Pearson LCCI Level 3 Cost Accounting (ASE3017)

|

|

|

- Cecil Bell

- 5 years ago

- Views:

Transcription

1 Pearson LCCI Level 3 Cost Accounting (ASE3017) Annual Qualification Review 2013/2014 For further information contact us: Tel. +44 (0) internationalenquiries@pearson.com

2 CONTENTS Introduction 2 Pass Rate Statistics 2 General Strengths and Weaknesses 3 Teaching Points by Syllabus Topic 4 Examples of Candidate Responses 9 1

3 INTRODUCTION The annual qualification review provides qualification specific support and guidance to centres. This information is designed to help teachers preparing to teach the subject and to help candidates preparing to take the examination. The reviews are published in September and take into account candidate performance, demonstrated in both on demand and series examinations, over the preceding 12 months. Global pass rates are published so you can measure the performance of your centre against these. The review identifies candidate strengths and weaknesses by syllabus topic area and provides examples of good and poorer candidate responses. It should therefore be read in conjunction with details of the structure and learning objectives contained within the syllabus for this qualification found on the website. The review also identifies any actual or proposed changes to the syllabus or question types together with their implications. PASS RATE STATISTICS The following statistics are based on the performance of candidates who sat this qualification between 1 September 2013 and 31 August Global pass rate 42.5%* Grade distributions of candidates achieving pass or higher Pass 15.6% Merit 16.1% Distinction 10.8% * This figure excludes absences on the day of the exam 2

4 GENERAL STRENGTHS AND WEAKNESSES After analysing the results of the cost accounting papers at level 3, it would appear that candidates basically fall into the two following categories. (i) Those who have an understanding of the subject and have prepared for the examination (ii) Those who have no understanding of the subject and have not prepared for the examination The following analysis relates to candidates in category (i). It is suggested that the candidates who fall into category (ii) and still wish to obtain a cost accounting qualification would benefit from a level 2 course before attempting level 3 again. Strengths An understanding of what is required by the question An understanding of the basic cost accounting terminology The ability to answer standard questions with inherent likeness to previously set questions. This indicates the candidates have studied previously published model answers Weaknesses Generally not prepared for this level Inability to deal with and work logically through information given in question Poor writing. Examiner not always being able to decipher candidates response Not providing workings to show how answer is arrived at. 3

5 TEACHING POINTS BY SYLLABUS TOPIC Syllabus Topic 1: Materials and stock control Questions set on calculation of material cost (series4/13) were generally answered well although a common error included the calculation of weight loss due to manufacturing and rejection. The product rejection rate was states at 10% and some candidates incorrectly added 10% to establish the required production instead of dividing by 90%. Descriptions relating to the Just in Time approach to stock management (series2/14) were not so well answered. Candidates need to be aware that Just in time principles of stock control, involves more than just keeping stock levels to a minimum. Stock record card presentation (series3/14) was generally handled well although a number of candidate s ether did not calculate, or miscalculated, the opening free stock. The common error with this calculation was not to include the stock on order. Calculation of stock levels (series3/14) was reasonably well answered although a common error was the missing out of the opening stock when calculating the average holding costs. Descriptions relating to stock terms (series3/14) were poorly answered. Candidates need to understand these stock level terms and not just rope learn as in many cases only part answers were provided. Some incorrect answers provided: Reorder level The level of stock in the stores. (no mention of reordering) Allocated stock Stock that has been allocated for use (This just repeats the question). Free stock Stock that is available for reservation or allocation. (Only a part answer see model answer). Syllabus Topic 2: Costing methods and systems Questions set on the preparation of trading accounts, in both marginal and absorption costing format, were not generally answered well (series2/14). The common errors being the calculation and valuation of the closing stock figures and the calculation of fixed overheads and layout of the marginal costing account. 4

6 The following points within this topic area question need addressing: The accounts should indicate the different sales and production levels and therefore should include closing stock figures. The accounts need to distinguish between the two different closing stocks (i.e. packed and unpacked stock) and not combine them together as one stock figure. Where different absorption rates apply to different departments different calculations are necessary. With this question the Machine and Finishing overheads are based on number of units manufactured whereas the dispatch department overhead is based on the number of products packed. With absorption costing the stock valuation includes a portion of the fixed costs where as in the marginal costing method it is not. Marginal costing format should include a figure for variable cost of production and contribution. Stock valuation figures only include the process account. Question (series3/14) required the joint costs to be calculated based on the net sales method. The account itself was reasonably well answered although many of the candidates profit statement did not reflect the net sales process method. The following points within this topic area question need addressing: Understand the different methods of apportioning joint cost. Many candidates incorrectly used the total sales instead of the net sales method. When calculating any additional costs the overheads must be included The income received by the sale of by-products is used to reduce the overall costs. A joint product process profit statement should only include the costs and income from its main products, the by-product income being used to reduce the process costs. The statement should not contain the labour, material or the overhead costs as these would have been converted into joint costs. The statement provides a profit figure for the main products only. Syllabus Topic 3: Cost-volume-profit (CVP) analysis Candidates seem well prepared for the calculation of contribution sales ratios, break even points, margins of safety and related profits (all three series) and performed the tasks well. However a minority of candidates, when dealing with multi product companies (series4/13&3/14) incorrectly added the individual contribution sales ratios to calculate the overall and again incorrectly tried to calculate the individual break even points for each product. With multi product companies only the overall break even sales revenue can be calculated however a few candidates made the correct calculation but incorrectly labelled the answer 5

7 as unit s. General questions relating CVP analysis were all reasonably well answered. More attention to detail was required when constructing the profit volume chart (series2/14). Many candidates used incorrect scales, with incorrect or no labelling to identify the specific points. The identification of the two salary structures and the level of sales where the change would be worthwhile was where candidates missed out on marks. A few candidates opted not to use the graph paper provided and missed out on marks because of incorrect scaling. Limitations identification of breakeven analysis (series3/14) was in general poorly answered as candidates did not fully qualify their answer. The limitation does not assume that variable costs remain constant it assumes that variable per unit remain constant and it assumes that it is total fixed cost that remain not fixed cost. A number of marks were missed out on because a full answer was not provided. Syllabus Topic 4: Budgetary planning and control The preparation of flexible budgets at a specific output from budgets set at different output levels was reasonably well answered. (Series 4/13) However common errors included not taking into consideration the two different cost levels when calculating the flexed material and labour costs. The use of the high/low method when calculating semi-variable maintenance also caused some candidates problems. Basic budgetary explanation (series 4/13) needs revising and understood rather than just committed to memory. Many candidates provided accurate explanations of flexed and fixed budget but could not state the main objective of preparing them. Questions set on standard cash budgets (series 2/2014) were on average generally well answered, however candidates need to be aware of the correct layout, which includes an additional set of figures for net cash flow. The following points within this topic area need addressing: When determining the value of purchases which have opening and closing stock constraint figures, adjustments need to be made to the cost of sales to arrive at the correct purchases figure. However the majority of candidates did follow this model. Candidates need to be aware labour costs can include piece work, with a bonus, and that separate calculations for both these costs have to be made as payment is usually spread over two payment periods. The wage expense in the profit statement included the bonus earned in that particular month hence to arrive at the basic pay the expense should be divided by 110%. This proved difficult for many candidates and marks were lost due to an incorrect basic wage being used. 6

