Balance Sheet Strategies For Changing Rate Environments

|

|

|

- Sheila McDonald

- 5 years ago

- Views:

Transcription

1 Balance Sheet Strategies For Changing Rate Environments Moss Adams 2017 Credit Union Conference Portland, OR June 22 nd, 2017 Ryan W. Hayhurst Managing Director

2 Credit Union Industry Trends 2

3 3

4 Regulatory Focus in2017 Credit Risk o o o Credit risk increasing because of strong loan growth combined with easing in underwriting standards Examiner surveys showing an easing in underwriting standards CRE concentration to get extra exam scrutiny this year Cybersecurity o Will this ever go away? (Hint: The Answer is No!) o FDIC has new IT Technology Risk Examination Program (June 2016) o FFIEC released Cybersecurity Assessment Tool (July 2015) Liquidity Risk Management o o o Rising L/D Ratios and falling Liquidity Ratios move Liquidity Risk up the priority list Do we have good risk management systems in place to measure and monitor our liquidity levels? Forward Looking & Dynamic Liquidity Modeling (Stress Testing!!) Interest Rate Risk o o Moved down the priority list last year or so, but with the recent move in the yield curve and the likelihood of more 2017 rate hikes, it will likely remain a high regulatory focus. Potential for NMD migration a particular concern for regulators 4

5

6

7

8

9

The")

10 Regulatory Focus: Liquidity Risk Management IRR & Liquidity Risk Are Closely Related Less Liquidity in the Banking System Due to Higher Loan Demand Focus on Measuring, Monitoring and Reporting Systems Forward Looking & Dynamic Sources & Uses Dynamic Cash Flow Analysis Stress Testing Contingency Funding Planning Diversified Funding Cushion of liquid assets (marketable investments) The Liquidity Regulatory Guidance is not new, however, there seems to be more focus on Liquidity Risk Management during recent examinations. 10

11 What Are Considered Liquid Assets? On Balance Sheet Liquid Assets: o Cash on Hand o Cash on Deposit in Banks & CUs o Cash Equivalents (<3mo, FFS, CD s) o Highly Liquid/Readily Marketable Securities US Credit Unions $100mm $3 Billion Total Assets $332mm Cash & Cash Equiv $45mm Investment Portfolio $96mm 11

12 12

13 13

14 14

15 15

16 Seminar Attendees: Excess Liquidity Portfolio Performance 16

Avg.")

17 May 2017 Portfolio Summary All Credit Union Portfolios Portfolios on Baker Bond Accounting (BBA) Avg. Book Yield = 2.8% Avg. Life = 3.4 years +300bps Avg. Life = 3.9 years +300bps Price Risk = 8.92% 17

18 Credit Union Investment Portfolio Management: Characteristics of High Performance Use The Investment Portfolio To Fight Margin Erosion The bond portfolio is the only place we can increase margin without hurting the membership Define, Measure & Manage Define your portfolio objectives & risk tolerance Measure your risk exposure quality analytics and easy to understand reporting is essential! Manage your risk actively manage the portfolio in the context of the entire balance sheet Develop a Written Investment Strategy Build a portfolio, don t be sold one Be proactive, not reactive with a disciplined investment strategy Diversify The Portfolio Across Sectors and Within Sectors Each sector has its pros & cons, diversity protects against a range of interest rate scenarios Minimize Cash/CD s in Favor of Bonds (esp. MBS/CMO) High performance portfolios tend to own less Cash/CDs/Agencies, more MBS/CMO Bottom quartile portfolios tend to own a lot of Cash/CDs/Agencies Build a Portfolio of Stable, Predictable Cash Flow Steady, consistent cash flow is the best natural hedge against rising rates Overreliance on volatile cash flows (e.g. callable agencies) will force you to reinvest too much cash flow when rates are low and not enough when rates are high 18

19 Fed Funds Target Rate June 1986 Today Orange County CA Bankruptcy Long Maturity Callable Advances, Corporates CDOs, Private Label MBS/CMO, Trust Preferreds, FN/FH Preferred Stock Structured Notes: Dual Index Range Notes Inverse Floaters? Structured Notes, Long Callables / Step-Ups, Extend-O-Matic CMOs 19

20 The Interest Rate Cycle and Asset Strategies Trough Rising Peak Falling Reduce duration Transition duration to neutral Extend duration Transition duration to neutral Premiums and/or higher coupons Roll up in coupon Buy negative convexity High cashflow bonds Transition from higher to lower coupons Discounts and/or lower coupons Roll down in coupon Reduce negative convexity Lockouts Transition from higher to lower coupons Buy ARMs & floaters Buy ARMs & floaters Sell ARMs & floaters Sell ARMs & floaters Current pay CMBS Current pay CMBS Lockout CMBS Lockout CMBS Prepay protection important Prepay protection less important Prepay protection more important 1X Callable Agencies Continuous calls outperform Bullet agencies or callables with call protection Cushion callables Discount callables Prepay protection critical Bullet agencies or callables with call protection 20

21 Possible Liquidity Risks from Rising Interest Rates Reduced Mortgage/Loan Payments Refinance incentive goes away Reduced Deposit Levels Migration / Disintermediation Increased Loan Demand Local economic activity improves Options Risk (Callable Bonds and MBS/CMOs) Reduced Asset Valuations Reduced Borrowing Capacity (Can be related to #5) Call Options no longer in the money Can no longer painlessly liquidate securities / monetize loans Increased haircuts / requirements for REPO lines, etc. 21

22 10 Year Treasury Yield Jan 2011 Today Taper Tantrum Trump Jump Reality Rally 22

23 Projected Cash Flow Volatility During 2013 Taper Tantrum Callable Agencies vs MBS/CMO Callable Agency Focus May 2013 MBS/CMO Focus May 2013 Investment portfolio cashflow is one of the most important sources of liquidity that can also provide the necessary earnings to increase net worth. But we must ensure that our cashflow is stable and predictable as rates rise. Callable Agency Focus June 2013 MBS/CMO Focus June

24 Extension Protection Menu: MBS/CMO Low Loan Balance Collateral o LLB pools have slowed the LEAST over the last 6mos of falling prepayments. Relocation Pools o Relos tend to be less rate sensitive and often prepay faster than their cohort when out of the money as the homeowners are relocated by their employees. Roll Down in MBS Terms and Up in Coupon o o Aggregate 10yr terms are now paying faster than 15yrs, 20yrs, and 30yrs! The lowest coupons in the stack are showing significant extension risks at current prepay speeds Agency CMBS: K Fred Lockout (A2) and/or FNMA DUS o Steady Predictable Cash Flows are crucial in a rising rate environment. PAC/VADM CMOs o o o Planned Amortization Class CMOs are often structured to limit extension risk by creating support tranches that give up their principal when prepays slow Very Accurately Defined Maturity CMOs can be structured to have virtually no change in cash flows across a range of prepay speeds Short stated final CMOs or those with short pay windows roll down the curve better than longer WAM MBS 24

25 Focus on Higher Coupon MBS To Limit Price Depreciation 15yr MBS Price Volatility By Coupon Taper Tantrum When Treasury yields rise and bond prices fall, lower coupon MBS normally fall much farther than higher coupons. To remain defensive in the face of a determined Fed, favor higher coupon MBS with good loan attributes. Trump Jump Px drop Nov 7 Dec 15 15yr 2.0 = 4.2% 15yr 2.5 = 3.6% 15yr 3.0 = 2.9% 15yr 3.5 = 1.9% 25

