You will be introduced to careers that are available in the Accounting and Finance Pathway.

|

|

|

- Hannah Foster

- 5 years ago

- Views:

Transcription

1 In this unit you will discover ways to apply sound decision-making skills, discover stable saving and spending habits, and practice using bank accounts to manage your money. You will be introduced to careers that are available in the Accounting and Finance Pathway. Standard 4: Students will explore skills, knowledge and concepts related to College and Career Pathways in Business and Marketing Objective 1: Explore the careers, education, and training related to accounting and finance, HR management, and hospitality and travel. Indicators: Understand basic personal money management including sales tax and payroll deductions. Explore how financial choices impact outcomes. Explore related career Pathways

2 Career Connection Assignment Accounting and Finance Accounting and Finance jobs perform duties that deal with money within a company. Some duties may be preparing financial reports, managing money, providing financial advice, analyzing finances, etc Accounting and Finance jobs are considered to be in high demand. Match the following Accounting and Finance jobs below to what you think the job duties are. Accountant evaluates financial backgrounds to decide whether to give a loan. Financial Manager provides financial advice to people. Loan Officer analyzes the finances of a bank to make sure they follow the laws. Tax Preparer creates and checks financial information. Financial Planner manages investments for companies. Securities Salesperson prepares tax returns. Financial Examiner buys and sells financial services.

3 Career Connection: Accounting and Finance Careers to Explore Accountant and Auditors: assemble, analyze, and check the accuracy of financial information. Education: Have a bachelor's degree Average Utah Wage: Hourly, 60, Yearly Bookkeeping and accounting clerks: manage the financial records of companies or clients. Education: Train through formal training programs or on the job Average Utah Wage: Hourly, 32, Yearly *Financial managers: manage budgets and investments for companies. Education: Have at least a bachelor's degree, plus work experience Average Utah Wage: Hourly, 96, Yearly Loan officers: evaluate applicants' financial backgrounds. They decide whether applicants will receive loans. Education: Most have a bachelor's degree Average Utah Wage: Hourly, 54, Yearly Tax examiners: determine the amount of taxes owed by businesses and citizens. Education: Have a bachelor's degree Average Utah Wage: Hourly, 45, Yearly Tax preparers: interview clients, review tax records, and fill out tax returns. Education: May need to be certified Average Utah Wage: Hourly, 33, Yearly Financial Planners: -counselors provide financial advice to people. Education: Have a bachelor's degree Average Utah Wage: Hourly, 52, Yearly Securities salesperson: buy and sell securities or offer financial services Education: Have a bachelor's degree Average Utah Wage: Hourly, 55, Yearly Vocabulary: Payroll Income Deductions Sales Tax Interest Principal Checks Debit Card Gross Pay Net Pay Budget Investment Financial examiners: analyze the finances of banks and other financial organizations to make sure they comply with laws and regulations. Education: Have a bachelor's degree Average Utah Wage: Hourly, 66, Yearly

4 Alexander Who Used To Be Rich Last Sunday by:judith Viorst Listen to the story and list each item and the amount that Alexander buys. Then determine whether the item was a good, service or other. Item Description Cost Good Service Other Total Spent: Did Alexander spend his money wisely? Why or why not? Explain your idea of wise spending: Watch Funny Money Man and determine Money Makers & Money Losers *************************************** Funny Money Man Item Money Maker Money Loser New Outfit Certificate of Deposit Investing in the Stock Market New Car Computer X-Box Game Savings Account

5 Exploring Money Makers Why Save? You are never too young to start saving for retirement. Don't put your financial future in someone else's hands. Learn to manage your own money. Understanding and handling your own personal finances will give you a strong foundation for your future, and will give you power in becoming a responsible adult. During your reading of Money Talks, you discovered the power of compound interest. By investing a little for a long time, you will end up with a lot. Today you will play with the Compound Interest Calculator, and discover the money you can make with different types of investing. Directions: Go to the Compound Interest Calculator ( ) and work through the following scenerios: Key vocabulary: Principal- The original amount invested Interest A t d Savings Accounts: A savings account is held at a bank or other financial institution that provides principal security and a modest interest rate. Savings accounts are generally for money that you don't intend to use for daily expenses. With a savings account you can usually get to your money easily. Savings accounts are a secure way of investing money with no risk. Scenerio 1: Change the monthly savings to 150 per month and put your current age for the starting age. Savings account interest is usually low, so change the interest rate to 1%, then calculate. How much money would you have by the time you retire at age 65? Did you pay more principal or earn more interest? Change the age to 35 with this same scenerio, how much money by age 65?

6 Certificate of Deposit: A certificate of deposit is a promissory note issued by a bank (similar to a savings account). It is a time deposit that restricts a person from withdrawing their money for a certain period of time. Interest rate for this type of account is usually higher because your money has restrictions. Scenerio 2: Change the monthly savings to 150 per month and put your current age for the starting age. Certificate of Deposit accounts are usually higher than a savings because you have to leave your money there for a longer period of time, change the interest rate to 3%, then calculate. How much money would you have by the time you retire at age 65? Did you pay more principal or earn more interest? Change the age to 35 with this same scenerio, how much money by age 65? Stock Market: Stocks are units of ownership in a company. When you buy stock, you become a shareholder, which means you now own a "part" of the company. If the company's profits go up, you "share" in those profits. If the company's profits fall, so does the price of your stock. Since this type of investment is risky, the interest rates are usually much higher than a safe investment. Scenerio 3: Change the monthly savings to 150 per month and put your current age for the starting age. Stocks usually pay a higher interest than a bank account because of the high risk, change the interest rate to 8%, then calculate. How much money would you have by the time you retire at age 65? Did you pay more principal or earn more interest? Change the age to 35 with this same scenerio, how much money by age 65? Review: What factors are important to making a lot of money by the time your retire? Do you believe investing is important? Why? Explore your own scenario and explain your results:

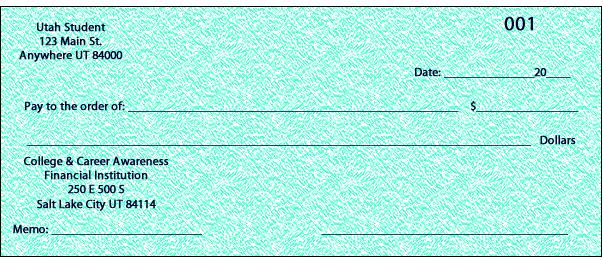

7 Checking Account Basics It won t be long, and you will be paying your own bills and managing your own money. There are different ways of handling your money: The envelope method, savings account, cashier checks, or checking account. Today we are going to learn how to manage a checking account. Go through the Managing Money with a Checking Account PowerPoint to gain the information on filling out a check and register, then return back to this worksheet and complete the following: 1. You just purchased a pair of jeans for at Old Navy. Fill out the check below. 2. Record the above transaction in the register below and complete a running balance. 3. Deposit your paycheck for in the register below and complete a running balance

