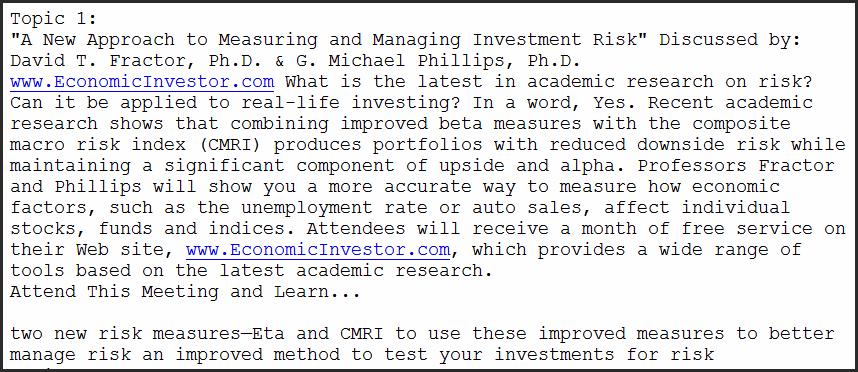

A New Approach to Measuring and Managing Investment Risk

|

|

|

- Mervin Porter

- 5 years ago

- Views:

Transcription

1

2 A New Approach to Measuring and Managing Investment Risk James Chong, Ph.D. *David T. Fractor, Ph.D. *G. Michael Phillips, Ph.D. June 19, 2010 (*presenting)

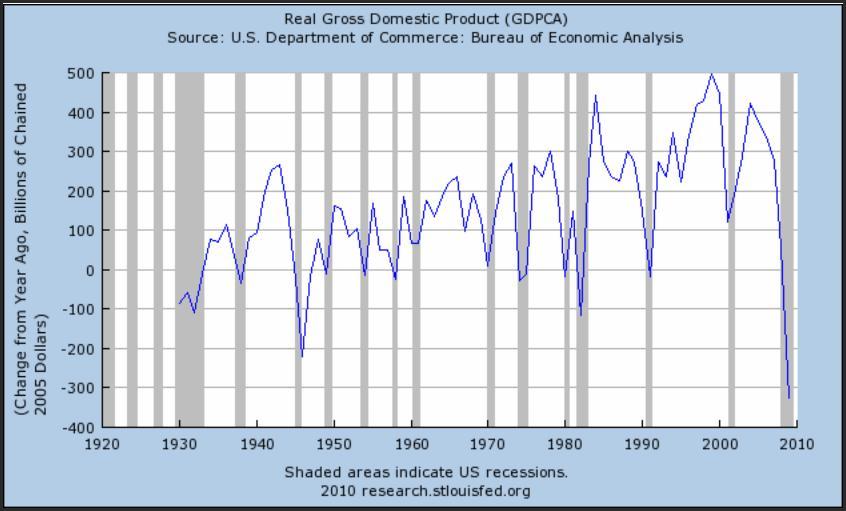

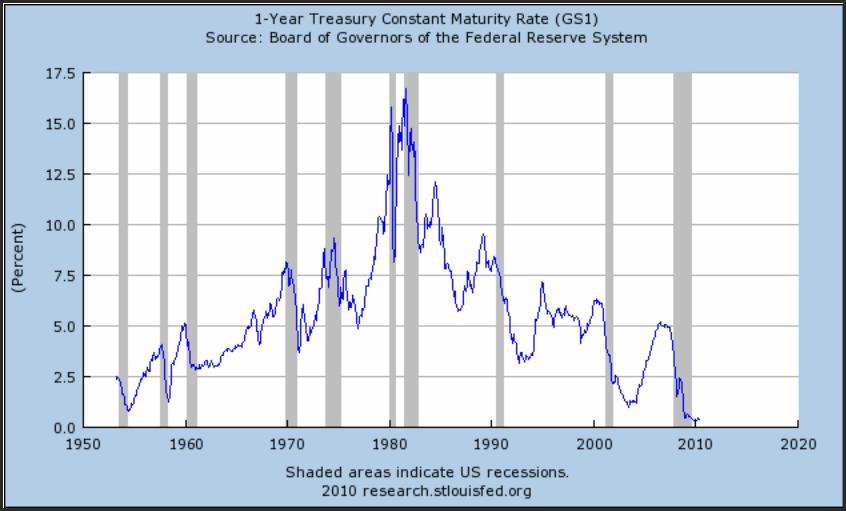

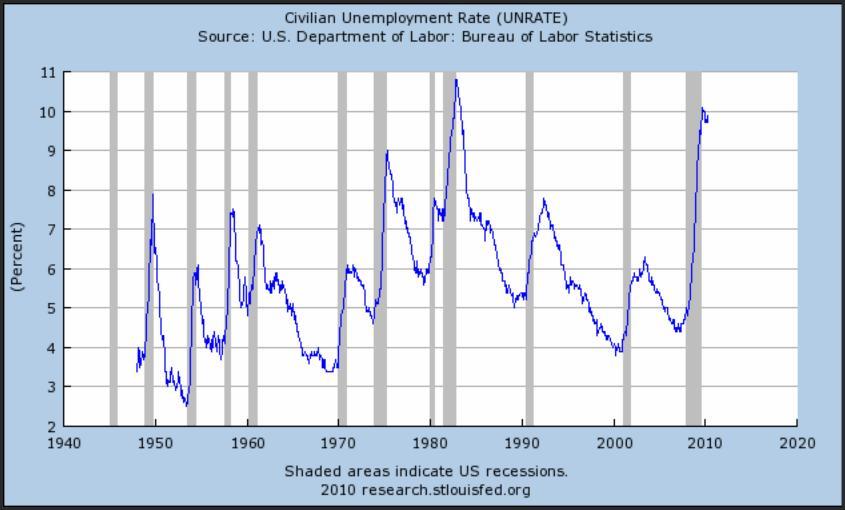

3 Part 1: The State of the Economy

4

5

6

7

8

9 S&P 500, NYSE Index, NASDAQ Index

10 The next few slides compare the S&P 500 index to several key economic factors.

11 S&P 500 vs. Gold

12 S&P 500 vs. U.S. Ag. Exports

13 S&P 500 vs. FTSE 100

14 S&P 500 vs. Tokyo Stock Exch. Index

15 S&P 500 vs. Housing Starts

16 S&P 500 vs. Monetary Base

17 S&P 500 vs. M2 Money Supply

18 S&P 500 vs. Corporate Cash Flow

19 S&P 500 vs. Auto Sales

20 S&P 500 vs. New Orders for Durable Goods

21 S&P 500 vs. Energy Price Index

22 S&P 500 vs. Unemployment Rate

23

24 The Center for Computationally Advanced Statistical Techniques has developed a new risk measure for stocks, funds, indexes, and portfolios based on their responses to 18 key economic variables, called Eta MacroRisk Factors. The next slide identifies those which have values that are outside the range that would have been expected given the past year s values.

25 The current MacroRisk Profile

26 Traditional measures of investment risk assume that economic turbulence is like the weather and you can t do anything about this systematic risk. Part 2 of our presentation will discuss a new approach to measuring and management investment risk that allows for better measurement and control of the economy s impact on investments.

