Seminar on Tax Deducted at Source

|

|

|

- Geoffrey Barry Leonard

- 5 years ago

- Views:

Transcription

1 Seminar on Tax Deducted at Source - Payment to non-residents, issues and certifications TDS Sem inar at the Institute of Chartered Accountants of India at ICAI Tower Mum bai BKC by CA Shailendra Sharma 05 January 2019

2 Agenda Brief overview of the T DS provisions Withholding tax (WHT ) concept for nonresident Lifecycle of WHT provision under Section 195 Part A 2

3 Overview of TDS provisions - Chapter XVII, Collection & Recovery of Tax Deduction at Source Provisions of WHT Part A - General Part B - Forms of WHT / TDS Part BB Collection at Source Part C Advance Payment of Tax Part D Collection and recovery Part F & G Interest / fee chargeable in certain cases Advance collection of tax by WHT Section 192 to 196D Section 206C to 206CA Section 207 to 219 Section 220 to 232 Section 234A to 234E Direct payment by the taxpayer Procedures of TDS Section 197 to 206AA 3

4 WHT concept for nonresident Compliance procedures Prevent tax evasions Determination and analysis Protect tax revenue for government Applicability of the provisions Easy tax collection m echanism from the parties 4

5 Lifecycle of WHT provisions under Section 195 Scope of WHT Compliance default Trigger point for Section 195 Alternate remedy for payee Section 195 Character of payment Alternate remedy for payer Quantifying WHT 5

6 Scope of WHT (1/2) Operative provision of Section 195 of the Income-tax Act, 1961 (IT Act) Other sums [(1) Any person responsible for paying to a non-resident, not being a company, or to a foreign company, any interest [(not being interest referred to in section 194LB or section 194LC)] [or section 194LD] or any other sum chargeable under the provisions of this Act (not being income chargeable under the head Salaries ) shall, at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier, deduct income-tax thereon at the rates in force Other clauses of Section 195 Clauses Other provisions applicable for Section 195 of IT Act 195(2) Application by Payer to Tax Authorities (AO) to determine appropriate proportion of income chargeable to tax 195(3) Application by Payee to AO for NIL WHT certificate 195(4) Validity of certificate issued by AO 195(5) Powers of CBDT to issue Notifications 195(6) Furnishing of information relating to payments 195(7)* Authority of board to specify class of person or cases to make application under Section 195(2 ) 195A Income payable net of tax Grossing-up 6

7 Scope of WHT (2/2) Responsibility of WHT Payers covered Any person covered irrespective of their status - Includes person under Section 2(31) responsible for paying (including individuals and HUF) Payer itself in case of company, and the company includes principal officer It also includes all nonresidents having taxable presence in India or not as per Explanation 2 to Section 195 and Circular No. 726 dated 18 October 1995 or extra territorial jurisprudence Payees covered Nonresident Agent / POA holder of a nonresident in India? Resident but not ordinary resident RNOR? Payment made to a foreign branch of an Indian Company? Foreign companies constituting PoEM in India? 7

8 Trigger point for Section 195 (1/3) Applicability of Section 195 Sum chargeable to tax T iming of WHT All payments covered (exclusions specified), no threshold limit prescribed Any other sum chargeable Composite provision: Extends to whole of India and Definition Previous year and Charge of income-tax Scope of Total Income: Received or deemed to be received in India Accrue or arises or deemed to accrue or arise in India Residence in India Amount paid that bears character of income on Gross basis that may or may not represent income or profits, CBDT Circular No. 152 of 1974 Tax to be withheld at the time of payment / credit whichever is earlier Tax to be withheld even where no remittance is made, adjustment of dues WHT in cases where RBI approval is required If no income accrues to nonresident irrespective of accounting system incorporating liability, no WHT. However, on cash basis Payee must be identifiable / ascertainable Time of deduction, from payers point of view and sum chargeable to tax in India from payee point of view 8

9 Trigger point for Section 195 (2/3) Sum chargeable to tax..brief insight Where, payment made by resident to non-resident, was an amount not chargeable to tax in India, no tax is deductible at source as per CBDT Instruction No. 2/2014 Assessee liable to deduct TDS under Section 195 on payment made to non-resident even though payment is not made in cash but made in kind Payer obligated to WHT, even if the receipt is not taxable in the hands of the payee in the country of residence Sums not liable to tax in India on satisfaction of conditions, the principles are enunciated under Circular 23/1969 and 786/2000 (now withdrawn) like (P to P, nonresident operates outside India, contract signed outside India, title of goods passed outside India, payment is directly remitted abroad, etc.). Payments to: Agency commission payable to foreign agents; Off-shore supply of goods and equipments; Consideration paid for outright purchase of designs and drawings is not royalty; Applicability of withholding tax to shipping Company taxed under Section 172; and Does amount paid as penalty to the regulators chargeable to tax under Section 195? Any significant impact on withdrawal of the Circulars? 9

10 Trigger point for Section 195 (3/3) Specific exclusions for WHT under 195 Sections Particulars 115-O Tax on distributed profits of domestic companies 192 Income from Salaries 194LB Income by way of interest from infrastructure debt fund 194LBA Income from units of a business trust 194LBB Income from units of investment funds 194LBC Income of investment in securitization trust 194LC Income by way of interest from Indian company 194LD Income by way of interest on certain bonds and Government securities Other specific sections 196B Income from units 196C Income from FCCBs or GDRs of Indian companies 196D Income from FIIs now FPI except Capital Gains 10

11 Character of paym ent Determining the nature of payment Nature of Income (payee perspective) Business / Profession income Basis of tax Taxable if Business Connection in India or property or asset or source of income in India or transfer of a capital asset is situated in India Income chargeable under IT Act Tax Treaty Section 9(1)(i) Article 5, 7 and 14 Capital Gain Taxable if situs of shares/ property is in India Section 9(1)(i) Article 6 and 13 Dividends* Taxable if paid by an Indian company Section 9(1)(iv) (subject to DDT) Article 10 Interest Section 9(1)(v) Article 11 Royalties Fees for Technical Services (FTS) Taxable if sourced in India with certain exceptions Section 9(1)(vi) Section 9(1)(vii) Article 12 Salaries* Taxable if services are rendered in India Section 9(1)(ii) Article 15 Provisions of the IT Act or Tax Treaty r.w. MLI to the extent more beneficial to the taxpayer to apply 11

12 The OECD BEPS Action Plan initiative OECD BEPS Action Plan and India Action Plan 1 Digital Economy Action Plan 2 Hybrid mismatch & arrangements Action Plan 3 CFC rules Action Plan 4 Interest deduction Action Plan 5 Harmful tax practices Action Plan 6 Prevent tax treaty abuse Introduction of equalization levy on online advertisements Part of MLI arrangement however, India has not included in its MLI commitment Introduction of 'Place of Effective Management' Rules for tax residency Thin capitalisation regulations introduced under Transfer Pricing Regulations India not on the OECD harmful tax practices progress report list as update in May 2018 Included in the MLI arrangement. India has accepted the simplified LOB and PPT rules under the MLI document Action Plan 7 Avoiding artificial PE status Forming part of its provisional MLI commitment 12

13 The OECD BEPS Action Plan initiative OECD BEPS Action Plan and India Action Plan 8-10 Transfer Pricing recommendations Action Plan 11 Measuring and monitoring BEPS Action Plan 12 Disclosure rules Revised OECD commentary incorporates the recommendations in the Action Plans for intangibles, Risk and Capital, etc. No action taken yet India yet to notify regulations for disclosure of aggressive tax positions Action Plan 13 Countryby-Country Reporting Introduction of CbC reporting as per OECD norms Action Plan 14 Dispute resolution Forming part of its provisional MLI commitment Action Plan 15 - Multilateral instrument (MLI) India adopted and notified all its 93 DTAAs to be covered under of MLIs with express reservations 13

14 Snapshot of India s m ajor trading and investment partner countries Applicable MLI with India 85 Countries signed MLI (as on 21 Dec 2018) with India adopting Art.7 PPT + S-LOB; Art.12 DAPE; Art.13 Option A + anti-fragmentation Key India tax treaty partners not signed MLI yet existing treaties remain unaffected USA, Brazil, Thailand India tax treaty partners signed MLI existing treaties modified based on matching of MLI position of both countries Australia, Canada, Cyprus, France, Japan, Netherlands, UK, Luxembourg, Ireland, Italy, Russia, South Africa, Singapore, Malaysia Treaty partners signed MLI but not included India in their provisional lists existing treaties remain unaffected Mauritius, China, Germany Implementation of MLI Ratified Proposed to be ratified 17 Countries over all till 21 December 2018 Notable list of countries making effective are: Australia, Austria, France IoM, Israel, Japan, New Zealand, Sweden, UK Singapore, 14

15 Quantifying WHT Rates in force Rates in force as defined under Section 2(37A) of the IT Act Rates of income-tax specified in IT Act / Tax Treaty under Section 2(37A)(iii), beneficial rates to apply CBDT Circular No. 728 dated 30 October 1995 or 740 dated 17/04/1996 The exchange rate is applicable as per Rule 26 SBI TT buying rate, what about rate fluctuations? Rates prescribed under the tax treaty are inclusive of surcharge and education cess? Tax to be withheld under Section 195: Is on gross basis; and Withholding tax rate under Section 195 is final Interplay between proposed Equalization levy under Finance Act, 2016 and the Income-tax Act, 1961 Significance to obtain PAN while making the remittance to nonresidents Section 206AA, is a non-obstante provision that overrides the IT Act effective Detailed provision of Section 206AA and nuances discussed in the ensuing slides 15

16 Quantifying WHT Section 195A Income payable net of tax (Grossing-up) In the event of tax chargeable on any income is borne by the payer For the purposes of WHT under Section 195, income should be increased to such amount as would, after WHT thereon at the rates in force, be equal to the net amount payable to the payee Section 195A does not apply on notional income under Section 44BB Tax credit claimed by the payee to be restricted commercially Compliance under Section 203? Can refund be claimed if taxes are withheld erroneously under Section 195? Illustration of Section 195A: Particulars Amount in INR Amount payable to nonresident 100 Add: WHT (assumed to be 10% as per the tax treaty) grossed-up (10*100/90) Total income Less: WHT applicable at 10% Net amount payable to the nonresident (Recipient) 100 Friction between Section 206AA and 195A is Section 206AA applicable for grossing purposes and its legitimacy? 16

17 Alternate rem edy for the payer Application by payer to the AO under Section 195(2) and (4) Application by whom? The application to be made by the payer before the jurisdictional tax authority When to apply? When the payer is in doubt and believes that the whole of sum payable is not chargeable to tax in India Process Consequence Payer to approach tax authority to determine portion of income chargeable to tax Online system validated certificate prescribed AO may issue a certificate, determining the portion of income chargeable to tax The permission is valid for the period specified No specified time limit available to pass the order under Section 195(2) Order under Section 195(2) is: appealable after payment of tax amenable to revision under Section 263 Decision under Section 195(2) is inconclusive in determination of income in case of foreign entity 17

18 Alternate rem edy for the payee Application by payee to the AO under Section 195(3),(4) and (5) Application by payee to the AO under Section 197(1) Payee to make application in the prescribed for m (Form 15C or form 15D) for no WHT Prescribed conditions under Rule 29B: Application to be made by the payee under Section 197(1) for lower / no WHT online in the prescribed for m (Form 13) carries on business / profession in India for 5 year s Prescribed conditions under Rule 28AA: and has prescribed value of assets in India; Advisory f ortax payable on estimated or existing income; been regularly assessed to Income-tax; online Tax paid of last 3 previous years; and not defaulted in tax, interest, penalty, fine a or p a p n l y ication & Details of advance tax, TDS & TCS other sum payable; and system va lid A a O te to issue certificate indicating r ate / rates of tax d not been subjected to penalty under Section 271 c (1 e ) r tific O at w hichever is higher of the following: e pres R cribe Average rate deter mined on the basis of advance d under 195(3) and Average of average rates of tax paid in last 3 years AO may issue provisional Nil WHT certificate Certificate issued by the AO valid for the Financial tax; or Year mentioned therein or until cancelled Renewal after the expir y or within 3 months before 197 AO to issue certificate for lower / Nil WHT expiry of the certificate Certificate issued by AO can be prospective only Application after the payme nt of tax not entertained - Circular 774 dated 17 March 1999 Certificate issued by the AO valid for such period mentioned therein or until cancelled Application to be made before the payme nt / credit whichever is earlier 18

19 Agenda Part B Practice and Operational rules Issues, concerns and Illustrations Key takeaways Questions 19

20 Practice and Operational rules Provisions for CA Certificate Circular 10/2002 authorizes remittance of money through a CA Certificate CA Certificate required also for trade payments RBI Circular No. 32 dated 19 July 2007 Provision under Section 195(6) introduced by the Finance Act, 2008 for CA certificate Rule 37BB introduced by CBDT vide Notification 30/2009 dated 25/03/2009 : Forms 15CA and 15CB to remit payments to nonresidents and intimate the manner of disclosure: Form 15CA, prescribes information to be furnished online by the payer; and Form 15CB, prescribes format of CA Certificate to be obtained Taxpayer not absolved from penalty / prosecution if found that WHT was lower than required CA certificate merely acts as a guidance and is not a substitute to adjudication by the AO Procedure for remittance was amended from 01 October 2013, with significant change in the procedure, being more technological robust and detailed Specified list of 28 payments like outbound investments, gifts, etc. exempt from the procedures Notification issued on 16 December 2015 to amend Rule 37BB for new forms and compliances Remittance certificate issued by CA subject to penal provisions prescribed per default 20

21 Practice and Operational rules Rule 37BB amended effective 1 April 2016 with an aim to strike balance between burden of compliance and collection of information Individuals exempt to comply with Form 15CA and 15CB procedures if: Payment or aggregate of such payment does not exceed INR 5 lacs or Specified List; and Remittance does not require RBI approval under LRS and Current Account Transactions Specified list of remittances expanded to 33 for non applicability of Rule and additions include: 1. Advance payment against imports 2. Payment towards imports-settlement of invoice 3. Imports by diplomatic missions 4. Intermediary trade 5. Imports below INR 5 lacs (for use by ECD offices) Enhanced compliance of 15CA and 15CB information to be shared with Principal Director of Income-ta x (Systems) including filing of quarterly information on remittance by the AD in Form 15CC Revised Form Nos. 15CA and 15CB divided in 4 parts: Part A Part B Remittance does not exceed INR 5 lacs and amounts chargeable to tax Subset of Part A and lower WHT certificate obtained under Section 195(2)/195(3)/197 Form 15CA & 15CB Mirror image of CA Certificate Form 15CB where payments exceed INR 5 lacs Sum not chargeable to tax under the provisions of the Act Part C Part D 21

22 Practice and Operational rules Amended procedures for CA Certificate Sample declaration from the Payee Only taxable remittances to be reported in Form 15CA Select Form 15CA in Parts: Part A: Applicable to remittances chargeable to tax for small payments that does not exceed INR 5 lacs or aggregate of such payments during the Financial Part B: For any other payments chargeable to tax and lower / NIL WHT certificate is obtained Part C: Form 15CA after obtaining CA certificate in Form 15CB for sums chargeable to tax Part D: Information of any sum not chargeable to tax Form 15CA to be electronically uploaded on i ncome-tax website. Amended process through generation of digital signatures for every payment Specific declaration / i ndemnity to be obtained by the payer for taxes and interest if payment is liable for WHT Undertaking to be obtained from the payee << On the letterhead of Payee >> Date: TO WHOMSOEVER IT MAY CONCERN We, the Payee, hereby confirm as follows : 1. We are a Lim ited Company incorporated and regis tered in with Unique Entity Num ber. 2. We are a tax res ident of _ as per Article 4 of the tax treaty and the place of world as s es sment of our incom e is in 3. We do not have any Perm anent Es tablis hment / Fi xed place in India as defined under Article 5 of the Treaty. Als o we will not have a Permanent Es tablis hment / Fi xed place in India within the meaning of the Treaty for the financial year. 4. The am ount payable and its nature under the tax treaty 5. The am ount is to be rem itted to payee are the beneficiaries hereof. 6. In the event there is any incom e-tax dem and (include interes t etc) rais ed in India in res pect of this rem ittance we undertake to pay the demand forthwith and provide with all inform ation/docum ents that may be necessary for any proceedings before incom e tax/appellate authority in India. 7. Indem nity to protect from General Anti-Avoidance Rules For Payee 22

23 Practice and Operational rules Suggested method for CA Certificate Tax Residency Certificate (T RC) Steps Payment covered under Section 195 Verify factual documents Determine character IT Act Tax treaty Specific orders Follow compliance Action plan and approach Payment from resident or from non resident to nonresident Invoice, Contracts, Legal Status, obtain declaration, PAN, etc. Classification of payment, Business profits, Royalty, FTS, etc. Evaluate taxability under the Income-tax rates, Grossing-up, Section 206AA, Case law update No PE, TP analysis, beneficial owner, entity characterization, Article, LOB clause, Obtain TRC, MFN, Protocol to the DTAA, MLI, OECD BEPS Technical explanation to the DTAA, Model commentaries Verify specific orders received from tax authorities, 195(2), 195(3), etc. Complete the Form to comply with WHT deadlines for deposit TRC requirement for nonresidents to claim tax treaty benefits Also confirmed by Circular on Section 206AA Furnishing of TRC mandatory to avail tax treaty benefits: SC in the case of UOI v. A zadi Bachao Andolan [2003] 263 ITR 706 (SC) Circular 789 dated 13 April 2000 Shome Committee report on GAAR recommends that Circular 789 of 2000 should be retained Prescribed additional information to be furnished along with TRC CBDT clarified that the additional information prescribed may not be required if it already forms part of the TRC Notification No. 57/2013 dated 1/08/2013 [F.No.142/16/2013- TPL] revised the Rule 21AB 23

of the taxpayer 2. PAN of the taxpayer, if allotted 3. Nationality (in case of an i ndividual) or country or specified territory of i ncorporation or registration (in case of others) 4.")

