All young people aged 5-18, but particularly those aged 11-18, accessed through schools, predominantly for financial capability.

|

|

|

- Malcolm Walters

- 5 years ago

- Views:

Transcription

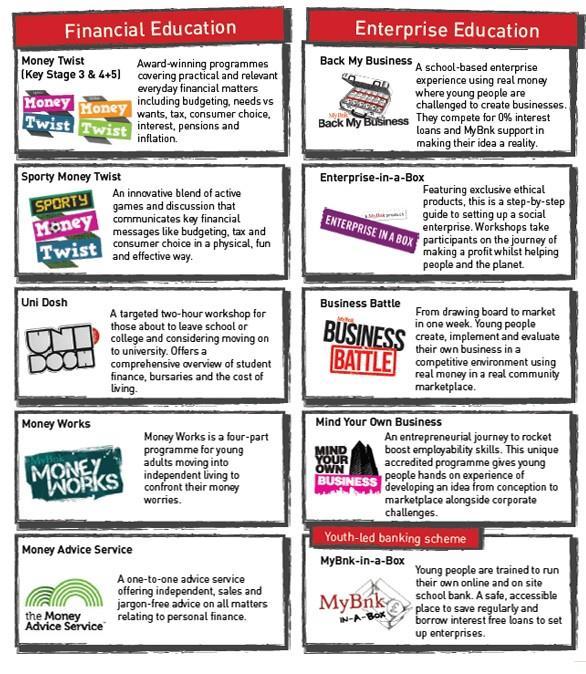

1 Background MyBnk is a charity that designs, develops and delivers financial and enterprise education programmes for year olds. Our experts deliver these workshops in schools and youth organisations in England. Our vision is to create a financially capable and enterprise-driven generation. Our mission is to empower young people to take charge of their future by bringing money and enterprise to life. Our Theory of Change focuses on the development of an individual s financial and career wellbeing through the provision of financial and enterprise education. Approximately half of our work is with: All young people aged 5-18, but particularly those aged 11-18, accessed through schools, predominantly for financial capability. Approximately half of our work is with: Vulnerable young people aged 16-25, primarily accessed outside of schools, for financial capability, enterprise and employability. Since inception in 2007 we have worked with more than 135,000 young people through 750 host organisations. We evaluate every programme we deliver for impact across a range of skills, knowledge and behaviours. MyBnk also tracks how effective participants thought sessions where and the value teachers placed on our aims, outcomes and methodology. Our flagship schools programme, Money Twist, has been given the UK s highest effectiveness rating of any youth financial literacy project by the Money Advice Service s (MAS) Evidence Hub. MyBnk also received the Impact Award from Project Oracle, The Mayor of London and Metropolitan University s children and youth evidence hub. In 2015 our survival money management programme, Money Works, won the Leaving Care Award from leading youth sector publication, Children and Young People Now. Throughout this response we have concentrated on giving insights based on our own direct experience of designing and delivering financial education programmes. Youth Financial Capability Group MyBnk is a founding member of the Youth Financial Capability Group, comprising of organisations committed to unbiased, relevant and effective financial education. We have worked together to help shape the government s Money Advice Service Financial Capability Strategy for the UK, with a particular focus on the children and youth strand. MyBnk is joined on the group by ifs University College, Personal Finance Education Group, National Skills Academy for Financial Services, The Money Charity and Stewart Ivory (Scotland).

2 Our programmes:

3 Summary and general comments MyBnk welcomes the opportunity to respond to the call for input for HM Treasury/ FCA consultation on the Financial Advice Market Review (FAMR). Our observations are in the context of us delivering financial and enterprise education to young people. In coming to our views we have consulted and collaborated closely with Youth Financial Capability Group. The views in our submission are our own. Our input MyBnk welcomes the Financial Advice Market Review. With the scale of change to the market set out in the review, it is clear that regulatory action is necessary to ensure that everyone, regardless of their financial circumstances, should have access to financial advice suitable for them. 1. We agree with the desire to focus on where we can make the greatest difference in terms of meeting needs for advice and for those products and people where advice can have the greatest positive impact. We question the focus should only be where complexity of decision making is greatest and advice could make the biggest difference e.g. Savings and investment, pensions and retirement planning and further do not agree with the almost exclusive concentration on a relatively small middle-income group with some money who are priced out of current regulated advice. We would put more emphasis on the much larger group of those with limited assets. 2. We believe that the terminology used to describe various forms of financial advice ought to be based on common sense terms that are best understood by the public. Throughout this consultation we refer to advice, from the regulated kind, through generic money advice (often referred to as guidance), to consumers use of price comparison websites as advice. 3. The FCA segmentation is useful in that it is very granular. In our view, three broader groups are sufficient to illustrate key points: a. A (large) group without the savings or income to make it commercially viable for IFAs to offer advice. (This includes those under 18 years of age not considered by the review). This group needs to be served by alternative advisors. b. A (relatively small) group representing a middle market of people with some money who are priced out of current regulated provision or who would not receive significant added value from it to justify the cost. c. A (relatively small) group of wealthy consumers who are well served by the existing regulated advice market. As a youth-focused charity with programmes aimed at the vulnerable, MyBnk deals almost exclusively with those within group a.

4 4. The focus of the questions posed are almost all concerned with improving access to regulated advice through IFAs. This results from the concentration on consumers with some money but not significant wealth (group b above). This is a real gap and we support considering the needs of this group, but we argue that the gap cannot and should not be met only by making it cheaper for regulated advisers to provide services. So as well as group a, group b also benefits from alternative providers being encouraged and allowed to go further with their advice offering. 5. We suggest group a. is the more significant group to consider for advice in all its forms. This group is making significant financial decisions with very little advice. Decisions could include whether to access student loans and whether to participate in workplace pensions. In both cases the government is in effect advising, through using implicit or explicit nudges to encourage participation. For example, the default option is set as participation for workplace pensions. As well as the positives, the financial negative implications to the individual of their decisions can be significant, in the case of student loans a future higher tax liability and for workplace pensions savings that may not be accessed for many decades. 6. The review states that people s need for financial advice starts with saving for short term needs and looks largely at investment advice. In reality, need begins with much more basic financial challenges such as budgeting. In order to attract people in all groups, financial advice needs to speak to these everyday needs and treat people s finances more holistically than simply discussing where best to make an investment. Currently alternative, online and not for profit (NPF) providers are meeting these needs better than IFAs will ever have an economic incentive to. A focus of the FAMR should be ensuring that this group has the nonregulated advice from alternative providers it needs. 7. The focus should be on positively defining what alternative providers can do. Currently, in each market (credit, mortgages, savings.) organisations are told what they cannot do. The extent of this varies from product to product, so organisations find it very difficult to know what they are able to say to consumers. These organisations are the future of financial advice for all but those with large investments to make, so what they are allowed to do must be defined positively, and rules should be in one place, not regulated from market to market. 8. MyBnk calls for an approach that tackles advice gaps from the bottom (low savings, relatively simple financial needs), as well as the top (with savings and complex financial decisions). There should be rules that allow regulated advisors to offer a form of advice at a cost that is appealing to more of the middle market, b, but also a single, easy to understand set of rules that lays out not only what alternative providers of advice cannot do, but gives them a positively defined role (whilst making clear that this sits outside the regulated perimeter). Through this approach, the aims of the FAMR could more easily go well beyond those with some money and produce an advice market capable of meeting the needs of everyone 9. Regulated IFAs are of particular relevance to those with substantial investible assets in particular owing to the complexity of taxation and regulation around pension and investment products. The FCA may be over-estimating the complexity of basic investment choices equities, property, fixed income securities and cash for example. It has been our experience

5 that the vast majority of young people can grasp the differing risks and returns of each asset class. The complications of tax and regulation are very significant for richer groups but unlikely to be so for those in group a on lower incomes and with few assets.

The Money Charity response to the 2018/19 Money Advice Service draft business plan

The Money Charity response to the 2018/19 Money Advice Service draft business plan The Money Charity is the UK s leading financial capability charity. We believe that being on top of your money means you

The Money Charity response to the 2018/19 Money Advice Service draft business plan The Money Charity is the UK s leading financial capability charity. We believe that being on top of your money means you

Consultation response: FCA Pension reforms

Consultation response: FCA Pension reforms Response by the Money Advice Trust Date: January 2016 Contents Page 2 Page 3 Page 4 Page 6 Contents Introduction / About the Money Advice Trust Introductory comment

Consultation response: FCA Pension reforms Response by the Money Advice Trust Date: January 2016 Contents Page 2 Page 3 Page 4 Page 6 Contents Introduction / About the Money Advice Trust Introductory comment

Financial Education Planning framework years

11-19 years Financial Education Planning framework 11-19 years Spend it, save it, give it, get it? Whatever we do with money, we need to manage it well. A planned programme of financial education, combining

11-19 years Financial Education Planning framework 11-19 years Spend it, save it, give it, get it? Whatever we do with money, we need to manage it well. A planned programme of financial education, combining

Sport England: Towards an Active Nation Strategy progress and work with councils

Sport England: Towards an Active Nation Strategy 2016-2021 progress and work with councils Purpose As background to the Sport England presentation and subsequent discussion. Summary Sport England s Towards

Sport England: Towards an Active Nation Strategy 2016-2021 progress and work with councils Purpose As background to the Sport England presentation and subsequent discussion. Summary Sport England s Towards

MEMBER SOLUTIONS. Partnering with Employers and Old Mutual retirement fund members to achieve the financial futures they deserve.

MEMBER SOLUTIONS Partnering with Employers and Old Mutual retirement fund members to achieve the financial futures they deserve. HELPING TO CREATE A BETTER FUTURE FOR ALL As one of southern Africa s oldest

MEMBER SOLUTIONS Partnering with Employers and Old Mutual retirement fund members to achieve the financial futures they deserve. HELPING TO CREATE A BETTER FUTURE FOR ALL As one of southern Africa s oldest

Consultation response: Financial Capability Strategy for the UK

Consultation response: Financial Capability Strategy for the UK Response by the Money Advice Trust Date: October 2014 Contents Page 2 Page 3 Page 4 Page 5 Contents Introduction / About the Money Advice

Consultation response: Financial Capability Strategy for the UK Response by the Money Advice Trust Date: October 2014 Contents Page 2 Page 3 Page 4 Page 5 Contents Introduction / About the Money Advice

Aon Defined Contribution. Aon s Global Defined Contribution Points of View

Aon Defined Contribution Aon s Global Defined Contribution Points of View Aon s Global Defined Contribution Points of View Around the globe Aon is helping our clients tackle the challenges that come with

Aon Defined Contribution Aon s Global Defined Contribution Points of View Aon s Global Defined Contribution Points of View Around the globe Aon is helping our clients tackle the challenges that come with

Protection of Vulnerable Groups Act: consultation on draft guidance and secondary legislation

Protection of Vulnerable Groups Act: consultation on draft guidance and secondary legislation Response from the Click here to read the consultation documents. Modification of Regulated Work with Children

Protection of Vulnerable Groups Act: consultation on draft guidance and secondary legislation Response from the Click here to read the consultation documents. Modification of Regulated Work with Children

Any gifts you make to the Engineers Trust (or any registered charity) during your lifetime or in your will will be exempt from Inheritance Tax.

during your lifetime or in your will will be exempt from Inheritance Tax.") Thank you Thank you for thinking of the Engineers Trust (the Worshipful Company of Engineers Charitable Trust) in connection with your Will, and for taking the time to read this booklet. We hope that you

Thank you Thank you for thinking of the Engineers Trust (the Worshipful Company of Engineers Charitable Trust) in connection with your Will, and for taking the time to read this booklet. We hope that you

True freedom is the ability to choose how you live your life

True freedom is the ability to choose how you live your life primepartners.com.au We help you predict your future by helping you create it. Prime Partners was established in July 2006 following a merger

True freedom is the ability to choose how you live your life primepartners.com.au We help you predict your future by helping you create it. Prime Partners was established in July 2006 following a merger

National Strategy for Financial Capability

Introducing National Strategy for Financial Capability Susan Cassar, Regional Manager, Financial Capability, Financial Services Authority Telephone: 07967 279064 email: susan.cassar@fsa.gov.uk Who is the

Introducing National Strategy for Financial Capability Susan Cassar, Regional Manager, Financial Capability, Financial Services Authority Telephone: 07967 279064 email: susan.cassar@fsa.gov.uk Who is the

Work and Pensions Committee inquiry on guidance and advice

Work and Pensions Committee inquiry on guidance and advice Response from the Money Advice Service August 2015 1 1. The Money Advice Service is pleased to have the opportunity to submit evidence to the

Work and Pensions Committee inquiry on guidance and advice Response from the Money Advice Service August 2015 1 1. The Money Advice Service is pleased to have the opportunity to submit evidence to the

MYTHS. The Truth about Poverty in Abbotsford

The Truth about Poverty in Abbotsford MYTHS Abbotsford has experienced tremendous growth in recent years. The population expanded by 7.2% between 2001 and 2006, higher than the provincial average. During

