Cognitive Constraints on Valuing Annuities. Jeffrey R. Brown Arie Kapteyn Erzo F.P. Luttmer Olivia S. Mitchell

|

|

|

- Daniella Strickland

- 5 years ago

- Views:

Transcription

1 Cognitive Constraints on Valuing Annuities Jeffrey R. Brown Arie Kapteyn Erzo F.P. Luttmer Olivia S. Mitchell

2 Under a wide range of assumptions people should annuitize to guard against length-of-life uncertainty What are supply side barriers? Adverse selection Incomplete annuity markets (aggregate risk) What are demand-side limitations? Bequest motives Formal or informal substitutes (e.g. family) Pretty much any explanation creates new puzzles: E.g. if family provides risk sharing, annuity demand should go up after a spouse dies

3 Behavioral aspects Decisions are complicated and there is little opportunity for learning If one does not understand an annuity product, then reluctant to buy it Presumably financially more literate individuals will be better at valuing annuities (and may be more willing to buy them).

4 Data from American Life Panel At the time of our survey, the ALP included about 4,000 active panel members. Two waves (at least two weeks apart): 1 st wave 2478 observations (rr=83.9%) 2 nd wave 2355 observations (rr=95%) Calculated individual SS entitlements: 4% said not be eligible for SS; asked to assume benefits equal to their age/education/sex mean. Our full sample included 2,112 complete responses for both waves 1 and 2.

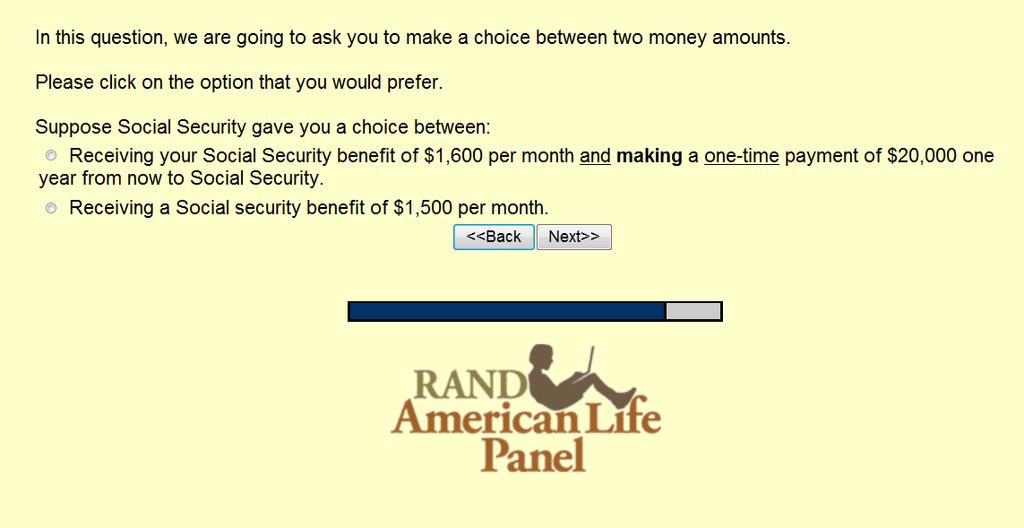

5 Our Experiment Use two waves of the American Life Panel and ask questions like the following (CV-SELL) In this question, we are going to ask you to make a choice between two money amounts. Please click on the option that you would prefer Suppose Social Security gave you a choice between: (1) Receiving your expected [current] Social Security benefit of $SSB per month. or (2) Receiving a Social Security benefit of $(SSB-X) per month and receiving a one-time payment of $LS at age Z [one year from now].

6 Screen shot: CV-Sell 6

7 Four versions of the annuity valuation tradeoff question Compensating Variation (CV) Equivalent Variation (EV) SELL -version BUY -version Choice A Choice B Choice A Choice B [SSB-X] + LS [SSB] [SSB+X] - LS [SSB] [SSB]+ LS [SSB+X] [SSB] - LS [SSB-X] X is typically $100 per month; this seems a fairly modest amount so one would expect the CV and EV versions to be fairly similar.

8 EV-Buy 8

9 Experimental variations Order of choices LS first or X first For CV SELL, vary X: $100, $500, SSB, X random from {200, 300, 400, 600, 700, SSB-100} Starting value of LS Actuarially fair 50% lower 50% higher A variant where we explicitly exclude political risk

10 CV-SELL (median is approximately act. fair) Fraction Below Median: $13,750 Lower Bound Upper Bound 0 $0 $20,000 $40,000 $60,000 $80,000 $100,000 Lump Sum Compensating for a $100/month Change in Social Security Benefits

11 CV-SELL (continued) 6% reports a valuation of $1500 or lower 12% wants $200,000 or more

12 CV-SELL and CV-BUY Fraction Below Median: $13,750 Median: $3,000 Valua on when Buying, Lower Bound Valua on when Buying, Upper Bound Valua on when Selling, Lower Bound Valua on when Selling, Upper Bound 0 $0 $20,000 $40,000 $60,000 $80,000 $100,000 Lump Sum Compensating for a $100/month Change in Social Security Benefits

13 CV-SELL and CV-BUY (continued) People place a much higher value on SS when asked to give up some of it than when asked their willingness to pay for some more This could be status quo bias/ endowment effect Liquidity constraints are an unlikely explanation (e.g. about 82 percent of respondents indicate that they could come up with the lowest lump-sum amount that they declined to pay. Of the 18 percent that indicated that they could not come up with this amount, half said that even if they had had the money, they would have declined to pay the lump sum)

14 EV-SELL and EV-BUY Fraction below Valua on when Buying, Lower Bound Valua on when Buying, Upper Bound Valua on when Selling, Lower Bound Median: $12,500 Valua on when Selling, Upper Bound Median: $3,000 $0 $20,000 $40,000 $60,000 $80,000 $100,000 Lump Sum Equivalent to a $100/month Change in Social Security Benefits

15 EV-SELL and EV-BUY (continued) A similar shift as with CV, but slightly less dramatic Note that with EV, endowment effects are less likely (since none of the alternatives includes the status quo)

16 Within Person Variation (correlations) Pairwise correlations CV-Sell (in logs) CV-Sell (in logs) 1 EV-Sell (in logs) CV-Buy (in logs) EV-Buy (in logs) EV-Sell (in logs) CV-Buy (in logs) EV-Buy (in logs) 0.31*** *** -0.17*** *** -0.15*** 0.72*** 1

17 Financial Literacy Index (1) Suppose you had $100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow: more than $102, exactly $102, or less than $102? {Do not know; refuse to answer}

18 Financial Literacy Index (2) Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year. After 1 year, would you be able to buy more than, exactly the same as, or less than today with the money in this account? More The same Less {Do not know; refuse to answer}

19 Financial Literacy Index (3) Do you think that the following statement is true or false? Buying a single company stock usually provides a safer return than a stock mutual fund. True False {Do not know; refuse to answer}

20 Six Number Scoring Tests Here is an example of a simple batch: Item Answer Correct: Correct: Correct: 13 Here is a more challenging one: Correct: Correct: Correct: 72, 76 or 78, 82 Based on six such batches and a scoring algorithm a respondent is assigned a score

21 EV Sell-Buy Spread EV Sell-Buy Spread by Financial Literacy Panel A or Financial Literacy (number of correct answers)

22 EV Sell-Buy Spread EV Sell-Buy Spread by Number Series Score Panel B Number Series Score (quintiles)

23 EV Sell-Buy Spread EV Sell-Buy Spread by Education Panel C HS dropout High school Some college Bachelor's degree Professional Degree Education

24 EV Sell-Buy Spread EV Sell-Buy Spread by Cognition Index Panel D Cognition Index (quintiles)

25 Explaining the Sell-Buy Spread Dependent Variable: Log CV-Sell - Log CV-Buy Explanatory Variables (1) (2) (3) (4) Age 35 to (0.13) (0.13) (0.13) (0.13) Age 50 to *** 0.34*** 0.42*** (0.12) (0.12) (0.12) (0.13) Age 65 and older 0.44*** 0.66*** 0.68*** 0.66*** (0.14) (0.14) (0.14) (0.16) Cognition index, standardized -0.59*** -0.42*** (0.04) (0.07) Financial literacy index, 0-3 scale -0.32*** (0.06) Education index, 1-5 scale -0.24*** (0.04) Number series score, standardized -0.31*** (0.05) Controls for demographics No No No Yes Controls for experimental v Yes Yes Yes Yes Adjusted R

26 Explanatory Variables Log of starting value More Randomizations Dependent Variable: log CV-Sell Entire sample Top quintile of cognition index Bottom quintile of cognition index Entire sample 0.37*** *** 0.39*** (0.07) (0.13) (0.21) (0.07) Asked after larger version Asked in wave *** 0.70*** 0.77*** 0.69*** (0.07) (0.12) (0.19) (0.07) ** 0.05 (0.07) (0.12) (0.19) (0.07) Lump-sum option shown last (0.07) (0.12) (0.19) (0.07) Log of starting value Cognition index Asked after larger version Cognition index Asked in wave 1 Cognition index Lump-sum option shown last Cognition index Cognition index -0.20** (0.08) (0.07) (0.07) 0.03 (0.07) -0.17*** (0.04) Adjusted R

27 Explanations Starting value: Starting value of size of lump sum Asked in wave 1: Whether questions were asked in first or second wave (the experiment was done over two waves) Lump sum option shown last If that would show an effect, it would indicate straight lining Asked after larger version: Order of increment sizes in CV_sell (Xs arranged in increasing order or Xs arranged in decreasing order)

28 Political risk? One version of the annuity valuation question states: From now on, please assume that you are absolutely certain that Social Security will make payments as promised, and that there is no chance at all of any benefit changes in the future other than the trade-offs discussed in the question below. We find that the response to the no-political-risk question is a statistically significant 7 percent lower than the response to the baseline CV-Sell question. Our question may have had the unintended effect of making political risk more salient, rather than less.

29 Explaining Annuity Valuations Dependent Variable: Mean of CV-Sell and CV-Buy (in logs) Explanatory Variables (1) (2) (3) (4) Log actuarial value 1.02*** 0.84*** (0.25) (0.26) Log theoretical utility-based annuity value (0.04) (0.13) (0.13) (0.13) (0.12) (0.13) R-squared Number of observations Columns (1) and (2): controls for age, sex, race, marital status, experimental variation; columns (3) and (4) additional controls for education, income, owns an annuity, home ownership, self-reported health, ever had kids, risk aversion, precaution, expects a return >3%.

2. Second quintile 0.76 0.686 1.246 0.0259 451 (0.59) 3. Third quintile 1.24** 0.618 1.163 0.0204 392 (0.49) 4. Fourth quintile 0.")

30 Predictive Power of Actuarial Value by Quintile of the Cognition Index Dependent Variable: Mean of log CV-Sell and log CV-Buy Coefficient on log actuarial value p-value on coefficient=1 Root MSE Adjusted R 2 1. Bottom quintile (0.77) 2. Second quintile (0.59) 3. Third quintile 1.24** (0.49) 4. Fourth quintile (0.50) 5. Fifth quintile 1.49*** (0.51) N 30

31 Correlation between Sell Valuations and Buy Valuations Correlations between buy and sell become more negative for lower values of the cognition index Panel B: Sell vs. Buy Cognition Index (quintiles)

32 Robustness

33 Compare results with and without 148 outliers We have repeated the analyses omitting 148 extreme values: Results change very little; In particular the negative correlation between buy and sell does not go away

34 Correlations for 50+ Pairwise correlations CV-Sell (in logs) EV-Sell (in logs) CV-Buy (in logs) EV-Buy (in logs) CV-Sell (in logs) 1 EV-Sell (in logs) CV-Buy (in logs) 0.29*** *** -0.17*** 1 EV-Buy (in logs) -0.11*** -0.17*** 0.72*** 1

35 Mean Sell-Buy Spread EV Sell-Buy Spread by Financial Literacy, 50+ Panel A or Financial Literacy (number of correct answers)

36 Mean Sell-Buy Spread EV Sell-Buy Spread by Number Series Score, 50+ Panel B Number Series Score (quintiles)

37 Mean Sell-Buy Spread EV Sell-Buy Spread by Education, 50+ Panel C HS dropout High school Some college Bachelor's degree Professional Degree Education

38 Mean Sell-Buy Spread EV Sell-Buy Spread by Cognition Index, 50+ Panel D Cognition Index (quintiles)

39 Logits indicating that respondent has at least one extreme value at the 80, 85, 90 and 95 th percentile

40 Extreme values are more likely for Older respondents Lower educated Minorities Women Non-home owners Respondents with lower incomes Respondents with lower wealth Lower financial literacy

41 How About Endowment Effects? A typical utility function would be: U(Y) = αy β(y-ref)1(y>ref) α>0 denotes the marginal utility of SS benefits below the reference level and 0<β<α denotes the decrease in marginal utility of Social Security that occurs at the reference point. 0<β<α<0 denotes the case where marginal utility falls discontinuously at the kind but remains positive.

42 Apply this to our setting Sell Version Buy Version Choice A Choice B Choice A Choice B CV [Ref-100]+13,000 [Ref] [Ref+100] 3,000 [Ref] EV [Ref]+13,000 [Ref+100] [Ref] 3,000 [Ref-100]

43 The Utility Function can Rationalize CV U(Y) = αy β(y-ref)1(y>ref), CV-Sell: U(Ref-100) + 13,000=U(Ref), or α(ref-100) = α Ref α = 130 CV-Buy: U(Ref+100) - 3,000=U(Ref), or α(ref+100)-100β = α Ref β = 100

44 But not EV α Ref = α(ref+100)-100β = 100(α-β) α Ref = α(ref-100) 3000 = 100α Hence: α = 30, β = -100 Recall, for CV we had α = 130, β = 100 Moreover, for EV marginal utility increases above the reference point: 30-(-100) =130

45 Discussion The task of valuing annuities is very challenging, even for individuals with high cognition and financial literacy. Nevertheless, there is a very robust and strong effect of cognitive measures on capability to value annuities at least somewhat coherently It appears that an unwillingness to trade is strongly related to inability to value the alternatives. This phenomenon may explain several anomalies in the literature

46 Center for Economic and Social Research Thank You

Are the American Future Elderly Prepared?

Are the American Future Elderly Prepared? Arie Kapteyn Center for Economic and Social Research, University of Southern California Based on joint work with Jeff Brown, Leandro Carvalho, Erzo Luttmer, Olivia

Are the American Future Elderly Prepared? Arie Kapteyn Center for Economic and Social Research, University of Southern California Based on joint work with Jeff Brown, Leandro Carvalho, Erzo Luttmer, Olivia

Online Appendices for: Cognitive Constraints on Valuing Annuities

Online Appendices for: Cognitive Constraints on Valuing Annuities Jeffrey R. Brown, Arie Kapteyn, Erzo F.P. Luttmer, and Olivia S. Mitchell Online Appendix Tables and Figures... page A-2 Online Appendix

Online Appendices for: Cognitive Constraints on Valuing Annuities Jeffrey R. Brown, Arie Kapteyn, Erzo F.P. Luttmer, and Olivia S. Mitchell Online Appendix Tables and Figures... page A-2 Online Appendix

Online Appendix for: Behavioral Impediments to Valuing Annuities: Evidence on the Effects of Complexity and Choice Bracketing

Online Appendix for: Behavioral Impediments to Valuing Annuities: Evidence on the Effects of Complexity and Choice Bracketing Jeffrey R. Brown, Arie Kapteyn, Erzo F.P. Luttmer, Olivia S. Mitchell, and

Online Appendix for: Behavioral Impediments to Valuing Annuities: Evidence on the Effects of Complexity and Choice Bracketing Jeffrey R. Brown, Arie Kapteyn, Erzo F.P. Luttmer, Olivia S. Mitchell, and

Complexity as a Barrier to Annuitization: Do Consumers Know How to Value Annuities?

Complexity as a Barrier to Annuitization: Do Consumers Know How to Value Annuities? Jeffrey R. Brown, Arie Kapteyn, Erzo F. P. Luttmer, and Olivia S. Mitchell March 2013 PRC WP2013-01 Pension Research

Complexity as a Barrier to Annuitization: Do Consumers Know How to Value Annuities? Jeffrey R. Brown, Arie Kapteyn, Erzo F. P. Luttmer, and Olivia S. Mitchell March 2013 PRC WP2013-01 Pension Research

The Role of Exponential-Growth Bias and Present Bias in Retirment Saving Decisions

The Role of Exponential-Growth Bias and Present Bias in Retirment Saving Decisions Gopi Shah Goda Stanford University & NBER Matthew Levy London School of Economics Colleen Flaherty Manchester University

The Role of Exponential-Growth Bias and Present Bias in Retirment Saving Decisions Gopi Shah Goda Stanford University & NBER Matthew Levy London School of Economics Colleen Flaherty Manchester University

Using Consequence Messaging to Improve Understanding of Social Security

Using Consequence Messaging to Improve Understanding of Social Security Anya Samek and Arie Kapteyn Center for Economic and Social Research University of Southern California 20 th Annual Joint Meeting

Using Consequence Messaging to Improve Understanding of Social Security Anya Samek and Arie Kapteyn Center for Economic and Social Research University of Southern California 20 th Annual Joint Meeting

Appendix A. Additional Results

Appendix A Additional Results for Intergenerational Transfers and the Prospects for Increasing Wealth Inequality Stephen L. Morgan Cornell University John C. Scott Cornell University Descriptive Results

Appendix A Additional Results for Intergenerational Transfers and the Prospects for Increasing Wealth Inequality Stephen L. Morgan Cornell University John C. Scott Cornell University Descriptive Results

The Lack of Persistence of Employee Contributions to Their 401(k) Plans May Lead to Insufficient Retirement Savings

Plans May Lead to Insufficient Retirement Savings") Upjohn Institute Policy Papers Upjohn Research home page 2011 The Lack of Persistence of Employee Contributions to Their 401(k) Plans May Lead to Insufficient Retirement Savings Leslie A. Muller Hope College

Upjohn Institute Policy Papers Upjohn Research home page 2011 The Lack of Persistence of Employee Contributions to Their 401(k) Plans May Lead to Insufficient Retirement Savings Leslie A. Muller Hope College

NBER WORKING PAPER SERIES COGNITIVE CONSTRAINTS ON VALUING ANNUITIES. Jeffrey R. Brown Arie Kapteyn Erzo F.P. Luttmer Olivia S.

NBER WORKING PAPER SERIES COGNITIVE CONSTRAINTS ON VALUING ANNUITIES Jeffrey R. Brown Arie Kapteyn Erzo F.P. Luttmer Olivia S. Mitchell Working Paper 19168 http://www.nber.org/papers/w19168 NATIONAL BUREAU

NBER WORKING PAPER SERIES COGNITIVE CONSTRAINTS ON VALUING ANNUITIES Jeffrey R. Brown Arie Kapteyn Erzo F.P. Luttmer Olivia S. Mitchell Working Paper 19168 http://www.nber.org/papers/w19168 NATIONAL BUREAU

The Role of the Annuity s Value on the Decision (Not) to Annuitize: Evidence from a Large Policy Change

to Annuitize: Evidence from a Large Policy Change") The Role of the Annuity s Value on the Decision (Not) to Annuitize: Evidence from a Large Policy Change Monika Bütler, Universität St. Gallen (joint with Stefan Staubli and Maria Grazia Zito) September

The Role of the Annuity s Value on the Decision (Not) to Annuitize: Evidence from a Large Policy Change Monika Bütler, Universität St. Gallen (joint with Stefan Staubli and Maria Grazia Zito) September

Cognitive Constraints on Valuing Annuities March 3, 2016

Cognitive Constraints on Valuing Annuities March 3, 2016 Jeffrey R. Brown Arie Kapteyn Department of Finance Center for Economic and Social Research University of Illinois University of Southern California

Cognitive Constraints on Valuing Annuities March 3, 2016 Jeffrey R. Brown Arie Kapteyn Department of Finance Center for Economic and Social Research University of Illinois University of Southern California

Evaluating Lump Sum Incentives for Delayed Social Security Claiming*

Evaluating Lump Sum Incentives for Delayed Social Security Claiming* Olivia S. Mitchell and Raimond Maurer October 2017 PRC WP2017 Pension Research Council Working Paper Pension Research Council The Wharton

Evaluating Lump Sum Incentives for Delayed Social Security Claiming* Olivia S. Mitchell and Raimond Maurer October 2017 PRC WP2017 Pension Research Council Working Paper Pension Research Council The Wharton

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners Stephanie Moulton, John Glenn College of Public Affairs, The Ohio State University Donald Haurin, Department

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners Stephanie Moulton, John Glenn College of Public Affairs, The Ohio State University Donald Haurin, Department

Inflation Expectations and Behavior: Do Survey Respondents Act on their Beliefs? October Wilbert van der Klaauw

Inflation Expectations and Behavior: Do Survey Respondents Act on their Beliefs? October 16 2014 Wilbert van der Klaauw The views presented here are those of the author and do not necessarily reflect those

Inflation Expectations and Behavior: Do Survey Respondents Act on their Beliefs? October 16 2014 Wilbert van der Klaauw The views presented here are those of the author and do not necessarily reflect those

Americans Willingness to Voluntarily Delay Retirement

Americans Willingness to Voluntarily Delay Retirement Raimond H. Maurer Olivia S. Mitchell The Wharton School MRRC Tatjana Schimetschek Ralph Rogalla Prepared for the 16 th Annual Joint Meeting of the

Americans Willingness to Voluntarily Delay Retirement Raimond H. Maurer Olivia S. Mitchell The Wharton School MRRC Tatjana Schimetschek Ralph Rogalla Prepared for the 16 th Annual Joint Meeting of the

Multiple Objective Asset Allocation for Retirees Using Simulation

Multiple Objective Asset Allocation for Retirees Using Simulation Kailan Shang and Lingyan Jiang The asset portfolios of retirees serve many purposes. Retirees may need them to provide stable cash flow

Multiple Objective Asset Allocation for Retirees Using Simulation Kailan Shang and Lingyan Jiang The asset portfolios of retirees serve many purposes. Retirees may need them to provide stable cash flow

Cognitive Constraints on Valuing Annuities

Cognitive Constraints on Valuing Annuities Jeffrey R. Brown, Arie Kapteyn, Erzo F. P. Luttmer, Olivia S. Mitchell March 2015 PRC WP2014-21 Pension Research Council The Wharton School, University of Pennsylvania

