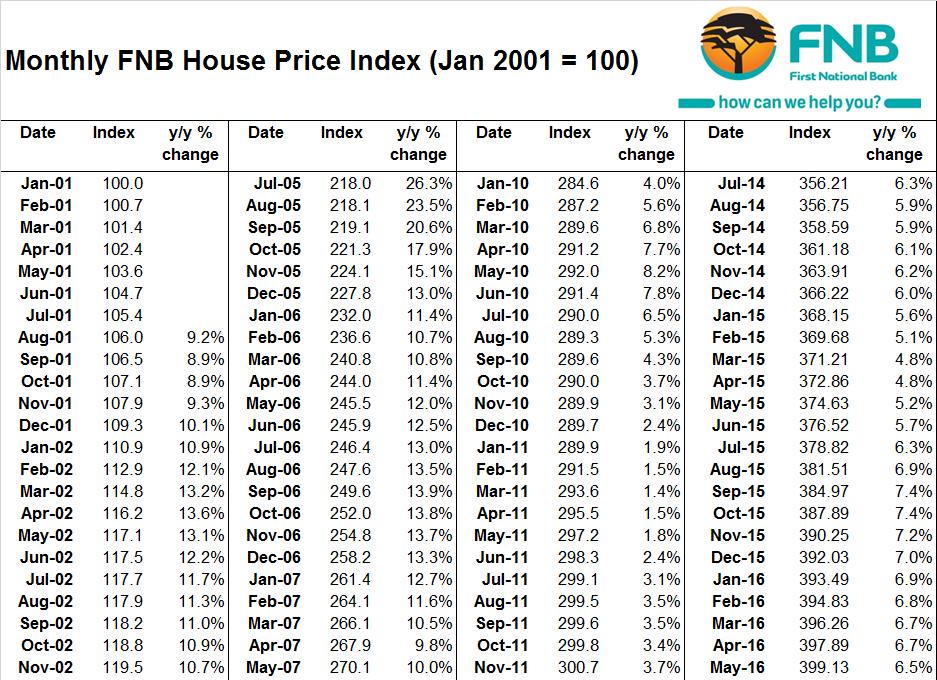

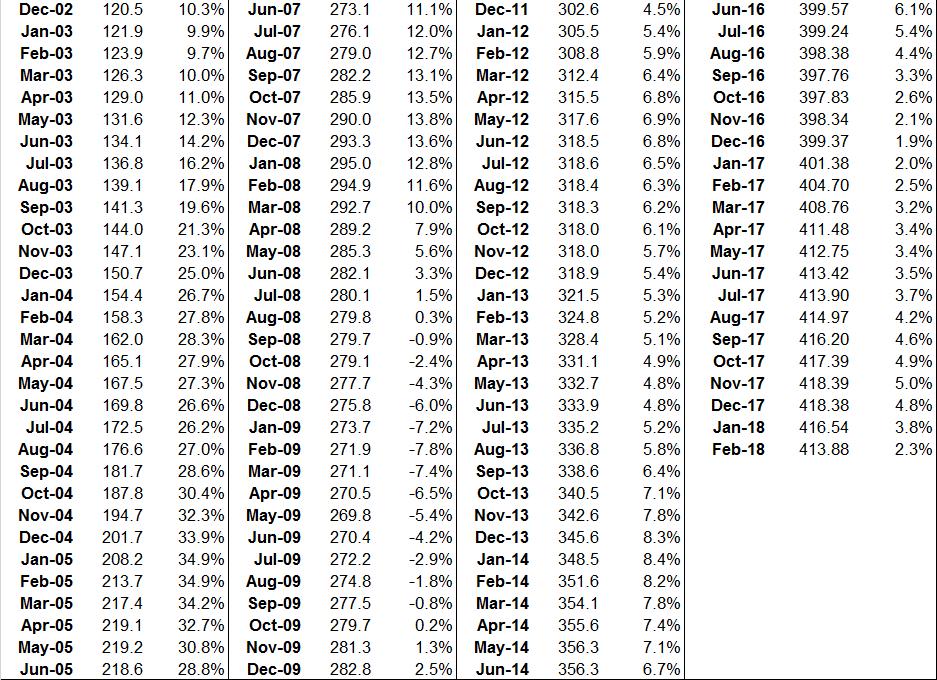

PROPERTY BAROMETER FNB House Price Index Still no sign of a positive national sentiment shift impacting on national house price trends yet

|

|

|

- Moses Sharp

- 5 years ago

- Views:

Transcription

1 1 March 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST THULANI LUVUNO: STATISTICIAN The information in this publication is derived from sources which are regarded as accurate and reliable, is of a general nature only, does not constitute advice and may not be applicable to all circumstances. Detailed advice should be obtained in individual cases. No responsibility for any error, omission or loss sustained by any person acting or refraining from acting as a result of this publication is accepted by Firstrand Group Limited and / or the authors of the material. PROPERTY BAROMETER FNB House Price Index Still no sign of a positive national sentiment shift impacting on national house price trends yet February 2018 saw the FNB House Price Index growing by a slower 2.3%, year-on-year, down from a revised 3.8% in January, and from 2017 s high of 5% reached in November. This does not, however, alter our view that 2018 should be a mildly stronger housing market year than We believe that this weak house price growth in early-2018 is reflective of the weak sentiment and market conditions late in 2017 still feeding through to prices with a lag. But with sentiment appearing to be much-improved early in 2018, we remain of the expectation that economic growth in 2018 will pick up, interest rates remain stable or even decline slightly, and housing demand should be a little stronger, all of which would cause mildly stronger house price growth in 2018 compared to FEBRUARY FNB HOUSE PRICE INDEX FINDINGS From a 2017 high of 5%, reached in November 2017, the FNB House Price Index s year-on-year growth rate has slowed once more to 2.3% by February 2018, a further slowing on January s revised rate of 3.8%. In real terms, when adjusting for CPI (Consumer Price Index) inflation, yearon-year house price deflation of -0.6% was recorded in January (February CPI data not yet available), with CPI inflation in that month measuring 4.4% yearon-year. The average price of homes transacted in February was R1,099,610. First National Bank a division of FirstRand Bank Limited. An Authorised Financial Services provider. Reg No. 1929/001225/06

