10/10/2018. AB 1200 Oversight Basics. AB1200 Oversight Basics

|

|

|

- Mervyn Cornelius Webster

- 5 years ago

- Views:

Transcription

1 AB 1200 Oversight Basics BASC Fall Conference AB1200 Oversight Basics Presented by: Chris Lombardo, Orange County Keith Crafton, Los Angeles County Tom Cassida, San Bernardino County Dean West, Orange County Priscilla Quinn, Kern County Kate Lane, Marin County 2 AB 1200 Oversight Basics Prepared with assistance from: Joy Massey, Nevada Sherry Tygart, Nevada Kathryn Rusk, San Joaquin Michelle Giacomini, FCMAT Denice Cora, Santa Barbara 3 1

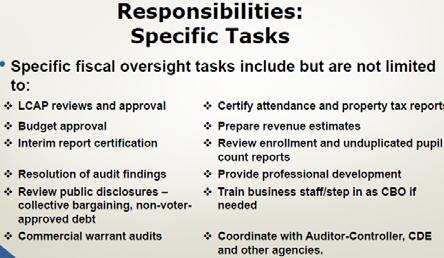

2 Agenda Understanding Our Purpose and Responsibilities Knowing Our Districts AB 1200 Fiscal Review Average Daily Attendance Trend Analysis/Criteria and Standards Multi Year Projections How do we Accomplish the Reviews? 4 Understanding Our Purpose and Responsibilities 5 Responsibilities of County Superintendents The California County Superintendents Education Services Association (CCSESA) has identified these general categories of responsibilities for County Superintendents: county superintendents/ Educating specific student populations (i.e., special education and disenfranchised youth) Monitoring and oversight of student academic environment Monitoring and oversight for district fiscal stability Providing academic support and assistance to districts and their schools Providing direct services to small school districts Implementing regional support activities to assist district and school staffs 6 2

3 Responsibilities of COE External Finance Departments Following is a sampling of how COE s describe their External Finance purpose and responsibilities. Note the various ways the purpose and responsibilities are described, beyond the technical aspects

4

5 KNOWING OUR DISTRICTS 13 Know the District Before we begin the fiscal review, we need to understand the district context: Board Characteristics Superintendent, CBO and other administrators Budget philosophy and accuracy Growing/declining enrollment Facilities Issues Fiscal Position Trust Level

6

7

8 22 THE AB 1200 FISCAL REVIEW 23 AB 1200 Fiscal Review Be Prepared document your review District A District B District C District D Check in budget/interim/ua DAT files and hard copies X X X X Load DAT files into a data analysis tool X X X X Create LCFF Calculator for each LEA X X X X Review budget/interim reports using a checklist X X X X FCMAT Fiscal Health Risk Analysis X X X X LCAP/Budget Verification X X X Phone conversation with each LEA (CBO or Director) X X Draft COE Letters for each LEA X Create a one page profile to recap the key points of your analysis X X X X 24 8

9 AB 1200 Fiscal Review Be prepared: A solid review process that is well documented and easily accessible is invaluable when issues arise. The remaining segments of this morning s presentation are devoted to the critical areas of financial and budgetary review we perform If you need a tool to help you in your review reach out to your colleagues! 25 AVERAGE DAILY ATTENDANCE 26 Average Daily Attendance Overview Average Daily Attendance is reported at P 1, P 2, and Annual P 2 and Annual ADA can be revised Prioritize how to calculate LCFF Funded ADA 27 9

Software Reports Your COE attendance staff should have access to these reports You may even have a spreadsheet or database Note: this is where you will")

10 Funded ADA - Where do you start? Principal Apportionment Data Collection (PADC) Software Reports Your COE attendance staff should have access to these reports You may even have a spreadsheet or database Note: this is where you will find the most up to date information Principal Apportionment Exhibits LCFF Calculator 28 CDE s Principal Apportionment Exhibits Principal Apportionment e.g Second Period (P 2) Apportionment Click on Funding Exhibits Second Principal Apportionment Choose the correct Period, then select School District, and select School District ADA

2.")

11 FCMAT LCFF Calculator Go to the District MYP Data worksheet Displays LCFF Funded ADA for through Greater of Current or Prior Year ADA Add these two amounts together for the current year and compare to the prior year total: 1. Regular ADA (P 2) 2. Extended Year Special Education (Annual) If the district ADA declines year over year, they will be funded using the prior year Regular and Extended Year Special Education ADA Don t forget to include the impact of the charter net shift to prior year ADA [EC (a)(2)] 32 Attendance School District (P-2) You get the Regular ADA from the P 2 Attendance School District form. Regular ADA includes opportunity classes, home and hospital, special day class, and continuation education

12 Attendance School District (Annual) The Annual report is where you ll find: Extended Year Special Education, Special Education Nonpublic, Extended Year Special Education Nonpublic, and Community Day School ADA. 34 Always Include Current Year ADA: After you have determined the greater of current year or prior year, you must now add the following items: Special Education Nonpublic (Annual) Extended Year Special Education Nonpublic (Annual) Community Day School (Annual) Attendance for District Funded County Programs County Community Schools (P 2) Special Education Special Day Class (P 2) Extended Year Special Education (Annual) 35 Calculation of LCFF Funded ADA - Example 36 12

13 TREND ANALYSIS/CRITERIA AND STANDARDS 37 What are the Criteria and Standards? LEAs are required (EC 33129) to use the Criteria and Standards adopted by the State Board of Education (SBE) in developing their budgets and managing their expenditures. In addition, Criteria and Standards are used to monitor the fiscal stability of LEAs. 38 Criteria and Standards Budget Criteria and Standards 1. Average Daily Attendance 2. Enrollment 3. ADA to Enrollment 4. LCFF Revenue 5. Salaries and Benefits 6. Other Revenue and Expenditures 7. Facilities Maintenance 8. Deficit Spending 9. Fund Balance 10. Reserves Supplemental Information 1. Contingent Liabilities 2. Use of one time revenues for ongoing expenditures 3. Use of ongoing revenues for one time expenditures 4. Contingent Revenues 5. Contributions 6. Long term Commitments 7. Unfunded Liabilities 8. Status of Labor Agreements 9. Local Control and Accountability Plan (LCAP) 10. LCAP Expenditures 39 13

14 Criteria and Standards - Budget Fiscal Indicators 1. Do cash flow projections show that the district will end the budget year with a negative cash balance in the general fund? 2. Is the system of personnel position control independent from the payroll system? 3. Is enrollment decreasing in both the prior year and budget year? 4. Are new charter schools operating in district boundaries that impact the district s enrollment, either in the prior fiscal year or budget year? 5. Does the district provide uncapped (100% employer paid) health benefits for current or retired employees? 6. Is the district s financial system independent of the county office system? 7. Have there been personnel changes in the superintendent or chief business officer positions within the last 12 months? 40 Average Daily Attendance Funded ADA For the budget year and the three prior years Drives LCFF transition entitlements When districts make revisions, you have to go back and recalculate funded ADA Funded ADA is displayed on SACS Form A 41 Enrollment District student enrollment is displayed for the three prior years, the budget year, and the two subsequent years Questions: Does current year enrollment match CALPADS enrollment? Do you know why the enrollment is growing, declining, or staying flat? Does the district have a demographer? Are enrollment projections optimistic, most likely, or conservative? 42 14

15 ADA to Enrollment The C&S shows a three year historical average for ADA/enrollment. The budget year and two subsequent fiscal years are compared to the historical average plus 0.5%. Questions: Why is the ADA/Enrollment ratio significantly different from the historical average? Do you quantify the ADA/Enrollment compared to the historical average in dollars? 43 ADA and Enrollment 6, % 97.0% 96.8% 6, % 96.7% 96.7% 98.0% 97.0% 6, % 6, % 6, % 6, % 6, % 6,050 6,000 6,344 6,142 6,189 6,337 6,176 6,200 6,334 6,146 6,193 6,356 6,146 6,163 6,356 6,146 6,163 6,356 6,146 6, % 90.0% Enrollment P 2 ADA LCFF Funded ADA ADA to Enrollment Ratio 44 LCFF Revenue The C&S displays LCFF broken down by change in population and by the change in funding level. LCFF Sources is the largest revenue source for school districts. County offices must verify LCFF entitlements in the budget year and subsequent fiscal years

16 LCFF Verification LCFF Entitlement OCDE LCFF Estimate w/ 3.7%/2.57%/2.67% 303,545, ,091, ,851, ,553,411 District LCFF Estimate 304,350, ,411, ,148, ,872,585 Difference (OCDE less District Estimate) (805,696) 1,679,863 1,702,873 1,680,826 Questions: What LCFF assumptions did the district use? Have you included LCFF Transfers? If the District estimate is higher than the COE estimate, what is the contingency plan? 46 Salaries and Benefits The C&S computes a three year historical average for unrestricted salaries and benefits as a percentage of unrestricted expenditures. If this ratio is too high, consider looking at the district s budgeting practices to identify the cause. Compare prior year unaudited actuals to the current budget or interim projection data. 47 Facilities Maintenance This is directly related to the Routine Restricted Maintenance (RRM) contribution requirement in Education Code For the to fiscal years, the required minimum amount to be deposited into the account shall be the greater of the following amounts: The lesser of three percent (3%) of the general fund expenditures for that fiscal year or the amount that the school district deposited into the account in the fiscal year. Two percent of the total general fund expenditures of the applicant school district for that fiscal year. Proposition 51 contains a provision to apportion funds as the Education Code read on January 1, (a) The RRMA requirement on January 1, 2015 for fiscal years beyond was to deposit 3% of total general fund expenditures. (b) Therefore, in the fiscal year after it receives Proposition 51 funding, the district should deposit 3% of the total general fund expenditures