Cognitive Constraints on Valuing Annuities Jeffrey R. Brown, Arie Kapteyn, Erzo F. P. Luttmer, Olivia S. Mitchell March 2015 PRC WP2014-21 Pension Research Council The Wharton School, University of Pennsylvania

NBER WORKING PAPER SERIES THE DECISION TO DELAY SOCIAL SECURITY BENEFITS: THEORY AND EVIDENCE. John B. Shoven Sita Nataraj Slavov

NBER WORKING PAPER SERIES THE DECISION TO DELAY SOCIAL SECURITY BENEFITS: THEORY AND EVIDENCE John B. Shoven Sita Nataraj Slavov Working Paper 17866 http://www.nber.org/papers/w17866 NATIONAL BUREAU OF

NBER WORKING PAPER SERIES THE DECISION TO DELAY SOCIAL SECURITY BENEFITS: THEORY AND EVIDENCE John B. Shoven Sita Nataraj Slavov Working Paper 17866 http://www.nber.org/papers/w17866 NATIONAL BUREAU OF

Future Beneficiary Expectations of the Returns to Delayed Social Security Benefit Claiming and Choice Behavior

Future Beneficiary Expectations of the Returns to Delayed Social Security Benefit Claiming and Choice Behavior Jeff Dominitz Angela Hung Arthur van Soest RAND Preliminary and Incomplete Draft Updated for

Future Beneficiary Expectations of the Returns to Delayed Social Security Benefit Claiming and Choice Behavior Jeff Dominitz Angela Hung Arthur van Soest RAND Preliminary and Incomplete Draft Updated for

How Much Should Americans Be Saving for Retirement?

How Much Should Americans Be Saving for Retirement? by B. Douglas Bernheim Stanford University The National Bureau of Economic Research Lorenzo Forni The Bank of Italy Jagadeesh Gokhale The Federal Reserve

How Much Should Americans Be Saving for Retirement? by B. Douglas Bernheim Stanford University The National Bureau of Economic Research Lorenzo Forni The Bank of Italy Jagadeesh Gokhale The Federal Reserve

Demographic Change, Retirement Saving, and Financial Market Returns

Preliminary and Partial Draft Please Do Not Quote Demographic Change, Retirement Saving, and Financial Market Returns James Poterba MIT and NBER and Steven Venti Dartmouth College and NBER and David A.

Preliminary and Partial Draft Please Do Not Quote Demographic Change, Retirement Saving, and Financial Market Returns James Poterba MIT and NBER and Steven Venti Dartmouth College and NBER and David A.

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: February 2012 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: February 2012 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

Jamie Wagner Ph.D. Student University of Nebraska Lincoln

An Empirical Analysis Linking a Person s Financial Risk Tolerance and Financial Literacy to Financial Behaviors Jamie Wagner Ph.D. Student University of Nebraska Lincoln Abstract Financial risk aversion

An Empirical Analysis Linking a Person s Financial Risk Tolerance and Financial Literacy to Financial Behaviors Jamie Wagner Ph.D. Student University of Nebraska Lincoln Abstract Financial risk aversion

Labor Economics Field Exam Spring 2011

Labor Economics Field Exam Spring 2011 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

Labor Economics Field Exam Spring 2011 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

The Impact of Credit Counseling on Consumer Outcomes: Evidence from a National Demonstration Program

The Impact of Credit Counseling on Consumer Outcomes: Evidence from a National Demonstration Program Stephen Roll Stephanie Moulton, PhD Credit Counseling Overview Reaches two million clients a year Provides

The Impact of Credit Counseling on Consumer Outcomes: Evidence from a National Demonstration Program Stephen Roll Stephanie Moulton, PhD Credit Counseling Overview Reaches two million clients a year Provides

Retirement Savings and Household Wealth in 2007

Retirement Savings and Household Wealth in 2007 Patrick Purcell Specialist in Income Security April 8, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of

Retirement Savings and Household Wealth in 2007 Patrick Purcell Specialist in Income Security April 8, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of

Wealth, money, knowledge: how much do people know? Where are the gaps? What s working? What s next?

Wealth, money, knowledge: how much do people know? Where are the gaps? What s working? What s next? Presentation to Financial Literacy 09 Retirement Commission, New Zealand June 26, 2009 Annamaria Lusardi

Wealth, money, knowledge: how much do people know? Where are the gaps? What s working? What s next? Presentation to Financial Literacy 09 Retirement Commission, New Zealand June 26, 2009 Annamaria Lusardi

Nordic Journal of Political Economy

Nordic Journal of Political Economy Volume 39 204 Article 3 The welfare effects of the Finnish survivors pension scheme Niku Määttänen * * Niku Määttänen, The Research Institute of the Finnish Economy

Nordic Journal of Political Economy Volume 39 204 Article 3 The welfare effects of the Finnish survivors pension scheme Niku Määttänen * * Niku Määttänen, The Research Institute of the Finnish Economy

Internet Appendix. The survey data relies on a sample of Italian clients of a large Italian bank. The survey,

Internet Appendix A1. The 2007 survey The survey data relies on a sample of Italian clients of a large Italian bank. The survey, conducted between June and September 2007, provides detailed financial and

Internet Appendix A1. The 2007 survey The survey data relies on a sample of Italian clients of a large Italian bank. The survey, conducted between June and September 2007, provides detailed financial and

Data Appendix. A.1. The 2007 survey

Data Appendix A.1. The 2007 survey The survey data used draw on a sample of Italian clients of a large Italian bank. The survey was conducted between June and September 2007 and elicited detailed financial

Data Appendix A.1. The 2007 survey The survey data used draw on a sample of Italian clients of a large Italian bank. The survey was conducted between June and September 2007 and elicited detailed financial

institutional setting in annuity valuation

Beyond framing: the role of information, the endowment effect and institutional setting in annuity valuation Hazel Bateman, Ralph Stevens, Jennifer Alonso Garcia, Eduard Ponds February, 2018 ABSTRACT In

Beyond framing: the role of information, the endowment effect and institutional setting in annuity valuation Hazel Bateman, Ralph Stevens, Jennifer Alonso Garcia, Eduard Ponds February, 2018 ABSTRACT In

The Causal Effects of Economic Incentives, Health and Job Characteristics on Retirement: Estimates Based on Subjective Conditional Probabilities*

The Causal Effects of Economic Incentives, Health and Job Characteristics on Retirement: Estimates Based on Subjective Conditional Probabilities* Péter Hudomiet, Michael D. Hurd, and Susann Rohwedder October,

The Causal Effects of Economic Incentives, Health and Job Characteristics on Retirement: Estimates Based on Subjective Conditional Probabilities* Péter Hudomiet, Michael D. Hurd, and Susann Rohwedder October,

NCSS Statistical Software. Reference Intervals

Chapter 586 Introduction A reference interval contains the middle 95% of measurements of a substance from a healthy population. It is a type of prediction interval. This procedure calculates one-, and

Chapter 586 Introduction A reference interval contains the middle 95% of measurements of a substance from a healthy population. It is a type of prediction interval. This procedure calculates one-, and

Have the Australians got it right? Converting Retirement Savings to Retirement Benefits: Lessons from Australia

Have the s got it right? Converting Retirement Savings to Retirement Benefits: Lessons from Australia Hazel Bateman Director, Centre for Pensions and Superannuation Risk and Actuarial Studies The University

Have the s got it right? Converting Retirement Savings to Retirement Benefits: Lessons from Australia Hazel Bateman Director, Centre for Pensions and Superannuation Risk and Actuarial Studies The University

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: March 2011 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: March 2011 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking?

