India Notes. Solid.Established.Committed.

|

|

|

- Shanon Robertson

- 5 years ago

- Views:

Transcription

1 Investor Update October, 2009 India Notes Against all consensus estimates industrial production rose by 10.4% YoY in August. On a seasonally-adjusted MoM basis, IIP was up 1.2% vs. -0.4% last month. Apart from a low base effect, trends were supported by: (1) doubledigit growth across sectors, with mining up 12.9%, while manufacturing and electricity rose 10.2% and 10.6% respectively; (2) as per the use-based classification, consumer durables posted buoyant trends, on the back of festive demand and government stimulus measures. The 2Q09 balance of payments (BoP) details show a smart rebound in foreign direct investment (FDI) inflows into India. Outbound FDI was weaker, thereby resulting in an even stronger upturn in net FDI. The jump in FDI is more important trend than the anticipated current account (CA) deficit in 2Q. Net FDI increased to US$6.8bn in 2Q, more than double the US$3.2bn in the prior quarter, and is already an impressive 39% of the full-year outcome for the last fiscal year. Inward FDI jumped to US$9.5bn (up from US$8.0bn in 1Q09), while outbound FDI declined to US$2.6bn from US$4.8bn over the same time. On the global level there is increasing optimism that economies are likely to come out of recession post stimulus packages infused by the Governments. The inflows from the FIIs have been positive in the Indian capital market with net inflow of Rs729bn (USD 15 bn) YTD. Overseas borrowing has more to pick up as Indian companies again start factoring in expectations of currency appreciation in their rupee cost of overseas borrowing. The rupee remains a structurally undervalued currency, and the ongoing pickup in capital inflows will increase the pressure for appreciation. Admittedly, shifting global risk appetite will cause volatility but the trend of rupee appreciation should still play out. Analyst s project INR/USD forecast of 46 and 43 for end-december 2009 and end-june In this issue: Economy & Markets 2 Real Estate 4 Market Summary 5 Contact Us Yatra Capital Limited 43/45 La Motte Street St. Helier Jersey JE4 8SD info@yatracapital.com Website: Gavin Wilkins Tel: +44 (0) Fax: +44 (0) Gavin.Wilkins@minerva-trust.com Investment Advisor Saffron Capital Advisors Limited Suite 2004 Level 2, Alexander House 35 Cybercity Mauritius Pg Ajoy Veer Kapoor Vijay Ganesh Tel: Fax: vganesh@saffroncapitaladvisors.mu ajoyveerkapoor@saffronadvisors.mu Website: 1

2 Economy & Markets Double-digit growth IIP India's industrial sector is back and back with a vengeance. The 10.4% year-on-year rise in August was the first double-digit increase in output since October 2007 and compares with a bottom of -0.2% in December. On a seasonally adjusted basis, analysts calculations suggest that output rose 2.3% on the month and 5.9% in 3 month-on-3 month terms (25.9% annualised). The latter is India's strongest increase since at least mid-1994 and can only be termed a powerful V-shaped recovery. Part of the improvement reflects stronger exports which were up a seasonally adjusted 13% in the 3 months to August relative to the previous 3 months, while domestic demand also remains robust according to the India manufacturing and services PMI series. The breakdown of the August release by industry showed mining (12.9%), manufacturing (10.2%) and electricity (10.6%) all registering double-digit growth. By category, the real star was consumer durables, which expanded 22.3% on the year the strongest rise since October Meanwhile, basic and intermediate goods were up 10% and 14.3% respectively, with capital goods production rising 8.3%. The last of these remains below the long-term average of 9.8% but is likely to continue trending higher as confidence in the durability of the recovery strengthens over time. Non-durable consumer goods were the only area to show a slowdown (to 3.7% from 5.8%). Inevitably the strength of the release will raise concerns that the Reserve Bank of India will move rates higher when it next meets on 27 October. In what has turned out to be a very public debate, it is obvious that while the RBI is thinking hard about the first rate rise, the Minister of Finance (and no doubt most of the government) is strongly against an early move. Analysts continue to expect the first Cash Reserve Ratio hike to come in early 2010, with policy interest rates increasing from the April to June quarter. Foreign direct investment posts a smart rebound The latest balance of payments (BoP) details for calendar 2Q09 (also the first quarter of India s fiscal year that ends in March) show a huge positive trend that appears to be ignored: foreign direct investment (FDI) posted a handsome rebound in the quarter. Several commentaries on the BoP trends will again lament on the current account (CA) deficit, the main story in the latest quarterly BoP is the surge in FDI, both on inflows and on net (inflows minus outflows) basis. Net FDI increased to US$6.8bn in 2Q, more than double the US$3.2bn in the prior quarter, and is already an impressive 39% of the full-year outcome for the last fiscal year. The pickup was due to higher inflows and lower outflows. Inward FDI jumped to US$9.5bn (up from US$8.0bn in 1Q09), while outbound FDI declined to US$2.6bn from US$4.8bn over the time. FDI to India was channelled mainly into manufacturing sector (19.2%), real estate activities (15.6%), financial services (15.4%), construction (12.2%) and business services (11.7%). Mauritius continued to be the major source of FDI during 2Q09 with a share of 48.9% followed by the US at 12.8%. 2

3 Key implications of higher FDI 1 There are two important implications of this early rebound in FDI 1) It will add to the magnitude of capital inflows into India, which in turn should more than offset the CA deficit, and cause further pressure on the rupee to appreciate. Analysts have forecasted INR/USD in the range 46 and 43 for end-december 2009 and end-june 2010, respectively. The INR has lagged other Asian currencies in its appreciation against USD. Admittedly, shifting global risk appetite will cause volatility but the broader trend of rupee appreciation should still play out. 2) It will improve the availability and flow of funds for investment activity. The financing for investment is already improving owing to multiple factors such as: (a) higher local bank lending; (b) an increase in equity-related financing; and (c) improving overseas borrowing by Indian companies. As expectations of further rupee appreciation solidify and global credits markets open up, Indian companies will increasingly be in a position to tap international capital markets. Higher overseas borrowing will further complement other capital inflows into India, and increase the scope for further rupee appreciation. Current Account Deficit should not be a concern The issue of India s current account (CA) deficits has always been a worry with investors. However, it is important to appreciate that India is a capitalstarved economy, and its investment rate will exceed domestic saving rate if it has to engineer 7 8% annual GDP growth. The key issue from macroeconomic stability perspective is the size of the current account deficit and how it is funded. Indeed, with its high pace of economic growth, a large stock of foreign exchange reserves, India can manage a CA deficit of 2 3% of GDP without serious challenges. The current account balance slipped into the red, posting a shortfall of US$5.8bn in 2Q09 after a surplus of US$4.7bn in 1Q09. The key reason for the wider deficit was a bigger shortfall on the trade account that was not offset by the surplus on the invisible balance (which includes software receipts and remittances from Indians working overseas). The slippage on the CA deficit was expected following the seasonal surplus in 1Q09. Monsoon Update Monsoon activity has seen a pick-up over the past month. Cumulative rainfall deficiency is now at 21% levels from 29% seen in mid-august. While the damage to summer crop sowing is already done, the improvement in rainfall is encouraging and bodes well for the winter crop, which accounts for ~50% of foodgrain output. Currency Markets The Indian Rupee faces a surprisingly strong recovery especially during the festive season, as the world psychologically and economically recovers from the crisis. The surge in FII flows in the past week has been responsible for the sharp move in USD/INR. From the 16th of September, Indian Markets have averaged about Rs 1,800 cr of net FII equity investments on a daily basis. USD/INR was rather resilient during these phases of inflows, probably as some argue that there was RBI intervention at that juncture. But finally come October and analysts see USD/INR at sub-47 levels. 1 3

