India s Growth Story. India Policy Forum July, Junaid Ahmad, Florian Blum, Poonam Gupta, Dhruv Jain

|

|

|

- Loraine Abigayle Parker

- 5 years ago

- Views:

Transcription

1 India s Growth Story India Policy Forum July, 2018 Junaid Ahmad, Florian Blum, Poonam Gupta, Dhruv Jain 1

2 Plan of the paper/presentation (i) India s long term growth (last years) (ii) Growth dynamics in the last decade and a half (since 2003) (iii) Recent economic developments (iv) Lingering challenges and emerging policy priorities 2

3 Long term growth has consistently accelerated and stabilized--declining standard deviation or coefficient of variation. GDP growth has accelerated over the long run 3

4 Acceleration has been faster in per capita income 4

5 Decomposition of GDP growth Acceleration and stability across sectors: Agriculture, Industry and Services Agricultural growth : has become more stable, no definite acceleration. Services growth: has become more stable, fastest acceleration. Industrial growth: too has become more stable, some acceleration Consumption, Investment, and Exports Acceleration in their contribution to growth over long run Share of consumption in GDP has declined, of investment and exports increased Contribution of factor inputs and productivity growth A balanced narrative: TFP has increased slowly, as has the labor productivity (Bosworth, Collins and Virmani, 2007; Bosworth and Collins, 2008) 5

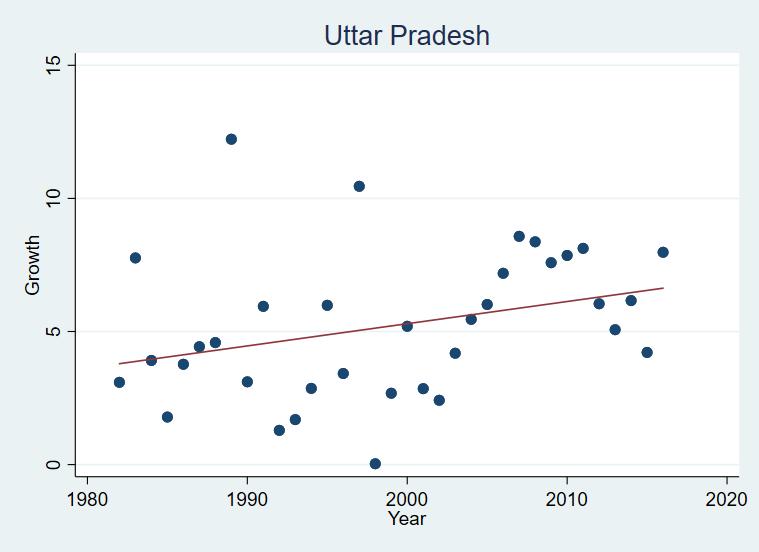

6 Inter state experience: growth has accelerated, stabilized on average, across states VARIABLES (1) (2) (3) (4) (5) Coefficie Growth Growth nt of Rate Rate Variation Growth Rate Coefficie nt of Variation Trend 0.089*** 0.099** 0.089*** -2.96*** -3.56*** (9.27) (2.47) (5.99) (4.53) (3.22) Ag. Share (1981) X Trend (0.251) GDP per capita > Median x Trend (0.064) (1.03) State Fixed Effects Yes Yes Yes Yes Yes Observations R-squared

7 Inter state experience: growth has accelerated across states 7

8 Inter state experience: growth has become more stable across states 8

9 (ii) Growth rates in the last decade and a half: Parsing the long run to understand when slowdown started FY Real GDP Growth Average Average Average Average

10 (ii) A distinct cycle in the Indian economy around the global financial crisis: High growth rates in , and a slowdown thereafter Growth faster than before in ; and somewhat faster than in many other emerging markets. Prominently reflected in investment and credit growth, coincided with rapid inflows of capital. Features of unsustainable boom? External factors clearly contributed to it (Shankar Acharya; Mohan and Kapur); India specific features too impact of economic reforms (Shankar Acharya; Arvind Panagariya) Policy response during the GFC impacted the pace of recovery (Mohan and Kapur; and Mundle, Rao and Bhanumurthy) 10

11 Global growth and trade outlook have implications for India India s growth rate correlates strongly with advanced economies and global growth India s goods exports growth are strongly correlated with world imports growth Rolling correlation 11

12 International comparisons EM7 or a larger set of EMDE Credit growth was far more rapid in India prior to the GFC Investment growth in India outpaced growth in the EM7, and the correction was sharper 12

13 (iv) Increase in investment rate prior to GFC was steeper, and the decline sharper for India 13

14 Slowdown since Slowdown in India coincided with the global financial crisis. Subsequent investment slowdown and credit slowdown sharper in India than in other large emerging markets related to the extent of increase in prior years and the specific policy mix during and thereafter. The policy response consisted of increased spending, monetary policy easing, tax rebates, regulatory forbearance in the banking sector, evergreening. Coincided with a pre election spending spree. 14

15 Investment rate has been slowing after peaking in

16 Credit growth has been declining after peaking in

17 Exports and trade as percent of GDP have been declining since the global financial crisis 17

18 (iii) Recent Economic Developments Demonetization and implementation of GST had an impact on growth when it declined below 7 percent Growth temporarily decelerated to 5.6 percent in Q1, ; but rebounded to 6.3 percent in Q2, ; 7.0 in Q3, and 7.7 percent in Q4, High frequency indicators such as trade, credit, investment, IIP, PMI, point to a continuing rebound in the economy 18

19 Continuing rebound 19

20 Continuing rebound. (contd.) 20

21 Continuing rebound (contd.) Credit growth has picked up Investment growth accelerates sharply 21

22 Economy shows signs of recovery (contd.) Export show signs of recovery; imports remain stronger Manufacturing output expands 22

23 (iv) Investment rate has declined for corporate and household sectors investment rate has declined since the GFC decline is evident in household investments and private corporate sector While public investment fell after GFC, it has increased modestly in recent years 23

24 (iv) India s share in world exports has stagnated/declined for goods and services Service and merchandise export growth has slowed down India s share in goods exports has plateaued in the recent years 24

25 (iv) India s share in world exports has stagnated/declined across destinations and products Contribution of different destinations to export growth Difference in Growth Rates between and