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

Investment Decisions and Negative Interest Rates

Investment Decisions and Negative Interest Rates No. 16-23 Anat Bracha Abstract: While the current European Central Bank deposit rate and 2-year German government bond yields are negative, the U.S. 2-year

Investment Decisions and Negative Interest Rates No. 16-23 Anat Bracha Abstract: While the current European Central Bank deposit rate and 2-year German government bond yields are negative, the U.S. 2-year

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: February 2013 By Sarah Riley Qing Feng Mark Lindblad Roberto Quercia Center for Community Capital

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: February 2013 By Sarah Riley Qing Feng Mark Lindblad Roberto Quercia Center for Community Capital

Behavioral Impediments to Valuing Annuities: Evidence on the Effects of Complexity and Choice Bracketing

Behavioral Impediments to Valuing Annuities: Evidence on the Effects of Complexity and Choice Bracketing Jeffrey R. Brown, Arie Kapteyn, Erzo F.P. Luttmer, Olivia S. Mitchell, and Anya Samek November 30,

Behavioral Impediments to Valuing Annuities: Evidence on the Effects of Complexity and Choice Bracketing Jeffrey R. Brown, Arie Kapteyn, Erzo F.P. Luttmer, Olivia S. Mitchell, and Anya Samek November 30,

5 Steps To Planning Success :

5 Steps To Planning Success : Developing and Testing New Strategies for Reaching Young Adults Aileen Heinberg Angela Hung Arie Kapteyn Annamaria Lusardi Joanne K. Yoong With DC Plans, Starting Early Can

5 Steps To Planning Success : Developing and Testing New Strategies for Reaching Young Adults Aileen Heinberg Angela Hung Arie Kapteyn Annamaria Lusardi Joanne K. Yoong With DC Plans, Starting Early Can

Redistribution Effects of Electricity Pricing in Korea

Redistribution Effects of Electricity Pricing in Korea Jung S. You and Soyoung Lim Rice University, Houston, TX, U.S.A. E-mail: jsyou10@gmail.com Revised: January 31, 2013 Abstract Domestic electricity

Redistribution Effects of Electricity Pricing in Korea Jung S. You and Soyoung Lim Rice University, Houston, TX, U.S.A. E-mail: jsyou10@gmail.com Revised: January 31, 2013 Abstract Domestic electricity

Late-in-Life Risks and the Under-Insurance Puzzle

Late-in-Life Risks and the Under-Insurance Puzzle John Ameriks Joseph Briggs Andrew Caplin Vanguard NYU NYU Matthew D. Shapiro Michigan Christopher Tonetti Stanford GSB 1 / 50 Long Term Care Expenditure

Late-in-Life Risks and the Under-Insurance Puzzle John Ameriks Joseph Briggs Andrew Caplin Vanguard NYU NYU Matthew D. Shapiro Michigan Christopher Tonetti Stanford GSB 1 / 50 Long Term Care Expenditure

Financial Literacy and Retirement Planning in Germany. Tabea Bucher-Koenen and Annamaria Lusardi

Financial Literacy and Retirement Planning in Germany Tabea Bucher-Koenen and Annamaria Lusardi FLat World Project Turin, 20.12.2010 1. Introduction: Increasing relevance of financial literacy Until 2001

Financial Literacy and Retirement Planning in Germany Tabea Bucher-Koenen and Annamaria Lusardi FLat World Project Turin, 20.12.2010 1. Introduction: Increasing relevance of financial literacy Until 2001

Internet Appendix to: Common Ownership, Competition, and Top Management Incentives

Internet Appendix to: Common Ownership, Competition, and Top Management Incentives Miguel Antón, Florian Ederer, Mireia Giné, and Martin Schmalz August 13, 2016 Abstract This internet appendix provides

Internet Appendix to: Common Ownership, Competition, and Top Management Incentives Miguel Antón, Florian Ederer, Mireia Giné, and Martin Schmalz August 13, 2016 Abstract This internet appendix provides

Labor Supply Responses to the Social Security Tax-Benefit Link *

Preliminary and incomplete Labor Supply Responses to the Social Security Tax-Benefit Link * Jeffrey B. Liebman Erzo F.P. Luttmer David G. Seif July 11, 2008 Abstract A key question for Social Security

Preliminary and incomplete Labor Supply Responses to the Social Security Tax-Benefit Link * Jeffrey B. Liebman Erzo F.P. Luttmer David G. Seif July 11, 2008 Abstract A key question for Social Security

ARC Centre of Excellence in Population Ageing Research. Working Paper 2018/17

ARC Centre of Excellence in Population Ageing Research Working Paper 2018/17 Learning to Value Annuities: The Role of Information and Engagement Hazel Bateman, Ralph Stevens, Jennifer Alonso Garcia and

ARC Centre of Excellence in Population Ageing Research Working Paper 2018/17 Learning to Value Annuities: The Role of Information and Engagement Hazel Bateman, Ralph Stevens, Jennifer Alonso Garcia and

Family Status Transitions, Latent Health, and the Post- Retirement Evolution of Assets

Family Status Transitions, Latent Health, and the Post- Retirement Evolution of Assets by James Poterba MIT and NBER Steven Venti Dartmouth College and NBER David A. Wise Harvard University and NBER May

Family Status Transitions, Latent Health, and the Post- Retirement Evolution of Assets by James Poterba MIT and NBER Steven Venti Dartmouth College and NBER David A. Wise Harvard University and NBER May

An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar.

Chapter 7 An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar. The relationship between risk and return is a tradeoff.

Chapter 7 An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar. The relationship between risk and return is a tradeoff.

Do Older Americans Have More Income Than We Think?

Do Older Americans Have More Income Than We Think? Adam Bee and Josh Mitchell U.S. Census Bureau Presented at National Tax Association Meetings Philadelphia November 9, 2017 The views expressed in this

Do Older Americans Have More Income Than We Think? Adam Bee and Josh Mitchell U.S. Census Bureau Presented at National Tax Association Meetings Philadelphia November 9, 2017 The views expressed in this

Is Retiree Demand for Life Annuities Rational? Evidence from Public Employees *

Is Retiree Demand for Life Annuities Rational? Evidence from Public Employees * John Chalmers and Jonathan Reuter Current Draft: December 2009 Abstract Oregon Public Employees Retirement System (PERS)

Is Retiree Demand for Life Annuities Rational? Evidence from Public Employees * John Chalmers and Jonathan Reuter Current Draft: December 2009 Abstract Oregon Public Employees Retirement System (PERS)

Prices or Knowledge? What drives demand for financial services in emerging markets?

