Property Taxes: Revenue Impact and Taxable Value Updates. MSBO Annual Conference April 19, 2018

|

|

|

- Griselda Beverley Shelton

- 5 years ago

- Views:

Transcription

1 Property Taxes: Revenue Impact and Taxable Value Updates MSBO Annual Conference April 19,

2 State Aid Formula State Revenue = Foundation Allowance X Pupil Membership Local Revenue 2

3 State Aid Formula Local Revenue = (Taxable Value minus Captured Assessed Value of Property) multiplied by School Operating Millage Note: At least 2 categories of property at different millage rates 3

4 Terminology: Non-Principal Residence (Nonhomestead) Property Non-principal residence property is considered to be second homes, business property, and rental housing. Non-principal residence property is subject to the local school operating millage, except for industrial personal property that is exempt and except for commercial personal property that is exempt from the first 12 mills. 4

5 State Aid Formula Non-PRE Taxable values: Tax years Non-PRE values only 18 operating mills Tax years 2008-present All Other (Non-PRE) 18 operating mills Commercial Personal Property 6 operating mills

6 State Aid Formula School Operating Millage (non-pre) = the lesser of 18 Mills or what the district levied in 1993 (FY 1994) Note: State Aid calculation assumes maximum allowable millage is levied. Per Section 20(4), no allowance is made for Millage Reduction Fractions. 6

7 State Aid Formula State Aid Per Pupil (StatePP) = Per Pupil Foundation Grant minus (Local Revenue divided by General Ed. Membership) General Ed. State Revenue under Section 20 = State Aid Per Pupil x General Pupil Count + Section 20(5) adjustment for nonresident pupils 7

8 State Aid Formula As taxable values increase, state aid payments decrease As taxable values decrease, state aid payments increase This SHOULD be automatic, but it requires active participation of your county treasurer s office Pay special attention to Capture row 8

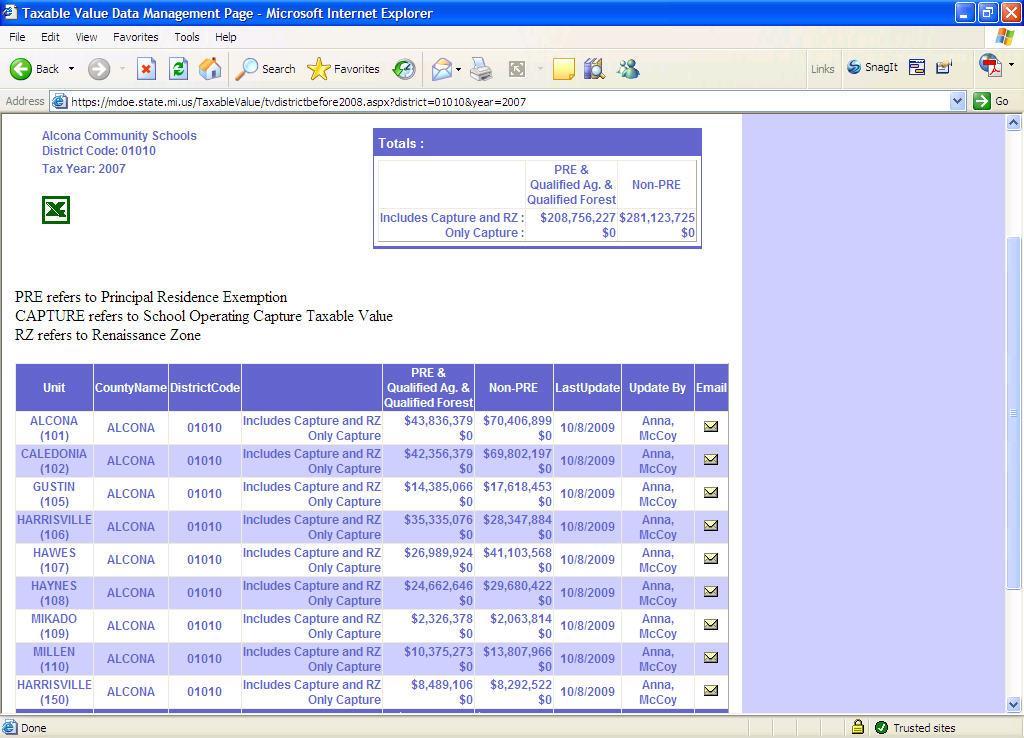

9 Taxable Valuation Collection Process Taxable Value collection is web-based Input no longer limited by old schedule Old schedule now a minimum guideline Initial values September 1 Revisions as of settlement May 1 Revisions after settlement October 20 Greater availability for school districts Improved oversight from State agencies 9

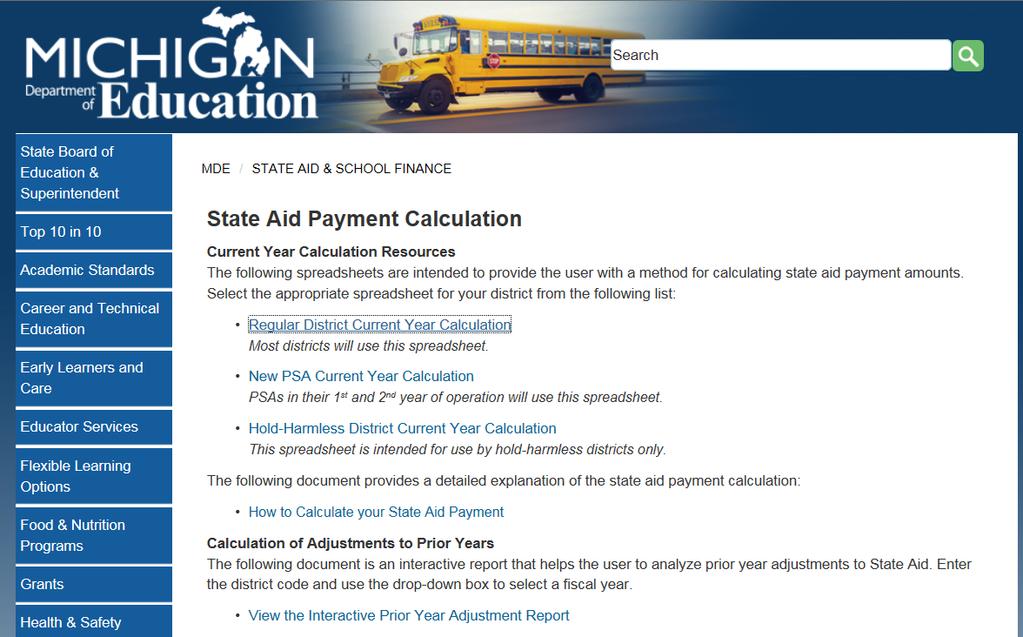

10 Taxable Valuation Collection Process Tax Years values PRE Includes Capture and RZ Non-PRE Includes Capture and RZ PRE Capture Only Non-PRE Capture Only All 4 values are totaled above Data can be downloaded as Excel file 10

