Intermediate Reporting nvision Reports and Variance Analysis

|

|

|

- Joanna Copeland

- 5 years ago

- Views:

Transcription

1 Intermediate Reporting nvision Reports and Variance Analysis 1

2 Created by Office of the Controller Office of Financial Planning/ Auxiliary & Enterprise Development Intermediate Reporting Training is designed for individuals working with budgets and transactions, to learn analysis techniques and system reporting tools, in order to better understand and explain variances.

3 Intermediate Reporting Training Agenda Learning Objectives and Important Terminology Review the Budget Process Basic Understanding of Budget Types What is a Variance? Overview of nvision Reports Case Study Actions and Resolving Deficits Important Tools and Resources

4 Learning Objectives By the end of this training, you will learn and/or be able to: Understand revenue and expense variance and how it is calculated Run and understand nvision reports within PS Financials for budget variance analysis Correctly explain budget variances in written form on reports Maintain rolling forecast(s) throughout the year

5 Important Terminology Actuals: Transactions that have posted to the General Ledger Budget: The plan for meeting probable revenues and expenses for a given period of time. Original Budget: The budget loaded into Commitment Control and available on July 1. Adjusted Budget: The original budget, plus or minus any budget transfers.

6 Review Budget Process Cycle of FIU Budgets and Fiscal Year

7 SUBMISSION To the BOG for approval and inclusion in the state-wide budget BUDGET EXECUTION Monthly performance monitoring and quarterly reporting BUDGET UPLOAD Load budget into PantherSoft Commitment Control PRELIMINARY Preparation of assumptions, process, and supporting systems APPROVAL Budget review and approval by the BOT DEVELOPMENT Current year forecast and next year s budget development Budget Cycle Budget Execution Phase includes monitoring the performance of the budget(s) 1. Compare Budgeted amounts to Actuals amounts on a regular basis 2. Investigate variances 3. Budget Adjustments & Actions

8 Fiscal Year Begins July 1st UNDERSTAND BUDGET RUN REPORTS MONITOR DATA TRANSACTIONS FLOWING Fiscal Year Ends June 30th Budget Execution Rolling Forecast

9 Favorable Unfavorable Budget Types Fund Groups, Revenue vs. Expense-Based

10 Budget A Worked on campus to help pay for tuition and expenses. Worked at Panera Bread during holiday breaks to help pay for expenses Money coming in from different sources & expenses Budget B Roommate had only personal expenses, parents gave her a budget Money coming in from parents, but mainly concerned with expenses

11 Budget A Revenue-Based Budget Revenues managed by the unit/dept Expenses dependent on revenue Budget B Expense-Based Budget Revenue managed centrally No Revenue on reports Expenses dependent on budget allocation

12 Fund Codes and Sources See Fund Matrix Control Guide Financial Glossary

13 What is a Variance? Types of Variances and How they are Calculated

+ - 94,857")

14 Definition: Any difference between budgeted amount and actuals. Variance Example: Budget Actuals Variance fav/(unfav) ,857 67,627 (27,231)

15 Variance Formula Result REVENUE VARIANCE EXPENSE VARIANCE = (Actuals Budget) = (Budget Actuals) Positive result = FAVORABLE Negative result = UNFAVORABLE Positive result = FAVORABLE (savings) Negative result = UNFAVORABLE (overspending)

16 Revenue Variance Budget Actuals Variance fav/(unfav) 154, ,580 73, ,580 (actuals) - 154,010 (budget) 73,570 Favorable Revenue Variance

17 Revenue Variance Budget Actuals Variance fav/(unfav) 1,846,876 1,781,393 (65,483) 1,781,393 (actuals) - 1,846,876 (budget) -65,483 (Unfavorable) Revenue Variance

18 Expense Variance Budget Actuals Variance fav/(unfav) 11, ,767 11,314 (budget) (actuals) 10,767 Favorable Revenue Variance

19 Expense Variance Budget Actuals Variance fav/(unfav) 73,238 75,590 (2,353) 73,238 (budget) - 75,590 (actuals) 2,353 (Unfavorable) Expense Variance

20 Whether favorable or (unfavorable), there are different causes of Variance: What assumptions were made when creating the budget? What are the Drivers in your unit/department related to your budget? Drivers: The factors and or assumptions used to formulate the budget. Analysis of these factors/assumptions provide information for the explanations of variances. Market Rate Programs, Specific Costs, Personnel Changes

21 Variance Causes 1. Budgeted in different periods (Timing/Delays) -Incorrect, missing charges 2. Budget assumptions incorrect, (True Real ) 3. Something did or did not happen (True Real )

22 Types of Variance True Real Variance A type of variance in which the explanation (cause) of the variance is either, deficit amounts or surplus/savings amounts.

23 Types of Variance True Real Variance within Budget Types Deficit Amounts (negative amount, unfavorable variance) Revenue-based Budgeted, but did not happen Expense-based Happened, but not budgeted Surplus/savings Amounts (positive amount, favorable variance). Revenue-based Happened, but not budgeted Expense-based Budgeted, but did not happen

24 Types of Variance A type of variance in which the explanation (cause) of the variance is that the Actuals amount will be absorbed or reallocated somewhere else in the university. This includes: budgeted funds that are returned to the university or allocated by the university budget transfers between units savings from budgeted expenses which will not occur and then used to cover unbudgeted expenditures.

25 Types of Variance Timing/Delays Variance A type of variance in which the explanation (cause) of the variance is due to Actual amounts happening either before a budgeted period OR after a budgeted period.

26 Overview of nvision Reports Reports for Budget Variance

27 SUBMISSION BUDGET EXECUTION All Other Reports PRELIMINARY FC, R2, RQ DEVELOPMENT BX What Report should I run? When should I run it? Budget Variance Reports (AS, XA) Transaction Report (DT) BUDGET UPLOAD APPROVAL

28 Name of Report Description (AS) Budget Variance This summary report provides budget variance for all Funds by Activity Number with subtotals across columns for Budget Account Categories. (XA) Budget Variance This detailed report provides budget variance for a single activity number. Shows beginning fund balance, inflows (revenues and transfers in), and outflows (expenses and transfers out) ending fund balance. This is setup like a typical profit and loss statement.

29 Name of Report (DI) E&G Budget Variance (DT) Detail Transaction (DS) Available Budget Balance Description This report provides the user with detailed variance analysis by account for expenses only. It is useful for E&G funded activity numbers only. It does not show inflows or fund balances. This report provides detailed transaction analysis on committed/paid expenses, as well as budget detail. It includes actuals, budget, and encumbrances. This report provides available budget information for total expenses for a range of activity numbers with a subtotal by activity number and funding source. This is an executive area budget balance report.

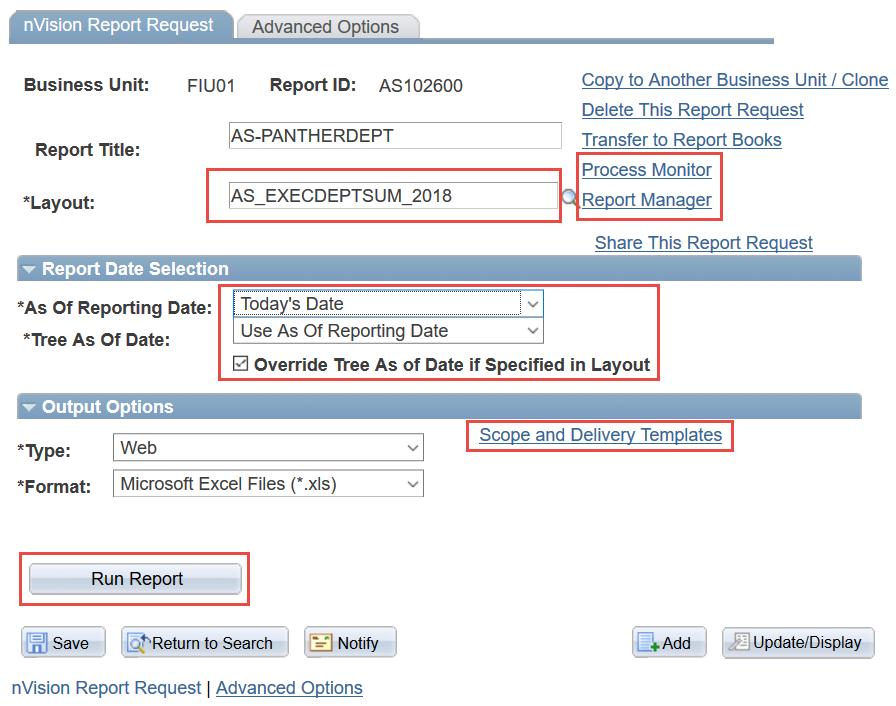

30 Running Reports in PS Financials Login to Production or Reporting Database (Need VPN) Know what type of report and Enter Report Request ID (AS, XA, DT and first 6 digits of department number) Layout, run the correct fiscal year layout Report Date Selection, run at the end of a period, today, etc. Scope, department number, activity number, something unique Delivery of report, Excel, , Schedule it

31 Running Reports in PS Financials

32 (AS) REPORT

33 (XA) Report

34 1. Look for the greatest variances at the activity level year to date (YTD). 2. Out of the biggest variance amounts, which are favorable, which are unfavorable?

35 3. Explain and answer, Why is there a variance?

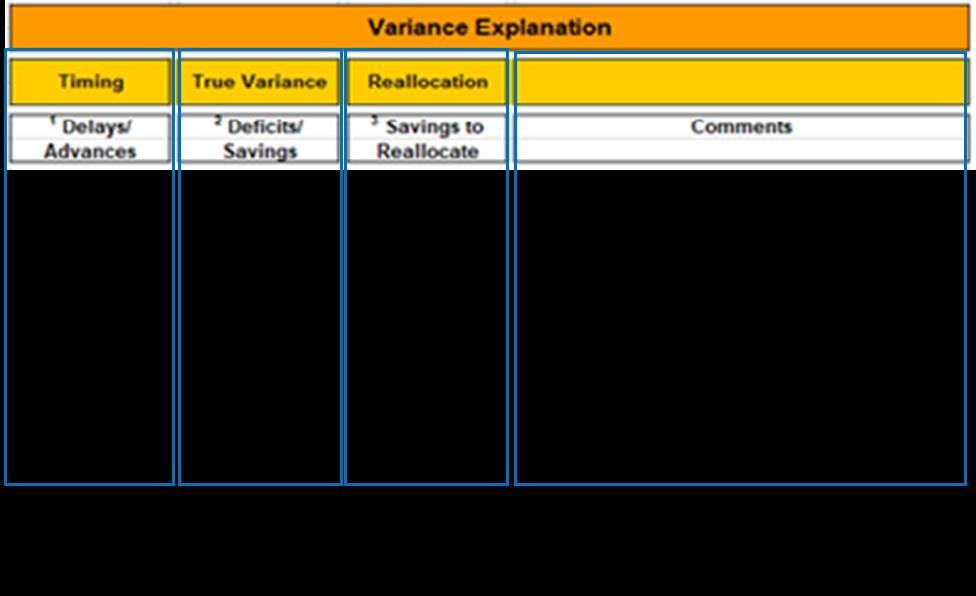

36 Variance Explanation Grid

37 Variance Explanations Enter variance explanations and comments into the Comments boxes next to a particular variance. Type variance amounts into the category that corresponds with the reason for the variance. Submit to OFP & AED

38 Case Study

39 Actions and Resolving Deficits

40 Rolling Forecast (RF) Why is the RF important to me? Monthly updates of the RF will increase your accuracy in preparation for the 8+4 official forecast submission in March. As you complete your monthly and quarterly variance analysis, updating the RF with those numeric changes will create a more accurate forecast, will take less time to complete the official forecast submission and ultimately lead to better budgeting. What do I need to do? You may start updating the forecasts starting in September, after the GL close for August (Period 2).

41 Rolling Forecast (RF) Month JUL AUG SEP OCT NOV DEC JAN FEB MAR APR MAY JUN Period Rolling Forecast Available - Ready for Monthly updates 3+9 Actual Actual Actual Original Budget Original Budget Original Budget Original Budget Original Budget Original Budget Original Budget Original Budget Original Budget F o r e c a s t s Actual Actual Actual Actual Period 4 Actual Loaded - Optional Updates Unit Updates Actual Actual Actual Actual Actual Unit Updates Unit Updates Unit Updates Period 5 Actual Loaded - Optional Updates Unit Updates Unit Updates Mandatory Submission Required Unit Updates Actual Actual Actual Actual Actual Actual Actual Actual Unit Updates Unit Updates Unit Updates Unit Updates Unit Updates Unit Updates Unit Updates Unit Updates Unit Updates Unit Updates Unit Updates Unit Updates. Period 10 Actual Loaded - Optional Updates 10+2 Actual Actual Actual Actual Actual Actual Actual Actual Actual Actual Unit Updates Unit Updates

42 Rolling Forecast (RF) How do I do it? You may modify the forecast through the Detail Budget Maintenance (DBM) tool in the Actual ledger. Where can I see it? The RF Report, similar to the FC report, will be available to run. It will show available funds after updating the forecast of revenues, salaries, and other expenses. Further instructions can be obtained here: Budget SharePoint website

Review amounts in budget overview, reports, queries Determine action to address the insufficient budget balance such as budget")

43 How to Determine Available Balances & Resolve Budget Deficits-Resource Find budget balance, cash balance, fund balance depending on fund code(s) Review amounts in budget overview, reports, queries Determine action to address the insufficient budget balance such as budget transfer etc.

44 Remedies for Budget Deficits Acting on budgeted items: smart bills, transfers, and cash IDSO Reimbursements Budget o Inter Unit Budget Transfer o BAA Actuals o Payroll Transfers o DSO reimbursement Foundation form o Expense Re-class o Cash Transfers o Close Req or POs o Close TAs

45 Important Tools and Resources Financial Reporting Manual Financial Glossary Fund Code Contacts and KK Grid nvision Report Guide How to Determine Available Balances Rolling Forecast Manual Online websites (Controller, OFP, AED)

46 Learning Objectives Review what you have learned. Do you or Can you, Understand revenue and expense variance and how it is calculated Run budget and transaction reports within PS Financials and analyze data within those reports related to budget variances (revenue/expense) Correctly explain budget variances in written form on reports Update the rolling forecast throughout the year

47 Questions? Thank You, for Attending and Learning about Intermediate Reporting Office of the Controller Office of Financial Planning/ Auxiliary Enterprise Development

PantherSoft Financials nvision Reports Guide

PantherSoft Financials nvision Reports Guide Financial and Reports This nvision Reports Guide provides information related to the types of FIU university-wide nvision reports run in PantherSoft Financials.

PantherSoft Financials nvision Reports Guide Financial and Reports This nvision Reports Guide provides information related to the types of FIU university-wide nvision reports run in PantherSoft Financials.

Financial Reporting Training. Office of the Controller

Financial Reporting Training Agenda 1. Accounting Review 2. What is a Budget and General Budget Concepts 3. nvision Financial Reports: Define nvision Variance Analysis Available Budget 4. Budget Inquiries

Financial Reporting Training Agenda 1. Accounting Review 2. What is a Budget and General Budget Concepts 3. nvision Financial Reports: Define nvision Variance Analysis Available Budget 4. Budget Inquiries

Budget Manager Meeting. February 20, 2018

Budget Manager Meeting February 20, 2018 Meeting Agenda DISCUSSION DRAFT NOT FOR DISTRIBUTION Budget Office Current Year Forecast Process Endowment Payout Control Charts FY19 Target Meetings Delphi Project

Budget Manager Meeting February 20, 2018 Meeting Agenda DISCUSSION DRAFT NOT FOR DISTRIBUTION Budget Office Current Year Forecast Process Endowment Payout Control Charts FY19 Target Meetings Delphi Project

General Fund Revenue

Millions Percent of Kathy Steinert, Director of Fiscal Services Phone: 541.923.8927 145 SE Salmon Ave Redmond, OR 97756 kathy.steinert@redmond.k12.or.us Date: May 23, 2014 To: Redmond School District Board

Millions Percent of Kathy Steinert, Director of Fiscal Services Phone: 541.923.8927 145 SE Salmon Ave Redmond, OR 97756 kathy.steinert@redmond.k12.or.us Date: May 23, 2014 To: Redmond School District Board

XML Publisher Balance Sheet Vision Operations (USA) Feb-02

Feb-02") Page:1 Apr-01 May-01 Jun-01 Jul-01 ASSETS Current Assets Cash and Short Term Investments 15,862,304 51,998,607 9,198,226 Accounts Receivable - Net of Allowance 2,560,786

Page:1 Apr-01 May-01 Jun-01 Jul-01 ASSETS Current Assets Cash and Short Term Investments 15,862,304 51,998,607 9,198,226 Accounts Receivable - Net of Allowance 2,560,786

Management Reports. June for PREPARED BY POWERED BY

Management Reports for June 217 PREPARED BY POWERED BY Contents 1. Management Reports Cashflow Forecast Actual vs Budget P&L Forecast Where Did Our Money Go? Net Worth 2. Understanding your Reports 3.

Management Reports for June 217 PREPARED BY POWERED BY Contents 1. Management Reports Cashflow Forecast Actual vs Budget P&L Forecast Where Did Our Money Go? Net Worth 2. Understanding your Reports 3.

QUARTERLY FINANCIAL REPORT December 31, 2017

California Independent System Operator QUARTERLY FINANCIAL REPORT December 31, 2017 Preliminary and Unaudited 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR

California Independent System Operator QUARTERLY FINANCIAL REPORT December 31, 2017 Preliminary and Unaudited 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR

Budget Process Tools: Introduction to CalPlanning FY

Budget Process Tools: Introduction to CalPlanning FY2018-19 HCP (Human Capital Planning) CalPlan CalRptg HCPRptg Smart View Introduction to CalPlanning September 2017 1 Agenda 1 2 3 4 CalPlanning Tools

Budget Process Tools: Introduction to CalPlanning FY2018-19 HCP (Human Capital Planning) CalPlan CalRptg HCPRptg Smart View Introduction to CalPlanning September 2017 1 Agenda 1 2 3 4 CalPlanning Tools

R o l l i n g F o r e c a s t i n g :

R o l l i n g F o r e c a s t i n g : A S t r a t e g y f o r E f f e c t i v e F i n a n c i a l M a n a g e m e n t Debra Miller Vice President Client Success January 22, 2016 Discussion Topics Overview

R o l l i n g F o r e c a s t i n g : A S t r a t e g y f o r E f f e c t i v e F i n a n c i a l M a n a g e m e n t Debra Miller Vice President Client Success January 22, 2016 Discussion Topics Overview

WESTWOOD LUTHERAN CHURCH Summary Financial Statement YEAR TO DATE - February 28, Over(Under) Budget WECC Fund Actual Budget

Budget WECC Fund Actual Budget") WESTWOOD LUTHERAN CHURCH Summary Financial Statement YEAR TO DATE - February 28, 2018 General Fund Actual A B C D E F WECC Fund Actual Revenue Revenue - Faith Giving 1 $ 213 $ 234 $ (22) - Tuition $ 226

WESTWOOD LUTHERAN CHURCH Summary Financial Statement YEAR TO DATE - February 28, 2018 General Fund Actual A B C D E F WECC Fund Actual Revenue Revenue - Faith Giving 1 $ 213 $ 234 $ (22) - Tuition $ 226

Review of Membership Developments

RIPE Network Coordination Centre Review of Membership Developments 7 October 2009/ GM / Lisbon http://www.ripe.net 1 Applications development RIPE Network Coordination Centre 140 120 100 80 60 2007 2008

RIPE Network Coordination Centre Review of Membership Developments 7 October 2009/ GM / Lisbon http://www.ripe.net 1 Applications development RIPE Network Coordination Centre 140 120 100 80 60 2007 2008

Florida International University Budget Concepts & On-Line Tool Training. February 25 28, 2014

Florida International University Budget Concepts & On-Line Tool Training February 25 28, 2014 1 Workshop Objectives Budget Assumptions Budget Development Important Concepts Forecast Versus Requested Budget

Florida International University Budget Concepts & On-Line Tool Training February 25 28, 2014 1 Workshop Objectives Budget Assumptions Budget Development Important Concepts Forecast Versus Requested Budget

Spheria Australian Smaller Companies Fund

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

Questions to Consider When You Implement Oracle Assets

Questions to Consider When You Implement Oracle Assets Cindy Cline Cline Consulting and Training Solutions, LLC During the implementation of Oracle Assets, several issues will arise and numerous decisions

Questions to Consider When You Implement Oracle Assets Cindy Cline Cline Consulting and Training Solutions, LLC During the implementation of Oracle Assets, several issues will arise and numerous decisions

Finance and Budgeting for NonFinance Professionals. Contents are subject to change. For the latest updates visit

Finance and Budgeting for NonFinance Professionals Page 1 of 10 Why Attend To succeed at any employment level and position, knowledge of basic financial principles is critical. The course transforms financial

Finance and Budgeting for NonFinance Professionals Page 1 of 10 Why Attend To succeed at any employment level and position, knowledge of basic financial principles is critical. The course transforms financial

MONTHLY FINANCIAL SUMMARY FISCAL YEAR (SEPTEMBER)

") MONTHLY FINANCIAL SUMMARY FISCAL YEAR 2017-2018 (SEPTEMBER) Original Budget Revenues Collected YTD % Collected of Annual Enrollment Based $ 109,171,283 $ 45,498,974 41.7% State Funding 85,551,407 21,308,376

MONTHLY FINANCIAL SUMMARY FISCAL YEAR 2017-2018 (SEPTEMBER) Original Budget Revenues Collected YTD % Collected of Annual Enrollment Based $ 109,171,283 $ 45,498,974 41.7% State Funding 85,551,407 21,308,376

QUARTERLY FINANCIAL REPORT March 31, 2018

California Independent System Operator QUARTERLY FINANCIAL REPORT March 31, 2018 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR CORPORATION QUARTERLY FINANCIAL

California Independent System Operator QUARTERLY FINANCIAL REPORT March 31, 2018 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR CORPORATION QUARTERLY FINANCIAL

QUARTERLY FINANCIAL REPORT June 30, 2017

California Independent System Operator QUARTERLY FINANCIAL REPORT June 30, 2017 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR CORPORATION QUARTERLY FINANCIAL

California Independent System Operator QUARTERLY FINANCIAL REPORT June 30, 2017 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR CORPORATION QUARTERLY FINANCIAL

London Borough of Barnet Pension Fund. Communication Strategy (2018)

") London Borough of Barnet Pension Fund Communication Strategy (2018) Background This document sets out the communication strategy for the London Borough of Barnet Pension Fund. The London Borough of Barnet

London Borough of Barnet Pension Fund Communication Strategy (2018) Background This document sets out the communication strategy for the London Borough of Barnet Pension Fund. The London Borough of Barnet

MONTHLY FINANCIAL SUMMARY FISCAL YEAR (MARCH)

") MONTHLY FINANCIAL SUMMARY FISCAL YEAR 20172018 (MARCH) Original Budget Revenues Collected YTD % Collected of Annual Enrollment Based $ 109,171,283 $ 101,304,928 92.8% State Funding 85,551,407 63,950,143

MONTHLY FINANCIAL SUMMARY FISCAL YEAR 20172018 (MARCH) Original Budget Revenues Collected YTD % Collected of Annual Enrollment Based $ 109,171,283 $ 101,304,928 92.8% State Funding 85,551,407 63,950,143

Unrestricted Cash / Board Designated Cash & Investments December 2015

Unrestricted Cash / Board Designated Cash & Investments December 2015 25.0 21.0 20.0 19.5 18.9 18.1 16.8 16.5 15.9 15.0 10.0 11.0 12.8 9.1 10.4 9.8 11.1 14.7 14.2 14.1 9.9 12.0 8.4 13.0 10.2 11.6 14.9

Unrestricted Cash / Board Designated Cash & Investments December 2015 25.0 21.0 20.0 19.5 18.9 18.1 16.8 16.5 15.9 15.0 10.0 11.0 12.8 9.1 10.4 9.8 11.1 14.7 14.2 14.1 9.9 12.0 8.4 13.0 10.2 11.6 14.9

QUESTION 2. QUESTION 3 Which one of the following is most indicative of a flexible short-term financial policy?

QUESTION 1 Compute the cash cycle based on the following information: Average Collection Period = 47 Accounts Payable Period = 40 Average Age of Inventory = 55 QUESTION 2 Jan 41,700 July 39,182 Feb 18,921

QUESTION 1 Compute the cash cycle based on the following information: Average Collection Period = 47 Accounts Payable Period = 40 Average Age of Inventory = 55 QUESTION 2 Jan 41,700 July 39,182 Feb 18,921

PantherSoft Budget Manual

PantherSoft Budget Manual FY 2012-13 Office of Financial Planning / Auxiliary & Enterprise Development 2/23/2012 A document to guide and assist finance managers in the annual forecast and budget process.

PantherSoft Budget Manual FY 2012-13 Office of Financial Planning / Auxiliary & Enterprise Development 2/23/2012 A document to guide and assist finance managers in the annual forecast and budget process.

Projections/Estimated - Unrestricted Cash / Board Designated Cash & Investments September 2017

Projections/Estimated - Unrestricted Cash / Board Designated Cash & Investments September 2017 25.0 20.0 17.1 16.9 15.0 10.0 11.7 11.0 9.1 10.1 9.7 7.7 7.0 6.8 15.1 14.8 11.5 13.1 13.8 9.9 11.4 12.2 8.4

Projections/Estimated - Unrestricted Cash / Board Designated Cash & Investments September 2017 25.0 20.0 17.1 16.9 15.0 10.0 11.7 11.0 9.1 10.1 9.7 7.7 7.0 6.8 15.1 14.8 11.5 13.1 13.8 9.9 11.4 12.2 8.4

CPA Australia Plan Your Own Enterprise Competition

Financial Plan Your financial plan should include: 1. A list of Start-Up Costs and how these will be paid for (eg from savings, bank loan or family loan) 2. A Breakeven Analysis, which includes: a list

Financial Plan Your financial plan should include: 1. A list of Start-Up Costs and how these will be paid for (eg from savings, bank loan or family loan) 2. A Breakeven Analysis, which includes: a list

Review of Registered Charites Compliance Rates with Annual Reporting Requirements 2016

Review of Registered Charites Compliance Rates with Annual Reporting Requirements 2016 October 2017 The Charities Regulator, in accordance with the provisions of section 14 of the Charities Act 2009, carried

Review of Registered Charites Compliance Rates with Annual Reporting Requirements 2016 October 2017 The Charities Regulator, in accordance with the provisions of section 14 of the Charities Act 2009, carried

Development of Economy and Financial Markets of Kazakhstan

Development of Economy and Financial Markets of Kazakhstan National Bank of Kazakhstan Macroeconomic development GDP, real growth, % 116 112 18 14 1 113,5 11,7 216,7223,8226,5 19,8 19,8 19,3 19,619,7 199,

Development of Economy and Financial Markets of Kazakhstan National Bank of Kazakhstan Macroeconomic development GDP, real growth, % 116 112 18 14 1 113,5 11,7 216,7223,8226,5 19,8 19,8 19,3 19,619,7 199,

VALENCIA COLLEGE FINANCIAL SUMMARY FISCAL YEAR As of March 31, 2016

VALENCIA COLLEGE FINANCIAL SUMMARY FISCAL YEAR 2015-16 As of March 31, 2016 Budgeted Annual Collected % Collected Revenue Year To Date Of Annual Enrollment Based 94,185,539 94,205,294 100% State Funding

VALENCIA COLLEGE FINANCIAL SUMMARY FISCAL YEAR 2015-16 As of March 31, 2016 Budgeted Annual Collected % Collected Revenue Year To Date Of Annual Enrollment Based 94,185,539 94,205,294 100% State Funding

Constructing a Cash Flow Forecast

Constructing a Cash Flow Forecast Method and Worked Example A cash flow forecast shows the estimates of the timing and amounts of cash inflows and outflows over a period of time. The sections of a cash

Constructing a Cash Flow Forecast Method and Worked Example A cash flow forecast shows the estimates of the timing and amounts of cash inflows and outflows over a period of time. The sections of a cash

1.2 The purpose of the Finance Committee is to assist the Board in fulfilling its oversight responsibilities related to:

Category: BOARD PROCESS Title: Terms of Reference for the Finance Committee Reference Number: AB-331 Last Approved: February 22, 2018 Last Reviewed: February 22, 2018 1. PURPOSE 1.1 Primary responsibility

Category: BOARD PROCESS Title: Terms of Reference for the Finance Committee Reference Number: AB-331 Last Approved: February 22, 2018 Last Reviewed: February 22, 2018 1. PURPOSE 1.1 Primary responsibility

Monthly Analysis: A Strategic Link to Operational Forecasting

Monthly Analysis: A Strategic Link to Operational Forecasting Presenters: Connie Kravitz, Controller, College of Lake County Tom Ridout, Senior Analytics Advisor, Forecast5 Analytics Paul Wessels, Senior

Monthly Analysis: A Strategic Link to Operational Forecasting Presenters: Connie Kravitz, Controller, College of Lake County Tom Ridout, Senior Analytics Advisor, Forecast5 Analytics Paul Wessels, Senior

FINANCIAL STATEMENTS

FINANCIAL STATEMENTS SEPTEMBER 2018 SMART CORPORATION EXECUTIVE SUMMARY FOR THE MONTH ENDING SEPTEMBER 30, 2018 (in thousands) INCOME STATEMENT Year to Date Annual Actual Budget Variance Forecast Budget

FINANCIAL STATEMENTS SEPTEMBER 2018 SMART CORPORATION EXECUTIVE SUMMARY FOR THE MONTH ENDING SEPTEMBER 30, 2018 (in thousands) INCOME STATEMENT Year to Date Annual Actual Budget Variance Forecast Budget

Business & Financial Services December 2017

Business & Financial Services December 217 Completed Procurement Transactions by Month 2 4 175 15 125 1 75 5 2 1 Business Days to Complete 25 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 217 Procurement

Business & Financial Services December 217 Completed Procurement Transactions by Month 2 4 175 15 125 1 75 5 2 1 Business Days to Complete 25 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 217 Procurement

FORTY-NINER SHOPS, INC. California State University Long Beach, CA. October 20, Q1 Results

October 20, 2017 1 Financial Overview Summary Operating Statement September and First Quarter Results Sales Assessment Investment Results Financial Statements September Year-over-year Comparison 2 Operating

October 20, 2017 1 Financial Overview Summary Operating Statement September and First Quarter Results Sales Assessment Investment Results Financial Statements September Year-over-year Comparison 2 Operating

FOR RELEASE: MONDAY, MARCH 21 AT 4 PM

Interviews with 1,012 adult Americans conducted by telephone by Opinion Research Corporation on March 18-20, 2011. The margin of sampling error for results based on the total sample is plus or minus 3

Interviews with 1,012 adult Americans conducted by telephone by Opinion Research Corporation on March 18-20, 2011. The margin of sampling error for results based on the total sample is plus or minus 3

TERMS OF REFERENCE FOR THE INVESTMENT COMMITTEE

I. PURPOSE The purpose of the Investment Committee (the Committee ) is to recommend to the Board the investment policy, including the asset mix policy and the appropriate benchmark for both ICBC and any

I. PURPOSE The purpose of the Investment Committee (the Committee ) is to recommend to the Board the investment policy, including the asset mix policy and the appropriate benchmark for both ICBC and any

NR614: Foundations of Health Care Economics, Accounting and Financial Management

NR614: Foundations of Health Care Economics, Accounting and Financial Management WEEK 7: Budgeting SLIDE 1: Week 7: Week Seven Sample Problem: Budgeting... There is one sample problem provided in week

NR614: Foundations of Health Care Economics, Accounting and Financial Management WEEK 7: Budgeting SLIDE 1: Week 7: Week Seven Sample Problem: Budgeting... There is one sample problem provided in week

Effective Budgeting and Cost Control. Contents are subject to change. For the latest updates visit

Effective Budgeting and Cost Page 1 of 9 Why Attend ning and budgeting are must-have skills for all professionals regardless of their function or managerial level. This course covers the concept of budgeting

Effective Budgeting and Cost Page 1 of 9 Why Attend ning and budgeting are must-have skills for all professionals regardless of their function or managerial level. This course covers the concept of budgeting

Washington State Health Insurance Pool Treasurer s Report April 2018 Financial Review