17 Deficit Spending Deficit spending occurs when total revenues (objects ) less total expenditures (objects ) results in an amount less than zero. For AB 1200 purposes, we focus on the unrestricted general fund. Questions: Does the district have a structural deficit? What is the cause of the deficit spending? Is the district spending down fund balance as part of a longterm plan? 49 Deficit Spending Examples Example #1 Example #2 This school district is projecting significant deficit spending. A closer look at revenue and expenditure budget assumptions may tell a different story. This district was experiencing planned deficits in prior years. Significant enrollment growth coupled with healthy COLAs result in MYP surpluses. 50 Reserves C&S displays general fund unrestricted reserves as the sum of: General Fund: Stabilization Arrangements 9750, Reserve for Economic Uncertainties (REU) 9789, and Unassigned/Unappropriated 9790 Special Reserve Fund: Stabilization Arrangements 9750, Reserve for Economic Uncertainties (REU) 9789, and Unassigned/Unappropriated 9790 Always divide the reserves by the total general fund expenditures + transfers out + other uses to compute the unrestricted reserve %

(2)(B)&(C) The governing board of a school district that proposes to adopt a budget that includes a combined assigned and unassigned ending fund balance in excess of the minimum recommended")

18 Reserve Requirement New reserve reporting requirements E.C (a)(2)(B)&(C) The governing board of a school district that proposes to adopt a budget that includes a combined assigned and unassigned ending fund balance in excess of the minimum recommended reserve for economic uncertainties shall, at the Budget Adoption public hearing, provide: 1. The minimum recommended reserve for economic uncertainties; 2. The combined assigned and unassigned ending fund balances that are in excess of the minimum recommended reserve for economic uncertainties for each fiscal year identified in the budget; and 3. A statement of reasons to substantiate the need for reserves that are higher than the minimum recommended reserve. 52 Unrestricted Reserves We generally look at the General Fund Reserve for Economic Uncertainties and the Unassigned fund balance. Don t forget about Committed and/or Assigned fund balance. 53 Contributions/Transfer In/Transfers Out What is happening to contributions, transfers in, and transfers out? Any spikes? Does it match the MYP? Why are the contributions changing from year to year? What s the impact of transfers in/out on deficit spending? 54 18

19 Long Term Commitments Capital leases, certificates of participation, supplemental early retirement programs, and general obligation bonds Is the district properly budgeting debt service payments? Did they forget to budget payments? Is anything falling off in the budget year or two subsequent years? Do you have debt service schedules to compare against? 55 Status of Labor Agreements C&S S8A/S8B/S8C displays useful information related to: a. Status of negotiations for certificated and classified b. Certificated FTEs c. Cost of 1% d. Salary schedule increases e. Health and welfare benefits f. Step and column g. Attrition 56 BREAK 57 19

20 Multi Year Projections 58 What is a Multiyear Financial Projection (MYP)? A plan that presents financial estimates of programs in tabular form for a period of years. The data in the plan should be organized along the lines of the program structure. These estimates show the future financial impact of current decisions. Source: content/uploads/sites/4/2015/01/fiscal Oversight Guide 2014 final interactive.pdf 59 What is a Multiyear Financial Projection (MYP)? At minimum, the MYP must include current year and subsequent two year s projection of the General Fund operating statement Unrestricted, Restricted, and Combined Revenues, expenditures, and by major object Fund balances Various acceptable formats: SACS software Form MYP Spreadsheets FCMAT Budget Explorer soon to be replaced with Projection Pro. Have you signed up for training? 60 20

21 Why Are MYPs Important? A district s fiscal solvency depends on accurate MYP development; and County Superintendents are required to monitor and make determinations regarding each district s ability to meet its multiyear financial commitments, providing support/intervention as needed. A careful analysis of a district s MYP is critical to this oversight role! 61 COE Responsibilities - MYPs Adopted Budgets: Due to the COE five days after adoption or by July 1, whichever occurs first (EC 42127(a)(2)(A)). EC 42127(c)(2) requires that the County Superintendent: Determine whether the adopted budget will allow the district to meet its financial obligations during the fiscal year and is consistent with a financial plan that will enable the school district to satisfy its multiyear financial commitments. 62 COE Responsibilities - MYPs Adopted Budgets: EC 42127(c)(2) cont: The county superintendent shall review and consider studies, reports, evaluations, or audits that contain evidence that the district is showing fiscal distress. The county superintendent shall either conditionally approve or disapprove a budget that does not provide adequate assurance that the school district will meet its current and future obligations and resolve any problems identified in studies, reports, evaluations, or audits described in this paragraph

22 COE Responsibilities - MYPs Interim Reports: Districts certify interim reports and file with County Superintendent. [EC 42310] 1 st Interim: Covers financial and budgetary status of the district through October nd Interim: Covers financial and budgetary status of the district through January 31. Must be approved by the district s governing board and submitted to County Superintendent no later than 45 days after the close of the reporting period. 64 Interim Report Certifications Positive Certification Assigned to any school district that, based upon current projections, will meet its financial obligations for the current fiscal year and subsequent two fiscal years. Qualified Assigned Certification to any school district that, based upon current projections, may not meet its financial obligations for the current fiscal year or two subsequent fiscal years. Negative Negative Certification Assigned to any school district that, based upon current projections, will be unable to meet its financial obligations for the remainder of the fiscal year or the subsequent fiscal year. EC 42131(a)(1) 65 Interim Report Certifications, cont. Interim Reports: County Superintendent may change the certification and, no later than 75 days after the close of the period being reported, shall provide notice of that action to the governing board of the school district and to the Superintendent. [EC 42131(a)(2)] 66 22

23 MYP Analysis More than Budgets and Interims Lack of Going Concern [EC ] Collective Bargaining Agreements: [EC 42142, Govt. Code , ] Non Voter Approved Debt Reviews [EC 17150, ] Ongoing Fiscal Health Risk Assessments 67 PANEL DISCUSSION Has your COE changed a district s certification? Reason for consideration Timelines Positive Budget If qualified or negative at second interim what happens at budget adoption? 68 How Do We Accomplish the Reviews? 69 23

24 Budget Assumptions! Obtain budget assumptions from the District Local Control Funding Formula (LCFF) Other revenues Cost of living adjustment (COLA) Categorical COLAs Enrollment Lottery Unduplicated pupil count Mandate Block Grant Average daily attendance by grade span One time funds Property Taxes LCFF Transfers Class Size Penalties 70 Budget Assumptions, con t. Expenditures Average teacher salary Certificated and Classified Salaries Step and column Health and welfare Staffing (adjustments for growth or decline) projections for 3 years K 3 Grade Span Adjustment progress Other Adjustments Budget Reductions LCAP support Other Financing Sources/Uses Contributions Transfers In Transfer Out Other Debt Issuance Sale of surplus property 71 MYP Reviews: Start at the Beginning Review the district s General Fund information (Form 01) in detail. When you understand the story being told in Form 01, you are ready to analyze the MYP

25 Tips for Reviewing the MYP Verify the budget assumptions that were used to develop the MYP. Does the budget reflect pension increases? Does the data for the budget year match SACS Form 01? Is there negative ending balance on the restricted MYP? Be sure to ask for details if the district uses Other Adjustments for certificated, classified or a catch all for total expenditures. Are collective bargaining agreements reflected in the MYP? 73 MYP Reviews - Revenues Review LCFF Calculator Summary Pages Review estimates of COLA, gap funding, ADA projections, unduplicated pupil count, one time revenues, revenues unique to certain districts (NSS, Basic Aid, Impact Aid) Use trend analyses to help determine reasonableness. Simple or Elaborate Information is critical 74 MYP Reviews Revenues, cont. One time revenues have they been removed for subsequent years? Review audit findings for potential impacts to revenues

26 MYP Reviews Revenues, cont. Transfers in from Reserves to support deficit spending or one time purchase Check the out years for changes and explanations Confirm contributions to Restricted Decreasing or Increasing why? If a restricted revenue stream has been declining, has the decline and the corresponding contribution from unrestricted been projected? 76 MYP Revenues A1. LCFF sources increase by 2.67% using a COLA of 2.57% and Gap funding of 100% A2. Federal revenues decrease by 2.55% due to elimination of Title 1 carryover A3. Other state revenues are projected to decrease by 34.46% due to elimination of one-time mandated costs reimbursement MYP Reviews - Expenditures Salaries/Benefits: Compare to prior year actuals, checking for: 1% to 2% increases for step and column Statutory benefit increases (Pension Increases) H&W benefits STRS/PERS increases Costs for multiyear collective bargaining agreements Adjustments corresponding to story of enrollment/staffing increases or decreases 78 26