11

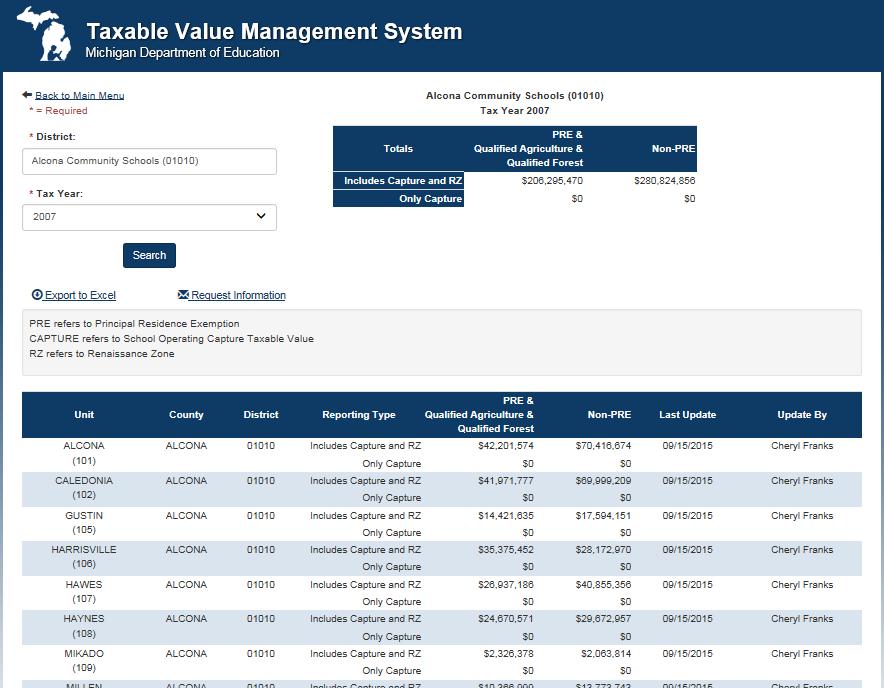

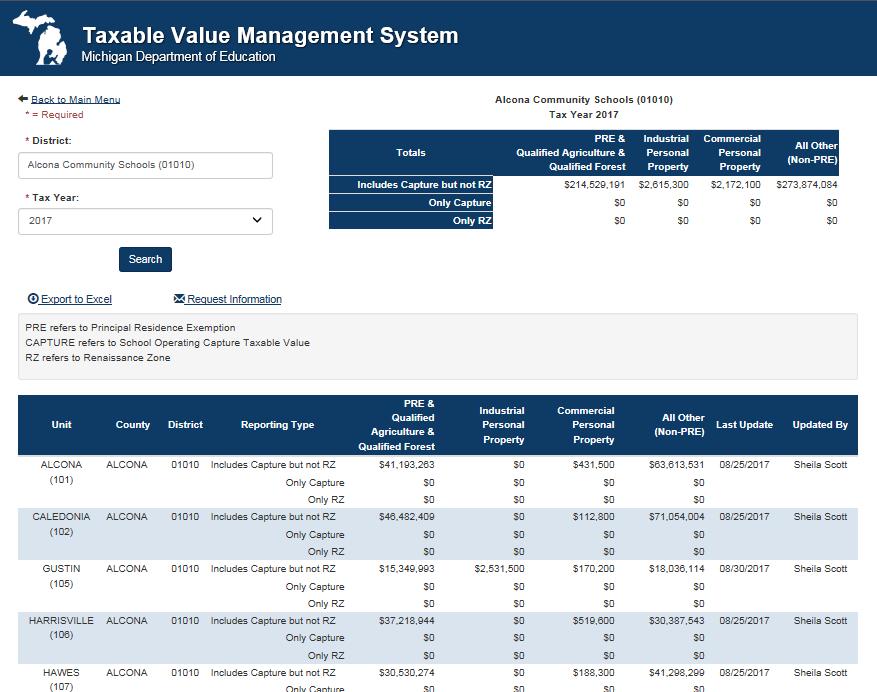

12 Taxable Valuation Collection Process Tax years 2008 present 4 columns for classes of property Row for taxable value of unit, less RZ Row for value of unit captured by local authority Row for Renaissance Zone property value of unit All 12 values totaled at top of page Data can be downloaded as Excel file

13

14 14

15 15

16 Reconciliation tools 16

17 Current Year Calculation 17

18 How To document 18

19 Prior Year Adjustment Report 19

20 Prior Year Adjustment Report 20

21 Prior Year Adjustment Report 21

22 Prior Year Adjustment Report 22

23 Prior Year Adjustment Report 23

24 Prior Year Adjustment Report 24

25 Taxable Valuation Management Tips Try to stay current Gather baseline information annually (mid-august) Becomes comparison tool for October 20 th prior year changes and May 1 st current year changes Check for specifics before contacting county Tax year Unit Which column Which row Specific questions lead to specific answers 25

26 Section 31A At-Risk Eligibility in the Hold-Harmless district Proposal A held harmless districts with foundations above $6500 in May levy mills against PRE properties to achieve full foundation. Levying Hold Harmless mills does not always maximize per-pupil revenue. Most do not qualify for 100% At-Risk funding through section 31A 26

27 Maintaining 100% 31A Eligibility Hold Harmless Eligibiliy Saugatuck Membership Basic Foundation $ 8, District Foundation $ 8, Local Revenue per GE $ 6, Sect. 20 State Per Pupil $ 1, PRE Property Value: $ 241,123, HH Mills: 1.22 HH revenue max: $ 294, HH revenue max per pupil: $ "Total per pupil": $ 8, Actual per pupil: $ 8, Is Eligible? NO At-risk count

28 Maintaining 100% 31A Eligibility Hold Harmless Eligibility River Rouge Membership 1, Basic Foundation $ 8, District Foundation $ 8, Local Revenue per GE $ 2, Sect. 20 State Per Pupil $ 5, PRE Property Value: $ 35,059, HH Mills: 2.5 HH revenue max: $ 87, HH revenue max per pupil: $ "Total per pupil": $ 7, Actual per pupil: $ 7, Is Eligible? YES At-risk count 1, A funding $ 1,184, A per pupil $

29 Maintaining 100% 31A Eligibility 31A At-Risk funding can exceed revenue from Hold Harmless Levy Beginning in FY % eligibility for districts with combined state and local section 20/20m revenue above basic foundation. FY 18 31A allocation = $499,000, FY 19 Executive Budget 31A = $499,000,

30 Taxable Value / State Aid Shortcuts Taxable Value Management System: State Aid Home Page: State Aid Calculation Page: _ ,00.html State School Aid Act: mcl-act-94-of-1979.pdf 30

31 Ad Valorem Property Tax Millage Levies, K-12 Millage Supplemental Hold Harmless Taxable Value Base PRE and Qual. Ag./Forest in the local school district Lesser of Annual School Code Limit Millage and the 1994 Certified Millage, as permanently reduced, times the current year millage reduction fraction for all property. (Letter ) 31

32 Exemption & Specific Taxation Programs Hold Harmless School Districts Because industrial and commercial personal property are treated like PRE and Ag property, hold harmless millage rates are levied on industrial and commercial personal property. Commercial personal property is only exempt from 12 school operating mills. It is only subjected to the first 12 hold harmless mills. 32

33 Hold-Harmless Mills When foundation allowance increases by more than inflation, hold-harmless districts must reduce their millage rate to limit state/local increase to inflation. To allow hold-harmless districts to receive full dollar increase in foundation allowance, their foundation increases were limited to inflation. Sec.20j payments were ended after FY 2011 and replaced by sec. 20m payments beginning for FY

34 Limits on Ad Valorem Property Tax Millage Levies, ISD 1. Allocated Operating Levy--150% of what was authorized in Special Education--175% of what was authorized in Vocational Education greater of 150% of what was authorized in 1993 or 1 mill. 4. Enhancement 3 mills 34

35 Distribution of Specific Taxes For industrial facilities tax, commercial facilities tax, technology park tax, commercial forest tax, MSHDA payments, neighborhood enterprise zone tax, obsolete properties tax, commercial rehabilitation act and ETRPST: the local school operating share is paid to the school aid fund. 35

36 Distribution of Specific Taxes (Continued) local school districts keep the share attributable to debt and sinking fund mills. for the MSHDA PILOT, technology park tax, commercial forest tax, and NEZ tax, the local school operating share of the specific taxes is calculated using the district s 1993 operating millage rate less 6 mills. for IFT, commercial facilities tax, OPRA, commercial rehabilitation tax and the ETRPST, the local school operating share of the specific taxes is calculated using the district s current operating millage rate. 36

37 Specific Taxes Distribution of ISD Special Ed. And Voc. Ed. mills For IFT, NEZ, OPRA, Commercial Facilities Tax, Commercial Forest Tax, and Commercial Rehabilitation Tax and ETRPST only: the share of the tax attributable to ISD special ed. mills is paid to the school aid fund if the ISD receives special ed. millage equalization funding under section 56 (ICD 450). the share of the tax attributable to ISD voc. ed. mills is paid to the school aid fund if the ISD receives voc. ed. millage equalization funding under section 62 (ICD 510). Otherwise, the ISD share of specific taxes is paid to the ISD. 37

38 MICHIGAN RENAISSANCE ZONE ACT A tax liability exemption enacted under PA 376 of 1996 Properties located in the zone are still listed on the local unit assessment roll An assessment and taxable value are established for the levy of non-operating millage rates Exempts property taxes except for debt, sinking fund, and ISD enhancement mills Schools districts and ISDs reimbursed through Sec 26a of the School Aid Act. Payment based on RZ TVs reported to Treasury by local assessors, not RZ TVs reported to MDE. 38

39 Tax Increment Financing Downtown Development Authorities (DDA) PA 197 of 1975 Tax Increment Financing Authorities (TIFA) PA 450 of 1980 Local Development Finance Authorities (LDFA) PA 281 of 1986 Brownfield Redevelopment Finance Authorities PA 381 of

40 Tax Increment Financing Allows authority to capture property taxes from incremental increase in value and spend money to develop area or finance specific project. Used for local economic development. Method to finance different types of projects ranging from commercial development to neighborhood revitalization. Appeals to communities by providing funds for economic development without levying more taxes and has the potential to increase the tax base. Redirecting of other property tax revenues to TIF plan may adversely affect other governmental units. 40

41 Tax Increment Financing Property Value in Current Year $15,000,000 Property Value in Initial Year $10,000,000 Captured Value $5,000,000 Tax Rate - 50 Mills Tax Increment $250,000 School Operating Impact: 5,000,000 x 18 mills = School Operating Portion - $90,000 41

42 Tax Increment Financing DDA and TIFA Acts: May capture debt taxes or may exclude them. LDFA and BRF Acts: May not capture debt mills. 42

43 Tax Increment Financing DDA, TIFA, and LDF plans may only capture school taxes for obligations issued or incurred before 1995, except for: LDF smart zones that can capture 1/2 of school taxes for up to 15 years Other minor exceptions BRF may capture school taxes to pay for: certain site investigations, baseline environmental assessment reports, and due care plans. - Other clean-up costs, with DEQ approval Infrastructure costs, with MSF approval 43

44 New Tax Increment Financing Laws No School Tax Capture, except as noted Historical Neighborhood TIF Authority Act 2004 PA 530 Corridor Improvement Authority Act *** 2005 PA 280 Neighborhood Improvement Authority Act 2007 PA 61 Water Resource Improvement TIF Authority Act 2008 PA 94 Nonprofit Street Railway Act 1867 PA 35 Am. By 2008 PA 486, added Transit Operations Finance Zone *** (May Capture School Taxes with approval of Michigan Strategic Fund) 44

45 Calculate Your Foundation Foundation per pupil $7,693 x Number of students 3, = Foundation Total _27,310,

46 State Source Expected Gross Foundation_ 27,310, Less Local Property Tax Revenue 4,332, Total Expected State Aid _22,978,044.65_ 46

47 Remember. There is no such thing as extra revenue with this formula or reconciliation. If you have collected more than your foundation calculation, it is not your money, so do not book it as revenue you owe somebody and eventually they will figure out you owe it and come take it back! 47

