Duration Models: Parametric Models

|

|

|

- Sheena McKinney

- 6 years ago

- Views:

Transcription

1 Duration Models: Parametric Models Brad 1 1 Department of Political Science University of California, Davis January 28, 2011

2

3 Parametric Models Some Motivation for Parametrics Consider the hazard rate: dh(t) dt > 0, Hazard increasing wrt time. dh(t) dt < 0, Hazard decreasing wrt time. dh(t) dt = 0, Hazard flat wrt time.

4 Parametric Models Parametric models give structure (shape) to the hazard function. N.B.: the structure is a function of the c.d.f., not necessarily of the real world.... though some c.d.f.s do a good job of approximating some failure-time processes. Any c.d.f. with positive support on the real number line will work. Lots of choices: exponential, Weibull, gamma, Gompertz, log-normal, log-logistic... etc.

5

6 Parametric Models For parametrics, we work with standard likelihood methods. Specify a distribution function and write out the log-likelihood for the data. The question is, which distribution function? In all software programs/computing environments, youre given a menu. Stata:streg, R:survreg, eha

7 Parametric Models Advantages of parametric models? If S(t) is known to follow, or closely approximate a known distribution, then estimates will be consistent the the theoretical survivor function. Unlike K-M or Cox (discussed later), the hazard may be used for forecasting (under KM or Cox, the hazard is only defined up until the last observed failure). Will return smooth functions of h(t) or S(t).

8 Parametric Models As noted, there are a wide variety of choices. I sometimes refer to these choices as plug and play estimators. Why? Consider the survivor function: S(t) = Pr(T > t) = t t f (u)d(u) = 1 f (u)d(u) = 1 F (t) 0 (1) If we know this function follows some distribution, then we write a likelihood function in terms of this distribution... If it follows a different distribution, just replace the previous likelihood with another pdf.

9 Parametric Models Most texts, including ours, typically begin with the exponential distribution. The reason is easy: it s an easy distribution to work with and visualize. It also may be unrealistic in many settings. The basic feature: the hazard rate is flat wrt time. That is: h(t) = λ (2)

10 Parametric Models Recall from the first week: where Substituting λ into (3), S(t) = exp{ H(t)} (3) H(t) = t 0 h(u)du t S(t) = exp{ λdu} 0 and so S(t) = exp( λt) This is the survivor function for the exponential distribution.

11 Parametric Models Since we know f (t) = h(t)s(t) then f (t) = λ exp( λt) This is the pdf of a random variable T that is exponentially distributed. Note how the unconditional probability of failure, f (t), handles censored cases. Consider the hazard function:

12

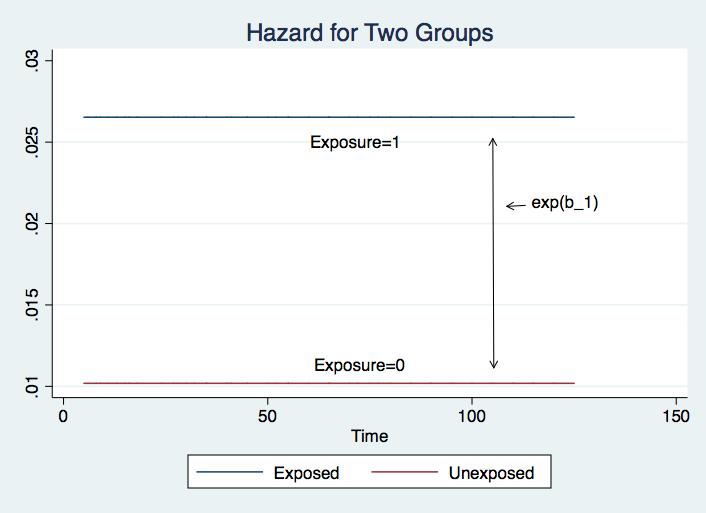

13 Parametric Models What is λ? Or put differently, where are the predictor variables? Typically λ will be parameterized in terms of regression coefficients and covariates, X. A model: h(t) = λ = exp(β 0 + β 1 T ) Suppose T is a treatment indicator and we re interested in the hazard of failure for the treated and untreated.

14 Parametric Models Two hazards: h(t T =1 ) = exp(β 0 + β 1 ) h(t T =0 ) = exp(β 0 ) If we plotted the hazards, we would have two parallel lines separated by exp(β 1 ). Or analogously, if we want to compare hazards: h(t T =1 ) h(t T =0 ) = exp(β 0 + β 1 ) exp(β 0 ) item 4- This expression must simplify to exp(β 1 ).

15 Parametric Models In words (sort of)...the ratio of the treated to the untreated simplifies to exp(β 1 ). So all we need to know to know the differences in the hazards is the coefficient for the treated. This is an important result because it shows the hazards are proportional hazards. Some simulated data. h(t) = (Z) Let Z denote whether or not a subject was exposed to some condition.

16 Parametric Models Since β 1 is positive, this implies exposure increases the risk. The hazard is higher for the exposed than for the unexposed. Treatment estimate is.96 implies difference in hazard is exp(.96) 2.6 Risk for exposed is about 2.6 times greater than for the unexposed. Consider the hazards:

17

18 Parametric Models PH property is important to understand. By way of analogy, think about what odds ratios are in a logit-type setting or recall the ordered logit model: the OR are invariant to the scale scores. The proportional difference in hazards is invariant to time. So under the exponential we are making two assumptions: 1. The hazards are flat wrt time. 2. The difference in hazards across levels of a covariate is a fixed proportion. Which is the stronger assumption?

19 Parametric Models Note that even with the PH assumption, we are not saying (in general) the hazards are invariant to time (though in the exponential case, we are). The hazards may change but the proportional difference between (say) two groups, does not change. That s the basic result of proportionality. Suppose it does not hold. Then what? Consider another model that relaxes the assumption of flat hazards (but not the PH assumption).

20 Parametric Models: Weibull A more flexible distribution function is given by the Weibull. Named for Waloddi Weibull, who derived it (1939, 1951) Why more general than the exponential? It is a two-parameter distribution: h(t) = λpt p 1 (4) where λ is a positive scale parameter and p is a shape parameter. Note: p > 1, the hazard rate is monotonically increasing with time. p < 1, the hazard rate is monotonically decreasing with time. p = 1, the hazard is flat.

21 Parametric Models: Weibull Thus if p = 1 then h(t) = λ1t 1 1 = λ. (5) Thus demonstrating that the exponential model is nested within the Weibull. For this reason (and for many other reasons), the Weibull is the most commonly applied parametric model in survival analysis. As with the exponential, the scale parameter λ is usually expressed in terms of covariates, exp(β k x i ). Hazard functions plotted for different p:

22

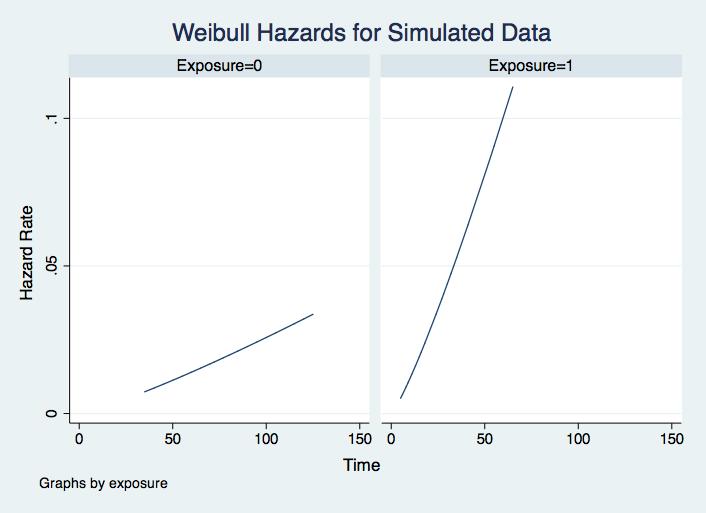

23 Parametric Models: Weibull Using the connection between S(t) and the cumulative hazard (see eq. [3]), the Weibull survivor function is given by t S(t) = exp{ λpu p 1 du} = exp( λt p ). 0 And since the pdf is h(t)s(t), the density for a random variable T distributed as a Weibull is f (t) = λpt p 1 exp( λt p ). Suppose we estimate a Weibull hazard using the data from before.

24

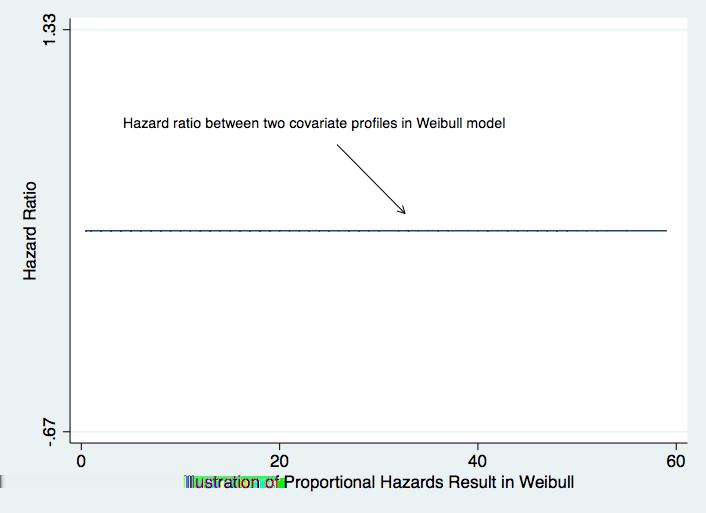

25 Parametric Models: Weibull Note: h(t E ) h(t NE ) = exp(β 0 + β 1 )pt p 1 exp(β 0 )pt p 1 = exp(β 1 ) In other words, the Weibull model is a proportional hazards model. So unlike the exponential, the hazards can change wrt time but like the exponential, the ratio of the hazards is a constant. They are offset by a proportionality factor of exp(β).

26 Parametric Models: Weibull The Weibull (and therefore) the exponential are interesting models. They are both proportional hazards models as well as accelerated failure time models. In other words, one can estimate the model in terms of the hazards or in terms of the survival times and reproduce equivalent results from different parameterizations. Under the PH model, the covariates are a multiplicative effect with respect to the baseline hazard function (see previous slide). Under the AFT, the covariates are multiplicative wrt the survival time.

27 Parametric Models: Weibull Proportional Hazards: h(t x) = h 0 t exp(β1x 1 + β 2 x β j x j ) Accelerated Failure Time: log(t ) = β 0 + β 1 x 1 + β 2 x β j x j + σɛ where ɛ is a stochastic disturbance term with type-1 extreme-value distribution scaled by σ. Note: σ = 1/p. Extreme-value has a close connection to Weibull: the distribution of the log of a Weibull distributed random variable yields a type-1 extreme value distribution.

28 Parametric Models: Weibull In the AFT formulation, the coefficients are sometimes referred to as acceleration factors. They give information about how the survival times are differentially accelerated for different levels of a covariate. Suppose we estimate a treatment effect for two groups: D and H. Imagine the estimated treatment effect yields a coefficient of 7. That is, group H is estimated to survive 7 times longer than group D. S D (t) = S H (7t) If D are dogs and H are humans, the acceleration factor suggests human lifespans are stretched out 7 times longer than dogs. (Example from K and K, p. 266.)

29 Parametric Models: Weibull Important to be aware of what your software is doing! The PH coefficients inform us about the hazard (i.e. risk). The AFT coefficients inform us about survival. Therefore, the coefficients will be signed differently.

30 Parametric Models: Weibull Weibull hazard is monotonic. Log-logistic and log-normal allow for nonmonotonic hazards. Both estimated only as AFT models: log(t ) = βx + σɛ. The AFT for each of these models has two parameters.

31 Parametric Models: Log-Logistic The log-logistic is one choice for non-monotonic hazards: h(t) = λptp λt p h(t) increases and then decreases if p > 1; monotonically decreasing when p 1.

32

33 Parametric Models: Log-Logistic Again, λ gives information on the covariates (i.e. here is where the regression coefficients are. While the log-logistic is not a PH model, it is a proportional odds model. Recall what this is from your previous course on MLE. Survivor function: S(t) = λt p = λtp 1 + λt p Substitute exp(β) in for λ and you can see the connection back to the logistic cdf.

34 Parametric Models: Log-Logistic The odds of failure: 1 S(t) S(t) = λt p 1+λt p 1 1+λt p = λt p In terms of parameters, exponentiating β will give the acceleration factor. Interpretation is really quite similar to a logit model (but it is not exactly the same!). Other models?

35 Parametric Models: Estimation Previous can be estimated through MLE Imagine n observations upon which t 1, t 2,... t n duration times are measured. Assume conditional independence of t i (may be herculean assumption; more later) Specify a PDF (or CDF); if f (t) is derived, S(t) easily follows Write out likelihood function and maximize (standard algorithm is Newton-Raphson)

36 Parametric Models: Estimation Generic Likelihood: L = n {f (t i )} δ i {S(t i )} 1 δ i i=1 where δ i is the censoring (failure) indicator. Example: Weibull Survivor function f (t) = λpt p 1 exp (λt p ) S(t) = exp (λt p ) The likelihood of the t duration times: n L = {λpt p 1 exp (λt p )} δ i {exp (λt p )} 1 δ i i=1

37 Getting Our Hands Dirty The only way to learn is to do. Useful to consider estimation and interpretation of some parametric models. Examples are based on cabinet duration data and most of the code is in Stata. Stata do file is accessible on SmartSite and website.

38 Exponential Cabinet duration as a function of post-election negotiations indicator and formation attempts. Table: Estimation results : PH Exponential Variable Coefficient (Std. Err.) format (0.039) postelec (0.124) Intercept (0.106)

39 Exponential Coefficients are in PH scale so a positively signed coefficient implies the hazard is increasing as a function of x. Post-election negotiations lowers the hazard; increased number of formation attempts increase the hazard. Graphical display of two covariate profiles.

40

41 Exponential Turn attention to the Stata examples (we will do this in class). Consider the AFT model. Recall the AFT model: log(t ) = β k x i + σɛ If ɛ is type-1 extreme value (aka Gumbel) then the Weibull is obtained. If σ = p = 1 then the exponential is obtained. The coefficients are multiples of the survivor function.

42 Exponential Table: Estimation results : AFT Exponential Variable Coefficient (Std. Err.) format (0.039) postelec (0.124) Intercept (0.106)

43 Exponential Contrast the PH and AFT models. Under the exponential, the signs shift but the coefficients are unchanged in value. Sign shift makes sense: AFT formulation tells us about survivorship. AFT Hazard: h o (t) exp (xβ) = exp (β 0 + xβ k ) Solving for t: t = [ log(s(t)] exp(β 0 + β 1 postelec) If t =.5, we solve for the median survival time. Turn back to the Stata examples.

44 Exponential From the application, note the equivalency of the two models. Note also that the ratio of two survival times for two covariate profiles (i.e. X = 1 vs. X = 0) will be constant and proportional wrt S(t). Hence either parameterization exhibits proportionality. Weibull example.

45 Weibull Under the exponential the hazard is flat.. Under the Weibull: h(t) = λpt p 1 (6) λ is positive scale parameter; p is the shape parameter. p > 1, the hazard rate is monotonically increasing with time. p < 1, the hazard rate is monotonically decreasing with time. p = 1, the hazard is flat, i.e. exponential. Note that λ corresponds to covariates: exp(β k x i )

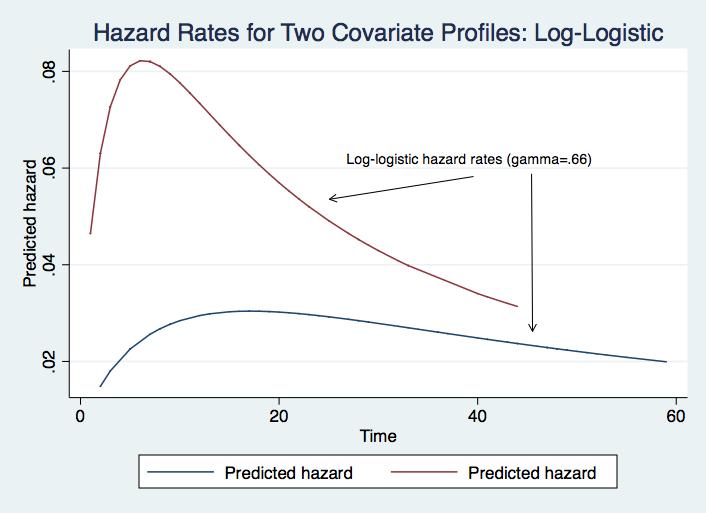

46 Weibull hazards Consider application again. Table: Estimation results : PH Weibull Variable Coefficient (Std. Err.) Equation 1 : t format (0.039) postelec (0.129) Intercept (0.199) Equation 2 : ln p Intercept (0.050)

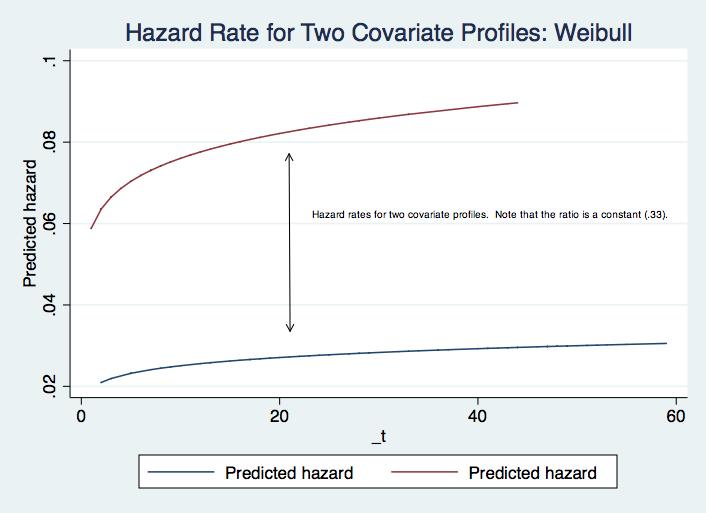

47 Weibull Coefficients are interpreted as before though now we have an additional parameter. p > 1 implying rising hazards for this model. Consider the hazard rates for two covariate profiles.

48

49 Weibull Observations? Note the shape is governed by p... But the difference in the two hazards are proportional. Looks may be deceiving; perhaps you think the lines show nonproportionality. Back to the application.

50

51 Weibull Consider the AFT formulation Table: Estimation results : weibull Variable Coefficient (Std. Err.) Equation 1 : t format (0.035) postelec (0.113) Intercept (0.096) Equation 2 : ln p Intercept (0.050)

52 Weibull Similar interpretation is afforded this model as was the case with the exponential AFT. Note under the AFT: S(t) = exp( λt p ) Therefore, t = [ log S(t)] 1/p 1. λ 1/p Expressing 1 in terms of the model parameters, we obtain λ 1/p t = [ log S(t)] 1/p exp(β 0 + β k x) As with the exponential, let q denote some S(t), then we can estimate S(t) for some value q: t = [ log S(q)] 1/p exp(β 0 + β k x) So for the median, q =.5. Go to example.

53 Log-Logistic Consider now the log-logistic. The log-logistic is only an AFT model. Table: Estimation results : AFT: Log-Logistic Variable Coefficient (Std. Err.) Equation 1 : t format (0.050) postelec (0.130) Intercept (0.126) Equation 2 : ln gam Intercept (0.051)

54

55 Log-Logistic Consider now the log-logistic. The log-logistic is only an AFT model. Note that Stata reports γ as the shape parameter. This is the inverse of p. Consider the survivor function: S(t) = 1 1+λt p = 1 1+(λ 1/p t)p Suppose we solve for t: t = [ 1 S(t) 1]1/p 1 λ 1/p Express the second term in terms of covariates, we obtain: t = [ 1 S(t) 1]1/p exp(β 0 + β k x) To the example.

56 Log-Logistic Because the log-logistic is AFT and proportional odds, this ratio should be equivalent to the acceleration factor (i.e. the odds ratio exp(β 1 )). So this too is a proportional model... in the odds ratios. This assumption may not hold.

57 Many Applications These are plug and play estimators. They are easy to do. Let s run through some illustrations, first in Stata and then in R I use the cabinet duration data.

58 Weibull. streg invest polar numst format postelec caretakr, dist(weib) time nolog failure _d: analysis time _t: censor durat Weibull regression -- accelerated failure-time form No. of subjects = 314 Number of obs = 314 No. of failures = 271 Time at risk = LR chi2(6) = Log likelihood = Prob > chi2 = _t Coef. Std. Err. z P> z [95% Conf. Interval] invest polar numst format postelec caretakr _cons /ln_p p /p

59 Exponential. streg invest polar numst format postelec caretakr, dist(exp) time nolog failure _d: analysis time _t: censor durat Exponential regression -- accelerated failure-time form No. of subjects = 314 Number of obs = 314 No. of failures = 271 Time at risk = LR chi2(6) = Log likelihood = Prob > chi2 = _t Coef. Std. Err. z P> z [95% Conf. Interval] invest polar numst format postelec caretakr _cons

60 Log-logistic. streg invest polar numst format postelec caretakr, dist(loglog) time nolog failure _d: analysis time _t: censor durat Log-logistic regression -- accelerated failure-time form No. of subjects = 314 Number of obs = 314 No. of failures = 271 Time at risk = LR chi2(6) = Log likelihood = Prob > chi2 = _t Coef. Std. Err. z P> z [95% Conf. Interval] invest polar numst format postelec caretakr _cons /ln_gam gamma

61 Log-normal. streg invest polar numst format postelec caretakr, dist(lognorm) time nolog failure _d: analysis time _t: censor durat Log-normal regression -- accelerated failure-time form No. of subjects = 314 Number of obs = 314 No. of failures = 271 Time at risk = LR chi2(6) = Log likelihood = Prob > chi2 = _t Coef. Std. Err. z P> z [95% Conf. Interval] invest polar numst format postelec caretakr _cons /ln_sig sigma

62 Weibull > cab.weib<-survreg(surv(durat,censor)~invest + polar + numst + + format + postelec + caretakr,data=cabinet, + dist= weibull ) > > summary(cab.weib) Call: survreg(formula = Surv(durat, censor) ~ invest + polar + numst + format + postelec + caretakr, data = cabinet, dist = "weibull") Value Std. Error z p (Intercept) e-120 invest e-03 polar e-05 numst e-06 format e-03 postelec e-11 caretakr e-11 Log(scale) e-07 Scale= Weibull distribution Loglik(model)= Loglik(intercept only)= Chisq= on 6 degrees of freedom, p= 0 Number of Newton-Raphson Iterations: 5 n= 314

63 Log-Logistic > cab.ll<-survreg(surv(durat,censor)~invest + polar + numst + + format + postelec + caretakr,data=cabinet, + dist= loglogistic ) > > summary(cab.ll) Call: survreg(formula = Surv(durat, censor) ~ invest + polar + numst + format + postelec + caretakr, data = cabinet, dist = "loglogistic") Value Std. Error z p (Intercept) e-65 invest e-03 polar e-05 numst e-05 format e-03 postelec e-07 caretakr e-08 Log(scale) e-28 Scale= Log logistic distribution Loglik(model)= Loglik(intercept only)= Chisq= on 6 degrees of freedom, p= 0 Number of Newton-Raphson Iterations: 4 n= 314

64 > ##Log-Normal can be fit using survreg: > > cab.ln<-survreg(surv(durat,censor)~invest + polar + numst + + format + postelec + caretakr,data=cabinet, + dist= lognormal ) > > summary(cab.ln) Call: survreg(formula = Surv(durat, censor) ~ invest + polar + numst + format + postelec + caretakr, data = cabinet, dist = "lognormal") Value Std. Error z p (Intercept) e-57 invest e-03 polar e-05 numst e-06 format e-03 postelec e-07 caretakr e-05 Log(scale) e-01 Scale= 1.01 Log Normal distribution Loglik(model)= Loglik(intercept only)= Chisq= on 6 degrees of freedom, p= 0 Number of Newton-Raphson Iterations: 4 n= 314

65 Comparing Log-Likelihoods (note: non-nested models). I did this in R: anova(cab.weib, cab.ln, cab.ll) 1 invest + polar + numst + format + postelec + caretakr 2 invest + polar + numst + format + postelec + caretakr 3 invest + polar + numst + format + postelec + caretakr Resid. Df -2*LL Test Df Deviance P(> Chi ) NA NA NA = NA = NA

66 Back to Stata: Generalized Gamma. streg invest polar numst format postelec caretakr, dist(gamma) nolog failure _d: analysis time _t: censor durat Gamma regression -- accelerated failure-time form No. of subjects = 314 Number of obs = 314 No. of failures = 271 Time at risk = LR chi2(6) = Log likelihood = Prob > chi2 = _t Coef. Std. Err. z P> z [95% Conf. Interval] invest polar numst format postelec caretakr _cons /ln_sig /kappa sigma

67 Adjudication Lots of Choices Selection can be arbitrary If parametrically nested, standard LR tests apply. Encompassing Distribution: generalized gamma: f (t) = λp(λt)pκ 1 exp[ (λt) p ] Γ(κ) When κ = 1, the Weibull is implied; when κ = p = 1, the exponential distribution is implied; when κ = 0, the log-normal distribution is implied; and when p = 1, the gamma distribution is implied. In illustrations above, verify that Weibull would be preferred model among the choices. AIC ( 2(log L) + 2(c + p + 1)) also confirms Weibull is preferred model among choices. (7)

68 Survivor Functions Cabinet Duration Figure: The figure graphs the generalized gamma and Weibull survivor functions for the cabinet duration data. The Weibull estimates are denoted by the O symbol and the generalized gamma estimates are

69 denoted by the line.

70 Table: AIC and Log-Likelihoods for Cabinet Models Model Log-Likelihood AIC Exponential Weibull Log-Logistic Log-Normal Gompertz Generalized Gamma

Duration Models: Modeling Strategies

Bradford S., UC-Davis, Dept. of Political Science Duration Models: Modeling Strategies Brad 1 1 Department of Political Science University of California, Davis February 28, 2007 Bradford S., UC-Davis,

Bradford S., UC-Davis, Dept. of Political Science Duration Models: Modeling Strategies Brad 1 1 Department of Political Science University of California, Davis February 28, 2007 Bradford S., UC-Davis,

Estimation Procedure for Parametric Survival Distribution Without Covariates

Estimation Procedure for Parametric Survival Distribution Without Covariates The maximum likelihood estimates of the parameters of commonly used survival distribution can be found by SAS. The following

Estimation Procedure for Parametric Survival Distribution Without Covariates The maximum likelihood estimates of the parameters of commonly used survival distribution can be found by SAS. The following

STATA log file for Time-Varying Covariates (TVC) Duration Model Estimations.

Duration Model Estimations.") STATA log file for Time-Varying Covariates (TVC) Duration Model Estimations. This STATA 8.0 log file reports estimations in which CDER Staff Aggregates and PDUFA variable are assigned to drug-months of

STATA log file for Time-Varying Covariates (TVC) Duration Model Estimations. This STATA 8.0 log file reports estimations in which CDER Staff Aggregates and PDUFA variable are assigned to drug-months of

Chapter 2 ( ) Fall 2012

Fall 2012") Bios 323: Applied Survival Analysis Qingxia (Cindy) Chen Chapter 2 (2.1-2.6) Fall 2012 Definitions and Notation There are several equivalent ways to characterize the probability distribution of a survival

Bios 323: Applied Survival Analysis Qingxia (Cindy) Chen Chapter 2 (2.1-2.6) Fall 2012 Definitions and Notation There are several equivalent ways to characterize the probability distribution of a survival

This notes lists some statistical estimates on which the analysis and discussion in the Health Affairs article was based.

Commands and Estimates for D. Carpenter, M. Chernew, D. G. Smith, and A. M. Fendrick, Approval Times For New Drugs: Does The Source Of Funding For FDA Staff Matter? Health Affairs (Web Exclusive) December

Commands and Estimates for D. Carpenter, M. Chernew, D. G. Smith, and A. M. Fendrick, Approval Times For New Drugs: Does The Source Of Funding For FDA Staff Matter? Health Affairs (Web Exclusive) December

An Introduction to Event History Analysis

An Introduction to Event History Analysis Oxford Spring School June 18-20, 2007 Day Three: Diagnostics, Extensions, and Other Miscellanea Data Redux: Supreme Court Vacancies, 1789-1992. stset service,

An Introduction to Event History Analysis Oxford Spring School June 18-20, 2007 Day Three: Diagnostics, Extensions, and Other Miscellanea Data Redux: Supreme Court Vacancies, 1789-1992. stset service,

Survival Analysis APTS 2016/17 Preliminary material

Survival Analysis APTS 2016/17 Preliminary material Ingrid Van Keilegom KU Leuven (ingrid.vankeilegom@kuleuven.be) August 2017 1 Introduction 2 Common functions in survival analysis 3 Parametric survival

Survival Analysis APTS 2016/17 Preliminary material Ingrid Van Keilegom KU Leuven (ingrid.vankeilegom@kuleuven.be) August 2017 1 Introduction 2 Common functions in survival analysis 3 Parametric survival

Logistic Regression Analysis

Revised July 2018 Logistic Regression Analysis This set of notes shows how to use Stata to estimate a logistic regression equation. It assumes that you have set Stata up on your computer (see the Getting

Revised July 2018 Logistic Regression Analysis This set of notes shows how to use Stata to estimate a logistic regression equation. It assumes that you have set Stata up on your computer (see the Getting

Statistical Analysis of Life Insurance Policy Termination and Survivorship

Statistical Analysis of Life Insurance Policy Termination and Survivorship Emiliano A. Valdez, PhD, FSA Michigan State University joint work with J. Vadiveloo and U. Dias Sunway University, Malaysia Kuala

Statistical Analysis of Life Insurance Policy Termination and Survivorship Emiliano A. Valdez, PhD, FSA Michigan State University joint work with J. Vadiveloo and U. Dias Sunway University, Malaysia Kuala

Logit Models for Binary Data

Chapter 3 Logit Models for Binary Data We now turn our attention to regression models for dichotomous data, including logistic regression and probit analysis These models are appropriate when the response

Chapter 3 Logit Models for Binary Data We now turn our attention to regression models for dichotomous data, including logistic regression and probit analysis These models are appropriate when the response

Maximum Likelihood Estimation Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised January 10, 2017

Maximum Likelihood Estimation Richard Williams, University of otre Dame, https://www3.nd.edu/~rwilliam/ Last revised January 0, 207 [This handout draws very heavily from Regression Models for Categorical

Maximum Likelihood Estimation Richard Williams, University of otre Dame, https://www3.nd.edu/~rwilliam/ Last revised January 0, 207 [This handout draws very heavily from Regression Models for Categorical

Maximum Likelihood Estimation Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised January 13, 2018

Maximum Likelihood Estimation Richard Williams, University of otre Dame, https://www3.nd.edu/~rwilliam/ Last revised January 3, 208 [This handout draws very heavily from Regression Models for Categorical

Maximum Likelihood Estimation Richard Williams, University of otre Dame, https://www3.nd.edu/~rwilliam/ Last revised January 3, 208 [This handout draws very heavily from Regression Models for Categorical

Maximum Likelihood Estimation

Maximum Likelihood Estimation EPSY 905: Fundamentals of Multivariate Modeling Online Lecture #6 EPSY 905: Maximum Likelihood In This Lecture The basics of maximum likelihood estimation Ø The engine that

Maximum Likelihood Estimation EPSY 905: Fundamentals of Multivariate Modeling Online Lecture #6 EPSY 905: Maximum Likelihood In This Lecture The basics of maximum likelihood estimation Ø The engine that

Panel Data with Binary Dependent Variables

Essex Summer School in Social Science Data Analysis Panel Data Analysis for Comparative Research Panel Data with Binary Dependent Variables Christopher Adolph Department of Political Science and Center

Essex Summer School in Social Science Data Analysis Panel Data Analysis for Comparative Research Panel Data with Binary Dependent Variables Christopher Adolph Department of Political Science and Center

sociology SO5032 Quantitative Research Methods Brendan Halpin, Sociology, University of Limerick Spring 2018 SO5032 Quantitative Research Methods

1 SO5032 Quantitative Research Methods Brendan Halpin, Sociology, University of Limerick Spring 2018 Lecture 10: Multinomial regression baseline category extension of binary What if we have multiple possible

1 SO5032 Quantitative Research Methods Brendan Halpin, Sociology, University of Limerick Spring 2018 Lecture 10: Multinomial regression baseline category extension of binary What if we have multiple possible

Gamma Distribution Fitting

Chapter 552 Gamma Distribution Fitting Introduction This module fits the gamma probability distributions to a complete or censored set of individual or grouped data values. It outputs various statistics

Chapter 552 Gamma Distribution Fitting Introduction This module fits the gamma probability distributions to a complete or censored set of individual or grouped data values. It outputs various statistics

PASS Sample Size Software

Chapter 850 Introduction Cox proportional hazards regression models the relationship between the hazard function λ( t X ) time and k covariates using the following formula λ log λ ( t X ) ( t) 0 = β1 X1

Chapter 850 Introduction Cox proportional hazards regression models the relationship between the hazard function λ( t X ) time and k covariates using the following formula λ log λ ( t X ) ( t) 0 = β1 X1

Survival Data Analysis Parametric Models

1 Survival Data Analysis Parametric Models January 21, 2015 Sandra Gardner, PhD Dalla Lana School of Public Health University of Toronto 2 January 21, 2015 Agenda Basic Parametric Models Review: hazard

1 Survival Data Analysis Parametric Models January 21, 2015 Sandra Gardner, PhD Dalla Lana School of Public Health University of Toronto 2 January 21, 2015 Agenda Basic Parametric Models Review: hazard

Equity, Vacancy, and Time to Sale in Real Estate.

Title: Author: Address: E-Mail: Equity, Vacancy, and Time to Sale in Real Estate. Thomas W. Zuehlke Department of Economics Florida State University Tallahassee, Florida 32306 U.S.A. tzuehlke@mailer.fsu.edu

Title: Author: Address: E-Mail: Equity, Vacancy, and Time to Sale in Real Estate. Thomas W. Zuehlke Department of Economics Florida State University Tallahassee, Florida 32306 U.S.A. tzuehlke@mailer.fsu.edu

Probability and Statistics

Kristel Van Steen, PhD 2 Montefiore Institute - Systems and Modeling GIGA - Bioinformatics ULg kristel.vansteen@ulg.ac.be CHAPTER 3: PARAMETRIC FAMILIES OF UNIVARIATE DISTRIBUTIONS 1 Why do we need distributions?

Kristel Van Steen, PhD 2 Montefiore Institute - Systems and Modeling GIGA - Bioinformatics ULg kristel.vansteen@ulg.ac.be CHAPTER 3: PARAMETRIC FAMILIES OF UNIVARIATE DISTRIBUTIONS 1 Why do we need distributions?

Intro to GLM Day 2: GLM and Maximum Likelihood

Intro to GLM Day 2: GLM and Maximum Likelihood Federico Vegetti Central European University ECPR Summer School in Methods and Techniques 1 / 32 Generalized Linear Modeling 3 steps of GLM 1. Specify the

Intro to GLM Day 2: GLM and Maximum Likelihood Federico Vegetti Central European University ECPR Summer School in Methods and Techniques 1 / 32 Generalized Linear Modeling 3 steps of GLM 1. Specify the

Multinomial Logit Models - Overview Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised February 13, 2017

Multinomial Logit Models - Overview Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised February 13, 2017 This is adapted heavily from Menard s Applied Logistic Regression

Multinomial Logit Models - Overview Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised February 13, 2017 This is adapted heavily from Menard s Applied Logistic Regression

The Weibull in R is actually parameterized a fair bit differently from the book. In R, the density for x > 0 is

Weibull in R The Weibull in R is actually parameterized a fair bit differently from the book. In R, the density for x > 0 is f (x) = a b ( x b ) a 1 e (x/b) a This means that a = α in the book s parameterization

Weibull in R The Weibull in R is actually parameterized a fair bit differently from the book. In R, the density for x > 0 is f (x) = a b ( x b ) a 1 e (x/b) a This means that a = α in the book s parameterization

Introduction to the Maximum Likelihood Estimation Technique. September 24, 2015

Introduction to the Maximum Likelihood Estimation Technique September 24, 2015 So far our Dependent Variable is Continuous That is, our outcome variable Y is assumed to follow a normal distribution having

Introduction to the Maximum Likelihood Estimation Technique September 24, 2015 So far our Dependent Variable is Continuous That is, our outcome variable Y is assumed to follow a normal distribution having

Confidence Intervals for an Exponential Lifetime Percentile

Chapter 407 Confidence Intervals for an Exponential Lifetime Percentile Introduction This routine calculates the number of events needed to obtain a specified width of a confidence interval for a percentile

Chapter 407 Confidence Intervals for an Exponential Lifetime Percentile Introduction This routine calculates the number of events needed to obtain a specified width of a confidence interval for a percentile

[D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright

![[D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright](/thumbs/92/107898301.jpg "[D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright") Faculty and Institute of Actuaries Claims Reserving Manual v.2 (09/1997) Section D7 [D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright 1. Introduction

Faculty and Institute of Actuaries Claims Reserving Manual v.2 (09/1997) Section D7 [D7] PROBABILITY DISTRIBUTION OF OUTSTANDING LIABILITY FROM INDIVIDUAL PAYMENTS DATA Contributed by T S Wright 1. Introduction

Introduction to POL 217

Introduction to POL 217 Brad Jones 1 1 Department of Political Science University of California, Davis January 9, 2007 Topics of Course Outline Models for Categorical Data. Topics of Course Models for

Introduction to POL 217 Brad Jones 1 1 Department of Political Science University of California, Davis January 9, 2007 Topics of Course Outline Models for Categorical Data. Topics of Course Models for

Log-linear Modeling Under Generalized Inverse Sampling Scheme

Log-linear Modeling Under Generalized Inverse Sampling Scheme Soumi Lahiri (1) and Sunil Dhar (2) (1) Department of Mathematical Sciences New Jersey Institute of Technology University Heights, Newark,

Log-linear Modeling Under Generalized Inverse Sampling Scheme Soumi Lahiri (1) and Sunil Dhar (2) (1) Department of Mathematical Sciences New Jersey Institute of Technology University Heights, Newark,

Bivariate Birnbaum-Saunders Distribution

Department of Mathematics & Statistics Indian Institute of Technology Kanpur January 2nd. 2013 Outline 1 Collaborators 2 3 Birnbaum-Saunders Distribution: Introduction & Properties 4 5 Outline 1 Collaborators

Department of Mathematics & Statistics Indian Institute of Technology Kanpur January 2nd. 2013 Outline 1 Collaborators 2 3 Birnbaum-Saunders Distribution: Introduction & Properties 4 5 Outline 1 Collaborators

Practice Exam 1. Loss Amount Number of Losses

Practice Exam 1 1. You are given the following data on loss sizes: An ogive is used as a model for loss sizes. Determine the fitted median. Loss Amount Number of Losses 0 1000 5 1000 5000 4 5000 10000

Practice Exam 1 1. You are given the following data on loss sizes: An ogive is used as a model for loss sizes. Determine the fitted median. Loss Amount Number of Losses 0 1000 5 1000 5000 4 5000 10000

tm / / / / / / / / / / / / Statistics/Data Analysis User: Klick Project: Limited Dependent Variables{space -6}

PS 4 Monday August 16 01:00:42 2010 Page 1 tm / / / / / / / / / / / / Statistics/Data Analysis User: Klick Project: Limited Dependent Variables{space -6} log: C:\web\PS4log.smcl log type: smcl opened on:

PS 4 Monday August 16 01:00:42 2010 Page 1 tm / / / / / / / / / / / / Statistics/Data Analysis User: Klick Project: Limited Dependent Variables{space -6} log: C:\web\PS4log.smcl log type: smcl opened on:

STA 4504/5503 Sample questions for exam True-False questions.

STA 4504/5503 Sample questions for exam 2 1. True-False questions. (a) For General Social Survey data on Y = political ideology (categories liberal, moderate, conservative), X 1 = gender (1 = female, 0

STA 4504/5503 Sample questions for exam 2 1. True-False questions. (a) For General Social Survey data on Y = political ideology (categories liberal, moderate, conservative), X 1 = gender (1 = female, 0

Categorical Outcomes. Statistical Modelling in Stata: Categorical Outcomes. R by C Table: Example. Nominal Outcomes. Mark Lunt.

Categorical Outcomes Statistical Modelling in Stata: Categorical Outcomes Mark Lunt Arthritis Research UK Epidemiology Unit University of Manchester Nominal Ordinal 28/11/2017 R by C Table: Example Categorical,

Categorical Outcomes Statistical Modelling in Stata: Categorical Outcomes Mark Lunt Arthritis Research UK Epidemiology Unit University of Manchester Nominal Ordinal 28/11/2017 R by C Table: Example Categorical,

EVA Tutorial #1 BLOCK MAXIMA APPROACH IN HYDROLOGIC/CLIMATE APPLICATIONS. Rick Katz

1 EVA Tutorial #1 BLOCK MAXIMA APPROACH IN HYDROLOGIC/CLIMATE APPLICATIONS Rick Katz Institute for Mathematics Applied to Geosciences National Center for Atmospheric Research Boulder, CO USA email: rwk@ucar.edu

1 EVA Tutorial #1 BLOCK MAXIMA APPROACH IN HYDROLOGIC/CLIMATE APPLICATIONS Rick Katz Institute for Mathematics Applied to Geosciences National Center for Atmospheric Research Boulder, CO USA email: rwk@ucar.edu

Lecture 21: Logit Models for Multinomial Responses Continued

Lecture 21: Logit Models for Multinomial Responses Continued Dipankar Bandyopadhyay, Ph.D. BMTRY 711: Analysis of Categorical Data Spring 2011 Division of Biostatistics and Epidemiology Medical University

Lecture 21: Logit Models for Multinomial Responses Continued Dipankar Bandyopadhyay, Ph.D. BMTRY 711: Analysis of Categorical Data Spring 2011 Division of Biostatistics and Epidemiology Medical University

**BEGINNING OF EXAMINATION** A random sample of five observations from a population is:

**BEGINNING OF EXAMINATION** 1. You are given: (i) A random sample of five observations from a population is: 0.2 0.7 0.9 1.1 1.3 (ii) You use the Kolmogorov-Smirnov test for testing the null hypothesis,

**BEGINNING OF EXAMINATION** 1. You are given: (i) A random sample of five observations from a population is: 0.2 0.7 0.9 1.1 1.3 (ii) You use the Kolmogorov-Smirnov test for testing the null hypothesis,

Basic Procedure for Histograms

Basic Procedure for Histograms 1. Compute the range of observations (min. & max. value) 2. Choose an initial # of classes (most likely based on the range of values, try and find a number of classes that

Basic Procedure for Histograms 1. Compute the range of observations (min. & max. value) 2. Choose an initial # of classes (most likely based on the range of values, try and find a number of classes that

Point Estimation. Copyright Cengage Learning. All rights reserved.

6 Point Estimation Copyright Cengage Learning. All rights reserved. 6.2 Methods of Point Estimation Copyright Cengage Learning. All rights reserved. Methods of Point Estimation The definition of unbiasedness

6 Point Estimation Copyright Cengage Learning. All rights reserved. 6.2 Methods of Point Estimation Copyright Cengage Learning. All rights reserved. Methods of Point Estimation The definition of unbiasedness

Commonly Used Distributions

Chapter 4: Commonly Used Distributions 1 Introduction Statistical inference involves drawing a sample from a population and analyzing the sample data to learn about the population. We often have some knowledge

Chapter 4: Commonly Used Distributions 1 Introduction Statistical inference involves drawing a sample from a population and analyzing the sample data to learn about the population. We often have some knowledge

Model fit assessment via marginal model plots

The Stata Journal (2010) 10, Number 2, pp. 215 225 Model fit assessment via marginal model plots Charles Lindsey Texas A & M University Department of Statistics College Station, TX lindseyc@stat.tamu.edu

The Stata Journal (2010) 10, Number 2, pp. 215 225 Model fit assessment via marginal model plots Charles Lindsey Texas A & M University Department of Statistics College Station, TX lindseyc@stat.tamu.edu

INSTITUTE AND FACULTY OF ACTUARIES. Curriculum 2019 SPECIMEN EXAMINATION

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 2019 SPECIMEN EXAMINATION Subject CS1A Actuarial Statistics Time allowed: Three hours and fifteen minutes INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 2019 SPECIMEN EXAMINATION Subject CS1A Actuarial Statistics Time allowed: Three hours and fifteen minutes INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate

Maximum Likelihood Estimates for Alpha and Beta With Zero SAIDI Days

Maximum Likelihood Estimates for Alpha and Beta With Zero SAIDI Days 1. Introduction Richard D. Christie Department of Electrical Engineering Box 35500 University of Washington Seattle, WA 98195-500 christie@ee.washington.edu

Maximum Likelihood Estimates for Alpha and Beta With Zero SAIDI Days 1. Introduction Richard D. Christie Department of Electrical Engineering Box 35500 University of Washington Seattle, WA 98195-500 christie@ee.washington.edu

Limited Dependent Variables

Limited Dependent Variables Christopher F Baum Boston College and DIW Berlin Birmingham Business School, March 2013 Christopher F Baum (BC / DIW) Limited Dependent Variables BBS 2013 1 / 47 Limited dependent

Limited Dependent Variables Christopher F Baum Boston College and DIW Berlin Birmingham Business School, March 2013 Christopher F Baum (BC / DIW) Limited Dependent Variables BBS 2013 1 / 47 Limited dependent

Chapter 4: Commonly Used Distributions. Statistics for Engineers and Scientists Fourth Edition William Navidi

Chapter 4: Commonly Used Distributions Statistics for Engineers and Scientists Fourth Edition William Navidi 2014 by Education. This is proprietary material solely for authorized instructor use. Not authorized

Chapter 4: Commonly Used Distributions Statistics for Engineers and Scientists Fourth Edition William Navidi 2014 by Education. This is proprietary material solely for authorized instructor use. Not authorized

Multiple Regression and Logistic Regression II. Dajiang 525 Apr

Multiple Regression and Logistic Regression II Dajiang Liu @PHS 525 Apr-19-2016 Materials from Last Time Multiple regression model: Include multiple predictors in the model = + + + + How to interpret the

Multiple Regression and Logistic Regression II Dajiang Liu @PHS 525 Apr-19-2016 Materials from Last Time Multiple regression model: Include multiple predictors in the model = + + + + How to interpret the

Some Characteristics of Data

Some Characteristics of Data Not all data is the same, and depending on some characteristics of a particular dataset, there are some limitations as to what can and cannot be done with that data. Some key

Some Characteristics of Data Not all data is the same, and depending on some characteristics of a particular dataset, there are some limitations as to what can and cannot be done with that data. Some key

Econometric Methods for Valuation Analysis

Econometric Methods for Valuation Analysis Margarita Genius Dept of Economics M. Genius (Univ. of Crete) Econometric Methods for Valuation Analysis Cagliari, 2017 1 / 25 Outline We will consider econometric

Econometric Methods for Valuation Analysis Margarita Genius Dept of Economics M. Genius (Univ. of Crete) Econometric Methods for Valuation Analysis Cagliari, 2017 1 / 25 Outline We will consider econometric

Module 9: Single-level and Multilevel Models for Ordinal Responses. Stata Practical 1

Module 9: Single-level and Multilevel Models for Ordinal Responses Pre-requisites Modules 5, 6 and 7 Stata Practical 1 George Leckie, Tim Morris & Fiona Steele Centre for Multilevel Modelling If you find

Module 9: Single-level and Multilevel Models for Ordinal Responses Pre-requisites Modules 5, 6 and 7 Stata Practical 1 George Leckie, Tim Morris & Fiona Steele Centre for Multilevel Modelling If you find

Lecture 34. Summarizing Data

Math 408 - Mathematical Statistics Lecture 34. Summarizing Data April 24, 2013 Konstantin Zuev (USC) Math 408, Lecture 34 April 24, 2013 1 / 15 Agenda Methods Based on the CDF The Empirical CDF Example:

Math 408 - Mathematical Statistics Lecture 34. Summarizing Data April 24, 2013 Konstantin Zuev (USC) Math 408, Lecture 34 April 24, 2013 1 / 15 Agenda Methods Based on the CDF The Empirical CDF Example:

Day 3C Simulation: Maximum Simulated Likelihood

Day 3C Simulation: Maximum Simulated Likelihood c A. Colin Cameron Univ. of Calif. - Davis... for Center of Labor Economics Norwegian School of Economics Advanced Microeconometrics Aug 28 - Sep 1, 2017

Day 3C Simulation: Maximum Simulated Likelihood c A. Colin Cameron Univ. of Calif. - Davis... for Center of Labor Economics Norwegian School of Economics Advanced Microeconometrics Aug 28 - Sep 1, 2017

Background. opportunities. the transformation. probability. at the lower. data come

The T Chart in Minitab Statisti cal Software Background The T chart is a control chart used to monitor the amount of time between adverse events, where time is measured on a continuous scale. The T chart

The T Chart in Minitab Statisti cal Software Background The T chart is a control chart used to monitor the amount of time between adverse events, where time is measured on a continuous scale. The T chart

The comparison of proportional hazards and accelerated failure time models in analyzing the first birth interval survival data

Journal of Physics: Conference Series PAPER OPEN ACCESS The comparison of proportional hazards and accelerated failure time models in analyzing the first birth interval survival data To cite this article:

Journal of Physics: Conference Series PAPER OPEN ACCESS The comparison of proportional hazards and accelerated failure time models in analyzing the first birth interval survival data To cite this article:

1. You are given the following information about a stationary AR(2) model:

model:") Fall 2003 Society of Actuaries **BEGINNING OF EXAMINATION** 1. You are given the following information about a stationary AR(2) model: (i) ρ 1 = 05. (ii) ρ 2 = 01. Determine φ 2. (A) 0.2 (B) 0.1 (C) 0.4

Fall 2003 Society of Actuaries **BEGINNING OF EXAMINATION** 1. You are given the following information about a stationary AR(2) model: (i) ρ 1 = 05. (ii) ρ 2 = 01. Determine φ 2. (A) 0.2 (B) 0.1 (C) 0.4

Modelling, Estimation and Hedging of Longevity Risk

IA BE Summer School 2016, K. Antonio, UvA 1 / 50 Modelling, Estimation and Hedging of Longevity Risk Katrien Antonio KU Leuven and University of Amsterdam IA BE Summer School 2016, Leuven Module II: Fitting

IA BE Summer School 2016, K. Antonio, UvA 1 / 50 Modelling, Estimation and Hedging of Longevity Risk Katrien Antonio KU Leuven and University of Amsterdam IA BE Summer School 2016, Leuven Module II: Fitting

Basic notions of probability theory: continuous probability distributions. Piero Baraldi

Basic notions of probability theory: continuous probability distributions Piero Baraldi Probability distributions for reliability, safety and risk analysis: discrete probability distributions continuous

Basic notions of probability theory: continuous probability distributions Piero Baraldi Probability distributions for reliability, safety and risk analysis: discrete probability distributions continuous

Jaime Frade Dr. Niu Interest rate modeling

Interest rate modeling Abstract In this paper, three models were used to forecast short term interest rates for the 3 month LIBOR. Each of the models, regression time series, GARCH, and Cox, Ingersoll,

Interest rate modeling Abstract In this paper, three models were used to forecast short term interest rates for the 3 month LIBOR. Each of the models, regression time series, GARCH, and Cox, Ingersoll,

CREDIT SCORING & CREDIT CONTROL XIV August 2015 Edinburgh. Aneta Ptak-Chmielewska Warsaw School of Ecoomics

CREDIT SCORING & CREDIT CONTROL XIV 26-28 August 2015 Edinburgh Aneta Ptak-Chmielewska Warsaw School of Ecoomics aptak@sgh.waw.pl 1 Background literature Hypothesis Data and methods Empirical example Conclusions

CREDIT SCORING & CREDIT CONTROL XIV 26-28 August 2015 Edinburgh Aneta Ptak-Chmielewska Warsaw School of Ecoomics aptak@sgh.waw.pl 1 Background literature Hypothesis Data and methods Empirical example Conclusions

The Multinomial Logit Model Revisited: A Semiparametric Approach in Discrete Choice Analysis

The Multinomial Logit Model Revisited: A Semiparametric Approach in Discrete Choice Analysis Dr. Baibing Li, Loughborough University Wednesday, 02 February 2011-16:00 Location: Room 610, Skempton (Civil

The Multinomial Logit Model Revisited: A Semiparametric Approach in Discrete Choice Analysis Dr. Baibing Li, Loughborough University Wednesday, 02 February 2011-16:00 Location: Room 610, Skempton (Civil

The Normal Distribution

The Normal Distribution The normal distribution plays a central role in probability theory and in statistics. It is often used as a model for the distribution of continuous random variables. Like all models,

The Normal Distribution The normal distribution plays a central role in probability theory and in statistics. It is often used as a model for the distribution of continuous random variables. Like all models,

ME3620. Theory of Engineering Experimentation. Spring Chapter III. Random Variables and Probability Distributions.