27 MYP Reviews Expenditures, cont. Are one time expenditures in/out? Debt: Are COP or other debt payments budgeted? Check Audit Report Review other funds for possible impact to the General Fund. Review transfers out and/or capital outlay One time? Short term support for specific program? Ongoing support for programs such as child development, child nutrition, or deferred maintenance? Do projections for supplies, services, capital outlay and other expenditures appear reasonable? Does the budget include sufficient expenditures to support LCAP goal and expenditures. 79 MYP Expenditures Other adjustments New School Transfer Out Reduction in the amount of Deferred Maintenance? 80 MYP Expenditures, cont. Other adjustments Declining enrollment Employee Benefits Increasing while salaries decreasing? 81 27

= Financial System Beginning and ending fund balances Correctly stated Reserve for Economic Uncertainties Minimum standard met Components of ending fund balances for each year")

28 MYP Reviews Ending Fund Balances and Reserves SACS Reports (.dat file) = Financial System Beginning and ending fund balances Correctly stated Reserve for Economic Uncertainties Minimum standard met Components of ending fund balances for each year Nonspendable / Restricted / Committed / Assigned 82 MYP Reviews Ending Fund Balances and Reserves, cont. Deficit spending? Know its root cause(s)! Unrestricted / restricted funds One time expenditures Planned spending of certain reserves Are operational expenditures exceeding projected revenues Analysis of unrestricted and restricted ending fund balances Both should be positive Is the restricted fund balance growing? Are either the unrestricted or restricted fund balance negative? MYP Reviews Ending Fund Balances and Reserves, cont. 28

29 Review Technical Notes If non material technical inaccuracies were noted in the COE review, you may want to summarize those findings for district staff, and suggest recommendations for future consideration. COUNTY OFFICE OF EDUCATION TECHNICAL CORRECTIONS AND RECOMMENDATIONS REVIEW DISTRICT: ABC ELEMENTARY LOCAL CONTROL AND ACCOUNTABILITY PLAN (LCAP): Page 10, Goal 1, Action/Services $5,000 of unrestricted materials are shown in support of this goal, however it appears that these materials will be paid from restricted funds (Title 1, Resource 3010). Please review. ADOPTED BUDGET: Form 01, Objects 8089 and 8691, pages 5 and 10 Non-Revenue Limit (50%) Adjustment between objects 8089 and 8691should net to zero. Please review. Although the amount is immaterial for this district, please make note of the intended reporting of these two object codes for future use, in accordance to CSAM Procedure How do we do the Reviews? Most COEs have review checklists see FCMAT COE Procedure Manual for more Beyond the SACS Reports Budget assumptions Narratives Trend analysis Community Televised and/or online Board Meetings 86 Budget/Interim Review Tools COE Fiscal Procedure Manual content/uploads/sites/4/2018/02/coe manual 2018 final.pdf Sample Checklists and Tools CASBO Workshops and Annual Conference Vendor materials Your COE friends here in this room! 87 29

30 Unaudited Actuals Too! Estimated Actuals compared to Unaudited Actuals MOEs SEMA / SEMB / NCMOE Form CEA (Current Expense Formula / Minimum Classroom Compensation) Form PCR (Program Cost Report) Indirect Cost Rate 88 Other Reports Audit Reports Adjustments and findings AB 2756 Fiscal Distress Reports/Studies/Evaluations/Audits AB 2197 Non Voter Approved Debt Disclosure Cash Flow Reports Other District Intangibles Culture Budget philosophy Staff Leadership Community 90 30

31 Summary There are numerous factors impacting the AB 1200 Process Tangible Factors Is the budget and MYP reasonable? Are the major components realistic? Are reserves adequate? Intangible Factors Budget philosophy, staff, leadership, community 91 THANK YOU 92 31

AB 1200 INTERACTIONS WITH DISTRICTS

AB 1200 INTERACTIONS WITH DISTRICTS Tools, Techniques, Tips Presented by the: External Services Subcommittee (ESSCO) of BASC/CCSESA October 12 and 17, 2016 1 Presenters & Contributors Sherry Beatty, Solano

AB 1200 INTERACTIONS WITH DISTRICTS Tools, Techniques, Tips Presented by the: External Services Subcommittee (ESSCO) of BASC/CCSESA October 12 and 17, 2016 1 Presenters & Contributors Sherry Beatty, Solano

Fiscal Health Risk Analysis Key Fiscal Indicators for K-12 Districts

Fiscal Health Risk Analysis Key Fiscal Indicators for K-12 Districts The Fiscal Crisis and Management Assistance Team (FCMAT) has developed the Fiscal Health Risk Analysis as a management tool to evaluate

Fiscal Health Risk Analysis Key Fiscal Indicators for K-12 Districts The Fiscal Crisis and Management Assistance Team (FCMAT) has developed the Fiscal Health Risk Analysis as a management tool to evaluate

LCFF LCAP. Local Control Accountability Plan

June 2, 2015 LCFF Local Control Funding Formula LCAP Local Control Accountability Plan Expenditures based on District experience, and LCAP projections. Revenue estimates based on Governor s May Budget

June 2, 2015 LCFF Local Control Funding Formula LCAP Local Control Accountability Plan Expenditures based on District experience, and LCAP projections. Revenue estimates based on Governor s May Budget

FCMAT LCFF Calculator

FCMAT LCFF Calculator CCSA Conference 2017 LCFF Calculator v17.2 Presented by FCMAT Staff: Andrea Dodson Intervention Specialist 1 What is the Local Control Funding Formula? Year 1: 2013-14 Year 2: 2014-15

FCMAT LCFF Calculator CCSA Conference 2017 LCFF Calculator v17.2 Presented by FCMAT Staff: Andrea Dodson Intervention Specialist 1 What is the Local Control Funding Formula? Year 1: 2013-14 Year 2: 2014-15

State Budget Message

1 2016-17 State Budget Message Governor Brown Advises caution and to be prepared for the next recession. LCFF (Local Control Funding Formula) is projected to be at 95.7% of target or full funding. At full

1 2016-17 State Budget Message Governor Brown Advises caution and to be prepared for the next recession. LCFF (Local Control Funding Formula) is projected to be at 95.7% of target or full funding. At full

Millbrae Elementary School District First Interim for Fiscal Year Board of Trustees

Millbrae Elementary School District First Interim for Fiscal Year 2016-2017 Board of Trustees Frank Barbaro Denis Fama Lynne Ferrario Maggie Musa D. Don Revelo Administration Vahn Phayprasert, Superintendent

Millbrae Elementary School District First Interim for Fiscal Year 2016-2017 Board of Trustees Frank Barbaro Denis Fama Lynne Ferrario Maggie Musa D. Don Revelo Administration Vahn Phayprasert, Superintendent

Natomas Unified School District

Natomas Unified School District : Item Inspector Natomas Unified School District Jun 25, 2014 : Regular Board Meeting : XIV. ACTION ITEMS c. Approve the District's 2014-15 Proposed Budget [Status: Completed]

Natomas Unified School District : Item Inspector Natomas Unified School District Jun 25, 2014 : Regular Board Meeting : XIV. ACTION ITEMS c. Approve the District's 2014-15 Proposed Budget [Status: Completed]

Los Gatos Union School District Proposed Budget and Multi-year Projection. Narrative

Los Gatos Union School District Proposed Budget and Multi-year Projection Public Hearing June 11, 2018 Adoption June 13, 2018 Revised Narrative to Proposed Budget (revisions in italics) Narrative 2018-2019

Los Gatos Union School District Proposed Budget and Multi-year Projection Public Hearing June 11, 2018 Adoption June 13, 2018 Revised Narrative to Proposed Budget (revisions in italics) Narrative 2018-2019

Yancy Hawkins, Assistant Superintendent - Business & Operations Nancy Walker, Director of Fiscal Services

N O V A T O U N I F I E D Business Services S C H O O L D I S T R I C T TO: FROM: Board of Trustees Yancy Hawkins, Assistant Superintendent - Business & Operations Nancy Walker, Director of Fiscal Services

N O V A T O U N I F I E D Business Services S C H O O L D I S T R I C T TO: FROM: Board of Trustees Yancy Hawkins, Assistant Superintendent - Business & Operations Nancy Walker, Director of Fiscal Services

Table of Contents. Fiscal Oversight

Table of Contents Section 700 Unaudited Actuals... 700-1 Overview... 700-1 Key Reminders... 700-1 Required Forms... 700-2 Form A - Average Daily Attendance... 700-3 Form A Tying to the LCFF Calculator...

Table of Contents Section 700 Unaudited Actuals... 700-1 Overview... 700-1 Key Reminders... 700-1 Required Forms... 700-2 Form A - Average Daily Attendance... 700-3 Form A Tying to the LCFF Calculator...