48 UNDERSTANDING THE BASICS OF ASSESSING FOR LOCAL UNIT OFFICIALS A free one day course 12 sessions scheduled throughout Michigan, April August _ ,00.html 48

49 Contact Info Howard Heideman Michigan Department of Treasury Phil Boone Michigan Department of Education (517)

Property Tax Advanced Seminar

Property Tax Advanced Seminar February 27, 2013 MELG Building Webinar 1 Need Help? o Click on link to check your system http://www.elluminate.com/support/index.jsp o If you are experiencing trouble, please

Property Tax Advanced Seminar February 27, 2013 MELG Building Webinar 1 Need Help? o Click on link to check your system http://www.elluminate.com/support/index.jsp o If you are experiencing trouble, please

Property Tax Hands-on Workshop

Property Tax Hands-on Workshop July 17, 2018 1 Why? 1 Dexter Community Schools 2016-17 Foundation Allowance $7,799 x 3,582.17 students* = $27,937,344** * Blended student counts 10% Feb 2016 and 90% Oct

Property Tax Hands-on Workshop July 17, 2018 1 Why? 1 Dexter Community Schools 2016-17 Foundation Allowance $7,799 x 3,582.17 students* = $27,937,344** * Blended student counts 10% Feb 2016 and 90% Oct

Property Tax Overview Seminar

Property Tax Overview Seminar February 23, 2017 MELG Building, Lansing/Webinar 1 Technical Questions? Click on link to check your system http://support.blackboardcollaborate.com Contact Tech Support -

Property Tax Overview Seminar February 23, 2017 MELG Building, Lansing/Webinar 1 Technical Questions? Click on link to check your system http://support.blackboardcollaborate.com Contact Tech Support -

The 4410: Taxable Values and the Local School District. Phil Boone February 8, 2016 Office of State Aid and School Finance

The 4410: Taxable Values and the Local School District Phil Boone February 8, 2016 Office of State Aid and School Finance State Aid Funding Per pupil funding is a set amount for the district ($7000 - $8000

The 4410: Taxable Values and the Local School District Phil Boone February 8, 2016 Office of State Aid and School Finance State Aid Funding Per pupil funding is a set amount for the district ($7000 - $8000

The 4410: Taxable Values and the Local School District. Phil Boone August 7, 2017 Office of State Aid and School Finance

The 4410: Taxable Values and the Local School District Phil Boone August 7, 2017 Office of State Aid and School Finance State Aid Funding Per pupil foundation funding is a set amount for the district ($7611

The 4410: Taxable Values and the Local School District Phil Boone August 7, 2017 Office of State Aid and School Finance State Aid Funding Per pupil foundation funding is a set amount for the district ($7611

PERSONAL PROPERTY TAX REIMBURSEMENTS UPDATE

PERSONAL PROPERTY TAX REIMBURSEMENTS UPDATE PRESENTERS: HOWARD HEIDEMAN, CARRIE KOLKA, AND ANDREW LOCKWOOD, MICHIGAN DEPARTMENT OF TREASURY PERSONAL PROPERTY TAX LEGISLATION In 2012, legislation was passed

PERSONAL PROPERTY TAX REIMBURSEMENTS UPDATE PRESENTERS: HOWARD HEIDEMAN, CARRIE KOLKA, AND ANDREW LOCKWOOD, MICHIGAN DEPARTMENT OF TREASURY PERSONAL PROPERTY TAX LEGISLATION In 2012, legislation was passed

Tax Increment Financing TIF Presented to the Leelanau County Brownfield Redevelopment Authority

Tax Increment Financing TIF Presented to the Leelanau County Brownfield Redevelopment Authority Presented by Envirologic Technologies, Inc. October 28, 2008 What is Tax Increment Financing? Use of ad valorem

Tax Increment Financing TIF Presented to the Leelanau County Brownfield Redevelopment Authority Presented by Envirologic Technologies, Inc. October 28, 2008 What is Tax Increment Financing? Use of ad valorem

Dianne Easterling, Coordinator Michigan Department of Education Office of Special Education October, 2017

Dianne Easterling, Coordinator Michigan Department of Education Office of Special Education October, 2017 Local Funds Non homestead property taxes (18 mills) ISD special education millage (Act 18) Federal

Dianne Easterling, Coordinator Michigan Department of Education Office of Special Education October, 2017 Local Funds Non homestead property taxes (18 mills) ISD special education millage (Act 18) Federal

SUBJECT: Property Tax and Equalization Calendar for 2019 STATE TAX COMMISSION 2019 PROPERTY TAX, COLLECTIONS AND EQUALIZATION CALENDAR

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER Bulletin No. 17 of 2018 October 22, 2018 Property Tax and Equalization Calendar for

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER Bulletin No. 17 of 2018 October 22, 2018 Property Tax and Equalization Calendar for

AMENDMENT TO THE MONTCALM COUNTY BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE 107 S LAFAYETTE, LLC REDEVELOPMENT PROJECT

AMENDMENT TO THE MONTCALM COUNTY BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE 107 S LAFAYETTE, LLC REDEVELOPMENT PROJECT January 30, 2017 Introduction 107 S Lafayette, LLC ("107 S Lafayette")

AMENDMENT TO THE MONTCALM COUNTY BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE 107 S LAFAYETTE, LLC REDEVELOPMENT PROJECT January 30, 2017 Introduction 107 S Lafayette, LLC ("107 S Lafayette")

The Basics of School Funding. Kathryn Summers, Associate Director Senate Fiscal Agency July 2015

The Basics of School Funding Kathryn Summers, Associate Director Senate Fiscal Agency www.senate.michigan.gov/sfa July 2015 School Finance How are Local School Districts Financed? Three Primary Sources

The Basics of School Funding Kathryn Summers, Associate Director Senate Fiscal Agency www.senate.michigan.gov/sfa July 2015 School Finance How are Local School Districts Financed? Three Primary Sources

The Basics of School Funding. Kathryn Summers, Chief Analyst Senate Fiscal Agency

The Basics of School Funding Kathryn Summers, Chief Analyst Senate Fiscal Agency www.senate.michigan.gov/sfa School Finance How are Local School Districts Financed? Three Primary Sources Local Taxation

The Basics of School Funding Kathryn Summers, Chief Analyst Senate Fiscal Agency www.senate.michigan.gov/sfa School Finance How are Local School Districts Financed? Three Primary Sources Local Taxation

STATE TAX COMMISSION 2018 PROPERTY TAX, COLLECTIONS AND EQUALIZATION CALENDAR

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER TO: FROM: Equalization Directors and Assessors The State Tax Commission Bulletin No.

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER TO: FROM: Equalization Directors and Assessors The State Tax Commission Bulletin No.

Guide To Your Property Taxes And Proposal A

Guide To Your Property Taxes And Proposal A PROPOSAL A : WHAT ARE PROPERTY TAXES BASED ON? Prior to 1995, your taxes were calculated on SEV (State Equalized Value). SEV is the Assessed Value of the property

Guide To Your Property Taxes And Proposal A PROPOSAL A : WHAT ARE PROPERTY TAXES BASED ON? Prior to 1995, your taxes were calculated on SEV (State Equalized Value). SEV is the Assessed Value of the property

MICHIGAN MUNICIPAL LEAGUE 2015 CAPITAL CONFERENCE

MICHIGAN MUNICIPAL LEAGUE 2015 CAPITAL CONFERENCE Moving Forward in the Wake of PPT Reform Scott Smith, Member General outline Policy conference, so policy, not generally nuts & bolts, is focus. Want to

MICHIGAN MUNICIPAL LEAGUE 2015 CAPITAL CONFERENCE Moving Forward in the Wake of PPT Reform Scott Smith, Member General outline Policy conference, so policy, not generally nuts & bolts, is focus. Want to

2010 FINANCIAL OVERVIEW Kent County, Michigan

2010 FINANCIAL OVERVIEW Kent County, Michigan Daryl J. Delabbio County Administrator/Controller Stephen W. Duarte Fiscal Services Director OFFICE OF THE ADMINISTRATOR Kent County Administration Building

2010 FINANCIAL OVERVIEW Kent County, Michigan Daryl J. Delabbio County Administrator/Controller Stephen W. Duarte Fiscal Services Director OFFICE OF THE ADMINISTRATOR Kent County Administration Building

Updated 5/17/2018 8:30 AM Oakland County Official Proposal List August 7, 2018 Primary Election

Oakland County Official Proposal List August 7, 2018 Primary Election Proposal Section Authority Oakland County Public Transportation Millage Renewal If approved, this proposal will renew and increase

Oakland County Official Proposal List August 7, 2018 Primary Election Proposal Section Authority Oakland County Public Transportation Millage Renewal If approved, this proposal will renew and increase

MICHIGAN RENAISSANCE ZONE ACT Act 376 of 1996

Act 376 of 1996 AN ACT to create and expand certain renaissance zones; to foster economic opportunities in this state; to facilitate economic development; to stimulate industrial, commercial, and residential

Act 376 of 1996 AN ACT to create and expand certain renaissance zones; to foster economic opportunities in this state; to facilitate economic development; to stimulate industrial, commercial, and residential

BROWNFIELD REDEVELOPMENT FINANCING ACT Act 381 of The People of the State of Michigan enact:

BROWNFIELD REDEVELOPMENT FINANCING ACT Act 381 of 1996 AN ACT to authorize municipalities to create a brownfield redevelopment authority to facilitate the implementation of brownfield plans; to create

BROWNFIELD REDEVELOPMENT FINANCING ACT Act 381 of 1996 AN ACT to authorize municipalities to create a brownfield redevelopment authority to facilitate the implementation of brownfield plans; to create

CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE ALBERT KAHN BUILDING REDEVELOPMENT PROJECT

EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE ALBERT KAHN BUILDING REDEVELOPMENT PROJECT Prepared by: Richard A. Barr, Esq. Honigman LLP 660 Woodward Avenue, Ste.

EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE ALBERT KAHN BUILDING REDEVELOPMENT PROJECT Prepared by: Richard A. Barr, Esq. Honigman LLP 660 Woodward Avenue, Ste.

MISSISSIPPI ADEQUATE EDUCATION PROGRAM (MAEP) AN OVERVIEW OF HOW THE FORMULA IS CALCULATED

AN OVERVIEW OF HOW THE FORMULA IS CALCULATED") MISSISSIPPI ADEQUATE EDUCATION PROGRAM (MAEP) AN OVERVIEW OF HOW THE FORMULA IS CALCULATED What is MAEP? The formula established by the Legislature to provide adequate operation funding levels for each

MISSISSIPPI ADEQUATE EDUCATION PROGRAM (MAEP) AN OVERVIEW OF HOW THE FORMULA IS CALCULATED What is MAEP? The formula established by the Legislature to provide adequate operation funding levels for each

Bulletin 16 of 2017 Inflation Rate Multiplier October 30, 2017

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER TO: FROM: Assessors and Equalization Directors State Tax Commission Bulletin 16 of

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER TO: FROM: Assessors and Equalization Directors State Tax Commission Bulletin 16 of

BROWNFIELD PLAN Water Street Redevelopment Area E Michigan Avenue City of Ypsilanti, Michigan

WASHTENAW COUNTY BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN Water Street Redevelopment Area 1-216 E Michigan Avenue City of Ypsilanti, Michigan PREPARED BY Washtenaw County Brownfield Redevelopment

WASHTENAW COUNTY BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN Water Street Redevelopment Area 1-216 E Michigan Avenue City of Ypsilanti, Michigan PREPARED BY Washtenaw County Brownfield Redevelopment

TRANSFORMATIONAL BROWNFIELD PLAN PROGRAM GUIDELINES

TRANSFORMATIONAL BROWNFIELD PLAN PROGRAM GUIDELINES PROGRAM OVERVIEW The Brownfield Redevelopment Financing Act, 1996 Public Act (PA) 381, as amended (Act 381), effective July 24, 2017, incorporates Transformational

TRANSFORMATIONAL BROWNFIELD PLAN PROGRAM GUIDELINES PROGRAM OVERVIEW The Brownfield Redevelopment Financing Act, 1996 Public Act (PA) 381, as amended (Act 381), effective July 24, 2017, incorporates Transformational

CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE 640 TEMPLE REDEVELOPMENT PROJECT

EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE 640 TEMPLE REDEVELOPMENT PROJECT Prepared by: Temple Group Holdings, LLC 1 Kercheval Avenue Grosse Pointe Farms, Michigan

EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE 640 TEMPLE REDEVELOPMENT PROJECT Prepared by: Temple Group Holdings, LLC 1 Kercheval Avenue Grosse Pointe Farms, Michigan

CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE BRUSH PARK SOUTH (PHASE 1) REDEVELOPMENT PROJECT

REDEVELOPMENT PROJECT") EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE BRUSH PARK SOUTH (PHASE 1) REDEVELOPMENT PROJECT Prepared by: Richard A. Barr, Esq. Honigman LLP 660 Woodward Avenue,

EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE BRUSH PARK SOUTH (PHASE 1) REDEVELOPMENT PROJECT Prepared by: Richard A. Barr, Esq. Honigman LLP 660 Woodward Avenue,

2017 General Fund Revenue Forecast

Livingston County 2017 General Fund Revenue Forecast Revenue Forecast Committee June 22, 2016 Revenue Committee William Green - County Commissioner Sally Reynolds - Register of Deeds Jennifer Nash Treasurer

Livingston County 2017 General Fund Revenue Forecast Revenue Forecast Committee June 22, 2016 Revenue Committee William Green - County Commissioner Sally Reynolds - Register of Deeds Jennifer Nash Treasurer

THE AUDITORS AUDITORS OF MICHIGAN SCHOOLS

THE AUDITORS AUDITORS OF MICHIGAN SCHOOLS Kim Lindsay, CPA Jamie Essenmacher, CPA Jennifer Watkins, CPA Bruce Dunn, CPA 1 GASB 75 OPEB Reporting Kim Lindsay, CPA klindsay@lewis knopf.com Accounting and

THE AUDITORS AUDITORS OF MICHIGAN SCHOOLS Kim Lindsay, CPA Jamie Essenmacher, CPA Jennifer Watkins, CPA Bruce Dunn, CPA 1 GASB 75 OPEB Reporting Kim Lindsay, CPA klindsay@lewis knopf.com Accounting and

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of The People of the State of Michigan enact:

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of 1980 AN ACT to prevent urban deterioration and encourage economic development and activity and to encourage neighborhood revitalization and historic preservation;

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of 1980 AN ACT to prevent urban deterioration and encourage economic development and activity and to encourage neighborhood revitalization and historic preservation;

CITY OF STURGIS, MICHIGAN FINANCIAL REPORT WITH SUPPLEMENTAL INFORMATION SEPTEMBER 30, 2017

, MICHIGAN FINANCIAL REPORT WITH SUPPLEMENTAL INFORMATION SEPTEMBER 30, 2017 TABLE OF CONTENTS Independent Auditor's Report 1 2 PAGE Management s Discussion and Analysis 3 12 Basic Financial Statements

, MICHIGAN FINANCIAL REPORT WITH SUPPLEMENTAL INFORMATION SEPTEMBER 30, 2017 TABLE OF CONTENTS Independent Auditor's Report 1 2 PAGE Management s Discussion and Analysis 3 12 Basic Financial Statements

ESTIMATED REVENUES AND OTHER FINANCING SOURCES: BUDGET SUMMARY Page A Final General Fund Budget (PDE-2028)

") Printed 6/25/2015 10:28:33 AM v2.1 ITEM AMOUNTS ESTIMATED REVENUES AND OTHER FINANCING SOURCES: BUDGET SUMMARY Page A-1 Estimated Beginning Unreserved Fund Balance Available for Appropriation and Reserves

Printed 6/25/2015 10:28:33 AM v2.1 ITEM AMOUNTS ESTIMATED REVENUES AND OTHER FINANCING SOURCES: BUDGET SUMMARY Page A-1 Estimated Beginning Unreserved Fund Balance Available for Appropriation and Reserves

2008 FINANCIAL OVERVIEW Kent County, Michigan

2008 FINANCIAL OVERVIEW Kent County, Michigan Daryl J. Delabbio County Administrator/Controller Robert J. White Fiscal Services Director OFFICE OF THE ADMINISTRATOR Kent County Administration Building

2008 FINANCIAL OVERVIEW Kent County, Michigan Daryl J. Delabbio County Administrator/Controller Robert J. White Fiscal Services Director OFFICE OF THE ADMINISTRATOR Kent County Administration Building

WHITE OAK PLACE. Brownfield Plan No East Grand River, Tax ID Spartan Ave, Tax ID

WHITE OAK PLACE 1301 East Grand River, Tax ID 33 20 02 18 415 009 1307 East Grand River, Tax ID 33 20 02 18 415 010 116-132 Spartan Ave, Tax ID 33 20 02 18 415 008 East Lansing, Michigan 48823 Brownfield

WHITE OAK PLACE 1301 East Grand River, Tax ID 33 20 02 18 415 009 1307 East Grand River, Tax ID 33 20 02 18 415 010 116-132 Spartan Ave, Tax ID 33 20 02 18 415 008 East Lansing, Michigan 48823 Brownfield

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of The People of the State of Michigan enact:

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of 1980 AN ACT to prevent urban deterioration and encourage economic development and activity and to encourage neighborhood revitalization and historic preservation;

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of 1980 AN ACT to prevent urban deterioration and encourage economic development and activity and to encourage neighborhood revitalization and historic preservation;

OVERVIEW MINNESOTA PROPERTY TAX SYSTEM AND SCHOOL DISTRICT LEVY PROCESS Payable 2008 Levy

OVERVIEW OF MINNESOTA PROPERTY TAX SYSTEM AND SCHOOL DISTRICT LEVY PROCESS 2007 Payable 2008 Levy Division of Program Finance October 2008 TABLE OF CONTENTS Overview of the Minnesota Property Tax System...

OVERVIEW OF MINNESOTA PROPERTY TAX SYSTEM AND SCHOOL DISTRICT LEVY PROCESS 2007 Payable 2008 Levy Division of Program Finance October 2008 TABLE OF CONTENTS Overview of the Minnesota Property Tax System...

B.O.R. & MTT. Michigan Assoc. of County Treasurers Sue Pertile, Gogebic County Treasurer

B.O.R. & MTT Michigan Assoc. of County Treasurers Sue Pertile, Gogebic County Treasurer BOARD OF REVIEWS LOCAL UNIT On the Tuesday immediately following the first Monday in March, the supervisor shall

B.O.R. & MTT Michigan Assoc. of County Treasurers Sue Pertile, Gogebic County Treasurer BOARD OF REVIEWS LOCAL UNIT On the Tuesday immediately following the first Monday in March, the supervisor shall

EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE JOE LOUIS ARENA REDEVELOPMENT PROJECT.

EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE JOE LOUIS ARENA REDEVELOPMENT PROJECT Prepared by: Detroit Economic Growth Corporation 500 Griswold, Suite 2200 Detroit,

EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE JOE LOUIS ARENA REDEVELOPMENT PROJECT Prepared by: Detroit Economic Growth Corporation 500 Griswold, Suite 2200 Detroit,

2007 MILLAGE REDUCTION FRACTION CALCULATIONS WORKSHEET INCLUDING MILLAGE REDUCTION FRACTIONS NOT SPECIFICALLY ASSIGNED TO EQUALIZATION DIRECTOR BY LAW

MICHIGAN DEPT OF TREASURY, STC L-4034 2166 (1-03) 2007 MILLAGE REDUCTION FRACTION CALCULATIONS WORKSHEET INCLUDING MILLAGE REDUCTION FRACTIONS NOT SPECIFICALLY ASSIGNED TO EQUALIZATION DIRECTOR BY LAW

MICHIGAN DEPT OF TREASURY, STC L-4034 2166 (1-03) 2007 MILLAGE REDUCTION FRACTION CALCULATIONS WORKSHEET INCLUDING MILLAGE REDUCTION FRACTIONS NOT SPECIFICALLY ASSIGNED TO EQUALIZATION DIRECTOR BY LAW

2006 MILLAGE REDUCTION FRACTION CALCULATIONS WORKSHEET INCLUDING MILLAGE REDUCTION FRACTIONS NOT SPECIFICALLY ASSIGNED TO EQUALIZATION DIRECTOR BY LAW

MICHIGAN DEPT OF TREASURY, STC L-4034 2166 (1-03) 2006 MILLAGE REDUCTION FRACTION CALCULATIONS WORKSHEET INCLUDING MILLAGE REDUCTION FRACTIONS NOT SPECIFICALLY ASSIGNED TO EQUALIZATION DIRECTOR BY LAW

MICHIGAN DEPT OF TREASURY, STC L-4034 2166 (1-03) 2006 MILLAGE REDUCTION FRACTION CALCULATIONS WORKSHEET INCLUDING MILLAGE REDUCTION FRACTIONS NOT SPECIFICALLY ASSIGNED TO EQUALIZATION DIRECTOR BY LAW

BALLOT PROPOSALS FOR AUGUST 7, 2018 PRIMARY ELECTION

BALLOT PROPOSALS FOR AUGUST 7, 2018 PRIMARY ELECTION County of Sanilac: RENEWAL OF SANILAC COUNTY DRUG TASK FORCE MILLAGE To provide continued funding for the Drug Task Force under the supervision of the

BALLOT PROPOSALS FOR AUGUST 7, 2018 PRIMARY ELECTION County of Sanilac: RENEWAL OF SANILAC COUNTY DRUG TASK FORCE MILLAGE To provide continued funding for the Drug Task Force under the supervision of the

EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE JOE LOUIS ARENA REDEVELOPMENT PROJECT.

EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE JOE LOUIS ARENA REDEVELOPMENT PROJECT Prepared by: Detroit Economic Growth Corporation 500 Griswold, Suite 2200 Detroit,

EXHIBIT A CITY OF DETROIT BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE JOE LOUIS ARENA REDEVELOPMENT PROJECT Prepared by: Detroit Economic Growth Corporation 500 Griswold, Suite 2200 Detroit,

PDE FINAL GENERAL FUND BUDGET Fiscal Year 07/01/ /30/2016

LEA Name: Spring-Ford Area SD Class: 3 AUN Number: 123467303 County: Montgomery PDE-2028 - FINAL GENERAL FUND BUDGET Fiscal Year 07/01/2015-06/30/2016 General Fund Budget Approval Date of Adoption of the

LEA Name: Spring-Ford Area SD Class: 3 AUN Number: 123467303 County: Montgomery PDE-2028 - FINAL GENERAL FUND BUDGET Fiscal Year 07/01/2015-06/30/2016 General Fund Budget Approval Date of Adoption of the

S T A T E O F M I C H I G A N BOARD OF COMMISSIONERS OF THE COUNTY OF ALLEGAN. WHEREAS, the Board of Commissioners of the County of

S T A T E O F M I C H I G A N BOARD OF COMMISSIONERS OF THE COUNTY OF ALLEGAN 2017 MILLAGE LEVY SET COUNTY MILLAGE RATES WHEREAS, the Board of Commissioners of the County of Allegan has held a public hearing

S T A T E O F M I C H I G A N BOARD OF COMMISSIONERS OF THE COUNTY OF ALLEGAN 2017 MILLAGE LEVY SET COUNTY MILLAGE RATES WHEREAS, the Board of Commissioners of the County of Allegan has held a public hearing

Page 1 Page 2 Page 3 2018-2019 Final General Fund Budget Validations LEA : 123466403 Pottstown SD Printed 10/31/2018 10:06:48 AM Page - 1 of 1 Val Number Description Justification 1550 Tax Data: The difference

Page 1 Page 2 Page 3 2018-2019 Final General Fund Budget Validations LEA : 123466403 Pottstown SD Printed 10/31/2018 10:06:48 AM Page - 1 of 1 Val Number Description Justification 1550 Tax Data: The difference

CAROLE KEETON STRAYHORN,

Truth-In-Taxation A Guide for Setting School District Tax Rates July 2006 CAROLE KEETON STRAYHORN, Texas Comptroller TEXAS PROPERTY TAX Truth-In-Taxation A Guide for Setting School District Tax Rates

Truth-In-Taxation A Guide for Setting School District Tax Rates July 2006 CAROLE KEETON STRAYHORN, Texas Comptroller TEXAS PROPERTY TAX Truth-In-Taxation A Guide for Setting School District Tax Rates

Personal Property Tax Reform

Personal Property Tax Reform Purpose 1 Purpose Significantly improve Michigan s business environment, competitiveness, and conditions for job growth and investment. Protect local units that rely on the

Personal Property Tax Reform Purpose 1 Purpose Significantly improve Michigan s business environment, competitiveness, and conditions for job growth and investment. Protect local units that rely on the

Ohio Legislative Service Commission

Ohio Legislative Service Commission Fiscal Note & Local Impact Statement Tom Middleton and other LSC staff Bill: H.B. 233 of the 131st G.A. Date: April 8, 2016 Status: As Reported by Senate Ways & Means

Ohio Legislative Service Commission Fiscal Note & Local Impact Statement Tom Middleton and other LSC staff Bill: H.B. 233 of the 131st G.A. Date: April 8, 2016 Status: As Reported by Senate Ways & Means

Williamston Community Schools Williamston, Michigan FINANCIAL STATEMENTS. June 30, 2017

Williamston, Michigan FINANCIAL STATEMENTS TABLE OF CONTENTS Page INDEPENDENT AUDITOR S REPORT ADMINISTRATION S DISCUSSION AND ANALYSIS i-ii iii-x BASIC FINANCIAL STATEMENTS District-wide Financial Statements:

Williamston, Michigan FINANCIAL STATEMENTS TABLE OF CONTENTS Page INDEPENDENT AUDITOR S REPORT ADMINISTRATION S DISCUSSION AND ANALYSIS i-ii iii-x BASIC FINANCIAL STATEMENTS District-wide Financial Statements:

BUDGET PORT HURON MICHIGAN

BUDGET PORT HURON MICHIGAN ADOPTED BY CITY COUNCIL MAY 29, 2018 FINAL ADOPTED BUDGET CITY OF PORT HURON FOR THE FISCAL YEAR Table of Contents CITY OF PORT HURON BUDGET FISCAL YEAR Page Number 1. Schedule

BUDGET PORT HURON MICHIGAN ADOPTED BY CITY COUNCIL MAY 29, 2018 FINAL ADOPTED BUDGET CITY OF PORT HURON FOR THE FISCAL YEAR Table of Contents CITY OF PORT HURON BUDGET FISCAL YEAR Page Number 1. Schedule

PDE FINAL GENERAL FUND BUDGET Fiscal Year 07/01/ /30/2015

LEA Name: Methacton SD Class: 3 AUN Number: 123465303 County: Montgomery PDE-2028 - FINAL GENERAL FUND BUDGET Fiscal Year 07/01/2014-06/30/2015 General Fund Budget Approval Date of Adoption of the General

LEA Name: Methacton SD Class: 3 AUN Number: 123465303 County: Montgomery PDE-2028 - FINAL GENERAL FUND BUDGET Fiscal Year 07/01/2014-06/30/2015 General Fund Budget Approval Date of Adoption of the General

Michigan s Shrinking Property Tax Base

Michigan s Shrinking Property Tax Base Michigan s Shrinking Property Tax Base Michigan Association of Counties 2016 Annual Conference September 17, 2016 Eric Lupher, President 2 Citizens Research Council

Michigan s Shrinking Property Tax Base Michigan s Shrinking Property Tax Base Michigan Association of Counties 2016 Annual Conference September 17, 2016 Eric Lupher, President 2 Citizens Research Council

PROPOSALS August 2, 2016 Election

PROPOSALS August 2, 2016 Election COUNTY PROPOSITION FOR SHIAWASSEE COUNTY MILLAGE TO FUND MICHIGAN STATE UNIVERSITY EXTENSION AND 4-H For the purpose of funding MSU Extension services in Shiawassee County,

PROPOSALS August 2, 2016 Election COUNTY PROPOSITION FOR SHIAWASSEE COUNTY MILLAGE TO FUND MICHIGAN STATE UNIVERSITY EXTENSION AND 4-H For the purpose of funding MSU Extension services in Shiawassee County,

Property Assessment and Taxation. An informational presentation brought to you by the City of Grand Ledge Assessing Department.

