Chapter 3 How Securities are Traded (Cont d) Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

|

|

|

- Ophelia Stephens

- 5 years ago

- Views:

Transcription

1 Chapter 3 How Securities are Traded (Cont d) McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

2 Margin Trading Magnifies Profits and Losses 3-2

3 Short Sales Purpose To profit from a decline in the price of a stock or security Mechanics Borrow stock from a broker/dealer, must post margin Sell it and deposit proceeds in a margin account Closing out the position: buy the stock and broker return to the party from which it was borrowed 3-3

4 Shortselling on Margin -Example 2 You short sell 100 shares of IBM stock at $100 per share. Your broker required 50% margin. How much is required in your account for you to be able to short sell IBM? If IBM.s stock drops to $70 per share and you close your short position, what are your profits (HPR)? Suppose your broker s maintenance margin is 30%. When will you receive a margin call? 3-4

5 Naked Shorts 3-5

6 NYSE Auction Market NASDAQ Dealer Market Dealer market is a market without centralized order flow NASDAQ: largest organized stock market for OTC trading; information system for individuals, brokers and dealers Securities: stocks, most bonds and some derivatives 3-6

7 Electronic Trading on the NYSE SuperDot Electronic order routing system allows brokers to electronically send orders directly to specialist. Useful for program trading DirectPlus Fully automated trade execution system Execution time < ½ second Electronic order placement is growing, large orders still require human intervention

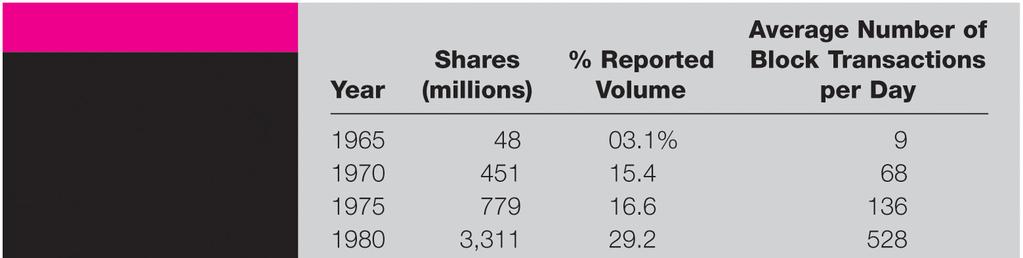

8 Block Transactions and Block Houses 3-8

9 Electronic Computer Networks (ECNs) ECNs allow institutional investors to post quotes and trade directly with each other. (4 th Market) Public limit order book Automatic execution ECNs 3-9

10 Program Trading and the Flash Crash of May 6, 2010 E-mini 3-10

11 Chapter 5 Risk and Return McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

12 Risk and Risk Premiums Rates of Return: Single Period HPR = P 1 P + 0 D 1 P P00 HPR = Holding Period Return P 0 = Beginning price P 1 = Ending price D 1 = Dividend during period one 3-12

13 Rates of Return: Single Period Example Ending Price = 48 Beginning Price = 40 Dividend = 2 HPR= ( )/ (40) = 25% 3-13

14 Annualizing HPRs Annualizing HPRs for holding periods of greater than one year: Without compounding (Simple or APR): HPR ann = HPR/n With compounding: EAR HPR ann = [(1+HPR) 1/n ]-1 where n = number of years held 5-14

15 Measuring Ex-Post (Past) Returns An example: Suppose you buy one share of a stock today for $45 and you hold it for two years and sell it for $52. You also received $8 in dividends at the end of the two years. (PB =, PS =, CF = ): HPR = HPR ann = $45 $52 $8 ( ) / 45 = 33.33% /2 = 16.66% Annualized w/out compounding The annualized HPR assuming annual compounding is (n = ): HPR ann = ( ) 1/2-1 = 15.47%

16 Arithmetic Average An example: You have the following rates of return on a stock: % % % % % % % HPR avg AAR = = n T= 1 HPR T n ( ) HPR avg = = 17.51% % 5-16

17 Geometric Average An example: You have the following rates of return on a stock: % % % % % % % With compounding (geometric average or GAR: Geometric Average Return): HPR avg GAR = n = T= 1 (1+ HPR T ) 1/ n 1 1/7 HPR avg = ( ) 1 = 15.61% 15.61% 5-17

18 Measuring Ex-Post (Past) Returns i. Dollar-weighted return procedure (DWR): Find the internal rate of return for the cash flows (i.e. find the discount rate that makes the NPV of the net cash flows equal zero.) Total Cash Flows Each Year Year $50 $ 2 $ 4 -$53 $108 Net -$50 -$51 $112 NPV = $0 = -$50/(1+IRR) 0 -$51/(1+IRR) 1 + $112/(1+IRR) 2 Solve for IRR: IRR = 7.117% average annual dollar weighted return The DWR gives you an average return based on the stock s performance and the dollar amount invested (number of shares bought and sold) each period. 5-18

