Institute of Chartered Accountants of India. Taxation of Foreign Remittances

|

|

|

- Easter Hawkins

- 5 years ago

- Views:

Transcription

1 Institute of Chartered Accountants of India Taxation of Foreign Remittances Presented by CA.Shweta Ajmera

2 "It was only for the good of his subjects that he collected taxes from them, just as the Sun draws moisture from the Earth to give it back a thousand fold" --Kalidas in Raghuvansh eulogizing KING DALIP. 2

3 Principles of Taxation Residence based Taxation 3

4 Introduction I have received an invoice from a foreign company for payment What should I do? Finance Manager ABC Limited 4

5 Following issues to be considered before making the remittance: Whether it is permissible under FEMA? Is it taxable in India under ITA or DTAA? If taxable rate of TDS? Which rate to apply ITA or DTAA? Also the MFN clause of DTAA is important If not taxable, proper reasoning why it is not taxable? 5

6 Provisions mentioned under Income Tax Act 1961 Section number Sec. 192 Sec. 194E Sec. 196 to 196D Sec. 195 Details WHT in case of Salary Payment Payments to Non-Resident Sportsmen or Sports Association Specific Sections In other than above mentioned cases 6

7 PRESENTATION DIVIDED INTO FOUR PARTS Part A : Overview Of Section 195 Part B : Scope Of Income Of A Non-resident Part C: Certain Cross Border Payments Withholding Tax Issues Part D: Remittance Certificate By CA & submission by assessee (Form 15CB/15CA) 7

8 Why discuss Section 195? Stringent consequences for all parties to the transaction Deductor Deductee CA! Scope expanded in recent times Retrospectively Extraterritorial Operation Tax Department s eye on international payments Controversy for Remittance Procedures Is it now clear? 8

9 UNIQUE FEATURES of section 195 as compared to other TDS Provisions Unlike personal payments exempted in section 194C etc; no exclusion for the same in section 195 (all payments covered excluding salaries provided chargeability there) eg payment to foreign architect for residential house construction etc. Unlike threshold criteria specified in section 194C etc, no basic limit in section 195 even Re 1 payment is covered. 44AB criteria? Unlike other provisions in Chapter XVII (TDS provisions), section 195 uses a special phrase chargeable to tax under the Act All payers covered irrespective of legal character HUF; Indl etc Multi-dimensional as involves understanding of DTAA/Treaty 9

10 Section Provisions 195(1) Scope and conditions of applicability 195(2) Application by the payer to the AO for lower/nil WH 195(3) Application by the payee to the AO for NIL WH 195(4) Validity of certificate issued by the AO of lower/nil WH 195(5) Powers of CBDT to issue Notifications/Rules 195(6) Furnish the information relating to the payment of any sum 195(7) CBDT to specify class of persons or cases where application to AO is compulsory 195A AN OVERVIEW OF TDS U/S. 195 Grossing up of tax 10

has to furnish")

11 Overview of section 195 Section 195 of the Income Tax Act, 1961 Make any payments or credit to.. Any person Non resident Withhold tax at the rates in force The person making such aforesaid payment (whether or not chargeable to tax) has to furnish information as prescribed in rule 37BB. CA.Shweta Ajmera 11

12 SECTION 195(1) Any person responsible for paying to a non-resident, not being a company or to a foreign company, any interest (not being interest refered to in section 194LB or sec 194 LC or sec 194LD) or any other sum chargeable under the provisions of the Act (not being the income chargeable under the head salaries) shall, at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by issue of cheque or draft or by any other mode deduct income tax thereon at the rates in force. 12

13 Any person responsible for paying to Non Resident Section 204 (iib) (new clause from 1 st April 2017) -Payer himself -or if payer is a company, the company itself including the principal officer thereof 13

14 194LB, 194LC & 194LD 194LB: Income by way of interest from infrastructure debt fund. 194LC: Concessional tax rate on interest in case of specifiest d Borrowings- 5% on the borrowings till 1 st July 2017, now extended to 1 st July LD:Concessional tax rate on interest to FII s & QFI s- 5% on the borrowings till 1 st July 2017, now extended to 1 st July

15 SECTION 195(1) Provided- In case of Interest Payable by government or a public sector Bank within the meaning of sec 10(23D) or a public FI within the meaning of that clause, WHT only on payment basis Provided no deduction shall be made in respect of any dividends referred to in section 115 O Explanation 1: Interest payable account or Suspense Account 15

16 AN OVERVIEW OF TDS U/S. 195 Wide Scope of the section Conditions for application of Section 195 a) any person - Includes a person having no taxable income. b) a non-resident - Includes NRIs - does not include R but NOR c) sum chargeable to tax (other than Salaries and exempt dividend u/s 115O) 16

17 Determination of Any sums chargeable to tax Charge of Income Tax Section 4 Scope of Total Income Section 5 Accruing or deemed to accrue Received or deemed to receive Residential Status Section 6 Deemed Income: section 7 & section 9 17

18 Scheme of Taxation for Non-Residents under the Income Tax Act,1961 Section 4 (Charge of Income Tax)- Income Tax shall be charged at the rates for that assessment year in accordance with the provisions of the Income Tax act 1961 in respect of total Income of every person. Section 2(31) Person includes An individual HUF A Company A firm AOP or BOI whether incorporated or not. Local Authority Every artificial Juridical Person, not falling above. 18

19 Why Compliances???-Compliances are under Deemed Concept.. Section 6 of the Income Tax Act 1961 states about the residential status of a person. Non Residents are separately categorised in it. According to section 5(2) of the Act, which states, the total income of any previous year of a person who is Non-resident includes all the income from whatever source derived which is received or is deemed to be received in India or accrues or arises or deemed to accrue or arise to him in India during the previous year. Section 7 and 9 of the act explains the term Income deemed to be received and Income deemed to accrue or arise in India. 19

20 Section 5 of Income Tax Act 1961 Section 5(2) The total income of any previous year of a person who is a non resident includes all income which: Is received or deemed to be received in India or Accrues or arises or is deemed to accrue or arise to him in India. section 2(30)- A non-resident means a person who is not a resident and does not includes the person who is resident but not ordinarily resident. 20

21 Scope of Income Income accrued or arised in India/received in India Income accrued outside India but deemed to accrue in India/First receipt In India Any other income accrued outside India & received outside India Resident & Ordinarily Resident Resident but not ordinarily resident Non Resident Taxable Taxable Taxable Taxable Taxable Taxable Taxable Not Taxable* Not Taxable * Exception: Income received by the individual is taxable only if the business set up is in India 21

22 Section 6-Residential Status An individual will be treated as a Resident in India in any previous year if he/she is in India for: At least 182 days in that year, or At least 365 days during 4 years preceding that year AND at least 60 days in that year. (if the individual leaves India for the purpose of employment or as a member of the crew of an Indian Ship, then the words 60 days will be substituted with 182 days ) An individual who does not satisfy both the conditions as mentioned above will be treated as non-resident in that previous year. 22

23 Section 6- Residential Status A person is said to be not ordinarily resident in India if: He has been a non- resident for 9 out of 10 previous year preceding that year, or during seven previous years, preceding that year, has been in India for 729 days or less ( in case of an HUF the above criteria will be applied to the karta of HUF to know the status of the HUF) Any HUF, firm or company is said to be resident in India if during the previous year the control and management of its affairs is situated wholly in India. 23

24 Section 9 of the Income Tax Act 1961 Section 9(1)(i) All income directly or indirectly through or from any business connection, or property, or asset or source of Income or through transfer of capital asset situated in India. A business connection involves: A relation between a business carried on by non-resident, some activity in India, which contributes directly or indirectly to the earning of the profits or gains. It predicates an element of continuity between the business of the non-resident and the activity in India. Taxable only if: relates to a source of income or asset in India: or if business connection under IT Act/ PE under the treaty exists. 24

25 Principles need to satisfy for BC Landmark judgement of the AP High Court in GVK Industries Ltd v/s ITO laid down following principles: Existence of close, real & intimate relationship Commonness of Interest Continuity of activity or operation. A stray or isolated transaction is not enough to establish a BC (Anglo French Textile Co. Ltd v/s CIT) 25

26 BC person acting on behalf of NR Has & habitually exercises in India,an authority to conclude contracts on behalf of NR, unless his activities are limited to purchase of goods or merchandise for the non resident or Has no such activity, but habitually maintains in India a stock of goods or merchandise from which he regularly delivers goods or merchandise on behalf of NR. Habitually secures orders in India, mainly or wholly for NR or for that NR and other NR controlling, controlled by, or subject to the same common control, as that NR If Agent having Independent status? 26

27 Income not to be treated as arising from business connection (a)income reasonably attributable to the operations carried out in India will be deemed to accrue or arise in India in case all the operations from business are not carried out in India; If the income from Indian operations cannot be definitely ascertained, than, the same may be computed on apportionment: i. At such percentage of Indian turnover as determined by the AO. ii. Taxable Profits=Total profits*receipts accruing /arising in India/Total receipts of business. iii. In any other manner as considered suitable by AO. 27

28 Income not to be treated as arising from business connection (b) Income of NR in respect of operations confined to purchase of goods in India for purpose of exports. (c) NR engaged in business of running news agency/publishing newspaper,magazines,income arising through or from activities confined to collection of news and views in India for transmission out of India shall not be deemed to accrue or arise in India (d) Income arising through or from operation confined to shooting of cinematographic films in India to NR being: 1. An individual who is not citizen 2. A firm not having partner who is either an Indian citizen or Resident in India 3. A Company not having any shareholder who is either Indian Citizen or Resident of India 28

29 Section 9(1)(i) Revenue lost the 11,000 crores battle to Vodafone which led to Retrospective amendment Explanation 4 through to retrospectively mean by means of, in consequence of and by reason of Explanation 5 Capital asset to be situated in India, if share or interest derives directly or indirectly its value substantially from assets located in India Explanation 5A retrospectively AY It says Expln. 5 does not apply to any asset or capital asset, being investment held by non-resident directly or indirectly in FPI s(fii s) 29

Exceeds Rs.10 crores & (ii) Represents atleast 50% of the value of all the assets owned by the company or entity as the case may be.")

30 Section 9(1)(i) Explanation 6- the share or interest, referred to in Explanation 5,shall be deemed to derive its value substantially from assets in India, if on the specified date, the value of such assets: (i) Exceeds Rs.10 crores & (ii) Represents atleast 50% of the value of all the assets owned by the company or entity as the case may be. Value of Asset= Fair Market value(without reduction of liabilities) Specified date-31 st March or as prescribed 30

31 Section 9(1)(i) Explanation 7: No income shall be deemed to accrue or arise in India to a NR from transfer outside India, of any share of or interest in any entity registered or incorporated outside India: Foreign company or entity directly or indirectly owns the asset situated in India and the transferor at any time in 12months preceding date of transfer does not hold: a) The right of management or control in relation to such company or entity or b) The voting power or share capital or interest exceeding 5% of the total voting power or total share capital or total interest, as the case may be of such company 31

32 Section 9- Salaries Section 9(1)(ii): (Eli Lilly Ltd) Income from salaries, if earned in India The term earned in India obviates the difficult question which arises regarding the place of accrual of salaries. The main effect of the clause is to charge non-residents on salary or pension earned in India even where it actually accrues abroad & is received abroad. 32

33 Section 9- Interest, Royalty & FTS Payer Government Resident Non- Resident Deemed to accrue or arise in India In all cases without exception In all cases, except where payable for the purposes of/ in business or profession carried on by such person outside India, or for the purposes of making or earning any income from any source outside India Only in cases where it is payable for the purposes of a business or profession carried on by such person in India, or for the purposes of making or earning any Income from any source in India 33

34 Royalty The transfer of all or any rights (including the granting of a licence) in respect of a patent, invention, model, design, secret formula or process or trademark or similar property. The imparting of any information concerning the working of the above mentioned assets or the intellectual properties The use of any of the above mentioned assets or intellectual properties. The imparting of any information concerning about the above mentioned assets or intellectual properties the transfer of all or any rights (including the granting of a license) in respect of any copyright, literary, artistic or scientific work 34

35 Section 9(1)(vi)- Explanation 4 Transfer of rights retrospectively includes transfer of right for use/ right to use a computer software irrespective of the medium of transfer. What is meant by Right to use Computer Software Explanation 5 Royalty includes consideration whether possession is with payer/ such right is used by the payer/ location of such right is in India. Explanation 6 Process shall retrospectively include transmission by satellite (including up-linking, amplification, conversion for down- linking of any signal), cable, optic fibre or other similar technology Not included those income covered under Capital Gains 35

36 Software payments? As held in Infrasoft s case: What is transferred is nither the copyright in the software nor the use of the copyright in the software, but what is transferred is right to use the copyrighted material or article which is clearly distinct from the rights in the copyright. Limited right to use the copyrighted material and does not give rise to royalty income Web server? As held in Right Floriata case 36

37 Fees for Technical Services Any consideration (including lump-sum) for rendering of any Managerial Technical or Consultancy Services Excludes Construction, assembly, mining or any other like project and income chargeable under the head salaries DTAA- Make available FIS 37

38 Section 9 (v)(vi)(vii) After the decision of Ishikawajima Harima(SC) Explanation was retrospectively inserted by Finance Act, 2007 Income of a non-resident shall be deemed to accrue or arise in India whether or not Non resident has a place of business or business connection in India. Non-resident has rendered services in India However, Karnataka High Court in Jindal Thermal Power has upheld that Ishikawajima Harima is still a good law despite retrospective amendment 38

39 Section 9- Synopsis Nature of Income Business/ Profession se. 9(1)(i) Capital Gains Sec. 9(1)(i) Interest income Sec. 9(1)(v) Royalties sec 9(1)(vi) Taxability Taxable if direct or indirect Business Connection in India or property or asset or source in India or transfer of a capital asset situated in India Taxable if situs of shares/ Property in India or derives its value substantially from assets in India Taxable if sourced in India Taxable if sourced in India FTS sec 9(1)(vii) Taxable if sourced in India 39

40 AN OVERVIEW OF TDS U/S. 195 Chargeability to tax governed by provisions of Act/DTAA Nature of Income Act* Treaty Business/Profession S. 9(1)(i) A.5, A.7 & A.14 Salary Income S. 9(1)(ii) A.15 Dividend Income S. 9(1)(iv), S.115A A.10 Interest Income S. 9(1)(v), S.115A A.11 Royalties S. 9(1)(vi), S.115A A.12 FTS S. 9(1)(vii), S.115A A.12 Capital Gains S. 9(1)(i), S.45 A.13 * Apart from S.5, wherever applicable ACT/DTAA, Whichever is beneficial prevails 40

41 AN OVERVIEW OF TDS U/S. 195 Q. Any sum chargeable to tax means:?????? Q. Whether tax is to be deducted on the gross amount or only on the income portion of the amount paid to NR? Rulings: Transmission corporation of AP Ltd. (105taxman 742)(SC) -Tax liable to be deducted by payer on the gross amount else go for section 195(2) Samsung Electronics Co. Ltd. (185 Taxmann 313)(Karnataka HC) - HC held that obligation to deduct tax arises the moment there is remittance to the NR abroad. Until certificate obtained u/s 195(2), he cannot interpret that income is not taxable in India. 41

42 AN OVERVIEW OF TDS U/S. 195 GE India Technology Centre (P) Ltd (234 CTR 153) (SC) SC held that sec 195(2) is based on Principle of Proportionality & gets attracted where the payment is composite payment. The moment there is a remittance out of India, it does not trigger Sec 195. The payer is bound to deduct tax only if the sum is chargeable to tax (i.e. there is an element of income) in India read with sec 4, 5 and 9. Sec 195 not only covers amounts which represents pure income payments but also covers composite payments which has an element of income embedded in them However, obligation to deduct TDS on such composite payments would be limited to the appropriate proportion of income forming part of the gross sum. SC- Karnataka HC losen its sight on plain language of sec 195(1) 42

43 AN OVERVIEW OF TDS U/S. 195 Based on GE India Ruling: CBDT issued Instruction no. 2/2014 (F.No. 500/33/2013-FTD-I) dated 26 th February 2014, instructing AO that if no application made u/s 195(2) & assessee failed to deduct TDS u/s 195 of the act, default amount u/s 201 is on sum chargeable to tax & not on the whole amount. 43

44 AN OVERVIEW OF TDS U/S. 195 Tax withholding from payment in kind Kanchanganga Sea Foods Ltd. (325 ITR 540) (SC) Payments by one non-resident to another non-resident inside / outside India? Sec 195 applies w.r.t. Payments made to a foreign company? Payment of sum exempt under sec 10 should not be subject to TDS (Hyderabad Industries Ltd. 188 ITR 749 Kar) Indian Branch of a foreign company rendering amount to foreign company? 44

45 AN OVERVIEW OF TDS U/S. 195 S.195(2) - Application by the Payer to the AO for determining appropriate portion of sum chargeable Appeal against order under S. 195(2) - S. 248 Amendment by Finance Act 2007 S. 248 allows the payer to file an appeal before the CIT(A) provided the tax is deposited by the payer in the exchequer of the Government If tax is borne by the payee, a payer cannot file an appeal under section 248 of the Act 45

46 AN OVERVIEW OF TDS U/S. 195 Whether an application can be made under S. 195(2) for NIL Withholding order? Held yes in case of Mangalore Refinery and Petrochemicals Ltd (113 ITD 85) (Mum) However, a contrary view has been taken in the following cases: Czechoslovak Ocean (81 ITR 162) (Cal) Graphite Vicarb India Ltd (28 TTJ 425) (Cal) Practical Purposes, Application u/s 195(2) is adopted for both nil as well as lower withholding tax rate order No time limit for passing order u/s 195(2): Blackwood Hodge (India) Pvt. Ltd. 81 ITR 807 (Cal) Central Associated Pigment Ltd. 80 ITR 631 (Cal) 46

47 AN OVERVIEW OF TDS U/S. 195 Whether applying for WHT certificate compulsory? Principles laid down in GE India Technology Centre P Ltd(SC) Application u/s 195(2) presupposes that the payer is in no doubt that tax is payable in respect of some part but is not sure as to what should be the amount on which tax is so deductible. Where a person is fairly certain about the portion of sum chargeable to tax, then he can make his own determination as to whether TDS is deductible and if so what should be the amount. In case of composite payments, where a payer has a doubt regarding determining the appropriate portion of sum chargeable under the act, he must make an application u/s

48 AN OVERVIEW OF TDS U/S. 195 Section 195(3) - Application by NR payee for NIL tax withholding (Rule 29B) Once such certificate granted, every person responsible for paying income shall make payment without TDS as long as the certificate is in force Conditions to be followed A certificate granted u/s 195(3) shall remain in force: for FY mentioned therein, or until cancelled by the AO before expiry of FY 48

49 Refund of tax Withheld u/s 195 Conditions to be satisfied for refund : contract is cancelled and no remittance is made to the NR the remittance is duly made to the NR, but the contract is cancelled and the remitted amount has been returned to the payee contract is cancelled after partial execution and no remittance is made to the NR for the non-executed part; contract is cancelled after partial execution and remittance related to nonexecuted part made to the NR has been returned to the payee or no remittance is made but tax was deducted and deposited when the amount was credited to the account of the NR; remitted amount gets exempted from tax either by amendment in law or by notification an order is passed under Sec 154 or 248 or 264 reducing the TDS liability of the payee; deduction of tax twice by mistake from the same income; payment of tax on account of grossing up which was not required payment of tax at a higher rate under the domestic law while a lower rate is prescribed in DTAA. 49

of the Act.")