Property Assessment and Taxation An informational presentation brought to you by the City of Grand Ledge Assessing Department. How Does Proposal A Affect Me? Proposal A Before and After BEFORE 1994 AFTER

Property Assessment and Taxation An informational presentation brought to you by the City of Grand Ledge Assessing Department. How Does Proposal A Affect Me? Proposal A Before and After BEFORE 1994 AFTER

$3,200,000 CITY OF ESCANABA COUNTY OF DELTA, STATE OF MICHIGAN CAPITAL IMPROVEMENT BONDS, SERIES

NEW ISSUE Book Entry Only RATING1* Standard & Poor s Ratings Services: AA- Miller, Canfield, Paddock and Stone P.L.C, Bond Counsel, is of the opinion that, under existing law, the interest on the Bonds

NEW ISSUE Book Entry Only RATING1* Standard & Poor s Ratings Services: AA- Miller, Canfield, Paddock and Stone P.L.C, Bond Counsel, is of the opinion that, under existing law, the interest on the Bonds

OVERVIEW MINNESOTA PROPERTY TAX SYSTEM AND SCHOOL DISTRICT LEVY PROCESS Payable 2006 Levy

OVERVIEW OF MINNESOTA PROPERTY TAX SYSTEM AND SCHOOL DISTRICT LEVY PROCESS 2005 Payable 2006 Levy Division of Program Finance March 2006 TABLE OF CONTENTS Overview of the Minnesota Property Tax System...

OVERVIEW OF MINNESOTA PROPERTY TAX SYSTEM AND SCHOOL DISTRICT LEVY PROCESS 2005 Payable 2006 Levy Division of Program Finance March 2006 TABLE OF CONTENTS Overview of the Minnesota Property Tax System...

Property Tax Levy Law. Mike Sobul, CFO/Treasurer, Granville EVSD Consultant, Public Finance Resources, Inc. OSBA Capital Conference November 11, 2013

Property Tax Levy Law Mike Sobul, CFO/Treasurer, Granville EVSD Consultant, Public Finance Resources, Inc. OSBA Capital Conference November 11, 2013 Constitutional Restrictions * O. Const. Art. XII, Sec.

Property Tax Levy Law Mike Sobul, CFO/Treasurer, Granville EVSD Consultant, Public Finance Resources, Inc. OSBA Capital Conference November 11, 2013 Constitutional Restrictions * O. Const. Art. XII, Sec.

Hernando County School Board, FL

Hernando County School Board, FL 1 Refunding Certificates of Participation (School Board of Hernando County, Florida Master Lease Program), Evidencing Fractional Undivided Interests of Owners thereof in

Hernando County School Board, FL 1 Refunding Certificates of Participation (School Board of Hernando County, Florida Master Lease Program), Evidencing Fractional Undivided Interests of Owners thereof in

Indirect Cost Rates. Phil Boone: MDE Office of Financial Management, State Aid School Finance

Indirect Cost Rates Phil Boone: MDE Office of Financial Management, State Aid School Finance Jessica Beagle: MDE Office of Financial Management, State Aid School Finance Lori Schomisch: Clinton County

Indirect Cost Rates Phil Boone: MDE Office of Financial Management, State Aid School Finance Jessica Beagle: MDE Office of Financial Management, State Aid School Finance Lori Schomisch: Clinton County

REPORT ACCOMPANYING THE SECOND AMENDMENT TO THE RIVER DISTRICT URBAN RENEWAL PLAN

Page 1 of 16 REPORT ACCOMPANYING THE SECOND AMENDMENT TO THE RIVER DISTRICT URBAN RENEWAL PLAN Portland Development Commission Page 2 of 16 TABLE OF CONTENTS I. INTRODUCTION... 1 II. A DESCRIPTION OF PHYSICAL,

Page 1 of 16 REPORT ACCOMPANYING THE SECOND AMENDMENT TO THE RIVER DISTRICT URBAN RENEWAL PLAN Portland Development Commission Page 2 of 16 TABLE OF CONTENTS I. INTRODUCTION... 1 II. A DESCRIPTION OF PHYSICAL,

AUGUST 2, 2016 PRIMARY ELECTION BALLOT PROPOSALS BRIGHTON AREA FIRE AUTHORITY FIRE MILLAGE PROPOSAL

Page 1 of 6 AUGUST 2, 2016 PRIMARY ELECTION BALLOT PROPOSALS BRIGHTON AREA FIRE AUTHORITY FIRE MILLAGE PROPOSAL Shall the limitation on the amount of taxes, which may be levied against all property in

Page 1 of 6 AUGUST 2, 2016 PRIMARY ELECTION BALLOT PROPOSALS BRIGHTON AREA FIRE AUTHORITY FIRE MILLAGE PROPOSAL Shall the limitation on the amount of taxes, which may be levied against all property in

Financing Education In Minnesota A Publication of the Minnesota House of Representatives Fiscal Analysis Department

Financing Education In Minnesota 2002-03 A Publication of the Minnesota House of Representatives Fiscal Analysis Department August 2002 Financing Education in Minnesota 2002-03 A Publication of the Minnesota

Financing Education In Minnesota 2002-03 A Publication of the Minnesota House of Representatives Fiscal Analysis Department August 2002 Financing Education in Minnesota 2002-03 A Publication of the Minnesota

OFFICIAL LIST OF PROPOSALS 11/04/ STATE GENERAL EATON COUNTY

Page 1 STATE PROPOSALS PROPOSAL 14-1 A REFERENDUM OF PUBLIC ACT 520 OF 2012, ESTABLISHING A HUNTING SEASON FOR WOLVES AND AUTHORIZING ANNUAL WOLF HUNTING SEASONS Public Act 520 of 2012 would: Designate

Page 1 STATE PROPOSALS PROPOSAL 14-1 A REFERENDUM OF PUBLIC ACT 520 OF 2012, ESTABLISHING A HUNTING SEASON FOR WOLVES AND AUTHORIZING ANNUAL WOLF HUNTING SEASONS Public Act 520 of 2012 would: Designate

Budget Resolution

2005-06 Budget Resolution Moved By: Councilperson Bell Date: June 20, 2005 Supported By: Councilperson Frasier BE IT RESOLVED: Consistent with the Uniform Budgeting and Accounting Act, expenditure authority

2005-06 Budget Resolution Moved By: Councilperson Bell Date: June 20, 2005 Supported By: Councilperson Frasier BE IT RESOLVED: Consistent with the Uniform Budgeting and Accounting Act, expenditure authority

Fulton Schools Middleton, Michigan FINANCIAL STATEMENTS. June 30, 2018

Middleton, Michigan FINANCIAL STATEMENTS Middleton, Michigan BOARD OF EDUCATION Karla Childers President Lee Williams Vice-President Deana Grover Secretary Amy Case Treasurer Edward V. Lorenz Trustee Matthew

Middleton, Michigan FINANCIAL STATEMENTS Middleton, Michigan BOARD OF EDUCATION Karla Childers President Lee Williams Vice-President Deana Grover Secretary Amy Case Treasurer Edward V. Lorenz Trustee Matthew

BUDGET PORT HURON MICHIGAN

BUDGET PORT HURON MICHIGAN ADOPTED BY CITY COUNCIL MAY 22, 2017 FINAL ADOPTED BUDGET CITY OF PORT HURON FOR THE FISCAL YEAR CITY OF PORT HURON BUDGET FISCAL YEAR Table of Contents Page Number 1. Schedule

BUDGET PORT HURON MICHIGAN ADOPTED BY CITY COUNCIL MAY 22, 2017 FINAL ADOPTED BUDGET CITY OF PORT HURON FOR THE FISCAL YEAR CITY OF PORT HURON BUDGET FISCAL YEAR Table of Contents Page Number 1. Schedule

Final General Fund Budget Validations LEA : Danville Area SD Printed 6/19/ :30:27 AM. Operating Reserve

Page 1 Page 2 Page 3 2018-2019 Final General Fund Budget Validations Printed 6/19/2018 10:30:27 AM Page - 1 of 1 Val Number Description Justification 5260 Expenditure Detail: 100 Salaries amount must be

Page 1 Page 2 Page 3 2018-2019 Final General Fund Budget Validations Printed 6/19/2018 10:30:27 AM Page - 1 of 1 Val Number Description Justification 5260 Expenditure Detail: 100 Salaries amount must be

FY SUMMARY BUDGET

FY2016-17 SUMMARY BUDGET SCHOOL DISTRICT DISTRICT CODE 10 General Fund 11 Charter School Fund 18 Insurance Reserve / Risk- Management 19 Colorado Preschool Program 0 0 ed Pupil Count 0.0 BEGINNING FUND

FY2016-17 SUMMARY BUDGET SCHOOL DISTRICT DISTRICT CODE 10 General Fund 11 Charter School Fund 18 Insurance Reserve / Risk- Management 19 Colorado Preschool Program 0 0 ed Pupil Count 0.0 BEGINNING FUND

Revenue Options. February 22, *Some slides taken from the Michigan Department of Treasury

Revenue Options February 22, 2018 *Some slides taken from the Michigan Department of Treasury All of the reductions we are recommending are difficult choices and reflect many of the services and amenities

Revenue Options February 22, 2018 *Some slides taken from the Michigan Department of Treasury All of the reductions we are recommending are difficult choices and reflect many of the services and amenities

INTRODUCTION TO FINANCIAL SERVICES

FINANCIAL SERVICES INTRODUCTION TO FINANCIAL SERVICES The Financial Services Area has 62 employees in the following areas: Accounting and Payroll Assessing Budget and Forecasting Information Technology