19 Real and Nominal Rates of Interest Nominal interest rate Growth rate of your money Real interest rate Growth rate of your purchasing power If Ris the nominal rate and rthe real rate and iis the inflation rate: r = R i 3-19

20 Factors Influencing Rates Supply Households Demand Businesses Government s Net Supply and/or Demand Federal Reserve Actions 3-20

21 Equilibrium Real Rate of Interest Determined by: Supply Demand Government actions Expected rate of inflation 3-21

22 Determination of the Equilibrium Real Rate of Interest r = R i 3-22

23 Equilibrium Nominal Rate of Interest As the inflation rate increases, investors will demand higher nominal rates of return If E(i) denotes current expectations of inflation, then we get the Fisher Equation: 3-23

24 Nominal and Real interest rates and Inflation 5-24

25 Taxes and the Real Rate of Interest Tax liabilities are based on nominal income Given a tax rate (t), nominal interest rate (R), after-tax interest rate is R(1-t) Real after-tax rate is: 3-25

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS. McGraw-Hill/Irwin

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

Risk and Return: Past and Prologue

Chapter 5 Risk and Return: Past and Prologue Bodie, Kane, and Marcus Essentials of Investments Tenth Edition What is in Chapter 5 5.1 Rates of Return HPR, arithmetic, geometric, dollar-weighted, APR, EAR

Chapter 5 Risk and Return: Past and Prologue Bodie, Kane, and Marcus Essentials of Investments Tenth Edition What is in Chapter 5 5.1 Rates of Return HPR, arithmetic, geometric, dollar-weighted, APR, EAR

Chapter 3. Securities Markets. Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 3 Securities Markets McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 3.1 How Firms Issue Securities 3-2 Primary vs. Secondary Market Security Sales Primary

Chapter 3 Securities Markets McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 3.1 How Firms Issue Securities 3-2 Primary vs. Secondary Market Security Sales Primary

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS. McGraw-Hill/Irwin

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 5 Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Supply Interest

CHAPTER 5 Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Supply Interest

CHAPTER 3. How Securities are Traded INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 3 How Securities are Traded INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 3-2 How Securities

CHAPTER 3 How Securities are Traded INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 3-2 How Securities

Risk and Return: Past and Prologue

Chapter 5 Risk and Return: Past and Prologue Bodie, Kane, and Marcus Essentials of Investments Tenth Edition 5.1 Rates of Return Holding-Period Return (HPR) Rate of return over given investment period

Chapter 5 Risk and Return: Past and Prologue Bodie, Kane, and Marcus Essentials of Investments Tenth Edition 5.1 Rates of Return Holding-Period Return (HPR) Rate of return over given investment period

FIN221: Lecture 2 Notes. Securities Markets. Markets in New Securities. The Role of Financial Markets. Investment Banking. Investment Banking

FIN221: Lecture 2 Notes Securities Markets Chapters 4 and 5 Chapter 4 Charles P. Jones, Investments: Analysis and Management, Eighth Edition, John Wiley & Sons Prepared by G.D. Koppenhaver, Iowa State

FIN221: Lecture 2 Notes Securities Markets Chapters 4 and 5 Chapter 4 Charles P. Jones, Investments: Analysis and Management, Eighth Edition, John Wiley & Sons Prepared by G.D. Koppenhaver, Iowa State

Chapter 1 - Investments: Background and Issues

Chapter 1 - Investments: Background and Issues Investment vs. investments Real assets vs. financial assets Financial markets and the economy Investment process Competitive markets Players in investment

Chapter 1 - Investments: Background and Issues Investment vs. investments Real assets vs. financial assets Financial markets and the economy Investment process Competitive markets Players in investment

Trading Global Markets using Technical Analysis. Andy Bower

Trading Global Markets using Technical Analysis Andy Bower www.alchemetrics.org Format Technical Analysis Data Chart Patterns Computers/Backtesting Neural Nets/Genetic Algorithms Essentials of Trading

Trading Global Markets using Technical Analysis Andy Bower www.alchemetrics.org Format Technical Analysis Data Chart Patterns Computers/Backtesting Neural Nets/Genetic Algorithms Essentials of Trading

Chapter. The Stock Market. The Stock Market. Private Equity and Venture Capital. Venture Capital, I. Selling Securities to the Public

Chapter The Stock Market Our goal in this chapter is to provide a big picture overview of: 5 The Stock Market Who owns stocks How a stock exchange works, and How to read and understand the stock market

Chapter The Stock Market Our goal in this chapter is to provide a big picture overview of: 5 The Stock Market Who owns stocks How a stock exchange works, and How to read and understand the stock market

For 9.220, Term 1, 2002/03 02_Lecture12.ppt Student Version. What is risk? An overview of market performance Measuring performance

Risk and Return Introduction For 9.220, erm, 2002/03 02_Lecture2.ppt Student Version Outline Introduction What is risk? performance Measuring performance Return and risk measures Summary and Conclusions

Risk and Return Introduction For 9.220, erm, 2002/03 02_Lecture2.ppt Student Version Outline Introduction What is risk? performance Measuring performance Return and risk measures Summary and Conclusions

Competing Business Models

Competing Business Models Liquidity Providers (Capital Commitment) None One Many Attain Archipelago B-Trade Brut Instinet Island MarketXT NexTrade REDIBook NYSE Amex Nasdaq Data as of January 2002. Liquidity

Competing Business Models Liquidity Providers (Capital Commitment) None One Many Attain Archipelago B-Trade Brut Instinet Island MarketXT NexTrade REDIBook NYSE Amex Nasdaq Data as of January 2002. Liquidity

FIN11. Trading and Market Microstructure. Autumn 2017

FIN11 Trading and Market Microstructure Autumn 2017 Lecturer: Klaus R. Schenk-Hoppé Session 7 Dealers Themes Dealers What & Why Market making Profits & Risks Wake-up video: Wall Street in 1920s http://www.youtube.com/watch?

FIN11 Trading and Market Microstructure Autumn 2017 Lecturer: Klaus R. Schenk-Hoppé Session 7 Dealers Themes Dealers What & Why Market making Profits & Risks Wake-up video: Wall Street in 1920s http://www.youtube.com/watch?

Savings and Investment. July 23, 2014

Savings and Investment July 23, 2014 Personal Financial Planning Process The personal financial planning process includes four main elements: Setting financial goals; Financial assessment; Developing and

Savings and Investment July 23, 2014 Personal Financial Planning Process The personal financial planning process includes four main elements: Setting financial goals; Financial assessment; Developing and

Outline. Equilibrium prices: Financial Markets How securities are traded. Professor Lasse H. Pedersen. What determines the price?

Financial Markets How securities are traded Professor Lasse H. Pedersen Prof. Lasse H. Pedersen 1 Outline What determines the price? Primary markets: new issues Secondary markets: re-trade of securities

Financial Markets How securities are traded Professor Lasse H. Pedersen Prof. Lasse H. Pedersen 1 Outline What determines the price? Primary markets: new issues Secondary markets: re-trade of securities

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 14-2 Bond Characteristics Bonds are debt. Issuers are borrowers and holders are

CHAPTER 14 Bond Prices and Yields McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 14-2 Bond Characteristics Bonds are debt. Issuers are borrowers and holders are

1 A Brief History of. Chapter. Risk and Return. Dollar Returns. PercentReturn. Learning Objectives. A Brief History of Risk and Return

Chapter Learning Objectives To become a wise investor (maybe even one with too much money), you need to know: 1 A Brief History of Risk and Return How to calculate the return on an investment using different

Chapter Learning Objectives To become a wise investor (maybe even one with too much money), you need to know: 1 A Brief History of Risk and Return How to calculate the return on an investment using different

D. Stocks that are listed on exchange floors are also traded in the over-the-counter market.

Volume: 325 Questions Question No: 1 Which of the following statements about the over-the-counter market is true? A. Only penny stocks are traded in the over-the-counter market. B. Trades in the over-the-counter

Volume: 325 Questions Question No: 1 Which of the following statements about the over-the-counter market is true? A. Only penny stocks are traded in the over-the-counter market. B. Trades in the over-the-counter

Finance 300 Spring 1999 Exam 2 Joe Smolira. Multiple Choice - Put all answers on the answer key - 18 questions - 72 total points

Finance 300 Spring 1999 Exam 2 Joe Smolira Multiple Choice - Put all answers on the answer key - 18 questions - 72 total points 1. Protective covenants are offered for the protection of a. common stockholders

Finance 300 Spring 1999 Exam 2 Joe Smolira Multiple Choice - Put all answers on the answer key - 18 questions - 72 total points 1. Protective covenants are offered for the protection of a. common stockholders

Chapter 1 - Investments: Background and Issues

Chapter 1 - Investments: Background and Issues Investment vs. investments Real assets vs. financial assets Financial markets and the economy Investment process Competitive markets Players in investment

Chapter 1 - Investments: Background and Issues Investment vs. investments Real assets vs. financial assets Financial markets and the economy Investment process Competitive markets Players in investment

Corporate Financial Management

Corporate Financial Management Professor James J. Barkocy There are three kinds of people: the ones that can count and the ones that can t. McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies,

Corporate Financial Management Professor James J. Barkocy There are three kinds of people: the ones that can count and the ones that can t. McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies,

Part I: Investment Environment (continued)

") Securities & Investments Analysis First few Weeks: Investment Environment Markets and Instruments Weeks 3 & 4: Issuing Securities Trading Securities (market microstructure items ) Part II: Fixed Income

Securities & Investments Analysis First few Weeks: Investment Environment Markets and Instruments Weeks 3 & 4: Issuing Securities Trading Securities (market microstructure items ) Part II: Fixed Income

Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2003

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2003 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2003 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

Principles of Corporate Finance

Principles of Corporate Finance Professor James J. Barkocy Time is money really McGraw-Hill/Irwin Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Time Value of Money Money has a

Principles of Corporate Finance Professor James J. Barkocy Time is money really McGraw-Hill/Irwin Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Time Value of Money Money has a

