Minsky, Financial Governance, Banking, and Financial Instability in Brazil

|

|

|

- Patience Mills

- 6 years ago

- Views:

Transcription

1 Minsky, Financial Governance, Banking, and Financial Instability in Brazil FELIPE REZENDE, PH.D., R e s e a r c h S c h o l a r, NY, USA R e m a r k s P r e p a r e d F o r T h e C o n f e r e n c e : F i n a n c i a l G o v e r n a n c e A f t e r T h e C r i s i s c o s p o n s o r e d B y T h e L e v y E c o n o m i c s I n s t i t u t e O f B a r d C o l l e g e A n d M I N D S M u l t i d i s c i p l i n a r y I n s t i t u t e F o r D e v e l o p m e n t A n d S t r a t e g i e s, W i t h S u p p o r t F r o m T h e F o r d F o u n d a t i o n E v e r e s t R i o H o t e l R i o D e J a n e i r o, B r a z i l S e p t e m b e r ,

2 MINDS The conference in Rio de Janeiro also represents the beginning of a multi-year grant awarded by the Ford Foundation to MINDS to conduct research on two intertwined projects Financial Governance, Banking, and Financial Instability in Brazil: Analysis and Policy Recommendations Financing Innovation and Development: The Role of Public Banks and Non-Banking Public Institutions. The Cases of Brazil, India and China.

3 Outline Regulatory and supervisory framework failure in AEs Minsky s alternative approach Instability Theory Banking and Financial Regulation Evolution of financial systems New Development strategy

4 Where Do We Stand?

5 Brazil: A Bubble Economy Kregel (2009) characterized the evolution of developing countries in the New Millennium as a bubble, for if the US economy was experiencing a financial bubble the counterpart of that bubble was the extremely beneficial conditions in developing countries and in particular in Latin American emerging markets we cannot foresee a return to the extremely positive conditions experience by developing countries in the recent past.

6 virtually all of the positive performance that led to achieving the Brazilian dream of meeting the target of the BRICs appear to be linked to a financial model and financial flows that is not likely to be reestablished. The degree of leverage that had become normal in developed country financial institutions will not return, the leverage generated by financial derivatives will now be couched in much stronger margin requirements. This will not only mean lower asset prices but lower global demand for emerging market exports and thus reduced financial flows to emerging markets including the BRICs there is general similarity across all BRIC economies for they all depend on expanding demand through increasing global trade and global imbalance financed by global financial flows.

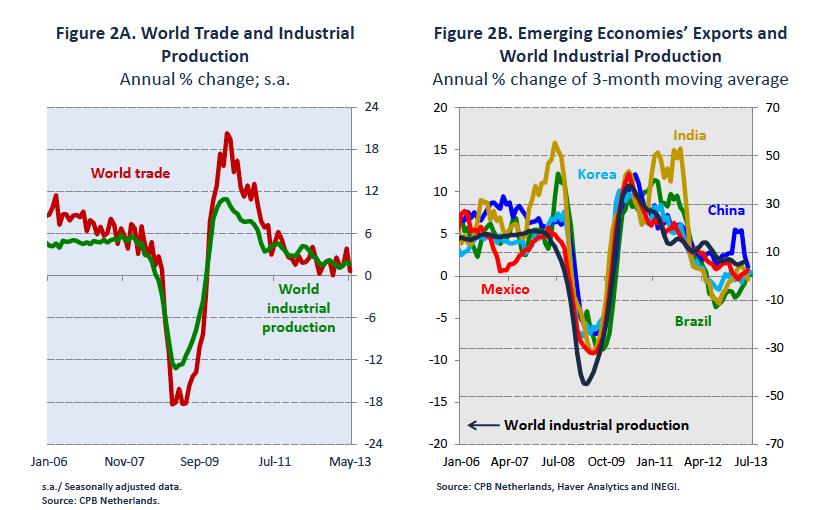

7 Unsustainable global demand and financing patterns Prior to the Great Recession, exports from developing and transition economies grew rapidly owing to buoyant consumer demand in the developed countries, mainly the United States. This seemed to justify the adoption of an export-oriented growth model. But the expansion of the world economy, though favourable for many developing countries, was built on unsustainable global demand and financing patterns. Thus, reverting to pre-crisis growth strategies cannot be an option. Rather, in order to adjust to what now appears to be a structural shift in the world economy, many developing and transition economies are obliged to review their development strategies that have been overly dependent on exports for growth. UNCTAD, Trade and Development Report, 2013, p.1-2

8 A New Global Structure Global trade growth grounding to a halt Demand supported by credit growth in EMEs

9

10

11

12 Minsky Instability Theory Periods of growth and tranquility validates expectations and existing financial structures, which change the dynamics of human behavior leading to endogenous instability, increasing risk appetite, mispricing of risky positions, and the erosion of margins of safety and liquid positions Kregel-Minsky model Provision of liquidity Macro condition Micro condition

13

14 Lifted the external constraint

15 Policy Rate Selic

16 Bank Credit % of GDP

17 Bank claims on the private sector, selected countries, (Per cent of GDP)

18

19 Macroeconomic and microeconomic aspects to financial fragility Core of Minsky s financial instability: Assets purchased through the issuance of debt. Kregel 2009: At the macro level: government deficits create cash. At the micro level: sources of cash flows and cash flow sensitivity, reliance on position making operations to raise cash. Banks, Business firms, and households are short cash. Cash to cover short position

20 Public Sector Net Debt

21 Public Debt Interest Payments

22 Principles of macro accounting one sector s surplus equals the other sector s deficit. Domestic Private Balance + Domestic Government Balance + Foreign Balance = 0 Domestic Private Balance = government deficit + Current Account Balance

23 Valor a preços correntes ( R$) Brazil: Financial Balances Currency issuer and Currency users (-) (-) (-) (-) Non-government financial balance Government sector balance

24 Financial Balances % of GDP (sign reversed for GSB and ESB) 8% 6% 4% 2% 0% % -4% -6% Government sector balance sign reversed External sector balance Domestic nongovernment sector balance

25 nov/02 abr/03 set/03 fev/04 jul/04 dez/04 mai/05 out/05 mar/06 ago/06 jan/07 jun/07 nov/07 abr/08 set/08 fev/09 jul/09 dez/09 mai/10 out/10 mar/11 ago/11 jan/12 jun/12 nov/12 abr/13 % GDP 8 Sectorial Financial Balances Financial Balances % GDP 12-month rolling sum Government balance External Balance Private sector balance

26 Brazilian Sectorial Financial Balances average average Financial balances as % of GDP Nonfinancial corporations -1% -2% -1% 2% 2% 1% 1% -1% -2% 0% 0.04% -1.11% Financial institutions 1% 3% 4% 2% 2% 3% 4% 5% 3% 3% 3.06% 2.80% Public Sector -5% -7% -6% -5% -3% -3% -5% -5% -3% -5% -4.76% -3.73% Households 1% 1% 1% 1% 1% 0% 0% 0% 0% 0% 0.84% 0.18% Rest of the World 4% 5% 1% 0% -1% -1% -1% 0% 2% 2% 0.82% 1.86%

27 Decomposition of Credit and household indebtedness

28 jan/05 jul/05 jan/06 jul/06 jan/07 jul/07 jan/08 jul/08 jan/09 jul/09 jan/10 jul/10 jan/11 jul/11 jan/12 jul/12 jan/13 50 Household Debt outstanding and debt service ratio Household debt service ratio - Seasonally adjusted data - % Household debt - % Household debt service ratio without mortgage loans - Seasonally adjusted data - % Household debt without mortgage loans - % 5 0

29 jan/05 abr/05 jul/05 out/05 jan/06 abr/06 jul/06 out/06 jan/07 abr/07 jul/07 out/07 jan/08 abr/08 jul/08 out/08 jan/09 abr/09 jul/09 out/09 jan/10 abr/10 jul/10 out/10 jan/11 abr/11 jul/11 out/11 jan/12 abr/12 jul/12 out/12 jan/13 abr/13 Household Debt Service Ratio Household debt service ratio - Principal - Seasonally adjusted data - % Household debt service ratio - Interest - Seasonally adjusted data - % Household debt service ratio - Seasonally adjusted data - %

30 jan/05 Household debt service ratio Principal and Interest (Jan 2005 = 100) mai/05 set/05 jan/06 mai/06 set/06 jan/07 mai/07 set/07 jan/08 mai/08 set/08 jan/09 mai/09 set/09 jan/10 mai/10 set/10 jan/11 mai/11 set/11 jan/12 mai/12 set/12 jan/13 mai/ Household debt service ratio - Principal (Jan 2005 = 100) Household debt service ratio - Interest (Jan 2005 = 100)

31 Minsky, Financial Governance, Banking, and Financial Instability in Brazil FELIPE REZENDE, PH.D., R e s e a r c h S c h o l a r, NY, USA R e m a r k s P r e p a r e d F o r T h e C o n f e r e n c e : F i n a n c i a l G o v e r n a n c e A f t e r T h e C r i s i s c o s p o n s o r e d B y T h e L e v y E c o n o m i c s I n s t i t u t e O f B a r d C o l l e g e A n d M I N D S M u l t i d i s c i p l i n a r y I n s t i t u t e F o r D e v e l o p m e n t A n d S t r a t e g i e s, W i t h S u p p o r t F r o m T h e F o r d F o u n d a t i o n E v e r e s t R i o H o t e l R i o D e J a n e i r o, B r a z i l S e p t e m b e r ,

32 MINDS The conference in Rio de Janeiro also represents the beginning of a multi-year grant awarded by the Ford Foundation to MINDS to conduct research on two intertwined projects Financial Governance, Banking, and Financial Instability in Brazil: Analysis and Policy Recommendations Financing Innovation and Development: The Role of Public Banks and Non-Banking Public Institutions. The Cases of Brazil, India and China.

33 Outline Regulatory and supervisory framework failure in AEs Minsky s alternative approach Instability Theory Banking and Financial Regulation Evolution of financial systems New Development strategy

34 Minsky s view of banking Buy assets by issuing liabilities. Endogenous money creation Growth of private endogenous liquidity during booms. Minsky: Banking is not money lending; to lend, a money lender must have money. The fundamental banking activity is accepting, that is, guaranteeing that some party is creditworthy. (1986)

35 Banks treasury security holdings and the Selic Rate % Nov-02 Mar-03 Jul-03 Nov-03 Mar-04 Jul-04 Nov-04 Mar-05 Jul-05 Nov-05 Mar-06 Jul-06 Nov-06 Mar-07 Jul-07 Nov-07 Mar-08 Jul-08 Nov-08 Mar-09 Jul-09 Nov-09 Mar-10 Jul-10 Nov-10 Mar-11 Jul-11 Nov-11 Mar % % % % % % % % Average interest rate on Net Domestic Public Debt (LHS) Treasury Securities holdings as a share of Deposit money banks assets (RHS)

36 jan/02 mai/02 set/02 jan/03 mai/03 set/03 jan/04 mai/04 set/04 jan/05 mai/05 set/05 jan/06 mai/06 set/06 jan/07 mai/07 set/07 jan/08 mai/08 set/08 jan/09 mai/09 set/09 jan/10 mai/10 set/10 jan/11 mai/11 set/11 jan/12 mai/12 40% Changes in the banks asset composition Deposit money banks asset composition 65% 35% 30% 60% 25% 55% 20% 15% 50% 10% 5% 45% 0% 40% Treasury securities Reserves Foreign Assets Claim on the private sector (RHS)

37 Balance of Credit Operations by capital origin of banking institutions US$ million

38 Housing Finance System (SFH) Under this system, the minimum lending requirement to housing loans is equal to 65% of savings deposits held at banks. Outstanding mortgage debt has almost twentyfold since However, it was widely believed that the growth of savings deposits would be below mortgage lending demand growth. The conventional argument of the advocates of the development of the securitization market is that savings deposits will be insufficient to meet the growing demand for mortgage loans in Brazil, the argument is that mortgage lending loans outstanding will exceed 65% of savings deposits

39 Liquidity Creation The creation of new sources of financing and funding are at the center of discussions to promote real capital development in the Brazil. It has been suggested that access to capital markets and longterm investors are a possible solution to the dilemma faced by Brazil s increasing financing requirements. The Brazilian response to the funding shortfall included policy initiatives to revive Brazil s capital market funding.

40 Breaking banks monopoly on Liquidity creation Regulatory reforms implemented in the late 1990s and during the 2000s have laid the foundation for the development of the securitization market and allowed the creation of new alternatives of liquidity creation. The development of the Sistema Financeiro Imobiliario (SFI), established in 1997, would presumably provide the funding necessary for the expansion of the housing market and the corresponding reduction of the housing gap in Brazil. The strategy adopted with recent regulatory reforms emphasized loan origination growth by lending institutions and the sale of asset pools to securitization structures (such as receivable investment funds and securitization companies) thus reducing banks on balance sheet asset liability mismatches and capital requirements. This policy initiative has been driven by the belief that access to capital markets would provide the funding necessary for the expansion of the housing market and the corresponding reduction of the housing gap in Brazil

41 Breaking banks monopoly on Liquidity creation The number of structured finance deals and securitization structures sharply increased in the past decade as a series of reforms were introduced to foster the growth of the securitization market in the country. Despite the original intent of regulatory reforms in the context of SFI to develop the mortgage lending market, asset-backed securities (ABS) backed by personal loans, auto loans, receivables future flows took off and are common ABS transactions. Since the creation of Receivable investment funds in 2001, or Fundos de Investimento em Direitos Creditórios (FIDCs), the range of underlying assets backing securitization deals has broadened including (but not limited to) consumer loans, auto loans, future flow receivables, and non-performing loan portfolios) and originators typical include banks, finance companies, companies (small, medium, and large), and governments.