FINANCIAL SERVICES INTRODUCTION TO FINANCIAL SERVICES The Financial Services Area has 62 employees in the following areas: Accounting and Payroll Assessing Budget and Forecasting Information Technology

Fiscal Year 2005 Adopted Budget

Fiscal Year 2005 Budget REVENUE SUMMARIES Revenue Summaries TAXABLE VERSUS GROSS VALUE EXEMPTIONS AT A GLANCE Ad valorem taxes are taxes levied against the assessed valuation of real and tangible persona

Fiscal Year 2005 Budget REVENUE SUMMARIES Revenue Summaries TAXABLE VERSUS GROSS VALUE EXEMPTIONS AT A GLANCE Ad valorem taxes are taxes levied against the assessed valuation of real and tangible persona

Final General Fund Budget Validations LEA : Highlands SD Printed 5/15/2018 9:43:17 AM. Page 4

Page 1 Page 2 Page 3 2017-2018 Final General Fund Budget Validations Printed 5/15/2018 9:43:17 AM Page - 1 of 1 Val Number Description Justification 8060 Ending Fund Balance Entry and Budgetary Reserve:

Page 1 Page 2 Page 3 2017-2018 Final General Fund Budget Validations Printed 5/15/2018 9:43:17 AM Page - 1 of 1 Val Number Description Justification 8060 Ending Fund Balance Entry and Budgetary Reserve:

FINAL GENERAL FUND BUDGET

LEA Name : Harrisburg City SD Class: 2 AUN Number : 115222752 County : Dauphin FINAL GENERAL FUND BUDGET Fiscal Year 2017-2018 General Fund Budget Approval Date of Adoption of the General Fund Budget:

LEA Name : Harrisburg City SD Class: 2 AUN Number : 115222752 County : Dauphin FINAL GENERAL FUND BUDGET Fiscal Year 2017-2018 General Fund Budget Approval Date of Adoption of the General Fund Budget:

Cash Balance June 30 15,940,136 15,271,647 13,479,243 12,241,640 11,698,295 10,837,831 9,756,394 8,379,673

Whitehall City School District Schedule Of Revenue, Expenditures and Changes In Fund Balances Actual and Forecasted Operating Fund ACTUAL FORECASTED Fiscal Year Fiscal Year Fiscal Year Fiscal Year Fiscal

Whitehall City School District Schedule Of Revenue, Expenditures and Changes In Fund Balances Actual and Forecasted Operating Fund ACTUAL FORECASTED Fiscal Year Fiscal Year Fiscal Year Fiscal Year Fiscal

McCreary Veselka Bragg & Allen P.C. Attorneys at Law. A Guide for Setting Tax Rates

McCreary Veselka Bragg & Allen P.C. Attorneys at Law A Guide for Setting Tax Rates TRUTH-IN-TAXATION 2018 for Our Clients We are pleased to present this easy-to-use guidebook to help you with this year

McCreary Veselka Bragg & Allen P.C. Attorneys at Law A Guide for Setting Tax Rates TRUTH-IN-TAXATION 2018 for Our Clients We are pleased to present this easy-to-use guidebook to help you with this year

COSTCO WHOLESALE WAREHOUSE. Brownfield Plan No.22

COSTCO WHOLESALE WAREHOUSE 58 Park Lake Road, Tax ID 332282764 No Known Address, Tax ID 332291513 East Lansing, Michigan 48823 Brownfield Plan No.22 Revised October 16, 216 Prepared with assistance from:

COSTCO WHOLESALE WAREHOUSE 58 Park Lake Road, Tax ID 332282764 No Known Address, Tax ID 332291513 East Lansing, Michigan 48823 Brownfield Plan No.22 Revised October 16, 216 Prepared with assistance from:

PDE-2028-FINAL GENERAL FUND BUDGET FISCAL YEAR 07/01/ /30/2015 PENNSBURY SCHOOL DISTRICT

PDE-228-FINAL GENERAL FUND BUDGET FISCAL YEAR 7/1/214-6/3/215 PENNSBURY SCHOOL DISTRICT LEA Name: Pennsbury SD Class: 2 AUN Number: 1229822 County: Bucks PDE-228 - FINAL GENERAL FUND BUDGET Fiscal Year

PDE-228-FINAL GENERAL FUND BUDGET FISCAL YEAR 7/1/214-6/3/215 PENNSBURY SCHOOL DISTRICT LEA Name: Pennsbury SD Class: 2 AUN Number: 1229822 County: Bucks PDE-228 - FINAL GENERAL FUND BUDGET Fiscal Year

The following is for informational purposes only:

ALLEGAN PUBLIC SCHOOLS SINKING FUND MILLAGE PROPOSAL Shall the limitation on the amount of taxes which may be assessed against all property in Allegan Public Schools, Allegan County, Michigan, be increased

ALLEGAN PUBLIC SCHOOLS SINKING FUND MILLAGE PROPOSAL Shall the limitation on the amount of taxes which may be assessed against all property in Allegan Public Schools, Allegan County, Michigan, be increased

A. Inflation Rate Used in the 2013 Capped Value Formula.

89 (Rev. 01-11) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING ANDY DILLON STATE TREASURER BULLETIN NO. 11 of 2012 CHANGES FOR 2013 TO: FROM: RE: Assessors Equalization Directors

89 (Rev. 01-11) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING ANDY DILLON STATE TREASURER BULLETIN NO. 11 of 2012 CHANGES FOR 2013 TO: FROM: RE: Assessors Equalization Directors

INGHAM COUNTY JUSTICE MILLAGE QUESTION YES [ ] NO [ ]

![INGHAM COUNTY JUSTICE MILLAGE QUESTION YES [ ] NO [ ]](/thumbs/83/88537150.jpg "INGHAM COUNTY JUSTICE MILLAGE QUESTION YES [ ] NO [ ]") INGHAM COUNTY JUSTICE MILLAGE QUESTION For the purpose of constructing, equipping, and financing a new combined justice complex facility and expanding correctional programming, to include a new county

INGHAM COUNTY JUSTICE MILLAGE QUESTION For the purpose of constructing, equipping, and financing a new combined justice complex facility and expanding correctional programming, to include a new county

The accompanying notes are an integral part of these financial statements. 13

COUNTY OF MARQUETTE, MICHIGAN STATEMENT OF NET POSITION December 31, 2012 Primary Government Governmental Business Type Component Activities Activities Total Units ASSETS Cash and equivalents $ 11,686,626

COUNTY OF MARQUETTE, MICHIGAN STATEMENT OF NET POSITION December 31, 2012 Primary Government Governmental Business Type Component Activities Activities Total Units ASSETS Cash and equivalents $ 11,686,626

Final General Fund Budget Validations LEA : Penn Cambria SD Printed 6/19/ :30:48 AM. Page 4

Page 3 2018-2019 Final General Fund Budget Validations Printed 6/19/2018 10:30:48 AM Page - 1 of 1 Val Number Description Justification 8060 Ending Fund Balance Entry and Budgetary Reserve: If 5900 Budgetary

Page 3 2018-2019 Final General Fund Budget Validations Printed 6/19/2018 10:30:48 AM Page - 1 of 1 Val Number Description Justification 8060 Ending Fund Balance Entry and Budgetary Reserve: If 5900 Budgetary

Understanding Your Tax Bill. A Basic Understanding of Tax Assessment and Taxation

Understanding Your Tax Bill A Basic Understanding of Tax Assessment and Taxation Taxation Cycle Assessment Process-Assessor places values on properties Equalization Process by DOR-equalized value total

Understanding Your Tax Bill A Basic Understanding of Tax Assessment and Taxation Taxation Cycle Assessment Process-Assessor places values on properties Equalization Process by DOR-equalized value total

Final General Fund Budget Validations LEA : Greencastle-Antrim SD Printed 6/15/ :50:49 AM. Page 4

Page 1 Page 2 Page 3 2018-2019 Final General Fund Budget Validations Printed 6/15/2018 10:50:49 AM Page - 1 of 1 Val Number Description Justification 8080 Ending Fund Balance Entry and Budgetary Reserve:

Page 1 Page 2 Page 3 2018-2019 Final General Fund Budget Validations Printed 6/15/2018 10:50:49 AM Page - 1 of 1 Val Number Description Justification 8080 Ending Fund Balance Entry and Budgetary Reserve:

ESCAMBIA COUNTY, FLORIDA COMMUNITY REDEVELOPMENT AGENCY FINANCIAL STATEMENTS AND REQUIRED SUPPLEMENTARY INFORMATION

ESCAMBIA COUNTY, FLORIDA FINANCIAL STATEMENTS AND REQUIRED SUPPLEMENTARY INFORMATION SEPTEMBER 30, 2014 WITH INDEPENDENT AUDITORS REPORT FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT SEPTEMBER 30,

ESCAMBIA COUNTY, FLORIDA FINANCIAL STATEMENTS AND REQUIRED SUPPLEMENTARY INFORMATION SEPTEMBER 30, 2014 WITH INDEPENDENT AUDITORS REPORT FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT SEPTEMBER 30,

FINAL GENERAL FUND BUDGET

LEA Name : Bethel Park SD Class : 2 AUN Number : 103021252 County : Allegheny FINAL GENERAL FUND BUDGET Fiscal Year 2018-2019 General Fund Budget Approval Date of Adoption of the General Fund Budget: 05/22/2018

LEA Name : Bethel Park SD Class : 2 AUN Number : 103021252 County : Allegheny FINAL GENERAL FUND BUDGET Fiscal Year 2018-2019 General Fund Budget Approval Date of Adoption of the General Fund Budget: 05/22/2018