2 Examining house price growth on a month-onmonth seasonally-adjusted basis, a better indicator of very recent price growth momentum than year-on-year rates, we have seen a recent period of deflation, reaching % in February. It is not uncommon to have short month-onmonth bouts of deflation, and we believe that this most recent one is still the effect of a period of very weak sentiment in the country late in 2017, still feeding through into house prices with a lag. That same negative sentiment was reflected in our FNB Estate Agent Survey Activity Rating through 2017, where we ask the sample of agents surveyed to give a rating to how they perceive activity in the market, on a scale of 1 to 10. By the 4 th quarter of 2017, this rating had declined to 5.29, down from a multi-year high of 6.78 reached back in early-2014, and the lowest Activity Rating since the 2 nd quarter of In addition to activity declining, the agents had reported a steady rise in the average time of homes on the market to a multi-year high of 17 weeks and 2 days by the final quarter of 2017, from less than 12 weeks early in 2016, implying a market moving further away from equilibrium between demand and supply towards an oversupplied market. These indicators by-and-large explain the weak year-on-year house price growth in early-2018, and the month-onmonth house price decline, with last year s weak market fundamentals still feeding through to house prices with a lag. However, we remain of the expectation that 2018 will be a mildly stronger year for the housing market and house price growth, projecting a 4.8% average growth rate for 2018 after a lower 3.8% for last year.

3 The signs are still there for an improved economic performance this year. Business Confidence in the country appears to have been boosted by the leadership change in the ruling party in December 2017, and now further by the composition of President Ramaphosa s cabinet, especially by the return of business-popular Ministers Nene and Gordhan to key cabinet posts. The Rand continues to perform solidly, a reflection of this improved sentiment, and it is likely that Consumer Confidence will move in a similar direction. Furthermore, with CPI inflation at a lowly 4.4% year-on-year in February, and the Rand s stronger performance likely to curb imported inflationary pressures going forward, the prospect is not only for mildly stronger economic growth, nearer to 1.5%, in 2018, but also an increased possibility of a further interest rate reduction. Nothing economically look very strong, just mildly better than where we come from, and mildly better for the economy probably means mildly better for the housing market.

4

5 ADDENDUM - NOTES: Note on The FNB Average House Price Index: Although also working on the average price principle (as opposed to median or repeat sales), the FNB House Price Index differs from a simple average house price index in that it could probably be termed a fixed weight average house price index. One of the practical problems we have found with house price indices is that relative short term activity shifts up and down the price ladder can lead to an average or median price index rising or declining where there was not necessarily genuine capital growth on homes. For example, if Full Title 3 Bedroom volumes remain unchanged from one month to the next, but Sectional Title 1 Bedroom and Less (the cheapest segment on average) transaction volumes hypothetically double, the overall national average price could conceivably decline due to this relative activity shift. This challenge of activity shifts between segments is faced by all constructors of house price indices. In an attempt to reduce this effect, we decided to fix the weightings of the FNB House Price Index s sub-segments in the overall national index. This, at best, can only be a partial solution, as activity shifts can still take place between smaller segments within the sub-segments. However, it does improve the situation. With our 2013 re-weighting exercise, we have begun to segment not only according to room number, but also to segment according to building size within the normal segments by room number, in order to further reduce the impact of activity shifts on average price estimates. The FNB House Price Index s main segments are now as follows: The weightings of the sub-segments are determined by their relative transaction volumes over the past 5 years, and will now change very slowly over time by applying a 5-year moving average to each new price data point. The sub-segments are: - Sectional Title: Less than 2 bedroom Large Less than 2 bedroom Medium Less than 2 bedroom Small 2 Bedroom Large 2 bedroom Medium 2 bedroom Small 3 Bedroom and More - Large 3 Bedroom and More - Medium 3 Bedroom and More - Small - Full Title: 2 Bedrooms and Less - Large 2 Bedrooms and Less - Medium 2 Bedrooms and Less - Small 3 Bedroom - Large 3 Bedroom - Medium 3 Bedroom - Small 4 Bedrooms and More - Large 4 Bedrooms and More - Medium 4 Bedrooms and More Small

6 The size cut-offs for small, medium and large differ per room number sub-segment. Large would refer to the largest one-third of homes within a particular room number segment over the past 5 year period, Medium to the middle one-third, and Small to the smallest one-third of homes within that segment. The Index is constructed using transaction price data from homes financed by FNB. The minimum size cut-off for full title stands is 200 square metres, and the maximum size is 4000 square metres The maximum price cut-off is R10m, and the lower price cut-off is R20,000 (largely to eliminate major outliers and glaring inputting errors). The index is very lightly smoothed using a Hodrick-Prescott smoothing function with a Lambda of 5.

PROPERTY BAROMETER FNB House Price Index The FNB House Price Index s year-on-year growth slowed in January, after prior months of acceleration

1 February 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254 thulani.luvuno@fnb.co.za

1 February 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254 thulani.luvuno@fnb.co.za

PROPERTY BAROMETER House Price Indices by Segment

PROPERTY BAROMETER House Price Indices by Segment The Sectional Title Housing Market Segment still mildly outperforms the Full Title Segment, and the Less than 2 Bedroom Sectional Title Sub-Segment has

PROPERTY BAROMETER House Price Indices by Segment The Sectional Title Housing Market Segment still mildly outperforms the Full Title Segment, and the Less than 2 Bedroom Sectional Title Sub-Segment has

1 March 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT. JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST

1 March 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST 087-328 0157 tswanepoel@fnb.co.za

1 March 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST 087-328 0157 tswanepoel@fnb.co.za

1 February 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT. JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST

1 February 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST 087-328 0157

1 February 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST 087-328 0157

PROPERTY BAROMETER. FNB Home Buying Estate Agent Survey Agents saw further market weakness in the 4 th quarter 2017 survey, but this may change soon

23 January 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za LIZE ERASMUS: STATISTICIAN 087-335 6664 lize.erasmus@@fnb.co.za

23 January 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za LIZE ERASMUS: STATISTICIAN 087-335 6664 lize.erasmus@@fnb.co.za

PROPERTY BAROMETER FNB Mining Towns House Price Indices

PROPERTY BAROMETER FNB Mining Towns House Price Indices The FNB Mining Towns House Price Index continues to point to slowing growth, and underperformance in these towns housing markets relative to the

PROPERTY BAROMETER FNB Mining Towns House Price Indices The FNB Mining Towns House Price Index continues to point to slowing growth, and underperformance in these towns housing markets relative to the