8 Depreciation although part of the overhead, is not cash budget outlay and should have been deducted prior to splitting the overhead payment over two periods. Most candidates however did complete this calculation. The layout of a cash budget should include an extra row for net cash flow figures. Again the majority of candidates did include these figures but a few incorrectly named it profit. Many candidates stated the advantages of general budgeting when the question specifically asked for advantages of a cash budget. A transport service budget question (series 3/14) was very poorly answered with candidates mixing costs per single vehicle with those for the fleet of 5 vehicles and not correctly following through their operational and office overheads to the required annual and month 5 cost statements. It would appear that this poor performance could be due to the fact that many candidates struggle with questions set outside a normal production environment. Syllabus Topic 5: Standard costing and variances Standard layout questions requiring calculation of labour, material, fixed overheads and sales variances from given information were generally well answered. However reasons for variance (series 3/14) and the calculation of production ratios (series4/13) proved more difficult. The following points in this section also need addressing: Variances should always be quoted in monetary terms not on a time or weight basis. The correct descriptions for variances is Favourable or Adverse however Fav or Adv or F or A are acceptable as an abbreviation. The use of + or - however is not acceptable and the candidate will miss out on marks as will no or incorrect description. Understand and interpret variances from given information rather than just stating global reasons for variances. Not many reasons relating to the transport company suggested transport reasons many incorrectly provided production reasons. Revise, calculate and understand the three production ratios. Many candidates provided correct calculations but attributed the answer to the wrong ratio. The explanation of the difference between ideal and attainable standards (series2/14) was generally well answered. 7

9 Syllabus Topic 6: Accounting systems. The posting of entries into the cost accounts ledger system were generally well answered (series 4/13). However a common error was the converting of opening and closing stock valuations from the financial control accounts to cost control accounts and in particular understanding whether to add or subtract the difference proved problematic. The posting of variance figures to the raw material account (series2/14) proved difficult for many candidates. This account should only have the price variance included but many incorrectly included the usage variance. 8