26 Often times, higher coupon MBS give you similar return with lower levels of price volatility and extension risk. 26

27 MBS Holdings Comparison: Federal Reserve vs. Baker BBA 27

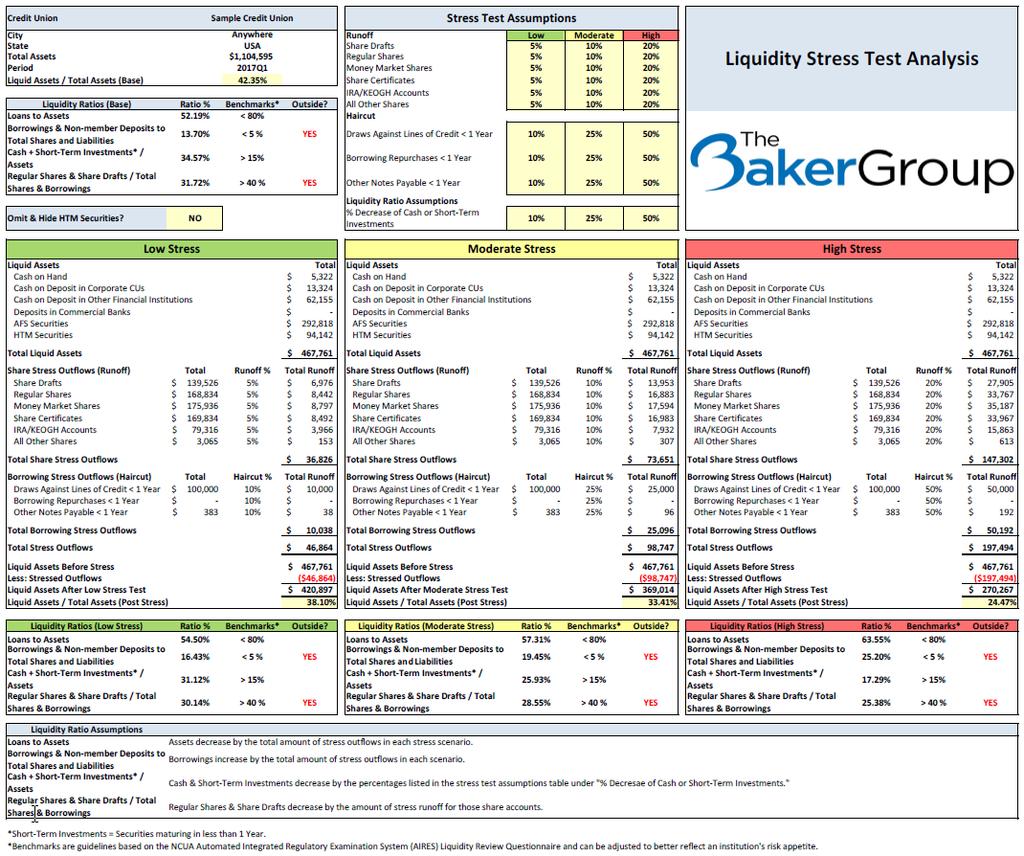

28 Dynamic Liquidity Monitor Case Study Base Case 28

29 Stress Testing Your Liquidity Risk Management Program Liquidity Stress Scenario # 1 Economic Recovery Scenario Stress Events o Market Interest Rates Increase 100bps o Increased Loan Demand 20% Annualized Loan Growth o Unfunded Commitments Fund at High Percentage 50% Draw Within 120 Days Strategic Questions to Ask o Do we have enough on balance sheet liquidity to fund these events? o Do we have adequate contingent sources of liquidity? o How does our cash flow change with an increase in market rates? o What are the roles and responsibilities of senior management? 29

30 Stress Test #1 Economic Recovery Scenario 30

31 Stress Testing Your Liquidity Risk Management Program Liquidity Stress Scenario # 2 Negative Publicity Scenario Stress Events o Non Maturity Depositor Runoff 10% Annualized Rate o Time Deposits Renewal Rate Decreases 80% Renewal Rate o Loss of Large Depositor $1 Million Depositor Leaves o Inability to Attract New Deposits 0% New Deposit Money Strategic Questions to Ask o Do we have enough on balance sheet liquidity to fund these events? o Do we have adequate contingent sources of liquidity? o What are the roles and responsibilities of senior management? 31

32 Stress Test #2 Negative Publicity Scenario 32

33 Stress Testing Your Liquidity Risk Management Program Liquidity Stress Scenario # 3 Apocalyptic Scenario Stress Events o Market Interest Rates Increase 400bps o Increased Loan Demand 20% Annualized Loan Growth o Non Maturity Depositor Runoff 20% Annualized Rate o Time Deposits Renewal Rate Decreases 50% Renewal Rate o Inability to Attract New Deposits 0% New Deposit Money o Loss of Large Depositor $1 Million Depositors Leaves Strategic Questions to Ask o Do we have enough on balance sheet liquidity to fund these events? Do we need to sell assets? o Do we have adequate contingent sources of liquidity? o How does our cash flow change with an increase in market rates? o What are the roles and responsibilities of senior management? 33

34 Stress Test #3 Apocalyptic Scenario 34

35 35

36

37 Sensitivity Testing: Non Maturity Deposits Whatever Baseline Assumptions You Use, Stress Test Them Institutions should incorporate stressed assumptions for non maturity deposits in IRR models FFIEC Three Ways to Stress NMS Assumptions (Sensitivity Tests) 1. Ratchet up pricing betas (shift sensitivities) and reduce time lags in order to mimic an aggressively competitive environment for NMS. (mainly impacts earnings at risk) 2. Reduce Average Life (and Duration) assumptions in order to assess the NEV impact of lower duration liabilities. 3. Simulate a migration of NMS balances into more rate sensitive funding (time deposits or wholesale funding) considered to be the most realistic depiction of what may happen in the next rate cycle. 37

38 NMS Surge Balance Analysis Can be easily generated for any credit union call to request This institution got 68% of total funding from NMD in 4Q2014 vs. a 25yr average of just 53%. If rates rise and NMD funding reverts to the long term average, this institution will have to replace funding for 15% of assets from CDs, Fed Funds or Borrowings. Simulating the impact of this deposit migration is critical to managing IRR in the next rate cycle. 38

39 NMS Migration Case Study This institution decided to simulate the impact of NMS funding returning to the 25 year average They ran two simulations showing 15% of total assets migrating out of NMS and into higher cost, more rate sensitive liabilities For Earnings at Risk simulation, migration occurred over 12 months. For NEV simulation, migration occurred immediately. Simulation # 1 All funds into overnight borrowings at 1.00% Simulation # 2 45% into FHLB 1yr 1.25% 33% into FHLB 2yr 1.45% 22% into FHLB 3yr 1.65% 39

Simulation # 2 (FHLB Laddered Funding) 40")

40 NMS Migration Case Study: Earnings at Risk Impact Simulation # 1 (Overnight Borrowings) Simulation # 2 (FHLB Laddered Funding) 40

41 Summary: Managing IRR, Liquidity & The Bond Portfolio Don t Be Complacent, Deploy Excess Liquidity To Fight Margin Erosion The bond portfolio is the only place we can increase margin without hurting the membership Margins continue to compress, it s critical to maximize portfolio earnings while managing risk Fed rate hikes expected to be slowest on record FF futures don t reach 1.5% before 2019 Stay fully invested and manage liquidity needs with FHLB/FNC or by selling short bonds Ensure Your Liquidity Management System Is Forward Looking & Dynamic IRR and Liquidity Risk are closely related how will your liquidity hold up when rates rise? Review Your IRR Process, Stress Your Assumptions & Simulation Migration Analyze your NMS to determine sensitivities/betas Run an NMS Surge Balance Analysis and simulate impact of NMD migration Develop A Written Investment Strategy A written investment strategy, updated quarterly, is the single most important thing you can do to ensure higher performance within acceptable risk parameters Build a portfolio, don t be sold one Security selection is critical don t chase yields in esoteric bonds. Stick with highly marketable bonds with stable cash flows. Build a High Performance Investment Portfolio Minimize Cash, CD s & Callable Agencies and favor MBS/CMOs with the right loan attributes Higher coupon 10 15yr MBS, PAC CMOs, Post Reset ARMs, < 5yr maturity Agencies/CDs Buy MBS/CMO with prepayment protection attributes LLB, Investor, NY/NJ/TX/PR, retail, etc. Build a Portfolio of Stable, Predictable Cash Flow There is no better hedge against rising rates than a portfolio of stable cash flow for reinvestment 41

Balance Sheet Strategies For Changing Rate Environments Asset/Liability Management Seminar

Balance Sheet Strategies For Changing Rate Environments Asset/Liability Management Seminar Pasadena & Concord, CA April 25-26, 2017 Ryan W. Hayhurst - Managing Director ryan@gobaker.com 800-962-9468 Market

Balance Sheet Strategies For Changing Rate Environments Asset/Liability Management Seminar Pasadena & Concord, CA April 25-26, 2017 Ryan W. Hayhurst - Managing Director ryan@gobaker.com 800-962-9468 Market

Asset/Liability Management

Asset/Liability Management FHLB System Sales and Marketing Meeting Scottsdale, AZ February 27 th, 2016 Ryan W. Hayhurst Managing Director Financial Strategies Group ryan@gobaker.com 800-962-9468 The Baker

Asset/Liability Management FHLB System Sales and Marketing Meeting Scottsdale, AZ February 27 th, 2016 Ryan W. Hayhurst Managing Director Financial Strategies Group ryan@gobaker.com 800-962-9468 The Baker

Investment Strategies for 1 st Quarter 2015

Investment Strategies for 1 st Quarter 2015 Conference Call will begin at 11:00am CT, lines open at 10:50am CT Audio: 855-749-4750 Access Code: 929 460 526 You can also listen to the conference call audio

Investment Strategies for 1 st Quarter 2015 Conference Call will begin at 11:00am CT, lines open at 10:50am CT Audio: 855-749-4750 Access Code: 929 460 526 You can also listen to the conference call audio

Investment Strategies For 1 st Quarter 2016

Investment Strategies For 1 st Quarter 2016 Conference Call will begin at 11:00am CT, lines open at 10:50am CT Audio: 855 749 4750 Access Code: 928 643 950# You can also listen to the conference call audio

Investment Strategies For 1 st Quarter 2016 Conference Call will begin at 11:00am CT, lines open at 10:50am CT Audio: 855 749 4750 Access Code: 928 643 950# You can also listen to the conference call audio

Fighting Margin Compression in a Zero Rate Environment

FHLBank Topeka 2013 Annual Management Conference Fighting Margin Compression in a Zero Rate Environment April 25, 2013 Presented by: Ryan Hayhurst, Manager Financial Strategies Group ryan@gobaker.com 800.962.9468

FHLBank Topeka 2013 Annual Management Conference Fighting Margin Compression in a Zero Rate Environment April 25, 2013 Presented by: Ryan Hayhurst, Manager Financial Strategies Group ryan@gobaker.com 800.962.9468

Advanced Asset/Liability Management

Advanced Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management Summary Developing Assumptions

Advanced Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management Summary Developing Assumptions

The Regulatory Focus on Interest Rate Risk: What to Expect and How to Comply

The Regulatory Focus on Interest Rate Risk: What to Expect and How to Comply Conference Call will begin at 10:00am CT, lines open at 10:50am CT Audio: 855-749-4750 Access Code: 920 722 897 # You can also

The Regulatory Focus on Interest Rate Risk: What to Expect and How to Comply Conference Call will begin at 10:00am CT, lines open at 10:50am CT Audio: 855-749-4750 Access Code: 920 722 897 # You can also

ALM Strategies In the Current Economic Environment Presented by: Frank Santucci Managing Director ALM Services (October 2015)

") 1 ALM Strategies In the Current Economic Environment Presented by: Frank Santucci Managing Director ALM Services (October 2015) 1 Asset Liability Management is the process of Measuring, Monitoring and

1 ALM Strategies In the Current Economic Environment Presented by: Frank Santucci Managing Director ALM Services (October 2015) 1 Asset Liability Management is the process of Measuring, Monitoring and

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Presented By: David W. Koch Chief Operating Officer FARIN & Associates, Inc.. dkoch@farin.com 1 Session Overview Session 1 Define

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Presented By: David W. Koch Chief Operating Officer FARIN & Associates, Inc.. dkoch@farin.com 1 Session Overview Session 1 Define

FHLB Des Moines Regional Member Meetings Profiting from a Rising Rate Environment

Risk Management Strategy & Solutions FHLB Des Moines Regional Member Meetings Profiting from a Rising Rate Environment Joseph Kennerson, Managing Director jkennerson@darlingconsulting.com Mark A. Haberland,

Risk Management Strategy & Solutions FHLB Des Moines Regional Member Meetings Profiting from a Rising Rate Environment Joseph Kennerson, Managing Director jkennerson@darlingconsulting.com Mark A. Haberland,

Weathering the Storm: Rates, Recession, and Risk

Weathering the Storm: Rates, Recession, and Risk Presenters: Charles McQueen Ed Lis Greg Gibson President VP of Finance & Compliance Chief Financial Officer McQueen Financial Adv. First Choice Financial

Weathering the Storm: Rates, Recession, and Risk Presenters: Charles McQueen Ed Lis Greg Gibson President VP of Finance & Compliance Chief Financial Officer McQueen Financial Adv. First Choice Financial

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP WVBA Convention July 29, 2014 Agenda Evaluating and Anticipating the Rate Environment Understanding Your Current

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP WVBA Convention July 29, 2014 Agenda Evaluating and Anticipating the Rate Environment Understanding Your Current

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Urum Urumoglu Senior Consultant FARIN & Associates, Inc.. Urum@farin.com 1 Session Overview Session 1 Define Interest Rate Risk IRR

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Urum Urumoglu Senior Consultant FARIN & Associates, Inc.. Urum@farin.com 1 Session Overview Session 1 Define Interest Rate Risk IRR

ALM Strategy in the Current Rate Environment. Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends

ALM Strategy in the Current Rate Environment Lisa Boylen Senior ALM Analyst December 12, 2018 1 Objectives Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends Lessons Learned

ALM Strategy in the Current Rate Environment Lisa Boylen Senior ALM Analyst December 12, 2018 1 Objectives Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends Lessons Learned

Investing in Mortgage-Backed Securities

Investing in Mortgage-Backed Securities Scott Wood Portfolio Strategist September 20, 2018 Securities offered through ProEquities, Inc., a registered Broker-Dealer and Member of FINRA and SIPC. Protective

Investing in Mortgage-Backed Securities Scott Wood Portfolio Strategist September 20, 2018 Securities offered through ProEquities, Inc., a registered Broker-Dealer and Member of FINRA and SIPC. Protective

Core Deposit Analytics Session 2: Beyond Basics - Applying Results

Core Deposit Analytics Session 2: Beyond Basics - Applying Results David Koch President/CEO dkoch@farin.com 800-236-3724 ext. 4217 1 Impact of Right Assumptions on ALCO Decision Making CORE DEPOSIT ASSUMPTIONS

Core Deposit Analytics Session 2: Beyond Basics - Applying Results David Koch President/CEO dkoch@farin.com 800-236-3724 ext. 4217 1 Impact of Right Assumptions on ALCO Decision Making CORE DEPOSIT ASSUMPTIONS

