Volunteer Instructor Notes

|

|

|

- Veronica Morton

- 5 years ago

- Views:

Transcription

1 Volunteer Instructor Notes

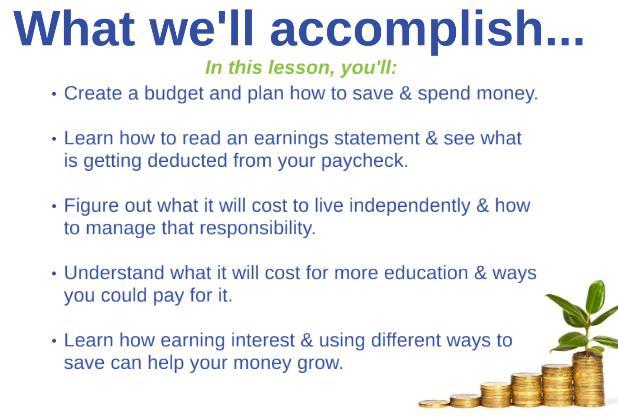

2 KEY Student Activity Important Note Go Do It Now! Call to Action 1

3 Some classrooms may not be able to play videos, the internet connection may be very slow, or may not have audio equipment. Check with the educator and test the videos before you present. Introduce Yourself (3 min) Pass out the name tents and have the students clearly write their names on them. Do your best to call students by their names throughout the lesson. Introduce yourself in a welcoming manner and make students feel comfortable. o Who are you? o What do you do? o Why do you volunteer for SecureFutures? What is SecureFutures? An organization that o delivers financial education to high school students. o provides teens with the financial education and tools needed to form good financial habits that get them ready them to live independently. Explain why financial education is important and that you will be teaching a financial education lesson to them. Set Ground Rules (2 min) Share these, or your own, expectations for student behavior: o Participate: ask and answer questions. Be curious! o Listen when others are talking. Don t interrupt. o Cell phone policy? Discuss this with the educator before presenting and request that they manage students usage according to school policy. o Ask the students if they have any other ground rules they would recommend. Discuss how to earn participation incentives (if you re offering one). Ex: raffle, candy, money. Distribute Pre-Surveys (5 min) Surveys will be completed at the beginning and end of the lessons to gauge what students know before and after participating. This is important because it allows us to measure program outcomes, effectiveness, and impact. TIP to speed this up: Hand out the surveys as students walk in or read through the questions as the students fill them out. Explain the purpose of the survey and let them know they will be taking another one at the end of the lesson. Ask students to read the Informed Assent box at the top of the survey before completing it. Completion of the survey is voluntary. If they do not want to complete it that is okay. They can still participate in the lesson. Reassure them that it is not a test. Students SHOULD NOT put their names on the surveys. Rather, they should fill out the Identifier Code box with their first and last initial, month of birth and date of birth (as two digit numbers). o For example, Cheryl Thompson who was born on March 13 th would right: C T O3 13 o They will put the same code on their post-survey, which allows us to match them up. o We cannot collect student names due to federal regulations around student privacy. If students don t know an answer, instruct them to select I don t know rather than guessing. Collect the surveys when complete. Do NOT review the answers with the students. Transition: Let s see what we are going to cover in this lesson 2

4 3

5 Discussion (2 min) Show the What does money mean to you? slide and have students answer the question by writing a one word answer on the back of their name tent. Get students talking right away by asking 4-5 students to share their answers. o Expand on student responses. Summarize why personal finance is important and share what the consequences of poor money management are. o Explain that money is necessary to support your needs and goals throughout your lifetime. Learning to manage your money well will help you to be successful in achieving your financial goals. ********************************************************************************* Review the What we ll accomplish slide. The foundation of our lesson is based on one of the most important financial concepts you will need to use to be financially successful now and throughout your life: Budgeting. Stories, Examples & Notes Share: Your own answer to the What does money mean to you? question. Transition: First, let s figure out what a budget actually is 4

6 5

7 Discussion (2 min) Ask: What is a budget? o Ask if anyone (or their family or friends) has a budget and how they use it. o Get student responses, then reveal the answers on the slide. Budgets should be used to plan how you will spend and save your money. Following your plan leads to success. ********************************************************************************* Introduce the three components of a budget: o Income o Savings o Spending Stories, Examples & Notes Share: Tell students about your budget. Transition: Let s start with income 6

8 7

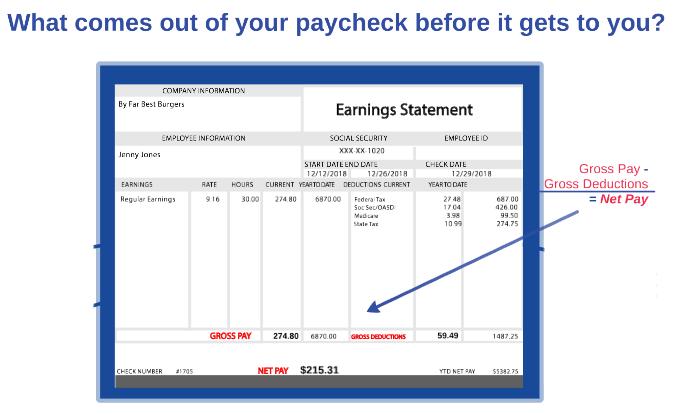

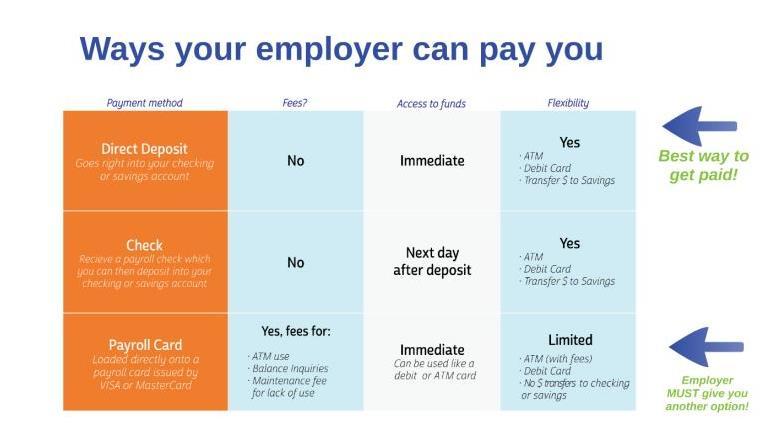

9 Discussion (2 min) Ask: Does anyone have a job? Where do you work? Ask: What s on your earnings statement? Have students to identify Jenny s o Hourly wage o Hours worked this pay period Ask: What is automatically deducted from Jenny s paycheck? o Once you get a few answers, advance the slide to highlight the different deductions. Ask: What is FICA? (Federal Insurance Contributions Act) o A percentage of your income is taken out to cover FICA taxes. o FICA has two parts: Social Security: Intended to provide you with part of your retirement income. Medicare: Provides you with health insurance when you turn age 65. Longterm saving is required to reach retirement goals. Social Security Taxes 6.2% on wages up to $118,500 For every $100 you earn, $7.65 goes Medicare Taxes 1.45% on all wages earned to the federal government for FICA. Other Deductions o Federal, state and local taxes vary depending on factors including your income and location. Generally, as your income increases, so do your taxes. o If you have federal, state, and local taxes withheld from your pay, you may not actually owe them. You must complete a tax return to see if you should get a refund. Don t let the government keep the extra money that you earned! o For most high school students, you won t owe any federal or state taxes. o When you are working full time, you may have the opportunity to have health care premiums, retirement fund contributions, and/or charitable donations automatically deducted from your paycheck. Student Workbook: Income Equation Activity Income Equation Fill-In Activity Ask: Gross Pay and Net Pay. What are they and how are they different? Once you get a few answers, advance the slide to show the equation: o Gross Pay Gross Deductions = Net Pay Have students copy this into their workbooks on page 1. Discussion Ask: How do you get paid? What are the various other ways you could get paid? Stress that direct deposit is by far the best. Encourage students to ask employer for other options if they are offered a pre-paid card. Stories, Examples & Notes Share: Tell the students how you get paid and what gets deducted from your paycheck. (1 min) (2 min) Transition: Now, let s talk about expenses. How do you spend your money? 8

10 9

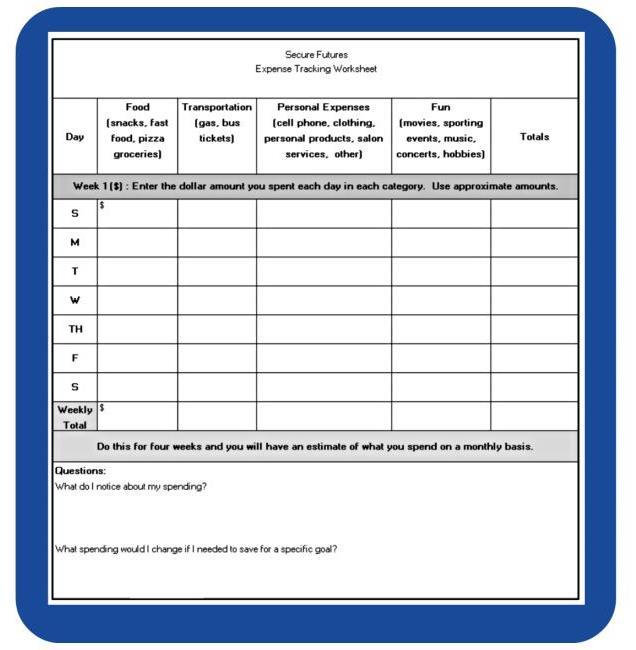

11 Student Workbook: Expense Tracking (5 min) Ask: What do you spend your money on? After getting some responses, ask if anyone keeps track of how much they spend. ********************************************************************************* Expense Tracking Activity Have students take 2 minutes and write down some of their expenses from the past week using the expense tracking worksheet on page 1 of their workbooks. o If students say that they don t have a regular income to spend, have them think about any money they may have been given and how they spent it. o If students say that they haven t spent anything in the last week, have them think about what others have spent on them. Ask several students to share their spending habits and to comment on their observations of how they spend. o What would they change if they needed to save for a goal? Summarize: Small purchases add up quickly. It s important to know how you spend your money. This is the first step to creating a budget. It s important to plan your expenses and to live within your means. Stories, Examples & Notes Share: Tell students how you track expenses and how it helps you. Transition: Which of your expenses were needs and which were wants? 10