50 Rate of TDS Sec 195(1)- Rates in Force Sec 2(37A)(iii)- for the purpose of TDS u/s 195, rates in force mean the rate specified in Part II of First Schedule to the Finance Act of the relevant year or the rates specified under DTAA, as may be beneficial u/s 90(2) of the Act. 50

51 Particulars Foreign companies Effective rate including Rate of tax surcharge Others Effective rate including surcharge Basic tax rate 40% 30% Surcharge if total income does not exceed 1 crore Surcharge if the total income is more than Rs. 1 crore but less than Rs.10 crore Surcharge if the total income is more than Rs.10 crore NIL 41.2% NIL 30.90% 2% 42.02% 12% 34.61% 5% 43.26% 12% 34.61% 51

52 TRC-Tax Residency Certificate Sec 90(4)- Every NR desirous to take DTAA benefit Sec 90(5) read with rule 21AB, requires payee to furnish info in form 10F: 1. Status of the assessee 2. PAN of the assessee if alloted 3. Nationality or country or specified territory of incorporation or registration 4. Assessee's Tax Identification Number in the country of Residence 5. Period for which the residential status as mentioned in TRC is applicable. 6. Address of assessee in country of Residence 52

53 Section 206AA At the rate specified in the relevant provisions of the act Or At the rates in force Or At the rate of 20% 53

54 206AA- The Finance Act 2016 Only on Payments include Interest, FTS, Royalty and Capital Gains For other cases: PAN is mandatory Rule 37BC vide CBDT Notification No.53/2016 dated 24 th June Basic information i.e name, id, contact number, and address in the country of tax residence. - TRC if the law of country of tax residence provides for issuance of such certificate. - Tax Identification Number(where no such number is available, other unique number by which such payee is identified in the country of tax residence) 54

55 Surcharge & Education cess & Grossing Up On DTAA rates? On Income tax Act Rates? Section 195A Grossing Up of tax Net of Tax arrangement where payer bears the tax liablity. Tax being calculated on the gross amount 55

56 Examples --section 195A Q1. X Co. (a foreign company holding a PAN) has agreed to provide certain technical services to Y Co. (an Indian Company) for a fee of Rs.100. Under the agreement, tax has to be borne by Y Co. The tax rate as per Part II of the First Schedule is %(including surcharge & cess) and tax rate under the DTAA is 10%.Calculate TDS? 56

57 Net Payment 100 Rate in force as per 2(37A)- 10%(i.e. the beneficial rate between % and 10%) 10% Increased income u/s 195A (100*100/90) Grossed up tax 11.11(10*100/90) TDS u/s 195 Rs (10% of Rs ) 57

58 Q2. X Co. doesnot have TAN and yet to obtain TRC? Net Payment 100 Rate in force as per 2(37A)- 10%(i.e. the beneficial rate between % and 10%) 10% Increased income u/s 195A (100*100/90) Grossed up tax 11.11(10*100/90) TDS u/s 195 r.w.s 206AA Rs (20% of Rs ) 58

59 Relevant Foreign Exchange Rates Rule 26 of the Rules: State Bank of India adopted TT buying rate of such currency on the date on which tax is required to be deducted u/s 195 of the Act Exchange rate fluctuation between credit and payment? Sandvik Asia Ltd(49 SOT 554)(ITAT Pune) 59

60 Questions? Payments by a non resident to another non-resident outside India? The Supreme Court in (2012) Vodafone International Holdings B.V. (341 ITR 1)(SC) Payments covered under section 195, but not involving an AD (e.g. payments by credit card, barter payments, book entries, payment to indian branch of a foreign company, payments within India etc)? BSR dummy code Transfer of funds from NRO to NRE account? 60

61 WHT taxes on some common transactions Import of Materials - Exporter has PE in India - Exporter donot have PE in India Commission Agent Outside India - Commission for Commercial Activities - Commission for technical activities 61

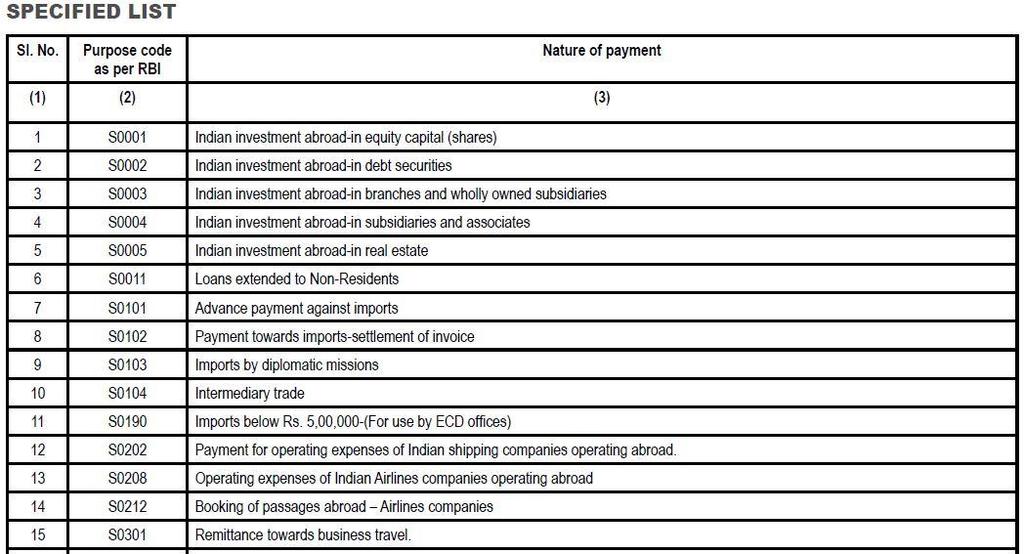

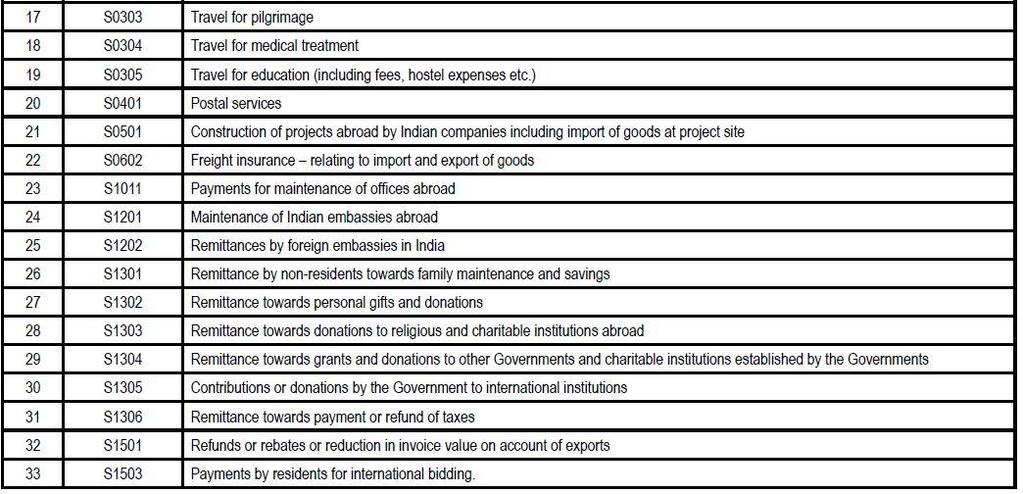

62 WHT taxes on some common transactions Bandwith Charges? Reimbursement of Expenses: If the main expenditure is not chargeable to tax in India either under IT Act or DTAA, than reimbursement of such expenses will also not be chargeable to tax in India. And vice-versa Remuneration of NR Directors: - Employer Employee relationship - Other 62

63 WHT taxes on some common transactions Payment of college fees to university? Repatriation of Money? Payment to conference Speakers? E- commerce transactions? Software payments? When the interest is paid to foreign branch of Indian Bank? 63

64 AIDS to determine taxability of the remittance & Applicable TDS Documentary - Agreement/Contract/ underlying the transaction - Invoice/Debit notes being paid - Other correspondence between parties for determining the exact nature of payment - Website of NR- how they have described their Indian operations - Copy of payee s TRC for relevant period & form 10F. - Application for TRC- if applied 64

,195(3),197")

65 AIDS to determine taxability of the remittance & Applicable TDS Written confirmation from Payee that: - It was a tax resident of the country of residence during the relevant perios and is eligible for the benefits of the applicable DTAA -It is the beneficiary of sum being remitted -It doesnot have a PE in India within the meaning of applicable DTAA Order certificate obtained- 195(2),195(3),197 SBI s certificate TT buying rates ICAI guidance note on Audit Reports & Certificates for special Purposes 65