Now What? Navigating Fearlessly Through a Turbulent Environment February 2, 2016

Risk Management Strategy & Solutions Now What? Navigating Fearlessly Through a Turbulent Environment February 2, 2016 Frank L. Farone, Managing Director ffarone@darlingconsulting.com 2015 2016 Darling

Risk Management Strategy & Solutions Now What? Navigating Fearlessly Through a Turbulent Environment February 2, 2016 Frank L. Farone, Managing Director ffarone@darlingconsulting.com 2015 2016 Darling

Interest Rate Risk Measurement

Interest Rate Risk Measurement August 10, 2018 Ricky Brillard, CPA Senior Vice President Strategic Solutions Group 901-762-6415 rbrillard@viningsparks.com 1 Outline Trends Impacting Bank Balance Sheets

Interest Rate Risk Measurement August 10, 2018 Ricky Brillard, CPA Senior Vice President Strategic Solutions Group 901-762-6415 rbrillard@viningsparks.com 1 Outline Trends Impacting Bank Balance Sheets

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS June 13, 2013 Presented By Mike Ensweiler Director of Business Development Agenda General duties of directors What questions should directors be able to answer

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS June 13, 2013 Presented By Mike Ensweiler Director of Business Development Agenda General duties of directors What questions should directors be able to answer

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1 Todd Patrick Senior Vice President - Capital Markets CenterState Bank Atlanta, Georgia tpatrick@centerstatebank.com 770-850-3403 August 7, 2017 Intro

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1 Todd Patrick Senior Vice President - Capital Markets CenterState Bank Atlanta, Georgia tpatrick@centerstatebank.com 770-850-3403 August 7, 2017 Intro

THE CURRENT CHALLENGES OF MANAGING A CREDIT UNION INVESTMENT PORTFOLIO

THE CURRENT CHALLENGES OF MANAGING A CREDIT UNION INVESTMENT PORTFOLIO June 11, 2014 Steve Twersky, CPA David Howard, CFA FTN Portfolio Strategies Group Agenda The challenging landscape Impact of new risk-weighted

THE CURRENT CHALLENGES OF MANAGING A CREDIT UNION INVESTMENT PORTFOLIO June 11, 2014 Steve Twersky, CPA David Howard, CFA FTN Portfolio Strategies Group Agenda The challenging landscape Impact of new risk-weighted

Liquidity and Contingency Funding Strategies for Today s Market

Liquidity and Contingency Funding Strategies for Today s Market Presented by www.firstempire.com Today s Presenter Frank Santucci, Managing Director ALM Services, BSMS Frank has been working with banks

Liquidity and Contingency Funding Strategies for Today s Market Presented by www.firstempire.com Today s Presenter Frank Santucci, Managing Director ALM Services, BSMS Frank has been working with banks

Your State Association Presents. Interest Rate Risk: What Does th Future Hold? Program Materials

Your State Association Presents Interest Rate Risk: What Does th Future Hold? Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the

Your State Association Presents Interest Rate Risk: What Does th Future Hold? Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the

Lecture Materials FUNDING. Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 August 7 & 8, 2017 Funding - Developing Funding Strategies

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 August 7 & 8, 2017 Funding - Developing Funding Strategies

Mike McGinnis- Vice President, Investment Sales SSI 1 - INTRODUCTION TO CREDIT UNION FINANCIAL MANAGEMENT

Mike McGinnis- Vice President, Investment Sales SSI 1 - INTRODUCTION TO CREDIT UNION FINANCIAL MANAGEMENT Reviews the basic financial components and variables that impact credit union financial performance.

Mike McGinnis- Vice President, Investment Sales SSI 1 - INTRODUCTION TO CREDIT UNION FINANCIAL MANAGEMENT Reviews the basic financial components and variables that impact credit union financial performance.

Ben Lemoine Institutional Advisor Darcy Weeks Manager, Investment Operations

Ben Lemoine Institutional Advisor Darcy Weeks Manager, Investment Operations 1 Permissible Credit Union Investments Investment Cash Flow Characteristics Prepayment Speeds Price/Yield Inverse Relationship

Ben Lemoine Institutional Advisor Darcy Weeks Manager, Investment Operations 1 Permissible Credit Union Investments Investment Cash Flow Characteristics Prepayment Speeds Price/Yield Inverse Relationship

Liquidity Basics Measuring and Managing Liquidity

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Farin & Associates, Inc. Farin Foresight Software Certification as of November 30, 2017

Farin & Associates, Inc. Farin Foresight Software Certification as of November 30, 2017 by Alpha-Numeric Consulting, LLC December 20, 2017 Introduction Financial institutions recognize the need for accurate

Farin & Associates, Inc. Farin Foresight Software Certification as of November 30, 2017 by Alpha-Numeric Consulting, LLC December 20, 2017 Introduction Financial institutions recognize the need for accurate

ASSET/LIABILITY MANAGEMENT - YEAR 2

ASSET/LIABILITY MANAGEMENT - YEAR 2 Interest Rate Risk Measurement & Management Raleigh A. Trovillion Executive Vice President UMB Bank Investment Division St. Louis, MO raleigh.trovillion@umb.com 314-612-8039

ASSET/LIABILITY MANAGEMENT - YEAR 2 Interest Rate Risk Measurement & Management Raleigh A. Trovillion Executive Vice President UMB Bank Investment Division St. Louis, MO raleigh.trovillion@umb.com 314-612-8039

Loan Pricing Deals/Relationships Session 2. Agenda

Loan Pricing Deals/Relationships Session 2 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

Loan Pricing Deals/Relationships Session 2 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

PNC Bank, NA. Board Report. June 30, Pittsburgh, PA. A/L BENCHMARKS Standards for Asset/Liability Management

A/L BENCHMARKS Standards for Asset/Liability Management Board Report PNC Bank, NA June 30, 2006 Olson Research Associates, Inc. 10290 Old Columbia Road, Columbia, MD 21046 Phone: 888-657-6680 Web: http://www.olsonresearch.com

A/L BENCHMARKS Standards for Asset/Liability Management Board Report PNC Bank, NA June 30, 2006 Olson Research Associates, Inc. 10290 Old Columbia Road, Columbia, MD 21046 Phone: 888-657-6680 Web: http://www.olsonresearch.com

Georgia Banking School

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management I 2016 Georgia Banking School May 5, 2016 Rachel Woods, CFA Associate, ALM SunTrust Robinson Humphrey Important Disclosure

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management I 2016 Georgia Banking School May 5, 2016 Rachel Woods, CFA Associate, ALM SunTrust Robinson Humphrey Important Disclosure

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 Raleigh A. Andy Trovillion Executive Vice President UMB Bank St. Louis, Missouri raleigh.trovillion@umb.com 800-433-5962 August 1, 2017 INTEREST RATE

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 Raleigh A. Andy Trovillion Executive Vice President UMB Bank St. Louis, Missouri raleigh.trovillion@umb.com 800-433-5962 August 1, 2017 INTEREST RATE

Developing Deposit Strategies for Rising Rates Session 2. Agenda

Developing Deposit Strategies for Rising Rates Session 2 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

Developing Deposit Strategies for Rising Rates Session 2 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

Credit Modeling, CECL, Concentration Risk, and Capital Stress Testing

Credit Modeling, CECL, Concentration Risk, and Capital Stress Testing Presented by Wilary Winn Douglas Winn, President Brenda Lidke, Director Frank Wilary, Principal Matt Erickson, Director September 26,

Credit Modeling, CECL, Concentration Risk, and Capital Stress Testing Presented by Wilary Winn Douglas Winn, President Brenda Lidke, Director Frank Wilary, Principal Matt Erickson, Director September 26,

Liquidity Management. 158 Route 206 Gladstone, NJ P: (908) Home FinPro, Inc.

Home FinPro, Inc.") Liquidity Management 158 Route 206 Gladstone, NJ 07934 P: (908) 234-9398 finpro@finpro.us www.finpro.us 0 Liquidity: you always have too much until you need it!! 1 Banks must take a holistic view of its

Liquidity Management 158 Route 206 Gladstone, NJ 07934 P: (908) 234-9398 finpro@finpro.us www.finpro.us 0 Liquidity: you always have too much until you need it!! 1 Banks must take a holistic view of its

Deposit Pricing in Rising Rates Session 2

Deposit Pricing in Rising Rates Session 2 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

Deposit Pricing in Rising Rates Session 2 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

BEST PRACTICES IN ASSET/LIABILITY MANAGEMENT. AMIfs Institute July 18, 2016 Monday Afternoon Session

BEST PRACTICES IN ASSET/LIABILITY MANAGEMENT AMIfs Institute July 18, 2016 Monday Afternoon Session 1 Agenda - Introduction to ALM Monday, July 18 Afternoon Best Practices in ALM Structuring the ALCO Process

BEST PRACTICES IN ASSET/LIABILITY MANAGEMENT AMIfs Institute July 18, 2016 Monday Afternoon Session 1 Agenda - Introduction to ALM Monday, July 18 Afternoon Best Practices in ALM Structuring the ALCO Process

Key ALM Assumptions for Rising Rates. Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends

CONNECT WITH US Key ALM Assumptions for Rising Rates Lisa Boylen Senior ALM Analyst February 21, 2018 Objectives Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends Planning

CONNECT WITH US Key ALM Assumptions for Rising Rates Lisa Boylen Senior ALM Analyst February 21, 2018 Objectives Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends Planning

Developing Deposit Strategies for Rising Rates Session 1. Agenda

Developing Deposit Strategies for Rising Rates Session 1 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

Developing Deposit Strategies for Rising Rates Session 1 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

Asset Liability Management for CU Boards The Basics of ALM Presented by: Frank Santucci - Managing Director ALM Services

Asset Liability Management for CU Boards The Basics of ALM Presented by: Frank Santucci - Managing Director ALM Services www.firstempire.com Frank Santucci - Managing Director ALM Services First Empire

Asset Liability Management for CU Boards The Basics of ALM Presented by: Frank Santucci - Managing Director ALM Services www.firstempire.com Frank Santucci - Managing Director ALM Services First Empire

Liquidity Basics Measuring and Managing Liquidity. Course Agenda

Liquidity Basics Measuring and Managing Liquidity David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Liquidity Basics Measuring and Managing Liquidity David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch. President\CEO FARIN & Associates, Inc.

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com Agenda Describe a functional definition

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com Agenda Describe a functional definition

Deposit Growth Strategies and Balance Sheet Management

Deposit Growth Strategies and Balance Sheet Management Presented by: Frank Santucci Managing Director ALM Services www.firstempire.com Frank Santucci - Managing Director ALM Services First Empire Securities,

Deposit Growth Strategies and Balance Sheet Management Presented by: Frank Santucci Managing Director ALM Services www.firstempire.com Frank Santucci - Managing Director ALM Services First Empire Securities,

Best Practices for Public Fund Investment Guidance and Performance

Best Practices for Public Fund Investment Guidance and Performance Deanne Woodring, CFA, MBA President, Senior Portfolio Advisor Luke Schneider, CFA Managing Director, Portfolio Advisor 1 FACTS: Rates

Best Practices for Public Fund Investment Guidance and Performance Deanne Woodring, CFA, MBA President, Senior Portfolio Advisor Luke Schneider, CFA Managing Director, Portfolio Advisor 1 FACTS: Rates

Introduction to Asset/Liability Management

Introduction to Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management and ALCO Meetings Defining

Introduction to Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management and ALCO Meetings Defining

How to Improve Liquidity

How to Improve Liquidity As Economic Conditions Change June 26, 2017 9:15 am Presented by: Joe Kennerson Managing Director Darling Consulting Group 260 Merrimac Street Newburyport, MA 01950 P: 978-463-0400

How to Improve Liquidity As Economic Conditions Change June 26, 2017 9:15 am Presented by: Joe Kennerson Managing Director Darling Consulting Group 260 Merrimac Street Newburyport, MA 01950 P: 978-463-0400

Callables/Structured Notes: Behind the Curtain Discussion with a Trading Desk

Callables/Structured Notes: Behind the Curtain Discussion with a Trading Desk GIOA 2019 Conference / March 21, 2019 George E.A. Barbar Senior Managing Director gbarbar@mesirowfinancial.com 2 Ever wonder

Callables/Structured Notes: Behind the Curtain Discussion with a Trading Desk GIOA 2019 Conference / March 21, 2019 George E.A. Barbar Senior Managing Director gbarbar@mesirowfinancial.com 2 Ever wonder

2015 Member Conference

2015 Member Conference Make the Loans Your Customers Want Brad Spears, VP/Director, Member Solutions Federal Home Loan Bank of Des Moines AGENDA Who is FHLB Des Moines? How can FHLB Des Moines help you?

2015 Member Conference Make the Loans Your Customers Want Brad Spears, VP/Director, Member Solutions Federal Home Loan Bank of Des Moines AGENDA Who is FHLB Des Moines? How can FHLB Des Moines help you?

RISING Rates Are Here Again Time to Celebrate or Danger Ahead?

Risk Management Strategy & Solutions RISING Rates Are Here Again Time to Celebrate or Danger Ahead? November 9, 2017 Frank Farone, Managing Director ffarone@darlingconsulting.com 2017 Darling Consulting

Risk Management Strategy & Solutions RISING Rates Are Here Again Time to Celebrate or Danger Ahead? November 9, 2017 Frank Farone, Managing Director ffarone@darlingconsulting.com 2017 Darling Consulting

ASSET/LIABILITY MANAGEMENT - YEAR 2

ASSET/LIABILITY MANAGEMENT - YEAR 2 Tying It All Together: Implementation of a Risk/Return Framework David W. Koch President & CEO FARIN Financial Risk Management Fitchburg, WI dkoch@farin.com 608-661-4217

ASSET/LIABILITY MANAGEMENT - YEAR 2 Tying It All Together: Implementation of a Risk/Return Framework David W. Koch President & CEO FARIN Financial Risk Management Fitchburg, WI dkoch@farin.com 608-661-4217

Leading Practices. Non-Maturity Deposit Modeling: June 26, :45 AM 12:45 PM. Presented by:

Non-Maturity Deposit Modeling: Leading Practices June 26, 2017 11:45 AM 12:45 PM Presented by: Thomas E Bowers, CFA Managing Director ZM Financial Systems, Inc. 1020 Southhill Drive, Ste. 200 Cary, North

Non-Maturity Deposit Modeling: Leading Practices June 26, 2017 11:45 AM 12:45 PM Presented by: Thomas E Bowers, CFA Managing Director ZM Financial Systems, Inc. 1020 Southhill Drive, Ste. 200 Cary, North

Developing a Funding Strategy for Rising Rates. Agenda

Developing a Funding Strategy for Rising Rates Thomas Farin Chairman tfarin@farin.com 1 Agenda Session 1: Lay out a best practices funding and pricing process? Identify internal issues impacting risk profile

Developing a Funding Strategy for Rising Rates Thomas Farin Chairman tfarin@farin.com 1 Agenda Session 1: Lay out a best practices funding and pricing process? Identify internal issues impacting risk profile

