INDEX-BASED LIVESTOCK INSURANCE: PROTECTING PASTORALISTS FROM DROUGHT-RELATED LIVESTOCK LOSSES

|

|

|

- Alexina Atkins

- 5 years ago

- Views:

Transcription

1 Session 1 INDEX-BASED LIVESTOCK INSURANCE: PROTECTING PASTORALISTS FROM DROUGHT-RELATED LIVESTOCK LOSSES Andrew Mude International Livestock Research Institute P.O. Box 30709, Nairobi 00100, Kenya Andrew Mude received a Ph.D. in economics (with concentrations in development economics and applied econometrics) from Cornell University (in the United States) and is currently lead scientist and project leader for the Index-Based Livestock Insurance program at the International Livestock Research Institute, based in Nairobi, Kenya. Dr. Mude s current portfolio focuses on issues of resilience and vulnerability amongst poor livestock-dependent households, particularly in pastoral areas. 68

2 Andrew Mude ABSTRACT This paper describes the design, logic and implementation of an award-winning innovation in the provision of formal insurance to help drought-vulnerable livestock keepers manage the risk of widespread livestock mortality. Much of the Horn of Africa is Arid and Semi-Arid lands (ASALs) populated by pastoralists. These are among the most vulnerable populations in the region as their livestock-dominated livelihoods are constantly threatened by increasingly severe droughts that has made the boom-and-bust dynamic a constant feature of their production systems. To help these populations better manage the risk of drought-related livestock losses, a pilot index-based livestock insurance (IBLI) product was launched in January 2010 in Marsabit District of Northern Kenya. Indexbased insurance products represent a promising and exciting innovation for managing the climate related risks that vulnerable households face ( This IBLI product has many innovative features. It appears to be the first to develop the index insurance product from longitudinal household data so as to minimize basis risk in product design. It is one of the first developed to protect the productive asset holdings of the poor and vulnerable rather than just their income streams. It is one of the first to be based on more spatially distributed remotely-sensed vegetation data, rather than rainfall series from a sparse set of fixed point meteorological stations, as the IBLI index is derived from satellite-based normalized differenced vegetation index (NDVI) series that summarize the state of rangeland forage availability at high spatiotemporal resolution. Finally, IBLI Marsabit was designed to complement a new (unconditional) cash transfer program (the Hunger Safety Nets Program, HSNP) the government launched in the area and the IBLI impact evaluation design explicitly enables identification of the independent and synergistic effects of HSNP and IBLI as alternative means of addressing the risk and financing constraints faced by the poor. This paper will discuss the process of identifying, developing and implementing the IBLI project. We shall highlight the design methodology of the insurance index, describe its key features and how it relates to the risk profile and production system it seeks to manage. The paper will also touch on the determinants of uptake and initial impact assessment results that are being generated. The paper will make use of the comprehensive project panel data based on annual household surveys launched in October Aimed at allowing for rigorous analysis of demand and impact assessment, the data employs an encouragement sampling design made up of differential access to insurance educational extension (in the form of an experimental insurance game, which allows players to learn the mechanics and value of IBLI) and discount coupons that, in varying the effective price of insurance, allows the estimation of a demand curve and the relevant price elasticities. The paper will tease out the implications of the analysis and the insights gained from implementation and draw out recommendations to guide efforts at scaling up the IBLI project as well as improving client targeting and the design of the product. Understanding the impact of various determinants will help identify effective approaches to catalyzing demand; including the appropriate pricing strategy. This quantitative assessment will be supplemented by the results of various qualitative interactions with clients, their representatives and various stakeholders in the area to help develop context and draw insights to explain some of the analytical findings. KEYWORDS Drought risk management, index insurance, pastoralists, livestock mortality, vegetation index 69

3 Session

4 Andrew Mude

5 Session

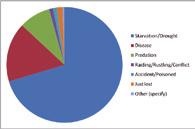

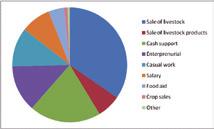

6 Andrew Mude Chairman Dr. Tomoyuki Kawashima: Let me introduce the third presenter, Dr. Andrew Mude. Dr. Andrew Mude has a Ph.D. in economics from Cornell University and he is Lead Scientist and Project Leader for the index-based livestock insurance program at the International Livestock Research Institute (ILRI), based in Nairobi. He is going to show his activities in ILRI. Dr. Andrew Mude: Thank you very much, Chair. Good afternoon ladies and gentlemen. I would first like to thank JIRCAS very much for giving me the honor of an invitation to give this presentation. We have been talking today about the importance of resilience and particularly also trying to bring together new technologies, so using technology to help improve resilience. The project that I m working on, index-based livestock insurance, is actually an attempt to design a new technology, and also to implement it and assess its impacts, to help protect pastoralists against drought-based livestock mortality. So I should also thank Junichi the previous speaker, who has helped me quite a bit by setting up the context, because he also works with pastoralists and one of his project sites is in Marsabit, which is the initial site where we began studying the conditions in 2008 that resulted in our design of this product and its launch in January You know a bit about Marsabit. It is in northern Kenya; it is a very arid area, and it is an area in which the Pastoral production system dominates. Why do we have index-based livestock insurance? What are the conditions that it is trying to cover? What you need to have first is an understanding of the importance of the livestock economy in the area, and also a bit of its risk profile. First of all, the shares of income. This is based on a household survey that we conducted in Marsabit in 2009, which was the baseline. We have been following these 924 households every year since then, so we have a four-year panel. This pie chart shows the component shares of income. Here in blue is the sale of livestock and in red is sale of livestock products like milk and hides and so on. You can see that for this population, livestock and livestock products contribute 40% of household income. So that is a really big proportion of the income coming from those two aspects. Just to also put it in context, you find that external support in these communities in the form of food aid and cash also constitute nearly 25% of household income. So these are relatively poor communities which require a lot of external support, largely in the form of food and cash aid. Livestock is very important to income, but livestock is also the key productive asset in the area. By productive asset we are talking about those assets that will help to build the wealth of the households, so of course livestock. We are not really talking about their homes or their huts, but if they have shops or if they have vehicles that are useful productive endeavor, if they have any farming equipment and so on. You can find that for the mean household, the livestock share of productive assets is 49%, but for the median household. It is 100%. So livestock is very critical in this economy. What are the threats to livestock? Livestock mortality is a key source of vulnerability in the area. You find that here in blue, drought contributes almost 70% of livestock mortality. In red is the incidence of mortality caused by disease and predation. Disease is likely to increase during times of drought, because the livestock are weak and their immune systems are negatively affected. So this is the context in which we designed this product known as index-based livestock insurance. I imagine that you are all familiar with traditional insurance that is used for assets such as your house, your car, or even your health. The idea is basically to take this concept, but to redesign it in a form that is suitable for an area such as Marsabit. The insurance product covers drought-related livestock mortality, as I have explained. Basically, how and index-based product works, which is an innovation in insurance is that the indemnity is not paid to an individual. The indemnity is based on an index that proxies or is related to the underlying risk that you are trying to cover, but is based on the geographical average of the area of interest. I will explain more. 73

