Advanced Risk Management

|

|

|

- Darlene Woods

- 6 years ago

- Views:

Transcription

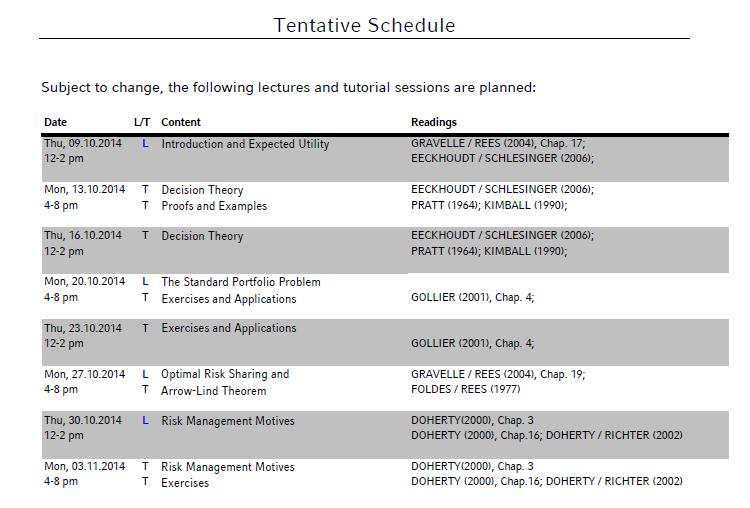

1 Winter 2014/2015 Advanced Risk Management Part I: Decision Theory and Risk Management Motives Lecture 1: Introduction and Expected Utility

2 Your Instructors for Part I: Prof. Dr. Andreas Richter Jun.-Prof. Dr. Richard Peter Office hour: By appointment Time & Location: Thursday, 12-2pm, M 110 Monday, 4-8pm, A 125 1

3 Course Outline Part I (Richter/Peter) Part I: Decision Theory and Risk Management Motives: Introduction and Expected Utility The Standard Portfolio Problem Optimal Risk Sharing and Arrow-Lind Theorem Risk Management Motives 2

4 Course Outline Parts II & III (Glaser, Elsas) Institute for Risk Management and Insurance Part II: Part III: Market Risk: Overview VaR-Methods I VaR-Methods II Hedging Credit Risk: Overview/Introduction Probability of Default/Rating Asset-/Default-Correlation Credit-Portfolio Models Backup/Review Session 3

5 Course outline - Part I 4

6 Course materials are available at: How to navigate to the website: Lehre Winter 2014/2015 Advanced Risk Management The password for protected files is: 5

7 6

8 7

9 Master level classes at the INRIVER 8

10 Master level classes at the INRIVER 9

risks")

11 Risk as an interdisciplinary subject Economics Cost-benefit analysis under risk Behavior of economic agents under risk Risk Mathematics Stochastics and probability theory Mathematical statistics Health care Risks to health (Multiplicative) risks associated with treatment Decision theory Risk attitudes Decision-making under risk and uncertainty Psychology Risk perception Cognitive processes 10

Speculative Risk Describes a situation in which there is a possibility of loss but also a possibility of gain.")

12 Definition and classification of risk Risk can be defined as the possibility of a (positive or negative) deviation from the expected outcome. (Ambivalent risk definition) Speculative Risk Describes a situation in which there is a possibility of loss but also a possibility of gain. Examples: Gambling Stock market investments Annual profit or loss of a company Pure Risk Describes a situation in which there is only the possibility of a loss, i.e. the possible outcomes are either loss or noloss. Examples: Personal risks: loss of income or assets Property risk: destruction, theft or damage of property Liability risk Risks arising from failure of others 11

![Risk management Risk management [in the traditional sense] is a scientific](/docs-images/74/70470466/images/13-3.jpg "approach to dealing with pure risk by anticipating possible accidental losses")

")

13 Risk management Risk management [in the traditional sense] is a scientific approach to dealing with pure risk by anticipating possible accidental losses and designing and implementing procedures that minimize the occurrence of loss or the financial impact of the losses that do occur. (Vaughan/Vaughan 2003) Risk management instruments Risk control: Risk avoidance Risk reduction Risk financing: Risk retention (active or passive) Risk transfer (e.g. to an insurer) 12

14 Risk management - Individual decision-making Institute for Risk Management and Insurance How can we evaluate risk? More specifically, how can we model decision-making in the face of risk? A workhorse model for decision-making under risk is expected utility theory (EUT) which has been applied to a multitude of problems. We will analyze properties of EUT in this lecture. Then, we will apply it to individual decision-making and exploit it to re-evaluate portfolio choice. The next level is to analyze how two or more individuals deal with risk, i.e., risk sharing and diversification. Finally, we will analyze corporate risk management decisions. 13

15 Expected utility theory A basic model Components A ( a 1,, a m ) Action space Set of all risky alternatives S { s 1,, s n } State space Set of all potential and relevant states Z Outcome space Set of all possible outcomes Outcome function f : A S Z maps every possible combination to an outcome f(a,s)=z 14

16 Decision matrix s 1 s 2 s m a 1 z 11 z 12 z 1. z 1m a 2 z 21 z 22 z 2. z 2m z.1 z.2 z.. z.m a n z n1 z n2 z n. z nm In this setup, an action a i implies the associated outcome random variable (or lottery ) z i (often also written as {(z i1, p 1 ),, (z im, p m )}). 15

17 Expected utility axioms i. Ordering Axiom: The decision maker can order all possible actions, i.e. a complete weak preference relation exists over A. For any three random variables z ~, z ~, z~ it holds that a) z~ z~ z~ ~ z ~ z~ z~ b) z~ z~ z~ z~ z~ z~ (Comparability, Completeness) (Transitivity) ii. Continuity Axiom: For any set of outcomes ~ z with ~ ~ ~ z, there is a probability p such that 1, ~ z2, ~ z 3 z1 z2 3 ~ z2 ~ ~ ~ { z1 p z3 }. 16

18 Expected utility axioms iii. Independence Axiom: Given two random variables ~z 1 and ~z 2 such that z~ ( ) ~. 1 z 2 Let ~z 3 be another random variable and let p be an arbitrary probability with Then, it holds that ~ ~ ~ ~ z p z ( ) z p z3 p (0,1). 17

19 Expected Utility Theorem Suppose that the decision-maker has preferences over all lotteries that are rationale and satisfy continuity and independence. Then, this preference relation can be represented by a preference functional that is linear in probabilities. This is, there is a utility function over outcomes which measures the wellbeing of the consumer and we can determine the consumer s satisfaction by evaluating the expected utility of a particular lottery. In other words: The decision-maker chooses the action that maximizes expected utility. 18

20 Expected Utility Theorem The expected utility theorem (among other things) provides the existence of the utility function. The utility function is also called Bernoulli utility function. Obtaining a Bernoulli utility function can be a challenging task in a real life situation. It is unique up to a positive affine transformation Why? In other words, utility in EUT is ordinal. 19

differential equations. the St. Petersburg Paradox. He proposed to use a utility function to evaluate risky gambles. This resolves the original St.")