3 July 2018 THE FNB HOUSEHOLD SECTOR DEBT-SERVICE RISK INDEX

3 July 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254 thulani.luvuno@fnb.co.za

3 July 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254 thulani.luvuno@fnb.co.za

FNB PROPERTY MARKET ANALYTICS

1 June 21 FNB MAY HOUSE PRICE INDEX AND PROPERTY ECONOMIC REVIEW - Price growth acceleration continues, with expected peak believed to be nearing MARKET ANALYTICS JOHN LOOS: FNB HOME LOANS STRATEGIST 11-64912

1 June 21 FNB MAY HOUSE PRICE INDEX AND PROPERTY ECONOMIC REVIEW - Price growth acceleration continues, with expected peak believed to be nearing MARKET ANALYTICS JOHN LOOS: FNB HOME LOANS STRATEGIST 11-64912

8 June 2017 KEY POINTS

8 June 2017 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za LIZE ERASMUS: STATISTICIAN 087-335 6664 lize.erasmus@fnb.co.za

8 June 2017 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za LIZE ERASMUS: STATISTICIAN 087-335 6664 lize.erasmus@fnb.co.za

HOUSEHOLD SECTOR FINANCIAL VULNERABILITY

September 213 JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST: FNB HOME LOANS 11-12 John.loos@fnb.co.za The information in this publication is derived from sources which are regarded as accurate and

September 213 JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST: FNB HOME LOANS 11-12 John.loos@fnb.co.za The information in this publication is derived from sources which are regarded as accurate and

18 June 2018 KEY POINTS

18 June 2018 FNB HOME LOANS: MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 John.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254

18 June 2018 FNB HOME LOANS: MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 John.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254

MORTGAGE MARKET BAROMETER

29 January 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST: FNB HOME LOANS 087-328 0151 John.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST

29 January 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST: FNB HOME LOANS 087-328 0151 John.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST

20 June 2017 KEY POINTS

20 June 2017 FNB HOME LOANS: MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 John.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST

20 June 2017 FNB HOME LOANS: MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 John.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST

PROPERTY BAROMETER FNB HOME BUYING ESTATE AGENT SURVEY RAND AREA

22 September 2015 FNB HOME LOANS: MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 John.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST

22 September 2015 FNB HOME LOANS: MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 John.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST

PROPERTY MARKETS The FNB August House Price Index

PROPERTY MARKETS The FNB August House Price Index - Slowing house price inflation as should be expected, but Residential Market Weakness is not fully reflected in house price trends 4 September JOHN LOOS:

PROPERTY MARKETS The FNB August House Price Index - Slowing house price inflation as should be expected, but Residential Market Weakness is not fully reflected in house price trends 4 September JOHN LOOS:

HOUSEHOLD SECTOR CREDIT RISK

HOME LOANS DIVISION HOUSEHOLD SECTOR CREDIT RISK While household sector credit quality may well be improving, risks remain high. PROPERTY MARKET ANALYTICS John Loos: Strategist 11-9 1 john.loos@fnb.co.za

HOME LOANS DIVISION HOUSEHOLD SECTOR CREDIT RISK While household sector credit quality may well be improving, risks remain high. PROPERTY MARKET ANALYTICS John Loos: Strategist 11-9 1 john.loos@fnb.co.za

SIGNS EMERGING OF A DELIBERATELY MORE CONSERVATIVE CONSUMER

HOUSEHOLD SECTOR HOUSEHOLD SECTOR FINANCES Ironically, perhaps, tougher economic and financial times are more likely to bring about a higher savings rate than the good times, despite it being theoretically

HOUSEHOLD SECTOR HOUSEHOLD SECTOR FINANCES Ironically, perhaps, tougher economic and financial times are more likely to bring about a higher savings rate than the good times, despite it being theoretically

PROPERTY BAROMETER FNB Gauteng Sub-Region House Price Indices

27 March 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254 thulani.luvuno@fnb.co.za

27 March 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254 thulani.luvuno@fnb.co.za

7 January Affordability of housing

7 January 2015 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST FNB HOME LOANS 011-6490125 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST

7 January 2015 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST FNB HOME LOANS 011-6490125 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST

PROPERTY BAROMETER Residential Market Stability Risk Review Residential Market stability risk continued its recent decline (improvement)

") 23 June 2017 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za LIZE ERASMUS: STATISTICIAN 087-335 6664 lize.erasmus@@fnb.co.za

23 June 2017 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za LIZE ERASMUS: STATISTICIAN 087-335 6664 lize.erasmus@@fnb.co.za

PROPERTY MARKETS. BEHIND THE DEMAND FOR HOUSING - An update on the Household sector s financial health

PROPERTY MARKETS BEHIND THE DEMAND FOR HOUSING - An update on the Household sector s financial health 11 September 2 JOHN LOOS: FNB HOME LOANS PROPERTY STRATEGIST 11-6912 John.loos@fnb.co.za The information

PROPERTY MARKETS BEHIND THE DEMAND FOR HOUSING - An update on the Household sector s financial health 11 September 2 JOHN LOOS: FNB HOME LOANS PROPERTY STRATEGIST 11-6912 John.loos@fnb.co.za The information

The ECB Survey of Professional Forecasters. Second quarter of 2017

The ECB Survey of Professional Forecasters Second quarter of 17 April 17 Contents 1 Near-term headline inflation expectations revised up, expectations for HICP inflation excluding food and energy broadly

The ECB Survey of Professional Forecasters Second quarter of 17 April 17 Contents 1 Near-term headline inflation expectations revised up, expectations for HICP inflation excluding food and energy broadly

Release Date : 26 February Economic update - January Key data highlights:

Release Date : 26 February 218 Economic update - uary 218 Key data highlights:. While uary figures showed an increase in consumer confidence and improvement in wage growth, the underlying long-term picture

Release Date : 26 February 218 Economic update - uary 218 Key data highlights:. While uary figures showed an increase in consumer confidence and improvement in wage growth, the underlying long-term picture

Ulster Bank Northern Ireland PMI

Embargoed until 0101 (UK) 14 January 2019 Ulster Bank Northern Ireland PMI New orders stagnate in December Key Findings No change in new business ends 25-month sequence of growth Further solid rises in

Embargoed until 0101 (UK) 14 January 2019 Ulster Bank Northern Ireland PMI New orders stagnate in December Key Findings No change in new business ends 25-month sequence of growth Further solid rises in

Ulster Bank Northern Ireland PMI

Embargoed until 0101 UK (0001 UTC) 10 September 2018 Ulster Bank Northern Ireland PMI New orders rise at weakest pace in four months Key Findings Weaker growth of output and new orders Further increase