The Truth about Poverty in Abbotsford MYTHS Abbotsford has experienced tremendous growth in recent years. The population expanded by 7.2% between 2001 and 2006, higher than the provincial average. During

West Midlands Pension Fund. Customer Engagement Strategy 2018

West Midlands Pension Fund Customer Engagement Strategy 2018 June 2018 Customer Engagement Strategy 2018 Background The West Midlands Pension Fund ( The Fund ) is one of the UK s largest pension funds

West Midlands Pension Fund Customer Engagement Strategy 2018 June 2018 Customer Engagement Strategy 2018 Background The West Midlands Pension Fund ( The Fund ) is one of the UK s largest pension funds

Young People and Money Report

Young People and Money Report 2018 marks the Year of Young People, a Scottish Government initiative giving young people a platform to voice issues that affect their lives and allowing us to celebrate their

Young People and Money Report 2018 marks the Year of Young People, a Scottish Government initiative giving young people a platform to voice issues that affect their lives and allowing us to celebrate their

Tailored and experiential training for the insurance industry

Tailored and experiential training for the insurance industry We believe in learning by doing. Our experiential approach to learning helps engage participants at a deep level and ensure they gain practical

Tailored and experiential training for the insurance industry We believe in learning by doing. Our experiential approach to learning helps engage participants at a deep level and ensure they gain practical

A New Future for Social Security in Scotland Consultation

AIC/16/22 Agenda item 11 7 September 2016 A New Future for Social Security in Scotland Consultation Purpose of the paper The purpose of this paper is to inform the AIC about the Scottish Government s consultation

AIC/16/22 Agenda item 11 7 September 2016 A New Future for Social Security in Scotland Consultation Purpose of the paper The purpose of this paper is to inform the AIC about the Scottish Government s consultation

Together leading in risk. Join the association for everyone with a responsibility in risk and insurance

Together leading in risk Join the association for everyone with a responsibility in risk and insurance Advancing the future of risk and insurance Airmic is the association for UK risk and insurance managers,

Together leading in risk Join the association for everyone with a responsibility in risk and insurance Advancing the future of risk and insurance Airmic is the association for UK risk and insurance managers,

9/4/2018. Start with Why. Financial Wellbeing. The reasons employers are investing in wellbeing are shifting. Rebecca Kruske September 2018

Rebecca Kruske September 2018 Financial Wellbeing 2 Start with Why The reasons employers are investing in wellbeing are shifting 1. Reducing healthcare costs (60%) 2. Creating a desirable culture (43%)

Rebecca Kruske September 2018 Financial Wellbeing 2 Start with Why The reasons employers are investing in wellbeing are shifting 1. Reducing healthcare costs (60%) 2. Creating a desirable culture (43%)

Delegation of Finnish Impact Investment Study Visit Katie Hill Social Investment Advisor City of London Corporation

Delegation of Finnish Impact Investment Study Visit Katie Hill Social Investment Advisor City of London Corporation Copyright with City of London Corporation Spectrum of social impact investments Social

Delegation of Finnish Impact Investment Study Visit Katie Hill Social Investment Advisor City of London Corporation Copyright with City of London Corporation Spectrum of social impact investments Social

RETIREMENT REPORT ADEQUATE SAVINGS INDEX

RETIREMENT REPORT 2017 ADEQUATE SAVINGS INDEX Since 2005, the annual Scottish Widows Retirement Report Adequate Savings Index has provided a barometer of retirement savings levels across the UK. Over the

RETIREMENT REPORT 2017 ADEQUATE SAVINGS INDEX Since 2005, the annual Scottish Widows Retirement Report Adequate Savings Index has provided a barometer of retirement savings levels across the UK. Over the

Guidance and the Financial Advice Market Review. Tom McPhail Head of policy

Guidance and the Financial Advice Market Review Tom McPhail Head of policy Purpose of FAMR Explore the regulatory framework governing the provision of financial advice and guidance and its effectiveness

Guidance and the Financial Advice Market Review Tom McPhail Head of policy Purpose of FAMR Explore the regulatory framework governing the provision of financial advice and guidance and its effectiveness

WORKING IN THE BANK OF ENGLAND S LEGAL DIRECTORATE

WORKING IN THE BANK OF ENGLAND S LEGAL DIRECTORATE 2 Working at the heart of the UK financial system throws up unique and intellectually stimulating challenges and our lawyers consistently rise to meet

WORKING IN THE BANK OF ENGLAND S LEGAL DIRECTORATE 2 Working at the heart of the UK financial system throws up unique and intellectually stimulating challenges and our lawyers consistently rise to meet

Financial Management in the Department for Children, Schools and Families

Financial Management in the Department for Children, Schools and Families LONDON: The Stationery Office 14.35 Ordered by the House of Commons to be printed on 28 April 2009 REPORT BY THE COMPTROLLER AND

Financial Management in the Department for Children, Schools and Families LONDON: The Stationery Office 14.35 Ordered by the House of Commons to be printed on 28 April 2009 REPORT BY THE COMPTROLLER AND

Pension freedoms inquiry IFoA response to Work and Pensions Committee

Pension freedoms inquiry IFoA response to Work and Pensions Committee 23 October 2017 About the Institute and Faculty of Actuaries The Institute and Faculty of Actuaries is the chartered professional body

Pension freedoms inquiry IFoA response to Work and Pensions Committee 23 October 2017 About the Institute and Faculty of Actuaries The Institute and Faculty of Actuaries is the chartered professional body

Review of the Money Advice Service

Telephone: 020 7066 9346 Email: enquiries@fs-cp.org.uk Independent Money Advice Service Review 1 Horse Guards Road London SW1A 2HQ 1 September 2014 Review of the Money Advice Service This is the Financial

Telephone: 020 7066 9346 Email: enquiries@fs-cp.org.uk Independent Money Advice Service Review 1 Horse Guards Road London SW1A 2HQ 1 September 2014 Review of the Money Advice Service This is the Financial

Preparing for Retirement: The Lost Generation Comes of Age

Preparing for Retirement: The Lost Generation Comes of Age About the Study T. Rowe Price engaged Brightwork Partners to conduct a national study of 3,022 adults aged 18 and older who have never retired

Preparing for Retirement: The Lost Generation Comes of Age About the Study T. Rowe Price engaged Brightwork Partners to conduct a national study of 3,022 adults aged 18 and older who have never retired

Retirement Planning. Introduction. Evidence and key issues. Financial capability and retirement

Retirement Planning Retirement Planning The entire retirement planning landscape has undergone significant change in the last decade, and this seems likely to continue. Given the evolving environment of

Retirement Planning Retirement Planning The entire retirement planning landscape has undergone significant change in the last decade, and this seems likely to continue. Given the evolving environment of

