Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem

|

|

|

- Anis Dawson

- 5 years ago

- Views:

Transcription

1 Mortgage-Backed Securities and the Financial Crisis of 28: a Post Mortem Juan Ospina 1 Harald Uhlig 1 1 Department of Economics University of Chicago October 217

2 Outline

3 Post Mortem post mortem: an examination of a dead body to determine the cause of death.

4 What we do Questions: What were the losses and returns on non-agency RMBS, in particular those rated AAA? How did the ex-ante rating compare to their ex-post performance? Role of house price boom and bust for RMBS performance? Approach: Create new data set of 143 thousand RMBS bonds. Obtain their ratings, their characteristics, their payoff stream. Calculate losses, returns. Compare to ratings. Compare to house price booms and busts, state-by-state.

5 Data Collection We needed to find a source that had some information about the universe of securities Mortgage Market Statistical Annual 213 Edition had information on all non-agency MBS deals issued between 26 and 212 About 5 pages of tables deals.

6 A sample table from the Stats Annual

7 Data Collection on Bloomberg Searched for the 2824 deals from the Stats Annual Searched also for related deals (for example by name of financial institution) Deal Example Once we find a deal, we look back at all deals with similar name. Goal: get the universe of deals. Total: 8615 deals Old Deal Example For each deal, get tranches (securities, bonds) Total: bonds. Principal: 5.7 trillion $. Tranches Example Per bond: obtain 93 variables plus losses and cash flows Security Challenge: Bloomberg places a limit on how much information can be downloaded per month: Max out below 15 thousand securities per month. We have more than 14 thousand securities It took more than a year to collect all the data

8 Bloomberg Deal Search I Back

9 Bloomberg Deal Search II Back

10 Bloomberg List of Securities (Tranches) Back

11 Bloomberg Security Example Back

12 Data specs: ( Distr.:min, max, mean, 25th, 5th,75th ) Security Identification Cusip ID Deal Name Deal Manager Issuer Company Security Classification Deal Type (eg. CMBS, RMBS) Collateral Type (Home, Auto, Student) Collateral Type (ARM vs FRM) Agency Backed (yes, no) Agency (Fannie Mae, Freddie Mac) Dates Issue Date Pricing Date Maturity Date Security Description Bond type (e.g. Floater, i Only) Tranche Subordination Description Coupon Type (e.g. Fixed, Floating) Coupon Frequency (e.g. Monthly) Coupon Index Rate (e.g. 3M-libor) Credit Rating Current and Original Ratings (5 ag.) Other Security Characteristics Credit Support at Issuance Original Principal Amount Collateral Description Mortg.Purp.(% Equ. Takeout, Refin.) LTV Distr.. Credit Score Distr. Mortgage Size Distr. MBS metrics 1: w. av. coupon MBS metrics 2: w. av. Life MBS metrics 3:w. av. maturity Fraction of ARM and FRM Occup. (% own, inv., vac.) Geographic Information Fraction of mortg. in top 5 states Cash Flow and Losses Monthly Interest, Principal Paym. Monthly Outstanding balance Monthly Losses

13 What we find Seven facts: 1. The bulk of these securities was rated AAA. 2. AAA securities did ok: on average, their total cumulated losses up to 213 are under six percent. Their rate of return was above 2 percent. 3. The subprime AAA-rated RMBS did particularly well. 4. The bulk of the losses were concentrated on a small share of all securities. 5. Later vintages did worse than earlier vintages, but not subprime-aaa. 6. Mis-ratings modest for AAA. 7. Controlling for home price bust, a home price boom was good for repayments. Together, these facts call into question the conventional narrative, that improper ratings of RMBS were a major factor in the financial crisis of 28.

14 Fact 1: The bulk of these securities was rated AAA. MBS Bonds Principal Amount Rating No. Pct. ($ Billion) Pct. AAA 65, , AA 13, A 13, BBB 13, BB 6, B 3, CCC CC C Rated 115, , Not Rated 26,

15 Frequency Frequency Frequency FICO scores vs Prime, Alt-A, Subprime.25.2 Subprime Alt-A Prime Mean FICO Score Subprime Alt-A Prime Subprime Alt-A Prime Mean Mortgage Loan Size Mean LTV

16 Loss Rate Losses on AAA securities Fact 2: AAA securities did ok: on average, their total cumulated losses up to 213 are under six percent. Their rate of return was above 2 percent. Fact 3: The subprime AAA-rated RMBS did particularly well.7.6 Prime AltA Subprime All AAA % % 31.8% Time

17 Probability Loss Losses on all RMBS Panel A: Value-Weighted Loss as Fraction of Principal All Ratings AAA Investment Grade Ex-AAA Non-InvestmentGrade All Ratings AAA Investment Grade Ex-AAA Non-InvestmentGrade Panel B: Unweighted Probability of Loss Time

18 Loss ($ billion) Dollar Amount of Losses in Non-Agency RMBS All RMBS AAA-rated Inv. Grade Ex-AAA Non-Inv. Grade

19 Cash flow example Example Deal JPALT 26-S1 Security Name JPALT 26-S2 A7 Mtge Security ID 46627MEX1 Original Rating AAA Year Coupon Rate Interest Payments 1,421 2,131 2,131 2,18 1,989 1, Principal Payment ,247 1,365 1, Loss ,844 14,39 7,55 3,82 Balance 34,547 34,547 34,547 33,3 27,91 11,878 3,898 -

20 Returns 1 P = T t=1 i t + p t (1 + r) t + TV T (1 + r) T (1)

21 Returns 2 Return Statistic 8% TV 9% TV 1% TV By Credit Rating AAA AA A BBB Inv. Grade Ex AAA By Type of Mortgage AAA Prime AAA SubPrime AAA AltA

22 Returns 3 Return Statistic 8% TV 9% TV 1% TV Fixed Rate MBS AAA Prime Fixed AAA SubPrime Fixed AAA AltA Fixed Floating Rate MBS AAA Prime Floating AAA SubPrime Floating AAA AltA Floating

23 Frequency Fraction With Loss < 5% Fraction With Loss > 5% Fact 4: The bulk of the losses were concentrated on a small share of all securities..7.6 Panel A: All RMBS 1 Panel B: By Credit Rating AAA Loss < 5% IG Ex-AAA Loss < 5% Non-IG Loss < 5% AAA Investment Grade Ex-AAA Non-InvestmentGrade Loss as a Fraction of Principal Loss as a Fraction of Principal

24 Fact 5: Later vintages did worse than earlier vintages. Principal-Weighted Losses in RMBS and Credit Ratings: Rating Full Sample Before AAA.218***.2.34***.483*** AA.396***.1.118***.591*** A.362***.55***.2***.6572*** BBB.448***.334***.3152***.6655*** BB.4923***.653***.4886***.5136*** B.5812***.938***.6989***.5619*** CCC.736***.4125***.412***.9465*** CC.236*** *** C or Below.3863***.661***.667***.364*** Observations 93,92 19,23 38,381 36,291 R-squared Standard errors in parentheses p <.1, p <.5, p <.1

25 Vintage FE Vintage FE Vintage FE Fact 5: Vintage FE for Weighted Losses increased All RMBS Year of Issuance AAA AA A Year of Issuance BBB Year of Issuance

26 Vintage FE Vintage FE Vintage FE... though AAA-Subprime did not do worse over time Prime Alt-A Subprime All RMBS Year of Issuance AAA AA A BBB Year of Issuance Year of Issuance

27 Fact 6: Misratings Compare actual loss rate lossrate i,t = L i,t /Principal i,t to expected loss rate in table by Moody s.

28 Moody s Table

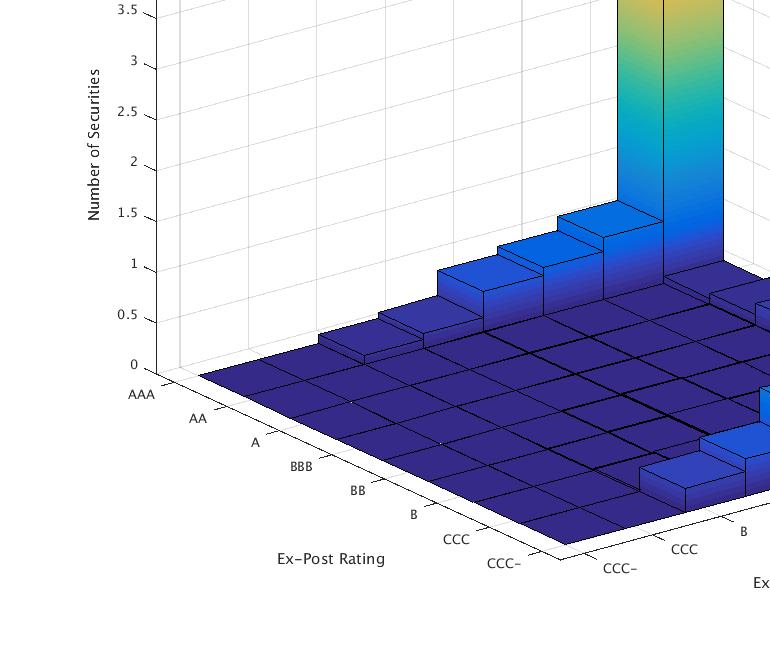

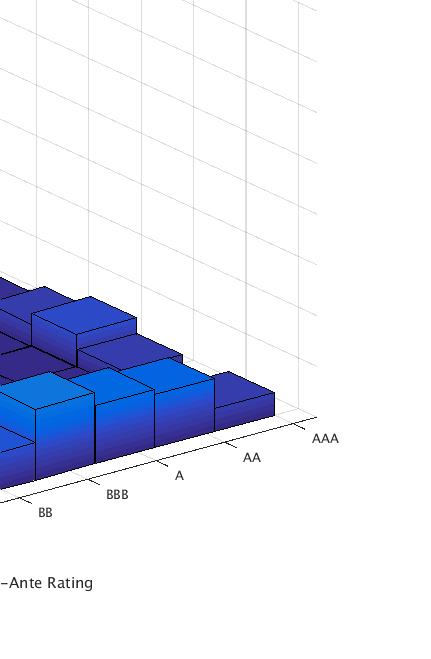

29 Fraction of Securities (%) Ex-Ante vs Ex-Post Rating Based on Moodys Ideal Table 9 8 Ex-Ante Rating Ex-Post Ideal Rating AAA AA A BBB BB B CCC CCC below Credit Rating Level

30 Fraction of Securities (%) Ex-Ante vs Ex-Post Rating: Unweighted 6 Ex-Ante Rating Ex-Post Ideal Rating AAA AA A BBB BB B CCC CCC below Credit Rating Level

31 Fraction of Securities (%) Ex-Ante vs Ex-Post Rating Based on Moodys Ideal Table 9 8 Correct Rating Inflated Rating Deflated Rating AAA AA A BBB BB B CCC CCC below Credit Rating Level

32 Misratings

33 Fact 7: Loss-Rates and House Price Boom/Busts lossrate i,t = β MA ω i,ma + β IL ω i,il β X X i + ɛ i where ω i,ma is the fraction of principal invested in the state MA, etc.. (with only five of these weights nonzero), and where X i are controls. lossrate i,t = = β boom (ω i,ma boom P MA + ω i,il boom P IL +...) + β bust (ω i,ma bust P MA + ω i,il bust P IL +...) where boom P MA is the percent change of house prices during the boom, 2-26, bust P MA is the percent change during the bust 26-29, etc..

34 State-Level Dummies for Loss Rates with Controls without Controls.3 / / / / / / / / / / -.4

35 State-Level House Price Boom and Bust Boom: 2-Q1 to 26-Q4 Bust: 26-Q4 to 29-Q4 23.2% / 38% 38% / 44.6% 44.6% / 72.1% 72.1% / 94.1% 94.1% / 165.2% -43.2% / -14.4% -14.4% / -9.6% -9.6% / -2.9% -2.9% /.2%.2% / 9.1%

36 House Prices and Loss Rates (1) (2) (3) (4) (5) HP *** -.218*** -.178*** (.3) (.1) (.12) HP *** -.63*** -.532*** (.6) (.21) (.2) Price Reversal -.238*** Controls No No No No Yes Observations 93,92 93,92 93,92 93,92 71,316 R-squared Standard errors in parentheses p <.1, p <.5, p <.1 Price Reversal = HP 26-29/ HP 2-26

37 House Prices and Loss Rates per Cohort, no controls HP 2-26: *** -.145*** -.183*** -.417*** (.5) (.4) (.5) (.1) (.24) (.31) (.31) HP 26-29: *** -.43*** -.665*** *** (.11) (.9) (.9) (.2) (.48) (.61) (.62) R N Standard errors in parentheses p <.1, p <.5, p <.1

38 House Prices and Loss Rates per Cohort, with controls HP *** -.29** -.67** -.151*** -.392*** (.6) (.6) (.6) (.11) (.29) (.21) (.29) HP ** -.42** -.286*** -.479*** -1.16*** (.11) (.1) (.9) (.18) (.42) (.37) (.51) AA ***.218***.676***.647*** A.17***.11***.7***.72***.47***.841***.514*** BBB.54***.51***.48***.163***.598***.834***.511*** BB.4***.35***.221***.378***.52***.536***.534*** B.51***.92***.351***.541***.878***.52***.875*** CCC...154**.269***.52***.98*.943*** CC *** Alt-A -.2* -..2**.1***.36***.64***.5*** Prime -.2* ***.17***.5 -.7* R N p <.1, p <.5, p <.1

39 Prices? Markit ABX-indices for Subprime RMBS AAA 12 AA Jan-6 Jan-8 Jan-1 Jan-12 Jan-14 Jan-6 Jan-8 Jan-1 Jan-12 Jan A 12 BBB Jan-6 Jan-8 Jan-1 Jan-12 Jan-14 Jan-6 Jan-8 Jan-1 Jan-12 Jan-14 ABX.HE indexes by Markit. Each line represents a vintage of subprime RMBS and the Index. Each panel shows the evolution of prices over time by credit rating. These indexes are constructed based on 2 deals.

40 Price Price... vs FINRA Survey 15 Investment Grade 1 Non-Investment Grade Weighted Mean 25th Pctile 75th Pctile Investment Grade Pre Investment Grade Summary statistics of daily transaction prices collected by the Financial Industry Regulatory Authority from May 211 through May 216 on Non-Agency MBS. Top: Investment Grade vs Non-Investment Grade. Bottom: vintages for Investment Grade. 22-day moving averages, principal weighted average and 25th and 75th percentiles.

41 Conclusions Seven facts: 1. The bulk of these securities was rated AAA. 2. AAA securities did ok: on average, their total cumulated losses up to 213 are under six percent. Their rate of return was above 2 percent. 3. The subprime AAA-rated RMBS did particularly well. 4. The bulk of the losses were concentrated on a small share of all securities. 5. Later vintages did worse than earlier vintages, but not subprime-aaa. 6. Mis-ratings modest for AAA. 7. Controlling for home price bust, a home price boom was good for repayments. Together, these facts call into question the conventional narrative, that improper ratings of RMBS were a major factor in the financial crisis of 28.

Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem

Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem Juan Ospina 1 Harald Uhlig 1 1 Department of Economics University of Chicago July 20, 2016 Outline Post Mortem post mortem: an

Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem Juan Ospina 1 Harald Uhlig 1 1 Department of Economics University of Chicago July 20, 2016 Outline Post Mortem post mortem: an

Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem

Mortgage-Backed Securities and the Financial Crisis of 28: a Post Mortem Juan Ospina University of Chicago Harald Uhlig University of Chicago First draft: January 21st, 216 This revision: October 26, 216

Mortgage-Backed Securities and the Financial Crisis of 28: a Post Mortem Juan Ospina University of Chicago Harald Uhlig University of Chicago First draft: January 21st, 216 This revision: October 26, 216

Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem

WORKING PAPER NO. 2018-24 Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem Juan Ospina and Harald Uhlig April 2018 1126 E. 59th St, Chicago, IL 60637 Main: 773.702.5599 bfi.uchicago.edu

WORKING PAPER NO. 2018-24 Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem Juan Ospina and Harald Uhlig April 2018 1126 E. 59th St, Chicago, IL 60637 Main: 773.702.5599 bfi.uchicago.edu

U.S. CAPITAL MARKETS DECK

U.S. CAPITAL MARKETS DECK SIFMA RESEARCH SEPTEMBER 217 Introduction The United States has the largest and deepest capital markets in the world according to the Federal Reserve, capital markets provide

U.S. CAPITAL MARKETS DECK SIFMA RESEARCH SEPTEMBER 217 Introduction The United States has the largest and deepest capital markets in the world according to the Federal Reserve, capital markets provide

A Guide to Investing In Corporate Bonds

A Guide to Investing In Corporate Bonds Access the corporate debt income portfolio TABLE OF CONTENTS What are Corporate Bonds?... 4 Corporate Bond Issuers... 4 Investment Benefits... 5 Credit Quality and

A Guide to Investing In Corporate Bonds Access the corporate debt income portfolio TABLE OF CONTENTS What are Corporate Bonds?... 4 Corporate Bond Issuers... 4 Investment Benefits... 5 Credit Quality and

Safe Harbor Statement

Third Quarter 2009 Safe Harbor Statement All statements made during today s investor presentation and in these webcast slides that address events, developments or results that we expect or anticipate may

Third Quarter 2009 Safe Harbor Statement All statements made during today s investor presentation and in these webcast slides that address events, developments or results that we expect or anticipate may

March 2017 For intermediaries and professional investors only. Not for further distribution.

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

American Financial Group, Inc.

Investor Supplement - Fourth Quarter 2015 February 2, 2016 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

Investor Supplement - Fourth Quarter 2015 February 2, 2016 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

American Financial Group, Inc. Investor Supplement Fourth Quarter 2016

Investor Supplement Fourth Quarter 2016 February 1, 2017 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

Investor Supplement Fourth Quarter 2016 February 1, 2017 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

FANNIE MAE POOLTALK GLOSSARY (Updated as of October 2013)

") FANNIE MAE POOLTALK GLOSSARY (Updated as of October 2013) Fannie Mae generally relies on its mortgage loan sellers/servicers to provide pool and loan level information to generate its MBS disclosures.

FANNIE MAE POOLTALK GLOSSARY (Updated as of October 2013) Fannie Mae generally relies on its mortgage loan sellers/servicers to provide pool and loan level information to generate its MBS disclosures.

American Financial Group, Inc.

Investor Supplement - Third Quarter 2018 October 31, 2018 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

Investor Supplement - Third Quarter 2018 October 31, 2018 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

American Financial Group, Inc.

Investor Supplement - Second Quarter 2018 August 1, 2018 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

Investor Supplement - Second Quarter 2018 August 1, 2018 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

AG Mortgage Investment Trust, Inc. Q Earnings Presentation

AG Mortgage Investment Trust, Inc. Q1 2018 Earnings Presentation May 3, 2018 Forward Looking Statements and Non-GAAP Financial Information Forward Looking Statements: This presentation includes "forward-looking

AG Mortgage Investment Trust, Inc. Q1 2018 Earnings Presentation May 3, 2018 Forward Looking Statements and Non-GAAP Financial Information Forward Looking Statements: This presentation includes "forward-looking

American Financial Group, Inc.

Investor Supplement - First Quarter 2018 May 2, 2018 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739 Table

Investor Supplement - First Quarter 2018 May 2, 2018 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739 Table

On-line Appendix for Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem

On-line Appendix for Mortgage-Backed Securities and the Financial Crisis of 28: a Post Mortem April 6, 218 Abstract This on-line appendix is divided into three sections. Section A explains in detail, step

On-line Appendix for Mortgage-Backed Securities and the Financial Crisis of 28: a Post Mortem April 6, 218 Abstract This on-line appendix is divided into three sections. Section A explains in detail, step

Investment Materials. February 9, Genworth Financial, Inc. All rights reserved.

Investment Materials February 9, 2009 2008 Genworth Financial, Inc. All rights reserved. Investment Portfolio Position $67.9B Investment Grade Fixed Maturity 44% High Quality Portfolio: 95% Of Fixed Maturities

Investment Materials February 9, 2009 2008 Genworth Financial, Inc. All rights reserved. Investment Portfolio Position $67.9B Investment Grade Fixed Maturity 44% High Quality Portfolio: 95% Of Fixed Maturities

Keefe, Bruyette & Woods Insurance Conference. S.A. Ibrahim, CEO NYSE: RDN September 7, 2010

Keefe, Bruyette & Woods Insurance Conference S.A. Ibrahim, CEO NYSE: RDN September 7, 2010 1 Safe Harbor Statements All statements made during today s investor presentation and in these webcast slides

Keefe, Bruyette & Woods Insurance Conference S.A. Ibrahim, CEO NYSE: RDN September 7, 2010 1 Safe Harbor Statements All statements made during today s investor presentation and in these webcast slides

American Financial Group, Inc.

Investor Supplement - Fourth Quarter 2017 February 7, 2018 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

Investor Supplement - Fourth Quarter 2017 February 7, 2018 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

AG Mortgage Investment Trust, Inc. Q Earnings Presentation. August 7, 2018

AG Mortgage Investment Trust, Inc. Q2 2018 Earnings Presentation August 7, 2018 Forward Looking Statements and Non-GAAP Financial Information Forward Looking Statements: This presentation includes "forward-looking

AG Mortgage Investment Trust, Inc. Q2 2018 Earnings Presentation August 7, 2018 Forward Looking Statements and Non-GAAP Financial Information Forward Looking Statements: This presentation includes "forward-looking

Primer: building a case

Marketing material for professional investors or advisers only Primer: building a case for Fool s infrastructure gold: mining for finance true value in the US commercial real estate debt market September

Marketing material for professional investors or advisers only Primer: building a case for Fool s infrastructure gold: mining for finance true value in the US commercial real estate debt market September

The Financial Turmoil in 2007 and 2008

The Financial Turmoil in 2007 and 2008 Gerald P. Dwyer June 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal Reserve System

The Financial Turmoil in 2007 and 2008 Gerald P. Dwyer June 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal Reserve System

The Mortgage and Housing Market Outlook

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

AXIS Capital Holdings Limited. Investment Portfolio Supplemental Information and Data March 31, 2010

AXIS Capital Holdings Limited Investment Portfolio Supplemental Information and Data March 31, 2010 Cautionary Note on Forward Looking Statements Statements in this presentation that are not historical

AXIS Capital Holdings Limited Investment Portfolio Supplemental Information and Data March 31, 2010 Cautionary Note on Forward Looking Statements Statements in this presentation that are not historical

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know April13, 2010 Agenda Introduction Presentation Steve Herscovici, Managing Principal, Analysis Group Bill Chambers, Finance

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know April13, 2010 Agenda Introduction Presentation Steve Herscovici, Managing Principal, Analysis Group Bill Chambers, Finance

MORTGAGE BACKED SECURITIES AN ACTUARIAL APPROACH TO CASH FLOW ANALYSIS

MORTGAGE BACKED SECURITIES AN ACTUARIAL APPROACH TO CASH FLOW ANALYSIS Kyle S. Mrotek, FCAS, MAAA Neal Dihora, ASA, CFA CAS Spring Meeting 1 Disclaimer This presentation contains our views and these views

MORTGAGE BACKED SECURITIES AN ACTUARIAL APPROACH TO CASH FLOW ANALYSIS Kyle S. Mrotek, FCAS, MAAA Neal Dihora, ASA, CFA CAS Spring Meeting 1 Disclaimer This presentation contains our views and these views

Beryl Credit Pulse on Structured Finance

Beryl Credit Pulse on Structured Finance This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the structured finance sector in light of the events of the past

Beryl Credit Pulse on Structured Finance This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the structured finance sector in light of the events of the past

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L6: The Bond Market www. notes638.wordpress.com 6-1 Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L6: The Bond Market www. notes638.wordpress.com 6-1 Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds

Second Quarter 2018 Earnings Call AUGUST 8, 2018

Second Quarter 2018 Earnings Call AUGUST 8, 2018 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions

Second Quarter 2018 Earnings Call AUGUST 8, 2018 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions

Wells Fargo Bank, N.A. General Information Statement

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

Fannie Mae 2009 Second Quarter Credit Supplement. August 6, 2009

Fannie Mae 2009 Second Quarter Credit Supplement August 6, 2009 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report

Fannie Mae 2009 Second Quarter Credit Supplement August 6, 2009 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report

M E M O R A N D U M Financial Crisis Inquiry Commission

M E M O R A N D U M Financial Crisis Inquiry Commission To: From: Commissioners Ron Borzekowski Wendy Edelberg Date: July 7, 2010 Re: Analysis of housing data As is well known, the rate of serious delinquency

M E M O R A N D U M Financial Crisis Inquiry Commission To: From: Commissioners Ron Borzekowski Wendy Edelberg Date: July 7, 2010 Re: Analysis of housing data As is well known, the rate of serious delinquency

Specific financial information Q3 08

03/ 11/2008 Specific financial information Q3 08 (based on FSF recommendations for financial transparency) Contents Unhedged CDOs exposed to the US residential mortgage sector Write-downs on assets of

03/ 11/2008 Specific financial information Q3 08 (based on FSF recommendations for financial transparency) Contents Unhedged CDOs exposed to the US residential mortgage sector Write-downs on assets of

Specific financial information Q1 10

05 / 05 / 2010 Specific financial information Q1 10 (based on FSF recommendations for financial transparency) We stand by you Contents Unhedged CDOs exposed to the US residential mortgage sector CDOs of

05 / 05 / 2010 Specific financial information Q1 10 (based on FSF recommendations for financial transparency) We stand by you Contents Unhedged CDOs exposed to the US residential mortgage sector CDOs of

Chapter 12. The Bond Market

Chapter 12 The Bond Market Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds are like money market instruments, but they have maturities that exceed one year. These include

Chapter 12 The Bond Market Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds are like money market instruments, but they have maturities that exceed one year. These include

Reforming the Selection of Rating Agencies in Securitization Markets: A Modest Proposal

Reforming the Selection of Rating Agencies in Securitization Markets: A Modest Proposal Howard Esaki Lawrence J. White (An edited version will be forthcoming in the Milken Institute Review) Introduction:

Reforming the Selection of Rating Agencies in Securitization Markets: A Modest Proposal Howard Esaki Lawrence J. White (An edited version will be forthcoming in the Milken Institute Review) Introduction:

MBS ratings and the mortgage credit boom

MBS ratings and the mortgage credit boom Adam Ashcraft (New York Fed) Paul Goldsmith Pinkham (Harvard University, HBS) James Vickery (New York Fed) Bocconi / CAREFIN Banking Conference September 21, 2009

MBS ratings and the mortgage credit boom Adam Ashcraft (New York Fed) Paul Goldsmith Pinkham (Harvard University, HBS) James Vickery (New York Fed) Bocconi / CAREFIN Banking Conference September 21, 2009

The Financial Crisis of 2008 and Subprime Securities. Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis of 2008 and Subprime Securities Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Paula Tkac Federal Reserve Bank of Atlanta Subprime mortgages are commonly

The Financial Crisis of 2008 and Subprime Securities Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Paula Tkac Federal Reserve Bank of Atlanta Subprime mortgages are commonly

Fannie Mae 2009 First Quarter Credit Supplement. May 8, 2009

Fannie Mae 2009 First Quarter Credit Supplement May 8, 2009 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

Fannie Mae 2009 First Quarter Credit Supplement May 8, 2009 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

4091 P-01 7/14/03 7:40 AM Page 1 PART. One. Introduction to Securitization

4091 P-01 7/14/03 7:40 AM Page 1 PART One Introduction to Securitization 4091 P-01 7/14/03 7:40 AM Page 2 4091 P-01 7/14/03 7:40 AM Page 3 CHAPTER 1 The Role of Securitization Every time a person or a

4091 P-01 7/14/03 7:40 AM Page 1 PART One Introduction to Securitization 4091 P-01 7/14/03 7:40 AM Page 2 4091 P-01 7/14/03 7:40 AM Page 3 CHAPTER 1 The Role of Securitization Every time a person or a

Notice regarding Revisions of Earnings Forecasts

To Whom It May Concern October 31, 2008 Listed Company: Mitsubishi UFJ Financial Group, Inc. Representative: Nobuo Kuroyanagi, President (Code:8306) Notice regarding Revisions of Earnings Forecasts Mitsubishi

To Whom It May Concern October 31, 2008 Listed Company: Mitsubishi UFJ Financial Group, Inc. Representative: Nobuo Kuroyanagi, President (Code:8306) Notice regarding Revisions of Earnings Forecasts Mitsubishi

JPMorgan Funds statistics report: Mortgage-Backed Securities Fund

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE JPMorgan Funds statistics report: Mortgage-Backed Securities Fund Must be preceded or accompanied by a prospectus. jpmorganfunds.com Table of contents

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE JPMorgan Funds statistics report: Mortgage-Backed Securities Fund Must be preceded or accompanied by a prospectus. jpmorganfunds.com Table of contents

Wells Fargo Bank, N.A. General Information Statement

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

The following information should be considered in conjunction with the Prior Securitized Pool reports: General Information Statement. The performance information for Prior Securitized Pools is based upon

esf securitisation data report Q1:2008

esf securitisation data report Q1:28 June 28 London New York Washington Hong Kong TABLE OF CONTENTS Market Highlights and Commentary 1 1. Issuance 1.1. European Historical Issuance.............. 2 1.2.

esf securitisation data report Q1:28 June 28 London New York Washington Hong Kong TABLE OF CONTENTS Market Highlights and Commentary 1 1. Issuance 1.1. European Historical Issuance.............. 2 1.2.

Mortgage Rates, Household Balance Sheets, and the Real Economy

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Fourth Quarter 2014 Financial Results Supplement

Fourth Quarter 20 Financial Results Supplement February 19, 2015 Table of contents Financial Results Segment Business Information 2 - Annual Financial Results 12 - Single-Family New Funding Volume 3 -

Fourth Quarter 20 Financial Results Supplement February 19, 2015 Table of contents Financial Results Segment Business Information 2 - Annual Financial Results 12 - Single-Family New Funding Volume 3 -

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

American Financial Group, Inc.

Investor Supplement - Second Quarter 2014 July 28, 2014 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

Investor Supplement - Second Quarter 2014 July 28, 2014 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

SUB-PRIME US RESIDENTIAL MORTGAGES Analysis and Overview of Dexia Group s Exposure

No achievement without commitment SUB-PRIME US RESIDENTIAL MORTGAGES Analysis and Overview of Dexia Group s Exposure Conference Call Tuesday March 27, 27 Jacques Guerber Vice-Chairman of the Management

No achievement without commitment SUB-PRIME US RESIDENTIAL MORTGAGES Analysis and Overview of Dexia Group s Exposure Conference Call Tuesday March 27, 27 Jacques Guerber Vice-Chairman of the Management

Commercial Consumerism. Jeffrey Gundlach Chief Executive Officer Chief Investment Officer

Commercial Consumerism Jeffrey Gundlach Chief Executive Officer Chief Investment Officer June 23, 2010 Domestic Credit Market Debt as % of Gross Domestic Product 1929-2009 400% 350% Year 1 FDR Year 1 BHO

Commercial Consumerism Jeffrey Gundlach Chief Executive Officer Chief Investment Officer June 23, 2010 Domestic Credit Market Debt as % of Gross Domestic Product 1929-2009 400% 350% Year 1 FDR Year 1 BHO

Specific financial information Q2 10

04/ 08 / 2010 Specific financial information Q2 10 (based on FSF recommendations for financial transparency) We stand by you Contents Unhedged CDOs exposed to the US residential mortgage sector CDOs of

04/ 08 / 2010 Specific financial information Q2 10 (based on FSF recommendations for financial transparency) We stand by you Contents Unhedged CDOs exposed to the US residential mortgage sector CDOs of

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

American Financial Group, Inc.

Investor Supplement - Second Quarter 2013 July 29, 2013 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

Investor Supplement - Second Quarter 2013 July 29, 2013 American Financial Group, Inc. Corporate Headquarters Great American Insurance Group Tower 301 E Fourth Street Cincinnati, OH 45202 513 579 6739

KBW Mortgage Finance Conference. June 1, 2016

KBW Mortgage Finance Conference June 1, 2016 Safe Harbor Statement F O R W A R D - L O O K I N G S T A T E M ENTS This presentation includes forward-looking statements within the meaning of the safe harbor

KBW Mortgage Finance Conference June 1, 2016 Safe Harbor Statement F O R W A R D - L O O K I N G S T A T E M ENTS This presentation includes forward-looking statements within the meaning of the safe harbor

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer (Visiting Scholar, Federal Reserve Board and NY Fed; Columbia Business School; & NBER) Discussion Summarize results and provide commentary

Comments on Understanding the Subprime Mortgage Crisis Chris Mayer (Visiting Scholar, Federal Reserve Board and NY Fed; Columbia Business School; & NBER) Discussion Summarize results and provide commentary

Enterprises' Disclosure Technical Specification for UMBS & all Single Class Securities Version November 2016

Enterprises' Disclosure Technical Specification for UMBS & all Single Class Securities Table of Contents Table Page # Description File Header Definitions 2 The table providing the definitions of the column

Enterprises' Disclosure Technical Specification for UMBS & all Single Class Securities Table of Contents Table Page # Description File Header Definitions 2 The table providing the definitions of the column

Enterprises' Disclosure Technical Specification for UMBS & all Single Class Securities Version June 2016

Enterprises' Disclosure Technical Specification for UMBS & all Single Class Securities Table of Contents Table Page # Description File Header Definitions 2 The table providing the definitions of the column

Enterprises' Disclosure Technical Specification for UMBS & all Single Class Securities Table of Contents Table Page # Description File Header Definitions 2 The table providing the definitions of the column

Second Quarter 2018 Investor Presentation

Second Quarter 2018 Investor Presentation 1 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions of the

Second Quarter 2018 Investor Presentation 1 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions of the

Financial Guaranty Insurance Company RMBS and ABS CDOs as of June 30, October 9, 2007

Financial Guaranty Insurance Company RMBS and ABS CDOs as of June 30, 2007 October 9, 2007 Table of Contents Overview 3-5 Part I MBS 6 Underwriting 7-9 Portfolio 10-16 Performance 17-19 Part II ABS CDOs

Financial Guaranty Insurance Company RMBS and ABS CDOs as of June 30, 2007 October 9, 2007 Table of Contents Overview 3-5 Part I MBS 6 Underwriting 7-9 Portfolio 10-16 Performance 17-19 Part II ABS CDOs

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices?

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices? John M. Griffin and Gonzalo Maturana This appendix is divided into three sections. The first section shows that a

Internet Appendix for Did Dubious Mortgage Origination Practices Distort House Prices? John M. Griffin and Gonzalo Maturana This appendix is divided into three sections. The first section shows that a

ChimeraARCover:ChimeraARCover 3/24/08 9:05 PM Page C Annual Report

2007 Annual Report Letter from the CEO and President Dear Fellow Shareholders: It gives me great pleasure to write my first annual letter to the shareholders of Chimera Investment Corporation. Chimera

2007 Annual Report Letter from the CEO and President Dear Fellow Shareholders: It gives me great pleasure to write my first annual letter to the shareholders of Chimera Investment Corporation. Chimera

Defining Issues. Regulators Finalize Risk- Retention Rule for ABS. November 2014, No Key Facts. Key Impacts

Defining Issues November 2014, No. 14-50 Regulators Finalize Risk- Retention Rule for ABS Contents Summary of Final Rule... 2 Qualified Residential Mortgage Exemption... 4 Other Exemptions... 4 Risk Retention...

Defining Issues November 2014, No. 14-50 Regulators Finalize Risk- Retention Rule for ABS Contents Summary of Final Rule... 2 Qualified Residential Mortgage Exemption... 4 Other Exemptions... 4 Risk Retention...

Wholesale Rate Sheet

a new lock may be requested at the current market price without incurring the relock fee. 5 Days 0.150% Conventional Fixed Products 30 Year Fixed 20 Year Fixed Rate 30 Day Price 45 Day Price 60 Day Price

a new lock may be requested at the current market price without incurring the relock fee. 5 Days 0.150% Conventional Fixed Products 30 Year Fixed 20 Year Fixed Rate 30 Day Price 45 Day Price 60 Day Price

Fannie Mae 2010 First Quarter Credit Supplement. May 10, 2010

Fannie Mae 2010 First Quarter Credit Supplement May 10, 2010 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

Fannie Mae 2010 First Quarter Credit Supplement May 10, 2010 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

esf Securitisation Data Report Q3:2009 downloadable data click here for Prepared in partnership with

esf Securitisation Data Report Q3:2009 click here for downloadable data Prepared in partnership with Market Highlights and Commentary... 1 1. Issuance 1.1. European Historical Issuance... 3 1.2. US Historical

esf Securitisation Data Report Q3:2009 click here for downloadable data Prepared in partnership with Market Highlights and Commentary... 1 1. Issuance 1.1. European Historical Issuance... 3 1.2. US Historical

The following information concerning Wells Fargo Bank s prior originations and purchases of Prime Adjustable-Rate Loans is included in this file:

The following information concerning Wells Fargo Bank s prior originations and purchases of Prime Adjustable-Rate Loans is included in this file: summary information regarding original characteristics

The following information concerning Wells Fargo Bank s prior originations and purchases of Prime Adjustable-Rate Loans is included in this file: summary information regarding original characteristics

Invesco Mortgage Capital Inc Fourth Quarter Earnings Call February 22, 2017

Invesco Mortgage Capital Inc. 2016 Fourth Quarter Earnings Call February 22, 2017 Richard King President & Chief Executive Officer John Anzalone Chief Investment Officer Rob Kuster Chief Operating Officer

Invesco Mortgage Capital Inc. 2016 Fourth Quarter Earnings Call February 22, 2017 Richard King President & Chief Executive Officer John Anzalone Chief Investment Officer Rob Kuster Chief Operating Officer

First Quarter 2017 Earnings Call MAY 4, 2017

First Quarter 2017 Earnings Call MAY 4, 2017 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions of the

First Quarter 2017 Earnings Call MAY 4, 2017 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions of the

Memorandum. Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of

Memorandum Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto Consultant to mortgage-finance industry and chief credit officer at Fannie Mae in the

Memorandum Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto Consultant to mortgage-finance industry and chief credit officer at Fannie Mae in the

Capital Market Trends and Forecasts

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Future State MBS Disclosures June 2018

Future State MBS Disclosures June 2018 Frequently Asked Questions Listed below are common questions related to Fannie Mae s future Single-Family MBS disclosure files that are scheduled to be implemented

Future State MBS Disclosures June 2018 Frequently Asked Questions Listed below are common questions related to Fannie Mae s future Single-Family MBS disclosure files that are scheduled to be implemented

The US Institutional Corporate Loan Market and an Overview of Ways to Invest

The US Institutional Corporate Loan Market and an Overview of Ways to Invest Moderator: Elliot Ganz, LSTA Panelists: Gretchen Bergstresser, CVC David Mechlin, CSAM Dan Norman, Voya Tel Aviv, November 14,

The US Institutional Corporate Loan Market and an Overview of Ways to Invest Moderator: Elliot Ganz, LSTA Panelists: Gretchen Bergstresser, CVC David Mechlin, CSAM Dan Norman, Voya Tel Aviv, November 14,

Chapter 14. The Mortgage Markets. Chapter Preview

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Chapter 4. Characteristics of Bonds. Chapter 4 Topic Overview. Bond Characteristics

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

Mortgage Rates, Household Balance Sheets, and Real Economy

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Mortgage Market Statistical Annual 2017 Yearbook. Table of Contents

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

Fixed income. income investors. Michael Korber Head of Credit. August 2009

Fixed income Old lessons re-learned for income investors Michael Korber Head of Credit August 2009 Role of fixed income in a portfolio The role of fixed income in a portfolio a fixed or floating rate of

Fixed income Old lessons re-learned for income investors Michael Korber Head of Credit August 2009 Role of fixed income in a portfolio The role of fixed income in a portfolio a fixed or floating rate of

Securitization Market Trends Survey Report Issuance Trends in the First Half of Fiscal 2012

November, Japan Securities Dealers Association Japanese Bankers Association Securitization Market Trends Survey Report Issuance Trends in the First Half of Fiscal The following report is a summary of the

November, Japan Securities Dealers Association Japanese Bankers Association Securitization Market Trends Survey Report Issuance Trends in the First Half of Fiscal The following report is a summary of the

HSBC Global Investment Funds - Global Asset-Backed Bond

HSBC Global Investment Funds - Global Asset-Backed Bond S Share Class AM2 AM2 31/08/2018 Fund Objective and Strategy Investment Objective The Fund invests for long-term total return (meaning capital growth

HSBC Global Investment Funds - Global Asset-Backed Bond S Share Class AM2 AM2 31/08/2018 Fund Objective and Strategy Investment Objective The Fund invests for long-term total return (meaning capital growth

mortgages, bank loans and structured credit

mortgages, bank loans and structured credit Contents Introduction... 1 Nuts and Bolts Mortgage-Backed Securities... 2 Bank Loans... 10 Structured Credit... 13 Conclusion... 17 Behind the Industry Jargon...

mortgages, bank loans and structured credit Contents Introduction... 1 Nuts and Bolts Mortgage-Backed Securities... 2 Bank Loans... 10 Structured Credit... 13 Conclusion... 17 Behind the Industry Jargon...

Demystifying European Asset Backed Securities

Demystifying European Asset Backed Securities July 2017 2 We are fixed income specialists it is the only asset class we cover. Our focus is on preserving our investors capital and taking advantage of capital

Demystifying European Asset Backed Securities July 2017 2 We are fixed income specialists it is the only asset class we cover. Our focus is on preserving our investors capital and taking advantage of capital

RISKS ASSOCIATED WITH INVESTING IN BONDS

RISKS ASSOCIATED WITH INVESTING IN BONDS 1 Risks Associated with Investing in s Interest Rate Risk Effect of changes in prevailing market interest rate on values. As i B p. Credit Risk Creditworthiness

RISKS ASSOCIATED WITH INVESTING IN BONDS 1 Risks Associated with Investing in s Interest Rate Risk Effect of changes in prevailing market interest rate on values. As i B p. Credit Risk Creditworthiness

European Structured Finance Rating Transitions:

Special Comment February 2007 Contact Phone New York Jian Hu 1.212.553.1653 Hadas Alexander Julia Tung Richard Cantor London David Rosa 44.20.7772.5454 Frankfurt Detlef Scholz 49.69.70730.700 Paris Paul

Special Comment February 2007 Contact Phone New York Jian Hu 1.212.553.1653 Hadas Alexander Julia Tung Richard Cantor London David Rosa 44.20.7772.5454 Frankfurt Detlef Scholz 49.69.70730.700 Paris Paul

U.S. Subprime Rating Surveillance Update

U.S. Subprime Rating Surveillance Update Glenn Costello Managing Director July 2007 Agenda Rating Actions And The July 2007 Under Analysis List Risk Factors Affecting Performance and Ratings Going Forward

U.S. Subprime Rating Surveillance Update Glenn Costello Managing Director July 2007 Agenda Rating Actions And The July 2007 Under Analysis List Risk Factors Affecting Performance and Ratings Going Forward

Fannie Mae 2012 Second-Quarter Credit Supplement. August 8, 2012

Fannie Mae 2012 Second-Quarter Credit Supplement August 8, 2012 This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for

Fannie Mae 2012 Second-Quarter Credit Supplement August 8, 2012 This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for

Guidelines Correspondent. Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits:

LTV Limits:") Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Second Home Investment & Non- Owner Property Type Condominiums are ineligible for this product.

Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Second Home Investment & Non- Owner Property Type Condominiums are ineligible for this product.

The Financial Turmoil in 2007 and 2008 Events

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

Online Appendix. In this section, we rerun our main test with alternative proxies for the effect of revolving

Online Appendix 1. Addressing Scaling Issues In this section, we rerun our main test with alternative proxies for the effect of revolving rating analysts. We first address the possibility that our main

Online Appendix 1. Addressing Scaling Issues In this section, we rerun our main test with alternative proxies for the effect of revolving rating analysts. We first address the possibility that our main

CONFORMING LIBOR ARMS PROGRAM HIGHLIGHTS

Program Summary Loan Term & Program Category A 30 year conforming conventional LIBOR ARM that is fixed for the initial 3, 5, or 7 years then rolls into a one year ARM for the remainder of the loan term.

Program Summary Loan Term & Program Category A 30 year conforming conventional LIBOR ARM that is fixed for the initial 3, 5, or 7 years then rolls into a one year ARM for the remainder of the loan term.

I. Asset Valuation. The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset.

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

HLA Rate Sheet FOR INTERNAL USE ONLY. 95% LTV. Extensions 5 Days 0.150% 10 Days 0.200% 15 Days 0.250% 20 Days 0.300% 25 Days 0.350% 30 Days 0.

Lock desk is open from 9:30am to 4:30am (ET). Rates and prices are considered expired outside that window. PROMOTION 0.25% Yield credit on Conventional Fixed Products $200,000 or greater with credit score

Lock desk is open from 9:30am to 4:30am (ET). Rates and prices are considered expired outside that window. PROMOTION 0.25% Yield credit on Conventional Fixed Products $200,000 or greater with credit score

Default & Loss Rates of Structured Finance Securities:

SEPTEMBER 24, 2010 GLOBAL CREDIT POLICY SPECIAL COMMENT Default & Loss Rates of Structured Finance Securities: 1993-2009 Table of Contents: SUMMARY 1 THE DISTRIBUTION OF GLOBAL STRUCTURED FINANCE RATINGS

SEPTEMBER 24, 2010 GLOBAL CREDIT POLICY SPECIAL COMMENT Default & Loss Rates of Structured Finance Securities: 1993-2009 Table of Contents: SUMMARY 1 THE DISTRIBUTION OF GLOBAL STRUCTURED FINANCE RATINGS

Freddie Mac Servicer Conference November 14 Bulletin Freddie Mac Servicer Success Scorecard

Freddie Mac Servicer Conference 2014 November 14 Bulletin Freddie Mac Servicer Success Scorecard Overview The Freddie Mac Servicer Success Scorecard (Scorecard) drives Servicer behavior consistent with

Freddie Mac Servicer Conference 2014 November 14 Bulletin Freddie Mac Servicer Success Scorecard Overview The Freddie Mac Servicer Success Scorecard (Scorecard) drives Servicer behavior consistent with

Analysis of Asset Spread Benchmarks. Report by the Deloitte UConn Actuarial Center. April 2008

Analysis of Asset Spread Benchmarks Report by the Deloitte UConn Actuarial Center April 2008 Introduction This report studies the various benchmarks for analyzing the option-adjusted spreads of the major

Analysis of Asset Spread Benchmarks Report by the Deloitte UConn Actuarial Center April 2008 Introduction This report studies the various benchmarks for analyzing the option-adjusted spreads of the major

Fourth Quarter 2018 Earnings Call FEBRUARY 7, 2019

Fourth Quarter 2018 Earnings Call FEBRUARY 7, 2019 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions

Fourth Quarter 2018 Earnings Call FEBRUARY 7, 2019 Safe Harbor Statement FORWARD-LOOKING STATEMENTS This presentation includes forward-looking statements within the meaning of the safe harbor provisions

The New Landscape. David Bowman, Special Advisor Board of Governors

The New Landscape David Bowman, Special Advisor Board of Governors Estimates of US Dollar LIBOR Exposures, Market Participants Group Report (2014) Derivatives make up roughly 90 percent of all USD LIBOR

The New Landscape David Bowman, Special Advisor Board of Governors Estimates of US Dollar LIBOR Exposures, Market Participants Group Report (2014) Derivatives make up roughly 90 percent of all USD LIBOR

Fannie Mae 2014 Second Quarter Credit Supplement. August 7, 2014

Fannie Mae Second Quarter Credit Supplement August 7, This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for the quarter

Fannie Mae Second Quarter Credit Supplement August 7, This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for the quarter

Guidelines Correspondent. Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits:

LTV Limits:") Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Property Type w/o Sec Fin. PURCHASE MORTGAGES w/sec Fin. Max TLTV Max HTLTV Loan Limits 1 Unit

Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Property Type w/o Sec Fin. PURCHASE MORTGAGES w/sec Fin. Max TLTV Max HTLTV Loan Limits 1 Unit

Sub-prime mortgages are just a niche within the US residential mortgage

4 The sub-prime mortgage crisis: a synopsis Karen Weaver Sub-prime mortgages are just a niche within the US residential mortgage lending market, yet in 2007 they took centre stage in the global financial

4 The sub-prime mortgage crisis: a synopsis Karen Weaver Sub-prime mortgages are just a niche within the US residential mortgage lending market, yet in 2007 they took centre stage in the global financial

Merrill Lynch Conference

Merrill Lynch Conference Michael Fraizer Chairman and CEO February 12, 2008 2008 Genworth Financial, Inc. All rights reserved. Forward-Looking Statements This presentation contains forward-looking statements

Merrill Lynch Conference Michael Fraizer Chairman and CEO February 12, 2008 2008 Genworth Financial, Inc. All rights reserved. Forward-Looking Statements This presentation contains forward-looking statements

Conseco, Inc. Second Quarter 2008 Financial and Operating Results Presentation

Conseco, Inc. selected slides from our Second Quarter 2008 Financial and Operating Results Presentation (as filed in our Current Report on Form 8-K dated August 12, 2008) Key Debt Covenants CNO ($ millions)

Conseco, Inc. selected slides from our Second Quarter 2008 Financial and Operating Results Presentation (as filed in our Current Report on Form 8-K dated August 12, 2008) Key Debt Covenants CNO ($ millions)