66 Applicable section Nature of default Consequence 40(a)(i) WHT not deducted or not deposited within prescribed time 201(1) Tax not withheld/deposited appropriately Interest u/s 201(1A) Penalty u/s221 Tax not withheld/deposited appropriately Tax withheld not paid Disallowance of expenses Recovery of tax not withheld/deposited or short withheld/deposited per month or part of the month for non deduction. Further per month is payable from the date of deduction till the date when tax is actually paid Penalty not exceeding the amount of tax not paid can be levied by AO 66

67 Applicable section Penalty u/s 271C Penalty u/s 272A Penalty u/s 271-I Prosecution u/s 276 B Nature of default Tax not withheld or short withheld Failure to file TDS return Non furnishing of Information or furnishing of incorrect information u/s 195(6) Failure to pay tax deducted Consequence Penalty, not exceeding the amount of tax not withheld can be withheld by Joint Commissioner Penalty of INR 100 per day of default subject to maximum of tax deductible Penalty of INR 1,00,000 per transaction Minimum: 3 months Maximum: 7 years 271J Penalty for furnishing incorrect information in reports / certificates Rs.10,000 for each such report(from 1 st April 2017) 67

68 Reporting of Foreign Remittances Section 195(6) of the Act provides that a person responsible for paying to a non-resident (hereafter referred to as payer ) shall furnish such information as may be prescribed under Rule 37BB. 68

certifying (actually expressing his opinion) the taxability (chargeability) of the income in the hands of the payee and the amount of tax required to be deducted by the payer.")

69 Rule 37BB Form No. 15CA is to be filled and submitted online by the deductor i.e. payer. Form 15CB is to be issued by the practicing Chartered Accountant (C.A) certifying (actually expressing his opinion) the taxability (chargeability) of the income in the hands of the payee and the amount of tax required to be deducted by the payer. In order to arrive at the amount of tax to be deducted the CA is required to take into account various applicable provisions of the Act (to compute the income of the nonresident payee) as well as provisions of the applicable Double Tax Avoidance Agreement (DTAA ) and other relevant supporting documents and agreement, if any. 69

70 Steps while making a Remittance Form 15CA is required to be furnished by the taxpayers for the purpose of remittance to a non-resident. It may be noted that Form 15CA should be filed in every case whether the remittance amount is chargeable to Incometax or not. However, exemption from filing of Form 15CA is provided in case of certain types of remittances. 70

71 Procedure where a remittance is not chargeable to tax: Such remittances are classified in the following two categories as follows: i. Non-reportable Transaction ii. Reportable transaction 71

72 Non-reportable Transactions In following two cases there is no requirement to furnish Form 15CA or Form 15CB. (i) Individuals making remittances under the Liberalised Remittance Scheme of FEMA and (ii) Certain specified remittances as listed herein below. 72

73 73

74 74

75 Reportable Transactions Any transaction other than the nonreportable category is considered as reportable transaction. In other words, even if the remittance is not chargeable to tax, information in respect of such remittance is required to be provided in Part D of Form 15CA. 75

76 What is the difference between earlier Rule 37BB and the new Rule 37BB which is effective from 1st April, 2016? Amendments in the new Rule 37BB as compared with earlier Rule 37BB are as follows: Form 15CA and Form 15CB will not be required if an individual is making a remittance, which does not require RBI s approval under FEMA or under the Liberalised Remittance Scheme (LRS). The list of items which do not require submission of Forms 15CA and Form 15CB has been expanded from 28 to 33. The newly introduced items are as under i. Advance Payments against imports ii. Payment towards import settlement of invoice iii. Imports by diplomatic missions iv. Intermediary trade v. Imports below Rs. 5 Lakh (For use by Exchange Control CA.Shweta Ajmera Department offices) 17/02/

77 What is the difference between earlier Rule 37BB and the new Rule 37BB which is effective from 1st April, 2016? Only the payments which are chargeable to tax under the provisions of Act in excess of Rs. 5 Lakh would require Certificate from a Chartered Accountant in Form 15CB. A new reporting obligation is introduced for the authorised dealers (ADs) (i.e. the Banks). ADs will have to file Form 15CC (quarterly) in respect of the foreign remittances made by them. 77

78 Form 15CA: Part A Small Value Taxable payments Small Value Taxable payments Position from 1 st April 2016 Part A Position upto 31 st March 2016 Part A Reporting in Part A- Threshold: Payments upto Rs.5,00,000 in a FY CA. Certificate: Not required Reporting in: Part A Thsreshold: Payments not exceeding Rs.50,000 singly and aggregate of Rs.2,50,000 in a FY CA certificate: Not required 78

79 Form 15CA-Part B High Value Taxable payments where certificate/order u/s 197,195(2),195(3) has been obtained High Value Taxable payments where certificate/order u/s 197,195(2),195(3) has been obtained Position from 1 st April 2016 Part B Position upto 31 st March 2016 Part B Reporting in Part B- Threshold: Payments exceeding Rs.5,00,000 in a FY CA. Certificate: Not required Reporting in: Part B Thsreshold: Payments exceeding Rs.50,000 singly and aggregate of Rs.2,50,000 in a FY CA certificate: Not required 79

80 Form 15CA-Part C High Value Taxable payments where certificate/order u/s 197,195(2),195(3) has not been obtained High Value Taxable payments where certificate/order u/s 197,195(2),195(3) has not been obtained Position from 1 st April 2016 Part C Position upto 31 st March 2016 Part B Reporting in Part C- Threshold: Payments exceeding Rs.5,00,000 in a FY CA. Certificate: required Reporting in: Part C Threshold: Payments exceeding Rs.50,000 singly and aggregate of Rs.2,50,000 in a FY CA certificate: required 80

81 Form 15CA-Part D Payments not taxable under the act (other than the specified payments which are exempt from reporting) Payments not taxable under the act (other than the specified payments which are exempt from reporting) Position from 1 st April 2016 Part D Position upto 31 st March 2016 Part D Reporting in Part D- CA. Certificate: not required Based on the past provisions, a position was possible that reporting did not apply to non taxable remmitances 81

82 82

83 CA.SHWETA AJMERA SHWETA AJMERA & COMPANY CHARTERED ACCOUNTANTS 83

Overview of Taxation of Non Residents

Overview of Taxation of Non Residents CTC Vispi T. Patel Vispi T. Patel & Associates 13 th December, 2013 Scheme of Taxation for Non Residents under Income-tax Act, 1961 Section 4 (Charge of Income-tax)

Overview of Taxation of Non Residents CTC Vispi T. Patel Vispi T. Patel & Associates 13 th December, 2013 Scheme of Taxation for Non Residents under Income-tax Act, 1961 Section 4 (Charge of Income-tax)

Tax Withholding Section 195 and CA certification

Tax Withholding Section 195 and CA certification October 1, 2011 Bijal Desai Presentation Outline Non-resident payments Withholding tax Lower or NIL withholding of tax CA Certification Consequences of

Tax Withholding Section 195 and CA certification October 1, 2011 Bijal Desai Presentation Outline Non-resident payments Withholding tax Lower or NIL withholding of tax CA Certification Consequences of

TDS under section 195 of the Income-tax Act. CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC

TDS under section 195 of the Income-tax Act CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC Overview of section 195 Overview of section 195 195(1) Any person paying to non-resident

TDS under section 195 of the Income-tax Act CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC Overview of section 195 Overview of section 195 195(1) Any person paying to non-resident

Overview of Section December, WIRC of ICAI

Overview of Section 195 30 December, 2017 WIRC of ICAI 1 Payments to Non-resident Payments to Non-residents Key implications FEMA law and compliances GST on RCM basis Banking compliances and documentation

Overview of Section 195 30 December, 2017 WIRC of ICAI 1 Payments to Non-resident Payments to Non-residents Key implications FEMA law and compliances GST on RCM basis Banking compliances and documentation

The Institute of Chartered Accountants Of India

The Institute of Chartered Accountants Of India 15CA- 15CB Filing, Issues & Precautions Natwar G. Thakrar Saturday, 30 th December, 2017 Presentation Outline Brief Analysis of section 195 Determination

The Institute of Chartered Accountants Of India 15CA- 15CB Filing, Issues & Precautions Natwar G. Thakrar Saturday, 30 th December, 2017 Presentation Outline Brief Analysis of section 195 Determination

Withholding tax u/s 195 and filing of Form 15CA/ 15CB - Key issues April 2017

Withholding tax u/s 195 and filing of Form 15CA/ 15CB - Key issues April 2017 Section 195 Overview Section Provisions 195(1) Scope and conditions for applicability 195(2) Application by the Payer for determination

Withholding tax u/s 195 and filing of Form 15CA/ 15CB - Key issues April 2017 Section 195 Overview Section Provisions 195(1) Scope and conditions for applicability 195(2) Application by the Payer for determination

TDS on Payments to Non-residents under section 195 Law and Procedures

Study Course on International Taxation for Beginners Organised by - Western India Regional Council of the Institute Chartered Accountants of India TDS on Payments to Non-residents under section 195 Law

Study Course on International Taxation for Beginners Organised by - Western India Regional Council of the Institute Chartered Accountants of India TDS on Payments to Non-residents under section 195 Law

TDS on Payments to Non-Residents u/s Laws & Procedures. CA Zeel Gala 13 December 2018