RE: Local Control Accountability Plans and Adopted Budget Fiscal Year

Denis Fama President, Governing Board Millbrae Elementary School District 555 Richmond Drive Millbrae, CA 94030-1600 RE: Local Control Accountability Plans and Adopted Budget Fiscal Year 2014-15 Dear Mr.

Denis Fama President, Governing Board Millbrae Elementary School District 555 Richmond Drive Millbrae, CA 94030-1600 RE: Local Control Accountability Plans and Adopted Budget Fiscal Year 2014-15 Dear Mr.

2016/17 Budget Development Presentation #1. Board of Trustees Meeting February 9, 2016

2016/17 Budget Development Presentation #1 Board of Trustees Meeting February 9, 2016 LCFF Funding Trends 2016/17 Budget Development Budget Guidelines Budget Assumptions Budget Calendar 2 3 Local Control

2016/17 Budget Development Presentation #1 Board of Trustees Meeting February 9, 2016 LCFF Funding Trends 2016/17 Budget Development Budget Guidelines Budget Assumptions Budget Calendar 2 3 Local Control

County Superintendent s Role for Fiscal Oversight

County Superintendent s Role for Fiscal Oversight AB 1200 Fall Conference Ventura and Yolo COE October 2017 Michael Fine, CEO FCMAT Adapted from CCSESA 2 Prior to AB 1200 Counties reviewed and approved

County Superintendent s Role for Fiscal Oversight AB 1200 Fall Conference Ventura and Yolo COE October 2017 Michael Fine, CEO FCMAT Adapted from CCSESA 2 Prior to AB 1200 Counties reviewed and approved

Action Item. Stephen Dickinson, Assistant Superintendent Administrative Services

Action Item TO: PREPARED BY: PRESENTED BY: Board of Trustees and Superintendent of Schools Patsy Thomas, Director Fiscal Services Stephen Dickinson, Assistant Superintendent Administrative Services BOARD

Action Item TO: PREPARED BY: PRESENTED BY: Board of Trustees and Superintendent of Schools Patsy Thomas, Director Fiscal Services Stephen Dickinson, Assistant Superintendent Administrative Services BOARD

TAMALPAIS UNION HIGH SCHOOL DISTRICT Adopted Budget Report and Multiyear Fiscal Projection

TAMALPAIS UNION HIGH SCHOOL DISTRICT 2015-2016 Adopted Budget Report and Multiyear Fiscal Projection June 23, 2015 Table of Contents Governor s Revised State Budget... 1 2014-15 TUHSD Primary Budget Components...

TAMALPAIS UNION HIGH SCHOOL DISTRICT 2015-2016 Adopted Budget Report and Multiyear Fiscal Projection June 23, 2015 Table of Contents Governor s Revised State Budget... 1 2014-15 TUHSD Primary Budget Components...

BUDGET ADOPTION CHECKLIST

2015 16 BUDGET ADOPTION CHECKLIST DISTRICT: DATE RECEIVED: WORKING ROLL: DATE J# BUDGET/LCAP PUBLIC HEARING: Xsfr Detail BUDGET/LCAP ADOPTION DATE: REVIEWED: FA: MODEL: YEAR NUMBER APPROVED ROLL: DATE

2015 16 BUDGET ADOPTION CHECKLIST DISTRICT: DATE RECEIVED: WORKING ROLL: DATE J# BUDGET/LCAP PUBLIC HEARING: Xsfr Detail BUDGET/LCAP ADOPTION DATE: REVIEWED: FA: MODEL: YEAR NUMBER APPROVED ROLL: DATE

Board of Education Budget Adoption June 28, 2016

SAN DIEGO UNIFIED SCHOOL DISTRICT Board of Education 2016-17 Budget Adoption June 28, 2016 Presentation Agenda Opening Remarks Local Control Funding Formula (LCFF) Multi-Year Assumptions 2016-17 Budget

SAN DIEGO UNIFIED SCHOOL DISTRICT Board of Education 2016-17 Budget Adoption June 28, 2016 Presentation Agenda Opening Remarks Local Control Funding Formula (LCFF) Multi-Year Assumptions 2016-17 Budget

Twin Rivers Unified School District 2018/19 ADOPTED BUDGET

Twin Rivers Unified School District 2018/19 ADOPTED BUDGET Presented to the Board of Trustees For Approval June 26, 2018 By Kate Ingersoll, Executive Director Fiscal Services Agenda The Budget Reporting

Twin Rivers Unified School District 2018/19 ADOPTED BUDGET Presented to the Board of Trustees For Approval June 26, 2018 By Kate Ingersoll, Executive Director Fiscal Services Agenda The Budget Reporting

2016/2017 SECOND INTERIM REPORT

2016/2017 SECOND INTERIM REPORT Golden Valley Unified School District March 14, 2017 What is 2 nd Interim Reporting? The Second Interim Budget report is a snapshot in time of the local educational agency

2016/2017 SECOND INTERIM REPORT Golden Valley Unified School District March 14, 2017 What is 2 nd Interim Reporting? The Second Interim Budget report is a snapshot in time of the local educational agency

RE: Local Control Accountability Plans and Adopted Budget Fiscal Year

Greg Land President, Governing Board 1825 Trousdale Drive Burlingame, CA 94010-4509 RE: Local Control Accountability Plans and Adopted Budget Fiscal Year 2014-15 Dear Mr. Land: In accordance with Education

Greg Land President, Governing Board 1825 Trousdale Drive Burlingame, CA 94010-4509 RE: Local Control Accountability Plans and Adopted Budget Fiscal Year 2014-15 Dear Mr. Land: In accordance with Education

PROPOSED BUDGET

2016-17 PROPOSED BUDGET Public Hearing on June 14, 2016 Adoption on June 28, 2016 Board of Trustees: Zerrall Mc Daniel Board President Gregory Gustafson Clerk Karan Bowsher Trustee Sherri Reusche Trustee

2016-17 PROPOSED BUDGET Public Hearing on June 14, 2016 Adoption on June 28, 2016 Board of Trustees: Zerrall Mc Daniel Board President Gregory Gustafson Clerk Karan Bowsher Trustee Sherri Reusche Trustee

Executive Summary Second Interim Budget Assumptions Duane Wolgamott, Chief Business Officer Laura Becker, Director of Fiscal Services

Executive Summary Second Interim Budget Assumptions 2016 17 Duane Wolgamott, Chief Business Officer Laura Becker, Director of Fiscal Services The purpose of the 2nd Interim Budget Assumptions is to provide

Executive Summary Second Interim Budget Assumptions 2016 17 Duane Wolgamott, Chief Business Officer Laura Becker, Director of Fiscal Services The purpose of the 2nd Interim Budget Assumptions is to provide

AB1200 Public Disclosure Collective Bargaining Agreement for (Teachers Association of Norwalk-La Mirada)

") School Board s Goals Engaging and Responsive Climate and Culture College and Career Ready Graduates Exemplary Staff Parent and Community Engagement Access to Rigorous Instruction and Support Operational

School Board s Goals Engaging and Responsive Climate and Culture College and Career Ready Graduates Exemplary Staff Parent and Community Engagement Access to Rigorous Instruction and Support Operational

CHULA VISTA ELEMENTARY SCHOOL DISTRICT GOVERNING BOARD AGENDA ITEM. (3) Certify District's Financial Status for Fiscal Year

Certify District's Financial Status for Fiscal Year") CHULA VISTA ELEMENTARY SCHOOL DISTRICT GOVERNING BOARD AGENDA ITEM Prepared by: Business Services and Support ITEM TITLE: (1) Approve Revisions to Fiscal Year 2016-17 Budget; (2) Approve First Interim

CHULA VISTA ELEMENTARY SCHOOL DISTRICT GOVERNING BOARD AGENDA ITEM Prepared by: Business Services and Support ITEM TITLE: (1) Approve Revisions to Fiscal Year 2016-17 Budget; (2) Approve First Interim

Solana Beach School District

B U D G E T W O R K S H O P Solana Beach School District 2017-18 Proposed Budget June 8, 2017 Our Mission is to provide a child-centered education of the highest quality, using the unique vision and resources

B U D G E T W O R K S H O P Solana Beach School District 2017-18 Proposed Budget June 8, 2017 Our Mission is to provide a child-centered education of the highest quality, using the unique vision and resources

LCAP Technical Assistance Navigating the New Template

LCAP Technical Assistance Navigating the New Template 2017 California County Superintendents Educational Services Association Chief Business Officials Conference February 22, 2017 Presented by Christine

LCAP Technical Assistance Navigating the New Template 2017 California County Superintendents Educational Services Association Chief Business Officials Conference February 22, 2017 Presented by Christine

First Interim Report

First Interim Report 2017-2018 Board Meeting: Tuesday, December 12, 2017 39139-49 N. 10 th Street East Palmdale, CA 93550 661-947-7191 Interim Report Certification Palmdale School District 2017-2018

First Interim Report 2017-2018 Board Meeting: Tuesday, December 12, 2017 39139-49 N. 10 th Street East Palmdale, CA 93550 661-947-7191 Interim Report Certification Palmdale School District 2017-2018