10 EXAMPLES OF CANDIDATE RESPONSES These candidate responses were taken from Series3/14 Question 4 Paper 1 9

11 10

12 11

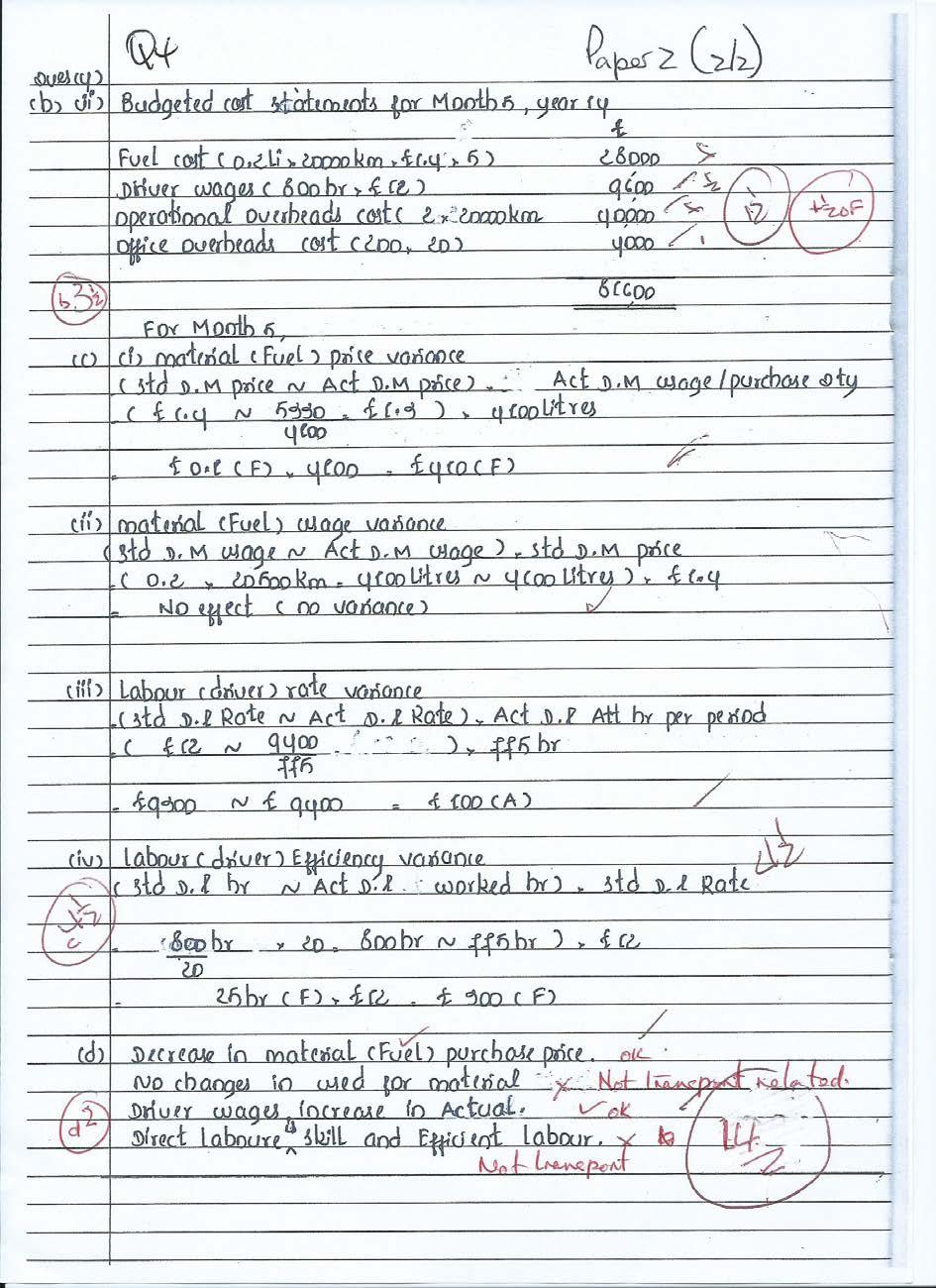

13 Paper 1 (a)(i) Operational Overheads Incorrectly calculated the tyre and the depreciation cost (However an own figure mark was awarded for the absorption rate figure). (ii) Office overheads correctly calculated. (awarded 4marks out of 5) (b)(i) Budgeted cost statement for year. Incorrect operational overhead figure brought down (ii) Budgeted cost statement for month 5 Incorrect calculation of the Fuel, Wage and overhead. In all three cases the candidate incorrectly assumed their calculation was for a single vehicle and multiplied by 5. (awarded 2½ marks out of 5) (c) (i) Price variance & (iii) labour rate variance were correctly calculated (ii) Material usage variance was incorrect. The candidate incorrectly used the budgeted use instead of the standard use for the distance travelled. (iv) Labour efficiency variance was incorrect. The candidate incorrectly used the budgeted time instead of the standard time for the distance travelled. (awarded 3 marks out of 6) (d) The candidate did not attempt to relate the reasons for the variances to the transport company situation (No marks awarded) This candidate, with 9½ marks out of 20, just failed to reach the pass mark. 12

14 Paper 2 13

15 14

16 Paper 2 (a)(i) Operational Overheads Individual costs correctly calculated, however the candidate incorrectly divided by the distance budgeted for a single vehicle instead of total distance budgeted for fleet of vehicles, when calculating the required absorption rate (ii) Office overheads correctly calculated (awarded 4marks out of 5) (b)(i) Budgeted cost statement for year. Individual costs for fuel and overheads correctly calculated However the candidate calculated a cost based on one vehicle instead of five. (ii) Budgeted cost statement for month 5 Incorrect calculation of the Fuel but operational overhead costs awarded an OF mark (awarded 31/2 out of 5) (c) Incorrect calculation of Labour efficiency variance. The candidate used the budgeted instead of the standard hours. (awarded 41/2 out of 6) (d) Only two out of the required reasons were related to the transport company (awarded 2marks out of 5) 15

17 Paper 3 16

18 17

19 Paper 3 Well-presented and easy to follow. (a) (b) All correct All correct (awarded 5 marks out of 5) (awarded 5 marks out of 5) (c) (d) Common error based labour efficiency variance on budgeted instead of standard hours (awarded 5 marks out of 5) Correctly related all four variance reasons to a transport company however more detail was required for the labour efficiency variance. 18

20 Pearson 190 High Holborn London WC1V 7BH Tel. +44 (0) Fax. +44 (0) uk.pearson.com/lcciinternational

Pearson LCCI Level 3 Certificate in Management Accounting (ASE3024)

") Pearson LCCI Level 3 Certificate in Management Accounting (ASE3024) Annual Qualification Review 2013/2014 For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com

Pearson LCCI Level 3 Certificate in Management Accounting (ASE3024) Annual Qualification Review 2013/2014 For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com

Cost Accounting Level 3

Cost Accounting Level 3 Model Answers Series 4 2013 (ASE3017) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk, www.pearson.com/uk

Cost Accounting Level 3 Model Answers Series 4 2013 (ASE3017) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk, www.pearson.com/uk

Pearson LCCI Level 3 Management Accounting (ASE3024)

") Pearson LCCI Level 3 Management Accounting (ASE3024) Annual Qualification Review 2014/2015 CONTENTS Introduction 2 Pass Rate Statistics 2 General Strengths and Weaknesses 3 Teaching Points by Syllabus

Pearson LCCI Level 3 Management Accounting (ASE3024) Annual Qualification Review 2014/2015 CONTENTS Introduction 2 Pass Rate Statistics 2 General Strengths and Weaknesses 3 Teaching Points by Syllabus

Mark Scheme (Results) Series Pearson LCCI Level 3 COST ACCOUNTING (ASE3017)

Series Pearson LCCI Level 3 COST ACCOUNTING (ASE3017)") Mark Scheme (Results) Series 3 2014 Pearson LCCI Level 3 COST ACCOUNTING (ASE3017) LCCI International Qualifications LCCI International Qualifications are awarded by Pearson, the UK s largest awarding

Mark Scheme (Results) Series 3 2014 Pearson LCCI Level 3 COST ACCOUNTING (ASE3017) LCCI International Qualifications LCCI International Qualifications are awarded by Pearson, the UK s largest awarding

Cost Accounting. Level 3. Model Answers. Series (Code 3016) 1 ASE /2/06

1 ASE /2/06") Cost Accounting Level 3 Model Answers Series 3 2007 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 3 2007 How to use this booklet Model Answers have been developed

Cost Accounting Level 3 Model Answers Series 3 2007 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 3 2007 How to use this booklet Model Answers have been developed

Pearson LCCI Level 3 Certificate in Accounting

Pearson LCCI Level 3 Certificate in Accounting Model Answers Series 4 2013 (ASE3012) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk,

Pearson LCCI Level 3 Certificate in Accounting Model Answers Series 4 2013 (ASE3012) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk,

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2010 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2010 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

Cost Accounting. Level 3. Model Answers. Series (Code 3616) 1 ASE /2/06

1 ASE /2/06") Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3616) 1 ASE 3016 2 06 3 3616/2/06 >f0t@w?h2`?[6zbk0j3d# Certificate in Cost Accounting Level 3 - Malaysia Series 2 2006 How to use this booklet

Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3616) 1 ASE 3016 2 06 3 3616/2/06 >f0t@w?h2`?[6zbk0j3d# Certificate in Cost Accounting Level 3 - Malaysia Series 2 2006 How to use this booklet

Level 3 Certificate in Accounting (IAS) Effective for examinations to be held after January 2008

Effective for examinations to be held after January 2008") LCCI International Qualifications Level 3 Certificate in Accounting (IAS) Syllabus Effective for examinations to be held after January 2008 For further information contact us: Tel. +44 (0) 8707 202909

LCCI International Qualifications Level 3 Certificate in Accounting (IAS) Syllabus Effective for examinations to be held after January 2008 For further information contact us: Tel. +44 (0) 8707 202909

Cost Accounting. Level 3. Model Answers. Series (Code 3016)

") Cost Accounting Level 3 Model Answers Series 4 2005 (Code 3016) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and learning

Cost Accounting Level 3 Model Answers Series 4 2005 (Code 3016) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and learning

Cambridge International Advanced Subsidiary and Advanced Level 9706 Accounting March 2016 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International Advanced Subsidiary and Advanced Level Paper 9706/12 Multiple Choice Question Number Key Question Number Key 1 D 16 C 2 A 17 B 3 D 18 B 4 C 19 D 5 A 20 B 6 D 21 C 7 C

ACCOUNTING Cambridge International Advanced Subsidiary and Advanced Level Paper 9706/12 Multiple Choice Question Number Key Question Number Key 1 D 16 C 2 A 17 B 3 D 18 B 4 C 19 D 5 A 20 B 6 D 21 C 7 C

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Level 2 Cost Accounting

Level 2 Cost Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners around

Level 2 Cost Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners around

9706 Accounting November 2008

Paper 9706/01 Multiple Choice 1 A 16 B 2 B 17 A 3 B 18 B 4 B 19 C 5 B 20 B 6 D 21 C 7 A 22 B 8 B 23 D 9 D 24 C 10 B 25 B 11 A 26 B 12 A 27 B 13 D 28 A 14 D 29 D 15 B 30 D General comments Many of the 7300

Paper 9706/01 Multiple Choice 1 A 16 B 2 B 17 A 3 B 18 B 4 B 19 C 5 B 20 B 6 D 21 C 7 A 22 B 8 B 23 D 9 D 24 C 10 B 25 B 11 A 26 B 12 A 27 B 13 D 28 A 14 D 29 D 15 B 30 D General comments Many of the 7300

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 2 2012 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 2 2012 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

Pearson LCCI Level 3 Certificate in Cost and Management Accounting (VRQ)

") Pearson LCCI Level 3 Certificate in Cost and Management Accounting (VRQ) (ASE20098) L3 SPECIFICATION Issue 2 First teaching from September 2015 Pearson LCCI Level 3 Certificate in Cost and Management

Pearson LCCI Level 3 Certificate in Cost and Management Accounting (VRQ) (ASE20098) L3 SPECIFICATION Issue 2 First teaching from September 2015 Pearson LCCI Level 3 Certificate in Cost and Management

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting November 2014 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice 1 B 16 B 2 B 17 B 3 B 18 D 4 C 19 D 5 C 20 C 6 D 21 C 7 B 22 C 8 B 23

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice 1 B 16 B 2 B 17 B 3 B 18 D 4 C 19 D 5 C 20 C 6 D 21 C 7 B 22 C 8 B 23

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2009 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2009 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

Annual Qualification Review

LCCI International Qualifications Level 2 Certificate in Book-Keeping and Accounts Annual Qualification Review 2008 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

LCCI International Qualifications Level 2 Certificate in Book-Keeping and Accounts Annual Qualification Review 2008 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

Institute of Certified Bookkeepers

Institute of Certified Bookkeepers Level III Diploma in Costing and Budgeting Introduction: Financial Accounting is the reporting of financial information to users of Financial Statements both internal

Institute of Certified Bookkeepers Level III Diploma in Costing and Budgeting Introduction: Financial Accounting is the reporting of financial information to users of Financial Statements both internal

Revision of management accounting

1 Revision of management accounting The following topics are covered in this chapter: Standard costing Flexible budgeting Absorption and marginal costing 1.1 STANDARD COSTING LEARNING SUMMARY After studying

1 Revision of management accounting The following topics are covered in this chapter: Standard costing Flexible budgeting Absorption and marginal costing 1.1 STANDARD COSTING LEARNING SUMMARY After studying

SERIES 4 EXAMINATION 2005 COST ACCOUNTING LEVEL 3. (Code No: 3016) FRIDAY 11 NOVEMBER

FRIDAY 11 NOVEMBER") SERIES 4 EXAMINATION 2005 COST ACCOUNTING LEVEL 3 (Code No: 3016) FRIDAY 11 NOVEMBER Instructions to Candidates (a) (b) (c) (d) (e) (f) (g) (h) The time allowed for this examination is 3 hours. Answer

SERIES 4 EXAMINATION 2005 COST ACCOUNTING LEVEL 3 (Code No: 3016) FRIDAY 11 NOVEMBER Instructions to Candidates (a) (b) (c) (d) (e) (f) (g) (h) The time allowed for this examination is 3 hours. Answer

FOREWORD... 1 ACCOUNTING... 2

FOREWORD... 1 ACCOUNTING... 2 GCE Advanced Level and GCE Advanced Subsidiary Level... 2 Paper 9706/01 Multiple Choice (Core)... 2 Paper 9706/02 Structured Questions... 3 Paper 9706/03 Multiple Choice (Extension)...

FOREWORD... 1 ACCOUNTING... 2 GCE Advanced Level and GCE Advanced Subsidiary Level... 2 Paper 9706/01 Multiple Choice (Core)... 2 Paper 9706/02 Structured Questions... 3 Paper 9706/03 Multiple Choice (Extension)...

Level 3 Management Accounting

Level 3 Management Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners

Level 3 Management Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2008 (3023) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2008 (3023) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Annual Qualification Review 2010

LCCI International Qualifications Level 2 Book-keeping & Accounts Annual Qualification Review 2010 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Level 2 Book-keeping & Accounts Annual Qualification Review 2010 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Unit 4: Elements of Managerial Accounting Syllabus Section Absorption (Total) costing

costing") www.xtremepapers.com Unit 4: Elements of Managerial Accounting Syllabus Section Absorption (Total) costing Learning Outcomes Suggested Teaching Activities Resources Online Resources Students will learn

www.xtremepapers.com Unit 4: Elements of Managerial Accounting Syllabus Section Absorption (Total) costing Learning Outcomes Suggested Teaching Activities Resources Online Resources Students will learn

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 4 Examination 2008 COST ACCOUNTING Level 3 Tuesday 11 November Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 4 Examination 2008 COST ACCOUNTING Level 3 Tuesday 11 November Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Write your answers in blue or black ink/ballpoint. You can only use pencil for graphs, charts, diagrams, etc.

Cost Accounting ASE3017 Level 3 Tuesday 6 November 2012 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Please ensure

Cost Accounting ASE3017 Level 3 Tuesday 6 November 2012 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Please ensure

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting November 2013 Principal Examiner Report for Teachers

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 D 2 C 17 B 3 C 18 B 4 B 19 A 5 C 20 B 6 B 21 C 7 C 22 D 8 C 23 D 9 C 24 C 10 A 25 B 11 A 26

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 D 2 C 17 B 3 C 18 B 4 B 19 A 5 C 20 B 6 B 21 C 7 C 22 D 8 C 23 D 9 C 24 C 10 A 25 B 11 A 26

Annual Qualification Review

LCCI International Qualifications Level 2 Certificate in Business Calculations Annual Qualification Review 2011 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

LCCI International Qualifications Level 2 Certificate in Business Calculations Annual Qualification Review 2011 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

Cambridge International Advanced Subsidiary and Advanced Level 9706 Accounting June 2016 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International Advanced Subsidiary and Advanced Level Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 C 2 A 17 A 3 C 18 B 4 D 19 B 5 B 20 A 6 C 21 C 7 C

ACCOUNTING Cambridge International Advanced Subsidiary and Advanced Level Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 C 2 A 17 A 3 C 18 B 4 D 19 B 5 B 20 A 6 C 21 C 7 C

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 2 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 2 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Cost Accounting. Level 3. Model Answers. Series (Code 3016) 1 ASE /2/06

1 ASE /2/06") Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 2 2006 How to use this booklet Model Answers have been developed

Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 2 2006 How to use this booklet Model Answers have been developed

CERTIFICATE IN MANAGEMENT ACCOUNTING

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 29 May Subject Code: 3623/M Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 29 May Subject Code: 3623/M Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2012 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice (Core) Question Number Key Question Number Key 1 A 16 A 2 B 17 C 3 D 18 A 4 D 19 C 5 B 20 B

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice (Core) Question Number Key Question Number Key 1 A 16 A 2 B 17 C 3 D 18 A 4 D 19 C 5 B 20 B

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2015 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 A 2 C 17 A 3 D 18 B 4 B 19 A 5 D 20 D 6 A 21

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 A 2 C 17 A 3 D 18 B 4 B 19 A 5 D 20 D 6 A 21

Management Accounting

Model Answers for Management Accounting THIRD LEVEL Series 2 2002 (Code 3023) LCCI Examinations Board ASP M 1147 >f0t@wjy2[2`ed:yed# Management Accounting Third Level Series 2 2002 How to use this booklet

Model Answers for Management Accounting THIRD LEVEL Series 2 2002 (Code 3023) LCCI Examinations Board ASP M 1147 >f0t@wjy2[2`ed:yed# Management Accounting Third Level Series 2 2002 How to use this booklet

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2011 Principal Examiner Report for Teachers

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice (Core) Question Number Key Question Number Key 1 D 16 C 2 D 17 C 3 C 18 C 4 B 19 B 5 D 20 D 6 A 21 C 7 D 22 B 8 A 23 D 9 A 24 A 10 C 25 A 11

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice (Core) Question Number Key Question Number Key 1 D 16 C 2 D 17 C 3 C 18 C 4 B 19 B 5 D 20 D 6 A 21 C 7 D 22 B 8 A 23 D 9 A 24 A 10 C 25 A 11

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2014 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 C 16 B 2 B 17 D 3 C 18 C 4 C 19 A 5 B 20 A 6 C 21

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 C 16 B 2 B 17 D 3 C 18 C 4 C 19 A 5 B 20 A 6 C 21

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 3 Examination 2008 COST ACCOUNTING Level 3 Friday 6 June Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your answers

Series 3 Examination 2008 COST ACCOUNTING Level 3 Friday 6 June Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your answers

December CS Executive Programme Module - I Paper - 2

December - 2015 CS Executive Programme Module - I Paper - 2 (New Syllabus) Cost and Management Accounting Total number of questions: 100 Maximum marks: 100 Assertion A: 1. In management accounting, firm

December - 2015 CS Executive Programme Module - I Paper - 2 (New Syllabus) Cost and Management Accounting Total number of questions: 100 Maximum marks: 100 Assertion A: 1. In management accounting, firm

Write your answers in blue or black ink/ballpoint. You can only use pencil for graphs, charts, diagrams, etc.

Cost Accounting ASE3017 Level 3 Wednesday 3 April 2013 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Instructions

Cost Accounting ASE3017 Level 3 Wednesday 3 April 2013 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Instructions

Cost Accounting. Level 3. Model Answers. Series (Code 3016)

") Cost Accounting Level 3 Model Answers Series 4 2007 (Code 3016) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and learning

Cost Accounting Level 3 Model Answers Series 4 2007 (Code 3016) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and learning

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2012 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2012 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Pearson Edexcel International Advanced Level Accounting

Pearson Edexcel International Advanced Level Accounting International Advanced Subsidiary (WAC11) The Accounting System and Costing Exemplar scripts with examiner commentaries Section A: Question 1 Issue

Pearson Edexcel International Advanced Level Accounting International Advanced Subsidiary (WAC11) The Accounting System and Costing Exemplar scripts with examiner commentaries Section A: Question 1 Issue

Management Accounting

Management Accounting Level 3 Model Answers Series 3 2008 (Code 3023) 1 ASE 3023 2 06 1 3023/2/06 >f0t@w9w2`?[i]bkbw5k# Management Accounting Level 3 Series 3 2008 How to use this booklet Model Answers

Management Accounting Level 3 Model Answers Series 3 2008 (Code 3023) 1 ASE 3023 2 06 1 3023/2/06 >f0t@w9w2`?[i]bkbw5k# Management Accounting Level 3 Series 3 2008 How to use this booklet Model Answers

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 4 2009 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 4 2009 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

Management Accounting

Management Accounting Level 3 Model Answers Series 2 2008 Malaysia (Code 3623) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment

Management Accounting Level 3 Model Answers Series 2 2008 Malaysia (Code 3623) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment

Please ensure your answers are written clearly, or marks may be lost. Do NOT open this paper until you are told to do so by the supervisor.

Cost Accounting ASE3017 Level 3 Tuesday 19 November 2013 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Please

Cost Accounting ASE3017 Level 3 Tuesday 19 November 2013 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Please

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting November 2011 Principal Examiner Report for Teachers

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 B 16 C 2 D 17 A 3 C 18 C 4 B 19 D 5 A 20 A 6 A 21 B 7 B 22 C 8 A 23 C 9 D 24 B 10 C 25 D 11 B 26

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 B 16 C 2 D 17 A 3 C 18 C 4 B 19 D 5 A 20 A 6 A 21 B 7 B 22 C 8 A 23 C 9 D 24 B 10 C 25 D 11 B 26

Management Accounting

Management Accounting Level 3 Model Answers Series 4 2007 (Code 3023) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and

Management Accounting Level 3 Model Answers Series 4 2007 (Code 3023) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and

Pearson LCCI Certificate in Accounting (VRQ) Level 3 (ASE20104)

Level 3 (ASE20104)") Pearson LCCI Certificate in Accounting (VRQ) Level 3 (ASE20104) Examiners Report November 2016 1 LCCI Certificate in Accounting ASE20104 LCCI Qualifications LCCI qualifications come from Pearson, the world

Pearson LCCI Certificate in Accounting (VRQ) Level 3 (ASE20104) Examiners Report November 2016 1 LCCI Certificate in Accounting ASE20104 LCCI Qualifications LCCI qualifications come from Pearson, the world

Ordering costs Any two of the following: Postage, Paperwork, Telephone, Internet, , Purchasing Officer's salary

EDUCATION DEVELOPMENT INTERNATIONAL PLC SAMPLE PAPER ANSWERS 2008 COST ACCOUNTING (ASE3017) LEVEL 3 QUESTION 1 (a) (i) Stock holding costs Any two of the following: Insurance, Material handling, Storekeeper's

EDUCATION DEVELOPMENT INTERNATIONAL PLC SAMPLE PAPER ANSWERS 2008 COST ACCOUNTING (ASE3017) LEVEL 3 QUESTION 1 (a) (i) Stock holding costs Any two of the following: Insurance, Material handling, Storekeeper's

Pearson LCCI Level 3 Certificate in Accounting (VRQ)

") Pearson LCCI Level 3 Certificate in Accounting (VRQ) (ASE3012X) L3 SPECIFICATION Issue 2 Pearson LCCI Level 3 Certificate in Accounting (VRQ) (ASE3012X) Specification Issue 2 Edexcel, BTEC and LCCI qualifications

Pearson LCCI Level 3 Certificate in Accounting (VRQ) (ASE3012X) L3 SPECIFICATION Issue 2 Pearson LCCI Level 3 Certificate in Accounting (VRQ) (ASE3012X) Specification Issue 2 Edexcel, BTEC and LCCI qualifications

MANAGEMENT INFORMATION

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 1 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 1 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

RELATIONAL DIAGRAM OF MAIN CAPABILITIES

Syllabus MAIN CAPABILITIES APM (P5) On successful completion of this paper, candidates should be able to: A Explain the nature and purpose of cost and management accounting PM (F5) FM (F9) B Describe costs

Syllabus MAIN CAPABILITIES APM (P5) On successful completion of this paper, candidates should be able to: A Explain the nature and purpose of cost and management accounting PM (F5) FM (F9) B Describe costs

Management Accounting 2 nd Year Solutions

Management Accounting 2 nd Year Solutions August 2016 Exam Paper, Solutions & Examiners Comments Page 1 of 25 NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by Accounting

Management Accounting 2 nd Year Solutions August 2016 Exam Paper, Solutions & Examiners Comments Page 1 of 25 NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by Accounting

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 3 2010 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 3 2010 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Question Key Number Number Key 1 D 16 C 2 C 17 A 3 C 18 C 4 B 19 C 5 D 20 D 6 A 21 C 7 A 22 A 8 D 23 D 9 C 24 B 10 C 25 B 11 A 26 A 12 B 27

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Question Key Number Number Key 1 D 16 C 2 C 17 A 3 C 18 C 4 B 19 C 5 D 20 D 6 A 21 C 7 A 22 A 8 D 23 D 9 C 24 B 10 C 25 B 11 A 26 A 12 B 27

PAPER C01 Fundamentals of Management Accounting Acorn chapters

PAPER C01 Fundamentals of Management Accounting Acorn chapters 1 Classification of costs 2 The context of management accounting 3 Absorbing fixed production overhead 4 Absorption and marginal costing 5

PAPER C01 Fundamentals of Management Accounting Acorn chapters 1 Classification of costs 2 The context of management accounting 3 Absorbing fixed production overhead 4 Absorption and marginal costing 5

Analysing costs and revenues

Osborne Books Tutor Zone Analysing costs and revenues Practice assessment 1 Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e This assessment relates to

Osborne Books Tutor Zone Analysing costs and revenues Practice assessment 1 Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e This assessment relates to

Mock One. Performance Management F5PM-MK1-Z16-A. Answers & Marking Scheme. Becker Study School DeVry/Becker Educational Development Corp.

Mock One Performance Management F5PM-MK-Z6-A Answers & Marking Scheme 206 DeVry/Becker Educational Development Corp. Question Answer Mark Question Answer Mark Section A Section B D 6 A 2 C 7 A 3 C 8 A

Mock One Performance Management F5PM-MK-Z6-A Answers & Marking Scheme 206 DeVry/Becker Educational Development Corp. Question Answer Mark Question Answer Mark Section A Section B D 6 A 2 C 7 A 3 C 8 A

Study the REQUIRED section of each question carefully and extract the data required for your answers from the information supplied.

Series 4 Examination 2010 COST ACCOUNTING Level 3 Monday 6 December Subject Code: 3717/S Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks. Study

Series 4 Examination 2010 COST ACCOUNTING Level 3 Monday 6 December Subject Code: 3717/S Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks. Study

Management Accounting

Examiner s Report and Model Answers for Management Accounting THIRD LEVEL Series 4 (Code 3023) 2000 LCCI Examinations Board MH N T336 9 RNM >f2[ew2r@o2`0t1f3]e]2r2[1_# Management Accounting Third Level

Examiner s Report and Model Answers for Management Accounting THIRD LEVEL Series 4 (Code 3023) 2000 LCCI Examinations Board MH N T336 9 RNM >f2[ew2r@o2`0t1f3]e]2r2[1_# Management Accounting Third Level

Cambridge International Advanced Subsidiary and Advanced Level 9706 Syllabus March 2018 Principal Examiner Report for Teachers. Question Key Number

ACCOUNTING 9706 Syllabus March 2018 Paper 9706/12 Multiple Choice Question Question Key Number Number Key 1 D 16 B 2 A 17 B 3 D 18 A 4 B 19 A 5 B 20 B 6 B 21 D 7 A 22 B 8 C 23 D 9 C 24 D 10 B 25 B 11 A

ACCOUNTING 9706 Syllabus March 2018 Paper 9706/12 Multiple Choice Question Question Key Number Number Key 1 D 16 B 2 A 17 B 3 D 18 A 4 B 19 A 5 B 20 B 6 B 21 D 7 A 22 B 8 C 23 D 9 C 24 D 10 B 25 B 11 A

MANAGEMENT INFORMATION

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

Part 1 Examination Paper 1.2. Section A 10 C 11 C 2 A 13 C 1 B 15 C 6 C 17 B 18 C 9 D 20 C 21 C 22 D 23 D 24 C 25 C