ME3620 Theory of Engineering Experimentation Chapter III. Random Variables and Probability Distributions Chapter III 1 3.2 Random Variables In an experiment, a measurement is usually denoted by a variable

ME3620 Theory of Engineering Experimentation Chapter III. Random Variables and Probability Distributions Chapter III 1 3.2 Random Variables In an experiment, a measurement is usually denoted by a variable

Financial Risk Management

Financial Risk Management Professor: Thierry Roncalli Evry University Assistant: Enareta Kurtbegu Evry University Tutorial exercices #4 1 Correlation and copulas 1. The bivariate Gaussian copula is given

Financial Risk Management Professor: Thierry Roncalli Evry University Assistant: Enareta Kurtbegu Evry University Tutorial exercices #4 1 Correlation and copulas 1. The bivariate Gaussian copula is given

Frequency Distribution Models 1- Probability Density Function (PDF)

") Models 1- Probability Density Function (PDF) What is a PDF model? A mathematical equation that describes the frequency curve or probability distribution of a data set. Why modeling? It represents and summarizes

Models 1- Probability Density Function (PDF) What is a PDF model? A mathematical equation that describes the frequency curve or probability distribution of a data set. Why modeling? It represents and summarizes

Loss Simulation Model Testing and Enhancement

Loss Simulation Model Testing and Enhancement Casualty Loss Reserve Seminar By Kailan Shang Sept. 2011 Agenda Research Overview Model Testing Real Data Model Enhancement Further Development Enterprise

Loss Simulation Model Testing and Enhancement Casualty Loss Reserve Seminar By Kailan Shang Sept. 2011 Agenda Research Overview Model Testing Real Data Model Enhancement Further Development Enterprise

Modelling component reliability using warranty data

ANZIAM J. 53 (EMAC2011) pp.c437 C450, 2012 C437 Modelling component reliability using warranty data Raymond Summit 1 (Received 10 January 2012; revised 10 July 2012) Abstract Accelerated testing is often

ANZIAM J. 53 (EMAC2011) pp.c437 C450, 2012 C437 Modelling component reliability using warranty data Raymond Summit 1 (Received 10 January 2012; revised 10 July 2012) Abstract Accelerated testing is often

Economics Multinomial Choice Models

Economics 217 - Multinomial Choice Models So far, most extensions of the linear model have centered on either a binary choice between two options (work or don t work) or censoring options. Many questions

Economics 217 - Multinomial Choice Models So far, most extensions of the linear model have centered on either a binary choice between two options (work or don t work) or censoring options. Many questions

A Comprehensive, Non-Aggregated, Stochastic Approach to. Loss Development

A Comprehensive, Non-Aggregated, Stochastic Approach to Loss Development By Uri Korn Abstract In this paper, we present a stochastic loss development approach that models all the core components of the

A Comprehensive, Non-Aggregated, Stochastic Approach to Loss Development By Uri Korn Abstract In this paper, we present a stochastic loss development approach that models all the core components of the

SOLUTION Fama Bliss and Risk Premiums in the Term Structure

SOLUTION Fama Bliss and Risk Premiums in the Term Structure Question (i EH Regression Results Holding period return year 3 year 4 year 5 year Intercept 0.0009 0.0011 0.0014 0.0015 (std err 0.003 0.0045

SOLUTION Fama Bliss and Risk Premiums in the Term Structure Question (i EH Regression Results Holding period return year 3 year 4 year 5 year Intercept 0.0009 0.0011 0.0014 0.0015 (std err 0.003 0.0045

Point Estimation. Some General Concepts of Point Estimation. Example. Estimator quality

Point Estimation Some General Concepts of Point Estimation Statistical inference = conclusions about parameters Parameters == population characteristics A point estimate of a parameter is a value (based

Point Estimation Some General Concepts of Point Estimation Statistical inference = conclusions about parameters Parameters == population characteristics A point estimate of a parameter is a value (based

Likelihood Methods of Inference. Toss coin 6 times and get Heads twice.

Methods of Inference Toss coin 6 times and get Heads twice. p is probability of getting H. Probability of getting exactly 2 heads is 15p 2 (1 p) 4 This function of p, is likelihood function. Definition:

Methods of Inference Toss coin 6 times and get Heads twice. p is probability of getting H. Probability of getting exactly 2 heads is 15p 2 (1 p) 4 This function of p, is likelihood function. Definition:

High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]

![High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]](/thumbs/79/79153367.jpg "High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]") 1 High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5] High-frequency data have some unique characteristics that do not appear in lower frequencies. At this class we have: Nonsynchronous

1 High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5] High-frequency data have some unique characteristics that do not appear in lower frequencies. At this class we have: Nonsynchronous

Unobserved Heterogeneity Revisited

Unobserved Heterogeneity Revisited Robert A. Miller Dynamic Discrete Choice March 2018 Miller (Dynamic Discrete Choice) cemmap 7 March 2018 1 / 24 Distributional Assumptions about the Unobserved Variables

Unobserved Heterogeneity Revisited Robert A. Miller Dynamic Discrete Choice March 2018 Miller (Dynamic Discrete Choice) cemmap 7 March 2018 1 / 24 Distributional Assumptions about the Unobserved Variables

Certified Quantitative Financial Modeling Professional VS-1243

Certified Quantitative Financial Modeling Professional VS-1243 Certified Quantitative Financial Modeling Professional Certification Code VS-1243 Vskills certification for Quantitative Financial Modeling

Certified Quantitative Financial Modeling Professional VS-1243 Certified Quantitative Financial Modeling Professional Certification Code VS-1243 Vskills certification for Quantitative Financial Modeling

Choice Probabilities. Logit Choice Probabilities Derivation. Choice Probabilities. Basic Econometrics in Transportation.

1/31 Choice Probabilities Basic Econometrics in Transportation Logit Models Amir Samimi Civil Engineering Department Sharif University of Technology Primary Source: Discrete Choice Methods with Simulation

1/31 Choice Probabilities Basic Econometrics in Transportation Logit Models Amir Samimi Civil Engineering Department Sharif University of Technology Primary Source: Discrete Choice Methods with Simulation

Pricing Dynamic Solvency Insurance and Investment Fund Protection

Pricing Dynamic Solvency Insurance and Investment Fund Protection Hans U. Gerber and Gérard Pafumi Switzerland Abstract In the first part of the paper the surplus of a company is modelled by a Wiener process.

Pricing Dynamic Solvency Insurance and Investment Fund Protection Hans U. Gerber and Gérard Pafumi Switzerland Abstract In the first part of the paper the surplus of a company is modelled by a Wiener process.

Building and Checking Survival Models

Building and Checking Survival Models David M. Rocke May 23, 2017 David M. Rocke Building and Checking Survival Models May 23, 2017 1 / 53 hodg Lymphoma Data Set from KMsurv This data set consists of information

Building and Checking Survival Models David M. Rocke May 23, 2017 David M. Rocke Building and Checking Survival Models May 23, 2017 1 / 53 hodg Lymphoma Data Set from KMsurv This data set consists of information

Using survival models for profit and loss estimation. Dr Tony Bellotti Lecturer in Statistics Department of Mathematics Imperial College London

Using survival models for profit and loss estimation Dr Tony Bellotti Lecturer in Statistics Department of Mathematics Imperial College London Credit Scoring and Credit Control XIII conference August 28-30,

Using survival models for profit and loss estimation Dr Tony Bellotti Lecturer in Statistics Department of Mathematics Imperial College London Credit Scoring and Credit Control XIII conference August 28-30,

WARRANTY SERVICING WITH A BROWN-PROSCHAN REPAIR OPTION

WARRANTY SERVICING WITH A BROWN-PROSCHAN REPAIR OPTION RUDRANI BANERJEE & MANISH C BHATTACHARJEE Center for Applied Mathematics & Statistics Department of Mathematical Sciences New Jersey Institute of

WARRANTY SERVICING WITH A BROWN-PROSCHAN REPAIR OPTION RUDRANI BANERJEE & MANISH C BHATTACHARJEE Center for Applied Mathematics & Statistics Department of Mathematical Sciences New Jersey Institute of

INDIAN INSTITUTE OF SCIENCE STOCHASTIC HYDROLOGY. Lecture -26 Course Instructor : Prof. P. P. MUJUMDAR Department of Civil Engg., IISc.

INDIAN INSTITUTE OF SCIENCE STOCHASTIC HYDROLOGY Lecture -26 Course Instructor : Prof. P. P. MUJUMDAR Department of Civil Engg., IISc. Summary of the previous lecture Hydrologic data series for frequency

INDIAN INSTITUTE OF SCIENCE STOCHASTIC HYDROLOGY Lecture -26 Course Instructor : Prof. P. P. MUJUMDAR Department of Civil Engg., IISc. Summary of the previous lecture Hydrologic data series for frequency

IEOR E4602: Quantitative Risk Management

IEOR E4602: Quantitative Risk Management Basic Concepts and Techniques of Risk Management Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

IEOR E4602: Quantitative Risk Management Basic Concepts and Techniques of Risk Management Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

9. Logit and Probit Models For Dichotomous Data

Sociology 740 John Fox Lecture Notes 9. Logit and Probit Models For Dichotomous Data Copyright 2014 by John Fox Logit and Probit Models for Dichotomous Responses 1 1. Goals: I To show how models similar

Sociology 740 John Fox Lecture Notes 9. Logit and Probit Models For Dichotomous Data Copyright 2014 by John Fox Logit and Probit Models for Dichotomous Responses 1 1. Goals: I To show how models similar

Duangporn Jearkpaporn, Connie M. Borror Douglas C. Montgomery and George C. Runger Arizona State University Tempe, AZ

Process Monitoring for Correlated Gamma Distributed Data Using Generalized Linear Model Based Control Charts Duangporn Jearkpaporn, Connie M. Borror Douglas C. Montgomery and George C. Runger Arizona State

Process Monitoring for Correlated Gamma Distributed Data Using Generalized Linear Model Based Control Charts Duangporn Jearkpaporn, Connie M. Borror Douglas C. Montgomery and George C. Runger Arizona State

A potentially useful approach to model nonlinearities in time series is to assume different behavior (structural break) in different subsamples

in different subsamples") 1.3 Regime switching models A potentially useful approach to model nonlinearities in time series is to assume different behavior (structural break) in different subsamples (or regimes). If the dates, the

1.3 Regime switching models A potentially useful approach to model nonlinearities in time series is to assume different behavior (structural break) in different subsamples (or regimes). If the dates, the

6. Genetics examples: Hardy-Weinberg Equilibrium

PBCB 206 (Fall 2006) Instructor: Fei Zou email: fzou@bios.unc.edu office: 3107D McGavran-Greenberg Hall Lecture 4 Topics for Lecture 4 1. Parametric models and estimating parameters from data 2. Method

PBCB 206 (Fall 2006) Instructor: Fei Zou email: fzou@bios.unc.edu office: 3107D McGavran-Greenberg Hall Lecture 4 Topics for Lecture 4 1. Parametric models and estimating parameters from data 2. Method

Final Exam - section 1. Thursday, December hours, 30 minutes

Econometrics, ECON312 San Francisco State University Michael Bar Fall 2013 Final Exam - section 1 Thursday, December 19 1 hours, 30 minutes Name: Instructions 1. This is closed book, closed notes exam.

Econometrics, ECON312 San Francisco State University Michael Bar Fall 2013 Final Exam - section 1 Thursday, December 19 1 hours, 30 minutes Name: Instructions 1. This is closed book, closed notes exam.

INTRODUCTION TO SURVIVAL ANALYSIS IN BUSINESS

INTRODUCTION TO SURVIVAL ANALYSIS IN BUSINESS By Jeff Morrison Survival model provides not only the probability of a certain event to occur but also when it will occur... survival probability can alert

INTRODUCTION TO SURVIVAL ANALYSIS IN BUSINESS By Jeff Morrison Survival model provides not only the probability of a certain event to occur but also when it will occur... survival probability can alert

Pakes (1986): Patents as Options: Some Estimates of the Value of Holding European Patent Stocks

: Patents as Options: Some Estimates of the Value of Holding European Patent Stocks") Pakes (1986): Patents as Options: Some Estimates of the Value of Holding European Patent Stocks Spring 2009 Main question: How much are patents worth? Answering this question is important, because it helps

Pakes (1986): Patents as Options: Some Estimates of the Value of Holding European Patent Stocks Spring 2009 Main question: How much are patents worth? Answering this question is important, because it helps

Quantile Regression. By Luyang Fu, Ph. D., FCAS, State Auto Insurance Company Cheng-sheng Peter Wu, FCAS, ASA, MAAA, Deloitte Consulting

Quantile Regression By Luyang Fu, Ph. D., FCAS, State Auto Insurance Company Cheng-sheng Peter Wu, FCAS, ASA, MAAA, Deloitte Consulting Agenda Overview of Predictive Modeling for P&C Applications Quantile

Quantile Regression By Luyang Fu, Ph. D., FCAS, State Auto Insurance Company Cheng-sheng Peter Wu, FCAS, ASA, MAAA, Deloitte Consulting Agenda Overview of Predictive Modeling for P&C Applications Quantile

Amath 546/Econ 589 Univariate GARCH Models

Amath 546/Econ 589 Univariate GARCH Models Eric Zivot April 24, 2013 Lecture Outline Conditional vs. Unconditional Risk Measures Empirical regularities of asset returns Engle s ARCH model Testing for ARCH

Amath 546/Econ 589 Univariate GARCH Models Eric Zivot April 24, 2013 Lecture Outline Conditional vs. Unconditional Risk Measures Empirical regularities of asset returns Engle s ARCH model Testing for ARCH

SYSM 6304 Risk and Decision Analysis Lecture 2: Fitting Distributions to Data

SYSM 6304 Risk and Decision Analysis Lecture 2: Fitting Distributions to Data M. Vidyasagar Cecil & Ida Green Chair The University of Texas at Dallas Email: M.Vidyasagar@utdallas.edu September 5, 2015

SYSM 6304 Risk and Decision Analysis Lecture 2: Fitting Distributions to Data M. Vidyasagar Cecil & Ida Green Chair The University of Texas at Dallas Email: M.Vidyasagar@utdallas.edu September 5, 2015

CS 361: Probability & Statistics

March 12, 2018 CS 361: Probability & Statistics Inference Binomial likelihood: Example Suppose we have a coin with an unknown probability of heads. We flip the coin 10 times and observe 2 heads. What can

March 12, 2018 CS 361: Probability & Statistics Inference Binomial likelihood: Example Suppose we have a coin with an unknown probability of heads. We flip the coin 10 times and observe 2 heads. What can

Back to estimators...

Back to estimators... So far, we have: Identified estimators for common parameters Discussed the sampling distributions of estimators Introduced ways to judge the goodness of an estimator (bias, MSE, etc.)

Back to estimators... So far, we have: Identified estimators for common parameters Discussed the sampling distributions of estimators Introduced ways to judge the goodness of an estimator (bias, MSE, etc.)

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay. Solutions to Final Exam.

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

Generalized MLE per Martins and Stedinger

Generalized MLE per Martins and Stedinger Martins ES and Stedinger JR. (March 2000). Generalized maximum-likelihood generalized extreme-value quantile estimators for hydrologic data. Water Resources Research

Generalized MLE per Martins and Stedinger Martins ES and Stedinger JR. (March 2000). Generalized maximum-likelihood generalized extreme-value quantile estimators for hydrologic data. Water Resources Research

Statistics & Flood Frequency Chapter 3. Dr. Philip B. Bedient

Statistics & Flood Frequency Chapter 3 Dr. Philip B. Bedient Predicting FLOODS Flood Frequency Analysis n Statistical Methods to evaluate probability exceeding a particular outcome - P (X >20,000 cfs)

Statistics & Flood Frequency Chapter 3 Dr. Philip B. Bedient Predicting FLOODS Flood Frequency Analysis n Statistical Methods to evaluate probability exceeding a particular outcome - P (X >20,000 cfs)

UNU MERIT Working Paper Series

UNU MERIT Working Paper Series #2013-039 How unemployment insurance savings accounts affect employment duration: Evidence from Chile Paula Nagler Maastricht Economic and social Research institute on Innovation

UNU MERIT Working Paper Series #2013-039 How unemployment insurance savings accounts affect employment duration: Evidence from Chile Paula Nagler Maastricht Economic and social Research institute on Innovation

The Two-Sample Independent Sample t Test

Department of Psychology and Human Development Vanderbilt University 1 Introduction 2 3 The General Formula The Equal-n Formula 4 5 6 Independence Normality Homogeneity of Variances 7 Non-Normality Unequal

Department of Psychology and Human Development Vanderbilt University 1 Introduction 2 3 The General Formula The Equal-n Formula 4 5 6 Independence Normality Homogeneity of Variances 7 Non-Normality Unequal

A Saddlepoint Approximation to Left-Tailed Hypothesis Tests of Variance for Non-normal Populations

UNF Digital Commons UNF Theses and Dissertations Student Scholarship 2016 A Saddlepoint Approximation to Left-Tailed Hypothesis Tests of Variance for Non-normal Populations Tyler L. Grimes University of

UNF Digital Commons UNF Theses and Dissertations Student Scholarship 2016 A Saddlepoint Approximation to Left-Tailed Hypothesis Tests of Variance for Non-normal Populations Tyler L. Grimes University of

Multivariate Cox PH model with log-skew-normal frailties

Multivariate Cox PH model with log-skew-normal frailties Department of Statistical Sciences, University of Padua, 35121 Padua (IT) Multivariate Cox PH model A standard statistical approach to model clustered

Multivariate Cox PH model with log-skew-normal frailties Department of Statistical Sciences, University of Padua, 35121 Padua (IT) Multivariate Cox PH model A standard statistical approach to model clustered

A Comprehensive, Non-Aggregated, Stochastic Approach to Loss Development

A Comprehensive, Non-Aggregated, Stochastic Approach to Loss Development by Uri Korn ABSTRACT In this paper, we present a stochastic loss development approach that models all the core components of the

A Comprehensive, Non-Aggregated, Stochastic Approach to Loss Development by Uri Korn ABSTRACT In this paper, we present a stochastic loss development approach that models all the core components of the

Maximum Likelihood Estimation

Maximum Likelihood Estimation The likelihood and log-likelihood functions are the basis for deriving estimators for parameters, given data. While the shapes of these two functions are different, they have

Maximum Likelihood Estimation The likelihood and log-likelihood functions are the basis for deriving estimators for parameters, given data. While the shapes of these two functions are different, they have