8 Managing Your Income and Bills with a Checking Account Complete the following real life scenario story problems using checks and a register. Read the problems carefully, some will have multiple steps to figuring out an answer, while others just give you directions to write a check or make a deposit. You may want to use a calculator and scratch paper to complete this assignment. 1. You just opened a checking account and deposited into your account. Make the necessary adjustments in your register. 2. You purchased a home for your family. It is necessary for you to make payments every month to pay for this home. Your mortgage payment is due for the month. Fill out check #1 for to Bank of America. 3. You have to pay for utility services to keep your home functioning. Monthly fees for water, sewer, and garbage pickup are due. Your city charges for water, for sewer, and 8.50 for garbage pickup. Make out check #2 to your city, for the total of these monthly fees. 4. You purchased a used car so you would have transportation to and from work. It is necessary for you to make payments every month to pay for the loan of the car. Make check #3 to Bank of Utah for It is the law for every driver to have car insurance. You need to pay for your monthly insurance coverage. Make out check #4 for 98 to Allstate Insurance. 6. If you want to drive your car, you must put gas in it. You bought 15 gallons of gas to fill up the tank. Each gallon cost Write out check #5 to Chevron for the total bill. 7. Everyone must have a job to receive income to survive. You are a bookkeeper, and you make an hour. You worked 80 hours during the pay period. Anyone who makes an income is required to pay taxes; your deductions are 20% of your gross income. Make a deposit in your register for your net pay. 8. You need to pay for the phone service in your home. You made 156 minutes worth of long distance calls to keep in touch with family and friends, each of those minutes costs 0.25.You also have a local service charge of 28, and a 5.00 charge for call waiting. Write out check #6 to AT&T for your monthly bill.

9 9. You and your spouse enjoyed an evening at Texas Roadhouse for dinner. You ordered the Sirloin Steak for 18.95, and your spouse ordered the Road Kill for It is custom to leave a 20% tip at dinnertime to show how grateful you are for the service. Make check #7 out for the total of dinner and the tip. 10. Harmon s grocery store was having a case lot sale, so you decided to finish up your month supply of food. You spent for groceries and 6% for sales tax. Make out check #8 for the correct amount. 11. You have 2 children that are in daycare while you go to work. Daycare cost 1.50 an hour per child. The children are in Little Tots Daycare 6 hours a day, 5 days a week. You need to pay for 4 weeks of service. Write check #9 for the correct amount. 12. It is your child s birthday, so you purchased a bike from Walmart. The bike cost and you also had to pay 6% tax. You are out of checks so you must swipe your debit card, which means the money still comes out of your account, so make the necessary deduction from your register.

10

11

12

13 Code Date Transaction Description Payment, Withdrawal (-) Deposit, Credit (+) Balance

14 Balancing Your Checkbook Each month the bank or credit union sends you a monthly record of your deposits, checks, and debit card transactions. This monthly record is called a bank statement. It is important to balance your checkbook at least once a month to make sure your figures match that of the bank, so you always know how much money is in your account. Today you will balance your checkbook using the statement and worksheet below. Step 1: Check off every transaction in the register that is listed on the statement. College & Career Awareness Financial Institution 250 E 500 S Salt Lake City UT Account # Balance: Transaction History: Code: Withdrawal/Debit Deposit/Credit Balance Deposit Debit Card Ending Balance: Step 2: Fill out the following steps to balance your checkbook: A. Ending balance on statement Outstanding Checks B. List deposit in register that are not included on statement Code: Amount: Subtotal: Add A and B C. List Outstanding Checks Ending Balance: Subtract C from Subtotal The ending balance should match your register balance. Total:

15 Creating a Budget After reading Money Talks, hopefully you understood the importance of creating a budget. A budget helps you keep track of money you have coming in and money you have going out. Keeping a precise record of every purchase allows you to make smarter choices when spending. It also allows you to visualize what you have left to make room for investing. Using a spreadsheet, follow the steps below carefully to create a budget with the bills you previously paid. In cell A1, type your name. In cell C4, type Monthly Budget. Format C4 to size 16, Bold, and change the font style. In cell A7, type Bills. In cell C7, type Amount. Hold the Control key down and select cells A7 and C7, format the cells to Bold, and size 12 In cell A9, type the first bill you paid in your register. Example: Mortgage In cell C9, type the amount you paid in your register. Do not type the symbol. Example: 952 Continue with the list of bills and amounts, until you have listed all bills from the register. Make sure you do not put deposits into this list. When you are finished with this step you will fill cells to A18 and C18. Select cell A21, type Total. Select cells C9 to C21, then select Format as Currency ( icon) Select the function Sum ( icon). If you did this correctly your sum will total 2, Select cells A9-A18, hold the Control key down and select C9-C18. Then in the Insert menu, select chart and choose a bar chart. Move and place the chart underneath the typed information. Select cell E7 and type Income. Select cell E8 and type Bills. Select cell E10 and type Available. Select cell F7 and select Format as Currency ( Icon), then type (this is the total income from your checkbook) Select F8 and press the = key, and then select cell C21, and press enter. Select cells F7-F10 and press the = key, then select F7, then press the subtract (-) key, then select F8 key and enter. If you did this correctly the answer will come out Create another chart by selecting cells E8, E9, F8, and F9, Insert chart, and choose a pie chart. Place the chart underneath the typed information.

4.01 Accounting and Finance

4.01 Accounting and Finance What is Accounting? Method of reporting financial activity of a business Financial transactions recorded in an orderly fashion Accounting Equation Assets = Liabilities + Owner

4.01 Accounting and Finance What is Accounting? Method of reporting financial activity of a business Financial transactions recorded in an orderly fashion Accounting Equation Assets = Liabilities + Owner

Money Management Financial Survivor: Understanding Credit and Banking

Money Management Financial Survivor: Understanding Credit and Banking In this workshop, youth will learn about credit, the importance of maintaining good credit, and how to access their credit report.

Money Management Financial Survivor: Understanding Credit and Banking In this workshop, youth will learn about credit, the importance of maintaining good credit, and how to access their credit report.