21 Daniel Bernoulli February 8, 1700 (Groningen) - March 17, 1782 (Basel) Swiss mathematician and physicist He worked on the mechanics of fluids. (Strömungsmechanik) differential equations. the St. Petersburg Paradox. He proposed to use a utility function to evaluate risky gambles. This resolves the original St. Petersburg Paradox. 20

~ z. (Note: Risk aversion does not mean that a decision-maker avoids every risk!")

22 Bernoulli utility functions and risk attitudes Institute for Risk Management and Insurance A risk-averse decision-maker prefers a certain payment to a (non-trivial) lottery with an expected value equal to the certain payment, i.e. E( ~ z ) ~ z. (Note: Risk aversion does not mean that a decision-maker avoids every risk!) In the expected utility context this translates to u( E( ~ z )) E( u( ~ z )). By Jensen s Inequality it follows that: u( E( z ~ )) E( u( z ~ )) ~ z, concave. for any non-trivial random variable if and only if u is strictly 21

23 The mathematical notion of concavity A function of one variable is concave if f ( tx (1 t) y) tf ( x) (1 t) f ( y) for all x and y and all t with 0 t 1. Graphically: u(z) Analytically: A function is concave if and only if f (x) 0 for all x. z Roughly speaking, a concave function grows more slowly than a linear function. 22

24 The mathematical notion of concavity A function of one variable is strictly concave if f ( tx (1 t) y) tf ( x) (1 t) f ( y) for all x and y and all t with 0 t 1. Analytically: A function is strictly concave if f (x) < 0 for all x. We can define convexity analogously. 23

25 Bernoulli utility functions and risk attitudes Institute for Risk Management and Insurance A risk-averse decision-maker prefers a certain payment to a (non-trivial) lottery with an expected value equal to the certain payment, i.e. E( ~ z ) ~ z. In the expected utility context this translates to u( E( ~ z )) E( u( ~ z )). This holds for all non-trivial risks if and only if u is strictly concave. A decision-maker is risk-loving if and only u( E( ~ z )) E( u( ~ z )). This holds for all non-trivial risks if and only if u is strictly convex. A decision-maker is risk-neutral if and only if u( E( ~ z )) E( u( ~ z )). This holds for all non-trivial risks if and only if u is linear. 24

26 Bernoulli utility functions and risk attitudes Institute for Risk Management and Insurance Linear utility functions imply risk-neutrality for instance u1( z) z (Strictly) convex utility functions imply a risk-loving attitude for instance 2 u2( z) z, z 0 (Strictly) concave utility functions imply risk-aversion for instance u3( z) z, z 0 25

27 Bernoulli utility functions and risk attitudes u 0 strictly convex u 0 linear u 0 strictly concave u 0 u(z) u 2 (z) u 1 (z) u 3 (z) z 26

28 Measures of risk aversion We can measure the intensity of a decision-maker s risk aversion. Consider a decision-maker with utility function u(z). The Arrow-Pratt measure of absolute risk aversion is defined as The Arrow-Pratt measure of relative risk aversion is defined as r R u''( z) r A ( z). u'( z) u''( z) ( z) z. u'( z) Both measures are local measures of risk aversion. 27

r A ( z). u'( z) u''( z) ( z) z.")

29 Measures of risk aversion We can measure the intensity of a decision-maker s risk aversion. Consider a decision-maker with utility function u(z). The Arrow-Pratt measure of absolute risk aversion is defined as The Arrow-Pratt measure of relative risk aversion is defined as r R u''( z) r A ( z). u'( z) u''( z) ( z) z. u'( z) Both measures are local measures of risk aversion. Why? 28

30 Your own degree of risk aversion Consider that you either gain or lose 10% of your wealth with equal probability (1/2). What is the share of your wealth,, you are willing to pay to escape this risk? Take your time to think about the problem and take down your answer. 29

31 Your own degree of risk aversion Under the assumption of constant relative risk aversion with parameter we have that We can solve for and obtain ( ) (1 )

32 Your own degree of risk aversion This is depicted in the following figure: RRA = = = = =

33 State-by-state dominance Lottery A dominates lottery B state-by-state if A yields a better outcome than B in every possible state of nature. Example: s 1 s 2 s 3 A B

34 First-order stochastic dominance Cumulative distribution function F A ( ) first-order stochastically dominates cumulative distribution function F B ( ) ( F for all z with F ( z ) F ( z ) for some z. A B A ( ) FSD F ( ) B ) if and only if F A ( z ) F B ( z ) Lottery A first-order stochastically dominates B, if for any outcome z the likelihood of receiving an outcome equal to or better than z is greater for A than for B. 33

35 First-order stochastic dominance F A ( ) FSD F B ( ) F(z) 1 F B F A z z max 34

36 First-order stochastic dominance Example EUR Likelihood (Lottery B) Likelihood (Lottery A) F(z) , , , EUR 35

37 First-order stochastic dominance First-order stochastic dominance theorem: F A ( ) F ( ) FSD B and u 0 E u E u. A B If distribution A first-order stochastically dominates B, any expected utility maximizing individual with positive marginal utility will prefer A to B. 36

38 First-order stochastic dominance First-order stochastic dominance theorem: F A ( ) F ( ) FSD B and u 0 E u E u. A B If distribution A first-order stochastically dominates B, any expected utility maximizing individual with positive marginal utility will prefer A to B. Proof? 37

39 Second-order stochastic dominance As a prerequisite define the area under the cumulative distribution function F up to z: T ( z) F( x) dx z Cumulative distribution function F A ( ) second-order stochastically dominates cumulative distribution function F B ( ) ( F for all z with T ( z) T ( z) for some z. A B A ( ) F ( ) SSD B ) if and only if T A ( z) T ( z) B First-order stochastic dominance implies second-order stochastic dominance. 38

40 Second-order stochastic dominance As a prerequisite define the area under the cumulative distribution function F up to z: T ( z) F( x) dx z Cumulative distribution function F A ( ) second-order stochastically dominates cumulative distribution function F B ( ) ( F for all z with T ( z) T ( z) for some z. A B A ( ) F ( ) SSD B ) if and only if T A ( z) T ( z) B First-order stochastic dominance implies second-order stochastic dominance. Why? 39

41 Second-order stochastic dominance EUR Likelihood (Lottery A) Likelihood (Lottery B) F(z) , , , EUR 40

42 Second-order stochastic dominance Second-order stochastic dominance theorem: F A ( ) F ( ) SSD B and u 0, u'' 0 E u E u. A B If F A second-order stochastically dominates F B, then every expected utility maximizer with positive and decreasing marginal utility prefers F A to F B. 41

43 Application: The merits of diversification Assume that there are n assets that are assumed to be i.i.d. ~ x 1 2 n, ~ x,, ~ x. A feasible strategy is characterized by a vector A = ( 1,, n ) where i is one s share in the ith asset, and This yields a net payoff of n i 1 1. The perfect diversification strategy is given by i ~ y n ~. i 1 ix i 1 1 A,,. n n The distribution of final wealth generated by the perfect diversification strategy second-order stochastically dominates any other feasible strategy 42

Advanced Risk Management

Winter 2012/2013 Advanced Risk Management Part I: Decision Theory & Risk Management Motives Lecture 1: Introduction & Review Teaching Staff for Part I : Dr. Yunjie (Winnie) Sun Email: sun@bwl.lmu.de Office

Winter 2012/2013 Advanced Risk Management Part I: Decision Theory & Risk Management Motives Lecture 1: Introduction & Review Teaching Staff for Part I : Dr. Yunjie (Winnie) Sun Email: sun@bwl.lmu.de Office

Comparison of Payoff Distributions in Terms of Return and Risk

Comparison of Payoff Distributions in Terms of Return and Risk Preliminaries We treat, for convenience, money as a continuous variable when dealing with monetary outcomes. Strictly speaking, the derivation

Comparison of Payoff Distributions in Terms of Return and Risk Preliminaries We treat, for convenience, money as a continuous variable when dealing with monetary outcomes. Strictly speaking, the derivation

Choice under risk and uncertainty

Choice under risk and uncertainty Introduction Up until now, we have thought of the objects that our decision makers are choosing as being physical items However, we can also think of cases where the outcomes

Choice under risk and uncertainty Introduction Up until now, we have thought of the objects that our decision makers are choosing as being physical items However, we can also think of cases where the outcomes

Expected Utility and Risk Aversion

Expected Utility and Risk Aversion Expected utility and risk aversion 1/ 58 Introduction Expected utility is the standard framework for modeling investor choices. The following topics will be covered:

Expected Utility and Risk Aversion Expected utility and risk aversion 1/ 58 Introduction Expected utility is the standard framework for modeling investor choices. The following topics will be covered:

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

If U is linear, then U[E(Ỹ )] = E[U(Ỹ )], and one is indifferent between lottery and its expectation. One is called risk neutral.

![If U is linear, then U[E(Ỹ )] = E[U(Ỹ )], and one is indifferent between lottery and its expectation. One is called risk neutral.](/thumbs/90/104465976.jpg "If U is linear, then U[E(Ỹ )] = E[U(Ỹ )], and one is indifferent between lottery and its expectation. One is called risk neutral.") Risk aversion For those preference orderings which (i.e., for those individuals who) satisfy the seven axioms, define risk aversion. Compare a lottery Ỹ = L(a, b, π) (where a, b are fixed monetary outcomes)

Risk aversion For those preference orderings which (i.e., for those individuals who) satisfy the seven axioms, define risk aversion. Compare a lottery Ỹ = L(a, b, π) (where a, b are fixed monetary outcomes)

Risk aversion and choice under uncertainty

Risk aversion and choice under uncertainty Pierre Chaigneau pierre.chaigneau@hec.ca June 14, 2011 Finance: the economics of risk and uncertainty In financial markets, claims associated with random future

Risk aversion and choice under uncertainty Pierre Chaigneau pierre.chaigneau@hec.ca June 14, 2011 Finance: the economics of risk and uncertainty In financial markets, claims associated with random future

Characterization of the Optimum

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

Comparative Risk Sensitivity with Reference-Dependent Preferences

The Journal of Risk and Uncertainty, 24:2; 131 142, 2002 2002 Kluwer Academic Publishers. Manufactured in The Netherlands. Comparative Risk Sensitivity with Reference-Dependent Preferences WILLIAM S. NEILSON

The Journal of Risk and Uncertainty, 24:2; 131 142, 2002 2002 Kluwer Academic Publishers. Manufactured in The Netherlands. Comparative Risk Sensitivity with Reference-Dependent Preferences WILLIAM S. NEILSON

Expected Utility And Risk Aversion

Expected Utility And Risk Aversion Econ 2100 Fall 2017 Lecture 12, October 4 Outline 1 Risk Aversion 2 Certainty Equivalent 3 Risk Premium 4 Relative Risk Aversion 5 Stochastic Dominance Notation From

Expected Utility And Risk Aversion Econ 2100 Fall 2017 Lecture 12, October 4 Outline 1 Risk Aversion 2 Certainty Equivalent 3 Risk Premium 4 Relative Risk Aversion 5 Stochastic Dominance Notation From

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty We always need to make a decision (or select from among actions, options or moves) even when there exists

Models and Decision with Financial Applications UNIT 1: Elements of Decision under Uncertainty We always need to make a decision (or select from among actions, options or moves) even when there exists

Module 1: Decision Making Under Uncertainty

Module 1: Decision Making Under Uncertainty Information Economics (Ec 515) George Georgiadis Today, we will study settings in which decision makers face uncertain outcomes. Natural when dealing with asymmetric

Module 1: Decision Making Under Uncertainty Information Economics (Ec 515) George Georgiadis Today, we will study settings in which decision makers face uncertain outcomes. Natural when dealing with asymmetric

Lecture 6 Introduction to Utility Theory under Certainty and Uncertainty

Lecture 6 Introduction to Utility Theory under Certainty and Uncertainty Prof. Massimo Guidolin Prep Course in Quant Methods for Finance August-September 2017 Outline and objectives Axioms of choice under

Lecture 6 Introduction to Utility Theory under Certainty and Uncertainty Prof. Massimo Guidolin Prep Course in Quant Methods for Finance August-September 2017 Outline and objectives Axioms of choice under

ECON Financial Economics

ECON 8 - Financial Economics Michael Bar August, 0 San Francisco State University, department of economics. ii Contents Decision Theory under Uncertainty. Introduction.....................................

ECON 8 - Financial Economics Michael Bar August, 0 San Francisco State University, department of economics. ii Contents Decision Theory under Uncertainty. Introduction.....................................

Micro Theory I Assignment #5 - Answer key

Micro Theory I Assignment #5 - Answer key 1. Exercises from MWG (Chapter 6): (a) Exercise 6.B.1 from MWG: Show that if the preferences % over L satisfy the independence axiom, then for all 2 (0; 1) and

Micro Theory I Assignment #5 - Answer key 1. Exercises from MWG (Chapter 6): (a) Exercise 6.B.1 from MWG: Show that if the preferences % over L satisfy the independence axiom, then for all 2 (0; 1) and

Expected utility theory; Expected Utility Theory; risk aversion and utility functions

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

; Expected Utility Theory; risk aversion and utility functions Prof. Massimo Guidolin Portfolio Management Spring 2016 Outline and objectives Utility functions The expected utility theorem and the axioms

ECON 581. Decision making under risk. Instructor: Dmytro Hryshko

ECON 581. Decision making under risk Instructor: Dmytro Hryshko 1 / 36 Outline Expected utility Risk aversion Certainty equivalence and risk premium The canonical portfolio allocation problem 2 / 36 Suggested

ECON 581. Decision making under risk Instructor: Dmytro Hryshko 1 / 36 Outline Expected utility Risk aversion Certainty equivalence and risk premium The canonical portfolio allocation problem 2 / 36 Suggested

Lecture 3: Utility-Based Portfolio Choice

Lecture 3: Utility-Based Portfolio Choice Prof. Massimo Guidolin Portfolio Management Spring 2017 Outline and objectives Choice under uncertainty: dominance o Guidolin-Pedio, chapter 1, sec. 2 Choice under

Lecture 3: Utility-Based Portfolio Choice Prof. Massimo Guidolin Portfolio Management Spring 2017 Outline and objectives Choice under uncertainty: dominance o Guidolin-Pedio, chapter 1, sec. 2 Choice under

MICROECONOMIC THEROY CONSUMER THEORY

LECTURE 5 MICROECONOMIC THEROY CONSUMER THEORY Choice under Uncertainty (MWG chapter 6, sections A-C, and Cowell chapter 8) Lecturer: Andreas Papandreou 1 Introduction p Contents n Expected utility theory

LECTURE 5 MICROECONOMIC THEROY CONSUMER THEORY Choice under Uncertainty (MWG chapter 6, sections A-C, and Cowell chapter 8) Lecturer: Andreas Papandreou 1 Introduction p Contents n Expected utility theory

Chapter 6: Risky Securities and Utility Theory

Chapter 6: Risky Securities and Utility Theory Topics 1. Principle of Expected Return 2. St. Petersburg Paradox 3. Utility Theory 4. Principle of Expected Utility 5. The Certainty Equivalent 6. Utility

Chapter 6: Risky Securities and Utility Theory Topics 1. Principle of Expected Return 2. St. Petersburg Paradox 3. Utility Theory 4. Principle of Expected Utility 5. The Certainty Equivalent 6. Utility

Chapter 18: Risky Choice and Risk

Chapter 18: Risky Choice and Risk Risky Choice Probability States of Nature Expected Utility Function Interval Measure Violations Risk Preference State Dependent Utility Risk-Aversion Coefficient Actuarially

Chapter 18: Risky Choice and Risk Risky Choice Probability States of Nature Expected Utility Function Interval Measure Violations Risk Preference State Dependent Utility Risk-Aversion Coefficient Actuarially

Rational theories of finance tell us how people should behave and often do not reflect reality.

FINC3023 Behavioral Finance TOPIC 1: Expected Utility Rational theories of finance tell us how people should behave and often do not reflect reality. A normative theory based on rational utility maximizers

FINC3023 Behavioral Finance TOPIC 1: Expected Utility Rational theories of finance tell us how people should behave and often do not reflect reality. A normative theory based on rational utility maximizers

Problem Set 2. Theory of Banking - Academic Year Maria Bachelet March 2, 2017

Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmai.com March, 07 Exercise Consider an agency relationship in which the principal contracts the agent, whose effort

Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmai.com March, 07 Exercise Consider an agency relationship in which the principal contracts the agent, whose effort

Stat 6863-Handout 1 Economics of Insurance and Risk June 2008, Maurice A. Geraghty

A. The Psychology of Risk Aversion Stat 6863-Handout 1 Economics of Insurance and Risk June 2008, Maurice A. Geraghty Suppose a decision maker has an asset worth $100,000 that has a 1% chance of being

A. The Psychology of Risk Aversion Stat 6863-Handout 1 Economics of Insurance and Risk June 2008, Maurice A. Geraghty Suppose a decision maker has an asset worth $100,000 that has a 1% chance of being

Utility and Choice Under Uncertainty

Introduction to Microeconomics Utility and Choice Under Uncertainty The Five Axioms of Choice Under Uncertainty We can use the axioms of preference to show how preferences can be mapped into measurable

Introduction to Microeconomics Utility and Choice Under Uncertainty The Five Axioms of Choice Under Uncertainty We can use the axioms of preference to show how preferences can be mapped into measurable

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2017

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program August 2017

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program August 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program August 2017 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Intertemporal Risk Attitude. Lecture 7. Kreps & Porteus Preference for Early or Late Resolution of Risk

Intertemporal Risk Attitude Lecture 7 Kreps & Porteus Preference for Early or Late Resolution of Risk is an intrinsic preference for the timing of risk resolution is a general characteristic of recursive

Intertemporal Risk Attitude Lecture 7 Kreps & Porteus Preference for Early or Late Resolution of Risk is an intrinsic preference for the timing of risk resolution is a general characteristic of recursive

Making Hard Decision. ENCE 627 Decision Analysis for Engineering. Identify the decision situation and understand objectives. Identify alternatives

CHAPTER Duxbury Thomson Learning Making Hard Decision Third Edition RISK ATTITUDES A. J. Clark School of Engineering Department of Civil and Environmental Engineering 13 FALL 2003 By Dr. Ibrahim. Assakkaf

CHAPTER Duxbury Thomson Learning Making Hard Decision Third Edition RISK ATTITUDES A. J. Clark School of Engineering Department of Civil and Environmental Engineering 13 FALL 2003 By Dr. Ibrahim. Assakkaf

Attitudes Toward Risk. Joseph Tao-yi Wang 2013/10/16. (Lecture 11, Micro Theory I)

") Joseph Tao-yi Wang 2013/10/16 (Lecture 11, Micro Theory I) Dealing with Uncertainty 2 Preferences over risky choices (Section 7.1) One simple model: Expected Utility How can old tools be applied to analyze

Joseph Tao-yi Wang 2013/10/16 (Lecture 11, Micro Theory I) Dealing with Uncertainty 2 Preferences over risky choices (Section 7.1) One simple model: Expected Utility How can old tools be applied to analyze

Choice Under Uncertainty

Chapter 6 Choice Under Uncertainty Up until now, we have been concerned with choice under certainty. A consumer chooses which commodity bundle to consume. A producer chooses how much output to produce

Chapter 6 Choice Under Uncertainty Up until now, we have been concerned with choice under certainty. A consumer chooses which commodity bundle to consume. A producer chooses how much output to produce

FINC3017: Investment and Portfolio Management

FINC3017: Investment and Portfolio Management Investment Funds Topic 1: Introduction Unit Trusts: investor s funds are pooled, usually into specific types of assets. o Investors are assigned tradeable

FINC3017: Investment and Portfolio Management Investment Funds Topic 1: Introduction Unit Trusts: investor s funds are pooled, usually into specific types of assets. o Investors are assigned tradeable

Standard Risk Aversion and Efficient Risk Sharing

MPRA Munich Personal RePEc Archive Standard Risk Aversion and Efficient Risk Sharing Richard M. H. Suen University of Leicester 29 March 2018 Online at https://mpra.ub.uni-muenchen.de/86499/ MPRA Paper

MPRA Munich Personal RePEc Archive Standard Risk Aversion and Efficient Risk Sharing Richard M. H. Suen University of Leicester 29 March 2018 Online at https://mpra.ub.uni-muenchen.de/86499/ MPRA Paper

Chapter 1. Utility Theory. 1.1 Introduction

Chapter 1 Utility Theory 1.1 Introduction St. Petersburg Paradox (gambling paradox) the birth to the utility function http://policonomics.com/saint-petersburg-paradox/ The St. Petersburg paradox, is a

Chapter 1 Utility Theory 1.1 Introduction St. Petersburg Paradox (gambling paradox) the birth to the utility function http://policonomics.com/saint-petersburg-paradox/ The St. Petersburg paradox, is a

Financial Economics: Risk Aversion and Investment Decisions

Financial Economics: Risk Aversion and Investment Decisions Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY March, 2015 1 / 50 Outline Risk Aversion and Portfolio Allocation Portfolios, Risk Aversion,

Financial Economics: Risk Aversion and Investment Decisions Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY March, 2015 1 / 50 Outline Risk Aversion and Portfolio Allocation Portfolios, Risk Aversion,

Risk preferences and stochastic dominance

Risk preferences and stochastic dominance Pierre Chaigneau pierre.chaigneau@hec.ca September 5, 2011 Preferences and utility functions The expected utility criterion Future income of an agent: x. Random

Risk preferences and stochastic dominance Pierre Chaigneau pierre.chaigneau@hec.ca September 5, 2011 Preferences and utility functions The expected utility criterion Future income of an agent: x. Random

Notes 10: Risk and Uncertainty

Economics 335 April 19, 1999 A. Introduction Notes 10: Risk and Uncertainty 1. Basic Types of Uncertainty in Agriculture a. production b. prices 2. Examples of Uncertainty in Agriculture a. crop yields

Economics 335 April 19, 1999 A. Introduction Notes 10: Risk and Uncertainty 1. Basic Types of Uncertainty in Agriculture a. production b. prices 2. Examples of Uncertainty in Agriculture a. crop yields

ECONOMICS 100A: MICROECONOMICS

ECONOMICS 100A: MICROECONOMICS Fall 2013 Tues, Thur 2:00-3:20pm Center Hall 101 Professor Mark Machina Office: Econ Bldg 217 Office Hrs: Wed 9am-1pm ( See other side for Section times & locations, and

ECONOMICS 100A: MICROECONOMICS Fall 2013 Tues, Thur 2:00-3:20pm Center Hall 101 Professor Mark Machina Office: Econ Bldg 217 Office Hrs: Wed 9am-1pm ( See other side for Section times & locations, and

The mean-variance portfolio choice framework and its generalizations

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY PART ± I CHAPTER 1 CHAPTER 2 CHAPTER 3 Foundations of Finance I: Expected Utility Theory Foundations of Finance II: Asset Pricing, Market Efficiency,

CONVENTIONAL FINANCE, PROSPECT THEORY, AND MARKET EFFICIENCY PART ± I CHAPTER 1 CHAPTER 2 CHAPTER 3 Foundations of Finance I: Expected Utility Theory Foundations of Finance II: Asset Pricing, Market Efficiency,

Risk Aversion, Stochastic Dominance, and Rules of Thumb: Concept and Application

Risk Aversion, Stochastic Dominance, and Rules of Thumb: Concept and Application Vivek H. Dehejia Carleton University and CESifo Email: vdehejia@ccs.carleton.ca January 14, 2008 JEL classification code:

Risk Aversion, Stochastic Dominance, and Rules of Thumb: Concept and Application Vivek H. Dehejia Carleton University and CESifo Email: vdehejia@ccs.carleton.ca January 14, 2008 JEL classification code:

We examine the impact of risk aversion on bidding behavior in first-price auctions.

Risk Aversion We examine the impact of risk aversion on bidding behavior in first-price auctions. Assume there is no entry fee or reserve. Note: Risk aversion does not affect bidding in SPA because there,

Risk Aversion We examine the impact of risk aversion on bidding behavior in first-price auctions. Assume there is no entry fee or reserve. Note: Risk aversion does not affect bidding in SPA because there,

1. Expected utility, risk aversion and stochastic dominance

. Epected utility, risk aversion and stochastic dominance. Epected utility.. Description o risky alternatives.. Preerences over lotteries..3 The epected utility theorem. Monetary lotteries and risk aversion..

. Epected utility, risk aversion and stochastic dominance. Epected utility.. Description o risky alternatives.. Preerences over lotteries..3 The epected utility theorem. Monetary lotteries and risk aversion..

A. Introduction to choice under uncertainty 2. B. Risk aversion 11. C. Favorable gambles 15. D. Measures of risk aversion 20. E.

Microeconomic Theory -1- Uncertainty Choice under uncertainty A Introduction to choice under uncertainty B Risk aversion 11 C Favorable gambles 15 D Measures of risk aversion 0 E Insurance 6 F Small favorable

Microeconomic Theory -1- Uncertainty Choice under uncertainty A Introduction to choice under uncertainty B Risk aversion 11 C Favorable gambles 15 D Measures of risk aversion 0 E Insurance 6 F Small favorable

Optimizing Portfolios

Optimizing Portfolios An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Investors may wish to adjust the allocation of financial resources including a mixture

Optimizing Portfolios An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Investors may wish to adjust the allocation of financial resources including a mixture

Microeconomic Theory May 2013 Applied Economics. Ph.D. PRELIMINARY EXAMINATION MICROECONOMIC THEORY. Applied Economics Graduate Program.

Ph.D. PRELIMINARY EXAMINATION MICROECONOMIC THEORY Applied Economics Graduate Program May 2013 *********************************************** COVER SHEET ***********************************************

Ph.D. PRELIMINARY EXAMINATION MICROECONOMIC THEORY Applied Economics Graduate Program May 2013 *********************************************** COVER SHEET ***********************************************

STOCHASTIC CONSUMPTION-SAVINGS MODEL: CANONICAL APPLICATIONS FEBRUARY 19, 2013

STOCHASTIC CONSUMPTION-SAVINGS MODEL: CANONICAL APPLICATIONS FEBRUARY 19, 2013 Model Structure EXPECTED UTILITY Preferences v(c 1, c 2 ) with all the usual properties Lifetime expected utility function

STOCHASTIC CONSUMPTION-SAVINGS MODEL: CANONICAL APPLICATIONS FEBRUARY 19, 2013 Model Structure EXPECTED UTILITY Preferences v(c 1, c 2 ) with all the usual properties Lifetime expected utility function

E&G, Chap 10 - Utility Analysis; the Preference Structure, Uncertainty - Developing Indifference Curves in {E(R),σ(R)} Space.

,σ(R)} Space.") 1 E&G, Chap 10 - Utility Analysis; the Preference Structure, Uncertainty - Developing Indifference Curves in {E(R),σ(R)} Space. A. Overview. c 2 1. With Certainty, objects of choice (c 1, c 2 ) 2. With

1 E&G, Chap 10 - Utility Analysis; the Preference Structure, Uncertainty - Developing Indifference Curves in {E(R),σ(R)} Space. A. Overview. c 2 1. With Certainty, objects of choice (c 1, c 2 ) 2. With

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

EconS Micro Theory I Recitation #8b - Uncertainty II

EconS 50 - Micro Theory I Recitation #8b - Uncertainty II. Exercise 6.E.: The purpose of this exercise is to show that preferences may not be transitive in the presence of regret. Let there be S states

EconS 50 - Micro Theory I Recitation #8b - Uncertainty II. Exercise 6.E.: The purpose of this exercise is to show that preferences may not be transitive in the presence of regret. Let there be S states

Behavioral Finance Driven Investment Strategies

Behavioral Finance Driven Investment Strategies Prof. Dr. Rudi Zagst, Technical University of Munich joint work with L. Brummer, M. Escobar, A. Lichtenstern, M. Wahl 1 Behavioral Finance Driven Investment

Behavioral Finance Driven Investment Strategies Prof. Dr. Rudi Zagst, Technical University of Munich joint work with L. Brummer, M. Escobar, A. Lichtenstern, M. Wahl 1 Behavioral Finance Driven Investment

Department of Economics The Ohio State University Midterm Questions and Answers Econ 8712

Prof. James Peck Fall 06 Department of Economics The Ohio State University Midterm Questions and Answers Econ 87. (30 points) A decision maker (DM) is a von Neumann-Morgenstern expected utility maximizer.

Prof. James Peck Fall 06 Department of Economics The Ohio State University Midterm Questions and Answers Econ 87. (30 points) A decision maker (DM) is a von Neumann-Morgenstern expected utility maximizer.

KIER DISCUSSION PAPER SERIES

KIER DISCUSSION PAPER SERIES KYOTO INSTITUTE OF ECONOMIC RESEARCH http://www.kier.kyoto-u.ac.jp/index.html Discussion Paper No. 657 The Buy Price in Auctions with Discrete Type Distributions Yusuke Inami

KIER DISCUSSION PAPER SERIES KYOTO INSTITUTE OF ECONOMIC RESEARCH http://www.kier.kyoto-u.ac.jp/index.html Discussion Paper No. 657 The Buy Price in Auctions with Discrete Type Distributions Yusuke Inami

Consumption and Asset Pricing

Consumption and Asset Pricing Yin-Chi Wang The Chinese University of Hong Kong November, 2012 References: Williamson s lecture notes (2006) ch5 and ch 6 Further references: Stochastic dynamic programming:

Consumption and Asset Pricing Yin-Chi Wang The Chinese University of Hong Kong November, 2012 References: Williamson s lecture notes (2006) ch5 and ch 6 Further references: Stochastic dynamic programming:

Universal Portfolios

CS28B/Stat24B (Spring 2008) Statistical Learning Theory Lecture: 27 Universal Portfolios Lecturer: Peter Bartlett Scribes: Boriska Toth and Oriol Vinyals Portfolio optimization setting Suppose we have

CS28B/Stat24B (Spring 2008) Statistical Learning Theory Lecture: 27 Universal Portfolios Lecturer: Peter Bartlett Scribes: Boriska Toth and Oriol Vinyals Portfolio optimization setting Suppose we have

Advanced Financial Economics Homework 2 Due on April 14th before class

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

BEEM109 Experimental Economics and Finance

University of Exeter Recap Last class we looked at the axioms of expected utility, which defined a rational agent as proposed by von Neumann and Morgenstern. We then proceeded to look at empirical evidence

University of Exeter Recap Last class we looked at the axioms of expected utility, which defined a rational agent as proposed by von Neumann and Morgenstern. We then proceeded to look at empirical evidence

Mossin s Theorem for Upper-Limit Insurance Policies

Mossin s Theorem for Upper-Limit Insurance Policies Harris Schlesinger Department of Finance, University of Alabama, USA Center of Finance & Econometrics, University of Konstanz, Germany E-mail: hschlesi@cba.ua.edu

Mossin s Theorem for Upper-Limit Insurance Policies Harris Schlesinger Department of Finance, University of Alabama, USA Center of Finance & Econometrics, University of Konstanz, Germany E-mail: hschlesi@cba.ua.edu

Microeconomics of Banking: Lecture 3

Microeconomics of Banking: Lecture 3 Prof. Ronaldo CARPIO Oct. 9, 2015 Review of Last Week Consumer choice problem General equilibrium Contingent claims Risk aversion The optimal choice, x = (X, Y ), is

Microeconomics of Banking: Lecture 3 Prof. Ronaldo CARPIO Oct. 9, 2015 Review of Last Week Consumer choice problem General equilibrium Contingent claims Risk aversion The optimal choice, x = (X, Y ), is

Asymmetric Information: Walrasian Equilibria, and Rational Expectations Equilibria

Asymmetric Information: Walrasian Equilibria and Rational Expectations Equilibria 1 Basic Setup Two periods: 0 and 1 One riskless asset with interest rate r One risky asset which pays a normally distributed

Asymmetric Information: Walrasian Equilibria and Rational Expectations Equilibria 1 Basic Setup Two periods: 0 and 1 One riskless asset with interest rate r One risky asset which pays a normally distributed

Citation for published version (APA): Oosterhof, C. M. (2006). Essays on corporate risk management and optimal hedging s.n.

: Oosterhof, C. M. (2006). Essays on corporate risk management and optimal hedging s.n.") University of Groningen Essays on corporate risk management and optimal hedging Oosterhof, Casper Martijn IMPORTANT NOTE: You are advised to consult the publisher's version (publisher's PDF) if you wish

University of Groningen Essays on corporate risk management and optimal hedging Oosterhof, Casper Martijn IMPORTANT NOTE: You are advised to consult the publisher's version (publisher's PDF) if you wish

Topics in Contract Theory Lecture 5. Property Rights Theory. The key question we are staring from is: What are ownership/property rights?

Leonardo Felli 15 January, 2002 Topics in Contract Theory Lecture 5 Property Rights Theory The key question we are staring from is: What are ownership/property rights? For an answer we need to distinguish

Leonardo Felli 15 January, 2002 Topics in Contract Theory Lecture 5 Property Rights Theory The key question we are staring from is: What are ownership/property rights? For an answer we need to distinguish

1 Consumption and saving under uncertainty

1 Consumption and saving under uncertainty 1.1 Modelling uncertainty As in the deterministic case, we keep assuming that agents live for two periods. The novelty here is that their earnings in the second

1 Consumption and saving under uncertainty 1.1 Modelling uncertainty As in the deterministic case, we keep assuming that agents live for two periods. The novelty here is that their earnings in the second

Models & Decision with Financial Applications Unit 3: Utility Function and Risk Attitude

Models & Decision with Financial Applications Unit 3: Utility Function and Risk Attitude Duan LI Department of Systems Engineering & Engineering Management The Chinese University of Hong Kong http://www.se.cuhk.edu.hk/

Models & Decision with Financial Applications Unit 3: Utility Function and Risk Attitude Duan LI Department of Systems Engineering & Engineering Management The Chinese University of Hong Kong http://www.se.cuhk.edu.hk/

ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty

![ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty](/thumbs/83/88403560.jpg "ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty") ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

ECONOMICS 100A: MICROECONOMICS

ECONOMICS 100A: MICROECONOMICS Summer Session II 2011 Tues, Thur 8:00-10:50am Center Hall 214 Professor Mark Machina Office: Econ Bldg 217 Office Hrs: Tu/Th 11:30-1:30 TA: Michael Futch Office: Sequoyah

ECONOMICS 100A: MICROECONOMICS Summer Session II 2011 Tues, Thur 8:00-10:50am Center Hall 214 Professor Mark Machina Office: Econ Bldg 217 Office Hrs: Tu/Th 11:30-1:30 TA: Michael Futch Office: Sequoyah

Investment and Portfolio Management. Lecture 1: Managed funds fall into a number of categories that pool investors funds

Lecture 1: Managed funds fall into a number of categories that pool investors funds Types of managed funds: Unit trusts Investors funds are pooled, usually into specific types of assets Investors are assigned

Lecture 1: Managed funds fall into a number of categories that pool investors funds Types of managed funds: Unit trusts Investors funds are pooled, usually into specific types of assets Investors are assigned

Advanced Microeconomic Theory

Advanced Microeconomic Theory Lecture Notes Sérgio O. Parreiras Fall, 2016 Outline Mathematical Toolbox Decision Theory Partial Equilibrium Search Intertemporal Consumption General Equilibrium Financial

Advanced Microeconomic Theory Lecture Notes Sérgio O. Parreiras Fall, 2016 Outline Mathematical Toolbox Decision Theory Partial Equilibrium Search Intertemporal Consumption General Equilibrium Financial

PORTFOLIO THEORY. Master in Finance INVESTMENTS. Szabolcs Sebestyén

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

Uncertainty in Equilibrium

Uncertainty in Equilibrium Larry Blume May 1, 2007 1 Introduction The state-preference approach to uncertainty of Kenneth J. Arrow (1953) and Gérard Debreu (1959) lends itself rather easily to Walrasian

Uncertainty in Equilibrium Larry Blume May 1, 2007 1 Introduction The state-preference approach to uncertainty of Kenneth J. Arrow (1953) and Gérard Debreu (1959) lends itself rather easily to Walrasian

A Preference Foundation for Fehr and Schmidt s Model. of Inequity Aversion 1

A Preference Foundation for Fehr and Schmidt s Model of Inequity Aversion 1 Kirsten I.M. Rohde 2 January 12, 2009 1 The author would like to thank Itzhak Gilboa, Ingrid M.T. Rohde, Klaus M. Schmidt, and

A Preference Foundation for Fehr and Schmidt s Model of Inequity Aversion 1 Kirsten I.M. Rohde 2 January 12, 2009 1 The author would like to thank Itzhak Gilboa, Ingrid M.T. Rohde, Klaus M. Schmidt, and

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

AMS Portfolio Theory and Capital Markets

AMS 69.0 - Portfolio Theory and Capital Markets I Class 5 - Utility and Pricing Theory Robert J. Frey Research Professor Stony Brook University, Applied Mathematics and Statistics frey@ams.sunysb.edu This

AMS 69.0 - Portfolio Theory and Capital Markets I Class 5 - Utility and Pricing Theory Robert J. Frey Research Professor Stony Brook University, Applied Mathematics and Statistics frey@ams.sunysb.edu This

Economic of Uncertainty

Economic of Uncertainty Risk Aversion Based on ECO 317, Princeton UC3M April 2012 (UC3M) Economics of Uncertainty. April 2012 1 / 16 Introduction 1 Space of Lotteries (UC3M) Economics of Uncertainty. April

Economic of Uncertainty Risk Aversion Based on ECO 317, Princeton UC3M April 2012 (UC3M) Economics of Uncertainty. April 2012 1 / 16 Introduction 1 Space of Lotteries (UC3M) Economics of Uncertainty. April

Financial Economics. A Concise Introduction to Classical and Behavioral Finance Chapter 2. Thorsten Hens and Marc Oliver Rieger

Financial Economics A Concise Introduction to Classical and Behavioral Finance Chapter 2 Thorsten Hens and Marc Oliver Rieger Swiss Banking Institute, University of Zurich / BWL, University of Trier July

Financial Economics A Concise Introduction to Classical and Behavioral Finance Chapter 2 Thorsten Hens and Marc Oliver Rieger Swiss Banking Institute, University of Zurich / BWL, University of Trier July

Choice under Uncertainty

Chapter 7 Choice under Uncertainty 1. Expected Utility Theory. 2. Risk Aversion. 3. Applications: demand for insurance, portfolio choice 4. Violations of Expected Utility Theory. 7.1 Expected Utility Theory

Chapter 7 Choice under Uncertainty 1. Expected Utility Theory. 2. Risk Aversion. 3. Applications: demand for insurance, portfolio choice 4. Violations of Expected Utility Theory. 7.1 Expected Utility Theory

Lecture 12: Introduction to reasoning under uncertainty. Actions and Consequences

Lecture 12: Introduction to reasoning under uncertainty Preferences Utility functions Maximizing expected utility Value of information Bandit problems and the exploration-exploitation trade-off COMP-424,

Lecture 12: Introduction to reasoning under uncertainty Preferences Utility functions Maximizing expected utility Value of information Bandit problems and the exploration-exploitation trade-off COMP-424,

PAULI MURTO, ANDREY ZHUKOV

GAME THEORY SOLUTION SET 1 WINTER 018 PAULI MURTO, ANDREY ZHUKOV Introduction For suggested solution to problem 4, last year s suggested solutions by Tsz-Ning Wong were used who I think used suggested

GAME THEORY SOLUTION SET 1 WINTER 018 PAULI MURTO, ANDREY ZHUKOV Introduction For suggested solution to problem 4, last year s suggested solutions by Tsz-Ning Wong were used who I think used suggested

Finance: Risk Management Module II: Optimal Risk Sharing and Arrow-Lind Theorem

Institte for Risk Management and Insrance Winter 00/0 Modle II: Optimal Risk Sharing and Arrow-Lind Theorem Part I: steinorth@bwl.lm.de Efficient risk-sharing between risk-averse individals Consider two

Institte for Risk Management and Insrance Winter 00/0 Modle II: Optimal Risk Sharing and Arrow-Lind Theorem Part I: steinorth@bwl.lm.de Efficient risk-sharing between risk-averse individals Consider two

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College April 3, 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College April 3, 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Part 4: Market Failure II - Asymmetric Information - Uncertainty

Part 4: Market Failure II - Asymmetric Information - Uncertainty Expected Utility, Risk Aversion, Risk Neutrality, Risk Pooling, Insurance July 2016 - Asymmetric Information - Uncertainty July 2016 1 /

Part 4: Market Failure II - Asymmetric Information - Uncertainty Expected Utility, Risk Aversion, Risk Neutrality, Risk Pooling, Insurance July 2016 - Asymmetric Information - Uncertainty July 2016 1 /

Game Theory - Lecture #8

Game Theory - Lecture #8 Outline: Randomized actions vnm & Bernoulli payoff functions Mixed strategies & Nash equilibrium Hawk/Dove & Mixed strategies Random models Goal: Would like a formulation in which

Game Theory - Lecture #8 Outline: Randomized actions vnm & Bernoulli payoff functions Mixed strategies & Nash equilibrium Hawk/Dove & Mixed strategies Random models Goal: Would like a formulation in which

CONSUMPTION-SAVINGS MODEL JANUARY 19, 2018

CONSUMPTION-SAVINGS MODEL JANUARY 19, 018 Stochastic Consumption-Savings Model APPLICATIONS Use (solution to) stochastic two-period model to illustrate some basic results and ideas in Consumption research

CONSUMPTION-SAVINGS MODEL JANUARY 19, 018 Stochastic Consumption-Savings Model APPLICATIONS Use (solution to) stochastic two-period model to illustrate some basic results and ideas in Consumption research

Behavioral Economics (Lecture 1)

") 14.127 Behavioral Economics (Lecture 1) Xavier Gabaix February 5, 2003 1 Overview Instructor: Xavier Gabaix Time 4-6:45/7pm, with 10 minute break. Requirements: 3 problem sets and Term paper due September

14.127 Behavioral Economics (Lecture 1) Xavier Gabaix February 5, 2003 1 Overview Instructor: Xavier Gabaix Time 4-6:45/7pm, with 10 minute break. Requirements: 3 problem sets and Term paper due September

UTILITY ANALYSIS HANDOUTS

UTILITY ANALYSIS HANDOUTS 1 2 UTILITY ANALYSIS Motivating Example: Your total net worth = $400K = W 0. You own a home worth $250K. Probability of a fire each yr = 0.001. Insurance cost = $1K. Question:

UTILITY ANALYSIS HANDOUTS 1 2 UTILITY ANALYSIS Motivating Example: Your total net worth = $400K = W 0. You own a home worth $250K. Probability of a fire each yr = 0.001. Insurance cost = $1K. Question:

Martingale Pricing Theory in Discrete-Time and Discrete-Space Models

IEOR E4707: Foundations of Financial Engineering c 206 by Martin Haugh Martingale Pricing Theory in Discrete-Time and Discrete-Space Models These notes develop the theory of martingale pricing in a discrete-time,

IEOR E4707: Foundations of Financial Engineering c 206 by Martin Haugh Martingale Pricing Theory in Discrete-Time and Discrete-Space Models These notes develop the theory of martingale pricing in a discrete-time,

Higher-Order Risk Attitudes

ANDBOOK OF INSURANCE January, 0 igher-order Risk Attitudes LOUIS EECKOUDT IESEG School of Management, 3 rue de la Digue, 59000 Lille (France) and CORE, 34 Voie du Roman Pays, 348 Louvain-la-Neuve (Belgium);

ANDBOOK OF INSURANCE January, 0 igher-order Risk Attitudes LOUIS EECKOUDT IESEG School of Management, 3 rue de la Digue, 59000 Lille (France) and CORE, 34 Voie du Roman Pays, 348 Louvain-la-Neuve (Belgium);

SAC 304: Financial Mathematics II

SAC 304: Financial Mathematics II Portfolio theory, Risk and Return,Investment risk, CAPM Philip Ngare, Ph.D April 25, 2013 P. Ngare (University Of Nairobi) SAC 304: Financial Mathematics II April 25,

SAC 304: Financial Mathematics II Portfolio theory, Risk and Return,Investment risk, CAPM Philip Ngare, Ph.D April 25, 2013 P. Ngare (University Of Nairobi) SAC 304: Financial Mathematics II April 25,

Financial Decisions and Markets: A Course in Asset Pricing. John Y. Campbell. Princeton University Press Princeton and Oxford

Financial Decisions and Markets: A Course in Asset Pricing John Y. Campbell Princeton University Press Princeton and Oxford Figures Tables Preface xiii xv xvii Part I Stade Portfolio Choice and Asset Pricing

Financial Decisions and Markets: A Course in Asset Pricing John Y. Campbell Princeton University Press Princeton and Oxford Figures Tables Preface xiii xv xvii Part I Stade Portfolio Choice and Asset Pricing

Outline for today. Stat155 Game Theory Lecture 19: Price of anarchy. Cooperative games. Price of anarchy. Price of anarchy

Outline for today Stat155 Game Theory Lecture 19:.. Peter Bartlett Recall: Linear and affine latencies Classes of latencies Pigou networks Transferable versus nontransferable utility November 1, 2016 1

Outline for today Stat155 Game Theory Lecture 19:.. Peter Bartlett Recall: Linear and affine latencies Classes of latencies Pigou networks Transferable versus nontransferable utility November 1, 2016 1

Topic Four Utility optimization and stochastic dominance for investment decisions. 4.1 Optimal long-term investment criterion log utility criterion

MATH4512 Fundamentals of Mathematical Finance Topic Four Utility optimization and stochastic dominance for investment decisions 4.1 Optimal long-term investment criterion log utility criterion 4.2 Axiomatic

MATH4512 Fundamentals of Mathematical Finance Topic Four Utility optimization and stochastic dominance for investment decisions 4.1 Optimal long-term investment criterion log utility criterion 4.2 Axiomatic

All Investors are Risk-averse Expected Utility Maximizers. Carole Bernard (UW), Jit Seng Chen (GGY) and Steven Vanduffel (Vrije Universiteit Brussel)

, Jit Seng Chen (GGY) and Steven Vanduffel (Vrije Universiteit Brussel)") All Investors are Risk-averse Expected Utility Maximizers Carole Bernard (UW), Jit Seng Chen (GGY) and Steven Vanduffel (Vrije Universiteit Brussel) First Name: Waterloo, April 2013. Last Name: UW ID #:

All Investors are Risk-averse Expected Utility Maximizers Carole Bernard (UW), Jit Seng Chen (GGY) and Steven Vanduffel (Vrije Universiteit Brussel) First Name: Waterloo, April 2013. Last Name: UW ID #:

Effects of Wealth and Its Distribution on the Moral Hazard Problem

Effects of Wealth and Its Distribution on the Moral Hazard Problem Jin Yong Jung We analyze how the wealth of an agent and its distribution affect the profit of the principal by considering the simple

Effects of Wealth and Its Distribution on the Moral Hazard Problem Jin Yong Jung We analyze how the wealth of an agent and its distribution affect the profit of the principal by considering the simple

Portfolio Selection with Quadratic Utility Revisited

The Geneva Papers on Risk and Insurance Theory, 29: 137 144, 2004 c 2004 The Geneva Association Portfolio Selection with Quadratic Utility Revisited TIMOTHY MATHEWS tmathews@csun.edu Department of Economics,

The Geneva Papers on Risk and Insurance Theory, 29: 137 144, 2004 c 2004 The Geneva Association Portfolio Selection with Quadratic Utility Revisited TIMOTHY MATHEWS tmathews@csun.edu Department of Economics,

PORTFOLIO OPTIMIZATION AND EXPECTED SHORTFALL MINIMIZATION FROM HISTORICAL DATA

PORTFOLIO OPTIMIZATION AND EXPECTED SHORTFALL MINIMIZATION FROM HISTORICAL DATA We begin by describing the problem at hand which motivates our results. Suppose that we have n financial instruments at hand,

PORTFOLIO OPTIMIZATION AND EXPECTED SHORTFALL MINIMIZATION FROM HISTORICAL DATA We begin by describing the problem at hand which motivates our results. Suppose that we have n financial instruments at hand,

Lecture 2 General Equilibrium Models: Finite Period Economies

Lecture 2 General Equilibrium Models: Finite Period Economies Introduction In macroeconomics, we study the behavior of economy-wide aggregates e.g. GDP, savings, investment, employment and so on - and

Lecture 2 General Equilibrium Models: Finite Period Economies Introduction In macroeconomics, we study the behavior of economy-wide aggregates e.g. GDP, savings, investment, employment and so on - and

ECON4510 Finance Theory Lecture 1

ECON4510 Finance Theory Lecture 1 Kjetil Storesletten Department of Economics University of Oslo 15 January 2018 Kjetil Storesletten, Dept. of Economics, UiO ECON4510 Finance Theory Lecture 1 15 January

ECON4510 Finance Theory Lecture 1 Kjetil Storesletten Department of Economics University of Oslo 15 January 2018 Kjetil Storesletten, Dept. of Economics, UiO ECON4510 Finance Theory Lecture 1 15 January

Outline. Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion

Uncertainty Outline Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion 2 Simple Lotteries 3 Simple Lotteries Advanced Microeconomic Theory

Uncertainty Outline Simple, Compound, and Reduced Lotteries Independence Axiom Expected Utility Theory Money Lotteries Risk Aversion 2 Simple Lotteries 3 Simple Lotteries Advanced Microeconomic Theory

Learning Objectives = = where X i is the i t h outcome of a decision, p i is the probability of the i t h

Learning Objectives After reading Chapter 15 and working the problems for Chapter 15 in the textbook and in this Workbook, you should be able to: Distinguish between decision making under uncertainty and

Learning Objectives After reading Chapter 15 and working the problems for Chapter 15 in the textbook and in this Workbook, you should be able to: Distinguish between decision making under uncertainty and