AB1200 Public Disclosure Collective Bargaining Agreement for January 28, 2015

School Board s Goals High Academic Achievement Effective Standards-Based Instruction Fiscally Solvent and Increase Enrollment Accountability for all Stakeholders Safety and Security of Students and Staff

School Board s Goals High Academic Achievement Effective Standards-Based Instruction Fiscally Solvent and Increase Enrollment Accountability for all Stakeholders Safety and Security of Students and Staff

AUBURN UNION SCHOOL DISTRICT Auburn, California. FINANCIAL STATEMENTS June 30, 2014

Auburn, California FINANCIAL STATEMENTS June 30, 2014 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2014 TABLE OF CONTENTS Page Independent Auditor's Report 1 Management's

Auburn, California FINANCIAL STATEMENTS June 30, 2014 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2014 TABLE OF CONTENTS Page Independent Auditor's Report 1 Management's

Vista Del Mar Union School District

Vista Del Mar Union School District Multiyear Financial Projection April 28, 2017 Joel D. Montero Chief Executive Officer Fiscal Crisis & Management Assistance Team April 28, 2017 Dr. Emilio Handall, Superintendent

Vista Del Mar Union School District Multiyear Financial Projection April 28, 2017 Joel D. Montero Chief Executive Officer Fiscal Crisis & Management Assistance Team April 28, 2017 Dr. Emilio Handall, Superintendent

Budget Development Workshop Internal Business Services. February 16, 2018 and February 22, 2018

Budget Development Workshop Internal Business Services February 16, 2018 and February 22, 2018 Governor s Proposals for the 2018-19 State Budget and K-12 Education The Education Budget Proposition 98:

Budget Development Workshop Internal Business Services February 16, 2018 and February 22, 2018 Governor s Proposals for the 2018-19 State Budget and K-12 Education The Education Budget Proposition 98:

Phase I. Phase II. July 2, L. Karen Monroe, Superintendent Alameda County Office of Education 313 W. Winton Avenue Hayward, CA 94544

July 2, 2018 L. Karen Monroe, Superintendent Alameda County Office of Education 313 W. Winton Avenue Hayward, CA 94544 Re: Oakland Unified School District Phase II Dear Superintendent Monroe: On January

July 2, 2018 L. Karen Monroe, Superintendent Alameda County Office of Education 313 W. Winton Avenue Hayward, CA 94544 Re: Oakland Unified School District Phase II Dear Superintendent Monroe: On January

Fruitvale School District

Fruitvale School District Excellence in Education Every Student, Every Day ANNUAL FINANCIAL AND BUDGET REPORT FISCAL YEAR 2017-18 PROPOSED BUDGET Presented on June 13, 2017 GOVERNING BOARD OF TRUSTEES

Fruitvale School District Excellence in Education Every Student, Every Day ANNUAL FINANCIAL AND BUDGET REPORT FISCAL YEAR 2017-18 PROPOSED BUDGET Presented on June 13, 2017 GOVERNING BOARD OF TRUSTEES

SACS BUDGET FORMS. Steve Mattern Connie Vargas Jordan Aquino Jennifer Noga Debbie Riedmiller Marcos Gamino

SACS BUDGET FORMS Steve Mattern Connie Vargas Jordan Aquino Jennifer Noga Debbie Riedmiller Marcos Gamino Required Forms FUND FORMS (ALL FUNDS) FORM A Average Daily Attendance FORM CEB Current Expense

SACS BUDGET FORMS Steve Mattern Connie Vargas Jordan Aquino Jennifer Noga Debbie Riedmiller Marcos Gamino Required Forms FUND FORMS (ALL FUNDS) FORM A Average Daily Attendance FORM CEB Current Expense

Rocky Point Charter School

Rocky Point Charter School Fiscal Review May 7, 2010 Joel D. Montero Chief Executive Officer May 7, 2010 Deborah Stierli, Director Rocky Point Charter School 3500 Tamarack Drive Redding, CA 96003 Dear

Rocky Point Charter School Fiscal Review May 7, 2010 Joel D. Montero Chief Executive Officer May 7, 2010 Deborah Stierli, Director Rocky Point Charter School 3500 Tamarack Drive Redding, CA 96003 Dear

2016/17 Budget Proposal June 20, 2016

2016/17 Budget Proposal June 20, 2016 Presenter Julie A. Betschart 6/22/2016 1 Tonight s Overview Local Control Funding Formula (LCFF) Assumptions for Revenue and Expenditures Fund Balance Criteria and

2016/17 Budget Proposal June 20, 2016 Presenter Julie A. Betschart 6/22/2016 1 Tonight s Overview Local Control Funding Formula (LCFF) Assumptions for Revenue and Expenditures Fund Balance Criteria and

OFFICE OF EDUCATION 1111 LAS GALLINAS AVENUE/P.O. BOX 4925 MARY JANE BURKE (415) SAN RAFAEL, CA MARIN COUNTY FAX (415)

SAN RAFAEL, CA MARIN COUNTY FAX (415)") MARIN COUNTY OFFICE OF EDUCATION 1111 LAS GALLINAS AVENUE/P.O. BOX 4925 MARY JANE BURKE (415) 472-4110 SAN RAFAEL, CA 94913-4925 MARIN COUNTY FAX (415) 491-6625 marincoe@marinschools.org SUPERINTENDENT

MARIN COUNTY OFFICE OF EDUCATION 1111 LAS GALLINAS AVENUE/P.O. BOX 4925 MARY JANE BURKE (415) 472-4110 SAN RAFAEL, CA 94913-4925 MARIN COUNTY FAX (415) 491-6625 marincoe@marinschools.org SUPERINTENDENT

Budget Forum

FREMONT UNIFIED SCHOOL DISTRICT Educate Challenge Inspire Budget Forum 2013 2014 Presented to: Irvington High School PTSA Division of Business Services April 11, 2013 Outline About FUSD Funding for Education

FREMONT UNIFIED SCHOOL DISTRICT Educate Challenge Inspire Budget Forum 2013 2014 Presented to: Irvington High School PTSA Division of Business Services April 11, 2013 Outline About FUSD Funding for Education

SANTA MONICA-MALIBU UNIFIED SCHOOL DISTRICT FIRST INTERIM REPORT DECEMBER 10, 2015 AGENDA ITEM A.24

SANTA MONICA-MALIBU UNIFIED SCHOOL DISTRICT DECEMBER 10, 2015 AGENDA ITEM A.24 SMMUSD 1 st Interim Report Shows the District s financial position as of October 31, 2015 Displays the Adopted Budget, Current

SANTA MONICA-MALIBU UNIFIED SCHOOL DISTRICT DECEMBER 10, 2015 AGENDA ITEM A.24 SMMUSD 1 st Interim Report Shows the District s financial position as of October 31, 2015 Displays the Adopted Budget, Current

RE: Local Control Accountability Plan and Adopted Budget Fiscal Year A. LOCAL CONTROL ACCOUNTABILITY PLAN

Carrie DuBois President, Governing Board Sequoia Union High School District 48 James Avenue Redwood City, CA 94062-1098 RE: Local Control Accountability Plan and Adopted Budget Fiscal Year 2017-18 Dear

Carrie DuBois President, Governing Board Sequoia Union High School District 48 James Avenue Redwood City, CA 94062-1098 RE: Local Control Accountability Plan and Adopted Budget Fiscal Year 2017-18 Dear

RE: Local Control Accountability Plan and Adopted Budget Fiscal Year

Frank Barbaro President, Governing Board 555 Richmond Drive Millbrae, CA 94030 RE: Local Control Accountability Plan and Adopted Budget Fiscal Year 2017-18 Dear Mr. Barbaro: The San Mateo County Office

Frank Barbaro President, Governing Board 555 Richmond Drive Millbrae, CA 94030 RE: Local Control Accountability Plan and Adopted Budget Fiscal Year 2017-18 Dear Mr. Barbaro: The San Mateo County Office

Useful Tips and Tricks to Understand the Principal Apportionment

Useful Tips and Tricks to Understand the Principal Apportionment 2017 CASBO CONFERENCE April 13, 2017 Presented by: Caryn Moore and Elizabeth Dearstyne SCHOOL FISCAL SERVICES DIVISION What to Expect Overview

Useful Tips and Tricks to Understand the Principal Apportionment 2017 CASBO CONFERENCE April 13, 2017 Presented by: Caryn Moore and Elizabeth Dearstyne SCHOOL FISCAL SERVICES DIVISION What to Expect Overview

SANTA CLARA COUNTY OFFICE OF EDUCATION AUDIT REPORT For the Fiscal Year Ended June 30, 2014

SANTA CLARA COUNTY OFFICE OF EDUCATION AUDIT REPORT For the Fiscal Year Ended June 30, 2014 For the Fiscal Year Ended June 30, 2014 Table of Contents FINANCIAL SECTION Page Independent Auditors Report...

SANTA CLARA COUNTY OFFICE OF EDUCATION AUDIT REPORT For the Fiscal Year Ended June 30, 2014 For the Fiscal Year Ended June 30, 2014 Table of Contents FINANCIAL SECTION Page Independent Auditors Report...

