Choice under risk and uncertainty

|

|

|

- Lily Wade

- 5 years ago

- Views:

Transcription

1 Choice under risk and uncertainty

2 Introduction Up until now, we have thought of the objects that our decision makers are choosing as being physical items However, we can also think of cases where the outcomes of the choices we make are uncertain - we don t know exactly what will happen when we do a particular choice. For example: You are deciding whether or not to invest in a business You are deciding whether or not to go skiing next month You are deciding whether or not to buy a house that straddles the San Andreas fault line

3 Risk and Uncertainty In each case the outcomes are uncertain. Here we are going to think about how to model a decision maker who is making such choices. Economists tend to differentiate between two different types of ways in which we may not know for certain what will happen in the future: risk and uncertainty (sometimes called ambiguity). Risk: the probabilities of different outcomes are known, Uncertainty: the probabilities of different outcomes are unknown Now we consider models of choice under risk,

4 An example of choice under risk For an amount of money x, you can flip a coin. If you get heads, you get 10. If you get tails, you get 0. Assume there is a 50% chance of heads and a 50% chance of tails. For what price x would you choose to play the game? i.e. you have a choice between the following two options. 1. Not play the game and get nothing 2. Play the game, and get -x for sure, plus a 50% chance of getting $10.

5 Figure out the expected value (or average pay-out) of playing the game, and see if it is bigger than 0. If it is, then play the game, if not, then don t. With a 50% chance you will get 10- x, With a 50% chance you will get -x. Thus, the average payoff is: 0.5(10 - x) + 0.5(- x) = 5 - x Thus the value of the game is 5 - x. you should play the game if the cost of playing is less than 5.

6 Lotteries (or prospects) Decision making under risk can be considered as a process of choosing between different lotteries. A lottery (or prospect) consists of a number of possible outcomes with their associated probability It can be described as: q = x 1, p 1 ; x 2, p 2 ; x n, p n where x i represents the i th outcome and p i is its associated probability, p i 0,1 i and i p i = 1.

7 In the example the choice is between: r = 10 x, 0.5; x, 0.5 s = 0, 1 in this last case we omit probability and we can write s = 0. When an outcomes is for sure (i.e. its probability is 1) we write only the outcome. s = x means that the outcome x is for sure Sometime we can omit the zero outcomes, so the lottery r = 10, 0.5; 5, 0.3; 0, 0.2 can be written as r = 10, 0.5; 5, 0.3

8 Compound lotteries Lotteries can be combined From the previous example: suppose you have the following lottery of lotteries: c = r, 1 ; s, where r = 10 x, 0.5; x, 0.5 and s = 0, 1. Then, the resulting lottery is: c = 10 x, 1 4 ; x, 1 4 ; 0, 1 2

9 More in general Consider the two following lotteries r = x 1, p 1 ; x n, p n and s = y 1, q 1 ; y n, q n, then c = r, a; s, 1 a = x 1, ap 1 ; x n, ap n ; y 1, 1 a q 1 ; y n, 1 a q n

10 Choice under risk: the axioms of von Neumann and Morgenstern (vnm) These axioms are related to the axioms on preferences and impose rationality to the individual s behaviour when individuals face choices among lotteries. satisfies: a. Completeness For all lotteries q and r we have that q r or r q (or both) b. Transitivity For any three lotteries q, r, s if q r and r s, then q s

11 c. Continuity For any three lotteries q, r, s where q r and r s, there exists some probability p such that there is indifference between the middle ranked prospect r and the prospect q, p; s, 1 p, i.e. q, p; s, 1 p r Equivalently there exist a, b 0, 1 such that: q, a; s, 1 a r q, b; s, 1 b

12 d. Independence Any state of the world that results in the same outcome regardless of one s choice can be ignored or cancelled For any three lotteries q, r, s and any p 0, 1 if q r then q, p; s, 1 p r, p; s, 1 p

13 Example If q = 3000, r = 4000, 0.8 and q r then q = 3000, 0.25, r = 4000, 0.2 and q r Note that: prospect q is the compound lottery q = q, 0.25; 0, 0.75 and prospects r is the compound lottery r = r, 0.25; 0, 0.75

14 Directly related to independence is the axiom of betweenness. If q r then for any a 0,1 : q q, a; r, 1 a r q, a; r, 1 a

15 e. Monotonicity a gamble which assigns a higher probability to a preferred outcome will be preferred to one which assigns a lower probability to a preferred outcome (as long as the other outcomes in the gambles remain unchanged) Concept od stochastically dominance.

16 Stochastic dominance Consider the following two lotteries: q = 10, 0.01; 15, 0.02; 30, 0.01; 45, 0.06 r = 15, 0.03; 45, 0.07 r dominates q, it is clear rewriting r as: r = 10, 0.00; 15, 0.03; 30, 0.00; 45, 0.07

17 Consider two prospects q and r Let x 1, x 2, x n the outcomes in q and r, ordered from the worst to the best. Let be: p qi the probability of outcome i in prospect q p ri the probability of outcome i in prospect r We say that prospect q stochastically dominates prospect r if: x i=1 x p qi i=1 p ri x 1,, n with strict inequality for at least one x

18 Expected Value The expected value of prospectr = x 1, p 1 ; x n, p n is Example E r = i p i x i r = 1000, 0.25; 500, 0.75 and u x i = x i E r =

19 St. Petersburg paradox A fair coin is tossed repeatedly until a tail appears, ending the game. The pot starts at 2 dollars and is doubled every time a head appears. Prize is whatever is in the pot after the game ends: 2 dollars if a tail appears on the first toss, 4 dollars if a head appears on the first toss and a tail on the second, 8 dollars if a head appears on the first two tosses and a tail on the third, 16 dollars if a head appears on the first three tosses and a tail on the fourth, etc. 2 k dollars if the coin is tossed k times until the first tail appears.

20 The expected value is : = = i=1 2 i 1 2 i = = = The experimental evidence is that people are willing to pay only limited amount of money to play this lottery Solution: the value that people attach to the first dollar of their wealth is larger tat the value they attach to the i th dollar they earn. A decreasing marginal value can explain this paradox

21 Expected Utility and Expected Value The expected utility of a prospect r = x 1, p 1 ; x n, p n is given by: U r = i p i u x i Example r = 1000, 0.25; 500, 0.75 and u x i = x i U r = St.Petersburg paradox when u x i = x i 2 i 2 1 i 2 i = 1 = = 2.41 i=1 i=1

22 Representation theorem Let be X the set of all possible lotteries. A binary relation satisfies vnm axioms if and only if there exists a function u: X R such that: q r if and only if u q u r

23 1) Asset integration Further assumptions a prospect is acceptable if and only if the utility resulting from integrating the prospect with one s assets exceeds the utility of those assets alone. Lottery r = x 1, p 1 ; x n, p n position w if U x 1 + w, p 1 ; x n + w, p n is acceptable at asset U w

24 2. Risk aversion a person is said to be risk averse if he prefers the certain prospect x to any risky prospect with expected value equal to x. Risk aversion is caused by the concavity in the utility function More in general we can talk of Risk Attitudes

25 A decision maker is risk neutral if he is indifferent between receiving a lottery s expected value and playing the lottery. Consider r = x 1, p 1 ; x n, p n u Risk Attitudes i p i x i = i then: p i u x i A decision maker is risk neutral if its utility function is linear, i.e. u x = a + b x

26 A decision maker is risk averse if he prefers receiving the lottery s expected value instead of playing the lottery. Consider r = x 1, p 1 ; x n, p n u i p i x i > i then: p i u x i A decision maker is risk averse if its utility function is strictly concave, i.e. u" x < 0

27 A decision maker is risk seeking if he prefers playing the lottery instead of receiving its expected value. Consider r = x 1, p 1 ; x n, p n u i p i x i < i then: p i u x i A decision maker is risk seeking if its utility function is strictly convex, i.e. u" x > 0

28 r = 100,

29 All these results are proved by Jensen s Inequality Let x be a random variable where E(x) is its expected value and f x is a concave function then: f E x E f x f x is a convex function then: f E x E f x

30 Measures of risk aversion For of a lottery q, the risk premium R q is defined as R q = E q CE q where CE q is the certainty equivalent wealth defined as U CE q = U q Interpretation: the risk premium R q is the amount of money that an agent is willing to pay to avoid a lottery.

31 Example. Person A has to play the following lottery q = 100, 0.5; 64, 0.5. Assume that his utility function is u x = x Compute the risk premium. U CE q = U q CE q = CE q = 81 R q = E q CE q = = 1 Person B utility function is u x = x. He proposes to person A to buy the lottery. Which is the minimum price that person A will accept? Answer: 81 Is convenient for person B? Answer: yes

32 Person A has to play the following lottery q = 100, 0.5; 64, 0.5. Assume that his utility function is u x = x We have computed that R q = 1 Selling the lottery at p=81 is equivalent to hold the lottery and pay 19 when lottery s outcome is 100 and to receive 17 when lottery s outcome is 64. In expected terms Person A pays 1 ( = 1)

33 r = 100, 0.5 R r = 50 CE r 0 CE r E r =

34 1. Arrow-Pratt measure of absolute risk-aversion: u" c A c = u c 2. Arrow-Pratt-De Finetti measure of relative riskaversion or coefficient of relative risk aversion c u" c R c = u c

35 Type of Risk-Aversion Example of utility functions Increasing absolute riskaversion u w = w c w2 Constant absolute riskaversion u w = e c w Decreasing absolute riskaversion u w = ln w

36 Type of Risk-Aversion Example of utility functions Increasing relative riskaversion w cw 2 Constant relative riskaversion ln(w) Decreasing relative riskaversion 1 e 2 w 2

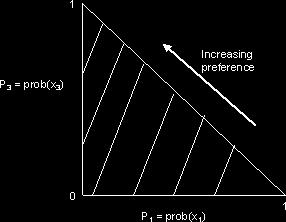

37 The Machina triangle two-dimensional representation 3 possible outcomes, x 1, x 2, and x 3, and x 3 x 2 x 1. they occur with probabilities p 1, p 2, and p 3 respectively, where i p i = 1 since p 2 = 1 - p 1 - p 3, we can represent these lotteries by points in a unit triangle in the (p 1, p 3 ) plane, known as the Machina triangle Example r = x 1, p 1, x 2, p 2 ; x 3, p 3, U r = p 1 u x 1 + p 2 u x 2 + p 3 u x 3 U r = p 1 u x p 1 p 3 u x 2 + p 3 u x 3

38 Example r = x 1, p 1, x 2, p 2 ; x 3, p 3, U r = p 1 u x 1 + p 2 u x 2 + p 3 u x 3 Replace p 2 = 1 p 1 p 3 U r = p 1 u x p 1 p 3 u x 2 + p 3 u x 3 Hold the utility constant at a level U and solve by p 3 p 3 = U u x 2 u x 3 u x 2 + u x 2 u x 1 u x 3 u x 2 p 1 Slope is positive, intercept could be either positive or negative

39

40 Representing risk attitudes using indifference curves p 3 The blue lines in both panels are iso-expected value lines p 1

41 Risk averse p 3 The blue lines are iso-expected value lines Black lines are indifference curves p 1

42 Risk seeking p 3 The blue lines are iso-expected value lines Black lines are indifference curves p 1

Rational theories of finance tell us how people should behave and often do not reflect reality.

FINC3023 Behavioral Finance TOPIC 1: Expected Utility Rational theories of finance tell us how people should behave and often do not reflect reality. A normative theory based on rational utility maximizers

FINC3023 Behavioral Finance TOPIC 1: Expected Utility Rational theories of finance tell us how people should behave and often do not reflect reality. A normative theory based on rational utility maximizers

MICROECONOMIC THEROY CONSUMER THEORY

LECTURE 5 MICROECONOMIC THEROY CONSUMER THEORY Choice under Uncertainty (MWG chapter 6, sections A-C, and Cowell chapter 8) Lecturer: Andreas Papandreou 1 Introduction p Contents n Expected utility theory

LECTURE 5 MICROECONOMIC THEROY CONSUMER THEORY Choice under Uncertainty (MWG chapter 6, sections A-C, and Cowell chapter 8) Lecturer: Andreas Papandreou 1 Introduction p Contents n Expected utility theory

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty We always need to make a decision (or select from among actions, options or moves) even when there exists

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty We always need to make a decision (or select from among actions, options or moves) even when there exists

Chapter 6: Risky Securities and Utility Theory

Chapter 6: Risky Securities and Utility Theory Topics 1. Principle of Expected Return 2. St. Petersburg Paradox 3. Utility Theory 4. Principle of Expected Utility 5. The Certainty Equivalent 6. Utility

Chapter 6: Risky Securities and Utility Theory Topics 1. Principle of Expected Return 2. St. Petersburg Paradox 3. Utility Theory 4. Principle of Expected Utility 5. The Certainty Equivalent 6. Utility

Comparison of Payoff Distributions in Terms of Return and Risk

Comparison of Payoff Distributions in Terms of Return and Risk Preliminaries We treat, for convenience, money as a continuous variable when dealing with monetary outcomes. Strictly speaking, the derivation

Comparison of Payoff Distributions in Terms of Return and Risk Preliminaries We treat, for convenience, money as a continuous variable when dealing with monetary outcomes. Strictly speaking, the derivation

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

ECON Financial Economics

ECON 8 - Financial Economics Michael Bar August, 0 San Francisco State University, department of economics. ii Contents Decision Theory under Uncertainty. Introduction.....................................

ECON 8 - Financial Economics Michael Bar August, 0 San Francisco State University, department of economics. ii Contents Decision Theory under Uncertainty. Introduction.....................................

Expected Utility and Risk Aversion

Expected Utility and Risk Aversion Expected utility and risk aversion 1/ 58 Introduction Expected utility is the standard framework for modeling investor choices. The following topics will be covered:

Expected Utility and Risk Aversion Expected utility and risk aversion 1/ 58 Introduction Expected utility is the standard framework for modeling investor choices. The following topics will be covered:

ECON 581. Decision making under risk. Instructor: Dmytro Hryshko

ECON 581. Decision making under risk Instructor: Dmytro Hryshko 1 / 36 Outline Expected utility Risk aversion Certainty equivalence and risk premium The canonical portfolio allocation problem 2 / 36 Suggested

ECON 581. Decision making under risk Instructor: Dmytro Hryshko 1 / 36 Outline Expected utility Risk aversion Certainty equivalence and risk premium The canonical portfolio allocation problem 2 / 36 Suggested

Chapter 18: Risky Choice and Risk

Chapter 18: Risky Choice and Risk Risky Choice Probability States of Nature Expected Utility Function Interval Measure Violations Risk Preference State Dependent Utility Risk-Aversion Coefficient Actuarially

Chapter 18: Risky Choice and Risk Risky Choice Probability States of Nature Expected Utility Function Interval Measure Violations Risk Preference State Dependent Utility Risk-Aversion Coefficient Actuarially

Micro Theory I Assignment #5 - Answer key

Micro Theory I Assignment #5 - Answer key 1. Exercises from MWG (Chapter 6): (a) Exercise 6.B.1 from MWG: Show that if the preferences % over L satisfy the independence axiom, then for all 2 (0; 1) and

Micro Theory I Assignment #5 - Answer key 1. Exercises from MWG (Chapter 6): (a) Exercise 6.B.1 from MWG: Show that if the preferences % over L satisfy the independence axiom, then for all 2 (0; 1) and

Chapter 1. Utility Theory. 1.1 Introduction

Chapter 1 Utility Theory 1.1 Introduction St. Petersburg Paradox (gambling paradox) the birth to the utility function http://policonomics.com/saint-petersburg-paradox/ The St. Petersburg paradox, is a

Chapter 1 Utility Theory 1.1 Introduction St. Petersburg Paradox (gambling paradox) the birth to the utility function http://policonomics.com/saint-petersburg-paradox/ The St. Petersburg paradox, is a

Choice Under Uncertainty

Chapter 6 Choice Under Uncertainty Up until now, we have been concerned with choice under certainty. A consumer chooses which commodity bundle to consume. A producer chooses how much output to produce

Chapter 6 Choice Under Uncertainty Up until now, we have been concerned with choice under certainty. A consumer chooses which commodity bundle to consume. A producer chooses how much output to produce

Choice under Uncertainty

Chapter 7 Choice under Uncertainty 1. Expected Utility Theory. 2. Risk Aversion. 3. Applications: demand for insurance, portfolio choice 4. Violations of Expected Utility Theory. 7.1 Expected Utility Theory

Chapter 7 Choice under Uncertainty 1. Expected Utility Theory. 2. Risk Aversion. 3. Applications: demand for insurance, portfolio choice 4. Violations of Expected Utility Theory. 7.1 Expected Utility Theory

Expected Utility And Risk Aversion

Expected Utility And Risk Aversion Econ 2100 Fall 2017 Lecture 12, October 4 Outline 1 Risk Aversion 2 Certainty Equivalent 3 Risk Premium 4 Relative Risk Aversion 5 Stochastic Dominance Notation From

Expected Utility And Risk Aversion Econ 2100 Fall 2017 Lecture 12, October 4 Outline 1 Risk Aversion 2 Certainty Equivalent 3 Risk Premium 4 Relative Risk Aversion 5 Stochastic Dominance Notation From

Utility and Choice Under Uncertainty

Introduction to Microeconomics Utility and Choice Under Uncertainty The Five Axioms of Choice Under Uncertainty We can use the axioms of preference to show how preferences can be mapped into measurable

Introduction to Microeconomics Utility and Choice Under Uncertainty The Five Axioms of Choice Under Uncertainty We can use the axioms of preference to show how preferences can be mapped into measurable

Risk aversion and choice under uncertainty

Risk aversion and choice under uncertainty Pierre Chaigneau pierre.chaigneau@hec.ca June 14, 2011 Finance: the economics of risk and uncertainty In financial markets, claims associated with random future

Risk aversion and choice under uncertainty Pierre Chaigneau pierre.chaigneau@hec.ca June 14, 2011 Finance: the economics of risk and uncertainty In financial markets, claims associated with random future

UTILITY ANALYSIS HANDOUTS

UTILITY ANALYSIS HANDOUTS 1 2 UTILITY ANALYSIS Motivating Example: Your total net worth = $400K = W 0. You own a home worth $250K. Probability of a fire each yr = 0.001. Insurance cost = $1K. Question:

UTILITY ANALYSIS HANDOUTS 1 2 UTILITY ANALYSIS Motivating Example: Your total net worth = $400K = W 0. You own a home worth $250K. Probability of a fire each yr = 0.001. Insurance cost = $1K. Question:

Expected Utility Theory

Expected Utility Theory Mark Dean Behavioral Economics Spring 27 Introduction Up until now, we have thought of subjects choosing between objects Used cars Hamburgers Monetary amounts However, often the

Expected Utility Theory Mark Dean Behavioral Economics Spring 27 Introduction Up until now, we have thought of subjects choosing between objects Used cars Hamburgers Monetary amounts However, often the

Foundations of Financial Economics Choice under uncertainty

Foundations of Financial Economics Choice under uncertainty Paulo Brito 1 pbrito@iseg.ulisboa.pt University of Lisbon March 9, 2018 Topics covered Contingent goods Comparing contingent goods Decision under

Foundations of Financial Economics Choice under uncertainty Paulo Brito 1 pbrito@iseg.ulisboa.pt University of Lisbon March 9, 2018 Topics covered Contingent goods Comparing contingent goods Decision under

3.1 The Marschak-Machina triangle and risk aversion

Chapter 3 Risk aversion 3.1 The Marschak-Machina triangle and risk aversion One of the earliest, and most useful, graphical tools used to analyse choice under uncertainty was a triangular graph that was

Chapter 3 Risk aversion 3.1 The Marschak-Machina triangle and risk aversion One of the earliest, and most useful, graphical tools used to analyse choice under uncertainty was a triangular graph that was

Expected utility theory; Expected Utility Theory; risk aversion and utility functions

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

Models & Decision with Financial Applications Unit 3: Utility Function and Risk Attitude

Models & Decision with Financial Applications Unit 3: Utility Function and Risk Attitude Duan LI Department of Systems Engineering & Engineering Management The Chinese University of Hong Kong http://www.se.cuhk.edu.hk/

Models & Decision with Financial Applications Unit 3: Utility Function and Risk Attitude Duan LI Department of Systems Engineering & Engineering Management The Chinese University of Hong Kong http://www.se.cuhk.edu.hk/

Notes for Session 2, Expected Utility Theory, Summer School 2009 T.Seidenfeld 1

Session 2: Expected Utility In our discussion of betting from Session 1, we required the bookie to accept (as fair) the combination of two gambles, when each gamble, on its own, is judged fair. That is,

Session 2: Expected Utility In our discussion of betting from Session 1, we required the bookie to accept (as fair) the combination of two gambles, when each gamble, on its own, is judged fair. That is,

Module 1: Decision Making Under Uncertainty

Module 1: Decision Making Under Uncertainty Information Economics (Ec 515) George Georgiadis Today, we will study settings in which decision makers face uncertain outcomes. Natural when dealing with asymmetric

Module 1: Decision Making Under Uncertainty Information Economics (Ec 515) George Georgiadis Today, we will study settings in which decision makers face uncertain outcomes. Natural when dealing with asymmetric

Name. Final Exam, Economics 210A, December 2014 Answer any 7 of these 8 questions Good luck!

Name Final Exam, Economics 210A, December 2014 Answer any 7 of these 8 questions Good luck! 1) For each of the following statements, state whether it is true or false. If it is true, prove that it is true.

Name Final Exam, Economics 210A, December 2014 Answer any 7 of these 8 questions Good luck! 1) For each of the following statements, state whether it is true or false. If it is true, prove that it is true.

Expected value is basically the average payoff from some sort of lottery, gamble or other situation with a randomly determined outcome.

Economics 352: Intermediate Microeconomics Notes and Sample Questions Chapter 18: Uncertainty and Risk Aversion Expected Value The chapter starts out by explaining what expected value is and how to calculate

Economics 352: Intermediate Microeconomics Notes and Sample Questions Chapter 18: Uncertainty and Risk Aversion Expected Value The chapter starts out by explaining what expected value is and how to calculate

Advanced Risk Management

Winter 2014/2015 Advanced Risk Management Part I: Decision Theory and Risk Management Motives Lecture 1: Introduction and Expected Utility Your Instructors for Part I: Prof. Dr. Andreas Richter Email:

Winter 2014/2015 Advanced Risk Management Part I: Decision Theory and Risk Management Motives Lecture 1: Introduction and Expected Utility Your Instructors for Part I: Prof. Dr. Andreas Richter Email:

BEEM109 Experimental Economics and Finance

University of Exeter Recap Last class we looked at the axioms of expected utility, which defined a rational agent as proposed by von Neumann and Morgenstern. We then proceeded to look at empirical evidence

University of Exeter Recap Last class we looked at the axioms of expected utility, which defined a rational agent as proposed by von Neumann and Morgenstern. We then proceeded to look at empirical evidence

Department of Economics The Ohio State University Final Exam Questions and Answers Econ 8712

Prof. Peck Fall 016 Department of Economics The Ohio State University Final Exam Questions and Answers Econ 871 1. (35 points) The following economy has one consumer, two firms, and four goods. Goods 1

Prof. Peck Fall 016 Department of Economics The Ohio State University Final Exam Questions and Answers Econ 871 1. (35 points) The following economy has one consumer, two firms, and four goods. Goods 1

Copyright (C) 2001 David K. Levine This document is an open textbook; you can redistribute it and/or modify it under the terms of version 1 of the

2001 David K. Levine This document is an open textbook; you can redistribute it and/or modify it under the terms of version 1 of the") Copyright (C) 2001 David K. Levine This document is an open textbook; you can redistribute it and/or modify it under the terms of version 1 of the open text license amendment to version 2 of the GNU General

Copyright (C) 2001 David K. Levine This document is an open textbook; you can redistribute it and/or modify it under the terms of version 1 of the open text license amendment to version 2 of the GNU General

Financial Economics: Making Choices in Risky Situations

Financial Economics: Making Choices in Risky Situations Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY March, 2015 1 / 57 Questions to Answer How financial risk is defined and measured How an investor

Financial Economics: Making Choices in Risky Situations Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY March, 2015 1 / 57 Questions to Answer How financial risk is defined and measured How an investor

PhD Qualifier Examination

PhD Qualifier Examination Department of Agricultural Economics May 29, 2014 Instructions This exam consists of six questions. You must answer all questions. If you need an assumption to complete a question,

PhD Qualifier Examination Department of Agricultural Economics May 29, 2014 Instructions This exam consists of six questions. You must answer all questions. If you need an assumption to complete a question,

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY PART ± I CHAPTER 1 CHAPTER 2 CHAPTER 3 Foundations of Finance I: Expected Utility Theory Foundations of Finance II: Asset Pricing, Market Efficiency,

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY PART ± I CHAPTER 1 CHAPTER 2 CHAPTER 3 Foundations of Finance I: Expected Utility Theory Foundations of Finance II: Asset Pricing, Market Efficiency,

Lecture 2 Basic Tools for Portfolio Analysis

1 Lecture 2 Basic Tools for Portfolio Analysis Alexander K Koch Department of Economics, Royal Holloway, University of London October 8, 27 In addition to learning the material covered in the reading and

1 Lecture 2 Basic Tools for Portfolio Analysis Alexander K Koch Department of Economics, Royal Holloway, University of London October 8, 27 In addition to learning the material covered in the reading and

What do Coin Tosses and Decision Making under Uncertainty, have in common?

What do Coin Tosses and Decision Making under Uncertainty, have in common? J. Rene van Dorp (GW) Presentation EMSE 1001 October 27, 2017 Presented by: J. Rene van Dorp 10/26/2017 1 About René van Dorp

What do Coin Tosses and Decision Making under Uncertainty, have in common? J. Rene van Dorp (GW) Presentation EMSE 1001 October 27, 2017 Presented by: J. Rene van Dorp 10/26/2017 1 About René van Dorp

Lecture 11 - Risk Aversion, Expected Utility Theory and Insurance

Lecture 11 - Risk Aversion, Expected Utility Theory and Insurance 14.03, Spring 2003 1 Risk Aversion and Insurance: Introduction To have a passably usable model of choice, we need to be able to say something

Lecture 11 - Risk Aversion, Expected Utility Theory and Insurance 14.03, Spring 2003 1 Risk Aversion and Insurance: Introduction To have a passably usable model of choice, we need to be able to say something

Learning Objectives = = where X i is the i t h outcome of a decision, p i is the probability of the i t h

Learning Objectives After reading Chapter 15 and working the problems for Chapter 15 in the textbook and in this Workbook, you should be able to: Distinguish between decision making under uncertainty and

Learning Objectives After reading Chapter 15 and working the problems for Chapter 15 in the textbook and in this Workbook, you should be able to: Distinguish between decision making under uncertainty and

Managerial Economics Uncertainty

Managerial Economics Uncertainty Aalto University School of Science Department of Industrial Engineering and Management January 10 26, 2017 Dr. Arto Kovanen, Ph.D. Visiting Lecturer Uncertainty general

Managerial Economics Uncertainty Aalto University School of Science Department of Industrial Engineering and Management January 10 26, 2017 Dr. Arto Kovanen, Ph.D. Visiting Lecturer Uncertainty general

Managerial Economics

Managerial Economics Unit 9: Risk Analysis Rudolf Winter-Ebmer Johannes Kepler University Linz Winter Term 2015 Managerial Economics: Unit 9 - Risk Analysis 1 / 49 Objectives Explain how managers should

Managerial Economics Unit 9: Risk Analysis Rudolf Winter-Ebmer Johannes Kepler University Linz Winter Term 2015 Managerial Economics: Unit 9 - Risk Analysis 1 / 49 Objectives Explain how managers should

Answers to chapter 3 review questions

Answers to chapter 3 review questions 3.1 Explain why the indifference curves in a probability triangle diagram are straight lines if preferences satisfy expected utility theory. The expected utility of

Answers to chapter 3 review questions 3.1 Explain why the indifference curves in a probability triangle diagram are straight lines if preferences satisfy expected utility theory. The expected utility of

Exercises for Chapter 8

Exercises for Chapter 8 Exercise 8. Consider the following functions: f (x)= e x, (8.) g(x)=ln(x+), (8.2) h(x)= x 2, (8.3) u(x)= x 2, (8.4) v(x)= x, (8.5) w(x)=sin(x). (8.6) In all cases take x>0. (a)

Exercises for Chapter 8 Exercise 8. Consider the following functions: f (x)= e x, (8.) g(x)=ln(x+), (8.2) h(x)= x 2, (8.3) u(x)= x 2, (8.4) v(x)= x, (8.5) w(x)=sin(x). (8.6) In all cases take x>0. (a)

Unit 4.3: Uncertainty

Unit 4.: Uncertainty Michael Malcolm June 8, 20 Up until now, we have been considering consumer choice problems where the consumer chooses over outcomes that are known. However, many choices in economics

Unit 4.: Uncertainty Michael Malcolm June 8, 20 Up until now, we have been considering consumer choice problems where the consumer chooses over outcomes that are known. However, many choices in economics

University of California, Davis Department of Economics Giacomo Bonanno. Economics 103: Economics of uncertainty and information PRACTICE PROBLEMS

University of California, Davis Department of Economics Giacomo Bonanno Economics 03: Economics of uncertainty and information PRACTICE PROBLEMS oooooooooooooooo Problem :.. Expected value Problem :..

University of California, Davis Department of Economics Giacomo Bonanno Economics 03: Economics of uncertainty and information PRACTICE PROBLEMS oooooooooooooooo Problem :.. Expected value Problem :..

Economic Risk and Decision Analysis for Oil and Gas Industry CE School of Engineering and Technology Asian Institute of Technology

Economic Risk and Decision Analysis for Oil and Gas Industry CE81.9008 School of Engineering and Technology Asian Institute of Technology January Semester Presented by Dr. Thitisak Boonpramote Department

Economic Risk and Decision Analysis for Oil and Gas Industry CE81.9008 School of Engineering and Technology Asian Institute of Technology January Semester Presented by Dr. Thitisak Boonpramote Department

Part 4: Market Failure II - Asymmetric Information - Uncertainty

Part 4: Market Failure II - Asymmetric Information - Uncertainty Expected Utility, Risk Aversion, Risk Neutrality, Risk Pooling, Insurance July 2016 - Asymmetric Information - Uncertainty July 2016 1 /

Part 4: Market Failure II - Asymmetric Information - Uncertainty Expected Utility, Risk Aversion, Risk Neutrality, Risk Pooling, Insurance July 2016 - Asymmetric Information - Uncertainty July 2016 1 /

Making Hard Decision. ENCE 627 Decision Analysis for Engineering. Identify the decision situation and understand objectives. Identify alternatives

CHAPTER Duxbury Thomson Learning Making Hard Decision Third Edition RISK ATTITUDES A. J. Clark School of Engineering Department of Civil and Environmental Engineering 13 FALL 2003 By Dr. Ibrahim. Assakkaf

CHAPTER Duxbury Thomson Learning Making Hard Decision Third Edition RISK ATTITUDES A. J. Clark School of Engineering Department of Civil and Environmental Engineering 13 FALL 2003 By Dr. Ibrahim. Assakkaf

Microeconomics of Banking: Lecture 2

Microeconomics of Banking: Lecture 2 Prof. Ronaldo CARPIO September 25, 2015 A Brief Look at General Equilibrium Asset Pricing Last week, we saw a general equilibrium model in which banks were irrelevant.

Microeconomics of Banking: Lecture 2 Prof. Ronaldo CARPIO September 25, 2015 A Brief Look at General Equilibrium Asset Pricing Last week, we saw a general equilibrium model in which banks were irrelevant.

April 28, Decision Analysis 2. Utility Theory The Value of Information

15.053 April 28, 2005 Decision Analysis 2 Utility Theory The Value of Information 1 Lotteries and Utility L1 $50,000 $ 0 Lottery 1: a 50% chance at $50,000 and a 50% chance of nothing. L2 $20,000 Lottery

15.053 April 28, 2005 Decision Analysis 2 Utility Theory The Value of Information 1 Lotteries and Utility L1 $50,000 $ 0 Lottery 1: a 50% chance at $50,000 and a 50% chance of nothing. L2 $20,000 Lottery

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall Module I

Fall Module I") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2018 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2018 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

If U is linear, then U[E(Ỹ )] = E[U(Ỹ )], and one is indifferent between lottery and its expectation. One is called risk neutral.

![If U is linear, then U[E(Ỹ )] = E[U(Ỹ )], and one is indifferent between lottery and its expectation. One is called risk neutral.](/thumbs/90/104465976.jpg "If U is linear, then U[E(Ỹ )] = E[U(Ỹ )], and one is indifferent between lottery and its expectation. One is called risk neutral.") Risk aversion For those preference orderings which (i.e., for those individuals who) satisfy the seven axioms, define risk aversion. Compare a lottery Ỹ = L(a, b, π) (where a, b are fixed monetary outcomes)

Risk aversion For those preference orderings which (i.e., for those individuals who) satisfy the seven axioms, define risk aversion. Compare a lottery Ỹ = L(a, b, π) (where a, b are fixed monetary outcomes)

Decision Theory. Refail N. Kasimbeyli

Decision Theory Refail N. Kasimbeyli Chapter 3 3 Utility Theory 3.1 Single-attribute utility 3.2 Interpreting utility functions 3.3 Utility functions for non-monetary attributes 3.4 The axioms of utility

Decision Theory Refail N. Kasimbeyli Chapter 3 3 Utility Theory 3.1 Single-attribute utility 3.2 Interpreting utility functions 3.3 Utility functions for non-monetary attributes 3.4 The axioms of utility

Lecture 12: Introduction to reasoning under uncertainty. Actions and Consequences

Lecture 12: Introduction to reasoning under uncertainty Preferences Utility functions Maximizing expected utility Value of information Bandit problems and the exploration-exploitation trade-off COMP-424,

Lecture 12: Introduction to reasoning under uncertainty Preferences Utility functions Maximizing expected utility Value of information Bandit problems and the exploration-exploitation trade-off COMP-424,

Lecture 6 Introduction to Utility Theory under Certainty and Uncertainty

Lecture 6 Introduction to Utility Theory under Certainty and Uncertainty Prof. Massimo Guidolin Prep Course in Quant Methods for Finance August-September 2017 Outline and objectives Axioms of choice under

Lecture 6 Introduction to Utility Theory under Certainty and Uncertainty Prof. Massimo Guidolin Prep Course in Quant Methods for Finance August-September 2017 Outline and objectives Axioms of choice under

Introduction to Economics I: Consumer Theory

Introduction to Economics I: Consumer Theory Leslie Reinhorn Durham University Business School October 2014 What is Economics? Typical De nitions: "Economics is the social science that deals with the production,

Introduction to Economics I: Consumer Theory Leslie Reinhorn Durham University Business School October 2014 What is Economics? Typical De nitions: "Economics is the social science that deals with the production,

1. Expected utility, risk aversion and stochastic dominance

. Epected utility, risk aversion and stochastic dominance. Epected utility.. Description o risky alternatives.. Preerences over lotteries..3 The epected utility theorem. Monetary lotteries and risk aversion..

. Epected utility, risk aversion and stochastic dominance. Epected utility.. Description o risky alternatives.. Preerences over lotteries..3 The epected utility theorem. Monetary lotteries and risk aversion..

Key concepts: Certainty Equivalent and Risk Premium

Certainty equivalents Risk premiums 19 Key concepts: Certainty Equivalent and Risk Premium Which is the amount of money that is equivalent in your mind to a given situation that involves uncertainty? Ex:

Certainty equivalents Risk premiums 19 Key concepts: Certainty Equivalent and Risk Premium Which is the amount of money that is equivalent in your mind to a given situation that involves uncertainty? Ex:

Problem Set 2. Theory of Banking - Academic Year Maria Bachelet March 2, 2017

Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmai.com March, 07 Exercise Consider an agency relationship in which the principal contracts the agent, whose effort

Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmai.com March, 07 Exercise Consider an agency relationship in which the principal contracts the agent, whose effort

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College April 3, 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College April 3, 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Economic of Uncertainty

Economic of Uncertainty Risk Aversion Based on ECO 317, Princeton UC3M April 2012 (UC3M) Economics of Uncertainty. April 2012 1 / 16 Introduction 1 Space of Lotteries (UC3M) Economics of Uncertainty. April

Economic of Uncertainty Risk Aversion Based on ECO 317, Princeton UC3M April 2012 (UC3M) Economics of Uncertainty. April 2012 1 / 16 Introduction 1 Space of Lotteries (UC3M) Economics of Uncertainty. April

Final Examination: Economics 210A December, 2015

Name Final Examination: Economics 20A December, 205 ) The island nation of Santa Felicidad has N skilled workers and N unskilled workers. A skilled worker can earn $w S per day if she works all the time

Name Final Examination: Economics 20A December, 205 ) The island nation of Santa Felicidad has N skilled workers and N unskilled workers. A skilled worker can earn $w S per day if she works all the time

ECON4510 Finance Theory Lecture 1

ECON4510 Finance Theory Lecture 1 Kjetil Storesletten Department of Economics University of Oslo 15 January 2018 Kjetil Storesletten, Dept. of Economics, UiO ECON4510 Finance Theory Lecture 1 15 January

ECON4510 Finance Theory Lecture 1 Kjetil Storesletten Department of Economics University of Oslo 15 January 2018 Kjetil Storesletten, Dept. of Economics, UiO ECON4510 Finance Theory Lecture 1 15 January

Microeconomic Theory III Spring 2009

MIT OpenCourseWare http://ocw.mit.edu 14.123 Microeconomic Theory III Spring 2009 For information about citing these materials or our Terms of Use, visit: http://ocw.mit.edu/terms. MIT 14.123 (2009) by

MIT OpenCourseWare http://ocw.mit.edu 14.123 Microeconomic Theory III Spring 2009 For information about citing these materials or our Terms of Use, visit: http://ocw.mit.edu/terms. MIT 14.123 (2009) by

Outline. Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion

Uncertainty Outline Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion 2 Simple Lotteries 3 Simple Lotteries Advanced Microeconomic Theory

Uncertainty Outline Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion 2 Simple Lotteries 3 Simple Lotteries Advanced Microeconomic Theory

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall Module I

Fall Module I") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2016 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2016 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

Attitudes Toward Risk. Joseph Tao-yi Wang 2013/10/16. (Lecture 11, Micro Theory I)

") Joseph Tao-yi Wang 2013/10/16 (Lecture 11, Micro Theory I) Dealing with Uncertainty 2 Preferences over risky choices (Section 7.1) One simple model: Expected Utility How can old tools be applied to analyze

Joseph Tao-yi Wang 2013/10/16 (Lecture 11, Micro Theory I) Dealing with Uncertainty 2 Preferences over risky choices (Section 7.1) One simple model: Expected Utility How can old tools be applied to analyze

Comparative Risk Sensitivity with Reference-Dependent Preferences

The Journal of Risk and Uncertainty, 24:2; 131 142, 2002 2002 Kluwer Academic Publishers. Manufactured in The Netherlands. Comparative Risk Sensitivity with Reference-Dependent Preferences WILLIAM S. NEILSON

The Journal of Risk and Uncertainty, 24:2; 131 142, 2002 2002 Kluwer Academic Publishers. Manufactured in The Netherlands. Comparative Risk Sensitivity with Reference-Dependent Preferences WILLIAM S. NEILSON

16 MAKING SIMPLE DECISIONS

247 16 MAKING SIMPLE DECISIONS Let us associate each state S with a numeric utility U(S), which expresses the desirability of the state A nondeterministic action A will have possible outcome states Result

247 16 MAKING SIMPLE DECISIONS Let us associate each state S with a numeric utility U(S), which expresses the desirability of the state A nondeterministic action A will have possible outcome states Result

Introduction. Two main characteristics: Editing Evaluation. The use of an editing phase Outcomes as difference respect to a reference point 2

Prospect theory 1 Introduction Kahneman and Tversky (1979) Kahneman and Tversky (1992) cumulative prospect theory It is classified as nonconventional theory It is perhaps the most well-known of alternative

Prospect theory 1 Introduction Kahneman and Tversky (1979) Kahneman and Tversky (1992) cumulative prospect theory It is classified as nonconventional theory It is perhaps the most well-known of alternative

Solution Guide to Exercises for Chapter 4 Decision making under uncertainty

THE ECONOMICS OF FINANCIAL MARKETS R. E. BAILEY Solution Guide to Exercises for Chapter 4 Decision making under uncertainty 1. Consider an investor who makes decisions according to a mean-variance objective.

THE ECONOMICS OF FINANCIAL MARKETS R. E. BAILEY Solution Guide to Exercises for Chapter 4 Decision making under uncertainty 1. Consider an investor who makes decisions according to a mean-variance objective.

Notes 10: Risk and Uncertainty

Economics 335 April 19, 1999 A. Introduction Notes 10: Risk and Uncertainty 1. Basic Types of Uncertainty in Agriculture a. production b. prices 2. Examples of Uncertainty in Agriculture a. crop yields

Economics 335 April 19, 1999 A. Introduction Notes 10: Risk and Uncertainty 1. Basic Types of Uncertainty in Agriculture a. production b. prices 2. Examples of Uncertainty in Agriculture a. crop yields

Choice Under Uncertainty

Choice Under Uncertainty Lotteries Without uncertainty, there is no need to distinguish between a consumer s choice between alternatives and the resulting outcome. A consumption bundle is the choice and

Choice Under Uncertainty Lotteries Without uncertainty, there is no need to distinguish between a consumer s choice between alternatives and the resulting outcome. A consumption bundle is the choice and

16 MAKING SIMPLE DECISIONS

253 16 MAKING SIMPLE DECISIONS Let us associate each state S with a numeric utility U(S), which expresses the desirability of the state A nondeterministic action a will have possible outcome states Result(a)

253 16 MAKING SIMPLE DECISIONS Let us associate each state S with a numeric utility U(S), which expresses the desirability of the state A nondeterministic action a will have possible outcome states Result(a)

CS 188: Artificial Intelligence. Maximum Expected Utility

CS 188: Artificial Intelligence Lecture 7: Utility Theory Pieter Abbeel UC Berkeley Many slides adapted from Dan Klein 1 Maximum Expected Utility Why should we average utilities? Why not minimax? Principle

CS 188: Artificial Intelligence Lecture 7: Utility Theory Pieter Abbeel UC Berkeley Many slides adapted from Dan Klein 1 Maximum Expected Utility Why should we average utilities? Why not minimax? Principle

ECO 203: Worksheet 4. Question 1. Question 2. (6 marks)

") ECO 203: Worksheet 4 Question 1 (6 marks) Russel and Ahmed decide to play a simple game. Russel has to flip a fair coin: if he gets a head Ahmed will pay him Tk. 10, if he gets a tail he will have to pay

ECO 203: Worksheet 4 Question 1 (6 marks) Russel and Ahmed decide to play a simple game. Russel has to flip a fair coin: if he gets a head Ahmed will pay him Tk. 10, if he gets a tail he will have to pay

Session 9: The expected utility framework p. 1

Session 9: The expected utility framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 9: The expected utility framework p. 1 Questions How do humans make decisions

Session 9: The expected utility framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 9: The expected utility framework p. 1 Questions How do humans make decisions

Microeconomics 3200/4200:

Microeconomics 3200/4200: Part 1 P. Piacquadio p.g.piacquadio@econ.uio.no September 25, 2017 P. Piacquadio (p.g.piacquadio@econ.uio.no) Micro 3200/4200 September 25, 2017 1 / 23 Example (1) Suppose I take

Microeconomics 3200/4200: Part 1 P. Piacquadio p.g.piacquadio@econ.uio.no September 25, 2017 P. Piacquadio (p.g.piacquadio@econ.uio.no) Micro 3200/4200 September 25, 2017 1 / 23 Example (1) Suppose I take

Lecture 3: Utility-Based Portfolio Choice

Lecture 3: Utility-Based Portfolio Choice Prof. Massimo Guidolin Portfolio Management Spring 2017 Outline and objectives Choice under uncertainty: dominance o Guidolin-Pedio, chapter 1, sec. 2 Choice under

Lecture 3: Utility-Based Portfolio Choice Prof. Massimo Guidolin Portfolio Management Spring 2017 Outline and objectives Choice under uncertainty: dominance o Guidolin-Pedio, chapter 1, sec. 2 Choice under

Microeconomics of Banking: Lecture 3

Microeconomics of Banking: Lecture 3 Prof. Ronaldo CARPIO Oct. 9, 2015 Review of Last Week Consumer choice problem General equilibrium Contingent claims Risk aversion The optimal choice, x = (X, Y ), is

Microeconomics of Banking: Lecture 3 Prof. Ronaldo CARPIO Oct. 9, 2015 Review of Last Week Consumer choice problem General equilibrium Contingent claims Risk aversion The optimal choice, x = (X, Y ), is

CHAPTER 6. Risk Aversion and Capital Allocation to Risky Assets INVESTMENTS BODIE, KANE, MARCUS

CHAPTER 6 Risk Aversion and Capital Allocation to Risky Assets INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 011 by The McGraw-Hill Companies, Inc. All rights reserved. 6- Allocation to Risky

CHAPTER 6 Risk Aversion and Capital Allocation to Risky Assets INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 011 by The McGraw-Hill Companies, Inc. All rights reserved. 6- Allocation to Risky

8/28/2017. ECON4260 Behavioral Economics. 2 nd lecture. Expected utility. What is a lottery?

ECON4260 Behavioral Economics 2 nd lecture Cumulative Prospect Theory Expected utility This is a theory for ranking lotteries Can be seen as normative: This is how I wish my preferences looked like Or

ECON4260 Behavioral Economics 2 nd lecture Cumulative Prospect Theory Expected utility This is a theory for ranking lotteries Can be seen as normative: This is how I wish my preferences looked like Or

Chapter 23: Choice under Risk

Chapter 23: Choice under Risk 23.1: Introduction We consider in this chapter optimal behaviour in conditions of risk. By this we mean that, when the individual takes a decision, he or she does not know

Chapter 23: Choice under Risk 23.1: Introduction We consider in this chapter optimal behaviour in conditions of risk. By this we mean that, when the individual takes a decision, he or she does not know

Uncertainty. Contingent consumption Subjective probability. Utility functions. BEE2017 Microeconomics

Uncertainty BEE217 Microeconomics Uncertainty: The share prices of Amazon and the difficulty of investment decisions Contingent consumption 1. What consumption or wealth will you get in each possible outcome

Uncertainty BEE217 Microeconomics Uncertainty: The share prices of Amazon and the difficulty of investment decisions Contingent consumption 1. What consumption or wealth will you get in each possible outcome

ANASH EQUILIBRIUM of a strategic game is an action profile in which every. Strategy Equilibrium

Draft chapter from An introduction to game theory by Martin J. Osborne. Version: 2002/7/23. Martin.Osborne@utoronto.ca http://www.economics.utoronto.ca/osborne Copyright 1995 2002 by Martin J. Osborne.

Draft chapter from An introduction to game theory by Martin J. Osborne. Version: 2002/7/23. Martin.Osborne@utoronto.ca http://www.economics.utoronto.ca/osborne Copyright 1995 2002 by Martin J. Osborne.

EconS Micro Theory I Recitation #8b - Uncertainty II

EconS 50 - Micro Theory I Recitation #8b - Uncertainty II. Exercise 6.E.: The purpose of this exercise is to show that preferences may not be transitive in the presence of regret. Let there be S states

EconS 50 - Micro Theory I Recitation #8b - Uncertainty II. Exercise 6.E.: The purpose of this exercise is to show that preferences may not be transitive in the presence of regret. Let there be S states

Department of Economics The Ohio State University Midterm Questions and Answers Econ 8712

Prof. James Peck Fall 06 Department of Economics The Ohio State University Midterm Questions and Answers Econ 87. (30 points) A decision maker (DM) is a von Neumann-Morgenstern expected utility maximizer.

Prof. James Peck Fall 06 Department of Economics The Ohio State University Midterm Questions and Answers Econ 87. (30 points) A decision maker (DM) is a von Neumann-Morgenstern expected utility maximizer.

Project Risk Analysis and Management Exercises (Part II, Chapters 6, 7)

") Project Risk Analysis and Management Exercises (Part II, Chapters 6, 7) Chapter II.6 Exercise 1 For the decision tree in Figure 1, assume Chance Events E and F are independent. a) Draw the appropriate

Project Risk Analysis and Management Exercises (Part II, Chapters 6, 7) Chapter II.6 Exercise 1 For the decision tree in Figure 1, assume Chance Events E and F are independent. a) Draw the appropriate

CS 4100 // artificial intelligence

CS 4100 // artificial intelligence instructor: byron wallace (Playing with) uncertainties and expectations Attribution: many of these slides are modified versions of those distributed with the UC Berkeley

CS 4100 // artificial intelligence instructor: byron wallace (Playing with) uncertainties and expectations Attribution: many of these slides are modified versions of those distributed with the UC Berkeley

UNCERTAINTY AND INFORMATION

UNCERTAINTY AND INFORMATION M. En C. Eduardo Bustos Farías 1 Objectives After studying this chapter, you will be able to: Explain how people make decisions when they are uncertain about the consequences

UNCERTAINTY AND INFORMATION M. En C. Eduardo Bustos Farías 1 Objectives After studying this chapter, you will be able to: Explain how people make decisions when they are uncertain about the consequences

05/05/2011. Degree of Risk. Degree of Risk. BUSA 4800/4810 May 5, Uncertainty

BUSA 4800/4810 May 5, 2011 Uncertainty We must believe in luck. For how else can we explain the success of those we don t like? Jean Cocteau Degree of Risk We incorporate risk and uncertainty into our

BUSA 4800/4810 May 5, 2011 Uncertainty We must believe in luck. For how else can we explain the success of those we don t like? Jean Cocteau Degree of Risk We incorporate risk and uncertainty into our

ANSWERS TO PRACTICE PROBLEMS oooooooooooooooo

University of California, Davis Department of Economics Giacomo Bonanno Economics 03: Economics of uncertainty and information TO PRACTICE PROBLEMS oooooooooooooooo PROBLEM # : The expected value of the

University of California, Davis Department of Economics Giacomo Bonanno Economics 03: Economics of uncertainty and information TO PRACTICE PROBLEMS oooooooooooooooo PROBLEM # : The expected value of the

Utilities and Decision Theory. Lirong Xia

Utilities and Decision Theory Lirong Xia Checking conditional independence from BN graph ØGiven random variables Z 1, Z p, we are asked whether X Y Z 1, Z p dependent if there exists a path where all triples

Utilities and Decision Theory Lirong Xia Checking conditional independence from BN graph ØGiven random variables Z 1, Z p, we are asked whether X Y Z 1, Z p dependent if there exists a path where all triples

FINC3017: Investment and Portfolio Management

FINC3017: Investment and Portfolio Management Investment Funds Topic 1: Introduction Unit Trusts: investor s funds are pooled, usually into specific types of assets. o Investors are assigned tradeable

FINC3017: Investment and Portfolio Management Investment Funds Topic 1: Introduction Unit Trusts: investor s funds are pooled, usually into specific types of assets. o Investors are assigned tradeable

Topic Four Utility optimization and stochastic dominance for investment decisions. 4.1 Optimal long-term investment criterion log utility criterion

MATH4512 Fundamentals of Mathematical Finance Topic Four Utility optimization and stochastic dominance for investment decisions 4.1 Optimal long-term investment criterion log utility criterion 4.2 Axiomatic

MATH4512 Fundamentals of Mathematical Finance Topic Four Utility optimization and stochastic dominance for investment decisions 4.1 Optimal long-term investment criterion log utility criterion 4.2 Axiomatic

E&G, Chap 10 - Utility Analysis; the Preference Structure, Uncertainty - Developing Indifference Curves in {E(R),σ(R)} Space.

,σ(R)} Space.") 1 E&G, Chap 10 - Utility Analysis; the Preference Structure, Uncertainty - Developing Indifference Curves in {E(R),σ(R)} Space. A. Overview. c 2 1. With Certainty, objects of choice (c 1, c 2 ) 2. With

1 E&G, Chap 10 - Utility Analysis; the Preference Structure, Uncertainty - Developing Indifference Curves in {E(R),σ(R)} Space. A. Overview. c 2 1. With Certainty, objects of choice (c 1, c 2 ) 2. With

CHAPTER 6: RISK AVERSION AND CAPITAL ALLOCATION TO RISKY ASSETS

CHAPTER 6: RISK AVERSION AND CAPITAL ALLOCATION TO RISKY ASSETS 1. a. The expected cash flow is: (0.5 $70,000) + (0.5 00,000) = $135,000 With a risk premium of 8% over the risk-free rate of 6%, the required

CHAPTER 6: RISK AVERSION AND CAPITAL ALLOCATION TO RISKY ASSETS 1. a. The expected cash flow is: (0.5 $70,000) + (0.5 00,000) = $135,000 With a risk premium of 8% over the risk-free rate of 6%, the required

that internalizes the constraint by solving to remove the y variable. 1. Using the substitution method, determine the utility function U( x)

") For the next two questions, the consumer s utility U( x, y) 3x y 4xy depends on the consumption of two goods x and y. Assume the consumer selects x and y to maximize utility subject to the budget constraint

For the next two questions, the consumer s utility U( x, y) 3x y 4xy depends on the consumption of two goods x and y. Assume the consumer selects x and y to maximize utility subject to the budget constraint

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes,

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes, resource costs, and utility. A) Decision tree B) Graphs

1. A is a decision support tool that uses a tree-like graph or model of decisions and their possible consequences, including chance event outcomes, resource costs, and utility. A) Decision tree B) Graphs

TECHNIQUES FOR DECISION MAKING IN RISKY CONDITIONS

RISK AND UNCERTAINTY THREE ALTERNATIVE STATES OF INFORMATION CERTAINTY - where the decision maker is perfectly informed in advance about the outcome of their decisions. For each decision there is only

RISK AND UNCERTAINTY THREE ALTERNATIVE STATES OF INFORMATION CERTAINTY - where the decision maker is perfectly informed in advance about the outcome of their decisions. For each decision there is only

Risk Aversion, Stochastic Dominance, and Rules of Thumb: Concept and Application

Risk Aversion, Stochastic Dominance, and Rules of Thumb: Concept and Application Vivek H. Dehejia Carleton University and CESifo Email: vdehejia@ccs.carleton.ca January 14, 2008 JEL classification code:

Risk Aversion, Stochastic Dominance, and Rules of Thumb: Concept and Application Vivek H. Dehejia Carleton University and CESifo Email: vdehejia@ccs.carleton.ca January 14, 2008 JEL classification code: