Things You Have To Have Heard About (In Double-Quick Time) The LIBOR market model: Björk 27. Swaption pricing too.

|

|

|

- Dale Bartholomew Fleming

- 5 years ago

- Views:

Transcription

1 Things You Have To Have Heard About (In Double-Quick Time) LIBORs, floating rate bonds, swaps.: Björk 22.3 Caps: Björk Fun with caps. The LIBOR market model: Björk 27. Swaption pricing too. 1

2 Simple forward rates; LIBOR A simple forward rate L(t;S,T) specifies the cash-flow for a loan agreement where The agreement is made at time t At time S the borrower receives $1 (or Euro, or DKK, or...) At time T the borrower pays back 1+(T S)L(t;S,T) 2

3 Note that this rate is quoted on a discretely compounded basis. If L(0;1,1.25) = 0.04 then you have to pay back 1.01; if the 0.04 were taken as continuously compounded you d have to pay back exp( ) = The usual simple no-arbitrage argument (DIY) shows that 1+(T S)L(t;S,T) = P(t,S) P(t,T) L(t;S,T) = 1 T S ( P(t,S) P(t,T) 1 ). Such simple rates are called LIBOR. Historical reasons for the acronym. (London Interbank Offer Rate.) The pleonasm LIBOR rate is hard to avoid!. They are widely used. 3

4 With T = S +δ we may write L δ (t;t) is called (δ-) spot LIBOR. L δ (t;s), Immediate (Technical) Observation L δ (t;t) is a Q T+δ martingale. 4

5 Floating rate bonds & Swaps Look at a tenor-structure; a set of dates where something interesting happens δ t T 0 T 1 = T 0 +δ T i = T i 1 +δ T N = T 0 +Nδ A floating rate bullet bond has the cash-flows δl δ (T i 1 ;T i 1 ) }{{} :=c i at T i for i N 1, and 1+δL δ (T N 1 ;T N 1 ) at date T N. The cash-flows are stochastic so finding the arbitrage-free price seems to require a dynamic model. 5

6 It doesn t. We have c i = 1 P(T i 1,T i ) 1 for i N 1 and the time-t value of the -1 is of course P(t,T i ). Now consider the following trading strategy: time t: Buy 1 T i 1 -ZCB (price: P(t,T i 1 )) time T i 1 : Invest the $1 received in T i -ZCB. You ll get 1/P(T i 1,T i ) units & a net-cash-flow of 0. 6

7 time T i : Sit back and receive $ 1/P(T i 1,T i ) from the T i -ZCB. At a cost of P(t,T i 1 ), this perfectly replicates the 1/P(T i 1,T i )-cashflow from the floating rate bullet. Hence the arbitrage-free price of cash-flow c i is P(t,T i 1 ) P(t,T i ). The arbitrage-free price of the floating rate bullet is FlBull(t) = N 1 i=1 (P(t,T i 1 ) P(t,T i ))+P(T N 1 ) = P(t;T 0 ), as the sum telescopes. In particular, if t = T 0 ( vi står på en terminsdato ) then the floating rate bullet has value 1.The floating rate bond has par value. 7

8 Note that this result is easily extended to any type of floating rate bond (eg. serial or annuity) with deterministic instalment plan. If H(T i ) denotes remaining principal and A(T i ) is the principal repaid at time T i then H(T i 1 ) = The T i -cash-flow from the bond is N j=i A(T j ). c i = A(T i )+δl δ (T i 1 ;T i 1 )H(T i 1 ) = A(T i )+δl δ (T i 1 ;T i 1 ) N j=i A(T j ). A portfolio with A(T i ) units of the T i -bullet has exactly the same cash-flows, and its price (assuming t = T 0 ) is ia(t i ) = H(0). So the new bond has par value too. 8

9 A plain vanilla interest rate swap is contract that consists of A long position in a floating rate bullet (or however many M you want as notional principal) A short position in a fixed rate bullet (say with fixed rate κ). You can think of this as contract that swaps floating rate interest payments for fixed rate payments (or vice versa). The value of the swap contract is Vswap(t) = P(t,T 0 ) P(t;T N ) N i=1 δκp(t;t i ) 9

10 In practice this equation is used backwards (at the time of initiation of the swap) to set the fixed rate such that Vswap(t) = 0, ie. κ (t) = P(t,T 0) P(t;T N ) Ni=1. δp(t;t i ) This is called the (par) swap rate. Note that it is specific to the swap considered; you get different swap rates if you move T 0, δ or N around. The message is then: floating rate bonds trade at par swaps can be valued without a dynamic model (there s no volatility dependence) 10

11 A couple of disclaimers/warnings: It is very important for the volatility independence that you swap the exact right rate at the exact right time. Swapping the 6M LIBOR every 3rd month induces volatility dependence. So does moving payments to where they are first known. So-called convexity adjustments try to remedy that. Swaps can be made a lot more exotic with all kinds of embedded option features & strange floating rates. Famous disaster: Proctor and Gamble vs. (literally) Bankers Trust. (Arguably, the problem here was not really the complexity, but the fact that P&G took a huge gamble on rates staying low.) 11

12 Option structures & LIBOR market models A caplet contract pays off δ(l δ (T i 1,T i 1 ) ω) + at time T i Owning a caplet can be thought of as having an insurance against paying high interest. (A small calculation shows that) 1 caplet can be seen as (1 + δω) expiry-t i 1 strike-1/(1+δω) put-options with the T i -ZCB as underlying. So we can price them in a Vasicek or multidimensional Gaussian model. But there s another way. 12

13 The time-t arbitrage-free price of a caplet is ( (Lδ (T i 1,T i 1 ) ω) + π caplet (t) = δβ(t)e Q t β(t i ) = δp(t,t i )E T i t ((L δ(t i 1,T i 1 ) ω) + ) ) Recall that L δ (;T i 1 ) is a Q T i martingale. 13

14 So one way to to specify an arbitrage-free model is as dl δ (t;t i 1 ) = γ (t;t i 1 )L δ (t;t i 1 )dw T i(t) (1) for some deterministic (possible vector-valued) function γ. This is called the (lognormal) LIBOR market model. Put v 2 (t,t) = T t γ(u;t) 2 du. Then a standard B/S-like calculation (DIY) shows that π caplet (t;t i 1,δ,κ) = δp(t,t i ) ( L δ (t;t i 1 )Φ ( ) d + κφ(d )), where d ± = (ln(l δ (t;t i 1 )/κ)± 2 1 v2 (t,t i 1 ))/v(t,t i 1 ). 14

15 If γ is 1D & constant (in 1st argument) then v 2 = γ 2 (T i 1 )T i 1 and the formula is the so-called Black s formula. Other assumption: γ(t, T) = γ(t t) where γ is piecewise constant. More natural. Not clear what a reasonable volatility specification is. A cap contract is a series of caplets; its price is simply the sum of caplet prices. Market practice is & has been for may years to price or at least quote caps with this so-called Black-76 formula. Here is a formal, arbitrage-free model that supports this. 15