Final General Fund Budget Validations LEA : Shanksville-Stonycreek SD Printed 6/29/2017 1:22:27 PM. Page 4

Page 1 Page 2 Page 3 2017-2018 Final General Fund Budget Validations Printed 6/29/2017 1:22:27 PM Page - 1 of 1 Val Number Description Justification 8060 Ending Fund Balance Entry and Budgetary Reserve:

Page 1 Page 2 Page 3 2017-2018 Final General Fund Budget Validations Printed 6/29/2017 1:22:27 PM Page - 1 of 1 Val Number Description Justification 8060 Ending Fund Balance Entry and Budgetary Reserve:

4,386,893 29,114,485. Page 4

Page 1 Page 2 Page 3 2016-2017 Final General Fund Budget (PDE-2028) Estimated Revenues and Other Financing Sources: Budget Summary Printed 6/16/2016 12:20:48 PM Page - 1 of 1 ITEM AMOUNTS Estimated Beginning

Page 1 Page 2 Page 3 2016-2017 Final General Fund Budget (PDE-2028) Estimated Revenues and Other Financing Sources: Budget Summary Printed 6/16/2016 12:20:48 PM Page - 1 of 1 ITEM AMOUNTS Estimated Beginning

BROWNFIELD REDEVELOPMENT PLAN THE VILLAGE MARKETPLACE + LOFTS 147, 159 AND 185 W. MICHIGAN AVENUE

BROWNFIELD REDEVELOPMENT PLAN THE VILLAGE MARKETPLACE + LOFTS 147, 159 AND 185 W. MICHIGAN AVENUE AND 104 HENRY STREET CITY OF SALINE, MICHIGAN for WASHTENAW COUNTY BROWNFIELD REDEVELOPMENT AUTHORITY WASHTENAW

BROWNFIELD REDEVELOPMENT PLAN THE VILLAGE MARKETPLACE + LOFTS 147, 159 AND 185 W. MICHIGAN AVENUE AND 104 HENRY STREET CITY OF SALINE, MICHIGAN for WASHTENAW COUNTY BROWNFIELD REDEVELOPMENT AUTHORITY WASHTENAW

Final General Fund Budget Validations LEA : Susquenita SD Printed 6/15/ :12:19 AM. Page 4

Page 1 Page 2 Page 3 2017-2018 Final General Fund Budget Validations Printed 6/15/2017 10:12:19 AM Page - 1 of 1 Val Number Description Justification 5230 Expenditure Detail: 100 Salaries amount must be

Page 1 Page 2 Page 3 2017-2018 Final General Fund Budget Validations Printed 6/15/2017 10:12:19 AM Page - 1 of 1 Val Number Description Justification 5230 Expenditure Detail: 100 Salaries amount must be

THE DEPARTMENT MICHIGAN DEPARTMENT OF EDUCATION

THE DEPARTMENT MICHIGAN DEPARTMENT OF EDUCATION ACCOUNTING & AUDITING ALERT - AUDITS GRANT AUDITOR REPORTS HTTPS://MDOE.STATE.MI.US/CMS/GRANTAUDITORREPORT.ASPX HAS THE CFDA, GRANT AND PROJECT NUMBERS TO

THE DEPARTMENT MICHIGAN DEPARTMENT OF EDUCATION ACCOUNTING & AUDITING ALERT - AUDITS GRANT AUDITOR REPORTS HTTPS://MDOE.STATE.MI.US/CMS/GRANTAUDITORREPORT.ASPX HAS THE CFDA, GRANT AND PROJECT NUMBERS TO

Special Education Funding

Special Education Funding Prepared by: Paul Johnson, CFO White Pine County School District Jeff Zander, Superintendent Elko County School District January 21, 2017 1 Federal Legislative Timeline http://iris.peabody.vanderbilt.edu/module/nur01-personnel/cresource/q1/p03/nur01_03_link_timeline/

Special Education Funding Prepared by: Paul Johnson, CFO White Pine County School District Jeff Zander, Superintendent Elko County School District January 21, 2017 1 Federal Legislative Timeline http://iris.peabody.vanderbilt.edu/module/nur01-personnel/cresource/q1/p03/nur01_03_link_timeline/

Final General Fund Budget Validations LEA : Palmerton Area SD Printed 7/2/ :49:05 AM. As approved by board.

Page 1 Page 2 2018-2019 Final General Fund Budget Validations Printed 7/2/2018 10:49:05 AM Page - 1 of 1 Val Number Description Justification 5260 Expenditure Detail: 100 Salaries amount must be greater

Page 1 Page 2 2018-2019 Final General Fund Budget Validations Printed 7/2/2018 10:49:05 AM Page - 1 of 1 Val Number Description Justification 5260 Expenditure Detail: 100 Salaries amount must be greater

SCHEDULE OF CASH AND INVESTMENTS (CAIN) Page F General Fund Budget (PDE-2028) Printed 3/27/2007 8:58:28 AM

Page F General Fund Budget (PDE-2028) Printed 3/27/2007 8:58:28 AM") Printed 3/27/2007 8:58:28 AM SCHEDULE OF CASH AND INVESTMENTS (CAIN) Page F-1 06/30/2005 Estimate 06/30/2006 Projection CASH AND SHORT-TERM INVESTMENTS General Fund 2,800,000 1,700,000 Special Revenue

Printed 3/27/2007 8:58:28 AM SCHEDULE OF CASH AND INVESTMENTS (CAIN) Page F-1 06/30/2005 Estimate 06/30/2006 Projection CASH AND SHORT-TERM INVESTMENTS General Fund 2,800,000 1,700,000 Special Revenue

TAX INCREMENT FINANCING ACT - OMNIBUS AMENDMENTS Act of Dec. 16, 1992, P.L. 1240, No. 164 Cl. 64 Session of 1992 No

TAX INCREMENT FINANCING ACT - OMNIBUS AMENDMENTS Act of Dec. 16, 1992, P.L. 1240, No. 164 Cl. 64 Session of 1992 No. 1992-164 HB 2439 AN ACT Amending the act of July 11, 1990 (P.L.465, No.113), entitled

TAX INCREMENT FINANCING ACT - OMNIBUS AMENDMENTS Act of Dec. 16, 1992, P.L. 1240, No. 164 Cl. 64 Session of 1992 No. 1992-164 HB 2439 AN ACT Amending the act of July 11, 1990 (P.L.465, No.113), entitled

The property tax is the predominant method communities use to raise additional revenues in Ohio. The property tax comes in two forms:

INTRODUCTION The cost to educate young people across the state is significant and those costs continue to rise. More Ohio tax dollars are spent for primary and secondary education than for any other single

INTRODUCTION The cost to educate young people across the state is significant and those costs continue to rise. More Ohio tax dollars are spent for primary and secondary education than for any other single

06.07 ALTERNATE METHODS OF TAXATION

06.07 ALTERNATE METHODS OF TAXATION Overview There are methods of property taxation that differ from the normal calculations described elsewhere in this manual. This section provides an overview of three

06.07 ALTERNATE METHODS OF TAXATION Overview There are methods of property taxation that differ from the normal calculations described elsewhere in this manual. This section provides an overview of three

HANCOCK PUBLIC SCHOOLS. REPORT ON FINANCIAL STATEMENTS (with required supplementary and additional information) YEAR ENDED JUNE 30, 2018

YEAR ENDED JUNE 30, 2018") REPORT ON FINANCIAL STATEMENTS (with required supplementary and additional information) YEAR ENDED JUNE 30, 2018 June 30, 2018 ADMINISTRATION Superintendent... Kipp Beaudoin High and Middle School Principal...

REPORT ON FINANCIAL STATEMENTS (with required supplementary and additional information) YEAR ENDED JUNE 30, 2018 June 30, 2018 ADMINISTRATION Superintendent... Kipp Beaudoin High and Middle School Principal...

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 1993 S 1 SENATE BILL May 25, 1994

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S SENATE BILL Short Title: Repeal Intangibles Tax. Sponsors: Senators Kerr; and Albertson. Referred to: Finance. (Public) May, 0 0 A BILL TO BE ENTITLED AN ACT

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S SENATE BILL Short Title: Repeal Intangibles Tax. Sponsors: Senators Kerr; and Albertson. Referred to: Finance. (Public) May, 0 0 A BILL TO BE ENTITLED AN ACT

TAX RATE ADOPTION & NOTICES

Oldham County Judge Don R. Allred TAX RATE ADOPTION & NOTICES!! 26.01 Submission of Rolls to Taxing Unit!! (a) By July 25 the chief appraiser shall prepare and certify to the assessor the appraisal roll.!!

Oldham County Judge Don R. Allred TAX RATE ADOPTION & NOTICES!! 26.01 Submission of Rolls to Taxing Unit!! (a) By July 25 the chief appraiser shall prepare and certify to the assessor the appraisal roll.!!

Final General Fund Budget Validations LEA : Mifflin County SD Printed 7/2/2018 2:22:46 PM. Page 4

Page 1 Page 2 Page 3 2018-2019 Final General Fund Budget Validations Printed 7/2/2018 2:22:46 PM Page - 1 of 1 Val Number Description Justification 8060 Ending Fund Balance Entry and Budgetary Reserve:

Page 1 Page 2 Page 3 2018-2019 Final General Fund Budget Validations Printed 7/2/2018 2:22:46 PM Page - 1 of 1 Val Number Description Justification 8060 Ending Fund Balance Entry and Budgetary Reserve: