pricing Environment Slide 3 Global

www.pwc.in Transfer Pricing Perspective Pharmaceuticals Industry 20 Contents Transfer Pricing environment Key TP Issues Recent Developments Best Practices Slide 2 Transfer Pricing Environment Slide 3 Global

Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer

CA. Vispi T. Patel, CA. Rajiv Shah and CA.Kejal Visharia Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer INTERNATIONAL PRICING PROVISIONS TRANSFER Introduction

CA. Vispi T. Patel, CA. Rajiv Shah and CA.Kejal Visharia Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer INTERNATIONAL PRICING PROVISIONS TRANSFER Introduction

Latest Developments in Transfer Pricing

Latest Developments in Transfer Pricing Bombay Chartered Accountant s Society October 11, 2017 Vispi T. Patel Vispi T. Patel & Associates Transfer Pricing (TP) Indian Perspective TP Regulations in India

Latest Developments in Transfer Pricing Bombay Chartered Accountant s Society October 11, 2017 Vispi T. Patel Vispi T. Patel & Associates Transfer Pricing (TP) Indian Perspective TP Regulations in India

Transfer Pricing Country Summary Israel

Page 1 of 11 Transfer Pricing Country Summary Israel September 2018 Page 2 of 11 Legislation Existence of Transfer Pricing Laws/Guidelines The current legal framework in Israel is based mainly upon Section

Page 1 of 11 Transfer Pricing Country Summary Israel September 2018 Page 2 of 11 Legislation Existence of Transfer Pricing Laws/Guidelines The current legal framework in Israel is based mainly upon Section

Transfer Pricing Country Summary Pakistan

Page 1 of 7 Transfer Pricing Country Summary Pakistan July 2018 Page 2 of 7 Legislation Existence of Transfer Pricing Laws/Guidelines There is a general anti-avoidance rule in the Pakistani tax law that

Page 1 of 7 Transfer Pricing Country Summary Pakistan July 2018 Page 2 of 7 Legislation Existence of Transfer Pricing Laws/Guidelines There is a general anti-avoidance rule in the Pakistani tax law that

An overview of Transfer Pricing

An overview of Transfer Pricing Vispi T. Patel Vispi T. Patel & Associates March 14, 2015 1 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations

An overview of Transfer Pricing Vispi T. Patel Vispi T. Patel & Associates March 14, 2015 1 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations

Recent Developments in Transfer Pricing in India. International Tax Conference Mumbai, December 7, 2013

Recent Developments in Transfer Pricing in India International Tax Conference Mumbai, December 7, 2013 Our Panelists G. C. Srivastava, Former DG International Tax Kamlesh Varshney, Commissioner APA Vinod

Recent Developments in Transfer Pricing in India International Tax Conference Mumbai, December 7, 2013 Our Panelists G. C. Srivastava, Former DG International Tax Kamlesh Varshney, Commissioner APA Vinod

Recent developments in Transfer Pricing

Recent developments in Transfer Pricing 18 August 2013 1 Transfer Pricing in the news Indian Revenue authorities are reckoned to be tough globally in TP matters, with India accounting for about 70% of

Recent developments in Transfer Pricing 18 August 2013 1 Transfer Pricing in the news Indian Revenue authorities are reckoned to be tough globally in TP matters, with India accounting for about 70% of

Methods of determining ALP

3 rd Intensive Study Course on Transfer Pricing Methods of determining ALP CA Vishwanath Kane 16 February 2013 Agenda Introduction Transfer Pricing Methods Overview Applicability of Transfer Pricing Methods

3 rd Intensive Study Course on Transfer Pricing Methods of determining ALP CA Vishwanath Kane 16 February 2013 Agenda Introduction Transfer Pricing Methods Overview Applicability of Transfer Pricing Methods

Indian Tax Administration releases final rules on Country-by-Country reporting and Master File implementation

6 November 2017 Global Tax Alert News from Transfer Pricing Indian Tax Administration releases final rules on Country-by-Country reporting and Master File implementation EY Global Tax Alert Library Access

6 November 2017 Global Tax Alert News from Transfer Pricing Indian Tax Administration releases final rules on Country-by-Country reporting and Master File implementation EY Global Tax Alert Library Access