Answers Part 1 Examination Paper 1.2 Financial Information for Management June 2007 Answers Section A 1 B 2 A 3 A 4 A 5 D 6 C 7 B 8 C 9 D 10 C 11 C 12 A 13 C 14 B 15 C 16 C 17 B 18 C 19 D 20 C 21 C 22

Answers Part 1 Examination Paper 1.2 Financial Information for Management June 2007 Answers Section A 1 B 2 A 3 A 4 A 5 D 6 C 7 B 8 C 9 D 10 C 11 C 12 A 13 C 14 B 15 C 16 C 17 B 18 C 19 D 20 C 21 C 22

Preparing and using budgets

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

Management Accounting Fundamentals (FMAF)

") POST EXM GUIE May 2001 Exam Management ccounting Fundamentals (FMF) IM publishes a Question and nswer booklet for each paper of the May 2001 exam which is essential reading for students and tutors. The

POST EXM GUIE May 2001 Exam Management ccounting Fundamentals (FMF) IM publishes a Question and nswer booklet for each paper of the May 2001 exam which is essential reading for students and tutors. The

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 3 Examination 2007 COST ACCOUNTING Level 3 Tuesday 5 June Subject Code: 3716 (S) Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 3 Examination 2007 COST ACCOUNTING Level 3 Tuesday 5 June Subject Code: 3716 (S) Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Management Accounting. Pilot Paper 3 Questions and Suggested Solutions

Management Accounting Pilot Paper 3 Questions and Suggested Solutions NOTES TO USERS ABOUT PILOT PAPERS Pilot papers are published by Accounting Technicians Ireland. They are intended to provide guidance

Management Accounting Pilot Paper 3 Questions and Suggested Solutions NOTES TO USERS ABOUT PILOT PAPERS Pilot papers are published by Accounting Technicians Ireland. They are intended to provide guidance

Paper P1 Performance Operations Post Exam Guide November 2012 Exam. General Comments

General Comments This sitting produced a reasonably good pass rate although lower than in the last two main exam sittings. Performance varied considerably by section and from previous sittings. There were

General Comments This sitting produced a reasonably good pass rate although lower than in the last two main exam sittings. Performance varied considerably by section and from previous sittings. There were

MANAGEMENT ACCOUNTING

Series 3 Examination 2007 MANAGEMENT ACCOUNTING Level 3 Tuesday 12 June Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 3 Examination 2007 MANAGEMENT ACCOUNTING Level 3 Tuesday 12 June Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Management Accounting (F2/FMA) September 2015 to August 2016 (for CBE exams up to 22 September 2016)

September 2015 to August 2016 (for CBE exams up to 22 September 2016)") Management Accounting (F2/FMA) September 2015 to August 2016 (for CBE exams up to 22 September 2016) This syllabus and study guide are designed to help with teaching and learning and is intended to provide

Management Accounting (F2/FMA) September 2015 to August 2016 (for CBE exams up to 22 September 2016) This syllabus and study guide are designed to help with teaching and learning and is intended to provide

2016 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC9: COSTING AND BUDGETARY CONTROL

EXAMINATION NO. 2016 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC9: COSTING AND BUDGETARY CONTROL FRIDAY 2 DECEMBER 2016 TIME ALLOWED: 3 HOURS 9.00 AM - 12.00 NOON INSTRUCTIONS 1. You are allowed

EXAMINATION NO. 2016 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC9: COSTING AND BUDGETARY CONTROL FRIDAY 2 DECEMBER 2016 TIME ALLOWED: 3 HOURS 9.00 AM - 12.00 NOON INSTRUCTIONS 1. You are allowed

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice 11 Question Number Key Question Number Key 1 C 16 A 2 B 17 B 3 A 18 B 4 C 19 D 5 D 20 B 6 D 21 B 7 A 22 D 8 A 23 C 9 C 24 B 10 D 25 D 11 C 26 A 12 A

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice 11 Question Number Key Question Number Key 1 C 16 A 2 B 17 B 3 A 18 B 4 C 19 D 5 D 20 B 6 D 21 B 7 A 22 D 8 A 23 C 9 C 24 B 10 D 25 D 11 C 26 A 12 A

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE SECONDARY EDUCATION CERTIFICATE EXAMINATION JUNE 2004

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE SECONDARY EDUCATION CERTIFICATE EXAMINATION JUNE 2004 PRINCIPLES OF ACCOUNTS Copyright 2004 Caribbean Examinations

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE SECONDARY EDUCATION CERTIFICATE EXAMINATION JUNE 2004 PRINCIPLES OF ACCOUNTS Copyright 2004 Caribbean Examinations

10,000 units x 24 = 240,000, or 5,000 hours x 48 = 240,000. the actual price of materials per kilogram

NVQ/SVQ Level 4 in Accounting Contributing to the Management of Performance and Enhancement of Value (PEV) (2003 standards) June 2006 SUGGESTED ANSWERS Note: The suggested answers may, in parts, be longer

NVQ/SVQ Level 4 in Accounting Contributing to the Management of Performance and Enhancement of Value (PEV) (2003 standards) June 2006 SUGGESTED ANSWERS Note: The suggested answers may, in parts, be longer

MGT402 - COST & MANAGEMENT ACCOUNTING

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

P1 Performance Operations Post Exam Guide May 2014 Exam. General Comments

General Comments Performance on this paper was reasonably good with the pass rate above average for the 2010 syllabus. Many candidates scored very highly and there were fewer marginal scripts. However

General Comments Performance on this paper was reasonably good with the pass rate above average for the 2010 syllabus. Many candidates scored very highly and there were fewer marginal scripts. However

Introduction to Finance. 1 March Examination Paper. Time: 3 hours

Introduction to Finance 1 March 2016 Examination Paper Answer any FOUR (4) questions. Clearly cross out surplus answers. Failure to do this will result in only the first FOUR (4) answers being marked.

Introduction to Finance 1 March 2016 Examination Paper Answer any FOUR (4) questions. Clearly cross out surplus answers. Failure to do this will result in only the first FOUR (4) answers being marked.

SUGGESTED SOLUTIONS. KE2 Management Accounting Information. March All Rights Reserved

SUGGESTED SOLUTIONS KE2 Management Accounting Information March 2015 All Rights Reserved SECTION 1 Answer 01 1(a) 1.1 Relevant Learning Outcome/s: 1.1.2 Correct answer: C Direct cost can either be variable

SUGGESTED SOLUTIONS KE2 Management Accounting Information March 2015 All Rights Reserved SECTION 1 Answer 01 1(a) 1.1 Relevant Learning Outcome/s: 1.1.2 Correct answer: C Direct cost can either be variable

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE CARIBBEAN ADVANCED PROFICIENCY EXAMINATION MAY/JUNE 2014

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE CARIBBEAN ADVANCED PROFICIENCY EXAMINATION MAY/JUNE 2014 ACCOUNTING Copyright 2014 Caribbean Examinations Council

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE CARIBBEAN ADVANCED PROFICIENCY EXAMINATION MAY/JUNE 2014 ACCOUNTING Copyright 2014 Caribbean Examinations Council

COST ACCOUNTING AND FINANCIAL MANAGEMENT

STUDY MATERIAL Intermediate (IPC) Course PAPER : 3 COST ACCOUNTING AND FINANCIAL MANAGEMENT Part 1 : Cost Accounting VOLUME I BOARD OF STUDIES THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA This study

STUDY MATERIAL Intermediate (IPC) Course PAPER : 3 COST ACCOUNTING AND FINANCIAL MANAGEMENT Part 1 : Cost Accounting VOLUME I BOARD OF STUDIES THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA This study

Management Accounting. Sample Paper 1 Questions and Suggested Solutions

Management Accounting Sample Paper 1 Questions and Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to provide guidance

Management Accounting Sample Paper 1 Questions and Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to provide guidance

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 2 Examination 2011 COST ACCOUNTING Level 3 Thursday 7 April Subject Code: 3017 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks. Write your

Series 2 Examination 2011 COST ACCOUNTING Level 3 Thursday 7 April Subject Code: 3017 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks. Write your

Paper 1.2. Financial Information for Management PART 1 FRIDAY 10 DECEMBER 2004 QUESTION PAPER. Time allowed 3 hours

Financial Information for Management PRT 1 FRIY 10 EEMER 2004 QUESTION PPER Time allowed 3 hours This paper is divided into two sections Section LL 25 questions are compulsory and MUST be answered Paper

Financial Information for Management PRT 1 FRIY 10 EEMER 2004 QUESTION PPER Time allowed 3 hours This paper is divided into two sections Section LL 25 questions are compulsory and MUST be answered Paper

Management Accounting (MA)/FMA September 2018 to August 2019

/FMA September 2018 to August 2019") Management Accounting (MA)/FMA September 2018 to August 2019 Guide to structure of the syllabus and Study guide This syllabus and study guide are designed to help with teaching and learning and is intended

Management Accounting (MA)/FMA September 2018 to August 2019 Guide to structure of the syllabus and Study guide This syllabus and study guide are designed to help with teaching and learning and is intended

STUDY MATERIAL BASED CONTENTS

STUDY MATERIAL BASED CONTENTS Paper 3 Cost and Management Accounting Syllabus....................................... 3. Examination Trend Analysis........................ 3.7 Line Chart Showing Relative

STUDY MATERIAL BASED CONTENTS Paper 3 Cost and Management Accounting Syllabus....................................... 3. Examination Trend Analysis........................ 3.7 Line Chart Showing Relative

Higher National Unit specification. General information for centres. Preparing Financial Forecasts. Unit code: F84R 35

Higher National Unit specification General information for centres Unit title: Preparing Financial Forecasts Unit code: F84R 35 Unit purpose: This Unit is designed to enable candidates to develop an understanding

Higher National Unit specification General information for centres Unit title: Preparing Financial Forecasts Unit code: F84R 35 Unit purpose: This Unit is designed to enable candidates to develop an understanding

Cambridge International General Certificate of Secondary Education 0452 Accounting June 2016 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key messages Candidates should read the question carefully before attempting to answer. A label for

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key messages Candidates should read the question carefully before attempting to answer. A label for

Management Accounting

Management Accounting 2 nd Year Examination August 2015 Solutions & Marking Scheme & Examiner s Comments Page 1 of 33 NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by

Management Accounting 2 nd Year Examination August 2015 Solutions & Marking Scheme & Examiner s Comments Page 1 of 33 NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by

SERIES 4 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL. (Code No: 3023) TUESDAY 13 NOVEMBER

TUESDAY 13 NOVEMBER") SERIES 4 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL (Code No: 3023) TUESDAY 13 NOVEMBER Instructions to Candidates (d) (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions.

SERIES 4 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL (Code No: 3023) TUESDAY 13 NOVEMBER Instructions to Candidates (d) (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions.

Pearson LCCI Level 4 Certificate in Management Accounting (VRQ)

") Pearson LCCI Level 4 Certificate in Management Accounting (VRQ) (ASE20102) L4 SPECIFICATION First teaching from January 2015 Pearson LCCI Level 4 Certificate in Management Accounting (VRQ) (ASE20102)

Pearson LCCI Level 4 Certificate in Management Accounting (VRQ) (ASE20102) L4 SPECIFICATION First teaching from January 2015 Pearson LCCI Level 4 Certificate in Management Accounting (VRQ) (ASE20102)

(AA22) COST ACCOUNTING AND REPORTING

COST ACCOUNTING AND REPORTING") All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JANUARY 2017 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JANUARY 2017 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

Level 3 Certificate in Advanced Business Calculations

LCCI International Qualifications Level 3 Certificate in Advanced Business Calculations Syllabus Effective from 2001 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

LCCI International Qualifications Level 3 Certificate in Advanced Business Calculations Syllabus Effective from 2001 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

Detailed competency map: Knowledge requirements. (AAT examination)

") Detailed competency map: Knowledge requirements (AAT examination) Fields of competency The items listed are shown with an indicator of the minimum acceptable level of competency, based on a three-point

Detailed competency map: Knowledge requirements (AAT examination) Fields of competency The items listed are shown with an indicator of the minimum acceptable level of competency, based on a three-point

INSTITUTE OF CHARTERED ACCOUNTANTS IN MALAWI

INSTITUTE OF CHARTERED ACCOUNTANTS IN MALAWI JUNE 2017 TC9 COSTING & BUDGETARY CONTROL EXAMINER S REPORT GENERAL COMMENTS The performance of students in the June 2017 examinations was not very different

INSTITUTE OF CHARTERED ACCOUNTANTS IN MALAWI JUNE 2017 TC9 COSTING & BUDGETARY CONTROL EXAMINER S REPORT GENERAL COMMENTS The performance of students in the June 2017 examinations was not very different

Management Accounting

Management Accounting Course map This document outlines the course structure. ACCA: FMA-F2.x Management Accounting Introduction course orientation Lesson 1: Welcome Lesson 2: What, when and why? Lesson

Management Accounting Course map This document outlines the course structure. ACCA: FMA-F2.x Management Accounting Introduction course orientation Lesson 1: Welcome Lesson 2: What, when and why? Lesson