Miguel Ferreira Universidade Nova de Lisboa Pedro Santa-Clara Universidade Nova de Lisboa and NBER Q Group Scottsdale, October 2010

|

|

|

- Rolf Goodman

- 6 years ago

- Views:

Transcription

1 Forecasting stock m arket re tu rn s: The sum of th e parts is m ore than th e w hole Miguel Ferreira Universidade Nova de Lisboa Pedro Santa-Clara Universidade Nova de Lisboa and NBER Q Group Scottsdale, October 2010

2 Forecasting stock market 1 returns Strong evidence that expected returns vary considerably over time with price multiples, macroeconomic variables, corporate actions, and measures of risk This variation has important implications for investments and corporate finance applications Discount rate is opportunity cost from the market However, the practical gains have remained elusive since there has been no approach to forecast returns that works robustly out of

3 Predictive regressions 2 Regression of returns on lagged predictors with data up to time s Forecast return at time s+1 with estimated coefficients and predictive variable at time s Roll forward until the end of the sample using a sequence of expanding windows

4 Measuring out-of-sample 3 performance Evaluate performance with out-of-sample R 2 relative to historical mean

5 Predictive regressions 4 Predictive regressions work in sample Campbell (1987), Fama and French (1988), Hodrick (1992), Cochrane (2008) Critiques of predictive regressions Biases due to persistent predictors Nelson and Kim (1993), Stambaugh (1999), Lewellen (2004) Data mining Ferson, Sarkissian, and Simin (2003) Out-of-sample performance Goyal and Welch (2008)

6 8 Predictive regressions - annual

7 9 Forecasting is hard... especially the future

8 Decomposing returns 10 Capital gains Dividend yield Total returns In logs 0.5% 5% 4%

9 11 Historic return components

10 12 Historic return components

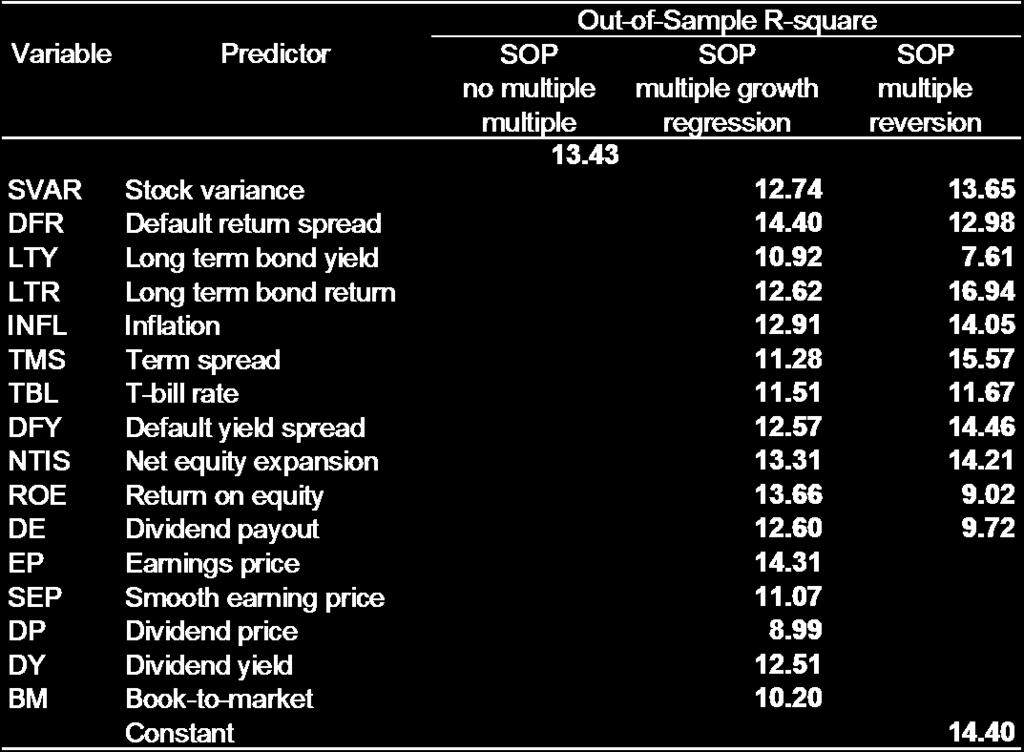

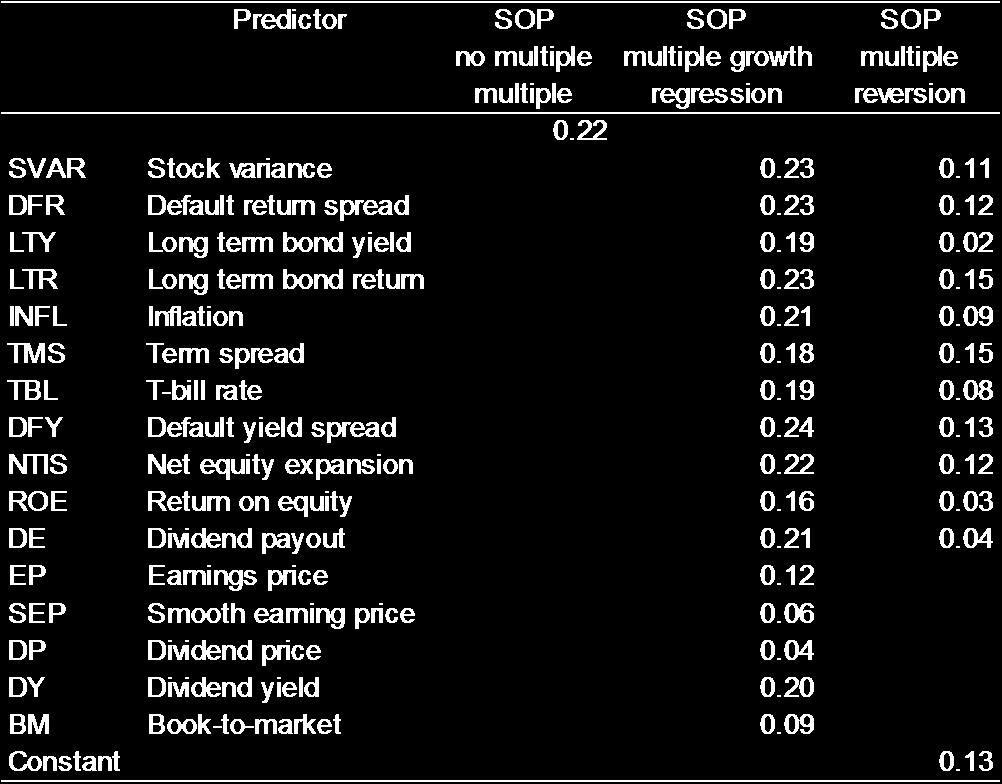

11 Sum-of-the-parts approach (SOP) 13 We forecast each component of returns separately Expected dividend price estimated by the current dividend-price ratio Assumes this ratio follows a random walk Expected earnings growth estimated with a 20- year past moving average Earnings growth nearly impossible to forecast Tried analyst consensus forecasts with worse results

12 Sum-of-the-parts approach (SOP) 14 3 alternatives to estimate expected multiple growth No multiple growth Multiple growth regression (with shrinkage) Multiple reversion (with shrinkage)