3. Time value of money

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

2: ASSET CLASSES AND FINANCIAL INSTRUMENTS MONEY MARKET SECURITIES

2: ASSET CLASSES AND FINANCIAL INSTRUMENTS MONEY MARKET SECURITIES Characteristics. Short-term IOUs. Highly Liquid (Like Cash). Nearly free of default-risk. Denomination. Issuers Types Treasury Bills Negotiable

2: ASSET CLASSES AND FINANCIAL INSTRUMENTS MONEY MARKET SECURITIES Characteristics. Short-term IOUs. Highly Liquid (Like Cash). Nearly free of default-risk. Denomination. Issuers Types Treasury Bills Negotiable

Chapter 5. Learning Objectives. Principals Applied in this Chapter. Time Value of Money. Principle 1: Money Has a Time Value.

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5. Time Value of Money

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Interactive Brokers Quarterly Order Routing Report Quarter Ending March 31, 2006

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending March 31, 2006 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending March 31, 2006 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

I. The Primary Market

University of California, Merced ECO 163-Economics of Investments Chapter 3 Lecture otes Professor Jason Lee I. The Primary Market A. Introduction Definition: The primary market is the market where new

University of California, Merced ECO 163-Economics of Investments Chapter 3 Lecture otes Professor Jason Lee I. The Primary Market A. Introduction Definition: The primary market is the market where new

E-120: Principles of Engineering Economics. Midterm Exam I Feb 28, 2007

E-120: Principles of Engineering Economics Midterm Exam I Feb 28, 2007 Name: (please print) SID: Clearly state all the formula and mathematical expressions that are needed to solve the problems. No credit

E-120: Principles of Engineering Economics Midterm Exam I Feb 28, 2007 Name: (please print) SID: Clearly state all the formula and mathematical expressions that are needed to solve the problems. No credit

CHAPTER 15. The Term Structure of Interest Rates INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 15 The Term Structure of Interest Rates INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 15 The Term Structure of Interest Rates INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS

Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2007

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2007 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2007 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

Measuring Interest Rates

Measuring Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Learn to compute present values, rates of return, rates of return. Learning Outcomes: LO3: Predict

Measuring Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Learn to compute present values, rates of return, rates of return. Learning Outcomes: LO3: Predict

An Overview COPYRIGHTED MATERIAL CHAPTER 1

CHAPTER 1 An Overview The Stock Markets The Exchange System NYSE Time Line Listed Stocks The Specialist System Who s Who on the Exchange Floor The SuperDOT System COPYRIGHTED MATERIAL 6 SAMMY CHUA S DAY

CHAPTER 1 An Overview The Stock Markets The Exchange System NYSE Time Line Listed Stocks The Specialist System Who s Who on the Exchange Floor The SuperDOT System COPYRIGHTED MATERIAL 6 SAMMY CHUA S DAY

Essentials of Corporate Finance, 7/e

PAGE # 1 Essentials of Corporate Finance, 7/e Solved McQs PAGE # 2 Introduction to Financial Management Q#1 Business finance includes determining which long-term assets a firm should purchase. Q#2 The

PAGE # 1 Essentials of Corporate Finance, 7/e Solved McQs PAGE # 2 Introduction to Financial Management Q#1 Business finance includes determining which long-term assets a firm should purchase. Q#2 The

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

Interactive Brokers Quarterly Order Routing Report Quarter Ending December 31, 2002

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending December 31, 2002 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending December 31, 2002 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

CHAPTER 4 TIME VALUE OF MONEY

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

1. Draw a timeline to determine the number of periods for which each cash flow will earn the rate-of-return 2. Calculate the future value of each

1. Draw a timeline to determine the number of periods for which each cash flow will earn the rate-of-return 2. Calculate the future value of each cash flow using Equation 5.1 3. Add the future values A

1. Draw a timeline to determine the number of periods for which each cash flow will earn the rate-of-return 2. Calculate the future value of each cash flow using Equation 5.1 3. Add the future values A

Chapter 2 Securities Markets. T 1. A major function of organized securities markets is to facilitate the transfers of securities among investors.

Chapter 2 Securities Markets TRUE/FALSE T 1. A major function of organized securities markets is to facilitate the transfers of securities among investors. T 2. A round lot is the general unit for trading

Chapter 2 Securities Markets TRUE/FALSE T 1. A major function of organized securities markets is to facilitate the transfers of securities among investors. T 2. A round lot is the general unit for trading

ANSWERS TO CHAPTER QUESTIONS. The Time Value of Money. 1) Compounding is interest paid on principal and interest accumulated.

Compounding is interest paid on principal and interest accumulated.") ANSWERS TO CHAPTER QUESTIONS Chapter 2 The Time Value of Money 1) Compounding is interest paid on principal and interest accumulated. It is important because normal compounding over many years can result

ANSWERS TO CHAPTER QUESTIONS Chapter 2 The Time Value of Money 1) Compounding is interest paid on principal and interest accumulated. It is important because normal compounding over many years can result

McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 12 Planning Investments: Capital Budgeting McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All rights reserved. What are the Steps in the Capital Budgeting Process? Identify

Chapter 12 Planning Investments: Capital Budgeting McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All rights reserved. What are the Steps in the Capital Budgeting Process? Identify

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Chapter 2 Securities Markets. T 1. A major function of organized securities markets is to facilitate the transfers of securities among investors.

Chapter 2 Securities Markets TRUE/FALSE T 1. A major function of organized securities markets is to facilitate the transfers of securities among investors. T 2. A round lot is the general unit for trading

Chapter 2 Securities Markets TRUE/FALSE T 1. A major function of organized securities markets is to facilitate the transfers of securities among investors. T 2. A round lot is the general unit for trading

Charles Schwab Institutional Pricing Guide

July 2006 Please read this important information carefully. Charles Schwab Institutional Pricing Guide Pricing information in this Charles Schwab Institutional Pricing Guide ( Pricing Guide ) supersedes

July 2006 Please read this important information carefully. Charles Schwab Institutional Pricing Guide Pricing information in this Charles Schwab Institutional Pricing Guide ( Pricing Guide ) supersedes

Investment Analysis (FIN 383) Fall Homework 2

Fall Homework 2") Investment Analysis (FIN 383) Fall 2009 Homework 2 Instructions: please read carefully You should show your work how to get the answer for each calculation question to get full credit The due date is Thu,

Investment Analysis (FIN 383) Fall 2009 Homework 2 Instructions: please read carefully You should show your work how to get the answer for each calculation question to get full credit The due date is Thu,

Solution to Problem Set 1

M.I.T. Spring 999 Sloan School of Management 5.45 Solution to Problem Set. Investment has an NPV of 0000 + 20000 + 20% = 6667. Similarly, investments 2, 3, and 4 have NPV s of 5000, -47, and 267, respectively.

M.I.T. Spring 999 Sloan School of Management 5.45 Solution to Problem Set. Investment has an NPV of 0000 + 20000 + 20% = 6667. Similarly, investments 2, 3, and 4 have NPV s of 5000, -47, and 267, respectively.

4. Understanding.. Interest Rates. Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1

4. Understanding. Interest Rates Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1 Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright

4. Understanding. Interest Rates Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1 Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright

Lecture 2. Investment Banking Prof. Droussiotis. RELATIONSHIP MANAGER Chapter 6

Lecture 2 RELATIONSHIP MANAGER Chapter 6 Definition: This person is responsible for establishing a relationship, maintaining it and deepening it. A good relationship manager builds so much customer loyalty

Lecture 2 RELATIONSHIP MANAGER Chapter 6 Definition: This person is responsible for establishing a relationship, maintaining it and deepening it. A good relationship manager builds so much customer loyalty

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2015

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2015 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2015 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2016

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending March 30, 2016

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending March 30, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending March 30, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Re: Rule 201 of Regulation SHO: Concerns with the lack of exemptive relief for single-priced opening, reopening and closing transactions

Mary L. Schapiro Chairman 100 F Street, NE Washington, D.C. 20549 January 19, 2011 Re: Rule 201 of Regulation SHO: Concerns with the lack of exemptive relief for single-priced opening, reopening and closing

Mary L. Schapiro Chairman 100 F Street, NE Washington, D.C. 20549 January 19, 2011 Re: Rule 201 of Regulation SHO: Concerns with the lack of exemptive relief for single-priced opening, reopening and closing

CHAPTER 15. The Term Structure of Interest Rates INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 15 The Term Structure of Interest Rates McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 15-2 Overview of Term Structure The yield curve is a graph that

CHAPTER 15 The Term Structure of Interest Rates McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 15-2 Overview of Term Structure The yield curve is a graph that

Example 3.1. You deposit $110 into a bank that pays 7% interest per year. How much will you have after 1 year? (117.70)

") Fin 3014 Principles of Finance Practice Examples Chapter 3: Example 3.1. You deposit $110 into a bank that pays 7% interest per year. How much will you have after 1 year? (117.70) Example. 3.2. You deposit

Fin 3014 Principles of Finance Practice Examples Chapter 3: Example 3.1. You deposit $110 into a bank that pays 7% interest per year. How much will you have after 1 year? (117.70) Example. 3.2. You deposit

How Securities. Are Traded PART I CHAPTER THREE. 3.1 How Firms Issue Securities

3 Are Traded CHAPTER THREE How Securities THIS CHAPTER WILL provide you with a broad introduction to the many venues and procedures available for trading securities in the United States and international

3 Are Traded CHAPTER THREE How Securities THIS CHAPTER WILL provide you with a broad introduction to the many venues and procedures available for trading securities in the United States and international

RECENT SEC MARKET STRUCTURE INITIATIVES

CLIENT MEMORANDUM RECENT SEC MARKET STRUCTURE INITIATIVES The Securities and Exchange Commission (the SEC ), continuing its efforts in the area of market structure, recently: voted to adopt Rule 15c3-5

CLIENT MEMORANDUM RECENT SEC MARKET STRUCTURE INITIATIVES The Securities and Exchange Commission (the SEC ), continuing its efforts in the area of market structure, recently: voted to adopt Rule 15c3-5

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2017

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2017 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2017 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Important Account-Related Information

ab Important Account-Related Information UBS Financial Services Inc. serves as the clearing firm for UBS International Inc., therefore most of the information in this material provided by UBS Financial

ab Important Account-Related Information UBS Financial Services Inc. serves as the clearing firm for UBS International Inc., therefore most of the information in this material provided by UBS Financial

What is a market? Brings buyers and sellers together to aid in the transfer of goods and services.

