Cost Accounting. Level 3. Model Answers. Series (Code 3616) 1 ASE /2/06

|

|

|

- Diana Miller

- 5 years ago

- Views:

Transcription

1")

1 Cost Accounting Level 3 Model Answers Series (Code 3616) 1 ASE /2/06 >f0t@w?h2`?[6zbk0j3d#

2 Certificate in Cost Accounting Level 3 - Malaysia Series How to use this booklet Model Answers have been developed by Education Development International plc (EDI) to offer additional information and guidance to Centres, teachers and candidates as they prepare for LCCI International qualifications. The contents of this booklet are divided into 3 elements: (1) Questions reproduced from the printed examination paper (2) Model Answers summary of the main points that the Chief Examiner expected to see in the answers to each question in the examination paper, plus a fully worked example or sample answer (where applicable) (3) Helpful Hints where appropriate, additional guidance relating to individual questions or to examination technique Teachers and candidates should find this booklet an invaluable teaching tool and an aid to success. EDI provides Model Answers to help candidates gain a general understanding of the standard required. The general standard of model answers is one that would achieve a Distinction grade. EDI accepts that candidates may offer other answers that could be equally valid. Education Development International plc 2006 All rights reserved; no part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without prior written permission of the Publisher. The book may not be lent, resold, hired out or otherwise disposed of by way of trade in any form of binding or cover, other than that in which it is published, without the prior consent of the Publisher. 3616/2/06/MA 2

3 QUESTION 1 Edge Limited makes and distributes a single product and budgeted to produce 2,000 units in a month. The standard production cost of one unit of the product is as follows: RM per unit Direct materials (8 kilos x RM7.50 per kilo) Direct labour (3 hours x RM24 per hour) Variable production overheads (3 hours x RM6 per hour) Fixed production overheads (3 hours x RM3 per hour) 9.00 Total Standard Production Cost (per unit) The actual production for the month was 2,200 units and the actual costs incurred were as follows: RM Direct materials purchased at 18,800 kilos 138,180 Direct labour at 7,000 hours 142,560 Variable production overheads 36,750 Fixed production overheads 19,500 The opening stock of raw materials was 3,000 kilos, valued at standard purchase price, the raw material price variance being calculated at the time of purchase. 19,800 kilos of materials were issued to production in the month. There was no opening stock or closing stock of work in progress. REQUIRED Prepare the following accounts in the company s integrated accounting system: (a) Raw Material Stock (b) Production Overhead (c) Work in Progress (5 marks) (6 marks) (9 marks) When compiling the above, show clearly all relevant variances within the three above accounts. (Total 20 marks) 3616/2/06/MA 3

4 MODEL ANSWERS TO QUESTION 1 (a) Raw Material Stock Account (RMs) Opening stock (3,000 x RM 7.50) 22,500 Work in Progress 148,500 Creditors 138,180 Closing stock (2,000 x RM 7.50) 15,000 Material Price Variance 2, , ,500 (b) Production Overhead Account (RMs) Creditors 56,250 W I P - Variable 42,000 Variable overhead expenditure 5,250 W I P - Fixed 18,000 variance Fixed overhead exp variance 1,500 61,500 61,500 (c) Work in Progress Account (RMs) Raw Materials 148,500 Labour efficiency variance 9,600 Direct Labour 168,000 Direct mat usage variance 16,500 Production overhead - variable 42,000 Var o/h efficiency variance 2,400 Production overhead - fixed 18,000 Transfer to Finished Goods 349,800 Fixed o/h volume variance 1, , , /2/06/MA 4

5 MODEL ANSWERS TO QUESTION 1 CONTINUED Workings: Material Price Variance Standard (18,800 x RM7.50) = 141,000 less actual 138,180 = RM2,820 Fav Material usage variance = Issued to production 148,500 (19,800 kgs x RM7.5) less standard usage 132,000 (2,200 units x RM60 ) = RM16,500 Adv Labour rate variance Standard (7,000 x RM24) = RM168,000 less actual RM142,560 = RM25,440 Fav Labour efficiency variance = Actual hrs 7,000 less standard hrs 6,600 (2,200 x 3) = 400 hours x RM24 = RM9,600 Adv Variable overhead expenditure variance = Standard (7,000 x RM6) RM42,000 less actual RM36,750 = RM5,250 Fav Variable overhead efficiency variance = Standard (2,200 x 3 x 6 ) RM39,600 less actual hours 7,000 x standard rate RM6 = RM42,000 = RM2,400 Adv OR 400 hrs x RM6 = RM2,400 Fixed overhead volume variance = Absorbed (2,200 x RM9) = RM19,800 less budget RM18,000 = RM1,800 Fav Fixed overhead expenditure variance = Budget (2,000 x RM9) RM18,000 less actual RM19,500 = RM1,500 Adv Work in Progress (19,800 x RM7.50) Transfer to Finished goods = 2,200 units x RM159 = RM148,500 = RM349, /2/06/MA 5

6 QUESTION 2 Lewis Court Limited manufactures a single product. The budget for a period includes the following: Sales/Production Standard selling price per unit Standard cost per unit 800 units RM145 RM125 During the period the actual results were as follows: Sales/Production 780 units Sales revenue RM116,450 Total cost RM95, 580 REQUIRED (a) Calculate the following variances for the period: (i) (ii) sales price variance sales volume profit variance (iii) total cost variance (iv) total profit variance (8 marks) Roland Wiseman Limited makes a single product and uses a standard absorption costing system. The production budgets for a period include the following: Production 18,000 units Direct labour hours per unit 4.5 During the period the actual results were: Production 18,600 units Direct labour hours 87,520 REQUIRED (b) Calculate for the period the following production ratios: (i) efficiency (iii) capacity (iii) production volume (activity) (c) Explain the meaning of the term Standard Hour (9 marks) (3 marks) (Total 20 marks) 3616/2/06/MA 6

7 MODEL ANSWERS TO QUESTION 2 (a) i) Sales price variance (780 x RM145) = 113,100 RM113,100 less RM116,450 = RM3,350 Fav ii) Sales volume profit variance ( ) 20 x RM20 (RM145 RM125) = RM400 Adv iii) Total cost variance (780 x RM125) = RM97,500 RM97,500 less 95,580 = RM1,920 Fav iv) Total profit variance (800 x RM20) = RM16,000 less (RM116,450 less RM95,580) RM20,870 = RM4,870 Fav (b) (i) Production efficiency ratio Standard direct labour hours of actual production x 100% Actual direct labour hours worked = 83,700 hrs x 100% 87,520 hrs (83,700 = 18,600 x 4.5) = % (ii) Production capacity ratio Actual direct labour hours worked x 100% Budgeted direct labour hours = 87,520 hrs x 100% 81,000 hrs = % (81,000 = 18,000 x 4.5) (iii) Production volume (activity) ratio Standard direct labour hours of actual production x 100% Budgeted direct labour hours = 83,700 hrs x 100% 81,000 hrs = % (c) The term Standard Hour refers to the QUANTITY of work achievable at standard efficiency in an hour. 3616/2/06/MA 7