12 11

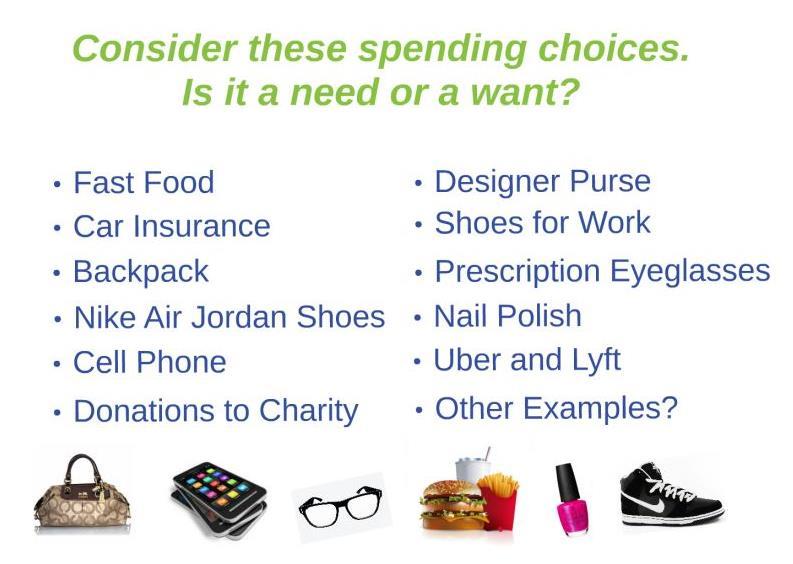

13 Discussion (5 min) Ask: What is the difference between a need and a want? o Get examples from their own spending and the previous activity. ********************************************************************************* Call on students and ask them if they view each item on the slide as a need or a want and why. Explain that opinions may differ and that everyone needs to make personal choices. ********************************************************************************* Play Video (optional) 2 min, 47 sec This video uses a real life scenario to demonstrate the thought process around determining if an expense is a need or a want. If the video doesn t work, it s okay to skip it. The concepts are covered in other slides. Summarize: The most basic definition of a need is that it is something you need in order to survive. Examples of the most basic needs are food, shelter and clothing. Most of us have many other needs in our lives also. Examples might be a car, computer, furniture, or a cell phone. The type you choose (more expensive vs less) has a big impact on your budget. A want is something you really wish you had, but you can still go through your day-to-day activities without it. Making good choices will help you save more for other short and long term needs. Stories, Examples & Notes Transition: Now, let s look at the savings side of things 12

14 13

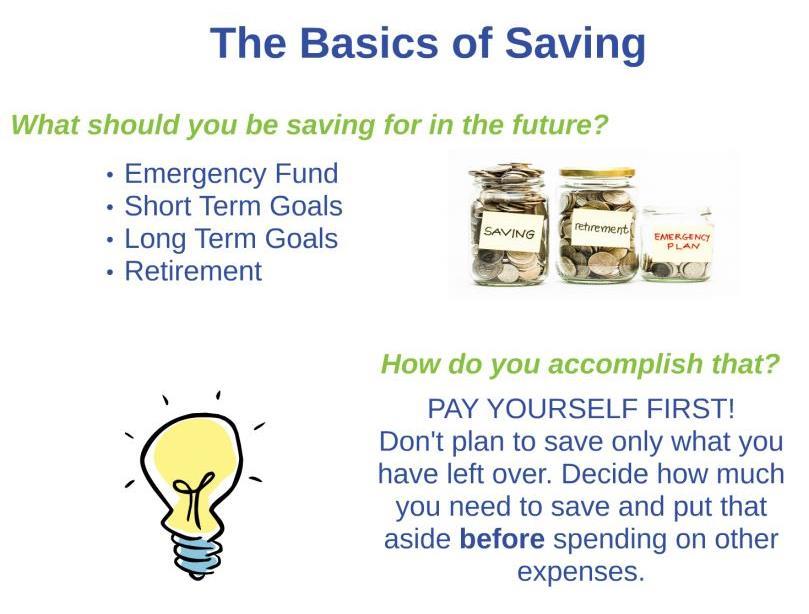

15 Discussion (2 min) Ask: What are you saving for now? Ask: How long do you think it will take for you to reach your goal? ********************************************************************************* Ask: What do you think you will be saving for in the future? Briefly review the types of savings goals that a person might have from the bulleted list. Having an emergency fund that covers 3-6 months of expenses can make all the difference when something unexpected happens (illness, injury, loss of employment, natural disaster, car accident). o If that seems too overwhelming, even a small emergency fund can help keep people above water when something unexpected happens and can help to build the habit of saving over time for things. Ask: How can you achieve those savings goals? Define Pay Yourself First : Setting aside a certain amount of money on a regular schedule, before spending on expenses, as opposed to only saving what you have left over. Emphasize that setting aside savings before spending will help you reach your goals faster than only saving what you have left over each week or month. Stories, Examples & Notes Share: Your savings goals, how you utilize pay yourself first. Transition: Now that we understand the components of a budget 14

16 15

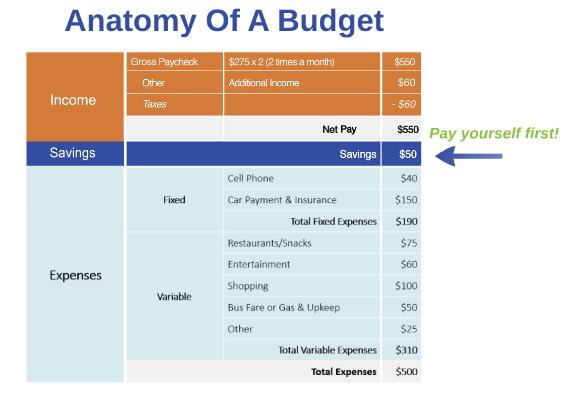

17 Discussion (2 min) Ask: Tell me again, what are the three main parts of a budget? o Income o Spending/Expenses o Savings ********************************************************************************* Income Expenses = Potential Savings o This needs to be a positive number! Ask: What is a fixed and variable expense? Fixed and Variable Expenses o A fixed expense is a recurring expense of approximately the same amount each month. o An expense is variable when you have control over when and how much you spend. Variable expenses may change from month to month. Ask: What are some additional examples of fixed and variable expenses? Advance the slide and show how the Potential Savings at the bottom becomes the first thing that you allocate your money to when you finalize your budget: PAY YOURSELF FIRST. Stories, Examples & Notes Share: Your budgeting method (written down, in a spreadsheet, on a budgeting app, etc.). Transition: Let s talk a bit more about income, since that is where all budgets start. 16

18 17

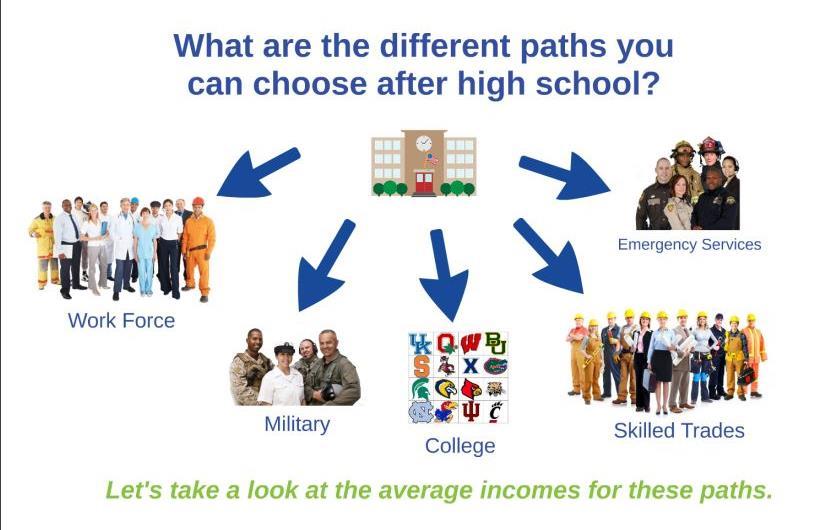

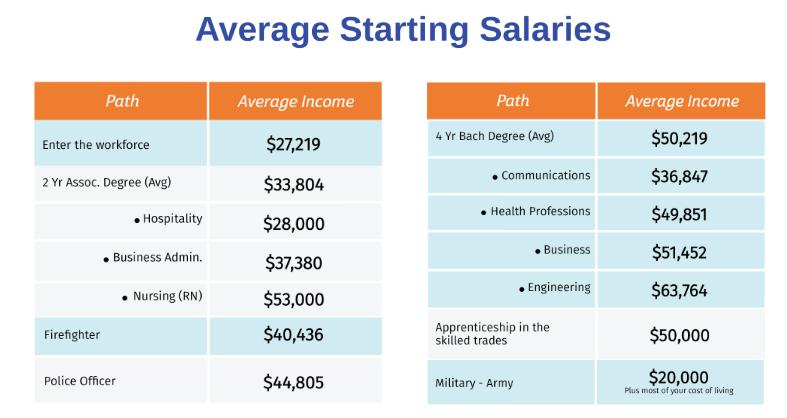

19 Discussion (3 min) Ask: What paths can you choose after high school? After getting responses, click to reveal the graphic of the paths and fill in any they missed. o Skilled Trades refer to professions that require an apprenticeship or other formal education apart from college. o Emergency Services refers to police officers, firefighters and other first responders that go through mandatory training/academies. Ask: Is there anything wrong with not going to college? Reassure students that college isn t for everyone and it isn t the only way to achieve a satisfying career. It is okay to choose a different option! Student Workbook: Average Starting Salaries (3 min) Fill in the Blank Activity Ask students to guess a few of the incomes on the chart, then click to reveal the answers. Have students fill in the salaries in their workbooks on page 2. o Source for Income Data: National Association of Colleges and Employers, Apprenticeship USA, US Army Ask: What are your observations as you compare and contrast these paths? The typical bachelor's degree recipient can expect to earn about 66% more during a 40-year working life than the typical high school graduate earns over the same period. Even if you choose not to go to college, continuing your learning and education in some way (formal or informal) will make a significant impact on your earning potential. No matter what, keep developing and improving your skills! Stories, Examples & Notes Share: How you decided on what path to take after high school. Transition: So, how much does it cost to go to college? 18