Embargoed until 0101 UK (0001 UTC) 10 September 2018 Ulster Bank Northern Ireland PMI New orders rise at weakest pace in four months Key Findings Weaker growth of output and new orders Further increase

In this report we discuss three important areas of the economy that have received a great deal of attention recently, namely:

March 26, 218 Executive Summary George Mokrzan, PH.D., Director of Economics In this report we discuss three important areas of the economy that have received a great deal of attention recently, namely:

March 26, 218 Executive Summary George Mokrzan, PH.D., Director of Economics In this report we discuss three important areas of the economy that have received a great deal of attention recently, namely:

MONTH IN PICTURES JULY 2018

MONTH IN PICTURES JULY 2018 MONTHLY SNAPSHOT NOTABLE EVENTS Boosted by strong returns from Financials (+4.7%), the local equity market ended in positive territory in July (+1.4%), despite negative returns

MONTH IN PICTURES JULY 2018 MONTHLY SNAPSHOT NOTABLE EVENTS Boosted by strong returns from Financials (+4.7%), the local equity market ended in positive territory in July (+1.4%), despite negative returns

Summary. Editor: Tristan Zhuo Senior Economist Phone:

Summary Editor: Tristan Zhuo Senior Economist Phone: +852 2826 6193 Email: tristanzhuo@bochk.com China s macro economy stabilized in May, and growth in the second quarter appears to be similar with the

Summary Editor: Tristan Zhuo Senior Economist Phone: +852 2826 6193 Email: tristanzhuo@bochk.com China s macro economy stabilized in May, and growth in the second quarter appears to be similar with the

Q3 SME Cost Inflation Report November 2013

Q3 SME Cost Inflation Report November 2013 Helping your business stay one step ahead through our insight Research Contents Executive Summary 3 4 6 20 22 Executive Summary UK Economic Overview SME Cost

Q3 SME Cost Inflation Report November 2013 Helping your business stay one step ahead through our insight Research Contents Executive Summary 3 4 6 20 22 Executive Summary UK Economic Overview SME Cost

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 2018

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

Indicator Watch for the South African Commercial Property Market Cycle

Indicator Watch for the South African Commercial Property Market Cycle April 2017 Cycle Position Summary Recent political events and the downgrading of South Africa s international credit rating have led

Indicator Watch for the South African Commercial Property Market Cycle April 2017 Cycle Position Summary Recent political events and the downgrading of South Africa s international credit rating have led

Monetary Policy Statement 1

Monetary Policy Statement 1 June 1997 This Statement is made pursuant to Section 15 of the Reserve Bank of New Zealand Act 1989. Contents I. Summary and policy assessment 2 II. Issues in monetary policy

Monetary Policy Statement 1 June 1997 This Statement is made pursuant to Section 15 of the Reserve Bank of New Zealand Act 1989. Contents I. Summary and policy assessment 2 II. Issues in monetary policy

Global PMI. Global economy set for robust Q2 growth. June 8 th IHS Markit. All Rights Reserved.

Global PMI Global economy set for robust Q2 growth June 8 th 2017 2 PMI indicates robust global growth in Q2 The global economy is on course for a robust second quarter, according to PMI survey data. The

Global PMI Global economy set for robust Q2 growth June 8 th 2017 2 PMI indicates robust global growth in Q2 The global economy is on course for a robust second quarter, according to PMI survey data. The

Ulster Bank Northern Ireland PMI

Embargoed until 0101 UK (0001 UTC) 13 August 2018 Ulster Bank Northern Ireland PMI Fastest rise in output since January Key Findings Sharper increases in both output and new orders Slowest rise in employment

Embargoed until 0101 UK (0001 UTC) 13 August 2018 Ulster Bank Northern Ireland PMI Fastest rise in output since January Key Findings Sharper increases in both output and new orders Slowest rise in employment

Outlook for the Japanese Economy in 2007

VOL2.NO.2 January 2007 Outlook for the Japanese Economy in 2007 Economic recovery surpasses Izanagi in length The economy is continuing its longest post-war economic recovery. Nearly five years have passed

VOL2.NO.2 January 2007 Outlook for the Japanese Economy in 2007 Economic recovery surpasses Izanagi in length The economy is continuing its longest post-war economic recovery. Nearly five years have passed

SME Monitor Q aldermore.co.uk

SME Monitor Q1 2014 aldermore.co.uk aldermore.co.uk Contents Executive summary UK economic overview SME inflation index one year review SME cost inflation trends SME business confidence SME credit conditions

SME Monitor Q1 2014 aldermore.co.uk aldermore.co.uk Contents Executive summary UK economic overview SME inflation index one year review SME cost inflation trends SME business confidence SME credit conditions

Growth Investing. in Times of Market Volatility. White Paper

White Paper Growth Investing in Times of Market Volatility April 2018 Executive Summary Many investors may be dismayed by the volatile nature of high-flying growth stocks. While, by definition, growth

White Paper Growth Investing in Times of Market Volatility April 2018 Executive Summary Many investors may be dismayed by the volatile nature of high-flying growth stocks. While, by definition, growth

Release Date : 26 June Economic update - May Key data highlights:

Release Date : 26 June Economic update - Key data highlights:. The UK economy is growing at its slowest pace in more than five years, marked by weaker manufacturing and construction growth. Consumer-facing

Release Date : 26 June Economic update - Key data highlights:. The UK economy is growing at its slowest pace in more than five years, marked by weaker manufacturing and construction growth. Consumer-facing

Domestic demand shows signs of life

Produced by the Economic Research Unit January 2013 A quarterly analysis of trends in the Irish economy Domestic demand shows signs of life Group Chief Economist: Dan McLaughlin 0.8% rise in GDP still

Produced by the Economic Research Unit January 2013 A quarterly analysis of trends in the Irish economy Domestic demand shows signs of life Group Chief Economist: Dan McLaughlin 0.8% rise in GDP still

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Highlights. Contact. The key data in review. Date Country Release/event Period Actual Prior

1 April 216 Contact Mamello Matikinca Economist 87 33 1678 Mamello.matikinca@fnb.co.za Jason Muscat Industry Analyst 87 33 189 Jason.Muscat@fnb.co.za Jarred Sullivan Economist 87 328 622 Jarred Sullivan@fnb.co.za

1 April 216 Contact Mamello Matikinca Economist 87 33 1678 Mamello.matikinca@fnb.co.za Jason Muscat Industry Analyst 87 33 189 Jason.Muscat@fnb.co.za Jarred Sullivan Economist 87 328 622 Jarred Sullivan@fnb.co.za

Victorian Economic Outlook

Tuesday, August 1 Victorian Economic Outlook Summary The Victorian economy has had its fair share of headwinds in recent years, but the tide may be turning. For some time, we have been optimistic that

Tuesday, August 1 Victorian Economic Outlook Summary The Victorian economy has had its fair share of headwinds in recent years, but the tide may be turning. For some time, we have been optimistic that

Global PMI. Solid Q2 growth masks widening growth differentials. July 7 th IHS Markit. All Rights Reserved.