Buena Park School District Annual Budget Governing Board Study Session

Buena Park School District 2017-18 Annual Budget Governing Board Study Session Presented by: June 12, 2017 Greg Magnuson, Superintendent Kelvin Tsunezumi, Assistant Superintendent Administrative Services

Buena Park School District 2017-18 Annual Budget Governing Board Study Session Presented by: June 12, 2017 Greg Magnuson, Superintendent Kelvin Tsunezumi, Assistant Superintendent Administrative Services

FCMAT. Chief Executive Officer Joel 0. Montero

About FCMAT The Fiscal Crisis and Management Assistance Team (FCMAT) was created by legislation in 1992 as an independent and external state agency. FCMAT's mission is to provide proactive and preventive

About FCMAT The Fiscal Crisis and Management Assistance Team (FCMAT) was created by legislation in 1992 as an independent and external state agency. FCMAT's mission is to provide proactive and preventive

Yosemite Unified School District

Yosemite Unified School District Fiscal and Business Services Review February 7, 2018 Michael H. Fine Chief Executive Officer Fiscal Crisis & Management Assistance Team February 7, 2018 Cecelia Lynn Greenberg,

Yosemite Unified School District Fiscal and Business Services Review February 7, 2018 Michael H. Fine Chief Executive Officer Fiscal Crisis & Management Assistance Team February 7, 2018 Cecelia Lynn Greenberg,

Budget FY May 20, Guidance Charter School th Street East Palmdale, CA (661)

") Guidance Charter School 37230 37th Street East Palmdale, CA. 93550 (661)2851600 Budget FY20162017 May 20, 2016 Presented by School Business Services The Guidance Charter School Page 1 of 20 Table of Content

Guidance Charter School 37230 37th Street East Palmdale, CA. 93550 (661)2851600 Budget FY20162017 May 20, 2016 Presented by School Business Services The Guidance Charter School Page 1 of 20 Table of Content

SAN LEANDRO UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT JUNE 30, 2016

SAN LEANDRO UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor s Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

SAN LEANDRO UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor s Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

SAN DIEGO UNIFIED SCHOOL DISTRICT. FINANCIAL STATEMENTS June 30, 2017

FINANCIAL STATEMENTS June 30, 2017 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2017 CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S DISCUSSION AND ANALYSIS...

FINANCIAL STATEMENTS June 30, 2017 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2017 CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S DISCUSSION AND ANALYSIS...

AND UNRESTRICTED GENERAL FUND (OUT-YEAR BUDGET PROJECTIONS)

") Board of Education Report No. 172 15/16 For 12/8/15 Board Meeting The General Fund cash balance (Restricted and Unrestricted) is projected to be $1.2 billion as of June 30, 2016. The District does not

Board of Education Report No. 172 15/16 For 12/8/15 Board Meeting The General Fund cash balance (Restricted and Unrestricted) is projected to be $1.2 billion as of June 30, 2016. The District does not

Budget Study Session 2012/13, 2013/14, and 2014/15. Business Services Division January 22, 2013

Budget Study Session 2012/13, 2013/14, and 2014/15 Business Services Division January 22, 2013 Budget Study Session #3 Common School Financial Terms CVUSD First Interim Multiyear Budget Recap Governor

Budget Study Session 2012/13, 2013/14, and 2014/15 Business Services Division January 22, 2013 Budget Study Session #3 Common School Financial Terms CVUSD First Interim Multiyear Budget Recap Governor

Governor s Proposals for the State Budget and K-12 Education

2010 School Services of California, Inc. Governor s Proposals for the 2010-11 State Budget and K-12 Education Presented by Song Chin-Bendib Assistant Superintendent, Business Services Regular Board Meeting

2010 School Services of California, Inc. Governor s Proposals for the 2010-11 State Budget and K-12 Education Presented by Song Chin-Bendib Assistant Superintendent, Business Services Regular Board Meeting

Budgeting Basics- Pt. 1. Interpreting the Interim Budgets and Multi-Year Projections

Budgeting Basics- Pt. 1 Interpreting the Interim Budgets and Multi-Year Projections Scott Weimer Merced Union High School District Prepared: April 17, 2017 1 Overview The Fiscal Services Department uses

Budgeting Basics- Pt. 1 Interpreting the Interim Budgets and Multi-Year Projections Scott Weimer Merced Union High School District Prepared: April 17, 2017 1 Overview The Fiscal Services Department uses

April 13, Debra LaVoi, Ed.D., Superintendent Woodland Joint Unified School District 435 Sixth Street Woodland, CA 95695

April 13, 2011 Debra LaVoi, Ed.D., Superintendent Woodland Joint Unified School District 435 Sixth Street Woodland, CA 95695 Dear Superintendent LaVoi: In accordance with the study agreement between Woodland

April 13, 2011 Debra LaVoi, Ed.D., Superintendent Woodland Joint Unified School District 435 Sixth Street Woodland, CA 95695 Dear Superintendent LaVoi: In accordance with the study agreement between Woodland

FAME Public Charter School

FAME Public Charter School Fiscal Review February 10, 2010 Joel D. Montero Chief Executive Officer Fiscal Crisis & Management Assistance Team February 10, 2010 Maram Alaiwat, Chief Executive Officer FAME

FAME Public Charter School Fiscal Review February 10, 2010 Joel D. Montero Chief Executive Officer Fiscal Crisis & Management Assistance Team February 10, 2010 Maram Alaiwat, Chief Executive Officer FAME

Sweetwater Union High School District. Fiscal Health Risk Analysis. December 17, 2018 DRAFT. Michael H. Fine Chief Executive Officer

Sweetwater Union High School District Fiscal Health Risk Analysis December 17, 2018 DRAFT Michael H. Fine Chief Executive Officer Fiscal Crisis & Management Assistance Team TABLE OF CONTENTS Contents About

Sweetwater Union High School District Fiscal Health Risk Analysis December 17, 2018 DRAFT Michael H. Fine Chief Executive Officer Fiscal Crisis & Management Assistance Team TABLE OF CONTENTS Contents About

CULVER CITY UNIFIED SCHOOL DISTRICT

AUDIT REPORT JUNE 30, 2018 TABLE OF CONTENTS JUNE 30, 2018 FINANCIAL SECTION Independent Auditors Report... 1 Management s Discussion and Analysis... 4 Basic Financial Statements Government-wide Financial

AUDIT REPORT JUNE 30, 2018 TABLE OF CONTENTS JUNE 30, 2018 FINANCIAL SECTION Independent Auditors Report... 1 Management s Discussion and Analysis... 4 Basic Financial Statements Government-wide Financial

SAN LEANDRO UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT JUNE 30, 2018

SAN LEANDRO UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

SAN LEANDRO UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

Basics of the Principal Apportionment

Basics of the Principal Apportionment AB 1200 Fall Conference October 12, 2016, Ventura COE October 17, 2016, Yolo COE Presented by: Caryn Moore, Associate Director and Elizabeth Dearstyne, Administrator

Basics of the Principal Apportionment AB 1200 Fall Conference October 12, 2016, Ventura COE October 17, 2016, Yolo COE Presented by: Caryn Moore, Associate Director and Elizabeth Dearstyne, Administrator

DAVIS JOINT UNIFIED SCHOOL DISTRICT UNAUDITED ACTUALS

DAVIS JOINT UNIFIED SCHOOL DISTRICT 2017-18 UNAUDITED ACTUALS October 4, 2018 2 UNAUDITED ACTUALS REPORT Actual Financial Report of the District Final accounting of District results for receipts and expenditures

DAVIS JOINT UNIFIED SCHOOL DISTRICT 2017-18 UNAUDITED ACTUALS October 4, 2018 2 UNAUDITED ACTUALS REPORT Actual Financial Report of the District Final accounting of District results for receipts and expenditures

SANTA CLARA COUNTY OFFICE OF EDUCATION Personnel Commission

SANTA CLARA COUNTY OFFICE OF EDUCATION Personnel Commission CLASS TITLE: DISTRICT BUSINESS ADVISOR BASIC FUNCTION: Under the direction of the Director III-District Business Services or the Senior - District

SANTA CLARA COUNTY OFFICE OF EDUCATION Personnel Commission CLASS TITLE: DISTRICT BUSINESS ADVISOR BASIC FUNCTION: Under the direction of the Director III-District Business Services or the Senior - District

AUBURN UNION SCHOOL DISTRICT. FINANCIAL STATEMENTS June 30, 2016

FINANCIAL STATEMENTS June 30, 2016 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2016 (Continued) CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S DISCUSSION AND

FINANCIAL STATEMENTS June 30, 2016 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2016 (Continued) CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S DISCUSSION AND

SECOND INTERIM FINANCIAL REPORT

2016-17 SECOND INTERIM FINANCIAL REPORT COVINA-VALLEY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION MEETING MARCH 6, 2017 BUSINESS AND FISCAL SERVICES 1 SECOND INTERIM REPORT AND CERTIFICATION Districts are

2016-17 SECOND INTERIM FINANCIAL REPORT COVINA-VALLEY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION MEETING MARCH 6, 2017 BUSINESS AND FISCAL SERVICES 1 SECOND INTERIM REPORT AND CERTIFICATION Districts are

Adopted Budget Date Submitted: June 29, 2017 Board of Education Meeting

Poway Unified School District 2017-2018 Adopted Budget Date Submitted: June 29, 2017 Board of Education Meeting 1 Description of Funds Fund 01 General Fund Fund 11 Adult Education Fund 12 Child Development

Poway Unified School District 2017-2018 Adopted Budget Date Submitted: June 29, 2017 Board of Education Meeting 1 Description of Funds Fund 01 General Fund Fund 11 Adult Education Fund 12 Child Development

July 1 Budget Fiscal Year Charter School Certification

California Montessori Project-Shingle Springs Campus Buckeye Union Elementary El Dorado County July 1 Budget Fiscal Year 2016-17 Charter School Certification 09 61838 0111724 Form CB Charter Number: 774

California Montessori Project-Shingle Springs Campus Buckeye Union Elementary El Dorado County July 1 Budget Fiscal Year 2016-17 Charter School Certification 09 61838 0111724 Form CB Charter Number: 774

SACS Forum May 16, 2018

Slide 3: CASBO SACS Workshops San Bernardino County Office of Education Basic Thursday, May 17, 2018 Advanced Friday, May 18, 2018 Sutter County Office of Education Basic Thursday, May 24, 2018 Advanced

Slide 3: CASBO SACS Workshops San Bernardino County Office of Education Basic Thursday, May 17, 2018 Advanced Friday, May 18, 2018 Sutter County Office of Education Basic Thursday, May 24, 2018 Advanced

BY: Teresa Hyden Diana Asseier Chief Business Official Chief Academic Officer (951) (951)

(951)") DATE: TO: FROM: Dr. Julie A. Vitale, District Superintendent Mrs. Sandra Tusant, Board President Mrs. Hilda Murallo, Chief Business Official Mr. Trevor Painton, Assistant Superintendent Kenneth M. Young,

DATE: TO: FROM: Dr. Julie A. Vitale, District Superintendent Mrs. Sandra Tusant, Board President Mrs. Hilda Murallo, Chief Business Official Mr. Trevor Painton, Assistant Superintendent Kenneth M. Young,

A CDE Overview: Current Issues in School Finance. California Association of School Business Officials 2017 Annual Conference April 14, 2017

A CDE Overview: Current Issues in School Finance California Association of School Business Officials 2017 Annual Conference April 14, 2017 Presenters Peter Foggiato, Director Christine Davis, Administrator

A CDE Overview: Current Issues in School Finance California Association of School Business Officials 2017 Annual Conference April 14, 2017 Presenters Peter Foggiato, Director Christine Davis, Administrator

Cotati-Rohnert Park Unified School District

Cotati-Rohnert Park Unified School District Management Review October 22, 2007 Joel D. Montero Chief Executive Officer Fiscal Crisis & Management Assistance Team October 22, 2007 Barbara Vrankovich, Superintendent

Cotati-Rohnert Park Unified School District Management Review October 22, 2007 Joel D. Montero Chief Executive Officer Fiscal Crisis & Management Assistance Team October 22, 2007 Barbara Vrankovich, Superintendent

1 st Interim Workshop. Steve Mattern Jennifer Noga Jordan Aquino Connie Vargas Marcos Gamino

1 st Interim Workshop Steve Mattern Jennifer Noga Jordan Aquino Connie Vargas Marcos Gamino Reconciling Board Financial Summary Reconciling Board Financial Summary Assets Cash in Bank (9120) Revolving

1 st Interim Workshop Steve Mattern Jennifer Noga Jordan Aquino Connie Vargas Marcos Gamino Reconciling Board Financial Summary Reconciling Board Financial Summary Assets Cash in Bank (9120) Revolving

FORESTHILL UNION SCHOOL DISTRICT COUNTY OF PLACER FORESTHILL, CALIFORNIA

COUNTY OF PLACER FORESTHILL, CALIFORNIA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORT TABLE OF CONTENTS FINANCIAL SECTION PAGE INDEPENDENT AUDITOR'S REPORT 1 MANAGEMENT'S DISCUSSION AND ANALYSIS

COUNTY OF PLACER FORESTHILL, CALIFORNIA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORT TABLE OF CONTENTS FINANCIAL SECTION PAGE INDEPENDENT AUDITOR'S REPORT 1 MANAGEMENT'S DISCUSSION AND ANALYSIS

LOS ALAMITOS UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT JUNE 30, 2015

LOS ALAMITOS UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

LOS ALAMITOS UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

LCAP / Supplemental and Concentration Regulations

LCAP / Supplemental and Concentration Regulations LCAP Overview The Local Control and Accountability Plan (LCAP) represents a fundamental shift in how LEAs will plan for, and be held accountable for, LCFF

LCAP / Supplemental and Concentration Regulations LCAP Overview The Local Control and Accountability Plan (LCAP) represents a fundamental shift in how LEAs will plan for, and be held accountable for, LCFF

SAN LUIS OBISPO COUNTY OFFICE OF EDUCATION ANNUAL FINANCIAL REPORT JUNE 30, 2018

SAN LUIS OBISPO COUNTY OFFICE OF EDUCATION ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

SAN LUIS OBISPO COUNTY OFFICE OF EDUCATION ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

Assistant Superintendents, Business Services Directors, Business Services ROC/Ps

November 6, 2009 To: Assistant Superintendents, Business Services Directors, Business Services ROC/Ps From: Wendy Benkert, Ed.D., Assistant Superintendent Business Services Subject: 2009-10 First Interim

November 6, 2009 To: Assistant Superintendents, Business Services Directors, Business Services ROC/Ps From: Wendy Benkert, Ed.D., Assistant Superintendent Business Services Subject: 2009-10 First Interim

BY: Teresa Hyden Cynthia Glover Woods Chief Business Official Chief Academic Officer (951) (951)

(951)") DATE: TO: FROM: Dr. Julie A. Vitale, District Superintendent Mrs. Sandra Tusant, Board President Mrs. Hilda Murallo, Chief Business Official Mr. Trevor Painton, Assistant Superintendent Kenneth M. Young,

DATE: TO: FROM: Dr. Julie A. Vitale, District Superintendent Mrs. Sandra Tusant, Board President Mrs. Hilda Murallo, Chief Business Official Mr. Trevor Painton, Assistant Superintendent Kenneth M. Young,

LOS ALAMITOS UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT JUNE 30, 2016

LOS ALAMITOS UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

LOS ALAMITOS UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

South Bay Union School District

South Bay Union School District Fiscal Review August 19, 2011 Joel D. Montero Chief Executive Officer Fiscal Crisis & Management Assistance Team August 19, 2011 Carol Parish, Ed.D., Superintendent South

South Bay Union School District Fiscal Review August 19, 2011 Joel D. Montero Chief Executive Officer Fiscal Crisis & Management Assistance Team August 19, 2011 Carol Parish, Ed.D., Superintendent South

Los Angeles County Office of Education. Gorman Joint Elementary School District

Los Angeles County Office of Education regarding the Gorman Joint Elementary School District Fiscal Review December 6, 2007 Joel D. Montero Chief Executive Officer Fiscal Crisis & Management Assistance

Los Angeles County Office of Education regarding the Gorman Joint Elementary School District Fiscal Review December 6, 2007 Joel D. Montero Chief Executive Officer Fiscal Crisis & Management Assistance

SAN DIEGO UNIFIED SCHOOL DISTRICT

SAN DIEGO UNIFIED SCHOOL DISTRICT 2015-16 THIRD INTERIM FINANCIAL REPORT UPDATE B O A R D O F E D U C A T I O N M A Y 1 0, 2 0 1 6 THIRD INTERIM AGENDA Requirements of the CA Education Code Changes to

SAN DIEGO UNIFIED SCHOOL DISTRICT 2015-16 THIRD INTERIM FINANCIAL REPORT UPDATE B O A R D O F E D U C A T I O N M A Y 1 0, 2 0 1 6 THIRD INTERIM AGENDA Requirements of the CA Education Code Changes to

ESPARTO UNIFIED SCHOOL DISTRICT COUNTY OF YOLO ESPARTO, CALIFORNIA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORT JUNE 30, 2014

COUNTY OF YOLO ESPARTO, CALIFORNIA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORT JUNE 30, 2014 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR'S REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 3 BASIC

COUNTY OF YOLO ESPARTO, CALIFORNIA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORT JUNE 30, 2014 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR'S REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 3 BASIC

NOVATO UNIFIED SCHOOL DISTRICT. March 25, Presented by: Karen Maloney, CFO

NOVATO UNIFIED SCHOOL DISTRICT March 25, 2014 Presented by: Karen Maloney, CFO 1 Where we ve been Where we are now Where we re going Revenue Limit Deficit Factors: 2 3 The Revenue Limit was not fully funded

NOVATO UNIFIED SCHOOL DISTRICT March 25, 2014 Presented by: Karen Maloney, CFO 1 Where we ve been Where we are now Where we re going Revenue Limit Deficit Factors: 2 3 The Revenue Limit was not fully funded