20 19

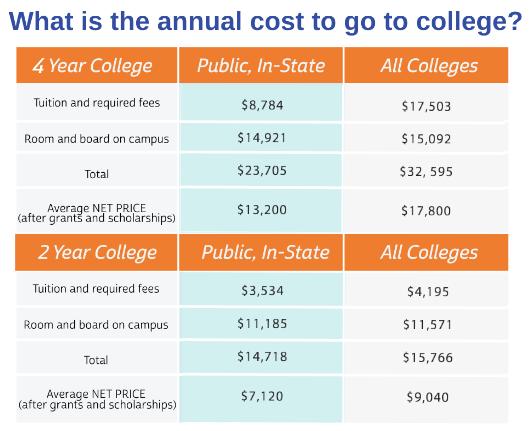

21 Student Workbook: Cost of College (3 min) Fill in the Blank Activity Ask: How much does it cost to attend a 2 year or 4 year college? After getting responses, reveal the answers. Have students copy the costs into their workbooks on page 2. These numbers seem big, but you can keep your costs low by planning ahead and saving now. Be sure to research the average NET PRICE of the schools you are interested in. There is a lot of aid out there if you put the work in to find it. o Every little bit helps, so don t pass up the small scholarship opportunities! Stories, Examples & Notes Transition: So, if you decided to go to college, where does the money come from? 20

22 21

23 Discussion (3 min) Ask: Where does the money come from to pay for college? What type of financial aid is available to go to school? After getting responses, reveal the answers on the slide. Students need to plan for how they will pay for their education (grants, scholarships, student loans, job, and savings). Money is available to help pay for college. Be sure you learn about the various ways you can apply for free money to help you pay for college. Ask the educator (before the lesson, if possible) if financial aid and FAFSA have already been covered or will be covered in depth through other lessons & activities. o If so, don t spend much time on this section. Move onto the next topic. o For urban students: Reinforcement of the need to complete the financial aid application process is very important. o For suburban/rural students: This section may be less relevant depending on how it is covered in the school and how affluent the community is. Ask: What very important form is necessary to complete to help you get student aid? o Free Application for Federal Student Aid (FAFSA): You MUST complete FAFSA to qualify for financial aid. Don t miss the application deadline! Talk to your guidance counselors at your school. Talk to your parents. Get all your documents together. Students have the above bullet points in their workbooks on page 2. You may have students who are undocumented. If they ask questions regarding FAFSA, suggest that they meet with their school counselor to determine the best path forward. o Undocumented students are not eligible for federal aid, but some universities still require them to complete the FAFSA to qualify for private funding. Summarize: Be sure you understand how much you will likely spend for tuition, room & board, books & fees, and other costs and what you may need to take out in student loans. Your goal is to make the amount of the student loan payment manageable relative to the income you will likely earn as you start your career. The decision to enter the workforce or continue your education is a personal choice. There s no right or wrong decision. Do what is best for your situation. END OF PART 1: If you are teaching a two part lesson and you still have time, continue onto the next slides and get as far as you can. Stories, Examples & Notes Share: Whether you went to college and, if so, how you paid for it. Transition: Now that we ve shown how income relates to your choices after high school, let s look at what your expenses might be once you are out on your own. 22

24 23

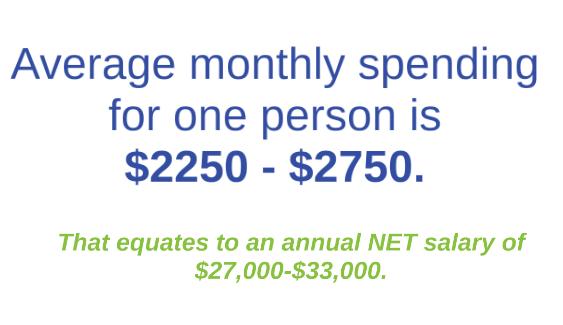

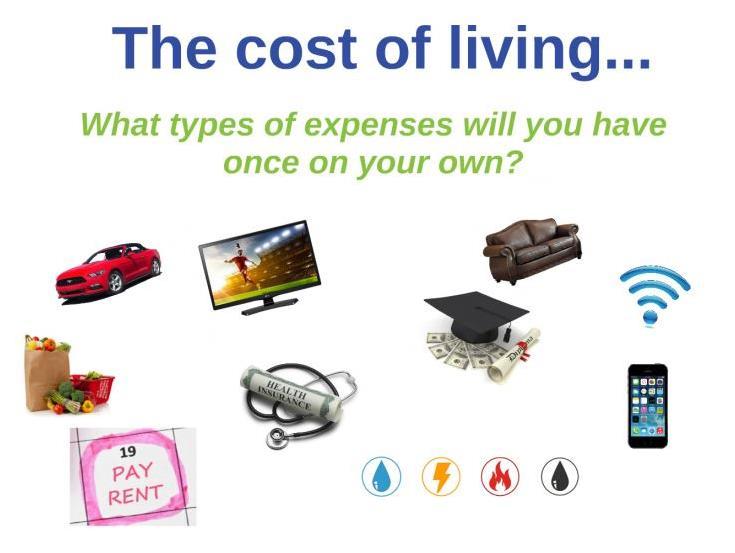

25 Discussion (5 min) START OF PART 2: If you are teaching a two part lesson, be sure to reintroduce yourself to the class before jumping into the curriculum. Ask the students what they remember from the last lesson. Ask them if they shared what they learned with anyone. If you did not make it this far in your first session, that is okay. Pick up where you left off. Ask: How much does it cost to live on your own? Once you get a few responses, reveal the next slide with the average expenses for one person. ********************************************************************************* Get reactions from students on the monthly cost of living. Advance the slide to reveal the net salary and ask students what that means. o Refer to Net Pay discussion in part 1 of this lesson. Reinforce that they would need to earn more than the net salary amount to account for deductions. ********************************************************************************* Ask: What types of expenses will you have? Once you get a few responses, advance the slide and fill in the details, as necessary. ********************************************************************************* Ask: What kind of financial goals will you want to save money for? Once you get a few responses, advance the slide and fill in the details, as necessary. o Car, House, Emergency Fund, Vacation, Starting a business, Retirement Ask: Why is it important to save for these goals? o Better odds of having money available to pay for your goal. o Less likely to borrow money to pay for your goals. o Having money for unexpected emergencies is important. (Ask for examples.) Ask: What do you think may be hard about managing money once you start to have more expenses? o Understanding the timing of my cash inflow and outflow. o Organizing how and when I pay bills. o Staying on top of making payments on time. Summarize: When you re living on your own, you will have a lot of responsibilities. Managing your finances well will be key for financial success. Stories, Examples & Notes Transition: Let s put budgeting into practice by having you complete a budget as if you are age 22 and have a full time job. 24

26 25

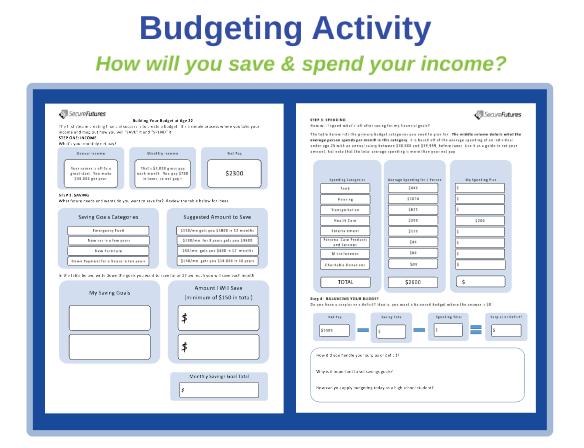

27 Student Workbook: Building Your Budget at Age 22 (12 min) Budget Activity Review the budget worksheet on page 3 and 4 of the student workbook. Review STEP 1: INCOME o Test your students recall by asking students to tell you what the $700 in taxes represents (Soc. Sec., Medicare, Federal and State taxes). Review how to complete STEP 2: SAVING o Write out your goals and assign a monthly savings amount to each. Then, add them up to get your monthly total. This needs to be at least $200. Review how to complete STEP 3: SPENDING o Review the average person s spending by category. Then, select the amount you will plan to spend based on your lifestyle. They will have to reduce some of the expenses because they only have $2300 of net income, while the average amount is over $2400 (not including savings). o Add up your spending choices to get your monthly total. Review STEP 4 BALANCING YOUR BUDGET o Do the math. You should be shooting for a ZERO surplus or deficit. o If Surplus: Review your expenses to make sure they are realistic and increase where appropriate. Increase savings. o If Deficit: Review your expenses and cut your spending in categories you could live with. Then, review your savings amounts to see if they are too high. Discussion Debrief the activity by asking students the following questions. o What did you learn about budgeting? o How do spending choices impact your ability to save? o What is likely to happen to you financially if you don t have a budget? o What other decision would you make to increase your savings? Make sure you have a PAY YOURSELF FIRST line in your budget. This is the key to not spending all of your income! Budgeting is about making choices, staying disciplined, and making a commitment to monitoring your spending so you can save money for your future goals. Advance the slide to illustrate this point. A budget isn t a plan you write and then never revisit. You have to continually compare your actual spending to your budget to ensure you are keeping on track. Budgets aren t set in stone! Adjust them as necessary. Savings potential isn t just about income. How you choose to spend your income is a key factor in saving money. Stories, Examples & Notes Share: an interesting story about budgeting that demonstrates positive practices or learning experiences. (3 min) Transition: So what happens if you ve set you budget, but you still aren t making your savings goals? 26