8 QUESTION 3 Barmby Limited manufactures and sells a single product A, which uses raw material X in its production. The sales budget for the next three month period is as follows: Month 1 Month 2 Month 3 Product A (units) 54,500 55,624 57,535 Stock of finished goods at the start of the budget period is 5,553 units. This is to be increased to 10,000 by the end of the first month and increased by 2,000 units a month thereafter. 2% of the finished goods produced are budgeted to be rejected. These will be disposed of with no further value The quantity of raw material X required per unit of finished product is 3 kilos. In addition to this requirement for raw material in the finished product, allowance has to be made for a 10% loss in weight in the preparation of material X. Stock of raw material X at the start of the budget period is to be 24,000 kilos. At the end of each month in the budget period the stock of material X should be increased by 10%. The price for material X is expected to be RM5 per kilo. REQUIRED (a) Prepare the following budgets for each of months 1, 2 and 3: (i) Production of product A (units) (7 marks) (ii) Purchases of raw material X (kilos and total RMs) (9 marks) (b) Define the term principle budget factor and explain its influence on the budget setting process. (4 marks) (Total 20 marks) 3616/2/06/MA 8

9 MODEL ANSWERS TO QUESTION 3 (a) (i) Production Budget (units of product A) Units Month 1 Month 2 Month 3 Sales 54,500 55,624 57,535 Less opening stock (5,553) (10,000) (12,000) Plus closing stock 10,000 12,000 14,000 Good production 58,947 57,624 59,535 Rejected manufacture 1,203 1,176 1,215 Gross Production 60,150 58,800 60,750 Example of rejected production = 58,947 / 98 x 2 = 1,203 (ii) Material Purchases Budget (kilos and total RMs of raw material X): Month 1 Month 2 Month 3 kilos kilos kilos Required for final production (W1) 180, , ,250 Plus wastage (W2) 20,050 19,600 20, , , ,500 Less opening stock (24,000) (26,400) (29,040) Plus closing stock 26,400 29,040 31,944 Purchases (kilos) 202, , ,404 x RM5 x RM5 x RM5 Purchases (RM) 1,014, ,200 1,027,020 W1 Gross Production units x 3kgs 60,150 x 3 = 180,450 Gross Production units x 3kgs 58,800 x 3 = 176,400 Gross Production units x 3kgs 60,750 x 3 = 182,250 W2 180,450 /90 x 10 = 20,050 kgs 176,400 /90 x 10 = 19,600 kgs 182,250 /90 x 10 = 20,250 kgs (b) The principal budget factor is the factor which restricts the activities of the organisation during the budget period. This budget must be prepared first and all the other budgets will be derived from it. 3616/2/06/MA 9

10 QUESTION 4 Burgess Facey Ltd has three production cost centres (A, B and C) and two service cost centres (Stores and Maintenance), in its factory. The company re-apportions the costs of the service cost centres to the production cost centres in order to calculate budgeted overhead absorption rates. The budgeted production overhead costs for a period allocated to the five cost centres were as follows: Production cost centres Service cost centres A B C Stores Maintenance Allocated overheads (RM) 225, , ,000 87,000 52,500 Other budgeted overheads, which have yet to be apportioned, are as follows (RM): Rent and Rates 180,000 Depreciation 225,000 Supervision 360,000 In addition, the following budgeted information is available for each cost centre: Production cost centres Service cost centres A B C Stores Maintenance Number of employees Floor area (m²) 4,500 3,600 2,400 3,000 1,500 Machine cost (RM) 420, , ,000 24,000 36,000 Usage of stores 40% 30% 20% Nil 10% Usage of maintenance 35% 30% 15% 20% nil Budgeted machine hours for the period were 60,000 for Production Cost Centre A, 39,850 for Production Cost Centre B, and 30,000 for Production Cost Centre C Actual results for the period were as follows: Production cost centres A B C Allocated overheads (RM) 585, , ,250 (allocated and apportioned) Actual machine hours 58,750 39,200 29,780 REQUIRED (a) Produce a budgeted overhead distribution table, for the period, showing the allocated and apportioned costs for the five cost centres (3 marks) 3616/2/06/MA 10

11 QUESTION 4 CONTINUED (b) Re-apportion the budgeted service cost centre overheads to the production cost centres, using simultaneous equations. (Full marks will not be awarded for other methods). (8 marks) (c) Calculate a pre-determined overhead absorption rate, to TWO decimal places of RM per machine hour, for each of the three production cost centres. (d) Calculate the over/under absorbed overhead for each production cost centre. (3 marks) (6 marks) (Total 20 marks) 3616/2/06/MA 11

12 MODEL ANSWERS TO QUESTION 4 (a) Production Cost Centres Service Cost Centres Cost (RM) A B C Stores Maintenance Allocated 225, , ,000 87,000 52,500 Rent and Rates (W1) 54,000 43,200 28,800 36,000 18,000 Depreciation (W2) 105,000 67,500 37,500 6,000 9,000 Supervision (W3) 132, ,000 90,000 12,000 24, , , , , ,500 W1 Rent and Rates based on floor area PCC A = RM180,000 / 15,000m2 x 4,500 m2 W2 Depreciation based on machine cost PCC A = RM225,000 / RM900,000 x RM420,000 W3 Supervision based on employees PCC A = RM360,000 / 180 x 66 = RM54,000 = RM105,000 = RM132,000 (b) Secondary apportionment of service cost centre overheads Production Cost Centres Service Cost Centres Cost (RM) A B C Stores Maintenance Balances b/d 516, , , , ,500 Stores 66,000 49,500 33,000 (165,000) 16,500 Maintenance 42,000 36,000 18,000 24,000 (120,000) 624, , ,300 nil nil Workings: Equation 1 Equation 2 S = 141, M M = 103, S Equation 1 x 5 5S = 705,000 + M Equation 2 re-arranged -0.1S = 103,500 - M Added together 4.9S = 808,500 S = 165,000 Substitute in equation 2 M = 103, ,500 (0.1 of 165,000) M = 120,000 Apportionment of stores Apportionment of maintenance A = 40% x RM165,000 = RM66,000 B = 30% x RM165,000 = RM49,500 C = 20% x RM165,000 = RM33,000 M =10% x RM165,000 = RM16,500 A = 35% x RM120,000 = RM42,000 B = 30% x RM120,000 = RM36,000 C = 15% x RM120,000 = RM18,000 S = 20% x RM120,000 = RM24, /2/06/MA 12