Adult Financial Literacy

MoneyWhizz Adult Financial Literacy An analysis Frank Conway State of Financial Literacy Among Adult Population In Ireland Frank Conway January 2016 INTRODUCTION - Across the globe, advances in financial

MoneyWhizz Adult Financial Literacy An analysis Frank Conway State of Financial Literacy Among Adult Population In Ireland Frank Conway January 2016 INTRODUCTION - Across the globe, advances in financial

Association of Accounting Technicians response to the HM Treasury and Department for Work and Pensions Public financial guidance review: consultation

Association of Accounting Technicians response to the HM Treasury and Department for Work and Pensions Public financial guidance review: consultation on a single body 1 Association of Accounting Technicians

Association of Accounting Technicians response to the HM Treasury and Department for Work and Pensions Public financial guidance review: consultation on a single body 1 Association of Accounting Technicians

HMT / DWP Public financial guidance review: Consultation on a single body ABI response to consultation

HMT / DWP Public financial guidance review: Consultation on a single body ABI response to consultation 13 February 2017 About the Association of British Insurers The Association of British Insurers is

HMT / DWP Public financial guidance review: Consultation on a single body ABI response to consultation 13 February 2017 About the Association of British Insurers The Association of British Insurers is

Donna L. Fisher, CFP. Senior Vice President Financial Advisor

Donna L. Fisher, CFP Senior Vice President Financial Advisor 7272 Wisconsin Avenue 4th Floor, Bethesda, Maryland 20814 301-657-6325 / Main 800-455-6622 / Toll-Free 301-656-1510 / fax donna.l.fisher@mssb.com

Donna L. Fisher, CFP Senior Vice President Financial Advisor 7272 Wisconsin Avenue 4th Floor, Bethesda, Maryland 20814 301-657-6325 / Main 800-455-6622 / Toll-Free 301-656-1510 / fax donna.l.fisher@mssb.com

Consultation Response

Consultation Response FCA consultation: Implementing information prompts in the annuity market February 2017 Ref: 1017 All rights reserved. Third parties may only reproduce this paper or parts of it for

Consultation Response FCA consultation: Implementing information prompts in the annuity market February 2017 Ref: 1017 All rights reserved. Third parties may only reproduce this paper or parts of it for

HM Treasury s consultation on amending the definition of financial advice

Telephone: 020 7066 9346 Email: enquiries@fs-cp.org.uk Assets, Savings and Consumers HM Treasury 1 Horse Guards Road London SW1A 2HQ 15 November 2016 Dear Sir, Madam, HM Treasury s consultation on amending

Telephone: 020 7066 9346 Email: enquiries@fs-cp.org.uk Assets, Savings and Consumers HM Treasury 1 Horse Guards Road London SW1A 2HQ 15 November 2016 Dear Sir, Madam, HM Treasury s consultation on amending

Association of Accounting Technicians response to the Department for Work and Pensions consultation Security and Sustainability in Defined Benefit

Association of Accounting Technicians response to the Department for Work and Pensions consultation Security and Sustainability in Defined Benefit Pension Schemes 1 Association of Accounting Technicians

Association of Accounting Technicians response to the Department for Work and Pensions consultation Security and Sustainability in Defined Benefit Pension Schemes 1 Association of Accounting Technicians

Planning for the future: Our 2017 General Election manifesto

Planning for the future: Our 2017 General Election manifesto Foreword This election is crucial for older people. By 2030, there will be an estimated 15.7 million people in the UK aged 65 and over. Whilst

Planning for the future: Our 2017 General Election manifesto Foreword This election is crucial for older people. By 2030, there will be an estimated 15.7 million people in the UK aged 65 and over. Whilst

ASSESSING AMERICANS FINANCIAL AND RETIREMENT SECURITY

ASSESSING AMERICANS FINANCIAL AND RETIREMENT SECURITY AMERICAN COUNCIL OF LIFE INSURERS September 2017 OVERVIEW Millions of American households are on track to a financially secure future as a result of

ASSESSING AMERICANS FINANCIAL AND RETIREMENT SECURITY AMERICAN COUNCIL OF LIFE INSURERS September 2017 OVERVIEW Millions of American households are on track to a financially secure future as a result of

Equity release. - an integral feature in a retirement account. Whitepaper. An examination of how equity release will be used in retirement planning

Equity release - an integral feature in a retirement account Whitepaper An examination of how equity release will be used in retirement planning Contents 3 Synopsis 4 A holistic retirement proposition

Equity release - an integral feature in a retirement account Whitepaper An examination of how equity release will be used in retirement planning Contents 3 Synopsis 4 A holistic retirement proposition

TAMESIDE CHILDREN S SERVICES IMPROVEMENT PLAN

Report to: EXECUTIVE CABINET Date: 22 March 2017 Executive Member / Reporting Officer: Subject: Report Summary: Recommendations: Links to Community Strategy: Financial Implications: (Authorised by the

Report to: EXECUTIVE CABINET Date: 22 March 2017 Executive Member / Reporting Officer: Subject: Report Summary: Recommendations: Links to Community Strategy: Financial Implications: (Authorised by the

The Money Charity is the UK s leading financial capability charity.

The Money Charity is the UK s leading financial capability charity. We believe that being on top of your money means you are more in control of your life, your finances and your debts, reducing stress

The Money Charity is the UK s leading financial capability charity. We believe that being on top of your money means you are more in control of your life, your finances and your debts, reducing stress

2015 General Election Manifesto. icaew.com2

2015 General Election Manifesto BUSINESS icaew.com WITH CONFIDENCE icaew.com2 Foreword Ahead of the 2015 General Election, Britain faces a choice. We can accept short-term growth with underlying structural

2015 General Election Manifesto BUSINESS icaew.com WITH CONFIDENCE icaew.com2 Foreword Ahead of the 2015 General Election, Britain faces a choice. We can accept short-term growth with underlying structural

DIPLOMA IN INSURANCE (Dip CII) CHARTERED INSURANCE INSTITUTE

CHARTERED INSURANCE INSTITUTE") DIPLOMA IN INSURANCE (Dip CII) CHARTERED INSURANCE INSTITUTE BANKING ACCOUNTING & FINANCE ISLAMIC FINANCE IT & PROJECT MANAGEMENT INSURANCE LEADERSHIP & MANAGEMENT EXECUTIVE LEADERSHIP ACADEMIC STUDIES

DIPLOMA IN INSURANCE (Dip CII) CHARTERED INSURANCE INSTITUTE BANKING ACCOUNTING & FINANCE ISLAMIC FINANCE IT & PROJECT MANAGEMENT INSURANCE LEADERSHIP & MANAGEMENT EXECUTIVE LEADERSHIP ACADEMIC STUDIES

DC INVESTOR SURVEY. Biannual Report. Financial stress impedes employees ability to take action and hurts the corporate bottom line.