13 Sum-of-the-parts approach - 16 annual

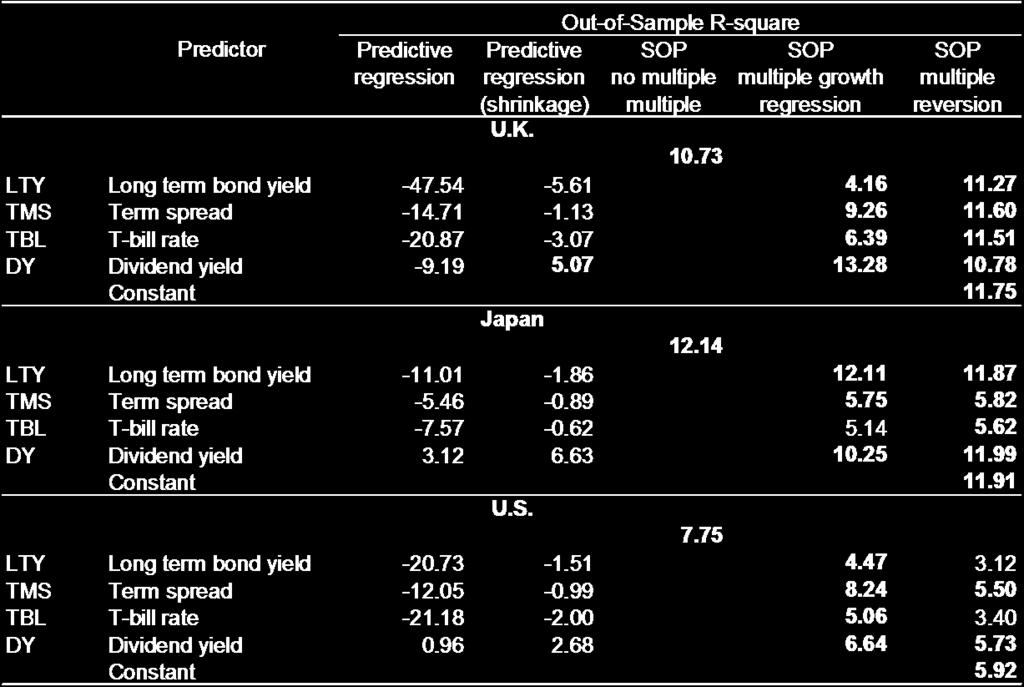

14 17 SOP return forecast (no multiple growth)

15 18 SOP return forecast vs T-bill rate

16 19 SOP forecast vs realized returns

17 SOP vs predictive regression vs 21 mean

18 22 Multiple reversion

19 23 SOP forecast (all variants)

20 26 Sharpe ratio gain

21 27 International evidence

22 28 International expected returns

23 30 Monte Carlo simulation

60% of corporations and 80% of financial")

24 Cost of capital for corporate finance 32 CAPM most used (Graham and Harvey, 2007) 60% of corporations and 80% of financial advisers use historical market risk premium in the CAPM 86% of Textbooks/Tradebooks advise to use the historical average market risk premium

25 The CAPM 33 Doesn t work very well out of sample... Out of sample R square (Sample: ) CAPM Small Growth 9.17 Value 3.21 Big Growth Value

26 The Fama-French model 34 Also doesn t work... Out of sample R square (Sample: ) Fama French 3 Factor Model Small Big Growth 3.33 Value 0.46 Growth 0.92 Value 2.18

27 The SOP model 35 Is what you should use! Out of sample R square (Sample: ) Small Growth Sum of the parts (SOP) 7.18*** Neutral 10.09*** Fama French 3 Factor Model CAPM Fama French 3 Factor Model CAPM (SOP estimates) ( SOP estimates) 7.29*** 7.18*** 7.38*** 6.81*** Value 6.00** ** 2.96** Growth 12.62*** *** 13.99*** Big Neutral 13.35*** *** 12.05*** Value 11.94*** *** 9.61***

28 Industry portfolios 36 Historical Mean SOP CAPM FF 3 Factor CAPM FF 3 Factor Books 4.38** 8.07*** 11.30*** 8.75*** Hshld 5.84** 8.71*** 11.80*** 5.10** BldMt *** 5.86 Util *** 13.39*** Telcm Trans ** 8.16*** 3.03** 7.42*** Whlst *** 9.03*** Rtail *** 7.62*** Meals 2.01* 1.89* 7.03*** 8.61*** Banks * 3.14** Insur ** 3.41** RlEst ** 5.24** Fin *** 6.36*** Average 40 Industry

29 Concluding remarks 37 We show that forecasting components of returns works better than traditional predictive regressions Instability of coefficients in predictive regressions Estimation error We combine a steady-state forecast for earnings growth with the market s current valuation Our results revive the long literature on market predictability showing it holds robustly out of sample

30 Concluding remarks 38 There are important implications for investments Tactical asset allocation And for corporate finance Time-varying discount rates for project valuation An open question is whether our results correspond to excessive predictability or timevarying risk premia?

The G Spot: Forecasting Dividend Growth to Predict Returns

The G Spot: Forecasting Dividend Growth to Predict Returns Pedro Santa-Clara 1 Filipe Lacerda 2 This version: July 2009 3 Abstract The dividend-price ratio changes over time due to variation in expected

The G Spot: Forecasting Dividend Growth to Predict Returns Pedro Santa-Clara 1 Filipe Lacerda 2 This version: July 2009 3 Abstract The dividend-price ratio changes over time due to variation in expected

Implied Funding Liquidity

Implied Funding Liquidity Minh Nguyen Yuanyu Yang Newcastle University Business School 3 April 2017 1 / 17 Outline 1 Background 2 Summary 3 Implied Funding Liquidity Measure 4 Data 5 Empirical Results

Implied Funding Liquidity Minh Nguyen Yuanyu Yang Newcastle University Business School 3 April 2017 1 / 17 Outline 1 Background 2 Summary 3 Implied Funding Liquidity Measure 4 Data 5 Empirical Results

Asset Pricing Models with Conditional Betas and Alphas: The Effects of Data Snooping and Spurious Regression

Asset Pricing Models with Conditional Betas and Alphas: The Effects of Data Snooping and Spurious Regression Wayne E. Ferson *, Sergei Sarkissian, and Timothy Simin first draft: January 21, 2005 this draft:

Asset Pricing Models with Conditional Betas and Alphas: The Effects of Data Snooping and Spurious Regression Wayne E. Ferson *, Sergei Sarkissian, and Timothy Simin first draft: January 21, 2005 this draft:

On the economic significance of stock return predictability: Evidence from macroeconomic state variables

On the economic significance of stock return predictability: Evidence from macroeconomic state variables Huacheng Zhang * University of Arizona This draft: 8/31/2012 First draft: 2/28/2012 Abstract We

On the economic significance of stock return predictability: Evidence from macroeconomic state variables Huacheng Zhang * University of Arizona This draft: 8/31/2012 First draft: 2/28/2012 Abstract We

Lecture 2: Forecasting stock returns

Lecture 2: Forecasting stock returns Prof. Massimo Guidolin Advanced Financial Econometrics III Winter/Spring 2016 Overview The objective of the predictability exercise on stock index returns Predictability

Lecture 2: Forecasting stock returns Prof. Massimo Guidolin Advanced Financial Econometrics III Winter/Spring 2016 Overview The objective of the predictability exercise on stock index returns Predictability

Addendum. Multifactor models and their consistency with the ICAPM

Addendum Multifactor models and their consistency with the ICAPM Paulo Maio 1 Pedro Santa-Clara This version: February 01 1 Hanken School of Economics. E-mail: paulofmaio@gmail.com. Nova School of Business