TDS on Payments to Non-Residents u/s 195 - Laws & Procedures CA Zeel Gala 13 December 2018 Payments to Non-resident Payments to Nonresidents Key implications FEMA law and compliances GST on RCM basis Banking

TDS on Payments to Non-Residents u/s 195 - Laws & Procedures CA Zeel Gala 13 December 2018 Payments to Non-resident Payments to Nonresidents Key implications FEMA law and compliances GST on RCM basis Banking

SECTION 195 OF THE INCOME TAX ACT,1961 PROVISIONS, AMENDMENTS AND CONTROVERSIES

1 WIRC Pune Camp CPE Study Circle January 19, 2013 SECTION 195 OF THE INCOME TAX ACT,1961 PROVISIONS, AMENDMENTS AND CONTROVERSIES CA JIGER SAIYA jigersaiya@mzsk.in Contents Introduction Recent Amendments

1 WIRC Pune Camp CPE Study Circle January 19, 2013 SECTION 195 OF THE INCOME TAX ACT,1961 PROVISIONS, AMENDMENTS AND CONTROVERSIES CA JIGER SAIYA jigersaiya@mzsk.in Contents Introduction Recent Amendments

Free of Cost ISBN: CS Executive Programme Module-I (Solution upto June & Questions of Dec Included)

") Free of Cost ISBN: 978-93-5034-584-9 Appendix CS Executive Programme Module-I (Solution upto June - 2013 & Questions of Dec - 2013 Included) Paper - 3: Tax Laws Chapter - 3: Basis of Charge and Scope of

Free of Cost ISBN: 978-93-5034-584-9 Appendix CS Executive Programme Module-I (Solution upto June - 2013 & Questions of Dec - 2013 Included) Paper - 3: Tax Laws Chapter - 3: Basis of Charge and Scope of

IN THE SUPREME COURT OF INDIA CIVIL APPELLATE JURISDICTION CIVIL APPEAL NOs OF 2010 (Arising out of SLP(C) No of 2009)

No of 2009)") IN THE SUPREME COURT OF INDIA CIVIL APPELLATE JURISDICTION CIVIL APPEAL NOs.7541-7542 OF 2010 (Arising out of SLP(C) No. 34306-34307 of 2009) GE India Technology Centre Private Ltd.. Appellant(s) Versus

IN THE SUPREME COURT OF INDIA CIVIL APPELLATE JURISDICTION CIVIL APPEAL NOs.7541-7542 OF 2010 (Arising out of SLP(C) No. 34306-34307 of 2009) GE India Technology Centre Private Ltd.. Appellant(s) Versus

An overview and practice aspects of withholding tax under Section 195 of the Income-tax Act Seminar on TDS, ICAI Western Region Mumbai

An overview and practice aspects of withholding tax under Section 195 of the Income-tax Act Seminar on TDS, ICAI Western Region Mumbai CA Shailendra S. Sharma 02 April 2016 Agenda Brief overview of TDS

An overview and practice aspects of withholding tax under Section 195 of the Income-tax Act Seminar on TDS, ICAI Western Region Mumbai CA Shailendra S. Sharma 02 April 2016 Agenda Brief overview of TDS

Withholding taxes on cross-border payments A conundrum? Ernst & Young Webcast Held on 10 February 5.00 p.m. (IST)

") Withholding taxes on cross-border payments A conundrum? Ernst & Young Webcast Held on 10 February 2010 @ 5.00 p.m. (IST) Contents Background Key issues/ challenges Karnataka High Court ruling Technical

Withholding taxes on cross-border payments A conundrum? Ernst & Young Webcast Held on 10 February 2010 @ 5.00 p.m. (IST) Contents Background Key issues/ challenges Karnataka High Court ruling Technical

Residence and Scope of Total Income

2 Residence and Scope of Total Income 2.1 Residential Status [Section 6] The incidence of tax on any assessee depends upon his residential status under the Act. Therefore, after determining whether a particular

2 Residence and Scope of Total Income 2.1 Residential Status [Section 6] The incidence of tax on any assessee depends upon his residential status under the Act. Therefore, after determining whether a particular

An overview of Section 195 and foreign payments of the Income-tax Act at The Institute of Chartered Accountants of India, Seminar of TDS

An overview of Section 195 and foreign payments of the Income-tax Act at The Institute of Chartered Accountants of India, Seminar of TDS by CA Shailendra Sharma 07 April 2018 Agenda Brief overview of the

An overview of Section 195 and foreign payments of the Income-tax Act at The Institute of Chartered Accountants of India, Seminar of TDS by CA Shailendra Sharma 07 April 2018 Agenda Brief overview of the

SIRC of ICAI CPE Study Circle Meeting Wednesday Issues!!! CA. V Sathyanarayanan, Kochi

SIRC of ICAI CPE Study Circle Meeting Wednesday 20.01.2016 Issues!!! CA. V Sathyanarayanan, Kochi Foreign Remittance Whether to liable to tax under The Income Tax Act No Yes No TDS No Whether liable to

SIRC of ICAI CPE Study Circle Meeting Wednesday 20.01.2016 Issues!!! CA. V Sathyanarayanan, Kochi Foreign Remittance Whether to liable to tax under The Income Tax Act No Yes No TDS No Whether liable to

TDS provisions for payment to nonresident under Section 195 of the Income-tax Act

TDS provisions for payment to nonresident under Section 195 of the Income-tax Act Seminar on issues in TDS ICAI, Mumbai CA Shailendra S. Sharma 23 January 2016 Agenda Brief overview of TDS provisions Concept

TDS provisions for payment to nonresident under Section 195 of the Income-tax Act Seminar on issues in TDS ICAI, Mumbai CA Shailendra S. Sharma 23 January 2016 Agenda Brief overview of TDS provisions Concept

Seminar on NRI Taxation

Seminar on NRI Taxation Section 9(1) and Treaty Provisions PP Anand April 2017 Income deemed to accrue or arise in India [Section 9] Income deemed to accrue or arise in India Section 9 Following categories

Seminar on NRI Taxation Section 9(1) and Treaty Provisions PP Anand April 2017 Income deemed to accrue or arise in India [Section 9] Income deemed to accrue or arise in India Section 9 Following categories

TDS on Non Residents. CA. Rajesh Patil

TDS on Non Residents. CA. Rajesh Patil Western India Regional Council 12 February 2011 Contents (1) Introduction Analysis of section 195 Payers covered Payees covered Payments covered Point of Tax Withholding

TDS on Non Residents. CA. Rajesh Patil Western India Regional Council 12 February 2011 Contents (1) Introduction Analysis of section 195 Payers covered Payees covered Payments covered Point of Tax Withholding

T. P. Ostwal & Associates (Regd.) Key Budget Proposal Budget 2012 CHARTERED ACCOUNTANTS

Key Budget Proposal Budget 2012 CHARTERED ACCOUNTANTS") IMPORTANT AMENDMENTS & MAJOR DIRECT TAX PROPOSALS IN FINANCE BILL, 2012 CORPORATE TAX No change in the head corporate tax. Extension of sunset date for tax holiday for power sector to 2013; Initial depreciation

IMPORTANT AMENDMENTS & MAJOR DIRECT TAX PROPOSALS IN FINANCE BILL, 2012 CORPORATE TAX No change in the head corporate tax. Extension of sunset date for tax holiday for power sector to 2013; Initial depreciation

TDS on Payments to Non Residents Law and Procedures

TDS on Payments to Non Residents Law and Procedures Regional Conference of CAs on GST & Income-tax Rajkot Branch of WIRC, Institute of Chartered Accountants of India 16 th December 2017 Rutvik Sanghvi

TDS on Payments to Non Residents Law and Procedures Regional Conference of CAs on GST & Income-tax Rajkot Branch of WIRC, Institute of Chartered Accountants of India 16 th December 2017 Rutvik Sanghvi

Law & Procedure for foreign remittances

Law & Procedure for foreign remittances Himanshu Parekh 13 January 2017 KPMG.com/in Overview of Section 195 Section Provision 195(1) Scope and conditions for applicability 195(2) Application by the Payer

Law & Procedure for foreign remittances Himanshu Parekh 13 January 2017 KPMG.com/in Overview of Section 195 Section Provision 195(1) Scope and conditions for applicability 195(2) Application by the Payer

TAX AUDIT POINTS TO BE CONSIDERED

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

Annexure to Circular No. CTD/Circ./TDS/ /01 dated

OIL AND NATURAL GAS CORPORATION LTD. CORPORATE TAX DIVISION Old Secretariat Building, Tel Bhawan Dehra Dun- 248 003 Tel: 0135-2793833 Fax: 0135-2758518 Annexure to Circular No. CTD/Circ./TDS/2017-18/01

OIL AND NATURAL GAS CORPORATION LTD. CORPORATE TAX DIVISION Old Secretariat Building, Tel Bhawan Dehra Dun- 248 003 Tel: 0135-2793833 Fax: 0135-2758518 Annexure to Circular No. CTD/Circ./TDS/2017-18/01

As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017.

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

TDS on payments to non-residents

TDS on payments to non-residents 291 ITR (Jour.) 18 (Part-5) -S.K. Tyagi 1 Of late, it has been observed that with the growth of the economy of the country the number of transactions of the tax-payers

TDS on payments to non-residents 291 ITR (Jour.) 18 (Part-5) -S.K. Tyagi 1 Of late, it has been observed that with the growth of the economy of the country the number of transactions of the tax-payers

CHANGES IN 3CD TAX AUDIT REPORT FOR THE A.Y

CHANGES IN 3CD TAX AUDIT REPORT FOR THE A.Y. 2013-2014 AMENDMENTS IN FINANCE ACT, 2012 HAVING IMPACT ON TAX AUDIT REPORT Rule 12 From A.Y. 2013-14 inter-alia e-filing of Audit Reports u/s. 44AB (Tax Audit

CHANGES IN 3CD TAX AUDIT REPORT FOR THE A.Y. 2013-2014 AMENDMENTS IN FINANCE ACT, 2012 HAVING IMPACT ON TAX AUDIT REPORT Rule 12 From A.Y. 2013-14 inter-alia e-filing of Audit Reports u/s. 44AB (Tax Audit

Residential Status, Scope Of Total Income Under Income Tax, and Foreign Tax Credit

1 KARTHIK RANGANATHAN ASSOCIATES Residential Status, Scope Of Total Income Under Income Tax, and Foreign Tax Credit Seminar on NRI Taxation ICAI SIRC, Chennai April 29, 2017 Karthik Ranganathan Tax and

1 KARTHIK RANGANATHAN ASSOCIATES Residential Status, Scope Of Total Income Under Income Tax, and Foreign Tax Credit Seminar on NRI Taxation ICAI SIRC, Chennai April 29, 2017 Karthik Ranganathan Tax and

Vinodh & Muthu Chartered Accountants. Newsletter MAY 2016

Vinodh & Muthu Chartered Accountants Newsletter MAY 2016 2 Dear Readers, Welcome to our newsletter. VMCA brings you the significant developments in taxation during the month of May 2016. We hope this edition

Vinodh & Muthu Chartered Accountants Newsletter MAY 2016 2 Dear Readers, Welcome to our newsletter. VMCA brings you the significant developments in taxation during the month of May 2016. We hope this edition

A BILL to give effect to the financial proposals of the Central Government for the financial year

FINANCE BILL, 2012* Bill No. 11 of 2012 A BILL to give effect to the financial proposals of the Central Government for the financial year 2012-2013. BE it enacted by Parliament in the Sixty-third Year

FINANCE BILL, 2012* Bill No. 11 of 2012 A BILL to give effect to the financial proposals of the Central Government for the financial year 2012-2013. BE it enacted by Parliament in the Sixty-third Year

Gurgaon Branch of NIRC of ICAI

Form 15 CB/15 CA A Discussion Gurgaon Branch of NIRC of ICAI 27 th August, 2016 by CA Sanjay Agrawal WHAT SHOULD BE OUR TAKE AWAYS? Understand the objective & importance of Form 15 CB & 15 CA.. Understand

Form 15 CB/15 CA A Discussion Gurgaon Branch of NIRC of ICAI 27 th August, 2016 by CA Sanjay Agrawal WHAT SHOULD BE OUR TAKE AWAYS? Understand the objective & importance of Form 15 CB & 15 CA.. Understand

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

DEDUCTION OF TAX AT SOURCE SECTION 195 H PADAMCHAND KHINCHA CHARTERED ACCOUNTANTS

DEDUCTION OF TAX AT SOURCE SECTION 195 H PADAMCHAND KHINCHA CHARTERED ACCOUNTANTS 1 Nature of TDS obligation Section 4(1) Charge of income tax Section 4(2) Income tax shall be deducted at source or paid

DEDUCTION OF TAX AT SOURCE SECTION 195 H PADAMCHAND KHINCHA CHARTERED ACCOUNTANTS 1 Nature of TDS obligation Section 4(1) Charge of income tax Section 4(2) Income tax shall be deducted at source or paid

(A) received from the Government in pursuance of an agreement made by the non-resident/ foreign company with the Government, or

received from the Government in pursuance of an agreement made by the non-resident/ foreign company with the Government, or") Section 115A - 10% on Royalty and FTS Where the total income of a foreign company or a non-resident includes any income by way of royalty or fees for technical services other than the income referred to

Section 115A - 10% on Royalty and FTS Where the total income of a foreign company or a non-resident includes any income by way of royalty or fees for technical services other than the income referred to

Payment of Export commission to Non-Resident Agent :-

Common Disputes:- Payment of Export commission to Non-Resident Agent :- Relevant Bare Act, Rules & Circulars:- Other Sums 195. [(1) Any person responsible for paying to a non-resident, not being a company,

Common Disputes:- Payment of Export commission to Non-Resident Agent :- Relevant Bare Act, Rules & Circulars:- Other Sums 195. [(1) Any person responsible for paying to a non-resident, not being a company,

Finance Bill, 2015 Direct Tax Highlights

Finance Bill, 2015 Direct Tax Highlights Bansi S. Mehta & Co. All the following amendment are made effective from Assessment Years 2016-17, unless specifically mentioned otherwise. I - Residential Status,

Finance Bill, 2015 Direct Tax Highlights Bansi S. Mehta & Co. All the following amendment are made effective from Assessment Years 2016-17, unless specifically mentioned otherwise. I - Residential Status,

Foreign Collaboration

CHAPTER 17 Foreign Collaboration Some Key Points (a) The tax liability of a foreign collaborator and the Indian counter part is dependent on their residential status and the applicable provisions of DTAA,

CHAPTER 17 Foreign Collaboration Some Key Points (a) The tax liability of a foreign collaborator and the Indian counter part is dependent on their residential status and the applicable provisions of DTAA,

TAX RECKONER

TAX RECKONER 2018-19 The rates are applicable for the Financial Year 2018-19 (AY 2019-20) and subject to enactment of the Finance Bill, 2018 Note: The tax rate card will be re-visited post enactment of

TAX RECKONER 2018-19 The rates are applicable for the Financial Year 2018-19 (AY 2019-20) and subject to enactment of the Finance Bill, 2018 Note: The tax rate card will be re-visited post enactment of

DEDUCTION OF TAX AT SOURCE

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

UNION BUDGET 2018 AMENDMENTS

INCOME TAX RATES UNION BUDGET 2018 AMENDMENTS FOR INDUVIDUALS, HUF, AOP AND BOI Total Income up to 2,50,000 - NIL Total Income from 2,50,000 to 5,00,000-5% Total Income from 5,00,000 to 10,00,000-20% Total

INCOME TAX RATES UNION BUDGET 2018 AMENDMENTS FOR INDUVIDUALS, HUF, AOP AND BOI Total Income up to 2,50,000 - NIL Total Income from 2,50,000 to 5,00,000-5% Total Income from 5,00,000 to 10,00,000-20% Total

Tax-treatment and TDS, in respect of remuneration payable to an employee of an Indian Company, located abroad

Tax-treatment and TDS, in respect of remuneration payable to an employee of an Indian Company, located abroad 1 Tax-treatment and TDS, in respect of salary, bonus and incentive, receivable by the CEO of

Tax-treatment and TDS, in respect of remuneration payable to an employee of an Indian Company, located abroad 1 Tax-treatment and TDS, in respect of salary, bonus and incentive, receivable by the CEO of

DEDUCTION, COLLECTION AND RECOVERY OF TAX

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

C O N V E N T I O N BETWEEN THE SWISS FEDERAL COUNCIL AND THE GOVERNMENT OF THE KINGDOM OF SAUDI ARABIA

C O N V E N T I O N BETWEEN THE SWISS FEDERAL COUNCIL AND THE GOVERNMENT OF THE KINGDOM OF SAUDI ARABIA FOR THE AVOIDANCE OF DOUBLE TAXATION WITH RESPECT TO TAXES ON INCOME AND ON CAPITAL AND THE PREVENTION

C O N V E N T I O N BETWEEN THE SWISS FEDERAL COUNCIL AND THE GOVERNMENT OF THE KINGDOM OF SAUDI ARABIA FOR THE AVOIDANCE OF DOUBLE TAXATION WITH RESPECT TO TAXES ON INCOME AND ON CAPITAL AND THE PREVENTION

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX MATTER. Income Tax Appeal No. 1167/2011. Reserved on: 21st October, 2011

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX MATTER Income Tax Appeal No. 1167/2011 Reserved on: 21st October, 2011 Date of Decision: 8th November, 2011 The Commissioner of Income Tax Delhi-IV,

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX MATTER Income Tax Appeal No. 1167/2011 Reserved on: 21st October, 2011 Date of Decision: 8th November, 2011 The Commissioner of Income Tax Delhi-IV,

Major direct tax proposals in Finance Bill, 2017

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

Foreign Tax Credit. June 2016

Foreign Tax Credit June 2016 Table of content 1 Introduction 2 Types of Relief 3 Exemption Method 4 Credit Method 5 Double non-taxation 6 Excess FTC 7 Documentation 8 Cases where FTC not available 9 Case

Foreign Tax Credit June 2016 Table of content 1 Introduction 2 Types of Relief 3 Exemption Method 4 Credit Method 5 Double non-taxation 6 Excess FTC 7 Documentation 8 Cases where FTC not available 9 Case

Union Budget 2014 Analysis of Major Direct tax proposals

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

International Taxation

International Taxation Presentation by: CA Amit Maheshwari Partner, Ashok Maheshwary & Associates Chartered Accountants, Gurgaon (Independent Member of the Leading Edge Alliance) E-Mail : info@akmglobal.com

International Taxation Presentation by: CA Amit Maheshwari Partner, Ashok Maheshwary & Associates Chartered Accountants, Gurgaon (Independent Member of the Leading Edge Alliance) E-Mail : info@akmglobal.com

In the High Court of Judicature at Madras. Date : The Hon'ble Mr. Justice R. Sudhakar and The Honble Ms. Justice K.B.K.