March 2015 DC INVESTOR SURVEY Biannual Report Financial stress impedes employees ability to take action and hurts the corporate bottom line i Investor Survey March 2015 ssga.com/definedcontribution About

March 2015 DC INVESTOR SURVEY Biannual Report Financial stress impedes employees ability to take action and hurts the corporate bottom line i Investor Survey March 2015 ssga.com/definedcontribution About

Automatic enrolment to workplace pensions

Report by the Comptroller and Auditor General Department for Work & Pensions Automatic enrolment to workplace pensions HC 417 SESSION 2015-16 4 NOVEMBER 2015 4 Key facts Automatic enrolment to workplace

Report by the Comptroller and Auditor General Department for Work & Pensions Automatic enrolment to workplace pensions HC 417 SESSION 2015-16 4 NOVEMBER 2015 4 Key facts Automatic enrolment to workplace

NATIONAL FINANCIAL LITERACY PROGRAMME TRINIDAD & TOBAGO

NATIONAL FINANCIAL LITERACY PROGRAMME TRINIDAD & TOBAGO Presented By: Ladi Franklin SUMMARY Financial Literacy in context Objectives Achievements Key Success Factors Challenges 2 FINANCIAL LITERACY IN

NATIONAL FINANCIAL LITERACY PROGRAMME TRINIDAD & TOBAGO Presented By: Ladi Franklin SUMMARY Financial Literacy in context Objectives Achievements Key Success Factors Challenges 2 FINANCIAL LITERACY IN

Food poverty in London: A submission from Child Poverty Action Group

Food poverty in London: A submission from Child Poverty Action Group Child Poverty Action is the leading national charity working to end poverty among children, young people and families in the UK. Our

Food poverty in London: A submission from Child Poverty Action Group Child Poverty Action is the leading national charity working to end poverty among children, young people and families in the UK. Our

The Revenue Scotland and Tax Powers Bill Call for Evidence Response from the Low Incomes Tax Reform Group ( LITRG )

") The Revenue Scotland and Tax Powers Bill Call for Evidence Response from the Low Incomes Tax Reform Group ( LITRG ) 1 Executive Summary 1.1 The LITRG welcomes the opportunity to respond to the Scottish

The Revenue Scotland and Tax Powers Bill Call for Evidence Response from the Low Incomes Tax Reform Group ( LITRG ) 1 Executive Summary 1.1 The LITRG welcomes the opportunity to respond to the Scottish

LSI YW12(SQA Unit Code-HD9H 04) Work with young people to manage resources for youth work activities

Work with young people to manage resources for youth work activities") Work with young people to manage resources for youth work activities Overview This standard is for youth workers who support young people to manage resources, including finances, for an event, activity

Work with young people to manage resources for youth work activities Overview This standard is for youth workers who support young people to manage resources, including finances, for an event, activity

Business Resilience Survey 2016

Business Resilience Survey 2016 Summary of results Introduction The CCPS business resilience survey is an annual survey providing an overview of how third sector social care and support providers are doing

Business Resilience Survey 2016 Summary of results Introduction The CCPS business resilience survey is an annual survey providing an overview of how third sector social care and support providers are doing

Programme Development and Funding Officer

Programme Development and Funding Officer Candidate Pack Thank you for showing an interest in working for Age International. Age International is a subsidiary charity of Age UK. As such, it is supported

Programme Development and Funding Officer Candidate Pack Thank you for showing an interest in working for Age International. Age International is a subsidiary charity of Age UK. As such, it is supported

FINANCIAL WELLNESS. We all need a little guidance sometimes. Let s talk.

FINANCIAL WELLNESS MMI s purpose is to enhance the lifetime Financial Wellness of people, their communities and their businesses. MMI s definition of Financial Wellness for a household or individual is

FINANCIAL WELLNESS MMI s purpose is to enhance the lifetime Financial Wellness of people, their communities and their businesses. MMI s definition of Financial Wellness for a household or individual is

Meeting the retirement challenge New approaches and solutions for the financial services industry

Meeting the retirement challenge New approaches and solutions for the financial services industry Sam Friedman Research Leader, Insurance Deloitte Center for Financial Services Val Srinivas Research Leader,

Meeting the retirement challenge New approaches and solutions for the financial services industry Sam Friedman Research Leader, Insurance Deloitte Center for Financial Services Val Srinivas Research Leader,

Viewpoint Results Summary. Bank of England October 2017

Viewpoint 2017 Results Summary Bank of England October 2017 Overview: Understanding how employees feel about working in the Bank is of huge importance to the Governors and senior management. Between 5

Viewpoint 2017 Results Summary Bank of England October 2017 Overview: Understanding how employees feel about working in the Bank is of huge importance to the Governors and senior management. Between 5

VC CATALYST. Request for Proposals

VC CATALYST Request for Proposals Legal Notices British Business Investments is the trading name of British Business Bank Investments Ltd, a wholly owned subsidiary of British Business Bank plc, registered

VC CATALYST Request for Proposals Legal Notices British Business Investments is the trading name of British Business Bank Investments Ltd, a wholly owned subsidiary of British Business Bank plc, registered

Monday, September 10, 2012

OECD-Bangko Sentral Ng Pilipinas Asian Seminar on Financial Literacy and Inclusion: Addressing the Upcoming Challenges 11 12 September 2012, Cebu, Philippines 1 2 3 Financial education (FE) initiatives

OECD-Bangko Sentral Ng Pilipinas Asian Seminar on Financial Literacy and Inclusion: Addressing the Upcoming Challenges 11 12 September 2012, Cebu, Philippines 1 2 3 Financial education (FE) initiatives

Make your financial future bright and easy. With your own financial plan. hatchplan.co.uk

Make your financial future bright and easy. With your own financial plan. hatchplan.co.uk Hatch in a nutshell We brighten employees financial futures in 3 simple steps 1 Set Goals 2 Get your Plan 3 Stay

Make your financial future bright and easy. With your own financial plan. hatchplan.co.uk Hatch in a nutshell We brighten employees financial futures in 3 simple steps 1 Set Goals 2 Get your Plan 3 Stay

MOVING THE NEEDLE ON EMPLOYEE FINANCIAL WELLNESS

HEALTH WEALTH CAREER FINDINGS FROM MERCER CANADA'S INSIDE EMPLOYEES' MINDS SURVEY MOVING THE NEEDLE ON EMPLOYEE PRACTICAL STEPS FOR CANADIAN EMPLOYERS 2 THE CHALLENGE OF EMPLOYEE A GROWING NUMBER OF EMPLOYERS