Washington State Health Insurance Pool Treasurer s Report April 2018 Financial Review 1. 2018 Interim I Assessment Required An assessment of $7.0 M is required to adequately fund the pool until the next

Washington State Health Insurance Pool Treasurer s Report April 2018 Financial Review 1. 2018 Interim I Assessment Required An assessment of $7.0 M is required to adequately fund the pool until the next

Washington State Health Insurance Pool Treasurer s Report September 2018 Financial Review

Washington State Health Insurance Pool Treasurer s Report September 2018 Financial Review 1. 2018 Interim III Assessment Required An assessment of $8.5 M was required to adequately fund the pool until

Washington State Health Insurance Pool Treasurer s Report September 2018 Financial Review 1. 2018 Interim III Assessment Required An assessment of $8.5 M was required to adequately fund the pool until

Washington State Health Insurance Pool Treasurer s Report January 2018 Financial Review

Washington State Health Insurance Pool Treasurer s Report January 2018 Financial Review 1. 2017 Interim III Assessment Required An assessment of $8.5 M was required to adequately fund the pool until the

Washington State Health Insurance Pool Treasurer s Report January 2018 Financial Review 1. 2017 Interim III Assessment Required An assessment of $8.5 M was required to adequately fund the pool until the

Washington State Health Insurance Pool Treasurer s Report March 2018 Financial Review

Washington State Health Insurance Pool Treasurer s Report March 2018 Financial Review 1. 2017 Interim III Assessment Required An assessment of $8.5 M was required to adequately fund the pool until the

Washington State Health Insurance Pool Treasurer s Report March 2018 Financial Review 1. 2017 Interim III Assessment Required An assessment of $8.5 M was required to adequately fund the pool until the

2018 Financial Management Classes

2018 Financial Management Classes MONEY MANAGEMENT CLASS/BANKING OPERATONS (1ST & 3RD FRIDAY) INVESTING BASICS (2ND FRIDAY) CREDIT MANAGEMENT BLENDED RETIREMENT SYSTEM/THRIFT SAVINGS PLAN (4TH FRIDAY)

2018 Financial Management Classes MONEY MANAGEMENT CLASS/BANKING OPERATONS (1ST & 3RD FRIDAY) INVESTING BASICS (2ND FRIDAY) CREDIT MANAGEMENT BLENDED RETIREMENT SYSTEM/THRIFT SAVINGS PLAN (4TH FRIDAY)

Fiscal Year 2018 Project 1 Annual Budget

Fiscal Year 2018 Project 1 Annual Budget Table of Contents Table Page Summary 3 Summary of Costs Table 1 4 Treasury Related Expenses Table 2 5 Summary of Full Time Equivalent Table 3 6 Positions Cost-to-Cash

Fiscal Year 2018 Project 1 Annual Budget Table of Contents Table Page Summary 3 Summary of Costs Table 1 4 Treasury Related Expenses Table 2 5 Summary of Full Time Equivalent Table 3 6 Positions Cost-to-Cash

SmallBizU WORKSHEET 1: REQUIRED START-UP FUNDS. Online elearning Classroom. Item Required Amount ($) Fixed Assets. 1 -Buildings $ 2 -Land $

Fixed Assets. 1 -Buildings $ 2 -Land $") WORKSHEET 1: REQUIRED START-UP FUNDS Item Required Amount () Fixed Assets 1 -Buildings 2 -Land 3 -Initial Inventory 4 -Equipment 5 -Furniture and Fixtures 6 -Vehicles 7 Total Fixed Assets Working Capital

WORKSHEET 1: REQUIRED START-UP FUNDS Item Required Amount () Fixed Assets 1 -Buildings 2 -Land 3 -Initial Inventory 4 -Equipment 5 -Furniture and Fixtures 6 -Vehicles 7 Total Fixed Assets Working Capital

Common stock prices 1. New York Stock Exchange indexes (Dec. 31,1965=50)2. Transportation. Utility 3. Finance

2. Transportation. Utility 3. Finance") Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis 000 97 98 99 I90 9 9 9 9 9 9 97 98 99 970 97 97 ""..".'..'.."... 97 97 97 97 977 978 979 980 98 98 98 98 98 98 987 988

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis 000 97 98 99 I90 9 9 9 9 9 9 97 98 99 970 97 97 ""..".'..'.."... 97 97 97 97 977 978 979 980 98 98 98 98 98 98 987 988

Projections/Estimated - Unrestricted Cash / Board Designated Cash & Investments March 2018

Projections/Estimated - Unrestricted Cash / Board Designated Cash & Investments March 2018 25.0 20.0 19.0 16.9 17.2 15.0 10.0 11.0 10.9 9.1 10.1 9.7 7.7 7.0 6.8 15.1 14.8 14.4 11.5 13.8 9.9 12.1 12.2 8.4

Projections/Estimated - Unrestricted Cash / Board Designated Cash & Investments March 2018 25.0 20.0 19.0 16.9 17.2 15.0 10.0 11.0 10.9 9.1 10.1 9.7 7.7 7.0 6.8 15.1 14.8 14.4 11.5 13.8 9.9 12.1 12.2 8.4

Board of Directors October 2018 and YTD Financial Report

Board of Directors October 2018 and YTD Financial Report Consolidated Financial Results Operating Margin October ($30,262) $129,301 ($159,563) Year-to-date $292,283 $931,358 ($639,076) Excess of Revenue

Board of Directors October 2018 and YTD Financial Report Consolidated Financial Results Operating Margin October ($30,262) $129,301 ($159,563) Year-to-date $292,283 $931,358 ($639,076) Excess of Revenue

Cost Estimation of a Manufacturing Company

Cost Estimation of a Manufacturing Company Name: Business: Date: Economics of One Unit: Manufacturing Company (Only complete if you are making a product, such as a bracelet or beauty product) Economics

Cost Estimation of a Manufacturing Company Name: Business: Date: Economics of One Unit: Manufacturing Company (Only complete if you are making a product, such as a bracelet or beauty product) Economics

Division of Bond Finance Interest Rate Calculations. Revenue Estimating Conference Interest Rates Used for Appropriations, including PECO Bond Rates

Division of Bond Finance Interest Rate Calculations Revenue Estimating Conference Interest Rates Used for Appropriations, including PECO Bond Rates November 16, 2018 Division of Bond Finance Calculation

Division of Bond Finance Interest Rate Calculations Revenue Estimating Conference Interest Rates Used for Appropriations, including PECO Bond Rates November 16, 2018 Division of Bond Finance Calculation

Using projections to manage your programs

Using projections to manage your programs To project total provider reimbursements To do what ifs based on caseloads or other metrics To project amounts of admin & support available for spending Based

Using projections to manage your programs To project total provider reimbursements To do what ifs based on caseloads or other metrics To project amounts of admin & support available for spending Based

Washington State Health Insurance Pool Treasurer s Report August 2017 Financial Review

Washington State Health Insurance Pool Treasurer s Report August 2017 Financial Review 1. 2017 Interim I Assessment Required An assessment of $9.5 M was required to adequately fund the pool until the next

Washington State Health Insurance Pool Treasurer s Report August 2017 Financial Review 1. 2017 Interim I Assessment Required An assessment of $9.5 M was required to adequately fund the pool until the next

NORTH SYRACUSE CENTRAL SCHOOL DISTRICT. Fund Balance & Budget Assumptions December 4, 2017

NORTH SYRACUSE CENTRAL SCHOOL DISTRICT Fund Balance & Budget Assumptions 2018-2019 December 4, 2017 1 AGENDA Fund Balance Reserves Economic Factors Revenue Assumptions Expenditure Assumptions Budget Timeline

NORTH SYRACUSE CENTRAL SCHOOL DISTRICT Fund Balance & Budget Assumptions 2018-2019 December 4, 2017 1 AGENDA Fund Balance Reserves Economic Factors Revenue Assumptions Expenditure Assumptions Budget Timeline

SHAKER HEIGHTS BOARD OF EDUCATION SHAKER HEIGHTS, OHIO. May 5, Members, Shaker Heights Board of Education

SHAKER HEIGHTS BOARD OF EDUCATION SHAKER HEIGHTS, OHIO TO: FROM: SUBJECT: Members, Shaker Heights Board of Education Bryan C. Christman, Treasurer Financial and Miscellaneous Briefs I. GENERAL FUND (As