In the High Court of Judicature at Madras Date : 14.07.2015 The Hon'ble Mr. Justice R. Sudhakar and The Honble Ms. Justice K.B.K. Vasuki T.C.A. No: 398 of 2007 M/s. Anusha Investments Ltd. 8 Haddows Road

In the High Court of Judicature at Madras Date : 14.07.2015 The Hon'ble Mr. Justice R. Sudhakar and The Honble Ms. Justice K.B.K. Vasuki T.C.A. No: 398 of 2007 M/s. Anusha Investments Ltd. 8 Haddows Road

Chapter 1 : Income Tax Concept and Computation of Income Tax

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

15 CA &15 CB. Presented by: CA Sheetal Mankani Partner R. C. Jain & Associates LLP. In association with: Rajeev Tahalramani

15 CA &15 CB Presented by: CA Sheetal Mankani Partner R. C. Jain & Associates LLP In association with: Rajeev Tahalramani What is Form 15CA? Form 15CA is a Declaration by Remitter and is used as a tool

15 CA &15 CB Presented by: CA Sheetal Mankani Partner R. C. Jain & Associates LLP In association with: Rajeev Tahalramani What is Form 15CA? Form 15CA is a Declaration by Remitter and is used as a tool

Notes on clauses.

52 Notes on clauses Clause 2, read with the First Schedule to the Bill, seeks to specify the rates at which income-tax is to be levied on income chargeable to tax for the assessment year 2009-2010 Further,

52 Notes on clauses Clause 2, read with the First Schedule to the Bill, seeks to specify the rates at which income-tax is to be levied on income chargeable to tax for the assessment year 2009-2010 Further,

Impact of section 206AA on the rates of TDS, particularly in respect of payments to non-residents

1 Impact of section 206AA on the rates of TDS, particularly in respect of payments to non-residents [Published in 388 ITR (Journ.) p.57 (Part-4)] By S.K. Tyagi Section 206AA was inserted in the Income-Tax

1 Impact of section 206AA on the rates of TDS, particularly in respect of payments to non-residents [Published in 388 ITR (Journ.) p.57 (Part-4)] By S.K. Tyagi Section 206AA was inserted in the Income-Tax

AGREEMENT BETWEEN THE GOVERNMENT OF MALAYSIA AND THE GOVERNMENT OF THE LEBANESE REPUBLIC FOR THE AVOIDANCE OF DOUBLE TAXATION AND

AGREEMENT BETWEEN THE GOVERNMENT OF MALAYSIA AND THE GOVERNMENT OF THE LEBANESE REPUBLIC FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME The Government

AGREEMENT BETWEEN THE GOVERNMENT OF MALAYSIA AND THE GOVERNMENT OF THE LEBANESE REPUBLIC FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME The Government

Hungary - Singapore Income Tax Treaty (1997)

") Hungary - Singapore Income Tax Treaty (1997) Status: In Force Conclusion Date: 17 April 1997. Entry into Force: 18 December 1998. Effective Date: 1 January 1999 (see Article 29). AGREEMENT BETWEEN THE

Hungary - Singapore Income Tax Treaty (1997) Status: In Force Conclusion Date: 17 April 1997. Entry into Force: 18 December 1998. Effective Date: 1 January 1999 (see Article 29). AGREEMENT BETWEEN THE

CONVENTION BETWEEN THAILAND AND JAPAN FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME

CONVENTION BETWEEN THAILAND AND JAPAN FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME Article 1 [Persons covered] This Convention shall apply to

CONVENTION BETWEEN THAILAND AND JAPAN FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME Article 1 [Persons covered] This Convention shall apply to

AGREEMENT BETWEEN THE TAIPEI REPRESENTATIVE OFFICE IN BELGIUM AND THE BELGIAN TRADE ASSOCIATION IN TAIPEI FOR THE AVOIDANCE OF DOUBLE TAXATION AND

AGREEMENT BETWEEN THE TAIPEI REPRESENTATIVE OFFICE IN BELGIUM AND THE BELGIAN TRADE ASSOCIATION IN TAIPEI FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES

AGREEMENT BETWEEN THE TAIPEI REPRESENTATIVE OFFICE IN BELGIUM AND THE BELGIAN TRADE ASSOCIATION IN TAIPEI FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES

H A R B I N G E R. B D Jokhakar & Co. Chartered Accountants October Updates on regulatory changes affecting your business

October 2014 B D Jokhakar & Co. Chartered Accountants www.bdjokhakar.com INDEX Sr. No Topics covered Page No. 1 Company Law 3 2 Reserve Bank of India 4 4 Income Tax 5 5 Service Tax 6 7 Summary of Judgments

October 2014 B D Jokhakar & Co. Chartered Accountants www.bdjokhakar.com INDEX Sr. No Topics covered Page No. 1 Company Law 3 2 Reserve Bank of India 4 4 Income Tax 5 5 Service Tax 6 7 Summary of Judgments

Taxation of Expatriates Issues which can be considered for taxation of Expatriates: - Residential Status. - Taxation of salary, perquisites, amenities

SIRC of ICAI Tirupur Branch Taxation of Expatriates 9 th February, 2008 Naresh Ajwani Partner Rashmin Sanghvi & Associates Chartered Accountants Taxation of Expatriates Issues which can be considered for

SIRC of ICAI Tirupur Branch Taxation of Expatriates 9 th February, 2008 Naresh Ajwani Partner Rashmin Sanghvi & Associates Chartered Accountants Taxation of Expatriates Issues which can be considered for

CONVENTION BETWEEN IRELAND AND THE REPUBLIC OF GHANA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES

CONVENTION BETWEEN IRELAND AND THE REPUBLIC OF GHANA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME AND CAPITAL GAINS The Government of Ireland

CONVENTION BETWEEN IRELAND AND THE REPUBLIC OF GHANA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME AND CAPITAL GAINS The Government of Ireland

TDS Seminar for Residents Welfare Associations

TDS Seminar for Residents Welfare Associations 27 th July 2018 What is TDS? Mode of quick and efficient collection of taxes Tax deducted at the point of generation of income Tax deducted by the payer &

TDS Seminar for Residents Welfare Associations 27 th July 2018 What is TDS? Mode of quick and efficient collection of taxes Tax deducted at the point of generation of income Tax deducted by the payer &

Cyprus South Africa Tax Treaties

Cyprus South Africa Tax Treaties AGREEMENT OF 26 TH NOVEMBER, 1997 This is the Agreement between the Government of the Republic of Cyprus and the Government of the Republic of South Africa for the avoidance

Cyprus South Africa Tax Treaties AGREEMENT OF 26 TH NOVEMBER, 1997 This is the Agreement between the Government of the Republic of Cyprus and the Government of the Republic of South Africa for the avoidance

2005 Income and Capital Gains Tax Convention and Notes

2005 Income and Capital Gains Tax Convention and Notes Treaty Partners: Botswana; United Kingdom Signed: September 9, 2005 In Force: September 4, 2006 Effective: In Botswana, from July 1, 2007. In the

2005 Income and Capital Gains Tax Convention and Notes Treaty Partners: Botswana; United Kingdom Signed: September 9, 2005 In Force: September 4, 2006 Effective: In Botswana, from July 1, 2007. In the

The Government of Ireland and the Government of the Republic of Croatia

Agreement between the Government of Ireland and the Government of the Republic of Croatia for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income and on

Agreement between the Government of Ireland and the Government of the Republic of Croatia for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income and on

E-TDS FILING PRESENTED BY. Vinod Kumar Jain FCA

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

thousand rupees of the total income but without being liable to tax], only for the purpose of charging income-tax in respect of the total income; and

![thousand rupees of the total income but without being liable to tax], only for the purpose of charging income-tax in respect of the total income; and](/thumbs/74/69854896.jpg "thousand rupees of the total income but without being liable to tax], only for the purpose of charging income-tax in respect of the total income; and") ACT FINANCE ACT *Finance Act, 2011 [8 OF 2011] An Act to give effect to the financial proposals of the Central Government for the financial year 2011-2012. BE it enacted by Parliament in the Sixty-second

ACT FINANCE ACT *Finance Act, 2011 [8 OF 2011] An Act to give effect to the financial proposals of the Central Government for the financial year 2011-2012. BE it enacted by Parliament in the Sixty-second

The Swiss Federal Council and the Government of the Hong Kong Special Administrative Region of the People s Republic of China,

AGREEMENT BETWEEN THE SWISS FEDERAL COUNCIL AND THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE S REPUBLIC OF CHINA FOR THE AVOIDANCE OF DOUBLE TAXATION WITH RESPECT TO TAXES

AGREEMENT BETWEEN THE SWISS FEDERAL COUNCIL AND THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE S REPUBLIC OF CHINA FOR THE AVOIDANCE OF DOUBLE TAXATION WITH RESPECT TO TAXES

Desiring to conclude an Agreement for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income,

AGREEMENT BETWEEN THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE S REPUBLIC OF CHINA AND THE GOVERNMENT OF THE SOCIALIST REPUBLIC OF VIETNAM FOR THE AVOIDANCE OF DOUBLE TAXATION

AGREEMENT BETWEEN THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE S REPUBLIC OF CHINA AND THE GOVERNMENT OF THE SOCIALIST REPUBLIC OF VIETNAM FOR THE AVOIDANCE OF DOUBLE TAXATION