27 Part 2: A New Approach to Measuring and Managing Investment Risk

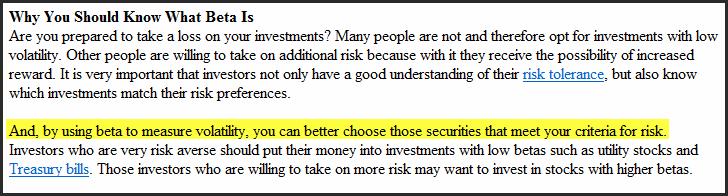

28 First, let s consider the conventional wisdom Use Betas to measure volatility Select low Beta stocks (Beta < 1) Select high Beta stocks for aggressive portfolio Create your portfolio Equally weight? MPT, maximize Sharpe ratio? 7/12 Portfolio? Just pick the best stocks or funds?

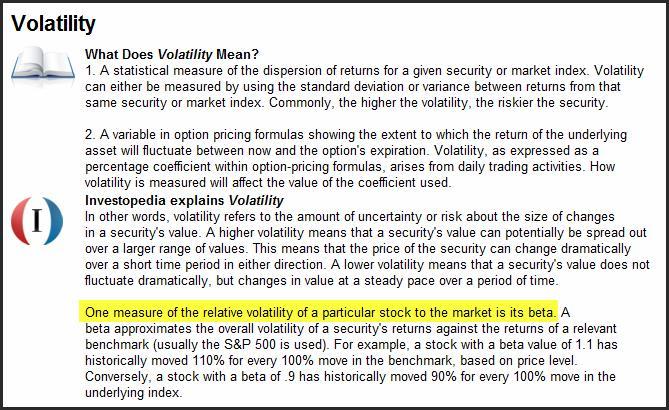

29 Beta The ratio of an investment s risk premium to the overall market s risk premium is a constant called Beta. The slope of a line drawn against the plot of an investment s return over time against an index s return is an estimate of Beta. Beta is often assumed to be symmetric, the same value whether the market is going up or down.

30 The CAPM and ß are everywhere A review of capital asset pricing models, Don U.A. Galagedera, Managerial Finance v33 n pp

31 Investopedia.com says: 31

32 (more, Investopedia.com) 32

33 The Motley Fool ( 33

34 Investment Advice: For relative safety, pick Beta < 1. Suppose that Jo Investor has her money in an IRA and does her rebalancing right before tax filing each year. Suppose in April, 2008, she put her investments in stocks with Beta less than 1. Would that have mattered in the 2008 crash? The next slide compares the S&P 500 index and an equally weighted portfolio of NYSE stocks with Betas less than 1 in April, Performance statistics are computed for the following year, 4/2008 5/

35 Portfolio of NYSE Beta < 1 and SPX, 4/15/08 5/1/09 35

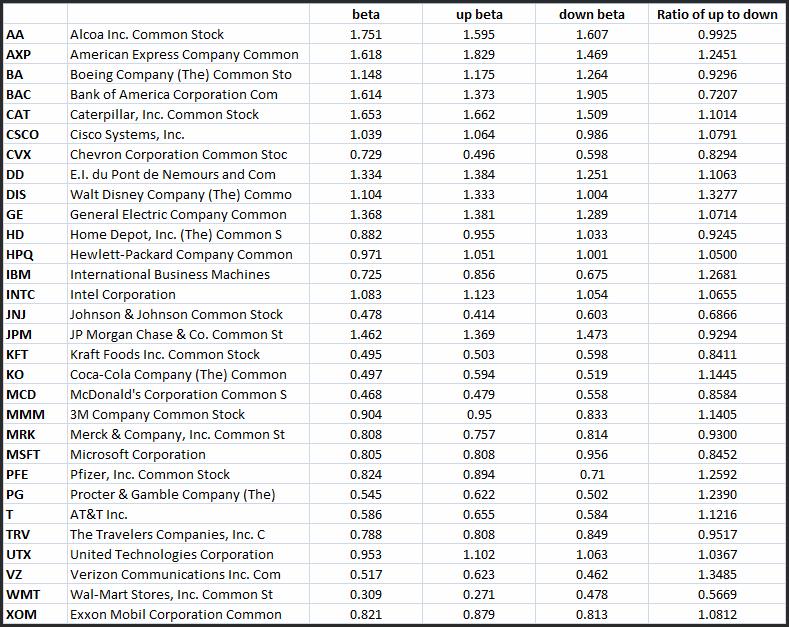

36 And, against the NYSE as a whole: 36

37 And, against the other NYSE stocks with Beta > 1: 37

38 Did different Betas matter? High Beta Stocks lost more value than Low Beta Stocks But, the safe stocks only did 100 bps better than the risky stocks Safe stocks (ß < 1) lost 30.17% Risky stocks (ß > 1) lost 31.18%

39 Another problem: Reported values of Beta are often reported inconsistently by popular sources Jennings and Phillips did an analysis of popular sources of estimated Beta used by investors, professors preparing lectures, and students performing class projects, and found a remarkable disagreement on the estimated values for those stocks listed in the Dow Jones Industrial Averages. Fun with Beta! (Or, applying Beta is a risky proposition) William P. Jennings and G. Michael Phillips Presentation to FMA Round Table

40 Fun with Beta! (Or, applying Beta is a risky proposition), William P. Jennings and G. Michael Phillips Presentation to FMA Round Table

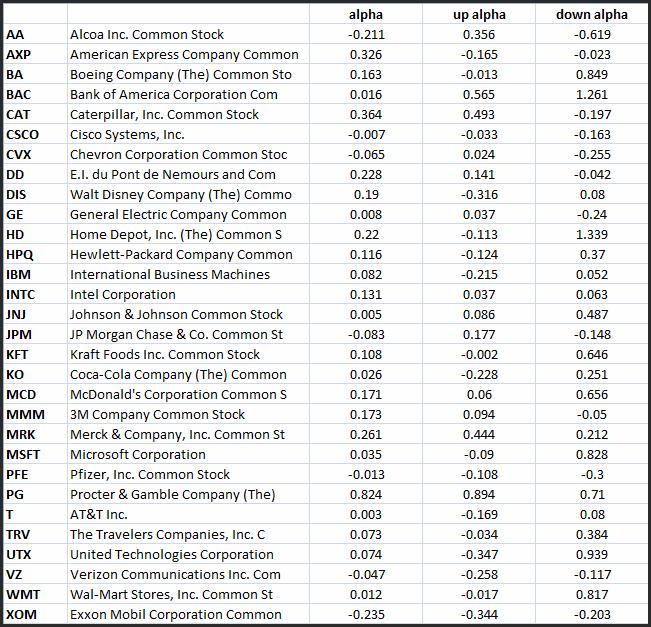

41 Here are some updated results from June 15, 2010:

42 The Dow 30 are among the most liquid, most watched, securities. Even so, these commercially provided Beta estimates showed great variety. There did not appear to be a common bias across stocks; no one source always provided large estimates, no one source always provided small estimates. It is not obvious how the different sources are estimating their Beta statistics but the underlying assumptions matter. 42

43 Betas are NOT symmetric across market conditions. Just because a stock goes up with the market doesn t mean it will go down at the same pace. Up-market and Down-market Betas allow for separate measurements of how an investment tracks with the overall market.

44 The following chart shows estimated overall Betas, up-market Betas, and down-market Betas for the Dow 30 components. These are estimated using the S&P 500 as the market index and using 1 year of daily returns. Calculations were performed using EconomicInvestor s Beta+ Tool.

45

46 Investment Hint: For safety, select investments with ß < 1. Note: ß < 0 often display larger overall risk and so we avoid them. If up-market and down-market days have an equal chance of happening, then favor investments with up-market ß greater than down-market ß.