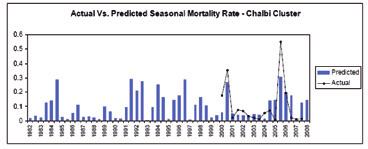

7 Session 1 In designing this index, we used satellite-based readings of forage availability on the ground and we matched those up with livestock mortality data that has been collected in the region by the government from Every month a select number of households in the area were surveyed. So we used to that livestock mortality data with a remotely sensed Normalized Difference Vegetation Index (NDVI). You calibrate an empirical relationship, which we are calling the response function, and from that you are able to predict area average livestock mortality. When you get that area average livestock mortality, that is the index upon which insurance is written. As I mentioned earlier, we first launched a commercial product that was mediated through the market by local insurance companies in Kenya and also reinsured by Swiss Re which is one of the world s largest reinsurance companies. It was first launched in January 2010 in northern Kenya, and we have also been working in southern Ethiopia and launched a product this August Why do we have this program? Why do we hypothesize that in such a system, an insurance program could be beneficial? First, it can prevent the downward slide of vulnerable populations into poverty. By this I mean that there is a lots of research that has been done in the area, some of it by some of my own colleagues that shows the presence of what we call asset-based poverty traps and what this means is that, given that the Pastoral production system and the way that they migrate from place to place, if you fall below a certain threshold, estimated to be an average of 10 livestock units, you begin to then enter a decumulation trajectory, because you are forced to sedentarize and you do not have access to forage and water and you fall into a low-level equilibrium. The idea is that perhaps insurance can compensate people to ensure that they keep above the threshold and keep a viable size of herds. There is also the idea of stabilizing expectations and encouraging the investments of the poor. What this means is that when you have one of your key assets that is very volatile, the incentives to invest might be a lot less than if you reduce the risks associated with this. Further, it can be hypothesized that it can induce financial deepening by crowding in-credit supply and demand, and basically this is by insurance reducing the risk of an asset as insurance will do, which increases the collateral value of that asset, and so it is possible that banks and other financial institutions in that area can offer credit on the basis of that collateralized insurance. So how do we design this product? Well, first of all, you have got to define the risk. I already talked about that; the risk is drought-related livestock mortality. But the risk has to be a particular type of risk, and it has to be a risk that is covariant in nature. And what this means is when the risk heads a particular area, most of the people in the area are affected in a similar way. This is because the index indicates the average condition. So if the average condition is covariant then it is unlikely to be experienced by most people. Then of course it needs to be a risk that can be predicted, so that it can be modeled and we can predict livestock mortality in an area. And the index itself has to have a certain qualities. It needs to be a specific measure that can be highly associated with the risk. The reason why in the pastoral production system, we can use these satellite-based measures of forage is a good predictor of livestock mortality is because in that system you do not have much supplementation. The livestock gets almost 100% of its nutrition from the forage, of which satellites are capturing their condition. Also, the index must be easy to measure; it should not be manipulated by either the individual getting insurance or the insurance company, and satellites are certainly not manipulable by either of those two parties. Satellite data is consistently available and freely available on the Internet at high levels of resolution. So, how do we design the index? I think I ve already talked about this, but this graphic at the bottom shows you the data that we are using. It is the NDVI from a sensor which is a satellite of the US National Oceanic and Atmospheric Agency. You can see that in normal years, such as in May 2007, it looks quite green, while in drought years. It looks very brown. That is the data that we are using and it is the signal that we use to predict livestock mortality based on how liberated empirical relationship. The index or the insurance is only as good as its performance. So one of the issues with index-based insurance is what is called basis risk, which defines the difference between the index and the actual experience. If the index has predicted average mortality in an area, it is not necessarily the case, and in fact it is not likely to be the case 74

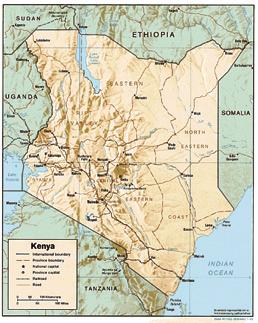

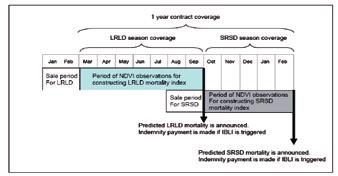

8 Andrew Mude that everybody is experiencing the same average. So the wider the dispersion, the weaker the product. That is why I said earlier, it is important for index insurance products that the risk you are trying to insure is highly covariant. This graph shows our data from 2000 to There are no black you see what the actual livestock mortality experienced in this particular area is, and the blue is the predicted. We can predict all the way from 1982, because we have satellite data available from You see, quite a high level of correlation between the predicted and the actual data. Once you have designed the product, in order to sell it on the ground. There are certain key contract features that you need to identify. First is how wide of a geographic area can a single index cover? This is a map of the Marsabit District. Marsabit District is one of the largest districts in Kenya and so you can expect that the conditions of pastoralists living in this area will be quite a bit different from those in lower Marsabit. And actually, they are; up in this area in the blue and green that we are calling the upper cluster, you have mostly camels, goats and sheep, and it is a lot drier in this area. Here at the bottom it is mostly cows and a bit less dry or vulnerable to droughts. So we have to have two separate indices. We have got a response function for what we call the upper cluster and another response function for what we are calling this low cluster. And that is just a relationship. But even then, we have still broken it down into five different divisions. So in this area for the upper cluster, we take the average NDVI reading in this area and plug that into the response function to get predicted livestock index in North Horr which is this green area, and for blue we take the average of the index NDVI readings in this area known as Maikona and we use that using the same response function to predict livestock mortality in that area. Another issue of the contract design is that you have to specify the temporal coverage. Junichi earlier mentioned that there are two rainy seasons in one the year in Marsabit. So these contracts are year-long contracts, but there are two selling Windows. There is a selling window in January/February, which is a dry season right before the beginning of the long rains. You want to do that because you want to make sure that an individual purchases the insurance before you see any signal of rain or so on or any signal of what the season might look like. If you purchase in January/February then you are covered all the way from March to February of the following year, and there are two potential payout periods: at the end of the long, dry season in September and at the end of the short dry season in February, where the insurance company looks at the index and pays out as a function of that. Moving forward, what will determine if this product is successful or not? There are two things. One of the things that we think is most important is that it has to demonstrate some positive welfare impacts. This study that is just coming out was based on anticipated behavioral changes due to payments in October You have heard that there was a big drought in the area in In 2011 every single contract holder received payments because the contracts triggered. We wanted to know the difference between those who are insured and those who are not insured; what were the different impacts on the household? What you see here is for households who were insured there was a 33% reduction in their employment of hunger strategies, which is reducing the number of meals per day. We heard earlier that this is very important because it has severe long-term consequences. If you have to reduce the intake of important nutrients and so on, the child might have long-term developmental impacts. We also see, for example, a 33% drop in food aid reliance for those who have insurance, which means that the fiscal budget that goes to food aid in the area can be reduced. The second determinant of the product is long-term sustainability. Ever since January 2010 when we had our first sale period, the number of contracts sold has been decreasing. At first the insurance company sold 1,974 contracts. This has gone down to 595 and just recently to 219 contracts. So why is this? There are many reasons that we have identified that can be remediated. But one of the reasons we feel is that as a project team, from the very beginning we gave the insurance company a lot of support, but we have been systematically reducing our report. The reason is that there is a lot of pressure for commercial sustainability. I think that pressure is premature, so I am in discussions with the donors and supporters in the government of Kenya to give us more time and to allow for more support in the system for us to be able to build sustainability long term. Because actually there are not 75

9 Session 1 many instances of agricultural insurance around the world, whether developing or developed countries, that are 100% commercially sustainable. That is because there must be some other reason that the government considers it to be important for the provision of some kind of report. That is why we do this research, to look and see what the actual benefits are. Going forward, the main purpose of the project is to generate a critical mass of informed pastoralists. This is very difficult and very important. The areas that we are talking about are areas that have the highest levels of illiteracy and innumeracy. Insurance is a new product so how do you ensure what they are buying before they buy it? But then also we want to make sure that this is mediated through the industry by a capacitated insurance industry. Right now most of the insurance companies in Kenya do not know how to design these products. This is a pilot so we have taken it upon ourselves as the team working on this to try to build capacity within the insurance industry and try to support the government with the development of agricultural insurance policies and under that index insurance policies, to help build the right kind of institutions. Our research agenda is based on four pillars. One is to continue a rigorous assessment of the behavioral change and the welfare impacts that IBLI index-based livestock insurance has on a pastoral production system. The second is the development of institutions and capacities necessary to build the market and create an institutional support system. The third is improving the design of the contracts and scaling out beyond just Marsabit to other areas of northern Kenya and beyond just Marsabit to other areas in northern Kenya and beyond Borana where we work in southern Ethiopia to other areas there. The fourth is to try and look at a different type of contract. Right now the contracts that we are providing are for individuals at the household level. But it is also possible that such products could be designed for let us say, county governments or even international institutions like the world food program that are tasked to respond to emergencies because there is a lot difficulty even in raising the resources that come about during times of drought and famine, and if they have insurance contracts that are based on a method that can easily predict the instances of famine, then it could be a lots more cost effective for them. Thank you very much for your attention. Chairman: Thank you, Andrew for a very nice presentation. 76

Market-provisioned social protection: The Index-based Livestock Insurance (IBLI) Experiment in Northern Kenya

Experiment in Northern Kenya") Market-provisioned social protection: The Index-based Livestock Insurance (IBLI) Experiment in Northern Kenya Chris Barrett Cornell University (on behalf of the ANU-Cornell-ILRI-Syracuse UC Davis IBLI

Market-provisioned social protection: The Index-based Livestock Insurance (IBLI) Experiment in Northern Kenya Chris Barrett Cornell University (on behalf of the ANU-Cornell-ILRI-Syracuse UC Davis IBLI

Index Based Livestock Insurance (IBLI): Toward Sustainable Risk Management for Pastoralist Herders

: Toward Sustainable Risk Management for Pastoralist Herders") Index Based Livestock Insurance (IBLI): Toward Sustainable Risk Management for Pastoralist Herders Andrew Mude, IBLI Program Lead, International Livestock Research Institute KLIP Executive Seminar for

Index Based Livestock Insurance (IBLI): Toward Sustainable Risk Management for Pastoralist Herders Andrew Mude, IBLI Program Lead, International Livestock Research Institute KLIP Executive Seminar for

Sustainable Livestock Insurance for Pastoralists: the Index-Based Livestock Insurance (IBLI) Experience

Experience") Sustainable Livestock Insurance for Pastoralists: the Index-Based Livestock Insurance (IBLI) Experience A SIZEABLE CONSTITUENT Over 50 million pastoralists in Sub-Saharan Africa: over 25 million in the

Sustainable Livestock Insurance for Pastoralists: the Index-Based Livestock Insurance (IBLI) Experience A SIZEABLE CONSTITUENT Over 50 million pastoralists in Sub-Saharan Africa: over 25 million in the

Index Insurance: Financial Innovations for Agricultural Risk Management and Development

Index Insurance: Financial Innovations for Agricultural Risk Management and Development Sommarat Chantarat Arndt-Corden Department of Economics Australian National University PSEKP Seminar Series, Gadjah

Index Insurance: Financial Innovations for Agricultural Risk Management and Development Sommarat Chantarat Arndt-Corden Department of Economics Australian National University PSEKP Seminar Series, Gadjah

Protecting Pastoralists from the Risk of Drought Related Livestock Mortality: Index Based Livestock Insurance in Northern Kenya and Sothern Ethiopia

Protecting Pastoralists from the Risk of Drought Related Livestock Mortality: Index Based Livestock Insurance in Northern Kenya and Sothern Ethiopia BRENDA WANDERA TFESSD Forum Dar es Salaam Tanzania,

Protecting Pastoralists from the Risk of Drought Related Livestock Mortality: Index Based Livestock Insurance in Northern Kenya and Sothern Ethiopia BRENDA WANDERA TFESSD Forum Dar es Salaam Tanzania,

The Favorable Impact of Index-Based Livestock Insurance (IBLI): Results among Ethiopian and Kenyan Pastoralists

: Results among Ethiopian and Kenyan Pastoralists") The Favorable Impact of Index-Based Livestock Insurance (IBLI): Results among Ethiopian and Kenyan Pastoralists Christopher B. Barrett, Cornell University Workshop on Innovations in Index Insurance to

The Favorable Impact of Index-Based Livestock Insurance (IBLI): Results among Ethiopian and Kenyan Pastoralists Christopher B. Barrett, Cornell University Workshop on Innovations in Index Insurance to

Add Presenter Name Here. Index Insurance for Agricultural Risk Management

Add Presenter Name Here Index Insurance for Agricultural Risk Management IMAGINE FOR A MOMENT: You re a smallholder farmer. You re just near the poverty line, either above or below just making ends meet

Add Presenter Name Here Index Insurance for Agricultural Risk Management IMAGINE FOR A MOMENT: You re a smallholder farmer. You re just near the poverty line, either above or below just making ends meet

Towards Evidence-Based and Data-Informed Policies and Practice: The case of the Index-Based Livestock Insurance (IBLI) in Kenya and Ethiopia

in Kenya and Ethiopia") Towards Evidence-Based and Data-Informed Policies and Practice: The case of the Index-Based Livestock Insurance (IBLI) in Kenya and Ethiopia Andrew Mude, IBLI Program Lead, International Livestock Research

Towards Evidence-Based and Data-Informed Policies and Practice: The case of the Index-Based Livestock Insurance (IBLI) in Kenya and Ethiopia Andrew Mude, IBLI Program Lead, International Livestock Research

KENYA LIVESTOCK INSURANCE PROGRAM

KENYA LIVESTOCK INSURANCE PROGRAM Progress of implementation of KLIP Richard Kyuma, PhD., OGW KLIP Program Coordinator State Department of Livestock Contents Justification - Why Livetock insurance KLIP

KENYA LIVESTOCK INSURANCE PROGRAM Progress of implementation of KLIP Richard Kyuma, PhD., OGW KLIP Program Coordinator State Department of Livestock Contents Justification - Why Livetock insurance KLIP

Learning Journey. International Livestock Research Institute (ILRI)

") Learning Journey International Livestock Research Institute (ILRI) Piloting IBLI in Marsabit: Building delivery infrastructure and fuelling knowledge-based adoption This Learning Journey was created with

Learning Journey International Livestock Research Institute (ILRI) Piloting IBLI in Marsabit: Building delivery infrastructure and fuelling knowledge-based adoption This Learning Journey was created with

Insuring Against Drought Related Livestock Mortality: Piloting Index Based Livestock Insurance in Northern Kenya

Syracuse University SURFACE Economics Faculty Scholarship Maxwell School of Citizenship and Public Affairs 6-1-2010 Insuring Against Drought Related Livestock Mortality: Piloting Index Based Livestock

Syracuse University SURFACE Economics Faculty Scholarship Maxwell School of Citizenship and Public Affairs 6-1-2010 Insuring Against Drought Related Livestock Mortality: Piloting Index Based Livestock

The objectives of KLIP are:

KENYA LIVESTOCK INSURANCE PROGRAMME (KLIP) GARISSA COUNTY STAKEHOLDER AWARENESS SENSITIZATION WORKSHOP HELD ON 10 th to 13 th DECEMBER AT HIDDING HOTEL IN GARISSA Introduction by Dr Richard Kyuma The Kenya

KENYA LIVESTOCK INSURANCE PROGRAMME (KLIP) GARISSA COUNTY STAKEHOLDER AWARENESS SENSITIZATION WORKSHOP HELD ON 10 th to 13 th DECEMBER AT HIDDING HOTEL IN GARISSA Introduction by Dr Richard Kyuma The Kenya

Insuring against drought-related livestock mortality: Piloting index-based livestock insurance in northern Kenya

Insuring against drought-related livestock mortality: Piloting index-based livestock insurance in northern Kenya Andrew Mude 1, Sommarat Chantarat 2, Christopher B. Barrett 3, Michael Carter 4, Munenobu

Insuring against drought-related livestock mortality: Piloting index-based livestock insurance in northern Kenya Andrew Mude 1, Sommarat Chantarat 2, Christopher B. Barrett 3, Michael Carter 4, Munenobu

Index Insurance to Enhance Productivity and Incomes for Small-scale Agricultural and Pastoral Households in Kenya & Mali

Index Insurance to Enhance Productivity and Incomes for Small-scale Agricultural and Pastoral Households in Kenya & Mali Chris Barrett Michael Carter Andrew Mude Cornell University University of California,

Index Insurance to Enhance Productivity and Incomes for Small-scale Agricultural and Pastoral Households in Kenya & Mali Chris Barrett Michael Carter Andrew Mude Cornell University University of California,

Index Based Livestock Insurance

Index Based Livestock Insurance Protec4ng Vulnerable Pastoralists from Drought-related Shocks UR2016 Geneva, May 20 th Panel: How Risks and Shocks Impact Poverty, and Why, When, and Where Can BeOer Financial

Index Based Livestock Insurance Protec4ng Vulnerable Pastoralists from Drought-related Shocks UR2016 Geneva, May 20 th Panel: How Risks and Shocks Impact Poverty, and Why, When, and Where Can BeOer Financial

DOES INSURANCE IMPROVE RESILIENCE?