Commissioner of Income Tax Appellant. Versus. M/s. Global Appliances Inc. USA Respondent

11 TH NANI PALKHIVALA MEMORIAL NATIONAL TAX MOOT COURT COMPETITION, 2015 IN THE HIGH COURT OF JUDICATURE AT MADRAS (Ordinary Original Civil Jurisdiction) IN APPEAL NO. OF 2014 IN THE MATTER OF: The Income-tax

11 TH NANI PALKHIVALA MEMORIAL NATIONAL TAX MOOT COURT COMPETITION, 2015 IN THE HIGH COURT OF JUDICATURE AT MADRAS (Ordinary Original Civil Jurisdiction) IN APPEAL NO. OF 2014 IN THE MATTER OF: The Income-tax

Current TP Litigation Scenario Alternative Resolution Mechanisms MAP & APA August 2010

Current TP Litigation Scenario Alternative Resolution Mechanisms MAP & APA Agenda Increasing focus on Transfer Pricing Current litigation status in India Experiences in TP Litigation Alternatives to Litigation

Current TP Litigation Scenario Alternative Resolution Mechanisms MAP & APA Agenda Increasing focus on Transfer Pricing Current litigation status in India Experiences in TP Litigation Alternatives to Litigation

Practical Issues in Transfer Pricing Assessment

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Practical Issues in Transfer Pricing Assessment CA DIGESH RAMBHIA Synopsis Current Indian Transfer Pricing ( TP ) Environment Experiences in TP Audits Key

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Practical Issues in Transfer Pricing Assessment CA DIGESH RAMBHIA Synopsis Current Indian Transfer Pricing ( TP ) Environment Experiences in TP Audits Key

HONG KONG. 1. Introduction. Contact Information Henry Fung Candice Ng

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCHES : I : NEW DELHI

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCHES : I : NEW DELHI BEFORE SHRI R.S. SYAL, AM AND SHRI GEORGE GEORGE K. JM ITA No.282/Del/2012 Assessment Year : 2003-04 DCIT, Circle 11(1), Room No.312,

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCHES : I : NEW DELHI BEFORE SHRI R.S. SYAL, AM AND SHRI GEORGE GEORGE K. JM ITA No.282/Del/2012 Assessment Year : 2003-04 DCIT, Circle 11(1), Room No.312,

The latest guidelines from the ICAI reaffirm specific responsibilities on various stakeholders of Indian companies

Page 1 The latest guidelines from the ICAI reaffirm specific responsibilities on various stakeholders of Indian companies India tax newsletter September, 2016 In this edition of our thought leadership

Page 1 The latest guidelines from the ICAI reaffirm specific responsibilities on various stakeholders of Indian companies India tax newsletter September, 2016 In this edition of our thought leadership

TRANSFER PRICING DEVELOPMENTS IN INDIA

TRANSFER PRICING DEVELOPMENTS IN INDIA T. P. Ostwal & Associates LLP Nanubhai Desai & Co. D T S & Associates For private circulation & internal use only This publication does not constitute professional

TRANSFER PRICING DEVELOPMENTS IN INDIA T. P. Ostwal & Associates LLP Nanubhai Desai & Co. D T S & Associates For private circulation & internal use only This publication does not constitute professional

Recent Judicial Decisions & Developments in Transfer Pricing in India

Recent Judicial Decisions & Developments in Transfer Pricing in India Presented at International Tax Conference, Mumbai 5 th Dec 2009 By Ms Alpana Saksena Indian Revenue Service Commissioner Income Tax

Recent Judicial Decisions & Developments in Transfer Pricing in India Presented at International Tax Conference, Mumbai 5 th Dec 2009 By Ms Alpana Saksena Indian Revenue Service Commissioner Income Tax

Indian Tax Administration releases draft rules on Country-by-Country reporting and Master File implementation for public comment

10 October 2017 Global Tax Alert News from Transfer Pricing Indian Tax Administration releases draft rules on Country-by-Country reporting and Master File implementation for public comment EY Global Tax