13 MODEL ANSWERS TO QUESTION 4 CONTINUED (c) Calculation of pre-determined overhead absorption rates (i) PCC A = RM624,000 / 60,000 machine hours = RM10.40 per machine hour (ii) PCC B = RM478,200 / 39,850 machine hours = RM12.00 per machine hour (iii) PCC C = RM351,300 / 30,000 machine hours = RM11.71 per machine hour (d) Calculation of over/under absorption Production Cost Centres A B C Actual activity m/c hours 58,750 39,200 29,780 Overhead absorption rate RM10.40 RM12.00 RM11.71 Overheads absorbed 611, , ,724 * Actual overheads 585, , ,250 Over (under) absorption 25,250 (10,175) (6,526) * * rounded 3616/2/06/MA 13

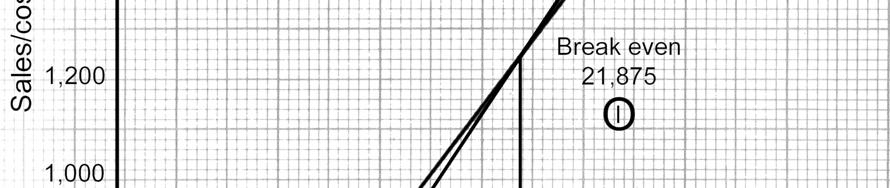

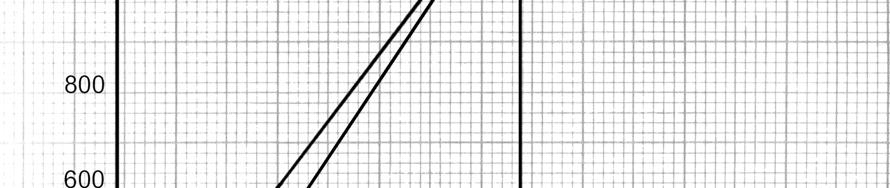

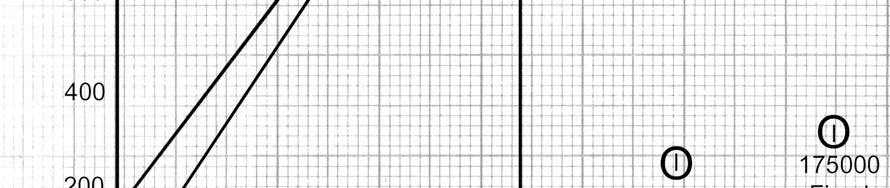

14 QUESTION 5 Ashbee Stockdale Limited has budgeted to sell 35,000 units of its product in a period. The following further budgeted information has been prepared for the period: Selling price RM60 per unit Direct labour 3 hrs per RM6 per hour Direct materials 2 kgs per RM7 per kg Variable production overheads RM4 per direct labour hour Variable selling and administration overheads RM8 per unit Fixed overheads RM5 per unit REQUIRED (a) Using marginal costing, calculate for the period the budgeted: (i) Contribution per unit (ii) Total contribution and total net profit (iii) Break even point (in units) (iv) Margin of safety as a % of sales (10 marks) (b) Using the graph paper provided, prepare a conventional break-even chart, clearly showing: (i) The break-even point (ii) The margin of safety (c) State THREE assumptions in cost-volume-profit analysis. (6 marks) (4 marks) (Total 20 marks) 3616/2/06/MA 14

15 MODEL ANSWERS TO QUESTION 5 (a) (i) & (ii) Calculation of budgeted contribution and profit: Per unit Sales 60 Variable costs Direct labour (3 hrs x RM6) 18 Direct materials (2 kilos x RM7) 14 Variable production overheads (3 hrs x RM4) 12 Selling and administrative overheads 8 Total variable costs 52 Contribution per unit 8 Total contribution (35,000 x RM8) 280,000 Less Fixed costs (35,000 x RM5) 175,000 Total Net Profit 105,000 Syllabus Topic 3: Marginal Costing (3.4) (iii) Break even point = 175,000/ 8 = 21,875 units (iv) Margin of safety 35,000 less 21,875 = 13,125 units = 13,125/35,000 = 37.5% of budgeted sales (b) See next page for break even chart (c) Assumptions in cost volume profit analysis THREE of the following Selling price per unit is constant across the range of activity Total fixed costs remain constant across the range of activity Total variable costs will vary in direct proportion to activity Costs can be split between fixed and variable 3616/2/06/MA 15

16 MODEL ANSWERS TO QUESTION 5 CONTINUED 3616/2/06/MA 16

17 QUESTION 6 Elliot Ellison Limited manufactures three products, details of which are as follows: Product A B C Selling price per unit (RM) Variable cost per unit (RM) Weekly demand (units) Machine hours per unit Additional information: Fixed costs are RM12,500 per week The firm currently has 40 machines, which have insufficient capacity to satisfy demand The company is considering three, separate, proposals: (i) To operate the machines at the present capacity of 2 x 7 hour shifts per day for a five day week. (ii) To change to 3 x 7 hours shifts per day for a 5 day week, where upon variable costs of each product would rise by 10% per unit and fixed costs would increase by RM5,000 per week. (iii) To install 10 extra machines, and to operate on the normal 2 x 7 hour shifts per day for a 5 day week, where upon fixed costs would increase by RM7,500 per week. REQUIRED (a) Calculate the short fall in capacity for the period, based on operating the existing machines for 2 x 7 hour shifts per day for a 5 day week. (2 marks) (b) Determine the maximum weekly profit possible from each proposal. (16 marks) (c) State which alternative you would recommend. (2 marks) (Total 20 marks) 3616/2/06/MA 17

18 MODEL ANSWERS TO QUESTION 6 (a) Current capacity = 40 x 2 x 7 x 5 = 2,800 machine hours per week Demand = A (300 x 4) B (400 x 3) C (500 x 4) = 4,400 machine hours per week Therefore there is a shortfall in capacity of 1,600 machine hours per week (b) 1. To operate 2 x 7 hr shifts per day: Product A B C Contribution per unit Machine hours per unit Contribution per m/c hour Order of priority Production schedule: Machine hours available per week 2,800 Product B 400 units x 3 hours 1,200 1,600 Product A 300 units x 4 hours 1, Product C 100 units x 4 hours 400 Nil Contribution schedule RMs Product B 400 units x RM36 14,400 Product A 300 units x RM40 12,000 Product C 100 units x RM32 3,200 Total contribution 29,600 Less Fixed costs 12,500 Profit 17, To operate 3 x 7 hr shifts per day Machine hours available = 40 x 5 x 7 x 3 = 4,200 Machine hours required = 4,400 Shortfall in capacity 200 A B C Selling Price Variable costs (10 % increase) Contribution (SP VC) Machine hours Contribution per m/c hour Order of priority Production schedule: Machine hours available 4,200 Product B 400 units x 3 hours 1,200 3,000 Product A 300 units x 4 hours 1,200 1,800 Product C 450 units x 4 hours 1,800 Nil Contribution schedule RMs Product B 400 units x RM ,960 Product A 300 units x RM ,680 Product C 450 units x RM ,050 Total contribution 36,690 Less Fixed costs 17,500 Profit 19, /2/06/MA 18