SHAKER HEIGHTS BOARD OF EDUCATION SHAKER HEIGHTS, OHIO TO: FROM: SUBJECT: Members, Shaker Heights Board of Education Bryan C. Christman, Treasurer Financial and Miscellaneous Briefs I. GENERAL FUND (As

PI WORKCENTER REFERENCE GUIDE

PI WORKCENTER REFERENCE GUIDE The Principal Investigator (PI) WorkCenter is a central navigation page for awards and project pages. Within the WorkCenter are numerous queries and system functionality designed

PI WORKCENTER REFERENCE GUIDE The Principal Investigator (PI) WorkCenter is a central navigation page for awards and project pages. Within the WorkCenter are numerous queries and system functionality designed

Beginning Date: January 2016 End Date: June Managers in Zephyr: Benchmark: Morningstar Short-Term Bond

Beginning Date: January 2016 End Date: June 2018 Managers in Zephyr: Benchmark: Manager Performance January 2016 - June 2018 (Single Computation) 11200 11000 10800 10600 10400 10200 10000 9800 Dec 2015

Beginning Date: January 2016 End Date: June 2018 Managers in Zephyr: Benchmark: Manager Performance January 2016 - June 2018 (Single Computation) 11200 11000 10800 10600 10400 10200 10000 9800 Dec 2015

Washington State Health Insurance Pool Treasurer s Report December 2017 Financial Review

Washington State Health Insurance Pool Treasurer s Report December 2017 Financial Review 1. 2017 Interim III Assessment Required An assessment of $8.5 M is required to adequately fund the pool until the

Washington State Health Insurance Pool Treasurer s Report December 2017 Financial Review 1. 2017 Interim III Assessment Required An assessment of $8.5 M is required to adequately fund the pool until the

Research Accounting & Analysis University of Washington Operational Performance Dashboard

Research Accounting & Analysis University of Washington Operational Performance Dashboard September 26 Quarter 1 - Fiscal Year 7 Grant and Contract Accounting Mission As a professional accounting team,

Research Accounting & Analysis University of Washington Operational Performance Dashboard September 26 Quarter 1 - Fiscal Year 7 Grant and Contract Accounting Mission As a professional accounting team,

UNIVERSITY OF NORTHERN COLORADO: FINANCIAL REPORT 12/31/2010

UNIVERSITY OF NORTHERN COLORADO: FINANCIAL REPORT 12/31/2010 OVERVIEW The following is a summary of the financial highlights contained in the second quarter report for fiscal year 2010-11: Cash and Accounts

UNIVERSITY OF NORTHERN COLORADO: FINANCIAL REPORT 12/31/2010 OVERVIEW The following is a summary of the financial highlights contained in the second quarter report for fiscal year 2010-11: Cash and Accounts

VALENCIA COLLEGE FINANCIAL SUMMARY FISCAL YEAR As of April 30, 2016

VALENCIA COLLEGE FINANCIAL SUMMARY FISCAL YEAR 201516 As of April 30, 2016 Budgeted Annual Collected % Collected Revenue Year To Date Of Annual Enrollment Based 94,185,539 96,696,137 103% State Funding

VALENCIA COLLEGE FINANCIAL SUMMARY FISCAL YEAR 201516 As of April 30, 2016 Budgeted Annual Collected % Collected Revenue Year To Date Of Annual Enrollment Based 94,185,539 96,696,137 103% State Funding

Beginning Date: January 2016 End Date: September Managers in Zephyr: Benchmark: Morningstar Short-Term Bond

Beginning Date: January 2016 End Date: September 2018 Managers in Zephyr: Benchmark: Manager Performance January 2016 - September 2018 (Single Computation) 11400 - Yorktown Funds 11200 11000 10800 10600

Beginning Date: January 2016 End Date: September 2018 Managers in Zephyr: Benchmark: Manager Performance January 2016 - September 2018 (Single Computation) 11400 - Yorktown Funds 11200 11000 10800 10600

Foundations of Investing

www.edwardjones.com Member SIPC Foundations of Investing 1 5 HOW CAN I STAY ON TRACK? 4 HOW DO I GET THERE? 1 WHERE AM I TODAY? MY FINANCIAL NEEDS 3 CAN I GET THERE? 2 WHERE WOULD I LIKE TO BE? 2 Develop

www.edwardjones.com Member SIPC Foundations of Investing 1 5 HOW CAN I STAY ON TRACK? 4 HOW DO I GET THERE? 1 WHERE AM I TODAY? MY FINANCIAL NEEDS 3 CAN I GET THERE? 2 WHERE WOULD I LIKE TO BE? 2 Develop

Factor Leave Accruals. Accruing Vacation and Sick Leave

Factor Leave Accruals Accruing Vacation and Sick Leave Factor Leave Accruals As part of the transition of non-exempt employees to biweekly pay, the UC Office of the President also requires standardization

Factor Leave Accruals Accruing Vacation and Sick Leave Factor Leave Accruals As part of the transition of non-exempt employees to biweekly pay, the UC Office of the President also requires standardization

Avocado Regional Composite. South Central Region

Avocado Regional Composite South Central Region January March: 2009 vs. 2010 1 Methodology Sales and Market Data is obtained using CAST (Category Avocado Sales Trend) Information Resources Inc. gathers

Avocado Regional Composite South Central Region January March: 2009 vs. 2010 1 Methodology Sales and Market Data is obtained using CAST (Category Avocado Sales Trend) Information Resources Inc. gathers

Balance Sheet - Consolidated August 31, 2018

1 ASSETS Current Assets - Funds Total Operating Total KVFD Reserve Total Restricted Total Capital Reserve Total Snow Removal Reserve Total COP Reserve Fund Total Current Assets - Funds Current Assets -

1 ASSETS Current Assets - Funds Total Operating Total KVFD Reserve Total Restricted Total Capital Reserve Total Snow Removal Reserve Total COP Reserve Fund Total Current Assets - Funds Current Assets -

Beatitudes Campus. Occupancy. Days of Cash on Hand. Occupancy. Operating Ratio. Debt Service Coverage Ratio

86% 96% 95% 80% 2018 Forecast 86% 95% 80% 2018 YTD 2017 2016 2015 2014 2013 Operating Ratio Operating Ratio (Revenue ) / (Expenses-(Depreciation & Amortization)) (Revenue)/(Expenses-(Depr & Amort)) Debt

86% 96% 95% 80% 2018 Forecast 86% 95% 80% 2018 YTD 2017 2016 2015 2014 2013 Operating Ratio Operating Ratio (Revenue ) / (Expenses-(Depreciation & Amortization)) (Revenue)/(Expenses-(Depr & Amort)) Debt

Forecast Position. Detailed financial statements are included in the Appendix attached to this report. March 2018 $Ms Year to Date $Ms Full Year $Ms

MEMO To: Board Members From: Eric Sinclair, GM Finance & Performance Date: 18 April 2018 Subject: Financial Report for February 2018 Status This report contains: For decision Update Regular report For

MEMO To: Board Members From: Eric Sinclair, GM Finance & Performance Date: 18 April 2018 Subject: Financial Report for February 2018 Status This report contains: For decision Update Regular report For

Certificate in Advanced Budgeting and Forecasting

Certificate in Advanced Budgeting and Forecasting Page 1 of 12 Why Attend This course is the second level course in budgeting after Meirc's 'Effective Budgeting and Cost Control' course. It goes beyond

Certificate in Advanced Budgeting and Forecasting Page 1 of 12 Why Attend This course is the second level course in budgeting after Meirc's 'Effective Budgeting and Cost Control' course. It goes beyond

PHOENIX ENERGY MARKETING CONSULTANTS INC. HISTORICAL NATURAL GAS & CRUDE OIL PRICES UPDATED TO July, 2018

Jan-01 $12.9112 $10.4754 $9.7870 $1.5032 $29.2595 $275.39 $43.78 $159.32 $25.33 Feb-01 $10.4670 $7.8378 $6.9397 $1.5218 $29.6447 $279.78 $44.48 $165.68 $26.34 Mar-01 $7.6303 $7.3271 $5.0903 $1.5585 $27.2714

Jan-01 $12.9112 $10.4754 $9.7870 $1.5032 $29.2595 $275.39 $43.78 $159.32 $25.33 Feb-01 $10.4670 $7.8378 $6.9397 $1.5218 $29.6447 $279.78 $44.48 $165.68 $26.34 Mar-01 $7.6303 $7.3271 $5.0903 $1.5585 $27.2714

CSU San Marcos Budget Training. Understanding the basics of managing a budget

CSU San Marcos Budget Training Understanding the basics of managing a budget A budget is a plan Budget Basics What is a budget? Budget is not another word for cash Budgeting provides a vehicle for translating

CSU San Marcos Budget Training Understanding the basics of managing a budget A budget is a plan Budget Basics What is a budget? Budget is not another word for cash Budgeting provides a vehicle for translating

HIPIOWA - IOWA COMPREHENSIVE HEALTH ASSOCIATION Unaudited Balance Sheet As of July 31

Unaudited Balance Sheet As of July 31 Total Enrollment: 407 Assets: Cash $ 9,541,661 $ 1,237,950 Invested Cash 781,689 8,630,624 Premiums Receivable 16,445 299,134 Prepaid 32,930 34,403 Assessments Receivable

Unaudited Balance Sheet As of July 31 Total Enrollment: 407 Assets: Cash $ 9,541,661 $ 1,237,950 Invested Cash 781,689 8,630,624 Premiums Receivable 16,445 299,134 Prepaid 32,930 34,403 Assessments Receivable

Unrestricted Cash / Board Designated Cash & Investments December 2014

Unrestricted Cash / Board Designated Cash & Investments December 2014 25.0 20.0 21.0 20.8 18.9 19.9 15.0 10.0 11.5 12.8 11.6 9.1 10.4 9.8 11.1 10.2 9.8 17.0 16.8 15.4 14.7 14.2 14.1 13.6 13.0 12.0 10.2

Unrestricted Cash / Board Designated Cash & Investments December 2014 25.0 20.0 21.0 20.8 18.9 19.9 15.0 10.0 11.5 12.8 11.6 9.1 10.4 9.8 11.1 10.2 9.8 17.0 16.8 15.4 14.7 14.2 14.1 13.6 13.0 12.0 10.2

HIPIOWA - IOWA COMPREHENSIVE HEALTH ASSOCIATION Unaudited Balance Sheet As of January 31

Unaudited Balance Sheet As of January 31 Total Enrollment: 371 Assets: Cash $ 1,408,868 $ 1,375,117 Invested Cash 4,664,286 4,136,167 Premiums Receivable 94,152 91,261 Prepaid 32,270 33,421 Assessments

Unaudited Balance Sheet As of January 31 Total Enrollment: 371 Assets: Cash $ 1,408,868 $ 1,375,117 Invested Cash 4,664,286 4,136,167 Premiums Receivable 94,152 91,261 Prepaid 32,270 33,421 Assessments

Avocado Regional Composite. South Central Region

Avocado Regional Composite South Central Region January September: 2009 vs. 2010 1 Methodology Sales and Market Data is obtained using CAST (Category Avocado Sales Trend) Information Resources Inc. gathers

Avocado Regional Composite South Central Region January September: 2009 vs. 2010 1 Methodology Sales and Market Data is obtained using CAST (Category Avocado Sales Trend) Information Resources Inc. gathers

SHAKER HEIGHTS BOARD OF EDUCATION SHAKER HEIGHTS, OHIO. April 12, Members, Shaker Heights Board of Education

SHAKER HEIGHTS BOARD OF EDUCATION SHAKER HEIGHTS, OHIO TO: FROM: SUBJECT: Members, Shaker Heights Board of Education Bryan C. Christman, Treasurer Financial and Miscellaneous Briefs I. GENERAL FUND (As

SHAKER HEIGHTS BOARD OF EDUCATION SHAKER HEIGHTS, OHIO TO: FROM: SUBJECT: Members, Shaker Heights Board of Education Bryan C. Christman, Treasurer Financial and Miscellaneous Briefs I. GENERAL FUND (As

Research Accounting & Analysis University of Washington

Research Accounting & Analysis Grant & Contract Accounting? Management Accounting & Analysis Operational Performance Dashboard for November 2 Quarter 2 FY 2 (October - December 2) Grant and Contract Accounting

Research Accounting & Analysis Grant & Contract Accounting? Management Accounting & Analysis Operational Performance Dashboard for November 2 Quarter 2 FY 2 (October - December 2) Grant and Contract Accounting

Executive Summary. July 17, 2015

Executive Summary July 17, 2015 The Revenue Estimating Conference adopted interest rates for use in the state budgeting process. The adopted interest rates take into consideration current benchmark rates

Executive Summary July 17, 2015 The Revenue Estimating Conference adopted interest rates for use in the state budgeting process. The adopted interest rates take into consideration current benchmark rates

STAFF REPORT Corporate Services

1 Corporate Services STAFF REPORT Corporate Services Title: Core Consumer Price Index Update Report Number: CORP2018-071 Author: Kim Reger & Brad Witzel Meeting Type: Finance & Strategic Planning Committee

1 Corporate Services STAFF REPORT Corporate Services Title: Core Consumer Price Index Update Report Number: CORP2018-071 Author: Kim Reger & Brad Witzel Meeting Type: Finance & Strategic Planning Committee

Rocco Sabino MBA, CPA

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

HUD NSP-1 Reporting Apr 2010 Grantee Report - New Mexico State Program

HUD NSP-1 Reporting Apr 2010 Grantee Report - State Program State Program NSP-1 Grant Amount is $19,600,000 $9,355,381 (47.7%) has been committed $4,010,874 (20.5%) has been expended Grant Number HUD Region

HUD NSP-1 Reporting Apr 2010 Grantee Report - State Program State Program NSP-1 Grant Amount is $19,600,000 $9,355,381 (47.7%) has been committed $4,010,874 (20.5%) has been expended Grant Number HUD Region

Budgeting. Mr Crosthwaite. Mindarie Senior College

Budgeting Mr Crosthwaite Mindarie Senior College Budgets A budget is a plan of the future expressed in money terms. It can be earmarked for a particular activity, time-frame or institution. It allows us

Budgeting Mr Crosthwaite Mindarie Senior College Budgets A budget is a plan of the future expressed in money terms. It can be earmarked for a particular activity, time-frame or institution. It allows us

FERC EL Settlement Agreement

FERC EL05-121-009 Settlement Agreement Ray Fernandez Manager, Market Settlements Development Market Settlements Subcommittee June 14, 2018 Settlement Agreement Details Settlement Agreement Details FERC

FERC EL05-121-009 Settlement Agreement Ray Fernandez Manager, Market Settlements Development Market Settlements Subcommittee June 14, 2018 Settlement Agreement Details Settlement Agreement Details FERC

SCHOOL BOARD OF POLK COUNTY

SCHOOL BOARD OF POLK COUNTY P.O. BOX 391 1915 SOUTH FLORAL AVENUE BARTOW, FLORIDA 33831 BARTOW, FLORIDA 33830 (863) 534-0500 SUNCOM 515-1321 FAX (863) 534-0705 April 14, 2015 To: School Board Members Kathryn

SCHOOL BOARD OF POLK COUNTY P.O. BOX 391 1915 SOUTH FLORAL AVENUE BARTOW, FLORIDA 33831 BARTOW, FLORIDA 33830 (863) 534-0500 SUNCOM 515-1321 FAX (863) 534-0705 April 14, 2015 To: School Board Members Kathryn

Financial & Business Highlights For the Year Ended June 30, 2017

Financial & Business Highlights For the Year Ended June, 17 17 16 15 14 13 12 Profit and Loss Account Operating Revenue 858 590 648 415 172 174 Investment gains net 5 162 909 825 322 516 Other 262 146

Financial & Business Highlights For the Year Ended June, 17 17 16 15 14 13 12 Profit and Loss Account Operating Revenue 858 590 648 415 172 174 Investment gains net 5 162 909 825 322 516 Other 262 146

Aug 7, 2017 Board of Directors Meeting. YTD June 2017 Financial Results

Aug 7, 2017 Board of Directors Meeting YTD June 2017 Financial Results 1 YTD June2017 Statement of Operations The YTD financials reflect $1.576M gift in kind revenue and expense for the Sharon Stone PSA