DOES INSURANCE IMPROVE RESILIENCE? MEASURING THE IMPACT OF INDEX-BASED LIVESTOCK INSURANCE ON DEVELOPMENT RESILIENCE IN NORTHERN KENYA Jennifer Denno Cissé 1 and Munenobu Ikegami 2 October 2016 ABSTRACT:

DOES INSURANCE IMPROVE RESILIENCE? MEASURING THE IMPACT OF INDEX-BASED LIVESTOCK INSURANCE ON DEVELOPMENT RESILIENCE IN NORTHERN KENYA Jennifer Denno Cissé 1 and Munenobu Ikegami 2 October 2016 ABSTRACT:

Risk & Resilience Ample evidence that risk Makes people poor by reducing incomes & destroying assets, sometimes pushing households into a situation fr

Scaling Tools for Resilient Drylands Professor, University of California, Davis, Giannini Foundation & NBER Director, Feed the Future Assets & Market Access Innovation Lab October 11, 2016 Risk & Resilience

Scaling Tools for Resilient Drylands Professor, University of California, Davis, Giannini Foundation & NBER Director, Feed the Future Assets & Market Access Innovation Lab October 11, 2016 Risk & Resilience

KENYAN EXPERIENCE WITH PARAMETRIC INSURANCE. Presented by: Joseph A. Owuor Insurance Regulatory Authority - Kenya

KENYAN EXPERIENCE WITH PARAMETRIC INSURANCE Presented by: Joseph A. Owuor Insurance Regulatory Authority - Kenya REGIONAL WORKSHOP ON PARAMETRIC INSURANCE - GUATEMALA -11 OCTOBER 2016 AGENDA 1. IBI Pilot

KENYAN EXPERIENCE WITH PARAMETRIC INSURANCE Presented by: Joseph A. Owuor Insurance Regulatory Authority - Kenya REGIONAL WORKSHOP ON PARAMETRIC INSURANCE - GUATEMALA -11 OCTOBER 2016 AGENDA 1. IBI Pilot

Assets Channel: Adaptive Social Protection Work in Africa

Assets Channel: Adaptive Social Protection Work in Africa Carlo del Ninno Climate Change and Poverty Conference, World Bank February 10, 2015 Chronic Poverty and Vulnerability in Africa Despite Growth,

Assets Channel: Adaptive Social Protection Work in Africa Carlo del Ninno Climate Change and Poverty Conference, World Bank February 10, 2015 Chronic Poverty and Vulnerability in Africa Despite Growth,

Testing for Poverty Traps: Asset Smoothing versus Consumption Smoothing in Burkina Faso (with some thoughts on what to do about it)

") Testing for Poverty Traps: Asset Smoothing versus Consumption Smoothing in Burkina Faso (with some thoughts on what to do about it) Travis Lybbert Michael Carter University of California, Davis Risk &

Testing for Poverty Traps: Asset Smoothing versus Consumption Smoothing in Burkina Faso (with some thoughts on what to do about it) Travis Lybbert Michael Carter University of California, Davis Risk &

Hunger Safety Net Programme. Options Paper for scaling up HSNP Payments February 2015

Hunger Safety Net Programme Options Paper for scaling up HSNP Payments February 2015 1. Introduction and Context 1.1 Purpose of this Paper 1. This paper has been developed to support NDMA and its national

Hunger Safety Net Programme Options Paper for scaling up HSNP Payments February 2015 1. Introduction and Context 1.1 Purpose of this Paper 1. This paper has been developed to support NDMA and its national

Index-Based Livestock Insurance (IBLI): On the Posi:ve Impacts of An Imperfect Product Christopher B. BarreA, Cornell University

: On the Posi:ve Impacts of An Imperfect Product Christopher B. BarreA, Cornell University") Index-Based Livestock Insurance (IBLI): On the Posi:ve Impacts of An Imperfect Product Christopher B. BarreA, Cornell University Interna:onal Programs- CALS Seminar Cornell University March 7, 2018 Motivation:

Index-Based Livestock Insurance (IBLI): On the Posi:ve Impacts of An Imperfect Product Christopher B. BarreA, Cornell University Interna:onal Programs- CALS Seminar Cornell University March 7, 2018 Motivation:

Drought and Informal Insurance Groups: A Randomised Intervention of Index based Rainfall Insurance in Rural Ethiopia

Drought and Informal Insurance Groups: A Randomised Intervention of Index based Rainfall Insurance in Rural Ethiopia Guush Berhane, Daniel Clarke, Stefan Dercon, Ruth Vargas Hill and Alemayehu Seyoum Taffesse

Drought and Informal Insurance Groups: A Randomised Intervention of Index based Rainfall Insurance in Rural Ethiopia Guush Berhane, Daniel Clarke, Stefan Dercon, Ruth Vargas Hill and Alemayehu Seyoum Taffesse

E Distribution: GENERAL. Executive Board Annual Session. Rome, June 2006

Executive Board Annual Session Rome, 12 16 June 2006 E Distribution: GENERAL 8 June 2006 ORIGINAL: ENGLISH This document is printed in a limited number of copies. Executive Board documents are available

Executive Board Annual Session Rome, 12 16 June 2006 E Distribution: GENERAL 8 June 2006 ORIGINAL: ENGLISH This document is printed in a limited number of copies. Executive Board documents are available

After the Drought: The Impact of Microinsurance on Consumption Smoothing and Asset Protection

After the Drought: The Impact of Microinsurance on Consumption Smoothing and Asset Protection December 29, 2017 Michael R. Carter Sarah A. Janzen Montana State University Ph: (406) 994-3714 sarah.janzen@montana.edu

After the Drought: The Impact of Microinsurance on Consumption Smoothing and Asset Protection December 29, 2017 Michael R. Carter Sarah A. Janzen Montana State University Ph: (406) 994-3714 sarah.janzen@montana.edu

TOPICS FOR DEBATE. By Haresh Bhojwani, Molly Hellmuth, Daniel Osgood, Anne Moorehead, James Hansen

TOPICS FOR DEBATE By Haresh Bhojwani, Molly Hellmuth, Daniel Osgood, Anne Moorehead, James Hansen This paper is a policy distillation adapted from IRI Technical Report 07-03 Working Paper - Poverty Traps

TOPICS FOR DEBATE By Haresh Bhojwani, Molly Hellmuth, Daniel Osgood, Anne Moorehead, James Hansen This paper is a policy distillation adapted from IRI Technical Report 07-03 Working Paper - Poverty Traps

How Basis Risk and Spatiotemporal Adverse Selection Influence Demand for Index Insurance: Evidence from Northern Kenya

How Basis Risk and Spatiotemporal Adverse Selection Influence Demand for Index Insurance: Evidence from Northern Kenya By Nathaniel D. Jensen *, Andrew G. Mude and Christopher B. Barrett August 28, 2017

How Basis Risk and Spatiotemporal Adverse Selection Influence Demand for Index Insurance: Evidence from Northern Kenya By Nathaniel D. Jensen *, Andrew G. Mude and Christopher B. Barrett August 28, 2017

SCALIBILITY OF REMOTELY SENSED LIVESTOCK INDEX INSURANCE IN EAST AFRICA. A Thesis. Presented to the Faculty of the Graduate School

SCALIBILITY OF REMOTELY SENSED LIVESTOCK INDEX INSURANCE IN EAST AFRICA A Thesis Presented to the Faculty of the Graduate School of Cornell University In Partial Fulfillment of the Requirements for the

SCALIBILITY OF REMOTELY SENSED LIVESTOCK INDEX INSURANCE IN EAST AFRICA A Thesis Presented to the Faculty of the Graduate School of Cornell University In Partial Fulfillment of the Requirements for the

E Distribution: GENERAL. Executive Board Second Regular Session. Rome, 6 10 November 2006

Executive Board Second Regular Session Rome, 6 10 November 2006 E Distribution: GENERAL 30 October 2006 ORIGINAL: ENGLISH This document is printed in a limited number of copies. Executive Board documents

Executive Board Second Regular Session Rome, 6 10 November 2006 E Distribution: GENERAL 30 October 2006 ORIGINAL: ENGLISH This document is printed in a limited number of copies. Executive Board documents

African Risk Capacity. Sovereign Disaster Risk Solutions A Project of the African Union

African Risk Capacity Sovereign Disaster Risk Solutions A Project of the African Union The Way Disaster Assistance Works Now EVENT ASSESS APPEAL FUNDING RESPONSE CNN EFFECT time The Way Disaster Assistance

African Risk Capacity Sovereign Disaster Risk Solutions A Project of the African Union The Way Disaster Assistance Works Now EVENT ASSESS APPEAL FUNDING RESPONSE CNN EFFECT time The Way Disaster Assistance

17 Demand for drought insurance in Ethiopia

128 The challenges of index-based insurance for food security in developing countries 17 Demand for drought insurance in Ethiopia Million Tadesse (1) (2), Frode Alfnes (1), Stein T. Holden (1), Olaf Erenstein

128 The challenges of index-based insurance for food security in developing countries 17 Demand for drought insurance in Ethiopia Million Tadesse (1) (2), Frode Alfnes (1), Stein T. Holden (1), Olaf Erenstein

Setting the scene. Benjamin Davis Jenn Yablonski. Methodological issues in evaluating the impact of social cash transfers in sub Saharan Africa

Setting the scene Benjamin Davis Jenn Yablonski Methodological issues in evaluating the impact of social cash transfers in sub Saharan Africa Naivasha, Kenya January 19-21, 2011 Why are we holding this

Setting the scene Benjamin Davis Jenn Yablonski Methodological issues in evaluating the impact of social cash transfers in sub Saharan Africa Naivasha, Kenya January 19-21, 2011 Why are we holding this

How Basis Risk and Spatiotemporal Adverse Selection Influence Demand for Index Insurance: Evidence from Northern Kenya

MPRA Munich Personal RePEc Archive How Basis Risk and Spatiotemporal Adverse Selection Influence Demand for Index Insurance: Evidence from Northern Kenya Nathaniel Jensen and Andrew Mude and Christopher

MPRA Munich Personal RePEc Archive How Basis Risk and Spatiotemporal Adverse Selection Influence Demand for Index Insurance: Evidence from Northern Kenya Nathaniel Jensen and Andrew Mude and Christopher

Welcome again to our Farm Management and Finance educational series. Borrowing money is something that is a necessary aspect of running a farm or

Welcome again to our Farm Management and Finance educational series. Borrowing money is something that is a necessary aspect of running a farm or ranch business for most of us, at least at some point in

Welcome again to our Farm Management and Finance educational series. Borrowing money is something that is a necessary aspect of running a farm or ranch business for most of us, at least at some point in

DESIGNING INDEX BASED LIVESTOCK INSURANCE FOR MANAGING ASSET RISK IN NORTHERN KENYA

DESIGNING INDEX BASED LIVESTOCK INSURANCE FOR MANAGING ASSET RISK IN NORTHERN KENYA Sommarat Chantarat, Andrew G. Mude, Christopher B. Barrett and Michael R. Carter July 2009 The authors are Ph.D. candidate,

DESIGNING INDEX BASED LIVESTOCK INSURANCE FOR MANAGING ASSET RISK IN NORTHERN KENYA Sommarat Chantarat, Andrew G. Mude, Christopher B. Barrett and Michael R. Carter July 2009 The authors are Ph.D. candidate,

RUTH VARGAS HILL MAY 2012 INTRODUCTION

COST BENEFIT ANALYSIS OF THE AFRICAN RISK CAPACITY FACILITY: ETHIOPIA COUNTRY CASE STUDY RUTH VARGAS HILL MAY 2012 INTRODUCTION The biggest source of risk to household welfare in rural areas of Ethiopia

COST BENEFIT ANALYSIS OF THE AFRICAN RISK CAPACITY FACILITY: ETHIOPIA COUNTRY CASE STUDY RUTH VARGAS HILL MAY 2012 INTRODUCTION The biggest source of risk to household welfare in rural areas of Ethiopia

ECONOMICS OF RESILIENCE TO DROUGHT IN ETHIOPIA, KENYA AND SOMALIA EXECUTIVE SUMMARY

ECONOMICS OF RESILIENCE TO DROUGHT IN ETHIOPIA, KENYA AND SOMALIA EXECUTIVE SUMMARY This executive summary was prepared by Courtenay Cabot Venton for the USAID Center for Resilience January 2018 1 INTRODUCTION

ECONOMICS OF RESILIENCE TO DROUGHT IN ETHIOPIA, KENYA AND SOMALIA EXECUTIVE SUMMARY This executive summary was prepared by Courtenay Cabot Venton for the USAID Center for Resilience January 2018 1 INTRODUCTION

Productive Spillovers of the Take-up of Index-Based Livestock Insurance

Productive Spillovers of the Take-up of Index-Based Livestock Insurance Russell Toth, Chris Barrett, Richard Bernstein, Patrick Clark, Carla Gomes, Shibia Mohamed, Andrew Mude, and Birhanu Taddesse Abstract

Productive Spillovers of the Take-up of Index-Based Livestock Insurance Russell Toth, Chris Barrett, Richard Bernstein, Patrick Clark, Carla Gomes, Shibia Mohamed, Andrew Mude, and Birhanu Taddesse Abstract

ENSO Impact regions 10/21/12. ENSO Prediction and Policy. Index Insurance for Drought in Africa. Making the world a better place with science

ENSO Prediction and Policy Making the world a better place with science Index Insurance for Drought in Africa Science in service of humanity Dan Osgoode & Eric Holthaus International Research Institute

ENSO Prediction and Policy Making the world a better place with science Index Insurance for Drought in Africa Science in service of humanity Dan Osgoode & Eric Holthaus International Research Institute

US Dollar Struggles as Euro Gains Top Spot - A review of the Major Global Currencies

US Dollar Struggles as Euro Gains Top Spot - A review of the Major Global Currencies 26 th November 2017 My colleagues have been urging me to write a weekly commentary on Bitcoin/Cryptocurrencies. However,

US Dollar Struggles as Euro Gains Top Spot - A review of the Major Global Currencies 26 th November 2017 My colleagues have been urging me to write a weekly commentary on Bitcoin/Cryptocurrencies. However,

Agricultural Insurance for Developing Countries The Role of Governments

FARM - Pluriagri conference on Insuring Agricultural Production Paris, France December 18, 2012 Agricultural Insurance for Developing Countries The Role of Governments Olivier Mahul Program Coordinator,

FARM - Pluriagri conference on Insuring Agricultural Production Paris, France December 18, 2012 Agricultural Insurance for Developing Countries The Role of Governments Olivier Mahul Program Coordinator,

Mr. Daniel Maria, you may now begin.

Rule 12g3 2(b)Exemption #82-35186 Free English Translation 1Q18 Earnings Conference Call May 11 th, 2018 OPERATOR - Good morning everyone and thank you for waiting. Welcome to Banco do Brasil 1Q2018 earnings

Rule 12g3 2(b)Exemption #82-35186 Free English Translation 1Q18 Earnings Conference Call May 11 th, 2018 OPERATOR - Good morning everyone and thank you for waiting. Welcome to Banco do Brasil 1Q2018 earnings

Global population projections by the United Nations John Wilmoth, Population Association of America, San Diego, 30 April Revised 5 July 2015

Global population projections by the United Nations John Wilmoth, Population Association of America, San Diego, 30 April 2015 Revised 5 July 2015 [Slide 1] Let me begin by thanking Wolfgang Lutz for reaching

Global population projections by the United Nations John Wilmoth, Population Association of America, San Diego, 30 April 2015 Revised 5 July 2015 [Slide 1] Let me begin by thanking Wolfgang Lutz for reaching

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this educational series is so that we can talk about managing

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this educational series is so that we can talk about managing

Index-based Livestock Insurance Project, Mongolia

Index-based Livestock Insurance Project, Mongolia Dr. Jerry Skees President, GlobalAgRisk, Inc. The H.B. Price Professor of Policy and Risk University of Kentucky Slides Prepared in Collaboration with

Index-based Livestock Insurance Project, Mongolia Dr. Jerry Skees President, GlobalAgRisk, Inc. The H.B. Price Professor of Policy and Risk University of Kentucky Slides Prepared in Collaboration with

The Impact of Social Capital on Managing Shocks to Achieve Resilience: Evidence from Ethiopia, Kenya, Uganda, Niger and Burkina Faso

The Impact of Social Capital on Managing Shocks to Achieve Resilience: Evidence from Ethiopia, Kenya, Uganda, Niger and Burkina Faso Tim Frankenberger TANGO International January 5, 2016 10:00 11:30 AM

The Impact of Social Capital on Managing Shocks to Achieve Resilience: Evidence from Ethiopia, Kenya, Uganda, Niger and Burkina Faso Tim Frankenberger TANGO International January 5, 2016 10:00 11:30 AM

Using Index-based Risk Transfer Products to Facilitate Rural Lending in Mongolia, Peru, Vietnam

Using Index-based Risk Transfer Products to Facilitate Rural Lending in Mongolia, Peru, Vietnam Dr. Jerry Skees President, GlobalAgRisk, and H.B. Price Professor, University of Kentucky October 18, 2007

Using Index-based Risk Transfer Products to Facilitate Rural Lending in Mongolia, Peru, Vietnam Dr. Jerry Skees President, GlobalAgRisk, and H.B. Price Professor, University of Kentucky October 18, 2007

Globalization is real and is just as real for

Closing Panel: Improving Rural Capital Markets Gary Warren Globalization is real and is just as real for the banking industry, if not more so, than most industries. Information technology advancements

Closing Panel: Improving Rural Capital Markets Gary Warren Globalization is real and is just as real for the banking industry, if not more so, than most industries. Information technology advancements

Evaluation of the European Union s Co-operation with Kenya Country level evaluation

"FICHE CONTRADICTOIRE" Evaluation of the European Union s Co-operation with Kenya Country level evaluation Recommendations Responses of Services: Follow-up (one year later) GENERAL RECOMMENDATIONS 1 Give

"FICHE CONTRADICTOIRE" Evaluation of the European Union s Co-operation with Kenya Country level evaluation Recommendations Responses of Services: Follow-up (one year later) GENERAL RECOMMENDATIONS 1 Give

Remarks of Nout Wellink Chairman, Basel Committee on Banking Supervision President, De Nederlandsche Bank

Remarks of Nout Wellink Chairman, Basel Committee on Banking Supervision President, De Nederlandsche Bank Korea FSB Financial Reform Conference: An Emerging Market Perspective Seoul, Republic of Korea

Remarks of Nout Wellink Chairman, Basel Committee on Banking Supervision President, De Nederlandsche Bank Korea FSB Financial Reform Conference: An Emerging Market Perspective Seoul, Republic of Korea

MENA-OECD WORKING GROUP ON CORPORATE GOVERNANCE

MENA-OECD WORKING GROUP ON CORPORATE GOVERNANCE Rabat, Morocco, 12-13 December 2017 SESSION 1: The business case for corporate governance and the evolution of the concept in the MENA (Middle East and North

MENA-OECD WORKING GROUP ON CORPORATE GOVERNANCE Rabat, Morocco, 12-13 December 2017 SESSION 1: The business case for corporate governance and the evolution of the concept in the MENA (Middle East and North

Index-based Livestock Insurance Project, Mongolia

Index-based Livestock Insurance Project, Mongolia Dr. Jerry Skees President, GlobalAgRisk, Inc. The H.B. Price Professor of Policy and Risk University of Kentucky Slides Prepared in Collaboration with

Index-based Livestock Insurance Project, Mongolia Dr. Jerry Skees President, GlobalAgRisk, Inc. The H.B. Price Professor of Policy and Risk University of Kentucky Slides Prepared in Collaboration with

From managing crises to managing risks: The African Risk Capacity (ARC)

") Page 1 of 7 Home > Topics > Risk Dialogue Magazine > Strengthening food security > From managing crises to managing risks: The African Risk Capacity (ARC) From managing crises to managing risks: The African

Page 1 of 7 Home > Topics > Risk Dialogue Magazine > Strengthening food security > From managing crises to managing risks: The African Risk Capacity (ARC) From managing crises to managing risks: The African

After the Drought: The Impact of Microinsurance on Consumption Smoothing and Asset Protection

After the Drought: The Impact of Microinsurance on Consumption Smoothing and Asset Protection February 1, 2017 Michael R. Carter Sarah A. Janzen Montana State University Ph: (406) 994-3714 sarah.janzen@montana.edu

After the Drought: The Impact of Microinsurance on Consumption Smoothing and Asset Protection February 1, 2017 Michael R. Carter Sarah A. Janzen Montana State University Ph: (406) 994-3714 sarah.janzen@montana.edu

Introduction to risk sharing and risk transfer with examples from Mongolia and Peru

Introduction to risk sharing and risk transfer with examples from Mongolia and Peru Dr. Jerry Skees H.B. Price Professor, University of Kentucky, and President, GlobalAgRisk, Inc. UNFCCC Workshop Lima,

Introduction to risk sharing and risk transfer with examples from Mongolia and Peru Dr. Jerry Skees H.B. Price Professor, University of Kentucky, and President, GlobalAgRisk, Inc. UNFCCC Workshop Lima,

Adjusted Gross Revenue Pilot Insurance Program: Rating Procedure (Report prepared for the Risk Management Agency Board of Directors) J.

J.") Staff Paper Adjusted Gross Revenue Pilot Insurance Program: Rating Procedure (Report prepared for the Risk Management Agency Board of Directors) J. Roy Black Staff Paper 2000-51 December, 2000 Department

Staff Paper Adjusted Gross Revenue Pilot Insurance Program: Rating Procedure (Report prepared for the Risk Management Agency Board of Directors) J. Roy Black Staff Paper 2000-51 December, 2000 Department

Dynamic Field Experiments in Development Economics: Risk Valuation in Morocco, Kenya, and Peru

Dynamic Field Experiments in Development Economics: Risk Valuation in Morocco, Kenya, and Peru Travis J. Lybbert, Francisco B. Galarza, John McPeak, Christopher B. Barrett, Stephen R. Boucher, Michael

Dynamic Field Experiments in Development Economics: Risk Valuation in Morocco, Kenya, and Peru Travis J. Lybbert, Francisco B. Galarza, John McPeak, Christopher B. Barrett, Stephen R. Boucher, Michael

Management response to the recommendations deriving from the evaluation of the Mali country portfolio ( )

") Executive Board Second regular session Rome, 26 29 November 2018 Distribution: General Date: 23 October 2018 Original: English Agenda item 7 WFP/EB.2/2018/7-C/Add.1 Evaluation reports For consideration

Executive Board Second regular session Rome, 26 29 November 2018 Distribution: General Date: 23 October 2018 Original: English Agenda item 7 WFP/EB.2/2018/7-C/Add.1 Evaluation reports For consideration

How to Explain and Use an Insurance Contract

How to Explain and Use an Insurance Contract Insurance contracts, in this case, are agreements between farmers and an insurance company. By signing the contract, the farmer agrees to pay a certain amount

How to Explain and Use an Insurance Contract Insurance contracts, in this case, are agreements between farmers and an insurance company. By signing the contract, the farmer agrees to pay a certain amount

Vulnerability to Poverty and Risk Management of Rural Farm Household in Northeastern of Thailand

2011 International Conference on Financial Management and Economics IPEDR vol.11 (2011) (2011) IACSIT Press, Singapore Vulnerability to Poverty and Risk Management of Rural Farm Household in Northeastern

2011 International Conference on Financial Management and Economics IPEDR vol.11 (2011) (2011) IACSIT Press, Singapore Vulnerability to Poverty and Risk Management of Rural Farm Household in Northeastern

Summary of main findings

IMPACT ASSESSMENT REPORT NUSAF2 - Northern Uganda Social Action Fund 12-13 Project in Moroto Municipality and Nadunget Sub-County Karamoja, Uganda Summary of main findings There is a reduction from % to

IMPACT ASSESSMENT REPORT NUSAF2 - Northern Uganda Social Action Fund 12-13 Project in Moroto Municipality and Nadunget Sub-County Karamoja, Uganda Summary of main findings There is a reduction from % to

The impact of present and future climate changes on the international insurance & reinsurance industry

Copyright 2007 Willis Limited all rights reserved. The impact of present and future climate changes on the international insurance & reinsurance industry Fiona Shaw MSc. ACII Executive Director Willis

Copyright 2007 Willis Limited all rights reserved. The impact of present and future climate changes on the international insurance & reinsurance industry Fiona Shaw MSc. ACII Executive Director Willis

LESSON TWO: Estimating the sales of produce

Making a Budget A Self Study Guide for Members and Staff of Agricultural Cooperatives LESSON TWO: Estimating the sales of produce Objective: In this lesson the committee discuss the estimates of how much

Making a Budget A Self Study Guide for Members and Staff of Agricultural Cooperatives LESSON TWO: Estimating the sales of produce Objective: In this lesson the committee discuss the estimates of how much

Index Insurance Quality and Basis Risk: Evidence from Northern Kenya

Index Insurance Quality and Basis Risk: Evidence from Northern Kenya Nathaniel D. Jensen, 1 Christopher B. Barrett, 2 and Andrew G. Mude 3 Abstract: The number of index insurance pilots in developing countries

Index Insurance Quality and Basis Risk: Evidence from Northern Kenya Nathaniel D. Jensen, 1 Christopher B. Barrett, 2 and Andrew G. Mude 3 Abstract: The number of index insurance pilots in developing countries

Kenya. Toward a National Crop and Livestock Insurance Program SUMMARY OF POLICY SUGGESTIONS OCTOBER Public Disclosure Authorized

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Kenya Toward a National Crop and Livestock Insurance Program SUMMARY OF POLICY SUGGESTIONS

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Kenya Toward a National Crop and Livestock Insurance Program SUMMARY OF POLICY SUGGESTIONS

Public-Private Partnerships for Agricultural Risk Management through Risk Layering