Global PMI Solid Q2 growth masks widening growth differentials July 7 th 2017 2 Widening developed and emerging world growth trends The global economy enjoyed further steady growth in June, according to

Global PMI Solid Q2 growth masks widening growth differentials July 7 th 2017 2 Widening developed and emerging world growth trends The global economy enjoyed further steady growth in June, according to

2015: FINALLY, A STRONG YEAR

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 10 May 2017

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 10 May 2017 Publication date: 11 May 2017 These are the minutes of the Monetary Policy Committee meeting ending on

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 10 May 2017 Publication date: 11 May 2017 These are the minutes of the Monetary Policy Committee meeting ending on

Outlook for Economic Activity and Prices (April 2010)

") April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

Outlook and Market Review Third Quarter 2018

Outlook and Market Review Third Quarter The U. S. economy grew at a 3.5% rate in the third quarter of following a 4.2% growth rate in the prior quarter, according to the revision by the Bureau of Economic

Outlook and Market Review Third Quarter The U. S. economy grew at a 3.5% rate in the third quarter of following a 4.2% growth rate in the prior quarter, according to the revision by the Bureau of Economic

Provided to you by Lee McLain

Provided to you by Lee McLain Lee McLain First Federal Bank of Kansas City 816.728.7700 lee.mclain@ffbkc.com NMLS:680316 Contents Weekly Review: week of November 26, 2018 Economic Calendar - week of December

Provided to you by Lee McLain Lee McLain First Federal Bank of Kansas City 816.728.7700 lee.mclain@ffbkc.com NMLS:680316 Contents Weekly Review: week of November 26, 2018 Economic Calendar - week of December

The real change in private inventories added 0.15 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy rebounded in the second quarter of 2007, growing at an annual rate of 3.4% Q/Q (+1.8% Y/Y), according to the GDP advance estimates

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy rebounded in the second quarter of 2007, growing at an annual rate of 3.4% Q/Q (+1.8% Y/Y), according to the GDP advance estimates

Release Date : 26 April Economic update - March Key data highlights:

Release Date : 26 April Economic update - ch Key data highlights:. The headline figures in ch showed positive developments across key economic fundamentals, pointing to normalising economic conditions.

Release Date : 26 April Economic update - ch Key data highlights:. The headline figures in ch showed positive developments across key economic fundamentals, pointing to normalising economic conditions.

Growth to accelerate. A quarterly analysis of trends in the Irish economy

Produced by the Economic Research Unit July 2014 A quarterly analysis of trends in the Irish economy Growth to accelerate Strong start to 2014 Recovery becoming more broad-based GDP growth revised up for

Produced by the Economic Research Unit July 2014 A quarterly analysis of trends in the Irish economy Growth to accelerate Strong start to 2014 Recovery becoming more broad-based GDP growth revised up for

Quarterly Economics Briefing

Quarterly Economics Briefing September March 2015 Review of Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic

Quarterly Economics Briefing September March 2015 Review of Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic

China Economic Update Q April 27, 2018

il 27, 2018 Key Developments in Brief Economic Development Drivers of Growth Risks Predicted GDP growth of 6.5% in Service and modern production Corporate debt, esp. stateowned 2018 grow fast enterprises

il 27, 2018 Key Developments in Brief Economic Development Drivers of Growth Risks Predicted GDP growth of 6.5% in Service and modern production Corporate debt, esp. stateowned 2018 grow fast enterprises

Retail Sales, Gasoline Price and the Impact of Brexit

July 20, 2016 : Retail Sales, Gasoline Price and the Impact of Brexit US US retail sales rose by more than had been expected in June as Americans bought furniture and spent more at gas stations, pointing

July 20, 2016 : Retail Sales, Gasoline Price and the Impact of Brexit US US retail sales rose by more than had been expected in June as Americans bought furniture and spent more at gas stations, pointing

The ECB Survey of Professional Forecasters. First quarter of 2018

The ECB Survey of Professional Forecasters First quarter of 218 January 218 Contents 1 Both HICP inflation and HICP excluding food and energy inflation expected to pick up steadily over the period 218-2

The ECB Survey of Professional Forecasters First quarter of 218 January 218 Contents 1 Both HICP inflation and HICP excluding food and energy inflation expected to pick up steadily over the period 218-2

The Economy is Solid!

THE ECONOMY IN 2018: PROBABLY BETTER THAN IN 2017 Presented by: Elliot F. Eisenberg, Ph.D. President: GraphsandLaughs, LLC April 19, 2018 Napa, CA The Economy is Solid! GDP = C+I+G+(X-M) The Stock Market

THE ECONOMY IN 2018: PROBABLY BETTER THAN IN 2017 Presented by: Elliot F. Eisenberg, Ph.D. President: GraphsandLaughs, LLC April 19, 2018 Napa, CA The Economy is Solid! GDP = C+I+G+(X-M) The Stock Market

Real Gross Domestic Product (GDP) of Hong Kong increased 0.9 percent in the first half

of Hong Kong increased 0.9 percent in the first half") Economic Prospects of Hong Kong in 2012-13 Win Lin Chou, City University of Hong Kong Prepared for United Nations Project LINK Meeting in New York, October 22-24, 2012 I. The Current Trends Real Gross

Economic Prospects of Hong Kong in 2012-13 Win Lin Chou, City University of Hong Kong Prepared for United Nations Project LINK Meeting in New York, October 22-24, 2012 I. The Current Trends Real Gross

The shape of the pending recovery

Sizwe Nxedlana Research Economics Economist sizwe.nxedlana@fnbcommercial.co.za (011) 352 3276 The shape of the pending recovery Domestic expenditure deteriorated in the second quarter Real expenditure

Sizwe Nxedlana Research Economics Economist sizwe.nxedlana@fnbcommercial.co.za (011) 352 3276 The shape of the pending recovery Domestic expenditure deteriorated in the second quarter Real expenditure