AGREEMENT BETWEEN THE GOVERNMENT OF THE KINGDOM OF THAILAND AND THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE

AGREEMENT BETWEEN THE GOVERNMENT OF THE KINGDOM OF THAILAND AND THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE S REPUBLIC OF CHINA FOR THE AVOIDANCE OF DOUBLE TAXATION AND

AGREEMENT BETWEEN THE GOVERNMENT OF THE KINGDOM OF THAILAND AND THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE S REPUBLIC OF CHINA FOR THE AVOIDANCE OF DOUBLE TAXATION AND

Income Computation and Disclosure Standards. CA Parul Mittal

Income Computation and Disclosure Standards CA Parul Mittal ICDS Overview In Finance Act 2014, vide amendment made in section 145(2), power granted to Central Government to notify income computation and

Income Computation and Disclosure Standards CA Parul Mittal ICDS Overview In Finance Act 2014, vide amendment made in section 145(2), power granted to Central Government to notify income computation and

GOVERNMENT NOTICE SOUTH AFRICAN REVENUE SERVICE INCOME TAX ACT, 1962

GOVERNMENT NOTICE SOUTH AFRICAN REVENUE SERVICE No. 391 18 May 2007 INCOME TAX ACT, 1962 CONVENTION BETWEEN THE GOVERNMENT OF THE REPUBLIC OF SOUTH AFRICA AND THE GOVERNMENT OF THE REPUBLIC OF GHANA FOR

GOVERNMENT NOTICE SOUTH AFRICAN REVENUE SERVICE No. 391 18 May 2007 INCOME TAX ACT, 1962 CONVENTION BETWEEN THE GOVERNMENT OF THE REPUBLIC OF SOUTH AFRICA AND THE GOVERNMENT OF THE REPUBLIC OF GHANA FOR

Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria

![Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria](/thumbs/90/101594279.jpg "Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria") Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria Key Amendments to Form 3CD. The Central Board of Direct Taxes (CBDT) via Notification No. 33/2018 dated 20th July, 2018 has

Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria Key Amendments to Form 3CD. The Central Board of Direct Taxes (CBDT) via Notification No. 33/2018 dated 20th July, 2018 has

Who can use this form Who cannot use this form Mode of filing. Individuals whose total income includes:

INCOME TAX: Central Board of Direct Taxes (CBDT) has notified the rules for filing incometax returns for the Assessment Year (AY) 2013-14: Income Tax Service Tax Central Excise Customs FEMA ITR Form Who

INCOME TAX: Central Board of Direct Taxes (CBDT) has notified the rules for filing incometax returns for the Assessment Year (AY) 2013-14: Income Tax Service Tax Central Excise Customs FEMA ITR Form Who

NOTIFICATION NO.35/2014 [F.NO.503/11/2005 FTD II], DATED

![NOTIFICATION NO.35/2014 [F.NO.503/11/2005 FTD II], DATED](/thumbs/89/97683347.jpg "NOTIFICATION NO.35/2014 [F.NO.503/11/2005 FTD II], DATED") SECTION 90 OF THE INCOME TAX ACT, 1961 DOUBLE TAXATION AGREEMENT AGREEMENT FOR AVOIDANCE OF DOUBLE TAXATION AND PREVENTION OF FISCAL EVASION WITH FOREIGN COUNTRIES FIJI NOTIFICATION NO.35/2014 [F.NO.503/11/2005

SECTION 90 OF THE INCOME TAX ACT, 1961 DOUBLE TAXATION AGREEMENT AGREEMENT FOR AVOIDANCE OF DOUBLE TAXATION AND PREVENTION OF FISCAL EVASION WITH FOREIGN COUNTRIES FIJI NOTIFICATION NO.35/2014 [F.NO.503/11/2005

CONVENTION BETWEEN THE GOVERNMENT OF IRELAND AND THE GOVERNMENT OF THE KINGDOM OF THAILAND FOR THE AVOIDANCE OF DOUBLE TAXATION AND

CONVENTION BETWEEN THE GOVERNMENT OF IRELAND AND THE GOVERNMENT OF THE KINGDOM OF THAILAND FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME AND

CONVENTION BETWEEN THE GOVERNMENT OF IRELAND AND THE GOVERNMENT OF THE KINGDOM OF THAILAND FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME AND

CONVENTION BETWEEN THE GOVERNMENT OF THE REPUBLIC OF ESTONIA AND THE GOVERNMENT OF TURKMENISTAN FOR THE AVOIDANCE OF DOUBLE TAXATION AND

CONVENTION BETWEEN THE GOVERNMENT OF THE REPUBLIC OF ESTONIA AND THE GOVERNMENT OF TURKMENISTAN FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME

CONVENTION BETWEEN THE GOVERNMENT OF THE REPUBLIC OF ESTONIA AND THE GOVERNMENT OF TURKMENISTAN FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME

2005 Income and Capital Gains Tax Convention

2005 Income and Capital Gains Tax Convention Treaty Partners: Barbados; Botswana Signed: February 23, 2005 In Force: August 25, 2005 Effective: In Barbados, from January 1, 2006. In Botswana, from July

2005 Income and Capital Gains Tax Convention Treaty Partners: Barbados; Botswana Signed: February 23, 2005 In Force: August 25, 2005 Effective: In Barbados, from January 1, 2006. In Botswana, from July

AGREEMENT OF 28 TH MAY, Moldova

AGREEMENT OF 28 TH MAY, 2009 Moldova CONVENTION BETWEEN IRELAND AND THE REPUBLIC OF MOLDOVA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME Ireland

AGREEMENT OF 28 TH MAY, 2009 Moldova CONVENTION BETWEEN IRELAND AND THE REPUBLIC OF MOLDOVA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME Ireland

Date of Conclusion: 6 October Entry into Force: 18 February 2000.

AGREEMENT BETWEEN THE GOVERNMENT OF THE REPUBLIC OF SINGAPORE AND THE GOVERNMENT OF THE REPUBLIC OF LATVIA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES

AGREEMENT BETWEEN THE GOVERNMENT OF THE REPUBLIC OF SINGAPORE AND THE GOVERNMENT OF THE REPUBLIC OF LATVIA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES

OECD Model Tax Convention on Income and Capital An overview. CA Vishal Palwe, 3 July 2015

OECD Model Tax Convention on Income and Capital An overview CA Vishal Palwe, 3 July 2015 1 Contents Overview of double taxation 3 Basics of tax treaty 6 Domestic law and tax treaty 11 Key provisions of

OECD Model Tax Convention on Income and Capital An overview CA Vishal Palwe, 3 July 2015 1 Contents Overview of double taxation 3 Basics of tax treaty 6 Domestic law and tax treaty 11 Key provisions of

Cyprus Bulgaria Tax Treaties

Cyprus Bulgaria Tax Treaties AGREEMENT OF 30 TH OCTOBER, 2000 This is the Convention between the Republic of Cyprus and the Republic of Bulgaria for the avoidance of double taxation with respect to taxes

Cyprus Bulgaria Tax Treaties AGREEMENT OF 30 TH OCTOBER, 2000 This is the Convention between the Republic of Cyprus and the Republic of Bulgaria for the avoidance of double taxation with respect to taxes

2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed

![2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed](/thumbs/84/90875315.jpg "2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed") 2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

EXECUTIVE SUMMARY FEMA Regulations

Doha Chapter of ICAI 5 th January 2014 Relevant Changes in FEMA regulations and Direct & Indirect Taxation affecting Real Estate Transactions, with reference to NRI by CA R.BUPATHY PAST PRESIDENT - ICAI

Doha Chapter of ICAI 5 th January 2014 Relevant Changes in FEMA regulations and Direct & Indirect Taxation affecting Real Estate Transactions, with reference to NRI by CA R.BUPATHY PAST PRESIDENT - ICAI

MINISTRY OF LAW AND JUSTICE (Legislative Department)

") MINISTRY OF LAW AND JUSTICE (Legislative Department) New Delhi, the 28th May, 2012/Jyaistha 7, 1934 (Saka) The following Act of Parliament received the assent of the President on the 28th May, 2012 and

MINISTRY OF LAW AND JUSTICE (Legislative Department) New Delhi, the 28th May, 2012/Jyaistha 7, 1934 (Saka) The following Act of Parliament received the assent of the President on the 28th May, 2012 and

SAMVIT ACADEMY IPCC MOCK EXAM

Disclaimer (Read carefully) SUGGESTED ANSWERS - Group 1 Taxation (Code GST) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working notes, notes

Disclaimer (Read carefully) SUGGESTED ANSWERS - Group 1 Taxation (Code GST) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working notes, notes

IMPORTANT AMENDMENTS OF THE FINANCE ACT, /6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi

IMPORTANT AMENDMENTS OF THE FINANCE ACT,2010 22/6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi 1 TAX RATES AND SLABS OF INCOME TAX RATES FOR INDIVIDUAL,HUF,AOP & BOI, ARTIFICIAL JUDICIAL PERSON U/S

IMPORTANT AMENDMENTS OF THE FINANCE ACT,2010 22/6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi 1 TAX RATES AND SLABS OF INCOME TAX RATES FOR INDIVIDUAL,HUF,AOP & BOI, ARTIFICIAL JUDICIAL PERSON U/S

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment Year 2014-15 - SIPOY SATISH Highlights of Change in Direct Taxes in the Union Budget 2013 1. Rate of Income Tax for Individual a) Slab Rate Assessment