Prices or Knowledge? What drives demand for financial services in emerging markets? Shawn Cole (Harvard), Thomas Sampson (Harvard), and Bilal Zia (World Bank) CeRP September 2009 Motivation Access to financial

Prices or Knowledge? What drives demand for financial services in emerging markets? Shawn Cole (Harvard), Thomas Sampson (Harvard), and Bilal Zia (World Bank) CeRP September 2009 Motivation Access to financial

Financial Literacy and Financial Behavior among Young Adults: Evidence and Implications

Numeracy Advancing Education in Quantitative Literacy Volume 6 Issue 2 Article 5 7-1-2013 Financial Literacy and Financial Behavior among Young Adults: Evidence and Implications Carlo de Bassa Scheresberg

Numeracy Advancing Education in Quantitative Literacy Volume 6 Issue 2 Article 5 7-1-2013 Financial Literacy and Financial Behavior among Young Adults: Evidence and Implications Carlo de Bassa Scheresberg

The Impact of Hypothetical Wealth Shocks on Retirement Timing

The Impact of Hypothetical Wealth Shocks on Retirement Timing NOVEMBER 11, 2017 1 Brooke Helppie-McFall University of Michigan Joanne W. Hsu Federal Reserve Board of Governors Matthew D. Shapiro University

The Impact of Hypothetical Wealth Shocks on Retirement Timing NOVEMBER 11, 2017 1 Brooke Helppie-McFall University of Michigan Joanne W. Hsu Federal Reserve Board of Governors Matthew D. Shapiro University

Chapter 3. Numerical Descriptive Measures. Copyright 2016 Pearson Education, Ltd. Chapter 3, Slide 1

Chapter 3 Numerical Descriptive Measures Copyright 2016 Pearson Education, Ltd. Chapter 3, Slide 1 Objectives In this chapter, you learn to: Describe the properties of central tendency, variation, and

Chapter 3 Numerical Descriptive Measures Copyright 2016 Pearson Education, Ltd. Chapter 3, Slide 1 Objectives In this chapter, you learn to: Describe the properties of central tendency, variation, and

a partial solution to the annuity puzzle

59 Disengagement: a partial solution to the annuity puzzle Hazel Bateman Director, Risk and Actuarial Studies, University of New South Wales, Sydney Christine Eckhert Marketing and CenSoC, University of

59 Disengagement: a partial solution to the annuity puzzle Hazel Bateman Director, Risk and Actuarial Studies, University of New South Wales, Sydney Christine Eckhert Marketing and CenSoC, University of

Financial Literacy and Subjective Expectations Questions: A Validation Exercise

Financial Literacy and Subjective Expectations Questions: A Validation Exercise Monica Paiella University of Naples Parthenope Dept. of Business and Economic Studies (Room 314) Via General Parisi 13, 80133

Financial Literacy and Subjective Expectations Questions: A Validation Exercise Monica Paiella University of Naples Parthenope Dept. of Business and Economic Studies (Room 314) Via General Parisi 13, 80133

In Debt and Approaching Retirement: Claim Social Security or Work Longer?

AEA Papers and Proceedings 2018, 108: 401 406 https://doi.org/10.1257/pandp.20181116 In Debt and Approaching Retirement: Claim Social Security or Work Longer? By Barbara A. Butrica and Nadia S. Karamcheva*

AEA Papers and Proceedings 2018, 108: 401 406 https://doi.org/10.1257/pandp.20181116 In Debt and Approaching Retirement: Claim Social Security or Work Longer? By Barbara A. Butrica and Nadia S. Karamcheva*

CHAPTER 4 ESTIMATES OF RETIREMENT, SOCIAL SECURITY BENEFIT TAKE-UP, AND EARNINGS AFTER AGE 50

CHAPTER 4 ESTIMATES OF RETIREMENT, SOCIAL SECURITY BENEFIT TAKE-UP, AND EARNINGS AFTER AGE 5 I. INTRODUCTION This chapter describes the models that MINT uses to simulate earnings from age 5 to death, retirement

CHAPTER 4 ESTIMATES OF RETIREMENT, SOCIAL SECURITY BENEFIT TAKE-UP, AND EARNINGS AFTER AGE 5 I. INTRODUCTION This chapter describes the models that MINT uses to simulate earnings from age 5 to death, retirement

The Rise of 401(k) Plans, Lifetime Earnings, and Wealth at Retirement

Plans, Lifetime Earnings, and Wealth at Retirement") The Rise of 401(k) Plans, Lifetime Earnings, and Wealth at Retirement By James Poterba MIT and NBER Steven Venti Dartmouth College and NBER David A. Wise Harvard University and NBER April 2007 Abstract:

The Rise of 401(k) Plans, Lifetime Earnings, and Wealth at Retirement By James Poterba MIT and NBER Steven Venti Dartmouth College and NBER David A. Wise Harvard University and NBER April 2007 Abstract:

Issue Number 51 July A publication of External Affairs Corporate Research

Research Dialogues Issue Number 51 July 1997 A publication of External Affairs Corporate Research Premium Allocations and Accumulations in TIAA-CREF Trends in Participant Choices among Asset Classes and

Research Dialogues Issue Number 51 July 1997 A publication of External Affairs Corporate Research Premium Allocations and Accumulations in TIAA-CREF Trends in Participant Choices among Asset Classes and

Labor Economics Field Exam Spring 2014

Labor Economics Field Exam Spring 2014 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

Labor Economics Field Exam Spring 2014 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

No THE MIRACLE OF COMPOUND INTEREST: DOES OUR INTUITION FAIL? By Johannes Binswanger, Katherine Grace Carman. December 2010 ISSN

No. 2010-137 THE MIRACLE OF COMPOUND INTEREST: DOES OUR INTUITION FAIL? By Johannes Binswanger, Katherine Grace Carman December 2010 ISSN 0924-7815 The Miracle of Compound Interest: Does our Intuition

No. 2010-137 THE MIRACLE OF COMPOUND INTEREST: DOES OUR INTUITION FAIL? By Johannes Binswanger, Katherine Grace Carman December 2010 ISSN 0924-7815 The Miracle of Compound Interest: Does our Intuition

Changes over Time in Subjective Retirement Probabilities

Marjorie Honig Changes over Time in Subjective Retirement Probabilities No. 96-036 HRS/AHEAD Working Paper Series July 1996 The Health and Retirement Study (HRS) and the Study of Asset and Health Dynamics

Marjorie Honig Changes over Time in Subjective Retirement Probabilities No. 96-036 HRS/AHEAD Working Paper Series July 1996 The Health and Retirement Study (HRS) and the Study of Asset and Health Dynamics

CRS Report for Congress

Order Code RL33116 CRS Report for Congress Received through the CRS Web Retirement Plan Participation and Contributions: Trends from 1998 to 2003 October 12, 2005 Patrick Purcell Specialist in Social Legislation

Order Code RL33116 CRS Report for Congress Received through the CRS Web Retirement Plan Participation and Contributions: Trends from 1998 to 2003 October 12, 2005 Patrick Purcell Specialist in Social Legislation

NBER WORKING PAPER SERIES THE GROWTH IN SOCIAL SECURITY BENEFITS AMONG THE RETIREMENT AGE POPULATION FROM INCREASES IN THE CAP ON COVERED EARNINGS

NBER WORKING PAPER SERIES THE GROWTH IN SOCIAL SECURITY BENEFITS AMONG THE RETIREMENT AGE POPULATION FROM INCREASES IN THE CAP ON COVERED EARNINGS Alan L. Gustman Thomas Steinmeier Nahid Tabatabai Working

NBER WORKING PAPER SERIES THE GROWTH IN SOCIAL SECURITY BENEFITS AMONG THE RETIREMENT AGE POPULATION FROM INCREASES IN THE CAP ON COVERED EARNINGS Alan L. Gustman Thomas Steinmeier Nahid Tabatabai Working

APPENDIX FOR FIVE FACTS ABOUT BELIEFS AND PORTFOLIOS

APPENDIX FOR FIVE FACTS ABOUT BELIEFS AND PORTFOLIOS Stefano Giglio Matteo Maggiori Johannes Stroebel Steve Utkus A.1 RESPONSE RATES We next provide more details on the response rates to the GMS-Vanguard

APPENDIX FOR FIVE FACTS ABOUT BELIEFS AND PORTFOLIOS Stefano Giglio Matteo Maggiori Johannes Stroebel Steve Utkus A.1 RESPONSE RATES We next provide more details on the response rates to the GMS-Vanguard

IMPACT OF THE SOCIAL SECURITY RETIREMENT EARNINGS TEST ON YEAR-OLDS

#2003-15 December 2003 IMPACT OF THE SOCIAL SECURITY RETIREMENT EARNINGS TEST ON 62-64-YEAR-OLDS Caroline Ratcliffe Jillian Berk Kevin Perese Eric Toder Alison M. Shelton Project Manager The Public Policy