FOR RELEASE: 10:00 A.M. (PARIS TIME), MONDAY, DECEMBER 19, 2011

, MONDAY, DECEMBER 19, 2011") FOR RELEASE: 10:00 A.M. (PARIS TIME), MONDAY, DECEMBER 19, 2011 The Conference Board France Business Cycle Indicators SM THE CONFERENCE BOARD LEADING ECONOMIC INDEX (LEI) FOR FRANCE AND RELATED COMPOSITE

FOR RELEASE: 10:00 A.M. (PARIS TIME), MONDAY, DECEMBER 19, 2011 The Conference Board France Business Cycle Indicators SM THE CONFERENCE BOARD LEADING ECONOMIC INDEX (LEI) FOR FRANCE AND RELATED COMPOSITE

The ECB Survey of Professional Forecasters (SPF) First quarter of 2016

First quarter of 2016") The ECB Survey of Professional Forecasters (SPF) First quarter of 16 January 16 Content 1 Inflation expectations maintain upward profile but have been revised down for 16 and 17 3 2 Longer-term inflation

The ECB Survey of Professional Forecasters (SPF) First quarter of 16 January 16 Content 1 Inflation expectations maintain upward profile but have been revised down for 16 and 17 3 2 Longer-term inflation

Outlook 2013: China. Growth expected to accelerate again

Outlook 13: China Growth expected to accelerate again Weakened external demand and only limited growth supporting policies from the Chinese government were the main factors explaining China s slowing growth

Outlook 13: China Growth expected to accelerate again Weakened external demand and only limited growth supporting policies from the Chinese government were the main factors explaining China s slowing growth

Outlook for Economic Activity and Prices

Not to be released until : p.m. Japan Standard Time on Saturday, October 31, 15. October 31, 15 Bank of Japan Outlook for Economic Activity and Prices October 15 (English translation prepared by the Bank's

Not to be released until : p.m. Japan Standard Time on Saturday, October 31, 15. October 31, 15 Bank of Japan Outlook for Economic Activity and Prices October 15 (English translation prepared by the Bank's

Outlook for the Hawai'i Economy

Outlook for the Hawai'i Economy May 3, 2001 Dr. Carl Bonham University of Hawai'i Economic Research Organization Summary The Hawaii economy entered 2001 in its best shape in more than a decade. While the

Outlook for the Hawai'i Economy May 3, 2001 Dr. Carl Bonham University of Hawai'i Economic Research Organization Summary The Hawaii economy entered 2001 in its best shape in more than a decade. While the

Advanced Market Analysis for Commercial Real Estate

Ward Center for Real Estate Studies www.ccim.com Advanced Market Analysis for Commercial Real Estate PPT Handout EXCELLENCE SUCCESS SKILL LEADERSHIP CHALLENGE STRENGTH Copyright 2012 by the CCIM Institute

Ward Center for Real Estate Studies www.ccim.com Advanced Market Analysis for Commercial Real Estate PPT Handout EXCELLENCE SUCCESS SKILL LEADERSHIP CHALLENGE STRENGTH Copyright 2012 by the CCIM Institute

Release date : 28 December Economic update - December Key data highlights:

Economic update - December Key data highlights:. ember saw inflation fall slightly to 2.3 per cent, reducing the likelihood of a Bank Rate rise from 0.75 per cent. Consumers remain wary of their day-to-day

Economic update - December Key data highlights:. ember saw inflation fall slightly to 2.3 per cent, reducing the likelihood of a Bank Rate rise from 0.75 per cent. Consumers remain wary of their day-to-day

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

Economic recovery dashboard

CURRENT AS OF OCTOBER 31, 2009 Economic recovery dashboard Summary of current state Market indicators Most indicators changed little over the previous month. VIX increased, closing the month at 30.69,

CURRENT AS OF OCTOBER 31, 2009 Economic recovery dashboard Summary of current state Market indicators Most indicators changed little over the previous month. VIX increased, closing the month at 30.69,

The Productivity to Paycheck Gap: What the Data Show

The Productivity to Paycheck Gap: What the Data Show The Real Cause of Lagging Wages Dean Baker April 2007 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite 400 Washington, D.C.

The Productivity to Paycheck Gap: What the Data Show The Real Cause of Lagging Wages Dean Baker April 2007 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite 400 Washington, D.C.

Office Market Analysis

Q1 2015 Accelerating success. Office Market Analysis Western Cape Report Contents Highlights 1 Summary 2 Statistics 2 Climate 3 Supply 5 Demand 8 Vacancies 9 Western Cape Rental Rates 10 Prognosis 11 Report

Q1 2015 Accelerating success. Office Market Analysis Western Cape Report Contents Highlights 1 Summary 2 Statistics 2 Climate 3 Supply 5 Demand 8 Vacancies 9 Western Cape Rental Rates 10 Prognosis 11 Report

Erdem Başçi: Recent economic and financial developments in Turkey

Erdem Başçi: Recent economic and financial developments in Turkey Speech by Mr Erdem Başçi, Governor of the Central Bank of the Republic of Turkey, at the press conference for the presentation of the April

Erdem Başçi: Recent economic and financial developments in Turkey Speech by Mr Erdem Başçi, Governor of the Central Bank of the Republic of Turkey, at the press conference for the presentation of the April

Q Catastrophe Bond & ILS Market Report

Q3 214 Catastrophe Bond & ILS Market Report A lazy summer for ILS ARTEMIS Focused on insurance-linked securities (ILS), catastrophe bonds, alternative reinsurance capital and related risk transfer markets.

Q3 214 Catastrophe Bond & ILS Market Report A lazy summer for ILS ARTEMIS Focused on insurance-linked securities (ILS), catastrophe bonds, alternative reinsurance capital and related risk transfer markets.

The ECB Survey of Professional Forecasters. First quarter of 2017

The ECB Survey of Professional Forecasters First quarter of 217 January 217 Contents 1 Near-term inflation expectations a little higher, due to oil price rises 3 2 Longer-term inflation expectations unchanged

The ECB Survey of Professional Forecasters First quarter of 217 January 217 Contents 1 Near-term inflation expectations a little higher, due to oil price rises 3 2 Longer-term inflation expectations unchanged

U.S. Economy Update. March Monthly Update Based On Leading Regional Manufacturing Indices.

