Capital Speedboat Session 2. Charting your way through troubling waters FARIN & Associates Inc. Agenda

|

|

|

- Simon Andrews

- 5 years ago

- Views:

Transcription

1 Capital Speedboat Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building Scenarios Probability vs. Stress Cross Risk Considerations Setting Capital Goals Determine Impact of Stress Test Contingency Capital Plan Incorporating Stress Scenarios with Business Plan 2 1

2 STRESS TESTING DEFINED 3 OCC Community Bank Stress Testing Issued 10/18/2012 Lays Out Supervisory Expectations Primarily focused on Credit Stress Testing Generally Stress Tests Should Lay Out Plausible What If Questions Assess Impact of What-If Incorporate Results into Institution Risk Management Process If Major Problems are Uncovered at the Basic Level, Additional Detailed Analysis May be Necessary 4 2

3 FDIC Stress Testing - Defined Stress testing is a forward-looking quantitative evaluation of stress scenarios that could impact a banking institution s financial condition and capital adequacy. These risk assessments are based on assumptions about potential adverse external events, such as changes in real estate or capital markets prices, or unanticipated deterioration in a borrower s repayment capacity. Stress tests are most useful when customized to reflect the characteristics particular to the institution and its market area, and can be used to evaluate credit risk in the overall loan portfolio, segments of portfolios, or individual loans. Stress tests also can be used to evaluate whether existing financial (such as capital and liquidity) and operational (such as staffing and internal systems) resources are sufficient to withstand an economic downturn or unexpected event. Focus of all Regulatory Documents is on CRE Lending though can be applied universally in Top Down Testing 5 5 Key Stress Testing Principles: 1. The framework should include activities and exercises that are tailored to and sufficiently capture the organization's material exposures, activities and risks. 2. An effective stress testing framework employs multiple conceptually sound stress testing activities and approaches 3. An effective stress testing framework is forward-looking and flexible 4. Stress test results should be clear, actionable, well supported, and inform decision-making. 5. Strong governance and effective internal controls help ensure that the framework contains core elements, from clearly defined stress testing objectives to recommended ones. 6 3

4 Two Approaches to Stress Testing Sensitivity Analysis: refers to assessment of risk when certain variables, parameters, and inputs are "stressed" or "shocked." Unlike scenario analysis, this is performed without an explicit underlying reason or narrative in order to explore what occurs under a range of inputs and at extreme or highly adverse levels. The guidance state: "It can help to assess a combined impact on several variables, parameters, factors, or drivers. For example, an organization could better understand the impact on its credit losses from a combined increase in default rates and a decrease in collateral values...an organization can also explore the impact of highly adverse capitalization rates, declines in net operating income, and reductions in collateral when evaluating risk from CRE exposure." 7 Two Approaches to Stress Testing Scenario Analysis: a technique where you apply a historical or hypothetical scenario to assess the impact of various events and circumstances, including the most extreme situations. Examples include severe recession, failure of a major counterparty, loss of major clients, localized economic downturn, or a sudden change in interest rates brought about by unfavorable inflation developments. This is what we tie into other ALCO risks we monitor 8 4

5 Sensitivity vs. Scenario Testing: A Baking (not banking) Analogy When Baking a cake, Directions Tell you Bake in a 350 degree oven for 30 Minutes If you are in High Altitude, bake 22 minutes at 325 degrees Scenario Test: 2 scenarios based on altitude Sensitivity Test Altitude was tested over time to determine changes in scenario needed. Assumptions changed based on tracking and control But, what is assumed is that when you set your oven to 350 degrees, the oven ACTUALLY gets to 350 What if your oven is off by 10% (35 degrees hot or cold)? Scenario and Sensitivity testing combine known relationships with different potential environments and assumptions. 9 Consider this Stress Testing is to be done both within a risk area AND across risk areas. (Inter-related risks) So, where do we use sensitivity testing vs. scenario testing in Capital Planning? Sensitivity Testing: What key variables have significant impact on results. Run first in the silo How confident are the assumptions? What are the outer boundaries? Scenario Testing: Run across Silos to see combined effect on performance Stress scenarios with sensitivity tests for planning Scenario & Sensitivity Testing: Assess Combined Plan results with major sensitivity assumptions 10 5

6 Business Planning Scenarios Sensitivity Test: Scenario A Rates Funding sources & costs Credit Quality Sensitivity Test: Scenario B Projected Growth 11 SILO TESTING RISK AREAS 12 6

7 Sensitivity Testing Within Silos Typical Sensitivity Testing Within Silos Interest Rate Risk Examples What If Prepayment Speeds are wrong? Test with Faster/Slower Speeds Assumes current model is not accurately modeling performance No indication on why the speeds would change. What is the cause? Liquidity Risk Example: What if runoff factors are too low. Run at 2x and recalculate ratio What do I do then? What if Securities Can t be sold? 13 Silo Stress Testing Example of Sensitivity Testing the loss ratio impact on earnings Note that all of previous example slides (session 1) showed the estimated impact of changes in a single key variable (loss ratio) Similar testing in place for other key risk silos Liquidity Risk Liquidity Coverage Ratio (LCR) or Net Stable Funding Ratio (NSFR) Interest Rate Risk Impact of Immediate Movement in Rates on a Projects Static Balance Sheet (Income at Risk) Change key variable on Non-maturity balances and retest results 14 7

8 Sensitivity Testing: Liquidity LCR Test Short Term, Asset Based Needs Modify variables for LCR Test Loan Repay/Prepayment Investment Repay/Prepayment Stable Non-Maturity Deposit Sensitivities Less Stable NMD Sensitivities Stable Maturing CD Runoff Less Stable CD runoff Maturing Wholesale Payoff Amounts Draws on Existing Lines/Letter of Credit Run Testing Across 2-4 tests Sensitivity Link to scenarios? 15 Sensitivity Testing: Liquidity Developed a series of potential factors given an Economic projection 16 8

9 Sensitivity Testing: Liquidity Given potential changes in LCR Risk Factors, short term liquidity appears to be OK Remember this is a point in time analysis Ideally, measure this out 3, 6 and/or 12 months 17 Interest Rate Risk Stress Testing Traditional IRR Testing Run interest rate shocks/ramps/forecasts Test Margin performance for volatility Make adjustments to plan for high volatility levels Balance sheet projections mostly static Testing the existing balance sheet (Bologna!) Assumed no change in volumes for all rates! EVE tests mostly done on prior balance sheets Some forward looking EVE being done by more progressive ALCOs 18 9

10 Static Interest Rate Risk: Income With immediate movements in rates, institution earns more until rates are up by 300 bp or more how would you explain that change in direction? With this test we see how a major move in all rates impacts the future earnings assuming no change in balance sheet size or mix What s missing is how credit risk would be impacted if rates moved and/or liquidity sources 19 Static Interest Rate Risk: Current EVE Minimal volatility Implies we aren t going to see large swings in earnings regardless of rates movements. We are matched

11 Benefits: Sensitivity Testing Allows all to understand how critical assumptions can move the findings Easy to implement Disadvantages: No Enterprise-wide impact Not a realistic approach to assessing institutional risks 21 Building Stress Tests in the Speed Boat First, this is a model where earnings are an INPUT to the plan, not a calculated level Good to help establish goals and risks True ALM/Forecasting Models tell us if we can meet the goals Building the Stress Test: Credit Loss Assumptions Step 1: Stratify Loans by Category/Type Step 2: Determine Loss Ratio for Stress Test Step 3: Apply Loss Ratio(s) by Category/Type and Future Period to Projected Loan Balances Can Modify Loss Rates Over Time Step 4: 22 11

12 Stress Testing in the Speedboat Projections from Plan Goals Note that corresponding Asset Growth and Balance Sheet Mix May Change with Scenario 23 Stress Testing in the Speedboat Loan Call Report Classifications Note that corresponding Asset Growth and Balance Sheet Mix May Change with Scenario 24 12

13 Stress Testing in the Speedboat Enter Loss Rates for Scenario Enter Projected Mix % of Loans by Type Note that corresponding Asset Growth and Balance Sheet Mix May Change with Scenario 25 Stress Testing in the Speedboat Enter Tax Rate and Annual PLL Expense in Base Plan Note that corresponding Asset Growth and Balance Sheet Mix May Change with Scenario 26 13

14 Stress Testing in the Speedboat Enter addition to ALLL from Loan Stress Test Enter planned dividends Note that corresponding Asset Growth and Balance Sheet Mix May Change with Scenario 27 Stress Testing in the Speedboat Enter addition to ALLL from Loan Stress Test Bottom of sheet shows Stressed Capital Ratio on all 4 measures Compare to Base Plan Results without stress How big is the difference? Is that the buffer we need? 28 14

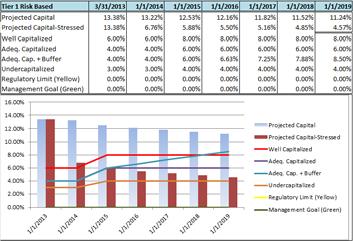

15 Capital Ratio Comparisons 29 BUILDING A BETTER STRESS TEST 30 15

16 Baseline Projections: Build Your Capital Plan General Economic Forecasts Base Case Key Forecast Assumptions (60%) Fiscal Policy Assumptions: Discretionary Spending. real nondefense federal government spending falls 1.7% in calendar 2012 and 2.6% in 2013 as budget cuts bite. Fiscal Policy: Expiring Stimulus. assume 2% payroll tax cut and emergency unemployment insurance benefits are extended for 2013, and phased out over several years, rather than disappearing overnight. Oil Prices Housing Demand Add in relevant parts to your planning Local Market & Institution Assumptions Asset Growth Assumed at 2-3% Loan Growth sluggish 3-5% Net Deposits growing to replace maturing Nonaccrual remaining at 5% for year 1 & 2 of plan Institution Capital Plan Goals Maintain > 7% Capital/Asset Increase ROA Define Alternative Business Plan Scenarios Economic Recovery Scenario Triggers: Improving job market Stable oil prices Housing market recovery Local business bring back 3 rd shift, increase production Impact on Capital Plan Anticipate Interest Rates increase in 6-12 months dramatically (Global Insight High Rate Forecast) Expect 10% increase in loan originations Expect non-accruals to rise to 10% before dropping late in Yr. 2 of the plan Anticipate a 5-10% runoff in existing non-maturity deposits in Yr

17 Building Stress Scenarios Create Stress Test Scenarios Must be based on potential risks in your situation Move beyond economic focus of business plan and stress key variables. Base tests on Balance sheet concentrations Local Market Risks Non-financial Risks Modify Test Relationships Duration Key impacts on other business lines Breaking of old relationships Review Results of Stress Test to Business Plan How much risk is in the plan? 33 Documenting Stress Scenarios Step 1: Describe the Scenario: Clear depiction of the issues that might cause impact on current and planned business plan objectives Step 2: Describe the Events and Impacts of Scenario on Business Plan Detailed description of the issues, events and stress impacts Silo based stress testing may drive the risk factors used Step 3: Model Results of Events on Business Plan Step 4: Review Impact and Build Potential Management Plans 34 17

18 Sample Stress Scenarios Major Loss of Key Employer Due to Weak Housing Sector: This scenario is based on a severe downturn in the local/national economy that results in significant drops in property values, employment, increased delinquency and charge-offs in the loan portfolio and possibly reductions in available wholesale funding sources Step 2: Describe the Events and Impacts of Scenario on Business Plan Anticipate increase in loan losses and delinquency to build over months Anticipate an additional outflow of non-maturity deposits of 5% in 12 months Expect a reduction in loan applications/originations We anticipate that the risk is valid in ALL of the GI Rate Forecasts 35 Alternative Scenarios Once you have defined the major events to model and assigned various assumption changes, Run all scenarios in the ALM model Knock out the irrelevant combinations to arrive at a better risk position Compare the results of the combined risk assessment to the stand alone 36 18

19 Step 3 - Comparing Scenarios: Reporting Time Series Trends Compares the key metrics over the forecast horizon Consistent with Capital Planning Goals ROA All 4 Capital Ratios Growth Rates Balance Sheet Mix Others Must watch all risk measures Interest Rate Risk Earnings at Risk Value at Risk Liquidity Risk Asset Based Cash Flow Credit Risk Decision Matrix: A good overview of relative performance between stress scenarios and Business Plan results Compares the financial results for Various measures and Projections down the left Across Various Interest Rate Projections (Economic Projections) along the top Key is to only focus on the combinations of results that are matches between forecast assumptions and rate/economic projections 37 Step 3: Reviewing Results Note that the Common Equity declined in both plans. Base plan results (solid lines) show slightly more capital if rates rise. Stress results (dashed lines) show lower results in all rates 38 19

20 Step 3: Reviewing Results Note that the Total Risk based declines below Well Capitalized levels, with stress costing roughly 25 bp more in worse case scenario. However, they remain well above Adequately Capitalized until the buffer is added at later date How much capital is enough? 39 Stress Testing Liquidity Cash Flow Gap The scenario above shows book capital declining below 7% within 2 years and a full 83 bp below base forecast Note the impact on ROA/ROE is inverted ROE = ROA * Leverage 40 20

21 Stress Testing Liquidity Cash Flow Gap Stress testing liquidity gap for economic recovery shows this institution dropping to -30.3% Liquidity Gap/Assets by End of Yr 2. What is ALCO s next move on this information? So we hold 30% of assets more in capital? We burned through available borrowing and saleable securities? 41 Alternative Scenarios Decision Matrix The following dashboard concept presents the Base Business Plan with each individual risk component, then the combined effect Incorporates all changes into financial results combined Green shaded areas are good combinations Red are not meant for review Note that these values are 1 year forecast results

22 Alternative Scenarios Decision Matrix This reporting offers opportunity to see impact of stress on many risks. 1 Yr Impact on Interest Rate Risk No significant difference in Margin volatility between pre/post stress After PLL levels decline due to increasing PLL expense building in Yr. 1 Cost of credit stress in yr 1 on Margin is less than 10 bp under nonparallel movements in rates Under Immediate rate movements, cost rises to roughly 10bp due to difference in asset size Under stress, assets actually increase as non-performing loans build up and stay on books increasing denominator for NIM 43 Alternative Scenarios Decision Matrix Let s Review Capital Levels at 12 Months Out Capital levels for the 3 ratios shown stay above Well Capitalized levels inside 1 year Stress Test hits during year 1 Illustrates need for minimum of 2 year horizon for forecasts If we are attempting to determine how much more capital we need to cover risks, is this the right way to measure, even if we looked at 2 year forecasts? 44 22

23 Looking out Long In order to evaluate the long-term effect of the risks, we believe the forward looking EVE runs should take place on valid combinations of risk parameters and rate projections Let s compare 1 year results GI High Forecast With and Without the combined stress events If we have real assumptions about growth and risk, is this a better measure of hedging needed? 45 Forecast EVE Results Under Traditional Business Plan Test Up 200, 300 and 400 bp EVE Ratio near minimum levels Stressed Plan incorporates effects of Income Projections on real capital ratio and future EVE Short on EVE by 2.11% in up 400 bp shock Would it make sense for the shop to hold at least an additional capital buffer of 2% based on EVE results? 46 23

24 Putting This To Work First, define business plan scenarios for multiple economic events Basis for dynamic management of the real business plan Movement away from static balance sheet Second, define stress events based on your concentrations and business plan What are the major vulnerabilities How bad could things get even if you don t think they will? How quickly could it happen and what might drive it Note we are focusing on the financial management risk areas, other risks like reputation risk from fraud or event risk from a natural disaster could be problematic. 47 Putting This To Work Third, assess the capital plan (macro level) with the stress events to see how plans and goals are impacted Fourth, run the plans through ALM model to determine impact of stress on earnings, capital & growth Run sensitivity testing within the scenarios Determine Buffer for capital ratio above regulatory minimums Based on Results, refine capital plan or set in place contingency plans for maintaining capital goals 48 24

Enterprise Risk Management and the ALCO Process

Enterprise Risk Management and the ALCO Process Session 1: Gathering the Parts David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 ext 4217 Agenda Session 1 Overview of ERM Evolution of ERM

Enterprise Risk Management and the ALCO Process Session 1: Gathering the Parts David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 ext 4217 Agenda Session 1 Overview of ERM Evolution of ERM

Credit Risk Management and the ALCO Process

Credit Risk Management and the ALCO Process David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Definition: Asset/Liability Management asset/liability management is the processes of

Credit Risk Management and the ALCO Process David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Definition: Asset/Liability Management asset/liability management is the processes of

Credit Risk Management and the ALCO Process. Asset/Liability Management

Credit Risk Management and the ALCO Process David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Asset/Liability Management Definition: asset/liability management is the processes of

Credit Risk Management and the ALCO Process David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Asset/Liability Management Definition: asset/liability management is the processes of

Liquidity Risk Managing an Effective Program Session #2. Course Agenda

Liquidity Risk Managing an Effective Program Session #2 David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Course Agenda Understanding Nature of Liquidity Asset based vs. Total Liquidity

Liquidity Risk Managing an Effective Program Session #2 David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Course Agenda Understanding Nature of Liquidity Asset based vs. Total Liquidity

What Is Asset/Liability Management?

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 David Koch President & CEO FARIN Financial Risk Management Madison, Wisconsin dkoch@farin.com 608-661-4217 August 3, 2017 TYING IT ALL TOGETHER: IMPLEMENTATION

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 2 David Koch President & CEO FARIN Financial Risk Management Madison, Wisconsin dkoch@farin.com 608-661-4217 August 3, 2017 TYING IT ALL TOGETHER: IMPLEMENTATION

Liquidity Basics Measuring and Managing Liquidity

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

ALCO: The Fundamentals

ALCO: The Fundamentals Presented by: Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 ext. 4210 1 What Is Asset/Liability Management? Asset/Liability Management (ALM) is the process of planning,

ALCO: The Fundamentals Presented by: Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 ext. 4210 1 What Is Asset/Liability Management? Asset/Liability Management (ALM) is the process of planning,

ASSET/LIABILITY MANAGEMENT - YEAR 2

ASSET/LIABILITY MANAGEMENT - YEAR 2 Tying It All Together: Implementation of a Risk/Return Framework David W. Koch President & CEO FARIN Financial Risk Management Fitchburg, WI dkoch@farin.com 608-661-4217

ASSET/LIABILITY MANAGEMENT - YEAR 2 Tying It All Together: Implementation of a Risk/Return Framework David W. Koch President & CEO FARIN Financial Risk Management Fitchburg, WI dkoch@farin.com 608-661-4217

What is a Dynamic ALCO

Managing a Dynamic ALCO Managing Earnings, Value and Liquidity Risks in your Decision Making Process Presented By: David Koch President & CEO dkoch@farin.com (608) 661-4217 1 What is a Dynamic ALCO Dynamic

Managing a Dynamic ALCO Managing Earnings, Value and Liquidity Risks in your Decision Making Process Presented By: David Koch President & CEO dkoch@farin.com (608) 661-4217 1 What is a Dynamic ALCO Dynamic

Liquidity Basics Measuring and Managing Liquidity. Course Agenda

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Liquidity Basics Measuring and Managing Liquidity Urum Urumoglu Senior Consultant Urum@farin.com 800-236-3724 x4210 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

ALCO: The Fundamentals

ALCO: The Fundamentals Presented by: David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 ext. 4217 1 What Is Asset/Liability Management? Asset/Liability Management (ALM) is the process of planning,

ALCO: The Fundamentals Presented by: David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 ext. 4217 1 What Is Asset/Liability Management? Asset/Liability Management (ALM) is the process of planning,

Liquidity Basics Measuring and Managing Liquidity. Course Agenda

Liquidity Basics Measuring and Managing Liquidity David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Liquidity Basics Measuring and Managing Liquidity David Koch Chief Operating Officer dkoch@farin.com 800-236-3724 x4217 1 Course Agenda Understanding Nature of Liquidity Definition of Liquidity Traditional

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Urum Urumoglu Senior Consultant FARIN & Associates, Inc.. Urum@farin.com 1 Session Overview Session 1 Define Interest Rate Risk IRR

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Urum Urumoglu Senior Consultant FARIN & Associates, Inc.. Urum@farin.com 1 Session Overview Session 1 Define Interest Rate Risk IRR

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Presented By: David W. Koch Chief Operating Officer FARIN & Associates, Inc.. dkoch@farin.com 1 Session Overview Session 1 Define

Interest Rate Risk Basics Measuring & Managing Earnings & Value at Risk Presented By: David W. Koch Chief Operating Officer FARIN & Associates, Inc.. dkoch@farin.com 1 Session Overview Session 1 Define

The Regulatory Focus on Interest Rate Risk: What to Expect and How to Comply

The Regulatory Focus on Interest Rate Risk: What to Expect and How to Comply Conference Call will begin at 10:00am CT, lines open at 10:50am CT Audio: 855-749-4750 Access Code: 920 722 897 # You can also

The Regulatory Focus on Interest Rate Risk: What to Expect and How to Comply Conference Call will begin at 10:00am CT, lines open at 10:50am CT Audio: 855-749-4750 Access Code: 920 722 897 # You can also

Liquidity Risk Basics Measuring and Managing Liquidity. Dad, What is Liquidity & Where Does it Come From?

Liquidity Risk Basics Measuring and Managing Liquidity David Koch Chief Operating Officer FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Dad, What is Liquidity & Where Does it Come From? 2 1 Our

Liquidity Risk Basics Measuring and Managing Liquidity David Koch Chief Operating Officer FARIN & Associates, Inc. dkoch@farin.com 608-661-4217 1 Dad, What is Liquidity & Where Does it Come From? 2 1 Our

THC Asset-Liability Management (ALM) Insight Issue 2

Insight Issue 2") Optimize Your Liquidity Position by Identifying Your Risk Capacity key words: risk capacity, uses and sources of funds, liquidity coverage ratio, contingency funding plan quantitative assessment, THC Asset-Liability

Optimize Your Liquidity Position by Identifying Your Risk Capacity key words: risk capacity, uses and sources of funds, liquidity coverage ratio, contingency funding plan quantitative assessment, THC Asset-Liability

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS June 13, 2013 Presented By Mike Ensweiler Director of Business Development Agenda General duties of directors What questions should directors be able to answer

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS June 13, 2013 Presented By Mike Ensweiler Director of Business Development Agenda General duties of directors What questions should directors be able to answer

Capital Planning Session 3

Capital Planning Session 3 Dave Koch - COO dkoch@farin.com Tom Farin - CEO tfarin@farin.com Farin & Associates, Inc. 1 Capital Planning Webinar Charting your way through troubling waters 2 1 Capital Planning

Capital Planning Session 3 Dave Koch - COO dkoch@farin.com Tom Farin - CEO tfarin@farin.com Farin & Associates, Inc. 1 Capital Planning Webinar Charting your way through troubling waters 2 1 Capital Planning

Demystifying the New Liquidity Requirements

Your State Association Presents Demystifying the New Liquidity Requirements Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the broadcast.

Your State Association Presents Demystifying the New Liquidity Requirements Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the broadcast.

Introduction to Asset/Liability Management

Introduction to Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management and ALCO Meetings Defining

Introduction to Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management and ALCO Meetings Defining

Developing a Funding Strategy for Rising Rates. Agenda

Developing a Funding Strategy for Rising Rates Thomas Farin Chairman tfarin@farin.com 1 Agenda Session 1: Lay out a best practices funding and pricing process? Identify internal issues impacting risk profile

Developing a Funding Strategy for Rising Rates Thomas Farin Chairman tfarin@farin.com 1 Agenda Session 1: Lay out a best practices funding and pricing process? Identify internal issues impacting risk profile

Core Deposit Analytics Session 2: Beyond Basics - Applying Results

Core Deposit Analytics Session 2: Beyond Basics - Applying Results David Koch President/CEO dkoch@farin.com 800-236-3724 ext. 4217 1 Impact of Right Assumptions on ALCO Decision Making CORE DEPOSIT ASSUMPTIONS

Core Deposit Analytics Session 2: Beyond Basics - Applying Results David Koch President/CEO dkoch@farin.com 800-236-3724 ext. 4217 1 Impact of Right Assumptions on ALCO Decision Making CORE DEPOSIT ASSUMPTIONS

RISING Rates Are Here Again Time to Celebrate or Danger Ahead?

Risk Management Strategy & Solutions RISING Rates Are Here Again Time to Celebrate or Danger Ahead? November 9, 2017 Frank Farone, Managing Director ffarone@darlingconsulting.com 2017 Darling Consulting

Risk Management Strategy & Solutions RISING Rates Are Here Again Time to Celebrate or Danger Ahead? November 9, 2017 Frank Farone, Managing Director ffarone@darlingconsulting.com 2017 Darling Consulting

Market and Liquidity Risk Examination Techniques. Federal Reserve System

Market and Liquidity Risk Examination Techniques Federal Reserve System Review: Linking Risk Hypothesis to Exams High Risk Weak RM Process High Exposure High Risk Strong RM Process Weak RM Process Strong

Market and Liquidity Risk Examination Techniques Federal Reserve System Review: Linking Risk Hypothesis to Exams High Risk Weak RM Process High Exposure High Risk Strong RM Process Weak RM Process Strong

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch. President\CEO FARIN & Associates, Inc.

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com Agenda Describe a functional definition

BASICS OF LIQUIDITY WHAT IS IT? WHAT RISKS DOES IT CONTRIBUTE TO YOUR CAPITAL PLAN & FUNDING NEEDS? David Koch President\CEO FARIN & Associates, Inc. dkoch@farin.com Agenda Describe a functional definition

Georgia Banking School

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management II 2017 Georgia Banking School May 10, 2017 Joel Updegraff Managing Director, ALM SunTrust Robinson Humphrey Important Disclosure

GEORGIA BANKERS ASSOCIATION Georgia Banking School Asset/Liability Management II 2017 Georgia Banking School May 10, 2017 Joel Updegraff Managing Director, ALM SunTrust Robinson Humphrey Important Disclosure

Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office

Liquidity Analysis and Reporting Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office jboebel@profitstars.com Objectives Current trends Recent regulatory releases Consider a new approach Better

Liquidity Analysis and Reporting Jerry Boebel, CFA Business Consultant ProfitStars Omaha Office jboebel@profitstars.com Objectives Current trends Recent regulatory releases Consider a new approach Better

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million. May Ce document est également disponible en français.

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

Interest Rate Risk Measurement

Interest Rate Risk Measurement August 10, 2018 Ricky Brillard, CPA Senior Vice President Strategic Solutions Group 901-762-6415 rbrillard@viningsparks.com 1 Outline Trends Impacting Bank Balance Sheets

Interest Rate Risk Measurement August 10, 2018 Ricky Brillard, CPA Senior Vice President Strategic Solutions Group 901-762-6415 rbrillard@viningsparks.com 1 Outline Trends Impacting Bank Balance Sheets

2018 Mid-Cycle Stress Test Disclosure

DB USA Corporation 2018 Mid-Cycle Stress Test Disclosure TABLE OF CONTENTS 1 OVERVIEW AND REQUIREMENTS... 3 1.1 Overview and Description of DB USA Corp. s Severely Adverse Scenario... 4 2 RISK TYPES...

DB USA Corporation 2018 Mid-Cycle Stress Test Disclosure TABLE OF CONTENTS 1 OVERVIEW AND REQUIREMENTS... 3 1.1 Overview and Description of DB USA Corp. s Severely Adverse Scenario... 4 2 RISK TYPES...

Your State Association Presents. Interest Rate Risk: What Does th Future Hold? Program Materials

Your State Association Presents Interest Rate Risk: What Does th Future Hold? Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the

Your State Association Presents Interest Rate Risk: What Does th Future Hold? Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the

PNC Bank, NA. Board Report. June 30, Pittsburgh, PA. A/L BENCHMARKS Standards for Asset/Liability Management

A/L BENCHMARKS Standards for Asset/Liability Management Board Report PNC Bank, NA June 30, 2006 Olson Research Associates, Inc. 10290 Old Columbia Road, Columbia, MD 21046 Phone: 888-657-6680 Web: http://www.olsonresearch.com

A/L BENCHMARKS Standards for Asset/Liability Management Board Report PNC Bank, NA June 30, 2006 Olson Research Associates, Inc. 10290 Old Columbia Road, Columbia, MD 21046 Phone: 888-657-6680 Web: http://www.olsonresearch.com

Advanced Asset/Liability Management

Advanced Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management Summary Developing Assumptions

Advanced Asset/Liability Management WBA BOLT Summer Leadership Summit June 14, 2018 Presented by: Marc Gall, Vice President mgall@bokf.com 1 Agenda Asset/Liability Management Summary Developing Assumptions

Revised Interest Rate Risk Supervision Effective January 1, 2017

Revised Interest Rate Risk Supervision Effective January 1, 2017 Key Changes to NCUA s interest rate risk supervision: 1. Development of Interest Rate Risk Review Procedures Workbook 2. Updated IRR tolerance

Revised Interest Rate Risk Supervision Effective January 1, 2017 Key Changes to NCUA s interest rate risk supervision: 1. Development of Interest Rate Risk Review Procedures Workbook 2. Updated IRR tolerance

2015 BOK Financial Corporation and BOKF, NA DFAST Public Disclosure

2015 BOK Financial Corporation and BOKF, NA DFAST Public Disclosure BOK Financial Corporation and BOKF, NA are required to perform annual company-run capital stress testing pursuant to the Dodd-Frank Wall

2015 BOK Financial Corporation and BOKF, NA DFAST Public Disclosure BOK Financial Corporation and BOKF, NA are required to perform annual company-run capital stress testing pursuant to the Dodd-Frank Wall

Core Deposit Analytics Session 1

Core Deposit Analytics Session 1 Thomas A. Farin tfarin@farin.com David Koch dkoch@farin.com 1 Agenda Session 1 - Deposit Analytics Contractual vs. Actual Behavior Pricing Betas Decay Rates Surge Balances

Core Deposit Analytics Session 1 Thomas A. Farin tfarin@farin.com David Koch dkoch@farin.com 1 Agenda Session 1 - Deposit Analytics Contractual vs. Actual Behavior Pricing Betas Decay Rates Surge Balances

Deposit Pricing in Rising Rates Session 1. Three Part Series

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

ALM Strategy in the Current Rate Environment. Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends

ALM Strategy in the Current Rate Environment Lisa Boylen Senior ALM Analyst December 12, 2018 1 Objectives Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends Lessons Learned

ALM Strategy in the Current Rate Environment Lisa Boylen Senior ALM Analyst December 12, 2018 1 Objectives Current Landscape Interest Rates CU Balance Sheet & Financial Performance Trends Lessons Learned

PEOPLE'S UNITED BANK, N.A Dodd-Frank Act Stress Test (DFAST) Disclosure. June 18, 2015

Disclosure. June 18, 2015") PEOPLE'S UNITED BANK, N.A. 2015 Dodd-Frank Act Stress Test (DFAST) Disclosure June 18, 2015 1. Requirements for Dodd-Frank Stress Test In accordance with the Dodd-Frank Wall Street Reform and Consumer

PEOPLE'S UNITED BANK, N.A. 2015 Dodd-Frank Act Stress Test (DFAST) Disclosure June 18, 2015 1. Requirements for Dodd-Frank Stress Test In accordance with the Dodd-Frank Wall Street Reform and Consumer

Deposit Pricing in Rising Rates Session 1. Three Part Series

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Effective Process Deposit Analysis Tools Betas Decay Rates

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Effective Process Deposit Analysis Tools Betas Decay Rates

Using ALM Models for PPNR and Securities OCI Peter Stoffelen September 27, BOARD OF GOVERNORS of the FEDERAL RESERVE SYSTEM

Using ALM Models for PPNR and Securities OCI Peter Stoffelen September 27, 2016 BOARD OF GOVERNORS of the FEDERAL RESERVE SYSTEM Disclaimer The opinions expressed in this presentations are those of the

Using ALM Models for PPNR and Securities OCI Peter Stoffelen September 27, 2016 BOARD OF GOVERNORS of the FEDERAL RESERVE SYSTEM Disclaimer The opinions expressed in this presentations are those of the

Excess liquidity can restrict NorthPark s profitability and have an adverse effect on its capital position.

Purpose Liquidity Risk is defined as the current and prospective risk to NorthPark Community Credit Union s (NorthPark) earnings and capital position. Potential risk develops when NorthPark s experiences

Purpose Liquidity Risk is defined as the current and prospective risk to NorthPark Community Credit Union s (NorthPark) earnings and capital position. Potential risk develops when NorthPark s experiences

FHLB Des Moines Regional Member Meetings Profiting from a Rising Rate Environment

Risk Management Strategy & Solutions FHLB Des Moines Regional Member Meetings Profiting from a Rising Rate Environment Joseph Kennerson, Managing Director jkennerson@darlingconsulting.com Mark A. Haberland,

Risk Management Strategy & Solutions FHLB Des Moines Regional Member Meetings Profiting from a Rising Rate Environment Joseph Kennerson, Managing Director jkennerson@darlingconsulting.com Mark A. Haberland,

ALCO BEST PRACTICES. Police Officers Credit Union Conference May 6, Presented By Stacey Wilkerson Financial Advisor

ALCO BEST PRACTICES Police Officers Credit Union Conference May 6, 2014 Presented By Stacey Wilkerson Financial Advisor Agenda Risk vs. reward The inherent conflict between earnings and risk Strategic

ALCO BEST PRACTICES Police Officers Credit Union Conference May 6, 2014 Presented By Stacey Wilkerson Financial Advisor Agenda Risk vs. reward The inherent conflict between earnings and risk Strategic

FIFTH THIRD BANCORP MARKET RISK DISCLOSURES. For the quarter ended March 31, 2016

FIFTH THIRD BANCORP MARKET RISK DISCLOSURES For the quarter ended March 31, 2016 The Market Risk Rule In order to better capture the risks inherent in trading positions the Office of the Comptroller of

FIFTH THIRD BANCORP MARKET RISK DISCLOSURES For the quarter ended March 31, 2016 The Market Risk Rule In order to better capture the risks inherent in trading positions the Office of the Comptroller of

Interest Rate Risk Managing Through The Uptick in Rates

Interest Rate Risk Managing Through The Uptick in Rates Outline Asset Liability Management as Performance Management Sensitivity and the Sources of Risk History of Interest Rate Risk Management How to

Interest Rate Risk Managing Through The Uptick in Rates Outline Asset Liability Management as Performance Management Sensitivity and the Sources of Risk History of Interest Rate Risk Management How to

Victoria Bennett Regional Lending Specialist. NCUA Hot Topics. CUNA Lending Council Conference. November 4, 2014

Victoria Bennett Regional Lending Specialist NCUA Hot Topics CUNA Lending Council Conference November 4, 2014 AGENDA Short update on credit unions Discussion of hot topics Suggestions 12000 Decline in

Victoria Bennett Regional Lending Specialist NCUA Hot Topics CUNA Lending Council Conference November 4, 2014 AGENDA Short update on credit unions Discussion of hot topics Suggestions 12000 Decline in

USAA Federal Savings Bank 2017 Dodd-Frank Act Stress Test Results Supervisory Severely Adverse Scenario

USAA Federal Savings Bank 2017 Dodd-Frank Act Stress Test Results Supervisory Severely Adverse Scenario June 15, 2017 In accordance with the Dodd-Frank Wall Street Reform and Consumer Protection Act (

USAA Federal Savings Bank 2017 Dodd-Frank Act Stress Test Results Supervisory Severely Adverse Scenario June 15, 2017 In accordance with the Dodd-Frank Wall Street Reform and Consumer Protection Act (

Dodd-Frank Act Company-Run Stress Test Disclosures

Dodd-Frank Act Company-Run Stress Test Disclosures June 21, 2018 Table of Contents The PNC Financial Services Group, Inc. Table of Contents INTRODUCTION... 3 BACKGROUND... 3 2018 SUPERVISORY SEVERELY ADVERSE

Dodd-Frank Act Company-Run Stress Test Disclosures June 21, 2018 Table of Contents The PNC Financial Services Group, Inc. Table of Contents INTRODUCTION... 3 BACKGROUND... 3 2018 SUPERVISORY SEVERELY ADVERSE

Southeast Bankers Outreach Forum

Southeast Bankers Outreach Forum IRR in a Protracted Low Rate Environment Date: September 30, 2014 Presented by: Trent Cowsert Director of Capital Markets The opinions expressed are those of the presenter

Southeast Bankers Outreach Forum IRR in a Protracted Low Rate Environment Date: September 30, 2014 Presented by: Trent Cowsert Director of Capital Markets The opinions expressed are those of the presenter

2016 Dodd-Frank Act Stress Test Disclosure

2016 Dodd-Frank Act Stress Test Disclosure October 2016 About ( AFH or the Company ) is a holding company whose primary business is the operation of its wholly owned subsidiary, Apple Bank for Savings

2016 Dodd-Frank Act Stress Test Disclosure October 2016 About ( AFH or the Company ) is a holding company whose primary business is the operation of its wholly owned subsidiary, Apple Bank for Savings

Asset/Liability Management (ALM) NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08)

NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08)") Asset/Liability Management (ALM) NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08) Dan Frilot Senior Vice President Balance Sheet Solutions, LLC Background Balance Sheet

Asset/Liability Management (ALM) NCUA s Revised Interest Rate Risk Supervision (Letter to Credit Unions 16-CU-08) Dan Frilot Senior Vice President Balance Sheet Solutions, LLC Background Balance Sheet

Developing Deposit Strategies for Rising Rates Session 1. Agenda

Developing Deposit Strategies for Rising Rates Session 1 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

Developing Deposit Strategies for Rising Rates Session 1 Thomas A. Farin President tfarin@farin.com 1 Agenda Session 1 - Deposit Analytics Are We In a Rising Rate Environment? Establishing Cash Flows Contractual

Asset/Liability Management

Asset/Liability Management FHLB System Sales and Marketing Meeting Scottsdale, AZ February 27 th, 2016 Ryan W. Hayhurst Managing Director Financial Strategies Group ryan@gobaker.com 800-962-9468 The Baker

Asset/Liability Management FHLB System Sales and Marketing Meeting Scottsdale, AZ February 27 th, 2016 Ryan W. Hayhurst Managing Director Financial Strategies Group ryan@gobaker.com 800-962-9468 The Baker

Liquidity and Contingency Funding Strategies for Today s Market

Liquidity and Contingency Funding Strategies for Today s Market Presented by www.firstempire.com Today s Presenter Frank Santucci, Managing Director ALM Services, BSMS Frank has been working with banks

Liquidity and Contingency Funding Strategies for Today s Market Presented by www.firstempire.com Today s Presenter Frank Santucci, Managing Director ALM Services, BSMS Frank has been working with banks

The Goldman Sachs Group, Inc Dodd-Frank Act Mid-Cycle Stress Test Results. September 16, 2013

The Goldman Sachs Group, Inc. 2013 Dodd-Frank Act Mid-Cycle Stress Test Results September 16, 2013 1 Dodd-Frank Act Mid-Cycle Stress Test Results for The Goldman Sachs Group, Inc. Overview and requirements

The Goldman Sachs Group, Inc. 2013 Dodd-Frank Act Mid-Cycle Stress Test Results September 16, 2013 1 Dodd-Frank Act Mid-Cycle Stress Test Results for The Goldman Sachs Group, Inc. Overview and requirements

LIQUIDITY STRESS TESTS: ARE YOU READY? February 2019

LIQUIDITY STRESS TESTS: ARE YOU READY? February 2019 1 THE AUTHOR 2 ABSTRACT Nathanael Sebbag Associate Partner Since the financial crisis, supervisory stress testing has become a powerful tool for banking

LIQUIDITY STRESS TESTS: ARE YOU READY? February 2019 1 THE AUTHOR 2 ABSTRACT Nathanael Sebbag Associate Partner Since the financial crisis, supervisory stress testing has become a powerful tool for banking

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018 Important Presentation Information The 2018 Dodd-Frank Act Mid-Cycle Stress Test Results

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018 Important Presentation Information The 2018 Dodd-Frank Act Mid-Cycle Stress Test Results

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended September 30, 2017

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended September 30, 2017 THE BANK OF NEW YORK MELLON CORPORATION Table of Contents Introduction... 2... 3 Quarterly Variance in the LCR... 3

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended September 30, 2017 THE BANK OF NEW YORK MELLON CORPORATION Table of Contents Introduction... 2... 3 Quarterly Variance in the LCR... 3

Annual Company-Run Stress Test Results

Wells Fargo & Company Annual Company-Run Stress Test Results Under the Supervisory Prescribed Severely Adverse Scenario June 22, 2017 Contents Overview...3 Supervisory Severely Adverse Scenario Overview...5

Wells Fargo & Company Annual Company-Run Stress Test Results Under the Supervisory Prescribed Severely Adverse Scenario June 22, 2017 Contents Overview...3 Supervisory Severely Adverse Scenario Overview...5

Making the Business Case for the CECL Approach

Making the Business Case for the CECL Approach Attend any recent or upcoming financial institution conference and you will find considerable discussion and debate about the new accounting guidance related

Making the Business Case for the CECL Approach Attend any recent or upcoming financial institution conference and you will find considerable discussion and debate about the new accounting guidance related

Linking: Liquidity Risk & Credit Portfolio Management

Annual Fall Conference November 18-19, 2014 Philadelphia, PA Linking: Liquidity Risk & Credit Portfolio Management Randy Clyde MUFG Union Bank Head of Portfolio Analytics & Strategy: Investment Portfolio

Annual Fall Conference November 18-19, 2014 Philadelphia, PA Linking: Liquidity Risk & Credit Portfolio Management Randy Clyde MUFG Union Bank Head of Portfolio Analytics & Strategy: Investment Portfolio

Seven Habits of Highly Effective Bankers: Lessons Learned from IFC Bank Visits in Michael J. Higgins Principal Banking Specialist

Seven Habits of Highly Effective Bankers: Lessons Learned from IFC Bank Visits in 2008 Michael J. Higgins Principal Banking Specialist MENA Introduction and Background During the Fourth Quarter of 2008,

Seven Habits of Highly Effective Bankers: Lessons Learned from IFC Bank Visits in 2008 Michael J. Higgins Principal Banking Specialist MENA Introduction and Background During the Fourth Quarter of 2008,

HSBC North America Holdings Inc Mid-Cycle Company-Run Dodd-Frank Act Stress Test Results. Date: September 15, 2014

Date: September 15, 2014 TABLE OF CONTENTS PAGE 1. Overview of the mid-cycle company-run Dodd-Frank Act stress test... 1 2. Description of the internal severely adverse scenario... 1 3. Forecasting methodologies

Date: September 15, 2014 TABLE OF CONTENTS PAGE 1. Overview of the mid-cycle company-run Dodd-Frank Act stress test... 1 2. Description of the internal severely adverse scenario... 1 3. Forecasting methodologies

Balance Sheet Strategies For Changing Rate Environments

Balance Sheet Strategies For Changing Rate Environments Moss Adams 2017 Credit Union Conference Portland, OR June 22 nd, 2017 Ryan W. Hayhurst Managing Director ryan@gobaker.com 800 962 9468 Credit Union

Balance Sheet Strategies For Changing Rate Environments Moss Adams 2017 Credit Union Conference Portland, OR June 22 nd, 2017 Ryan W. Hayhurst Managing Director ryan@gobaker.com 800 962 9468 Credit Union

Asset Liability Management: The Fundamentals

Asset Liability Management: The Fundamentals By Toby Lawrence, Principal Financial Institution Advisory Services CLAconnect.com Disclaimers To ensure compliance imposed by IRS Circular 230, any U. S. federal

Asset Liability Management: The Fundamentals By Toby Lawrence, Principal Financial Institution Advisory Services CLAconnect.com Disclaimers To ensure compliance imposed by IRS Circular 230, any U. S. federal

ICAAP Andy Poprawa Suzanne Tu Suzanne T cker cker Steve Kokaliaris, June 23, 2014

ICAAP Internal Capital Adequacy Assessment Process Andy Poprawa, President & CEO, DICO Suzanne Tucker, Senior Manager, DICO Steve Kokaliaris, Manager, DICO June 23, 2014 Agenda Overview Key Metrics Report

ICAAP Internal Capital Adequacy Assessment Process Andy Poprawa, President & CEO, DICO Suzanne Tucker, Senior Manager, DICO Steve Kokaliaris, Manager, DICO June 23, 2014 Agenda Overview Key Metrics Report

Annual Company-Run Stress Test Results

Wells Fargo & Company Annual Company-Run Stress Test Results Under the Supervisory Prescribed Severely Adverse Scenario June 21, 2018 Contents Overview... 3 Supervisory Severely Adverse Scenario Overview...

Wells Fargo & Company Annual Company-Run Stress Test Results Under the Supervisory Prescribed Severely Adverse Scenario June 21, 2018 Contents Overview... 3 Supervisory Severely Adverse Scenario Overview...

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP WVBA Convention July 29, 2014 Agenda Evaluating and Anticipating the Rate Environment Understanding Your Current

MANAGING INTEREST RATE RISK: SETTING THE STAGE FOR TOMORROW MIKE DELISLE, ALM ADVISORS GROUP WVBA Convention July 29, 2014 Agenda Evaluating and Anticipating the Rate Environment Understanding Your Current

Loan Pricing Deals & Relationships Session 1. Agenda

Loan Pricing Deals & Relationships Session 1 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

Loan Pricing Deals & Relationships Session 1 Thomas Farin President Farin & Associates, Inc tfarin@farin.com 1 Agenda Session 1 Inputs What We Need to Know Role of Benchmarks Four Models to Look at Profitability

14. What Use Can Be Made of the Specific FSIs?

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

Wintrust Financial Corporation

Wintrust Financial Corporation 2017 Annual Stress Test Disclosures Dodd-Frank Act Stress Test Results Supervisory Severely Adverse Scenario October 27, 2017 Table of Contents Overview 4 Supervisory Severely

Wintrust Financial Corporation 2017 Annual Stress Test Disclosures Dodd-Frank Act Stress Test Results Supervisory Severely Adverse Scenario October 27, 2017 Table of Contents Overview 4 Supervisory Severely

Bank of America 2016 Dodd-Frank Act Annual Stress Test Results Supervisory Severely Adverse Scenario June 23, 2016

Bank of America 2016 Dodd-Frank Act Annual Stress Test Results Supervisory Severely Adverse Scenario June 23, 2016 Important Presentation Information The 2016 Dodd-Frank Act Annual Stress Test Results

Bank of America 2016 Dodd-Frank Act Annual Stress Test Results Supervisory Severely Adverse Scenario June 23, 2016 Important Presentation Information The 2016 Dodd-Frank Act Annual Stress Test Results

Regulatory Capital Pillar 3 Disclosures

Regulatory Capital Pillar 3 Disclosures December 31, 2016 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply

Regulatory Capital Pillar 3 Disclosures December 31, 2016 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply

Managing liquidity risk under regulatory pressure. Kunghehian Nicolas

Managing liquidity risk under regulatory pressure Kunghehian Nicolas May 2012 Impact of the new Basel III regulation on the liquidity framework 2 Liquidity and business strategy alignment 79% of respondents

Managing liquidity risk under regulatory pressure Kunghehian Nicolas May 2012 Impact of the new Basel III regulation on the liquidity framework 2 Liquidity and business strategy alignment 79% of respondents

RESERVE BANK OF MALAWI

RESERVE BANK OF MALAWI GUIDELINES ON INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS (ICAAP) Bank Supervision Department March 2013 Table of Contents 1.0 INTRODUCTION... 2 2.0 MANDATE... 2 3.0 RATIONALE...

RESERVE BANK OF MALAWI GUIDELINES ON INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS (ICAAP) Bank Supervision Department March 2013 Table of Contents 1.0 INTRODUCTION... 2 2.0 MANDATE... 2 3.0 RATIONALE...

Managing liquidity risk in a changed and global world

Managing liquidity risk in a changed and global world September 15 th, 2010 PwC Agenda 1) Introduction to Liquidity Risk and Monetary Policy 2) Liquidity Risk from a supranational regulatory perspective

Managing liquidity risk in a changed and global world September 15 th, 2010 PwC Agenda 1) Introduction to Liquidity Risk and Monetary Policy 2) Liquidity Risk from a supranational regulatory perspective

Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies

General Stress Testing Guidance for Insurance Companies") Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies 1 INTRODUCTION AND PURPOSE The business of insurance is

Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies 1 INTRODUCTION AND PURPOSE The business of insurance is

Interagency Advisory on Interest Rate Risk Management

Interagency Management As part of our continued efforts to help our clients navigate through these volatile times, we recently sent out the attached checklist that briefly describes how c. myers helps

Interagency Management As part of our continued efforts to help our clients navigate through these volatile times, we recently sent out the attached checklist that briefly describes how c. myers helps

FIFTH THIRD BANCORP MARKET RISK DISCLOSURES. For the quarter ended September 30, 2015

FIFTH THIRD BANCORP MARKET RISK DISCLOSURES For the quarter ended September 30, 2015 The Market Risk Rule In order to better capture the risks inherent in trading positions the Office of the Comptroller

FIFTH THIRD BANCORP MARKET RISK DISCLOSURES For the quarter ended September 30, 2015 The Market Risk Rule In order to better capture the risks inherent in trading positions the Office of the Comptroller

FIFTH THIRD BANCORP MARKET RISK DISCLOSURES

FIFTH THIRD BANCORP MARKET RISK DISCLOSURES For the year ended December 31st, 2018 PLEASE NOTE: For purposes of consistency and clarity, Table 1, Chart 1, and Table 3 have been updated to reflect that

FIFTH THIRD BANCORP MARKET RISK DISCLOSURES For the year ended December 31st, 2018 PLEASE NOTE: For purposes of consistency and clarity, Table 1, Chart 1, and Table 3 have been updated to reflect that

Liquidity Coverage Ratio Disclosure. Bank AlBilad Liquidity Coverage Ratio Disclosure Dec 31, 2015

Bank AlBilad Liquidity Coverage Ratio Disclosure Dec 31, 2015 1 I. LIQUIDITY COVERAGE RATIO (LCR): QUANTITATIVE DISCLOSURE Date: 31 Dec 2015 LCR Common Disclosure Template (In SR 000`s) Total UNWEIGHTED

Bank AlBilad Liquidity Coverage Ratio Disclosure Dec 31, 2015 1 I. LIQUIDITY COVERAGE RATIO (LCR): QUANTITATIVE DISCLOSURE Date: 31 Dec 2015 LCR Common Disclosure Template (In SR 000`s) Total UNWEIGHTED

Lecture Materials FUNDING. Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 August 7 & 8, 2017 Funding - Developing Funding Strategies

Lecture Materials FUNDING Thomas A. Farin Chairman of the Board FARIN Financial Risk Management Fitchburg, Wisconsin tfarin@farin.com 608-661-4219 August 7 & 8, 2017 Funding - Developing Funding Strategies

Weathering the Storm: Rates, Recession, and Risk

Weathering the Storm: Rates, Recession, and Risk Presenters: Charles McQueen Ed Lis Greg Gibson President VP of Finance & Compliance Chief Financial Officer McQueen Financial Adv. First Choice Financial

Weathering the Storm: Rates, Recession, and Risk Presenters: Charles McQueen Ed Lis Greg Gibson President VP of Finance & Compliance Chief Financial Officer McQueen Financial Adv. First Choice Financial

SUPERVISORY STRESS TESTING (SST) MOHAMED AFZAL NORAT

MOHAMED AFZAL NORAT") SUPERVISORY STRESS TESTING (SST) MOHAMED AFZAL NORAT Financial Supervision and Regulation Division Monetary and Capital Markets Department October 17, 2012 1 Stress Testing Stress Tests Variations Top

SUPERVISORY STRESS TESTING (SST) MOHAMED AFZAL NORAT Financial Supervision and Regulation Division Monetary and Capital Markets Department October 17, 2012 1 Stress Testing Stress Tests Variations Top

DFAST Public Disclosure: Texas Capital Bancshares 2015

& Dodd-Frank Act Company-Run Stress Test 2015 Public Disclosure June 15, 2015 Page 1 Contents 1. Introduction... 3 2. Supervisory Severely Adverse Scenario... 3 3. Risks Accounted For in Stress Testing

& Dodd-Frank Act Company-Run Stress Test 2015 Public Disclosure June 15, 2015 Page 1 Contents 1. Introduction... 3 2. Supervisory Severely Adverse Scenario... 3 3. Risks Accounted For in Stress Testing

Hancock Holding Company Dodd Frank Act Annual Stress Test 2015 Results Disclosure

Hancock Holding Company Dodd Frank Act Annual Stress Test 2015 Results Disclosure June 23, 2015 In this report, when we refer to Hancock, HHC or the Company we mean Hancock Holding Company and its consolidated

Hancock Holding Company Dodd Frank Act Annual Stress Test 2015 Results Disclosure June 23, 2015 In this report, when we refer to Hancock, HHC or the Company we mean Hancock Holding Company and its consolidated

STRESS TESTING Transition to DFAST compliance

WHITE PAPER STRESS TESTING Transition to DFAST compliance Abstract The objective of this document is to explain the challenges related to stress testing that arise when a Community Bank crosses $0 Billion

WHITE PAPER STRESS TESTING Transition to DFAST compliance Abstract The objective of this document is to explain the challenges related to stress testing that arise when a Community Bank crosses $0 Billion

How to review an ORSA

How to review an ORSA Patrick Kelliher FIA CERA, Actuarial and Risk Consulting Network Ltd. Done properly, the Own Risk and Solvency Assessment (ORSA) can be a key tool for insurers to understand the evolution

How to review an ORSA Patrick Kelliher FIA CERA, Actuarial and Risk Consulting Network Ltd. Done properly, the Own Risk and Solvency Assessment (ORSA) can be a key tool for insurers to understand the evolution

INTEREST RATE RISK MAKING YOUR MODEL UNDERSTANDABLE AND RELEVANT

INTEREST RATE RISK MAKING YOUR MODEL UNDERSTANDABLE AND RELEVANT Scott J. Hopf, CPA Senior Manager BKD, LLP 375 North Shore Drive, Suite 501 Pittsburgh, PA 15212 shopf@bkd.com 412.364.9395 AGENDA The Basics

INTEREST RATE RISK MAKING YOUR MODEL UNDERSTANDABLE AND RELEVANT Scott J. Hopf, CPA Senior Manager BKD, LLP 375 North Shore Drive, Suite 501 Pittsburgh, PA 15212 shopf@bkd.com 412.364.9395 AGENDA The Basics

Liquidity Management. 158 Route 206 Gladstone, NJ P: (908) Home FinPro, Inc.

Home FinPro, Inc.") Liquidity Management 158 Route 206 Gladstone, NJ 07934 P: (908) 234-9398 finpro@finpro.us www.finpro.us 0 Liquidity: you always have too much until you need it!! 1 Banks must take a holistic view of its

Liquidity Management 158 Route 206 Gladstone, NJ 07934 P: (908) 234-9398 finpro@finpro.us www.finpro.us 0 Liquidity: you always have too much until you need it!! 1 Banks must take a holistic view of its

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended March 31, 2018 THE BANK OF NEW YORK MELLON CORPORATION

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended March 31, 2018 THE BANK OF NEW YORK MELLON CORPORATION Table of Contents Introduction... 2... 3 Quarterly Variance in the LCR... 3 Drivers

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended March 31, 2018 THE BANK OF NEW YORK MELLON CORPORATION Table of Contents Introduction... 2... 3 Quarterly Variance in the LCR... 3 Drivers

Asset Liability Management An Integrated Approach to Managing Liquidity, Capital, and Earnings

Actuaries Club of Philadelphia Asset Liability Management An Integrated Approach to Managing Liquidity, Capital, and Earnings Alan Newsome, FSA, MAAA February 28, 2018 Today s Agenda What is Asset Liability

Actuaries Club of Philadelphia Asset Liability Management An Integrated Approach to Managing Liquidity, Capital, and Earnings Alan Newsome, FSA, MAAA February 28, 2018 Today s Agenda What is Asset Liability

Market Risk Disclosures For the Quarter Ended March 31, 2013

Market Risk Disclosures For the Quarter Ended March 31, 2013 Contents Overview... 3 Trading Risk Management... 4 VaR... 4 Backtesting... 6 Total Trading Revenue... 6 Stressed VaR... 7 Incremental Risk

Market Risk Disclosures For the Quarter Ended March 31, 2013 Contents Overview... 3 Trading Risk Management... 4 VaR... 4 Backtesting... 6 Total Trading Revenue... 6 Stressed VaR... 7 Incremental Risk

Quantifiable Risk Management Data Driven Approaches to Building a Predictive Risk Framework. Andrew Auslander, CFA, FRM

Quantifiable Risk Management Data Driven Approaches to Building a Predictive Risk Framework Andrew Auslander, CFA, FRM Quantifiable Risk Management Data driven Approaches to Building a Predictive Risk

Quantifiable Risk Management Data Driven Approaches to Building a Predictive Risk Framework Andrew Auslander, CFA, FRM Quantifiable Risk Management Data driven Approaches to Building a Predictive Risk

Enterprise-wide Scenario Analysis

Finance and Private Sector Development Forum Washington April 2007 Enterprise-wide Scenario Analysis Jeffrey Carmichael CEO 25 April 2007 Date 1 Context Traditional stress testing is useful but limited

Finance and Private Sector Development Forum Washington April 2007 Enterprise-wide Scenario Analysis Jeffrey Carmichael CEO 25 April 2007 Date 1 Context Traditional stress testing is useful but limited

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

Risk Management. Credit Risk Management

Credit Risk Management Credit risk is defined as the risk of loss arising from any failure by a borrower or a counterparty to fulfill its financial obligations as and when they fall due. Credit risk is

Credit Risk Management Credit risk is defined as the risk of loss arising from any failure by a borrower or a counterparty to fulfill its financial obligations as and when they fall due. Credit risk is