Lessons from the Failures in Risk Management during The Subprime Crisis

|

|

|

- Alberta Barnett

- 5 years ago

- Views:

Transcription

1 Lessons from the Failures in Risk Management during The Subprime Crisis Michel Crouhy Head of Research & Development NATIXIS Corporate and Investment Bank Conference on Quantitative Risk Management In honour of Huyên Pham NATIXIS Foundation for Quantitative Research University Paris Diderot, September 18, 2009 Natixis 2006

2 Agenda I. Introduction II. Basics of securitization and the manufacturing of triple-a securities III. What went wrong in risk management and risk modeling? IV. Lessons from this fiasco V. Concluding remarks Presentation partly based on M. Crouhy, R. Jarrow and S. Turnbull: The Subprime Crisis, Journal of Derivatives, Fall 2008, , and M. Crouhy: Risk Management Failures during the Financial Crisis, to appear in the proceedings of the International Banking Conference sponsored by the FRB of Chicago and the European Central Bank: The Credit Market Turmoil of : Implications for Public Policy Chicago, September 25-26,

3 I. Introduction 3

4 The credit crisis of 2007 started in the subprime mortgage market in the U.S. but has affected investors all over the world and shut down the ABCP market, securitization. Hedge funds have halted redemptions or failed, SIVs have been wound-down: The amount of write-off could reach $ 2 trillion Banks have been taken over in Germany (Satchen and IKB) and Great Britain had its first bank run in 140 years and ended up nationalizing the troubled bank (Northern Rock) Libor and spreads over Libor for inter-bank lending has skyrocketed as banks don t trust each other U.S. banks had to call global investors such as sovereign funds for massive capital infusions Contagion affects other segments of the credit market Credit crunch and fear of deep economic recession 4

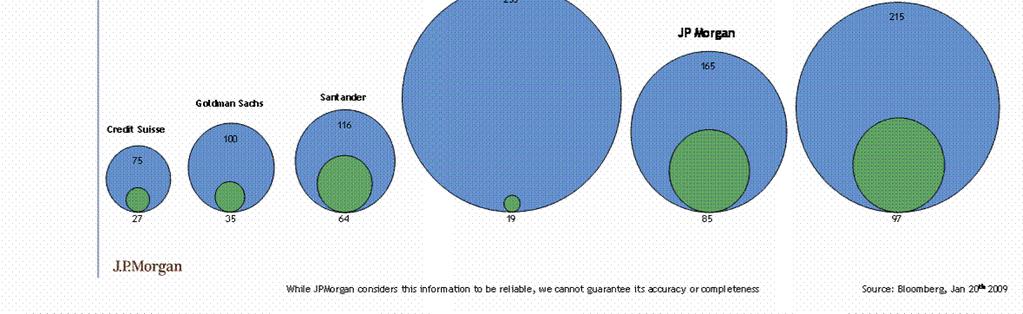

5 Bank Write Downs billions; through February 9, 2009 Wachovia Citi Merrill UBS UBS WaMu BofA HSBC JPMC National City Morgan Stanley Wells Fargo Deutsche Bank Lehman CS Goldman Bear Stearns* Total: $816 bn (and counting ) Total Capital Raise: $856bn 97.9 $- $10 $20 $30 $40 $50 $60 $70 $80 $90 $100 Source: Bloomberg (WDCI) 5

6 6

7 Background Delinquencies in the Subprime Market There were four reasons why delinquencies began to increase after mid Typical subprime borrowers are not very credit worthy often highly levered with high debt to income ratios, and often had mortgages with high loan-to-value ratios (often 100% or more). 2. In 2005/6 teaser loans had low fixed rates for the first two or three years, then re-set semi annually to an index plus margin. Short term mortgage rates began to increase from mid Many borrowers had counted on being able to re-finance or to sell their home. However in April 2005, home price appreciation began to decline. 4. A decline in lending standards and increased fraud. 7

8 8

9 Trigger to the Crisis The current crisis was thus an accident waiting to happen. The trigger was a series of events that striked out of the blue: In June 2007, attempt by Bear Sterns to bail out two hedge funds hurt by subprime mortgage losses then, attempt by Merrill Lynch to liquidate some of the funds assets revealed how illiquid the market for such securities has become. In July, first bailout by German regulators of IKB. In July also, BNP Paribas froze three investment funds with assets of 2 billion euros because the bank could not value the subprime assets in the funds. It seems that all of a sudden the market realized that MBSs, CDOs of ABS and other structured products were mispriced 9

10 Subprime index: , AAA 10

11 Subprime index: , BBB 11

12 II. Basics of securitization and the manufacturing of triple-a securities 12

13 SPV (Special Purpose Vehicule) Assets Liabilities Collateral (pool of assets) : Funding of tranches - Corporate investment grade loans - Leveraged loans - Mortgages - ABS (auto loans, credit card receivables, ) SENIOR MEZZANINE Junior/Equity 13

14 14

15 15

16 Basic Structure of a CDO of ABS or Mezz CDO Subprime Morgages Senior Tranche (75 %) AAA Mezzanine Tranche (20 %) BBB Equity Tranche (5 %) Not Rated The Mezzanine tranche is repackaged with other mezzanine tranches Senior Tranche (75 %) AAA Mezzanine Tranche (20 %) BBB Equity Tranche (5 %) A total of 90% of triple-a rated securities has then been created: 75% * 75% = 90% In practice: - RMBS: pools of approximately 3,000 individual mortgages - Mezz CDO: pools of approximately 100 mortgage bonds (80%) + a few CMBS, CDOs, 16

17 AAA/Aaa ABS CDO Securitization Residential Morgages RMBS Securities AA+/Aa1 AA/Aa2 AA-/Aa3 A+/A1 A/A2 A-/A3 BBB+/Baa1 BBB/Baa2 Mezzanine ABS CDO AAA/Aaa (Super Senior) AAA/Aaa (Mezz) AA/Aa2 A/A2 BBB-/Baa3 BB+/Ba1 BBB/Baa2 Equity AAA/Aaa CLO Securitization Senior Secured Corporate Loans CLO % AA/Aa2 A/A2 BBB/Baa2 BB/Ba2 Equity 17

18 III. What went wrong in risk management and risk modeling? 18

19 Over-reliance on: 1. Wrong ratings from rating agencies; 2. Unrealistically simple risk models, i.e., models which were not designed to deal with the complexity of structured credit products; 3. Inaccurate data; 4. Short-term financing with little consideration for liquidity risk. 5. Myopic risk analysis with no consideration to systemic risk As a consequence risks were massively underestimated 19

20 1. Over-reliance on suspicious ratings: 1. Example of a RMBS deal from New Century 20

21 Example of a deal from New Century 21

22 Example of a deal from New Century 22

23 Tranching for GSAMP Trust 2006-NC2 Tranche description Credit Ratings Coupon Rate Class Notional Width Sub S&P Moody s -1-2 A-1 $239,618, % 72.82% AAA Aaa 0.15% 0.30% A-2A $214,090, % 48.53% AAA Aaa 0.07% 0.14% A-2B $102,864, % 36.86% AAA Aaa 0.09% 0.18% A-2C $99,900, % 25.53% AAA Aaa 0.15% 0.30% A-2D $42,998, % 20.65% AAA Aaa 0.24% 0.48% M-1 $35,700, % 16.60% AA+ Aa1 0.30% 0.45% M-2 $28,649, % 13.35% AA Aa2 0.31% 0.47% M-3 $16,748, % 11.45% AA- Aa3 0.32% 0.48% M-4 $14,986, % 9.75% A+ A1 0.35% 0.53% M-5 $14,545, % 8.10% A A2 0.37% 0.56% M-6 $13,663, % 6.55% A- A3 0.46% 0.69% M-7 $12,341, % 5.15% BBB+ Baa1 0.90% 1.35% M-8 $11,019, % 3.90% BBB Baa2 1.00% 1.50% M-9 $7,052, % 3.10% BBB- Baa3 2.05% 3.08% B-1 $6,170, % 2.40% BB+ Ba1 2.50% 3.75% B-2 $8,815, % 1.40% BB Ba2 2.50% 3.75% X $12,340, % 0.00% NR NR N/A N/A 23

24 2. Reliance on oversimplified models which did not capture the full dimensionality of the risk being undertaken UBS: 2 nd largest bank in the world by total assets, end of 2006, winner of Euromoney magazine s Global Best Risk Management House award for excellence in 2005 As of August 2008: write-downs of $45 billion and capital infusion of $28 billion Post mortem shareholder report on UBS s write-downs indicates that short cuts were taken to speed up the production of risk reports. But these short cuts were systematically gamed so that risks were structured in such a way they did not show up at all in the calculations of risk. 24

25 Cliff effect or non-linearities in the risk of subprime CDO tranches Perhaps one of the biggest failing in the crisis was the failure to understand the binary (zero-one) nature of mortgage CDOs. The assets of a mortgage related CDO were subprime asset backed bonds. These bonds were themselves tranches on a pool of individual subprime mortgages. The typical CDO had pools of mortgage backed bonds rated double B to double A, average triple B. Average attachment point for the MB tranches was between 3 to 5% and the width was very thin from 2.5 to 4%. Assuming a recovery rate of 50% and a default rate of 20%, a realistic number in the current environment, then it was to be expected that triple B tranches would be hit. 25

26 In the current downturn in the housing market and a recessionary economic environment, if one triple B tranche is hit, then it is likely that other triple B tranches will be hit during the same period, especially given the thin width of the tranches. AB Bonds CDO Collateral Pool: Subprime mortgages Triple B bonds Collateral Pool: Triple B bonds Super senior tranches Either the cumulative default of the subprime mortgages keeps the MB bonds untouched and the super senior tranches will not incur losses, or the default rate wipes out the bonds and the super senior tranches. 26

27 3. Lack of data and inability to calibrate the models No history Regime change ignored by rating agencies, monolines and structurers in risk assessment and pricing 27

28 28

29 29

30 30

31 31

32 32

33 4. Huge reliance of banks and off-balance sheet vehicules on shortterm wholesale funding (Sachsen Bank, Northern Rock, Bear Sterns, ) SIVs invest in medium and long term highly rated assets and fund these purchases with short term asset backed commercial paper (ABCP), medium term notes (MTNs) and capital. The rating of the ABCP and MTNs relies on the ability of the SIV to roll over its debt. Each SIV must have multiple back stop lines of credit. However the ability to roll over debt also depends on the value of the collateral the assets of the SIV. The rating agencies do not consider valuation issues. Risk management systems ignored this as a credit or liquidity risk at best consider this risk as an operational risk. In the case of Sachsen the Dublin s affiliate engaged in investing in subprime CDOs had a back-up loan facility from the parent bank Sachsen itself approaching 25% of the total balance sheet of the parent bank! 33

34 5. Over-reliance on myopic risk analysis with no consideration to systemic risk. Monolines and insurance companies, e.g. AIG, sell insurance to guarantee timely payment on municipal bonds. During the last decade moved into the business of providing surety wraps for asset backed bonds and CDOs. Viewed as a highly profitable business. Systemic risk: If a monoline is downgraded, all of the paper it has insured must be downgraded. 1.This will cause holders of the paper to mark down their holdings under fair value accounting. 2. Enhanced money market funds that must hold assets rated at least triple- A, this means selling downgraded assets. 3. As more and more assets are marked down primary dealers, and other counterparties, are asking for more collateral, forcing selling assets (good and bad) at distressed prices in illiquid markets. 4. This downward spiral in asset prices triggers deleveraging and contagion to markets that are not directly related to subprime mortgages. 34

35 IV. Lessons from this fiasco 35

36 1. CDO tranches are different from corporate bonds : It is therefore necessary to model: 1. the cash flows generated by the assets in the collateral pool. 2. prepayments 3. default dependence among the assets 4. how the covariates that explain default by the assets varies over the life of the structure 5. the waterfall structure of the CDO The use of well understood assets, such as corporate bonds, as proxies for the risk of CDO tranches led to mistakes and underappreciation of risk. 36

37 1. CDO tranches are different from corporate bonds (cont.): Subprime ABS ratings differ from corporate debt ratings on a number of dimensions: - Corporate bond ratings are largely based on firm-specific risk, while CDO tranches represent claims on cash flows from a portfolio of correlated assets. - The rating of CDO tranches rely heavily on quantitative models, while corporate debt ratings rely essentially on the analyst s judgement. - Although the rating of a CDO tranche should have the same expected loss as a corporate bond for a given rating, the volatility of loss (unexpected loss) is quite different and strongly depend on the correlation structure of the underlying assets in the pool of the CDO. 37

38 1. CDO tranches are different from corporate bonds (cont.): Rating agencies, structurers and investors occulted the fact that: - the securitization process substitutes specific risks which are largely diversifiable in a benign economic environment, for systemic risk which is not diversifiable during a severe economic downturn as correlations increase risk is shifted from junior to senior tranches; - contrary to a corporate bond, small errors in the evaluation of PDs, LGDs, correlations can result in major changes in the expected loss of the senior tranches of a CDO, and consequently their rating (sensitivity is even higher for CDO-squareds such as subprime CDOs). As a consequence senior tranche holders should demand far larger risk premia than for holding a corporate bond with the same rating. 38

39 Basic Structure of a CDO of ABS or Mezz CDO Subprime Morgages Senior Tranche (75 %) AAA Mezzanine Tranche (20 %) BBB Equity Tranche (5 %) Not Rated The Mezzanine tranche is repackaged with other mezzanine tranches Senior Tranche (75 %) AAA Mezzanine Tranche (20 %) BBB Equity Tranche (5 %) A total of 90% of triple-a rated securities has then been created: 75% * 75% = 90% Leverage effect: Assume a loss rate on the underlying mortgage portfolios of 20% - MBS: 5% of losses borne by the equity tranche and 15% by the mezzanine tranche The mezz has 20% of principal so that 15/20 = 75% of the principal of each MBS is lost - ABS CDO: Each underlying asset bears a 75% lost 5% is borne by the equity, 20% by the mezz and 50% by the senior tranche, i.e. 50/75 = 66.7% of its principal 39

40 2. Check the quality of the data about the underlying assets and make sure it is complete and timely Given the use of historical data, it did not reflect the changing nature of the subprime market declining lending standards, the growing number of no document mortgages, high loan to value mortgages. Normally mortgages have high recovery rates. But with high debt to value ratios, declining home prices, this was not longer the case. Again, this was not reflected in the data used to rate the CDOs. Rating agencies receive data from the issuers and arrangers and assumed that appropriate due diligence has been performed. They do not check the quality of the data. 40

41 2. Check the quality of the data about the underlying assets and make sure it is complete and timely (Cont.) It is essential to perform due diligence on the raw data neither the rating agencies nor the banks which structured the CDOs have done it. (The situation is analogous to an accountant accepting at face value the figures given to them - no auditing function) 41

42 3. A major source of model risk is the accuracy of the key parameters in the valuation of a CDO: Need to calibrate forward looking PDs, LGDs, default correlations, prepayment rates. PDs: For CDOs we can extract the term structure of PDs from the term structure of CDSs (assuming some recovery rate). But for MBSs there is only one maturity the maturity of the bond. 42

43 LGDs: For mortgages, LGDs depend more than for corporates on the state of the economy and of the housing market at the time of default. Default correlations: Clearly, there are at least two regimes: Normal markets (20%) «crisis» regime where correlation jump to a level close to 1 (at least in some geographic areas with similar socio-professional characteristics) 43

44 Prepayment: Prepayment is hard to predict because it will depend on the future course of interest rates and also on "non-economic" factors. These include: people move, borrowers default transactions costs affect the refinancing decision "non-rational" reasons, such as lack of information, may cause suboptimal prepayment behavior 44

45 4. In a market that can produce unprecedented price moves and significant tail risk: Risk assessment cannot rely on a single risk metric, i.e., VaR At least, there is a need to complement traditional risk measures by well designed, consistent, stress testing and scenario analysis that include business cycle stresses as well as event specific tail risks. Ensure that the methodology identifies and takes into account: - concentration risk - correlation risk - liquidity risk (need a dynamic framework) and covers on-balance sheet as well as off-balance sheet assets. 45

46 5. Do not neglect wrong-way way correlation risk : In the light of what happened with the monolines it is important to account for the risk that the deterioration of the quality of the assets is concomitant with a significant increase in the risk of default of the counterparty. 46

47 6. Derivatives are marked-to-market or marked-to-model Risk Management should run worst-case scenarios to measure the risk of future collateral calls and write-downs which can have a devastating effect on the finances of the firm. AIG has been forced to post about $50 billion in collateral to its trading partners to offset drops in the value of securities it insured with credit default swaps, and has written-down several billion dollars. No scenario was run that considered a sharp drop in housing prices. 47

48 V. Concluding Remarks 48

49 Detailed analytic description of Risk Management Policy, Methodology and Infrastructure framework Comprehensive user friendly description of Risk Management 49

50 Conclusion Dad was in mortgage securitization Please, no subprime! 50

II. What went wrong in risk modeling. IV. Appendix: Need for second generation pricing models for credit derivatives

Risk Models and Model Risk Michel Crouhy NATIXIS Corporate and Investment Bank Federal Reserve Bank of Chicago European Central Bank Eleventh Annual International Banking Conference: : Implications for

Risk Models and Model Risk Michel Crouhy NATIXIS Corporate and Investment Bank Federal Reserve Bank of Chicago European Central Bank Eleventh Annual International Banking Conference: : Implications for

7 Deadly Frictions in Subprime Mortgage Securitization

7 Deadly Frictions in Subprime Mortgage Securitization Adam Ashcraft, Til Schuermann FRBNY Research Q-Group, October 2008 Bank Write Downs billions; through September 25, 2008 Citi 55.1 Merrill 52.2 UBS

7 Deadly Frictions in Subprime Mortgage Securitization Adam Ashcraft, Til Schuermann FRBNY Research Q-Group, October 2008 Bank Write Downs billions; through September 25, 2008 Citi 55.1 Merrill 52.2 UBS

Global Financial Crisis

Global Financial Crisis Hand in the homework that is due today What caused the Global Financial Crisis? We ll focus today on Financial Innovation and Regulatory Issues Other issues have been cited, including

Global Financial Crisis Hand in the homework that is due today What caused the Global Financial Crisis? We ll focus today on Financial Innovation and Regulatory Issues Other issues have been cited, including

Financial Guaranty Insurance Company RMBS and ABS CDOs as of June 30, October 9, 2007

Financial Guaranty Insurance Company RMBS and ABS CDOs as of June 30, 2007 October 9, 2007 Table of Contents Overview 3-5 Part I MBS 6 Underwriting 7-9 Portfolio 10-16 Performance 17-19 Part II ABS CDOs

Financial Guaranty Insurance Company RMBS and ABS CDOs as of June 30, 2007 October 9, 2007 Table of Contents Overview 3-5 Part I MBS 6 Underwriting 7-9 Portfolio 10-16 Performance 17-19 Part II ABS CDOs

Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II

Derivatives Markets, Part II") November 2011 Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II A Review of Monoline Exposures Introduction This past August, ISDA published a short paper

November 2011 Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II A Review of Monoline Exposures Introduction This past August, ISDA published a short paper

The Financial Turmoil in 2007 and 2008 Events

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

The Financial Turmoil in 2007 and 2008

The Financial Turmoil in 2007 and 2008 Gerald P. Dwyer June 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal Reserve System

The Financial Turmoil in 2007 and 2008 Gerald P. Dwyer June 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal Reserve System

Credit Ratings and Securitization

Credit Ratings and Securitization Bachelier Congress June 2010 John Hull 1 Agenda To examine the derivatives that were created from subprime mortgages To determine whether the criteria used by rating agencies

Credit Ratings and Securitization Bachelier Congress June 2010 John Hull 1 Agenda To examine the derivatives that were created from subprime mortgages To determine whether the criteria used by rating agencies

Security Capital Assurance Ltd Structured Finance Investor Call. August 3, 2007

Security Capital Assurance Ltd Structured Finance Investor Call August 3, 2007 Important Notice This presentation provides certain information regarding Security Capital Assurance Ltd (SCA). By accepting

Security Capital Assurance Ltd Structured Finance Investor Call August 3, 2007 Important Notice This presentation provides certain information regarding Security Capital Assurance Ltd (SCA). By accepting

The State of New York Deferred Compensation Board Stable Income Fund INVESTMENT POLICIES AND GUIDELINES. Table of Contents

The State of New York Deferred Compensation Board Stable Income Fund INVESTMENT POLICIES AND GUIDELINES June 12, 2009 Table of Contents I. Investment Objectives II. Investment Strategy A. Permitted Investments

The State of New York Deferred Compensation Board Stable Income Fund INVESTMENT POLICIES AND GUIDELINES June 12, 2009 Table of Contents I. Investment Objectives II. Investment Strategy A. Permitted Investments

Selected Exposures based on recommendations of the Financial Stability Board

Selected Exposures based on recommendations of the Financial Stability Board As at 31 December 2009 1 Disclaimer Figures included in this presentation are unaudited. This presentation includes forward-looking

Selected Exposures based on recommendations of the Financial Stability Board As at 31 December 2009 1 Disclaimer Figures included in this presentation are unaudited. This presentation includes forward-looking

1.2 Product nature of credit derivatives

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

March 2017 For intermediaries and professional investors only. Not for further distribution.

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

Inside Scoop on ABCP Debacle. June 8, Daryl Ching

CIFPs 7 th Annual National Conference Inside Scoop on ABCP Debacle June 8, 2009 Daryl Ching Transaction Diagram Traditional Securitization A securitization transactions involves multiple parties that all

CIFPs 7 th Annual National Conference Inside Scoop on ABCP Debacle June 8, 2009 Daryl Ching Transaction Diagram Traditional Securitization A securitization transactions involves multiple parties that all

The Sub Prime Debacle and Financial Turmoil

The Sub Prime Debacle and Financial Turmoil Presented at the 13th Finsia and Melbourne Centre for Financial Studies Banking and Finance Conference Monday 29th and Tuesday 30th September, 2008 The University

The Sub Prime Debacle and Financial Turmoil Presented at the 13th Finsia and Melbourne Centre for Financial Studies Banking and Finance Conference Monday 29th and Tuesday 30th September, 2008 The University

The Subprime Crisis. Literature: Blanchard, O. (2009), The Crisis: Basic Mechanisms, and Appropriate Policies, IMF, WP 09/80.

, The Crisis: Basic Mechanisms, and Appropriate Policies, IMF, WP 09/80.") The Subprime Crisis Literature: Blanchard, O. (2009), The Crisis: Basic Mechanisms, and Appropriate Policies, IMF, WP 09/80. Hellwig, Martin (2008), The Causes of the Financial Crisis, CESifo Forum 9 (4),

The Subprime Crisis Literature: Blanchard, O. (2009), The Crisis: Basic Mechanisms, and Appropriate Policies, IMF, WP 09/80. Hellwig, Martin (2008), The Causes of the Financial Crisis, CESifo Forum 9 (4),

Pierpont Securities LLC. pierpontsecurities.com 2012 Pierpont Securities, a member of FINRA and SIPC

Pierpont Securities LLC SECURITIZATION OVERVIEW SECURITIZATION Section I: Section II: Section III: Appendix: Definition Process Analysis Market Defined Terms P R O P R I E T A R Y A N D C O N F I D E N

Pierpont Securities LLC SECURITIZATION OVERVIEW SECURITIZATION Section I: Section II: Section III: Appendix: Definition Process Analysis Market Defined Terms P R O P R I E T A R Y A N D C O N F I D E N

Selected exposures based on recommendations of the Financial Stability Board. 04 May 2011

Selected exposures based on recommendations of the Financial Stability Board 04 May 2011 1 Disclaimer The exposures based on the recommendation of the Financial Stability Board as at 31March 2011 are not

Selected exposures based on recommendations of the Financial Stability Board 04 May 2011 1 Disclaimer The exposures based on the recommendation of the Financial Stability Board as at 31March 2011 are not

Selected Exposures based on recommendations of the Financial Stability Board

Selected Exposures based on recommendations of the Financial Stability Board As at 30 June 2010 1 Disclaimer Figures included in this presentation are unaudited. On 19 April 2010, BNP Paribas issued a

Selected Exposures based on recommendations of the Financial Stability Board As at 30 June 2010 1 Disclaimer Figures included in this presentation are unaudited. On 19 April 2010, BNP Paribas issued a

RISK. Investor Community Conference Call REVIEW. BOB McGLASHAN Executive Vice President and Chief Risk Officer. November

Q4 2007 RISK REVIEW Investor Community Conference Call BOB McGLASHAN Executive Vice President and Chief Risk Officer November 27 2007 FORWARD LOOKING STATEMENTS CAUTION REGARDING FORWARD-LOOKING STATEMENTS

Q4 2007 RISK REVIEW Investor Community Conference Call BOB McGLASHAN Executive Vice President and Chief Risk Officer November 27 2007 FORWARD LOOKING STATEMENTS CAUTION REGARDING FORWARD-LOOKING STATEMENTS

Navigating through difficult waters Dr. Hugo Banziger

Navigating through difficult waters Dr. Hugo Banziger Chief Risk Officer Merrill Lynch Wholesale Banking Risk Seminar London, 12 September 2007 Sub-prime mortgage woes unfold in three phases Concerns have

Navigating through difficult waters Dr. Hugo Banziger Chief Risk Officer Merrill Lynch Wholesale Banking Risk Seminar London, 12 September 2007 Sub-prime mortgage woes unfold in three phases Concerns have

Wie schlecht waren Ratings von Verbriefungen wirklich? Und warum?

Wie schlecht waren Ratings von Verbriefungen wirklich? Und warum? Daniel Rösch Leibniz Universität Hannover Hamburg, December 3, 2010 Default Rates of Bonds vs. MBS/HEL Securitizations Quotation Cornell

Wie schlecht waren Ratings von Verbriefungen wirklich? Und warum? Daniel Rösch Leibniz Universität Hannover Hamburg, December 3, 2010 Default Rates of Bonds vs. MBS/HEL Securitizations Quotation Cornell

Tom Flynn Executive Vice President and Chief Risk Officer

Investor Community Conference Call 2008 Risk Review Tom Flynn Executive Vice President and Chief Risk Officer May 27 2008 Forward Looking Statements Caution Regarding Forward-Looking Statements Bank of

Investor Community Conference Call 2008 Risk Review Tom Flynn Executive Vice President and Chief Risk Officer May 27 2008 Forward Looking Statements Caution Regarding Forward-Looking Statements Bank of

The Financial Crisis. Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

Measuring the impact of securitization on imputed bank output

Measuring the impact of securitization on imputed bank output Adam B. Ashcraft * Research Officer Financial Intermediation Function Federal Reserve Bank of New York adam.ashcraft@ny.frb.org Charles Steindel

Measuring the impact of securitization on imputed bank output Adam B. Ashcraft * Research Officer Financial Intermediation Function Federal Reserve Bank of New York adam.ashcraft@ny.frb.org Charles Steindel

The Financial Crisis and the Bailout

The Financial Crisis and the Bailout Steven Kaplan University of Chicago Graduate School of Business 1 S. Kaplan Intro This talk: What is the problem? How did we get here? What do we need to do? What does

The Financial Crisis and the Bailout Steven Kaplan University of Chicago Graduate School of Business 1 S. Kaplan Intro This talk: What is the problem? How did we get here? What do we need to do? What does

The Financial Crisis of 2008 and Subprime Securities. Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis of 2008 and Subprime Securities Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Paula Tkac Federal Reserve Bank of Atlanta Subprime mortgages are commonly

The Financial Crisis of 2008 and Subprime Securities Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Paula Tkac Federal Reserve Bank of Atlanta Subprime mortgages are commonly

The Future of Securitization

The Future of Securitization Günter Franke University of Konstanz (Germany), CFS Jan P. Krahnen Goethe University (Frankfurt, Germany), CFS, CEPR Brookings-Tokyo Club-Wharton Conference Washington - October

The Future of Securitization Günter Franke University of Konstanz (Germany), CFS Jan P. Krahnen Goethe University (Frankfurt, Germany), CFS, CEPR Brookings-Tokyo Club-Wharton Conference Washington - October

Understanding Investments in Collateralized Loan Obligations ( CLOs )

") Understanding Investments in Collateralized Loan Obligations ( CLOs ) Disclaimer This document contains the current, good faith opinions of Ares Management Corporation ( Ares ). The document is meant for

Understanding Investments in Collateralized Loan Obligations ( CLOs ) Disclaimer This document contains the current, good faith opinions of Ares Management Corporation ( Ares ). The document is meant for

Information, Liquidity, and the (Ongoing) Panic of 2007*

Panic of 2007*") Information, Liquidity, and the (Ongoing) Panic of 2007* Gary Gorton Yale School of Management and NBER Prepared for AER Papers & Proceedings, 2009. This version: December 31, 2008 Abstract The credit

Information, Liquidity, and the (Ongoing) Panic of 2007* Gary Gorton Yale School of Management and NBER Prepared for AER Papers & Proceedings, 2009. This version: December 31, 2008 Abstract The credit

1 U.S. Subprime Crisis

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

THE ABCP MARKET Anatomy of a Meltdown

THE ABCP MARKET Anatomy of a Meltdown November 2007 Colin Kilgour, Connor Clark & Lunn Wholesale Finance AGENDA Objectives The Canadian ABCP Market The Market Disruption Key Lessons Going Forward 2 Objectives

THE ABCP MARKET Anatomy of a Meltdown November 2007 Colin Kilgour, Connor Clark & Lunn Wholesale Finance AGENDA Objectives The Canadian ABCP Market The Market Disruption Key Lessons Going Forward 2 Objectives

Notice regarding Revisions of Earnings Forecasts

To Whom It May Concern October 31, 2008 Listed Company: Mitsubishi UFJ Financial Group, Inc. Representative: Nobuo Kuroyanagi, President (Code:8306) Notice regarding Revisions of Earnings Forecasts Mitsubishi

To Whom It May Concern October 31, 2008 Listed Company: Mitsubishi UFJ Financial Group, Inc. Representative: Nobuo Kuroyanagi, President (Code:8306) Notice regarding Revisions of Earnings Forecasts Mitsubishi

Financial innovation and the financial crisis of 2007 and 2008: A Coincidence?

Financial innovation and the financial crisis of 2007 and 2008: A Coincidence? Abstract Financial innovation is blamed to be responsible for the financial crisis of 2007 and 2008. This research analyzes

Financial innovation and the financial crisis of 2007 and 2008: A Coincidence? Abstract Financial innovation is blamed to be responsible for the financial crisis of 2007 and 2008. This research analyzes

Basel II Pillar 3 disclosures 6M 09

Basel II Pillar 3 disclosures 6M 09 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group

Basel II Pillar 3 disclosures 6M 09 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks Presentation for Bank of Italy Workshop on ABM in Banking and Finance: Turin Feb 9-11 Sheri Markose,, Yang Dong, Bewaji Oluwasegun

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks Presentation for Bank of Italy Workshop on ABM in Banking and Finance: Turin Feb 9-11 Sheri Markose,, Yang Dong, Bewaji Oluwasegun

COLLATERALIZED LOAN OBLIGATIONS (CLO) Dr. Janne Gustafsson

Dr. Janne Gustafsson") COLLATERALIZED LOAN OBLIGATIONS (CLO) 4.12.2017 Dr. Janne Gustafsson OUTLINE 1. Structured Credit 2. Collateralized Loan Obligations (CLOs) 3. Pricing of CLO tranches 2 3 Structured Credit WHAT IS STRUCTURED

COLLATERALIZED LOAN OBLIGATIONS (CLO) 4.12.2017 Dr. Janne Gustafsson OUTLINE 1. Structured Credit 2. Collateralized Loan Obligations (CLOs) 3. Pricing of CLO tranches 2 3 Structured Credit WHAT IS STRUCTURED

Capital Market Trends and Forecasts

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Specific financial information Q3 08

03/ 11/2008 Specific financial information Q3 08 (based on FSF recommendations for financial transparency) Contents Unhedged CDOs exposed to the US residential mortgage sector Write-downs on assets of

03/ 11/2008 Specific financial information Q3 08 (based on FSF recommendations for financial transparency) Contents Unhedged CDOs exposed to the US residential mortgage sector Write-downs on assets of

The Search for the Real Causes of the Current Global Financial Crisis: Role of Financial Innovations

The Search for the Real Causes of the Current Global Financial Crisis: Role of Financial Innovations Presentation at The Korea Institute for International Economic Policy Seoul, Korea Yoon-shik Park Professor

The Search for the Real Causes of the Current Global Financial Crisis: Role of Financial Innovations Presentation at The Korea Institute for International Economic Policy Seoul, Korea Yoon-shik Park Professor

In various tables, use of - indicates not meaningful or not applicable.

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

ESF Securitisation. Data Report

ESF Securitisation Data Report Autumn 2007 www.europeansecuritisation.com European Securitisation Forum St. Michael s House 1 George Yard London EC3V 9DH T +44.20.77 43 93 11 F +44.20.77 43 93 01 www.europeansecuritisation.com

ESF Securitisation Data Report Autumn 2007 www.europeansecuritisation.com European Securitisation Forum St. Michael s House 1 George Yard London EC3V 9DH T +44.20.77 43 93 11 F +44.20.77 43 93 01 www.europeansecuritisation.com

Beryl Credit Pulse on Structured Finance

Beryl Credit Pulse on Structured Finance This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the structured finance sector in light of the events of the past

Beryl Credit Pulse on Structured Finance This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the structured finance sector in light of the events of the past

KBW Diversified Financials Conference Douglas Renfield-Miller Executive Vice President, Ambac Financial Group. June 4, 2008

KBW Diversified Financials Conference Douglas Renfield-Miller Executive Vice President, Ambac Financial Group June 4, 2008. Key Messages Strong capital and liquidity Exceed Moody s and S&P s Triple-A target

KBW Diversified Financials Conference Douglas Renfield-Miller Executive Vice President, Ambac Financial Group June 4, 2008. Key Messages Strong capital and liquidity Exceed Moody s and S&P s Triple-A target

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

The Credit Crisis in Commercial Real Estate

The Credit Crisis in Commercial Real Estate 1 Summary Commercial real estate accounts for a meaningful 6% of GDP Commercial real estate entered the downturn reasonably well balanced However, $400 billion

The Credit Crisis in Commercial Real Estate 1 Summary Commercial real estate accounts for a meaningful 6% of GDP Commercial real estate entered the downturn reasonably well balanced However, $400 billion

The Role of Counterparty Risk in the Credit Crisis

The Role of Counterparty Risk in the Credit Crisis Jon Gregory jon@oftraining.com www.oftraining.com Jon Gregory (jon@oftraining.com), Credit Risk Summit, 15 th October 2009 page 1 Jon Gregory (jon@oftraining.com),

The Role of Counterparty Risk in the Credit Crisis Jon Gregory jon@oftraining.com www.oftraining.com Jon Gregory (jon@oftraining.com), Credit Risk Summit, 15 th October 2009 page 1 Jon Gregory (jon@oftraining.com),

AXIS Capital Holdings Limited. Investment Portfolio Supplemental Information and Data March 31, 2010

AXIS Capital Holdings Limited Investment Portfolio Supplemental Information and Data March 31, 2010 Cautionary Note on Forward Looking Statements Statements in this presentation that are not historical

AXIS Capital Holdings Limited Investment Portfolio Supplemental Information and Data March 31, 2010 Cautionary Note on Forward Looking Statements Statements in this presentation that are not historical

Semper MBS Total Return Fund. Semper Short Duration Fund. Prospectus March 30, 2018

Semper MBS Total Return Fund Class A Institutional Class Investor Class SEMOX SEMMX SEMPX Semper Short Duration Fund Institutional Class Investor Class SEMIX SEMRX (Each a Fund, together the Funds ) Each

Semper MBS Total Return Fund Class A Institutional Class Investor Class SEMOX SEMMX SEMPX Semper Short Duration Fund Institutional Class Investor Class SEMIX SEMRX (Each a Fund, together the Funds ) Each

Bank Capital Relief. October 2018

Bank Capital Relief October 2018 Table of contents Executive summary.... 1 What is a bank capital relief strategy?... 1 Role within a portfolio... 4 Potential considerations... 4 Conclusion... 6 Executive

Bank Capital Relief October 2018 Table of contents Executive summary.... 1 What is a bank capital relief strategy?... 1 Role within a portfolio... 4 Potential considerations... 4 Conclusion... 6 Executive

Basel II Pillar 3 disclosures

Basel II Pillar 3 disclosures 6M12 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

Basel II Pillar 3 disclosures 6M12 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

Insurance. Financial Guarantors Subprime Risks: From RMBS to ABS CDOs. Special Comment. Moody s Global. Summary Opinion.

www.moodys.com Special Comment Moody s Global Insurance September 2007 Table of Contents: Summary Opinion 1 Where to Find Subprime Mortgages: A Primer on Financial Engineering 3 Risks of Direct Subprime

www.moodys.com Special Comment Moody s Global Insurance September 2007 Table of Contents: Summary Opinion 1 Where to Find Subprime Mortgages: A Primer on Financial Engineering 3 Risks of Direct Subprime

European Structured Finance Rating Transitions:

Special Comment February 2007 Contact Phone New York Jian Hu 1.212.553.1653 Hadas Alexander Julia Tung Richard Cantor London David Rosa 44.20.7772.5454 Frankfurt Detlef Scholz 49.69.70730.700 Paris Paul

Special Comment February 2007 Contact Phone New York Jian Hu 1.212.553.1653 Hadas Alexander Julia Tung Richard Cantor London David Rosa 44.20.7772.5454 Frankfurt Detlef Scholz 49.69.70730.700 Paris Paul

Queensland Treasury Corporation

QTC - 45 Queensland Treasury Corporation ROLE Founded in 1988, Queensland Treasury Corporation (QTC) is a corporation sole, constituted by the Under Treasurer in accordance with the Queensland Treasury

QTC - 45 Queensland Treasury Corporation ROLE Founded in 1988, Queensland Treasury Corporation (QTC) is a corporation sole, constituted by the Under Treasurer in accordance with the Queensland Treasury

CDO Market Overview & Outlook. CDOs in the Heartland. Lang Gibson Director of Structured Credit Research March 25, 2004

CDO Market Overview & Outlook CDOs in the Heartland Lang Gibson Director of Structured Credit Research March 25, 24 23 featured record volumes despite diminishing arbitrage Global CDO Growth: 1995-23 $

CDO Market Overview & Outlook CDOs in the Heartland Lang Gibson Director of Structured Credit Research March 25, 24 23 featured record volumes despite diminishing arbitrage Global CDO Growth: 1995-23 $

Credit Derivatives. By A. V. Vedpuriswar

Credit Derivatives By A. V. Vedpuriswar September 17, 2017 Historical perspective on credit derivatives Traditionally, credit risk has differentiated commercial banks from investment banks. Commercial

Credit Derivatives By A. V. Vedpuriswar September 17, 2017 Historical perspective on credit derivatives Traditionally, credit risk has differentiated commercial banks from investment banks. Commercial

The Arbitrage CDO Market

Global Markets Research Relative Value March 21, 2000 Table of Contents Introduction: Lay of the land... 2 Cash Flow CDOs: Managing Default Risk. 4 Market Value CDOs: Managing Price Risk... 13 Risk & Return:

Global Markets Research Relative Value March 21, 2000 Table of Contents Introduction: Lay of the land... 2 Cash Flow CDOs: Managing Default Risk. 4 Market Value CDOs: Managing Price Risk... 13 Risk & Return:

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know April13, 2010 Agenda Introduction Presentation Steve Herscovici, Managing Principal, Analysis Group Bill Chambers, Finance

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know April13, 2010 Agenda Introduction Presentation Steve Herscovici, Managing Principal, Analysis Group Bill Chambers, Finance

The Mortgage Debt Market: A Tragedy

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

Tranche Warfare, CDOs in Default

2008 ANNUAL MEETING AND EDUCATION CONFERENCE American College of Investment Counsel New York, NY Tranche Warfare, CDOs in Default 9:30 a.m. - 10:30 a.m. October 24, 2008 MODERATOR: Cynthia J. Williams

2008 ANNUAL MEETING AND EDUCATION CONFERENCE American College of Investment Counsel New York, NY Tranche Warfare, CDOs in Default 9:30 a.m. - 10:30 a.m. October 24, 2008 MODERATOR: Cynthia J. Williams

Securitisation: Benefits for Emerging Markets and Lessons from the Global Financial Crisis

Securitisation: Benefits for Emerging Markets and Lessons from the Global Financial Crisis SEC Securities Markets Workshop Washington DC May 1, 2009 1 Securitisation: Benefits for Emerging Markets Investors

Securitisation: Benefits for Emerging Markets and Lessons from the Global Financial Crisis SEC Securities Markets Workshop Washington DC May 1, 2009 1 Securitisation: Benefits for Emerging Markets Investors

Section 1. Long Term Risk

Section 1 Long Term Risk 1 / 49 Long Term Risk Long term risk is inherently credit risk, that is the risk that a counterparty will fail in some contractual obligation. Market risk is of course capable

Section 1 Long Term Risk 1 / 49 Long Term Risk Long term risk is inherently credit risk, that is the risk that a counterparty will fail in some contractual obligation. Market risk is of course capable

Applications of CDO Modeling Techniques in Credit Portfolio Management

Applications of CDO Modeling Techniques in Credit Portfolio Management Christian Bluhm Credit Portfolio Management (CKR) Credit Suisse, Zurich Date: October 12, 2006 Slide Agenda* Credit portfolio management

Applications of CDO Modeling Techniques in Credit Portfolio Management Christian Bluhm Credit Portfolio Management (CKR) Credit Suisse, Zurich Date: October 12, 2006 Slide Agenda* Credit portfolio management

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Safe Harbor Statement

Third Quarter 2009 Safe Harbor Statement All statements made during today s investor presentation and in these webcast slides that address events, developments or results that we expect or anticipate may

Third Quarter 2009 Safe Harbor Statement All statements made during today s investor presentation and in these webcast slides that address events, developments or results that we expect or anticipate may

Strategic Mortgage Income Fund 3Q 2015 Presentation

Strategic Mortgage Income Fund 3Q 2015 Presentation October 22 nd, 2015 Nothing presented herein is intended to constitute investment advice and no investment decision should be made based on any information

Strategic Mortgage Income Fund 3Q 2015 Presentation October 22 nd, 2015 Nothing presented herein is intended to constitute investment advice and no investment decision should be made based on any information

Specific financial information Q1 10

05 / 05 / 2010 Specific financial information Q1 10 (based on FSF recommendations for financial transparency) We stand by you Contents Unhedged CDOs exposed to the US residential mortgage sector CDOs of

05 / 05 / 2010 Specific financial information Q1 10 (based on FSF recommendations for financial transparency) We stand by you Contents Unhedged CDOs exposed to the US residential mortgage sector CDOs of

P2.T6. Credit Risk Measurement & Management. Michael Crouhy, Dan Galai and Robert Mark, The Essentials of Risk Management, 2nd Edition

P2.T6. Credit Risk Measurement & Management Michael Crouhy, Dan Galai and Robert Mark, The Essentials of Risk Management, 2nd Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com

P2.T6. Credit Risk Measurement & Management Michael Crouhy, Dan Galai and Robert Mark, The Essentials of Risk Management, 2nd Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com

Lessons of the Subprime Crisis for Corporate Governance, Risk Management and Valuation

for Corporate Governance, Risk Management and Valuation Conference on the Future of Credit Default Swaps Sponsored by Atlantic Legal Foundation and Pillsbury November 6, 2008 Rick Grove CEO, LLC 212-949-1181

for Corporate Governance, Risk Management and Valuation Conference on the Future of Credit Default Swaps Sponsored by Atlantic Legal Foundation and Pillsbury November 6, 2008 Rick Grove CEO, LLC 212-949-1181

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

RETURN ENHANCEMENT WITH EUROPEAN ABS AND BANK LOANS IN SWISS INSTITUTIONAL PORTFOLIOS

H E A L T H W E A L T H C A R E E R RETURN ENHANCEMENT WITH EUROPEAN ABS AND BANK LOANS IN SWISS INSTITUTIONAL PORTFOLIOS JUNE 2017 INTRODUCTION In the aftermath of the global financial crisis, conventional

H E A L T H W E A L T H C A R E E R RETURN ENHANCEMENT WITH EUROPEAN ABS AND BANK LOANS IN SWISS INSTITUTIONAL PORTFOLIOS JUNE 2017 INTRODUCTION In the aftermath of the global financial crisis, conventional

Basel Committee on Banking Supervision. The Joint Forum. Credit Risk Transfer. Developments from 2005 to 2007

Basel Committee on Banking Supervision The Joint Forum Credit Risk Transfer Developments from 2005 to 2007 July 2008 Requests for copies of publications, or for additions/changes to the mailing list,

Basel Committee on Banking Supervision The Joint Forum Credit Risk Transfer Developments from 2005 to 2007 July 2008 Requests for copies of publications, or for additions/changes to the mailing list,

How Subprime Lending Led to a Systemic Crisis

The Darker Side of Securitization: How Subprime Lending Led to a Systemic Crisis Richard J. Herring The Wharton Finance Club The Wharton School, University of Pennsylvania herring@wharton.upenn.edu April

The Darker Side of Securitization: How Subprime Lending Led to a Systemic Crisis Richard J. Herring The Wharton Finance Club The Wharton School, University of Pennsylvania herring@wharton.upenn.edu April

The Case for A Rated Issuers

The Case for A Rated Issuers August 31, 2012 PFM Asset Management LLC One Keystone Plaza, Suite 300 N. Front & Market Sts Harrisburg, PA 17101 (717) 232-2723 Contents Tab I Overview of the Corporate Market

The Case for A Rated Issuers August 31, 2012 PFM Asset Management LLC One Keystone Plaza, Suite 300 N. Front & Market Sts Harrisburg, PA 17101 (717) 232-2723 Contents Tab I Overview of the Corporate Market

Maiden Lane LLC (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York)

") (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements for the Period March 14, 2008 to December 31, 2008, and Independent Auditors Report MAIDEN

(A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements for the Period March 14, 2008 to December 31, 2008, and Independent Auditors Report MAIDEN

Second Quarter, 2008 Investor Presentation

CIBC May 29, 2008 Forward Looking Statements From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including in this presentation, in other

CIBC May 29, 2008 Forward Looking Statements From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including in this presentation, in other

GLOBAL CREDIT RATING CO. Rating Methodology. Structured Finance. Global Consumer ABS Rating Criteria Updated April 2014

GCR GLOBAL CREDIT RATING CO. Local Expertise Global Presence Rating Methodology Structured Finance Global Consumer ABS Rating Criteria Updated April 2014 Introduction GCR s Global Consumer ABS Rating Criteria

GCR GLOBAL CREDIT RATING CO. Local Expertise Global Presence Rating Methodology Structured Finance Global Consumer ABS Rating Criteria Updated April 2014 Introduction GCR s Global Consumer ABS Rating Criteria

Economic History of the US

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Asset Securitization. From Moody s Perspective. Presented by: Li Ma, VP Senior Analyst, Structured Finance Group Hong Kong. November 7, 2005 Shanghai

Asset Securitization From Moody s Perspective Presented by: Li Ma, VP Senior Analyst, Structured Finance Group Hong Kong November 7, 2005 Shanghai Agenda What is Securitization? What Can be Securitized?

Asset Securitization From Moody s Perspective Presented by: Li Ma, VP Senior Analyst, Structured Finance Group Hong Kong November 7, 2005 Shanghai Agenda What is Securitization? What Can be Securitized?

September Market Overview: Private Distressed Debt. Eric J. Petroff, CFA Director of Research WURTS & ASSOCIATES

September 2008 Market Overview: Private Distressed Debt Eric J. Petroff, CFA Director of Research epetroff@wurts.com WURTS & ASSOCIATES SEATTLE 999 Third Avenue Suite 3650 Seattle, Washington 98104 206.622.3700

September 2008 Market Overview: Private Distressed Debt Eric J. Petroff, CFA Director of Research epetroff@wurts.com WURTS & ASSOCIATES SEATTLE 999 Third Avenue Suite 3650 Seattle, Washington 98104 206.622.3700

Black Diamond CLO DAC

Presale: Black Diamond CLO 2017-2 DAC This presale report is based on information as of Nov. 15, 2017. The ratings shown are preliminary. This report does not constitute a recommendation to buy, hold,

Presale: Black Diamond CLO 2017-2 DAC This presale report is based on information as of Nov. 15, 2017. The ratings shown are preliminary. This report does not constitute a recommendation to buy, hold,

CDO Litigation Reaching Crucial Stage

CDO Litigation Reaching Crucial Stage A Securities Docket Webcast Jay Tambe, Jones Day James Goldfarb, Jones Day Gene Deetz, Navigant Consulting Jeff Nielsen, Navigant Consulting June 10, 2009 2:00 p.m.

CDO Litigation Reaching Crucial Stage A Securities Docket Webcast Jay Tambe, Jones Day James Goldfarb, Jones Day Gene Deetz, Navigant Consulting Jeff Nielsen, Navigant Consulting June 10, 2009 2:00 p.m.

HSBC Global Investment Funds - Global Asset-Backed Bond

HSBC Global Investment Funds - Global Asset-Backed Bond S Share Class AM2 AM2 31/08/2018 Fund Objective and Strategy Investment Objective The Fund invests for long-term total return (meaning capital growth

HSBC Global Investment Funds - Global Asset-Backed Bond S Share Class AM2 AM2 31/08/2018 Fund Objective and Strategy Investment Objective The Fund invests for long-term total return (meaning capital growth

BONDS AND CREDIT RATING

BONDS AND CREDIT RATING 2017 1 Typical Bond Features The indenture - a written agreement between the borrower and a trust company - usually lists Amount of Issue, Date of Issue, Maturity Denomination (Par

BONDS AND CREDIT RATING 2017 1 Typical Bond Features The indenture - a written agreement between the borrower and a trust company - usually lists Amount of Issue, Date of Issue, Maturity Denomination (Par

2016 RISK AND PILLAR III REPORT SECOND UPDATE AS OF JUNE 30, 2017

2016 RISK AND PILLAR III REPORT SECOND UPDATE AS OF JUNE 30, 2017 NATIXIS - 2016 Risk & Pillar III Report second update as of June 30, 2017 2 TABLE OF CONTENTS Update by chapter of the Risk and Pillar

2016 RISK AND PILLAR III REPORT SECOND UPDATE AS OF JUNE 30, 2017 NATIXIS - 2016 Risk & Pillar III Report second update as of June 30, 2017 2 TABLE OF CONTENTS Update by chapter of the Risk and Pillar

AXIS Specialty Limited. Financial Statements and Independent Auditors Report

AXIS Specialty Limited Financial Statements and Independent Auditors Report 1 Pages No. Independent Auditors Report 3 Balance Sheets as at 4 Statements of Operations and Comprehensive Income (Loss) for

AXIS Specialty Limited Financial Statements and Independent Auditors Report 1 Pages No. Independent Auditors Report 3 Balance Sheets as at 4 Statements of Operations and Comprehensive Income (Loss) for

The enduring case for high-yield bonds

November 2016 The enduring case for high-yield bonds TIAA Investments Kevin Lorenz, CFA Managing Director High Yield Portfolio Manager Jean Lin, CFA Managing Director High Yield Portfolio Manager Mark

November 2016 The enduring case for high-yield bonds TIAA Investments Kevin Lorenz, CFA Managing Director High Yield Portfolio Manager Jean Lin, CFA Managing Director High Yield Portfolio Manager Mark

Asset Strategy for Matching Adjustment Business Challenges and Choices

This document is intended for use at the Insurance Investment Exchange event only. Not for onward distribution. Asset Strategy for Matching Adjustment Business Challenges and Choices June 2016 Agenda Background

This document is intended for use at the Insurance Investment Exchange event only. Not for onward distribution. Asset Strategy for Matching Adjustment Business Challenges and Choices June 2016 Agenda Background

General comments. 1 See

BNP Paribas Response to the EBA Draft RTS on the determination of the overall exposure to a client or a group of connected clients in respect of transactions with underlying assets Object: BNP Paribas

BNP Paribas Response to the EBA Draft RTS on the determination of the overall exposure to a client or a group of connected clients in respect of transactions with underlying assets Object: BNP Paribas

Q109. Tom Flynn. Defining great customer experience. Risk Review. Executive Vice President & Chief Risk Officer

Defining great customer experience. Q109 Risk Review Tom Flynn Executive Vice President & Chief Risk Officer March 3, 2009 Forward Looking Statements Caution Regarding Forward-Looking Statements Bank of

Defining great customer experience. Q109 Risk Review Tom Flynn Executive Vice President & Chief Risk Officer March 3, 2009 Forward Looking Statements Caution Regarding Forward-Looking Statements Bank of

SUMMARY PROSPECTUS SIIT Opportunistic Income Fund (ENIAX) Class A

Class A") September 30, 2017 SUMMARY PROSPECTUS SIIT Opportunistic Income Fund (ENIAX) Class A Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its risks.

September 30, 2017 SUMMARY PROSPECTUS SIIT Opportunistic Income Fund (ENIAX) Class A Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its risks.

MPI Collective Goods Martin Hellwig. Systemic Risk, Macro Shocks, and Banking Regulation. ECB Frankfurt, May 2018

MPI Collective Goods Martin Hellwig Systemic Risk, Macro Shocks, and Banking Regulation ECB Frankfurt, May 2018 Innovations after the Crisis Systemic Risk Analysis Macroprudential regulation and policy

MPI Collective Goods Martin Hellwig Systemic Risk, Macro Shocks, and Banking Regulation ECB Frankfurt, May 2018 Innovations after the Crisis Systemic Risk Analysis Macroprudential regulation and policy

MATH FOR CREDIT. Purdue University, Feb 6 th, SHIKHAR RANJAN Credit Products Group, Morgan Stanley

MATH FOR CREDIT Purdue University, Feb 6 th, 2004 SHIKHAR RANJAN Credit Products Group, Morgan Stanley Outline The space of credit products Key drivers of value Mathematical models Pricing Trading strategies

MATH FOR CREDIT Purdue University, Feb 6 th, 2004 SHIKHAR RANJAN Credit Products Group, Morgan Stanley Outline The space of credit products Key drivers of value Mathematical models Pricing Trading strategies

Fixed-Income Insights

Fixed-Income Insights The Appeal of Short Duration Credit in Strategic Cash Management Yields more than compensate cash managers for taking on minimal credit risk. by Joseph Graham, CFA, Investment Strategist

Fixed-Income Insights The Appeal of Short Duration Credit in Strategic Cash Management Yields more than compensate cash managers for taking on minimal credit risk. by Joseph Graham, CFA, Investment Strategist

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended March 31, 2018 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended March 31, 2018 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

Third Quarter, 2008 Investor Presentation

CIBC August 27, 2008 Forward Looking Statements From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including in this presentation, in other

CIBC August 27, 2008 Forward Looking Statements From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including in this presentation, in other

ANNUAL FUND OPERATING EXPENSES

Semper MBS Total Return Fund Summary Prospectus March 30, 2018 Class A Institutional Class Investor Class SEMOX SEMMX SEMPX Before you invest, you may want to review the Semper MBS Total Return Fund s

Semper MBS Total Return Fund Summary Prospectus March 30, 2018 Class A Institutional Class Investor Class SEMOX SEMMX SEMPX Before you invest, you may want to review the Semper MBS Total Return Fund s

Mechanics and Benefits of Securitization

Mechanics and Benefits of Securitization Executive Summary Securitization is not a new concept. In its most basic form, securitization dates back to the late 18th century. The first modern residential

Mechanics and Benefits of Securitization Executive Summary Securitization is not a new concept. In its most basic form, securitization dates back to the late 18th century. The first modern residential

How Curb Risk In Wall Street. Luigi Zingales. University of Chicago

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

First Quarter 2016 Supplemental Information

First Quarter 2016 Supplemental Information May 4, 2016 Safe Harbor Notice This presentation, other written or oral communications and our public documents to which we refer contain or incorporate by reference

First Quarter 2016 Supplemental Information May 4, 2016 Safe Harbor Notice This presentation, other written or oral communications and our public documents to which we refer contain or incorporate by reference