FINANCIAL LESSONS FROM A HURRICANE

K ATRINA S CL ASSROOM: FINANCIAL LESSONS FROM A HURRICANE LESSON 1: KATRINA STRIKES This introductory video sets the scene for Hurricane Katrina by portraying the storm striking, showing some of the devastation

K ATRINA S CL ASSROOM: FINANCIAL LESSONS FROM A HURRICANE LESSON 1: KATRINA STRIKES This introductory video sets the scene for Hurricane Katrina by portraying the storm striking, showing some of the devastation

Nick s family Jacquelyn s family Jamie s family

VISUAL 1-1 NEEDS, WANTS, AND GOALS Nick s family Jacquelyn s family Jamie s family Needs (predicted) Needs (actual) Wants (predicted) Wants (actual) Goals (predicted) Goals (actual) FEDERAL RESERVE BANK

VISUAL 1-1 NEEDS, WANTS, AND GOALS Nick s family Jacquelyn s family Jamie s family Needs (predicted) Needs (actual) Wants (predicted) Wants (actual) Goals (predicted) Goals (actual) FEDERAL RESERVE BANK

HOW TO USE A FINANCIAL INSTITUTION. BUILDING A better FUTURE

HOW TO USE A FINANCIAL INSTITUTION BUILDING A better FUTURE HOW TO USE A FINANCIAL INSTITUTION LATINO COMMUNITY CREDIT UNION & LATINO COMMUNITY DEVELOPMENT CENTER Copyright 2011 Latino Community Credit

HOW TO USE A FINANCIAL INSTITUTION BUILDING A better FUTURE HOW TO USE A FINANCIAL INSTITUTION LATINO COMMUNITY CREDIT UNION & LATINO COMMUNITY DEVELOPMENT CENTER Copyright 2011 Latino Community Credit

2. To earn as much interest as possible, you should open a savings account that earns () interest Hide answers

interest Hide answers") 1. Interest is? Hide answers A charge for lending money to a bank amount owed for borrowing money amount added into your savings when opening a n account a charge for accessing the money in your savings

1. Interest is? Hide answers A charge for lending money to a bank amount owed for borrowing money amount added into your savings when opening a n account a charge for accessing the money in your savings

Budgeting: Making the Most of Your Money

? Did You Know? Almost 60% of millionaires use a budget to manage their money. The Millionaire Next Door: The Surprising Secrets of America s Wealthy. In this unit, you will: Examine your spending habits

? Did You Know? Almost 60% of millionaires use a budget to manage their money. The Millionaire Next Door: The Surprising Secrets of America s Wealthy. In this unit, you will: Examine your spending habits

Personal Financial Literacy

Personal Financial Literacy 7 Unit Overview Being financially literate means taking responsibility for learning how to manage your money. In this unit, you will learn about banking services that can help

Personal Financial Literacy 7 Unit Overview Being financially literate means taking responsibility for learning how to manage your money. In this unit, you will learn about banking services that can help

Banks and Paychecks Role Play

Banks and Paychecks Role Play Part I: Getting Paid Roles: Employer, Employee Employer: Thank you for your hard work for the last 2 weeks. Here is your paycheck. The Employer hands the sample paycheck to

Banks and Paychecks Role Play Part I: Getting Paid Roles: Employer, Employee Employer: Thank you for your hard work for the last 2 weeks. Here is your paycheck. The Employer hands the sample paycheck to

Budgeting Module. a. True b. False

Budgeting Pretest 1. What is gross monthly pay? a. The monthly pay after taxes are deducted. b. The monthly pay before taxes and insurance are deducted. c. The hourly pay times 2080. 2. What is net monthly

Budgeting Pretest 1. What is gross monthly pay? a. The monthly pay after taxes are deducted. b. The monthly pay before taxes and insurance are deducted. c. The hourly pay times 2080. 2. What is net monthly

Math 5.1: Mathematical process standards

Lesson Description This lesson gives students the opportunity to explore the different methods a consumer can pay for goods and services. Students first identify something they want to purchase. They then

Lesson Description This lesson gives students the opportunity to explore the different methods a consumer can pay for goods and services. Students first identify something they want to purchase. They then

Personal Financial Literacy

Personal Financial Literacy 7 Unit Overview Being financially literate means taking responsibility for learning how to calculate income taxes on wages and how to create a budget to plan your spending and

Personal Financial Literacy 7 Unit Overview Being financially literate means taking responsibility for learning how to calculate income taxes on wages and how to create a budget to plan your spending and

Using Credit. Grade Five. Overview. Lesson Objectives. Prerequisite Skills. Materials List

Grade Five Using Credit Overview Students share several chapters from the book Not for a Billion Gazillion Dollars, by Paula Danzinger, to learn about earning money, saving, credit, and debt. Students

Grade Five Using Credit Overview Students share several chapters from the book Not for a Billion Gazillion Dollars, by Paula Danzinger, to learn about earning money, saving, credit, and debt. Students

Credit Cards Friend or Foe? An exploration of credit cards and debit cards utilizing Internet resources and spreadsheets.

Credit Cards Friend or Foe? An exploration of credit cards and debit cards utilizing Internet resources and spreadsheets. Day One Investigating Credit Cards and Debit Cards The students will need access

Credit Cards Friend or Foe? An exploration of credit cards and debit cards utilizing Internet resources and spreadsheets. Day One Investigating Credit Cards and Debit Cards The students will need access

Like the federal government, individual consumers must manage their money. In this section, you will learn about budgeting and saving money.

Budgeting Section 1 Like the federal government, individual consumers must manage their money. In this section, you will learn about budgeting and saving money. Vocabulary discretionary expense: an expense

Budgeting Section 1 Like the federal government, individual consumers must manage their money. In this section, you will learn about budgeting and saving money. Vocabulary discretionary expense: an expense

6.1 Simple Interest page 243

page 242 6 Students learn about finance as it applies to their daily lives. Two of the most important types of financial decisions for many people involve either buying a house or saving for retirement.

page 242 6 Students learn about finance as it applies to their daily lives. Two of the most important types of financial decisions for many people involve either buying a house or saving for retirement.

VOLUNTEER TRAINING INFORMATION

VOLUNTEER TRAINING INFORMATION VOLUNTEER TRAINING Volunteers generally feel more comfortable in staffing a table if they have been provided with advance information about the concept and have time to read

VOLUNTEER TRAINING INFORMATION VOLUNTEER TRAINING Volunteers generally feel more comfortable in staffing a table if they have been provided with advance information about the concept and have time to read

Financial Field Trips

The Green Event Financial Field Trips Parent Packet Dear Parent / Guardian, We are excited to have your child participate with us in Utah s 4-H Strong Futures Green Event program. I assure you that your

The Green Event Financial Field Trips Parent Packet Dear Parent / Guardian, We are excited to have your child participate with us in Utah s 4-H Strong Futures Green Event program. I assure you that your

Banking Basics. Banks and Credit Unions. Warm-Up Activity. Why should you put your money in a bank?