")

47 (On 6/15/2010, 17 of the Dow 30 have higher Up than Down Betas)

48 Another related statistic is the investment s Alpha, which is the average return expected in excess of money market rates regardless of the overall market return. When estimated using annual data, this can be a proxy for stock momentum. Like Betas, Alphas are not symmetric. If a stock behaves very differently in up-market and down-market conditions, it is even possible for the overall Alpha to be positive while both Directional Alphas are negative! The following table compares Alphas for the Dow 30.

49

50 Investment Hint: For safety, consider selecting investments with > 0. (Why invest in assets with built-in loss?) In a perfect world, investments would have (up) > 0 and (down) > 0 as well.

51 (On 6/15/2010, 6 of the Dow 30 have positive Alpha measures in both down and up market conditions. 23 had positive overall Alphas but a negative directional Alpha.)

4/15/08 6/15/10 S&P: -18.")

52 Suppose that you created a portfolio from the S&P 500 of those stocks with Alpha greater than zero. Then, suppose you created another one with stocks having Alpha greater than zero and Beta less than one. Total Returns (No rebalancing) 4/15/08 6/15/10 S&P: -18.2% Positive Alpha: % Beta < 1: -8.68% Alpha > 0, Beta < 1: -6.13%

53 Investment Hint: Portfolios of investments with both positive Alpha and with Betas less than 1 often provide superior returns to portfolios constructed using just one of the measures.

54 Now, consider a Modern Portfolio Theory Approach The Sharpe Ratio is the average excess return per unit of risk (measured by the standard deviation of returns). Consider the portfolio selected from S&P 500 stocks that maximizes the Sharpe Ratio in 4/15/2008. (Portfolio weights were obtained using the MacroRisk.com professional optimizer.)

4/15/08 6/15/10 S&P: -18.2% Maximum Sharpe: -18.84% Alpha > 0, Beta < 1: -6.")

55 Compare MPT Optimized Portfolio (Maximum Sharpe Ratio) to Equally Weighted >0, ß<1 Portfolio Total Returns (No rebalancing) 4/15/08 6/15/10 S&P: -18.2% Maximum Sharpe: % Alpha > 0, Beta < 1: -6.13%

56 The and ß relate asset returns to a single benchmark. However, there are many economic factors that influence investment performance.

57 The Eta Profile is a graphical tool that helps investors understand how 18 key MacroRisk Factors impact investments These key factors are the same for all U.S. stocks, indexes, mutual funds, ETFs, ADRs, etc. These factors apply to many exchange rates. The impact of each factor can be compared across investments, across factors, and across time. The impact of each factor can be combined at the portfolio level.

58 18 Eta MacroRisk Factors statistically explain a substantial part of most stock, fund, and index prices. The Red Bars indicate factors which are outside the normal range and therefore are having extra impact on some assets.

.")

59 The MacroRisk Status indicates the current standardized value of each of the 18 factors. This describes the overall economy at a point in time. The Eta Profile is unique for each asset or portfolio. It shows the relative impact of a change in each MacroRisk factor on the asset price. The profile here is for Microsoft (MSFT). For example, MSFT stock prices historically have responded positively to Unemployment and Energy Prices, and negatively to the CPI. (All 18 Eta responses are shown on the chart.)

60 Now a Diversification Experiment consider Microsoft vs. EcoLab

61 Microsoft vs. EcoLab Microsoft (MSFT) is a technology company specializing in applications software. MSFT has about 93,000 employees and about $59.5 billion in revenues. EcoLab (ECL) is a consumer goods firm specializing in cleaning products and janitorial supply. ECL has about 26,000 employees and about $5.98 billion in revenues.

62 These two assets have similar Eta Profiles (though MSFT has more economic exposure than ECL).

63 MSFT and ECL, with similar Eta Profiles, have similar price patterns.

64 Here s another one: MSFT vs. Lorillard (LO), the cigarette manufacturing company

65 In contrast, consider Microsoft vs. Tyson Foods (TSN)

66 MSFT and TSN, with generally opposite Eta Profiles, tend to have different price patterns.

67 Here s another one: MSFT vs. Compass Minerals (CMP)

68 Investment Tip: When Eta Profiles are similar, stocks tend to move up and down together; when they are opposite shaped, they tend to move up and down oppositely. When diversification is the goal, search for investments with opposite Eta profiles to smooth out the resulting portfolio profile. When an investment is identified that should do well in the current economy, purchasing other investments with similar Eta profiles can diversify firm specific effects while maintaining the same economic exposure.

69 The CMRI (Composite MacroRisk Index) is computed by adding the absolute values of Eta Measures which are statistically important (t statistic >= 1). The CMRI value changes from asset to asset and may change over time. Because of economic diversification, the average of CMRI statistics for a portfolio is usually not the portfolio s CMRI.

Profile. (These weights were determined using the MacroRisk.com professional optimizer.)")

70 A recipe for reducing economic risk: On this particular date, combine 4 parts of the white portfolio Eta Profile with 1 part of the red MSFT Eta Profile to get the blue Portfolio (20% MSFT, 80% other) Profile. (These weights were determined using the MacroRisk.com professional optimizer.)

71 This compares MSFT with a portfolio designed to have a low CMRI, containing 20% MSFT and 80% other stocks chosen to offset the MSFT economic exposure. These data are as of 6/15/2008.

is red and the S&P Index is grey.")

72 The resulting portfolio still had Microsoft s resiliency but a far smoother path as economic risk is removed. MSFT is blue, the Low CMRI portfolio (with 20% MSFT) is red and the S&P Index is grey.

for eight sample stocks.")

73 The CMRI forecasts future volatility. Theoretically the values range from 0 to infinity, but for the most part CMRIs range from 0 to The following report from EconomicInvestor.com shows some current CMRI values (as well as a few other statistics) for eight sample stocks.

74 The Alpha, Beta, and CMRI filters can be combined to create statistically safer portfolios. (Nothing can prevent financial craziness, but on average you can improve the odds by reducing the likely negative outcomes.) In the following example, an equally weighted portfolio of NYSE traded stocks was created on 4/15/2008. The stocks had positive Alpha, Beta less than 1, and CMRI less than 300. (They also all had an economic climate rating of at least 4. This statistic, shown on the previous table, measures how favorable the current economic conditions are for a given investment and can help in forecasting performance. It is based on a combination of the MacroRisk Status and the Eta Profile of the investment being analyzed. This provides very different information than other stars ratings.)

75 Equally weighted portfolio using basic risk screens and NYSE traded stocks

76 Now, using same criteria, compare equally weighted and minimum CMRI portfolios (using 4/15/08 data)

77

78 Investment Tips (Summary): Consider both Alpha and Beta. Consider both up-market and down-market values. Don t assume that two stocks in different industries provide diversification; examine their Eta Profiles. Use CMRI as a measure of economic risk. When expected holding periods are longer than a year, try to obtain the lowest CMRI portfolio from your buy-list. This all applies to ETFs and Mutual Funds too. For shorter term holdings, use the Alpha, Beta, CMRI, and Economic Climate ratings (demonstrated in the appendix).

79 Some current NYSE screens

80 Some current NASDAQ screens

81 Some current ETF screens

82 (Appendix: An experiment using economic climate rating >= 4 as a filter on NYSE stocks, and a minimum CMRI portfolio based on those same stocks, both portfolios constructed using information as of 6/11/2009.)

83 Want to see how the Economy Matters to you? Want access to patented Investment Tools for a Changing Economy? Use this exclusive offer to get a FREE month-long Premium Subscription to ($129 value)! To get your free account: 1. Go to 2. Fill in your information and above offer code 3. Select your subscription level To run an overview report: 1. Scroll to online research 2. Click Overview Report (under Eta Analysis) 3. Select your security and click get report

Low Volatility Portfolio Tools for Investors

Low Volatility Portfolio Tools for Investors By G. Michael Phillips, Ph.D., with contributions from James Chong, Ph.D. and William Jennings, Ph.D. Introduction Reprint from November 2011 The world is a

Low Volatility Portfolio Tools for Investors By G. Michael Phillips, Ph.D., with contributions from James Chong, Ph.D. and William Jennings, Ph.D. Introduction Reprint from November 2011 The world is a

Lena Press and A. Lynn Phillips assisted with the analysis for this report.

The Economy in Review: 2011 By G. Michael Phillips, Ph.D. James Chong, Ph.D. William Jennings, Ph.D. Contact: Research@MacroRisk.com ----------- Lena Press and A. Lynn Phillips assisted with the analysis

The Economy in Review: 2011 By G. Michael Phillips, Ph.D. James Chong, Ph.D. William Jennings, Ph.D. Contact: Research@MacroRisk.com ----------- Lena Press and A. Lynn Phillips assisted with the analysis

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Portfolio Management & Analysis

Index Portfolio Monitor, Analysis and Maintenance Page 2 Portfolio Rebalancing Emotional Control Annual Performance Page 3 Detailed Analysis Page 4 Portfolio Risk Level Portfolio Management & Analysis

Index Portfolio Monitor, Analysis and Maintenance Page 2 Portfolio Rebalancing Emotional Control Annual Performance Page 3 Detailed Analysis Page 4 Portfolio Risk Level Portfolio Management & Analysis

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

MacroRisk Factor - FTSE 100

MacroRisk Analytics - MacroRisk Factor - FTSE 100 https://app.macrorisk.com/factors/show/0 1 of 1 10/18/2011 12:17 PM MacroRisk Factors» MacroRisk Factor - FTSE 100 MacroRisk Factor - FTSE 100 The FTSE

MacroRisk Analytics - MacroRisk Factor - FTSE 100 https://app.macrorisk.com/factors/show/0 1 of 1 10/18/2011 12:17 PM MacroRisk Factors» MacroRisk Factor - FTSE 100 MacroRisk Factor - FTSE 100 The FTSE

Chapter 5: Answers to Concepts in Review

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Getting Smart About Beta

Getting Smart About Beta December 1, 2015 by Sponsored Content from Invesco Due to its simplicity, market-cap weighting has long been a popular means of calculating the value of market indexes. But as

Getting Smart About Beta December 1, 2015 by Sponsored Content from Invesco Due to its simplicity, market-cap weighting has long been a popular means of calculating the value of market indexes. But as

Geoff Considine, Ph.D.

Choosing Your Portfolio Risk Tolerance Geoff Considine, Ph.D. Copyright Quantext, Inc. 2008 1 In a recent article, I laid out a series of steps for portfolio planning that emphasized how to get the most

Choosing Your Portfolio Risk Tolerance Geoff Considine, Ph.D. Copyright Quantext, Inc. 2008 1 In a recent article, I laid out a series of steps for portfolio planning that emphasized how to get the most

Modern Portfolio Theory The Most Diversified Portfolio

WallStreetCourier.com Research Paper Modern Portfolio Theory 2.0 - The Most Diversified Portfolio This article was published and awarded as Editor's Pick on Seeking Alpha on Nov. 28th, 2012 www.wallstreetcourier.com

WallStreetCourier.com Research Paper Modern Portfolio Theory 2.0 - The Most Diversified Portfolio This article was published and awarded as Editor's Pick on Seeking Alpha on Nov. 28th, 2012 www.wallstreetcourier.com

Chapter 13. Managing Your Own Portfolio

Chapter 13 Managing Your Own Portfolio Portfolio Investments Selection based on expected returns risks tax considerations Compare actual performance to expected performance 13-2 Investment Policy Statements

Chapter 13 Managing Your Own Portfolio Portfolio Investments Selection based on expected returns risks tax considerations Compare actual performance to expected performance 13-2 Investment Policy Statements

Expected Return Methodologies in Morningstar Direct Asset Allocation

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Washington University Fall Economics 487

Washington University Fall 2009 Department of Economics James Morley Economics 487 Project Proposal due Tuesday 11/10 Final Project due Wednesday 12/9 (by 5:00pm) (20% penalty per day if the project is

Washington University Fall 2009 Department of Economics James Morley Economics 487 Project Proposal due Tuesday 11/10 Final Project due Wednesday 12/9 (by 5:00pm) (20% penalty per day if the project is

The Case for TD Low Volatility Equities

The Case for TD Low Volatility Equities By: Jean Masson, Ph.D., Managing Director April 05 Most investors like generating returns but dislike taking risks, which leads to a natural assumption that competition

The Case for TD Low Volatility Equities By: Jean Masson, Ph.D., Managing Director April 05 Most investors like generating returns but dislike taking risks, which leads to a natural assumption that competition

Reprint from July Summary

Fiduciary and Economic Scoring of Mutual Funds Enhances Portfolios By G. Michael Phillips, Ph.D., George Arzumanyan, Sarah Underwood, James Chong, Ph.D. Summary Reprint from July 2014 Using data from December

Fiduciary and Economic Scoring of Mutual Funds Enhances Portfolios By G. Michael Phillips, Ph.D., George Arzumanyan, Sarah Underwood, James Chong, Ph.D. Summary Reprint from July 2014 Using data from December

Washington University Fall Economics 487. Project Proposal due Monday 10/22 Final Project due Monday 12/3

Washington University Fall 2001 Department of Economics James Morley Economics 487 Project Proposal due Monday 10/22 Final Project due Monday 12/3 For this project, you will analyze the behaviour of 10

Washington University Fall 2001 Department of Economics James Morley Economics 487 Project Proposal due Monday 10/22 Final Project due Monday 12/3 For this project, you will analyze the behaviour of 10

R02 Performance Measure and evaluation

R02 Performance Measure and evaluation Investment assessment is the final part of the advice process. There are several measures and can be split into three groups. Absolute returns Relative returns Risk

R02 Performance Measure and evaluation Investment assessment is the final part of the advice process. There are several measures and can be split into three groups. Absolute returns Relative returns Risk

Statistically Speaking

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

BUILDING INVESTMENT PORTFOLIOS WITH AN INNOVATIVE APPROACH

BUILDING INVESTMENT PORTFOLIOS WITH AN INNOVATIVE APPROACH Asset Management Services ASSET MANAGEMENT SERVICES WE GO FURTHER When Bob James founded Raymond James in 1962, he established a tradition of

BUILDING INVESTMENT PORTFOLIOS WITH AN INNOVATIVE APPROACH Asset Management Services ASSET MANAGEMENT SERVICES WE GO FURTHER When Bob James founded Raymond James in 1962, he established a tradition of

Module 6 Portfolio risk and return

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and services. Financial markets perform an important function

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and services. Financial markets perform an important function

PowerPoint. to accompany. Chapter 11. Systematic Risk and the Equity Risk Premium

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

Quantitative Measure. February Axioma Research Team

February 2018 How When It Comes to Momentum, Evaluate Don t Cramp My Style a Risk Model Quantitative Measure Risk model providers often commonly report the average value of the asset returns model. Some

February 2018 How When It Comes to Momentum, Evaluate Don t Cramp My Style a Risk Model Quantitative Measure Risk model providers often commonly report the average value of the asset returns model. Some

20% 20% Conservative Moderate Balanced Growth Aggressive

The Global View Tactical Asset Allocation series offers five risk-based model portfolios specifically designed for the Retirement Account (PCRA), which is a self-directed brokerage account option offered

The Global View Tactical Asset Allocation series offers five risk-based model portfolios specifically designed for the Retirement Account (PCRA), which is a self-directed brokerage account option offered

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

Unit01. Introduction, Creation of Financial Assets, and Security Markets

FCS 5510 Concept Review Notes: Unit01. Introduction, Creation of Financial Assets, and Security Markets Chapter 01. Definition of investment Portfolio Primary and secondary markets Value and valuation

FCS 5510 Concept Review Notes: Unit01. Introduction, Creation of Financial Assets, and Security Markets Chapter 01. Definition of investment Portfolio Primary and secondary markets Value and valuation

The purpose of this paper is to briefly review some key tools used in the. The Basics of Performance Reporting An Investor s Guide

Briefing The Basics of Performance Reporting An Investor s Guide Performance reporting is a critical part of any investment program. Accurate, timely information can help investors better evaluate the

Briefing The Basics of Performance Reporting An Investor s Guide Performance reporting is a critical part of any investment program. Accurate, timely information can help investors better evaluate the

Certified Portfolio Manager VS-1094

VS-1094 Certified Portfolio Manager Certification Code VS-1094 Vskills certification is a program for candidates seeking a career in technical analysis. The study focuses on understanding the market actions

VS-1094 Certified Portfolio Manager Certification Code VS-1094 Vskills certification is a program for candidates seeking a career in technical analysis. The study focuses on understanding the market actions

Schafer Cullen Capital Management High Dividend Value

Product Type: Separate Account Manager Headquarters: New York, NY Total Staff: 56 Geography Focus: Domestic Year Founded: 1983 Investment Professionals: 21 Type of Portfolio: Equity Total AUM: $17,896

Product Type: Separate Account Manager Headquarters: New York, NY Total Staff: 56 Geography Focus: Domestic Year Founded: 1983 Investment Professionals: 21 Type of Portfolio: Equity Total AUM: $17,896

an investor-centric approach nontraditional indexing evolves

FLEXIBLE INDEXING Shundrawn A. Thomas Executive Vice President Head of Funds and Managed Accounts Group The opinions expressed herein are those of the author and do not necessarily represent the views

FLEXIBLE INDEXING Shundrawn A. Thomas Executive Vice President Head of Funds and Managed Accounts Group The opinions expressed herein are those of the author and do not necessarily represent the views

In Search of Alpha: Are you looking in the wrong box?

FPA proudly thanks our Retreat 2006 sponsor for their support 1 C. Thomas Howard, PhD President, Athena Investment Services and University of Denver In Search of Alpha: Are you looking in the wrong box?

FPA proudly thanks our Retreat 2006 sponsor for their support 1 C. Thomas Howard, PhD President, Athena Investment Services and University of Denver In Search of Alpha: Are you looking in the wrong box?

Fayez Sarofim & Co Large Cap Equity

Product Type: Separate Account Manager Headquarters: Houston, TX Total Staff: 90 Geography Focus: Domestic Year Founded: 1958 Investment Professionals: 20 Type of Portfolio: Equity Total AUM: $22,458 million

Product Type: Separate Account Manager Headquarters: Houston, TX Total Staff: 90 Geography Focus: Domestic Year Founded: 1958 Investment Professionals: 20 Type of Portfolio: Equity Total AUM: $22,458 million

Evaluation of the fi360 Fiduciary Scores

Released: December 15, 2013 EXECUTIVE SUMMARY Using data from December 31, 2000 through March 31, 2013, the fi360 Fiduciary Scores for mutual funds were evaluated by MacroRisk Analytics to assess the scores

Released: December 15, 2013 EXECUTIVE SUMMARY Using data from December 31, 2000 through March 31, 2013, the fi360 Fiduciary Scores for mutual funds were evaluated by MacroRisk Analytics to assess the scores

VelocityShares Equal Risk Weighted Large Cap ETF (ERW): A Balanced Approach to Low Volatility Investing. December 2013

: A Balanced Approach to Low Volatility Investing. December 2013") VelocityShares Equal Risk Weighted Large Cap ETF (ERW): A Balanced Approach to Low Volatility Investing December 2013 Please refer to Important Disclosures and the Glossary of Terms section of this material.

VelocityShares Equal Risk Weighted Large Cap ETF (ERW): A Balanced Approach to Low Volatility Investing December 2013 Please refer to Important Disclosures and the Glossary of Terms section of this material.

an Investor-centrIc approach FlexIBle IndexIng nontraditional IndexIng evolves

FlexIBle IndexIng Shundrawn A. Thomas executive vice president head of Funds and Managed accounts group The opinions expressed herein are those of the author and do not necessarily represent the views

FlexIBle IndexIng Shundrawn A. Thomas executive vice president head of Funds and Managed accounts group The opinions expressed herein are those of the author and do not necessarily represent the views

Risk and Return - Capital Market Theory. Chapter 8

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

1 Risk and Return - Capital Market Theory Chapter 8 Learning Objectives 2 1. Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects

Cash. Period Ending 06/30/2016 Period Ending 3/31/2016. Equity. Fixed Income. Other

Product Type: Multi-Product Portfolio Headquarters: Austin, TX Total Staff: 46 Geography Focus: Global Year Founded: 1996 Investment Professionals: 16 Type of Portfolio: Balanced Total AUM: $12,046 million

Product Type: Multi-Product Portfolio Headquarters: Austin, TX Total Staff: 46 Geography Focus: Global Year Founded: 1996 Investment Professionals: 16 Type of Portfolio: Balanced Total AUM: $12,046 million

Risk and Return - Capital Market Theory. Chapter 8

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

Risk and Return - Capital Market Theory Chapter 8 Principles Applied in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 4: Market Prices Reflect Information. Portfolio Returns and

Portfolio Theory Project

Portfolio Theory Project M442, Spring 2003 1 Overview On October 22, 1929, Yale economics professor Irving Fisher was quoted in a New York Times article entitled Fisher says prices of stocks are low, that

Portfolio Theory Project M442, Spring 2003 1 Overview On October 22, 1929, Yale economics professor Irving Fisher was quoted in a New York Times article entitled Fisher says prices of stocks are low, that

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 2 Due: October 20

COMM 34 INVESTMENTS ND PORTFOLIO MNGEMENT SSIGNMENT Due: October 0 1. In 1998 the rate of return on short term government securities (perceived to be risk-free) was about 4.5%. Suppose the expected rate

COMM 34 INVESTMENTS ND PORTFOLIO MNGEMENT SSIGNMENT Due: October 0 1. In 1998 the rate of return on short term government securities (perceived to be risk-free) was about 4.5%. Suppose the expected rate

The Process of Portfolio Management. Presentation by: William Wood CFP

The Process of Portfolio Management Presentation by: William Wood CFP 1 Investments Traditional investment processes cover: Security analysis Involves estimating the merits of individual investments Portfolio

The Process of Portfolio Management Presentation by: William Wood CFP 1 Investments Traditional investment processes cover: Security analysis Involves estimating the merits of individual investments Portfolio

Insight.Clarity.Purpose.

Charles Sherry Director, Institutional Education Group Blue Ocean Global Wealth 9841 Washingtonian Blvd., #200 Gaithersburg, MD 20878 Tel: 720.308.4560 csherry@blueoceanglobalwealth.com 2017 February Financial

Charles Sherry Director, Institutional Education Group Blue Ocean Global Wealth 9841 Washingtonian Blvd., #200 Gaithersburg, MD 20878 Tel: 720.308.4560 csherry@blueoceanglobalwealth.com 2017 February Financial

Your Keys to Successful Investing

877-822-1445 1 info@dynamicinvestorpro.com www.dynamicinvestorpro.com Special Report 1 of 6 Your Keys to Successful Investing Successful investing requires a few keys, all of which anyone, including you,

877-822-1445 1 info@dynamicinvestorpro.com www.dynamicinvestorpro.com Special Report 1 of 6 Your Keys to Successful Investing Successful investing requires a few keys, all of which anyone, including you,

Manager Comparison Report June 28, Report Created on: July 25, 2013

Manager Comparison Report June 28, 213 Report Created on: July 25, 213 Page 1 of 14 Performance Evaluation Manager Performance Growth of $1 Cumulative Performance & Monthly s 3748 3578 348 3238 368 2898

Manager Comparison Report June 28, 213 Report Created on: July 25, 213 Page 1 of 14 Performance Evaluation Manager Performance Growth of $1 Cumulative Performance & Monthly s 3748 3578 348 3238 368 2898

Nasdaq Chaikin Power US Small Cap Index

Nasdaq Chaikin Power US Small Cap Index A Multi-Factor Approach to Small Cap Introduction Multi-factor investing has become very popular in recent years. The term smart beta has been coined to categorize

Nasdaq Chaikin Power US Small Cap Index A Multi-Factor Approach to Small Cap Introduction Multi-factor investing has become very popular in recent years. The term smart beta has been coined to categorize

Sample Reports for The Expert Allocator by Investment Technologies

Sample Reports for The Expert Allocator by Investment Technologies Telephone 212/724-7535 Fax 212/208-4384 Support Telephone 203/364-9915 Fax 203/547-6164 e-mail support@investmenttechnologies.com Website

Sample Reports for The Expert Allocator by Investment Technologies Telephone 212/724-7535 Fax 212/208-4384 Support Telephone 203/364-9915 Fax 203/547-6164 e-mail support@investmenttechnologies.com Website

Risk and Return Fundamentals. Risk, Return, and Asset Pricing Model. Risk and Return Fundamentals: Risk and Return Defined

Risk and Return Fundamentals Risk, Return, and Asset Pricing Model Financial Risk Management Nattawut Jenwittayaroje, PhD, CFA NIDA Business School National Institute of Development Administration In most

Risk and Return Fundamentals Risk, Return, and Asset Pricing Model Financial Risk Management Nattawut Jenwittayaroje, PhD, CFA NIDA Business School National Institute of Development Administration In most

Social Security & Progressive Taxation

Social Security & Progressive Taxation There are two sections to this software. The first deals with taxation of Social Security. The topic of the second section is progressive tax rates. You go from one

Social Security & Progressive Taxation There are two sections to this software. The first deals with taxation of Social Security. The topic of the second section is progressive tax rates. You go from one

WHY PORTFOLIO MANAGERS SHOULD BE USING BETA FACTORS

Page 2 The Securities Institute Journal WHY PORTFOLIO MANAGERS SHOULD BE USING BETA FACTORS by Peter John C. Burket Although Beta factors have been around for at least a decade they have not been extensively

Page 2 The Securities Institute Journal WHY PORTFOLIO MANAGERS SHOULD BE USING BETA FACTORS by Peter John C. Burket Although Beta factors have been around for at least a decade they have not been extensively

NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS

Nationwide Funds A Nationwide White Paper NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS May 2017 INTRODUCTION In the market decline of 2008, the S&P 500 Index lost more than 37%, numerous equity strategies

Nationwide Funds A Nationwide White Paper NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS May 2017 INTRODUCTION In the market decline of 2008, the S&P 500 Index lost more than 37%, numerous equity strategies

Does Portfolio Theory Work During Financial Crises?

Does Portfolio Theory Work During Financial Crises? Harry M. Markowitz, Mark T. Hebner, Mary E. Brunson It is sometimes said that portfolio theory fails during financial crises because: All asset classes

Does Portfolio Theory Work During Financial Crises? Harry M. Markowitz, Mark T. Hebner, Mary E. Brunson It is sometimes said that portfolio theory fails during financial crises because: All asset classes

Expected Return and Portfolio Rebalancing

Expected Return and Portfolio Rebalancing Marcus Davidsson Newcastle University Business School Citywall, Citygate, St James Boulevard, Newcastle upon Tyne, NE1 4JH E-mail: davidsson_marcus@hotmail.com

Expected Return and Portfolio Rebalancing Marcus Davidsson Newcastle University Business School Citywall, Citygate, St James Boulevard, Newcastle upon Tyne, NE1 4JH E-mail: davidsson_marcus@hotmail.com

Port(A,B) is a combination of two stocks, A and B, with standard deviations A and B. A,B = correlation (A,B) = 0.

is a combination of two stocks, A and B, with standard deviations A and B. A,B = correlation (A,B) = 0.") Corporate Finance, Module 6: Risk, Return, and Cost of Capital Practice Problems (The attached PDF file has better formatting.) Updated: July 19, 2007 Exercise 6.1: Minimum Variance Portfolio Port(A,B)

Corporate Finance, Module 6: Risk, Return, and Cost of Capital Practice Problems (The attached PDF file has better formatting.) Updated: July 19, 2007 Exercise 6.1: Minimum Variance Portfolio Port(A,B)

Your Asset Allocation: The Sound Stewardship Portfolio Construction Methodology Explained

Your Asset Allocation: The Sound Stewardship Portfolio Construction Methodology Explained Author: Dan Weeks, CFP At Sound Stewardship, we take a principled approach to investing. That means our investment

Your Asset Allocation: The Sound Stewardship Portfolio Construction Methodology Explained Author: Dan Weeks, CFP At Sound Stewardship, we take a principled approach to investing. That means our investment

Modern Portfolio Theory

66 Trusts & Trustees, Vol. 15, No. 2, April 2009 Modern Portfolio Theory Ian Shipway* Abstract All investors, be they private individuals, trustees or professionals are faced with an extraordinary range

66 Trusts & Trustees, Vol. 15, No. 2, April 2009 Modern Portfolio Theory Ian Shipway* Abstract All investors, be they private individuals, trustees or professionals are faced with an extraordinary range

Types of Stocks. Stock. Common stock. Preferred stock. An equity or an ownership stake in a firm.

Stock Markets Types of Stocks Stock An equity or an ownership stake in a firm. Common stock Common stockholders have the right to vote. Common stockholders receive dividends. Preferred stock Are a hybrid

Stock Markets Types of Stocks Stock An equity or an ownership stake in a firm. Common stock Common stockholders have the right to vote. Common stockholders receive dividends. Preferred stock Are a hybrid

The benefits of core-satellite investing

The benefits of core-satellite investing Contents 1 Core-satellite: A powerful investment approach 3 The key benefits of indexing the portfolio s core 6 Core-satellite methodology Core-satellite: A powerful

The benefits of core-satellite investing Contents 1 Core-satellite: A powerful investment approach 3 The key benefits of indexing the portfolio s core 6 Core-satellite methodology Core-satellite: A powerful

Solutions to the problems in the supplement are found at the end of the supplement

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Diversification: The most important thing you forgot to measure

Diversification: The most important thing you forgot to measure James E. Damschroder Founder & Chief of Financial Engineering Gravity Investments damschroder@gravityinvestments.com www.gravityinvestments.com

Diversification: The most important thing you forgot to measure James E. Damschroder Founder & Chief of Financial Engineering Gravity Investments damschroder@gravityinvestments.com www.gravityinvestments.com

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

Chapter 5. Asset Allocation - 1. Modern Portfolio Concepts

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Morgan Stanley Dynamic Balance Index

Morgan Stanley Dynamic Balance Index Return MORGAN STANLEY DYNAMIC BALANCE INDEX Morgan Stanley Dynamic Balance Index A rules-based index offering risk-controlled exposure to a broad range of asset classes

Morgan Stanley Dynamic Balance Index Return MORGAN STANLEY DYNAMIC BALANCE INDEX Morgan Stanley Dynamic Balance Index A rules-based index offering risk-controlled exposure to a broad range of asset classes

Black Box Trend Following Lifting the Veil

AlphaQuest CTA Research Series #1 The goal of this research series is to demystify specific black box CTA trend following strategies and to analyze their characteristics both as a stand-alone product as

AlphaQuest CTA Research Series #1 The goal of this research series is to demystify specific black box CTA trend following strategies and to analyze their characteristics both as a stand-alone product as

Building and Managing a Diversified Portfolio

Building and Managing a Diversified Portfolio Craig L. Israelsen, Ph.D. Designer of the Portfolio Presentation AAII Silicon Valley Chapter April 14, 2018 Based on research by Craig L. Israelsen, Ph.D.

Building and Managing a Diversified Portfolio Craig L. Israelsen, Ph.D. Designer of the Portfolio Presentation AAII Silicon Valley Chapter April 14, 2018 Based on research by Craig L. Israelsen, Ph.D.

INVESTMENTS Lecture 2: Measuring Performance

Philip H. Dybvig Washington University in Saint Louis portfolio returns unitization INVESTMENTS Lecture 2: Measuring Performance statistical measures of performance the use of benchmark portfolios Copyright

Philip H. Dybvig Washington University in Saint Louis portfolio returns unitization INVESTMENTS Lecture 2: Measuring Performance statistical measures of performance the use of benchmark portfolios Copyright

Macro Economics Covering the Federal Reserve Bank and the FOMC (Federal Open Market Committee)

") Fall 2009 FTS Real Time Trading Exercises The FTS Real Time Trading Exercises have two basic goals: To introduce the current real world financial markets into your course Let your students learn concepts

Fall 2009 FTS Real Time Trading Exercises The FTS Real Time Trading Exercises have two basic goals: To introduce the current real world financial markets into your course Let your students learn concepts

Crestmont Research. Rowing vs. The Roller Coaster By Ed Easterling January 26, 2007 All Rights Reserved

Crestmont Research Rowing vs. The Roller Coaster By Ed Easterling January 26, 2007 All Rights Reserved Why are so many of the most knowledgeable institutions and individuals shifting away from investment

Crestmont Research Rowing vs. The Roller Coaster By Ed Easterling January 26, 2007 All Rights Reserved Why are so many of the most knowledgeable institutions and individuals shifting away from investment

Modeling Portfolios that Contain Risky Assets Risk and Return I: Introduction

Modeling Portfolios that Contain Risky Assets Risk and Return I: Introduction C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling January 26, 2012 version c 2011 Charles

Modeling Portfolios that Contain Risky Assets Risk and Return I: Introduction C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling January 26, 2012 version c 2011 Charles

Notably, longer-term bond yields have actually dipped from recent highs see Figure 1.

Charles Sherry Director, Institutional Education Group Blue Ocean Global Wealth 9841 Washingtonian Blvd., #200 Gaithersburg, MD 20878 Tel: 720.308.4560 csherry@blueoceanglobalwealth.com 2017 May Financial

Charles Sherry Director, Institutional Education Group Blue Ocean Global Wealth 9841 Washingtonian Blvd., #200 Gaithersburg, MD 20878 Tel: 720.308.4560 csherry@blueoceanglobalwealth.com 2017 May Financial

Alternatives in action: A guide to strategies for portfolio diversification

October 2015 Christian J. Galipeau Senior Investment Director Brendan T. Murray Senior Investment Director Seamus S. Young, CFA Investment Director Alternatives in action: A guide to strategies for portfolio

October 2015 Christian J. Galipeau Senior Investment Director Brendan T. Murray Senior Investment Director Seamus S. Young, CFA Investment Director Alternatives in action: A guide to strategies for portfolio

A Motivating Case Study

Testing Monte Carlo Risk Projections Geoff Considine, Ph.D. Quantext, Inc. Copyright Quantext, Inc. 2005 1 Introduction If you have used or read articles about Monte Carlo portfolio planning tools, you

Testing Monte Carlo Risk Projections Geoff Considine, Ph.D. Quantext, Inc. Copyright Quantext, Inc. 2005 1 Introduction If you have used or read articles about Monte Carlo portfolio planning tools, you

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Columbus Asset Allocation Report For Portfolio Rebalancing on

Columbus Asset Allocation Report For Portfolio Rebalancing on 2017-08-31 Strategy Overview Columbus is a global asset allocation strategy designed to adapt to prevailing market conditions. It dynamically

Columbus Asset Allocation Report For Portfolio Rebalancing on 2017-08-31 Strategy Overview Columbus is a global asset allocation strategy designed to adapt to prevailing market conditions. It dynamically

Complete Guide to Investing. 5 th Edition

Complete Guide to Investing 5 th Edition Chapter 1 Getting Started as an Investor... 1 Learning Objectives... 1 Introduction... 1 Investing... 2 What Are the Sources of Money for Investing?... 2 What Are

Complete Guide to Investing 5 th Edition Chapter 1 Getting Started as an Investor... 1 Learning Objectives... 1 Introduction... 1 Investing... 2 What Are the Sources of Money for Investing?... 2 What Are

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

Capital Asset Pricing Model - CAPM

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

What Is An INDEX? by dqr Aug 5, 2018 Academy, Crypto Trading. De nition

U a What Is An INDEX? by dqr Aug 5, 2018 Academy, Crypto Trading De nition When examining the speci c topic of investments and portfolio management, an INDEX is a carefully selected sample from a larger

U a What Is An INDEX? by dqr Aug 5, 2018 Academy, Crypto Trading De nition When examining the speci c topic of investments and portfolio management, an INDEX is a carefully selected sample from a larger

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Capital Idea: Expect More From the Core.

SM Capital Idea: Expect More From the Core. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. Core equity strategies, such

SM Capital Idea: Expect More From the Core. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. Core equity strategies, such

Setting The Record Straight: Achieving Success Beyond a Day with Leveraged and Inverse Funds. Live Webinar September 16, p.m.

Setting The Record Straight: Achieving Success Beyond a Day with Leveraged and Inverse Funds Live Webinar September 16, 2009 2 3 p.m. EDT Welcome Ma. Hougan Managing Director ETF Analy?cs IndexUniverse.com

Setting The Record Straight: Achieving Success Beyond a Day with Leveraged and Inverse Funds Live Webinar September 16, 2009 2 3 p.m. EDT Welcome Ma. Hougan Managing Director ETF Analy?cs IndexUniverse.com

Index January Return* 2018 YTD Return % DJIA NASDAQ Composite S&P 500 Index

Charles Sherry Director, Institutional Education Group Blue Ocean Global Wealth 9841 Washingtonian Blvd., #200 Gaithersburg, MD 20878 Tel: 720.308.4560 csherry@blueoceanglobalwealth.com 2018 January Financial

Charles Sherry Director, Institutional Education Group Blue Ocean Global Wealth 9841 Washingtonian Blvd., #200 Gaithersburg, MD 20878 Tel: 720.308.4560 csherry@blueoceanglobalwealth.com 2018 January Financial

Portfolio Construction Research by

Portfolio Construction Research by Real World Case Studies in Portfolio Construction Using Robust Optimization By Anthony Renshaw, PhD Director, Applied Research July 2008 Copyright, Axioma, Inc. 2008

Portfolio Construction Research by Real World Case Studies in Portfolio Construction Using Robust Optimization By Anthony Renshaw, PhD Director, Applied Research July 2008 Copyright, Axioma, Inc. 2008

How Good is 1/n Portfolio?

How Good is 1/n Portfolio? at Hausdorff Research Institute for Mathematics May 28, 2013 Woo Chang Kim wkim@kaist.ac.kr Assistant Professor, ISysE, KAIST Along with Koray D. Simsek, and William T. Ziemba

How Good is 1/n Portfolio? at Hausdorff Research Institute for Mathematics May 28, 2013 Woo Chang Kim wkim@kaist.ac.kr Assistant Professor, ISysE, KAIST Along with Koray D. Simsek, and William T. Ziemba

Applicability of Capital Asset Pricing Model in the Indian Stock Market

Applicability of Capital Asset Pricing Model in the Indian Stock Market Abstract: Capital Asset Pricing Model (CAPM) was a revolution in financial theory. CAPM postulates an equilibrium linear association

Applicability of Capital Asset Pricing Model in the Indian Stock Market Abstract: Capital Asset Pricing Model (CAPM) was a revolution in financial theory. CAPM postulates an equilibrium linear association

David Stendahl And Position Sizing

On Improving Your Results David Stendahl And Position Sizing David Stendahl is the portfolio manager at Capitalogix, a Commodity Trading Advisor (CTA) firm specializing in systematic trading. He is also

On Improving Your Results David Stendahl And Position Sizing David Stendahl is the portfolio manager at Capitalogix, a Commodity Trading Advisor (CTA) firm specializing in systematic trading. He is also

Seeking Beta in the Bond Market: A Mathdriven Investment Strategy for Higher Returns

Seeking Beta in the Bond Market: A Mathdriven Investment Strategy for Higher Returns November 23, 2010 by Georg Vrba, P.E. Advisor Perspectives welcomes guest contributions. The views presented here do

Seeking Beta in the Bond Market: A Mathdriven Investment Strategy for Higher Returns November 23, 2010 by Georg Vrba, P.E. Advisor Perspectives welcomes guest contributions. The views presented here do

SKYBRIDGEVIEWS Why Investors Should Allocate To Hedge Funds

SKYBRIDGEVIEWS Why Investors Should Allocate To Hedge Funds Second Edition: Original release was January 2015 SUMMER 2017 UPDATE When we originally published this White Paper in January 2015, we laid out

SKYBRIDGEVIEWS Why Investors Should Allocate To Hedge Funds Second Edition: Original release was January 2015 SUMMER 2017 UPDATE When we originally published this White Paper in January 2015, we laid out

Financial Markets Economics Fall, 2013

Financial Markets Economics Fall, 2013 What Can You Do With Your Money? Spend it or save it Savings: income not used for consumption Marginal propensity to consume: the change in personal spending that

Financial Markets Economics Fall, 2013 What Can You Do With Your Money? Spend it or save it Savings: income not used for consumption Marginal propensity to consume: the change in personal spending that

PUTW. WisdomTree CBOE S&P 500 PutWrite Strategy Fund

WisdomTree CBOE S&P 500 PutWrite Strategy Fund PUTW The S&P 500 Index (SPX) is one of the most widely followed indexes for U.S. stock market exposure. And many investors have an investment (or two) that

WisdomTree CBOE S&P 500 PutWrite Strategy Fund PUTW The S&P 500 Index (SPX) is one of the most widely followed indexes for U.S. stock market exposure. And many investors have an investment (or two) that

Analysis of fi360 Fiduciary Score : Red is STOP, Green is GO

Analysis of fi360 Fiduciary Score : Red is STOP, Green is GO January 27, 2017 Contact: G. Michael Phillips, Ph.D. Director, Center for Financial Planning & Investment David Nazarian College of Business

Analysis of fi360 Fiduciary Score : Red is STOP, Green is GO January 27, 2017 Contact: G. Michael Phillips, Ph.D. Director, Center for Financial Planning & Investment David Nazarian College of Business

Which Investment Option Would You Choose?

CHAPTER 9 Investment Management: Concepts and Strategies Elements of risk Which Investment Option Would You Choose? FIXED INCOME SECURITIES FIXED-INCOME SECURITY RETURN Where does it come from? FIXED-INCOME

CHAPTER 9 Investment Management: Concepts and Strategies Elements of risk Which Investment Option Would You Choose? FIXED INCOME SECURITIES FIXED-INCOME SECURITY RETURN Where does it come from? FIXED-INCOME

SDOG ALPS SECTOR DIVIDEND DOGS ETF VALUE, INCOME, DIVERSIFICATION

ALPS SECTOR DIVIDEND DOGS ETF VALUE, INCOME, DIVERSIFICATION discipline diversification analysis SDOG provides the potential opportunity to capture above-market returns and high dividend income in a disciplined,

ALPS SECTOR DIVIDEND DOGS ETF VALUE, INCOME, DIVERSIFICATION discipline diversification analysis SDOG provides the potential opportunity to capture above-market returns and high dividend income in a disciplined,

Navigator High Dividend Equity

CCM-17-09-6 As of 9/30/2017 Navigator High Dividend Equity Navigate the U.S. Equity Markets with a Focus on Dividend Growth We believe it is prudent to focus on dividend growth through fundamental analysis,

CCM-17-09-6 As of 9/30/2017 Navigator High Dividend Equity Navigate the U.S. Equity Markets with a Focus on Dividend Growth We believe it is prudent to focus on dividend growth through fundamental analysis,

Dividend Growth The Ultimate Equity Strategy

Breiter Capital Management, Inc. Anna Maria, FL 34216 www.breitercapital.com Dividend Growth The Ultimate Equity Strategy Why Rising Dividends Matter As the largest generation ever to approach retirement

Breiter Capital Management, Inc. Anna Maria, FL 34216 www.breitercapital.com Dividend Growth The Ultimate Equity Strategy Why Rising Dividends Matter As the largest generation ever to approach retirement

Lecture # Applications of Utility Maximization

Lecture # 10 -- Applications of Utility Maximization I. Matching vs. Non-matching Grants Here we consider how direct aid compares to a subsidy. Matching grants the federal government subsidizes local spending.

Lecture # 10 -- Applications of Utility Maximization I. Matching vs. Non-matching Grants Here we consider how direct aid compares to a subsidy. Matching grants the federal government subsidizes local spending.

Risks and Returns of Relative Total Shareholder Return Plans Andy Restaino Technical Compensation Advisors Inc.

Risks and Returns of Relative Total Shareholder Return Plans Andy Restaino Technical Compensation Advisors Inc. INTRODUCTION When determining or evaluating the efficacy of a company s executive compensation

Risks and Returns of Relative Total Shareholder Return Plans Andy Restaino Technical Compensation Advisors Inc. INTRODUCTION When determining or evaluating the efficacy of a company s executive compensation

Financial Analysis The Price of Risk. Skema Business School. Portfolio Management 1.

Financial Analysis The Price of Risk bertrand.groslambert@skema.edu Skema Business School Portfolio Management Course Outline Introduction (lecture ) Presentation of portfolio management Chap.2,3,5 Introduction

Financial Analysis The Price of Risk bertrand.groslambert@skema.edu Skema Business School Portfolio Management Course Outline Introduction (lecture ) Presentation of portfolio management Chap.2,3,5 Introduction

Please choose the most correct answer. You can choose only ONE answer for every question.

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation