An Overview of Volatility Derivatives and Recent Developments

|

|

|

- Douglas Wiggins

- 5 years ago

- Views:

Transcription

1 An Overview of Volatility Derivatives and Recent Developments September 17th, 2013 Zhenyu Cui Math Club Colloquium Department of Mathematics Brooklyn College, CUNY Math Club Colloquium Volatility Derivatives 1

2 Outline Introduction The Volatility Market History and Development of Volatility Derivatives Recent Developments and Current Research Projects Conclusion and Future Research Directions Math Club Colloquium Volatility Derivatives 2

3

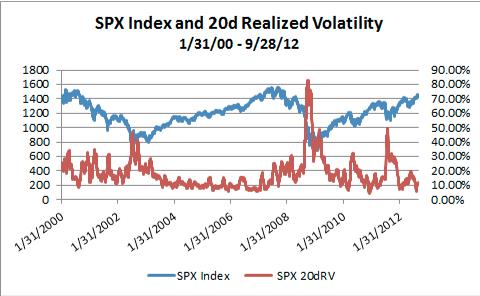

4 Stock index has significant variations across time. Study of finance: Tradeoff between Return and Risk. Practical way to measure volatility/variation : accumulated squared log stock returns: RV = n n i=1 ( ln S ) 2 t i (1) S ti 1 where 0 = t 0 < t 1 <... < t n = T for a time period [0, T ]. This is named Realized Volatility( Historical Volatility). Math Club Colloquium Volatility Derivatives 4

5

6 Black-Scholes Paradigm Model the stock price as Geometric Brownian Motions: ds t = rs t dt + σs t dw t. where W t is a standard Brownian motion. Call option payoff: (S T K) +. Gives you upside potential. The famous Black-Scholes formula: where C = E[e rt (S T K) + ] = S 0 N (d 1 ) Ke rt N (d 2 ), d 1 = ln S 0 K + ( r + σ2 σ T d 2 = d 1 σ T. 2 ) T Math Club Colloquium Volatility Derivatives 6

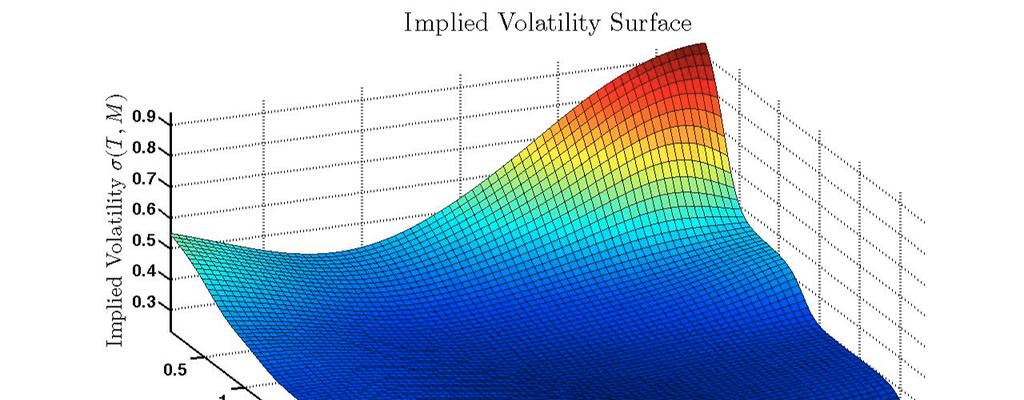

7 Implied Volatility: An Inverse Problem Denote C = BS(σ). We observe the call option surface C 0, how to concisely summarize the information? Black-Scholes formula is monotone in σ. Equate C 0 = BS(σ). Solve the unique implied volatility σ imp = BS 1 (C 0 ). σ imp depends on strike K and time to maturity T. Denote σ imp = σ imp (K, T ). Math Club Colloquium Volatility Derivatives 7

8 Volatility Smiles :-) Plot σ imp against the strike K. The graph is not flat. The graph depicts a smile shape. Draw the implied volatility against the strike and maturity: non-flat surface. Black-Scholes assumption is not practical. All model is wrong, but some are useful! Math Club Colloquium Volatility Derivatives 8

9

10

11 Volatility Smiles: research topics Fitting the implied volatility surface instead of the option price surface. Use the fitted implied volatility surface to predict future option price movement or price options. For close-to-maturity fitting, important to know asymptotics of implied volatility as T 0. Can we express the implied volatility explicitly using model parameters? Math Club Colloquium Volatility Derivatives 11

12 Volatility Smiles: my research Express C 0 as an infinite analytical series of σ imp : C 0 = a i σimp i (2) and determine the coefficients a i, i = 0, 1,... Use Lagrange inversion theorem to represent σ imp as an infinite series of C 0 : σ imp = i=0 b j C j 0, (3) and determine the coefficients b j, j = 0, 1,... For a particular model used, C 0 = f (α 1, α 2,...), where α i are model parameters. Plug in the above expression in (3). j=0 Math Club Colloquium Volatility Derivatives 12

13 A Volatility Index: VIX In 1993, the Chicago Board Options Exchange (CBOE) introduced VIX to measure the market s expectation of 30 day volatility implied by at-the-money S&P100 Index (OEX) option prices. Formula 1 for VIX: VIX = K i T Ki 2 e RT Q(K i ) 1 [ ] F 2 1 T K 0 i F: forward index level derived from index option prices; K 0 : first strike below the forward index level F K i : strike price of the ith out-of-the-money option; K i = K i+1 K i 1 2 ; Q(K i ): the midpoint of the bid-ask spread for each option with strike K i. 1 More than you ever wanted to know about volatility swaps by Demeterfi et al. (1999) Math Club Colloquium Volatility Derivatives 13

14

15 Empirical Facts about Volatility Declining stock prices are more likely to give rise to massive portfolio re-balancing (and thus volatility) than increasing stock prices. This asymmetry arises naturally from the existence of thresholds below which positions must be cut unconditionally for regulatory reasons. Realized volatility of traded assets displays significant variability. Volatility is subject to fluctuations. Math Club Colloquium Volatility Derivatives 15

16 How do we model volatility? Stochastic Volatility (SV) denotes a class of models where the stock price is modeled as ds t = rs t dt + V t S t dw t, S 0 = 1. V t itself is another stochastic process that satisfies dv t = µ(v t )dt + σ(v t )dw (1) t, V 0 = v 0. We assume E[dW t W (1) t ] = ρdt In equity markets, usually this correlation level ρ is negative. Math Club Colloquium Volatility Derivatives 16

17 Common Stochastic Volatility Models Some popular stochastic volatility models are Model µ(.) σ(.) Heston κ(θ x) ξ x 3/2 ωx θx 2 ξx 3/2 Hull-White µx σx Math Club Colloquium Volatility Derivatives 17

18 Features of Stochastic Volatility Models Heston model: volatility process follows a mean-reverting Feller diffusion. The dynamics of the calibrated Heston model predict that: volatility can reach zero, stay at zero for some time, or stay extremely low or very high for long periods of time. Hull-White model: volatility process follows another Geometric Brownian Motion. Market calibration very likely leads to µ < 0. The dynamics of the Hull-White stochastic volatility model predict that: both expectation and most likely value of instantaneous volatility converge to zero. Math Club Colloquium Volatility Derivatives 18