10 October 2017 Global Tax Alert News from Transfer Pricing Indian Tax Administration releases draft rules on Country-by-Country reporting and Master File implementation for public comment EY Global Tax

WIRC INTENSIVE COURSE ON TRANSFER PRICING

1 WIRC INTENSIVE COURSE ON TRANSFER PRICING (From 1.08.2011 to 12.08.2011) I. INTRODUCTION What is Transfer Pricing? OVERVIEW OF TRANSFER PRICING By Nilesh Patel; Ex-IRS Officer, CPA(USA) Ph: 9819060323

1 WIRC INTENSIVE COURSE ON TRANSFER PRICING (From 1.08.2011 to 12.08.2011) I. INTRODUCTION What is Transfer Pricing? OVERVIEW OF TRANSFER PRICING By Nilesh Patel; Ex-IRS Officer, CPA(USA) Ph: 9819060323

India releases Annual Report covering transfer pricing and international tax developments

5 September 2014 Global Tax Alert News from Transfer Pricing EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/

5 September 2014 Global Tax Alert News from Transfer Pricing EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/

OECD TP Guidelines July 2017 Brief synopsis

OECD TP Guidelines July 2017 Brief synopsis Introduction to the OECD TP Guidelines Snapshot OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations Commonly referred to as

OECD TP Guidelines July 2017 Brief synopsis Introduction to the OECD TP Guidelines Snapshot OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations Commonly referred to as

OECD DISCUSSION DRAFT ON TRANSFER PRICING COMPARABILITY AND DEVELOPING COUNTRIES

Paris: 11 April 2014 OECD DISCUSSION DRAFT ON TRANSFER PRICING COMPARABILITY AND DEVELOPING COUNTRIES Submitted by email: TransferPricing@oecd.org Dear Joe, Please find below BIAC s comments on the OECD

Paris: 11 April 2014 OECD DISCUSSION DRAFT ON TRANSFER PRICING COMPARABILITY AND DEVELOPING COUNTRIES Submitted by email: TransferPricing@oecd.org Dear Joe, Please find below BIAC s comments on the OECD

BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING

CONTENTS BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING CHAPTER 1 : INTRODUCTION 3 CHAPTER 2 : FEATURES OF THE TRANSFER PRICING REGIME UNDER CHAPTER X 10 CHAPTER 3 : TRANSFER PRICING PROVISIONS OF CHAPTER

CONTENTS BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING CHAPTER 1 : INTRODUCTION 3 CHAPTER 2 : FEATURES OF THE TRANSFER PRICING REGIME UNDER CHAPTER X 10 CHAPTER 3 : TRANSFER PRICING PROVISIONS OF CHAPTER

September WHAT'S INSIDE... Direct Tax Transfer Pricing Indirect Tax

September 16-30 WHAT'S INSIDE... Direct Tax Transfer Pricing Indirect Tax What s inside DIRECT TAX 1. Payment for technical services made for earning future source of income outside India is covered by

September 16-30 WHAT'S INSIDE... Direct Tax Transfer Pricing Indirect Tax What s inside DIRECT TAX 1. Payment for technical services made for earning future source of income outside India is covered by

Issues in Domestic Transfer Pricing including various methods for determining ALP

Issues in Domestic Transfer Pricing including various methods for determining ALP Rakesh Alshi, Anand Thacker - 6 th October 2014 2014 Deloitte Haskins & Sells LLP 1 Contents 1. Specified Domestic Transactions

Issues in Domestic Transfer Pricing including various methods for determining ALP Rakesh Alshi, Anand Thacker - 6 th October 2014 2014 Deloitte Haskins & Sells LLP 1 Contents 1. Specified Domestic Transactions

Domestic Transfer Pricing

Domestic Transfer Pricing By CA Nihar Jambusaria Central Council Member ICAI {Mumbai} Overview Transfer pricing (referred to as TP) regulations introduced in India in 2001, previously covered only cross

Domestic Transfer Pricing By CA Nihar Jambusaria Central Council Member ICAI {Mumbai} Overview Transfer pricing (referred to as TP) regulations introduced in India in 2001, previously covered only cross