26 (iv) Public sector banks have fared differently/less well NPA Credit growth 26

27 (iv) Ownership of Banking sector remains predominantly in public sector 22 A: Share of private sector continues to increase in the aviation and telecom industry 22 B: But remains low and sticky in the Banking space. 27

28 Summary India s growth has been credible over the long run: accelerated, steadier, diversified, balanced. Growth averaged 7 percent in the last decade, as growth decelerated after the global financial crisis. A slowdown below that was seemingly transitory and now signs of revival. Growth at higher levels would require a supportive global economy, reversing declining trends in investment and exports; an efficient and resilient financial sector; and continuing reform momentum. 28

29 Thank you 29

30 Emerging policy priorities Policy certainty how does one ensure it in an evolving policy paradigm A financial sector for a 2.5 trillion economy, growing at double digit nominally. Wisely handling global integration maximizing gains and withstanding volatility. Easier said than done. Public vs private goods and their provision, skills for the changing nature of jobs (is it a private or public good. Who finances and who provides), regulation of markets and sectors that have a healthy presence of public and private or only private providers, Land/labor (silent reforms by stealth?) 30

31 Correlates and Policy Framework for sustained growth rate A conducive global economy, increasing integration while being cautious on capital flows. Given the structural nature of the slowdown little rationale or room for countercyclical policies. Macroeconomic stability hard won macroeconomic stability should not be compromised Financial sector (some but perhaps insufficient progress on Recognize, Resolve, and Recapitalize; and missing Reforms) Reinstating the competitiveness of exports real competitiveness; nominal competitiveness. Role of exchange rate. Policy tools? Inflation targeting framework, Policy tools available to central banks Increasing decentralization Fiscal architecture. 31

32 Global Integration of the Indian Economy India is a large emerging market: Increasingly integrated on trade and capital account An oil importer Impacted by: Global growth Global trade volumes Oil prices Monetary policy in advanced economies Global liquidity and risk aversion 32

33 (ii) Growth rates in the last decade and a half A distinct cycle in the Indian economy, around the global financial crisis External factors clearly contributed to it somewhat similar cycles in other countries (Shankar Acharya; Mohan, and Kapur) India specific features too impact of economic reforms, and the pre crisis boom (Shankar Acharya; Arvind Panagariya) Policy response during the GFC impacted the pace of recovery (Mohan, and Kapur; and Mundle, Rao and Bhanumurthy) 33

34 (ii) A distinct cycle in the Indian economy, around the global financial crisis: High growth rates in , and a slowdown thereafter External factors clearly contributed to it somewhat similar cycles in other countries (Shankar Acharya; Mohan and Kapur) India specific features too impact of economic reforms, and the pre crisis boom (Shankar Acharya; Arvind Panagariya) Policy response during the GFC impacted the pace of recovery (Mohan and Kapur; and Mundle, Rao and Bhanumurthy) 34

India Policy Forum July 10 11, 2018

India s Growth Story Junaid Ahmad, Florian Blum Poonam Gupta and Dhruv Jain World Bank India Policy Forum July 1 11, 18 NCAER National Council of Applied Economic Research 11 IP Estate, New Delhi 11 Tel:

India s Growth Story Junaid Ahmad, Florian Blum Poonam Gupta and Dhruv Jain World Bank India Policy Forum July 1 11, 18 NCAER National Council of Applied Economic Research 11 IP Estate, New Delhi 11 Tel:

SOUTH ASIA. Chapter 2. Recent developments

SOUTH ASIA GLOBAL ECONOMIC PROSPECTS January 2014 Chapter 2 s GDP growth rose to an estimated 4.6 percent in 2013 from 4.2 percent in 2012, but was well below its average in the past decade, reflecting

SOUTH ASIA GLOBAL ECONOMIC PROSPECTS January 2014 Chapter 2 s GDP growth rose to an estimated 4.6 percent in 2013 from 4.2 percent in 2012, but was well below its average in the past decade, reflecting

Managing Sudden Stops

Managing Sudden Stops Barry Eichengreen and Poonam Gupta Presented at The Bank of Spain November 17, 2016 Views are personal Context Capital flows to emerging markets continue to be volatile-- pointing

Managing Sudden Stops Barry Eichengreen and Poonam Gupta Presented at The Bank of Spain November 17, 2016 Views are personal Context Capital flows to emerging markets continue to be volatile-- pointing

How Successful is China s Economic Rebalancing?*

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Economic ProjEctions for

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

MEDIUM-TERM FORECAST

MEDIUM-TERM FORECAST Q2 2010 Published by: Národná banka Slovenska Address: Národná banka Slovenska Imricha Karvaša 1 813 25 Bratislava Slovakia Contact: Monetary Policy Department +421 2 5787 2611 +421

MEDIUM-TERM FORECAST Q2 2010 Published by: Národná banka Slovenska Address: Národná banka Slovenska Imricha Karvaša 1 813 25 Bratislava Slovakia Contact: Monetary Policy Department +421 2 5787 2611 +421

STCI Primary Dealer Ltd

Macroeconomic Update: GDP Q3 FY18 Beating expectations, India s Real GDP noted a sharp rebound, coming in at 7.2% for Q3 FY18, higher than the revised estimate of 6.5% witnessed in the previous quarter.

Macroeconomic Update: GDP Q3 FY18 Beating expectations, India s Real GDP noted a sharp rebound, coming in at 7.2% for Q3 FY18, higher than the revised estimate of 6.5% witnessed in the previous quarter.

Economic projections

Economic projections 2017-2020 December 2017 Outlook for the Maltese economy Economic projections 2017-2020 The pace of economic activity in Malta has picked up in 2017. The Central Bank s latest economic

Economic projections 2017-2020 December 2017 Outlook for the Maltese economy Economic projections 2017-2020 The pace of economic activity in Malta has picked up in 2017. The Central Bank s latest economic

Macroeconomic Context and Budget Priorities Shankar Acharya * ICRIER KAS Seminar 2013, February 21, 2013

Macroeconomic Context and Budget Priorities 2013-14 by Shankar Acharya * ICRIER KAS Seminar 2013, February 21, 2013 * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India,

Macroeconomic Context and Budget Priorities 2013-14 by Shankar Acharya * ICRIER KAS Seminar 2013, February 21, 2013 * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India,

Economic Outlook Survey September 2015

FICCI s Economic Outlook Survey: GDP growth at 7.6% for 2015-16 Results of FICCI s latest Economic Outlook Survey indicate moderation in GDP growth estimates. Based on the responses received, the median

FICCI s Economic Outlook Survey: GDP growth at 7.6% for 2015-16 Results of FICCI s latest Economic Outlook Survey indicate moderation in GDP growth estimates. Based on the responses received, the median

The Evolving Role of Trade in Asia: Opening a New Chapter. Fall 2018 REO Background Paper

The Evolving Role of Trade in Asia: Opening a New Chapter Fall 2018 REO Background Paper Outline Trade Tensions and Spillovers: Spotlight on Asia Gains from Liberalization 2 Trade tensions have escalated.

The Evolving Role of Trade in Asia: Opening a New Chapter Fall 2018 REO Background Paper Outline Trade Tensions and Spillovers: Spotlight on Asia Gains from Liberalization 2 Trade tensions have escalated.

The euro area economy: an update Euro Challenge November 2016

The euro area economy: an update Euro Challenge November 2016 Delegation of the European Union to the United States www.euro-challenge.org What this presentation will cover A. Update on the economic situation

The euro area economy: an update Euro Challenge November 2016 Delegation of the European Union to the United States www.euro-challenge.org What this presentation will cover A. Update on the economic situation

Economic Projections :1

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Country Risk Analytics

Emerging Markets Country Risk Analytics MacroFinance Research Quarterly - 2018 Q2 www.taceconomics.com www.taceconomics.com 2 Country Risk Analytics EM Quarterly MacroFinance Research 2018 Q2 Description

Emerging Markets Country Risk Analytics MacroFinance Research Quarterly - 2018 Q2 www.taceconomics.com www.taceconomics.com 2 Country Risk Analytics EM Quarterly MacroFinance Research 2018 Q2 Description

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Sada Reddy: Fiji s economy

Sada Reddy: Fiji s economy Presentation by Mr Sada Reddy, Deputy Governor of the Reserve Bank of Fiji, to the FIJI NZ Business Council, Suva, 3 October 2008. * * * Outline The outline of my presentation

Sada Reddy: Fiji s economy Presentation by Mr Sada Reddy, Deputy Governor of the Reserve Bank of Fiji, to the FIJI NZ Business Council, Suva, 3 October 2008. * * * Outline The outline of my presentation

Economic Forecast OUTPUT AND EMPLOYMENT WHAT THE TABLE SHOWS:

December 3, 13 Economic Forecast OUTPUT AND EMPLOYMENT 7 8 9 1 11 1 13 1 United States Real GDP $ billions (fourth quarter) $1,99 $1,7 $1, $1,9 $1, $1, $1,97 $1, % change over the four quarters 1.9% -.8%

December 3, 13 Economic Forecast OUTPUT AND EMPLOYMENT 7 8 9 1 11 1 13 1 United States Real GDP $ billions (fourth quarter) $1,99 $1,7 $1, $1,9 $1, $1, $1,97 $1, % change over the four quarters 1.9% -.8%

Eurozone. EY Eurozone Forecast June 2014

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Malta

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Malta

2.10 PROJECTIONS. Macroeconomic scenario for Italy (percentage changes on previous year, unless otherwise indicated)

") . PROJECTIONS The projections for growth and inflation presented in this Economic Bulletin point to a strengthening of the economic recovery in Italy (Table ), based on the assumption that the weaker stimulus

. PROJECTIONS The projections for growth and inflation presented in this Economic Bulletin point to a strengthening of the economic recovery in Italy (Table ), based on the assumption that the weaker stimulus

Economic Update. Port Finance Seminar. Paul Bingham. Global Insight, Inc. Copyright 2006 Global Insight, Inc.

Economic Update Copyright 26 Global Insight, Inc. Port Finance Seminar Paul Bingham Global Insight, Inc. Baltimore, MD May 16, 26 The World Economy: Is the Risk of a Boom-Bust Rising? As the U.S. Economy

Economic Update Copyright 26 Global Insight, Inc. Port Finance Seminar Paul Bingham Global Insight, Inc. Baltimore, MD May 16, 26 The World Economy: Is the Risk of a Boom-Bust Rising? As the U.S. Economy

Outlook for the Hawai'i Economy

Outlook for the Hawai'i Economy May 3, 2001 Dr. Carl Bonham University of Hawai'i Economic Research Organization Summary The Hawaii economy entered 2001 in its best shape in more than a decade. While the

Outlook for the Hawai'i Economy May 3, 2001 Dr. Carl Bonham University of Hawai'i Economic Research Organization Summary The Hawaii economy entered 2001 in its best shape in more than a decade. While the

Global Business Cycles

Global Business Cycles M. Ayhan Kose, Prakash Loungani, and Marco E. Terrones April 29 The 29 forecasts of economic activity, if realized, would qualify this year as the most severe global recession during

Global Business Cycles M. Ayhan Kose, Prakash Loungani, and Marco E. Terrones April 29 The 29 forecasts of economic activity, if realized, would qualify this year as the most severe global recession during

Quarterly Economic Monitor

Overview of Quarterly Economic Monitor December 214 Queenstown s economy boomed during 214, with ' provisional estimate of GDP showing that the Queenstown-Lakes District economy grew by 4.5% over the year

Overview of Quarterly Economic Monitor December 214 Queenstown s economy boomed during 214, with ' provisional estimate of GDP showing that the Queenstown-Lakes District economy grew by 4.5% over the year

MANAGEMENT DISCUSSION AND ANALYSIS REPORT

ECONOMIC REVIEW GLOBAL ECONOMY MANAGEMENT DISCUSSION AND ANALYSIS REPORT Global growth slowed down to 3.1 percent in 2015 from 3.3 percent in 2014. According to the IMF, global growth is projected to increase

ECONOMIC REVIEW GLOBAL ECONOMY MANAGEMENT DISCUSSION AND ANALYSIS REPORT Global growth slowed down to 3.1 percent in 2015 from 3.3 percent in 2014. According to the IMF, global growth is projected to increase

Japan's Economy and Monetary Policy

September 28, 2015 B ank of Japan Japan's Economy and Monetary Policy Speech at a Meeting with Business Leaders in Osaka Haruhiko Kuroda Governor of the Bank of Japan (English translation based on the

September 28, 2015 B ank of Japan Japan's Economy and Monetary Policy Speech at a Meeting with Business Leaders in Osaka Haruhiko Kuroda Governor of the Bank of Japan (English translation based on the

Economic Forecast OUTPUT AND EMPLOYMENT WHAT THE TABLE SHOWS:

December 7, 13 Economic Forecast OUTPUT AND EMPLOYMENT 7 8 9 1 11 1 13 1 United States Real GDP $ billions (fourth quarter) $1,99 $1,575 $1,5 $1,9 $15, $15,5 $15,97 $1, % change over the four quarters

December 7, 13 Economic Forecast OUTPUT AND EMPLOYMENT 7 8 9 1 11 1 13 1 United States Real GDP $ billions (fourth quarter) $1,99 $1,575 $1,5 $1,9 $15, $15,5 $15,97 $1, % change over the four quarters

Haruhiko Kuroda: Japan s economy and monetary policy

Haruhiko Kuroda: Japan s economy and monetary policy Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at a meeting with business leaders, Osaka, 28 September 2015. Introduction * * * It is

Haruhiko Kuroda: Japan s economy and monetary policy Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at a meeting with business leaders, Osaka, 28 September 2015. Introduction * * * It is

Summary and Economic Outlook

Pentti Vartia Managing director Pasi Sorjonen Head of forecasting group 1.1 Summary The world economy started to recover rapidly at the start of the year. Despite this rebound in activity, near-term growth

Pentti Vartia Managing director Pasi Sorjonen Head of forecasting group 1.1 Summary The world economy started to recover rapidly at the start of the year. Despite this rebound in activity, near-term growth

Potential Output in Denmark

43 Potential Output in Denmark Asger Lau Andersen and Morten Hedegaard Rasmussen, Economics 1 INTRODUCTION AND SUMMARY The concepts of potential output and output gap are among the most widely used concepts

43 Potential Output in Denmark Asger Lau Andersen and Morten Hedegaard Rasmussen, Economics 1 INTRODUCTION AND SUMMARY The concepts of potential output and output gap are among the most widely used concepts

Meeting with Analysts

CNB s New Forecast (Inflation Report III/2018) Meeting with Analysts Karel Musil Prague, 3 August 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

CNB s New Forecast (Inflation Report III/2018) Meeting with Analysts Karel Musil Prague, 3 August 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

The FDI-driven export growth story continues to power ahead despite the US withdrawal from TPP

Vietnam s economy grew 6.2% yoy in 2016, versus 6.7% in 2015, weighed down by a slowdown in the agriculture and mining sectors. There was a further moderation to 5.1% growth in 1Q17. Nonetheless, on the

Vietnam s economy grew 6.2% yoy in 2016, versus 6.7% in 2015, weighed down by a slowdown in the agriculture and mining sectors. There was a further moderation to 5.1% growth in 1Q17. Nonetheless, on the

Developments in inflation and its determinants

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

Transmission in India:

Asymmetry in Monetary Policy Transmission in India: Aggregate and Sectoral Analysis Brajamohan Misra Officer in Charge Department of Economic and Policy Research Reserve Bank of India VI Meeting of Open

Asymmetry in Monetary Policy Transmission in India: Aggregate and Sectoral Analysis Brajamohan Misra Officer in Charge Department of Economic and Policy Research Reserve Bank of India VI Meeting of Open

Viet Nam GDP growth by sector Crude oil output Million metric tons 20

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

In fiscal year 2016, for the first time since 2009, the

Summary In fiscal year 216, for the first time since 29, the federal budget deficit increased in relation to the nation s economic output. The Congressional Budget Office projects that over the next decade,

Summary In fiscal year 216, for the first time since 29, the federal budget deficit increased in relation to the nation s economic output. The Congressional Budget Office projects that over the next decade,

India s Economic Outlook

India s Economic Outlook Draft Report 2017-18 & 2018-19 India-LINK Team* September 2017 *These forecasts, developed as part of World Project Link, are based on the India-LINK (earlier known as CDE- DSE

India s Economic Outlook Draft Report 2017-18 & 2018-19 India-LINK Team* September 2017 *These forecasts, developed as part of World Project Link, are based on the India-LINK (earlier known as CDE- DSE

Republic of Korea Contributions to growth (demand) Quarterly GDP growth

Quarterly GDP growth") Republic of Korea The export sector was surprisingly strong in, but domestic demand wilted, resulting in economic growth below potential. Subpar growth is expected again this year, with the uncertain global

Republic of Korea The export sector was surprisingly strong in, but domestic demand wilted, resulting in economic growth below potential. Subpar growth is expected again this year, with the uncertain global

HIGHLIGHTS OF INTERIM BUDGET

From the SelectedWorks of Sreeraj M Fall January 6, 2009 HIGHLIGHTS OF INTERIM BUDGET - 2009 Sreeraj M Available at: https://works.bepress.com/sreerajm/4/ Highlights of the Interim Budget 2009 -All efforts

From the SelectedWorks of Sreeraj M Fall January 6, 2009 HIGHLIGHTS OF INTERIM BUDGET - 2009 Sreeraj M Available at: https://works.bepress.com/sreerajm/4/ Highlights of the Interim Budget 2009 -All efforts

Asset Allocation Model March Update

The month of February was marked by a sell-off in global equity markets and a sudden increase in market volatility with the CBOE Volatility Index reaching its highest level since August 2015. The rout

The month of February was marked by a sell-off in global equity markets and a sudden increase in market volatility with the CBOE Volatility Index reaching its highest level since August 2015. The rout

Resilience in Emerging Market and Developing Economies: Will It Last?

International Monetary Fund World Economic Outlook October 212 Resilience in Emerging Market and Developing Economies: Will It Last? Abdul Abiad, John Bluedorn, Jaime Guajardo, and Petia Topalova with

International Monetary Fund World Economic Outlook October 212 Resilience in Emerging Market and Developing Economies: Will It Last? Abdul Abiad, John Bluedorn, Jaime Guajardo, and Petia Topalova with

Summary. Chinese equities remained mired in a bear market, with the Shanghai composite losing nearly

Summary Editor: Tristan Zhuo Senior Economist Phone: +852 2826 6193 Email: tristanzhuo@bochk.com In spite of fixed asset investment, industrial production, and exports all missing their targets, China

Summary Editor: Tristan Zhuo Senior Economist Phone: +852 2826 6193 Email: tristanzhuo@bochk.com In spite of fixed asset investment, industrial production, and exports all missing their targets, China

India and the Global Crisis

India and the Global Crisis by Shankar Acharya * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India, 1993-2001) 1 India's GDP growth since 1991/92 12 10 8 6 4 2 0 percent

India and the Global Crisis by Shankar Acharya * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India, 1993-2001) 1 India's GDP growth since 1991/92 12 10 8 6 4 2 0 percent

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

China Economic Update Q1 2015

Key Developments in Brief Economic development Growth drivers Risks GDP growth slows to 7. Slowdown challenging, but manageable More easing policies expected Reforms progressing slowly Services and retail

Key Developments in Brief Economic development Growth drivers Risks GDP growth slows to 7. Slowdown challenging, but manageable More easing policies expected Reforms progressing slowly Services and retail

Economic Forecast OUTPUT AND EMPLOYMENT WHAT THE TABLE SHOWS:

Economic Forecast OUTPUT AND EMPLOYMENT 7 8 9 1 11 1 13 1 United States Real GDP $ billions (fourth quarter) $1,99 $1,7 $1, $1,9 $1, $1, $1,97 $1, % change over the four quarters 1.9% -.8% -.%.8%.%.%.%

Economic Forecast OUTPUT AND EMPLOYMENT 7 8 9 1 11 1 13 1 United States Real GDP $ billions (fourth quarter) $1,99 $1,7 $1, $1,9 $1, $1, $1,97 $1, % change over the four quarters 1.9% -.8% -.%.8%.%.%.%

JAPANESE ECONOMY Private consumption may prove to be resilient US ECONOMY The economy remains buoyant despite some soft patches.

JAPANESE ECONOMY Private consumption may prove to be resilient.... US ECONOMY The economy remains buoyant despite some soft patches. EUROPEAN ECONOMY U.K. economy is slowing mildly.... CHINESE ECONOMY

JAPANESE ECONOMY Private consumption may prove to be resilient.... US ECONOMY The economy remains buoyant despite some soft patches. EUROPEAN ECONOMY U.K. economy is slowing mildly.... CHINESE ECONOMY

Global PMI. Global economy suffers loss of momentum in March. April 10 th IHS Markit. All Rights Reserved.

Global PMI Global economy suffers loss of momentum in March April 10 th 2018 2 Global economy suffers marked loss of growth momentum Global economic growth slowed sharply to the weakest for over a year

Global PMI Global economy suffers loss of momentum in March April 10 th 2018 2 Global economy suffers marked loss of growth momentum Global economic growth slowed sharply to the weakest for over a year

Quarterly Monetary Policy Report Press Conference. Brian Wynter. Governor. Bank of Jamaica

Quarterly Monetary Policy Report Press Conference Brian Wynter Governor Bank of Jamaica 29 August 2018 1 Good morning and welcome to the Quarterly Monetary Policy Report press conference. The Decision

Quarterly Monetary Policy Report Press Conference Brian Wynter Governor Bank of Jamaica 29 August 2018 1 Good morning and welcome to the Quarterly Monetary Policy Report press conference. The Decision

BANK OF FINLAND ARTICLES ON THE ECONOMY

BANK OF FINLAND ARTICLES ON THE ECONOMY Table of Contents Finland struggling to defend its market share on rapidly expanding markets 3 Finland struggling to defend its market share on rapidly expanding

BANK OF FINLAND ARTICLES ON THE ECONOMY Table of Contents Finland struggling to defend its market share on rapidly expanding markets 3 Finland struggling to defend its market share on rapidly expanding

YEREVAN 2014 MACROECONOMIC OVERVIEW OF ARMENIA

YEREVAN 2014 MACROECONOMIC OVERVIEW OF ARMENIA MACROECONOMIC OVERVIEW In the early 1990s, a sharp boost of unemployment, reduction of real wages, shrinkage of tax-base, persistent cash shortages of GoA

YEREVAN 2014 MACROECONOMIC OVERVIEW OF ARMENIA MACROECONOMIC OVERVIEW In the early 1990s, a sharp boost of unemployment, reduction of real wages, shrinkage of tax-base, persistent cash shortages of GoA

Economic Profile of Bhutan

Economic Profile of Bhutan Submitted to: Dr. Ahmed Tazmeen Assistant Professor, Department of Economics North South University Submitted By: Namgay Wangmo MPPG 6th Batch ID # 1612872085 Date of Submission:

Economic Profile of Bhutan Submitted to: Dr. Ahmed Tazmeen Assistant Professor, Department of Economics North South University Submitted By: Namgay Wangmo MPPG 6th Batch ID # 1612872085 Date of Submission:

Country Risk Analysis

SEB MERCHANT BANKING COUNTRY RISK ANALYSIS December 11, 2014 Analyst: Martin Carlens. Tel: +46-8-7639605. E-mail: martin.carlens@seb.se Economic growth has bottomed, sentiment is rising following the elections

SEB MERCHANT BANKING COUNTRY RISK ANALYSIS December 11, 2014 Analyst: Martin Carlens. Tel: +46-8-7639605. E-mail: martin.carlens@seb.se Economic growth has bottomed, sentiment is rising following the elections

The Economic Outlook

The Economic Outlook Nigel Gault Group Managing Director North American Macroeconomic Services FTA Revenue Estimating Conference Portland, Oregon September 8, Copyright Global Insight, Inc. U.S. Growth

The Economic Outlook Nigel Gault Group Managing Director North American Macroeconomic Services FTA Revenue Estimating Conference Portland, Oregon September 8, Copyright Global Insight, Inc. U.S. Growth

Retrospective on 1997

Mr. Meyer gives his views on the US economic outlook and the challenges facing monetary policy Remarks by Mr. Laurence H. Meyer, a member of the Board of Governors of the US Federal Reserve System, before

Mr. Meyer gives his views on the US economic outlook and the challenges facing monetary policy Remarks by Mr. Laurence H. Meyer, a member of the Board of Governors of the US Federal Reserve System, before

The Economic Outlook of Taiwan

The Economic Outlook of Taiwan by Ray Yeutien Chou and An-Chi Wu The Institute of Economics, Academia Sinica, Taipei October 2017 1 Prepared for Project LINK 2017 Fall Meeting, Geneva, Oct. 3-5, 2017 2

The Economic Outlook of Taiwan by Ray Yeutien Chou and An-Chi Wu The Institute of Economics, Academia Sinica, Taipei October 2017 1 Prepared for Project LINK 2017 Fall Meeting, Geneva, Oct. 3-5, 2017 2

Economic Outlook Survey. January 2017

January 2017 GDP growth estimated at 6.8% in 2016-17: FICCI s Economic Outlook Survey HIGHLIGHTS GDP growth for FY 17 estimated at 6.8% The latest round of FICCI s Economic Outlook Survey puts forth an

January 2017 GDP growth estimated at 6.8% in 2016-17: FICCI s Economic Outlook Survey HIGHLIGHTS GDP growth for FY 17 estimated at 6.8% The latest round of FICCI s Economic Outlook Survey puts forth an

HSBC Trade Connections: Trade Forecast Quarterly Update October 2011

HSBC Trade Connections: Trade Forecast Quarterly Update October 2011 New quarterly forecast exploring the future of world trade and the opportunities for international businesses World trade will grow

HSBC Trade Connections: Trade Forecast Quarterly Update October 2011 New quarterly forecast exploring the future of world trade and the opportunities for international businesses World trade will grow

REFERENCE NOTE. No. 28/RN/Ref./November /2013

LOK SABHA SECRETARIAT PARLIAMENT LIBRARY AND REFERENCE, RESEARCH, DOCUMENTATION AND INFORMATION SERVICE (LARRDIS) MEMBERS REFERENCE SERVICE REFERENCE NOTE. No. 28/RN/Ref./November /2013 For the use of

LOK SABHA SECRETARIAT PARLIAMENT LIBRARY AND REFERENCE, RESEARCH, DOCUMENTATION AND INFORMATION SERVICE (LARRDIS) MEMBERS REFERENCE SERVICE REFERENCE NOTE. No. 28/RN/Ref./November /2013 For the use of

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

Kaua i Economy Shows Signs of Cooling

Kaua i Economic Outlook Summary: Kaua i Economy Shows Signs of Cooling prepared for the County of Kaua i by the University of Hawai i Economic Research Organization July 1, 26 Kaua i Economic Outlook Summary

Kaua i Economic Outlook Summary: Kaua i Economy Shows Signs of Cooling prepared for the County of Kaua i by the University of Hawai i Economic Research Organization July 1, 26 Kaua i Economic Outlook Summary

OECD Interim Economic Projections Real GDP 1 Percentage change September 2015 Interim Projections. Outlook

ass Interim Economic Outlook 16 September 2015 Puzzles and uncertainties Global growth prospects have weakened slightly and become less clear in recent months. World trade growth has stagnated and financial

ass Interim Economic Outlook 16 September 2015 Puzzles and uncertainties Global growth prospects have weakened slightly and become less clear in recent months. World trade growth has stagnated and financial

With large service sector based economy, high saving rate and low external

With large service sector based economy, high saving rate and low external dependency, capital movements can be controlled. Indian government can stop borrowing and repay high interest loans. The government

With large service sector based economy, high saving rate and low external dependency, capital movements can be controlled. Indian government can stop borrowing and repay high interest loans. The government

Economic Outlook: Global and India. Ajit Ranade IEEMA T & D Conclave December 12, 2014

Economic Outlook: Global and India Ajit Ranade IEEMA T & D Conclave December 12, 2014 Global scenario US expected to drive global growth in 2015 Difference from % YoY Growth October Actual October Projections

Economic Outlook: Global and India Ajit Ranade IEEMA T & D Conclave December 12, 2014 Global scenario US expected to drive global growth in 2015 Difference from % YoY Growth October Actual October Projections

Macroeconomic perspectives

12 July 2018 Macroeconomic perspectives Csaba Bálint OTP Bank Romania Global context: Ultra-loose monetary policy seemingly came to an end; precaution is warranted (1) SUMMARY: In the beginning of 2018,

12 July 2018 Macroeconomic perspectives Csaba Bálint OTP Bank Romania Global context: Ultra-loose monetary policy seemingly came to an end; precaution is warranted (1) SUMMARY: In the beginning of 2018,

Structural Changes in the Maltese Economy

Structural Changes in the Maltese Economy Dr. Aaron George Grech Modelling and Research Department, Central Bank of Malta, Castille Place, Valletta, Malta Email: grechga@centralbankmalta.org Doi:10.5901/mjss.2015.v6n5p423

Structural Changes in the Maltese Economy Dr. Aaron George Grech Modelling and Research Department, Central Bank of Malta, Castille Place, Valletta, Malta Email: grechga@centralbankmalta.org Doi:10.5901/mjss.2015.v6n5p423

INFLATION REPORT PRESS CONFERENCE. Thursday 8 th February Opening Remarks by the Governor

INFLATION REPORT PRESS CONFERENCE Thursday 8 th February 2018 Opening Remarks by the Governor This has been a notable week for anniversaries. On Monday, the nation celebrated the centenary of women gaining

INFLATION REPORT PRESS CONFERENCE Thursday 8 th February 2018 Opening Remarks by the Governor This has been a notable week for anniversaries. On Monday, the nation celebrated the centenary of women gaining

IMF Executive Board Concludes 2010 Article IV Consultation with Indonesia Public Information Notice (PIN) No. 10/130 September 16, 2010

No. 10/130 September 16, 2010") IMF Executive Board Concludes 2010 Article IV Consultation with Indonesia Public Information Notice (PIN) No. 10/130 September 16, 2010 Public Information Notices (PINs) form part of the IMF's efforts

IMF Executive Board Concludes 2010 Article IV Consultation with Indonesia Public Information Notice (PIN) No. 10/130 September 16, 2010 Public Information Notices (PINs) form part of the IMF's efforts

NATIONAL BANK OF SERBIA. Speech at the presentation of the Inflation Report May Dr Jorgovanka Tabaković, Governor

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report May Dr Jorgovanka Tabaković, Governor Belgrade, May Ladies and gentlemen, representatives of the press, dear colleagues, Welcome

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report May Dr Jorgovanka Tabaković, Governor Belgrade, May Ladies and gentlemen, representatives of the press, dear colleagues, Welcome

INTERMEDIATE OPEN ECONOMY MACROECONOMICS - WINTER

INTERMEDIATE OPEN ECONOMY MACROECONOMICS - WINTER 2019 - Francesco Trebbi 1 Course Preliminaries Lecture Notes: I upload them online before class. They are comprehensive and detailed. All material is posted

INTERMEDIATE OPEN ECONOMY MACROECONOMICS - WINTER 2019 - Francesco Trebbi 1 Course Preliminaries Lecture Notes: I upload them online before class. They are comprehensive and detailed. All material is posted

Emerging Markets: Compelling Long-Term Value or Value Trap?

INSIGHTS Emerging Markets: Compelling Long-Term Value or Value Trap? November 2015 203.621.1700 2015, Rocaton Investment Advisors, LLC EXECUTIVE SUMMARY * Emerging market asset classes, primarily equities

INSIGHTS Emerging Markets: Compelling Long-Term Value or Value Trap? November 2015 203.621.1700 2015, Rocaton Investment Advisors, LLC EXECUTIVE SUMMARY * Emerging market asset classes, primarily equities

Banking on Turkey, October 21, 2008

Banking on Turkey, October 21, 2008 Slide 1. Title Slide Good morning. The global economic downturn and financial turmoil mean that economic growth will slow down in Turkey. There will be much slower growth,

Banking on Turkey, October 21, 2008 Slide 1. Title Slide Good morning. The global economic downturn and financial turmoil mean that economic growth will slow down in Turkey. There will be much slower growth,

6-8 September 2011, Manila, Philippines. Jointly organized by UNESCAP and BANGKO SENTRAL NG PILIPINAS. Country Experiences 1: ASEAN Economies

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

Investment and its Financing: A Macro Perspective

G R O U P O F T W E N T Y Investment and its Financing: A Macro Perspective Annex to the G Surveillance Note Meetings of G Finance Ministers and Central Bank Governors February, 3 Prepared by Staff of

G R O U P O F T W E N T Y Investment and its Financing: A Macro Perspective Annex to the G Surveillance Note Meetings of G Finance Ministers and Central Bank Governors February, 3 Prepared by Staff of

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL. Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL Joint Bank-Fund Debt Sustainability Analysis

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION INTERNATIONAL MONETARY FUND NEPAL Joint Bank-Fund Debt Sustainability Analysis

EUROPEAN EXPORT INDEX Q4 2017

EUROPEAN EXPORT INDEX Q4 2017 BDO EXPORT INDEX KEY FIGURES The BDO Export Indices are composite indicators which provide snapshots of the export markets in Europe s five largest economies Germany, UK,

EUROPEAN EXPORT INDEX Q4 2017 BDO EXPORT INDEX KEY FIGURES The BDO Export Indices are composite indicators which provide snapshots of the export markets in Europe s five largest economies Germany, UK,

Ukraine Macroeconomic Situation

In 2012, industrial production was down by 1.8% yoy as weakening global demand for steel exerted a toll on the Ukrainian metallurgical industry. Last year, harvested 46.2 tons of grains and overseas shipments

In 2012, industrial production was down by 1.8% yoy as weakening global demand for steel exerted a toll on the Ukrainian metallurgical industry. Last year, harvested 46.2 tons of grains and overseas shipments

Demonetisation. November 3, 2017

Demonetisation November 3, 2017 Contents 1 Introduction 2 The event 3 Affected stakeholders 4 Impact 5 India in November 2017 2 Contents 1 Introduction 2 The event 3 Affected stakeholders 4 Impact 5 India

Demonetisation November 3, 2017 Contents 1 Introduction 2 The event 3 Affected stakeholders 4 Impact 5 India in November 2017 2 Contents 1 Introduction 2 The event 3 Affected stakeholders 4 Impact 5 India

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Asia/Pacific Economic Overview

Copyright E. I. du Pont de Nemours and Company. All rights reserved. Distribution, reproduction or copying of this copyrighted work without express written permission of DuPont is prohibited. Asia/Pacific

Copyright E. I. du Pont de Nemours and Company. All rights reserved. Distribution, reproduction or copying of this copyrighted work without express written permission of DuPont is prohibited. Asia/Pacific

Global Economics Monthly Review

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

NIESR MONTHLY GDP TRACKER: July 2018

Press Release NIESR MONTHLY GDP TRACKER: July 2018 GDP Tracker indicates growth of 0.4 per cent in 2018 Q2 and 0.5 per cent in 2018 Q3 Figure 1: UK GDP growth (3 months on previous 3 months, per cent)

Press Release NIESR MONTHLY GDP TRACKER: July 2018 GDP Tracker indicates growth of 0.4 per cent in 2018 Q2 and 0.5 per cent in 2018 Q3 Figure 1: UK GDP growth (3 months on previous 3 months, per cent)

Buoyancy in industrial sector growth continues. This year s first quarter IIP growth is at 10.3% compared to 7.7% in

Prepared by N. R. Bhanumurthy August 25 Buoyancy in industrial sector growth continues. This year s first quarter IIP growth is at 1.3% compared to 7.7% in 24-5. TOP STORIES The index of industrial production

Prepared by N. R. Bhanumurthy August 25 Buoyancy in industrial sector growth continues. This year s first quarter IIP growth is at 1.3% compared to 7.7% in 24-5. TOP STORIES The index of industrial production

CONSUMPTION TRENDS AN ECONOMIC ANALYSIS OF ASIA S CHANGING TRADE. Brian Jackson, Senior Economist,

CONSUMPTION TRENDS AN ECONOMIC ANALYSIS OF ASIA S CHANGING TRADE Brian Jackson, Senior Economist, brian.jackson@ihsmarkit.com 1 IHS Markit. All Rights Reserved. Asia overview 1 IHS Markit. All Rights Reserved.

CONSUMPTION TRENDS AN ECONOMIC ANALYSIS OF ASIA S CHANGING TRADE Brian Jackson, Senior Economist, brian.jackson@ihsmarkit.com 1 IHS Markit. All Rights Reserved. Asia overview 1 IHS Markit. All Rights Reserved.

THE OUTLOOK FOR EMERGING MARKETS

THE OUTLOOK FOR EMERGING MARKETS Will They Ever Re-emerge? That the global economy has failed to return to its pre-crisis pace of growth is well known. This deceleration has been remarkably broad-based,

THE OUTLOOK FOR EMERGING MARKETS Will They Ever Re-emerge? That the global economy has failed to return to its pre-crisis pace of growth is well known. This deceleration has been remarkably broad-based,

The Economic Outlook of Taiwan

The Economic Outlook of Taiwan by Ray Yeutien Chou and Shou-Yung Yin The Institute of Economics, Academia Sinica, Taipei October 2016 Prepared for Project LINK 2016 Fall Meeting, Toronto City, Oct. 19-21,

The Economic Outlook of Taiwan by Ray Yeutien Chou and Shou-Yung Yin The Institute of Economics, Academia Sinica, Taipei October 2016 Prepared for Project LINK 2016 Fall Meeting, Toronto City, Oct. 19-21,

Questions may be referred to Ms. Fichera, APD (ext ).

.") To: Members of the Executive Board April 22, 2005 From: The Secretary Subject: Timor-Leste Statement by the IMF Staff Representative at the Donors Meeting Attached for the information of the Executive

To: Members of the Executive Board April 22, 2005 From: The Secretary Subject: Timor-Leste Statement by the IMF Staff Representative at the Donors Meeting Attached for the information of the Executive

BANKING SECTOR PERFORMANCE STUDY H1FY14

BANKING SECTOR PERFORMANCE STUDY H1FY14 Our study covers 39 banks 26 Public Sector Banks & 13 Private Sector Banks. Banking December 11, 2013 Foreword As per the Central Statistical Organization (CSO)

BANKING SECTOR PERFORMANCE STUDY H1FY14 Our study covers 39 banks 26 Public Sector Banks & 13 Private Sector Banks. Banking December 11, 2013 Foreword As per the Central Statistical Organization (CSO)

Economy Check-In: Post 2008 Crisis Market Update Special Report

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

The Five Critical Factors of the LMRI

FIXED INCOME July 6, 2018 Templeton Global Macro makes a compelling case that finding attractive opportunities in emerging markets lies in distinguishing the more resilient countries from the rest. Here,

FIXED INCOME July 6, 2018 Templeton Global Macro makes a compelling case that finding attractive opportunities in emerging markets lies in distinguishing the more resilient countries from the rest. Here,

Fixed Income Update October 2015

Month Overview Average Liquidity Support by RBI Rs -5,527 Cr. Includes: LAF, MSF, SLF & Term Repo Bank Credit Growth Money Market Bank Deposit Growth 9.6% 11.6% Change in basis points Tenure CD Change

Month Overview Average Liquidity Support by RBI Rs -5,527 Cr. Includes: LAF, MSF, SLF & Term Repo Bank Credit Growth Money Market Bank Deposit Growth 9.6% 11.6% Change in basis points Tenure CD Change

NIESR Monthly GDP Tracker 10 September, NIESR MONTHLY GDP TRACKER: September UK economic growth gathers momentum. 0.7 NIESR forecast 0.

Press Release NIESR MONTHLY GDP TRACKER: September 2018 UK economic growth gathers momentum Figure 1: UK GDP growth (3 months on previous 3 months, per cent) 0.7 NIESR forecast 0.6 0.4 0.3 0.2 0.1 0 2017

Press Release NIESR MONTHLY GDP TRACKER: September 2018 UK economic growth gathers momentum Figure 1: UK GDP growth (3 months on previous 3 months, per cent) 0.7 NIESR forecast 0.6 0.4 0.3 0.2 0.1 0 2017

Economic Projections :2

Economic Projections 2018-2020 2018:2 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2018-2020 2018:2 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Meeting with Analysts

CNB s New Forecast (Inflation Report I/2018) Meeting with Analysts Tomáš Holub Prague, 2 February 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

CNB s New Forecast (Inflation Report I/2018) Meeting with Analysts Tomáš Holub Prague, 2 February 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

China Economic Outlook 2013

China Economic Outlook 2 Key Developments in Brief - Mild recovery of GDP growth: +8 8.5% - Construction and consumption as main drivers - Inflationary pressure to increase: +3% - Tight labor market and

China Economic Outlook 2 Key Developments in Brief - Mild recovery of GDP growth: +8 8.5% - Construction and consumption as main drivers - Inflationary pressure to increase: +3% - Tight labor market and

Economic Projections For 2014 And 2015

Economic Projections For 2014 And 2015 Article published in the Quarterly Review 2014:3, pp. 77-81 7. ECONOMIC PROJECTIONS FOR 2014 AND 2015 Outlook for the Maltese economy 1 The Bank s latest macroeconomic

Economic Projections For 2014 And 2015 Article published in the Quarterly Review 2014:3, pp. 77-81 7. ECONOMIC PROJECTIONS FOR 2014 AND 2015 Outlook for the Maltese economy 1 The Bank s latest macroeconomic

Thailand Update. Asset Markets. The baht has depreciated significantly.

Thailand Update Asset Markets 15 125 1 75 5 Figure 1: Exchange Rate and Stock Price Indexes (last week of 1997June=1) 25 27 Jun 1997 1 Apr 1998 5 Feb 1999 3 Dec 29 Sep 2 SET Index, Weekly Average US Dollar

Thailand Update Asset Markets 15 125 1 75 5 Figure 1: Exchange Rate and Stock Price Indexes (last week of 1997June=1) 25 27 Jun 1997 1 Apr 1998 5 Feb 1999 3 Dec 29 Sep 2 SET Index, Weekly Average US Dollar

The AMRO Inaugural Flagship Report: ASEAN+3 Regional Economic Outlook May 2017, Yokohama, Japan

The AMRO Inaugural Flagship Report: ASEAN+3 Regional Economic Outlook 2017 4 May 2017, Yokohama, Japan Introduction: About AMRO Mandate Conduct macroeconomic and financial surveillance of global and regional

The AMRO Inaugural Flagship Report: ASEAN+3 Regional Economic Outlook 2017 4 May 2017, Yokohama, Japan Introduction: About AMRO Mandate Conduct macroeconomic and financial surveillance of global and regional