Account Management Account Management You will be introduced to the banking process. You will learn how to locate a bank or credit union with which you want to do business, what accounts you should have

Account Management Account Management You will be introduced to the banking process. You will learn how to locate a bank or credit union with which you want to do business, what accounts you should have

Keeping Score: Why Credit Matters

Keeping Score: Why Credit Matters LESSON 6: TEACHERS GUIDE In the middle of a championship football game, keeping score is the norm. But when it comes to life, many young adults don t realize how important

Keeping Score: Why Credit Matters LESSON 6: TEACHERS GUIDE In the middle of a championship football game, keeping score is the norm. But when it comes to life, many young adults don t realize how important

Value of Education: Education and Earning Power

Value of Education: Education and Earning Power Preparation Grade Level: 4-9 Group Size: 20-30 Time: 45-60 Minutes Presenters: 3-5 Objectives Students will be able to: Calculate monthly & annual earnings

Value of Education: Education and Earning Power Preparation Grade Level: 4-9 Group Size: 20-30 Time: 45-60 Minutes Presenters: 3-5 Objectives Students will be able to: Calculate monthly & annual earnings

7 th Grade Math STAAR Review Booklet

7 th Grade Math STAAR Review Booklet Reporting Category 4 Student Name: Teacher Name: 1 2 Table of Contents Reporting Category 4 Sales Tax and Income Tax.4-9 Personal Budget.10-13 Net Worth Statement 14-16

7 th Grade Math STAAR Review Booklet Reporting Category 4 Student Name: Teacher Name: 1 2 Table of Contents Reporting Category 4 Sales Tax and Income Tax.4-9 Personal Budget.10-13 Net Worth Statement 14-16

Unit 4 More Banking: Checks, Savings and ATMs

Unit 4 More Banking: Checks, Savings and ATMs Banking: Vocabulary Review Directions: Draw a line to match the word with its meaning. 1. bank 2. credit 3. ATM 4. minimum 5. maximum 6. teller 7. balance

Unit 4 More Banking: Checks, Savings and ATMs Banking: Vocabulary Review Directions: Draw a line to match the word with its meaning. 1. bank 2. credit 3. ATM 4. minimum 5. maximum 6. teller 7. balance

This page intentionally left blank

This page intentionally left blank This page intentionally left blank. Table of Contents CreditSmart Module 2: Managing Your Money Welcome to Freddie Mac s CreditSmart Initiative... 6 Program Structure...

This page intentionally left blank This page intentionally left blank. Table of Contents CreditSmart Module 2: Managing Your Money Welcome to Freddie Mac s CreditSmart Initiative... 6 Program Structure...

check debit card overdraw deposit slip endorse bank statement certified check cashier s check money order traveler s check

How can a checking account help me to manage my money? Chapter 25 Key Terms check debit card overdraw deposit slip endorse bank statement certified check cashier s check money order traveler s check Chapter

How can a checking account help me to manage my money? Chapter 25 Key Terms check debit card overdraw deposit slip endorse bank statement certified check cashier s check money order traveler s check Chapter

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Texas Essential Knowledge and Skills (Prerequisite standards)

Texas Essential Knowledge and Skills (Prerequisite standards)") Lesson Description Students will analyze families finances to identify assets and liabilities. They will use this information to calculate the families net worth and learn the benefits of having a positive

Lesson Description Students will analyze families finances to identify assets and liabilities. They will use this information to calculate the families net worth and learn the benefits of having a positive

Before How can lines on a graph show the effect of interest rates on savings accounts?

Compound Interest LAUNCH (7 MIN) Before How can lines on a graph show the effect of interest rates on savings accounts? During How can you tell what the graph of simple interest looks like? After What

Compound Interest LAUNCH (7 MIN) Before How can lines on a graph show the effect of interest rates on savings accounts? During How can you tell what the graph of simple interest looks like? After What

Unit 2 Basic Banking Services. High-Intermediate and Advanced

Unit 2 Basic Banking Services High-Intermediate and Advanced Objectives Identify vocabulary and concepts related to basic banking services. Identify checking account services and understand related fees.

Unit 2 Basic Banking Services High-Intermediate and Advanced Objectives Identify vocabulary and concepts related to basic banking services. Identify checking account services and understand related fees.

Name Date Period. Money Management for Teens

Name Date Period Money Management for Teens Wants Vs. Needs It is not uncommon to hear teens and even adults use the terms wants and needs interchangeably. You might even hear a child say, I need a candy

Name Date Period Money Management for Teens Wants Vs. Needs It is not uncommon to hear teens and even adults use the terms wants and needs interchangeably. You might even hear a child say, I need a candy

PFIN 5: Banking Procedures 24

PFIN 5: Banking Procedures 24 5 1 Checking Accounts OBJECTIVES Explain the purpose and use of a checking account. Prepare a checkbook register. Write a check and prepare a deposit slip. Prepare a bank

PFIN 5: Banking Procedures 24 5 1 Checking Accounts OBJECTIVES Explain the purpose and use of a checking account. Prepare a checkbook register. Write a check and prepare a deposit slip. Prepare a bank

Worksheet and Example How Much House Can I Afford?

Worksheet and Example How Much House Can I Afford? Instructions: Just follow along with each line of the worksheet and the associated instructions, filling in and calculating the values as instructed.

Worksheet and Example How Much House Can I Afford? Instructions: Just follow along with each line of the worksheet and the associated instructions, filling in and calculating the values as instructed.

Income taxes in Quebec module

Income taxes in Quebec module Trainer s introduction Most people are aware that they must file income tax returns in Canada and Quebec, if only to claim back any excess taxes that were withheld from their

Income taxes in Quebec module Trainer s introduction Most people are aware that they must file income tax returns in Canada and Quebec, if only to claim back any excess taxes that were withheld from their

MODULE 7: Borrowing Basics INSTRUCTOR GUIDE. MONEY SMART for Adults

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

HOMELESS PREVENTION 101 Lesson Plan 2

HOMELESS PREVENTION 101 Lesson Plan 2 Inquiry Question: How does creating a budget help me become a more goal oriented person? Lesson Title: On My Own Description: Students will create a budget, which

HOMELESS PREVENTION 101 Lesson Plan 2 Inquiry Question: How does creating a budget help me become a more goal oriented person? Lesson Title: On My Own Description: Students will create a budget, which

Module 3 - Budgeting ACTIVITY SHEET 3-1. Write down any other ideas the group came up with, especially ideas that fit your situation.