Aug 7, 2017 Board of Directors Meeting YTD June 2017 Financial Results 1 YTD June2017 Statement of Operations The YTD financials reflect $1.576M gift in kind revenue and expense for the Sharon Stone PSA

SUMMARY OF OPERATING RESULTS DECEMBER UWHC Finance Committee & Authority Board

SUMMARY OF OPERATING RESULTS DECEMBER 20 UWHC Finance Committee & Authority Board Adult Admissions,679,263,263 2,039 1,932 1,929 December 20 2014 YTD 2 Pediatrics Admissions 1,781 1,799 1,776 257 280 274

SUMMARY OF OPERATING RESULTS DECEMBER 20 UWHC Finance Committee & Authority Board Adult Admissions,679,263,263 2,039 1,932 1,929 December 20 2014 YTD 2 Pediatrics Admissions 1,781 1,799 1,776 257 280 274

Asset Manager Performance Comparison

Cape Peninsula University of Technology Retirement Fund August 2017 DISCLAIMER AND WARNINGS: Towers Watson (Pty) Ltd, a Willis Towers Watson company, is an authorised financial services provider. Although

Cape Peninsula University of Technology Retirement Fund August 2017 DISCLAIMER AND WARNINGS: Towers Watson (Pty) Ltd, a Willis Towers Watson company, is an authorised financial services provider. Although

THE B E A CH TO WN S O F P ALM B EA CH

THE B E A CH TO WN S O F P ALM B EA CH C OU N T Y F LO R I D A August www.luxuryhomemarketing.com PALM BEACH TOWNS SINGLE-FAMILY HOMES LUXURY INVENTORY VS. SALES JULY Sales Luxury Benchmark Price : 7,

THE B E A CH TO WN S O F P ALM B EA CH C OU N T Y F LO R I D A August www.luxuryhomemarketing.com PALM BEACH TOWNS SINGLE-FAMILY HOMES LUXURY INVENTORY VS. SALES JULY Sales Luxury Benchmark Price : 7,

Trade Finance, Letters of Credit and Bank Guarantees

Trade Finance, Letters of Credit and Bank Guarantees Page 1 of 10 Why Attend Securing company s assets while transacting with local and international customers is critical for the success and sustainability

Trade Finance, Letters of Credit and Bank Guarantees Page 1 of 10 Why Attend Securing company s assets while transacting with local and international customers is critical for the success and sustainability

Asset Manager Performance Comparison

Cape Peninsula University of Technology Retirement Fund September 2017 DISCLAIMER AND WARNINGS: Towers Watson (Pty) Ltd, a Willis Towers Watson company, is an authorised financial services provider. Although

Cape Peninsula University of Technology Retirement Fund September 2017 DISCLAIMER AND WARNINGS: Towers Watson (Pty) Ltd, a Willis Towers Watson company, is an authorised financial services provider. Although

Financial Report for the Month of SEPTEMBER

WILLOUGHBY, OH Financial Report for the Month of SEPTEMBER Month Ended SEPTEMBER 30, 2013 BOARD OF EDUCATION Mrs. Margaret Warner, President SUPERINTENDENT Mr. Steve Thompson Mrs. Sharon Scott, Vice President

WILLOUGHBY, OH Financial Report for the Month of SEPTEMBER Month Ended SEPTEMBER 30, 2013 BOARD OF EDUCATION Mrs. Margaret Warner, President SUPERINTENDENT Mr. Steve Thompson Mrs. Sharon Scott, Vice President

(Internet version) Financial & Statistical Report November 2018

Financial & Statistical Report November 2018") (Internet version) Financial & Statistical Report November 2018 12/17/2018 Statement of Operations For the Period Ended November 30, 2018 (in millions) Current Month Year-to-Date Operating Revenue $ 31.4

(Internet version) Financial & Statistical Report November 2018 12/17/2018 Statement of Operations For the Period Ended November 30, 2018 (in millions) Current Month Year-to-Date Operating Revenue $ 31.4

Looking at a Variety of Municipal Valuation Metrics

Looking at a Variety of Municipal Valuation Metrics Muni vs. Treasuries, Corporates YEAR MUNI - TREASURY RATIO YEAR MUNI - CORPORATE RATIO 200% 80% 175% 150% 75% 70% 65% 125% Average Ratio 0% 75% 50% 60%

Looking at a Variety of Municipal Valuation Metrics Muni vs. Treasuries, Corporates YEAR MUNI - TREASURY RATIO YEAR MUNI - CORPORATE RATIO 200% 80% 175% 150% 75% 70% 65% 125% Average Ratio 0% 75% 50% 60%

Last Revised: 1/28/11. Finance Data Warehouse Dashboard and Report Guide OPERATIONS

Last Revised: 1/28/11 Finance Data Warehouse Dashboard and Report Guide OPERATIONS REVISION CONTROL Document Title: Author: File Reference: Finance Data Warehouse Dashboard and Report Guide Enterprise

Last Revised: 1/28/11 Finance Data Warehouse Dashboard and Report Guide OPERATIONS REVISION CONTROL Document Title: Author: File Reference: Finance Data Warehouse Dashboard and Report Guide Enterprise

Cash & Liquidity The chart below highlights CTA s cash position at December 2017 compared to December 2016.

To: Chicago Transit Authority Board From: Jeremy Fine, Chief Financial Officer Re: Financial Results for December 2017 Date: February 14, 2018 I. Summary CTA s financial results are $4.7 million favorable

To: Chicago Transit Authority Board From: Jeremy Fine, Chief Financial Officer Re: Financial Results for December 2017 Date: February 14, 2018 I. Summary CTA s financial results are $4.7 million favorable

Cash & Liquidity The chart below highlights CTA s cash position at March 2017 compared to March 2016.

To: Chicago Transit Authority Board From: Jeremy Fine, Chief Financial Officer Re: Financial Results for March 2017 Date: May 10, 2017 I. Summary CTA s financial results are $0.6 million favorable to budget

To: Chicago Transit Authority Board From: Jeremy Fine, Chief Financial Officer Re: Financial Results for March 2017 Date: May 10, 2017 I. Summary CTA s financial results are $0.6 million favorable to budget

Big Walnut Local School District

Big Walnut Local School District Monthly Financial Report for the month ended September 30, 2013 Prepared By: Felicia Drummey Treasurer BIG WALNUT LOCAL SCHOOL DISTRICT SUMMARY OF YEAR TO DATE FINANCIAL

Big Walnut Local School District Monthly Financial Report for the month ended September 30, 2013 Prepared By: Felicia Drummey Treasurer BIG WALNUT LOCAL SCHOOL DISTRICT SUMMARY OF YEAR TO DATE FINANCIAL

FINANCIAL MANAGEMENT STRATEGY REPORT ON OUTCOMES FOR THE YEAR ENDED MARCH 31, 2016

FINANCIAL MANAGEMENT STRATEGY REPORT ON OUTCOMES FOR THE YEAR ENDED MARCH 31, 2016 Manitoba Finance General Inquiries: Room 109, Legislative Building Winnipeg, Manitoba R3C 0V8 Phone: 204-945-5343 Fax:

FINANCIAL MANAGEMENT STRATEGY REPORT ON OUTCOMES FOR THE YEAR ENDED MARCH 31, 2016 Manitoba Finance General Inquiries: Room 109, Legislative Building Winnipeg, Manitoba R3C 0V8 Phone: 204-945-5343 Fax:

Washington State Health Insurance Pool Treasurer s Report February 2018 Financial Review

Washington State Health Insurance Pool Treasurer s Report February 2018 Financial Review 1. 2017 Interim III Assessment Required An assessment of $8.5 M was required to adequately fund the pool until the

Washington State Health Insurance Pool Treasurer s Report February 2018 Financial Review 1. 2017 Interim III Assessment Required An assessment of $8.5 M was required to adequately fund the pool until the

Certificate in Treasury and Cash Management. Contents are subject to change. For the latest updates visit

Certificate in Treasury and Cash Page 1 of 12 Why Attend It is essential for every organization to effectively utilize its funds and manage its exposure to key risks arising from fluctuations in interest

Certificate in Treasury and Cash Page 1 of 12 Why Attend It is essential for every organization to effectively utilize its funds and manage its exposure to key risks arising from fluctuations in interest