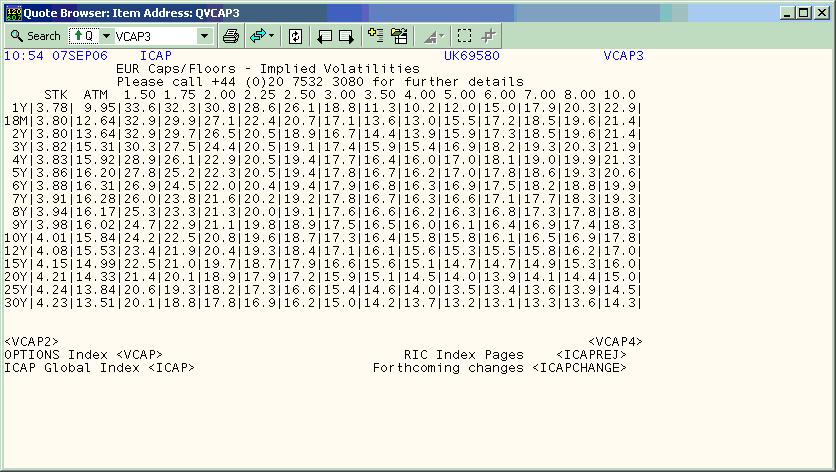

16 16

17 Logically, a picture like this non-constant implied volatilities across expiry and in particular strike/moneyness tells you that the lognormal LIBOR model is not consistent with observed cap-prices! A Vasicek model can capture a skew (vol decreasing with strike) but not a smile (vol low strike, high strike - stochastic volatility model?), in particular a steep short expiries (jumps?), and not the term structure of ATM-vols (increasing in expiry - risk-premia?) And then the smaller matter that the vol-surface moves around from day to day. 17

18 Papers with the model by [Miltersen, Sandmann, Sondermann], [Brace, Gatarek, Musiela] and [Jamshidian] appeared virtually simultaneously in Immediate hit. Understandably so. Justifies what was being done & takes as input real observables. And you can reuse everything from stock option models. Quoting prices in terms of Black-volatility does not actually mean that you belive in the lognormal model. Cap prices are quoted as flat volatility, ie. the same constant γ that when plugged into caplets & summed gives the price. 18

19 The models are actually more complicated than they look: Strange bond price dynamics σ P (t,t) = (T t)/δ k=1 δl δ (t,t δk) γ(t,t δk). 1+δL δ (t,t δk) Not a Markovian structure. So simulation requires a lot of bookkeeping. Lognormality is not preserved on measure changes. And if 3M LIBOR has lognormal volatility structure, then 6M LIBOR hasn t. 19

20 Hard to price anything that is not a cap. Requires considerable concentration to keep track of all necessary time-indices & integrations. There is an extensive literature on market models. Nice recent articles by Pelsser, Driessen, dejong. 20

21 Another option-type contract is the swaption today swaption expiry, i.e. decide whether or not to enter fixed rate ω swap 1st swap swap starts cashflow swap ends, i.e. last cashflow date t T l T m T m+1 = T m +δ T n The time-t l value of the swaption (i.e. the swaption price at its expiry date) is π swopt (T l ;T l,t m,t n,δ,ω) = δ(κ(t l ;T m,t n,δ) ω) + n j=m+1 P(T l,t j ). 21

22 So for t < T l, the swaption price can be written as π swopt (t;...) = P(t;T l )E QT l t δ(κ(t l ;T m,t n,δ) ω) + n j=m+1 P(T l,t j ). If T l = T m then that we can rewrite the swaption pay-off as 1 n j=m+1 α j P(T m,t j ) + with α j = δω for j n 1 & α n = 1 + δω. So the swaption is really a put option on a coupon-bearing bond. The ideas from earlier in the day was used by BGM to derive an approximate swaption-price formula in a lognormal LIBOR market model., 22

23 Put X(t) = δ n j=m+1 P(t;T j ). This a perfectly legitimate choice of numeraire, so it induces an equivalent martingale measure Q X. Then π swopt (t;t l,t m,t n,δ,ω) = X(t)E QX t ( (κ(tl ;T m,t n,δ) ω) +). and the process {κ(t;t m,t n,δ)} t is a Q X -martingale. This, known as the swap-measure approach, can lead to Black-type formulas for swaptions. A few calculations show that lognormal volatility of swap-rates is not consistent with lognormal LIBOR volatility. 23

Libor Market Model Version 1.0

Libor Market Model Version.0 Introduction This plug-in implements the Libor Market Model (also know as BGM Model, from the authors Brace Gatarek Musiela). For a general reference on this model see [, [2

Libor Market Model Version.0 Introduction This plug-in implements the Libor Market Model (also know as BGM Model, from the authors Brace Gatarek Musiela). For a general reference on this model see [, [2

Market interest-rate models

Market interest-rate models Marco Marchioro www.marchioro.org November 24 th, 2012 Market interest-rate models 1 Lecture Summary No-arbitrage models Detailed example: Hull-White Monte Carlo simulations

Market interest-rate models Marco Marchioro www.marchioro.org November 24 th, 2012 Market interest-rate models 1 Lecture Summary No-arbitrage models Detailed example: Hull-White Monte Carlo simulations

Inflation-indexed Swaps and Swaptions

Inflation-indexed Swaps and Swaptions Mia Hinnerich Aarhus University, Denmark Vienna University of Technology, April 2009 M. Hinnerich (Aarhus University) Inflation-indexed Swaps and Swaptions April 2009

Inflation-indexed Swaps and Swaptions Mia Hinnerich Aarhus University, Denmark Vienna University of Technology, April 2009 M. Hinnerich (Aarhus University) Inflation-indexed Swaps and Swaptions April 2009

L 2 -theoretical study of the relation between the LIBOR market model and the HJM model Takashi Yasuoka

Journal of Math-for-Industry, Vol. 5 (213A-2), pp. 11 16 L 2 -theoretical study of the relation between the LIBOR market model and the HJM model Takashi Yasuoka Received on November 2, 212 / Revised on

Journal of Math-for-Industry, Vol. 5 (213A-2), pp. 11 16 L 2 -theoretical study of the relation between the LIBOR market model and the HJM model Takashi Yasuoka Received on November 2, 212 / Revised on

Lecture on Interest Rates

Lecture on Interest Rates Josef Teichmann ETH Zürich Zürich, December 2012 Josef Teichmann Lecture on Interest Rates Mathematical Finance Examples and Remarks Interest Rate Models 1 / 53 Goals Basic concepts

Lecture on Interest Rates Josef Teichmann ETH Zürich Zürich, December 2012 Josef Teichmann Lecture on Interest Rates Mathematical Finance Examples and Remarks Interest Rate Models 1 / 53 Goals Basic concepts