Addendum Multifactor models and their consistency with the ICAPM Paulo Maio 1 Pedro Santa-Clara This version: February 01 1 Hanken School of Economics. E-mail: paulofmaio@gmail.com. Nova School of Business

Reconciling the Return Predictability Evidence

RFS Advance Access published December 10, 2007 Reconciling the Return Predictability Evidence Martin Lettau Columbia University, New York University, CEPR, NBER Stijn Van Nieuwerburgh New York University

RFS Advance Access published December 10, 2007 Reconciling the Return Predictability Evidence Martin Lettau Columbia University, New York University, CEPR, NBER Stijn Van Nieuwerburgh New York University

A Note on Predicting Returns with Financial Ratios

A Note on Predicting Returns with Financial Ratios Amit Goyal Goizueta Business School Emory University Ivo Welch Yale School of Management Yale Economics Department NBER December 16, 2003 Abstract This

A Note on Predicting Returns with Financial Ratios Amit Goyal Goizueta Business School Emory University Ivo Welch Yale School of Management Yale Economics Department NBER December 16, 2003 Abstract This

Lecture 2: Forecasting stock returns

Lecture 2: Forecasting stock returns Prof. Massimo Guidolin Advanced Financial Econometrics III Winter/Spring 2018 Overview The objective of the predictability exercise on stock index returns Predictability

Lecture 2: Forecasting stock returns Prof. Massimo Guidolin Advanced Financial Econometrics III Winter/Spring 2018 Overview The objective of the predictability exercise on stock index returns Predictability

Appendix to Dividend yields, dividend growth, and return predictability in the cross-section of. stocks

Appendix to Dividend yields, dividend growth, and return predictability in the cross-section of stocks Paulo Maio 1 Pedro Santa-Clara 2 This version: February 2015 1 Hanken School of Economics. E-mail:

Appendix to Dividend yields, dividend growth, and return predictability in the cross-section of stocks Paulo Maio 1 Pedro Santa-Clara 2 This version: February 2015 1 Hanken School of Economics. E-mail:

tay s as good as cay

Finance Research Letters 2 (2005) 1 14 www.elsevier.com/locate/frl tay s as good as cay Michael J. Brennan a, Yihong Xia b, a The Anderson School, UCLA, 110 Westwood Plaza, Los Angeles, CA 90095-1481,

Finance Research Letters 2 (2005) 1 14 www.elsevier.com/locate/frl tay s as good as cay Michael J. Brennan a, Yihong Xia b, a The Anderson School, UCLA, 110 Westwood Plaza, Los Angeles, CA 90095-1481,

The Cross-Section and Time-Series of Stock and Bond Returns

The Cross-Section and Time-Series of Ralph S.J. Koijen, Hanno Lustig, and Stijn Van Nieuwerburgh University of Chicago, UCLA & NBER, and NYU, NBER & CEPR UC Berkeley, September 10, 2009 Unified Stochastic

The Cross-Section and Time-Series of Ralph S.J. Koijen, Hanno Lustig, and Stijn Van Nieuwerburgh University of Chicago, UCLA & NBER, and NYU, NBER & CEPR UC Berkeley, September 10, 2009 Unified Stochastic

NBER WORKING PAPER SERIES SPURIOUS REGRESSIONS IN FINANCIAL ECONOMICS? Wayne E. Ferson Sergei Sarkissian Timothy Simin

NBER WORKING PAPER SERIES SPURIOUS REGRESSIONS IN FINANCIAL ECONOMICS? Wayne E. Ferson Sergei Sarkissian Timothy Simin Working Paper 9143 http://www.nber.org/papers/w9143 NATIONAL BUREAU OF ECONOMIC RESEARCH

NBER WORKING PAPER SERIES SPURIOUS REGRESSIONS IN FINANCIAL ECONOMICS? Wayne E. Ferson Sergei Sarkissian Timothy Simin Working Paper 9143 http://www.nber.org/papers/w9143 NATIONAL BUREAU OF ECONOMIC RESEARCH

The bottom-up beta of momentum

The bottom-up beta of momentum Pedro Barroso First version: September 2012 This version: November 2014 Abstract A direct measure of the cyclicality of momentum at a given point in time, its bottom-up beta

The bottom-up beta of momentum Pedro Barroso First version: September 2012 This version: November 2014 Abstract A direct measure of the cyclicality of momentum at a given point in time, its bottom-up beta

The pricing of volatility risk across asset classes. and the Fama-French factors

The pricing of volatility risk across asset classes and the Fama-French factors Zhi Da and Ernst Schaumburg, Version: May 6, 29 Abstract In the Merton (1973) ICAPM, state variables that capture the evolution

The pricing of volatility risk across asset classes and the Fama-French factors Zhi Da and Ernst Schaumburg, Version: May 6, 29 Abstract In the Merton (1973) ICAPM, state variables that capture the evolution

Sector Return Predictability With a Link to the Business Cycle

Master Thesis Sector Return Predictability With a Link to the Business Cycle Author: Jonas Bøegh-Lervang M.Sc. Applied Economics & Finance Copenhagen Business School, Department of Economics Supervisor:

Master Thesis Sector Return Predictability With a Link to the Business Cycle Author: Jonas Bøegh-Lervang M.Sc. Applied Economics & Finance Copenhagen Business School, Department of Economics Supervisor:

The Importance (or Non-Importance) of Distributional Assumptions in Monte Carlo Models of Saving. James P. Dow, Jr.

of Distributional Assumptions in Monte Carlo Models of Saving. James P. Dow, Jr.") The Importance (or Non-Importance) of Distributional Assumptions in Monte Carlo Models of Saving James P. Dow, Jr. Department of Finance, Real Estate and Insurance California State University, Northridge

The Importance (or Non-Importance) of Distributional Assumptions in Monte Carlo Models of Saving James P. Dow, Jr. Department of Finance, Real Estate and Insurance California State University, Northridge

The Long-Run Equity Risk Premium

The Long-Run Equity Risk Premium John R. Graham, Fuqua School of Business, Duke University, Durham, NC 27708, USA Campbell R. Harvey * Fuqua School of Business, Duke University, Durham, NC 27708, USA National

The Long-Run Equity Risk Premium John R. Graham, Fuqua School of Business, Duke University, Durham, NC 27708, USA Campbell R. Harvey * Fuqua School of Business, Duke University, Durham, NC 27708, USA National

Spurious Regressions in Financial Economics?

Spurious Regressions in Financial Economics? WAYNE E. FERSON, SERGEI SARKISSIAN, AND TIMOTHY T. SIMIN * ABSTRACT Even though stock returns are not highly autocorrelated, there is a spurious regression

Spurious Regressions in Financial Economics? WAYNE E. FERSON, SERGEI SARKISSIAN, AND TIMOTHY T. SIMIN * ABSTRACT Even though stock returns are not highly autocorrelated, there is a spurious regression

What does the crisis of 2008 imply for 2009 and beyond?

What does the crisis of 28 imply for 29 and beyond? Vanguard Investment Counseling & Research Executive summary. The financial crisis of 28 engendered severe declines in equity markets and economic activity

What does the crisis of 28 imply for 29 and beyond? Vanguard Investment Counseling & Research Executive summary. The financial crisis of 28 engendered severe declines in equity markets and economic activity

Robust Econometric Inference for Stock Return Predictability

Robust Econometric Inference for Stock Return Predictability Alex Kostakis (MBS), Tassos Magdalinos (Southampton) and Michalis Stamatogiannis (Bath) Alex Kostakis, MBS Marie Curie, Konstanz (Alex Kostakis,

Robust Econometric Inference for Stock Return Predictability Alex Kostakis (MBS), Tassos Magdalinos (Southampton) and Michalis Stamatogiannis (Bath) Alex Kostakis, MBS Marie Curie, Konstanz (Alex Kostakis,

Time-varying Cointegration Relationship between Dividends and Stock Price

Time-varying Cointegration Relationship between Dividends and Stock Price Cheolbeom Park Korea University Chang-Jin Kim Korea University and University of Washington December 21, 2009 Abstract: We consider

Time-varying Cointegration Relationship between Dividends and Stock Price Cheolbeom Park Korea University Chang-Jin Kim Korea University and University of Washington December 21, 2009 Abstract: We consider

Lecture 5. Predictability. Traditional Views of Market Efficiency ( )

") Lecture 5 Predictability Traditional Views of Market Efficiency (1960-1970) CAPM is a good measure of risk Returns are close to unpredictable (a) Stock, bond and foreign exchange changes are not predictable

Lecture 5 Predictability Traditional Views of Market Efficiency (1960-1970) CAPM is a good measure of risk Returns are close to unpredictable (a) Stock, bond and foreign exchange changes are not predictable

Davids, Goliaths, and Business Cycles

Davids, Goliaths, and Business Cycles Jefferson Duarte and Nishad Kapadia April 2013 Abstract We show that a simple, intuitive variable, (Goliath versus David) reflects timevariation in discount rates

Davids, Goliaths, and Business Cycles Jefferson Duarte and Nishad Kapadia April 2013 Abstract We show that a simple, intuitive variable, (Goliath versus David) reflects timevariation in discount rates

Models of expected European equity returns incorporating implied volatility and a simple measure of investor sentiment

TILBURG UNIVERSITY Models of expected European equity returns incorporating implied volatility and a simple measure of investor sentiment Ioannis Laliotis Department of Finance 11/17/2013 Abstract This

TILBURG UNIVERSITY Models of expected European equity returns incorporating implied volatility and a simple measure of investor sentiment Ioannis Laliotis Department of Finance 11/17/2013 Abstract This

A1. Relating Level and Slope to Expected Inflation and Output Dynamics

Appendix 1 A1. Relating Level and Slope to Expected Inflation and Output Dynamics This section provides a simple illustrative example to show how the level and slope factors incorporate expectations regarding

Appendix 1 A1. Relating Level and Slope to Expected Inflation and Output Dynamics This section provides a simple illustrative example to show how the level and slope factors incorporate expectations regarding

NBER WORKING PAPER SERIES PREDICTING THE EQUITY PREMIUM OUT OF SAMPLE: CAN ANYTHING BEAT THE HISTORICAL AVERAGE? John Y. Campbell Samuel B.

NBER WORKING PAPER SERIES PREDICTING THE EQUITY PREMIUM OUT OF SAMPLE: CAN ANYTHING BEAT THE HISTORICAL AVERAGE? John Y. Campbell Samuel B. Thompson Working Paper 11468 http://www.nber.org/papers/w11468

NBER WORKING PAPER SERIES PREDICTING THE EQUITY PREMIUM OUT OF SAMPLE: CAN ANYTHING BEAT THE HISTORICAL AVERAGE? John Y. Campbell Samuel B. Thompson Working Paper 11468 http://www.nber.org/papers/w11468

Spurious Regression and Data Mining in Conditional Asset Pricing Models*

Spurious Regression and Data Mining in Conditional Asset Pricing Models* for the Handbook of Quantitative Finance, C.F. Lee, Editor, Springer Publishing by: Wayne Ferson, University of Southern California

Spurious Regression and Data Mining in Conditional Asset Pricing Models* for the Handbook of Quantitative Finance, C.F. Lee, Editor, Springer Publishing by: Wayne Ferson, University of Southern California

Evidence on Industry Cost of Equity Estimators. Author. Published. Journal Title. Copyright Statement. Downloaded from. Link to published version

Evidence on Industry Cost of Equity Estimators Author Gharaibeh, Omar, Bornholt, Graham, Dempsey, Michael Published 2014 Journal Title The International Journal of Business and Finance Research Copyright

Evidence on Industry Cost of Equity Estimators Author Gharaibeh, Omar, Bornholt, Graham, Dempsey, Michael Published 2014 Journal Title The International Journal of Business and Finance Research Copyright

Yale ICF Working Paper No November 21, 2002

Yale ICF Working Paper No. 02-04 November 21, 2002 PREDICTING THE EQUITY PREMIUM (WITH DIVIDEND RATIOS) Amit Goyal Goizueta Business School at Emory Ivo Welch Yale School of Management NBER This paper

Yale ICF Working Paper No. 02-04 November 21, 2002 PREDICTING THE EQUITY PREMIUM (WITH DIVIDEND RATIOS) Amit Goyal Goizueta Business School at Emory Ivo Welch Yale School of Management NBER This paper

Expectations of equity risk premia, volatility and asymmetry from a corporate finance perspective

WORK IN PROGRESS TO BE AUGMENTED WITH DATA FROM FUTURE SURVEYS Expectations of equity risk premia, volatility and asymmetry from a corporate finance perspective John R. Graham, Fuqua School of Business,

WORK IN PROGRESS TO BE AUGMENTED WITH DATA FROM FUTURE SURVEYS Expectations of equity risk premia, volatility and asymmetry from a corporate finance perspective John R. Graham, Fuqua School of Business,

Predicting Excess Stock Returns Out of Sample: Can Anything Beat the Historical Average?

Predicting Excess Stock Returns Out of Sample: Can Anything Beat the Historical Average? The Harvard community has made this article openly available. Please share how this access benefits you. Your story

Predicting Excess Stock Returns Out of Sample: Can Anything Beat the Historical Average? The Harvard community has made this article openly available. Please share how this access benefits you. Your story

Bagging Constrained Forecasts with Application to Forecasting Equity Premium

Bagging Constrained Forecasts with Application to Forecasting Equity Premium Eric Hillebrand Tae-Hwy Lee y Marcelo C. Medeiros z August 2009 Abstract The literature on excess return prediction has considered

Bagging Constrained Forecasts with Application to Forecasting Equity Premium Eric Hillebrand Tae-Hwy Lee y Marcelo C. Medeiros z August 2009 Abstract The literature on excess return prediction has considered

Empirical Evidence. r Mt r ft e i. now do second-pass regression (cross-sectional with N 100): r i r f γ 0 γ 1 b i u i

: r i r f γ 0 γ 1 b i u i") Empirical Evidence (Text reference: Chapter 10) Tests of single factor CAPM/APT Roll s critique Tests of multifactor CAPM/APT The debate over anomalies Time varying volatility The equity premium puzzle

Empirical Evidence (Text reference: Chapter 10) Tests of single factor CAPM/APT Roll s critique Tests of multifactor CAPM/APT The debate over anomalies Time varying volatility The equity premium puzzle

Mean Reversion and Market Predictability. Jon Exley, Andrew Smith and Tom Wright

Mean Reversion and Market Predictability Jon Exley, Andrew Smith and Tom Wright Abstract: This paper examines some arguments for the predictability of share price and currency movements. We examine data

Mean Reversion and Market Predictability Jon Exley, Andrew Smith and Tom Wright Abstract: This paper examines some arguments for the predictability of share price and currency movements. We examine data

Maximum likelihood estimation of the equity premium

Maximum likelihood estimation of the equity premium Efstathios Avdis University of Alberta Jessica A. Wachter University of Pennsylvania and NBER May 19, 2015 Abstract The equity premium, namely the expected

Maximum likelihood estimation of the equity premium Efstathios Avdis University of Alberta Jessica A. Wachter University of Pennsylvania and NBER May 19, 2015 Abstract The equity premium, namely the expected

Tuomo Lampinen Silicon Cloud Technologies LLC

Tuomo Lampinen Silicon Cloud Technologies LLC www.portfoliovisualizer.com Background and Motivation Portfolio Visualizer Tools for Investors Overview of tools and related theoretical background Investment

Tuomo Lampinen Silicon Cloud Technologies LLC www.portfoliovisualizer.com Background and Motivation Portfolio Visualizer Tools for Investors Overview of tools and related theoretical background Investment

IS STOCK RETURN PREDICTABILITY SPURIOUS?

JOIM JOURNAL OF INVESTMENT MANAGEMENT, Vol. 1, No. 3, (2003), pp. 1 10 JOIM 2003 www.joim.com IS STOCK RETURN PREDICTABILITY SPURIOUS? Wayne E. Ferson a,, Sergei Sarkissian b, and Timothy Simin c Two problems,

JOIM JOURNAL OF INVESTMENT MANAGEMENT, Vol. 1, No. 3, (2003), pp. 1 10 JOIM 2003 www.joim.com IS STOCK RETURN PREDICTABILITY SPURIOUS? Wayne E. Ferson a,, Sergei Sarkissian b, and Timothy Simin c Two problems,

Predictability of aggregate and firm-level returns

Predictability of aggregate and firm-level returns Namho Kang Nov 07, 2012 Abstract Recent studies find that the aggregate implied cost of capital (ICC) can predict market returns. This paper shows, however,

Predictability of aggregate and firm-level returns Namho Kang Nov 07, 2012 Abstract Recent studies find that the aggregate implied cost of capital (ICC) can predict market returns. This paper shows, however,

How Predictable Is the Chinese Stock Market?

David E. Rapach Jack K. Strauss How Predictable Is the Chinese Stock Market? Jiang Fuwei a, David E. Rapach b, Jack K. Strauss b, Tu Jun a, and Zhou Guofu c (a: Lee Kong Chian School of Business, Singapore

David E. Rapach Jack K. Strauss How Predictable Is the Chinese Stock Market? Jiang Fuwei a, David E. Rapach b, Jack K. Strauss b, Tu Jun a, and Zhou Guofu c (a: Lee Kong Chian School of Business, Singapore

Online Appendix to. The Structure of Information Release and the Factor Structure of Returns

Online Appendix to The Structure of Information Release and the Factor Structure of Returns Thomas Gilbert, Christopher Hrdlicka, Avraham Kamara 1 February 2017 In this online appendix, we present supplementary

Online Appendix to The Structure of Information Release and the Factor Structure of Returns Thomas Gilbert, Christopher Hrdlicka, Avraham Kamara 1 February 2017 In this online appendix, we present supplementary

Predicting Market Returns Using Aggregate Implied Cost of Capital

Predicting Market Returns Using Aggregate Implied Cost of Capital Yan Li, David T. Ng, and Bhaskaran Swaminathan 1 Theoretically, the aggregate implied cost of capital (ICC) computed using earnings forecasts

Predicting Market Returns Using Aggregate Implied Cost of Capital Yan Li, David T. Ng, and Bhaskaran Swaminathan 1 Theoretically, the aggregate implied cost of capital (ICC) computed using earnings forecasts

The Share of Systematic Variation in Bilateral Exchange Rates

The Share of Systematic Variation in Bilateral Exchange Rates Adrien Verdelhan MIT Sloan and NBER March 2013 This Paper (I/II) Two variables account for 20% to 90% of the monthly exchange rate movements

The Share of Systematic Variation in Bilateral Exchange Rates Adrien Verdelhan MIT Sloan and NBER March 2013 This Paper (I/II) Two variables account for 20% to 90% of the monthly exchange rate movements

The intertemporal relation between expected returns and risk $

Journal of Financial Economics 87 (2008) 101 131 www.elsevier.com/locate/jfec The intertemporal relation between expected returns and risk $ Turan G. Bali Baruch College, Zicklin School of Business, One

Journal of Financial Economics 87 (2008) 101 131 www.elsevier.com/locate/jfec The intertemporal relation between expected returns and risk $ Turan G. Bali Baruch College, Zicklin School of Business, One

Department of Finance Working Paper Series

NEW YORK UNIVERSITY LEONARD N. STERN SCHOOL OF BUSINESS Department of Finance Working Paper Series FIN-03-005 Does Mutual Fund Performance Vary over the Business Cycle? Anthony W. Lynch, Jessica Wachter

NEW YORK UNIVERSITY LEONARD N. STERN SCHOOL OF BUSINESS Department of Finance Working Paper Series FIN-03-005 Does Mutual Fund Performance Vary over the Business Cycle? Anthony W. Lynch, Jessica Wachter

Portfolio Risk Management and Linear Factor Models

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

CFA Level II - LOS Changes

CFA Level II - LOS Changes 2018-2019 Topic LOS Level II - 2018 (465 LOS) LOS Level II - 2019 (471 LOS) Compared Ethics 1.1.a describe the six components of the Code of Ethics and the seven Standards of

CFA Level II - LOS Changes 2018-2019 Topic LOS Level II - 2018 (465 LOS) LOS Level II - 2019 (471 LOS) Compared Ethics 1.1.a describe the six components of the Code of Ethics and the seven Standards of

CFA Level II - LOS Changes

CFA Level II - LOS Changes 2017-2018 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level II - 2017 (464 LOS) LOS Level II - 2018 (465 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 1.3.a

CFA Level II - LOS Changes 2017-2018 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level II - 2017 (464 LOS) LOS Level II - 2018 (465 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 1.3.a

Maximum likelihood estimation of the equity premium

Maximum likelihood estimation of the equity premium Efstathios Avdis University of Alberta Jessica A. Wachter University of Pennsylvania and NBER March 11, 2016 Abstract The equity premium, namely the

Maximum likelihood estimation of the equity premium Efstathios Avdis University of Alberta Jessica A. Wachter University of Pennsylvania and NBER March 11, 2016 Abstract The equity premium, namely the

Notes. 1 Fundamental versus Technical Analysis. 2 Investment Performance. 4 Performance Sensitivity

Notes 1 Fundamental versus Technical Analysis 1. Further findings using cash-flow-to-price, earnings-to-price, dividend-price, past return, and industry are broadly consistent with those reported in the

Notes 1 Fundamental versus Technical Analysis 1. Further findings using cash-flow-to-price, earnings-to-price, dividend-price, past return, and industry are broadly consistent with those reported in the

Online Appendix to Bond Return Predictability: Economic Value and Links to the Macroeconomy. Pairwise Tests of Equality of Forecasting Performance

Online Appendix to Bond Return Predictability: Economic Value and Links to the Macroeconomy This online appendix is divided into four sections. In section A we perform pairwise tests aiming at disentangling

Online Appendix to Bond Return Predictability: Economic Value and Links to the Macroeconomy This online appendix is divided into four sections. In section A we perform pairwise tests aiming at disentangling

Predictability of Stock Market Returns

Predictability of Stock Market Returns May 3, 23 Present Value Models and Forecasting Regressions for Stock market Returns Forecasting regressions for stock market returns can be interpreted in the framework

Predictability of Stock Market Returns May 3, 23 Present Value Models and Forecasting Regressions for Stock market Returns Forecasting regressions for stock market returns can be interpreted in the framework

Common Factors in Return Seasonalities

Common Factors in Return Seasonalities Matti Keloharju, Aalto University Juhani Linnainmaa, University of Chicago and NBER Peter Nyberg, Aalto University AQR Insight Award Presentation 1 / 36 Common factors

Common Factors in Return Seasonalities Matti Keloharju, Aalto University Juhani Linnainmaa, University of Chicago and NBER Peter Nyberg, Aalto University AQR Insight Award Presentation 1 / 36 Common factors

Combining State-Dependent Forecasts of Equity Risk Premium

Combining State-Dependent Forecasts of Equity Risk Premium Daniel de Almeida, Ana-Maria Fuertes and Luiz Koodi Hotta Universidad Carlos III de Madrid September 15, 216 Almeida, Fuertes and Hotta (UC3M)

Combining State-Dependent Forecasts of Equity Risk Premium Daniel de Almeida, Ana-Maria Fuertes and Luiz Koodi Hotta Universidad Carlos III de Madrid September 15, 216 Almeida, Fuertes and Hotta (UC3M)

A Note on the Economics and Statistics of Predictability: A Long Run Risks Perspective

A Note on the Economics and Statistics of Predictability: A Long Run Risks Perspective Ravi Bansal Dana Kiku Amir Yaron November 14, 2007 Abstract Asset return and cash flow predictability is of considerable

A Note on the Economics and Statistics of Predictability: A Long Run Risks Perspective Ravi Bansal Dana Kiku Amir Yaron November 14, 2007 Abstract Asset return and cash flow predictability is of considerable

Dividend Smoothing and Predictability

Dividend Smoothing and Predictability Long Chen Olin Business School Washington University in St. Louis Richard Priestley Norwegian School of Management Sep 15, 2008 Zhi Da Mendoza College of Business

Dividend Smoothing and Predictability Long Chen Olin Business School Washington University in St. Louis Richard Priestley Norwegian School of Management Sep 15, 2008 Zhi Da Mendoza College of Business

Media News and Cross Industry Information Diffusion

Media News and Cross Industry Information Diffusion Li Guo Singapore Management Univeristy June 13, 2017 Motivatioin Cross Asset Return Predictability: Information Diffusion: Hong and Stein (1999): Theory

Media News and Cross Industry Information Diffusion Li Guo Singapore Management Univeristy June 13, 2017 Motivatioin Cross Asset Return Predictability: Information Diffusion: Hong and Stein (1999): Theory

Institutional Ownership and Return Predictability Across Economically Unrelated Stocks Internet Appendix: Robustness Checks

Institutional Ownership and Return Predictability Across Economically Unrelated Stocks Internet Appendix: Robustness Checks George P. Gao, Pamela C. Moulton, and David T. Ng Table IA-1: CAPM and FF3 alphas

Institutional Ownership and Return Predictability Across Economically Unrelated Stocks Internet Appendix: Robustness Checks George P. Gao, Pamela C. Moulton, and David T. Ng Table IA-1: CAPM and FF3 alphas

Are hedge fund returns predictable? Author. Published. Journal Title. Copyright Statement. Downloaded from. Link to published version

Are hedge fund returns predictable? Author Bianchi, Robert, Wijeratne, Thanula Published 2009 Journal Title Jassa: The finsia journal of applied finance Copyright Statement 2009 JASSA and the Authors.

Are hedge fund returns predictable? Author Bianchi, Robert, Wijeratne, Thanula Published 2009 Journal Title Jassa: The finsia journal of applied finance Copyright Statement 2009 JASSA and the Authors.

Robust Econometric Inference for Stock Return Predictability

Robust Econometric Inference for Stock Return Predictability Alex Kostakis (MBS), Tassos Magdalinos (Southampton) and Michalis Stamatogiannis (Bath) Alex Kostakis, MBS 2nd ISNPS, Cadiz (Alex Kostakis,

Robust Econometric Inference for Stock Return Predictability Alex Kostakis (MBS), Tassos Magdalinos (Southampton) and Michalis Stamatogiannis (Bath) Alex Kostakis, MBS 2nd ISNPS, Cadiz (Alex Kostakis,

Empirical studies on stock return predictability

Empirical studies on stock return predictability A thesis submitted to the University of Manchester for the degree of Doctor of Philosophy in the Faculty of Humanities 2015 Jingya Wang Manchester Business

Empirical studies on stock return predictability A thesis submitted to the University of Manchester for the degree of Doctor of Philosophy in the Faculty of Humanities 2015 Jingya Wang Manchester Business

Models of asset pricing: The implications for asset allocation Tim Giles 1. June 2004

Tim Giles 1 June 2004 Abstract... 1 Introduction... 1 A. Single-factor CAPM methodology... 2 B. Multi-factor CAPM models in the UK... 4 C. Multi-factor models and theory... 6 D. Multi-factor models and

Tim Giles 1 June 2004 Abstract... 1 Introduction... 1 A. Single-factor CAPM methodology... 2 B. Multi-factor CAPM models in the UK... 4 C. Multi-factor models and theory... 6 D. Multi-factor models and

A New Approach to Asset Integration: Methodology and Mystery. Robert P. Flood and Andrew K. Rose

A New Approach to Asset Integration: Methodology and Mystery Robert P. Flood and Andrew K. Rose Two Obectives: 1. Derive new methodology to assess integration of assets across instruments/borders/markets,

A New Approach to Asset Integration: Methodology and Mystery Robert P. Flood and Andrew K. Rose Two Obectives: 1. Derive new methodology to assess integration of assets across instruments/borders/markets,

Research Division Federal Reserve Bank of St. Louis Working Paper Series

Research Division Federal Reserve Bank of St. Louis Working Paper Series Understanding Stock Return Predictability Hui Guo and Robert Savickas Working Paper 2006-019B http://research.stlouisfed.org/wp/2006/2006-019.pdf

Research Division Federal Reserve Bank of St. Louis Working Paper Series Understanding Stock Return Predictability Hui Guo and Robert Savickas Working Paper 2006-019B http://research.stlouisfed.org/wp/2006/2006-019.pdf

A Nonlinear Approach to the Factor Augmented Model: The FASTR Model

A Nonlinear Approach to the Factor Augmented Model: The FASTR Model B.J. Spruijt - 320624 Erasmus University Rotterdam August 2012 This research seeks to combine Factor Augmentation with Smooth Transition

A Nonlinear Approach to the Factor Augmented Model: The FASTR Model B.J. Spruijt - 320624 Erasmus University Rotterdam August 2012 This research seeks to combine Factor Augmentation with Smooth Transition

Portfolio Optimization with Return Prediction Models. Evidence for Industry Portfolios

Portfolio Optimization with Return Prediction Models Evidence for Industry Portfolios Abstract. Several studies suggest that using prediction models instead of historical averages results in more efficient

Portfolio Optimization with Return Prediction Models Evidence for Industry Portfolios Abstract. Several studies suggest that using prediction models instead of historical averages results in more efficient

Predicting Dividends in Log-Linear Present Value Models

Predicting Dividends in Log-Linear Present Value Models Andrew Ang Columbia University and NBER This Version: 8 August, 2011 JEL Classification: C12, C15, C32, G12 Keywords: predictability, dividend yield,

Predicting Dividends in Log-Linear Present Value Models Andrew Ang Columbia University and NBER This Version: 8 August, 2011 JEL Classification: C12, C15, C32, G12 Keywords: predictability, dividend yield,

Bad, Good and Excellent: An ICAPM with bond risk premia JOB MARKET PAPER

Bad, Good and Excellent: An ICAPM with bond risk premia JOB MARKET PAPER Paulo Maio* Abstract In this paper I derive an ICAPM model based on an augmented definition of market wealth by incorporating bonds,