Positioning Your Portfolio as the Fed Tightens Monetary Policy

Positioning Your Portfolio as the Fed Tightens Monetary Policy Scott Wood Portfolio Strategist January 30, 2018 Securities offered through ProEquities, Inc., a registered Broker-Dealer and Member of FINRA

Positioning Your Portfolio as the Fed Tightens Monetary Policy Scott Wood Portfolio Strategist January 30, 2018 Securities offered through ProEquities, Inc., a registered Broker-Dealer and Member of FINRA

Credit Union Survival in a Challenging

Credit Union Survival in a Challenging Environment How to Make Balance Sheet Strategy Decisions with Confidence January 24, 2013 C O M P L E T E ALM SOLUTIONS Frank L. Farone Managing Director Darling

Credit Union Survival in a Challenging Environment How to Make Balance Sheet Strategy Decisions with Confidence January 24, 2013 C O M P L E T E ALM SOLUTIONS Frank L. Farone Managing Director Darling

10 th Annual GIOA Conference. Las Vegas, NV March 27, 2014

1 th Annual GIOA Conference Las Vegas, NV March 27, 214 This is not an offer to sell. FHLBank debt is not an obligation of or guaranteed by the United States and may not be offered or sold in any jurisdiction

1 th Annual GIOA Conference Las Vegas, NV March 27, 214 This is not an offer to sell. FHLBank debt is not an obligation of or guaranteed by the United States and may not be offered or sold in any jurisdiction

U. S. Economic Projections. GDP Core PCE Price Index Unemployment Rate (YE)

") The Federal Reserve will likely hold short-term interest rates steady until late 2015. U. S. Economic Projections 2014 2015 2014 2015 2014 2015 Stifel FI Strategy Group Forecast 2.5% 3.1% 1.4% 1.7% 6.4%

The Federal Reserve will likely hold short-term interest rates steady until late 2015. U. S. Economic Projections 2014 2015 2014 2015 2014 2015 Stifel FI Strategy Group Forecast 2.5% 3.1% 1.4% 1.7% 6.4%

Liquidity Basics Measuring and Managing Liquidity. Course Agenda

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

KeyCorp. Third Quarter 2017 Earnings Review. Don Kimble Chief Financial Officer. Beth E. Mooney Chairman and Chief Executive Officer.

KeyCorp Third Quarter 2017 Earnings Review October 19, 2017 Beth E. Mooney Chairman and Chief Executive Officer Don Kimble Chief Financial Officer FORWARD-LOOKING STATEMENTS AND ADDITIONAL INFORMATION

KeyCorp Third Quarter 2017 Earnings Review October 19, 2017 Beth E. Mooney Chairman and Chief Executive Officer Don Kimble Chief Financial Officer FORWARD-LOOKING STATEMENTS AND ADDITIONAL INFORMATION

Elevate Your Credit Union s Performance Now is NOT the Time for Business as Usual!

Risk Management Strategy & Solutions Elevate Your Credit Union s Performance Now is NOT the Time for Business as Usual! 2017 Darling Consulting Group, Inc. 260 Merrimac Street Newburyport, MA 01950 Tel:

Risk Management Strategy & Solutions Elevate Your Credit Union s Performance Now is NOT the Time for Business as Usual! 2017 Darling Consulting Group, Inc. 260 Merrimac Street Newburyport, MA 01950 Tel:

Doing More with Your Balance Sheet

Doing More with Your Balance Sheet John P. Biestman, CFA - VP/Senior Relationship Manager Brett L.A. Manning, CFA - VP/Director, Member Strategies October 27, 2015 Who is FHLB Des Moines? Current Balance

Doing More with Your Balance Sheet John P. Biestman, CFA - VP/Senior Relationship Manager Brett L.A. Manning, CFA - VP/Director, Member Strategies October 27, 2015 Who is FHLB Des Moines? Current Balance

SBA Securities A Strategic Addition to your Portfolio

Objectives History & Characteristics SBA Securities A Strategic Addition to your Portfolio Fred Eisel Chief Investment Officer Investment Guidelines & Analysis Examples Other considerations & best practices

Objectives History & Characteristics SBA Securities A Strategic Addition to your Portfolio Fred Eisel Chief Investment Officer Investment Guidelines & Analysis Examples Other considerations & best practices

What is a Dynamic ALCO

Managing a Dynamic ALCO Managing Earnings, Value and Liquidity Risks in your Decision Making Process Presented By: David Koch President & CEO dkoch@farin.com (608) 661-4217 1 What is a Dynamic ALCO Dynamic

Managing a Dynamic ALCO Managing Earnings, Value and Liquidity Risks in your Decision Making Process Presented By: David Koch President & CEO dkoch@farin.com (608) 661-4217 1 What is a Dynamic ALCO Dynamic

Lakhbir Hayre (212)

") Lakhbir Hayre (212) 783-6349 lhayre@sbi.com Debashis Bhattacharya (212) 783-768 bhattacharya@sbi.com Analysis of Hybrid ARMs Over the last few years, hybrids have become one of the most popular sectors

Lakhbir Hayre (212) 783-6349 lhayre@sbi.com Debashis Bhattacharya (212) 783-768 bhattacharya@sbi.com Analysis of Hybrid ARMs Over the last few years, hybrids have become one of the most popular sectors

Two Harbors Investment Corp.

Two Harbors Investment Corp. Webinar Series October 2013 Fundamental Concepts in Hedging Welcoming Remarks William Roth Chief Investment Officer July Hugen Director of Investor Relations 2 Safe Harbor

Two Harbors Investment Corp. Webinar Series October 2013 Fundamental Concepts in Hedging Welcoming Remarks William Roth Chief Investment Officer July Hugen Director of Investor Relations 2 Safe Harbor

Applied Loan Pricing

Applied Loan Pricing Session 1 Thomas Farin President tfarin@farin.com 1 Applied Loan Pricing Four Part Series Homework case assignments on iprice Loan Pricing Model (LoanEdge) between sessions and after

Applied Loan Pricing Session 1 Thomas Farin President tfarin@farin.com 1 Applied Loan Pricing Four Part Series Homework case assignments on iprice Loan Pricing Model (LoanEdge) between sessions and after

Lecture Materials LOAN PORTFOLIO MANAGEMENT YEAR 1

Lecture Materials LOAN PORTFOLIO MANAGEMENT YEAR 1 Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 August 10, 2016 GSB Credit Track

Lecture Materials LOAN PORTFOLIO MANAGEMENT YEAR 1 Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 August 10, 2016 GSB Credit Track

Conseco, Inc. Second Quarter 2008 Financial and Operating Results Presentation

Conseco, Inc. selected slides from our Second Quarter 2008 Financial and Operating Results Presentation (as filed in our Current Report on Form 8-K dated August 12, 2008) Key Debt Covenants CNO ($ millions)

Conseco, Inc. selected slides from our Second Quarter 2008 Financial and Operating Results Presentation (as filed in our Current Report on Form 8-K dated August 12, 2008) Key Debt Covenants CNO ($ millions)

KeyCorp Beth E. Mooney Don Kimble

KeyCorp Fourth Quarter 2017 Earnings Review January 18, 2018 Beth E. Mooney Chairman and Chief Executive Officer Don Kimble Chief Financial Officer FORWARD-LOOKING STATEMENTS AND ADDITIONAL INFORMATION

KeyCorp Fourth Quarter 2017 Earnings Review January 18, 2018 Beth E. Mooney Chairman and Chief Executive Officer Don Kimble Chief Financial Officer FORWARD-LOOKING STATEMENTS AND ADDITIONAL INFORMATION

Lecture Materials FUNDING

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 & Darryl Mataya SVP & Chief Development Officer FARIN

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 & Darryl Mataya SVP & Chief Development Officer FARIN

COLLATERALIZED LOAN OBLIGATIONS (CLO) Dr. Janne Gustafsson

Dr. Janne Gustafsson") COLLATERALIZED LOAN OBLIGATIONS (CLO) 4.12.2017 Dr. Janne Gustafsson OUTLINE 1. Structured Credit 2. Collateralized Loan Obligations (CLOs) 3. Pricing of CLO tranches 2 3 Structured Credit WHAT IS STRUCTURED

COLLATERALIZED LOAN OBLIGATIONS (CLO) 4.12.2017 Dr. Janne Gustafsson OUTLINE 1. Structured Credit 2. Collateralized Loan Obligations (CLOs) 3. Pricing of CLO tranches 2 3 Structured Credit WHAT IS STRUCTURED

Allowable Investments Under The Texas Public Funds Investment Act

Allowable Investments Under The Texas Public Funds Investment Act December 2017 Benjamin M. Clark SVP Portfolio Strategies Houston, TX Objectives of this Session Understand the General Requirements of

Allowable Investments Under The Texas Public Funds Investment Act December 2017 Benjamin M. Clark SVP Portfolio Strategies Houston, TX Objectives of this Session Understand the General Requirements of

Capital Speedboat Session 2. Charting your way through troubling waters FARIN & Associates Inc. Agenda

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

CALLABLE BONDS: FRIEND AND FOE GIOA INVESTMENT CONFERENCE George E.A. Barbar Mesirow Financial William M. Quinn, CFA FTN Financial

CALLABLE BONDS: FRIEND AND FOE GIOA INVESTMENT CONFERENCE 2017 George E.A. Barbar Mesirow Financial William M. Quinn, CFA FTN Financial GSE Callables Market Update Quick Refresh Why? and Why Not? Friend

CALLABLE BONDS: FRIEND AND FOE GIOA INVESTMENT CONFERENCE 2017 George E.A. Barbar Mesirow Financial William M. Quinn, CFA FTN Financial GSE Callables Market Update Quick Refresh Why? and Why Not? Friend

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 David Koch President & CEO FARIN Financial Risk Management Madison, Wisconsin dkoch@farin.com 608-661-4217 August 3, 2017 TYING IT ALL TOGETHER: IMPLEMENTATION

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 David Koch President & CEO FARIN Financial Risk Management Madison, Wisconsin dkoch@farin.com 608-661-4217 August 3, 2017 TYING IT ALL TOGETHER: IMPLEMENTATION

IS YOUR INSTITUTION AN INTEREST RATE RISK OUTLIER?

IS YOUR INSTITUTION AN INTEREST RATE RISK OUTLIER? What s at Risk? Examination teams from the OCC, FDIC, NCUA and other regulatory bodies are on the lookout for interest rate risk outliers. It s more important

IS YOUR INSTITUTION AN INTEREST RATE RISK OUTLIER? What s at Risk? Examination teams from the OCC, FDIC, NCUA and other regulatory bodies are on the lookout for interest rate risk outliers. It s more important

1Q 2015 Stockholder Supplement

1Q 2015 Stockholder Supplement May 6, 2015 Safe Harbor Notice This news release and our public documents to which we refer contain or incorporate by reference certain forward-looking statements which are

1Q 2015 Stockholder Supplement May 6, 2015 Safe Harbor Notice This news release and our public documents to which we refer contain or incorporate by reference certain forward-looking statements which are

CREDIT UNION INVESTMENT PRICE RISK

A CU*ANSWERS/CALLAHAN & ASSOCIATES WHITEPAPER OCTOBER 24, 2013 CREDIT UNION INVESTMENT PRICE RISK Jim Vilker Patrick Sickels and Chip Filson Expect NCUA and state examiners to stress credit union investment

A CU*ANSWERS/CALLAHAN & ASSOCIATES WHITEPAPER OCTOBER 24, 2013 CREDIT UNION INVESTMENT PRICE RISK Jim Vilker Patrick Sickels and Chip Filson Expect NCUA and state examiners to stress credit union investment

Federal Home Loan Bank of Des Moines. A Case for Diversifying the Right-Hand Side of the Balance Sheet

Federal Home Loan Bank of Des Moines A Case for Diversifying the Right-Hand Side of the Balance Sheet 1 Agenda 1. YIELD CURVE FUNDING STRATEGIES 2. BUILDING A CASE FOR FUNDING DIVERSIFICATION 3. BLENDED

Federal Home Loan Bank of Des Moines A Case for Diversifying the Right-Hand Side of the Balance Sheet 1 Agenda 1. YIELD CURVE FUNDING STRATEGIES 2. BUILDING A CASE FOR FUNDING DIVERSIFICATION 3. BLENDED

Goldman Sachs U.S. Financial Services Conference

Goldman Sachs U.S. Financial Services Conference Greg D. Carmichael Chairman, President & Chief Executive Officer December 4, 208 FORWARD-LOOKING STATEMENTS This communication contains forward-looking

Goldman Sachs U.S. Financial Services Conference Greg D. Carmichael Chairman, President & Chief Executive Officer December 4, 208 FORWARD-LOOKING STATEMENTS This communication contains forward-looking

Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office

Liquidity Analysis and Reporting Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office jboebel@profitstars.com Objectives Current trends Recent regulatory releases Consider a new approach Better

Liquidity Analysis and Reporting Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office jboebel@profitstars.com Objectives Current trends Recent regulatory releases Consider a new approach Better

Second Quarter 2018 Earnings Conference Call July 19, 2018

Second Quarter 2018 Earnings Conference Call July 19, 2018 WBS 2Q18 Earnings Highlights ($ in millions, except EPS data) Significant progress on our key strategic initiatives: 35 consecutive quarters of

Second Quarter 2018 Earnings Conference Call July 19, 2018 WBS 2Q18 Earnings Highlights ($ in millions, except EPS data) Significant progress on our key strategic initiatives: 35 consecutive quarters of

Third Quarter 2018 Earnings Presentation. October 31, 2018

Third Quarter 2018 Earnings Presentation October 31, 2018 Safe Harbor Statement NOTE: This presentation contains certain statements that are not historical facts and that constitute forward-looking statements

Third Quarter 2018 Earnings Presentation October 31, 2018 Safe Harbor Statement NOTE: This presentation contains certain statements that are not historical facts and that constitute forward-looking statements

The Mortgage-backed Securities Market: Risks, Returns and Replication. Evangelos Karagiannis Ph.D., CFA June 3, 2005

The Mortgage-backed Securities Market: Risks, Returns and Replication By Evangelos Karagiannis Ph.D., CFA June 3, 2005 Introduction The securitized mortgage-backed securities (MBS) market has experienced

The Mortgage-backed Securities Market: Risks, Returns and Replication By Evangelos Karagiannis Ph.D., CFA June 3, 2005 Introduction The securitized mortgage-backed securities (MBS) market has experienced

FHLB Symposium. Scott Buchta Head: Fixed Income Strategy. Tuesday, August 21st, 2018 Indianapolis Tuesday August 28 th, 2018 Grand Rapids

FHLB Symposium Scott Buchta Head: Fixed Income Strategy Tuesday, August 21st, 2018 Indianapolis Tuesday August 28 th, 2018 Grand Rapids FIStrategy@breancapital.com Table of Contents I. Housing Market Overview

FHLB Symposium Scott Buchta Head: Fixed Income Strategy Tuesday, August 21st, 2018 Indianapolis Tuesday August 28 th, 2018 Grand Rapids FIStrategy@breancapital.com Table of Contents I. Housing Market Overview

CREDIT UNION LIQUIDITY MANAGEMENT

Economic Forum October 3 5, CREDIT UNION LIQUIDITY MANAGEMENT Jeff Vorhees, Sr. ALM Analyst Topics of discussion Liquidity Risk Explained Liquidity Sources Liquidity Risk Management 1 Economic Forum October

Economic Forum October 3 5, CREDIT UNION LIQUIDITY MANAGEMENT Jeff Vorhees, Sr. ALM Analyst Topics of discussion Liquidity Risk Explained Liquidity Sources Liquidity Risk Management 1 Economic Forum October

Ellington Financial LLC (NYSE: EFC) Fourth Quarter 2016 Earnings Conference Call February 14, 2017

Fourth Quarter 2016 Earnings Conference Call February 14, 2017") Ellington Financial LLC (NYSE: EFC) Fourth Quarter 2016 Earnings Conference Call February 14, 2017 Important Notice Forward-Looking Statements This presentation contains forward-looking statements within

Ellington Financial LLC (NYSE: EFC) Fourth Quarter 2016 Earnings Conference Call February 14, 2017 Important Notice Forward-Looking Statements This presentation contains forward-looking statements within

Core Deposit Analytics Session 1

Core Deposit Analytics Session 1 Thomas A. Farin tfarin@farin.com David Koch dkoch@farin.com 1 Agenda Session 1 - Deposit Analytics Contractual vs. Actual Behavior Pricing Betas Decay Rates Surge Balances

Core Deposit Analytics Session 1 Thomas A. Farin tfarin@farin.com David Koch dkoch@farin.com 1 Agenda Session 1 - Deposit Analytics Contractual vs. Actual Behavior Pricing Betas Decay Rates Surge Balances

Loan Pricing Structure and the Nature of Interest Rates

Loan Pricing Structure and the Nature of Interest Rates S. Blake Scharlach Senior Vice President / Director of Capital Markets Sales TIB- The Independent BankersBank, N.A. S. Blake Scharlach Blake joined

Loan Pricing Structure and the Nature of Interest Rates S. Blake Scharlach Senior Vice President / Director of Capital Markets Sales TIB- The Independent BankersBank, N.A. S. Blake Scharlach Blake joined

Liquidity Risk Basics Measuring and Managing Liquidity. Dad, What is Liquidity & Where Does it Come From?

Liquidity Risk Basics Measuring and Managing Liquidity David Koch Chief Operating Officer FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Dad, What is Liquidity & Where Does it Come From? 2 1 Our

Liquidity Risk Basics Measuring and Managing Liquidity David Koch Chief Operating Officer FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Dad, What is Liquidity & Where Does it Come From? 2 1 Our

Core Deposit Analytics Session 1: Determining Core The Basics

Core Deposit Analytics Session 1: Determining Core The Basics Thomas A. Farin Chairman of the Board tfarin@farin.com 1 Building Blocks for Deposit Analysis Pricing Betas Decay Rates Surge Balance Identification

Core Deposit Analytics Session 1: Determining Core The Basics Thomas A. Farin Chairman of the Board tfarin@farin.com 1 Building Blocks for Deposit Analysis Pricing Betas Decay Rates Surge Balance Identification

MBS Market Strategies

U.S. Housing & the MBS Market - 2014 in Review and 2015 Outlook Contents Mortgage Activity and Housing - Refinance applications down 53% from the peak but recently increasing, a 500%+ surge in multifamily

U.S. Housing & the MBS Market - 2014 in Review and 2015 Outlook Contents Mortgage Activity and Housing - Refinance applications down 53% from the peak but recently increasing, a 500%+ surge in multifamily

Understanding Investments in Collateralized Loan Obligations ( CLOs )

") Understanding Investments in Collateralized Loan Obligations ( CLOs ) Disclaimer This document contains the current, good faith opinions of Ares Management Corporation ( Ares ). The document is meant for

Understanding Investments in Collateralized Loan Obligations ( CLOs ) Disclaimer This document contains the current, good faith opinions of Ares Management Corporation ( Ares ). The document is meant for

ALCO: The Fundamentals

ALCO: The Fundamentals Presented by: Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 ext. 4210 1 What Is Asset/Liability Management? Asset/Liability Management (ALM) is the process of planning,

ALCO: The Fundamentals Presented by: Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 ext. 4210 1 What Is Asset/Liability Management? Asset/Liability Management (ALM) is the process of planning,

Chapter 11. Valuation of Mortgage Securities. Mortgage Backed Bonds. Chapter 11 Learning Objectives TRADITIONAL DEBT SECURITY VALUATION

Chapter 11 Valuation of Mortgage Securities Chapter 11 Learning Objectives Understand the valuation of mortgage securities Understand cash flows from various types of mortgage securities Understand how

Chapter 11 Valuation of Mortgage Securities Chapter 11 Learning Objectives Understand the valuation of mortgage securities Understand cash flows from various types of mortgage securities Understand how

ALM Process & Strategies

ALM Process & Strategies Requirements for a Solid Foundation Chad McKeithen, Managing Director Duncan-Williams Inc. Al Forrester, CEO FiCast Data Corp Outline History of Interest Rate Risk Management How

ALM Process & Strategies Requirements for a Solid Foundation Chad McKeithen, Managing Director Duncan-Williams Inc. Al Forrester, CEO FiCast Data Corp Outline History of Interest Rate Risk Management How

Course Materials STRATEGICALLY MANAGING THE INVESTMENT PORTFOLIO FOR LONG-TERM PERFORMANCE

Course Materials STRATEGICALLY MANAGING THE INVESTMENT PORTFOLIO FOR LONG-TERM PERFORMANCE Raleigh A. Andy Trovillion Executive Vice President Investment Division UMB Bank St. Louis, Missouri raleigh.trovillion@umb.com

Course Materials STRATEGICALLY MANAGING THE INVESTMENT PORTFOLIO FOR LONG-TERM PERFORMANCE Raleigh A. Andy Trovillion Executive Vice President Investment Division UMB Bank St. Louis, Missouri raleigh.trovillion@umb.com

Investing for Small Governments

Tuesday MAY, 23 2017 10:20AM 12PM Investing for Small Governments MODERATOR SPEAKERS Al Rolek Finance Director, River Falls, WI John Grady Managing Director, Public Trust Advisors Darrel Thomas Assistant

Tuesday MAY, 23 2017 10:20AM 12PM Investing for Small Governments MODERATOR SPEAKERS Al Rolek Finance Director, River Falls, WI John Grady Managing Director, Public Trust Advisors Darrel Thomas Assistant

MBS Market Update: Reconsidering the Fed

Title Presenter Date MBS Market Update: Reconsidering the Fed Walt Schmidt, CFA March, 214 Four Main Themes (While We Wait for Future) The Fed has BEGUN to unwind extraordinary assistance. Certainty about

Title Presenter Date MBS Market Update: Reconsidering the Fed Walt Schmidt, CFA March, 214 Four Main Themes (While We Wait for Future) The Fed has BEGUN to unwind extraordinary assistance. Certainty about

October 16, Managing Your Investments in a Rising Rate Environment. Danny Nelson Sr. Managing Consultant. Kathleen Edwards Senior Analyst

October 16, 2013 Danny Nelson Sr. Managing Consultant Kathleen Edwards Senior Analyst Managing Your Investments in a Rising Rate Environment 222 North LaSalle Suite 910 Chicago, IL 60601 www.pfm.com Running

October 16, 2013 Danny Nelson Sr. Managing Consultant Kathleen Edwards Senior Analyst Managing Your Investments in a Rising Rate Environment 222 North LaSalle Suite 910 Chicago, IL 60601 www.pfm.com Running