Year End Financial Report

2017-18 Year End Financial Report PRESENTED BY JOHN FOGARTY SEPTEMBER 11, 2018 IUSD Unaudited Actuals 2017-18 Unaudited Actuals represent the cumulative financial activity for the fiscal year. Subject

2017-18 Year End Financial Report PRESENTED BY JOHN FOGARTY SEPTEMBER 11, 2018 IUSD Unaudited Actuals 2017-18 Unaudited Actuals represent the cumulative financial activity for the fiscal year. Subject

NATOMAS UNIFIED SCHOOL DISTRICT Sacramento, California. FINANCIAL STATEMENTS June 30, 2014

Sacramento, California FINANCIAL STATEMENTS June 30, 2014 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2014 TABLE OF CONTENTS Page Independent Auditor's Report 1 Management's

Sacramento, California FINANCIAL STATEMENTS June 30, 2014 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2014 TABLE OF CONTENTS Page Independent Auditor's Report 1 Management's

First Interim Budget

2017-18 First Interim Budget December 7, 2017 Presented by: Jason E. Vann Chief Financial Officer Purpose of Presentation Summarize Budget Cycle Provide Cambrian School Districts Budget Update Discuss

2017-18 First Interim Budget December 7, 2017 Presented by: Jason E. Vann Chief Financial Officer Purpose of Presentation Summarize Budget Cycle Provide Cambrian School Districts Budget Update Discuss

TULARE COUNTY OFFICE OF EDUCATION AUDIT REPORT JUNE 30, 2016

AUDIT REPORT JUNE 30, 2016 Received 12/15/2016 TABLE OF CONTENTS FOR THE YEAR ENDED JUNE 30, 2016 FINANCIAL SECTION Independent Auditors Report... 1 Management s Discussion and Analysis... 4 Basic Financial

AUDIT REPORT JUNE 30, 2016 Received 12/15/2016 TABLE OF CONTENTS FOR THE YEAR ENDED JUNE 30, 2016 FINANCIAL SECTION Independent Auditors Report... 1 Management s Discussion and Analysis... 4 Basic Financial

Preliminary General Fund Budget for Board of Education Presentation Janece L. Maez, Chief Financial Officer June 6, 2013

Preliminary General Fund Budget for 2013 14 Board of Education Presentation Janece L. Maez, Chief Financial Officer June 6, 2013 Agenda Item D.01 SMMUSD 2013 14 Budget Development Highlights November 1

Preliminary General Fund Budget for 2013 14 Board of Education Presentation Janece L. Maez, Chief Financial Officer June 6, 2013 Agenda Item D.01 SMMUSD 2013 14 Budget Development Highlights November 1

COVINA-VALLEY UNIFIED SCHOOL DISTRICT ANNUAL FINANCIAL REPORT JUNE 30, 2016

ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide Financial Statements Statement

ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide Financial Statements Statement

WASHINGTON UNIFIED SCHOOL DISTRICT West Sacramento, California. FINANCIAL STATEMENTS June 30, 2015

West Sacramento, California FINANCIAL STATEMENTS June 30, 2015 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2015 (Continued) CONTENTS INDEPENDENT AUDITOR'S REPORT...

West Sacramento, California FINANCIAL STATEMENTS June 30, 2015 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2015 (Continued) CONTENTS INDEPENDENT AUDITOR'S REPORT...

LUTHER BURBANK SCHOOL DISTRICT

LUTHER BURBANK SCHOOL DISTRICT 2014-15 First Interim Report Dr. Michelle Richardson, Superintendent Rodolfo Alvalos-Sanchez, CBO December 9, 2014 Contents of Report LCAP Update Fiscal Update Local Control

LUTHER BURBANK SCHOOL DISTRICT 2014-15 First Interim Report Dr. Michelle Richardson, Superintendent Rodolfo Alvalos-Sanchez, CBO December 9, 2014 Contents of Report LCAP Update Fiscal Update Local Control

Budget Adoption

2015-16 Budget Adoption Oakland USD Board of Education June 24, 2015 v.6 2 Table of Contents Executive Summary 2015-16 Budget All Funds Total General Fund General Fund Unrestricted Appendix OUSD 2015-16

2015-16 Budget Adoption Oakland USD Board of Education June 24, 2015 v.6 2 Table of Contents Executive Summary 2015-16 Budget All Funds Total General Fund General Fund Unrestricted Appendix OUSD 2015-16

CSBA Sample Administrative Regulation

CSBA Sample Administrative Regulation Business and Noninstructional Operations AR 3460(a) FINANCIAL REPORTS AND ACCOUNTABILITY Interim Reports Note: Education Code 42130 requires that the district issue

CSBA Sample Administrative Regulation Business and Noninstructional Operations AR 3460(a) FINANCIAL REPORTS AND ACCOUNTABILITY Interim Reports Note: Education Code 42130 requires that the district issue

NATOMAS UNIFIED SCHOOL DISTRICT. FINANCIAL STATEMENTS June 30, 2017

FINANCIAL STATEMENTS June 30, 2017 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2017 CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S DISCUSSION AND ANALYSIS...

FINANCIAL STATEMENTS June 30, 2017 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2017 CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S DISCUSSION AND ANALYSIS...

ATWATER ELEMENTARY SCHOOL DISTRICT

ATWATER ELEMENTARY SCHOOL DISTRICT FIRST INTERIM December 12, 2017 Sandra Schiber, Superintendent Carol Longobardi, Fiscal Services Supervisor Linda Levesque, Assistant Superintendent of Business Services

ATWATER ELEMENTARY SCHOOL DISTRICT FIRST INTERIM December 12, 2017 Sandra Schiber, Superintendent Carol Longobardi, Fiscal Services Supervisor Linda Levesque, Assistant Superintendent of Business Services

Appendix E Glossary of Common School Finance Terms

ADA Average daily attendance. There are several kinds of attendance, and these are counted in different ways. For regular attendance, ADA is equal to the average number of pupils actually attending classes

ADA Average daily attendance. There are several kinds of attendance, and these are counted in different ways. For regular attendance, ADA is equal to the average number of pupils actually attending classes

MONROVIA UNIFIED SCHOOL DISTRICT COUNTY OF LOS ANGELES MONROVIA, CALIFORNIA. AUDIT REPORT June 30, 2017

COUNTY OF LOS ANGELES MONROVIA, CALIFORNIA AUDIT REPORT June 30, 2017 TABLE OF CONTENTS June 30, 2017 FINANCIAL SECTION Independent Auditor s Report... 1 Management s Discussion and Analysis... 4 Basic

COUNTY OF LOS ANGELES MONROVIA, CALIFORNIA AUDIT REPORT June 30, 2017 TABLE OF CONTENTS June 30, 2017 FINANCIAL SECTION Independent Auditor s Report... 1 Management s Discussion and Analysis... 4 Basic

Guidance Charter School th Street East Palmdale, CA (661) Budget FY

Budget FY") Guidance Charter School 37230 37th Street East Palmdale, CA. 93550 (661)285-1600 Budget FY2015-16 May 20, 2015 Presented by School Business Services The Guidance Charter School Page 1 of 20 Table of Content

Guidance Charter School 37230 37th Street East Palmdale, CA. 93550 (661)285-1600 Budget FY2015-16 May 20, 2015 Presented by School Business Services The Guidance Charter School Page 1 of 20 Table of Content

Sacramento City Unified School District. Fiscal Health Risk Analysis. December 12, 2018 DRAFT. Michael H. Fine Chief Executive Officer

Sacramento City Unified School District Fiscal Health Risk Analysis December 12, 2018 DRAFT Michael H. Fine Chief Executive Officer Fiscal Crisis & Management Assistance Team TABLE OF CONTENTS Contents

Sacramento City Unified School District Fiscal Health Risk Analysis December 12, 2018 DRAFT Michael H. Fine Chief Executive Officer Fiscal Crisis & Management Assistance Team TABLE OF CONTENTS Contents

EL CENTRO ELEMENTARY SCHOOL DISTRICT

EL CENTRO ELEMENTARY SCHOOL DISTRICT 2016-17 ESTIMATED ACTUALS AND 2017-18 ORIGINAL BUDGET REPORT OVERVIEW The following narrative provides administrative comments and notations for the El Centro Elementary

EL CENTRO ELEMENTARY SCHOOL DISTRICT 2016-17 ESTIMATED ACTUALS AND 2017-18 ORIGINAL BUDGET REPORT OVERVIEW The following narrative provides administrative comments and notations for the El Centro Elementary

SONOMA COUNTY OFFICE OF EDUCATION AUDIT REPORT For the Fiscal Year Ended June 30, 2018

SONOMA COUNTY OFFICE OF EDUCATION AUDIT REPORT For the Fiscal Year Ended June 30, 2018 For the Fiscal Year Ended June 30, 2018 Table of Contents FINANCIAL SECTION Page Independent Auditors Report... 1

SONOMA COUNTY OFFICE OF EDUCATION AUDIT REPORT For the Fiscal Year Ended June 30, 2018 For the Fiscal Year Ended June 30, 2018 Table of Contents FINANCIAL SECTION Page Independent Auditors Report... 1