Bad, Good and Excellent: An ICAPM with bond risk premia JOB MARKET PAPER Paulo Maio* Abstract In this paper I derive an ICAPM model based on an augmented definition of market wealth by incorporating bonds,

Market Efficiency and Idiosyncratic Volatility in Vietnam

International Journal of Business and Management; Vol. 10, No. 6; 2015 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education Market Efficiency and Idiosyncratic Volatility

International Journal of Business and Management; Vol. 10, No. 6; 2015 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education Market Efficiency and Idiosyncratic Volatility

Predictability of the Aggregate Danish Stock Market

AARHUS UNIVERSITY BUSINESS & SOCIAL SCIENCES DEPARTMENT OF ECONOMICS & BUSINESS Department of Economics and Business Bachelor Thesis Bachelor of Economics and Business Administration Authors: Andreas Holm

AARHUS UNIVERSITY BUSINESS & SOCIAL SCIENCES DEPARTMENT OF ECONOMICS & BUSINESS Department of Economics and Business Bachelor Thesis Bachelor of Economics and Business Administration Authors: Andreas Holm

The Challenges to Market-Timing Strategies and Tactical Asset Allocation

The Challenges to Market-Timing Strategies and Tactical Asset Allocation Joseph H. Davis, PhD The Vanguard Group Investment Counseling & Research and Fixed Income Groups Agenda Challenges to traditional

The Challenges to Market-Timing Strategies and Tactical Asset Allocation Joseph H. Davis, PhD The Vanguard Group Investment Counseling & Research and Fixed Income Groups Agenda Challenges to traditional

Portfolio Optimization with Industry Return Prediction Models

Portfolio Optimization with Industry Return Prediction Models Wolfgang Bessler Center for Finance and Banking Justus-Liebig-University Giessen, Germany Dominik Wolff Deka Investment GmbH, Frankfurt, Germany

Portfolio Optimization with Industry Return Prediction Models Wolfgang Bessler Center for Finance and Banking Justus-Liebig-University Giessen, Germany Dominik Wolff Deka Investment GmbH, Frankfurt, Germany

Journal of Multinational Financial Management

J. of Multi. Fin. Manag. 20 (2010) 35 47 Contents lists available at ScienceDirect Journal of Multinational Financial Management journal homepage: www.elsevier.com/locate/econbase Correlation dynamics

J. of Multi. Fin. Manag. 20 (2010) 35 47 Contents lists available at ScienceDirect Journal of Multinational Financial Management journal homepage: www.elsevier.com/locate/econbase Correlation dynamics

Value Timing: Risk and Return Across Asset Classes

Value Timing: Risk and Return Across Asset Classes Fahiz Baba Yara * Nova SBE Martijn Boons Nova SBE February 5, 2018 Andrea Tamoni LSE Abstract Returns to value strategies in individual equities, commodities,

Value Timing: Risk and Return Across Asset Classes Fahiz Baba Yara * Nova SBE Martijn Boons Nova SBE February 5, 2018 Andrea Tamoni LSE Abstract Returns to value strategies in individual equities, commodities,

Foundations of Asset Pricing

Foundations of Asset Pricing C Preliminaries C Mean-Variance Portfolio Choice C Basic of the Capital Asset Pricing Model C Static Asset Pricing Models C Information and Asset Pricing C Valuation in Complete

Foundations of Asset Pricing C Preliminaries C Mean-Variance Portfolio Choice C Basic of the Capital Asset Pricing Model C Static Asset Pricing Models C Information and Asset Pricing C Valuation in Complete

Predicting Market Returns Using Aggregate Implied Cost of Capital

Predicting Market Returns Using Aggregate Implied Cost of Capital Yan Li, David T. Ng, and Bhaskaran Swaminathan 1 First Draft: March 2011 This Draft: November 2012 Theoretically the market-wide implied

Predicting Market Returns Using Aggregate Implied Cost of Capital Yan Li, David T. Ng, and Bhaskaran Swaminathan 1 First Draft: March 2011 This Draft: November 2012 Theoretically the market-wide implied

Forecasting the Equity Premium

Forecasting the Equity Premium Bernt Arne Ødegaard 6 September 2018 Contents 1 The Equity Market Premium 1 2 Is the equity market premium predictable? 1 2.1 How predictable can the market be?..............................

Forecasting the Equity Premium Bernt Arne Ødegaard 6 September 2018 Contents 1 The Equity Market Premium 1 2 Is the equity market premium predictable? 1 2.1 How predictable can the market be?..............................

in-depth Invesco Actively Managed Low Volatility Strategies The Case for

Invesco in-depth The Case for Actively Managed Low Volatility Strategies We believe that active LVPs offer the best opportunity to achieve a higher risk-adjusted return over the long term. Donna C. Wilson

Invesco in-depth The Case for Actively Managed Low Volatility Strategies We believe that active LVPs offer the best opportunity to achieve a higher risk-adjusted return over the long term. Donna C. Wilson

The mathematical model of portfolio optimal size (Tehran exchange market)

") WALIA journal 3(S2): 58-62, 205 Available online at www.waliaj.com ISSN 026-386 205 WALIA The mathematical model of portfolio optimal size (Tehran exchange market) Farhad Savabi * Assistant Professor of

WALIA journal 3(S2): 58-62, 205 Available online at www.waliaj.com ISSN 026-386 205 WALIA The mathematical model of portfolio optimal size (Tehran exchange market) Farhad Savabi * Assistant Professor of

Macro Variables and International Stock Return Predictability

Macro Variables and International Stock Return Predictability (International Journal of Forecasting, forthcoming) David E. Rapach Department of Economics Saint Louis University 3674 Lindell Boulevard Saint

Macro Variables and International Stock Return Predictability (International Journal of Forecasting, forthcoming) David E. Rapach Department of Economics Saint Louis University 3674 Lindell Boulevard Saint

Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]

![Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]](/thumbs/90/101609040.jpg "Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]") Problem set 1 Answers: 1. (a) The first order conditions are with 1+ 1so 0 ( ) [ 0 ( +1 )] [( +1 )] ( +1 ) Consumption follows a random walk. This is approximately true in many nonlinear models. Now we

Problem set 1 Answers: 1. (a) The first order conditions are with 1+ 1so 0 ( ) [ 0 ( +1 )] [( +1 )] ( +1 ) Consumption follows a random walk. This is approximately true in many nonlinear models. Now we

Certification Examination Detailed Content Outline

Certification Examination Detailed Content Outline Certification Examination Detailed Content Outline Percentage of Exam I. FUNDAMENTALS 15% A. Statistics and Methods 5% 1. Basic statistical measures (e.g.,

Certification Examination Detailed Content Outline Certification Examination Detailed Content Outline Percentage of Exam I. FUNDAMENTALS 15% A. Statistics and Methods 5% 1. Basic statistical measures (e.g.,

The Conditional CAPM Does Not Explain Asset- Pricing Anomalies. Jonathan Lewellen * Dartmouth College and NBER

The Conditional CAPM Does Not Explain Asset- Pricing Anomalies Jonathan Lewellen * Dartmouth College and NBER jon.lewellen@dartmouth.edu Stefan Nagel + Stanford University and NBER Nagel_Stefan@gsb.stanford.edu

The Conditional CAPM Does Not Explain Asset- Pricing Anomalies Jonathan Lewellen * Dartmouth College and NBER jon.lewellen@dartmouth.edu Stefan Nagel + Stanford University and NBER Nagel_Stefan@gsb.stanford.edu

Estimating the Ex Ante Equity Premium

Estimating the Ex Ante Equity Premium R. Glen Donaldson Sauder School of Business University of British Columbia glen.donaldson AT sauder.ubc.ca Mark J. Kamstra Schulich School of Business York University

Estimating the Ex Ante Equity Premium R. Glen Donaldson Sauder School of Business University of British Columbia glen.donaldson AT sauder.ubc.ca Mark J. Kamstra Schulich School of Business York University

Is The Value Spread A Useful Predictor of Returns?

Is The Value Spread A Useful Predictor of Returns? Naiping Liu The Wharton School University of Pennsylvania Lu Zhang Simon School University of Rochester and NBER September 2005 Abstract Recent studies

Is The Value Spread A Useful Predictor of Returns? Naiping Liu The Wharton School University of Pennsylvania Lu Zhang Simon School University of Rochester and NBER September 2005 Abstract Recent studies

Extrapolation of the Past: The Most Important Investment Mistake? Nicholas Barberis. Yale University. November 2015

Extrapolation of the Past: The Most Important Investment Mistake? Nicholas Barberis Yale University November 2015 1 Overview behavioral finance tries to make sense of financial phenomena using models that

Extrapolation of the Past: The Most Important Investment Mistake? Nicholas Barberis Yale University November 2015 1 Overview behavioral finance tries to make sense of financial phenomena using models that

Predicting the equity premium via its components

Predicting the equity premium via its components Fabian Baetje and Lukas Menkhoff Abstract We propose a refined way of forecasting the equity premium. Our approach rests on the sum-ofparts approach which

Predicting the equity premium via its components Fabian Baetje and Lukas Menkhoff Abstract We propose a refined way of forecasting the equity premium. Our approach rests on the sum-ofparts approach which

Global connectedness across bond markets

Global connectedness across bond markets Stig V. Møller Jesper Rangvid June 2018 Abstract We provide first tests of gradual diffusion of information across bond markets. We show that excess returns on

Global connectedness across bond markets Stig V. Møller Jesper Rangvid June 2018 Abstract We provide first tests of gradual diffusion of information across bond markets. We show that excess returns on

Predicting the Equity Premium with Implied Volatility Spreads

Predicting the Equity Premium with Implied Volatility Spreads Charles Cao, Timothy Simin, and Han Xiao Department of Finance, Smeal College of Business, Penn State University Department of Economics, Penn

Predicting the Equity Premium with Implied Volatility Spreads Charles Cao, Timothy Simin, and Han Xiao Department of Finance, Smeal College of Business, Penn State University Department of Economics, Penn

NBER WORKING PAPER SERIES A REHABILITATION OF STOCHASTIC DISCOUNT FACTOR METHODOLOGY. John H. Cochrane

NBER WORKING PAPER SERIES A REHABILIAION OF SOCHASIC DISCOUN FACOR MEHODOLOGY John H. Cochrane Working Paper 8533 http://www.nber.org/papers/w8533 NAIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

NBER WORKING PAPER SERIES A REHABILIAION OF SOCHASIC DISCOUN FACOR MEHODOLOGY John H. Cochrane Working Paper 8533 http://www.nber.org/papers/w8533 NAIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

What is the Expected Return on a Stock?

What is the Expected Return on a Stock? Ian Martin Christian Wagner November, 2017 Martin & Wagner (LSE & CBS) What is the Expected Return on a Stock? November, 2017 1 / 38 What is the expected return

What is the Expected Return on a Stock? Ian Martin Christian Wagner November, 2017 Martin & Wagner (LSE & CBS) What is the Expected Return on a Stock? November, 2017 1 / 38 What is the expected return

Government spending and firms dynamics

Government spending and firms dynamics Pedro Brinca Nova SBE Miguel Homem Ferreira Nova SBE December 2nd, 2016 Francesco Franco Nova SBE Abstract Using firm level data and government demand by firm we

Government spending and firms dynamics Pedro Brinca Nova SBE Miguel Homem Ferreira Nova SBE December 2nd, 2016 Francesco Franco Nova SBE Abstract Using firm level data and government demand by firm we

GDP, Share Prices, and Share Returns: Australian and New Zealand Evidence

Journal of Money, Investment and Banking ISSN 1450-288X Issue 5 (2008) EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm GDP, Share Prices, and Share Returns: Australian and New

Journal of Money, Investment and Banking ISSN 1450-288X Issue 5 (2008) EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm GDP, Share Prices, and Share Returns: Australian and New

Discussion of "Yield Curve Premia" by Brooks and Moskowitz

Discussion of "Yield Curve Premia" by Brooks and Moskowitz Monika Piazzesi Stanford & NBER SI AP Meeting 2017 Piazzesi (Stanford) SI AP Meeting 2017 1 / 16 summary "carry" and "value" predict excess returns

Discussion of "Yield Curve Premia" by Brooks and Moskowitz Monika Piazzesi Stanford & NBER SI AP Meeting 2017 Piazzesi (Stanford) SI AP Meeting 2017 1 / 16 summary "carry" and "value" predict excess returns

Properties of the estimated five-factor model

Informationin(andnotin)thetermstructure Appendix. Additional results Greg Duffee Johns Hopkins This draft: October 8, Properties of the estimated five-factor model No stationary term structure model is

Informationin(andnotin)thetermstructure Appendix. Additional results Greg Duffee Johns Hopkins This draft: October 8, Properties of the estimated five-factor model No stationary term structure model is

Introduction to Asset Pricing: Overview, Motivation, Structure

Introduction to Asset Pricing: Overview, Motivation, Structure Lecture Notes Part H Zimmermann 1a Prof. Dr. Heinz Zimmermann Universität Basel WWZ Advanced Asset Pricing Spring 2016 2 Asset Pricing: Valuation

Introduction to Asset Pricing: Overview, Motivation, Structure Lecture Notes Part H Zimmermann 1a Prof. Dr. Heinz Zimmermann Universität Basel WWZ Advanced Asset Pricing Spring 2016 2 Asset Pricing: Valuation

New Orders and Asset Prices

Christopher S. Jones Marshall School of Business, University of Southern California Selale Tuzel Marshall School of Business, University of Southern California We investigate the asset pricing and macroeconomic

Christopher S. Jones Marshall School of Business, University of Southern California Selale Tuzel Marshall School of Business, University of Southern California We investigate the asset pricing and macroeconomic

Applied Macro Finance

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

Do stock fundamentals explain idiosyncratic volatility? Evidence for Australian stock market

Do stock fundamentals explain idiosyncratic volatility? Evidence for Australian stock market Bin Liu School of Economics, Finance and Marketing, RMIT University, Australia Amalia Di Iorio Faculty of Business,

Do stock fundamentals explain idiosyncratic volatility? Evidence for Australian stock market Bin Liu School of Economics, Finance and Marketing, RMIT University, Australia Amalia Di Iorio Faculty of Business,

If Exchange Rates Are Random Walks, Then Almost Everything We Say About Monetary Policy Is Wrong

If Exchange Rates Are Random Walks, Then Almost Everything We Say About Monetary Policy Is Wrong By Fernando Alvarez, Andrew Atkeson, and Patrick J. Kehoe* The key question asked of standard monetary models

If Exchange Rates Are Random Walks, Then Almost Everything We Say About Monetary Policy Is Wrong By Fernando Alvarez, Andrew Atkeson, and Patrick J. Kehoe* The key question asked of standard monetary models