42 Lack of Savings and financing mechanisms or shortterm portfolio preferences?

43 IMF 2012: Brazil is still stuck in a high interest ratelow duration equilibrium

44 jun/02 fev/03 out/03 jun/04 fev/05 out/05 jun/06 fev/07 out/07 jun/08 fev/09 out/09 jun/10 fev/11 out/11 % 35,00 Loan Portfolio Yield and funding costs 30,00 25,00 20,00 15,00 10,00 Loan Portfolio Yield Funding cost Average spread Average Policy Rate- Selic 5,00 -

45

46 Brazilian Bank s return on equity

47 Capital and Leverage Ratio

48 Financing Long Term Assets Roberto Setubal, chief executive of Itaú Unibanco, points out that [Mortgage funding] will need to be developed in Brazil, but in a different way. We will not be financing long-term assets with short-term deposits in the way it was done elsewhere in the world Since we are facing this liquidity perspective, and let s assume mortgages will grow at 40% a year because today they are less than 5% of the total portfolio, and let s also take account of Basel III liquidity requirements, [then] it s obvious we cannot use savings or demand deposits to close this gap. That s why there is a big discussion in Brazil about what would be the right funding for mortgages Given the high level of interest rates this is a problem and this is why Brazil has never developed this before. A lot of current proposals, such as covered bonds, will help but if we don t have single-digit interest rates it will not happen (Caplen 2011)

49 Banks Maturity Mismatch

50

51 Liability Structure of Brazilian Banks

52 How to characterize financial systems? The important question is related to the costs of carrying a mismatch between the duration of assets and liabilities on the bank balance sheet, that is, if interest and funding risks are carried on banks balance sheets. Following Kregel (1993), rather than characterizing financial systems as market based or bank based, one should distinguish between the risks that are carried on the balance sheets of banks and other financial institutions

53 Banks capital and liquidity ratios

54 Portfolio preferences

55 Interest Risk Exposure During the second quarter of 2013 the top three private banks Itau Unibanco, Bradesco, and Santanderexperienced massive losses, about R$ 11,7 billion, due to a negative adjustment to the market value in their portfolio of securities classified as available for sale caused by changes in the yield curve. It is, thus, a high and volatile interest rate environment, due to active manipulations of the central bank s policy rate, known as Selic rate, that has shifted portfolio preferences towards low duration, short-term assets

56 Mutual Funds

57

58 Thank you

59 Investment as % of GDP

60 More aggressive increase in treasury investment as % of GDP

61 A New Perspective on the role of the Public sector to Support a National Development Agenda It is not a new insight that growth strategies that rely primarily on exports must sooner or later reach their limits when many countries pursue them simultaneously: competition among economies based on low unit labour costs and taxes leads to a race to the bottom, with few development gains but potentially disastrous social consequences. At the present juncture, where growth of demand from developed countries is expected to remain weak for a protracted period of time, the limitations of such a growth strategy are becoming even more obvious. Therefore, a rebalancing of the drivers of growth, with greater weight given to domestic demand, is indispensable. This will be a formidable challenge for all developing countries, though more difficult for some than for others. In any case, it will require a new perspective on the role of wages and the public sector in the development process. Distinct from export-led growth, development strategies that give a greater role than in the past to domestic demand for growth can be pursued by all countries simultaneously without beggar-thy-neighbour effects, and without counterproductive wage and tax competition. Moreover, if many trade partners in the developing world manage to expand their domestic demand simultaneously, they can spur South-South trade. UNCTAD, Trade and Development Report, 2013, p.3

62 Elements of a National Development Agenda No need to rely on external savings, shift to domestic demand led growth, support domestic income growth and domestic consumption via fiscal policy, Increase government supported infrastructure investment projects, enhancing automatic stabilizers, job guarantee program. fostering the purchasing power of the population in general, and of wage earners in particular, should be the main ingredient of a domestic-demanddriven growth strategy. While export-led strategies focus on the cost aspect of wages, a domestic-demand-oriented strategy would focus primarily on the income aspect of wages, as it is based on household spending as the largest component of effective demand. if wage growth follows the path of productivity growth, it will create a sufficient amount of domestic demand to fully employ the growing productive capacities of the economy targeted social transfers and public sector employment schemes can play an important complementary role. (UNCTAD, Trade and Development Report, 2013, p. VII-IX)

P R O J E T A THE ECONOMIST

SCENARIOS OF THE BRAZILIAN ECONOMY Carlos Geraldo Langoni PricewaterhouseCoopers September / 2010 THE ECONOMIST STRUCTURAL CHANGES WORLD LEVEL: MULTIPOLARITY; DOMESTICALLY: MACRO CONSENSUS. MULTIPOLAR

SCENARIOS OF THE BRAZILIAN ECONOMY Carlos Geraldo Langoni PricewaterhouseCoopers September / 2010 THE ECONOMIST STRUCTURAL CHANGES WORLD LEVEL: MULTIPOLARITY; DOMESTICALLY: MACRO CONSENSUS. MULTIPOLAR

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

The Economic Consequences of the Real. Economic Department

The Economic Consequences of the Real Economic Department I/2002 III/2008 IV/2008 IV/2009 I/2010 IV/2013 I/2014 II/2016 The great recession: A Four Act Drama. GDP (YoY accumulated) Source: IBGE 8,00% 6,00%

The Economic Consequences of the Real Economic Department I/2002 III/2008 IV/2008 IV/2009 I/2010 IV/2013 I/2014 II/2016 The great recession: A Four Act Drama. GDP (YoY accumulated) Source: IBGE 8,00% 6,00%

DISCUSSION PAPER NO 1 TEXTO PARA DISCUSSÃO NO 1 FINANCIAL FRAGILITY, INSTABILITY AND THE BRAZILIAN CRISIS: A KEYNES-MINSKY-GODLEY APPROACH

DISCUSSION PAPER NO 1 TEXTO PARA DISCUSSÃO NO 1 FINANCIAL FRAGILITY, INSTABILITY AND THE BRAZILIAN CRISIS: A KEYNES-MINSKY-GODLEY APPROACH FRAGILIDADE FINANCEIRA, INSTABILIDADE E A CRISE BRASILEIRA: UMA

DISCUSSION PAPER NO 1 TEXTO PARA DISCUSSÃO NO 1 FINANCIAL FRAGILITY, INSTABILITY AND THE BRAZILIAN CRISIS: A KEYNES-MINSKY-GODLEY APPROACH FRAGILIDADE FINANCEIRA, INSTABILIDADE E A CRISE BRASILEIRA: UMA

Sixtieth session of the Trade and Development Board September Items 4 and 8: Interdependence and Development Strategies

Sixtieth session of the Trade and Development Board 16 27 September 2013 Items 4 and 8: Interdependence and Development Strategies Mr. President, Distinguished Panellists, Excellencies, Ladies and Gentlemen,

Sixtieth session of the Trade and Development Board 16 27 September 2013 Items 4 and 8: Interdependence and Development Strategies Mr. President, Distinguished Panellists, Excellencies, Ladies and Gentlemen,

TRADE AND DEVELOPMENT REPORT, 2013

United Nations Conference on Trade And Development TRADE AND DEVELOPMENT REPORT, 2013 OVERVIEW EMBARGO The contents of this Report must not be quoted or summarized in the print, broadcast or electronic

United Nations Conference on Trade And Development TRADE AND DEVELOPMENT REPORT, 2013 OVERVIEW EMBARGO The contents of this Report must not be quoted or summarized in the print, broadcast or electronic

What is the global economic outlook?