ParticipantHandbook ACTIVITY SHEET 3-1 The B word budget 1 Write down any other ideas the group came up with, especially ideas that fit your situation. What is a budget? Why budget? A way to keep track

ParticipantHandbook ACTIVITY SHEET 3-1 The B word budget 1 Write down any other ideas the group came up with, especially ideas that fit your situation. What is a budget? Why budget? A way to keep track

APPLICATION GUIDE. Where can I get help? Who can apply?

APPLICATION GUIDE Where can I get help? If someone is helping you complete your application, such as a support worker with a community or social service agency, please provide their contact information

APPLICATION GUIDE Where can I get help? If someone is helping you complete your application, such as a support worker with a community or social service agency, please provide their contact information

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC. Financial Literacy Workbook, Grades 9-12

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC Financial Literacy Workbook, Grades 9-12 FINANCIAL PLANNING Financial planning is about defining and following a set of steps in

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC Financial Literacy Workbook, Grades 9-12 FINANCIAL PLANNING Financial planning is about defining and following a set of steps in

Share Draft/Checking Account Basics

Share Draft/Checking Account Basics A check is a written order that represents cash. Credit union checking accounts are called share draft accounts. Share drafts, like checks, are accepted almost everywhere.

Share Draft/Checking Account Basics A check is a written order that represents cash. Credit union checking accounts are called share draft accounts. Share drafts, like checks, are accepted almost everywhere.

FINANCIAL FOUNDATIONS

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program BUDGETING Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program BUDGETING Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

LEARNING TASKS These tasks match pages in Student Guide 1.

STUDENT LEARNING PLAN Lesson 1-4: Spending Plan OVERVIEW You've analyzed what you've been spending money on and set some SMART goals to strive for. Now, the rubber meets the road and it's time to start

STUDENT LEARNING PLAN Lesson 1-4: Spending Plan OVERVIEW You've analyzed what you've been spending money on and set some SMART goals to strive for. Now, the rubber meets the road and it's time to start

Checking Account and Debit Card Simulation

Checking Account and Debit Card Simulation Student Instructions and Worksheets Introductory Level Take Charge Today May 2006 Checking Account & Debit Card Simulation Page 1 Checking Account Student Instructions

Checking Account and Debit Card Simulation Student Instructions and Worksheets Introductory Level Take Charge Today May 2006 Checking Account & Debit Card Simulation Page 1 Checking Account Student Instructions

Life Insurance Buyer s Guide

Contents What type of insurance should I buy? How much insurance should I buy? How long should my term life insurance last? How do I compare life insurance quotes? How do I compare quotes from difference

Contents What type of insurance should I buy? How much insurance should I buy? How long should my term life insurance last? How do I compare life insurance quotes? How do I compare quotes from difference

budget fixed expense flexible expense

How do I make my income cover my expenses? Chapter 24 Key Terms budget fixed expense flexible expense Chapter Objectives After studying this chapter, you will be able to identify sources of income. list

How do I make my income cover my expenses? Chapter 24 Key Terms budget fixed expense flexible expense Chapter Objectives After studying this chapter, you will be able to identify sources of income. list

Food Resource Management

Know how. Know now. Learn at Home: Nutrition Lessons for Healthy Living Food Resource Management By choosing to complete this mail lesson, you have taken the first step in learning more about the importance

Know how. Know now. Learn at Home: Nutrition Lessons for Healthy Living Food Resource Management By choosing to complete this mail lesson, you have taken the first step in learning more about the importance

Using a Credit Card. Name Date

Unit 4 Using a Credit Card Name Date Objective In this lesson, you will learn to explain and provide examples of the benefits and disadvantages of using a credit card. This lesson will also discuss the

Unit 4 Using a Credit Card Name Date Objective In this lesson, you will learn to explain and provide examples of the benefits and disadvantages of using a credit card. This lesson will also discuss the

Reading Essentials and Study Guide

Lesson 3 Banking Today ESSENTIAL QUESTION How has technology affected the way we use money today? Reading HELPDESK Academic Vocabulary products things that are sold Content Vocabulary credit union nonprofit

Lesson 3 Banking Today ESSENTIAL QUESTION How has technology affected the way we use money today? Reading HELPDESK Academic Vocabulary products things that are sold Content Vocabulary credit union nonprofit

Financial Literacy. Budgeting

Financial Literacy Budgeting ACTIVITY SHEET 3-1 The B word budget 1 What do you think about when you hear the word budget? What words or feelings come to mind? Write down any other ideas the group came

Financial Literacy Budgeting ACTIVITY SHEET 3-1 The B word budget 1 What do you think about when you hear the word budget? What words or feelings come to mind? Write down any other ideas the group came

Money Management & Budgeting Skills Workshop

Money Management & Budgeting Skills Workshop Making Money Work for You Financial Education Supported by: Concept Checklist What will I learn today? [ ] Goals [ ] Needs vs.wants [ ] Budgeting Basics [ ]

Money Management & Budgeting Skills Workshop Making Money Work for You Financial Education Supported by: Concept Checklist What will I learn today? [ ] Goals [ ] Needs vs.wants [ ] Budgeting Basics [ ]

credit crunch lesson 6: student outcomes Chapter 30 from Reality Check time relationship to national standards assessment materials

Chapter 30 from Reality Check time 50 minutes relationship to national standards FCS National Standards: 2.1.2, 2.6.2, 3.3.3 JumpStart Financial Literacy Standards PMM3, CD 1 assessment Do I Have to Have

Chapter 30 from Reality Check time 50 minutes relationship to national standards FCS National Standards: 2.1.2, 2.6.2, 3.3.3 JumpStart Financial Literacy Standards PMM3, CD 1 assessment Do I Have to Have

Volunteer Instructor Notes

Volunteer Instructor Notes KEY Student Activity Important Note Go Do It Now! Call to Action 1 Some classrooms may not be able to play videos, the internet connection may be very slow, or may not have audio

Volunteer Instructor Notes KEY Student Activity Important Note Go Do It Now! Call to Action 1 Some classrooms may not be able to play videos, the internet connection may be very slow, or may not have audio

Checking Account and Debit Card Simulation

Checking Account and Debit Card Simulation Student Instructions and Worksheets Get Ready to Take Charge of Your Finances Family Economics & Financial Education May 2006 Get Ready to Take Charge of Your

Checking Account and Debit Card Simulation Student Instructions and Worksheets Get Ready to Take Charge of Your Finances Family Economics & Financial Education May 2006 Get Ready to Take Charge of Your

Lesson Module 1: The Fundamentals of Net Worth

Lesson Module 1: The Fundamentals of Net Worth Module 1 Overview The entire game of football is based on a few basic skills: blocking, tackling, passing and running. To be a successful football player,

Lesson Module 1: The Fundamentals of Net Worth Module 1 Overview The entire game of football is based on a few basic skills: blocking, tackling, passing and running. To be a successful football player,

Get Ready to Take Charge of Your Finances

Checking Account & Debit Card Simulation Grade Level 7-9 Get Ready to Take Charge of Your Finances Time to complete: 180 minutes National Content Standards Family and Consumer Science Standards: 1.1.6,

Checking Account & Debit Card Simulation Grade Level 7-9 Get Ready to Take Charge of Your Finances Time to complete: 180 minutes National Content Standards Family and Consumer Science Standards: 1.1.6,

Lesson Description. Concepts. Objectives. Content Standards. Cards, Cars and Currency Lesson 3: Banking on Debit Cards

Lesson Description After discussing basic information about debit cards, students work in pairs to balance a bank account statement and calculate the costs of using a debit card irresponsibly. The students

Lesson Description After discussing basic information about debit cards, students work in pairs to balance a bank account statement and calculate the costs of using a debit card irresponsibly. The students

Using my PAYCHEK PLUS!

Using my The Basics 1: Getting started 4 2: How my card works 9 3: Making work for me 11 4: Getting cash at an ATM 13 5: Making a purchase at a store 15 My account information 1-800-578-2966 or www.cashcardsite.com

Using my The Basics 1: Getting started 4 2: How my card works 9 3: Making work for me 11 4: Getting cash at an ATM 13 5: Making a purchase at a store 15 My account information 1-800-578-2966 or www.cashcardsite.com

2. How to Increase my Savings and Write a Budget

2. How to Increase my Savings and Write a Budget Building a Better Future 67 68 Building a Better Future UNIT 2: HOW TO INCREASE MY SAVINGS AND WRITE A BUDGET Lesson 1: How to Increase my Savings Lesson

2. How to Increase my Savings and Write a Budget Building a Better Future 67 68 Building a Better Future UNIT 2: HOW TO INCREASE MY SAVINGS AND WRITE A BUDGET Lesson 1: How to Increase my Savings Lesson

TEACHING UNIT. Grade Level: Grade 10 Recommended Curriculum Area: Language Arts Other Relevant Curriculum Area(s): Mathematics

: Mathematics") TEACHING UNIT General Topic: Borrowing and Using Credit Unit Title: Managing Debt and Credit Grade Level: Grade 10 Recommended Curriculum Area: Language Arts Other Relevant Curriculum Area(s): Mathematics

TEACHING UNIT General Topic: Borrowing and Using Credit Unit Title: Managing Debt and Credit Grade Level: Grade 10 Recommended Curriculum Area: Language Arts Other Relevant Curriculum Area(s): Mathematics

Video 4 - Get the Credit You Deserve

Video 4 - Get the Credit You Deserve Video 4: Get the Credit You Deserve VIDEO SUMMARY This video explores the costs and benefits of using credit. Credit instruments allow consumers to take advantage of

Video 4 - Get the Credit You Deserve Video 4: Get the Credit You Deserve VIDEO SUMMARY This video explores the costs and benefits of using credit. Credit instruments allow consumers to take advantage of

Overview: This is an activity to help students gain a better understanding of Financial Literacy

Title: Personal Finance 4 Corners Game Subject: CTE Intro Author: Mike Wood and Jeff Hinton Grade Level: 7-12 Utah Core Curriculum: Standard 4, Objective 3 Time Duration: 20-30 Minutes Overview: This is

Title: Personal Finance 4 Corners Game Subject: CTE Intro Author: Mike Wood and Jeff Hinton Grade Level: 7-12 Utah Core Curriculum: Standard 4, Objective 3 Time Duration: 20-30 Minutes Overview: This is

RESPs and Other Ways to Save

for Indigenous Peoples Workbook 4 RESPs and Other Ways to Save Copyright 2017 ABC Life Literacy Canada First published in 2016 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada

for Indigenous Peoples Workbook 4 RESPs and Other Ways to Save Copyright 2017 ABC Life Literacy Canada First published in 2016 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada

WHAT IS MONEY? Unit of Exchange. Types of Money. Pine Gulch Skit 12/12/2016

Pine Gulch Skit WHAT IS MONEY? Unit of Exchange Under the Barter System Barter (trade) is the exchange of one good or service for another Requires double coincidence of want both people have to want what

Pine Gulch Skit WHAT IS MONEY? Unit of Exchange Under the Barter System Barter (trade) is the exchange of one good or service for another Requires double coincidence of want both people have to want what

Money Matters 1: Setting a Budget How can budgeting now help me make a big purchase later?

UNIT 6 MONEY MATTERS Lesson Descriptions Money Matters 1: Setting a Budget How can budgeting now help me make a big purchase later? Money Matters 2: Take it to the Bank! Why should I have a bank account

UNIT 6 MONEY MATTERS Lesson Descriptions Money Matters 1: Setting a Budget How can budgeting now help me make a big purchase later? Money Matters 2: Take it to the Bank! Why should I have a bank account

Resources for Raising Financially Fit Kids

Resources for Raising Financially Fit Kids Growing Financially Fit Children Toddlers and Pre-School Children As soon as children can count, introduce them to money. Take an active role in providing them

Resources for Raising Financially Fit Kids Growing Financially Fit Children Toddlers and Pre-School Children As soon as children can count, introduce them to money. Take an active role in providing them

Understanding The Benefits

Understanding The Benefits 2012 Contacting Social Security Visit our website Our website, www.socialsecurity.gov, is a valuable resource for information about all of Social Security s programs. At our

Understanding The Benefits 2012 Contacting Social Security Visit our website Our website, www.socialsecurity.gov, is a valuable resource for information about all of Social Security s programs. At our

DRIVING MY FINANCIAL FUTURE

STUDENT ACTIVITY 2 Write all of the things you d like to have or do that cost money, you can make the list as long as you want. Review the items you have listed and group them into the 3 category boxes

STUDENT ACTIVITY 2 Write all of the things you d like to have or do that cost money, you can make the list as long as you want. Review the items you have listed and group them into the 3 category boxes

Depository Institution Discovery Grade Level 7-9

2.7.2 Depository Institution Discovery Grade Level 7-9 Get Ready to Take Charge of Your Finances Time to complete: 90 minutes Content Standard Family and Consumer Science Standards: 2.5.1, 2.5.4, 2.6.1,

2.7.2 Depository Institution Discovery Grade Level 7-9 Get Ready to Take Charge of Your Finances Time to complete: 90 minutes Content Standard Family and Consumer Science Standards: 2.5.1, 2.5.4, 2.6.1,

What you know about life insurance

What you need to know about life insurance MONICA HARRIS Efficient Estates 888-997-8667 ext. 101 info@efficientestatesannuityandinsurance.com This piece has been reproduced with the permission of Life

What you need to know about life insurance MONICA HARRIS Efficient Estates 888-997-8667 ext. 101 info@efficientestatesannuityandinsurance.com This piece has been reproduced with the permission of Life

Personal budgeting 101

Personal budgeting 101 GRADE 12 In this lesson, students learn the fundamentals of budgeting. The action in the lesson includes tracking income and spending using a journal, the design and use of a simple

Personal budgeting 101 GRADE 12 In this lesson, students learn the fundamentals of budgeting. The action in the lesson includes tracking income and spending using a journal, the design and use of a simple

Setting Financial Goals

Setting Financial Goals FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Purpose Learn how to manage money by preparing a personal spending plan Identify ways to decrease spending

Setting Financial Goals FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Purpose Learn how to manage money by preparing a personal spending plan Identify ways to decrease spending

Checking 101. Property of Penn State Federal Credit Union

Checking 101 Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share draft is equivalent to a check,

Checking 101 Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share draft is equivalent to a check,

Student Guide: RWC Simulation Lab. Free Market Educational Services: RWC Curriculum

Free Market Educational Services: RWC Curriculum Student Guide: RWC Simulation Lab Table of Contents Getting Started... 4 Preferred Browsers... 4 Register for an Account:... 4 Course Key:... 4 The Student

Free Market Educational Services: RWC Curriculum Student Guide: RWC Simulation Lab Table of Contents Getting Started... 4 Preferred Browsers... 4 Register for an Account:... 4 Course Key:... 4 The Student

Schedule J: Your Expenses 12/13

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of (State) Case number _ (If known) Check if this is an amended filing

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of (State) Case number _ (If known) Check if this is an amended filing

You re On Your Own Checking Account Exercise

Checking Account Exercise Supplement to Making The Right Money Moves Check Writing Exercise You re On Your Own Imagine that you are now out on your own - moving on out to the big time and that new apartment.

Checking Account Exercise Supplement to Making The Right Money Moves Check Writing Exercise You re On Your Own Imagine that you are now out on your own - moving on out to the big time and that new apartment.

Lesson 4: Back to School Part 4: Saving

Lesson 4: Back to School Part 4: Saving Lesson Description In this five-part lesson, students look at the financial lessons that a teen and her family learned while they were displaced from their home

Lesson 4: Back to School Part 4: Saving Lesson Description In this five-part lesson, students look at the financial lessons that a teen and her family learned while they were displaced from their home

First Timer s Guide: Credit Cards. Used the right way, your credit card can be your new financial BFF.

First Timer s Guide: Credit Cards Used the right way, your credit card can be your new financial BFF. Like most things, with great power comes great responsibility. And credit cards are no different. Used

First Timer s Guide: Credit Cards Used the right way, your credit card can be your new financial BFF. Like most things, with great power comes great responsibility. And credit cards are no different. Used

PURCHASING, LEASING OR SELLING A HOME HOMEBUYER S FINANCIAL WORKSHEET

- DISCLAIMER - The following form is provided by FindLaw, a Thomson Business, for informational purposes only and is intended to be used as a guide prior to consultation with an attorney familiar with

- DISCLAIMER - The following form is provided by FindLaw, a Thomson Business, for informational purposes only and is intended to be used as a guide prior to consultation with an attorney familiar with

How to Bank and Save In Canada

for Newcomers and New Canadians Workbook 1 How to Bank and Save In Canada Welcome! We made this workshop for newcomers to Canada. Knowing more about how banking works here can help you settle in faster,

for Newcomers and New Canadians Workbook 1 How to Bank and Save In Canada Welcome! We made this workshop for newcomers to Canada. Knowing more about how banking works here can help you settle in faster,

Monthly Cash Flow Exercise

Name Monthly Cash Flow Exercise Directions: Use the following scenario cards to fill out the Monthly Cash Flow Statement Worksheet on the next page. Each of the items should be recorded in the appropriate

Name Monthly Cash Flow Exercise Directions: Use the following scenario cards to fill out the Monthly Cash Flow Statement Worksheet on the next page. Each of the items should be recorded in the appropriate

Money Issues That Concern Married Couples

AKD Consultants Adam Dworkin CPA 188 Whiting Street Suite 10 Hingham, MA 02043 781-556-5554 Adam@AKDConsultants.com Money Issues That Concern Married Couples Page 1 of 6, see disclaimer on final page Money

AKD Consultants Adam Dworkin CPA 188 Whiting Street Suite 10 Hingham, MA 02043 781-556-5554 Adam@AKDConsultants.com Money Issues That Concern Married Couples Page 1 of 6, see disclaimer on final page Money

Name: Period: Date. Financial Fitness. TEACHER: For the next few days we are going to be focusing on Family, Career and

Financial Fitness Introductory Skit: TEACHER: For the next few days we are going to be focusing on Family, Career and Community Leaders of America s (FCCLA s) Financial Fitness Program. STUDENT: Financial

Financial Fitness Introductory Skit: TEACHER: For the next few days we are going to be focusing on Family, Career and Community Leaders of America s (FCCLA s) Financial Fitness Program. STUDENT: Financial

Week #4: Review of The Heart of Algebra

Week #4: Review of The Heart of Algebra 1. Which of the following best describes the solutions to the inequality 3l 6 8? A) l K L B) l 2 C) l PQ L D) l 14 2. In the equation, 3 + 10x 5 = a + 1 x 2, a is

Week #4: Review of The Heart of Algebra 1. Which of the following best describes the solutions to the inequality 3l 6 8? A) l K L B) l 2 C) l PQ L D) l 14 2. In the equation, 3 + 10x 5 = a + 1 x 2, a is

Pre-Discharge Debtor Education Material

Pre-Discharge Debtor Education Material This workbook has been designed as a companion to the Pre-Discharge Financial Education Course offered by Debt Education and Certification Foundation. As you participate

Pre-Discharge Debtor Education Material This workbook has been designed as a companion to the Pre-Discharge Financial Education Course offered by Debt Education and Certification Foundation. As you participate

Loans: Banks or credit unions can loan you money. You pay the money back a little at a time. They charge you interest for the loan.

Basic Banking Services and Checking Accounts Intermediate MATERIALS What Can a Bank Do for You? Lesson 1: Introduction to Banking Services Worksheet 1-1 page 1 Beginner & Low- What Can a Bank Do for You?

Basic Banking Services and Checking Accounts Intermediate MATERIALS What Can a Bank Do for You? Lesson 1: Introduction to Banking Services Worksheet 1-1 page 1 Beginner & Low- What Can a Bank Do for You?

Checking Accounts. There are three basic types of banks.

Checking Accounts What s Next Project (DUE: Thursday 2/25 for periods 2 and 4; Friday 2/26 for period 7) Scoring will be based on highlighting/annotating key content and completing ALL activity pages accurately.

Checking Accounts What s Next Project (DUE: Thursday 2/25 for periods 2 and 4; Friday 2/26 for period 7) Scoring will be based on highlighting/annotating key content and completing ALL activity pages accurately.

LEARNING TASKS These tasks match pages 3-21 in Student Guide 5.

STUDENT LEARNING PLAN Lesson 5-1: Checking Accounts OVERVIEW Nothing beats the feel of a crisp new $20 bill in your hand. But as you move toward the real world after high school, you ll run into situations

STUDENT LEARNING PLAN Lesson 5-1: Checking Accounts OVERVIEW Nothing beats the feel of a crisp new $20 bill in your hand. But as you move toward the real world after high school, you ll run into situations

Money 101 Presenter s Guide

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

FINANCIAL LESSONS FROM A HURRICANE

K ATRINA S CL ASSROOM: FINANCIAL LESSONS FROM A HURRICANE INTRODUCTION OVERVIEW: THE IMPORTANCE OF BEING FINANCIALLY PREPARED During ordinary times, people with financial knowledge and skills contribute

K ATRINA S CL ASSROOM: FINANCIAL LESSONS FROM A HURRICANE INTRODUCTION OVERVIEW: THE IMPORTANCE OF BEING FINANCIALLY PREPARED During ordinary times, people with financial knowledge and skills contribute

Smart Phone. SECONDARY School Module ACTIVITY BOOKLET

ACTIVITY BOOKLET Smart Phone AFOA Canada acknowledges the generous support of the TD Bank Group in making this project possible. All rights reserved. No part of this publication may be reproduced or transmitted

ACTIVITY BOOKLET Smart Phone AFOA Canada acknowledges the generous support of the TD Bank Group in making this project possible. All rights reserved. No part of this publication may be reproduced or transmitted

Financial Matters. Optional Extension Tips: Optional Extension Tips: Below Level Differentiation. Above Level Differentiation

Below Level Differentiation Reading and Discussion Tips: When discussing the explanations to the test questions, provide students with the pre-test answer key so they can follow along. Students may use

Below Level Differentiation Reading and Discussion Tips: When discussing the explanations to the test questions, provide students with the pre-test answer key so they can follow along. Students may use

Equestrian Professional s Horse Business Challenge. Member s Support Program Workbook. Steps 1-3

Equestrian Professional s Horse Business Challenge Member s Support Program Workbook Steps 1-3 STEP 1 Get Your Books Ready for Year-end Step 1: Complete our bookkeeping checklist and get your books ready

Equestrian Professional s Horse Business Challenge Member s Support Program Workbook Steps 1-3 STEP 1 Get Your Books Ready for Year-end Step 1: Complete our bookkeeping checklist and get your books ready

Money Math for Teens. The Emergency Fund

Money Math for Teens The Emergency Fund This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation,

Money Math for Teens The Emergency Fund This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation,

Checking 101 Checking Out Checking Accounts

Checking 101 Checking Out Checking Accounts Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share

Checking 101 Checking Out Checking Accounts Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share

Planning 10/CLE - Financial Terms

Planning 10/CLE - Financial Terms These are the concepts you should be learning as opposed to exact definitions to memorize. To help with you learn the terms, students will teach some of them to the class

Planning 10/CLE - Financial Terms These are the concepts you should be learning as opposed to exact definitions to memorize. To help with you learn the terms, students will teach some of them to the class

Budgeting for Success

UNIT 1 Being Financially Responsible Topic Budgeting for Success LEARNING OBJECTIVE(S) Students will: understand the steps involved in developing a budget, including identifying sources of income and the

UNIT 1 Being Financially Responsible Topic Budgeting for Success LEARNING OBJECTIVE(S) Students will: understand the steps involved in developing a budget, including identifying sources of income and the

Bookkeepers are the accountant s eyes and ears. Few accountants actually take the time

Chapter 1 Deciphering the Basics In This Chapter Cash vs. accrual Understanding assets, liabilities, and equity Putting it all on paper Managing transactions daily Introducing the financial statements

Chapter 1 Deciphering the Basics In This Chapter Cash vs. accrual Understanding assets, liabilities, and equity Putting it all on paper Managing transactions daily Introducing the financial statements

Assignment 5-2: Use a Checking Account Transaction Page

YOU CAN DO IT! Assignment 5-2: Use a Checking Account Transaction Page Directions: Ron Ziesmer is a single 24-year-old who lives in Rochester, Minn. He recently opened a new checking account at the Rochester

YOU CAN DO IT! Assignment 5-2: Use a Checking Account Transaction Page Directions: Ron Ziesmer is a single 24-year-old who lives in Rochester, Minn. He recently opened a new checking account at the Rochester

LEARNING OUTCOMES $250 never learned how to play. KEY TERMS

SAVINGS What do other high school students know about saving? We asked high school students to describe something they really wanted and thought they had to buy, only to realize later that they wasted

SAVINGS What do other high school students know about saving? We asked high school students to describe something they really wanted and thought they had to buy, only to realize later that they wasted

Money Made Simple. The Ultimate Guide to Personal Finance

Money Made Simple The Ultimate Guide to Personal Finance Table of Contents Section 1 Back to Basics: What is Money? 5 Section 2 Clearing Out the Clutter. 17 Section 3 Where Does All My Money Go? 27 Section

Money Made Simple The Ultimate Guide to Personal Finance Table of Contents Section 1 Back to Basics: What is Money? 5 Section 2 Clearing Out the Clutter. 17 Section 3 Where Does All My Money Go? 27 Section

Work with a partner. All these words are connected to getting a mortgage. Do you know their meaning?

Warm Up Work with a partner. Are you planning to move house in the near future? Conversation Practice with a partner. Well I finally did it! I ve decided to buy a house! That s great! Have you found a

Warm Up Work with a partner. Are you planning to move house in the near future? Conversation Practice with a partner. Well I finally did it! I ve decided to buy a house! That s great! Have you found a

Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET

MONEY What You Should Know About... Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET YourMoneyCounts You probably realize that managing your money is a good idea, but you might also figure if

MONEY What You Should Know About... Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET YourMoneyCounts You probably realize that managing your money is a good idea, but you might also figure if