What is a market? Brings buyers and sellers together to aid in the transfer of goods and services. Does not require a physical location. The market does not necessarily own the goods or services involved.

What is a market? Brings buyers and sellers together to aid in the transfer of goods and services. Does not require a physical location. The market does not necessarily own the goods or services involved.

INVESTMENT CRITERIA. Net Present Value (NPV)

") 227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

Real Estate Investment Analysis using Excel

Graduate Certificate in Real Estate Finance (GCREF) course Real Estate Investment Analysis using Excel Sing Tien Foo Department of Real Estate 27 May 2016 2 Website for sample template http://www.rst.nus.edu.sg/staff/singtienfoo/

Graduate Certificate in Real Estate Finance (GCREF) course Real Estate Investment Analysis using Excel Sing Tien Foo Department of Real Estate 27 May 2016 2 Website for sample template http://www.rst.nus.edu.sg/staff/singtienfoo/

Understanding Interest Rates

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending June 30, 2014

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending June 30, 2014 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending June 30, 2014 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

Solutions to End of Chapter and MiFID Questions. Chapter 1

Solutions to End of Chapter and MiFID Questions Chapter 1 1. What is the NBBO (National Best Bid and Offer)? From 1978 onwards, it is obligatory for stock markets in the U.S. to coordinate the display

Solutions to End of Chapter and MiFID Questions Chapter 1 1. What is the NBBO (National Best Bid and Offer)? From 1978 onwards, it is obligatory for stock markets in the U.S. to coordinate the display

The Federal Reserve System

The Structure of Central Banks: The U.S. Federal Reserve and the European Central Bank McGraw-Hill/Irwin Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved. Twelve Regional Banks 16-2

The Structure of Central Banks: The U.S. Federal Reserve and the European Central Bank McGraw-Hill/Irwin Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved. Twelve Regional Banks 16-2

SEC-Required Report on Routing of Customer Orders For Quarter Ending June 30, 2011

Morgan Stanley & Co. LLC 1585 Broadway New York, NY 10036 SEC-Required Report on Routing of Customer Orders For Quarter Ending June 30, 2011 The Securities and Exchange Commission ("SEC" or "Commission")

Morgan Stanley & Co. LLC 1585 Broadway New York, NY 10036 SEC-Required Report on Routing of Customer Orders For Quarter Ending June 30, 2011 The Securities and Exchange Commission ("SEC" or "Commission")

Chapter 2 Self Study Questions

Chapter 2 Self Study Questions True/False Indicate whether the sentence or statement is true or false. 1. If an individual investor buys and sells existing stocks through a broker, these are primary market

Chapter 2 Self Study Questions True/False Indicate whether the sentence or statement is true or false. 1. If an individual investor buys and sells existing stocks through a broker, these are primary market

Your Name: Student Number: Signature:

Financiering P 6011P0088/ Finance PE 6011P0109 Midterm exam 23 April 2012 Your Name: Student Number: Signature: This is a closed-book exam. You are allowed to use a non-programmable calculator and a dictionary.

Financiering P 6011P0088/ Finance PE 6011P0109 Midterm exam 23 April 2012 Your Name: Student Number: Signature: This is a closed-book exam. You are allowed to use a non-programmable calculator and a dictionary.

Valuing Stock Options: The Black-Scholes-Merton Model. Chapter 13

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 1 The Black-Scholes-Merton Random Walk Assumption l Consider a stock whose price is S l In a short period of time of length t the return

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 1 The Black-Scholes-Merton Random Walk Assumption l Consider a stock whose price is S l In a short period of time of length t the return

Chapter 11. Portfolios. Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 11 Managing Bond Portfolios McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11.1 Interest Rate Risk 11-2 Interest Rate Sensitivity 1. Inverse relationship

Chapter 11 Managing Bond Portfolios McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11.1 Interest Rate Risk 11-2 Interest Rate Sensitivity 1. Inverse relationship

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

A Note on Effective Teaching and Interpretation of Compound Return Measures of Investment Performance

Financial Decisions, Fall 2002, Article 3. A Note on Effective Teaching and Interpretation of Compound Return Measures of Investment Performance Abstract J. Howard Finch* H. Shelton Weeks* *College of

Financial Decisions, Fall 2002, Article 3. A Note on Effective Teaching and Interpretation of Compound Return Measures of Investment Performance Abstract J. Howard Finch* H. Shelton Weeks* *College of

