Giving USA 2015 The Annual Report on Philanthropy for the Year 2014

|

|

|

- Edgar Sullivan

- 5 years ago

- Views:

Transcription

1 AllianceForNevadaNonprofits.org 1 Welcome to the 2015 Giving USA Alliance for Nevada Nonprofits Briefing Giving USA 2015 The Annual Report on Philanthropy for the Year 2014 Richard Tollefson, President

2 AllianceForNevadaNonprofits.org 2 3 Giving USA 2015 The Annual Report on Philanthropy for the Year 2014 Researched and written by 4 What is Giving USA? Who is the Giving Institute? The longest running, annual report on U.S. charitable giving Published by Giving USA Foundation TM, a part of the Giving Institute Begun in 1956 Researched and written by the Indiana University Lilly Family School of Philanthropy Made possible by contributions from The Giving Institute member firms, foundations, and other donors Is a part of member firms public service to the profession

3 AllianceForNevadaNonprofits.org 3 Overview 5 What is Giving USA? 2014 contributions, by source and recipient type Rates of change for giving in last two years Trends in total giving, giving by source, giving by recipient type Economic trends which impact giving Trends in volunteering Trends in number of nonprofit organizations 2014 contributions: $ billion by source (in billions of dollars all figures are rounded) 6

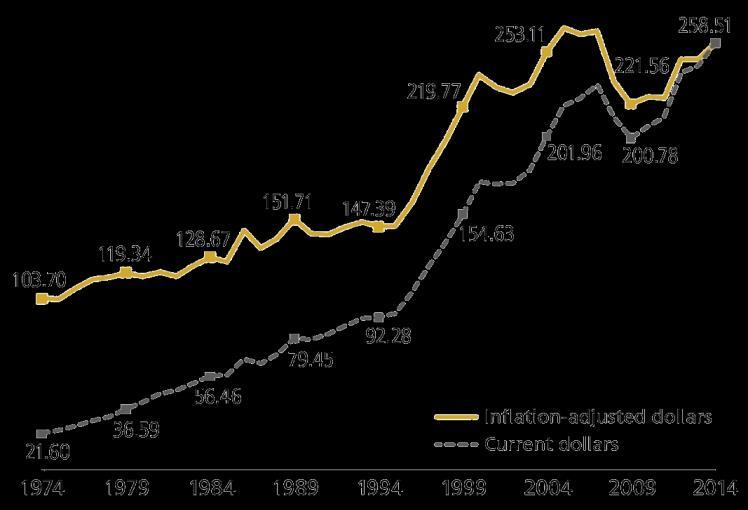

4 AllianceForNevadaNonprofits.org 4 Changes in giving by source , , and (in current dollars) 7 Changes in giving by source , , and (in inflation-adjusted dollars, 2014 = $100) 8

5 AllianceForNevadaNonprofits.org 5 Total giving, Giving by individuals,

6 AllianceForNevadaNonprofits.org 6 Giving by foundations, Giving by bequest,

7 AllianceForNevadaNonprofits.org 7 Giving by corporations, Giving by source: Percentage of the total in five-year spans, (in inflation-adjusted dollars, 2014 = $100) 14

8 AllianceForNevadaNonprofits.org 8 Total giving by source in five-year spans, (in billions of inflation-adjusted dollars, 2014 = $100) 15 Trends in total giving,

17 18 Total charitable")

9 AllianceForNevadaNonprofits.org 9 Total giving as a percentage of Gross Domestic Product, (in inflation-adjusted dollars, 2014 = $100) Total charitable giving graphed with the Standard & Poor's 500 Index, (in billions of inflation-adjusted dollars, 2014 = $100)

10 AllianceForNevadaNonprofits.org 10 Individual giving as a percentage of disposable personal income, (in current dollars) 19 Corporate giving as a percentage of corporate pre-tax profits, (in current dollars) 20

11 AllianceForNevadaNonprofits.org contributions: $ billion by type of recipient organization (in billions of dollars all figures are rounded) 21 Changes in giving by type of recipient organization, , , and (in current dollars) 22

12 AllianceForNevadaNonprofits.org Changes in giving by type of recipient organization, , , and (in inflation-adjusted dollars, 2014 = $100) Giving to religion,

13 AllianceForNevadaNonprofits.org 13 Giving to education, Giving to human services,

14 AllianceForNevadaNonprofits.org 14 Giving to foundations, * 27 Giving to health,

15 AllianceForNevadaNonprofits.org 15 Giving to public-society benefit, Giving to arts, culture, and humanities,

16 AllianceForNevadaNonprofits.org 16 Giving to international affairs, * 31 Giving to environment/animals, * 32

17 AllianceForNevadaNonprofits.org Giving by type of recipient as a percentage of the total in five-year spans, * (adjusted for inflation, 2014 = $100; does not include unallocated ) 34 Total giving by type of recipient organization in five-year spans, (in billions of inflation-adjusted dollars, 2014 = $100; does not include unallocated )

18 AllianceForNevadaNonprofits.org 18 Number of volunteers in millions of people, Volunteer rate,

(3) organizations,")

19 AllianceForNevadaNonprofits.org 19 The number of 501(c)(3) organizations, Like what you heard? Visit to purchase the complete report! To receive your 30% discount enter code 3015GI

20 AllianceForNevadaNonprofits.org 20 Thank you!

Giving USA 2015 The Annual Report on Philanthropy for the Year 2014

Giving USA 2015 The Annual Report on Philanthropy for the Year 2014 Giving USA 2015 PowerPoint Presentation User s Guide Graphs in this PowerPoint presentation are developed for use in presentations only.

Giving USA 2015 The Annual Report on Philanthropy for the Year 2014 Giving USA 2015 PowerPoint Presentation User s Guide Graphs in this PowerPoint presentation are developed for use in presentations only.

Now What? Stewarding the Planned Gift Donor

Now What? Stewarding the Planned Gift Donor Planned Giving Council of NE Florida February 8, 2018 Pierre N. Allaire, PhD Senior Vice President Baptist Health Foundation What do you think you need for a

Now What? Stewarding the Planned Gift Donor Planned Giving Council of NE Florida February 8, 2018 Pierre N. Allaire, PhD Senior Vice President Baptist Health Foundation What do you think you need for a

Mechanisms of Action. Three strategies to connect with your donors and inspire big gifts.

Mechanisms of Action Three strategies to connect with your donors and inspire big gifts. Presenter Eric B. Javier, Principal & Managing Director, CCS Fundraising June 13, 2018 1 Agenda 1. Current Trends

Mechanisms of Action Three strategies to connect with your donors and inspire big gifts. Presenter Eric B. Javier, Principal & Managing Director, CCS Fundraising June 13, 2018 1 Agenda 1. Current Trends

spotlight Giving during recessions and economic slowdowns GIVING USA

Published by Giving USA Foundation and written and researched at the Center on Philanthropy at Indiana University spotlight GIVING USA ISSUE 3, 2008 Giving during recessions and economic slowdowns Introduction

Published by Giving USA Foundation and written and researched at the Center on Philanthropy at Indiana University spotlight GIVING USA ISSUE 3, 2008 Giving during recessions and economic slowdowns Introduction

2018 FUNDRAISING OUTLOOK. A synopsis of America s donation habits and trends for the future

2018 FUNDRAISING OUTLOOK A synopsis of America s donation habits and trends for the future Giving USA published its latest report¹ in June of last year revealing that giving by individuals had increased

2018 FUNDRAISING OUTLOOK A synopsis of America s donation habits and trends for the future Giving USA published its latest report¹ in June of last year revealing that giving by individuals had increased

The 2008 Bank of America Study of High Net Worth Philanthropy Issues Driving Charitable Activities Among Affluent Households

The 2008 Bank of America Study of High Net Worth Philanthropy Issues Driving Charitable Activities Among Affluent Households April 20, 2010 Ramsay H. Slugg Senior Vice President National Wealth Strategies

The 2008 Bank of America Study of High Net Worth Philanthropy Issues Driving Charitable Activities Among Affluent Households April 20, 2010 Ramsay H. Slugg Senior Vice President National Wealth Strategies

The 2008 Study of High Net Worth Philanthropy

The 2008 Study of High Net Worth Philanthropy Issues Driving Charitable Activities among Affluent Households March 2009 Sponsored by Researched and Written by We especially thank the Indiana University

The 2008 Study of High Net Worth Philanthropy Issues Driving Charitable Activities among Affluent Households March 2009 Sponsored by Researched and Written by We especially thank the Indiana University

The 2010 Study of High Net Worth Philanthropy

The 2010 Study of High Net Worth Philanthropy Issues Driving Charitable Activities among Affluent Households November 2010 1 Sponsored by Researched and Written by We especially thank Indiana University

The 2010 Study of High Net Worth Philanthropy Issues Driving Charitable Activities among Affluent Households November 2010 1 Sponsored by Researched and Written by We especially thank Indiana University

Hawai i Community Foundation

2015 SUMMARY HIGHLIGHTS Hawai i continues to have high levels (93%) of household participation in giving cash, goods or time (volunteering). Volunteering is at the highest level seen in these giving studies

2015 SUMMARY HIGHLIGHTS Hawai i continues to have high levels (93%) of household participation in giving cash, goods or time (volunteering). Volunteering is at the highest level seen in these giving studies

The Charitable Gift Annuity

Mid-America Planned Giving Conference August 14, 2015 The Charitable Gift Annuity Presented by John F. Marshall Senior Vice President Jeffrey Byrne + Associates, Inc. Jeffrey Byrne + Associates, Inc. National

Mid-America Planned Giving Conference August 14, 2015 The Charitable Gift Annuity Presented by John F. Marshall Senior Vice President Jeffrey Byrne + Associates, Inc. Jeffrey Byrne + Associates, Inc. National

Session 2 Philanthropic Trends: Impact of High Net Worth, Gender, and Generational Trends on Giving and Volunteering

Session 2 Philanthropic Trends: Impact of High Net Worth, Gender, and Generational Trends on Giving and Volunteering Sisters of Charity of Nazareth Advancing Mission Session #2 Wednesday, October 28, 2015

Session 2 Philanthropic Trends: Impact of High Net Worth, Gender, and Generational Trends on Giving and Volunteering Sisters of Charity of Nazareth Advancing Mission Session #2 Wednesday, October 28, 2015

The Alford Group Summer Webinar Series

The Alford Group Summer Webinar Series July September 2016 Check back for announcements of additional webinars at www.alford.com Strengthening the not-for-profit community About The Alford Group Mission:

The Alford Group Summer Webinar Series July September 2016 Check back for announcements of additional webinars at www.alford.com Strengthening the not-for-profit community About The Alford Group Mission:

The Effect of the Economy On the Nonprofit Sector

GuideStar, June 2010 Survey 1 The Effect of the Economy On the Nonprofit Sector A June 2010 Survey Chuck McLean, Vice President of Research Carol Brouwer, Research Assistant GuideStar, June 2010 Survey

GuideStar, June 2010 Survey 1 The Effect of the Economy On the Nonprofit Sector A June 2010 Survey Chuck McLean, Vice President of Research Carol Brouwer, Research Assistant GuideStar, June 2010 Survey

How to Talk to Clients About Philanthropy: What They Need and Expect. Kathryn W. Miree & Associates, Inc.

How to Talk to Clients About Philanthropy: What They Need and Expect Kathryn W. Miree & Associates, Inc. What We Know About Charitable Giving in the United States Source Amount in Billions Percentage of

How to Talk to Clients About Philanthropy: What They Need and Expect Kathryn W. Miree & Associates, Inc. What We Know About Charitable Giving in the United States Source Amount in Billions Percentage of

The 2018 U.S. Trust Study of High Net Worth Philanthropy 1

The 2018 U.S. Trust Study of High Net Worth Philanthropy 1 Conducted in partnership with the Indiana University Lilly Family School of Philanthropy Executive Summary Insights into the motivations, priorities

The 2018 U.S. Trust Study of High Net Worth Philanthropy 1 Conducted in partnership with the Indiana University Lilly Family School of Philanthropy Executive Summary Insights into the motivations, priorities

Region Report Oceania

Region Report Oceania Regional Reviewer: Susan Barker Institutional Affiliation: Sue Barker Charities Law With contributions from staff at the Indiana University Lilly Family School of Philanthropy Overview

Region Report Oceania Regional Reviewer: Susan Barker Institutional Affiliation: Sue Barker Charities Law With contributions from staff at the Indiana University Lilly Family School of Philanthropy Overview

Canada QUICK FACTS. Five main social issues addressed by these organizations: Higher Education, Arts and Culture, Religion, Human Rights, Health

Canada Expert: Arthur B.C.Drache Institutional Affiliation: Drache Aptowitzer LLP Reviewer: Kathi Badertscher. IUPUI Lilly Family School of Philanthropy. With contributions from staff at the Indiana University

Canada Expert: Arthur B.C.Drache Institutional Affiliation: Drache Aptowitzer LLP Reviewer: Kathi Badertscher. IUPUI Lilly Family School of Philanthropy. With contributions from staff at the Indiana University

chevron humankind program guidelines

chevron humankind program guidelines Table of contents Chevron Humankind... 1 Scope... 1 Contribution limits... 2 Eligible participants... 2 Eligible recipient organizations... 2 Restrictions on contribution

chevron humankind program guidelines Table of contents Chevron Humankind... 1 Scope... 1 Contribution limits... 2 Eligible participants... 2 Eligible recipient organizations... 2 Restrictions on contribution

Gift Policy. Responsible Officer. Vice-Chancellor Approved by

Gift Policy Responsible Officer Vice-Chancellor Approved by Council Approved and commenced August, 2012 Review by August, 2015 Relevant Legislation, Ordinance, Rule and/or Governance Level Principle Scholarships

Gift Policy Responsible Officer Vice-Chancellor Approved by Council Approved and commenced August, 2012 Review by August, 2015 Relevant Legislation, Ordinance, Rule and/or Governance Level Principle Scholarships

Planned Giving 101 The Basics or So, this is how we ll build our endowment! A Presentation for 2014 Management Conference Magic and Mayhem

Planned Giving 101 The Basics or So, this is how we ll build our endowment! A Presentation for 2014 Management Conference Magic and Mayhem by James E. Gillespie, President & CEO of P.O. Box 50332 Indianapolis,

Planned Giving 101 The Basics or So, this is how we ll build our endowment! A Presentation for 2014 Management Conference Magic and Mayhem by James E. Gillespie, President & CEO of P.O. Box 50332 Indianapolis,

FRIENDS OF FONDATION DE FRANCE, INC. FINANCIAL STATEMENTS DECEMBER 31, 2015 AND 2014

FINANCIAL STATEMENTS INDEPENDENT AUDITORS REPORT To the Board of Directors of Friends of Fondation De France, Inc. We have audited the accompanying financial statements of Friends of Fondation De France,

FINANCIAL STATEMENTS INDEPENDENT AUDITORS REPORT To the Board of Directors of Friends of Fondation De France, Inc. We have audited the accompanying financial statements of Friends of Fondation De France,

Oregon Country Fair Gift Acceptance Policies adopted May 2018

Oregon Country Fair Gift Acceptance Policies adopted May 2018 The Oregon Country Fair (OCF, or The Fair) creates events and experiences that nourish the spirit, explore living artfully and authentically

Oregon Country Fair Gift Acceptance Policies adopted May 2018 The Oregon Country Fair (OCF, or The Fair) creates events and experiences that nourish the spirit, explore living artfully and authentically

Kuwait QUICK FACTS. Average time established by law to register a philanthropic organization: 0-30 days

Kuwait Expert: Abdulrazzak Al Shayji and Samir Abu Rumman Institutional Affiliation: Kuwait University and Gulf Opinions With contributions from staff at the Indiana University Lilly Family School of Philanthropy

Kuwait Expert: Abdulrazzak Al Shayji and Samir Abu Rumman Institutional Affiliation: Kuwait University and Gulf Opinions With contributions from staff at the Indiana University Lilly Family School of Philanthropy

Thank you for attending Giving USA 2017: The State of Philanthropy

Thank you for attending Giving USA 2017: The State of Philanthropy August 1, 2017 Seattle Breakfast Hosted by The Alford Group and Pacific Continental Bank Presented by: Thomas W. Mesaros Karen Rotko-Wynn,

Thank you for attending Giving USA 2017: The State of Philanthropy August 1, 2017 Seattle Breakfast Hosted by The Alford Group and Pacific Continental Bank Presented by: Thomas W. Mesaros Karen Rotko-Wynn,

Giving in the Netherlands 2013

Giving in the Netherlands 2013 Prof. Th.N.M. Schuyt, Ph.D., Gouwenberg, B.M. & Prof. R.H.F.P. Bekkers, Ph.D. (Eds., 2013). Giving in the Netherlands: Donations, Bequests, Sponsorship and Volunteering.

Giving in the Netherlands 2013 Prof. Th.N.M. Schuyt, Ph.D., Gouwenberg, B.M. & Prof. R.H.F.P. Bekkers, Ph.D. (Eds., 2013). Giving in the Netherlands: Donations, Bequests, Sponsorship and Volunteering.

Donor-advised Fund Agreement

Donor-advised Fund Agreement Welcome to the Community Foundation family. Thank you for choosing the Community Foundation for Greater Atlanta. Our staff is available to assist you at any time with a wide

Donor-advised Fund Agreement Welcome to the Community Foundation family. Thank you for choosing the Community Foundation for Greater Atlanta. Our staff is available to assist you at any time with a wide

Professional Advisor and Community Foundation Collaborations. Presented by Bryan Clontz, CFP, CAP

Professional Advisor and Community Foundation Collaborations Presented by Bryan Clontz, CFP, CAP bryan@charitablesolutionsllc.com (404) 375-5496 Agenda Why are Professional Advisors so Critical to Community

Professional Advisor and Community Foundation Collaborations Presented by Bryan Clontz, CFP, CAP bryan@charitablesolutionsllc.com (404) 375-5496 Agenda Why are Professional Advisors so Critical to Community

SEMPRA ENERGY FOUNDATION. Financial Statements December 31, 2016 and 2015 (With Independent Auditor s Report Thereon)

") Financial Statements December 31, 2016 and 2015 (With Independent Auditor s Report Thereon) Table of Contents Independent Auditor s Report... 1 Financial Statements Page Statements of Financial Position...

Financial Statements December 31, 2016 and 2015 (With Independent Auditor s Report Thereon) Table of Contents Independent Auditor s Report... 1 Financial Statements Page Statements of Financial Position...

NEW FUND AGREEMENT. P. O. Box 4334 Grand Junction, CO 81502

NEW FUND AGREEMENT I/We agree to make an irrevocable donation to The Western Colorado Community Foundation, Inc. (WCCF) in accordance with the terms of this New Fund Agreement. I/We acknowledge that I/we

NEW FUND AGREEMENT I/We agree to make an irrevocable donation to The Western Colorado Community Foundation, Inc. (WCCF) in accordance with the terms of this New Fund Agreement. I/We acknowledge that I/we

Articles of Incorporation. Of the. North Star Community Foundation

2 Articles of Incorporation Of the North Star Community Foundation The undersigned incorporators, of the age of nineteen (19) or more, do this day voluntarily associate for the purpose of forming a non-profit

2 Articles of Incorporation Of the North Star Community Foundation The undersigned incorporators, of the age of nineteen (19) or more, do this day voluntarily associate for the purpose of forming a non-profit

A Legacy for the Betterment of the World. How Planned Giving Can Make a Lasting Difference

A Legacy for the Betterment of the World. How Planned Giving Can Make a Lasting Difference About Mona Mona Foundation was founded in 1999 by a small group of people committed to making life better for

A Legacy for the Betterment of the World. How Planned Giving Can Make a Lasting Difference About Mona Mona Foundation was founded in 1999 by a small group of people committed to making life better for

India QUICK FACTS. Legal forms of philanthropic organizations included in the law: Trust, Society, Limited Liability Company

India Expert: Noshir Dadrawala Institutional Affiliation: Centre for Advancement of Philanthropy With contributions from staff at the Indiana University Lilly Family School of Philanthropy QUICK FACTS

India Expert: Noshir Dadrawala Institutional Affiliation: Centre for Advancement of Philanthropy With contributions from staff at the Indiana University Lilly Family School of Philanthropy QUICK FACTS

Philanthropic Freedom Pilot Study: China Country Report Overall Philanthropic Freedom Score: 2.18

Philanthropic Freedom Pilot Study: China Country Report Overall Philanthropic Freedom Score: 2.18 General Background Information on China GDP per capita: $5,445 1 Population: 1.3 billion 2 Percent of population

Philanthropic Freedom Pilot Study: China Country Report Overall Philanthropic Freedom Score: 2.18 General Background Information on China GDP per capita: $5,445 1 Population: 1.3 billion 2 Percent of population

The Global Philanthropy Environment Index 2018

The Global Philanthropy Environment Index 2018 European Edition LILLY FAMILY SCHOOL OF PHILANTHROPY INDIANA UNIVERSITY OCTOBER, 2018 EUROPE AT A GLANCE The European special edition of the 2018 Global Philanthropy

The Global Philanthropy Environment Index 2018 European Edition LILLY FAMILY SCHOOL OF PHILANTHROPY INDIANA UNIVERSITY OCTOBER, 2018 EUROPE AT A GLANCE The European special edition of the 2018 Global Philanthropy

Donor-advised Fund Agreement

Donor-advised Fund Agreement WELCOME TO THE COMMUNITY FOUNDATION FAMILY Thank you for choosing the Community Foundation for Greater Atlanta. Our staff is available to assist you at any time with a wide

Donor-advised Fund Agreement WELCOME TO THE COMMUNITY FOUNDATION FAMILY Thank you for choosing the Community Foundation for Greater Atlanta. Our staff is available to assist you at any time with a wide

Effects of Limiting Charitable Deductions on Nonprofit Finances

Effects of Limiting Charitable Deductions on Nonprofit Finances Joseph Cordes The George Washington University Center on Nonprofits and Philanthropy The Urban Institute Talking Points Why elasticity matters:

Effects of Limiting Charitable Deductions on Nonprofit Finances Joseph Cordes The George Washington University Center on Nonprofits and Philanthropy The Urban Institute Talking Points Why elasticity matters:

HOUSE TAX REFORM BILL SUMMARY

HOUSE TAX REFORM BILL SUMMARY Section Bill Proposal Current Law Proposed Change Notes 1002 1306 Enhancement of standard deduction Charitable Contributions The standard deduction is $6,350 for single individuals

HOUSE TAX REFORM BILL SUMMARY Section Bill Proposal Current Law Proposed Change Notes 1002 1306 Enhancement of standard deduction Charitable Contributions The standard deduction is $6,350 for single individuals

October 2010 PRESENTED BY. Visual SenseMaking by Humantific 2010 Liquidnet Holdings, Inc.

October 2010 Liquidnet is the premier global marketplace for institutional investors. Since 2007, the company has devoted a percentage of revenues to social causes through an award-winning corporate social

October 2010 Liquidnet is the premier global marketplace for institutional investors. Since 2007, the company has devoted a percentage of revenues to social causes through an award-winning corporate social

Hong Kong QUICK FACTS. Legal forms of philanthropic organizations included in the law: Company Limited by Guarantee, Trust, Society

Hong Kong Expert: Kin-man CHAN Institutional Affiliation: The Chinese University of Hong Kong With contributions from staff at the Indiana University Lilly Family School of Philanthropy QUICK FACTS Legal

Hong Kong Expert: Kin-man CHAN Institutional Affiliation: The Chinese University of Hong Kong With contributions from staff at the Indiana University Lilly Family School of Philanthropy QUICK FACTS Legal

Creating Philanthropy using Noncash Assets: Community Foundation Case Studies

Creating Philanthropy using Noncash Assets: Community Foundation Case Studies 1 Agenda Quick Intros Benefits to using Community Foundations Donor-Advised Funds Noncash Assets Statistics Case Studies 2

Creating Philanthropy using Noncash Assets: Community Foundation Case Studies 1 Agenda Quick Intros Benefits to using Community Foundations Donor-Advised Funds Noncash Assets Statistics Case Studies 2

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS Joseph Rosenberg and Eugene Steuerle November 15, 2018 The federal tax treatment of charitable giving and the nonprofit sector

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS Joseph Rosenberg and Eugene Steuerle November 15, 2018 The federal tax treatment of charitable giving and the nonprofit sector

Bank of America Study of High Net-Worth Philanthropy Initial Report. Researched and Written by

Bank of America Study of High Net-Worth Philanthropy Initial Report Researched and Written by October 2006 Bank of America The Philanthropic Management group within Bank of America delivers expertise and

Bank of America Study of High Net-Worth Philanthropy Initial Report Researched and Written by October 2006 Bank of America The Philanthropic Management group within Bank of America delivers expertise and

Global Impact Funding Trust

Global Impact Funding Trust 1 Welcome to GIFT. One of the great dividends of financial success is the pleasure of giving back to your community, in support of a social cause, to benefit those in need or

Global Impact Funding Trust 1 Welcome to GIFT. One of the great dividends of financial success is the pleasure of giving back to your community, in support of a social cause, to benefit those in need or

Untapped Fundraising Potential: Demystifying Donor-Advised Funds

Untapped Fundraising Potential: Demystifying Donor-Advised Funds March 20, 2018 Presenters: Eva Nico, Senior Director of Programs, GuideStar Amy Pirozzolo, VP Marketing, Fidelity Charitable Today s Speakers

Untapped Fundraising Potential: Demystifying Donor-Advised Funds March 20, 2018 Presenters: Eva Nico, Senior Director of Programs, GuideStar Amy Pirozzolo, VP Marketing, Fidelity Charitable Today s Speakers

A Resource for Charitable Giving

A Resource for Charitable Giving Your clients care about giving. At the Community Foundation we help people contribute to their community during their lifetime, and through planned giving. Partnering with

A Resource for Charitable Giving Your clients care about giving. At the Community Foundation we help people contribute to their community during their lifetime, and through planned giving. Partnering with

TAX POLICY & CHARITABLE GIVING

TAX POLICY & CHARITABLE GIVING October 5, 2017 Joyce Dulworth, CPA Partner jdulworth@bkd.com Una Osili Associate Dean for Research & International Programs Lilly Family School of Philanthropy uosili@iupui.edu

TAX POLICY & CHARITABLE GIVING October 5, 2017 Joyce Dulworth, CPA Partner jdulworth@bkd.com Una Osili Associate Dean for Research & International Programs Lilly Family School of Philanthropy uosili@iupui.edu

SEMPRA ENERGY FOUNDATION. Financial Statements December 31, 2017 and 2016 (With Independent Auditor s Report Thereon)

") Financial Statements December 31, 2017 and 2016 (With Independent Auditor s Report Thereon) Table of Contents Independent Auditor s Report... 1 Financial Statements Page Statements of Financial Position...

Financial Statements December 31, 2017 and 2016 (With Independent Auditor s Report Thereon) Table of Contents Independent Auditor s Report... 1 Financial Statements Page Statements of Financial Position...

Guide to The Philanthropy Outlook Model 2019 & Marts & Lundy. Indiana University Lilly Family School of Philanthropy RESEARCHED AND

Guide to The Philanthropy Outlook Model 2019 & 2020 P R E S E N T E D BY Marts & Lundy RESEARCHED AND W R I T T E N BY Indiana University Lilly Family School of Philanthropy JA N UA RY 2019 Variable Definitions

Guide to The Philanthropy Outlook Model 2019 & 2020 P R E S E N T E D BY Marts & Lundy RESEARCHED AND W R I T T E N BY Indiana University Lilly Family School of Philanthropy JA N UA RY 2019 Variable Definitions

COMMUNITY FOUNDATION. for Palm Beach and Martin Counties. Your Philanthropy Our Community Better Together. a guide for you

COMMUNITY FOUNDATION for Palm Beach and Martin Counties Your Philanthropy Our Community Better Together a guide for you 1 thank you. 2 yourcommunityfoundation.org Thank you for understanding the importance

COMMUNITY FOUNDATION for Palm Beach and Martin Counties Your Philanthropy Our Community Better Together a guide for you 1 thank you. 2 yourcommunityfoundation.org Thank you for understanding the importance

GIVING THROUGH THE COMMUNITY FOUNDATION

GIVING THROUGH THE COMMUNITY FOUNDATION We are a public charity founded in 1949 by and for the people of Linn County. Our mission is to help donors give in meaningful ways, to strengthen nonprofits, and

GIVING THROUGH THE COMMUNITY FOUNDATION We are a public charity founded in 1949 by and for the people of Linn County. Our mission is to help donors give in meaningful ways, to strengthen nonprofits, and

Contents TWELFTH ANNUAL REPORT CARD ON CHARITABLE GIVING FOR METRO MILWAUKEE

TWELFTH ANNUAL REPORT CARD ON CHARITABLE GIVING FOR METRO MILWAUKEE November 2008 PUBLISHED BY GREATER MILWAUKEE FOUNDATION SPONSORS Donors Forum of Wisconsin The Faye McBeath Foundation United Way of

TWELFTH ANNUAL REPORT CARD ON CHARITABLE GIVING FOR METRO MILWAUKEE November 2008 PUBLISHED BY GREATER MILWAUKEE FOUNDATION SPONSORS Donors Forum of Wisconsin The Faye McBeath Foundation United Way of

Annual Giving Report 2015

Annual Giving Report 2015 2 Annual Giving Report 2015 Fiscal Year 2015 Highlights Inspired donors to unlock assets for charitable good Helped donors give more Made giving easier and more convenient Helped

Annual Giving Report 2015 2 Annual Giving Report 2015 Fiscal Year 2015 Highlights Inspired donors to unlock assets for charitable good Helped donors give more Made giving easier and more convenient Helped

Federal and State Policy Impacting your Nonprofit -Advocacy in Action. Southeast Rural Philanthropy Days June 14, 2018

Federal and State Policy Impacting your Nonprofit -Advocacy in Action Southeast Rural Philanthropy Days June 14, 2018 Outline Advocacy and Lobbying Rules Key Federal Tax and Policy Issues Key State Policies

Federal and State Policy Impacting your Nonprofit -Advocacy in Action Southeast Rural Philanthropy Days June 14, 2018 Outline Advocacy and Lobbying Rules Key Federal Tax and Policy Issues Key State Policies

Planned Giving Made Simple

The webinar will begin at 12 p.m. Central Daylight Time Planned Giving Made Simple April 29, 2015 PRESENTED BY Lynn M. Gaumer, J.D. Senior Technical Consultant The Stelter Company Philip Purcell, J.D.

The webinar will begin at 12 p.m. Central Daylight Time Planned Giving Made Simple April 29, 2015 PRESENTED BY Lynn M. Gaumer, J.D. Senior Technical Consultant The Stelter Company Philip Purcell, J.D.

Welcome to Foundation For The Carolinas. We look forward to being your partner in philanthropy.

Welcome to Foundation For The Carolinas. We look forward to being your partner in philanthropy. Please complete this Agency Fund Agreement form (the Agreement) to establish an Agency Fund ( Agency Fund

Welcome to Foundation For The Carolinas. We look forward to being your partner in philanthropy. Please complete this Agency Fund Agreement form (the Agreement) to establish an Agency Fund ( Agency Fund

Boomer, Gen X, Millennial Women: Do they give differently?

Boomer, Gen X, Millennial Women: Do they give differently? November 29, 2017 Abbie J von Schlegell, CFRE Principal a. von schlegell & co Who Are Boomers? Born 1946 to 1964 AKA: Woodstock Generation 78

Boomer, Gen X, Millennial Women: Do they give differently? November 29, 2017 Abbie J von Schlegell, CFRE Principal a. von schlegell & co Who Are Boomers? Born 1946 to 1964 AKA: Woodstock Generation 78

INCOME Data Dictionary

INCOME 4-0000 MYOB 4-0000 Income For the purposes of this Chart of s, Income is also referred to as Revenue. Revenues are inflows or other enhancements of assets or decreases of liabilities that result

INCOME 4-0000 MYOB 4-0000 Income For the purposes of this Chart of s, Income is also referred to as Revenue. Revenues are inflows or other enhancements of assets or decreases of liabilities that result

PREPARING FOR PHILANTHROPY

PREPARING FOR PHILANTHROPY Hello and welcome. Northern Trust is proud to sponsor this podcast, Preparing for Philanthropy, the fourth in a series based on our book titled Legacy: Conversations about Wealth

PREPARING FOR PHILANTHROPY Hello and welcome. Northern Trust is proud to sponsor this podcast, Preparing for Philanthropy, the fourth in a series based on our book titled Legacy: Conversations about Wealth

15 Not-for-Profit Organizations Regulatory, Taxation, and Performance Issues

Chapter 15 Not-for-Profit Organizations Regulatory, Taxation, and Performance Issues McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 15-2 Learning Objectives After

Chapter 15 Not-for-Profit Organizations Regulatory, Taxation, and Performance Issues McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 15-2 Learning Objectives After

Vanguard Charitable Endowment Program. Financial Statements. For the Years Ended June 30, 2017 and 2016

Financial Statements For the Years Ended June 30, 2017 and 2016 Report of Independent Auditors To the Board of Trustees of Vanguard Charitable Endowment Program We have audited the accompanying financial

Financial Statements For the Years Ended June 30, 2017 and 2016 Report of Independent Auditors To the Board of Trustees of Vanguard Charitable Endowment Program We have audited the accompanying financial

The Economic Impact of Idaho Nonprofits

The Economic Impact of Idaho Nonprofits Janice Fulkerson Executive Director Idaho Nonprofit Center Steven Peterson Clinical Assistant Professor, Economics* University of Idaho * The results and findings

The Economic Impact of Idaho Nonprofits Janice Fulkerson Executive Director Idaho Nonprofit Center Steven Peterson Clinical Assistant Professor, Economics* University of Idaho * The results and findings

PROFESSIONAL COMPENSATION. A Position Paper. Prepared by the AFP Ethics Committee Adopted March, 1992 Revised September 2016

PROFESSIONAL COMPENSATION A Position Paper Prepared by the AFP Ethics Committee Adopted March, 1992 Revised September 2016 SUMMARY For purposes of this paper: Percentage-based compensation for contributions

PROFESSIONAL COMPENSATION A Position Paper Prepared by the AFP Ethics Committee Adopted March, 1992 Revised September 2016 SUMMARY For purposes of this paper: Percentage-based compensation for contributions

Ireland QUICK FACTS. Legal forms of philanthropic organizations included in the law: Association, Corporation, Company Limited by Guarantee, Society

Ireland Expert: Dr. Oonagh B. Breen Institutional Affiliation: Sutherland School of Law, University College Dublin With contributions from staff at the Indiana University Lilly Family School of Philanthropy

Ireland Expert: Dr. Oonagh B. Breen Institutional Affiliation: Sutherland School of Law, University College Dublin With contributions from staff at the Indiana University Lilly Family School of Philanthropy

Individual giving survey 2008

Individual giving survey 2008 BRIEFING FOR NON-PROFIT ORGANISATIONS 18 September 2008 All figures, including percentages, are estimates. Percentages may not add up to 100% due to rounding or multiple answers

Individual giving survey 2008 BRIEFING FOR NON-PROFIT ORGANISATIONS 18 September 2008 All figures, including percentages, are estimates. Percentages may not add up to 100% due to rounding or multiple answers

Austria QUICK FACTS. Five main social issues addressed by these organizations: Basic Needs, Youth and Family, Religion, Animals, International causes

Austria Expert: Ruth Gabler Institutional Affiliation: Independent Expert; Fulbright Austria Austrian-American Educational Commission With contributions from staff at the Indiana University Lilly Family

Austria Expert: Ruth Gabler Institutional Affiliation: Independent Expert; Fulbright Austria Austrian-American Educational Commission With contributions from staff at the Indiana University Lilly Family

Statement on Tax Reform

Statement on Tax Reform Submitted to the Senate Finance Committee United States Senate July 2017 National Association of Charitable Gift Planners 200 S. Meridian Street, Suite 510 Indianapolis, Indiana

Statement on Tax Reform Submitted to the Senate Finance Committee United States Senate July 2017 National Association of Charitable Gift Planners 200 S. Meridian Street, Suite 510 Indianapolis, Indiana

PLANNED GIVING ESSENTIALS

PLANNED GIVING ESSENTIALS PRESENTED BY: ELISA M. SMITH, CPA/PFS PRESENTED FOR: COMMUNITY FOUNDATION OF GREATER FORT WAYNE PRESENTED ON: OCTOBER 7, 2015 OVERVIEW OF PRESENTATION Why you NEED a Planned

PLANNED GIVING ESSENTIALS PRESENTED BY: ELISA M. SMITH, CPA/PFS PRESENTED FOR: COMMUNITY FOUNDATION OF GREATER FORT WAYNE PRESENTED ON: OCTOBER 7, 2015 OVERVIEW OF PRESENTATION Why you NEED a Planned

GIVING USA Executive Summary. The Annual Report on Philanthropy for the Year Researched and written at

GIVING USA 2012 The Annual Report on Philanthropy for the Year 2011 Executive Summary Researched and written at Contributors We are grateful for the generous gifts to Giving USA Foundation for Giving USA

GIVING USA 2012 The Annual Report on Philanthropy for the Year 2011 Executive Summary Researched and written at Contributors We are grateful for the generous gifts to Giving USA Foundation for Giving USA

Summary The Administration s 2010 and 2011 budget outlines contain a proposal to cap the value of itemized deductions at 28%, for high-income taxpayer

Charitable Contributions: The Itemized Deduction Cap and Other FY2011 Budget Options Jane G. Gravelle Senior Specialist in Economic Policy Donald J. Marples Specialist in Public Finance March 18, 2010

Charitable Contributions: The Itemized Deduction Cap and Other FY2011 Budget Options Jane G. Gravelle Senior Specialist in Economic Policy Donald J. Marples Specialist in Public Finance March 18, 2010

CLARK COUNTY PUBLIC EDUCATION FOUNDATION, INC. YEARS ENDED SEPTEMBER 30, 2017 AND 2016

YEARS ENDED SEPTEMBER 30, 2017 AND 2016 YEARS ENDED SEPTEMBER 30, 2017 AND 2016 CONTENTS Page Independent auditors' report 1-2 Financial statements: Statements of financial position 3 Statements of activities

YEARS ENDED SEPTEMBER 30, 2017 AND 2016 YEARS ENDED SEPTEMBER 30, 2017 AND 2016 CONTENTS Page Independent auditors' report 1-2 Financial statements: Statements of financial position 3 Statements of activities

GIFT ACCEPTANCE POLICY The mission of the xxxxx is to xxxx.

GIFT ACCEPTANCE POLICY The mission of the xxxxx is to xxxx. The xxxxxx is a nonprofit 501(c)(3) corporation (tax number xxxx) organized under the laws of the State of Washington. The xxxx encourages the

GIFT ACCEPTANCE POLICY The mission of the xxxxx is to xxxx. The xxxxxx is a nonprofit 501(c)(3) corporation (tax number xxxx) organized under the laws of the State of Washington. The xxxx encourages the

THE ART AND SCIENCE OF ESTIMATING BEQUESTS:

THE ART AND SCIENCE OF ESTIMATING BEQUESTS: GIVING USA AT FIFTY Craig C. Wruck with Melissa S. Brown IT IS THE MARK OF AN EDUCATED MIND TO REST SATISFIED WITH THE DEGREE OF PRECISION WHICH THE NATURE OF

THE ART AND SCIENCE OF ESTIMATING BEQUESTS: GIVING USA AT FIFTY Craig C. Wruck with Melissa S. Brown IT IS THE MARK OF AN EDUCATED MIND TO REST SATISFIED WITH THE DEGREE OF PRECISION WHICH THE NATURE OF

UNIVERSITY OF WISCONSIN OSHKOSH FOUNDATION GIFT ACCEPTANCE POLICY

UNIVERSITY OF WISCONSIN OSHKOSH FOUNDATION GIFT ACCEPTANCE POLICY Approved by the Foundation Board of Directors 10/23/08 PART ONE: GLOSSARY OF KEY TERMS Gift: A voluntary transfer of cash and kind, from

UNIVERSITY OF WISCONSIN OSHKOSH FOUNDATION GIFT ACCEPTANCE POLICY Approved by the Foundation Board of Directors 10/23/08 PART ONE: GLOSSARY OF KEY TERMS Gift: A voluntary transfer of cash and kind, from

Findings from the Minnesota CFO Survey

Findings from the Minnesota CFO Survey Kari Aanestad, development manager, Minnesota Council of Nonprofits; Kate Barr, president and C.E.O., Propel Nonprofits; and Jon Pratt, executive director, Minnesota

Findings from the Minnesota CFO Survey Kari Aanestad, development manager, Minnesota Council of Nonprofits; Kate Barr, president and C.E.O., Propel Nonprofits; and Jon Pratt, executive director, Minnesota

PRESENT LAW AND BACKGROUND RELATING TO THE FEDERAL TAX TREATMENT OF CHARITABLE CONTRIBUTIONS

PRESENT LAW AND BACKGROUND RELATING TO THE FEDERAL TAX TREATMENT OF CHARITABLE CONTRIBUTIONS Scheduled for a Public Hearing Before the SENATE COMMITTEE ON FINANCE on October 18, 2011 Prepared by the Staff

PRESENT LAW AND BACKGROUND RELATING TO THE FEDERAL TAX TREATMENT OF CHARITABLE CONTRIBUTIONS Scheduled for a Public Hearing Before the SENATE COMMITTEE ON FINANCE on October 18, 2011 Prepared by the Staff

APPROVED BY BOARD OF TRUSTEES 5/28/09 WITH AMENDMENTS

I. INTRODUCTION FUNDRAISING POLICY APPROVED BY BOARD OF TRUSTEES 5/28/09 WITH AMENDMENTS Vermont College of Fine Arts (VCFA) and its Board of Trustees recognize the importance of charitable giving to the

I. INTRODUCTION FUNDRAISING POLICY APPROVED BY BOARD OF TRUSTEES 5/28/09 WITH AMENDMENTS Vermont College of Fine Arts (VCFA) and its Board of Trustees recognize the importance of charitable giving to the

STANDARDS FOR CHARITABLE ACCOUNTABILITY. This policy was officially approved by the Board of Directors of SERES Global on October 30, 2016.

STANDARDS FOR CHARITABLE ACCOUNTABILITY This policy was officially approved by the Board of Directors of SERES Global on October 30, 2016. Preface SERES Global has committed to adhering to the Standards

STANDARDS FOR CHARITABLE ACCOUNTABILITY This policy was officially approved by the Board of Directors of SERES Global on October 30, 2016. Preface SERES Global has committed to adhering to the Standards

How Changes in Tax Rates Might Affect Itemized Charitable Deductions. The Center on Philanthropy at Indiana University March 2009

Executive Summary How Changes in Tax Rates Might Affect Itemized Charitable Deductions The Center on Philanthropy at Indiana University March 2009 President Obama s budget proposal for 2010 and beyond

Executive Summary How Changes in Tax Rates Might Affect Itemized Charitable Deductions The Center on Philanthropy at Indiana University March 2009 President Obama s budget proposal for 2010 and beyond

INTERFAITH FOOD MINISTRY OF NEVADA COUNTY FINANCIAL STATEMENTS DECEMBER 31, 2017

INTERFAITH FOOD MINISTRY OF NEVADA COUNTY FINANCIAL STATEMENTS FINANCIAL STATEMENTS TABLE OF CONTENTS Independent Auditor s Report...1 Financial Statements Statement of Financial Position...3 Statement

INTERFAITH FOOD MINISTRY OF NEVADA COUNTY FINANCIAL STATEMENTS FINANCIAL STATEMENTS TABLE OF CONTENTS Independent Auditor s Report...1 Financial Statements Statement of Financial Position...3 Statement

The Importance of the Not-for-Profit Sector in the International Community. Workability International

The Importance of the Not-for-Profit Sector in the International Community Workability International Annual Conference and General Meeting Arlington, Virginia, 7 September 2006 Paul Atkinson Senior Fellow

The Importance of the Not-for-Profit Sector in the International Community Workability International Annual Conference and General Meeting Arlington, Virginia, 7 September 2006 Paul Atkinson Senior Fellow

PNC CENTER FOR FINANCIAL INSIGHT

PNC CENTER FOR FINANCIAL INSIGHT Tax Reform and Philanthropy: Exploring Why and How You Give The new tax law will have sweeping implications on charitable giving, creating a greater urgency to examine

PNC CENTER FOR FINANCIAL INSIGHT Tax Reform and Philanthropy: Exploring Why and How You Give The new tax law will have sweeping implications on charitable giving, creating a greater urgency to examine

Non-Profit Executives Perceptions of the Vermont Non-Profit Sector. Prepared by Michael Moser The Center for Rural Studies University of Vermont

Non-Profit Executives Perceptions of the Vermont Non-Profit Sector Prepared by Michael Moser The Center for Rural Studies University of Vermont Table of Contents Methodology:... 1 Overall, do you feel

Non-Profit Executives Perceptions of the Vermont Non-Profit Sector Prepared by Michael Moser The Center for Rural Studies University of Vermont Table of Contents Methodology:... 1 Overall, do you feel

High Net Worth Philanthropy

THE 2016 U.S. TRUST STUDY OF High Net Worth Philanthropy CHARITABLE PRACTICES AND PREFERENCES OF WEALTHY HOUSEHOLDS OCTOBER 2016 A collaboration between U.S. Trust and the Indiana University Lilly Family

THE 2016 U.S. TRUST STUDY OF High Net Worth Philanthropy CHARITABLE PRACTICES AND PREFERENCES OF WEALTHY HOUSEHOLDS OCTOBER 2016 A collaboration between U.S. Trust and the Indiana University Lilly Family

Top Ten Charitable Trends Every Advisor Should Know in 2017

Top Ten Charitable Trends Every Advisor Should Know in 2017 Bryan Clontz, CFP, CAP President, Charitable Solutions, LLC www.charitablesolutionsllc.com (404) 375-5496 Agenda 1. Philanthropy Is Alive and

Top Ten Charitable Trends Every Advisor Should Know in 2017 Bryan Clontz, CFP, CAP President, Charitable Solutions, LLC www.charitablesolutionsllc.com (404) 375-5496 Agenda 1. Philanthropy Is Alive and

The UK Voluntary Sector: funding and resources

National Council for Voluntary Organisations The UK Voluntary Sector: funding and resources Findings from the Civil Society Almanac 2010 Twitter: #almanac2010 Feel free to share, but please cite NCVO as

National Council for Voluntary Organisations The UK Voluntary Sector: funding and resources Findings from the Civil Society Almanac 2010 Twitter: #almanac2010 Feel free to share, but please cite NCVO as

FRIENDS OF AULLWOOD, INC. FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT. For the Years Ended June 30, 2016 and 2015

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT For the Years Ended June 30, 2016 and 2015 C O N T E N T S INDEPENDENT AUDITORS' REPORT 3 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL POSITION 4 PAGE

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT For the Years Ended June 30, 2016 and 2015 C O N T E N T S INDEPENDENT AUDITORS' REPORT 3 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL POSITION 4 PAGE

Community Foundation of North Central Florida, Inc.

Community Foundation of North Central Florida, Inc. Financial Statements And Independent Auditors Reports CONTENTS Independent Auditors Report 1 Financial Statements: Statements of Financial Position 2

Community Foundation of North Central Florida, Inc. Financial Statements And Independent Auditors Reports CONTENTS Independent Auditors Report 1 Financial Statements: Statements of Financial Position 2

What Is the Definition of Charity, and Who Decides How to Define It?

What Is the Definition of Charity, and Who Decides How to Define It? April 15, 2013 Alexander Reid 202.739.5941 areid@morganlewis.com www.morganlewis.com 1 1. Charity Is Civil Society Every Charity Begins

What Is the Definition of Charity, and Who Decides How to Define It? April 15, 2013 Alexander Reid 202.739.5941 areid@morganlewis.com www.morganlewis.com 1 1. Charity Is Civil Society Every Charity Begins

DISCRETIONARY SCHOLARSHIP PASS-THROUGH FUND AGREEMENT BETWEEN LEGACY FOUNDATION, INC., AND ( DONORS )

") DISCRETIONARY SCHOLARSHIP PASS-THROUGH FUND AGREEMENT BETWEEN LEGACY FOUNDATION, INC., AND ( DONORS ) THIS AGREEMENT (the Agreement ) is made and entered into as of, 20, by and between Legacy Foundation,

DISCRETIONARY SCHOLARSHIP PASS-THROUGH FUND AGREEMENT BETWEEN LEGACY FOUNDATION, INC., AND ( DONORS ) THIS AGREEMENT (the Agreement ) is made and entered into as of, 20, by and between Legacy Foundation,

Impact Investing: At a Tipping Point?

Impact Investing: At a Tipping Point? This 2018 briefing provides data gathered from a survey of affluent and high-net-worth people who give to charity to understand their interest in, knowledge of and

Impact Investing: At a Tipping Point? This 2018 briefing provides data gathered from a survey of affluent and high-net-worth people who give to charity to understand their interest in, knowledge of and

THE COLUMBUS FOUNDATION COMBINED FINANCIAL STATEMENTS

COMBINED FINANCIAL STATEMENTS and 2015 John Gerlach & Company, LLP Certified Public Accountants To the Governing Committee/Board of Trustees of The Columbus Foundation Report on the Financial Statements

COMBINED FINANCIAL STATEMENTS and 2015 John Gerlach & Company, LLP Certified Public Accountants To the Governing Committee/Board of Trustees of The Columbus Foundation Report on the Financial Statements

Bequests and Donations for Library and Information Science Research

Bequests and Donations for Library and Information Science Research The ALIA Research Fund welcomes gifts and bequests to enable it to fund Library and Information Science research now and in the future,

Bequests and Donations for Library and Information Science Research The ALIA Research Fund welcomes gifts and bequests to enable it to fund Library and Information Science research now and in the future,

Making a Bequest. Professor Jayanti Bandyopadhyay

Making a Bequest WITH YOUR ESTATE PLAN, YOU CAN NAME SALEM STATE AS THE BENEFICIARY OF A PORTION OF YOUR ESTATE, OR ASSETS WITHIN YOUR ESTATE. For many alumni and friends, this is the surest way to make

Making a Bequest WITH YOUR ESTATE PLAN, YOU CAN NAME SALEM STATE AS THE BENEFICIARY OF A PORTION OF YOUR ESTATE, OR ASSETS WITHIN YOUR ESTATE. For many alumni and friends, this is the surest way to make

DISCRETIONARY SCHOLARSHIP ENDOWMENT FUND AGREEMENT BETWEEN STEUBEN COUNTY COMMUNITY FOUNDATION, INC., AND ( DONORS )

") DISCRETIONARY SCHOLARSHIP ENDOWMENT FUND AGREEMENT BETWEEN STEUBEN COUNTY COMMUNITY FOUNDATION, INC., AND ( DONORS ) THIS AGREEMENT (the Agreement ) is made and entered into as of, 20, by and between Steuben

DISCRETIONARY SCHOLARSHIP ENDOWMENT FUND AGREEMENT BETWEEN STEUBEN COUNTY COMMUNITY FOUNDATION, INC., AND ( DONORS ) THIS AGREEMENT (the Agreement ) is made and entered into as of, 20, by and between Steuben

INFORMATION STATEMENT POOLED INCOME TRUST FUND III

INFORMATION STATEMENT POOLED INCOME TRUST FUND III (As of June 30, 2017) THE LUTHERAN CHURCH MISSOURI SYNOD FOUNDATION 1333 SOUTH KIRKWOOD ROAD ST LOUIS, MO 63122-7295 (800) 325-7912 INTRODUCTION You are

INFORMATION STATEMENT POOLED INCOME TRUST FUND III (As of June 30, 2017) THE LUTHERAN CHURCH MISSOURI SYNOD FOUNDATION 1333 SOUTH KIRKWOOD ROAD ST LOUIS, MO 63122-7295 (800) 325-7912 INTRODUCTION You are

South Africa QUICK FACTS. Legal forms of philanthropic organizations included in the law: Association,Company Limited by Guarantee,Trust

South Africa Expert: Ricardo Wyngaard Institutional Affiliation: Ricardo Wyngaard Attorneys With contributions from staff at the Indiana University Lilly Family School of Philanthropy QUICK FACTS Legal

South Africa Expert: Ricardo Wyngaard Institutional Affiliation: Ricardo Wyngaard Attorneys With contributions from staff at the Indiana University Lilly Family School of Philanthropy QUICK FACTS Legal

Welcome to Foundation For The Carolinas. We look forward to making your giving easy, flexible and effective.

Welcome to Foundation For The Carolinas. We look forward to making your giving easy, flexible and effective. Please complete this Gift Fund Agreement form (this Agreement) to establish a Designated Fund

Welcome to Foundation For The Carolinas. We look forward to making your giving easy, flexible and effective. Please complete this Gift Fund Agreement form (this Agreement) to establish a Designated Fund

THE LADDER ALLIANCE, INC. Financial Statements. For the Year Ended December 31, 2011

Financial Statements For the Year Ended December 31, 2011 Charles O. Paul Certified Public Accountant 7408 Continental Trail P.O. Box 820402 N. Richland Hills, TX 76182 Fort Worth, TX 76182 (817) 498-0884

Financial Statements For the Year Ended December 31, 2011 Charles O. Paul Certified Public Accountant 7408 Continental Trail P.O. Box 820402 N. Richland Hills, TX 76182 Fort Worth, TX 76182 (817) 498-0884

DONOR ADVISED ENDOWMENT FUND AGREEMENT BETWEEN COMMUNITY FOUNDATION, INC., AND ( DONORS )

") DONOR ADVISED ENDOWMENT FUND AGREEMENT BETWEEN COMMUNITY FOUNDATION, INC., AND ( DONORS ) THIS AGREEMENT (the Agreement ) is made and entered into as of, 20, by and between Community Foundation, Inc. (the

DONOR ADVISED ENDOWMENT FUND AGREEMENT BETWEEN COMMUNITY FOUNDATION, INC., AND ( DONORS ) THIS AGREEMENT (the Agreement ) is made and entered into as of, 20, by and between Community Foundation, Inc. (the

INDEPENDENT ACCOUNTANT S REVIEW REPORT

MONICA J. STERN, CPA, PLLC CERTIFIED PUBLIC ACCOUNTANT 11225 NORTH 28TH DRIVE, SUITE A-100 PHOENIX, ARIZONA 85029 INDEPENDENT ACCOUNTANT S REVIEW REPORT To the Board of Directors Audrey's Angels Phoenix,

MONICA J. STERN, CPA, PLLC CERTIFIED PUBLIC ACCOUNTANT 11225 NORTH 28TH DRIVE, SUITE A-100 PHOENIX, ARIZONA 85029 INDEPENDENT ACCOUNTANT S REVIEW REPORT To the Board of Directors Audrey's Angels Phoenix,