19 Variance Swaps A derivative product purely dependent on the underlying volatility. The variance swap is an OTC contract: ( ) 1 Notional Realized Variance(RV) Strike(K) T RV = n 1 i=0 ( ln St i+1 S ti ) 2 with 0 = t0 < t 1 <... < t n = T. Volatility as an asset class. A tool to trade volatility and make profits. Like any swap, a variance swap is an OTC contract with zero upfront premium. In contrast to most swaps, a variance swap has a payment only at expiration. Math Club Colloquium Volatility Derivatives 19

20 Variance Swaps (Cont d) From Carr and Lee (2009): According to Michael Weber, now with J.P. Morgan, the first volatility derivative appears to have been a variance swap dealt in 1993 by him at the Union Bank of Switzerland (UBS). The emergence of variance swaps in 1998: due to the historically high implied volatilities experienced in that year. Hedge funds found it attractive to sell realized variance at rates that exceeded by wide margins the econometric forecasts of future realized variance based on time series analysis of returns on the underlying index. Variance swap rate VS = E Q [RV ], where Q is the risk-neutral measure. Math Club Colloquium Volatility Derivatives 20

21 Variance Swaps (Cont d) Define the Variance Risk premium as VRP = E P [RV ] VS, where P is the physical probability measure. Selling realized variance has positive alpha? Or VRP is usually negative. Generally accepted or believed by hedge funds from 1998 to 2008 (Carr and Lee (2010), Carr and Wu (2009)). Until the financial melt-down, when short-variance funds are wiped out due to leverage. Math Club Colloquium Volatility Derivatives 21

22

23

24 Variance Options Successful rollout of variance swaps on stock indices. Next step: introduce variance swaps on individual stocks In 2005, options on realized variance was introduced. Payoff: (RV K) +. Bet on the realized variance level in the future. Other exotic payoff structure and products. Math Club Colloquium Volatility Derivatives 24

25 Timer Options A (perpetual) timer option: an option with random maturity. Investors specify a variance budget B. The random maturity: { τ := inf u > 0, The payoff at time τ: u 0 max(s τ K, 0) } V s ds B. Math Club Colloquium Volatility Derivatives 25

26 Why would timer options be attractive? In April 2007, Société Générale Corporate and Investment Banking (SG CIB) started to sell this timer option that allows buyers to specify the level of volatility used to price the instrument. Sawyer (2007) explains that this product is designed to give investors more flexibility and ensure they do not overpay for an option [...] But the level of implied volatility is often higher than realized volatility, reflecting the uncertainty of future market direction. [...] In fact, having analyzed all stocks in the Euro Stoxx 50 index since 2000, SG CIB calculates that 80% of three-month calls that have matured in-the-money were overpriced. Math Club Colloquium Volatility Derivatives 26

27 Price Variance Swap under Practical Models In practice, variance swaps are discretely sampled. Broadie and Jain (2008): a closed-form formula of the fair strike of the discrete variance swap for the Heston model. Bernard and Cui (2013): a general expression for the fair strike of a discrete variance swap in the time-homogeneous stochastic volatility model In several models (Heston, Hull-White, Schoebel-Zhu), we obtain explicit formula for the fair strike. Asymptotic expansion of the fair strike with respect to n and T. Math Club Colloquium Volatility Derivatives 27

28 Hong s Approach and Forward Characteristic Functions In a presentation by Hong (2004), he looks at the forward characteristic function of the log stock price returns. φ(u) = E [ ] e iu ln St i+1 St i Then after differentiation [ ( E ln S ) ] 2 t i+1 S ti = d 2 φ(u) du 2 u=0 Then it is possible to evaluate the discrete variance swap, or in general discrete moment swaps with payoff ( ) m n i=1 ln St i+1 S ti Math Club Colloquium Volatility Derivatives 28

29 Research Directions along the Hong approach There are quite a few models where the forward characteristic function can be calculated. Affine processes by Duffie et al. (2000): reduced to solve systems of ODEs. Levy processes: from the Levy-Khinchin Formula, and stationary and independent increment property. An example of non-affine process: 3/2 model My recent research: obtain the CF for the 3/2 model, and price discrete variance swap in this model. Math Club Colloquium Volatility Derivatives 29

30 Bernard and Cui (2011), JCF Recall: dv t = µ(v t )dt + σ(v t )dw t. The joint law of (τ, V τ ) is (τ, V τ ) law ( B 0 ) 1 ds, X B X s here X t is governed by the SDE { dx t = µ(xt) X t dt + σ(xt) Xt dw t, X 0 = V 0 where B is a standard Brownian motion. Math Club Colloquium Volatility Derivatives 30

31 Analytical Pricing of Variance Options A variance option: ( T 0 V tdt K) +, K > 0. Compare with a standard call option: (V T K) +, K > 0. Key observation: t 0 V sds is increasing in t almost surely. Once in the money = always in the money afterwards. The first instant the variance option is in the money : the first passage time of T 0 V sds to K. Math Club Colloquium Volatility Derivatives 31

32 Variance Option and First Hitting time of Integrated Process Define τ := inf{u > 0, u 0 V tdt K}. { T 0 V tdt K} {τ T }. [ ( T ) + ] C 0 = e rt E V t dt K 0 [( T = e rt E 0 ) V t dt K 1{ [(( τ = e rt E V t dt + 0 [(( = e rt E K + T τ T τ ) V t dt T 0 ) V t dt [( T ) ] = e rt E V t dt 1{τ T } τ ] V t dt K} ) ] K 1{τ T} ) ] K 1{τ T } Math Club Colloquium Volatility Derivatives 32

33 Connecting Discrete to Continuous Sampling Define Quadratic Variation: QV = lim RV. n, max (t i+1 t i ) 0 i=0,1,...,n 1 We know that RV converges to QV in probability. But we are interested in whether this convergence takes place in L1 or not. Jarrow et al (2013) gives preliminary answer, but for the case of 3/2 mode it remains an open problem. The fair strike of the discrete variance swap is [ K M d (n) := 1 n 1 ( T E ln S ) ] 2 t i+1 = 1 S ti T E[RV ] i=0 The fair strike of the continuous variance swap is := 1 [ T ] T E V s ds = 1 T E[QV ] K M c 0 Math Club Colloquium Volatility Derivatives 33

34 General representation of the discrete fair strike I obtain a general representation of the discrete strike in terms of continuous strike. Define, for n 1, t i = i, i = 1, 2,... n = T / and [ C( ) = 1 n 1 ( ti + E T i=0 t i ) 2 ] m 2 (V s )ds. Assuming that the third moments exists, [ γ( ) = 1 n 1 ( ti + ) 3 ] E m(v t )dw (2) t. T t i i=0 Assumption 1: For some > 0, C( ) <. Math Club Colloquium Volatility Derivatives 34

35 Convergence in Time-homogeneous Diffusion Case Theorem Assume a the general time-homogeneous diffusion model, and Assumption 1. The fair strike of a discrete variance swap is given by where K d ( ) = K c + r 2 rk c + 1 C( ) ρb( ), 4 B( ) = 1 n 1 [( ti + E T i=0 = 1 3 γ( ). t i a Theorem 1 of Bernard, Cui and McLeish (2013) ) ( ti m 2 + )] (V s )ds m(v t )dw (2) t t i Math Club Colloquium Volatility Derivatives 35

36 Theorem We have K d ( ) K c as 0 for all ρ if and only if Assumption 1 holds. Proposition In the case of time-homogeneous diffusion models, the following statements are equivalent: (1) Assumption 1; (2) K d ( ) L 1 for some n 1; (3) K d ( ) K c as 0 for all 1 ρ 1. Math Club Colloquium Volatility Derivatives 36

37 Conclusion We have provided a brief introduction to the volatility market. We provide an overview of stochastic volatility models. We present the history of volatility derivatives and motivations behind them. We present some current research topics in this area. Math Club Colloquium Volatility Derivatives 37

38 Thank You Q & A Math Club Colloquium Volatility Derivatives 38

39 References (partial list) Bernard, C., and Cui, Z. (2011): Pricing timer options, Journal of Computational Finance, 15(1), Bernard, C., and Cui, Z. (2013): Prices and asymptotics of discrete variance swaps, Applied Mathematical Finance, forthcoming. Bernard, C., Cui, Z., and Mcleish, D.L. (2013): Convergence of discrete variance swap in time-homogeneous diffusion models, working paper. Carr, P. and Lee, R. (2009): Volatility Derivatives, Annual Review of Financial Economics, 1, Carr, P. and Wu, L. (2009): Variance Risk Premiums, Review of Financial Studies, 22, Demeterfi, K., E. Derman, M. Kamal, and J, Zou (1999): More than you ever wanted to know about volatility swaps, Goldman Sachs Quantitative Strategies Research Notes, Hong, G. (2004): Forward Smile and Derivative Pricing, presentation at Cambridge University, Math Club Colloquium Volatility Derivatives 39

Advanced Topics in Derivative Pricing Models. Topic 4 - Variance products and volatility derivatives

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

The Implied Volatility Index

The Implied Volatility Index Risk Management Institute National University of Singapore First version: October 6, 8, this version: October 8, 8 Introduction This document describes the formulation and

The Implied Volatility Index Risk Management Institute National University of Singapore First version: October 6, 8, this version: October 8, 8 Introduction This document describes the formulation and

Exploring Volatility Derivatives: New Advances in Modelling. Bruno Dupire Bloomberg L.P. NY

Exploring Volatility Derivatives: New Advances in Modelling Bruno Dupire Bloomberg L.P. NY bdupire@bloomberg.net Global Derivatives 2005, Paris May 25, 2005 1. Volatility Products Historical Volatility

Exploring Volatility Derivatives: New Advances in Modelling Bruno Dupire Bloomberg L.P. NY bdupire@bloomberg.net Global Derivatives 2005, Paris May 25, 2005 1. Volatility Products Historical Volatility

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL YOUNGGEUN YOO Abstract. Ito s lemma is often used in Ito calculus to find the differentials of a stochastic process that depends on time. This paper will introduce

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL YOUNGGEUN YOO Abstract. Ito s lemma is often used in Ito calculus to find the differentials of a stochastic process that depends on time. This paper will introduce

Stochastic Volatility (Working Draft I)

") Stochastic Volatility (Working Draft I) Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu 1 Introduction When using the Black-Scholes-Merton model to price derivative

Stochastic Volatility (Working Draft I) Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu 1 Introduction When using the Black-Scholes-Merton model to price derivative

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case Guang-Hua Lian Collaboration with Robert Elliott University of Adelaide Feb. 2, 2011 Robert Elliott,

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case Guang-Hua Lian Collaboration with Robert Elliott University of Adelaide Feb. 2, 2011 Robert Elliott,

1 Introduction. 2 Old Methodology BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM DIVISION OF RESEARCH AND STATISTICS

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM DIVISION OF RESEARCH AND STATISTICS Date: October 6, 3 To: From: Distribution Hao Zhou and Matthew Chesnes Subject: VIX Index Becomes Model Free and Based

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM DIVISION OF RESEARCH AND STATISTICS Date: October 6, 3 To: From: Distribution Hao Zhou and Matthew Chesnes Subject: VIX Index Becomes Model Free and Based

A Consistent Pricing Model for Index Options and Volatility Derivatives

A Consistent Pricing Model for Index Options and Volatility Derivatives 6th World Congress of the Bachelier Society Thomas Kokholm Finance Research Group Department of Business Studies Aarhus School of

A Consistent Pricing Model for Index Options and Volatility Derivatives 6th World Congress of the Bachelier Society Thomas Kokholm Finance Research Group Department of Business Studies Aarhus School of

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

Valuation of Volatility Derivatives. Jim Gatheral Global Derivatives & Risk Management 2005 Paris May 24, 2005

Valuation of Volatility Derivatives Jim Gatheral Global Derivatives & Risk Management 005 Paris May 4, 005 he opinions expressed in this presentation are those of the author alone, and do not necessarily

Valuation of Volatility Derivatives Jim Gatheral Global Derivatives & Risk Management 005 Paris May 4, 005 he opinions expressed in this presentation are those of the author alone, and do not necessarily

Pricing Volatility Derivatives with General Risk Functions. Alejandro Balbás University Carlos III of Madrid

Pricing Volatility Derivatives with General Risk Functions Alejandro Balbás University Carlos III of Madrid alejandro.balbas@uc3m.es Content Introduction. Describing volatility derivatives. Pricing and

Pricing Volatility Derivatives with General Risk Functions Alejandro Balbás University Carlos III of Madrid alejandro.balbas@uc3m.es Content Introduction. Describing volatility derivatives. Pricing and

Definition Pricing Risk management Second generation barrier options. Barrier Options. Arfima Financial Solutions

Arfima Financial Solutions Contents Definition 1 Definition 2 3 4 Contenido Definition 1 Definition 2 3 4 Definition Definition: A barrier option is an option on the underlying asset that is activated

Arfima Financial Solutions Contents Definition 1 Definition 2 3 4 Contenido Definition 1 Definition 2 3 4 Definition Definition: A barrier option is an option on the underlying asset that is activated

Unified Credit-Equity Modeling

Unified Credit-Equity Modeling Rafael Mendoza-Arriaga Based on joint research with: Vadim Linetsky and Peter Carr The University of Texas at Austin McCombs School of Business (IROM) Recent Advancements

Unified Credit-Equity Modeling Rafael Mendoza-Arriaga Based on joint research with: Vadim Linetsky and Peter Carr The University of Texas at Austin McCombs School of Business (IROM) Recent Advancements

STOCHASTIC VOLATILITY AND OPTION PRICING

STOCHASTIC VOLATILITY AND OPTION PRICING Daniel Dufresne Centre for Actuarial Studies University of Melbourne November 29 (To appear in Risks and Rewards, the Society of Actuaries Investment Section Newsletter)