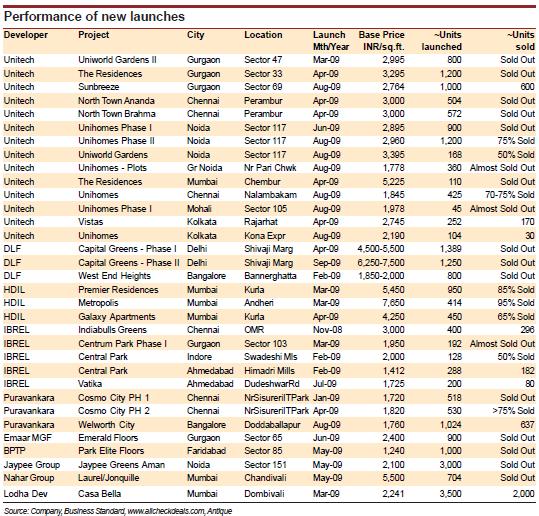

4 Model Real Estate (Regulation of Development) Act A draft Model Real Estate (Regulation of Development) Act has been circulated among States by the Ministry of Housing & Urban Poverty Alleviation, as documented in press reports. The intention is to create a real estate regulatory authority that will monitor the sector. It is expected that such a move could improve sector transparency in the long run and protect buyers. However, the process of adapting to new regulations may be time consuming. Also, with realty being a State subject, it may be up to State governments to implement and enforce the proposals so it remains to be seen if and when the current proposals, or a watered-down version, are implemented. Some key points of Model Act as per press reports: 1. Construction of apartments cannot be undertaken without registration with regulatory authority. 2. Promoters cannot advertise project before registration is completed i.e. we believe this could prevent soft launching and selling before approvals are granted. 3. Promoter has to furnish bank guarantee to competent authority, equal to 5% of estimated development cost. 4. No deposit or advance to be taken by Promoter without first entering into an agreement of sale. 5. Regulatory Authority will have all project information on its website 6. Buyers/prospective buyers to be provided with all details such as registration, title, names of sale agents etc. 7. Promoters to compensate buyers that have suffered loss/damage due to misleading advertisements. 8. Any defects brought to notice within two years from date of possession to be rectified by Promoter without charge to buyers. 9. If Promoter fails to give possession on time, will be liable to give refund of amounts already received, with interest/penalties. 10. Failure to comply with provisions of Act will attract penalties. This proposed regulation is in the draft stage and has been published by the Ministry of Housing as a part of its 100 day agenda. The current draft has been made open to the opinion of people and industry bodies. After having taken the feedback of the people at large and the industry, this will be debated in the parliament and implemented as a law subject being passed by the majority of the voted representatives. Is the worst over? Fundamentals of the real estate sector are improving as seen by better liquidity and improved demand in the residential segment. Enhanced affordability, lower mortgage rates and better job security have helped revive demand for homes. The worst seems to be over and the sector is progressively recovering led by the residential segment. Key signs of improvement include: 1) Attractively priced new launches in the residential segment have seen good bookings with some projects being sold out within a few days of launch; 2) Improved balance sheets of developers through infusion of funds from QIPs and sale of nonstrategic assets. While the residential segment is witnessing a recovery in demand, the office and retail segments are still sluggish and will take some time to recover as the economy gradually gets back on track. Last year s slowdown has caused several developers to rethink their strategies: 1) Focus has shifted to affordable/midincome housing from luxury housing; 2) In commercial projects, several developers to manage liquidity are moving to 'sale model' rather than leasing space. Some developers are also converting commercial projects into residential, where possible; 3) Developers are exiting low visibility large township projects and are instead targeting strategically located land parcels in and around key cities; 4) Developers are delaying SEZ projects, especially IT SEZs, because of poor demand. 4

5 Focus on affordable housing From 2005 to 2008, developers were largely concentrating on luxury residential projects. However, with rising property prices and home loan rates and large ticket sizes, residential property became out of reach for the large majority of homebuyers. With affordability adversely impacted, residential demand saw a significant slowdown. To bring back demand, developers shifted focus from luxury to affordable housing with the objective of reducing the overall cost of homes. This was achieved by launching new projects where in addition to lower prices per sq. ft., developers also offered smaller sized homes. Revival of Residential demand After seeing a sharp slowdown in demand in the latter half of 2008, residential demand began picking up from March-April 2009 on the back of better affordability and increased job security. Improved affordability has been a function of lower property prices, smaller apartment sizes and lower interest rates. Several new projects launched since March-April 2009, have seen good demand with many of the projects being sold out within a few days of launch. Demand in the current festive season will be an important indicator of recovery in the residential segment. Residential prices have declined substantially Property prices rose rapidly from 2005 to early 2008 and became a deterrent for home buyers resulting in a sharp slowdown in the residential demand. However, since end of 2008 and in early 2009, property prices began correcting and have declined up to 25 30% from their peak levels. This has helped bring back demand in the residential segment. The exceptions to this industry trends have been the cities of Mumbai and Delhi which have seen significant interest at lower prices. Developers have based on limited availability and the interest started raising prices of apartments again. Commercial Space Leasing in commercial space has not picked up significantly however as per channel checks there has been a significant increase in enquiries from corporate houses for commercial space. Current estimates still suggest that that though transaction activity is yet to pick up interest has risen on stronger business performance and pick up in hiring. Retail Space Retail space demand is currently slow with sales activity not having picked up significantly. Retailers are still in cautious mode before embarking on expansions due to cash flow concerns where expansion would mean additional stress on already stretched balance sheets. Retailers who are looking at expanding continue to negotiate revenue shares rather than fixed rate rentals. The festive season should be a crucial as pickup in sales activity should see a return of retailer confidence. 5

6 6

India Notes. Solid.Established.Committed. Monetary Policy Update: RBI raises CRR, Repo/Reverse- Repo Rates Unchanged

Investor Update February,2010 India Notes Monetary Policy Update: RBI raises CRR, Repo/Reverse- Repo Rates Unchanged Contrary to street expectations, the RBI raised the CRR by 75bps v/s expectations of

Investor Update February,2010 India Notes Monetary Policy Update: RBI raises CRR, Repo/Reverse- Repo Rates Unchanged Contrary to street expectations, the RBI raised the CRR by 75bps v/s expectations of

India Notes. Solid.Established.Committed.