19 MODEL ANSWERS TO QUESTION 6 CONTINUED 3. To operate 50 machines x 2 x 7hr shifts per day: Machine hours available = 50 x 5 x 7 x 2 = 3,500 Machine hours required = 4,400 Shortfall in capacity 900 Contribution per machine hour and production schedule same as number one Production schedule: Machine hours available 3,500 Product B 400 units x 3 hours 1,200 2,300 Product A 300 units x 4 hours 1,200 1,100 Product C 275 units x 4 hours 1,100 Nil Contribution schedule RMs Product B 400 units x RM36 14,400 Product A 300 units x RM40 12,000 Product C 275 units x RM32 8,800 Total contribution 35,200 Less Fixed costs 20,000 Profit 15,200 (c) The second alternative makes the greatest profit 3616/2/06/MA 19 Education Development International plc 2006

Cost Accounting. Level 3. Model Answers. Series (Code 3016)

") Cost Accounting Level 3 Model Answers Series 4 2007 (Code 3016) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and learning

Cost Accounting Level 3 Model Answers Series 4 2007 (Code 3016) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and learning

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2010 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2010 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 2 2012 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 2 2012 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

Cost Accounting. Level 3. Model Answers. Series (Code 3016) 1 ASE /2/06

1 ASE /2/06") Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 2 2006 How to use this booklet Model Answers have been developed

Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 2 2006 How to use this booklet Model Answers have been developed

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2008 (3023) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2008 (3023) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Cost Accounting. Level 3. Model Answers. Series (Code 3016)

") Cost Accounting Level 3 Model Answers Series 4 2005 (Code 3016) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and learning

Cost Accounting Level 3 Model Answers Series 4 2005 (Code 3016) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and learning

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2009 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2009 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

Management Accounting

Management Accounting Level 3 Model Answers Series 4 2007 (Code 3023) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and

Management Accounting Level 3 Model Answers Series 4 2007 (Code 3023) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and

Cost Accounting Level 3

Cost Accounting Level 3 Model Answers Series 4 2013 (ASE3017) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk, www.pearson.com/uk

Cost Accounting Level 3 Model Answers Series 4 2013 (ASE3017) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk, www.pearson.com/uk

Management Accounting

Management Accounting Level 3 Model Answers Series 3 2008 (Code 3023) 1 ASE 3023 2 06 1 3023/2/06 >f0t@w9w2`?[i]bkbw5k# Management Accounting Level 3 Series 3 2008 How to use this booklet Model Answers

Management Accounting Level 3 Model Answers Series 3 2008 (Code 3023) 1 ASE 3023 2 06 1 3023/2/06 >f0t@w9w2`?[i]bkbw5k# Management Accounting Level 3 Series 3 2008 How to use this booklet Model Answers

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 2 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 2 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Management Accounting

Management Accounting Level 3 Model Answers Series 2 2008 Malaysia (Code 3623) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment

Management Accounting Level 3 Model Answers Series 2 2008 Malaysia (Code 3623) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment

Cost Accounting. Level 3. Model Answers. Series (Code 3016) 1 ASE /2/06

1 ASE /2/06") Cost Accounting Level 3 Model Answers Series 3 2007 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 3 2007 How to use this booklet Model Answers have been developed

Cost Accounting Level 3 Model Answers Series 3 2007 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 3 2007 How to use this booklet Model Answers have been developed

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2012 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2012 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 3 2010 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 3 2010 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 4 2009 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 4 2009 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

Management Accounting

Management Accounting Level 3 Model Answers Series 4 2004 (Code 3023) ASP M 1697 >f0t@wjy2[2`6zpw4m # Vision Statement Our vision is to contribute to the achievements of learners around the world by providing

Management Accounting Level 3 Model Answers Series 4 2004 (Code 3023) ASP M 1697 >f0t@wjy2[2`6zpw4m # Vision Statement Our vision is to contribute to the achievements of learners around the world by providing

Cost Accounting. Level 3. Model Answers. Series (Code 3016)

") Cost Accounting Level 3 Model Answers Series 2 2008 (Code 3016) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and learning

Cost Accounting Level 3 Model Answers Series 2 2008 (Code 3016) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and learning

Management Accounting

Management Accounting Level 3 Model Answers Series 4 2006 Singapore (Code 3723) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment

Management Accounting Level 3 Model Answers Series 4 2006 Singapore (Code 3723) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment

Management Accounting

Model Answers for Management Accounting THIRD LEVEL Series 2 2002 (Code 3023) LCCI Examinations Board ASP M 1147 >f0t@wjy2[2`ed:yed# Management Accounting Third Level Series 2 2002 How to use this booklet

Model Answers for Management Accounting THIRD LEVEL Series 2 2002 (Code 3023) LCCI Examinations Board ASP M 1147 >f0t@wjy2[2`ed:yed# Management Accounting Third Level Series 2 2002 How to use this booklet

Management Accounting

>f0t@wjy2[2`5k2[2h# Management Accounting Level 3 Series 2 2003 (Code 3023) Model Answers ASP M 1445 Management Accounting Level 3 Series 2 2003 How to use this booklet Model Answers have been developed

>f0t@wjy2[2`5k2[2h# Management Accounting Level 3 Series 2 2003 (Code 3023) Model Answers ASP M 1445 Management Accounting Level 3 Series 2 2003 How to use this booklet Model Answers have been developed

Book-Keeping and Accounts Level 2

LCCI International Qualifications Book-Keeping and Accounts Level 2 Model Answers Series 3 2011 (2007) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Book-Keeping and Accounts Level 2 Model Answers Series 3 2011 (2007) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 3 Examination 2008 COST ACCOUNTING Level 3 Friday 6 June Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your answers

Series 3 Examination 2008 COST ACCOUNTING Level 3 Friday 6 June Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your answers

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 4 Examination 2008 COST ACCOUNTING Level 3 Tuesday 11 November Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 4 Examination 2008 COST ACCOUNTING Level 3 Tuesday 11 November Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Management Accounting

Examiner s Report and Model Answers for Management Accounting THIRD LEVEL Series 4 (Code 3023) 2000 LCCI Examinations Board MH N T336 9 RNM >f2[ew2r@o2`0t1f3]e]2r2[1_# Management Accounting Third Level

Examiner s Report and Model Answers for Management Accounting THIRD LEVEL Series 4 (Code 3023) 2000 LCCI Examinations Board MH N T336 9 RNM >f2[ew2r@o2`0t1f3]e]2r2[1_# Management Accounting Third Level

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 2 Examination 2008 COST ACCOUNTING Level 3 Tuesday 27 May Subject Code: 3616/M Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your answers

Series 2 Examination 2008 COST ACCOUNTING Level 3 Tuesday 27 May Subject Code: 3616/M Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your answers

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 3 Examination 2007 COST ACCOUNTING Level 3 Tuesday 5 June Subject Code: 3716 (S) Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 3 Examination 2007 COST ACCOUNTING Level 3 Tuesday 5 June Subject Code: 3716 (S) Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

LCCI International Qualifications. Book-keeping Level 1. Model Answers Series (1017)

") LCCI International Qualifications Book-keeping Level 1 Model Answers Series 4 2011 (1017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Book-

LCCI International Qualifications Book-keeping Level 1 Model Answers Series 4 2011 (1017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Book-

Study the REQUIRED section of each question carefully and extract the data required for your answers from the information supplied.

Series 4 Examination 2010 COST ACCOUNTING Level 3 Monday 6 December Subject Code: 3717/S Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks. Study

Series 4 Examination 2010 COST ACCOUNTING Level 3 Monday 6 December Subject Code: 3717/S Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks. Study

Pearson LCCI Level 3 Certificate in Accounting

Pearson LCCI Level 3 Certificate in Accounting Model Answers Series 4 2013 (ASE3012) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk,

Pearson LCCI Level 3 Certificate in Accounting Model Answers Series 4 2013 (ASE3012) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk,

Mark Scheme (Results) Series Pearson LCCI Level 3 COST ACCOUNTING (ASE3017)

Series Pearson LCCI Level 3 COST ACCOUNTING (ASE3017)") Mark Scheme (Results) Series 3 2014 Pearson LCCI Level 3 COST ACCOUNTING (ASE3017) LCCI International Qualifications LCCI International Qualifications are awarded by Pearson, the UK s largest awarding

Mark Scheme (Results) Series 3 2014 Pearson LCCI Level 3 COST ACCOUNTING (ASE3017) LCCI International Qualifications LCCI International Qualifications are awarded by Pearson, the UK s largest awarding

LCCI International Qualifications. Accounting (IAS) Level 3. Model Answers Series (3902)

Level 3. Model Answers Series (3902)") LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 2 2012 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 2 2012 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

Pearson LCCI Level 3 Cost Accounting (ASE3017)

") Pearson LCCI Level 3 Cost Accounting (ASE3017) Annual Qualification Review 2013/2014 For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk,

Pearson LCCI Level 3 Cost Accounting (ASE3017) Annual Qualification Review 2013/2014 For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk,

Final Examination Semester 2 / Year 2011

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2011 COURSE : BASIC COSTING COURSE CODE : ACCT2013 TIME : 2 1/2 HOURS DEPARTMENT : FINANCE AND ACCOUNTING LECTURER : GAN HWI SIN

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2011 COURSE : BASIC COSTING COURSE CODE : ACCT2013 TIME : 2 1/2 HOURS DEPARTMENT : FINANCE AND ACCOUNTING LECTURER : GAN HWI SIN

CERTIFICATE IN MANAGEMENT ACCOUNTING

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 29 May Subject Code: 3623/M Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 29 May Subject Code: 3623/M Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

LCCI International Qualifications. Accounting (IAS) Level 3. Model Answers Series (3902)

Level 3. Model Answers Series (3902)") LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 4 2012 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 4 2012 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

LCCI International Qualifications. Accounting (IAS) Level 3. Model Answers Series (3902)

Level 3. Model Answers Series (3902)") LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 3 2011 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 3 2011 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

Level 2 Cost Accounting

Level 2 Cost Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners around

Level 2 Cost Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners around

Book-keeping and Accounts Level 2

LCCI International Qualifications Book-keeping and Accounts Level 2 Model Answers Series 3 2012 (2007) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Book-keeping and Accounts Level 2 Model Answers Series 3 2012 (2007) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

MANAGEMENT ACCOUNTING 2. Module Code: ACCT08004

School of Business & Enterprise Paisley & Hamilton Campus Session 015-016 Trimester 1 MANAGEMENT ACCOUNTING Module Code: ACCT08004 Date: 1st January 016 Time: 1400-1600 Answer THREE questions Question

School of Business & Enterprise Paisley & Hamilton Campus Session 015-016 Trimester 1 MANAGEMENT ACCOUNTING Module Code: ACCT08004 Date: 1st January 016 Time: 1400-1600 Answer THREE questions Question

Preparing and using budgets

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

LCCI International Qualifications. Accounting (IAS) Level 3. Model Answers Series (3902)

Level 3. Model Answers Series (3902)") LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 2 2011 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 2 2011 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

SUGGESTED SOLUTIONS Fundamentals of Management Accounting and Business Finance Certificate in Accounting and Business II Examination March 2013

SUGGESTED SOLUTIONS 05204 Fundamentals of Management Accounting and Business Finance Certificate in Accounting and Business II Examination March 2013 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA

SUGGESTED SOLUTIONS 05204 Fundamentals of Management Accounting and Business Finance Certificate in Accounting and Business II Examination March 2013 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA

MANAGEMENT ACCOUNTING

SERIES 4 EXAMINATION 2004 MANAGEMENT ACCOUNTING LEVEL 3 (Code No: 3023) FRIDAY 19 NOVEMBER Instructions to Candidates (d) (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions.

SERIES 4 EXAMINATION 2004 MANAGEMENT ACCOUNTING LEVEL 3 (Code No: 3023) FRIDAY 19 NOVEMBER Instructions to Candidates (d) (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions.

CERTIFICATE IN MANAGEMENT ACCOUNTING

Series 2 Examination 2011 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 12 April Subject Code: 3024 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry

Series 2 Examination 2011 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 12 April Subject Code: 3024 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry

SERIES 4 EXAMINATION 2005 COST ACCOUNTING LEVEL 3. (Code No: 3016) FRIDAY 11 NOVEMBER

FRIDAY 11 NOVEMBER") SERIES 4 EXAMINATION 2005 COST ACCOUNTING LEVEL 3 (Code No: 3016) FRIDAY 11 NOVEMBER Instructions to Candidates (a) (b) (c) (d) (e) (f) (g) (h) The time allowed for this examination is 3 hours. Answer

SERIES 4 EXAMINATION 2005 COST ACCOUNTING LEVEL 3 (Code No: 3016) FRIDAY 11 NOVEMBER Instructions to Candidates (a) (b) (c) (d) (e) (f) (g) (h) The time allowed for this examination is 3 hours. Answer

MARK SCHEME for the October/November 2014 series 9706 ACCOUNTING

CAMBRIDGE INTERNATIONAL EXAMINATIONS Cambridge International Advanced Subsidiary and Advanced Level MARK SCHEME for the October/November 2014 series 9706 ACCOUNTING 9706/22 Paper 2 (Structured Questions

CAMBRIDGE INTERNATIONAL EXAMINATIONS Cambridge International Advanced Subsidiary and Advanced Level MARK SCHEME for the October/November 2014 series 9706 ACCOUNTING 9706/22 Paper 2 (Structured Questions

The budgeted information on the two business opportunities that Green Bush records are currently considering investing in is as follows:

ICB Cost and Management Accounting Playlist Handbook SECTION A: REVISION VIDEO QUESTIONS Break-even analysis The budgeted information on the two business opportunities that Green Bush records are currently

ICB Cost and Management Accounting Playlist Handbook SECTION A: REVISION VIDEO QUESTIONS Break-even analysis The budgeted information on the two business opportunities that Green Bush records are currently

ACCA Paper F5. Performance Management. Class Notes

ACCA Paper F5 Performance Management Class Notes December 2011 The Accountancy College Ltd, June 2011 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or

ACCA Paper F5 Performance Management Class Notes December 2011 The Accountancy College Ltd, June 2011 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or

322 Roll No : 1 : Time allowed : 3 hours Maximum marks : 100

2/2013/CMA (N/S) Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 7 NOTE : 1. Answer ALL Questions. 2. All working notes should be

2/2013/CMA (N/S) Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 7 NOTE : 1. Answer ALL Questions. 2. All working notes should be

(59) MANAGEMENT ACCOUNTING & BUSINESS FINANCE

MANAGEMENT ACCOUNTING & BUSINESS FINANCE") All Rights Reserved THE ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA FINAL EXAMINATION JULY 2013 (59) MANAGEMENT ACCOUNTING & BUSINESS FINANCE Time: 03 hours Instructions to candidates: (1) This

All Rights Reserved THE ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA FINAL EXAMINATION JULY 2013 (59) MANAGEMENT ACCOUNTING & BUSINESS FINANCE Time: 03 hours Instructions to candidates: (1) This

MANAGEMENT ACCOUNTING

Series 4 Examination 2009 MANAGEMENT ACCOUNTING Level 3 Tuesday 1 December Subject Code: 3724 S Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks.

Series 4 Examination 2009 MANAGEMENT ACCOUNTING Level 3 Tuesday 1 December Subject Code: 3724 S Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks.

VARIANCE ANALYSIS: ILLUSTRATION

VARIANCE ANALYSIS: ILLUSTRATION The following information relates to the production of product Alpha for the month of August Standard Cost Card Budgeted production overhead based on 10,000 units $ $ Selling

VARIANCE ANALYSIS: ILLUSTRATION The following information relates to the production of product Alpha for the month of August Standard Cost Card Budgeted production overhead based on 10,000 units $ $ Selling

Analysing costs and revenues

Osborne Books Tutor Zone Analysing costs and revenues Practice assessment 1 Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e This assessment relates to

Osborne Books Tutor Zone Analysing costs and revenues Practice assessment 1 Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e This assessment relates to

THE MOMBASA POLYTECHNIC UNIVERSITY COLLEGE

THE MOMBASA POLYTECHNIC UNIVERSITY COLLEGE Faculty of Business & Social Studies DEPARTMENT OF BUSINESS STUDIES BACHELOR OF BUSINESS ADMINISTRATION HBC 2117: COST ACCOUNTING BBA 2 ND YEAR 1 ST SEMESTER

THE MOMBASA POLYTECHNIC UNIVERSITY COLLEGE Faculty of Business & Social Studies DEPARTMENT OF BUSINESS STUDIES BACHELOR OF BUSINESS ADMINISTRATION HBC 2117: COST ACCOUNTING BBA 2 ND YEAR 1 ST SEMESTER

Ordering costs Any two of the following: Postage, Paperwork, Telephone, Internet, , Purchasing Officer's salary

EDUCATION DEVELOPMENT INTERNATIONAL PLC SAMPLE PAPER ANSWERS 2008 COST ACCOUNTING (ASE3017) LEVEL 3 QUESTION 1 (a) (i) Stock holding costs Any two of the following: Insurance, Material handling, Storekeeper's

EDUCATION DEVELOPMENT INTERNATIONAL PLC SAMPLE PAPER ANSWERS 2008 COST ACCOUNTING (ASE3017) LEVEL 3 QUESTION 1 (a) (i) Stock holding costs Any two of the following: Insurance, Material handling, Storekeeper's

Date: Duration: Total marks:

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT: ACCOUNTING, ECONOMICS & FINANCE BACHELOR OF ACCOUNTING COST & MANAGEMENT ACCOUNTING 201 (CMA 611 S) FIRST OPPORTUNITY EXAMINATION QUESTION

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT: ACCOUNTING, ECONOMICS & FINANCE BACHELOR OF ACCOUNTING COST & MANAGEMENT ACCOUNTING 201 (CMA 611 S) FIRST OPPORTUNITY EXAMINATION QUESTION

Write your answers in blue or black ink/ballpoint. You can only use pencil for graphs, charts, diagrams, etc.

Cost Accounting ASE3017 Level 3 Tuesday 6 November 2012 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Please ensure

Cost Accounting ASE3017 Level 3 Tuesday 6 November 2012 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Please ensure

SUGGESTED SOLUTION IPCC MAY 2017EXAM. Test Code - I M J

SUGGESTED SOLUTION IPCC MAY 2017EXAM COSTING Test Code - I M J 7 1 3 5 BRANCH - (MULTIPLE) (Date : 01.01.2017) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022)

SUGGESTED SOLUTION IPCC MAY 2017EXAM COSTING Test Code - I M J 7 1 3 5 BRANCH - (MULTIPLE) (Date : 01.01.2017) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022)

Part 1 Examination Paper 1.2. Section A 10 C 11 C 2 A 13 C 1 B 15 C 6 C 17 B 18 C 9 D 20 C 21 C 22 D 23 D 24 C 25 C

Answers Part 1 Examination Paper 1.2 Financial Information for Management June 2007 Answers Section A 1 B 2 A 3 A 4 A 5 D 6 C 7 B 8 C 9 D 10 C 11 C 12 A 13 C 14 B 15 C 16 C 17 B 18 C 19 D 20 C 21 C 22

Answers Part 1 Examination Paper 1.2 Financial Information for Management June 2007 Answers Section A 1 B 2 A 3 A 4 A 5 D 6 C 7 B 8 C 9 D 10 C 11 C 12 A 13 C 14 B 15 C 16 C 17 B 18 C 19 D 20 C 21 C 22

INTER CA MAY Test Code M32 Branch: MULTIPLE Date: (50 Marks) Note: All questions are compulsory.

Note: All questions are compulsory.") (5 Marks) Note: All questions are compulsory. INTER CA MAY 218 COSTING Topic: Contract Costing, Budgetary Control, Labour, Joint & By- Product, Absorption Costing, Overheads, Integral & Non Integral, Marginal

(5 Marks) Note: All questions are compulsory. INTER CA MAY 218 COSTING Topic: Contract Costing, Budgetary Control, Labour, Joint & By- Product, Absorption Costing, Overheads, Integral & Non Integral, Marginal

ACCA. Paper F2 and FMA. Management Accounting December 2014 to June Interim Assessment Answers

ACCA Paper F2 and FMA Management Accounting December 204 to June 205 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment questions

ACCA Paper F2 and FMA Management Accounting December 204 to June 205 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment questions

Version 3.0. klm. General Certificate of Education June Accounting ACCN4. Further Aspects of Management Accounting. Final.

Version 3.0 klm General Certificate of Education June 2010 Accounting ACCN4 Unit 4: Further Aspects of Management Accounting Final Mark Scheme Mark schemes are prepared by the Principal Examiner and considered,

Version 3.0 klm General Certificate of Education June 2010 Accounting ACCN4 Unit 4: Further Aspects of Management Accounting Final Mark Scheme Mark schemes are prepared by the Principal Examiner and considered,

CERTIFICATE IN MANAGEMENT ACCOUNTING

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Monday 2 April Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Monday 2 April Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

(b) Flexible Budget For The Year Ended 31 May 2003

Flexible Budget For The Year Ended 31 May 2003") Paper 2 Section A Question 1 Flexible budgets recognise the difference in cost behaviour (1) between fixed and variable costs in relation to fluctuations in output, (1) turnover, or other variable factors.

Paper 2 Section A Question 1 Flexible budgets recognise the difference in cost behaviour (1) between fixed and variable costs in relation to fluctuations in output, (1) turnover, or other variable factors.

Analysing cost and revenues

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost accounting

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost accounting

CERTIFICATE IN MANAGEMENT ACCOUNTING

Series 3 Examination 2010 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 8 June Subject Code: 3024 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal

Series 3 Examination 2010 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 8 June Subject Code: 3024 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal

CS Executive Programme Module - I December Paper - 2 : Cost and Management Accounting

ISBN : 978-93-5034-747-8 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1 : Introduction to Cost and Management Accounting

ISBN : 978-93-5034-747-8 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1 : Introduction to Cost and Management Accounting

LU4: Accounting for Overhead

LU4: Accounting for Overhead Contents Introduction Applied manufacturing overheads Allocation of manufacturing overheads Learning objectives Define overhead costs Distinguish between manufacturing and

LU4: Accounting for Overhead Contents Introduction Applied manufacturing overheads Allocation of manufacturing overheads Learning objectives Define overhead costs Distinguish between manufacturing and

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level. Published

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level ACCOUNTING 9706/23 Paper 2 Structured Questions (Core) October/November 2016 MARK SCHEME Maximum Mark:

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level ACCOUNTING 9706/23 Paper 2 Structured Questions (Core) October/November 2016 MARK SCHEME Maximum Mark:

Institute of Certified Bookkeepers

Institute of Certified Bookkeepers Level III Diploma in Costing and Budgeting Introduction: Financial Accounting is the reporting of financial information to users of Financial Statements both internal

Institute of Certified Bookkeepers Level III Diploma in Costing and Budgeting Introduction: Financial Accounting is the reporting of financial information to users of Financial Statements both internal

Write your answers in blue or black ink/ballpoint. You can only use pencil for graphs, charts, diagrams, etc.

Cost Accounting ASE3017 Level 3 Wednesday 3 April 2013 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Instructions

Cost Accounting ASE3017 Level 3 Wednesday 3 April 2013 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Instructions

MOCK EXAMINATION PRINCIPLES OF ACCOUNTS A-LEVEL PAPER 2

HONG KONG ASSOCIATION FOR BUSINESS EDUCATION HONG KONG INSTITUTE OF VOCATIONAL EDUCATION (CHAI WAN & TUEN MUN) HONG KONG ADVANCED LEVEL EXAMINATION 2009 MOCK EXAMINATION PRINCIPLES OF ACCOUNTS A-LEVEL

HONG KONG ASSOCIATION FOR BUSINESS EDUCATION HONG KONG INSTITUTE OF VOCATIONAL EDUCATION (CHAI WAN & TUEN MUN) HONG KONG ADVANCED LEVEL EXAMINATION 2009 MOCK EXAMINATION PRINCIPLES OF ACCOUNTS A-LEVEL

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 PERFORMANCE MANAGEMENT

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 PERFORMANCE MANAGEMENT PERFORMANCE MEASUREMENT NON- FINANCIAL MEASUREMENT PERFOMANCE MEASUREMENT OF A NON- PROFIT ORGANISATION DIVISIONAL PERFORMANCE MEASURE

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 PERFORMANCE MANAGEMENT PERFORMANCE MEASUREMENT NON- FINANCIAL MEASUREMENT PERFOMANCE MEASUREMENT OF A NON- PROFIT ORGANISATION DIVISIONAL PERFORMANCE MEASURE

BATCH All Batches. DATE: MAXIMUM MARKS: 100 TIMING: 3 Hours. PAPER 3 : Cost Accounting

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

THE PUBLIC ACCOUNTANTS EXAMINATION COUNCIL OF MALAWI 2014 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC9: COSTING AND BUDGETARY CONTROL

EXAMINATION NO. THE PUBLIC ACCOUNTANTS EXAMINATION COUNCIL OF MALAWI 2014 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC9: COSTING AND BUDGETARY CONTROL MONDAY 2 JUNE 2014 TIME ALLOWED: 3 HOURS

EXAMINATION NO. THE PUBLIC ACCOUNTANTS EXAMINATION COUNCIL OF MALAWI 2014 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC9: COSTING AND BUDGETARY CONTROL MONDAY 2 JUNE 2014 TIME ALLOWED: 3 HOURS

Please ensure your answers are written clearly, or marks may be lost. Do NOT open this paper until you are told to do so by the supervisor.

Cost Accounting ASE3017 Level 3 Tuesday 19 November 2013 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Please

Cost Accounting ASE3017 Level 3 Tuesday 19 November 2013 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Please

Level 3 Certificate in Accounting (IAS) Effective for examinations to be held after January 2008

Effective for examinations to be held after January 2008") LCCI International Qualifications Level 3 Certificate in Accounting (IAS) Syllabus Effective for examinations to be held after January 2008 For further information contact us: Tel. +44 (0) 8707 202909

LCCI International Qualifications Level 3 Certificate in Accounting (IAS) Syllabus Effective for examinations to be held after January 2008 For further information contact us: Tel. +44 (0) 8707 202909

PWN! I'IFIITIIBIR UITIVERSITY. Sheehama, K.G.H. QUALIFICATION: COMMERCIAL ADVANCED TRAINING SCHEME (CATS) QUALIFICATION CODE: VARIOUS LEVEL: 5

QUALIFICATION CODE: VARIOUS LEVEL: 5") .. v I, I I. r 1... I. IIFIITIIBIR UITIVERSITY 0F SCIEIICE FIIID TECHI IOLOGY CENTRE FOR ENTREPRENEURIAL DEVELOPMENT QUALIFICATION: COMMERCIAL ADVANCED TRAINING SCHEME (CATS) QUALIFICATION CODE: VARIOUS

.. v I, I I. r 1... I. IIFIITIIBIR UITIVERSITY 0F SCIEIICE FIIID TECHI IOLOGY CENTRE FOR ENTREPRENEURIAL DEVELOPMENT QUALIFICATION: COMMERCIAL ADVANCED TRAINING SCHEME (CATS) QUALIFICATION CODE: VARIOUS

Management Accounting. Sample Paper / 2017 Questions and Suggested Solutions

Management Accounting Sample Paper 1 2016 / 2017 Questions and Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to

Management Accounting Sample Paper 1 2016 / 2017 Questions and Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to

Answer to PTP_Intermediate_Syllabus 2008_Jun2015_Set 1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Institute of Certified Management Accountants of Sri Lanka

Copyright Reserved Serial No Foundation Level Pilot Paper Instructions to Candidates 1. Time allowed is two (2) hours. 2. Total 100 Marks. 3. Answer all questions. 4. Encircle the number of your choice

Copyright Reserved Serial No Foundation Level Pilot Paper Instructions to Candidates 1. Time allowed is two (2) hours. 2. Total 100 Marks. 3. Answer all questions. 4. Encircle the number of your choice

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 2 Examination 2011 COST ACCOUNTING Level 3 Thursday 7 April Subject Code: 3017 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks. Write your

Series 2 Examination 2011 COST ACCOUNTING Level 3 Thursday 7 April Subject Code: 3017 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks. Write your

Paper 1.2. Financial Information for Management PART 1 FRIDAY 10 DECEMBER 2004 QUESTION PAPER. Time allowed 3 hours

Financial Information for Management PRT 1 FRIY 10 EEMER 2004 QUESTION PPER Time allowed 3 hours This paper is divided into two sections Section LL 25 questions are compulsory and MUST be answered Paper

Financial Information for Management PRT 1 FRIY 10 EEMER 2004 QUESTION PPER Time allowed 3 hours This paper is divided into two sections Section LL 25 questions are compulsory and MUST be answered Paper

MANAGEMENT INFORMATION

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 1 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 1 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 M BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 M BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

MANAGEMENT ACCOUNTING

Series 3 Examination 2008 MANAGEMENT ACCOUNTING Level 3 Monday 9 June Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 3 Examination 2008 MANAGEMENT ACCOUNTING Level 3 Monday 9 June Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Examinations for Academic Year 2017 Semester I / Academic Year 2016/2017 Semester II

Programme BSc (Hons) Human Resource Management BSc (Hons) Management (L+G+F+M) Diploma in Procurement and Supply Management COHORT BHRM/12B/13B/14B/ 15A/16A/15B/FT/PT BMANG/F/L/M/12B/13A/ 13B/14A/14B/15A/15B/1

Programme BSc (Hons) Human Resource Management BSc (Hons) Management (L+G+F+M) Diploma in Procurement and Supply Management COHORT BHRM/12B/13B/14B/ 15A/16A/15B/FT/PT BMANG/F/L/M/12B/13A/ 13B/14A/14B/15A/15B/1

Method of Costing (II) (Process & Operation Costing, Joint Products & By Products)

(Process & Operation Costing, Joint Products & By Products)") 7 Method of Costing (II) (Process & Operation Costing, Joint Products & By Products) Question 1 JKL Limited produces two products J and K together with a by-product L from a single main process (process

7 Method of Costing (II) (Process & Operation Costing, Joint Products & By Products) Question 1 JKL Limited produces two products J and K together with a by-product L from a single main process (process

Management Accounting. Sample Paper 1 Questions and Suggested Solutions

Management Accounting Sample Paper 1 Questions and Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to provide guidance

Management Accounting Sample Paper 1 Questions and Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to provide guidance

PAPER 10: COST & MANAGEMENT ACCOUNTANCY

MTP_Intermediate_Syllabus 01_Jun016_Set 1 PAPER 10: COST & MANAGEMENT ACCOUNTANCY Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 MTP_Intermediate_Syllabus

MTP_Intermediate_Syllabus 01_Jun016_Set 1 PAPER 10: COST & MANAGEMENT ACCOUNTANCY Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 MTP_Intermediate_Syllabus

Revision of management accounting

1 Revision of management accounting The following topics are covered in this chapter: Standard costing Flexible budgeting Absorption and marginal costing 1.1 STANDARD COSTING LEARNING SUMMARY After studying

1 Revision of management accounting The following topics are covered in this chapter: Standard costing Flexible budgeting Absorption and marginal costing 1.1 STANDARD COSTING LEARNING SUMMARY After studying

INTER CA MAY COSTING Topic: Standard Costing, Budgetary Control, Integral and Non Integral, Materials, Marginal Costing.

INTER CA MAY 218 COSTING Topic: Standard Costing, Budgetary Control, Integral and Non Integral, Materials, Marginal Costing. Note: All questions are compulsory. Test Code M33 Branch: MULTIPLE Date: 21.1.218

INTER CA MAY 218 COSTING Topic: Standard Costing, Budgetary Control, Integral and Non Integral, Materials, Marginal Costing. Note: All questions are compulsory. Test Code M33 Branch: MULTIPLE Date: 21.1.218

COST ACCOUNTING AND FINANCIAL MANAGEMENT

STUDY MATERIAL Intermediate (IPC) Course PAPER : 3 COST ACCOUNTING AND FINANCIAL MANAGEMENT Part 1 : Cost Accounting VOLUME I BOARD OF STUDIES THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA This study

STUDY MATERIAL Intermediate (IPC) Course PAPER : 3 COST ACCOUNTING AND FINANCIAL MANAGEMENT Part 1 : Cost Accounting VOLUME I BOARD OF STUDIES THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA This study

SECTION I 14,000 14,200 19,170 10,000 8,000 10,400 12,400 9,600 8,400 11,200 13,600 18,320

QUESTION ONE SECTION I The following budget and actual results relates to Cypo Ltd. for the last three quarters for the year ended 31 March 200. Budget: Quarter 2 Quarter 3 Quarter to 30/9/2003 to 31/12/2003

QUESTION ONE SECTION I The following budget and actual results relates to Cypo Ltd. for the last three quarters for the year ended 31 March 200. Budget: Quarter 2 Quarter 3 Quarter to 30/9/2003 to 31/12/2003

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

Pearson LCCI Level 3 Certificate in Management Accounting (ASE3024)

") Pearson LCCI Level 3 Certificate in Management Accounting (ASE3024) Annual Qualification Review 2013/2014 For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com

Pearson LCCI Level 3 Certificate in Management Accounting (ASE3024) Annual Qualification Review 2013/2014 For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM. Test Code -

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM COSTING Test Code - BRANCH - (MUMBAI-2 (DB) (Date : 01.07.2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM COSTING Test Code - BRANCH - (MUMBAI-2 (DB) (Date : 01.07.2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS 1. (i) ABC Ltd. had an opening inventory value of 1760 (550 units valued at 3.20 each) on 1 st April 2010. The following

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS 1. (i) ABC Ltd. had an opening inventory value of 1760 (550 units valued at 3.20 each) on 1 st April 2010. The following