Martingale Methods in Financial Modelling

Marek Musiela Marek Rutkowski Martingale Methods in Financial Modelling Second Edition \ 42 Springer - . Preface to the First Edition... V Preface to the Second Edition... VII I Part I. Spot and Futures

Marek Musiela Marek Rutkowski Martingale Methods in Financial Modelling Second Edition \ 42 Springer - . Preface to the First Edition... V Preface to the Second Edition... VII I Part I. Spot and Futures

Martingale Methods in Financial Modelling

Marek Musiela Marek Rutkowski Martingale Methods in Financial Modelling Second Edition Springer Table of Contents Preface to the First Edition Preface to the Second Edition V VII Part I. Spot and Futures

Marek Musiela Marek Rutkowski Martingale Methods in Financial Modelling Second Edition Springer Table of Contents Preface to the First Edition Preface to the Second Edition V VII Part I. Spot and Futures

Valuation of Caps and Swaptions under a Stochastic String Model

Valuation of Caps and Swaptions under a Stochastic String Model June 1, 2013 Abstract We develop a Gaussian stochastic string model that provides closed-form expressions for the prices of caps and swaptions

Valuation of Caps and Swaptions under a Stochastic String Model June 1, 2013 Abstract We develop a Gaussian stochastic string model that provides closed-form expressions for the prices of caps and swaptions

A Hybrid Commodity and Interest Rate Market Model

A Hybrid Commodity and Interest Rate Market Model University of Technology, Sydney June 1 Literature A Hybrid Market Model Recall: The basic LIBOR Market Model The cross currency LIBOR Market Model LIBOR

A Hybrid Commodity and Interest Rate Market Model University of Technology, Sydney June 1 Literature A Hybrid Market Model Recall: The basic LIBOR Market Model The cross currency LIBOR Market Model LIBOR

Introduction. Practitioner Course: Interest Rate Models. John Dodson. February 18, 2009

Practitioner Course: Interest Rate Models February 18, 2009 syllabus text sessions office hours date subject reading 18 Feb introduction BM 1 25 Feb affine models BM 3 4 Mar Gaussian models BM 4 11 Mar

Practitioner Course: Interest Rate Models February 18, 2009 syllabus text sessions office hours date subject reading 18 Feb introduction BM 1 25 Feb affine models BM 3 4 Mar Gaussian models BM 4 11 Mar

LIBOR models, multi-curve extensions, and the pricing of callable structured derivatives

Weierstrass Institute for Applied Analysis and Stochastics LIBOR models, multi-curve extensions, and the pricing of callable structured derivatives John Schoenmakers 9th Summer School in Mathematical Finance

Weierstrass Institute for Applied Analysis and Stochastics LIBOR models, multi-curve extensions, and the pricing of callable structured derivatives John Schoenmakers 9th Summer School in Mathematical Finance

Term Structure Lattice Models

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh Term Structure Lattice Models These lecture notes introduce fixed income derivative securities and the modeling philosophy used to

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh Term Structure Lattice Models These lecture notes introduce fixed income derivative securities and the modeling philosophy used to

The Black Model and the Pricing of Options on Assets, Futures and Interest Rates. Richard Stapleton, Guenter Franke

The Black Model and the Pricing of Options on Assets, Futures and Interest Rates Richard Stapleton, Guenter Franke September 23, 2005 Abstract The Black Model and the Pricing of Options We establish a

The Black Model and the Pricing of Options on Assets, Futures and Interest Rates Richard Stapleton, Guenter Franke September 23, 2005 Abstract The Black Model and the Pricing of Options We establish a

Pricing of a European Call Option Under a Local Volatility Interbank Offered Rate Model

American Journal of Theoretical and Applied Statistics 2018; 7(2): 80-84 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20180702.14 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

American Journal of Theoretical and Applied Statistics 2018; 7(2): 80-84 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20180702.14 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

Multi-Curve Pricing of Non-Standard Tenor Vanilla Options in QuantLib. Sebastian Schlenkrich QuantLib User Meeting, Düsseldorf, December 1, 2015

Multi-Curve Pricing of Non-Standard Tenor Vanilla Options in QuantLib Sebastian Schlenkrich QuantLib User Meeting, Düsseldorf, December 1, 2015 d-fine d-fine All rights All rights reserved reserved 0 Swaption

Multi-Curve Pricing of Non-Standard Tenor Vanilla Options in QuantLib Sebastian Schlenkrich QuantLib User Meeting, Düsseldorf, December 1, 2015 d-fine d-fine All rights All rights reserved reserved 0 Swaption

CONSISTENCY AMONG TRADING DESKS

CONSISTENCY AMONG TRADING DESKS David Heath 1 and Hyejin Ku 2 1 Department of Mathematical Sciences, Carnegie Mellon University, Pittsburgh, PA, USA, email:heath@andrew.cmu.edu 2 Department of Mathematics

CONSISTENCY AMONG TRADING DESKS David Heath 1 and Hyejin Ku 2 1 Department of Mathematical Sciences, Carnegie Mellon University, Pittsburgh, PA, USA, email:heath@andrew.cmu.edu 2 Department of Mathematics

LOGNORMAL MIXTURE SMILE CONSISTENT OPTION PRICING

LOGNORMAL MIXTURE SMILE CONSISTENT OPTION PRICING FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it Daiwa International Workshop on Financial Engineering, Tokyo, 26-27 August 2004 1 Stylized

LOGNORMAL MIXTURE SMILE CONSISTENT OPTION PRICING FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it Daiwa International Workshop on Financial Engineering, Tokyo, 26-27 August 2004 1 Stylized

Lecture 5: Review of interest rate models

Lecture 5: Review of interest rate models Xiaoguang Wang STAT 598W January 30th, 2014 (STAT 598W) Lecture 5 1 / 46 Outline 1 Bonds and Interest Rates 2 Short Rate Models 3 Forward Rate Models 4 LIBOR and

Lecture 5: Review of interest rate models Xiaoguang Wang STAT 598W January 30th, 2014 (STAT 598W) Lecture 5 1 / 46 Outline 1 Bonds and Interest Rates 2 Short Rate Models 3 Forward Rate Models 4 LIBOR and

INTEREST RATES AND FX MODELS

INTEREST RATES AND FX MODELS 4. Convexity Andrew Lesniewski Courant Institute of Mathematics New York University New York February 24, 2011 2 Interest Rates & FX Models Contents 1 Convexity corrections

INTEREST RATES AND FX MODELS 4. Convexity Andrew Lesniewski Courant Institute of Mathematics New York University New York February 24, 2011 2 Interest Rates & FX Models Contents 1 Convexity corrections

Introduction to Financial Mathematics

Department of Mathematics University of Michigan November 7, 2008 My Information E-mail address: marymorj (at) umich.edu Financial work experience includes 2 years in public finance investment banking

Department of Mathematics University of Michigan November 7, 2008 My Information E-mail address: marymorj (at) umich.edu Financial work experience includes 2 years in public finance investment banking

Fixed-Income Analysis. Assignment 7

FIN 684 Professor Robert B.H. Hauswald Fixed-Income Analysis Kogod School of Business, AU Assignment 7 Please be reminded that you are expected to use contemporary computer software to solve the following

FIN 684 Professor Robert B.H. Hauswald Fixed-Income Analysis Kogod School of Business, AU Assignment 7 Please be reminded that you are expected to use contemporary computer software to solve the following

A Brief Review of Derivatives Pricing & Hedging

IEOR E4602: Quantitative Risk Management Spring 2016 c 2016 by Martin Haugh A Brief Review of Derivatives Pricing & Hedging In these notes we briefly describe the martingale approach to the pricing of

IEOR E4602: Quantitative Risk Management Spring 2016 c 2016 by Martin Haugh A Brief Review of Derivatives Pricing & Hedging In these notes we briefly describe the martingale approach to the pricing of

1 Interest Based Instruments

1 Interest Based Instruments e.g., Bonds, forward rate agreements (FRA), and swaps. Note that the higher the credit risk, the higher the interest rate. Zero Rates: n year zero rate (or simply n-year zero)

1 Interest Based Instruments e.g., Bonds, forward rate agreements (FRA), and swaps. Note that the higher the credit risk, the higher the interest rate. Zero Rates: n year zero rate (or simply n-year zero)

Forwards, Futures, Options and Swaps

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Forward Risk Adjusted Probability Measures and Fixed-income Derivatives

Lecture 9 Forward Risk Adjusted Probability Measures and Fixed-income Derivatives 9.1 Forward risk adjusted probability measures This section is a preparation for valuation of fixed-income derivatives.

Lecture 9 Forward Risk Adjusted Probability Measures and Fixed-income Derivatives 9.1 Forward risk adjusted probability measures This section is a preparation for valuation of fixed-income derivatives.

The Pricing of Bermudan Swaptions by Simulation

The Pricing of Bermudan Swaptions by Simulation Claus Madsen to be Presented at the Annual Research Conference in Financial Risk - Budapest 12-14 of July 2001 1 A Bermudan Swaption (BS) A Bermudan Swaption

The Pricing of Bermudan Swaptions by Simulation Claus Madsen to be Presented at the Annual Research Conference in Financial Risk - Budapest 12-14 of July 2001 1 A Bermudan Swaption (BS) A Bermudan Swaption

1.1 Implied probability of default and credit yield curves

Risk Management Topic One Credit yield curves and credit derivatives 1.1 Implied probability of default and credit yield curves 1.2 Credit default swaps 1.3 Credit spread and bond price based pricing 1.4

Risk Management Topic One Credit yield curves and credit derivatives 1.1 Implied probability of default and credit yield curves 1.2 Credit default swaps 1.3 Credit spread and bond price based pricing 1.4

Rho and Delta. Paul Hollingsworth January 29, Introduction 1. 2 Zero coupon bond 1. 3 FX forward 2. 5 Rho (ρ) 4. 7 Time bucketing 6

4. 7 Time bucketing 6") Rho and Delta Paul Hollingsworth January 29, 2012 Contents 1 Introduction 1 2 Zero coupon bond 1 3 FX forward 2 4 European Call under Black Scholes 3 5 Rho (ρ) 4 6 Relationship between Rho and Delta 5

Rho and Delta Paul Hollingsworth January 29, 2012 Contents 1 Introduction 1 2 Zero coupon bond 1 3 FX forward 2 4 European Call under Black Scholes 3 5 Rho (ρ) 4 6 Relationship between Rho and Delta 5

Managing the Newest Derivatives Risks

Managing the Newest Derivatives Risks Michel Crouhy IXIS Corporate and Investment Bank / A subsidiary of NATIXIS Derivatives 2007: New Ideas, New Instruments, New markets NYU Stern School of Business,

Managing the Newest Derivatives Risks Michel Crouhy IXIS Corporate and Investment Bank / A subsidiary of NATIXIS Derivatives 2007: New Ideas, New Instruments, New markets NYU Stern School of Business,

Hedging Credit Derivatives in Intensity Based Models

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

The LIBOR Market Model and the volatility smile

University of South Africa The LIBOR Market Model and the volatility smile Author: Michael Tavares Supervisor: Professor. B Swart Abstract The LIBOR Market Model (LLM) is a popular term structure interest

University of South Africa The LIBOR Market Model and the volatility smile Author: Michael Tavares Supervisor: Professor. B Swart Abstract The LIBOR Market Model (LLM) is a popular term structure interest

Callable Libor exotic products. Ismail Laachir. March 1, 2012

5 pages 1 Callable Libor exotic products Ismail Laachir March 1, 2012 Contents 1 Callable Libor exotics 1 1.1 Bermudan swaption.............................. 2 1.2 Callable capped floater............................

5 pages 1 Callable Libor exotic products Ismail Laachir March 1, 2012 Contents 1 Callable Libor exotics 1 1.1 Bermudan swaption.............................. 2 1.2 Callable capped floater............................

Vanilla interest rate options

Vanilla interest rate options Marco Marchioro derivati2@marchioro.org October 26, 2011 Vanilla interest rate options 1 Summary Probability evolution at information arrival Brownian motion and option pricing

Vanilla interest rate options Marco Marchioro derivati2@marchioro.org October 26, 2011 Vanilla interest rate options 1 Summary Probability evolution at information arrival Brownian motion and option pricing

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

Financial Engineering with FRONT ARENA

Introduction The course A typical lecture Concluding remarks Problems and solutions Dmitrii Silvestrov Anatoliy Malyarenko Department of Mathematics and Physics Mälardalen University December 10, 2004/Front

Introduction The course A typical lecture Concluding remarks Problems and solutions Dmitrii Silvestrov Anatoliy Malyarenko Department of Mathematics and Physics Mälardalen University December 10, 2004/Front

A new approach to multiple curve Market Models of Interest Rates. Rodney Hoskinson

A new approach to multiple curve Market Models of Interest Rates Rodney Hoskinson Rodney Hoskinson This presentation has been prepared for the Actuaries Institute 2014 Financial Services Forum. The Institute

A new approach to multiple curve Market Models of Interest Rates Rodney Hoskinson Rodney Hoskinson This presentation has been prepared for the Actuaries Institute 2014 Financial Services Forum. The Institute

A Hybrid Commodity and Interest Rate Market Model

A Hybrid Commodity and Interest Rate Market Model K.F. Pilz and E. Schlögl University of Technology Sydney Australia September 5, Abstract A joint model of commodity price and interest rate risk is constructed

A Hybrid Commodity and Interest Rate Market Model K.F. Pilz and E. Schlögl University of Technology Sydney Australia September 5, Abstract A joint model of commodity price and interest rate risk is constructed

Callability Features

2 Callability Features 2.1 Introduction and Objectives In this chapter, we introduce callability which gives one party in a transaction the right (but not the obligation) to terminate the transaction early.

2 Callability Features 2.1 Introduction and Objectives In this chapter, we introduce callability which gives one party in a transaction the right (but not the obligation) to terminate the transaction early.

The Black-Scholes Model

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

Linear-Rational Term-Structure Models

Linear-Rational Term-Structure Models Anders Trolle (joint with Damir Filipović and Martin Larsson) Ecole Polytechnique Fédérale de Lausanne Swiss Finance Institute AMaMeF and Swissquote Conference, September

Linear-Rational Term-Structure Models Anders Trolle (joint with Damir Filipović and Martin Larsson) Ecole Polytechnique Fédérale de Lausanne Swiss Finance Institute AMaMeF and Swissquote Conference, September

Option Models for Bonds and Interest Rate Claims

Option Models for Bonds and Interest Rate Claims Peter Ritchken 1 Learning Objectives We want to be able to price any fixed income derivative product using a binomial lattice. When we use the lattice to

Option Models for Bonds and Interest Rate Claims Peter Ritchken 1 Learning Objectives We want to be able to price any fixed income derivative product using a binomial lattice. When we use the lattice to

Risk managing long-dated smile risk with SABR formula

Risk managing long-dated smile risk with SABR formula Claudio Moni QuaRC, RBS November 7, 2011 Abstract In this paper 1, we show that the sensitivities to the SABR parameters can be materially wrong when

Risk managing long-dated smile risk with SABR formula Claudio Moni QuaRC, RBS November 7, 2011 Abstract In this paper 1, we show that the sensitivities to the SABR parameters can be materially wrong when

Pricing basket options with an eye on swaptions

Pricing basket options with an eye on swaptions Alexandre d Aspremont ORFE Part of thesis supervised by Nicole El Karoui. Data from BNP-Paribas, London. A. d Aspremont, ORFE ORF557, stochastic analysis

Pricing basket options with an eye on swaptions Alexandre d Aspremont ORFE Part of thesis supervised by Nicole El Karoui. Data from BNP-Paribas, London. A. d Aspremont, ORFE ORF557, stochastic analysis

Derivatives Options on Bonds and Interest Rates. Professor André Farber Solvay Business School Université Libre de Bruxelles

Derivatives Options on Bonds and Interest Rates Professor André Farber Solvay Business School Université Libre de Bruxelles Caps Floors Swaption Options on IR futures Options on Government bond futures

Derivatives Options on Bonds and Interest Rates Professor André Farber Solvay Business School Université Libre de Bruxelles Caps Floors Swaption Options on IR futures Options on Government bond futures

European call option with inflation-linked strike

Mathematical Statistics Stockholm University European call option with inflation-linked strike Ola Hammarlid Research Report 2010:2 ISSN 1650-0377 Postal address: Mathematical Statistics Dept. of Mathematics

Mathematical Statistics Stockholm University European call option with inflation-linked strike Ola Hammarlid Research Report 2010:2 ISSN 1650-0377 Postal address: Mathematical Statistics Dept. of Mathematics

Extended Libor Models and Their Calibration

Extended Libor Models and Their Calibration Denis Belomestny Weierstraß Institute Berlin Vienna, 16 November 2007 Denis Belomestny (WIAS) Extended Libor Models and Their Calibration Vienna, 16 November

Extended Libor Models and Their Calibration Denis Belomestny Weierstraß Institute Berlin Vienna, 16 November 2007 Denis Belomestny (WIAS) Extended Libor Models and Their Calibration Vienna, 16 November

Interest rate models in continuous time

slides for the course Interest rate theory, University of Ljubljana, 2012-13/I, part IV József Gáll University of Debrecen Nov. 2012 Jan. 2013, Ljubljana Continuous time markets General assumptions, notations

slides for the course Interest rate theory, University of Ljubljana, 2012-13/I, part IV József Gáll University of Debrecen Nov. 2012 Jan. 2013, Ljubljana Continuous time markets General assumptions, notations

OPTION VALUATION Fall 2000

OPTION VALUATION Fall 2000 2 Essentially there are two models for pricing options a. Black Scholes Model b. Binomial option Pricing Model For equities, usual model is Black Scholes. For most bond options

OPTION VALUATION Fall 2000 2 Essentially there are two models for pricing options a. Black Scholes Model b. Binomial option Pricing Model For equities, usual model is Black Scholes. For most bond options

COMPARING DISCRETISATIONS OF THE LIBOR MARKET MODEL IN THE SPOT MEASURE

COMPARING DISCRETISATIONS OF THE LIBOR MARKET MODEL IN THE SPOT MEASURE CHRISTOPHER BEVERIDGE, NICHOLAS DENSON, AND MARK JOSHI Abstract. Various drift approximations for the displaced-diffusion LIBOR market

COMPARING DISCRETISATIONS OF THE LIBOR MARKET MODEL IN THE SPOT MEASURE CHRISTOPHER BEVERIDGE, NICHOLAS DENSON, AND MARK JOSHI Abstract. Various drift approximations for the displaced-diffusion LIBOR market

Basic Arbitrage Theory KTH Tomas Björk

Basic Arbitrage Theory KTH 2010 Tomas Björk Tomas Björk, 2010 Contents 1. Mathematics recap. (Ch 10-12) 2. Recap of the martingale approach. (Ch 10-12) 3. Change of numeraire. (Ch 26) Björk,T. Arbitrage

Basic Arbitrage Theory KTH 2010 Tomas Björk Tomas Björk, 2010 Contents 1. Mathematics recap. (Ch 10-12) 2. Recap of the martingale approach. (Ch 10-12) 3. Change of numeraire. (Ch 26) Björk,T. Arbitrage

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester Our exam is Wednesday, December 19, at the normal class place and time. You may bring two sheets of notes (8.5

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester Our exam is Wednesday, December 19, at the normal class place and time. You may bring two sheets of notes (8.5

θ(t ) = T f(0, T ) + σ2 T

= T f(0, T ) + σ2 T") 1 Derivatives Pricing and Financial Modelling Andrew Cairns: room M3.08 E-mail: A.Cairns@ma.hw.ac.uk Tutorial 10 1. (Ho-Lee) Let X(T ) = T 0 W t dt. (a) What is the distribution of X(T )? (b) Find E[exp(

1 Derivatives Pricing and Financial Modelling Andrew Cairns: room M3.08 E-mail: A.Cairns@ma.hw.ac.uk Tutorial 10 1. (Ho-Lee) Let X(T ) = T 0 W t dt. (a) What is the distribution of X(T )? (b) Find E[exp(

************************

Derivative Securities Options on interest-based instruments: pricing of bond options, caps, floors, and swaptions. The most widely-used approach to pricing options on caps, floors, swaptions, and similar

Derivative Securities Options on interest-based instruments: pricing of bond options, caps, floors, and swaptions. The most widely-used approach to pricing options on caps, floors, swaptions, and similar

Control variates for callable Libor exotics

Control variates for callable Libor exotics J. Buitelaar August 2006 Abstract In this thesis we investigate the use of control variates for the pricing of callable Libor exotics in the Libor Market Model.

Control variates for callable Libor exotics J. Buitelaar August 2006 Abstract In this thesis we investigate the use of control variates for the pricing of callable Libor exotics in the Libor Market Model.

Multi-Curve Convexity

Multi-Curve Convexity CMS Pricing with Normal Volatilities and Basis Spreads in QuantLib Sebastian Schlenkrich London, July 12, 2016 d-fine d-fine All rights All rights reserved reserved 0 Agenda 1. CMS

Multi-Curve Convexity CMS Pricing with Normal Volatilities and Basis Spreads in QuantLib Sebastian Schlenkrich London, July 12, 2016 d-fine d-fine All rights All rights reserved reserved 0 Agenda 1. CMS

Discrete time semi-markov switching interest rate models

Discrete time semi-markov switching interest rate models Julien Hunt Joint work with Pierre Devolder January 29, 2009 On the importance of interest rate models Borrowing and lending: a dangerous business...cfr.

Discrete time semi-markov switching interest rate models Julien Hunt Joint work with Pierre Devolder January 29, 2009 On the importance of interest rate models Borrowing and lending: a dangerous business...cfr.

Some notes on term structure modelling

Chapter 8 Some notes on term structure modelling 8. Introduction After the brief encounter with continuous time modelling in Chapter 7 we now return to the discrete time, finite state space models of Chapter

Chapter 8 Some notes on term structure modelling 8. Introduction After the brief encounter with continuous time modelling in Chapter 7 we now return to the discrete time, finite state space models of Chapter

INTEREST RATES AND FX MODELS

INTEREST RATES AND FX MODELS 3. The Volatility Cube Andrew Lesniewski Courant Institute of Mathematics New York University New York February 17, 2011 2 Interest Rates & FX Models Contents 1 Dynamics of

INTEREST RATES AND FX MODELS 3. The Volatility Cube Andrew Lesniewski Courant Institute of Mathematics New York University New York February 17, 2011 2 Interest Rates & FX Models Contents 1 Dynamics of

LIBOR Convexity Adjustments for the Vasiček and Cox-Ingersoll-Ross models

LIBOR Convexity Adjustments for the Vasiček and Cox-Ingersoll-Ross models B. F. L. Gaminha 1, Raquel M. Gaspar 2, O. Oliveira 1 1 Dep. de Física, Universidade de Coimbra, 34 516 Coimbra, Portugal 2 Advance

LIBOR Convexity Adjustments for the Vasiček and Cox-Ingersoll-Ross models B. F. L. Gaminha 1, Raquel M. Gaspar 2, O. Oliveira 1 1 Dep. de Física, Universidade de Coimbra, 34 516 Coimbra, Portugal 2 Advance

Forward Risk Adjusted Probability Measures and Fixed-income Derivatives

Lecture 9 Forward Risk Adjusted Probability Measures and Fixed-income Derivatives 9.1 Forward risk adjusted probability measures This section is a preparation for valuation of fixed-income derivatives.

Lecture 9 Forward Risk Adjusted Probability Measures and Fixed-income Derivatives 9.1 Forward risk adjusted probability measures This section is a preparation for valuation of fixed-income derivatives.

TITLE OF THESIS IN CAPITAL LETTERS. by Your Full Name Your first degree, in Area, Institution, Year Your second degree, in Area, Institution, Year

TITLE OF THESIS IN CAPITAL LETTERS by Your Full Name Your first degree, in Area, Institution, Year Your second degree, in Area, Institution, Year Submitted to the Institute for Graduate Studies in Science

TITLE OF THESIS IN CAPITAL LETTERS by Your Full Name Your first degree, in Area, Institution, Year Your second degree, in Area, Institution, Year Submitted to the Institute for Graduate Studies in Science

Smile-consistent CMS adjustments in closed form: introducing the Vanna-Volga approach

Smile-consistent CMS adjustments in closed form: introducing the Vanna-Volga approach Antonio Castagna, Fabio Mercurio and Marco Tarenghi Abstract In this article, we introduce the Vanna-Volga approach

Smile-consistent CMS adjustments in closed form: introducing the Vanna-Volga approach Antonio Castagna, Fabio Mercurio and Marco Tarenghi Abstract In this article, we introduce the Vanna-Volga approach

AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management ( )

") AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management (26.4-26.7) 1 / 30 Outline Term Structure Forward Contracts on Bonds Interest Rate Futures Contracts

AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management (26.4-26.7) 1 / 30 Outline Term Structure Forward Contracts on Bonds Interest Rate Futures Contracts

Amortizing and Accreting Caps Vaulation

Amortizing and Accreting Caps Vaulation Alan White FinPricing http://www.finpricing.com Summary Interest Rate Amortizing and Accreting Cap Introduction The Benefits of an Amortizing or Accreting Cap Caplet

Amortizing and Accreting Caps Vaulation Alan White FinPricing http://www.finpricing.com Summary Interest Rate Amortizing and Accreting Cap Introduction The Benefits of an Amortizing or Accreting Cap Caplet

INTEREST RATES AND FX MODELS

INTEREST RATES AND FX MODELS 6. LIBOR Market Model Andrew Lesniewski Courant Institute of Mathematical Sciences New York University New York March 6, 2013 2 Interest Rates & FX Models Contents 1 Introduction

INTEREST RATES AND FX MODELS 6. LIBOR Market Model Andrew Lesniewski Courant Institute of Mathematical Sciences New York University New York March 6, 2013 2 Interest Rates & FX Models Contents 1 Introduction

Managing Systematic Mortality Risk in Life Annuities: An Application of Longevity Derivatives

Managing Systematic Mortality Risk in Life Annuities: An Application of Longevity Derivatives Simon Man Chung Fung, Katja Ignatieva and Michael Sherris School of Risk & Actuarial Studies University of

Managing Systematic Mortality Risk in Life Annuities: An Application of Longevity Derivatives Simon Man Chung Fung, Katja Ignatieva and Michael Sherris School of Risk & Actuarial Studies University of

Plain Vanilla - Black model Version 1.2

Plain Vanilla - Black model Version 1.2 1 Introduction The Plain Vanilla plug-in provides Fairmat with the capability to price a plain vanilla swap or structured product with options like caps/floors,

Plain Vanilla - Black model Version 1.2 1 Introduction The Plain Vanilla plug-in provides Fairmat with the capability to price a plain vanilla swap or structured product with options like caps/floors,

FX Smile Modelling. 9 September September 9, 2008

FX Smile Modelling 9 September 008 September 9, 008 Contents 1 FX Implied Volatility 1 Interpolation.1 Parametrisation............................. Pure Interpolation.......................... Abstract

FX Smile Modelling 9 September 008 September 9, 008 Contents 1 FX Implied Volatility 1 Interpolation.1 Parametrisation............................. Pure Interpolation.......................... Abstract

Crashcourse Interest Rate Models

Crashcourse Interest Rate Models Stefan Gerhold August 30, 2006 Interest Rate Models Model the evolution of the yield curve Can be used for forecasting the future yield curve or for pricing interest rate

Crashcourse Interest Rate Models Stefan Gerhold August 30, 2006 Interest Rate Models Model the evolution of the yield curve Can be used for forecasting the future yield curve or for pricing interest rate

Phase Transition in a Log-Normal Interest Rate Model

in a Log-normal Interest Rate Model 1 1 J. P. Morgan, New York 17 Oct. 2011 in a Log-Normal Interest Rate Model Outline Introduction to interest rate modeling Black-Derman-Toy model Generalization with

in a Log-normal Interest Rate Model 1 1 J. P. Morgan, New York 17 Oct. 2011 in a Log-Normal Interest Rate Model Outline Introduction to interest rate modeling Black-Derman-Toy model Generalization with

The irony in the derivatives discounting

MPRA Munich Personal RePEc Archive The irony in the derivatives discounting Marc Henrard BIS 26. March 2007 Online at http://mpra.ub.uni-muenchen.de/3115/ MPRA Paper No. 3115, posted 8. May 2007 THE IRONY

MPRA Munich Personal RePEc Archive The irony in the derivatives discounting Marc Henrard BIS 26. March 2007 Online at http://mpra.ub.uni-muenchen.de/3115/ MPRA Paper No. 3115, posted 8. May 2007 THE IRONY

Pricing Interest Rate Derivatives: An Application to the Uruguayan Market

Pricing Interest Rate Derivatives: An Application to the Uruguayan Market Guillermo Magnou 1 July 2017 Abstract In recent years, the volatility of the international financial system has become a serious

Pricing Interest Rate Derivatives: An Application to the Uruguayan Market Guillermo Magnou 1 July 2017 Abstract In recent years, the volatility of the international financial system has become a serious

A new approach to LIBOR modeling

A new approach to LIBOR modeling Antonis Papapantoleon FAM TU Vienna Based on joint work with Martin Keller-Ressel and Josef Teichmann Istanbul Workshop on Mathematical Finance Istanbul, Turkey, 18 May

A new approach to LIBOR modeling Antonis Papapantoleon FAM TU Vienna Based on joint work with Martin Keller-Ressel and Josef Teichmann Istanbul Workshop on Mathematical Finance Istanbul, Turkey, 18 May

FIXED INCOME SECURITIES

FIXED INCOME SECURITIES Valuation, Risk, and Risk Management Pietro Veronesi University of Chicago WILEY JOHN WILEY & SONS, INC. CONTENTS Preface Acknowledgments PART I BASICS xix xxxiii AN INTRODUCTION

FIXED INCOME SECURITIES Valuation, Risk, and Risk Management Pietro Veronesi University of Chicago WILEY JOHN WILEY & SONS, INC. CONTENTS Preface Acknowledgments PART I BASICS xix xxxiii AN INTRODUCTION

Volatility Smiles and Yield Frowns

Volatility Smiles and Yield Frowns Peter Carr NYU CBOE Conference on Derivatives and Volatility, Chicago, Nov. 10, 2017 Peter Carr (NYU) Volatility Smiles and Yield Frowns 11/10/2017 1 / 33 Interest Rates

Volatility Smiles and Yield Frowns Peter Carr NYU CBOE Conference on Derivatives and Volatility, Chicago, Nov. 10, 2017 Peter Carr (NYU) Volatility Smiles and Yield Frowns 11/10/2017 1 / 33 Interest Rates

Advanced Topics in Derivative Pricing Models. Topic 4 - Variance products and volatility derivatives

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

Back-of-the-envelope swaptions in a very parsimonious multicurve interest rate model

Back-of-the-envelope swaptions in a very parsimonious multicurve interest rate model Roberto Baviera December 19, 2017 arxiv:1712.06466v1 [q-fin.pr] 18 Dec 2017 ( ) Politecnico di Milano, Department of

Back-of-the-envelope swaptions in a very parsimonious multicurve interest rate model Roberto Baviera December 19, 2017 arxiv:1712.06466v1 [q-fin.pr] 18 Dec 2017 ( ) Politecnico di Milano, Department of

25. Interest rates models. MA6622, Ernesto Mordecki, CityU, HK, References for this Lecture:

25. Interest rates models MA6622, Ernesto Mordecki, CityU, HK, 2006. References for this Lecture: John C. Hull, Options, Futures & other Derivatives (Fourth Edition), Prentice Hall (2000) 1 Plan of Lecture

25. Interest rates models MA6622, Ernesto Mordecki, CityU, HK, 2006. References for this Lecture: John C. Hull, Options, Futures & other Derivatives (Fourth Edition), Prentice Hall (2000) 1 Plan of Lecture

d St+ t u. With numbers e q = The price of the option in three months is

Exam in SF270 Financial Mathematics. Tuesday June 3 204 8.00-3.00. Answers and brief solutions.. (a) This exercise can be solved in two ways. i. Risk-neutral valuation. The martingale measure should satisfy

Exam in SF270 Financial Mathematics. Tuesday June 3 204 8.00-3.00. Answers and brief solutions.. (a) This exercise can be solved in two ways. i. Risk-neutral valuation. The martingale measure should satisfy

Volatility Smiles and Yield Frowns

Volatility Smiles and Yield Frowns Peter Carr NYU IFS, Chengdu, China, July 30, 2018 Peter Carr (NYU) Volatility Smiles and Yield Frowns 7/30/2018 1 / 35 Interest Rates and Volatility Practitioners and

Volatility Smiles and Yield Frowns Peter Carr NYU IFS, Chengdu, China, July 30, 2018 Peter Carr (NYU) Volatility Smiles and Yield Frowns 7/30/2018 1 / 35 Interest Rates and Volatility Practitioners and

IEOR E4602: Quantitative Risk Management

IEOR E4602: Quantitative Risk Management Model Risk Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Outline Introduction to

IEOR E4602: Quantitative Risk Management Model Risk Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Outline Introduction to

Tangent Lévy Models. Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford.

Oxford-Man Institute of Quantitative Finance University of Oxford.") Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Interest Rate Modeling

Chapman & Hall/CRC FINANCIAL MATHEMATICS SERIES Interest Rate Modeling Theory and Practice Lixin Wu CRC Press Taylor & Francis Group Boca Raton London New York CRC Press is an imprint of the Taylor & Francis

Chapman & Hall/CRC FINANCIAL MATHEMATICS SERIES Interest Rate Modeling Theory and Practice Lixin Wu CRC Press Taylor & Francis Group Boca Raton London New York CRC Press is an imprint of the Taylor & Francis

Local Volatility Dynamic Models

René Carmona Bendheim Center for Finance Department of Operations Research & Financial Engineering Princeton University Columbia November 9, 27 Contents Joint work with Sergey Nadtochyi Motivation 1 Understanding

René Carmona Bendheim Center for Finance Department of Operations Research & Financial Engineering Princeton University Columbia November 9, 27 Contents Joint work with Sergey Nadtochyi Motivation 1 Understanding

1 Mathematics in a Pill 1.1 PROBABILITY SPACE AND RANDOM VARIABLES. A probability triple P consists of the following components:

1 Mathematics in a Pill The purpose of this chapter is to give a brief outline of the probability theory underlying the mathematics inside the book, and to introduce necessary notation and conventions

1 Mathematics in a Pill The purpose of this chapter is to give a brief outline of the probability theory underlying the mathematics inside the book, and to introduce necessary notation and conventions

MATHEMATICAL FINANCE EXAM 2003/4 RP s solutions & comments

MATHEMATICAL FINANCE EXAM 23/4 RP s solutions & comments This version is from January 8, 24, ie. after the exam and after I ve gone through your answers. Since I m not the one taking the exam, I can be

MATHEMATICAL FINANCE EXAM 23/4 RP s solutions & comments This version is from January 8, 24, ie. after the exam and after I ve gone through your answers. Since I m not the one taking the exam, I can be

Valuing Coupon Bond Linked to Variable Interest Rate

MPRA Munich Personal RePEc Archive Valuing Coupon Bond Linked to Variable Interest Rate Giandomenico, Rossano 2008 Online at http://mpra.ub.uni-muenchen.de/21974/ MPRA Paper No. 21974, posted 08. April

MPRA Munich Personal RePEc Archive Valuing Coupon Bond Linked to Variable Interest Rate Giandomenico, Rossano 2008 Online at http://mpra.ub.uni-muenchen.de/21974/ MPRA Paper No. 21974, posted 08. April

BOND MARKET MODEL. ROBERTO BAVIERA Abaxbank, corso Monforte, 34 I Milan, Italy

International Journal of Theoretical and Applied Finance Vol. 9, No. 4 (2006) 577 596 c World Scientific Publishing Company BOND MARKET MODEL ROBERTO BAVIERA Abaxbank, corso Monforte, 34 I-2022 Milan,

International Journal of Theoretical and Applied Finance Vol. 9, No. 4 (2006) 577 596 c World Scientific Publishing Company BOND MARKET MODEL ROBERTO BAVIERA Abaxbank, corso Monforte, 34 I-2022 Milan,

Chapter 15: Jump Processes and Incomplete Markets. 1 Jumps as One Explanation of Incomplete Markets

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

Model Risk Assessment

Model Risk Assessment Case Study Based on Hedging Simulations Drona Kandhai (PhD) Head of Interest Rates, Inflation and Credit Quantitative Analytics Team CMRM Trading Risk - ING Bank Assistant Professor

Model Risk Assessment Case Study Based on Hedging Simulations Drona Kandhai (PhD) Head of Interest Rates, Inflation and Credit Quantitative Analytics Team CMRM Trading Risk - ING Bank Assistant Professor

Practical example of an Economic Scenario Generator

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

Interest Rate Volatility

Interest Rate Volatility III. Working with SABR Andrew Lesniewski Baruch College and Posnania Inc First Baruch Volatility Workshop New York June 16-18, 2015 Outline Arbitrage free SABR 1 Arbitrage free

Interest Rate Volatility III. Working with SABR Andrew Lesniewski Baruch College and Posnania Inc First Baruch Volatility Workshop New York June 16-18, 2015 Outline Arbitrage free SABR 1 Arbitrage free

No-Arbitrage Conditions for the Dynamics of Smiles

No-Arbitrage Conditions for the Dynamics of Smiles Presentation at King s College Riccardo Rebonato QUARC Royal Bank of Scotland Group Research in collaboration with Mark Joshi Thanks to David Samuel The

No-Arbitrage Conditions for the Dynamics of Smiles Presentation at King s College Riccardo Rebonato QUARC Royal Bank of Scotland Group Research in collaboration with Mark Joshi Thanks to David Samuel The

Introduction to Financial Mathematics

Introduction to Financial Mathematics MTH 210 Fall 2016 Jie Zhong November 30, 2016 Mathematics Department, UR Table of Contents Arbitrage Interest Rates, Discounting, and Basic Assets Forward Contracts

Introduction to Financial Mathematics MTH 210 Fall 2016 Jie Zhong November 30, 2016 Mathematics Department, UR Table of Contents Arbitrage Interest Rates, Discounting, and Basic Assets Forward Contracts

Policy iterated lower bounds and linear MC upper bounds for Bermudan style derivatives

Finance Winterschool 2007, Lunteren NL Policy iterated lower bounds and linear MC upper bounds for Bermudan style derivatives Pricing complex structured products Mohrenstr 39 10117 Berlin schoenma@wias-berlin.de

Finance Winterschool 2007, Lunteren NL Policy iterated lower bounds and linear MC upper bounds for Bermudan style derivatives Pricing complex structured products Mohrenstr 39 10117 Berlin schoenma@wias-berlin.de

Financial Markets & Risk

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

Pricing Bermudan swap options using the BGM model with arbitrage-free discretisation and boundary based option exercise

Master thesis MS 2003 13 Mathematical Statistics Pricing Bermudan swap options using the BGM model with arbitrage-free discretisation and boundary based option exercise Henrik Alpsten aquilat@kth.se, +46-(0)736

Master thesis MS 2003 13 Mathematical Statistics Pricing Bermudan swap options using the BGM model with arbitrage-free discretisation and boundary based option exercise Henrik Alpsten aquilat@kth.se, +46-(0)736

FINANCIAL OPTION ANALYSIS HANDOUTS

FINANCIAL OPTION ANALYSIS HANDOUTS 1 2 FAIR PRICING There is a market for an object called S. The prevailing price today is S 0 = 100. At this price the object S can be bought or sold by anyone for any

FINANCIAL OPTION ANALYSIS HANDOUTS 1 2 FAIR PRICING There is a market for an object called S. The prevailing price today is S 0 = 100. At this price the object S can be bought or sold by anyone for any

Chapter 24 Interest Rate Models

Chapter 4 Interest Rate Models Question 4.1. a F = P (0, /P (0, 1 =.8495/.959 =.91749. b Using Black s Formula, BSCall (.8495,.9009.959,.1, 0, 1, 0 = $0.0418. (1 c Using put call parity for futures options,

Chapter 4 Interest Rate Models Question 4.1. a F = P (0, /P (0, 1 =.8495/.959 =.91749. b Using Black s Formula, BSCall (.8495,.9009.959,.1, 0, 1, 0 = $0.0418. (1 c Using put call parity for futures options,

Interest rate models and Solvency II

www.nr.no Outline Desired properties of interest rate models in a Solvency II setting. A review of three well-known interest rate models A real example from a Norwegian insurance company 2 Interest rate

www.nr.no Outline Desired properties of interest rate models in a Solvency II setting. A review of three well-known interest rate models A real example from a Norwegian insurance company 2 Interest rate