#2003-15 December 2003 IMPACT OF THE SOCIAL SECURITY RETIREMENT EARNINGS TEST ON 62-64-YEAR-OLDS Caroline Ratcliffe Jillian Berk Kevin Perese Eric Toder Alison M. Shelton Project Manager The Public Policy

Tests for the Difference Between Two Linear Regression Intercepts

Chapter 853 Tests for the Difference Between Two Linear Regression Intercepts Introduction Linear regression is a commonly used procedure in statistical analysis. One of the main objectives in linear regression

Chapter 853 Tests for the Difference Between Two Linear Regression Intercepts Introduction Linear regression is a commonly used procedure in statistical analysis. One of the main objectives in linear regression

On the provision of incentives in finance experiments. Web Appendix

On the provision of incentives in finance experiments. Daniel Kleinlercher Thomas Stöckl May 29, 2017 Contents Web Appendix 1 Calculation of price efficiency measures 2 2 Additional information for PRICE

On the provision of incentives in finance experiments. Daniel Kleinlercher Thomas Stöckl May 29, 2017 Contents Web Appendix 1 Calculation of price efficiency measures 2 2 Additional information for PRICE

Genetic Ability, Wealth and Financial Decision-Making

Genetic Ability, Wealth and Financial Decision-Making Danny Barth Affiliated Faculty, CESR Kevin Thom New York University Nicholas W. Papageorge Johns Hopkins University Econometric Society Summer Meeting

Genetic Ability, Wealth and Financial Decision-Making Danny Barth Affiliated Faculty, CESR Kevin Thom New York University Nicholas W. Papageorge Johns Hopkins University Econometric Society Summer Meeting

Explaining Consumption Excess Sensitivity with Near-Rationality:

Explaining Consumption Excess Sensitivity with Near-Rationality: Evidence from Large Predetermined Payments Lorenz Kueng Northwestern University and NBER Motivation: understanding consumption is important

Explaining Consumption Excess Sensitivity with Near-Rationality: Evidence from Large Predetermined Payments Lorenz Kueng Northwestern University and NBER Motivation: understanding consumption is important

Labor Supply Responses to Marginal Social Security Benefits: Evidence from Discontinuities *

Labor Supply Responses to Marginal Social Security Benefits: Evidence from Discontinuities * Jeffrey B. Liebman Erzo F.P. Luttmer David G. Seif December 9, 2008 Abstract A key question for Social Security

Labor Supply Responses to Marginal Social Security Benefits: Evidence from Discontinuities * Jeffrey B. Liebman Erzo F.P. Luttmer David G. Seif December 9, 2008 Abstract A key question for Social Security

The Time Cost of Documents to Trade

The Time Cost of Documents to Trade Mohammad Amin* May, 2011 The paper shows that the number of documents required to export and import tend to increase the time cost of shipments. However, this relationship

The Time Cost of Documents to Trade Mohammad Amin* May, 2011 The paper shows that the number of documents required to export and import tend to increase the time cost of shipments. However, this relationship

Labor Supply Responses to the Social Security Tax-Benefit Link *

Labor Supply Responses to the Social Security Tax-Benefit Link * Jeffrey B. Liebman Erzo F.P. Luttmer David G. Seif December 22, 2006 Abstract A key question for Social Security reform is whether workers

Labor Supply Responses to the Social Security Tax-Benefit Link * Jeffrey B. Liebman Erzo F.P. Luttmer David G. Seif December 22, 2006 Abstract A key question for Social Security reform is whether workers

All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the

and not those of the Wharton School or the") All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the Pension Research Council. 2010 Pension Research Council

All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the Pension Research Council. 2010 Pension Research Council

Premium Timing with Valuation Ratios

RESEARCH Premium Timing with Valuation Ratios March 2016 Wei Dai, PhD Research The predictability of expected stock returns is an old topic and an important one. While investors may increase expected returns

RESEARCH Premium Timing with Valuation Ratios March 2016 Wei Dai, PhD Research The predictability of expected stock returns is an old topic and an important one. While investors may increase expected returns

Financial Economics Field Exam August 2011

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

While real incomes in the lower and middle portions of the U.S. income distribution have

CONSUMPTION CONTAGION: DOES THE CONSUMPTION OF THE RICH DRIVE THE CONSUMPTION OF THE LESS RICH? BY MARIANNE BERTRAND AND ADAIR MORSE (CHICAGO BOOTH) Overview While real incomes in the lower and middle

CONSUMPTION CONTAGION: DOES THE CONSUMPTION OF THE RICH DRIVE THE CONSUMPTION OF THE LESS RICH? BY MARIANNE BERTRAND AND ADAIR MORSE (CHICAGO BOOTH) Overview While real incomes in the lower and middle

Acemoglu, et al (2008) cast doubt on the robustness of the cross-country empirical relationship between income and democracy. They demonstrate that

cast doubt on the robustness of the cross-country empirical relationship between income and democracy. They demonstrate that") Acemoglu, et al (2008) cast doubt on the robustness of the cross-country empirical relationship between income and democracy. They demonstrate that the strong positive correlation between income and democracy

Acemoglu, et al (2008) cast doubt on the robustness of the cross-country empirical relationship between income and democracy. They demonstrate that the strong positive correlation between income and democracy

Do Older Americans Have More Income Than We Think?

Do Older Americans Have More Income Than We Think? Josh Mitchell and Adam Bee U.S. Census Bureau December 14, 2017 The views expressed in this research, including those related to statistical, methodological,

Do Older Americans Have More Income Than We Think? Josh Mitchell and Adam Bee U.S. Census Bureau December 14, 2017 The views expressed in this research, including those related to statistical, methodological,

Distribution of Household Wealth in the U.S.: 2000 to 2011

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 2014 Distribution of Household Wealth in the U.S.: Marina Vornovitsky U.S. Census Bureau Alfred Gottschalck

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 2014 Distribution of Household Wealth in the U.S.: Marina Vornovitsky U.S. Census Bureau Alfred Gottschalck

A Tough Act to Follow: Contrast Effects in Financial Markets. Samuel Hartzmark University of Chicago. May 20, 2016

A Tough Act to Follow: Contrast Effects in Financial Markets Samuel Hartzmark University of Chicago May 20, 2016 Contrast eects Contrast eects: Value of previously-observed signal inversely biases perception

A Tough Act to Follow: Contrast Effects in Financial Markets Samuel Hartzmark University of Chicago May 20, 2016 Contrast eects Contrast eects: Value of previously-observed signal inversely biases perception

Accounting for Patterns of Wealth Inequality

. 1 Accounting for Patterns of Wealth Inequality Lutz Hendricks Iowa State University, CESifo, CFS March 28, 2004. 1 Introduction 2 Wealth is highly concentrated in U.S. data: The richest 1% of households

. 1 Accounting for Patterns of Wealth Inequality Lutz Hendricks Iowa State University, CESifo, CFS March 28, 2004. 1 Introduction 2 Wealth is highly concentrated in U.S. data: The richest 1% of households

Executive Summary: Aging in Place: Analyzing the Use of Reverse Mortgages to Preserve Independent Living. Highlights Report of Survey Results

Executive Summary: Aging in Place: Analyzing the Use of Reverse Mortgages to Preserve Independent Living Highlights Report of Survey Results January 21, 2016 Research Study Team Stephanie Moulton,* Donald

Executive Summary: Aging in Place: Analyzing the Use of Reverse Mortgages to Preserve Independent Living Highlights Report of Survey Results January 21, 2016 Research Study Team Stephanie Moulton,* Donald

Long-run Effects of Lottery Wealth on Psychological Well-being. Online Appendix

Long-run Effects of Lottery Wealth on Psychological Well-being Online Appendix May 2018 Erik Lindqvist Robert Östling David Cesarini 1 Introduction The Analysis Plan described our intention to compare

Long-run Effects of Lottery Wealth on Psychological Well-being Online Appendix May 2018 Erik Lindqvist Robert Östling David Cesarini 1 Introduction The Analysis Plan described our intention to compare

The text reports the results of two experiments examining the influence of two war tax

Supporting Information for Kriner et al. CMPS 2015 Page 1 The text reports the results of two experiments examining the influence of two war tax instruments on public support for war. The complete wording

Supporting Information for Kriner et al. CMPS 2015 Page 1 The text reports the results of two experiments examining the influence of two war tax instruments on public support for war. The complete wording

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND Magnus Dahlquist 1 Ofer Setty 2 Roine Vestman 3 1 Stockholm School of Economics and CEPR 2 Tel Aviv University 3 Stockholm University and Swedish House

ON THE ASSET ALLOCATION OF A DEFAULT PENSION FUND Magnus Dahlquist 1 Ofer Setty 2 Roine Vestman 3 1 Stockholm School of Economics and CEPR 2 Tel Aviv University 3 Stockholm University and Swedish House

Economics 345 Applied Econometrics

Economics 345 Applied Econometrics Problem Set 4--Solutions Prof: Martin Farnham Problem sets in this course are ungraded. An answer key will be posted on the course website within a few days of the release

Economics 345 Applied Econometrics Problem Set 4--Solutions Prof: Martin Farnham Problem sets in this course are ungraded. An answer key will be posted on the course website within a few days of the release

Retirement Saving, Annuity Markets, and Lifecycle Modeling. James Poterba 10 July 2008

Retirement Saving, Annuity Markets, and Lifecycle Modeling James Poterba 10 July 2008 Outline Shifting Composition of Retirement Saving: Rise of Defined Contribution Plans Mortality Risks in Retirement

Retirement Saving, Annuity Markets, and Lifecycle Modeling James Poterba 10 July 2008 Outline Shifting Composition of Retirement Saving: Rise of Defined Contribution Plans Mortality Risks in Retirement

AN ANNUITY THAT PEOPLE MIGHT ACTUALLY BUY

July 2007, Number 7-10 AN ANNUITY THAT PEOPLE MIGHT ACTUALLY BUY By Anthony Webb, Guan Gong, and Wei Sun* Introduction Immediate annuities provide insurance against outliving one s wealth. Previous research

July 2007, Number 7-10 AN ANNUITY THAT PEOPLE MIGHT ACTUALLY BUY By Anthony Webb, Guan Gong, and Wei Sun* Introduction Immediate annuities provide insurance against outliving one s wealth. Previous research

Insights: Financial Capability. Gender, Generation and Financial Knowledge: A Six-Year Perspective. Women, Men and Financial Literacy

Insights: Financial Capability March 2018 Author: Gary Mottola, Ph.D. FINRA Investor Education Foundation What s Inside: Women, Men and Financial Literacy 1 Gender Differences in Investor Literacy 4 Self-Assessed

Insights: Financial Capability March 2018 Author: Gary Mottola, Ph.D. FINRA Investor Education Foundation What s Inside: Women, Men and Financial Literacy 1 Gender Differences in Investor Literacy 4 Self-Assessed

What You Don t Know Can t Help You: Knowledge and Retirement Decision Making

VERY PRELIMINARY PLEASE DO NOT QUOTE COMMENTS WELCOME What You Don t Know Can t Help You: Knowledge and Retirement Decision Making February 2003 Sewin Chan Wagner Graduate School of Public Service New

VERY PRELIMINARY PLEASE DO NOT QUOTE COMMENTS WELCOME What You Don t Know Can t Help You: Knowledge and Retirement Decision Making February 2003 Sewin Chan Wagner Graduate School of Public Service New

Investor Competence, Information and Investment Activity

Investor Competence, Information and Investment Activity Anders Karlsson and Lars Nordén 1 Department of Corporate Finance, School of Business, Stockholm University, S-106 91 Stockholm, Sweden Abstract

Investor Competence, Information and Investment Activity Anders Karlsson and Lars Nordén 1 Department of Corporate Finance, School of Business, Stockholm University, S-106 91 Stockholm, Sweden Abstract

Are Americans Saving Optimally for Retirement?

Figure : Median DB Pension Wealth, Social Security Wealth, and Net Worth (excluding DB Pensions) by Lifetime Income, (99 dollars) 400,000 Are Americans Saving Optimally for Retirement? 350,000 300,000

Figure : Median DB Pension Wealth, Social Security Wealth, and Net Worth (excluding DB Pensions) by Lifetime Income, (99 dollars) 400,000 Are Americans Saving Optimally for Retirement? 350,000 300,000

CHAPTER 2 Describing Data: Numerical

CHAPTER Multiple-Choice Questions 1. A scatter plot can illustrate all of the following except: A) the median of each of the two variables B) the range of each of the two variables C) an indication of

CHAPTER Multiple-Choice Questions 1. A scatter plot can illustrate all of the following except: A) the median of each of the two variables B) the range of each of the two variables C) an indication of

All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the

and not those of the Wharton School or the") All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the Pension Research Council. 2010 Pension Research Council

All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the Pension Research Council. 2010 Pension Research Council

The Consistency between Analysts Earnings Forecast Errors and Recommendations

The Consistency between Analysts Earnings Forecast Errors and Recommendations by Lei Wang Applied Economics Bachelor, United International College (2013) and Yao Liu Bachelor of Business Administration,

The Consistency between Analysts Earnings Forecast Errors and Recommendations by Lei Wang Applied Economics Bachelor, United International College (2013) and Yao Liu Bachelor of Business Administration,

Supplementary Appendix to Financial Intermediaries and the Cross Section of Asset Returns

Supplementary Appendix to Financial Intermediaries and the Cross Section of Asset Returns Tobias Adrian tobias.adrian@ny.frb.org Erkko Etula etula@post.harvard.edu Tyler Muir t-muir@kellogg.northwestern.edu

Supplementary Appendix to Financial Intermediaries and the Cross Section of Asset Returns Tobias Adrian tobias.adrian@ny.frb.org Erkko Etula etula@post.harvard.edu Tyler Muir t-muir@kellogg.northwestern.edu

Retirement Savings: How Much Will Workers Have When They Retire?

Order Code RL33845 Retirement Savings: How Much Will Workers Have When They Retire? January 29, 2007 Patrick Purcell Specialist in Social Legislation Domestic Social Policy Division Debra B. Whitman Specialist

Order Code RL33845 Retirement Savings: How Much Will Workers Have When They Retire? January 29, 2007 Patrick Purcell Specialist in Social Legislation Domestic Social Policy Division Debra B. Whitman Specialist

HOW EARNINGS AND FINANCIAL RISK AFFECT PRIVATE ACCOUNTS IN SOCIAL SECURITY REFORM PROPOSALS

HOW EARNINGS AND FINANCIAL RISK AFFECT PRIVATE ACCOUNTS IN SOCIAL SECURITY REFORM PROPOSALS Background The American public widely believes that the Social Security program faces a long-term financing problem

HOW EARNINGS AND FINANCIAL RISK AFFECT PRIVATE ACCOUNTS IN SOCIAL SECURITY REFORM PROPOSALS Background The American public widely believes that the Social Security program faces a long-term financing problem