The outlook What is the global economic outlook? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent United States.... Euro area. -. -.. Japan -.... Total OECD....

The outlook What is the global economic outlook? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent United States.... Euro area. -. -.. Japan -.... Total OECD....

Portugal Q Portugal. Lisbon, April 26th 2012

Q1 2012 Lisbon, April 26th 2012 Disclaimer 2 Banco Santander, S.A. ("Santander") cautions that this presentation contains forward-looking statements within the meaning of the US Private Securities Litigation

Q1 2012 Lisbon, April 26th 2012 Disclaimer 2 Banco Santander, S.A. ("Santander") cautions that this presentation contains forward-looking statements within the meaning of the US Private Securities Litigation

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, Barry Bosworth

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

Securitisation: Benefits for Emerging Markets and Lessons from the Global Financial Crisis

Securitisation: Benefits for Emerging Markets and Lessons from the Global Financial Crisis SEC Securities Markets Workshop Washington DC May 1, 2009 1 Securitisation: Benefits for Emerging Markets Investors

Securitisation: Benefits for Emerging Markets and Lessons from the Global Financial Crisis SEC Securities Markets Workshop Washington DC May 1, 2009 1 Securitisation: Benefits for Emerging Markets Investors

Russia: Macro Outlook for 2019

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

Sovereign Credit Outlook. Richard Francis Director, Latin America Sovereigns Corficolombiana Conference December 5, 2018

Sovereign Credit Outlook Richard Francis Director, Latin America Sovereigns Corficolombiana Conference December 5, 218 Agenda Global Perspective Regional Overview Sovereign Ratings and Recent Actions Colombia

Sovereign Credit Outlook Richard Francis Director, Latin America Sovereigns Corficolombiana Conference December 5, 218 Agenda Global Perspective Regional Overview Sovereign Ratings and Recent Actions Colombia

Exchange Rate, Inflation, Growth and Development in Brazil

Exchange Rate, Inflation, Growth and Development in Brazil Nelson Barbosa Presented at the Conference Financial Governance After the Crisis Cosponsored by the Levy Economics Institute of Bard College and

Exchange Rate, Inflation, Growth and Development in Brazil Nelson Barbosa Presented at the Conference Financial Governance After the Crisis Cosponsored by the Levy Economics Institute of Bard College and

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Country Risk Analytics

Emerging Markets Country Risk Analytics MacroFinance Research Quarterly - 2018 Q2 www.taceconomics.com www.taceconomics.com 2 Country Risk Analytics EM Quarterly MacroFinance Research 2018 Q2 Description

Emerging Markets Country Risk Analytics MacroFinance Research Quarterly - 2018 Q2 www.taceconomics.com www.taceconomics.com 2 Country Risk Analytics EM Quarterly MacroFinance Research 2018 Q2 Description

Globalization. International Financial (Chap. 8) and Monetary (Chap. 9) Relations

and Monetary (Chap. 9) Relations") Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

MANAGING CAPITAL FLOWS

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

Rodrigo Orair International Policy Centre for Inclusive Growth (IPC-IG) Institute for Applied Economic Research (IPEA), Brazil

Institute for Applied Economic Research (IPEA), Brazil") SASPEN and FES International Conference Sustainability of Social Protection in the SADC: Economic Returns, Political Will and Fiscal Space 21 Oct 2015 How Brazil has cut its Inequality through Fiscal Policy:

SASPEN and FES International Conference Sustainability of Social Protection in the SADC: Economic Returns, Political Will and Fiscal Space 21 Oct 2015 How Brazil has cut its Inequality through Fiscal Policy:

Global Financial Crisis and China s Countermeasures

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

The Economic Consequences of the Real. Economic Department

The Economic Consequences of the Real Economic Department I/2002 III/2008 IV/2008 IV/2009 I/2010 IV/2013 I/2014 II/2016 The great recession: A Four Act Drama. GDP (YoY accumulated) Source: IBGE 8,00% 6,00%

The Economic Consequences of the Real Economic Department I/2002 III/2008 IV/2008 IV/2009 I/2010 IV/2013 I/2014 II/2016 The great recession: A Four Act Drama. GDP (YoY accumulated) Source: IBGE 8,00% 6,00%

External Factors, Macro Policies and Growth in LAC: Is Performance that Good?

External Factors, Macro Policies and Growth in LAC: Is Performance that Good? Alejandro Izquierdo IADB Emerging Powers in Global Governance Conference Paris, July 6, 2007 (based on work with Ernesto Talvi)

External Factors, Macro Policies and Growth in LAC: Is Performance that Good? Alejandro Izquierdo IADB Emerging Powers in Global Governance Conference Paris, July 6, 2007 (based on work with Ernesto Talvi)

Economic Policy in the Crisis. Lars Calmfors Jönköping International Business School, 2 November 2009

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Notes on the monetary transmission mechanism in the Czech economy

Notes on the monetary transmission mechanism in the Czech economy Luděk Niedermayer 1 This paper discusses several empirical aspects of the monetary transmission mechanism in the Czech economy. The introduction

Notes on the monetary transmission mechanism in the Czech economy Luděk Niedermayer 1 This paper discusses several empirical aspects of the monetary transmission mechanism in the Czech economy. The introduction

Y qué está pasando en Brasil?

Y qué está pasando en Brasil? Ilan Goldfajn Chief Economist and Partner, Itaú Unibanco August, 2013 Summary Why has the Brazilian economy decelerated? The low growth and full employment paradox (new middle

Y qué está pasando en Brasil? Ilan Goldfajn Chief Economist and Partner, Itaú Unibanco August, 2013 Summary Why has the Brazilian economy decelerated? The low growth and full employment paradox (new middle

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

Notes on Hyman Minsky s Financial Instability Hypothesis

FINANCIAL INSTABILITY Prof. Pavlina R. Tcherneva Econ 331/WS 2006 Notes on Hyman Minsky s Financial Instability Hypothesis Summary Prior to WWII, economies were described by frequent and severe depressions

FINANCIAL INSTABILITY Prof. Pavlina R. Tcherneva Econ 331/WS 2006 Notes on Hyman Minsky s Financial Instability Hypothesis Summary Prior to WWII, economies were described by frequent and severe depressions

UNCTAD s Seventh Debt Management Conference. Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective

UNCTAD s Seventh Debt Management Conference 9-11 November 2009 Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective by Mr. Udaibir S. Das Monetary and Capital

UNCTAD s Seventh Debt Management Conference 9-11 November 2009 Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective by Mr. Udaibir S. Das Monetary and Capital

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EUROPEAN COMMISSION Brussels, 9.4.2018 COM(2018) 172 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on Effects of Regulation (EU) 575/2013 and Directive 2013/36/EU on the Economic

EUROPEAN COMMISSION Brussels, 9.4.2018 COM(2018) 172 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on Effects of Regulation (EU) 575/2013 and Directive 2013/36/EU on the Economic

Stylized Financial System

Procyclicality and Capital Flows: Emerging Market Perspective Hyun Song Shin Bank of Thailand International Symposium 2010: Challenges to Central Banks in the Era of the New Globalization October 14 15,

Procyclicality and Capital Flows: Emerging Market Perspective Hyun Song Shin Bank of Thailand International Symposium 2010: Challenges to Central Banks in the Era of the New Globalization October 14 15,

VANDERBILT AVENUE ASSET MANAGEMENT. The Market Impact of the Proposed U.S. Treasury Debt Buyback

The Market Impact of the Proposed U.S. Treasury Debt Buyback Much has been written lately about the government s announced plans to repurchase debt and reduce or eliminate the federal deficit by the second

The Market Impact of the Proposed U.S. Treasury Debt Buyback Much has been written lately about the government s announced plans to repurchase debt and reduce or eliminate the federal deficit by the second

AUSTRALIA S STRESS TESTING EXPERIENCE. Introduction

AUSTRALIA S STRESS TESTING EXPERIENCE Introduction In early 26, the International Monetary Fund (IMF) concluded an assessment of Australia s financial system under the auspices of the Financial Sector

AUSTRALIA S STRESS TESTING EXPERIENCE Introduction In early 26, the International Monetary Fund (IMF) concluded an assessment of Australia s financial system under the auspices of the Financial Sector

LACEA/LAMES 2007 BRAZIL" 05/10/2007

LACEA/LAMES 2007 Policy Responses to Sudden Stops in BRAZIL" 05/10/2007 Márcio Garcia www.econ.puc-rio/mgarcia Introduction (1/2) Brazil suffered in 2002 a sudden stop. Capital flows fell by some USD 24

LACEA/LAMES 2007 Policy Responses to Sudden Stops in BRAZIL" 05/10/2007 Márcio Garcia www.econ.puc-rio/mgarcia Introduction (1/2) Brazil suffered in 2002 a sudden stop. Capital flows fell by some USD 24

MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS The following discussion contains an analysis of our financial condition and results of operations for the nine months

MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS The following discussion contains an analysis of our financial condition and results of operations for the nine months

Executive Directors welcomed the continued

ANNEX IMF EXECUTIVE BOARD DISCUSSION OF THE OUTLOOK, AUGUST 2006 The following remarks by the Acting Chair were made at the conclusion of the Executive Board s discussion of the World Economic Outlook

ANNEX IMF EXECUTIVE BOARD DISCUSSION OF THE OUTLOOK, AUGUST 2006 The following remarks by the Acting Chair were made at the conclusion of the Executive Board s discussion of the World Economic Outlook

GDP Ranking on the 1st quarter How did Brazil reach such a situation?

GDP Ranking on the 1st quarter 2016 How did Brazil reach such a situation? It is politics, s... The elected President had a bellow 10% approval rate for more than one year The country went out the election

GDP Ranking on the 1st quarter 2016 How did Brazil reach such a situation? It is politics, s... The elected President had a bellow 10% approval rate for more than one year The country went out the election

Balance-Sheet Adjustments and the Global Economy

November 16, 2009 Bank of Japan Balance-Sheet Adjustments and the Global Economy Speech at the Paris EUROPLACE Financial Forum in Tokyo Masaaki Shirakawa Governor of the Bank of Japan Introduction Thank

November 16, 2009 Bank of Japan Balance-Sheet Adjustments and the Global Economy Speech at the Paris EUROPLACE Financial Forum in Tokyo Masaaki Shirakawa Governor of the Bank of Japan Introduction Thank

Economic Outlook. Macro Research Itaú Unibanco

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS. Economics 134 Spring 2018 Professor David Romer LECTURE 19

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS Economics 134 Spring 2018 Professor David Romer LECTURE 19 INCOME INEQUALITY AND MACROECONOMIC BEHAVIOR APRIL 4, 2018 I. OVERVIEW A. Changes in inequality

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS Economics 134 Spring 2018 Professor David Romer LECTURE 19 INCOME INEQUALITY AND MACROECONOMIC BEHAVIOR APRIL 4, 2018 I. OVERVIEW A. Changes in inequality

THE OECD SELECTION. Construction, sales, trade and transport. Economic activity in foreign countries Business and consumer

THE OECD SELECTION Subject Indicator % Brazil % OECD Production, stocks and orders Crude steel production 11.1 7.7 Construction, sales, trade and transport...... 10.9 Labour force...... 1.9 Prices, costs

THE OECD SELECTION Subject Indicator % Brazil % OECD Production, stocks and orders Crude steel production 11.1 7.7 Construction, sales, trade and transport...... 10.9 Labour force...... 1.9 Prices, costs

Rebalancing Toward Sustainable Growth. Thomas M. Hoenig President and Chief Executive Officer Federal Reserve Bank of Kansas City

Rebalancing Toward Sustainable Growth Thomas M. Hoenig President and Chief Executive Officer Federal Reserve Bank of Kansas City The Rotary Club of Des Moines and the Greater Des Moines Partnership Des

Rebalancing Toward Sustainable Growth Thomas M. Hoenig President and Chief Executive Officer Federal Reserve Bank of Kansas City The Rotary Club of Des Moines and the Greater Des Moines Partnership Des

Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

What is Monetary Policy?

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

Banking efficiency, governance and financial regulation in Brazil

Brazilian Journal of Political Economy, vol. 31, nº 5 (125), pp. 867-873, Special edition 2011 Banking efficiency, governance and financial regulation in Brazil Luiz Fernando de Paula* In this short paper

Brazilian Journal of Political Economy, vol. 31, nº 5 (125), pp. 867-873, Special edition 2011 Banking efficiency, governance and financial regulation in Brazil Luiz Fernando de Paula* In this short paper

Macroeconomic Outlook: Implications for Agriculture. It has been 26 years since we have experienced a significant recession

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

PRESENTATION ON Fiscal Policy for Development and Budgetary Implications: Experience in Other Parts of Asia

PRESENTATION ON Fiscal Policy for Development and Budgetary Implications: Experience in Other Parts of Asia By Dr. Ashfaque H. Khan Principal NUST Business School National University of Sciences & Technology,

PRESENTATION ON Fiscal Policy for Development and Budgetary Implications: Experience in Other Parts of Asia By Dr. Ashfaque H. Khan Principal NUST Business School National University of Sciences & Technology,

Normalizing Monetary Policy

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

Panel on Brazilian Economy

Panel on Brazilian Economy International Consultative Council FUNDAÇÃO DOM CABRAL - FDC October 2012 Luciano Coutinho Luciano Coutinho President 1 Uncertainties in the International scenery: Developed

Panel on Brazilian Economy International Consultative Council FUNDAÇÃO DOM CABRAL - FDC October 2012 Luciano Coutinho Luciano Coutinho President 1 Uncertainties in the International scenery: Developed

Economic state of the union, EuroMemo Engelbert Stockhammer Kingston University

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

BRICs: actual growth and cooperation perspectives. International Advisory Council 3 rd Metting August 15, Luciano Coutinho President

BRICs: actual growth and cooperation perspectives International Advisory Council 3 rd Metting August 15, 2011 Luciano Coutinho President Emerging countries remain ahead in worldwide growth Annual Growth

BRICs: actual growth and cooperation perspectives International Advisory Council 3 rd Metting August 15, 2011 Luciano Coutinho President Emerging countries remain ahead in worldwide growth Annual Growth

Macroeconomic Perspectives for Thailand

1 Macroeconomic Perspectives for Thailand Pattama Teanravisitsagool Macroeconomic Strategy and Planning, Director Office of the National Economic and Social Development Board 27 April 2009 WWW.NESDB.GO.TH

1 Macroeconomic Perspectives for Thailand Pattama Teanravisitsagool Macroeconomic Strategy and Planning, Director Office of the National Economic and Social Development Board 27 April 2009 WWW.NESDB.GO.TH

Europe Outlook. Third Quarter 2015

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Monetary Policy: A Key Driver for Long Term Macroeconomic Stability

Monetary Policy: A Key Driver for Long Term Macroeconomic Stability Julio Velarde Governor Central Bank of Peru March 2016 Agenda 1. Peru s growth is based on strong fundamentals 2. Recent economic developments

Monetary Policy: A Key Driver for Long Term Macroeconomic Stability Julio Velarde Governor Central Bank of Peru March 2016 Agenda 1. Peru s growth is based on strong fundamentals 2. Recent economic developments

Economic activity gathers pace

Produced by the Economic Research Unit October 2014 A quarterly analysis of trends in the Irish economy Economic activity gathers pace Positive data flow Recovery broadening out GDP growth revised up to

Produced by the Economic Research Unit October 2014 A quarterly analysis of trends in the Irish economy Economic activity gathers pace Positive data flow Recovery broadening out GDP growth revised up to

CROATIA S EU CONVERGENCE REPORT: REACHING AND SUSTAINING HIGHER RATES OF ECONOMIC GROWTH, Document of the World Bank, June 2009, pp.

CROATIA S EU CONVERGENCE REPORT: REACHING AND SUSTAINING HIGHER RATES OF ECONOMIC GROWTH, Document of the World Bank, June 2009, pp. 208 Review * The causes behind achieving different economic growth rates

CROATIA S EU CONVERGENCE REPORT: REACHING AND SUSTAINING HIGHER RATES OF ECONOMIC GROWTH, Document of the World Bank, June 2009, pp. 208 Review * The causes behind achieving different economic growth rates

II. Underlying domestic macroeconomic imbalances fuelled current account deficits

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

Macro Research Economic outlook

Macro Research Economic outlook Macroeconomic Research Itaú Unibanco April 2017 Roadmap Global Economy The global outlook remains favorable Global growth positive momentum continues, with a synchronized

Macro Research Economic outlook Macroeconomic Research Itaú Unibanco April 2017 Roadmap Global Economy The global outlook remains favorable Global growth positive momentum continues, with a synchronized

financial report 1 st quarter of 2012 Itaú Unibanco Holding S.A. Management Discussion & Analysis and Complete Financial Statements

financial report 1 st quarter of 2012 Itaú Unibanco Holding S.A. Management Discussion & Analysis and Complete Financial Statements Contents Management Discussion & Analysis 3 Executive Summary 3 Analysis

financial report 1 st quarter of 2012 Itaú Unibanco Holding S.A. Management Discussion & Analysis and Complete Financial Statements Contents Management Discussion & Analysis 3 Executive Summary 3 Analysis

Santander s Economic Report

Inicio Santander s Economic Report Research Second quarter 2016 WORLD ECONOMIC OUTLOOK > In US, better prospects for employment and activity, coupled with a rise in inflation, portend an imminent rise

Inicio Santander s Economic Report Research Second quarter 2016 WORLD ECONOMIC OUTLOOK > In US, better prospects for employment and activity, coupled with a rise in inflation, portend an imminent rise

Portuguese Banking System: latest developments. 2 nd quarter 2018

Portuguese Banking System: latest developments 2 nd quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 26 th September of 218. Macroeconomic indicators and banking system data

Portuguese Banking System: latest developments 2 nd quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 26 th September of 218. Macroeconomic indicators and banking system data

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

National Monetary Policy Forum. Chris Loewald, Head: Policy Development and Research 10 April 2016 Pretoria

National Monetary Policy Forum Chris Loewald, Head: Policy Development and Research 1 April 1 Pretoria In the April 17 MPR Executive summary & overview of the policy stance Overview of the world economy

National Monetary Policy Forum Chris Loewald, Head: Policy Development and Research 1 April 1 Pretoria In the April 17 MPR Executive summary & overview of the policy stance Overview of the world economy

The Fertile Soil of Corporate Bond Market

Oct 09 Sep 10 Aug 11 Jul 12 Jun 13 May 14 Oct 09 Apr 10 Oct 10 Apr 11 Oct 11 Apr 12 Oct 12 Apr 13 Oct 13 Apr 14 Basis Points Basis Points PERSPECTIVES The Fertile Soil of Corporate Bond Market May 2014

Oct 09 Sep 10 Aug 11 Jul 12 Jun 13 May 14 Oct 09 Apr 10 Oct 10 Apr 11 Oct 11 Apr 12 Oct 12 Apr 13 Oct 13 Apr 14 Basis Points Basis Points PERSPECTIVES The Fertile Soil of Corporate Bond Market May 2014

Portuguese Banking System: latest developments. 1 st quarter 2018

Portuguese Banking System: latest developments 1 st quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 27 th June of 218. Macroeconomic indicators and banking system data are quarterly

Portuguese Banking System: latest developments 1 st quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 27 th June of 218. Macroeconomic indicators and banking system data are quarterly

HSBC Brazil 2011 update Presentation to Investors

Wednesday 09 November 2011 HSBC Brazil 2011 update Presentation to Investors Conrado Engel Alvaro Azevedo Chief Executive Officer HSBC Brazil Chief Financial Officer HSBC Brazil Forward-looking statements

Wednesday 09 November 2011 HSBC Brazil 2011 update Presentation to Investors Conrado Engel Alvaro Azevedo Chief Executive Officer HSBC Brazil Chief Financial Officer HSBC Brazil Forward-looking statements

Central Banking in Emerging Markets

Central Banking in Emerging Markets International Center for Monetary and Banking Studies () Governor of the Central Bank of Brazil Ilan Goldfajn January 15, 2019 Monetary policy is challenging in Emerging

Central Banking in Emerging Markets International Center for Monetary and Banking Studies () Governor of the Central Bank of Brazil Ilan Goldfajn January 15, 2019 Monetary policy is challenging in Emerging

Banking on Turkey, October 21, 2008

Banking on Turkey, October 21, 2008 Slide 1. Title Slide Good morning. The global economic downturn and financial turmoil mean that economic growth will slow down in Turkey. There will be much slower growth,

Banking on Turkey, October 21, 2008 Slide 1. Title Slide Good morning. The global economic downturn and financial turmoil mean that economic growth will slow down in Turkey. There will be much slower growth,

Greece. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 215 rebalancing recovery Outlook for Delay in agreeing reform agenda has undermined the recovery Published in collaboration with Highlights The immediate economic outlook for continues

EY Forecast June 215 rebalancing recovery Outlook for Delay in agreeing reform agenda has undermined the recovery Published in collaboration with Highlights The immediate economic outlook for continues

Global Economic Outlook John Hawksworth Chief Economist, PwC September 2012

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

Asset Allocation Monthly

For professional investors Asset Allocation Monthly September 2015 Joost van Leenders, CFA Chief Economist, Multi Asset Solutions joost.vanleenders@bnpparibas.com +31 20 527 5126 Growth weakness in emerging

For professional investors Asset Allocation Monthly September 2015 Joost van Leenders, CFA Chief Economist, Multi Asset Solutions joost.vanleenders@bnpparibas.com +31 20 527 5126 Growth weakness in emerging

1- Macroeconomic Scenario

PREVI NOVARTIS MONTHLY REPORT March 17, 2014 1- Macroeconomic Scenario In the global scenario, the highlights are the severe winter which has been affecting negatively the United States economy. In spite

PREVI NOVARTIS MONTHLY REPORT March 17, 2014 1- Macroeconomic Scenario In the global scenario, the highlights are the severe winter which has been affecting negatively the United States economy. In spite

PURSUING SHARED PROSPERITY IN AN ERA OF TURBULENCE AND HIGH COMMODITY PRICES

2012 Key messages Asia-Pacific growth to slow in 2012 amidst global turbulence: Spillovers of the euro zone turmoil Global oil price hikes Excess liquidity and volatile capital flows Key long-term challenge:

2012 Key messages Asia-Pacific growth to slow in 2012 amidst global turbulence: Spillovers of the euro zone turmoil Global oil price hikes Excess liquidity and volatile capital flows Key long-term challenge:

BRAZILIAN HIGH-TECH LITIGATION: Law, Business & Policy

BRAZILIAN HIGH-TECH LITIGATION: Law, Business & Policy Thursday, May 12 Washington, DC Scan to download this presentation or to receive link via e-mail Introduction Susan L. Karamanian Associate Dean B

BRAZILIAN HIGH-TECH LITIGATION: Law, Business & Policy Thursday, May 12 Washington, DC Scan to download this presentation or to receive link via e-mail Introduction Susan L. Karamanian Associate Dean B

China s Economic Growth Model Medium and Long Term Challenges

China s Economic Growth Model Medium and Long Term Challenges Geng XIAO Fung Global Institute www.funglobal institute.org Centre of economic gravity is shifting back to East Asian Century Scenario by Asian

China s Economic Growth Model Medium and Long Term Challenges Geng XIAO Fung Global Institute www.funglobal institute.org Centre of economic gravity is shifting back to East Asian Century Scenario by Asian

Spring Forecast: slowly recovering from a protracted recession

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

2012 Review and Outlook: Plus ça change... BY JASON M. THOMAS

Economic Outlook 2012 Review and Outlook: Plus ça change... September 10, 2012 BY JASON M. THOMAS Over the past several years, central banks have taken unprecedented actions to suppress both short-andlong-term

Economic Outlook 2012 Review and Outlook: Plus ça change... September 10, 2012 BY JASON M. THOMAS Over the past several years, central banks have taken unprecedented actions to suppress both short-andlong-term

AS Economics: ECON2 Economics: The National Economy 2009/10

2 weeks 1 st Sep - 11 th Sep Term 1 Introduction to the objectives and instruments of government This is an introduction to 3.2.3, 3.2.1 macroeconomic policy the Unit and most of the content Candidates

2 weeks 1 st Sep - 11 th Sep Term 1 Introduction to the objectives and instruments of government This is an introduction to 3.2.3, 3.2.1 macroeconomic policy the Unit and most of the content Candidates

The fiscal adjustment after the crisis in Argentina

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

Income Inequality and Labor Market Dynamics in Brazil

Income Inequality and Labor Market Dynamics in Brazil Fernando de Holanda Barbosa Filho IBRE FGV Brazilian Institute of Economics Getulio Vargas Foundation Facts Income inequality declined in Brazil over

Income Inequality and Labor Market Dynamics in Brazil Fernando de Holanda Barbosa Filho IBRE FGV Brazilian Institute of Economics Getulio Vargas Foundation Facts Income inequality declined in Brazil over

The OECD Global Economic Outlook

The OECD Global Economic Outlook Nigel Pain OECD Economics Department Edinburgh, 11 July 2013 NCSL Symposium for Legislative Leaders 1 Overview Presentation structure Current situation and prospects. Global

The OECD Global Economic Outlook Nigel Pain OECD Economics Department Edinburgh, 11 July 2013 NCSL Symposium for Legislative Leaders 1 Overview Presentation structure Current situation and prospects. Global

BBVA Bancomer. Focused on continuing growth

BBVA Bancomer Focused on continuing growth 1 Disclaimer This document is only provided for information purposes and does not constitute, nor must it be interpreted as, an offer to sell or exchange or acquire,

BBVA Bancomer Focused on continuing growth 1 Disclaimer This document is only provided for information purposes and does not constitute, nor must it be interpreted as, an offer to sell or exchange or acquire,

Financial stability risks: old and new

Financial stability risks: old and new Hyun Song Shin* Bank for International Settlements 4 December 2014 Brookings Institution Washington DC *Views expressed here are mine, not necessarily those of the

Financial stability risks: old and new Hyun Song Shin* Bank for International Settlements 4 December 2014 Brookings Institution Washington DC *Views expressed here are mine, not necessarily those of the

Long-term uncertainty and social security systems

Long-term uncertainty and social security systems Jesús Ferreiro and Felipe Serrano University of the Basque Country (Spain) The New Economics as Mainstream Economics Cambridge, January 28 29, 2010 1 Introduction

Long-term uncertainty and social security systems Jesús Ferreiro and Felipe Serrano University of the Basque Country (Spain) The New Economics as Mainstream Economics Cambridge, January 28 29, 2010 1 Introduction

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

Debt vs Growth: Correlation or Causation

Debt vs Growth: Correlation or Causation February 24, 2016 by Lance Roberts of Real Investment Advice Recently, my article on weak economic underpinnings led to an interesting exchange, via Twitter, with

Debt vs Growth: Correlation or Causation February 24, 2016 by Lance Roberts of Real Investment Advice Recently, my article on weak economic underpinnings led to an interesting exchange, via Twitter, with

Monetary and Exchange Rate Policy Responses to the Global Financial Crisis: The Case of Colombia

Monetary and Exchange Rate Policy Responses to the Global Financial Crisis: The Case of Colombia Hernando Vargas Banco de la República Colombia March, 2009 Contents I. The state of the Colombian economy

Monetary and Exchange Rate Policy Responses to the Global Financial Crisis: The Case of Colombia Hernando Vargas Banco de la República Colombia March, 2009 Contents I. The state of the Colombian economy

ECO 209Y MACROECONOMIC THEORY AND POLICY

Department of Economics Prof. Gustavo Indart University of Toronto December 7, 2011 ECO 209Y MACROECONOMIC THEORY AND POLICY Term Test #2 LAST NAME FIRST NAME STUDENT NUMBER Circle your section of the

Department of Economics Prof. Gustavo Indart University of Toronto December 7, 2011 ECO 209Y MACROECONOMIC THEORY AND POLICY Term Test #2 LAST NAME FIRST NAME STUDENT NUMBER Circle your section of the

Edmonton Real Estate Forum. Ron Gilbertson President and CEO Edmonton Economic Development Corporation

Edmonton Real Estate Forum Ron Gilbertson President and CEO Edmonton Economic Development Corporation The Latest Economic News Depression Economic Downturn The Economy What s Going On? Edmonton and Alberta

Edmonton Real Estate Forum Ron Gilbertson President and CEO Edmonton Economic Development Corporation The Latest Economic News Depression Economic Downturn The Economy What s Going On? Edmonton and Alberta

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

Macro Vision June 13, 2017

Macro Vision June 13, 2017 Country risk: how far can it reach? The global environment has been favorable to emerging markets, despite the recent drop in commodity prices. Better global growth and lower

Macro Vision June 13, 2017 Country risk: how far can it reach? The global environment has been favorable to emerging markets, despite the recent drop in commodity prices. Better global growth and lower

Macroeconomic Measurement 3: The Accumulation of Value

International Economics and Business Dynamics Class Notes Macroeconomic Measurement 3: The Accumulation of Value Revised: October 30, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm

International Economics and Business Dynamics Class Notes Macroeconomic Measurement 3: The Accumulation of Value Revised: October 30, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

Jürgen Stark: Financial stability the role of central banks. A new task? A new strategy? New tools?

Jürgen Stark: Financial stability the role of central banks. A new task? A new strategy? New tools? Speech by Mr Jürgen Stark, Member of the Executive Board of the European Central Bank, at the Frankfurt

Jürgen Stark: Financial stability the role of central banks. A new task? A new strategy? New tools? Speech by Mr Jürgen Stark, Member of the Executive Board of the European Central Bank, at the Frankfurt

Understanding the Rupee Shortfall: A Macroeconomic Policy Challenge for Bhutan and the Way Forward

Understanding the Rupee Shortfall: A Macroeconomic Policy Challenge for Bhutan and the Way Forward Hamid Rashid, Ph.D. Senior Adviser for Macroeconomic Policy UN Department of Economic and Social Affairs,

Understanding the Rupee Shortfall: A Macroeconomic Policy Challenge for Bhutan and the Way Forward Hamid Rashid, Ph.D. Senior Adviser for Macroeconomic Policy UN Department of Economic and Social Affairs,

From Crisis to Recovery: The Challenges ahead for the European Economy

From Crisis to Recovery: The Challenges ahead for the European Economy Moreno Bertoldi Head of Unit Countries of the G-20, IMF, G-groups European Commission COMEXI 24 June 2014 PART I: Current Economic

From Crisis to Recovery: The Challenges ahead for the European Economy Moreno Bertoldi Head of Unit Countries of the G-20, IMF, G-groups European Commission COMEXI 24 June 2014 PART I: Current Economic

Economic and housing outlook for New South Wales. Warwick Temby, Acting Chief Economist HIA Industry Outlook Breakfast Sydney, August 2017

Economic and housing outlook for New South Wales Warwick Temby, Acting Chief Economist HIA Industry Outlook Breakfast Sydney, August 2017 Risks to residential building moving from global to local World

Economic and housing outlook for New South Wales Warwick Temby, Acting Chief Economist HIA Industry Outlook Breakfast Sydney, August 2017 Risks to residential building moving from global to local World

It has been suggested in the literature that a shortage of sound and liquid financial

I. Local Bond Markets During the Global Financial Crisis II. Abstract (117 words) It has been suggested in the literature that a shortage of sound and liquid financial instruments in emerging economies

I. Local Bond Markets During the Global Financial Crisis II. Abstract (117 words) It has been suggested in the literature that a shortage of sound and liquid financial instruments in emerging economies

Credit Market Imperfections, Credit Frictions and Financial Crises. Instructor: Dmytro Hryshko

Credit Market Imperfections, Credit Frictions and Financial Crises Instructor: Dmytro Hryshko 1 / 23 Outline Credit Market Imperfections and Consumption. Asymmetric Information and the Financial Crisis.

Credit Market Imperfections, Credit Frictions and Financial Crises Instructor: Dmytro Hryshko 1 / 23 Outline Credit Market Imperfections and Consumption. Asymmetric Information and the Financial Crisis.

Labour. Overview Latin America and the Caribbean. Executive Summary. ILO Regional Office for Latin America and the Caribbean

2017 Labour Overview Latin America and the Caribbean Executive Summary ILO Regional Office for Latin America and the Caribbean Executive Summary ILO Regional Office for Latin America and the Caribbean

2017 Labour Overview Latin America and the Caribbean Executive Summary ILO Regional Office for Latin America and the Caribbean Executive Summary ILO Regional Office for Latin America and the Caribbean

March 6, Why Is The Fed Tapering? Michael Purves Chief Global Strategist Head of Equity Derivatives Research (203)

") Michael Purves Chief Global Strategist Head of Equity Derivatives Research (203) 861-7725 mpurves@weedenco.com March 6, 2014 Why Is The Fed Tapering? As Yellen has taken the helm of the Federal Reserve,

Michael Purves Chief Global Strategist Head of Equity Derivatives Research (203) 861-7725 mpurves@weedenco.com March 6, 2014 Why Is The Fed Tapering? As Yellen has taken the helm of the Federal Reserve,