28 27

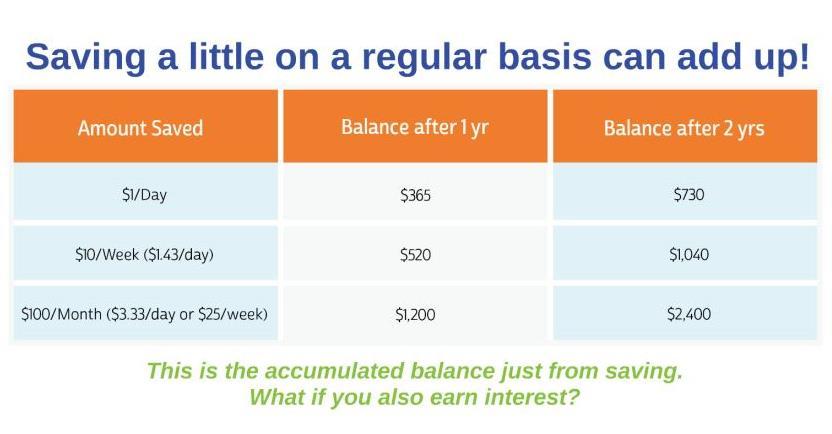

29 Discussion (3 min) Ask: What are ways you can save more or spend less? o Show the answers after getting responses. Check cashing stores are commonly found in communities where there are few traditional financial institutions that serve that area. They are most common in low-income communities and urban areas. Emphasize that students can cash or deposit their checks for free if they have an account at a bank or credit union. This will save them money in fees. o The fee is usually $5-$8 for checks under $100. Check cashing stores will be discussed at length in the upcoming Check It Out lesson. If the students will be recieving that lesson, there is no need to spend a lot of time on this. If they are not, you may want to emphasize it a bit more. ********************************************************************************* Explain how getting a part time job can really drive your savings. If there are students in the class that have jobs, ask them if having a job helps them to save. ********************************************************************************* Advance to the slide detailing the three periodic savings plans. Stress it is important to start early with some sort of plan. Stories, Examples & Notes Share: Your own stories of savings examples. Transition: Once you begin saving money it is important to give your money a chance to grow. Let s take a look at compound interest. 28

30 29

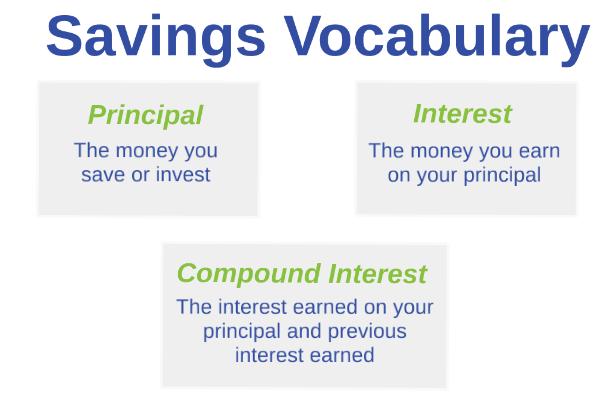

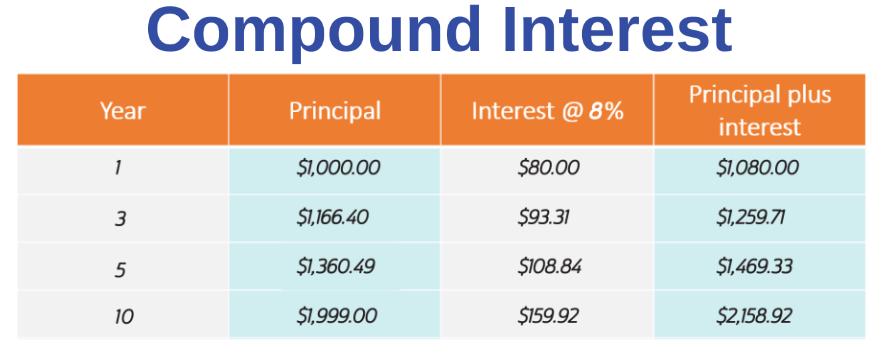

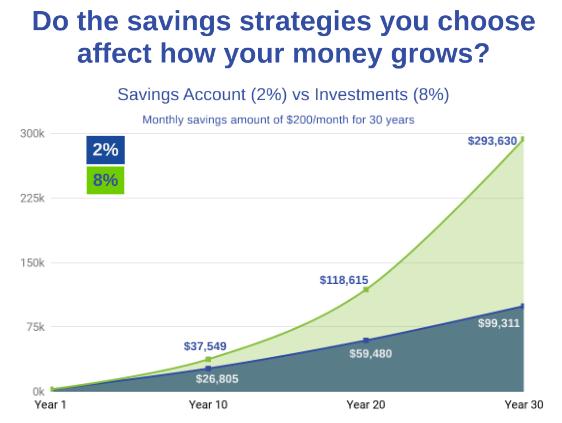

31 Discussion (3 min) Ask: What is compound interest? o Gauge how familiar the students are with this concept to determine how thorough your explanation should be. Have the students define principal and interest. Reveal the definitions after getting responses. Compound interest is interest that you earn on both the principal and the interest earned. ********************************************************************************* Review the table to illustrate how interest is continuously added to their principal and the new amount earns the interest or growth rate. o The example is set at 8% to demonstrate the power of compound interest and clarify the concept. Stories, Examples & Notes Transition: Do the savings strategies you choose affect how your money grows? 30

32 31

33 Discussion (3 min) Ask: Do the savings strategies you choose affect how your money grows? After getting responses, reveal the Systematic Saving Plan graph to illustrate the power of investing regularly and compare how your money grows at 2% vs. 8%. ********************************************************************************* Compare and contrast saving with a savings account and investing. o Stress that there is a use for both types of strategies and choosing how to take advantage of them depends on your personal goals and needs. Stress that they should all work to Pay Yourself First as they begin their careers. Stories, Examples & Notes Transition: Let s take a closer look at a couple types of investments: stocks and bonds 32

34 33

35 Discussion (4 min) Play Video (optional) 1 min, 42 sec This video describes the difference between a stock and a bond. Use your judgement to determine if these concepts are too advanced for your students. If they are, skip the video. If the video doesn t work, it s okay to skip it. ********************************************************************************* Advance to the next slide and have students name some companies that make products or provide services they use and that they think will continue to be good companies in the future. Once you get a few answers, advance the slide to show other suggestions. Share that the key to a good investment is finding companies that make products or provide services that will grow in demand. If the company is well run this will drive an increase in profits over time and will result in a rising stock price. Stories, Examples & Notes Transition: What do you think is more important when it comes to compound interest, the amount of money you save or how long you save for? 34

36 35

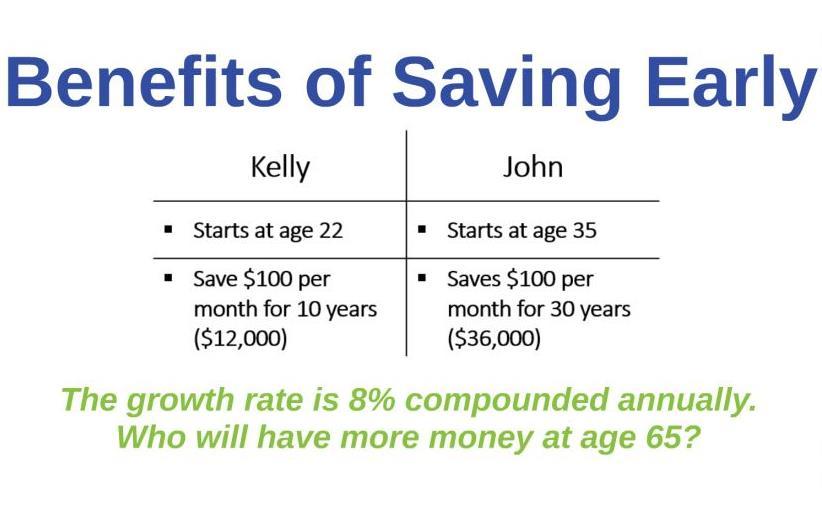

37 Discussion (3 min) Review this scenario and use it as an example of why beginning to saving early in your career is important: o Kelly learned about financial literacy in high school, so she understood the benefits of saving early. She started saving right after college. o John had huge credit card debt when he graduated from college and it took him years to pay off. He didn t know how important it was to start saving early, so he waited until he was age 35. Ask: Who will have more money at the age of 65? ********************************************************************************* After getting responses, reveal the slide with the values for each scenario illustrated. Ask: Why does Kelly end up with so much more money having only invested $12,000 vs. John s $36,000? o Stress how time is one of the most important ingredients in compounding/ growing your money. o John ended up with nearly $100,000 less than Kelly at age 65 because he started saving later. Stories, Examples & Notes Transition: Let s review the Financial Capability Checklist and see how you can put all these concepts we ve learned into action 36

38 37

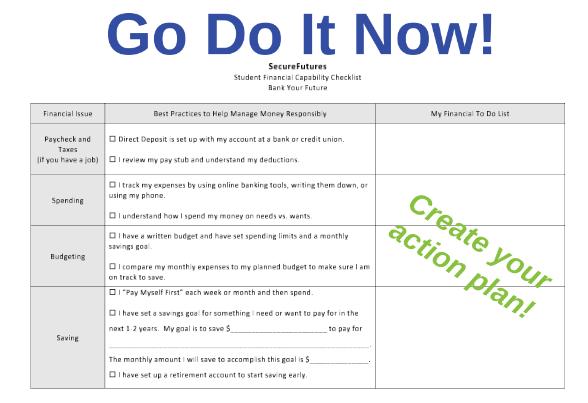

39 Student Workbook: Financial Capability Checklist (3 min) Review the Student Financial Capability Checklist on page 6 of the student workbook and explain that they can use this as a checklist for building strong financial behaviors. Challenge students to put all of the best practices in place to help manage their financial lives successfully. Ask: Which steps do you plan to take right away? Page 5 of the student workbook lists resources for the students to explore after the lesson and reinforces the components/anatomy of a budget. You do not need to review this page with the students. Distribute the Post-Survey (5 min) Have each student complete a post-survey to determine their knowledge now. Remind students how to fill out the Identifier Code and that they need to fill it out the same way they did the first time. Once students are finished, collect the surveys. If time permits, you can go over the surveys with the class. Ask students to provide the answers. The idea here is learning by repetition; the students first saw the concept in the pre-program survey, then in-depth during the presentation, then again in the post-program survey, and now in this review. Please return all surveys to SecureFutures after you have completed your entire program commitment. 38

40 SecureFutures 710 N. Plankinton Ave, Suite 310 Milwaukee, WI Updated 8/2018

Money 101 Presenter s Guide

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

This page intentionally left blank

This page intentionally left blank This page intentionally left blank. Table of Contents CreditSmart Module 2: Managing Your Money Welcome to Freddie Mac s CreditSmart Initiative... 6 Program Structure...