HEALTH WEALTH CAREER FINDINGS FROM MERCER CANADA'S INSIDE EMPLOYEES' MINDS SURVEY MOVING THE NEEDLE ON EMPLOYEE PRACTICAL STEPS FOR CANADIAN EMPLOYERS 2 THE CHALLENGE OF EMPLOYEE A GROWING NUMBER OF EMPLOYERS

Financial Capability. For Europe s Youth And Pre-retirees: Financial Capability. For Europe s Youth And Pre-retirees:

Financial Capability For Europe s Youth And Pre-retirees: Improving The Provision Of Financial Education And Advice Citi Foundation The Citi Foundation is committed to the economic empowerment and financial

Financial Capability For Europe s Youth And Pre-retirees: Improving The Provision Of Financial Education And Advice Citi Foundation The Citi Foundation is committed to the economic empowerment and financial

Innovation and growth factsheet series

Innovation and growth factsheet series 13 March 2017 Introduction This factsheet 1 provides a high-level overview of finance relevant to universities funding local growth, regeneration and capital projects.

Innovation and growth factsheet series 13 March 2017 Introduction This factsheet 1 provides a high-level overview of finance relevant to universities funding local growth, regeneration and capital projects.

Financial Wellness. HOUSEHOLD FINANCIAL CAPABILITY.

Financial Wellness. HOUSEHOLD FINANCIAL CAPABILITY. November 16 Annamaria Lusardi, Ph.D., is the founder and academic director of the Global Financial Literacy Excellence Center (GFLEC) at the George Washington

Financial Wellness. HOUSEHOLD FINANCIAL CAPABILITY. November 16 Annamaria Lusardi, Ph.D., is the founder and academic director of the Global Financial Literacy Excellence Center (GFLEC) at the George Washington

TAX EXPENDITURES FOR RETIREMENT PLANS

TAX EXPENDITURES FOR RETIREMENT PLANS The tax law recently enacted by Congress includes a great many provisions Some are easy to understand Others are not Among the least understood provisions are those

TAX EXPENDITURES FOR RETIREMENT PLANS The tax law recently enacted by Congress includes a great many provisions Some are easy to understand Others are not Among the least understood provisions are those

CH ISSUE Minding the assets isn t enough: you need to take care of the whole family, says Stonehage Fleming s Jacqui Cheshire

CH CITYWIRE.CH Minding the assets isn t enough: you need to take care of the whole family, says Fleming s Jacqui Cheshire FOR SWISS INDEPENDENT ASSET MANAGERS The of planning Today s international family

CH CITYWIRE.CH Minding the assets isn t enough: you need to take care of the whole family, says Fleming s Jacqui Cheshire FOR SWISS INDEPENDENT ASSET MANAGERS The of planning Today s international family

The Real Deal 2018 Retirement Income Adequacy Study

The Real Deal 2018 Retirement Income Adequacy Study Table of Contents Introduction.... 3 What's New in The Real Deal?... 6 Retirement Readiness The Averages.... 7 Savings Rates... 10 Income.... 15 Generations....

The Real Deal 2018 Retirement Income Adequacy Study Table of Contents Introduction.... 3 What's New in The Real Deal?... 6 Retirement Readiness The Averages.... 7 Savings Rates... 10 Income.... 15 Generations....

Independent safeguarding authority and statement of Secretary of State for Education on scheme changes

Briefing 09-68 December 2009 Independent safeguarding authority and statement of Secretary of State for Education on scheme changes This briefing is provided to APSE contacts in England, Scotland, Wales

Briefing 09-68 December 2009 Independent safeguarding authority and statement of Secretary of State for Education on scheme changes This briefing is provided to APSE contacts in England, Scotland, Wales

Is the UK retirement ready?

Is the UK ready? We surveyed British adults of all ages and analysed industry research to find out the answer to this much contemplated question. Explore the results. Whitepaper by Age Partnership, released

Is the UK ready? We surveyed British adults of all ages and analysed industry research to find out the answer to this much contemplated question. Explore the results. Whitepaper by Age Partnership, released

AIM Inheritance Tax Portfolio

AIM Inheritance Tax Portfolio Aiming to reduce your inheritance tax bill For those investors prepared to accept the additional risks of investing in AIM, there are tax benefits. AIM stocks are free of

AIM Inheritance Tax Portfolio Aiming to reduce your inheritance tax bill For those investors prepared to accept the additional risks of investing in AIM, there are tax benefits. AIM stocks are free of

A positive outlook on auto-enrolment contributions phasing. High

A positive outlook on auto-enrolment contributions phasing High Summary UK businesses are focusing on securing the organisation s future by strengthening their competitive position, increasing revenue

A positive outlook on auto-enrolment contributions phasing High Summary UK businesses are focusing on securing the organisation s future by strengthening their competitive position, increasing revenue

StepChange Debt Charity consultation response to HM Treasury

Goods Mortgages Bill: Consultation StepChange Debt Charity consultation response to HM Treasury October 2017 StepChange Debt Charity London Office 6th Floor, Lynton House, 7-12 Tavistock Square, London

Goods Mortgages Bill: Consultation StepChange Debt Charity consultation response to HM Treasury October 2017 StepChange Debt Charity London Office 6th Floor, Lynton House, 7-12 Tavistock Square, London

February earnings.

Written evidence submitted by Citizens Advice to the Department of Work and Pensions, HM Treasury and HM Revenue & Customs consultation on the abolition of Class National Insurance and introducing a benefit

Written evidence submitted by Citizens Advice to the Department of Work and Pensions, HM Treasury and HM Revenue & Customs consultation on the abolition of Class National Insurance and introducing a benefit

METROPOLITAN POLICE SERVICE: GENDER PAY GAP ANALYSIS 2018

EXECUTIVE SUMMARY METROPOLITAN POLICE SERVICE: GENDER PAY GAP ANALYSIS 2018 1. As an organisation with more than 250 employees, we are required by law to publish our gender pay figures. This is the third

EXECUTIVE SUMMARY METROPOLITAN POLICE SERVICE: GENDER PAY GAP ANALYSIS 2018 1. As an organisation with more than 250 employees, we are required by law to publish our gender pay figures. This is the third

Meaningful financial planning. Putting you in the best place to achieve your financial goals

Meaningful financial planning Putting you in the best place to achieve your financial goals Helping you achieve your financial goals We believe having a financial plan in place will help you achieve your

Meaningful financial planning Putting you in the best place to achieve your financial goals Helping you achieve your financial goals We believe having a financial plan in place will help you achieve your

FINANCING THE FUTURE

FINANCING THE FUTURE A report on student awareness of the impact of poor money management while at university Introduction Managing money can be one of the biggest challenges students face at university.

FINANCING THE FUTURE A report on student awareness of the impact of poor money management while at university Introduction Managing money can be one of the biggest challenges students face at university.

Protecting Families. Getting the conversation started. Retirement Investments Insurance Health

Retirement Investments Insurance Health Protecting Families Getting the conversation started For financial adviser use only. Not approved for use with customers. Unearthing opportunities in an ever-changing

Retirement Investments Insurance Health Protecting Families Getting the conversation started For financial adviser use only. Not approved for use with customers. Unearthing opportunities in an ever-changing

Helping People Make the Most of Their Pensions David Berenbaum, TPAS Philip Brown, Head of Policy LV=

Helping People Make the Most of Their Pensions David Berenbaum, TPAS Philip Brown, Head of Policy LV= David Berenbaum TPAS 1 The pension landscape has changed so that individuals need to take responsibility

Helping People Make the Most of Their Pensions David Berenbaum, TPAS Philip Brown, Head of Policy LV= David Berenbaum TPAS 1 The pension landscape has changed so that individuals need to take responsibility

Building Your Future. Basics in Budgeting. in BLOG. Extraco Banks is a Member FDIC.

Building Your Future Basics in Budgeting Extraco Banks is a Member FDIC. f in BLOG TABLE OF CONTENTS DEBT Assessment WEALTH What is wealth? Net worth 2 3-5 BUDGET 6-7 Financial goals Budget worksheet INVEST

Building Your Future Basics in Budgeting Extraco Banks is a Member FDIC. f in BLOG TABLE OF CONTENTS DEBT Assessment WEALTH What is wealth? Net worth 2 3-5 BUDGET 6-7 Financial goals Budget worksheet INVEST

Association of Accounting Technicians response to the HMRC Consultation on salary sacrifice for the provision of benefits in kind

Association of Accounting Technicians response to the HMRC Consultation on salary sacrifice for the provision of benefits in kind 1 Association of Accounting Technicians response to the HMRC Consultation

Association of Accounting Technicians response to the HMRC Consultation on salary sacrifice for the provision of benefits in kind 1 Association of Accounting Technicians response to the HMRC Consultation

For review, comment and to spark conversations.version as at 01 September 2016

2.6 Local economy 2.6.1 Markets and sectors This section looks at some of Newcastle s economic strengths together with some of the risks facing the local economy. Note: Gross Value Added (GVA) is the standard

2.6 Local economy 2.6.1 Markets and sectors This section looks at some of Newcastle s economic strengths together with some of the risks facing the local economy. Note: Gross Value Added (GVA) is the standard

HMRC Consultation: Large Business compliance enhancing our risk assessment approach Response by the Chartered Institute of Taxation

HMRC Consultation: Large Business compliance enhancing our risk assessment approach Response by the Chartered Institute of Taxation 1 Introduction 1.1 This consultation document is examining how HM Revenue

HMRC Consultation: Large Business compliance enhancing our risk assessment approach Response by the Chartered Institute of Taxation 1 Introduction 1.1 This consultation document is examining how HM Revenue

The Warm Home Discount Scheme Consultation response by National Energy Action (NEA)

") The Warm Home Discount Scheme Consultation response by National Energy Action (NEA) 1. About NEA 1.1 NEA is an independent charity working to protect low income and vulnerable households from fuel poverty

The Warm Home Discount Scheme Consultation response by National Energy Action (NEA) 1. About NEA 1.1 NEA is an independent charity working to protect low income and vulnerable households from fuel poverty

Pension Report. Retirement Reality

Pension Report Retirement Reality Exec summary The number of people saving into a pension is at a record high but the amount they are saving on average is at a record low 1. This report surveyed 2 2,010

Pension Report Retirement Reality Exec summary The number of people saving into a pension is at a record high but the amount they are saving on average is at a record low 1. This report surveyed 2 2,010

Your guide to the fundamentals of investing

Your guide to the fundamentals of investing Your money. Our expertise. This guide is for information purposes only. It should not be seen as advice. Investments in the stock market may fall as well as

Your guide to the fundamentals of investing Your money. Our expertise. This guide is for information purposes only. It should not be seen as advice. Investments in the stock market may fall as well as

The Grasmeder Team at Morgan Stanley

The Grasmeder Team at Morgan Stanley 20 MAPLE ST GLENS FALLS, NY 12801 518-793-4181 / MAIN 800-526-1866 / TOLL-FREE 518-793-7046 / FAX www.morganstanleyfa.com/grasmeder Kathleen.R.Grasmeder@morganstanley.com

The Grasmeder Team at Morgan Stanley 20 MAPLE ST GLENS FALLS, NY 12801 518-793-4181 / MAIN 800-526-1866 / TOLL-FREE 518-793-7046 / FAX www.morganstanleyfa.com/grasmeder Kathleen.R.Grasmeder@morganstanley.com

All of your pension information in one trusted place

All of your pension information in one trusted place provides an alternative to the big insurance companies and pension providers who are building their own commercial dashboards, but who cannot provide

All of your pension information in one trusted place provides an alternative to the big insurance companies and pension providers who are building their own commercial dashboards, but who cannot provide

The five biggest DB pensions challenges today

Aon Hewitt Retirement and Investment The five biggest DB pensions challenges today and how to solve them Enter What are the biggest challenges facing UK Defined Benefit (DB) schemes today? The DB pensions

Aon Hewitt Retirement and Investment The five biggest DB pensions challenges today and how to solve them Enter What are the biggest challenges facing UK Defined Benefit (DB) schemes today? The DB pensions

Gift Aid and reliefs on donations

Report by the Comptroller and Auditor General HM Revenue & Customs Gift Aid and reliefs on donations HC 733 SESSION 2013-14 21 NOVEMBER 2013 4 Key facts Gift Aid and reliefs on donations Key facts 2bn

Report by the Comptroller and Auditor General HM Revenue & Customs Gift Aid and reliefs on donations HC 733 SESSION 2013-14 21 NOVEMBER 2013 4 Key facts Gift Aid and reliefs on donations Key facts 2bn

A church-eyed view of going concern

A church-eyed view of going concern February 2017 Stewardship Briefing Paper Stewardship, 1 Lamb s Passage, London EC1Y 8AB t: 020 8502 5600 e: enquiries@stewardship.org.uk w: stewardship.org.uk This Briefing

A church-eyed view of going concern February 2017 Stewardship Briefing Paper Stewardship, 1 Lamb s Passage, London EC1Y 8AB t: 020 8502 5600 e: enquiries@stewardship.org.uk w: stewardship.org.uk This Briefing

Foreign Direct Innovation?

Foreign Direct Innovation? The effect of FDI on innovation in the UK and what to do about it Introduction Foreign direct investment (FDI) occurs when overseas businesses invest in the UK, either by acquiring

Foreign Direct Innovation? The effect of FDI on innovation in the UK and what to do about it Introduction Foreign direct investment (FDI) occurs when overseas businesses invest in the UK, either by acquiring

Scottish Parliament Gender Pay Gap Report

2017 Scottish Parliament Gender Pay Gap Report Published in Scotland by the Scottish Parliamentary Corporate Body. For information on the Scottish Parliament contact Public Information on: Telephone: 0131

2017 Scottish Parliament Gender Pay Gap Report Published in Scotland by the Scottish Parliamentary Corporate Body. For information on the Scottish Parliament contact Public Information on: Telephone: 0131

I'm delighted to welcome you to the November edition of Regulation round-up. I'd like to take the opportunity to raise awareness of our guidance

November 2016 Banks & building societies // Investment managers & stockbrokers Financial advisers // Wealth managers & private banks Mortgage advisers // Insurers & insurance intermediaries Consumer credit

November 2016 Banks & building societies // Investment managers & stockbrokers Financial advisers // Wealth managers & private banks Mortgage advisers // Insurers & insurance intermediaries Consumer credit

Workplace Benefits Report:

RETIREMENT & BENEFIT PLAN SERVICES WORKPLACE INSIGHTS TM Workplace Benefits Report: Employers changing role in helping employees achieve financial wellness December 2013 Disclosures 2 Bank of America Merrill

RETIREMENT & BENEFIT PLAN SERVICES WORKPLACE INSIGHTS TM Workplace Benefits Report: Employers changing role in helping employees achieve financial wellness December 2013 Disclosures 2 Bank of America Merrill

Personal health budgets for mental health

Personal health budgets for mental health The webinar will start at 12.00 Please join by phone a few minutes before Dial 0800 917 1950 or 020 3463 9740 Then use the access code: 570 117 86 1 Personal health

Personal health budgets for mental health The webinar will start at 12.00 Please join by phone a few minutes before Dial 0800 917 1950 or 020 3463 9740 Then use the access code: 570 117 86 1 Personal health

A Discussion Document on Assurance of Social and Environmental Valuations

A Discussion Document on Assurance of Social and Environmental Valuations Social Value UK Winslow House, Rumford Court, Liverpool, L3 9DG +44 (0)151 703 9229 This document is not intended to be an assurance

A Discussion Document on Assurance of Social and Environmental Valuations Social Value UK Winslow House, Rumford Court, Liverpool, L3 9DG +44 (0)151 703 9229 This document is not intended to be an assurance

Communities Committee

Communities Committee Item No Report title: Voluntary & Community Sector Engagement Contract Date of meeting: 25 January 2017 Responsible Chief Tom McCabe Executive Director, Community Officer: and Environmental

Communities Committee Item No Report title: Voluntary & Community Sector Engagement Contract Date of meeting: 25 January 2017 Responsible Chief Tom McCabe Executive Director, Community Officer: and Environmental

The Demographics of Wealth

Demographics and the Future of American Families The Demographics of Wealth May 13, 2015 William R. Emmons Bryan J. Noeth Center for Household Financial Stability Federal Reserve Bank of St. Louis William.R.Emmons@stls.frb.org

Demographics and the Future of American Families The Demographics of Wealth May 13, 2015 William R. Emmons Bryan J. Noeth Center for Household Financial Stability Federal Reserve Bank of St. Louis William.R.Emmons@stls.frb.org

Pensions, Pensioner Poverty and the Pensions Commission Final Report

Briefing Pensions, Pensioner Poverty and the Pensions Commission Final Report Lord Turner's Pensions Commission Report has refashioned the landscape of the pensions debate. In this briefing Help the Aged

Briefing Pensions, Pensioner Poverty and the Pensions Commission Final Report Lord Turner's Pensions Commission Report has refashioned the landscape of the pensions debate. In this briefing Help the Aged

HMRC Tax-Free Childcare: Draft Guidance for comment Response from the Low Incomes Tax Reform Group (LITRG)

") HMRC Tax-Free Childcare: Draft Guidance for comment Response from the Low Incomes Tax Reform Group (LITRG) 1 General comments 1.1 We welcome this opportunity to comment on the Tax-Free Childcare (TFC)

HMRC Tax-Free Childcare: Draft Guidance for comment Response from the Low Incomes Tax Reform Group (LITRG) 1 General comments 1.1 We welcome this opportunity to comment on the Tax-Free Childcare (TFC)

Introduction / About the Money Advice Trust Introductory Comment Responses to individual questions

Page 2 Page 3 Page 4 Page 5 Contents Introduction / About the Money Advice Trust Introductory Comment Responses to individual questions The Money Advice Trust is a charity founded in 1991 to help people

Page 2 Page 3 Page 4 Page 5 Contents Introduction / About the Money Advice Trust Introductory Comment Responses to individual questions The Money Advice Trust is a charity founded in 1991 to help people

October Background

Response to the Welsh Assembly s Finance Committee inquiry into the Land Transaction Tax and Anti-avoidance of Devolved Taxes (Wales) Bill from National Association of Estate Agents (NAEA) Background October

Response to the Welsh Assembly s Finance Committee inquiry into the Land Transaction Tax and Anti-avoidance of Devolved Taxes (Wales) Bill from National Association of Estate Agents (NAEA) Background October

Regulating Defined Benefit pension schemes. Buck Consultants response to consultation by the Pensions Regulator

Regulating Defined Benefit pension schemes Buck Consultants response to consultation by the Pensions Regulator February 2014 2014 Xerox Corporation and Buck Consultants, LLC. All rights reserved. Xerox

Regulating Defined Benefit pension schemes Buck Consultants response to consultation by the Pensions Regulator February 2014 2014 Xerox Corporation and Buck Consultants, LLC. All rights reserved. Xerox

National Strategy for Financial Education: Thailand Experience

National Strategy for Financial Education: Thailand Experience 2014 IFIE-IOSCO Global Investor Education Conference Washington, D.C., USA Saovanee Suwannarong Director- Financial Literacy Department Securities

National Strategy for Financial Education: Thailand Experience 2014 IFIE-IOSCO Global Investor Education Conference Washington, D.C., USA Saovanee Suwannarong Director- Financial Literacy Department Securities