STOCHASTIC VOLATILITY AND OPTION PRICING Daniel Dufresne Centre for Actuarial Studies University of Melbourne November 29 (To appear in Risks and Rewards, the Society of Actuaries Investment Section Newsletter)

Math 416/516: Stochastic Simulation

Math 416/516: Stochastic Simulation Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 13 Haijun Li Math 416/516: Stochastic Simulation Week 13 1 / 28 Outline 1 Simulation

Math 416/516: Stochastic Simulation Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 13 Haijun Li Math 416/516: Stochastic Simulation Week 13 1 / 28 Outline 1 Simulation

A Brief Introduction to Stochastic Volatility Modeling

A Brief Introduction to Stochastic Volatility Modeling Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu Introduction When using the Black-Scholes-Merton model to

A Brief Introduction to Stochastic Volatility Modeling Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu Introduction When using the Black-Scholes-Merton model to

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

Hedging Credit Derivatives in Intensity Based Models

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

4. Black-Scholes Models and PDEs. Math6911 S08, HM Zhu

4. Black-Scholes Models and PDEs Math6911 S08, HM Zhu References 1. Chapter 13, J. Hull. Section.6, P. Brandimarte Outline Derivation of Black-Scholes equation Black-Scholes models for options Implied

4. Black-Scholes Models and PDEs Math6911 S08, HM Zhu References 1. Chapter 13, J. Hull. Section.6, P. Brandimarte Outline Derivation of Black-Scholes equation Black-Scholes models for options Implied

Stochastic Volatility and Jump Modeling in Finance

Stochastic Volatility and Jump Modeling in Finance HPCFinance 1st kick-off meeting Elisa Nicolato Aarhus University Department of Economics and Business January 21, 2013 Elisa Nicolato (Aarhus University

Stochastic Volatility and Jump Modeling in Finance HPCFinance 1st kick-off meeting Elisa Nicolato Aarhus University Department of Economics and Business January 21, 2013 Elisa Nicolato (Aarhus University

The Black-Scholes Model

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

Large Deviations and Stochastic Volatility with Jumps: Asymptotic Implied Volatility for Affine Models

Large Deviations and Stochastic Volatility with Jumps: TU Berlin with A. Jaquier and A. Mijatović (Imperial College London) SIAM conference on Financial Mathematics, Minneapolis, MN July 10, 2012 Implied

Large Deviations and Stochastic Volatility with Jumps: TU Berlin with A. Jaquier and A. Mijatović (Imperial College London) SIAM conference on Financial Mathematics, Minneapolis, MN July 10, 2012 Implied

WKB Method for Swaption Smile

WKB Method for Swaption Smile Andrew Lesniewski BNP Paribas New York February 7 2002 Abstract We study a three-parameter stochastic volatility model originally proposed by P. Hagan for the forward swap

WKB Method for Swaption Smile Andrew Lesniewski BNP Paribas New York February 7 2002 Abstract We study a three-parameter stochastic volatility model originally proposed by P. Hagan for the forward swap

Modeling and Pricing of Variance Swaps for Local Stochastic Volatilities with Delay and Jumps

Modeling and Pricing of Variance Swaps for Local Stochastic Volatilities with Delay and Jumps Anatoliy Swishchuk Department of Mathematics and Statistics University of Calgary Calgary, AB, Canada QMF 2009

Modeling and Pricing of Variance Swaps for Local Stochastic Volatilities with Delay and Jumps Anatoliy Swishchuk Department of Mathematics and Statistics University of Calgary Calgary, AB, Canada QMF 2009

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 14 Lecture 14 November 15, 2017 Derivation of the

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 14 Lecture 14 November 15, 2017 Derivation of the

Heston Stochastic Local Volatility Model

Heston Stochastic Local Volatility Model Klaus Spanderen 1 R/Finance 2016 University of Illinois, Chicago May 20-21, 2016 1 Joint work with Johannes Göttker-Schnetmann Klaus Spanderen Heston Stochastic

Heston Stochastic Local Volatility Model Klaus Spanderen 1 R/Finance 2016 University of Illinois, Chicago May 20-21, 2016 1 Joint work with Johannes Göttker-Schnetmann Klaus Spanderen Heston Stochastic

2 f. f t S 2. Delta measures the sensitivityof the portfolio value to changes in the price of the underlying

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Lecture 8: The Black-Scholes theory

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Lecture 11: Stochastic Volatility Models Cont.

E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont. Page 1 of 8 Lecture 11: Stochastic Volatility Models Cont. E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont.

E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont. Page 1 of 8 Lecture 11: Stochastic Volatility Models Cont. E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont.

Calibration Lecture 4: LSV and Model Uncertainty

Calibration Lecture 4: LSV and Model Uncertainty March 2017 Recap: Heston model Recall the Heston stochastic volatility model ds t = rs t dt + Y t S t dw 1 t, dy t = κ(θ Y t ) dt + ξ Y t dw 2 t, where

Calibration Lecture 4: LSV and Model Uncertainty March 2017 Recap: Heston model Recall the Heston stochastic volatility model ds t = rs t dt + Y t S t dw 1 t, dy t = κ(θ Y t ) dt + ξ Y t dw 2 t, where

European call option with inflation-linked strike

Mathematical Statistics Stockholm University European call option with inflation-linked strike Ola Hammarlid Research Report 2010:2 ISSN 1650-0377 Postal address: Mathematical Statistics Dept. of Mathematics

Mathematical Statistics Stockholm University European call option with inflation-linked strike Ola Hammarlid Research Report 2010:2 ISSN 1650-0377 Postal address: Mathematical Statistics Dept. of Mathematics

1 Implied Volatility from Local Volatility

Abstract We try to understand the Berestycki, Busca, and Florent () (BBF) result in the context of the work presented in Lectures and. Implied Volatility from Local Volatility. Current Plan as of March

Abstract We try to understand the Berestycki, Busca, and Florent () (BBF) result in the context of the work presented in Lectures and. Implied Volatility from Local Volatility. Current Plan as of March

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

Volatility Smiles and Yield Frowns

Volatility Smiles and Yield Frowns Peter Carr NYU CBOE Conference on Derivatives and Volatility, Chicago, Nov. 10, 2017 Peter Carr (NYU) Volatility Smiles and Yield Frowns 11/10/2017 1 / 33 Interest Rates

Volatility Smiles and Yield Frowns Peter Carr NYU CBOE Conference on Derivatives and Volatility, Chicago, Nov. 10, 2017 Peter Carr (NYU) Volatility Smiles and Yield Frowns 11/10/2017 1 / 33 Interest Rates

1.1 Basic Financial Derivatives: Forward Contracts and Options

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

Tangent Lévy Models. Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford.

Oxford-Man Institute of Quantitative Finance University of Oxford.") Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Asset Pricing Models with Underlying Time-varying Lévy Processes

Asset Pricing Models with Underlying Time-varying Lévy Processes Stochastics & Computational Finance 2015 Xuecan CUI Jang SCHILTZ University of Luxembourg July 9, 2015 Xuecan CUI, Jang SCHILTZ University

Asset Pricing Models with Underlying Time-varying Lévy Processes Stochastics & Computational Finance 2015 Xuecan CUI Jang SCHILTZ University of Luxembourg July 9, 2015 Xuecan CUI, Jang SCHILTZ University

Rough volatility models: When population processes become a new tool for trading and risk management

Rough volatility models: When population processes become a new tool for trading and risk management Omar El Euch and Mathieu Rosenbaum École Polytechnique 4 October 2017 Omar El Euch and Mathieu Rosenbaum

Rough volatility models: When population processes become a new tool for trading and risk management Omar El Euch and Mathieu Rosenbaum École Polytechnique 4 October 2017 Omar El Euch and Mathieu Rosenbaum

Dynamic Relative Valuation

Dynamic Relative Valuation Liuren Wu, Baruch College Joint work with Peter Carr from Morgan Stanley October 15, 2013 Liuren Wu (Baruch) Dynamic Relative Valuation 10/15/2013 1 / 20 The standard approach

Dynamic Relative Valuation Liuren Wu, Baruch College Joint work with Peter Carr from Morgan Stanley October 15, 2013 Liuren Wu (Baruch) Dynamic Relative Valuation 10/15/2013 1 / 20 The standard approach

Math 623 (IOE 623), Winter 2008: Final exam

, Winter 2008: Final exam") Math 623 (IOE 623), Winter 2008: Final exam Name: Student ID: This is a closed book exam. You may bring up to ten one sided A4 pages of notes to the exam. You may also use a calculator but not its memory

Math 623 (IOE 623), Winter 2008: Final exam Name: Student ID: This is a closed book exam. You may bring up to ten one sided A4 pages of notes to the exam. You may also use a calculator but not its memory

AMH4 - ADVANCED OPTION PRICING. Contents

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

M5MF6. Advanced Methods in Derivatives Pricing

Course: Setter: M5MF6 Dr Antoine Jacquier MSc EXAMINATIONS IN MATHEMATICS AND FINANCE DEPARTMENT OF MATHEMATICS April 2016 M5MF6 Advanced Methods in Derivatives Pricing Setter s signature...........................................

Course: Setter: M5MF6 Dr Antoine Jacquier MSc EXAMINATIONS IN MATHEMATICS AND FINANCE DEPARTMENT OF MATHEMATICS April 2016 M5MF6 Advanced Methods in Derivatives Pricing Setter s signature...........................................

Variance derivatives and estimating realised variance from high-frequency data. John Crosby

Variance derivatives and estimating realised variance from high-frequency data John Crosby UBS, London and Centre for Economic and Financial Studies, Department of Economics, Glasgow University Presentation

Variance derivatives and estimating realised variance from high-frequency data John Crosby UBS, London and Centre for Economic and Financial Studies, Department of Economics, Glasgow University Presentation

Counterparty Credit Risk Simulation

Counterparty Credit Risk Simulation Alex Yang FinPricing http://www.finpricing.com Summary Counterparty Credit Risk Definition Counterparty Credit Risk Measures Monte Carlo Simulation Interest Rate Curve

Counterparty Credit Risk Simulation Alex Yang FinPricing http://www.finpricing.com Summary Counterparty Credit Risk Definition Counterparty Credit Risk Measures Monte Carlo Simulation Interest Rate Curve

Stochastic Volatility Effects on Defaultable Bonds

Stochastic Volatility Effects on Defaultable Bonds Jean-Pierre Fouque Ronnie Sircar Knut Sølna December 24; revised October 24, 25 Abstract We study the effect of introducing stochastic volatility in the

Stochastic Volatility Effects on Defaultable Bonds Jean-Pierre Fouque Ronnie Sircar Knut Sølna December 24; revised October 24, 25 Abstract We study the effect of introducing stochastic volatility in the

The Pricing of Variance, Volatility, Covariance, and Correlation Swaps

The Pricing of Variance, Volatility, Covariance, and Correlation Swaps Anatoliy Swishchuk, Ph.D., D.Sc. Associate Professor of Mathematics & Statistics University of Calgary Abstract Swaps are useful for

The Pricing of Variance, Volatility, Covariance, and Correlation Swaps Anatoliy Swishchuk, Ph.D., D.Sc. Associate Professor of Mathematics & Statistics University of Calgary Abstract Swaps are useful for

The Black-Scholes PDE from Scratch

The Black-Scholes PDE from Scratch chris bemis November 27, 2006 0-0 Goal: Derive the Black-Scholes PDE To do this, we will need to: Come up with some dynamics for the stock returns Discuss Brownian motion

The Black-Scholes PDE from Scratch chris bemis November 27, 2006 0-0 Goal: Derive the Black-Scholes PDE To do this, we will need to: Come up with some dynamics for the stock returns Discuss Brownian motion

Lecture 3: Asymptotics and Dynamics of the Volatility Skew

Lecture 3: Asymptotics and Dynamics of the Volatility Skew Jim Gatheral, Merrill Lynch Case Studies in Financial Modelling Course Notes, Courant Institute of Mathematical Sciences, Fall Term, 2001 I am

Lecture 3: Asymptotics and Dynamics of the Volatility Skew Jim Gatheral, Merrill Lynch Case Studies in Financial Modelling Course Notes, Courant Institute of Mathematical Sciences, Fall Term, 2001 I am

Pricing and hedging with rough-heston models

Pricing and hedging with rough-heston models Omar El Euch, Mathieu Rosenbaum Ecole Polytechnique 1 January 216 El Euch, Rosenbaum Pricing and hedging with rough-heston models 1 Table of contents Introduction

Pricing and hedging with rough-heston models Omar El Euch, Mathieu Rosenbaum Ecole Polytechnique 1 January 216 El Euch, Rosenbaum Pricing and hedging with rough-heston models 1 Table of contents Introduction

Optimal robust bounds for variance options and asymptotically extreme models

Optimal robust bounds for variance options and asymptotically extreme models Alexander Cox 1 Jiajie Wang 2 1 University of Bath 2 Università di Roma La Sapienza Advances in Financial Mathematics, 9th January,

Optimal robust bounds for variance options and asymptotically extreme models Alexander Cox 1 Jiajie Wang 2 1 University of Bath 2 Università di Roma La Sapienza Advances in Financial Mathematics, 9th January,

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN LECTURE 9: LOCAL AND STOCHASTIC VOLATILITY RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 9: LOCAL AND STOCHASTIC VOLATILITY RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK The only ingredient of the Black and Scholes formula which is

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 9: LOCAL AND STOCHASTIC VOLATILITY RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK The only ingredient of the Black and Scholes formula which is

arxiv: v1 [q-fin.pr] 18 Feb 2010

![arxiv: v1 [q-fin.pr] 18 Feb 2010](/thumbs/87/96175643.jpg "arxiv: v1 [q-fin.pr] 18 Feb 2010") CONVERGENCE OF HESTON TO SVI JIM GATHERAL AND ANTOINE JACQUIER arxiv:1002.3633v1 [q-fin.pr] 18 Feb 2010 Abstract. In this short note, we prove by an appropriate change of variables that the SVI implied

CONVERGENCE OF HESTON TO SVI JIM GATHERAL AND ANTOINE JACQUIER arxiv:1002.3633v1 [q-fin.pr] 18 Feb 2010 Abstract. In this short note, we prove by an appropriate change of variables that the SVI implied

Greek parameters of nonlinear Black-Scholes equation

International Journal of Mathematics and Soft Computing Vol.5, No.2 (2015), 69-74. ISSN Print : 2249-3328 ISSN Online: 2319-5215 Greek parameters of nonlinear Black-Scholes equation Purity J. Kiptum 1,

International Journal of Mathematics and Soft Computing Vol.5, No.2 (2015), 69-74. ISSN Print : 2249-3328 ISSN Online: 2319-5215 Greek parameters of nonlinear Black-Scholes equation Purity J. Kiptum 1,

FE610 Stochastic Calculus for Financial Engineers. Stevens Institute of Technology

FE610 Stochastic Calculus for Financial Engineers Lecture 13. The Black-Scholes PDE Steve Yang Stevens Institute of Technology 04/25/2013 Outline 1 The Black-Scholes PDE 2 PDEs in Asset Pricing 3 Exotic

FE610 Stochastic Calculus for Financial Engineers Lecture 13. The Black-Scholes PDE Steve Yang Stevens Institute of Technology 04/25/2013 Outline 1 The Black-Scholes PDE 2 PDEs in Asset Pricing 3 Exotic

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay. Solutions to Final Exam.

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

Lecture 4. Finite difference and finite element methods

Finite difference and finite element methods Lecture 4 Outline Black-Scholes equation From expectation to PDE Goal: compute the value of European option with payoff g which is the conditional expectation

Finite difference and finite element methods Lecture 4 Outline Black-Scholes equation From expectation to PDE Goal: compute the value of European option with payoff g which is the conditional expectation

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 MAS3904. Stochastic Financial Modelling. Time allowed: 2 hours

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

Extrapolation analytics for Dupire s local volatility

Extrapolation analytics for Dupire s local volatility Stefan Gerhold (joint work with P. Friz and S. De Marco) Vienna University of Technology, Austria 6ECM, July 2012 Implied vol and local vol Implied

Extrapolation analytics for Dupire s local volatility Stefan Gerhold (joint work with P. Friz and S. De Marco) Vienna University of Technology, Austria 6ECM, July 2012 Implied vol and local vol Implied

1. What is Implied Volatility?

Numerical Methods FEQA MSc Lectures, Spring Term 2 Data Modelling Module Lecture 2 Implied Volatility Professor Carol Alexander Spring Term 2 1 1. What is Implied Volatility? Implied volatility is: the

Numerical Methods FEQA MSc Lectures, Spring Term 2 Data Modelling Module Lecture 2 Implied Volatility Professor Carol Alexander Spring Term 2 1 1. What is Implied Volatility? Implied volatility is: the

Heston Model Version 1.0.9

Heston Model Version 1.0.9 1 Introduction This plug-in implements the Heston model. Once installed the plug-in offers the possibility of using two new processes, the Heston process and the Heston time

Heston Model Version 1.0.9 1 Introduction This plug-in implements the Heston model. Once installed the plug-in offers the possibility of using two new processes, the Heston process and the Heston time

Approximation Methods in Derivatives Pricing

Approximation Methods in Derivatives Pricing Minqiang Li Bloomberg LP September 24, 2013 1 / 27 Outline of the talk A brief overview of approximation methods Timer option price approximation Perpetual

Approximation Methods in Derivatives Pricing Minqiang Li Bloomberg LP September 24, 2013 1 / 27 Outline of the talk A brief overview of approximation methods Timer option price approximation Perpetual

King s College London

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

CEV Implied Volatility by VIX

CEV Implied Volatility by VIX Implied Volatility Chien-Hung Chang Dept. of Financial and Computation Mathematics, Providence University, Tiachng, Taiwan May, 21, 2015 Chang (Institute) Implied volatility

CEV Implied Volatility by VIX Implied Volatility Chien-Hung Chang Dept. of Financial and Computation Mathematics, Providence University, Tiachng, Taiwan May, 21, 2015 Chang (Institute) Implied volatility

Lecture 11: Ito Calculus. Tuesday, October 23, 12

Lecture 11: Ito Calculus Continuous time models We start with the model from Chapter 3 log S j log S j 1 = µ t + p tz j Sum it over j: log S N log S 0 = NX µ t + NX p tzj j=1 j=1 Can we take the limit

Lecture 11: Ito Calculus Continuous time models We start with the model from Chapter 3 log S j log S j 1 = µ t + p tz j Sum it over j: log S N log S 0 = NX µ t + NX p tzj j=1 j=1 Can we take the limit

Basic Concepts in Mathematical Finance

Chapter 1 Basic Concepts in Mathematical Finance In this chapter, we give an overview of basic concepts in mathematical finance theory, and then explain those concepts in very simple cases, namely in the

Chapter 1 Basic Concepts in Mathematical Finance In this chapter, we give an overview of basic concepts in mathematical finance theory, and then explain those concepts in very simple cases, namely in the

Introduction to Affine Processes. Applications to Mathematical Finance

and Its Applications to Mathematical Finance Department of Mathematical Science, KAIST Workshop for Young Mathematicians in Korea, 2010 Outline Motivation 1 Motivation 2 Preliminary : Stochastic Calculus

and Its Applications to Mathematical Finance Department of Mathematical Science, KAIST Workshop for Young Mathematicians in Korea, 2010 Outline Motivation 1 Motivation 2 Preliminary : Stochastic Calculus

Pricing Barrier Options under Local Volatility

Abstract Pricing Barrier Options under Local Volatility Artur Sepp Mail: artursepp@hotmail.com, Web: www.hot.ee/seppar 16 November 2002 We study pricing under the local volatility. Our research is mainly

Abstract Pricing Barrier Options under Local Volatility Artur Sepp Mail: artursepp@hotmail.com, Web: www.hot.ee/seppar 16 November 2002 We study pricing under the local volatility. Our research is mainly

Analytical formulas for local volatility model with stochastic. Mohammed Miri

Analytical formulas for local volatility model with stochastic rates Mohammed Miri Joint work with Eric Benhamou (Pricing Partners) and Emmanuel Gobet (Ecole Polytechnique Modeling and Managing Financial

Analytical formulas for local volatility model with stochastic rates Mohammed Miri Joint work with Eric Benhamou (Pricing Partners) and Emmanuel Gobet (Ecole Polytechnique Modeling and Managing Financial

Changing Probability Measures in GARCH Option Pricing Models

Changing Probability Measures in GARCH Option Pricing Models Wenjun Zhang Department of Mathematical Sciences School of Engineering, Computer and Mathematical Sciences Auckland University of Technology

Changing Probability Measures in GARCH Option Pricing Models Wenjun Zhang Department of Mathematical Sciences School of Engineering, Computer and Mathematical Sciences Auckland University of Technology

arxiv: v2 [q-fin.pr] 23 Nov 2017

![arxiv: v2 [q-fin.pr] 23 Nov 2017](/thumbs/73/68844191.jpg "arxiv: v2 [q-fin.pr] 23 Nov 2017") VALUATION OF EQUITY WARRANTS FOR UNCERTAIN FINANCIAL MARKET FOAD SHOKROLLAHI arxiv:17118356v2 [q-finpr] 23 Nov 217 Department of Mathematics and Statistics, University of Vaasa, PO Box 7, FIN-6511 Vaasa,

VALUATION OF EQUITY WARRANTS FOR UNCERTAIN FINANCIAL MARKET FOAD SHOKROLLAHI arxiv:17118356v2 [q-finpr] 23 Nov 217 Department of Mathematics and Statistics, University of Vaasa, PO Box 7, FIN-6511 Vaasa,

CONSTRUCTING NO-ARBITRAGE VOLATILITY CURVES IN LIQUID AND ILLIQUID COMMODITY MARKETS

CONSTRUCTING NO-ARBITRAGE VOLATILITY CURVES IN LIQUID AND ILLIQUID COMMODITY MARKETS Financial Mathematics Modeling for Graduate Students-Workshop January 6 January 15, 2011 MENTOR: CHRIS PROUTY (Cargill)

CONSTRUCTING NO-ARBITRAGE VOLATILITY CURVES IN LIQUID AND ILLIQUID COMMODITY MARKETS Financial Mathematics Modeling for Graduate Students-Workshop January 6 January 15, 2011 MENTOR: CHRIS PROUTY (Cargill)

Pricing Convertible Bonds under the First-Passage Credit Risk Model

Pricing Convertible Bonds under the First-Passage Credit Risk Model Prof. Tian-Shyr Dai Department of Information Management and Finance National Chiao Tung University Joint work with Prof. Chuan-Ju Wang

Pricing Convertible Bonds under the First-Passage Credit Risk Model Prof. Tian-Shyr Dai Department of Information Management and Finance National Chiao Tung University Joint work with Prof. Chuan-Ju Wang

Math489/889 Stochastic Processes and Advanced Mathematical Finance Solutions to Practice Problems

Math489/889 Stochastic Processes and Advanced Mathematical Finance Solutions to Practice Problems Steve Dunbar No Due Date: Practice Only. Find the mode (the value of the independent variable with the

Math489/889 Stochastic Processes and Advanced Mathematical Finance Solutions to Practice Problems Steve Dunbar No Due Date: Practice Only. Find the mode (the value of the independent variable with the

Volatility Smiles and Yield Frowns

Volatility Smiles and Yield Frowns Peter Carr NYU IFS, Chengdu, China, July 30, 2018 Peter Carr (NYU) Volatility Smiles and Yield Frowns 7/30/2018 1 / 35 Interest Rates and Volatility Practitioners and

Volatility Smiles and Yield Frowns Peter Carr NYU IFS, Chengdu, China, July 30, 2018 Peter Carr (NYU) Volatility Smiles and Yield Frowns 7/30/2018 1 / 35 Interest Rates and Volatility Practitioners and

Saddlepoint Approximation Methods for Pricing. Financial Options on Discrete Realized Variance

Saddlepoint Approximation Methods for Pricing Financial Options on Discrete Realized Variance Yue Kuen KWOK Department of Mathematics Hong Kong University of Science and Technology Hong Kong * This is

Saddlepoint Approximation Methods for Pricing Financial Options on Discrete Realized Variance Yue Kuen KWOK Department of Mathematics Hong Kong University of Science and Technology Hong Kong * This is

Rohini Kumar. Statistics and Applied Probability, UCSB (Joint work with J. Feng and J.-P. Fouque)

") Small time asymptotics for fast mean-reverting stochastic volatility models Statistics and Applied Probability, UCSB (Joint work with J. Feng and J.-P. Fouque) March 11, 2011 Frontier Probability Days,

Small time asymptotics for fast mean-reverting stochastic volatility models Statistics and Applied Probability, UCSB (Joint work with J. Feng and J.-P. Fouque) March 11, 2011 Frontier Probability Days,

Time-changed Brownian motion and option pricing

Time-changed Brownian motion and option pricing Peter Hieber Chair of Mathematical Finance, TU Munich 6th AMaMeF Warsaw, June 13th 2013 Partially joint with Marcos Escobar (RU Toronto), Matthias Scherer

Time-changed Brownian motion and option pricing Peter Hieber Chair of Mathematical Finance, TU Munich 6th AMaMeF Warsaw, June 13th 2013 Partially joint with Marcos Escobar (RU Toronto), Matthias Scherer

IEOR E4703: Monte-Carlo Simulation

IEOR E4703: Monte-Carlo Simulation Simulating Stochastic Differential Equations Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

IEOR E4703: Monte-Carlo Simulation Simulating Stochastic Differential Equations Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

Monte Carlo Simulations

Monte Carlo Simulations Lecture 1 December 7, 2014 Outline Monte Carlo Methods Monte Carlo methods simulate the random behavior underlying the financial models Remember: When pricing you must simulate

Monte Carlo Simulations Lecture 1 December 7, 2014 Outline Monte Carlo Methods Monte Carlo methods simulate the random behavior underlying the financial models Remember: When pricing you must simulate

Sample Path Large Deviations and Optimal Importance Sampling for Stochastic Volatility Models

Sample Path Large Deviations and Optimal Importance Sampling for Stochastic Volatility Models Scott Robertson Carnegie Mellon University scottrob@andrew.cmu.edu http://www.math.cmu.edu/users/scottrob June

Sample Path Large Deviations and Optimal Importance Sampling for Stochastic Volatility Models Scott Robertson Carnegie Mellon University scottrob@andrew.cmu.edu http://www.math.cmu.edu/users/scottrob June

Option Pricing and Calibration with Time-changed Lévy processes

Option Pricing and Calibration with Time-changed Lévy processes Yan Wang and Kevin Zhang Warwick Business School 12th Feb. 2013 Objectives 1. How to find a perfect model that captures essential features

Option Pricing and Calibration with Time-changed Lévy processes Yan Wang and Kevin Zhang Warwick Business School 12th Feb. 2013 Objectives 1. How to find a perfect model that captures essential features

PRICING TIMER OPTIONS UNDER FAST MEAN-REVERTING STOCHASTIC VOLATILITY

CANADIAN APPLIED MATHEMATICS QUARTERLY Volume 17, Number 4, Winter 009 PRICING TIMER OPTIONS UNDER FAST MEAN-REVERTING STOCHASTIC VOLATILITY DAVID SAUNDERS ABSTRACT. Timer options are derivative securities

CANADIAN APPLIED MATHEMATICS QUARTERLY Volume 17, Number 4, Winter 009 PRICING TIMER OPTIONS UNDER FAST MEAN-REVERTING STOCHASTIC VOLATILITY DAVID SAUNDERS ABSTRACT. Timer options are derivative securities

Applying the Principles of Quantitative Finance to the Construction of Model-Free Volatility Indices

Applying the Principles of Quantitative Finance to the Construction of Model-Free Volatility Indices Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg

Applying the Principles of Quantitative Finance to the Construction of Model-Free Volatility Indices Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg

Calculating Implied Volatility

Statistical Laboratory University of Cambridge University of Cambridge Mathematics and Big Data Showcase 20 April 2016 How much is an option worth? A call option is the right, but not the obligation, to

Statistical Laboratory University of Cambridge University of Cambridge Mathematics and Big Data Showcase 20 April 2016 How much is an option worth? A call option is the right, but not the obligation, to

Quadratic hedging in affine stochastic volatility models

Quadratic hedging in affine stochastic volatility models Jan Kallsen TU München Pittsburgh, February 20, 2006 (based on joint work with F. Hubalek, L. Krawczyk, A. Pauwels) 1 Hedging problem S t = S 0

Quadratic hedging in affine stochastic volatility models Jan Kallsen TU München Pittsburgh, February 20, 2006 (based on joint work with F. Hubalek, L. Krawczyk, A. Pauwels) 1 Hedging problem S t = S 0

Modeling the Implied Volatility Surface. Jim Gatheral Global Derivatives and Risk Management 2003 Barcelona May 22, 2003

Modeling the Implied Volatility Surface Jim Gatheral Global Derivatives and Risk Management 2003 Barcelona May 22, 2003 This presentation represents only the personal opinions of the author and not those

Modeling the Implied Volatility Surface Jim Gatheral Global Derivatives and Risk Management 2003 Barcelona May 22, 2003 This presentation represents only the personal opinions of the author and not those

Application of Stochastic Calculus to Price a Quanto Spread

Application of Stochastic Calculus to Price a Quanto Spread Christopher Ting http://www.mysmu.edu/faculty/christophert/ Algorithmic Quantitative Finance July 15, 2017 Christopher Ting July 15, 2017 1/33

Application of Stochastic Calculus to Price a Quanto Spread Christopher Ting http://www.mysmu.edu/faculty/christophert/ Algorithmic Quantitative Finance July 15, 2017 Christopher Ting July 15, 2017 1/33

Crashcourse Interest Rate Models

Crashcourse Interest Rate Models Stefan Gerhold August 30, 2006 Interest Rate Models Model the evolution of the yield curve Can be used for forecasting the future yield curve or for pricing interest rate

Crashcourse Interest Rate Models Stefan Gerhold August 30, 2006 Interest Rate Models Model the evolution of the yield curve Can be used for forecasting the future yield curve or for pricing interest rate

Economathematics. Problem Sheet 1. Zbigniew Palmowski. Ws 2 dw s = 1 t

Economathematics Problem Sheet 1 Zbigniew Palmowski 1. Calculate Ee X where X is a gaussian random variable with mean µ and volatility σ >.. Verify that where W is a Wiener process. Ws dw s = 1 3 W t 3

Economathematics Problem Sheet 1 Zbigniew Palmowski 1. Calculate Ee X where X is a gaussian random variable with mean µ and volatility σ >.. Verify that where W is a Wiener process. Ws dw s = 1 3 W t 3

Managing Systematic Mortality Risk in Life Annuities: An Application of Longevity Derivatives

Managing Systematic Mortality Risk in Life Annuities: An Application of Longevity Derivatives Simon Man Chung Fung, Katja Ignatieva and Michael Sherris School of Risk & Actuarial Studies University of

Managing Systematic Mortality Risk in Life Annuities: An Application of Longevity Derivatives Simon Man Chung Fung, Katja Ignatieva and Michael Sherris School of Risk & Actuarial Studies University of

Credit Risk : Firm Value Model

Credit Risk : Firm Value Model Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe and Karlsruhe Institute of Technology (KIT) Prof. Dr. Svetlozar Rachev

Credit Risk : Firm Value Model Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe and Karlsruhe Institute of Technology (KIT) Prof. Dr. Svetlozar Rachev

Youngrok Lee and Jaesung Lee

orean J. Math. 3 015, No. 1, pp. 81 91 http://dx.doi.org/10.11568/kjm.015.3.1.81 LOCAL VOLATILITY FOR QUANTO OPTION PRICES WITH STOCHASTIC INTEREST RATES Youngrok Lee and Jaesung Lee Abstract. This paper

orean J. Math. 3 015, No. 1, pp. 81 91 http://dx.doi.org/10.11568/kjm.015.3.1.81 LOCAL VOLATILITY FOR QUANTO OPTION PRICES WITH STOCHASTIC INTEREST RATES Youngrok Lee and Jaesung Lee Abstract. This paper

Lecture on advanced volatility models

FMS161/MASM18 Financial Statistics Stochastic Volatility (SV) Let r t be a stochastic process. The log returns (observed) are given by (Taylor, 1982) r t = exp(v t /2)z t. The volatility V t is a hidden

FMS161/MASM18 Financial Statistics Stochastic Volatility (SV) Let r t be a stochastic process. The log returns (observed) are given by (Taylor, 1982) r t = exp(v t /2)z t. The volatility V t is a hidden

Probability in Options Pricing

Probability in Options Pricing Mark Cohen and Luke Skon Kenyon College cohenmj@kenyon.edu December 14, 2012 Mark Cohen and Luke Skon (Kenyon college) Probability Presentation December 14, 2012 1 / 16 What

Probability in Options Pricing Mark Cohen and Luke Skon Kenyon College cohenmj@kenyon.edu December 14, 2012 Mark Cohen and Luke Skon (Kenyon college) Probability Presentation December 14, 2012 1 / 16 What

Market interest-rate models

Market interest-rate models Marco Marchioro www.marchioro.org November 24 th, 2012 Market interest-rate models 1 Lecture Summary No-arbitrage models Detailed example: Hull-White Monte Carlo simulations

Market interest-rate models Marco Marchioro www.marchioro.org November 24 th, 2012 Market interest-rate models 1 Lecture Summary No-arbitrage models Detailed example: Hull-White Monte Carlo simulations

Structural Models of Credit Risk and Some Applications

Structural Models of Credit Risk and Some Applications Albert Cohen Actuarial Science Program Department of Mathematics Department of Statistics and Probability albert@math.msu.edu August 29, 2018 Outline

Structural Models of Credit Risk and Some Applications Albert Cohen Actuarial Science Program Department of Mathematics Department of Statistics and Probability albert@math.msu.edu August 29, 2018 Outline

Forwards and Futures. Chapter Basics of forwards and futures Forwards

Chapter 7 Forwards and Futures Copyright c 2008 2011 Hyeong In Choi, All rights reserved. 7.1 Basics of forwards and futures The financial assets typically stocks we have been dealing with so far are the

Chapter 7 Forwards and Futures Copyright c 2008 2011 Hyeong In Choi, All rights reserved. 7.1 Basics of forwards and futures The financial assets typically stocks we have been dealing with so far are the

Estimation of Stochastic Volatility Models with Implied. Volatility Indices and Pricing of Straddle Option

Estimation of Stochastic Volatility Models with Implied Volatility Indices and Pricing of Straddle Option Yue Peng Steven C. J. Simon June 14, 29 Abstract Recent market turmoil has made it clear that modelling

Estimation of Stochastic Volatility Models with Implied Volatility Indices and Pricing of Straddle Option Yue Peng Steven C. J. Simon June 14, 29 Abstract Recent market turmoil has made it clear that modelling