24 Practice and Operational rules Prescribed Form 10F Sample T RC The additional details required to be furnished in Form 10F under Rule 21AB: 1. Status (Individual, Company, Firm, etc.) of the taxpayer 2. PAN of the taxpayer, if allotted 3. Nationality (in case of an i ndividual) or country or specified territory of i ncorporation or registration (in case of others) 4. Taxpayer's tax identification number or a unique number, as the case may be 5. Period for which the residential status, as mentioned in the TRC, is applicable and 6. Address of the taxpayer duri ng the period for which the certificate is applicable CBDT clarified that declaration may not be required if T RC contains above particulars 24

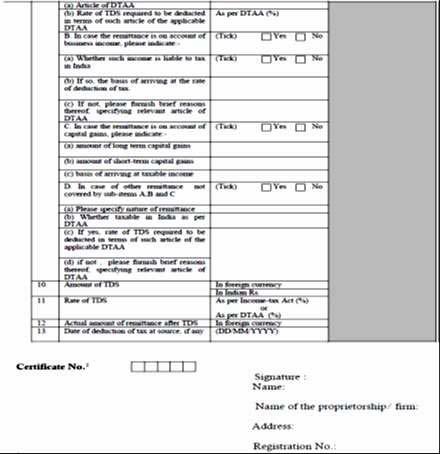

25 Practice and Operational rules Form 15CA Part A Form 15CA Part B 25

26 Practice and Operational rules Form 15CA - Part C Form 15CB 26

27 Practice and Operational rules Form 15CA - Part C Form 15CB 27

28 Practice and Operational rules Form 15CA - Part C Form 15CB 28

29 Practice and Operational rules Form 15CA Part D Form 15CC 29

30 Practice and Operational rules Remitter obtains digital CA certificate in Form 15CB in relevant Part after paying tax as determined for the remittance Electronically upload the remittance details as per Form 15CB issued in Form 15CA (using the Digital Signature) STEPS Single upload of Form 15CA online on the income-tax website Take hard print of the Form 15CA along with system generated acknowledgement number Registered user to login and navigate to e-file under Prepare and Submit Online Form 15CA using Digital Signature Submit in duplicate Form 15CA and Form 15CB along with Form A2 to the Authorized Dealer RBI / Bank makes remittance to the Payee 1. AD Bank to furnish electronic copy of (Form 15CA) and CA Certificate (Form 15CB) to the tax authorities 2. AD Bank to also file Form 15CC quarterly with the Principal Director General of Income-tax (Systems) Select appropriate Forms, Part A / Part B / Part C and Part D as applicable Fill the requisite details / information and submit the Form On submission transaction ID and acknowledgement is generated To view status / print the submitted form go to My Account View Form 15CA 30

31 Typical concerns of withholding tax for non-residents Salary payment of deputed employees Payment for software, use of / access to database Reimbursement of actual expenses Third party cost sharing reimbursement to parent Online advertisement or related services Payment towards significant economic presence Tax deduction for transfer of immovable by NRI Payment for export or supply of equipment's / goods Marketing survey and testing charges 31

32 Illustration 1 Reimbursement of expense Applicable WHT rate for F Co in absence of PAN F Co $ Reim bursement of Expens e Offs hore India Section 206AA provides for WHT at the higher of the following rates, namely: Specified rate in the relevant provisions of the IT Act; or Rate / rates in force; or 20% F Co has a valid TRC Expens es incurred for I Co I Co What should be the WHT rate under Section 195? 32

33 Illustration 2 Export Commission Applicable WHT rate for F Co in absence of PAN F Co Implications when commission income paid to an associate enterprise? If payment is made to Cyprus? Agency Services 100% Cyprus India $ Com m ission I Co 33

34 Illustration 3 Group Restructuring Applicable WHT provisions for F Co case of share sale F Co Gains arising on transfer of shares are exempt under the applicable tax treaty Trans fer of Shares 100% Offs hore India Is a PAN required? Is withholding tax provisions applicable? Does F Co has to file a return of income in India? I Co 34

35 Key takeaways and safeguards 1. Ignorance of rules may lead to undesirable litigation and cost, thus impacting business focus 2. Other business functions should also support on the foreign payments made by the clients 3. Preliminary assessment of transfer pricing would be essential for related party transactions 4. Cumbersome compliance process for non-resident payers, noncompliance result in penalty 5. Safeguard to the taxpayer by taking an opinion and suggest paper trail if Part D is opted 6. Ensure patience and trust in Indian tax judiciary, accurate interpretation will lead to success 35

36 WHERE? HOW? WHAT? QUESTIONS? WHY? WHEN? WHO? WHAT IF? 36

37 Thank you! Your feedback is valuable and will help me improvise my skill-sets Disclaimer note: The views / opinions explicit or implicit expressed during the presentation of the tax technical paper, is exclusively that of the author being personal in nature, based on his professional practical experience. The content of the tax technical paper are general in nature and does not reflect / resemble any client advice delivered directly / indirectly. The participant relying on the tax technical paper is e xpected to consult his / her tax advisors before implementing the ideas suggested during the presentation. The presenter is in no case liable for any damages incurred by relying on the ideas implemented without adequate consultation with the competent tax professional on the instant facts and legal arguments 37

An overview of Section 195 and foreign payments of the Income-tax Act at The Institute of Chartered Accountants of India, Seminar of TDS

An overview of Section 195 and foreign payments of the Income-tax Act at The Institute of Chartered Accountants of India, Seminar of TDS by CA Shailendra Sharma 07 April 2018 Agenda Brief overview of the

An overview of Section 195 and foreign payments of the Income-tax Act at The Institute of Chartered Accountants of India, Seminar of TDS by CA Shailendra Sharma 07 April 2018 Agenda Brief overview of the

An overview and practice aspects of withholding tax under Section 195 of the Income-tax Act Seminar on TDS, ICAI Western Region Mumbai

An overview and practice aspects of withholding tax under Section 195 of the Income-tax Act Seminar on TDS, ICAI Western Region Mumbai CA Shailendra S. Sharma 02 April 2016 Agenda Brief overview of TDS

An overview and practice aspects of withholding tax under Section 195 of the Income-tax Act Seminar on TDS, ICAI Western Region Mumbai CA Shailendra S. Sharma 02 April 2016 Agenda Brief overview of TDS

TDS provisions for payment to nonresident under Section 195 of the Income-tax Act

TDS provisions for payment to nonresident under Section 195 of the Income-tax Act Seminar on issues in TDS ICAI, Mumbai CA Shailendra S. Sharma 23 January 2016 Agenda Brief overview of TDS provisions Concept

TDS provisions for payment to nonresident under Section 195 of the Income-tax Act Seminar on issues in TDS ICAI, Mumbai CA Shailendra S. Sharma 23 January 2016 Agenda Brief overview of TDS provisions Concept

TDS under section 195 of the Income-tax Act. CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC

TDS under section 195 of the Income-tax Act CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC Overview of section 195 Overview of section 195 195(1) Any person paying to non-resident

TDS under section 195 of the Income-tax Act CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC Overview of section 195 Overview of section 195 195(1) Any person paying to non-resident

Tax Withholding Section 195 and CA certification

Tax Withholding Section 195 and CA certification October 1, 2011 Bijal Desai Presentation Outline Non-resident payments Withholding tax Lower or NIL withholding of tax CA Certification Consequences of

Tax Withholding Section 195 and CA certification October 1, 2011 Bijal Desai Presentation Outline Non-resident payments Withholding tax Lower or NIL withholding of tax CA Certification Consequences of

The Institute of Chartered Accountants Of India

The Institute of Chartered Accountants Of India 15CA- 15CB Filing, Issues & Precautions Natwar G. Thakrar Saturday, 30 th December, 2017 Presentation Outline Brief Analysis of section 195 Determination

The Institute of Chartered Accountants Of India 15CA- 15CB Filing, Issues & Precautions Natwar G. Thakrar Saturday, 30 th December, 2017 Presentation Outline Brief Analysis of section 195 Determination

Withholding tax u/s 195 and filing of Form 15CA/ 15CB - Key issues April 2017

Withholding tax u/s 195 and filing of Form 15CA/ 15CB - Key issues April 2017 Section 195 Overview Section Provisions 195(1) Scope and conditions for applicability 195(2) Application by the Payer for determination

Withholding tax u/s 195 and filing of Form 15CA/ 15CB - Key issues April 2017 Section 195 Overview Section Provisions 195(1) Scope and conditions for applicability 195(2) Application by the Payer for determination

SOME RELEVANT TREATY ISSUES

SOME RELEVANT TREATY ISSUES Rahul Charkha August 29, 2018 CONTENT Sr. No. Topic 1 Glossary 2 Most Favoured Nation Principle 3 Tax Credit 4 Mutual Agreement Procedures 5 Annexure - 1 6 Our Team GLOSSARY

SOME RELEVANT TREATY ISSUES Rahul Charkha August 29, 2018 CONTENT Sr. No. Topic 1 Glossary 2 Most Favoured Nation Principle 3 Tax Credit 4 Mutual Agreement Procedures 5 Annexure - 1 6 Our Team GLOSSARY

TDS on Payments to Non-residents under section 195 Law and Procedures

Study Course on International Taxation for Beginners Organised by - Western India Regional Council of the Institute Chartered Accountants of India TDS on Payments to Non-residents under section 195 Law

Study Course on International Taxation for Beginners Organised by - Western India Regional Council of the Institute Chartered Accountants of India TDS on Payments to Non-residents under section 195 Law

International Taxation

International Taxation Presentation by: CA Amit Maheshwari Partner, Ashok Maheshwary & Associates Chartered Accountants, Gurgaon (Independent Member of the Leading Edge Alliance) E-Mail : info@akmglobal.com

International Taxation Presentation by: CA Amit Maheshwari Partner, Ashok Maheshwary & Associates Chartered Accountants, Gurgaon (Independent Member of the Leading Edge Alliance) E-Mail : info@akmglobal.com

OECD Model Tax Convention on Income and Capital An overview. CA Vishal Palwe, 3 July 2015

OECD Model Tax Convention on Income and Capital An overview CA Vishal Palwe, 3 July 2015 1 Contents Overview of double taxation 3 Basics of tax treaty 6 Domestic law and tax treaty 11 Key provisions of

OECD Model Tax Convention on Income and Capital An overview CA Vishal Palwe, 3 July 2015 1 Contents Overview of double taxation 3 Basics of tax treaty 6 Domestic law and tax treaty 11 Key provisions of

Overview of Section December, WIRC of ICAI

Overview of Section 195 30 December, 2017 WIRC of ICAI 1 Payments to Non-resident Payments to Non-residents Key implications FEMA law and compliances GST on RCM basis Banking compliances and documentation

Overview of Section 195 30 December, 2017 WIRC of ICAI 1 Payments to Non-resident Payments to Non-residents Key implications FEMA law and compliances GST on RCM basis Banking compliances and documentation

Overview of Taxation of Non Residents

Overview of Taxation of Non Residents CTC Vispi T. Patel Vispi T. Patel & Associates 13 th December, 2013 Scheme of Taxation for Non Residents under Income-tax Act, 1961 Section 4 (Charge of Income-tax)

Overview of Taxation of Non Residents CTC Vispi T. Patel Vispi T. Patel & Associates 13 th December, 2013 Scheme of Taxation for Non Residents under Income-tax Act, 1961 Section 4 (Charge of Income-tax)

SECTION 195 OF THE INCOME TAX ACT,1961 PROVISIONS, AMENDMENTS AND CONTROVERSIES

1 WIRC Pune Camp CPE Study Circle January 19, 2013 SECTION 195 OF THE INCOME TAX ACT,1961 PROVISIONS, AMENDMENTS AND CONTROVERSIES CA JIGER SAIYA jigersaiya@mzsk.in Contents Introduction Recent Amendments

1 WIRC Pune Camp CPE Study Circle January 19, 2013 SECTION 195 OF THE INCOME TAX ACT,1961 PROVISIONS, AMENDMENTS AND CONTROVERSIES CA JIGER SAIYA jigersaiya@mzsk.in Contents Introduction Recent Amendments

Multilateral Instruments - Indian Perspective

Multilateral Instruments - Indian Perspective CA Hiten Sutar 15 December 2018 KPMG.com/in 1 Agenda Setting the Context Introduction to MLI India s Positions on MLI Denial of Treaty Benefits Artificial

Multilateral Instruments - Indian Perspective CA Hiten Sutar 15 December 2018 KPMG.com/in 1 Agenda Setting the Context Introduction to MLI India s Positions on MLI Denial of Treaty Benefits Artificial

SIRC of ICAI CPE Study Circle Meeting Wednesday Issues!!! CA. V Sathyanarayanan, Kochi

SIRC of ICAI CPE Study Circle Meeting Wednesday 20.01.2016 Issues!!! CA. V Sathyanarayanan, Kochi Foreign Remittance Whether to liable to tax under The Income Tax Act No Yes No TDS No Whether liable to

SIRC of ICAI CPE Study Circle Meeting Wednesday 20.01.2016 Issues!!! CA. V Sathyanarayanan, Kochi Foreign Remittance Whether to liable to tax under The Income Tax Act No Yes No TDS No Whether liable to

TDS on Payments to Non Residents Law and Procedures

TDS on Payments to Non Residents Law and Procedures Regional Conference of CAs on GST & Income-tax Rajkot Branch of WIRC, Institute of Chartered Accountants of India 16 th December 2017 Rutvik Sanghvi

TDS on Payments to Non Residents Law and Procedures Regional Conference of CAs on GST & Income-tax Rajkot Branch of WIRC, Institute of Chartered Accountants of India 16 th December 2017 Rutvik Sanghvi

INDIA IMPORTANT CORPORATE TAX UPDATES

INDIA IMPORTANT CORPORATE TAX UPDATES Introduction Reducing tax litigation has been a key focus area for the Modi government. Several initiatives have been taken by the Central Board of Direct Taxes (the

INDIA IMPORTANT CORPORATE TAX UPDATES Introduction Reducing tax litigation has been a key focus area for the Modi government. Several initiatives have been taken by the Central Board of Direct Taxes (the

KPMG Japan Tax Newsletter

KPMG Japan Tax Newsletter 28 September 2018 MULTILATERAL INSTRUMENT (MLI) I. Outline of the MLI 1. Background of Development of the MLI and History of Signature/Entry into Force.. 2 2. Features of the

KPMG Japan Tax Newsletter 28 September 2018 MULTILATERAL INSTRUMENT (MLI) I. Outline of the MLI 1. Background of Development of the MLI and History of Signature/Entry into Force.. 2 2. Features of the

Foreign Tax Credit. June 2016

Foreign Tax Credit June 2016 Table of content 1 Introduction 2 Types of Relief 3 Exemption Method 4 Credit Method 5 Double non-taxation 6 Excess FTC 7 Documentation 8 Cases where FTC not available 9 Case

Foreign Tax Credit June 2016 Table of content 1 Introduction 2 Types of Relief 3 Exemption Method 4 Credit Method 5 Double non-taxation 6 Excess FTC 7 Documentation 8 Cases where FTC not available 9 Case

IN THE SUPREME COURT OF INDIA CIVIL APPELLATE JURISDICTION CIVIL APPEAL NOs OF 2010 (Arising out of SLP(C) No of 2009)

No of 2009)") IN THE SUPREME COURT OF INDIA CIVIL APPELLATE JURISDICTION CIVIL APPEAL NOs.7541-7542 OF 2010 (Arising out of SLP(C) No. 34306-34307 of 2009) GE India Technology Centre Private Ltd.. Appellant(s) Versus

IN THE SUPREME COURT OF INDIA CIVIL APPELLATE JURISDICTION CIVIL APPEAL NOs.7541-7542 OF 2010 (Arising out of SLP(C) No. 34306-34307 of 2009) GE India Technology Centre Private Ltd.. Appellant(s) Versus

TDS on Payments to Non-Residents u/s Laws & Procedures. CA Zeel Gala 13 December 2018

TDS on Payments to Non-Residents u/s 195 - Laws & Procedures CA Zeel Gala 13 December 2018 Payments to Non-resident Payments to Nonresidents Key implications FEMA law and compliances GST on RCM basis Banking

TDS on Payments to Non-Residents u/s 195 - Laws & Procedures CA Zeel Gala 13 December 2018 Payments to Non-resident Payments to Nonresidents Key implications FEMA law and compliances GST on RCM basis Banking

As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017.

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

Withholding taxes on cross-border payments A conundrum? Ernst & Young Webcast Held on 10 February 5.00 p.m. (IST)

") Withholding taxes on cross-border payments A conundrum? Ernst & Young Webcast Held on 10 February 2010 @ 5.00 p.m. (IST) Contents Background Key issues/ challenges Karnataka High Court ruling Technical

Withholding taxes on cross-border payments A conundrum? Ernst & Young Webcast Held on 10 February 2010 @ 5.00 p.m. (IST) Contents Background Key issues/ challenges Karnataka High Court ruling Technical

Payment of Export commission to Non-Resident Agent :-

Common Disputes:- Payment of Export commission to Non-Resident Agent :- Relevant Bare Act, Rules & Circulars:- Other Sums 195. [(1) Any person responsible for paying to a non-resident, not being a company,

Common Disputes:- Payment of Export commission to Non-Resident Agent :- Relevant Bare Act, Rules & Circulars:- Other Sums 195. [(1) Any person responsible for paying to a non-resident, not being a company,

BEPS - Current Status of Implementation in EU Countries. Prof. Guglielmo Maisto 1 March 2019

BEPS - Current Status of Implementation in EU Countries Prof. Guglielmo Maisto 1 March 2019 1 Pillar I COHERENCE Action 2 Neutralizing Hybrid Mismatch Arrangements Action 3 CFC Rules Action 4 Interest

BEPS - Current Status of Implementation in EU Countries Prof. Guglielmo Maisto 1 March 2019 1 Pillar I COHERENCE Action 2 Neutralizing Hybrid Mismatch Arrangements Action 3 CFC Rules Action 4 Interest

Law & Procedure for foreign remittances

Law & Procedure for foreign remittances Himanshu Parekh 13 January 2017 KPMG.com/in Overview of Section 195 Section Provision 195(1) Scope and conditions for applicability 195(2) Application by the Payer

Law & Procedure for foreign remittances Himanshu Parekh 13 January 2017 KPMG.com/in Overview of Section 195 Section Provision 195(1) Scope and conditions for applicability 195(2) Application by the Payer

By CA ANIKET S. TALATI. M.COM., FCA., Regional Council Member- WIRC of ICAI

By CA ANIKET S. TALATI M.COM., FCA., Regional Council Member- WIRC of ICAI Genesis Government of India constituted a high power committee of experts under the chairmanship of Sri Justice K.N. Wanchoo,

By CA ANIKET S. TALATI M.COM., FCA., Regional Council Member- WIRC of ICAI Genesis Government of India constituted a high power committee of experts under the chairmanship of Sri Justice K.N. Wanchoo,

International Taxation perspectives and recent developments. Hitesh D. Gajaria 20 August 2016 WIRC DTAA Refresher Course

International Taxation perspectives and recent developments Hitesh D. Gajaria 20 August 2016 WIRC DTAA Refresher Course Table of Contents 1 Tax Treaty - Application and Issues 2 International Tax Planning

International Taxation perspectives and recent developments Hitesh D. Gajaria 20 August 2016 WIRC DTAA Refresher Course Table of Contents 1 Tax Treaty - Application and Issues 2 International Tax Planning

Finance Bill, 2015 Direct Tax Highlights

Finance Bill, 2015 Direct Tax Highlights Bansi S. Mehta & Co. All the following amendment are made effective from Assessment Years 2016-17, unless specifically mentioned otherwise. I - Residential Status,

Finance Bill, 2015 Direct Tax Highlights Bansi S. Mehta & Co. All the following amendment are made effective from Assessment Years 2016-17, unless specifically mentioned otherwise. I - Residential Status,

Simplifying BEPS Action Plan

Simplifying BEPS Action Plan BEPS and GST Conference 2 nd September 2016 1 About the pic: 16 Nov 2015, In Antalya, Leaders expressed support for the package of measures developed under the G-20/OECD Base

Simplifying BEPS Action Plan BEPS and GST Conference 2 nd September 2016 1 About the pic: 16 Nov 2015, In Antalya, Leaders expressed support for the package of measures developed under the G-20/OECD Base

CPE STUDY CIRCLE MEETING FOREIGN TAX CREDIT MAY 2016

CPE STUDY CIRCLE MEETING FOREIGN TAX CREDIT MAY 2016 INTRODUCTION Objectives of a tax treaty Elimination of double taxation Clarification of fiscal situation of tax payers Certainty on nature of income

CPE STUDY CIRCLE MEETING FOREIGN TAX CREDIT MAY 2016 INTRODUCTION Objectives of a tax treaty Elimination of double taxation Clarification of fiscal situation of tax payers Certainty on nature of income

TDS on Non Residents. CA. Rajesh Patil

TDS on Non Residents. CA. Rajesh Patil Western India Regional Council 12 February 2011 Contents (1) Introduction Analysis of section 195 Payers covered Payees covered Payments covered Point of Tax Withholding

TDS on Non Residents. CA. Rajesh Patil Western India Regional Council 12 February 2011 Contents (1) Introduction Analysis of section 195 Payers covered Payees covered Payments covered Point of Tax Withholding

Foreign Collaboration

CHAPTER 17 Foreign Collaboration Some Key Points (a) The tax liability of a foreign collaborator and the Indian counter part is dependent on their residential status and the applicable provisions of DTAA,

CHAPTER 17 Foreign Collaboration Some Key Points (a) The tax liability of a foreign collaborator and the Indian counter part is dependent on their residential status and the applicable provisions of DTAA,

MULTILATERAL INSTRUMENT

MULTILATERAL INSTRUMENT View from (Dutch) tax practice ACTL seminar / 13 February 2017 Bartjan Zoetmulder / tax partner chair Dutch investment climate team NOB 1 Introduction 2 BEPS implementation phase

MULTILATERAL INSTRUMENT View from (Dutch) tax practice ACTL seminar / 13 February 2017 Bartjan Zoetmulder / tax partner chair Dutch investment climate team NOB 1 Introduction 2 BEPS implementation phase

International Taxation Recent Developments in India

International Taxation Recent Developments in India April 2017 B. D. Jokhakar & Co., www.bdjokhakar.com Table of Contents Sr. No. Topic Page No. 1. Introduction 3 2. Amendment to Tax Treaties 4 3. Base

International Taxation Recent Developments in India April 2017 B. D. Jokhakar & Co., www.bdjokhakar.com Table of Contents Sr. No. Topic Page No. 1. Introduction 3 2. Amendment to Tax Treaties 4 3. Base

Transfer Pricing Forum

Transfer Pricing Forum Transfer Pricing for the International Practitioner Reproduced with permission from Transfer Pricing Forum, 09 TPTPFU 36, 7/1/18. Copyright 2018 by The Bureau of National Affairs,

Transfer Pricing Forum Transfer Pricing for the International Practitioner Reproduced with permission from Transfer Pricing Forum, 09 TPTPFU 36, 7/1/18. Copyright 2018 by The Bureau of National Affairs,

TAX RECKONER

TAX RECKONER 2018-19 The rates are applicable for the Financial Year 2018-19 (AY 2019-20) and subject to enactment of the Finance Bill, 2018 Note: The tax rate card will be re-visited post enactment of

TAX RECKONER 2018-19 The rates are applicable for the Financial Year 2018-19 (AY 2019-20) and subject to enactment of the Finance Bill, 2018 Note: The tax rate card will be re-visited post enactment of

Asia-Pacific update. TEI International Tax Planning Houston. 21 February 2017

Asia-Pacific update TEI International Tax Planning Houston 21 February 2017 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited,

Asia-Pacific update TEI International Tax Planning Houston 21 February 2017 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited,

Decisions and updates

Article 10, 11 and 13 - Recent Decisions and updates Seminar on Recent Updates in International Tax WIRC ICAI 23 February 2013, Mumbai CA. Shabbir Motorwala 1 Contents Overview Recent updates Recent decisions

Article 10, 11 and 13 - Recent Decisions and updates Seminar on Recent Updates in International Tax WIRC ICAI 23 February 2013, Mumbai CA. Shabbir Motorwala 1 Contents Overview Recent updates Recent decisions

TAX AUDIT POINTS TO BE CONSIDERED

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

BEPS Multilateral Instrument (MLI), India s Corresponding Positions, Implementation (GAAR)

, India s Corresponding Positions, Implementation (GAAR)") BEPS Multilateral Instrument (MLI), India s Corresponding Positions, Implementation (GAAR) Dr. Parthasarathi Shome Chairman International Tax Research and Analysis Foundation (ITRAF) www.itraf.org Visiting

BEPS Multilateral Instrument (MLI), India s Corresponding Positions, Implementation (GAAR) Dr. Parthasarathi Shome Chairman International Tax Research and Analysis Foundation (ITRAF) www.itraf.org Visiting

Key changes / amendments to take effect from June 1, 2016

1. Equalisation Levy Section 10 Key changes / amendments to take effect from June 1, 2016 Under section 10, a new Clause 50 has been inserted that provides for exemption of income from specified services

1. Equalisation Levy Section 10 Key changes / amendments to take effect from June 1, 2016 Under section 10, a new Clause 50 has been inserted that provides for exemption of income from specified services

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE COMPILED BY: CA.ARUN GUPTA ca.arungupta77@gmail.com A. Rates of Taxes: 1. It is proposed to make the following changes in tax rates: In case of Resident

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE COMPILED BY: CA.ARUN GUPTA ca.arungupta77@gmail.com A. Rates of Taxes: 1. It is proposed to make the following changes in tax rates: In case of Resident

Latest Changes in AIR Reporting norms, Form 15CA-CB and E-initiative(s) of the Income Tax Department

of the Income Tax Department") Latest Changes in AIR Reporting norms, Form 15CA-CB and E-initiative(s) of the Income Tax Department Suresh Wadhwa, LL.B., FCA Time: 19:30 Hrs to 21:30 Hrs Monday, February 15, 2016 at East Delhi C.A.

Latest Changes in AIR Reporting norms, Form 15CA-CB and E-initiative(s) of the Income Tax Department Suresh Wadhwa, LL.B., FCA Time: 19:30 Hrs to 21:30 Hrs Monday, February 15, 2016 at East Delhi C.A.

Controlled Foreign Corporation

Controlled Foreign Corporation Certificate Course on International Taxation, Chennai Arpit Jain Director International Tax Background Spread of CFC legislation across the world in last 30-40 years US-perhaps

Controlled Foreign Corporation Certificate Course on International Taxation, Chennai Arpit Jain Director International Tax Background Spread of CFC legislation across the world in last 30-40 years US-perhaps

15 CA &15 CB. Presented by: CA Sheetal Mankani Partner R. C. Jain & Associates LLP. In association with: Rajeev Tahalramani

15 CA &15 CB Presented by: CA Sheetal Mankani Partner R. C. Jain & Associates LLP In association with: Rajeev Tahalramani What is Form 15CA? Form 15CA is a Declaration by Remitter and is used as a tool

15 CA &15 CB Presented by: CA Sheetal Mankani Partner R. C. Jain & Associates LLP In association with: Rajeev Tahalramani What is Form 15CA? Form 15CA is a Declaration by Remitter and is used as a tool

The Multilateral Convention and BEPS Investment in and from India

www.pwc.in The Multilateral Convention and BEPS Investment in and from India October 2017 Contents Glossary... 3 Introduction... 4 Modalities of the MLI... 5 Application of the MLI... 8 India s perspective

www.pwc.in The Multilateral Convention and BEPS Investment in and from India October 2017 Contents Glossary... 3 Introduction... 4 Modalities of the MLI... 5 Application of the MLI... 8 India s perspective

INDIA BUDGET 2016 SUMMARY OF IMPORTANT PROPOSED AMENDMENTS.

INDIA BUDGET 2016 SUMMARY OF IMPORTANT PROPOSED AMENDMENTS. Income Tax Amendment - Personal SN Description Impact Author remarks 1 For Income more than one crore surcharge Negative More tax from super

INDIA BUDGET 2016 SUMMARY OF IMPORTANT PROPOSED AMENDMENTS. Income Tax Amendment - Personal SN Description Impact Author remarks 1 For Income more than one crore surcharge Negative More tax from super

India signs the Multilateral Convention Provisional List of reservations and notifications released

Direct Tax Alert 8 June 2017 India signs the Multilateral Convention Provisional List of reservations and notifications released 68 countries, including India and several of its important treaty partners,

Direct Tax Alert 8 June 2017 India signs the Multilateral Convention Provisional List of reservations and notifications released 68 countries, including India and several of its important treaty partners,

Applicability of GAAR Fundamental requirements. Index

Applicability of GAAR Fundamental requirements Naresh Ajwani Chartered Accountant Index Sr. No. Particulars Page No. 1. Preamble: 2. When can GAAR apply? 3. Onus on whom? 4. Impermissible Avoidance Arrangement

Applicability of GAAR Fundamental requirements Naresh Ajwani Chartered Accountant Index Sr. No. Particulars Page No. 1. Preamble: 2. When can GAAR apply? 3. Onus on whom? 4. Impermissible Avoidance Arrangement

Tax-treatment and TDS, in respect of remuneration payable to an employee of an Indian Company, located abroad

Tax-treatment and TDS, in respect of remuneration payable to an employee of an Indian Company, located abroad 1 Tax-treatment and TDS, in respect of salary, bonus and incentive, receivable by the CEO of

Tax-treatment and TDS, in respect of remuneration payable to an employee of an Indian Company, located abroad 1 Tax-treatment and TDS, in respect of salary, bonus and incentive, receivable by the CEO of

DOUBLE TAX TREATIES: COMPANIES ICAZ TAX SEMINAR. Presented by M. NGORIMA 22 February 2018

DOUBLE TAX TREATIES: COMPANIES ICAZ TAX SEMINAR Presented by M. NGORIMA 22 February 2018 DISCUSSION POINTS 1. What are double tax treaties? 2. Model Treaties 3. OECD Model Treaty Basic template 4. Model

DOUBLE TAX TREATIES: COMPANIES ICAZ TAX SEMINAR Presented by M. NGORIMA 22 February 2018 DISCUSSION POINTS 1. What are double tax treaties? 2. Model Treaties 3. OECD Model Treaty Basic template 4. Model

BEPS Impact on Private Equity

BEPS Impact on Private Equity BEPS impact on private equityspace An Indian perspective In this age of increasing focus on bottomlines, it is indeed tempting for a global tax director of a multinational

BEPS Impact on Private Equity BEPS impact on private equityspace An Indian perspective In this age of increasing focus on bottomlines, it is indeed tempting for a global tax director of a multinational

Vinodh & Muthu Chartered Accountants. Newsletter MAY 2016

Vinodh & Muthu Chartered Accountants Newsletter MAY 2016 2 Dear Readers, Welcome to our newsletter. VMCA brings you the significant developments in taxation during the month of May 2016. We hope this edition

Vinodh & Muthu Chartered Accountants Newsletter MAY 2016 2 Dear Readers, Welcome to our newsletter. VMCA brings you the significant developments in taxation during the month of May 2016. We hope this edition

Seamless tax solutions from territory to territory

Seamless tax solutions from territory to territory www.rsmindia.in Newsflash: The OECD s Multilateral Instrument and its Potential Impact on n Tax Treaties - June 2017 1.0 Background On 7 June 2017, became

Seamless tax solutions from territory to territory www.rsmindia.in Newsflash: The OECD s Multilateral Instrument and its Potential Impact on n Tax Treaties - June 2017 1.0 Background On 7 June 2017, became

Bombay Chartered Accountants Society DTAA Course Multilateral Instrument (MLI) Note for discussion 20 th January Contents

Note for discussion 20 th January Contents") Bombay Chartered Accountants Society DTAA Course Multilateral Instrument (MLI) Note for discussion 20 th January 2018 Naresh Ajwani Chartered Accountant Para No. Contents Particulars Page No. A. Operation

Bombay Chartered Accountants Society DTAA Course Multilateral Instrument (MLI) Note for discussion 20 th January 2018 Naresh Ajwani Chartered Accountant Para No. Contents Particulars Page No. A. Operation

The Chamber of Tax Consultants

The Chamber of Tax Consultants Workshop on Taxation of Foreign Remittances Students, Directors fees, Other income, Artistes & Sportsperson. 14 th December, 2013 Naresh Ajwani Rashmin Sanghvi & Associates

The Chamber of Tax Consultants Workshop on Taxation of Foreign Remittances Students, Directors fees, Other income, Artistes & Sportsperson. 14 th December, 2013 Naresh Ajwani Rashmin Sanghvi & Associates

The Institute of Chartered Accountants of India Ahmedabad Branch

The Institute of Chartered Accountants of India Ahmedabad Branch Elimination of Double Taxation 9 th August, 2008 Naresh Ajwani Partner Rashmin Sanghvi & Associates Chartered Accountants Topics Involved

The Institute of Chartered Accountants of India Ahmedabad Branch Elimination of Double Taxation 9 th August, 2008 Naresh Ajwani Partner Rashmin Sanghvi & Associates Chartered Accountants Topics Involved

DEDUCTION OF TAX AT SOURCE

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

Webcast on recent changes in form 3CD AY th August CA. D K Bholusaria

Webcast on recent changes in form 3CD AY 2018-19 20 th August 2018 CA. D K Bholusaria Disclaimer This presentation has been prepared for academic use only for sharing knowledge on the subject. Though every

Webcast on recent changes in form 3CD AY 2018-19 20 th August 2018 CA. D K Bholusaria Disclaimer This presentation has been prepared for academic use only for sharing knowledge on the subject. Though every

Institute of Chartered Accountants of India. Taxation of Foreign Remittances

Institute of Chartered Accountants of India Taxation of Foreign Remittances 17.02.2017 Presented by CA.Shweta Ajmera cashwetaajmera@gmail.com "It was only for the good of his subjects that he collected

Institute of Chartered Accountants of India Taxation of Foreign Remittances 17.02.2017 Presented by CA.Shweta Ajmera cashwetaajmera@gmail.com "It was only for the good of his subjects that he collected

Overview of Transfer Pricing Regulations. CA Akshay Kenkre

Overview of Transfer Pricing Regulations CA Akshay Kenkre 1 What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services, tangible or/ and intangibles

Overview of Transfer Pricing Regulations CA Akshay Kenkre 1 What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services, tangible or/ and intangibles

Income Tax Act DIVISION ONE 1 DIVISION TWO 2

Income Tax Act SECTION DIVISION ONE 1 Income-tax Act, 1961 Arrangement of Sections I-3 Text of the Income-tax Act, 1961 as amended by the Finance (No. 2) Act, 2014 1.1 Appendix : Text of remaining provisions

Income Tax Act SECTION DIVISION ONE 1 Income-tax Act, 1961 Arrangement of Sections I-3 Text of the Income-tax Act, 1961 as amended by the Finance (No. 2) Act, 2014 1.1 Appendix : Text of remaining provisions

Residential Status, Scope Of Total Income Under Income Tax, and Foreign Tax Credit

1 KARTHIK RANGANATHAN ASSOCIATES Residential Status, Scope Of Total Income Under Income Tax, and Foreign Tax Credit Seminar on NRI Taxation ICAI SIRC, Chennai April 29, 2017 Karthik Ranganathan Tax and

1 KARTHIK RANGANATHAN ASSOCIATES Residential Status, Scope Of Total Income Under Income Tax, and Foreign Tax Credit Seminar on NRI Taxation ICAI SIRC, Chennai April 29, 2017 Karthik Ranganathan Tax and

Funds Management. Tax and Regulatory Issues. March KPMG.com/in

Funds Management Tax and Regulatory Issues March 2017 KPMG.com/in 1 Contents 1 Investment routes An overview 2 Key Tax Developments and Issues 3 Key Policy Changes 2 Investment Routes An Overview 3 Type

Funds Management Tax and Regulatory Issues March 2017 KPMG.com/in 1 Contents 1 Investment routes An overview 2 Key Tax Developments and Issues 3 Key Policy Changes 2 Investment Routes An Overview 3 Type

Digital Economy. Dr. Amar Mehta October Chambers Of Tax Consultant, Mumbai.

Digital Economy Chambers Of Tax Consultant, Mumbai Dr. Amar Mehta October 2018 Categories 1 OECD s BEPS Action 1 Final Report 4 Digital PE: The EU Version 7 Italy 2 OECD s BEPS Interim Report Action 1

Digital Economy Chambers Of Tax Consultant, Mumbai Dr. Amar Mehta October 2018 Categories 1 OECD s BEPS Action 1 Final Report 4 Digital PE: The EU Version 7 Italy 2 OECD s BEPS Interim Report Action 1

International Tax Sweden Highlights 2019

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Sweden, see Deloitte tax@hand. Investment basics: Currency Swedish Krona (SEK) Foreign exchange control

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Sweden, see Deloitte tax@hand. Investment basics: Currency Swedish Krona (SEK) Foreign exchange control

BEPS Action Plans - Future of International Tax Landscape Rohan K Phatarphekar

BEPS Action Plans - Future of International Tax Landscape Rohan K Phatarphekar 8 April 2017 Contents BEPS Action Plans - implementation status in India Action Plan 1 Digital Economy Action Plan 4 Interest

BEPS Action Plans - Future of International Tax Landscape Rohan K Phatarphekar 8 April 2017 Contents BEPS Action Plans - implementation status in India Action Plan 1 Digital Economy Action Plan 4 Interest

Budget Presented For: Klaus Vogel Group Presented By: Mr. Kuntal Dave Date: March 8, 2013

Budget 2013 Presented For: Klaus Vogel Group Presented By: Mr. Kuntal Dave Date: March 8, 2013 Index Direct Tax Proposals Implications of amendments proposed in the Finance Bill, 2013 2 Direct Tax Proposals

Budget 2013 Presented For: Klaus Vogel Group Presented By: Mr. Kuntal Dave Date: March 8, 2013 Index Direct Tax Proposals Implications of amendments proposed in the Finance Bill, 2013 2 Direct Tax Proposals

E-TDS FILING PRESENTED BY. Vinod Kumar Jain FCA

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

Union Budget 2014 Analysis of Major Direct tax proposals

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS

17 July 2017 Global Tax Alert Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

17 July 2017 Global Tax Alert Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

Norway signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS

18 August 2017 Global Tax Alert Norway signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

18 August 2017 Global Tax Alert Norway signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

SPECIFIED DOMESTIC TRANSACTION SECTION 40a(2) -Nihar Jambusaria

-Nihar Jambusaria") SPECIFIED DOMESTIC TRANSACTION SECTION 40a(2) -Nihar Jambusaria TP Regulations to apply to certain Specified Domestic Transactions [New Section 92BA] TP provisions are applicable to the following Domestic

SPECIFIED DOMESTIC TRANSACTION SECTION 40a(2) -Nihar Jambusaria TP Regulations to apply to certain Specified Domestic Transactions [New Section 92BA] TP provisions are applicable to the following Domestic

Cyprus signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS

25 July 2017 Global Tax Alert Cyprus signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

25 July 2017 Global Tax Alert Cyprus signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

Introduction to Tax Treaties and its application

Introduction to Tax Treaties and its application Western India Regional Council ICAI Rajesh Patil 5 October 2013 Overview Every nation has a right to tax its residents/nationals on their global income

Introduction to Tax Treaties and its application Western India Regional Council ICAI Rajesh Patil 5 October 2013 Overview Every nation has a right to tax its residents/nationals on their global income

TDS & TCS Recent Updates & Amendments.

TDS & TCS Recent Updates & Amendments. By. CA. Tarun Jain. B.com, FCA. Synopsis of Discussion Amendments in Finance act 2016. Amendment to Section 206AA New provisions relating to TCS Other Miscellaneous

TDS & TCS Recent Updates & Amendments. By. CA. Tarun Jain. B.com, FCA. Synopsis of Discussion Amendments in Finance act 2016. Amendment to Section 206AA New provisions relating to TCS Other Miscellaneous

KPMG Japan tax newsletter

Japan tax newsletter KPMG Tax Corporation 24 December 2015 KPMG Japan tax newsletter Amended Japan-Germany Tax Treaty 1. Preamble... 2 2. Hybrid Entities (Article 1)... 2 3. Business Profits (Article 7)...

Japan tax newsletter KPMG Tax Corporation 24 December 2015 KPMG Japan tax newsletter Amended Japan-Germany Tax Treaty 1. Preamble... 2 2. Hybrid Entities (Article 1)... 2 3. Business Profits (Article 7)...

New US income tax treaty and protocol with Italy enters into force

22 December 2009 International Tax Alert News and views from Foreign Tax Desks New US income tax treaty and protocol with Italy enters into force Executive summary On 16 December 2009, the United States

22 December 2009 International Tax Alert News and views from Foreign Tax Desks New US income tax treaty and protocol with Italy enters into force Executive summary On 16 December 2009, the United States

Seminar E IFA/OECD. The Multilateral Instrument IFA & OECD 2017

Seminar E IFA/OECD The Multilateral Instrument IFA & OECD 2017 Panel members Pascal Saint-Amans, Director, OECD, Centre for Tax Policy and Administration Maikel Evers, Advisor, OECD, Tax Treaties, Transfer

Seminar E IFA/OECD The Multilateral Instrument IFA & OECD 2017 Panel members Pascal Saint-Amans, Director, OECD, Centre for Tax Policy and Administration Maikel Evers, Advisor, OECD, Tax Treaties, Transfer

Investing In and Through Singapore

Investing In and Through Singapore Shanker Iyer 17 May 2012 Contents Benefits of Singapore Setting Up and Ongoing Requirements Territorial Tax System Taxation of Passive Income and Other income Tax Incentives

Investing In and Through Singapore Shanker Iyer 17 May 2012 Contents Benefits of Singapore Setting Up and Ongoing Requirements Territorial Tax System Taxation of Passive Income and Other income Tax Incentives

Anti Avoidance Rules and Treaty Shopping (including Limitation of Benefits) CA Sanjay Tolia. December 2014

CA Sanjay Tolia. December 2014") Anti Avoidance Rules and Treaty Shopping (including Limitation of Benefits) CA Sanjay Tolia Agenda Treaty shopping - Concept Key anti-avoidance measures in tax treaties Limitation on Benefits Beneficial

Anti Avoidance Rules and Treaty Shopping (including Limitation of Benefits) CA Sanjay Tolia Agenda Treaty shopping - Concept Key anti-avoidance measures in tax treaties Limitation on Benefits Beneficial

Recent Transfer Pricing Developments

Recent Transfer Pricing Developments CA Rachesh Kotak September 08, 2017 Setting the context Old world New world Compliance driven Reliance on local documentation One-sided approaches Protracted litigation

Recent Transfer Pricing Developments CA Rachesh Kotak September 08, 2017 Setting the context Old world New world Compliance driven Reliance on local documentation One-sided approaches Protracted litigation

Tax Dispute Resolution in India - How to effectively handle? Sanjay Sanghvi 29 April 2017

Tax Dispute Resolution in India - How to effectively handle? Sanjay Sanghvi 29 April 2017 Income Tax in India An overview Residents taxed on worldwide income Non-residents taxed on Indian sourced income

Tax Dispute Resolution in India - How to effectively handle? Sanjay Sanghvi 29 April 2017 Income Tax in India An overview Residents taxed on worldwide income Non-residents taxed on Indian sourced income

How to read Tax Treaties Salient features of select Indian DTAA. Arpit Jain Chartered Accountant

How to read Tax Treaties Salient features of select Indian DTAA Arpit Jain Chartered Accountant Introduction Salient Features India has signed more than 90 DTAAs till date India does not have Model DTAA

How to read Tax Treaties Salient features of select Indian DTAA Arpit Jain Chartered Accountant Introduction Salient Features India has signed more than 90 DTAAs till date India does not have Model DTAA

Equalisation levy Genesis, Provisions and Interpretation Issues

Equalisation levy Genesis, Provisions and Interpretation Issues By Shaily Gupta, Senior Associate, Vaish Associates Advocates Email: shailygupta@vaishlaw.com 1. Digital Economy The new Economy 'Digital

Equalisation levy Genesis, Provisions and Interpretation Issues By Shaily Gupta, Senior Associate, Vaish Associates Advocates Email: shailygupta@vaishlaw.com 1. Digital Economy The new Economy 'Digital

The Centre of Excellence for GST. GST: Returns. JULY 09, 2017 ICAI Tower, BKC MUMBAI. CA. Hemant P. Vastani. The Centre of Excellence for GST

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

The Czech Republic signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS

19 July 2017 Global Tax Alert The Czech Republic signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of

19 July 2017 Global Tax Alert The Czech Republic signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of

Workshop on Taxation of Foreign Remittances

THE CHAMBER OF TAX CONSULTANTS 3, Rewa Chambers, Ground Floor, 31, New Marine Lines, Mumbai - 400 020 Tel.: 2200 1787 / 2209 0423 Fax: 2200 2455 E-mail: office@ctconline.org Visit us at: Website: http://www.ctconline.org

THE CHAMBER OF TAX CONSULTANTS 3, Rewa Chambers, Ground Floor, 31, New Marine Lines, Mumbai - 400 020 Tel.: 2200 1787 / 2209 0423 Fax: 2200 2455 E-mail: office@ctconline.org Visit us at: Website: http://www.ctconline.org

WESTERN INDIA REGIONAL COUNCIL OF ICAI

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

Impact of section 206AA on the rates of TDS, particularly in respect of payments to non-residents

1 Impact of section 206AA on the rates of TDS, particularly in respect of payments to non-residents [Published in 388 ITR (Journ.) p.57 (Part-4)] By S.K. Tyagi Section 206AA was inserted in the Income-Tax

1 Impact of section 206AA on the rates of TDS, particularly in respect of payments to non-residents [Published in 388 ITR (Journ.) p.57 (Part-4)] By S.K. Tyagi Section 206AA was inserted in the Income-Tax

TDS on payments to non-residents

TDS on payments to non-residents 291 ITR (Jour.) 18 (Part-5) -S.K. Tyagi 1 Of late, it has been observed that with the growth of the economy of the country the number of transactions of the tax-payers

TDS on payments to non-residents 291 ITR (Jour.) 18 (Part-5) -S.K. Tyagi 1 Of late, it has been observed that with the growth of the economy of the country the number of transactions of the tax-payers

T. P. Ostwal & Associates (Regd.) Key Budget Proposal Budget 2012 CHARTERED ACCOUNTANTS

Key Budget Proposal Budget 2012 CHARTERED ACCOUNTANTS") IMPORTANT AMENDMENTS & MAJOR DIRECT TAX PROPOSALS IN FINANCE BILL, 2012 CORPORATE TAX No change in the head corporate tax. Extension of sunset date for tax holiday for power sector to 2013; Initial depreciation

IMPORTANT AMENDMENTS & MAJOR DIRECT TAX PROPOSALS IN FINANCE BILL, 2012 CORPORATE TAX No change in the head corporate tax. Extension of sunset date for tax holiday for power sector to 2013; Initial depreciation

INCOME TAX. -COPY OF- CIRCULAR NO.19/2015 Dated 27 th November, 2015

INCOME TAX -COPY OF- CIRCULAR NO.19/2015 Dated 27 th November, 2015 F.No.142/14/2015-TPL Government of India Ministry of Finance Department of Revenue (Central Board of Direct Taxes) New Delhi ** ** **

INCOME TAX -COPY OF- CIRCULAR NO.19/2015 Dated 27 th November, 2015 F.No.142/14/2015-TPL Government of India Ministry of Finance Department of Revenue (Central Board of Direct Taxes) New Delhi ** ** **

International Tax Malta Highlights 2019

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Malta, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control No

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Malta, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control No

Bombay Chamber of Commerce. Attribution of Profits to. Permanent Establishment.

Bombay Chamber of Commerce 22 nd March, 2010 Presentation on Attribution of Profits to Permanent Establishment By CA Rashmin C. Sanghvi Contents Page No. Preface 2-4 Concepts & Interpretation. (i) OECD

Bombay Chamber of Commerce 22 nd March, 2010 Presentation on Attribution of Profits to Permanent Establishment By CA Rashmin C. Sanghvi Contents Page No. Preface 2-4 Concepts & Interpretation. (i) OECD

GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) (CENTRAL BOARD OF DIRECT TAXES) New Delhi, the 25 th July, 2014 NOTIFICATION

(CENTRAL BOARD OF DIRECT TAXES) New Delhi, the 25 th July, 2014 NOTIFICATION") GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) (CENTRAL BOARD OF DIRECT TAXES) New Delhi, the 25 th July, 2014 NOTIFICATION INCOME-TAX S.O. 1902 (E) In exercise of the powers conferred

GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) (CENTRAL BOARD OF DIRECT TAXES) New Delhi, the 25 th July, 2014 NOTIFICATION INCOME-TAX S.O. 1902 (E) In exercise of the powers conferred

Outbound investment Post BEPS - Planning and Challenges

Outbound investment Post BEPS - Planning and Challenges Vishal Gada Dhruva Advisors International Fiscal Association 18 th June, 2016, Mumbai Index International Tax Scenario - BEPS & GAAR Treaty Shopping

Outbound investment Post BEPS - Planning and Challenges Vishal Gada Dhruva Advisors International Fiscal Association 18 th June, 2016, Mumbai Index International Tax Scenario - BEPS & GAAR Treaty Shopping

Highlights of Easwar Committee s Draft Report on Income Tax Law Simplification in India

Highlights of Easwar Committee s Draft Report on Income Tax Law Simplification in India Executive Summary India is leaving no stone unturned to simplify the tax situation. Recently formed Easwar Committee,

Highlights of Easwar Committee s Draft Report on Income Tax Law Simplification in India Executive Summary India is leaving no stone unturned to simplify the tax situation. Recently formed Easwar Committee,