I4 Brief no. 2011-01 April 2011 Public-Private Partnerships for Agricultural Risk Management through Risk Layering by Michael Carter, Elizabeth Long and Stephen Boucher Public and Private Risk Management

I4 Brief no. 2011-01 April 2011 Public-Private Partnerships for Agricultural Risk Management through Risk Layering by Michael Carter, Elizabeth Long and Stephen Boucher Public and Private Risk Management

Policy Implementation for Enhancing Community. Resilience in Malawi

Volume 10 Issue 1 May 2014 Status of Policy Implementation for Enhancing Community Resilience in Malawi Policy Brief ECRP and DISCOVER Disclaimer This policy brief has been financed by United Kingdom (UK)

Volume 10 Issue 1 May 2014 Status of Policy Implementation for Enhancing Community Resilience in Malawi Policy Brief ECRP and DISCOVER Disclaimer This policy brief has been financed by United Kingdom (UK)

Broad and Deep: The Extensive Learning Agenda in YouthSave

Broad and Deep: The Extensive Learning Agenda in YouthSave Center for Social Development August 17, 2011 Campus Box 1196 One Brookings Drive St. Louis, MO 63130-9906 (314) 935.7433 www.gwbweb.wustl.edu/csd

Broad and Deep: The Extensive Learning Agenda in YouthSave Center for Social Development August 17, 2011 Campus Box 1196 One Brookings Drive St. Louis, MO 63130-9906 (314) 935.7433 www.gwbweb.wustl.edu/csd

The Potential and Uptake of Remote Sensing in Insurance: A Review

Remote Sens. 2014, 6, 10888-10912; doi:10.3390/rs61110888 Review OPEN ACCESS remote sensing ISSN 2072-4292 www.mdpi.com/journal/remotesensing The Potential and Uptake of Remote Sensing in Insurance: A

Remote Sens. 2014, 6, 10888-10912; doi:10.3390/rs61110888 Review OPEN ACCESS remote sensing ISSN 2072-4292 www.mdpi.com/journal/remotesensing The Potential and Uptake of Remote Sensing in Insurance: A

Building Household Resilience through Productive Inclusion. Carlo del Ninno, Thomas Bossuroy, Patrick Premand, World Bank

Building Household Resilience through Productive Inclusion Carlo del Ninno, Thomas Bossuroy, Patrick Premand, World Bank Adaptive Social Protection (ASP) 1) Build household resilience, ex ante Household

Building Household Resilience through Productive Inclusion Carlo del Ninno, Thomas Bossuroy, Patrick Premand, World Bank Adaptive Social Protection (ASP) 1) Build household resilience, ex ante Household

FundiFix: exploring a new model for maintenance of rural water supplies

FundiFix: exploring a new model for maintenance of rural water supplies Type: Short Paper (up to 2,000 words) Authors J. Katuva (PhD researcher, Oxford University, UK, Jacob.katuva@spc.ox.ac.uk, +447707248632);

FundiFix: exploring a new model for maintenance of rural water supplies Type: Short Paper (up to 2,000 words) Authors J. Katuva (PhD researcher, Oxford University, UK, Jacob.katuva@spc.ox.ac.uk, +447707248632);

Keynote Speech Seminar on

Keynote Speech Seminar on Development of Productive Economy in order to Support Minapolitan Program Dr. Hendar Deputy Governor of Bank Indonesia Bismillahirrahmanirrahim, Assalamu alaikum warahmatullahi

Keynote Speech Seminar on Development of Productive Economy in order to Support Minapolitan Program Dr. Hendar Deputy Governor of Bank Indonesia Bismillahirrahmanirrahim, Assalamu alaikum warahmatullahi

Environmental Spillovers of the Take-up of Index-Based Livestock Insurance

Environmental Spillovers of the Take-up of Index-Based Livestock Insurance Chris Barrett, Richard Bernstein, Patrick Clark, Carla Gomes, Shibia Mohamed, Andrew Mude, Birhanu Taddesse, and Russell Toth

Environmental Spillovers of the Take-up of Index-Based Livestock Insurance Chris Barrett, Richard Bernstein, Patrick Clark, Carla Gomes, Shibia Mohamed, Andrew Mude, Birhanu Taddesse, and Russell Toth

PRF Insurance: background

Rainfall Index and Margin Protection Insurance Plans 2017 Ag Lenders Conference Garden City, KS October 2017 Dr. Monte Vandeveer KSU Extension Agricultural Economist PRF Insurance: background Pasture,

Rainfall Index and Margin Protection Insurance Plans 2017 Ag Lenders Conference Garden City, KS October 2017 Dr. Monte Vandeveer KSU Extension Agricultural Economist PRF Insurance: background Pasture,

JOHN MORIKIS: SEAN HENNESSY:

JOHN MORIKIS: You ll be hearing from Jay Davisson, our president of the Americas Group, Cheri Pfeiffer, our president of our Diversified Brands Division, Joel Baxter, our president of our Global Supply

JOHN MORIKIS: You ll be hearing from Jay Davisson, our president of the Americas Group, Cheri Pfeiffer, our president of our Diversified Brands Division, Joel Baxter, our president of our Global Supply

Africa RiskView Customisation Review. Terms of Reference of the Customisation Review Committee & Customisation Review Process

Africa RiskView Customisation Review Terms of Reference of the Customisation Review Committee & Customisation Review Process April 2018 1 I. Introduction a. Background African Risk Capacity Agency (ARC

Africa RiskView Customisation Review Terms of Reference of the Customisation Review Committee & Customisation Review Process April 2018 1 I. Introduction a. Background African Risk Capacity Agency (ARC

TRAINING CATALOGUE ON IMPACT INSURANCE Building practitioner skills in providing valuable and viable insurance products

TRAINING CATALOGUE ON IMPACT INSURANCE Building practitioner skills in providing valuable and viable insurance products 2017 Contents of the training catalogue The ILO s Impact Insurance Facility... 3

TRAINING CATALOGUE ON IMPACT INSURANCE Building practitioner skills in providing valuable and viable insurance products 2017 Contents of the training catalogue The ILO s Impact Insurance Facility... 3

Luxembourg High-level Symposium: Preparing for the 2012 DCF

Luxembourg High-level Symposium: Preparing for the 2012 DCF Panel 2: Using aid to help developing countries to promote domestic revenue mobilization 18 October 2011 Contribution by Mr Hans Wollny, Deputy

Luxembourg High-level Symposium: Preparing for the 2012 DCF Panel 2: Using aid to help developing countries to promote domestic revenue mobilization 18 October 2011 Contribution by Mr Hans Wollny, Deputy

Agriculture insurance. Urgent needed actions and recommended Policy change to move Ag-Insurance forward

Agriculture insurance Urgent needed actions and recommended Policy change to move Ag-Insurance forward Contents of the presentation: I. What is the agriculture Insurance? II. Analysis of the Ag-Insurance

Agriculture insurance Urgent needed actions and recommended Policy change to move Ag-Insurance forward Contents of the presentation: I. What is the agriculture Insurance? II. Analysis of the Ag-Insurance

Andrew Goodland RISK MANAGEMENT: THE CASE OF THE LIVESTOCK SECTOR IN MONGOLIA

Andrew Goodland RISK MANAGEMENT: THE CASE OF THE LIVESTOCK SECTOR IN MONGOLIA Outline 1. Brief context nature of risk in Mongolia 2. Conceptual framework for understanding and addressing risk in the agricultural

Andrew Goodland RISK MANAGEMENT: THE CASE OF THE LIVESTOCK SECTOR IN MONGOLIA Outline 1. Brief context nature of risk in Mongolia 2. Conceptual framework for understanding and addressing risk in the agricultural

Cash transfers, impact evaluation & social policy: the case of El Salvador

September 8th, 2016 GPED Forum Vanderbilt University Cash transfers, impact evaluation & social policy: the case of El Salvador The talk aims to present the experience of El Salvador in the implementation

September 8th, 2016 GPED Forum Vanderbilt University Cash transfers, impact evaluation & social policy: the case of El Salvador The talk aims to present the experience of El Salvador in the implementation

Implementing the Expected Credit Loss model for receivables A case study for IFRS 9

Implementing the Expected Credit Loss model for receivables A case study for IFRS 9 Corporates Treasury Many companies are struggling with the implementation of the Expected Credit Loss model according

Implementing the Expected Credit Loss model for receivables A case study for IFRS 9 Corporates Treasury Many companies are struggling with the implementation of the Expected Credit Loss model according

Western Power Distribution: consumerled pension strategy

www.pwc.com Western Power Distribution: consumerled pension strategy Workstream 3: Stakeholder engagement Phase 2 Domestic and Business bill-payers focus groups October 2016 Contents Workstream overview

www.pwc.com Western Power Distribution: consumerled pension strategy Workstream 3: Stakeholder engagement Phase 2 Domestic and Business bill-payers focus groups October 2016 Contents Workstream overview

shocks do not have long-lasting adverse development consequences (Food Security Information Network)

") Submission by the World Food Programme to the Executive Committee of the Warsaw International Mechanism for Loss and Damage on best practices, challenges and lessons learned from existing financial instruments

Submission by the World Food Programme to the Executive Committee of the Warsaw International Mechanism for Loss and Damage on best practices, challenges and lessons learned from existing financial instruments

Measuring Resilience at USAID. Tiffany M. Griffin, PhD

Measuring Resilience at USAID Tiffany M. Griffin, PhD TOPS Knowledge Sharing Meeting Washington DC July 10, 2014 Defining and Conceptualizing Resilience USAID defines resilience as: The ability of people,

Measuring Resilience at USAID Tiffany M. Griffin, PhD TOPS Knowledge Sharing Meeting Washington DC July 10, 2014 Defining and Conceptualizing Resilience USAID defines resilience as: The ability of people,

Active or passive? Tips for building a portfolio

Active or passive? Tips for building a portfolio Jim Nelson: Actively managed funds or passive index funds? It s a common question that many investors and their advisors confront during portfolio construction.

Active or passive? Tips for building a portfolio Jim Nelson: Actively managed funds or passive index funds? It s a common question that many investors and their advisors confront during portfolio construction.

Andrew Goodland INDEX BASED INSURANCE AND DISASTER RISK MANAGEMENT IN MONGOLIA

Andrew Goodland INDEX BASED INSURANCE AND DISASTER RISK MANAGEMENT IN MONGOLIA Brief context of Mongolia livestock sector Mongolia is a country of 2.5 m people and 33 million livestock Mongolia is one

Andrew Goodland INDEX BASED INSURANCE AND DISASTER RISK MANAGEMENT IN MONGOLIA Brief context of Mongolia livestock sector Mongolia is a country of 2.5 m people and 33 million livestock Mongolia is one

SPANISH AGRICULTURAL INSURANCE SYSTEM. ENESA s Approach. Madrid, 9th February

SPANISH AGRICULTURAL INSURANCE SYSTEM ENESA s Approach Madrid, 9th February 2014 1 Paper Outline. 1. Introduction. 2. Objective. 3. Background. 4. Stakeholders. 5. ENESA. 6. Limitations & Advantages. 7.

SPANISH AGRICULTURAL INSURANCE SYSTEM ENESA s Approach Madrid, 9th February 2014 1 Paper Outline. 1. Introduction. 2. Objective. 3. Background. 4. Stakeholders. 5. ENESA. 6. Limitations & Advantages. 7.

ValueWalk Interview With Ravee Mehta Of Nishkama Capital LLC

ValueWalk Interview With Ravee Mehta Of Nishkama Capital LLC ValueWalk Interview With Ravee Mehta Of Nishkama Capital LLC ValueWalk: You re the author of The Emotionally Intelligent Investor: How self-awareness,

ValueWalk Interview With Ravee Mehta Of Nishkama Capital LLC ValueWalk Interview With Ravee Mehta Of Nishkama Capital LLC ValueWalk: You re the author of The Emotionally Intelligent Investor: How self-awareness,

Solvency II is a huge step forward for policyholder protection and the implementation of a true single market for insurers and reinsurers in the EU.

Interview with Manuela Zweimueller, Head of Policy Department of EIOPA European Insurance and Occupational Pensions Authority with Svijet Osiguranja by Natasa Gajski November 2016 1. The implementation

Interview with Manuela Zweimueller, Head of Policy Department of EIOPA European Insurance and Occupational Pensions Authority with Svijet Osiguranja by Natasa Gajski November 2016 1. The implementation

Susan S Bies: Lessons to be re-learned from recent breakdowns in corporate accounting

Susan S Bies: Lessons to be re-learned from recent breakdowns in corporate accounting Remarks by Ms Susan S Bies, Member of the Board of Governors of the US Federal Reserve System, before the Institute

Susan S Bies: Lessons to be re-learned from recent breakdowns in corporate accounting Remarks by Ms Susan S Bies, Member of the Board of Governors of the US Federal Reserve System, before the Institute

Investment for development: Investing in the Sustainable Development Goals: An Action Plan

TRADE AND DEVELOPMENT BOARD 61 st Session Agenda Item 9 Investment for development: Investing in the Sustainable Development Goals: An Action Plan Geneva, 17 September 2014 Statement by James Zhan Director

TRADE AND DEVELOPMENT BOARD 61 st Session Agenda Item 9 Investment for development: Investing in the Sustainable Development Goals: An Action Plan Geneva, 17 September 2014 Statement by James Zhan Director

The ERC Situation and Response Analysis Framework Reinforcing Institutional Capacity for Timely Food Security Emergency Response to Slow Onset Crises

The ERC Situation and Response Analysis Framework Reinforcing Institutional Capacity for Timely Food Security Emergency Response to Slow Onset Crises at Scale ERC SRAF Guiding Principles Timing is Critical:

The ERC Situation and Response Analysis Framework Reinforcing Institutional Capacity for Timely Food Security Emergency Response to Slow Onset Crises at Scale ERC SRAF Guiding Principles Timing is Critical:

Weathering the Risks: Scalable Weather Index Insurance in East Africa

Weathering the Risks: Scalable Weather Index Insurance in East Africa Having enough food in East Africa depends largely on the productivity of smallholder farms, which in turn depends on farmers ability

Weathering the Risks: Scalable Weather Index Insurance in East Africa Having enough food in East Africa depends largely on the productivity of smallholder farms, which in turn depends on farmers ability

The role of index-based triggers in social protection shock response

April 2015 Report The role of index-based triggers in social protection shock response Francesca Bastagli and Luke Harman The inclusion of index-based triggers in social protection programmes is one of

April 2015 Report The role of index-based triggers in social protection shock response Francesca Bastagli and Luke Harman The inclusion of index-based triggers in social protection programmes is one of

PZU - presentation of financial results for Q1 2016: 12 May 2016

PZU - presentation of financial results for Q1 2016: 12 May 2016 Piotr Wiśniewski Manager of the Investor Relations Team at the PZU Group: Good morning. I would like to welcome you to the meeting devoted

PZU - presentation of financial results for Q1 2016: 12 May 2016 Piotr Wiśniewski Manager of the Investor Relations Team at the PZU Group: Good morning. I would like to welcome you to the meeting devoted

Lessons learnt from Agriculture Projects. Microinsurance Innovation Facility International Labour Organization 13 June 2012, Rome

Lessons learnt from Agriculture Projects Microinsurance Innovation Facility International Labour Organization 13 June 2012, Rome Microinsurance Innovation Facility in action Challenges to viability q Why

Lessons learnt from Agriculture Projects Microinsurance Innovation Facility International Labour Organization 13 June 2012, Rome Microinsurance Innovation Facility in action Challenges to viability q Why

CLIENT VALUE & INDEX INSURANCE

CLIENT VALUE & INDEX INSURANCE TARA STEINMETZ, ASSISTANT DIRECTOR FEED THE FUTURE INNOVATION LAB FOR ASSETS & MARKET ACCESS Fairview Hotel, Nairobi, Kenya 4 JULY 2017 basis.ucdavis.edu Photo Credit Goes

CLIENT VALUE & INDEX INSURANCE TARA STEINMETZ, ASSISTANT DIRECTOR FEED THE FUTURE INNOVATION LAB FOR ASSETS & MARKET ACCESS Fairview Hotel, Nairobi, Kenya 4 JULY 2017 basis.ucdavis.edu Photo Credit Goes

Making Index Insurance Work for the Poor

Making Index Insurance Work for the Poor Xavier Giné, DECFP April 7, 2015 It is odd that there appear to have been no practical proposals for establishing a set of markets to hedge the biggest risks to

Making Index Insurance Work for the Poor Xavier Giné, DECFP April 7, 2015 It is odd that there appear to have been no practical proposals for establishing a set of markets to hedge the biggest risks to

Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies

General Stress Testing Guidance for Insurance Companies") Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies 1 INTRODUCTION AND PURPOSE The business of insurance is

Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies 1 INTRODUCTION AND PURPOSE The business of insurance is