This page intentionally left blank This page intentionally left blank. Table of Contents CreditSmart Module 2: Managing Your Money Welcome to Freddie Mac s CreditSmart Initiative... 6 Program Structure...

RESPs and Other Ways to Save

for Indigenous Peoples Workbook 4 RESPs and Other Ways to Save Copyright 2017 ABC Life Literacy Canada First published in 2016 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada

for Indigenous Peoples Workbook 4 RESPs and Other Ways to Save Copyright 2017 ABC Life Literacy Canada First published in 2016 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada

Session Overview. Budgeting Skills Training - Instructor Notes. Thank you for teaching the Budgeting Skills Training Class :D

Session Overview Budgeting Skills Training - Instructor Notes Thank you for teaching the Budgeting Skills Training Class :D The instructor notes contain suggestions for you on how to teach this class.

Session Overview Budgeting Skills Training - Instructor Notes Thank you for teaching the Budgeting Skills Training Class :D The instructor notes contain suggestions for you on how to teach this class.

2017 DollarWise Summer Youth Contest Final Quiz Study Guide

2017 DollarWise Summer Youth Contest Final Quiz Study Guide The DollarWise Summer Youth Contest Final Exam questions are designed to test your full knowledge of the information provided in the contest.

2017 DollarWise Summer Youth Contest Final Quiz Study Guide The DollarWise Summer Youth Contest Final Exam questions are designed to test your full knowledge of the information provided in the contest.

Your money goals. Choosing a goal

Choosing a goal 01 Your money goals Next, think about a money goal that you most want to pursue towards that dream. Write down some ideas on how you could start working towards them. My money goal is:

Choosing a goal 01 Your money goals Next, think about a money goal that you most want to pursue towards that dream. Write down some ideas on how you could start working towards them. My money goal is:

yourmoney a guide to managing your credit and debt Volume 6 Life After Debt

yourmoney a guide to managing your credit and debt Volume 6 Life After Debt Call InCharge Debt Solutions today at 1-877-544-9126 or contact us at www.incharge.org Life After Debt You can do it. A life

yourmoney a guide to managing your credit and debt Volume 6 Life After Debt Call InCharge Debt Solutions today at 1-877-544-9126 or contact us at www.incharge.org Life After Debt You can do it. A life

What is credit and why does it matter to me?

Understanding Credit 1 Money Matters The BIG Idea What is credit and why does it matter to me? AGENDA Approx. 45 minutes I. Warm Up: What Do You Know About Credit? (10 minutes) II. Credit: The Good, The

Understanding Credit 1 Money Matters The BIG Idea What is credit and why does it matter to me? AGENDA Approx. 45 minutes I. Warm Up: What Do You Know About Credit? (10 minutes) II. Credit: The Good, The

LEARNING OUTCOMES $250 never learned how to play. KEY TERMS

SAVINGS What do other high school students know about saving? We asked high school students to describe something they really wanted and thought they had to buy, only to realize later that they wasted

SAVINGS What do other high school students know about saving? We asked high school students to describe something they really wanted and thought they had to buy, only to realize later that they wasted

Take control of your future. The time is. now

Take control of your future The time is now 1 Participating in your employer-sponsored retirement plan is one of the best ways to 3 save for your future. And the time to save more is now. No doubt, you

Take control of your future The time is now 1 Participating in your employer-sponsored retirement plan is one of the best ways to 3 save for your future. And the time to save more is now. No doubt, you

Workbook 2. Banking Basics

Workbook 2 Banking Basics Copyright 2017 ABC Life Literacy Canada First published in 2011 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada gratefully thanks Founding Sponsor TD

Workbook 2 Banking Basics Copyright 2017 ABC Life Literacy Canada First published in 2011 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada gratefully thanks Founding Sponsor TD

YNAB Budgeting System User Guide

Budgeting System User Guide Table of Contents Introduction... 3 User Interface... 3 Legend... 4 Features... 4 A portable budget... 4 Budget with strategy... 4 Simple management... 5 Save money faster...

Budgeting System User Guide Table of Contents Introduction... 3 User Interface... 3 Legend... 4 Features... 4 A portable budget... 4 Budget with strategy... 4 Simple management... 5 Save money faster...

Keeping Score: Why Credit Matters

Keeping Score: Why Credit Matters LESSON 6: TEACHERS GUIDE In the middle of a championship football game, keeping score is the norm. But when it comes to life, many young adults don t realize how important

Keeping Score: Why Credit Matters LESSON 6: TEACHERS GUIDE In the middle of a championship football game, keeping score is the norm. But when it comes to life, many young adults don t realize how important

SAMPLE. Chapter 1 DAVE RAMSEY

Chapter 1 DAVE RAMSEY Case Study Savings Rob and Carol were married recently and both have good jobs coming out of college. Rob was hired by The Lather Group as an assistant designer making a starting

Chapter 1 DAVE RAMSEY Case Study Savings Rob and Carol were married recently and both have good jobs coming out of college. Rob was hired by The Lather Group as an assistant designer making a starting

WHAT HAPPENS IF I DON T PAY

LESSON 7 WHAT HAPPENS IF I DON T PAY THE LESSON IN A NUTSHELL Not paying your bills has consequences. Even when you re late, pay as soon as you can. Overview...2 Activity #1: You ve Been Pre-Approved!...

LESSON 7 WHAT HAPPENS IF I DON T PAY THE LESSON IN A NUTSHELL Not paying your bills has consequences. Even when you re late, pay as soon as you can. Overview...2 Activity #1: You ve Been Pre-Approved!...

OBJECTIVES. The BIG Idea. How can I find scholarships that suit my situation, and how do I keep track of my efforts? Searching for Scholarships II

3 Financial Aid Searching for Scholarships II The BIG Idea How can I find scholarships that suit my situation, and how do I keep track of my efforts? AGENDA Approx. 45 minutes I. Warm Up (5 minutes) II.

3 Financial Aid Searching for Scholarships II The BIG Idea How can I find scholarships that suit my situation, and how do I keep track of my efforts? AGENDA Approx. 45 minutes I. Warm Up (5 minutes) II.

Workbook 3. Borrowing Money

Workbook 3 Borrowing Money Copyright 2019 ABC Life Literacy Canada First published in 2011 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada gratefully thanks Founding Sponsor TD

Workbook 3 Borrowing Money Copyright 2019 ABC Life Literacy Canada First published in 2011 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada gratefully thanks Founding Sponsor TD

Money Math for Teens. The Emergency Fund

Money Math for Teens The Emergency Fund This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation,

Money Math for Teens The Emergency Fund This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation,

Student Guide: RWC Simulation Lab. Free Market Educational Services: RWC Curriculum

Free Market Educational Services: RWC Curriculum Student Guide: RWC Simulation Lab Table of Contents Getting Started... 4 Preferred Browsers... 4 Register for an Account:... 4 Course Key:... 4 The Student

Free Market Educational Services: RWC Curriculum Student Guide: RWC Simulation Lab Table of Contents Getting Started... 4 Preferred Browsers... 4 Register for an Account:... 4 Course Key:... 4 The Student

Want more background and training tips?

Learner Outcomes Outcome #1: Participants will be able to explain what credit is. Outcome #2: Participants will be able to explain why using a credit card is a form of borrowing. Outcome #3: Participants

Learner Outcomes Outcome #1: Participants will be able to explain what credit is. Outcome #2: Participants will be able to explain why using a credit card is a form of borrowing. Outcome #3: Participants

FINANCIAL FOUNDATIONS

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program BUDGETING Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program BUDGETING Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

YOUR GUIDE TO THE NEXT BIG TALK: THE MONEY TALK

YOUR GUIDE TO THE NEXT BIG TALK: Having the money talk with your teen is as important as speaking to them about any other life challenges. A healthy relationship with money starts at an early age. This

YOUR GUIDE TO THE NEXT BIG TALK: Having the money talk with your teen is as important as speaking to them about any other life challenges. A healthy relationship with money starts at an early age. This

Managing Money Together. A Workbook for Couples

Managing Money Together A Workbook for Couples Introduction Growing up, my parents argued about money. It wasn t a lot now that I look back, but I do remember thinking that I never wanted to do that. So,

Managing Money Together A Workbook for Couples Introduction Growing up, my parents argued about money. It wasn t a lot now that I look back, but I do remember thinking that I never wanted to do that. So,

Retirement Planning & Savings

For many people, retirement is one of the rewards for a long and successful career or a lifetime of hard work. Retirees do many things with their time: volunteer, work on hobbies or other interests that

For many people, retirement is one of the rewards for a long and successful career or a lifetime of hard work. Retirees do many things with their time: volunteer, work on hobbies or other interests that

Lesson Module 1: The Fundamentals of Net Worth

Lesson Module 1: The Fundamentals of Net Worth Module 1 Overview The entire game of football is based on a few basic skills: blocking, tackling, passing and running. To be a successful football player,

Lesson Module 1: The Fundamentals of Net Worth Module 1 Overview The entire game of football is based on a few basic skills: blocking, tackling, passing and running. To be a successful football player,

Table of Contents. Money Smart for Adults Curriculum Page 2 of 45

Table of Contents Getting Started... 3 Module 5: Pay Yourself First Layering Table... 4 Icons Guide... 5 Module Overview... 6 Checking In... 7 Pre-Test... 9 Overview of Saving... 11 Savings Tips... 12

Table of Contents Getting Started... 3 Module 5: Pay Yourself First Layering Table... 4 Icons Guide... 5 Module Overview... 6 Checking In... 7 Pre-Test... 9 Overview of Saving... 11 Savings Tips... 12

YOU ARE NOT ALONE Hello, my name is <name> and I m <title>.

So I know why you re here: I bet you ve got some questions about your money: what to do with it, how to make the most of it and how to hopefully get more of it. You ve got questions and the good news is

So I know why you re here: I bet you ve got some questions about your money: what to do with it, how to make the most of it and how to hopefully get more of it. You ve got questions and the good news is

This page intentionally left blank.

This page intentionally left blank. CreditSmart Module 1: Your Credit and Why It Is Important Table of Contents Welcome to Freddie Mac s CreditSmart Initiative... 5 Program Structure... 5 Using the Instructor

This page intentionally left blank. CreditSmart Module 1: Your Credit and Why It Is Important Table of Contents Welcome to Freddie Mac s CreditSmart Initiative... 5 Program Structure... 5 Using the Instructor

Full file at

2 MONEY MANAGEMENT STRATEGY: FINANCIAL STATEMENTS AND BUDGETING CHAPTER OVERVIEW Successful money management is based on organized financial records, accurate personal financial statements, and effective

2 MONEY MANAGEMENT STRATEGY: FINANCIAL STATEMENTS AND BUDGETING CHAPTER OVERVIEW Successful money management is based on organized financial records, accurate personal financial statements, and effective

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN 1. This free report will show you the tax benefits of owning your own home as well as: 2. How to get pre-approved

STOP RENTING AND OWN A HOME FOR LESS THAN YOU ARE PAYING IN RENT WITH VERY LITTLE MONEY DOWN 1. This free report will show you the tax benefits of owning your own home as well as: 2. How to get pre-approved

Civics and Economics Personal Budget Project

Civics and Economics Personal Budget Project Objective The Economics/Budget Project is designed to assist students in considering your financial future. The project consists of various real world situations/decisions

Civics and Economics Personal Budget Project Objective The Economics/Budget Project is designed to assist students in considering your financial future. The project consists of various real world situations/decisions

LEARNING TASKS These tasks match pages in Student Guide 1.

STUDENT LEARNING PLAN Lesson 1-4: Spending Plan OVERVIEW You've analyzed what you've been spending money on and set some SMART goals to strive for. Now, the rubber meets the road and it's time to start

STUDENT LEARNING PLAN Lesson 1-4: Spending Plan OVERVIEW You've analyzed what you've been spending money on and set some SMART goals to strive for. Now, the rubber meets the road and it's time to start

Budgeting: Making the Most of Your Money

? Did You Know? Almost 60% of millionaires use a budget to manage their money. The Millionaire Next Door: The Surprising Secrets of America s Wealthy. In this unit, you will: Examine your spending habits

? Did You Know? Almost 60% of millionaires use a budget to manage their money. The Millionaire Next Door: The Surprising Secrets of America s Wealthy. In this unit, you will: Examine your spending habits

Budgeting: 101 Financial Literacy Program

Program Schedule Budgeting: 101 Financial Literacy Program Introduction: 5 minutes Introduce yourself - Name, company, mention that you are a CPA. Ask the students - What does CPA stand for? Briefly explain

Program Schedule Budgeting: 101 Financial Literacy Program Introduction: 5 minutes Introduce yourself - Name, company, mention that you are a CPA. Ask the students - What does CPA stand for? Briefly explain

Budgeting for Success

UNIT 1 Being Financially Responsible Topic Budgeting for Success LEARNING OBJECTIVE(S) Students will: understand the steps involved in developing a budget, including identifying sources of income and the

UNIT 1 Being Financially Responsible Topic Budgeting for Success LEARNING OBJECTIVE(S) Students will: understand the steps involved in developing a budget, including identifying sources of income and the

ECO155L19.doc 1 OKAY SO WHAT WE WANT TO DO IS WE WANT TO DISTINGUISH BETWEEN NOMINAL AND REAL GROSS DOMESTIC PRODUCT. WE SORT OF

ECO155L19.doc 1 OKAY SO WHAT WE WANT TO DO IS WE WANT TO DISTINGUISH BETWEEN NOMINAL AND REAL GROSS DOMESTIC PRODUCT. WE SORT OF GOT A LITTLE BIT OF A MATHEMATICAL CALCULATION TO GO THROUGH HERE. THESE

ECO155L19.doc 1 OKAY SO WHAT WE WANT TO DO IS WE WANT TO DISTINGUISH BETWEEN NOMINAL AND REAL GROSS DOMESTIC PRODUCT. WE SORT OF GOT A LITTLE BIT OF A MATHEMATICAL CALCULATION TO GO THROUGH HERE. THESE

Script to follow the Orientation Presentation

Orientation Presentation Script to follow the Orientation Presentation January 23, 2018 Finastra January 23, 201823 January 2018 Orientation Presentation Script to follow the Orientation Presentation 1

Orientation Presentation Script to follow the Orientation Presentation January 23, 2018 Finastra January 23, 201823 January 2018 Orientation Presentation Script to follow the Orientation Presentation 1

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

P.Y.F. Participant s Guide

P.Y.F. Participant s Guide 1 Table of Contents Welcome Pre-Test Pay Yourself First Saving for Purchases Emergency Savings Retirement Savings Daily Decisions Matter Savings Tips How Your Money Grows (Simple

P.Y.F. Participant s Guide 1 Table of Contents Welcome Pre-Test Pay Yourself First Saving for Purchases Emergency Savings Retirement Savings Daily Decisions Matter Savings Tips How Your Money Grows (Simple

How to Bank and Save In Canada

for Newcomers and New Canadians Workbook 1 How to Bank and Save In Canada Welcome! We made this workshop for newcomers to Canada. Knowing more about how banking works here can help you settle in faster,

for Newcomers and New Canadians Workbook 1 How to Bank and Save In Canada Welcome! We made this workshop for newcomers to Canada. Knowing more about how banking works here can help you settle in faster,

Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET

MONEY What You Should Know About... Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET YourMoneyCounts You probably realize that managing your money is a good idea, but you might also figure if

MONEY What You Should Know About... Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET YourMoneyCounts You probably realize that managing your money is a good idea, but you might also figure if

Financial Literacy. Budgeting

Financial Literacy Budgeting ACTIVITY SHEET 3-1 The B word budget 1 What do you think about when you hear the word budget? What words or feelings come to mind? Write down any other ideas the group came

Financial Literacy Budgeting ACTIVITY SHEET 3-1 The B word budget 1 What do you think about when you hear the word budget? What words or feelings come to mind? Write down any other ideas the group came

The Problems With Reverse Mortgages

The Problems With Reverse Mortgages On Monday, we discussed the nuts and bolts of reverse mortgages. On Wednesday, Josh Mettle went into more detail with some of the creative uses for a reverse mortgage.

The Problems With Reverse Mortgages On Monday, we discussed the nuts and bolts of reverse mortgages. On Wednesday, Josh Mettle went into more detail with some of the creative uses for a reverse mortgage.

Presented by Dr. Rebecca Neumann for Academic Staff

April 21, 2017 Presented by Dr. Rebecca Neumann for Academic Staff University of Wisconsin Milwaukee Mind your Money, Mind your Future Goals for today: Basic money management skills Tracking expenses Budgeting

April 21, 2017 Presented by Dr. Rebecca Neumann for Academic Staff University of Wisconsin Milwaukee Mind your Money, Mind your Future Goals for today: Basic money management skills Tracking expenses Budgeting

Club Accounts - David Wilson Question 6.

Club Accounts - David Wilson. 2011 Question 6. Anyone familiar with Farm Accounts or Service Firms (notes for both topics are back on the webpage you found this on), will have no trouble with Club Accounts.

Club Accounts - David Wilson. 2011 Question 6. Anyone familiar with Farm Accounts or Service Firms (notes for both topics are back on the webpage you found this on), will have no trouble with Club Accounts.

PROJECT PRO$PER. The Basics of Building Wealth

PROJECT PRO$PER PRESENTS The Basics of Building Wealth Investing and Retirement Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo's Hands on Banking The Hands

PROJECT PRO$PER PRESENTS The Basics of Building Wealth Investing and Retirement Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo's Hands on Banking The Hands

Lesson 4: Back to School Part 4: Saving

Lesson 4: Back to School Part 4: Saving Lesson Description In this five-part lesson, students look at the financial lessons that a teen and her family learned while they were displaced from their home

Lesson 4: Back to School Part 4: Saving Lesson Description In this five-part lesson, students look at the financial lessons that a teen and her family learned while they were displaced from their home

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC. Financial Literacy Workbook, Grades 9-12

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC Financial Literacy Workbook, Grades 9-12 FINANCIAL PLANNING Financial planning is about defining and following a set of steps in

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC Financial Literacy Workbook, Grades 9-12 FINANCIAL PLANNING Financial planning is about defining and following a set of steps in

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY Contents Perceptions About Saving for Retirement & College Education Respondent College Experience Family Financial Profile Saving for College Paying

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY Contents Perceptions About Saving for Retirement & College Education Respondent College Experience Family Financial Profile Saving for College Paying

TEACHING UNIT. Grade Level: Grade 10 Recommended Curriculum Area: Language Arts Other Relevant Curriculum Area(s): Mathematics

: Mathematics") TEACHING UNIT General Topic: Borrowing and Using Credit Unit Title: Managing Debt and Credit Grade Level: Grade 10 Recommended Curriculum Area: Language Arts Other Relevant Curriculum Area(s): Mathematics

TEACHING UNIT General Topic: Borrowing and Using Credit Unit Title: Managing Debt and Credit Grade Level: Grade 10 Recommended Curriculum Area: Language Arts Other Relevant Curriculum Area(s): Mathematics

The Mortgage Guide. Helping you find the right mortgage for you. Brought to you by. V a

The Mortgage Guide Helping you find the right mortgage for you Brought to you by V0050713a Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us

The Mortgage Guide Helping you find the right mortgage for you Brought to you by V0050713a Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us

MODULE 1 // SAVING AMATEUR: AGES 11-14

MODULE 1 // SAVING AMATEUR: AGES 11-14 MODULE 1 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial management issues they

MODULE 1 // SAVING AMATEUR: AGES 11-14 MODULE 1 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial management issues they

Understanding Your Paycheck

Understanding Your Paycheck Instructors Guide Today s Session: This session is flexible in length, from 35 to 65 minutes. It is intended for adults with diverse abilities who want to understand the various

Understanding Your Paycheck Instructors Guide Today s Session: This session is flexible in length, from 35 to 65 minutes. It is intended for adults with diverse abilities who want to understand the various

Checks and Balances TV: America s #1 Source for Balanced Financial Advice

The TruTh about SOCIAL SECURITY Social Security: a simple idea that s grown out of control. Social Security is the widely known retirement safety net for the American Workforce. When it began in 1935,

The TruTh about SOCIAL SECURITY Social Security: a simple idea that s grown out of control. Social Security is the widely known retirement safety net for the American Workforce. When it began in 1935,

FINANCIAL FOUNDATIONS

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program CREDIT Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program CREDIT Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

Part 1: Situation and Savings (35 minutes)

") Volunteer Guide Introduction: Do you remember the first big decision you faced in using money? Were you prepared to make a good choice? How we manage our income really affects our lives and our families.

Volunteer Guide Introduction: Do you remember the first big decision you faced in using money? Were you prepared to make a good choice? How we manage our income really affects our lives and our families.

MODULE 1 // SAVING HALL OF FAME: AGES 18+

MODULE 1 // SAVING HALL OF FAME: AGES 18+ MODULE 1 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial management issues they

MODULE 1 // SAVING HALL OF FAME: AGES 18+ MODULE 1 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial management issues they

TEACHER LESSON PLAN Lesson 2-4: Rights and Responsibilities OVERVIEW LEARNING OUTCOMES PREPARATION WHAT YOU WILL NEED NOTES:

TEACHER LESSON PLAN Lesson 2-4: Rights and Responsibilities OVERVIEW You probably don t think of a loan or credit-card application as a contract, but it is. By signing on the dotted line, you re entering

TEACHER LESSON PLAN Lesson 2-4: Rights and Responsibilities OVERVIEW You probably don t think of a loan or credit-card application as a contract, but it is. By signing on the dotted line, you re entering

How to Strategically Manage Your Debt

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Retirement. on the Brain. A Woman s Guide to a Financially Secure Future - Workbook

Retirement on the Brain A Woman s Guide to a Financially Secure Future - Workbook Secure your future starting now Women face unique challenges when it comes to saving and investing for the future. We

Retirement on the Brain A Woman s Guide to a Financially Secure Future - Workbook Secure your future starting now Women face unique challenges when it comes to saving and investing for the future. We

The Right Attitude. Preparing for your retirement: Workbook One

The Right Attitude Preparing for your retirement: Workbook One About Retirement Planning Retirement is something that is often eagerly anticipated for years before it actually occurs. In the years preceding

The Right Attitude Preparing for your retirement: Workbook One About Retirement Planning Retirement is something that is often eagerly anticipated for years before it actually occurs. In the years preceding

CreditSmart Module 10: Planning for Your Future

Table of Contents CreditSmart Module 10: Planning for Your Future Welcome to Freddie Mac s CreditSmart Initiative... 4 Program Structure... 4 Using the Instructor Guides... 5 Lesson Concepts and Icons...

Table of Contents CreditSmart Module 10: Planning for Your Future Welcome to Freddie Mac s CreditSmart Initiative... 4 Program Structure... 4 Using the Instructor Guides... 5 Lesson Concepts and Icons...

Ric was named Best Talk Show Host in 1993 (AIR Awards) and continues to host weekly radio and television shows in Washington, D.C.

and continues to host weekly radio and television shows in Washington, D.C.") Wi$e Up Teleconference Call Budget to Save August 31, 2006 Speaker 2 Ric Edelman Jane Walstedt: Now, I'm going to turn the program over to Gail Patterson, who is part of the Women s Bureau team that plans

Wi$e Up Teleconference Call Budget to Save August 31, 2006 Speaker 2 Ric Edelman Jane Walstedt: Now, I'm going to turn the program over to Gail Patterson, who is part of the Women s Bureau team that plans

You have many choices when it comes to money and investing. Only one was created with you in mind. A Structured Settlement can provide hope and a

You have many choices when it comes to money and investing. Only one was created with you in mind. A Structured Settlement can provide hope and a secure future. Tax-Free. Guaranteed Benefits. Custom-Designed.

You have many choices when it comes to money and investing. Only one was created with you in mind. A Structured Settlement can provide hope and a secure future. Tax-Free. Guaranteed Benefits. Custom-Designed.

Well Being, Well Done

Well Being, Well Done A Project of the Sudden Money Institute Well Being: A profound state of being found at the intersection of Life and Money. You can have it before you have accumulated large amounts

Well Being, Well Done A Project of the Sudden Money Institute Well Being: A profound state of being found at the intersection of Life and Money. You can have it before you have accumulated large amounts

Module 3 - Budgeting ACTIVITY SHEET 3-1. Write down any other ideas the group came up with, especially ideas that fit your situation.

ParticipantHandbook ACTIVITY SHEET 3-1 The B word budget 1 Write down any other ideas the group came up with, especially ideas that fit your situation. What is a budget? Why budget? A way to keep track

ParticipantHandbook ACTIVITY SHEET 3-1 The B word budget 1 Write down any other ideas the group came up with, especially ideas that fit your situation. What is a budget? Why budget? A way to keep track

Take it to the Bank: Buying Power. Instructor s Manual

Take it to the Bank: Buying Power Instructor s Manual Start the activity with introductions. Tell the girls your name. Put on a name tag. Activity 1: Compare Costs and Options 20 minutes Let each girl

Take it to the Bank: Buying Power Instructor s Manual Start the activity with introductions. Tell the girls your name. Put on a name tag. Activity 1: Compare Costs and Options 20 minutes Let each girl

The Mortgage Guide Helping you find the right mortgage for you

The Mortgage Guide Helping you find the right mortgage for you Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever make. And it can be stressful.

The Mortgage Guide Helping you find the right mortgage for you Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever make. And it can be stressful.

PROTECTING YOUR ASSETS

PROTECTING YOUR ASSETS Always encourage your students to take notes. Also, remember to leave yourself 5 minutes before the end of class to go over the post-test and collect them! Making a connection to

PROTECTING YOUR ASSETS Always encourage your students to take notes. Also, remember to leave yourself 5 minutes before the end of class to go over the post-test and collect them! Making a connection to

Part Two: The Details

Table of ConTenTs INTRODUCTION...1 Part One: The Basics CHAPTER 1 The Money for LIFE Five-Step System...11 CHAPTER 2 Three Ways to Generate Lifetime Retirement Income...21 CHAPTER 3 CHAPTER 4 CHAPTER 5

Table of ConTenTs INTRODUCTION...1 Part One: The Basics CHAPTER 1 The Money for LIFE Five-Step System...11 CHAPTER 2 Three Ways to Generate Lifetime Retirement Income...21 CHAPTER 3 CHAPTER 4 CHAPTER 5

BINARY OPTIONS: A SMARTER WAY TO TRADE THE WORLD'S MARKETS NADEX.COM

BINARY OPTIONS: A SMARTER WAY TO TRADE THE WORLD'S MARKETS NADEX.COM CONTENTS To Be or Not To Be? That s a Binary Question Who Sets a Binary Option's Price? And How? Price Reflects Probability Actually,

BINARY OPTIONS: A SMARTER WAY TO TRADE THE WORLD'S MARKETS NADEX.COM CONTENTS To Be or Not To Be? That s a Binary Question Who Sets a Binary Option's Price? And How? Price Reflects Probability Actually,

budget fixed expense flexible expense

How do I make my income cover my expenses? Chapter 24 Key Terms budget fixed expense flexible expense Chapter Objectives After studying this chapter, you will be able to identify sources of income. list

How do I make my income cover my expenses? Chapter 24 Key Terms budget fixed expense flexible expense Chapter Objectives After studying this chapter, you will be able to identify sources of income. list

YOUR MONEY, YOUR GOALS. A financial empowerment toolkit

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

Learner Outcomes. Target Audience. Materials. Timing. Want more background and training tips? Invest Well The Basics of Investments. Teens.

Learner Outcomes Outcome #1: Participants will be able to identify what an investment is. Outcome #2: Participants will be able to explain how investing helps people meet financial goals. Outcome #3: Participants

Learner Outcomes Outcome #1: Participants will be able to identify what an investment is. Outcome #2: Participants will be able to explain how investing helps people meet financial goals. Outcome #3: Participants

HOW TO SET UP DENTAL INSURANCE PLANS IN DENTRIX FOR TRACKING INDIVIDUAL PLAN PERFORMANCE TO SEE THE WINNERS AND THE LOSERS

HOW TO SET UP DENTAL INSURANCE PLANS IN DENTRIX FOR TRACKING INDIVIDUAL PLAN PERFORMANCE TO SEE THE WINNERS AND THE LOSERS JILL NESBITT PRACTICE ADMINISTRATOR & DENTAL CONSULTANT MISSION 77, LLC 615-970-8405

HOW TO SET UP DENTAL INSURANCE PLANS IN DENTRIX FOR TRACKING INDIVIDUAL PLAN PERFORMANCE TO SEE THE WINNERS AND THE LOSERS JILL NESBITT PRACTICE ADMINISTRATOR & DENTAL CONSULTANT MISSION 77, LLC 615-970-8405

Building Your Future. with the Kohl s 401(k) Savings Plan. Kohl s supports planning for your financial future with increased confidence.

Savings Plan. Kohl s supports planning for your financial future with increased confidence.") Building Your Future with the Kohl s 401(k) Savings Plan Kohl s supports planning for your financial future with increased confidence. FINANCIAL Me? Save for Retirement? YES. THE MOST IMPORTANT REASON

Building Your Future with the Kohl s 401(k) Savings Plan Kohl s supports planning for your financial future with increased confidence. FINANCIAL Me? Save for Retirement? YES. THE MOST IMPORTANT REASON

VOLUNTEER TRAINING INFORMATION

VOLUNTEER TRAINING INFORMATION VOLUNTEER TRAINING Volunteers generally feel more comfortable in staffing a table if they have been provided with advance information about the concept and have time to read

VOLUNTEER TRAINING INFORMATION VOLUNTEER TRAINING Volunteers generally feel more comfortable in staffing a table if they have been provided with advance information about the concept and have time to read

Tanya s Money Problem A Reading A Z Level U Leveled Book Word Count: 1,776

Tanya s Money Problem A Reading A Z Level U Leveled Book Word Count: 1,776 LEVELED BOOK U Tanya s Money Problem Written by Ned Jensen Illustrated by Arthur Lin Visit www.readinga-z.com for thousands of

Tanya s Money Problem A Reading A Z Level U Leveled Book Word Count: 1,776 LEVELED BOOK U Tanya s Money Problem Written by Ned Jensen Illustrated by Arthur Lin Visit www.readinga-z.com for thousands of

Money Management Curriculum

Module 2: Loans and Credit Cards Money Management Curriculum Module 2: Loans and Credit Cards Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom, Associate Director of Tribal Extension,

Module 2: Loans and Credit Cards Money Management Curriculum Module 2: Loans and Credit Cards Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom, Associate Director of Tribal Extension,

Helping your loved ones. Simple steps to providing for your family and friends

Helping your loved ones Simple steps to providing for your family and friends Contents 01 How can I take control of who gets what? 02 Inheritance Tax 05 Do you know how much you re worth? 07 Making lifetime

Helping your loved ones Simple steps to providing for your family and friends Contents 01 How can I take control of who gets what? 02 Inheritance Tax 05 Do you know how much you re worth? 07 Making lifetime

FINANCIAL LESSONS FROM A HURRICANE

K ATRINA S CL ASSROOM: FINANCIAL LESSONS FROM A HURRICANE LESSON 1: KATRINA STRIKES This introductory video sets the scene for Hurricane Katrina by portraying the storm striking, showing some of the devastation

K ATRINA S CL ASSROOM: FINANCIAL LESSONS FROM A HURRICANE LESSON 1: KATRINA STRIKES This introductory video sets the scene for Hurricane Katrina by portraying the storm striking, showing some of the devastation

BUDGETING SESSION OBJECTIVES SUBJECT INDEX

BUDGETING SESSION OBJECTIVES 8 Budgeting is the foundation of personal financial planning. Budgeting allows us to manage our money by tracking our income and expenses. Since every person is different,

BUDGETING SESSION OBJECTIVES 8 Budgeting is the foundation of personal financial planning. Budgeting allows us to manage our money by tracking our income and expenses. Since every person is different,

A GUIDE TO PREPARING FOR RETIREMENT

A GUIDE TO PREPARING FOR RETIREMENT MaineSaves A Guide to Preparing for Retirement MaineSaves, the State of Maine s voluntary retirement savings plan, is designed to help you move forward on your journey

A GUIDE TO PREPARING FOR RETIREMENT MaineSaves A Guide to Preparing for Retirement MaineSaves, the State of Maine s voluntary retirement savings plan, is designed to help you move forward on your journey

paying off student loans

paying off student loans PAYING OFF STUDENT LOANS Student loans are a national crisis impacting millions of people. The class of 2016 borrowed an average of $37,172 in student loans.* Total student loan

paying off student loans PAYING OFF STUDENT LOANS Student loans are a national crisis impacting millions of people. The class of 2016 borrowed an average of $37,172 in student loans.* Total student loan

A better approach to Roth conversions

A better approach to Roth conversions Jason Method: One beneficial aspect of our current retirement system is that it allows you to choose when to pay taxes on at least some of the money you ve saved.

A better approach to Roth conversions Jason Method: One beneficial aspect of our current retirement system is that it allows you to choose when to pay taxes on at least some of the money you ve saved.

How Do You Calculate Cash Flow in Real Life for a Real Company?

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

Principal Funds. Women and Wealth. Invest in yourself. You deserve it. A step-by-step guide to help you achieve your financial goals.

Principal Funds Women and Wealth Invest in yourself. You deserve it. A step-by-step guide to help you achieve your financial goals. Take Time for You As a woman, you probably have a lot of responsibilities.

Principal Funds Women and Wealth Invest in yourself. You deserve it. A step-by-step guide to help you achieve your financial goals. Take Time for You As a woman, you probably have a lot of responsibilities.

Life Insurance Buyer s Guide

Contents What type of insurance should I buy? How much insurance should I buy? How long should my term life insurance last? How do I compare life insurance quotes? How do I compare quotes from difference

Contents What type of insurance should I buy? How much insurance should I buy? How long should my term life insurance last? How do I compare life insurance quotes? How do I compare quotes from difference

ABOUT FREEDOM CLUB ABOUT DR. TONY

1 ABOUT FREEDOM CLUB The Freedom Club is a mentoring and coaching program designed to guide you along the path to Financial Freedom. The Freedom Club is also a place where like-minded people can associate

1 ABOUT FREEDOM CLUB The Freedom Club is a mentoring and coaching program designed to guide you along the path to Financial Freedom. The Freedom Club is also a place where like-minded people can associate

Using Credit. Grade Five. Overview. Lesson Objectives. Prerequisite Skills. Materials List

Grade Five Using Credit Overview Students share several chapters from the book Not for a Billion Gazillion Dollars, by Paula Danzinger, to learn about earning money, saving, credit, and debt. Students

Grade Five Using Credit Overview Students share several chapters from the book Not for a Billion Gazillion Dollars, by Paula Danzinger, to learn about earning money, saving, credit, and debt. Students

Banks and Paychecks Role Play

Banks and Paychecks Role Play Part I: Getting Paid Roles: Employer, Employee Employer: Thank you for your hard work for the last 2 weeks. Here is your paycheck. The Employer hands the sample paycheck to

Banks and Paychecks Role Play Part I: Getting Paid Roles: Employer, Employee Employer: Thank you for your hard work for the last 2 weeks. Here is your paycheck. The Employer hands the sample paycheck to

Getting Ready For Tax Season

Getting Ready For Tax Season Topics of Discussion Filing requirements Process overview Timing Records verification Cost basis reporting changes Scope of bivio program Tax loss harvesting Things to do before

Getting Ready For Tax Season Topics of Discussion Filing requirements Process overview Timing Records verification Cost basis reporting changes Scope of bivio program Tax loss harvesting Things to do before

This Week s Timeline

RETIREMENT AND COLLEGE PLANNING This Week s Timeline Pre-Video Discussion... 10 minutes Watch Recap... 5 minutes Victories.... 5 minutes Small Group Discussion (including supplemental questions)....15

RETIREMENT AND COLLEGE PLANNING This Week s Timeline Pre-Video Discussion... 10 minutes Watch Recap... 5 minutes Victories.... 5 minutes Small Group Discussion (including supplemental questions)....15

Introduction To The Income Statement

Introduction To The Income Statement This is the downloaded transcript of the video presentation for this topic. More downloads and videos are available at The Kaplan Group Commercial Collection Agency

Introduction To The Income Statement This is the downloaded transcript of the video presentation for this topic. More downloads and videos are available at The Kaplan Group Commercial Collection Agency

IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes)

") IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes) Hello, and welcome to our first sample case study. This is a three-statement modeling case study and we're using this

IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes) Hello, and welcome to our first sample case study. This is a three-statement modeling case study and we're using this

BUDGETING IT IS FOR EVERYONE

BUDGETING IT IS FOR EVERYONE GRADES 7-12 DAVID FAERBER TIME ALLOTMENT: Two 50-minute classes. OVERVIEW: Many people think that budgeting is only for those who do not make very much money or who are having

BUDGETING IT IS FOR EVERYONE GRADES 7-12 DAVID FAERBER TIME ALLOTMENT: Two 50-minute classes. OVERVIEW: Many people think that budgeting is only for those who do not make very much money or who are having

What to do if you re Drowning in Debt

What to do if you re Drowning in Debt A Beginner s Guide to Debt and Debt Relief Brought to you by: Copyright creditworld 2012 1 INTRODUCTION Are you drowning in debt? Do you feel like no matter what you

What to do if you re Drowning in Debt A Beginner s Guide to Debt and Debt Relief Brought to you by: Copyright creditworld 2012 1 INTRODUCTION Are you drowning in debt? Do you feel like no matter what you

Making the Most of Your Money

Making the Most of Your Money A Handbook for Young Adults Table of Contents Let s start from the beginning:.....................1 Creating a budget:.............................. 2 Budget Worksheet:.............................

Making the Most of Your Money A Handbook for Young Adults Table of Contents Let s start from the beginning:.....................1 Creating a budget:.............................. 2 Budget Worksheet:.............................

Let me turn it over now and kind of get the one of the questions that s burning in all of our minds is about Social Security and what can we expect.

Wi$e Up Webinar Catching On to Retirement September 28, 2007 Speaker 2 Diana Varela Let me turn it over now and kind of get the one of the questions that s burning in all of our minds is about Social Security

Wi$e Up Webinar Catching On to Retirement September 28, 2007 Speaker 2 Diana Varela Let me turn it over now and kind of get the one of the questions that s burning in all of our minds is about Social Security

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES MONEY CONCEPTS FOR TEENS AND YOUNG ADULTS Empowering people to lead financially healthy lives. TABLE OF CONTENTS Introduction...2 Your First Job!...2 Big Decisions...5

GREENPATH FINANCIAL WELLNESS SERIES MONEY CONCEPTS FOR TEENS AND YOUNG ADULTS Empowering people to lead financially healthy lives. TABLE OF CONTENTS Introduction...2 Your First Job!...2 Big Decisions...5