Transfer Pricing Issues in India A Practitioner View

Transfer Pricing Issues in India A Practitioner View Mumbai December 2, 2005 Shyamal Mukherjee Agenda Transfer Pricing (TP) audits Application of TP principles for attributing profits to Permanent Establishments

Transfer Pricing Issues in India A Practitioner View Mumbai December 2, 2005 Shyamal Mukherjee Agenda Transfer Pricing (TP) audits Application of TP principles for attributing profits to Permanent Establishments

Taxpayers TPO's computation Post Tribunal's rulings. No. of comparab les % 2.05% % (Excellence Data) 3

3") KPMG FLASH NEWS KPMG IN INDIA The Hyderabad Tribunal adjudicates on rejection of certain comparables from the standard ITES set selected by the TPO in three different rulings, consequentially dropping

KPMG FLASH NEWS KPMG IN INDIA The Hyderabad Tribunal adjudicates on rejection of certain comparables from the standard ITES set selected by the TPO in three different rulings, consequentially dropping

Decoding Enhanced Transfer Pricing Documentation Requirements in India

Decoding Enhanced Transfer Pricing Documentation Requirements in India Meghnand Dungarwal Principal, Transfer Pricing Advisory Contents Indian transfer pricing documentation requirements - recent updates

Decoding Enhanced Transfer Pricing Documentation Requirements in India Meghnand Dungarwal Principal, Transfer Pricing Advisory Contents Indian transfer pricing documentation requirements - recent updates

Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria

![Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria](/thumbs/90/101594279.jpg "Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria") Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria Key Amendments to Form 3CD. The Central Board of Direct Taxes (CBDT) via Notification No. 33/2018 dated 20th July, 2018 has

Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria Key Amendments to Form 3CD. The Central Board of Direct Taxes (CBDT) via Notification No. 33/2018 dated 20th July, 2018 has

Transfer Pricing and Other Provisions to Check Avoidance of Tax

16 Transfer Pricing and Other Provisions to Check Avoidance of Tax Question 1 State the consequences that would follow if the Assessing Officer makes adjustment to arm s length price in international transactions

16 Transfer Pricing and Other Provisions to Check Avoidance of Tax Question 1 State the consequences that would follow if the Assessing Officer makes adjustment to arm s length price in international transactions

India releases final rules on country-by-country reporting and master file

Arm s Length Standard Global views within reach. India releases final rules on country-by-country reporting and master file India s Central Board of Direct Taxes (CBDT) on 31 October released the final

Arm s Length Standard Global views within reach. India releases final rules on country-by-country reporting and master file India s Central Board of Direct Taxes (CBDT) on 31 October released the final

INTERNATIONAL TAXATION Case Law Update

CA Tarunkumar Singhal & Sunil Moti Lala, Advocate INTERNATIONAL TAXATION A. SUPREME COURT RULINGS 1. Where the transfer pricing addition made in the final assessment order pursuant to original assessment

CA Tarunkumar Singhal & Sunil Moti Lala, Advocate INTERNATIONAL TAXATION A. SUPREME COURT RULINGS 1. Where the transfer pricing addition made in the final assessment order pursuant to original assessment

Advance Pricing Agreement Scope & Procedure Will it mitigate Litigation?

SPECIAL STORY Advance Rulings & Settlement Commission CA. Rajesh S. Athavale Advance Pricing Agreement Scope & Procedure Will it mitigate Litigation? Globally, transfer pricing has emerged as one of the

SPECIAL STORY Advance Rulings & Settlement Commission CA. Rajesh S. Athavale Advance Pricing Agreement Scope & Procedure Will it mitigate Litigation? Globally, transfer pricing has emerged as one of the

BY CA MAYUR B NAYAK 1

BY CA MAYUR B NAYAK 1 Govt. should collect taxes from citizens the way a Bee collects Honey from the flowers - quietly without inflicting pain". -Chanakya BY CA MAYUR B NAYAK 2 Financial Year Transfer

BY CA MAYUR B NAYAK 1 Govt. should collect taxes from citizens the way a Bee collects Honey from the flowers - quietly without inflicting pain". -Chanakya BY CA MAYUR B NAYAK 2 Financial Year Transfer