U.S. Economy Update March 2018 Monthly Update Based On Leading Regional Manufacturing Indices What Is This Report About? (1/2) This presentation is discussing the latest results of the five most important

U.S. Economy Update March 2018 Monthly Update Based On Leading Regional Manufacturing Indices What Is This Report About? (1/2) This presentation is discussing the latest results of the five most important

Home Loans. Housing review Fourth quarter 2016

Home Loans Contents Economic overview 2 Household sector overview 2 Property sector overview House prices Building costs Land values 7 Affordability of housing 7 Outlook 7 Graphs 9 Statistics 11 Compiled

Home Loans Contents Economic overview 2 Household sector overview 2 Property sector overview House prices Building costs Land values 7 Affordability of housing 7 Outlook 7 Graphs 9 Statistics 11 Compiled

Baseline U.S. Economic Outlook, Summary Table*

December 18 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Continued Solid Job Growth;

December 18 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Continued Solid Job Growth;

Business in Britain. A survey of opinions and trends 50th edition June For your next step

Business in Britain A survey of opinions and trends th edition June 17 For your next step OUR CONTRIBUTORS CONTENTS 3 INTRODUCTION 4 EXECUTIVE SUMMARY Hann-Ju Ho Senior Economist Economic Research Lloyds

Business in Britain A survey of opinions and trends th edition June 17 For your next step OUR CONTRIBUTORS CONTENTS 3 INTRODUCTION 4 EXECUTIVE SUMMARY Hann-Ju Ho Senior Economist Economic Research Lloyds

PROPERTY INSIGHTS. Market Overview. Subdued economic growth dampen investment sentiments. Citigold Private Client

Citigold Private Client PROPERTY INSIGHTS Malaysia Quarter 2, 2016 Subdued economic growth dampen investment sentiments Market Overview Malaysia s economy grew at a slower pace in Q1 2016 due to slower

Citigold Private Client PROPERTY INSIGHTS Malaysia Quarter 2, 2016 Subdued economic growth dampen investment sentiments Market Overview Malaysia s economy grew at a slower pace in Q1 2016 due to slower

HKU Announced 2011 Q3 HK Macroeconomic Forecast

COMMUNICATIONS & PUBLIC AFFAIRS OFFICE THE UNIVERSITY OF HONG KONG Enquiry: 2859 1106 Website: http://www.hku.hk/cpao For Immediate Release HKU Announced 2011 Q3 HK Macroeconomic Forecast Economic Outlook

COMMUNICATIONS & PUBLIC AFFAIRS OFFICE THE UNIVERSITY OF HONG KONG Enquiry: 2859 1106 Website: http://www.hku.hk/cpao For Immediate Release HKU Announced 2011 Q3 HK Macroeconomic Forecast Economic Outlook

The Regional Economist January Inflation: Ijrooo.Ijror ijnouani. By William T. Gavin and Rachel J. Mandal

The Regional Economist January 2002 Inflation: Ijrooo.Ijror ijnouani By William T. Gavin and Rachel J. Mandal "When I was your age, I walked 20 miles uphill in the snow to get to school and a gallon of

The Regional Economist January 2002 Inflation: Ijrooo.Ijror ijnouani By William T. Gavin and Rachel J. Mandal "When I was your age, I walked 20 miles uphill in the snow to get to school and a gallon of

Growth and Inflation Prospects and Monetary Policy

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

October 2014 Strong Dollar Effects to Investors Dollar Trend Forecast

October 2014 Strong Dollar Effects to Investors In last month investment report, we have discussed our view for the dollar trend in the next 1 to 2 years (We said that following the changing monetary policy,

October 2014 Strong Dollar Effects to Investors In last month investment report, we have discussed our view for the dollar trend in the next 1 to 2 years (We said that following the changing monetary policy,

Inflation Outlook and Monetary Easing

Thomas Shik Acting Chief Economist thomasshik@hangseng.com Inflation Outlook and Monetary Easing Although annual consumer price inflation rose for a second consecutive month in July, the underlying trend

Thomas Shik Acting Chief Economist thomasshik@hangseng.com Inflation Outlook and Monetary Easing Although annual consumer price inflation rose for a second consecutive month in July, the underlying trend

MYTH BUSTING COMMENTARY MYTH 1: THE YIELD CURVE KEY TAKEAWAYS LPL RESEARCH WEEKLY MARKET. April

LPL RESEARCH WEEKLY MARKET COMMENTARY April 23 2018 MYTH BUSTING John Lynch Chief Investment Strategist, LPL Financial Ryan Detrick, CMT Senior Market Strategist, LPL Financial KEY TAKEAWAYS The underlying

LPL RESEARCH WEEKLY MARKET COMMENTARY April 23 2018 MYTH BUSTING John Lynch Chief Investment Strategist, LPL Financial Ryan Detrick, CMT Senior Market Strategist, LPL Financial KEY TAKEAWAYS The underlying

US Economy Update May 2014

US Economy Update May 2014 MACRO REPORT Key Insights Monica Defend Head of Global Asset Allocation Research Annalisa Usardi Economist, US & LATAM Global Asset Allocation Research Also contributing Riccardo

US Economy Update May 2014 MACRO REPORT Key Insights Monica Defend Head of Global Asset Allocation Research Annalisa Usardi Economist, US & LATAM Global Asset Allocation Research Also contributing Riccardo

Banks at a Glance: Alaska

Banks at a Glance: Financial Institution Supervision and Credit sf.fisc.publications@sf.frb.org Economic and Banking Highlights Data as of 12/31/216 's economy continued to struggle, driven by weaknesses

Banks at a Glance: Financial Institution Supervision and Credit sf.fisc.publications@sf.frb.org Economic and Banking Highlights Data as of 12/31/216 's economy continued to struggle, driven by weaknesses

4. Economic Outlook. ASSUMPTIONS AND SCENARIOS Condition of the International Economy World economic growth is predicted. to remain strong in 2007,

Monetary Policy Report - Quarter II-2007 4. Economic Outlook Overall, the accelerated pace of economic growth of 2007-2008 is predicted to carry forward, being accompanied by sustained macroeconomic stability.

Monetary Policy Report - Quarter II-2007 4. Economic Outlook Overall, the accelerated pace of economic growth of 2007-2008 is predicted to carry forward, being accompanied by sustained macroeconomic stability.

NEDGROUP INVESTMENTS PROPERTY FUND. Quarter One, 2018

NEDGROUP INVESTMENTS PROPERTY FUND Quarter One, 2018 For the period ended 31 March 2018 NEDGROUP INVESTMENTS PROPERTY FUND PERFORMANCE Performance to 31 March 2018 Nedgroup Investments Property Fund 1

NEDGROUP INVESTMENTS PROPERTY FUND Quarter One, 2018 For the period ended 31 March 2018 NEDGROUP INVESTMENTS PROPERTY FUND PERFORMANCE Performance to 31 March 2018 Nedgroup Investments Property Fund 1

Cycle Monitor Real Estate Market Cycles

Cycle Monitor Real Estate Market Cycles First Quarter 2012 Analysis May 2012 Physical Market Cycle Analysis of All Five Major Property Types in More Than 50 MSAs. Job growth slowed back to the 100,000

Cycle Monitor Real Estate Market Cycles First Quarter 2012 Analysis May 2012 Physical Market Cycle Analysis of All Five Major Property Types in More Than 50 MSAs. Job growth slowed back to the 100,000

Phoenix Management Services Lending Climate in America Survey

Phoenix Management Services Lending Climate in America Survey 2 nd Quarter 2016 Summary, Trends and Implications PHOENIX LENDING CLIMATE IN AMERICA 2 nd Quarter 2016 SUMMARY, TRENDS AND IMPLICATIONS 1.

Phoenix Management Services Lending Climate in America Survey 2 nd Quarter 2016 Summary, Trends and Implications PHOENIX LENDING CLIMATE IN AMERICA 2 nd Quarter 2016 SUMMARY, TRENDS AND IMPLICATIONS 1.

The President s Report to the Board of Directors

The President s Report to the Board of Directors April 4, 214 Current Economic Developments - April 4, 214 Data released since your last Directors' meeting show the economy was a bit stronger in the fourth

The President s Report to the Board of Directors April 4, 214 Current Economic Developments - April 4, 214 Data released since your last Directors' meeting show the economy was a bit stronger in the fourth

Minutes of the Monetary Policy Committee meeting, August 2018

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, August 2018 Published 12 September 2018 The Act on the Central Bank of Iceland stipulates

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, August 2018 Published 12 September 2018 The Act on the Central Bank of Iceland stipulates

HOTEL CONTINUES ON A POSITIVE TRACK TRENDS FOR DEMAND AND ADR REMAIN SOLID, BUT COMING DELIVERIES REMAIN A CONCERN

HOTEL MARKET REPORT: 3Q2013 HOTEL CONTINUES ON A POSITIVE TRACK TRENDS FOR DEMAND AND ADR REMAIN SOLID, BUT COMING DELIVERIES REMAIN A CONCERN DEMAND: Although the pace is slowing, room night demand growth

HOTEL MARKET REPORT: 3Q2013 HOTEL CONTINUES ON A POSITIVE TRACK TRENDS FOR DEMAND AND ADR REMAIN SOLID, BUT COMING DELIVERIES REMAIN A CONCERN DEMAND: Although the pace is slowing, room night demand growth

Monitor Euro area deflation

Investment Research General Market Conditions 17 July 2014 Euro area deflation Inflation outlook Euro inflation remained very low at 0.5% in June and is still far below the ECB s target. In response, the

Investment Research General Market Conditions 17 July 2014 Euro area deflation Inflation outlook Euro inflation remained very low at 0.5% in June and is still far below the ECB s target. In response, the

Global PMI. Global economy suffers loss of momentum in March. April 10 th IHS Markit. All Rights Reserved.

Global PMI Global economy suffers loss of momentum in March April 10 th 2018 2 Global economy suffers marked loss of growth momentum Global economic growth slowed sharply to the weakest for over a year

Global PMI Global economy suffers loss of momentum in March April 10 th 2018 2 Global economy suffers marked loss of growth momentum Global economic growth slowed sharply to the weakest for over a year

Oct-Dec st Preliminary GDP Estimate

Japan's Economy 15 February 2016 (No. of pages: 5) Japanese report: 15 Feb 2016 Oct-Dec 2015 1 st Preliminary GDP Estimate GDP experiences negative growth for first time in two quarters hinting at risk

Japan's Economy 15 February 2016 (No. of pages: 5) Japanese report: 15 Feb 2016 Oct-Dec 2015 1 st Preliminary GDP Estimate GDP experiences negative growth for first time in two quarters hinting at risk

Japanese Stock Market Outlook. SMAM monthly comments & views - June

Japanese Stock Market Outlook SMAM monthly comments & views - June 2018 - Executive summary Japanese Economy Extremely cold winter and early spring ended in Japan. Consumer sentiment was negatively affected

Japanese Stock Market Outlook SMAM monthly comments & views - June 2018 - Executive summary Japanese Economy Extremely cold winter and early spring ended in Japan. Consumer sentiment was negatively affected

The Current State of the US Economy

The Current State of the US Economy This short article is based on the most recent report of the Chairman of the Federal Reserve to the Congress on US monetary policy and the current state of the US economy.

The Current State of the US Economy This short article is based on the most recent report of the Chairman of the Federal Reserve to the Congress on US monetary policy and the current state of the US economy.

Embargoed until 30 November :45am CT

Contact: Jack L Bishop Jr PhD Kingsbury International, Ltd. 245 Ridge Road Highland Park, IL 635 Phone 847 831-477 Fax 847 831-2846 email: napmc@kingbiz.com http://www.kingbiz.com Press Release Embargoed

Contact: Jack L Bishop Jr PhD Kingsbury International, Ltd. 245 Ridge Road Highland Park, IL 635 Phone 847 831-477 Fax 847 831-2846 email: napmc@kingbiz.com http://www.kingbiz.com Press Release Embargoed

Quarterly Report April June 2017 August 30th, 2017

Quarterly Report April June August th, Outline 1 Monetary Policy and Inflation External Conditions Evolution of the Mexican Economy Forecasts and Final Remarks Quarterly Report April - June 1 Conduction

Quarterly Report April June August th, Outline 1 Monetary Policy and Inflation External Conditions Evolution of the Mexican Economy Forecasts and Final Remarks Quarterly Report April - June 1 Conduction

2012 Owasso Economic Outlook

Center for Applied Economic Research Center for Applied Economic Research 2012 Owasso Economic Outlook Prepared by Mouhcine Guettabi Research Economist Dan S. Rickman Regents Professor of Economics Oklahoma

Center for Applied Economic Research Center for Applied Economic Research 2012 Owasso Economic Outlook Prepared by Mouhcine Guettabi Research Economist Dan S. Rickman Regents Professor of Economics Oklahoma