Investor Update January,200 India Notes India: Rebalancing in 200 The overarching story in India this year is that of releveraging and the return of risk-taking, as a combination of easy capital and capacity

Investor Update January,200 India Notes India: Rebalancing in 200 The overarching story in India this year is that of releveraging and the return of risk-taking, as a combination of easy capital and capacity

India Notes. Solid.Established.Committed. India Inc hiring activity rises 22% in Sept

Investor Update September, 2010 India Notes India Inc hiring activity rises 22% in Sept Hiring by India Inc surged by 22 per cent in September this year, driven by improved confidence in the economy, a

Investor Update September, 2010 India Notes India Inc hiring activity rises 22% in Sept Hiring by India Inc surged by 22 per cent in September this year, driven by improved confidence in the economy, a

India Notes. Solid.Established.Committed. RBI announces its policy Tightens up on Real Estate

Investor Update November, 2010 India Notes RBI announces its policy Tightens up on Real Estate The Reserve Bank of India (RBI) lifted both the repo rate and reverse repo rates by 25bps to 6.25% and 5.25%

Investor Update November, 2010 India Notes RBI announces its policy Tightens up on Real Estate The Reserve Bank of India (RBI) lifted both the repo rate and reverse repo rates by 25bps to 6.25% and 5.25%

India Notes. Solid. Established. Committed.

Investor Update Vol. 1, Issue 4 March- April, 2009 India Notes In this issue: Pg The political temperature has begun rising steadily as India s 714 million electorate (the largest in any democracy) prepare

Investor Update Vol. 1, Issue 4 March- April, 2009 India Notes In this issue: Pg The political temperature has begun rising steadily as India s 714 million electorate (the largest in any democracy) prepare

MONTHLY UPDATE NOVEMBER 2018

MONTHLY UPDATE NOVEMBER 2018 November 2018 A champion is defined not by their wins but by how they can recover when they fall. Equity markets - Serena Williams Indices 31 st Oct 2018 30 th Nov 2018 1 Month

MONTHLY UPDATE NOVEMBER 2018 November 2018 A champion is defined not by their wins but by how they can recover when they fall. Equity markets - Serena Williams Indices 31 st Oct 2018 30 th Nov 2018 1 Month

Prepared by Basanta K Pradhan & Sangeeta Chakravarty January and February 2013

Prepared by Basanta K Pradhan & Sangeeta Chakravarty January and February 2013 Highlights Sharp fluctuation in Industrial activity Headline inflation is down marginally Marginal rise in CPI inflation Rupee

Prepared by Basanta K Pradhan & Sangeeta Chakravarty January and February 2013 Highlights Sharp fluctuation in Industrial activity Headline inflation is down marginally Marginal rise in CPI inflation Rupee

Prepared by Basanta K Pradhan & Sangeeta Chakravarty December 2012

Prepared by Basanta K Pradhan & Sangeeta Chakravarty December 2012 Highlights Sharp fluctuation in Industrial activity Headline inflation is down marginally CPI inflation fell very marginally Rupee stabilizing

Prepared by Basanta K Pradhan & Sangeeta Chakravarty December 2012 Highlights Sharp fluctuation in Industrial activity Headline inflation is down marginally CPI inflation fell very marginally Rupee stabilizing

India Notes. Solid.Established.Committed. India GDP grows most since Dec 2007; tightening seen

Investor Update September, 2010 India Notes India GDP grows most since Dec 2007; tightening seen India's economy grew at its fastest pace in nearly three years in the April-June 2010 quarter on strong

Investor Update September, 2010 India Notes India GDP grows most since Dec 2007; tightening seen India's economy grew at its fastest pace in nearly three years in the April-June 2010 quarter on strong

Prepared by Basanta K Pradhan & Sangeeta Chakravarty August 2010

Prepared by Basanta K Pradhan & Sangeeta Chakravarty August 21 Highlights Industrial growth cools down WPI inflation falls marginally. Rupee appreciates marginally The annual growth of Index of Industrial

Prepared by Basanta K Pradhan & Sangeeta Chakravarty August 21 Highlights Industrial growth cools down WPI inflation falls marginally. Rupee appreciates marginally The annual growth of Index of Industrial

FINCLUSION Newsletter No. 31 (dated 14th May 2014). Contact us at

. Contact us at") As highlighted in a previous newsletter, the macroeconomic indicators for the Indian economy have shown substantial improvement over the past year. In this newsletter, we provide an update on the frequently

As highlighted in a previous newsletter, the macroeconomic indicators for the Indian economy have shown substantial improvement over the past year. In this newsletter, we provide an update on the frequently

India Notes. Solid.Established.Committed.

Investor Update Vol. 1, Issue 4 May, 2009 India Notes In this issue: Pg As India s month-long exercise in adult franchise enters its final phase, there is no clear indication on who will emerge the winner.

Investor Update Vol. 1, Issue 4 May, 2009 India Notes In this issue: Pg As India s month-long exercise in adult franchise enters its final phase, there is no clear indication on who will emerge the winner.

MonitorING Turkey ING BANK A.Ş. Further fiscal support in the Medium Term Plan. Emerging Markets 4 October 2017

q ING BANK A.Ş. ECONOMIC RESEARCH GROUP MonitorING Turkey October 17 Emerging Markets October 17 USD/TRY MonitorING Turkey Further fiscal support in the Medium Term Plan In 17, accelerated spending and

q ING BANK A.Ş. ECONOMIC RESEARCH GROUP MonitorING Turkey October 17 Emerging Markets October 17 USD/TRY MonitorING Turkey Further fiscal support in the Medium Term Plan In 17, accelerated spending and

Prepared by Basanta K Pradhan & Sangeeta Chakravarty November 2009

Prepared by Basanta K Pradhan & Sangeeta Chakravarty November 2009 Index of industrial production shows sign of economic recovery IIP increased by 9.1 percent Inflation now turning positive High food prices

Prepared by Basanta K Pradhan & Sangeeta Chakravarty November 2009 Index of industrial production shows sign of economic recovery IIP increased by 9.1 percent Inflation now turning positive High food prices

Country Risk Analysis

SEB MERCHANT BANKING COUNTRY RISK ANALYSIS December 11, 2014 Analyst: Martin Carlens. Tel: +46-8-7639605. E-mail: martin.carlens@seb.se Economic growth has bottomed, sentiment is rising following the elections

SEB MERCHANT BANKING COUNTRY RISK ANALYSIS December 11, 2014 Analyst: Martin Carlens. Tel: +46-8-7639605. E-mail: martin.carlens@seb.se Economic growth has bottomed, sentiment is rising following the elections

REFERENCE NOTE. No. 28/RN/Ref./November /2013

LOK SABHA SECRETARIAT PARLIAMENT LIBRARY AND REFERENCE, RESEARCH, DOCUMENTATION AND INFORMATION SERVICE (LARRDIS) MEMBERS REFERENCE SERVICE REFERENCE NOTE. No. 28/RN/Ref./November /2013 For the use of

LOK SABHA SECRETARIAT PARLIAMENT LIBRARY AND REFERENCE, RESEARCH, DOCUMENTATION AND INFORMATION SERVICE (LARRDIS) MEMBERS REFERENCE SERVICE REFERENCE NOTE. No. 28/RN/Ref./November /2013 For the use of

Balance of Payment Q3 FY (October-December 2012)

") Balance of Payment Q3 FY2012-13 (October-December 2012) Key Highlights: - India s Current Account Deficit (CAD) widened to a record high of 6.7% of GDP in Q3 FY2012-13 on the back of surging oil and gold

Balance of Payment Q3 FY2012-13 (October-December 2012) Key Highlights: - India s Current Account Deficit (CAD) widened to a record high of 6.7% of GDP in Q3 FY2012-13 on the back of surging oil and gold

FICCI Economic Outlook Survey

FICCI Economic Outlook Survey January 2010 FICCI, Federation House, 1, Tansen Marg, New Delhi About the Survey The Economic Outlook Survey was conducted during the period January 1 to January 15, 2010.

FICCI Economic Outlook Survey January 2010 FICCI, Federation House, 1, Tansen Marg, New Delhi About the Survey The Economic Outlook Survey was conducted during the period January 1 to January 15, 2010.

RBI s Q Monetary Policy: Expectations

Amol Agrawal amol@stcipd.com +91-22-66202234 RBI s Q2 2011-12 Monetary Policy: Expectations RBI is scheduled to announce its second quarter 2011-12 monetary policy review on October 25, 2011. We expect

Amol Agrawal amol@stcipd.com +91-22-66202234 RBI s Q2 2011-12 Monetary Policy: Expectations RBI is scheduled to announce its second quarter 2011-12 monetary policy review on October 25, 2011. We expect

MONTHLY UPDATE SEPTEMBER 2017

MONTHLY UPDATE SEPTEMBER 2017 September 2017 "I am a better investor because I am a businessman and a better businessman because I am an investor. - Warren Buffett Equity Markets Indices 31 st Aug 2017

MONTHLY UPDATE SEPTEMBER 2017 September 2017 "I am a better investor because I am a businessman and a better businessman because I am an investor. - Warren Buffett Equity Markets Indices 31 st Aug 2017

The FDI-driven export growth story continues to power ahead despite the US withdrawal from TPP

Vietnam s economy grew 6.2% yoy in 2016, versus 6.7% in 2015, weighed down by a slowdown in the agriculture and mining sectors. There was a further moderation to 5.1% growth in 1Q17. Nonetheless, on the

Vietnam s economy grew 6.2% yoy in 2016, versus 6.7% in 2015, weighed down by a slowdown in the agriculture and mining sectors. There was a further moderation to 5.1% growth in 1Q17. Nonetheless, on the

MONTHLY ECONOMIC BULLETIN

MONTHLY ECONOMIC BULLETIN Febru ruary 2015,, Volume 1, Issue 4 Vanijya Bhavan (1st Floor) International Trade Facilitation Centre 1/1 Wood Street Kolkata - 700016 http://www.eepcindia.org E E PC India

MONTHLY ECONOMIC BULLETIN Febru ruary 2015,, Volume 1, Issue 4 Vanijya Bhavan (1st Floor) International Trade Facilitation Centre 1/1 Wood Street Kolkata - 700016 http://www.eepcindia.org E E PC India

Viet Nam GDP growth by sector Crude oil output Million metric tons 20

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

CRS Report for Congress

CRS Report for Congress Received through the CRS Web Order Code RS21951 October 12, 2004 Changing Causes of the U.S. Trade Deficit Summary Marc Labonte and Gail Makinen Government and Finance Division

CRS Report for Congress Received through the CRS Web Order Code RS21951 October 12, 2004 Changing Causes of the U.S. Trade Deficit Summary Marc Labonte and Gail Makinen Government and Finance Division

Equity Update August 2018

Market Overview (as on July 31, 2018) Flows July-18 June-18 May-18 FIIs (Net Purchases / Sales) (Rs cr) MFs (Net Purchases / Sales) (Rs cr) Domestic Markets Macro Indicators GDP (YoY%) IIP (YoY%) Crude

Market Overview (as on July 31, 2018) Flows July-18 June-18 May-18 FIIs (Net Purchases / Sales) (Rs cr) MFs (Net Purchases / Sales) (Rs cr) Domestic Markets Macro Indicators GDP (YoY%) IIP (YoY%) Crude

WHAT'S NEW. International Developments. U.S. GDP expanded an annualized 0.50% in the first quarter of 2016, the slowest pace in two years.

International Developments U.S. GDP expanded an annualized 0.50% in the first quarter of 2016, the slowest pace in two years. China's GDP grew 6.70% in first quarter of 2016, down from 6.80% in fourth

International Developments U.S. GDP expanded an annualized 0.50% in the first quarter of 2016, the slowest pace in two years. China's GDP grew 6.70% in first quarter of 2016, down from 6.80% in fourth

The Stock Market's Final Four

The Stock Market's Final Four April 2, 2019 by John Lynch of LPL Financial The NCAA Final Four is set. On the men s side, Auburn, Michigan State, Texas Tech, and Virginia are headed to Minneapolis to determine

The Stock Market's Final Four April 2, 2019 by John Lynch of LPL Financial The NCAA Final Four is set. On the men s side, Auburn, Michigan State, Texas Tech, and Virginia are headed to Minneapolis to determine

Economic ProjEctions for

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Buoyancy in industrial sector growth continues. This year s first quarter IIP growth is at 10.3% compared to 7.7% in

Prepared by N. R. Bhanumurthy August 25 Buoyancy in industrial sector growth continues. This year s first quarter IIP growth is at 1.3% compared to 7.7% in 24-5. TOP STORIES The index of industrial production

Prepared by N. R. Bhanumurthy August 25 Buoyancy in industrial sector growth continues. This year s first quarter IIP growth is at 1.3% compared to 7.7% in 24-5. TOP STORIES The index of industrial production

Current Economic Scenario: Some Indicators

LOK SABHA SECRETARIAT PARLIAMENT LIBRARY AND REFERENCE, RESEARCH, DOCUMENTATION AND INFORMATION SERVICE (LARRDIS) MEMBERS REFERENCE SERVICE REFERENCE NOTE. No. 26 /RN/Ref./August /2013 For the use of Members

LOK SABHA SECRETARIAT PARLIAMENT LIBRARY AND REFERENCE, RESEARCH, DOCUMENTATION AND INFORMATION SERVICE (LARRDIS) MEMBERS REFERENCE SERVICE REFERENCE NOTE. No. 26 /RN/Ref./August /2013 For the use of Members

All the BRICs dampening world trade in 2015

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

WHAT'S NEW. International Developments

International Developments Bank of Canada raised its target for the overnight rate to 1% citing strongerthan-expected economic performance warranting a removal of some of the considerable stimulus in place

International Developments Bank of Canada raised its target for the overnight rate to 1% citing strongerthan-expected economic performance warranting a removal of some of the considerable stimulus in place

Market Update. Market Update: Global Economic Themes. Overview

Market Update Late August 2013 Market Update: Global Economic Themes So far this summer, we have produced two Market Update papers covering capital market themes and geopolitical risks. In this final paper

Market Update Late August 2013 Market Update: Global Economic Themes So far this summer, we have produced two Market Update papers covering capital market themes and geopolitical risks. In this final paper

BELIZE. 1. General trends

Economic Survey of Latin America and the Caribbean 2015 1 BELIZE 1. General trends The economy recovered in 2014 with growth strengthening to 3.6% up from 1.5% in 2013. Growth was driven by increased dynamism

Economic Survey of Latin America and the Caribbean 2015 1 BELIZE 1. General trends The economy recovered in 2014 with growth strengthening to 3.6% up from 1.5% in 2013. Growth was driven by increased dynamism

Mongolia Economic Brief

September 216 http://www.worldbank.org/mongolia Mongolia Economic Brief The budget deficit sharply rose in the first seven months of 216 amid spending increases and revenue shortfalls. The deficit reached

September 216 http://www.worldbank.org/mongolia Mongolia Economic Brief The budget deficit sharply rose in the first seven months of 216 amid spending increases and revenue shortfalls. The deficit reached

Review of the Economy. E.1 Global trends. January 2014

Export performance was robust during the third quarter, partly on account of the sharp depreciation in the exchange rate of the rupee and partly on account of a modest recovery in major advanced economies.

Export performance was robust during the third quarter, partly on account of the sharp depreciation in the exchange rate of the rupee and partly on account of a modest recovery in major advanced economies.

Economic Outlook Survey September 2015

FICCI s Economic Outlook Survey: GDP growth at 7.6% for 2015-16 Results of FICCI s latest Economic Outlook Survey indicate moderation in GDP growth estimates. Based on the responses received, the median

FICCI s Economic Outlook Survey: GDP growth at 7.6% for 2015-16 Results of FICCI s latest Economic Outlook Survey indicate moderation in GDP growth estimates. Based on the responses received, the median

MCB INDIA SOVEREIGN BOND ETF the "FUND" INTERIM REPORT FOR THE QUARTER ENDED SEPTEMBER 30, 2018

the "FUND" INTERIM REPORT FOR THE QUARTER ENDED SEPTEMBER 30, 2018 INTERIM FINANCIAL STATEMENTS - FOR THE QUARTER ENDED SEPTEMBER 30, 2018 TABLE OF CONTENTS PAGES MANAGEMENT & ADMINISTRATION 1 MANAGER'S

the "FUND" INTERIM REPORT FOR THE QUARTER ENDED SEPTEMBER 30, 2018 INTERIM FINANCIAL STATEMENTS - FOR THE QUARTER ENDED SEPTEMBER 30, 2018 TABLE OF CONTENTS PAGES MANAGEMENT & ADMINISTRATION 1 MANAGER'S

LETTER. economic THE CANADA / U.S. PRODUCTIVITY GAP: THE EFFECT OF FIRM SIZE FEBRUARY Canada. United States. Interest rates.

economic LETTER FEBRUARY 2014 THE CANADA / U.S. PRODUCTIVITY GAP: THE EFFECT OF FIRM SIZE For many years now, Canada s labour productivity has been weaker than that of the United States. One of the theories

economic LETTER FEBRUARY 2014 THE CANADA / U.S. PRODUCTIVITY GAP: THE EFFECT OF FIRM SIZE For many years now, Canada s labour productivity has been weaker than that of the United States. One of the theories

Report Summary. Expectations of reduction in repo rates by RBI. Uptick in global risk appetite sentiments

Decision enabling cash market analysis & price outlook For the week beginning Oct 01, 2012 USDINR last closing (24 hrs market) Fundamental Summary Report Summary 52.84 ( 0.52) as on Sep 28, 2012 Price

Decision enabling cash market analysis & price outlook For the week beginning Oct 01, 2012 USDINR last closing (24 hrs market) Fundamental Summary Report Summary 52.84 ( 0.52) as on Sep 28, 2012 Price

RBI s Monetary Policy Q : Expectations

RBI s Monetary Policy Q2 2012-13: Expectations RBI s Monetary Policy for Second Quarter 2012-13 is scheduled to be announced on 30-Oct- 12. The market expectations are once again divided over rate cut

RBI s Monetary Policy Q2 2012-13: Expectations RBI s Monetary Policy for Second Quarter 2012-13 is scheduled to be announced on 30-Oct- 12. The market expectations are once again divided over rate cut

2012 6 http://www.bochk.com 2 3 4 ECONOMIC REVIEW(A Monthly Issue) June, 2012 Economics & Strategic Planning Department http://www.bochk.com An Analysis on the Plunge in Hong Kong s GDP Growth and Prospects

2012 6 http://www.bochk.com 2 3 4 ECONOMIC REVIEW(A Monthly Issue) June, 2012 Economics & Strategic Planning Department http://www.bochk.com An Analysis on the Plunge in Hong Kong s GDP Growth and Prospects

Indian Economy. Industrial output grew highest in four months in June 2015 but volatility continued

Indian Economy Industrial Production Industrial output grew highest in four months in June 2015 but volatility continued After a slowdown in May 2015, industrial production grew by 3.8% during the month

Indian Economy Industrial Production Industrial output grew highest in four months in June 2015 but volatility continued After a slowdown in May 2015, industrial production grew by 3.8% during the month

A PROPOSAL FOR MONTH YEAR (ALL CAPS) CHARTBOOK. Market Indicators

CHARTBOOK. Market Indicators") A PROPOSAL FOR MONTH YEAR (ALL CAPS) CHARTBOOK Market Indicators November 2015 For more information, contact: Janlo de los Reyes Manager Research and Consultancy janlo.delosreyes@ap.cushwake.com Leo De

A PROPOSAL FOR MONTH YEAR (ALL CAPS) CHARTBOOK Market Indicators November 2015 For more information, contact: Janlo de los Reyes Manager Research and Consultancy janlo.delosreyes@ap.cushwake.com Leo De

Economic activity gathers pace

Produced by the Economic Research Unit October 2014 A quarterly analysis of trends in the Irish economy Economic activity gathers pace Positive data flow Recovery broadening out GDP growth revised up to

Produced by the Economic Research Unit October 2014 A quarterly analysis of trends in the Irish economy Economic activity gathers pace Positive data flow Recovery broadening out GDP growth revised up to

STCI Primary Dealer Ltd

Macroeconomic Update: GDP Q3 FY18 Beating expectations, India s Real GDP noted a sharp rebound, coming in at 7.2% for Q3 FY18, higher than the revised estimate of 6.5% witnessed in the previous quarter.

Macroeconomic Update: GDP Q3 FY18 Beating expectations, India s Real GDP noted a sharp rebound, coming in at 7.2% for Q3 FY18, higher than the revised estimate of 6.5% witnessed in the previous quarter.

Macroeconomic Context and Budget Priorities Shankar Acharya * ICRIER KAS Seminar 2013, February 21, 2013

Macroeconomic Context and Budget Priorities 2013-14 by Shankar Acharya * ICRIER KAS Seminar 2013, February 21, 2013 * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India,

Macroeconomic Context and Budget Priorities 2013-14 by Shankar Acharya * ICRIER KAS Seminar 2013, February 21, 2013 * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India,

Malaysia- GDP & BOP 1Q17

Real GDP growth surprised on the upside in 1Q17 Real GDP growth rose by 5.6% in 1Q17, exceeding market expectations Malaysia s real GDP growth rose by 5.6% yoy in 1Q17 (4.5% in 4Q16), significantly higher

Real GDP growth surprised on the upside in 1Q17 Real GDP growth rose by 5.6% in 1Q17, exceeding market expectations Malaysia s real GDP growth rose by 5.6% yoy in 1Q17 (4.5% in 4Q16), significantly higher

GUATEMALA. 1. General trends

Economic Survey of Latin America and the Caribbean 2014 1 GUATEMALA 1. General trends GDP grew by 3.7% in 2013 in real terms, versus 3.0% in 2012, reflecting the robustness of domestic demand, mainly from

Economic Survey of Latin America and the Caribbean 2014 1 GUATEMALA 1. General trends GDP grew by 3.7% in 2013 in real terms, versus 3.0% in 2012, reflecting the robustness of domestic demand, mainly from

% % Global Economy Strong global economic recovery remains a distant dream as the global economy is expected to grow moderately in the next couple of years. The Organization for Economic Cooperation and

% % Global Economy Strong global economic recovery remains a distant dream as the global economy is expected to grow moderately in the next couple of years. The Organization for Economic Cooperation and

Malaysia. Real Sector. Economic recovery is gaining momentum.

Malaysia Real Sector Economic recovery is gaining momentum. Malaysia s economy grew 4.7% in the first three quarters of 23, well above the year-earlier pace of 3.7%. GDP rose 5.1% in the third quarter,

Malaysia Real Sector Economic recovery is gaining momentum. Malaysia s economy grew 4.7% in the first three quarters of 23, well above the year-earlier pace of 3.7%. GDP rose 5.1% in the third quarter,

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

BCC UK Economic Forecast Q4 2015

BCC UK Economic Forecast Q4 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and

BCC UK Economic Forecast Q4 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and

Economic Projections For 2014 And 2015

Economic Projections For 2014 And 2015 Article published in the Quarterly Review 2014:3, pp. 77-81 7. ECONOMIC PROJECTIONS FOR 2014 AND 2015 Outlook for the Maltese economy 1 The Bank s latest macroeconomic

Economic Projections For 2014 And 2015 Article published in the Quarterly Review 2014:3, pp. 77-81 7. ECONOMIC PROJECTIONS FOR 2014 AND 2015 Outlook for the Maltese economy 1 The Bank s latest macroeconomic

RICS Economic Research

RICS Economic Research / February 7 th 2014 Michael Hanley Economist www.rics.org/economics The Outlook for the Construction Sector Growth of 4% expected over 2014 Private housing and infrastructure to

RICS Economic Research / February 7 th 2014 Michael Hanley Economist www.rics.org/economics The Outlook for the Construction Sector Growth of 4% expected over 2014 Private housing and infrastructure to

Macroeconomic Update: CPI, WPI and IIP

Macroeconomic Update: CPI, WPI and IIP India s retail inflation for the month of July rose from a record-low to a three-month high of 2.36% on account of an uptick in prices of food items including vegetables

Macroeconomic Update: CPI, WPI and IIP India s retail inflation for the month of July rose from a record-low to a three-month high of 2.36% on account of an uptick in prices of food items including vegetables

ACUMEN. Life of CPI. Three Year Average Inflation

Life of CPI Monetary policy in India has shifted decisively to using the Consumer Price Index (CPI) based inflation rather than Wholesale Price inflation since September 2013. We look at the history of

Life of CPI Monetary policy in India has shifted decisively to using the Consumer Price Index (CPI) based inflation rather than Wholesale Price inflation since September 2013. We look at the history of

Economic Outlook Survey. January 2017

January 2017 GDP growth estimated at 6.8% in 2016-17: FICCI s Economic Outlook Survey HIGHLIGHTS GDP growth for FY 17 estimated at 6.8% The latest round of FICCI s Economic Outlook Survey puts forth an

January 2017 GDP growth estimated at 6.8% in 2016-17: FICCI s Economic Outlook Survey HIGHLIGHTS GDP growth for FY 17 estimated at 6.8% The latest round of FICCI s Economic Outlook Survey puts forth an

GLOBAL SLOWDOWN AND INDIAN ECONOMY

GLOBAL SLOWDOWN AND INDIAN ECONOMY Principal Kasturis College of Arts, Commerce & science Shikhrapur, Pune (MS) INDIA India s financial sector is not deeply integrated with the global financial system,

GLOBAL SLOWDOWN AND INDIAN ECONOMY Principal Kasturis College of Arts, Commerce & science Shikhrapur, Pune (MS) INDIA India s financial sector is not deeply integrated with the global financial system,

STCI Primary Dealer Ltd

Macroeconomic Update : Revision in GDP estimates India s GDP growth rate for FY13 has been revised downwards from 5.0% to 4.5%. All the sectors incorporating agriculture & allied activities, industry and

Macroeconomic Update : Revision in GDP estimates India s GDP growth rate for FY13 has been revised downwards from 5.0% to 4.5%. All the sectors incorporating agriculture & allied activities, industry and

STCI Primary Dealer Ltd

Macroeconomic Update: CPI Inflation and IIP CPI Inflation (Apr-14) Highlights: Headline retail inflation rose to 8.59% for Apr-14 compared to 8.31% in the previous month. Core CPI inflation stood virtually

Macroeconomic Update: CPI Inflation and IIP CPI Inflation (Apr-14) Highlights: Headline retail inflation rose to 8.59% for Apr-14 compared to 8.31% in the previous month. Core CPI inflation stood virtually

Indian Economy. GDP growth slowed down but remained above the comfortable 7% Manufacturing GVAbp

Indian Economy Economic Growth GDP growth slowed down but remained above the comfortable 7% Domestic economy witnessed 7.1% GDP growth during the first quarter (Apr - Jun) of fiscal 2016-17 (Q1FY17) as

Indian Economy Economic Growth GDP growth slowed down but remained above the comfortable 7% Domestic economy witnessed 7.1% GDP growth during the first quarter (Apr - Jun) of fiscal 2016-17 (Q1FY17) as

The Problem of Widening Current Account Deficit of India

The Problem of Widening Current Account Deficit of India Article by Subho Mukherjee (2013) Source: http://www.economicsdiscussion.net/india/the-problem-of-widening-current-accountdeficit-of-india/10909

The Problem of Widening Current Account Deficit of India Article by Subho Mukherjee (2013) Source: http://www.economicsdiscussion.net/india/the-problem-of-widening-current-accountdeficit-of-india/10909

Markit Global Business Outlook

News Release Markit Global Business Outlook EMBARGOED UNTIL: 00:01, 16 March 2015 Global business confidence and hiring intentions slip to post-crisis low Expectations regarding activity and employment

News Release Markit Global Business Outlook EMBARGOED UNTIL: 00:01, 16 March 2015 Global business confidence and hiring intentions slip to post-crisis low Expectations regarding activity and employment

LKP SECURITIES LIMITED 13th Floor Raheja Center, Free Press Marg, Nariman Point, Mumbai

Free Press Marg, Nariman Point, Mumbai-400021 Item Open High Low Close % Cng Net Cng Trend Market Update Gold $ Silver $ LME Alum. LME Copper LME Lead LME Nickel LME Zinc Crude $ Nat. Gas $ Precious Metals

Free Press Marg, Nariman Point, Mumbai-400021 Item Open High Low Close % Cng Net Cng Trend Market Update Gold $ Silver $ LME Alum. LME Copper LME Lead LME Nickel LME Zinc Crude $ Nat. Gas $ Precious Metals

made available a few days after the next regularly scheduled and the Board's Annual Report. The summary descriptions of

FEDERAL RESERVE press release For Use at 4:00 p.m. October 20, 1978 The Board of Governors of the Federal Reserve System and the Federal Open Market Committee today released the attached record of policy

FEDERAL RESERVE press release For Use at 4:00 p.m. October 20, 1978 The Board of Governors of the Federal Reserve System and the Federal Open Market Committee today released the attached record of policy

The USD/CNY Adjustment Is It Complete?

The USD/CNY Adjustment Is It Complete? Derek Halpenny European Head of Global Currency Research European Central Bank June 29 1 Substantial REER Appreciation 1 USD/CNY vs Renminbi REER 9 8 7 6 5 12 11

The USD/CNY Adjustment Is It Complete? Derek Halpenny European Head of Global Currency Research European Central Bank June 29 1 Substantial REER Appreciation 1 USD/CNY vs Renminbi REER 9 8 7 6 5 12 11

MONTHLY UPDATE APRIL 2018

MONTHLY UPDATE APRIL 2018 April 2018 The stock market is the story of cycles and of the human behavior that is responsible for overreactions in both directions. Equity Markets - Seth Klarman Indices 28

MONTHLY UPDATE APRIL 2018 April 2018 The stock market is the story of cycles and of the human behavior that is responsible for overreactions in both directions. Equity Markets - Seth Klarman Indices 28

Finland falling further behind euro area growth

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

Fund Manager Commentary

Fund Manager Commentary October 2018 Indian Equity & Fixed Income Market Overview Market sentiments turned weak during September Equity markets saw heightened volatility during the month and the performance

Fund Manager Commentary October 2018 Indian Equity & Fixed Income Market Overview Market sentiments turned weak during September Equity markets saw heightened volatility during the month and the performance

Irish Economic Update AIB Treasury Economic Research Unit

Irish Economic Update AIB Treasury Economic Research Unit 9th October 2018 Budget 2019 Public Finances in Balance The Irish economy has performed strongly in recent years, boosting tax revenues. Corporation

Irish Economic Update AIB Treasury Economic Research Unit 9th October 2018 Budget 2019 Public Finances in Balance The Irish economy has performed strongly in recent years, boosting tax revenues. Corporation

External Account and Foreign Debt Management

The Lahore Journal of Economics Special Edition External Account and Foreign Debt Management Ashfaque H. Khan * Abstract The paper highlights strong gains in the macro area. The author also shows how total

The Lahore Journal of Economics Special Edition External Account and Foreign Debt Management Ashfaque H. Khan * Abstract The paper highlights strong gains in the macro area. The author also shows how total

MONTHLY REPORT. USDINR Gone By. 2 nd March 2015

USDINR Gone By 2 nd March 2015 Rupee opened the month at 61.99 levels and initially remained on weaker note owing to negative sentiments in Global equities. According to the latest data, US GDP faltered

USDINR Gone By 2 nd March 2015 Rupee opened the month at 61.99 levels and initially remained on weaker note owing to negative sentiments in Global equities. According to the latest data, US GDP faltered

Weekly Macroeconomic Review

20/12/2011 Weekly Macroeconomic Review Expectations derived from the capital market Our forecast Inflation in the coming months Future cumulative inflation next 12 CPIs (through November 2012 CPI) Inflation

20/12/2011 Weekly Macroeconomic Review Expectations derived from the capital market Our forecast Inflation in the coming months Future cumulative inflation next 12 CPIs (through November 2012 CPI) Inflation

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

MARKET REVIEW & OUTLOOK February 2018

MARKET REVIEW & OUTLOOK February 2018 1.0 Fixed Income Economics During the month, Malaysia s 4Q2017 GDP was released. Real Gross Domestic Product ( GDP ) grew 5.9% YoY, slightly slower than the 6.2% recorded

MARKET REVIEW & OUTLOOK February 2018 1.0 Fixed Income Economics During the month, Malaysia s 4Q2017 GDP was released. Real Gross Domestic Product ( GDP ) grew 5.9% YoY, slightly slower than the 6.2% recorded

Editor: Thomas Nilsson. The Week Ahead Key Events 31 Jul 6 Aug, 2017

Editor: Thomas Nilsson The Week Ahead Key Events 31 Jul 6 Aug, 2017 European Sovereign Rating Reviews Recent rating reviews Friday, 21 July 2017 Agency previous new action Greece S&P B- / Stable B- /

Editor: Thomas Nilsson The Week Ahead Key Events 31 Jul 6 Aug, 2017 European Sovereign Rating Reviews Recent rating reviews Friday, 21 July 2017 Agency previous new action Greece S&P B- / Stable B- /

Daily Copper Price Outlook and Strategy

Decision enabling market analysis & price outlook Feb 02, 2015 Market Recap and Summary Outlook for next 3days LME copper, during Friday s trading session, traded in a positive note amidst a sharp short

Decision enabling market analysis & price outlook Feb 02, 2015 Market Recap and Summary Outlook for next 3days LME copper, during Friday s trading session, traded in a positive note amidst a sharp short

LETTER. economic COULD INTEREST RATES HEAD UP IN 2015? JANUARY Canada. United States. Interest rates. Oil price. Canadian dollar.

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

Ontario Economic Accounts

SECOND QUARTER OF 2017 April, May, June Ontario Economic Accounts ONTARIO MINISTRY OF FINANCE Table of Contents ECONOMIC ACCOUNTS Highlights 1 Ontario s Economy Continues to Grow Expenditure Details 2

SECOND QUARTER OF 2017 April, May, June Ontario Economic Accounts ONTARIO MINISTRY OF FINANCE Table of Contents ECONOMIC ACCOUNTS Highlights 1 Ontario s Economy Continues to Grow Expenditure Details 2

Economic Projections for

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

Nepal Rastra Bank. Research Department. Current Macroeconomic and Financial Situation of Nepal. (Based on Eleven Months' Data of 2016/17)

") Nepal Rastra Bank Research Department Current Macroeconomic and Financial Situation of Nepal Macrofinancial Outlook (Based on Eleven Months' Data of 2016/17) 1. Developments in four areas relating to weather,

Nepal Rastra Bank Research Department Current Macroeconomic and Financial Situation of Nepal Macrofinancial Outlook (Based on Eleven Months' Data of 2016/17) 1. Developments in four areas relating to weather,

Svein Gjedrem: The outlook for the Norwegian economy

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

RBI Q1 FY11 Monetary Policy Review

RBI Q1 FY11 Monetary Policy Review The Policy Measures In Brief In its First Quarter Review of the Annual Monetary Policy for 2010-11, the Reserve Bank of India increased its policy rates with immediate

RBI Q1 FY11 Monetary Policy Review The Policy Measures In Brief In its First Quarter Review of the Annual Monetary Policy for 2010-11, the Reserve Bank of India increased its policy rates with immediate

18. Real gross domestic product

18. Real gross domestic product 6 Percentage change from quarter to quarter 4 2-2 6 4 2-2 1997 1998 1999 2 21 22 Total Non-agricultural sectors Seasonally adjusted and annualised rates South Africa s real

18. Real gross domestic product 6 Percentage change from quarter to quarter 4 2-2 6 4 2-2 1997 1998 1999 2 21 22 Total Non-agricultural sectors Seasonally adjusted and annualised rates South Africa s real

Monthly Report of Prospects for Japan's Economy

Monthly Report of Prospects for Japan's Economy March 15 Macro Economic Research Centre Economics Department http://www.jri.co.jp/english/periodical/ This report is the revised English version of the February

Monthly Report of Prospects for Japan's Economy March 15 Macro Economic Research Centre Economics Department http://www.jri.co.jp/english/periodical/ This report is the revised English version of the February

India and the Global Crisis

India and the Global Crisis by Shankar Acharya * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India, 1993-2001) 1 India's GDP growth since 1991/92 12 10 8 6 4 2 0 percent

India and the Global Crisis by Shankar Acharya * Honorary Professor, ICRIER (former Chief Economic Adviser to the Government of India, 1993-2001) 1 India's GDP growth since 1991/92 12 10 8 6 4 2 0 percent

LKP SECURITIES LIMITED 13th Floor Raheja Center, Free Press Marg, Nariman Point, Mumbai

Free Press Marg, Nariman Point, Mumbai-400021 Item Open High Low Close % Cng Net Cng Trend Market Update Gold $ Silver $ LME Alum. LME Copper LME Lead LME Nickel LME Zinc Crude $ Nat. Gas $ Precious Metals

Free Press Marg, Nariman Point, Mumbai-400021 Item Open High Low Close % Cng Net Cng Trend Market Update Gold $ Silver $ LME Alum. LME Copper LME Lead LME Nickel LME Zinc Crude $ Nat. Gas $ Precious Metals

Saudi Economic Chartbook

Saudi Economic Chartbook Third Quarter 218 Hans-Peter Huber, PhD Chief Investment Officer Riyad Capital 6775 Takhassusi St. Olaya Riyadh 12331-3712 rcciooffice@riyadcapital.com Third Quarter 218 Oil and

Saudi Economic Chartbook Third Quarter 218 Hans-Peter Huber, PhD Chief Investment Officer Riyad Capital 6775 Takhassusi St. Olaya Riyadh 12331-3712 rcciooffice@riyadcapital.com Third Quarter 218 Oil and

Questions may be referred to Ms. Fichera, APD (ext ).

.") To: Members of the Executive Board April 22, 2005 From: The Secretary Subject: Timor-Leste Statement by the IMF Staff Representative at the Donors Meeting Attached for the information of the Executive

To: Members of the Executive Board April 22, 2005 From: The Secretary Subject: Timor-Leste Statement by the IMF Staff Representative at the Donors Meeting Attached for the information of the Executive

European Capital Markets Institute

ECMI Commentary No. 7 31 May 26 Iceland: Big lessons from a small country? By Charles Gottlieb 1 Global monetary policy is tightening. Following Japan s return to an inflationary environment, liquidity

ECMI Commentary No. 7 31 May 26 Iceland: Big lessons from a small country? By Charles Gottlieb 1 Global monetary policy is tightening. Following Japan s return to an inflationary environment, liquidity

Grant Spencer: Trends in the New Zealand housing market

Grant Spencer: Trends in the New Zealand housing market Speech by Mr Grant Spencer, Deputy Governor and Head of Financial Stability of the Reserve Bank of New Zealand, to the Property Council of New Zealand,

Grant Spencer: Trends in the New Zealand housing market Speech by Mr Grant Spencer, Deputy Governor and Head of Financial Stability of the Reserve Bank of New Zealand, to the Property Council of New Zealand,

Guatemala. 1. General trends. 2. Economic policy. In 2009, the Guatemalan economy faced serious challenges as attempts were made to mitigate

Economic Survey of Latin America and the Caribbean 2009-2010 161 Guatemala 1. General trends In 2009, the Guatemalan economy faced serious challenges as attempts were made to mitigate the impact of the

Economic Survey of Latin America and the Caribbean 2009-2010 161 Guatemala 1. General trends In 2009, the Guatemalan economy faced serious challenges as attempts were made to mitigate the impact of the

Economy Report - Malaysia

Economy Report - Malaysia (Extracted from 2001 Economic Outlook) REAL GROSS DOMESTIC PRODUCT Economic activity in Malaysia expanded strongly in 2000 under the stimulus of strong export growth as well as

Economy Report - Malaysia (Extracted from 2001 Economic Outlook) REAL GROSS DOMESTIC PRODUCT Economic activity in Malaysia expanded strongly in 2000 under the stimulus of strong export growth as well as

Economic Projections :1

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

World trade rises 5.3% in Q1 2010

June 2010 TABLE OF CONTENTS World trade rises 5.3% in Q1 2010 1 Highlights 2 The Canadian economy 2 The U.S. economy 3 Oil prices tumble after US jobs report 4 Flight to quality hits Canadian dollar 4

June 2010 TABLE OF CONTENTS World trade rises 5.3% in Q1 2010 1 Highlights 2 The Canadian economy 2 The U.S. economy 3 Oil prices tumble after US jobs report 4 Flight to quality hits Canadian dollar 4

MONTHLY REPORT. USDINR Gone By. 31 st March 2017

USDINR Gone By 31 st March 2017 March remained the month of gains for the Indian currency, which surged to a 17-month high of 64.7900 levels. The huge win for the Prime Minister Narendra Modi-led Bharatiya

USDINR Gone By 31 st March 2017 March remained the month of gains for the Indian currency, which surged to a 17-month high of 64.7900 levels. The huge win for the Prime Minister Narendra Modi-led Bharatiya

Equity Update December 2018

Market Overview (as on November 30, 2018) Flows Nov-18 Oct-18 Sep-18 FIIs (Net Purchases / Sales) (Rs cr) MFs (Net Purchases / Sales) (Rs cr) Domestic Markets Macro Indicators GDP (YoY%) IIP (YoY%) Crude

Market Overview (as on November 30, 2018) Flows Nov-18 Oct-18 Sep-18 FIIs (Net Purchases / Sales) (Rs cr) MFs (Net Purchases / Sales) (Rs cr) Domestic Markets Macro Indicators GDP (YoY%) IIP (YoY%) Crude

JAPANESE ECONOMY Mixed scenarios regarding corporate earnings... 1

JAPANESE ECONOMY Mixed scenarios regarding corporate earnings... 1 US ECONOMY The U.S. economy remains steady.... 3 Second quarter current account deficits fell to $19.7 billion.... 3 EUROPEAN ECONOMY

JAPANESE ECONOMY Mixed scenarios regarding corporate earnings... 1 US ECONOMY The U.S. economy remains steady.... 3 Second quarter current account deficits fell to $19.7 billion.... 3 EUROPEAN ECONOMY

Taiwan chart book Policy remains neutral

Economics Taiwan chart book Policy remains neutral Group Research October 18 Ma Tieying Economist Please direct distribution queries to Violet Lee +6 687881 violetleeyh@dbs.com Charts of the month Export

Economics Taiwan chart book Policy remains neutral Group Research October 18 Ma Tieying Economist Please direct distribution queries to Violet Lee +6 687881 violetleeyh@dbs.com Charts of the month Export