Chapter Sixteen Equipment Acquisition and Disposal

Purchasing and Supply Chain Management by W.C. Benton Chapter Sixteen Equipment Acquisition and Disposal McGraw-Hill/Irwin Copyright 2010 The McGraw-Hill Companies. All Rights Reserved. Learning Objectives

Purchasing and Supply Chain Management by W.C. Benton Chapter Sixteen Equipment Acquisition and Disposal McGraw-Hill/Irwin Copyright 2010 The McGraw-Hill Companies. All Rights Reserved. Learning Objectives

Lecture 4. Risk and Return: Lessons from Market History

Lecture 4 Risk and Return: Lessons from Market History Outline 1 Returns 2 Holding-Period Returns 3 Return Statistics 4 Average Stock Returns and Risk-Free Returns 5 Risk Statistics 6 More on Average Returns

Lecture 4 Risk and Return: Lessons from Market History Outline 1 Returns 2 Holding-Period Returns 3 Return Statistics 4 Average Stock Returns and Risk-Free Returns 5 Risk Statistics 6 More on Average Returns

Chapter 9 Debt Valuation and Interest Rates

Chapter 9 Debt Valuation and Interest Rates Slide Contents Learning Objectives Principles Used in This Chapter 1.Overview of Corporate Debt 2.Valuing Corporate Debt 3.Bond Valuation: Four Key Relationships

Chapter 9 Debt Valuation and Interest Rates Slide Contents Learning Objectives Principles Used in This Chapter 1.Overview of Corporate Debt 2.Valuing Corporate Debt 3.Bond Valuation: Four Key Relationships

Chapter 4. Discounted Cash Flow Valuation

Chapter 4 Discounted Cash Flow Valuation 1 Acknowledgement This work is reproduced, based on the book [Ross, Westerfield, Jaffe and Jordan Core Principles and Applications of Corporate Finance ]. This

Chapter 4 Discounted Cash Flow Valuation 1 Acknowledgement This work is reproduced, based on the book [Ross, Westerfield, Jaffe and Jordan Core Principles and Applications of Corporate Finance ]. This

Chapter 10:SECURITIES MARKETS

Chapter 10:SECURITIES MARKETS Trading Financial Resources 1 LOOKING AHEAD What are the different types of securities issued by a corporation? How are securities issued in the primary market and traded

Chapter 10:SECURITIES MARKETS Trading Financial Resources 1 LOOKING AHEAD What are the different types of securities issued by a corporation? How are securities issued in the primary market and traded

CHAPTER TWO Financial Statements and Cash Flow The Balance Sheet 19 Accounting Liquidity 20 Debt versus Equity 21

PART ONE CHAPTER ONE OVERVIEW Introduction to Corporate Finance 1 1.1 What Is Corporate Finance? 1 The Balance Sheet Model of the Firm 1 The Financial Manager 3 1.2 The Corporate Firm 4 The Sole Proprietorship

PART ONE CHAPTER ONE OVERVIEW Introduction to Corporate Finance 1 1.1 What Is Corporate Finance? 1 The Balance Sheet Model of the Firm 1 The Financial Manager 3 1.2 The Corporate Firm 4 The Sole Proprietorship

Market Microstructure

Market Microstructure (Text reference: Chapter 3) Topics Issuance of securities Types of markets Trading on exchanges Margin trading and short selling Trading costs Some regulations Nasdaq and the odd-eighths

Market Microstructure (Text reference: Chapter 3) Topics Issuance of securities Types of markets Trading on exchanges Margin trading and short selling Trading costs Some regulations Nasdaq and the odd-eighths

CHAPTER 9 SOME LESSONS FROM CAPITAL MARKET HISTORY

CHAPTER 9 SOME LESSONS FROM CAPITAL MARKET HISTORY Answers to Concepts Review and Critical Thinking Questions 1. They all wish they had! Since they didn t, it must have been the case that the stellar performance

CHAPTER 9 SOME LESSONS FROM CAPITAL MARKET HISTORY Answers to Concepts Review and Critical Thinking Questions 1. They all wish they had! Since they didn t, it must have been the case that the stellar performance

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21193 Nasdaq s Pursuit of Exchange Status and an Initial Public Offering Gary W. Shorter, Government and Finance Division

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21193 Nasdaq s Pursuit of Exchange Status and an Initial Public Offering Gary W. Shorter, Government and Finance Division

NASDAQ GEMX INET SYSTEM SETTINGS

NASDAQ GEMX INET SYSTEM SETTINGS 1. Hours of Operation 6:00 a.m. ET System begins accepting orders. 9:30 a.m. ET System begins disseminating imbalance and price information for the opening auction. 9:30

NASDAQ GEMX INET SYSTEM SETTINGS 1. Hours of Operation 6:00 a.m. ET System begins accepting orders. 9:30 a.m. ET System begins disseminating imbalance and price information for the opening auction. 9:30

Reading. Valuation of Securities: Bonds

Valuation of Securities: Bonds Econ 422: Investment, Capital & Finance University of Washington Last updated: April 11, 2010 Reading BMA, Chapter 3 http://finance.yahoo.com/bonds http://cxa.marketwatch.com/finra/marketd

Valuation of Securities: Bonds Econ 422: Investment, Capital & Finance University of Washington Last updated: April 11, 2010 Reading BMA, Chapter 3 http://finance.yahoo.com/bonds http://cxa.marketwatch.com/finra/marketd

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

Chapter 4. Investment Return and Risk

Chapter 4 Investment Return and Risk Return The reward for investing. Most returns are not guaranteed. E(r) is important factor in selection. Total Return consists of Current Income Appreciation 4-2 Importance

Chapter 4 Investment Return and Risk Return The reward for investing. Most returns are not guaranteed. E(r) is important factor in selection. Total Return consists of Current Income Appreciation 4-2 Importance

SEC Rule 606 Report & Rule 607 Disclosure

SEC Rule 607 Disclosure SEC Rule 607 requires all registered broker-dealers to provide disclosures to customers of payment for order flow practices upon the opening of a new account and annually thereafter.

SEC Rule 607 Disclosure SEC Rule 607 requires all registered broker-dealers to provide disclosures to customers of payment for order flow practices upon the opening of a new account and annually thereafter.

Investment Companies Pool funds of individual investors and invest in a wide range of securities or other assets. pooling of assets Mutual Funds and Other Investment Companies Provide several functions

Investment Companies Pool funds of individual investors and invest in a wide range of securities or other assets. pooling of assets Mutual Funds and Other Investment Companies Provide several functions

Chapter Organization 8.1. Common Stock Valuation 8.2. Some Features of Common and Preferred Stock 8.3. Stock Markets

Chapter 8 Stock Valuation Chapter Organization 8.. Some Features of Common and referred Stock A share of common stock is more difficult to value in practice than a bond for at least three reasons:. with

Chapter 8 Stock Valuation Chapter Organization 8.. Some Features of Common and referred Stock A share of common stock is more difficult to value in practice than a bond for at least three reasons:. with

Future Value of Multiple Cash Flows

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

Management. Christopher G. Lamoureux. March 28, Market (Micro-)Structure for Asset. Management. What? Recent History. Revolution in Trading

Structure for Asset. Management. What? Recent History. Revolution in Trading") Christopher G. Lamoureux March 28, 2014 Microstructure -is the study of how transactions take place. -is closely related to the concept of liquidity. It has descriptive and prescriptive aspects. In the

Christopher G. Lamoureux March 28, 2014 Microstructure -is the study of how transactions take place. -is closely related to the concept of liquidity. It has descriptive and prescriptive aspects. In the

Chapter 21: Savings Models Lesson Plan

Lesson Plan For All Practical Purposes Arithmetic Growth and Simple Interest Geometric Growth and Compound Interest Mathematical Literacy in Today s World, 8th ed. A Limit to Compounding A Model for Saving

Lesson Plan For All Practical Purposes Arithmetic Growth and Simple Interest Geometric Growth and Compound Interest Mathematical Literacy in Today s World, 8th ed. A Limit to Compounding A Model for Saving

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES Present value A dollar tomorrow is worth less than a dollar today. Why? 1) Present consumption preferred

Lesson 7 and 8 THE TIME VALUE OF MONEY. ACTUALIZATION AND CAPITALIZATION. CAPITAL BUDGETING TECHNIQUES Present value A dollar tomorrow is worth less than a dollar today. Why? 1) Present consumption preferred

Principles of Corporate Finance

Principles of Corporate Finance Professor James J. Barkocy The times they are a changin Bob Dylan McGraw-Hill/Irwin Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Dividend & Stock

Principles of Corporate Finance Professor James J. Barkocy The times they are a changin Bob Dylan McGraw-Hill/Irwin Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Dividend & Stock

Ian Domowitz Liquidity, Transaction Costs, and Reintermediation in Electronic Markets

Ian Domowitz Liquidity, Transaction Costs, and Reintermediation in Electronic Markets Comments George Sofianos February 23, 2001 An unbiased view? Goldman Sachs is a fully diversified firm upstairs desk

Ian Domowitz Liquidity, Transaction Costs, and Reintermediation in Electronic Markets Comments George Sofianos February 23, 2001 An unbiased view? Goldman Sachs is a fully diversified firm upstairs desk

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 1: The Corporation The Three Types of Firms -Sole Proprietorships -Owned and ran by one person -Owner has unlimited liability

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 1: The Corporation The Three Types of Firms -Sole Proprietorships -Owned and ran by one person -Owner has unlimited liability

Before and After Book COR1-GB Foundations of Finance

Before and After Book For COR1-GB.2311 Foundations of Finance William L. Silber Homepage: www.stern.nyu.edu/~wsilber Fall 2017 Contents of This Pamphlet For each topic in the syllabus this pamphlet provides:

Before and After Book For COR1-GB.2311 Foundations of Finance William L. Silber Homepage: www.stern.nyu.edu/~wsilber Fall 2017 Contents of This Pamphlet For each topic in the syllabus this pamphlet provides: